Reduced-Rank Covariance Estimation

in Vector Autoregressive Modeling

Abstract

We consider reduced-rank modeling of the white noise covariance matrix in a large dimensional vector autoregressive (VAR) model. We first propose the reduced-rank covariance estimator under the setting where independent observations are available. We derive the reduced-rank estimator based on a latent variable model for the vector observation and give the analytical form of its maximum likelihood estimate.

Simulation results show that the reduced-rank covariance estimator outperforms two competing covariance estimators for estimating large dimensional covariance matrices from independent observations. Then we describe how to integrate the proposed reduced-rank estimator into the fitting of large dimensional VAR models, where we consider two scenarios that require different model fitting procedures. In the VAR modeling context, our reduced-rank covariance estimator not only provides interpretable descriptions of the dependence structure of VAR processes but also leads to improvement in model-fitting and forecasting over unrestricted covariance estimators. Two real data examples are presented to illustrate these fitting procedures.

Keywords: Covariance Estimation; Vector Autoregressive (VAR) Models; Matrix Decomposition.

1 Introduction

Suppose is a -dimensional stationary time series that follows the vector autoregressive model of order (VAR())

| (1.1) |

where is a real-valued -dimensional vector; are real-valued matrices of autoregressive (AR) coefficients; and is a sequence of iid noise with mean and covariance matrix . We further assume that the process is causal, i.e., , for , e.g., see Helmut1991. The VAR model (1.1) has been applied for modeling the joint evolution of multivariate series in many fields, such as political science Freeman1989, macroeconomics Sims1980, biological science Holter2001 and finance Eun1989.

One indispensable aspect of fitting the VAR model (1.1) is the estimation of the noise covariance matrix : an estimate of the noise covariance matrix is needed for exploring the dependence structure of the VAR process Demiralp2003; Moneta2004 while an estimate of the inverse of the noise covariance matrix is required in constructing confidence intervals for AR coefficients or for computing the mean squared error of VAR forecasting Helmut1991. A natural estimator for in a VAR model is the sample covariance matrix of the residuals from fitting an autoregression Helmut1991. To this end, the residuals are viewed as independent samples, conditioned on the AR coefficient estimates, from an underlying distribution with covariance matrix . Therefore estimating the noise covariance matrix in a VAR model can be cast as a covariance estimation problem where independent observations are available.

Covariance estimation from independent observations is a fundamental problem in many areas, such as portfolio selection Ledoit2004, functional genomics Schafer2005, fMRI study Daniels2001 and graphical models Lauritzen1989. Estimating a covariance matrix posits many challenges for large since the number of parameters to be estimated grows quadratically in the dimension . The sample covariance matrix of the observations serves as a natural estimator when the dimension is much smaller than the sample size. But it is also well-known that the sample covariance matrix can be severely ill-conditioned in small- to medium- samples. As a result, various methods have been proposed to estimate large dimensional covariance matrices. The three most common approaches are shrinkage, where the covariance estimator is obtained by shrinking the sample covariance matrix towards a pre-specified covariance structure Ledoit2004; Schafer2005; regularization, where the covariance estimator is derived based on regularization methods, such as banding Bickel2008, thresholding Karoui2008 and penalized estimation Huang2006; and structural, where structural constraints, such as factor structures Tipping1999 or autoregressive structures Daniels2001, are imposed to reduce the effective dimension of the covariance estimator.

In this paper, we propose a reduced-rank estimator for the noise covariance matrix in a large dimensional VAR model. In Section 2 we first derive the reduced-rank estimator under the setting when observations are independent. The reduced-rank estimator is based on a latent variable model for the data and its effective dimension can be much lower than the dimension of the population covariance matrix. So the reduced-rank estimator can be viewed as a structural covariance estimator. The reduced-rank estimator is attractive since it is not only well-conditioned, but also provides an interpretable description of the covariance structure. Simulation results show that the reduced-rank covariance estimator outperforms two competing shrinkage estimators for estimating large dimensional covariance matrices. In Section 2.2, we proceed to the context of VAR modeling. We describe how to integrate the proposed reduced-rank estimator into the fitting of large dimensional VAR models, for which we consider two scenarios that require different model fitting procedures. The first scenario is that there are no constraints on the AR coefficients, for which the VAR model can be fitted using a 2-step method; while in the second scenario there exist constraints on the AR coefficients, where the VAR model needs to be fitted by an iterative procedure. In Section 3.2, the reduced-rank covariance estimator is applied to the VAR modeling of two real data examples. The first example is concerned with stock returns from S&P 500 and the second example is a time series of temperatures in southeast China.

2 Reduced-rank covariance estimation

We first derive the reduced-rank covariance estimator based on independent observations. Then we proceed to VAR modeling and describe how to integrate the reduced-rank estimator into the fitting of large dimensional VAR models.

2.1 For independent observations

We assume that are independent replicates from a -dimensional Gaussian distribution with covariance matrix 111Here we make the assumption of Gaussianity. If is non-Gaussian, our proposed reduced-rank covariance estimation method can still be applied, where the Gaussian likelihood is interpreted as a quasi-likelihood.. Without loss of generality, we assume that has mean zero. The problem of interest is to estimate , which can be large dimensional. To derive our covariance estimator, we further assume that each vector observation follows the latent variable model

| (2.1) |

where the latent variables are independent replicates from a -dimensional () Gaussian with mean and a diagonal covariance matrix (); is a column-orthonormal matrix, i.e., ; and the errors are independent replicates from a -dimensional Gaussian with mean and isotropic covariance matrix . As shown in Section 2.1.1, this isotropy assumption of the covariance matrix is important in ensuring the identifiability of the latent variance model (2.1) under Gaussianity.

Under the latent variable model (2.1), the covariance matrix is seen to be

| (2.2) |

The first component in the decomposition (2.2) has reduced-rank () and contains the core information about the dependence structure between the dimensions of . The second component has a sparse structure and accounts for unexplained variability in individual dimensions. The decomposition (2.2) approximates the -dimensional dependence structure encoded by with a rank- matrix . Such an approximation is useful for separating important dependence patterns from large dimensional noisy observations.

2.1.1 Connection and distinction with factor models

The motivation of the latent variable model (2.1) is that the -dimensional vector can be related to a -dimensional vector of latent (unobserved) variables through a column-orthonormal matrix . With , the latent variable provides a more parsimonious description of the dependence structure of . This motivation is similar to that of factor models, see e.g., Anderson2003. In the factor model setup, the relation (2.1) is also used to link the observation with the latent variable and the matrix is called the factor loading; but it is usually assumed that the latent variable has an isotropic covariance matrix while the error has a non-isotropic covariance matrix. It is known that factor models have identifiability issues. Specifically, for any orthogonal matrix , the pairs and will lead to two equivalent factor models. In contrast, identifiability is not an issue in our latent variable model (2.1). This is because in the latent variable model we make different assumptions on the covariance structures of the latent variable and the error , as summarized in Table 1. In the latent variable model, the covariance matrix of the vector is , which in general is not equal to the original covariance matrix . So the two latent variable models corresponding to the pairs and are not equivalent; in other words, the assumption of a non-isotropic covariance matrix for the latent vector leads to the identifiability of the latent variable model (2.1). As a result, interpretation of the matrix parameter becomes meaningful.

| Model | ||

|---|---|---|

| latent variable model (2.1) | ||

| factor model |

2.1.2 Maximum likelihood estimation

We derive the maximum likelihood estimator of the reduced-rank covariance matrix (2.2). Based on observations , log-likelihood, ignoring an additive constant, is given by

| (2.3) |

where . The following proposition shows that there exists an analytical form for the maximum likelihood estimator of the reduced-rank covariance matrix .

Proposition 2.1.

Let be the eigenvalues of the sample covariance matrix and assume that the reduced-rank is known. The maximum likelihood estimator of the reduced-rank covariance matrix is given by

| (2.4) |

where

| (2.5) | ||||

| (2.6) | ||||

| (2.7) |

We defer the proof to the Appendix LABEL:section_appendix_proof_rr.

2.1.3 Properties of the reduced-rank covariance estimator

From (2.5) we can see that there exist links between the latent variable model (2.1) and principal component analysis (PCA), which is perhaps the most widely used statistical tool for dimension reduction. The common setup of PCA is based on a series of mutually-orthogonal projections of vector observations that maximize the retained variance, where the directions of these projections are called principal axes, see e.g., Jolliffe2002. This setup is not based on a probabilistic model but comes from a projection perspective. In contrast, the latent variable model (2.1) provides a model-based formulation of PCA, in which the principal axes coincide with the columns of the maximum likelihood estimator as given by (2.5). In the literature, such a probabilistic formulation of PCA was first investigated by Lawley1953 within the context of factor analysis and was then studied by Tipping1999 under probabilistic principal component analysis (PPCA). A discussion on the advantages of this probabilistic formulation of PCA over the traditional projection-based setup is given in Tipping1999.

We also investigate the conditioning property of the reduced-rank estimator (2.4). It can be shown that the eigenvalues, denoted by (), of the reduced-rank estimator are

which means that the reduced-rank estimator retains the largest eigenvalues but shrinks the remaining eigenvalues of towards their average. Therefore, the condition number, i.e., the ratio between the largest and smallest eigenvalues of the covariance estimator, of the reduced-rank estimator is smaller and often much smaller than that of the sample covariance matrix. In other words, the reduced-rank estimator can be better conditioned than the sample covariance matrix. In addition, as long as the reduced-rank is smaller than the sample size , the reduced-rank estimator will be invertible even if the dimension exceeds the sample size .

Next we discuss how to control the complexity of a reduced-rank covariance estimator through the choice of its reduced-rank . From (2.4) we can see that there exist two extremes for as the reduced-rank varies: when , i.e., there is no dimension reduction, becomes the full covariance model; and when , i.e., there is no structured component , becomes the isotropic covariance model. In other words, the reduced-rank covariance estimator is obtained by balancing between the unbiased but highly variable sample covariance matrix and the biased but well-conditioned isotropic covariance matrix, where the balance is controlled by the reduced-rank . In practice, the reduced-rank is unknown and needs to be estimated from data. Here we use the Bayesian information criterion (BIC), e.g., see Schwarz1978, to determine the reduced-rank . The BIC is computed as

| (2.9) |

where is the maximized likelihood and is the number of free parameters in the reduced-rank covariance estimator. We select the reduced-rank from according to a minimum BIC. Tipping1999 give similar results on controlling the complexity of PPCA.

Finally we describe a diagnostic tool for the reduced-rank covariance model. The latent variable in (2.1) can be estimated by

| (2.10) |

where is given by (2.5). According to model assumptions, should behave like independent replicates from a -dimensional Gaussian with a diagonal covariance matrix. So correlation functions of the estimated latent variable (2.10) can be used for model diagnostics.

2.2 For VAR series

In this section, we proceed from the setting of independent observations to VAR processes and apply the reduced-rank covariance estimator to the noise covariance matrix in a VAR model (1.1).

As described in Section 1, the reduced-rank estimator for in a VAR model is computed based on the residuals from fitted autoregression. Therefore, in order to apply the reduced-rank covariance estimator, we need to estimate the AR coefficient matrices in (1.1) as well, for which we consider two scenarios. The first scenario is that there are no constraints on the AR coefficient matrices ; while the second scenario is that there exist constraints on the AR coefficients. The second scenario occurs, for example, when some of the AR coefficients are constrained be to zero. Such zero constraints on AR coefficients arise when we model Granger causality of , see e.g., Granger1969, or when we fit sparse vector autoregressive models to , see e.g., Davis2012. Here we use zero constraints on AR coefficients as the example of the second scenario. Zero constraints on the AR coefficient matrices can be expressed as

| (2.11) |

where is the -dimensional vector obtained by stacking the columns of the AR coefficient matrices ; is a matrix of known constants with rank ; and is a -dimensional vector of unknown parameters. The matrix is referred to as the constraint matrix Davis2012 and it specifies which AR coefficients are zero by choosing one entry in each column to be and all the other entries in that column to be . The rank of the constraint matrix is equal to the number of non-zero AR coefficients. Using results on constrained VAR estimation in Helmut1991 and on the reduced-rank covariance estimation in Section 2.1, it can be shown that, under the constraint (2.11) and the reduced-rank covariance model (2.2), the maximum likelihood estimator of the AR coefficients is given by

| (2.12) |

where

and in (2.12) is the reduced-rank maximum likelihood estimator for the noise covariance matrix based on the residuals from the fitted autoregression.

The model fitting procedure for the first scenario.

When there are no constraints on the AR coefficients (scenario 1), we have in (2.11) and (2.12) becomes

| (2.13) | |||||

So for the first scenario, (2.13) shows that the estimation of the AR coefficients does not involve the reduced-rank estimation of the noise covariance matrix . Therefore the reduced-rank covariance estimator can be applied to a VAR model using the following 2-step method.

The model fitting procedure for the second scenario.

Where there exist zero constraints on the AR coefficients (scenario 2), (2.12) shows that the estimation of the AR coefficients is confounded with the reduced-rank estimation of the noise covariance matrix . Therefore the reduced-rank covariance estimator is applied to a VAR model using the following iterative procedure.

-

•

Start with initial estimators and .

-

•

Assume that at the th iteration, the current estimators are and , respectively. Repeat the following steps 1 and 2 until convergence.

A latent space interpretation.

We conclude this section by introducing a latent space setup that facilitates understanding and interpretation of a reduced-rank covariance VAR model. In particular, this latent space setup is useful in exploring contemporaneous dependence structure of the VAR process , which describes how synchronous values of different marginal series of impact each other, see e.g., Tunnicliffe2001; Demiralp2003; Moneta2004. For , let be the th row of the matrix in (2.2). Then for two different marginal series of , say and (), we have

| (2.14) |

The relation (2.14) shows that the conditional contemporaneous covariance between two different marginal series of is represented by a weighted inner-product of the corresponding rows of . To help interpret (2.14), we postulate the existence of a -dimensional Euclidean space of unobserved (latent) characteristics. The latent characteristics determine the contemporaneous dependence between the marginal series of . We further assume that each marginal series of is associated with a position in this latent space and the pattern of contemporaneous dependence among the marginal series of can be characterized by their latent positions. Such a setup is also used in latent space network models, see e.g., Hoff2002; Hoff2005. From (2.14) we can see that, when the above latent space setup is adopted to the reduced-rank covariance model (2.2), the dimensions of the latent space are represented by the columns of while the latent positions are given by the rows of . Therefore the matrix provides a tool to represent the -dimensional contemporaneous dependence structure in a lower-dimensional space. In addition, if we are able to find interpretations for different columns of by taking advantage of exogenous information, such interpretations will help identify the unobserved characteristics that are important in forming the contemporaneous dependence relationship. The heuristics behind such a latent space setup is similar to that of multidimensional scaling (MDS), see e.g., Borg1997, in that both methods are concerned with “spatial” representations of observed patterns of dependence among a group of subjects, such as the marginal series of in our case. However, the MDS method is not model-based and it constructs spatial representations in an ad-hoc manner; in contrast, the above latent space setup leads to model-based graphical representations of the contemporaneous dependence structure via inference of the reduced-rank covariance model. In Section 3.2, we illustrate via real data examples the use of this latent space setup in interpreting results from the reduced-rank covariance estimator in a VAR model.

3 Numerical results

3.1 Simulation

As mentioned in Section 1, there are three major classes of covariance estimators under large dimensionality: shrinkage, regularization and structural covariance. The reduced-rank (RR) estimator can be viewed as a structure covariance estimator, as discussed in Section 2.1. One difference between the three classes of covariance estimators is that, under finite samples, invertibility of the covariance estimator holds for the shrinkage and the structural approach, but not guaranteed for the regularization method. Due to this difference, in the simulation study we compare the reduced-rank covariance estimator with shrinkage estimators for their performance of estimating large dimensional covariance matrices from independent observations. The earliest attempt of shrinkage covariance estimation is given in Stein1975 and since then many shrinkage estimators have been proposed, see e.g., Dey1985; Daniels2001; Ledoit2003; Ledoit2004; Schafer2005. A shrinkage covariance estimator is obtained by shrinking the sample covariance matrix towards a target covariance structure. The balance between these two extremes is controlled by the shrinkage intensity, a tuning parameter that needs to be estimated from data. A review of commonly-used target covariance structures is given in Schafer2005.

We consider two shrinkage covariance estimators: one is proposed in Ledoit2004 (LW2004) and the other one is given by Schafer2005 (SS2005). The two shrinkage estimators differ in their choices of the target covariance structure. We generate independent replicates from a -dimensional Gaussian under three cases:

-

(I)

.

-

(II)

has all covariances set to 0.16 and variances set to (the first two entries are 1.0 and the remaining entries are 0.5).

-

(III)

has the th covariance set to and variances set to (the ascending sequence from 0.47 to 0.75 with increment 0.02).

Case (I) gives a very simple covariance structure; Case (II) serves as an example of the reduced-rank covariance structure (2.2) with the reduced-rank ; Case (III) does not satisfy the reduced-rank covariance model (2.2). We take the dimension and the sample size . In applying the RR covariance estimator, the reduced-rank is selected from according to a minimum BIC, which is computed as in (2.9). In applying the two shrinkage estimators LW2004 and SS2005, their shrinkage intensities are determined analytically as described in Ledoit2004 and Schafer2005, respectively.

First we investigate the RR covariance estimator’s performance of inferring the reduced-rank when the true underlying covariance matrix admits a reduced-rank structure (2.1). We use the in Case (II) as an example, which satisfies the reduced-rank covariance assumption with the reduced-rank . Table 2 summarizes the frequencies (out of 500 replications) of the estimated reduced-rank for different sample sizes. We can see that when the sample size is relatively small, e.g., and , the RR covariance estimator tends to under-estimate the reduced-rank; as the sample size increases, the probability of selecting the correct reduced-rank increases accordingly. In particular, when the sample size reaches 400, the RR covariance estimator has a large probability of selecting the correct reduced-rank .

| 50 | 447 | 52 | 1 | 0 |

| 100 | 304 | 153 | 43 | 0 |

| 200 | 30 | 146 | 324 | 0 |

| 400 | 0 | 0 | 500 | 0 |

Next we compare the performance of the RR covariance estimator with the two shrinkage covariance estimators LW2004 and SS2005. We use two metrics for the comparison: the first metric is based on Stein’s loss (SL) James1961, which is defined by . It can be shown that Stein’s loss is equal to (up to a constant multiplier) the Kullback-Leibler divergence Kullback1951 between two -dimensional Gaussians and ; and the second metric is the mean squared error (MSE), which is defined by . We use Stein’s loss to characterize the eigen-structure of covariance estimators while we also consider point-wise estimation accuracy of covariance estimators by comparing their MSE.

Table 3 summarizes the percentage reductions (with standard errors in brackets) in Stein’s loss and MSE of each covariance estimator as compared to the sample covariance matrix. For each setting, the largest reduction among the three estimators is marked in bold. We can see that all three covariance estimators lead to improvement over the sample covariance matrix for both Stein’s loss and MSE. For Case (I), where the true has a very simple structure, all three covariance estimators achieve similar improvement over the sample covariance matrix for both Stein’s loss and MSE. It is more interesting to compare the three covariance estimators when the structure of becomes more complicated in Cases (II) and (III). For Case (II), where the reduced-rank covariance assumption (2.1) is satisfied, we can see that the RR covariance estimator leads to significant improvement over the sample covariance matrix in Stein’s loss for various sample sizes. At the same time, for small-to-medium sample sizes, such as and , the improvement in Stein’s loss from the two shrinkage estimators LW2004 and SS2005 is comparable to that from the RR covariance estimator; as the sample size increases, such as and , the improvement in Stein’s loss from the two shrinkage estimators becomes much less significant. We can also see that the improvement in MSE from all three covariance estimators is less significant as compared to their improvement in Stein’s loss. For Case (III), it is interesting to see that even if does not satisfy the reduced-rank covariance model (2.1), the RR covariance estimator still results in significant improvement in Stein’s loss over the sample covariance matrix for all sample sizes. In addition, the improvement in Stein’s loss from both the RR covariance estimator and the two shrinkage estimators is much more significant than their improvement in MSE. To explain the performance of the RR covariance estimator in Case (III), we point out that the largest eigen-value of in Case (III) is dominant over the remaining eigen-values. As a result, the eigen-structure of is close to that of a reduced-rank covariance matrix, even though in Case (III) does not satisfy the reduced-rank covariance model (2.2).

| percentage reduction in SL | percentage reduction in MSE | ||||||

|---|---|---|---|---|---|---|---|

| RR | LW2004 | SS2005 | RR | LW2004 | SS2005 | ||

| I | 50 | 99.1 (0.053) | 98.3 (0.080) | 97.8 (0.096) | 99.0 (0.067) | 98.1 (0.094) | 97.5 (0.111) |

| 100 | 99.2 (0.051) | 98.5 (0.076) | 97.9 (0.100) | 99.1 (0.056) | 98.4 (0.082) | 97.7 (0.105) | |

| 200 | 99.2 (0.055) | 98.6 (0.074) | 97.8 (0.101) | 99.1 (0.060) | 98.5 (0.079) | 97.8 (0.106) | |

| 400 | 99.2 (0.045) | 98.6 (0.073) | 97.7 (0.109) | 99.2 (0.047) | 98.5 (0.074) | 97.6 (0.110) | |

| II | 50 | 68.3 (0.242) | 50.1 (0.219) | 47.4 (0.226) | 18.3 (0.460) | 12.4 (1.243) | 14.8 (1.228) |

| 100 | 48.7 (0.468) | 30.3 (0.162) | 27.5 (0.139) | 0.0 (0.531) | 6.5 (1.067) | 8.6 (1.017) | |

| 200 | 51.2 (0.927) | 16.3 (0.102) | 14.5 (0.079) | 7.3 (1.056) | 2.7 (0.839) | 4.0 (0.799) | |

| 400 | 64.3 (0.277) | 8.6 (0.073) | 7.5 (0.056) | 22.9 (0.298) | 1.5 (0.612) | 2.2 (0.580) | |

| III | 50 | 77.8 (0.334) | 69.7 (0.204) | 68.1 (0.242) | 37.2 (1.562) | 38.5 (0.880) | 39.4 (0.888) |

| 100 | 71.4 (0.254) | 50.5 (0.183) | 47.2 (0.264) | 47.6 (0.601) | 23.0 (0.911) | 23.9 (0.878) | |

| 200 | 53.9 (0.275) | 31.8 (0.128) | 28.7 (0.196) | 37.5 (0.381) | 12.5 (0.813) | 14.0 (0.756) | |

| 400 | 20.5 (0.458) | 18.0 (0.097) | 15.7 (0.163) | 16.3 (0.348) | 7.7 (0.633) | 8.6 (0.571) | |

3.2 Real data examples

We apply the reduced-rank covariance estimator to VAR modeling of two real data examples. The first example is concerned with stock returns in S&P 500 and corresponds to the first scenario in Section 2.2, i.e., there are no constraints on the AR coefficients of the VAR model. The second example is a time series of temperatures in southeast China and corresponds to the second scenario, i.e., there are zero-constraints on the AR coefficients. For both examples, we use the latent space setup introduced in Section 2.2 to interpret results of the reduced-rank covariance estimation.

Stock returns from S&P 500. In the first example, the data consist of daily returns of stocks in S&P 500 and the stocks come from 4 sectors: energy, industry, finance and technology. The returns are calculated as the logarithm of the ratio between two consecutive daily closing prices from the trading days in 2006. Figure 1 displays the first 60 observations of the return series.

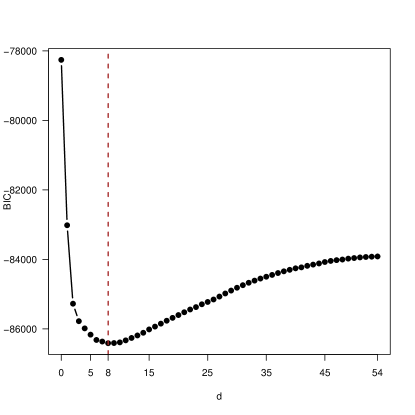

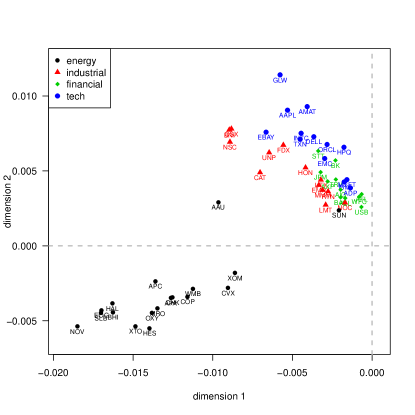

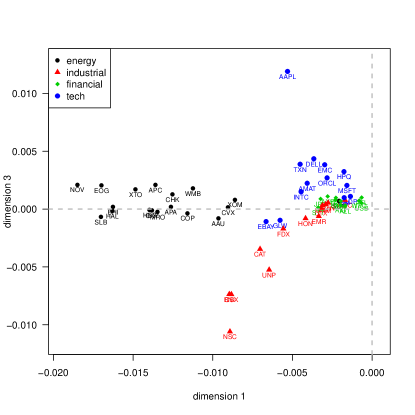

Our interest is to describe the pattern of contemporaneous dependence between the returns of the 55 stocks. For this purpose, we apply the reduced-rank covariance estimator to the VAR modeling of the 55-dimensional return series. We first use the 2-step method, which is described in the first scenario in Section 2.2, to fit a VAR model with unconstrained AR coefficients and a reduced-rank noise covariance matrix. In particular, we first fit an unconstrained VAR(1) model to the 55-dimensional return series, where the autoregression order is selected from according to a minimum BIC. Then we obtain the reduced-rank covariance estimator based on the residuals from the fitted autoregression. We select the reduced-rank from according to a minimum BIC, which is computed in equation (2.9). Panel (a) in Figure LABEL:spStock_rr_combine displays the BIC curve as varies and it shows that the minimum BIC occurs when . In other words, the contemporaneous dependence structure between the 55 stocks’ returns can be well represented in a 8-dimensional latent space. Panels (b), (c) and (d) in Figure LABEL:spStock_rr_combine display the layouts of the 55 stocks in the first 3 dimensions of the 8-dimensional latent space, where the color indicates the sector each stock belongs to. Panel (b) corresponds to the first 2 dimensions of the latent space and we can observe a “clustering” phenomenon of the 55 stocks in these 2 dimensions. Specifically, the within-sector contemporaneous dependence is most noticeable among the energy stocks, since they are positioned close to each other while far away from the origin of the latent space. We also observe that most of the energy stocks have the opposite sign along the second dimension of the latent space as compared to stocks from the industry, finance and technology sectors. This means that returns of the energy stocks are negatively contemporaneously related to stock returns from the other 3 sectors. On the other hand, the within-sector contemporaneous dependence is much weaker among the finance stocks, since those stocks are positioned close to the origin of the latent space. Moreover, panel (b) also shows that the first 2 dimensions provide information for separating the energy sector from the other 3 sectors, but not for distinguishing among the industry, finance and technology stocks. One exception is that there also exists separation between the industry and the technology sectors. This separation becomes more noticeable after we take into account the third dimension of the latent space. From panels (c) and (d), both of which display the third dimension along the vertical direction, we can see that the third dimension is informative for separating the industry from the technology stocks, while it has little power for distinguishing between the energy and the finance sectors.

As a diagnostic check, Figure LABEL:spStock_rr_ACF_CCF_delta displays the auto-correlation (ACF) and cross-correlation functions (CCF) among the first 4 dimensions of the estimated latent variable as computed in (2.10) and it exhibits little significant auto- or cross- correlation. In fact, we observe little significant auto- or cross- correlation among all 8 dimensions of . This observation is consistent with the assumptions of the reduced-rank covariance model.