Estimation of Joint Distribution of Demand and Available Renewables for Generation Adequacy Assessment

Abstract

In recent years there has been a resurgence of interest in generation adequacy risk assessment, due to the need to include variable generation renewables within such calculations. This paper will describe new statistical approaches to estimating the joint distribution of demand and available VG capacity; this is required for the LOLE calculations used in many statutory adequacy studies, for example those of GB and PJM.

The most popular estimation technique in the VG-integration literature is ‘hindcast’, in which the historic joint distribution of demand and available VG is used as a predictive distribution. Through the use of bootstrap statistical analysis, this paper will show that due to extreme sparsity of data on times of high demand and low VG, hindcast results can suffer from sampling uncertainty to the extent that they have little practical meaning. An alternative estimation approach, in which a marginal distribution of available VG is rescaled according to demand level, is thus proposed. This reduces sampling uncertainty at the expense of the additional model structure assumption, and further provides a means of assessing the sensitivity of model outputs to the VG-demand relationship by varying the function of demand by which the marginal VG distribution is rescaled.

Keywords - power system planning; power system reliability; risk analysis; wind power

1 Introduction

Probabilistic risk assessment has been used widely for many years in generation and network capacity planning, both in industry and in academic research [1, 2, 3, 4]. There has been particular focus recently on the inclusion of variable generation (VG) technologies within these calculations, on which there is a wide literature on topics such as wind ([5] and references therein), solar ([6] and references therein), tidal [7] and wave [8].

As with any modelling work, estimation of model inputs from data forms a critical part of resource adequacy assessment. The literature on this is vast and cannot be reviewed in full within a single research paper, however the IEEE Task Force on Capacity Value of Wind Power survey [5] and the recent Special Section of IEEE Transactions on Power Systems on Adequacy in Power Systems provides a representative survey [9] of current activity. All these papers use model inputs which must in some way be estimated from data, with [10] placing particular emphasis on time series modelling of the VG resource.

The approach taken to the statistical modelling of available VG capacity depends on the modelling outputs which are required. Where only expected value risk indices are required then, unless significant storage has a substantial effect of results, it is entirely sufficient to use a ‘time-collapsed’ or ‘snapshot’ model, which does not need to consider statistical associations over time in demand and generation availability. In contrast, where outputs such as frequency and duration indices (which depend on time correlations in generation availability and demand) are required, then it is necessary to build a time series model of VG output, for instance the ARMA model used in [10]. This paper will consider only the former case, i.e. time-collapsed models – practical adequacy studies such as those in GB [11] and PJM [12] typically use this class of model.

Within adequacy models it is often natural to assume that available conventional capacity is independent of all else, and it is then necessary to estimate a predictive joint distribution of demand and available VG relevant to a future point in time. The most popular approach to this in the VG-integration literature is to use the empirical historical distribution of demand-net-of-VG [5] (this is sometimes referred to as the ‘hindcast’ approach). While this approach by definition accounts for any relationship between demand and available capacity as seen in the historical data, results are usually presented without consideration of sampling uncertainty arising from the finite quantity of data available for statistical estimation. Of those papers which do discuss this issue, [5] provides discussion of the need for multiple years of data in order to provide meaningful model results, but does not discuss in detail quantitative assessment of uncertainty in model outputs such as risk and capacity value indices. [13] provides an assessment of how many years of data are required for a robust calculation in Ireland, but the approach is limited by an implicit assumption that the longest available historic record is sufficient to make a precise point estimate.

Such uncertainty assessment is particularly important in adequacy, as the risk tends to be dominated by a small number of periods of high demand and low VG availability, and thus the available quantity of directly relevant data on times of high demand and low VG is usually small. Without an assessment of this statistical uncertainty, the relationship between risk model outputs and the real world cannot be assessed.

Bootstrap analysis of uncertainty [14] places a confidence interval on a model output such as LOLE or capacity value metrics, by repeating the output calculation using a large number of input datasets of the same size as the original one, each created by resampling with replacement from within the original dataset. This paper will show how realistic uncertainty assessments may be obtained by resampling in blocks of 1 week to account for serial correlations within the input demand and generation data; even within the time collapsed model, it is necessary when assessing confidence intervals on results to account for such serial correlations in the historical data. This proposed approach is a major advance on previous work, in that unlike [13] it allows quantitative confidence intervals to be placed on risk model outputs, and requires no prior assumption as to the quantity of data required.

While the hindcast approach naturally accounts for the demand-VG relationship as seen in the data, model outputs derived from hindcast may be driven mostly by a very small number of historical records with high demand and low VG resource. Thus, as our analysis demonstrates, the uncertainty associated with outputs estimated via this approach may be very high. This paper proposes an alternative approach, in which the marginal distribution of available VG conditional on being in the peak season (when extremes of demand might occur) is estimated, and the distribution of VG output conditional on demand is constructed by rescaling the marginal VG distribution according to a factor which depends on the demand level; this scaling function is estimated from historical data. This provides a degree of statistical smoothing enabling both considerably more accurate estimation and an ability to perform sensitivity analysis through varying the parameters of the scaling function, albeit at the expense of the, relatively modest, additional model structure assumptions required.

The paper [15] combined a detailed survey of the available results in the probability theory of capacity values with a brief preliminary discussion of statistical modelling issues. The present paper provides a very substantial advance over [15] in its fully detailed treatment of statistical issues, including consideration of serial associations in data when assessing sampling uncertainty in model outputs, and possible approaches to remedying the failures of the hindcast approach at high wind penetrations.

The probability model used for adequacy assessment is presented in Section 2, and then the new statistical modelling approaches (the fully developed bootstrap analysis, and the rescaling the VG distribution according to demand) are described in detail in Section 3. While these statistical approaches have recently been used in the GB statutory Electricity Capacity Assessment Study [11], this is the first time that the underlying modelling methodology or similar approaches has been presented and analysed in full in the technical literature. The data used for the examples are then described in Section 4, and the corresponding results are given in Section 5. Finally conclusions and discussion of wider application are presented in Section 6.

2 Mathematical Model

2.1 Probability Model

This paper will consider a single-area or spatially-aggregated model, i.e. it ignores transmission constraints to estimate the distribution of the surplus of total supply over total demand within a region, without reference to the geographical locations within the region of individual supplies and demands. This is sometimes also referred to in the power systems literature as a Hierarchical Level 1 (HL1), copper-sheet or single bus model.

The model considers a randomly chosen, or typical, time instant within the season to be considered, and consists of a specification of the joint distribution of the random variables , and which represent respectively available conventional generation, available variable generation and demand at a randomly chosen point in time. This is referred to as a time-collapsed or snapshot model, and is the class of model used in many practical adequacy studies, e.g. the GB Capacity Assessment Report [11] explicitly uses the term time-collapsed, and other studies which output expected value indices and use this class of model are described in [16, 12].

Then the random variable

models the excess of supply over demand at that time. Statistical analysis consists of the estimation of the joint distribution of the random variables , and (see below), and the output of the model is the estimated distribution of .

The random variable , modelling available conventional generation, is assumed to be independent of the pair . In a model for a peak season, when there will be limited planned maintenance due the possibility of very high demand and associated high prices, this assumption is typically made, and is natural under most circumstances. While there is recent experience of this assumption breaking down (cold weather events in Great Britain Feb 2012, Texas Feb 2011, Eastern Interconnection winter 2013-14), the quantity of relevant data is so minimal that this may only be treated by scenario analysis. In other seasons this assumption might not be so natural if maintenance schedules can be flexed in response to anticipated tight margins. The marginal distribution of is taken as an input to the model, i.e. we proceed on the basis that it is known; typically the distribution of will be taken as that of the convolution of the distributions of the available capacities of the individual generating units, those outputs being themselves assumed statistically independent.

2.2 Adequacy Indices

In particular, the loss of load probability (LOLP) and expected power unserved (EPU) are defined by

| (1) | |||||

| (2) |

where and denote probability and expectation respectively. The LOLE is then defined to be LOLP multiplied by the number of demand periods (e.g. hours or days depending on time resolution of demand data) in the season modelled, while the EEU is defined to be EPU multiplied by the length of the season.

If , and are the demand and available generating capacities at a randomly chosen point in time, this formulation is precisely equivalent to the more usual specification of LOLE and EEU as respectively the expected number of periods of shortfall, and the expected total energy demanded but not supplied, in the future season under study. The snapshot formulation will prove convenient for specifying statistical estimation procedures in the next section, and is used in [15, 17] to derive a number of analytical results associated with generation adequacy and capacity values.

2.3 Capacity Value Metrics

It is common also to use capacity value metrics to visualise the contribution of VG capacity within adequacy assessments. In general, these specify a deterministic quantity which is equivalent in adequacy terms to the VG capacity within the calculation under consideration.

The two most commonly used capacity value metrics are Effective Load Carrying Capability (ELCC), the additional demand which the VG resource supports while maintaining the same risk level, and Equivalent Firm Capacity (EFC), the completely reliable capacity which would give the same risk level if it replaced .

Defining , the margin of conventional capacity over demand, the ELCC may be defined as the solution of

| (3) |

and the EFC as the solution of

| (4) |

The choice of capacity value metric for a particular application should be the definition most appropriate to that application, which may be ELCC, EFC or another alternative. The metrics ELCC and EFC are closely related mathematically, and results and techniques applicable to one may easily be transferred to the other [17].

This paper will use EFC for examples of capacity value estimation, as it visualises the contribution of VG resource within a particular future scenario, and thus answers a quite generally relevant question when studying such a scenario. However, in our examples below, similar conclusions would be obtained were ELCC to be used instead.

3 Statistical estimation

Various assumptions may be made about the statistical relation between and for the purpose of estimating the joint distribution of the pair . This section will describe the principal options available, and the consequent assessment of uncertainty in model outputs. As discussed in the introduction, without such uncertainty assessment the relationship between model results and the real system is unclear, and thus robust interpretation of modelling results is not possible.

3.1 Possible modelling assumptions

Typically one has available for estimation a time series of historical observations of the pair . For demand, an ‘observation’ will typically mean historical metered demand appropriately rescaled to the underlying demand levels in the future scenario under study. For renewables, an ‘observation’ may refer to either metered historical output rescaled to the scenario under study, or a synthetic observation of renewable output combining historical resource (wind speed or solar irradiance) data with the future installed capacity scenario.

If no assumption is made regarding the statistical relation between and , the distribution of (i.e. demand-net-of-variable-generation) is estimated directly from the empirical distribution of the observations (with the observations and , appropriately rescaled as described earlier). The simplest option, where the distribution of is taken to be the empirical distribution of , is often called the hindcast approach; it then follows from the independence of and all else that, for example, we have

where is the cumulative distribution function of and is the total number of observation periods. The hindcast approach has been used widely in the literature, for instance by the IEEE Task Force on Capacity Value of Wind Power [5].

Typically, however, historical measurements corresponding to the extreme right tail of the distribution of are extremely sparse. This means that without making some reasonable assumption about the form of the statistical relationship between and , confidence intervals associated with quantities such as LOLE and EEU (which are determined primarily by this right tail) are so wide that the results are of limited practical use.

Making some such assumption usually results in considerably narrower confidence intervals representing sampling uncertainty in model outputs, as compared to those obtained from the use of hindcast, at the expense of any additional uncertainty arising from the assumption itself. Additionally, a further benefit of assuming a parametrised form of the relationship may be the ability to perform transparently an analysis of the sensitivity of model outputs to that relationship.

The simplest such assumption is that and are independent. In most systems, a general assumption of year-round independence of and will be unrealistic for most practical applications; however, where there is no strong diurnal variability in variable generation availability (e.g. for wind in the peak winter season in GB), an assumption of independence conditional on being in the peak season may be quite reasonable.

A further possibility is to assume that the distribution of conditional on is given, for each value of , by the marginal distribution of rescaled by some factor , i.e. by the distribution function where is the marginal distribution function of . Note that, given , the marginal density of Y which is being implicitly assumed in our analysis is given by

| (5) |

(where the pdf is the derivative of the distribution function specified earlier in this paragraph), and this is not in general quite the density . However, in the case where, as here, we take except for in a set of small probability, we have approximate equality between these two densities. Further when, again as here, we have for all , the approximation is conservative in that it assumes, if anything, less VG than might be suggested by its empirical marginal distribution.

When some assumption is made as above about the statistical relationship between and , the marginal distributions of these random variables are then estimated separately from the available data for each, and combined with this assumption to obtain the distribution of . The distribution of is then the convolution of the distributions of and of .

This approach was taken in the 2014 GB Capacity Adequacy Study, where the reference case (wind-demand independence conditional on being in the peak season) was contrasted with a sensitivity in which the scale factor above was taken to be close to one except for the most extreme values of demand , where it was reduced to as low as , corresponding to the assumption of reduced wind at times of very high demand.

3.2 Assessment of Uncertainty in Model Outputs

In the case where the joint distribution of all the variables involved has an assumed analytical representation – e.g. that these variables are independent and that the distribution of each has some assumed parametric form – we may use standard analytical techniques for the derivation of standard errors, confidence intervals, etc. However, it is usually the case that such an assumed framework is not available. We may then use instead modern simulation techniques, notably bootstrapping [18, 14]. This is applicable to any adequacy calculation approach, including those described earlier in this section.

In the case where successive instances of the pair may be treated as independent and identically distributed, i.e. there is no serial association over time, bootstrapping consists of resampling with replacement individual records from the original data; each such bootstrap sample is of the same size , say, as the original data set, and for each sample the statistic of interest (e.g. the chosen estimate of ) is calculated; the distribution of this statistic over a sufficiently large number of bootstrap samples mirrors the sampling properties of the original estimator, under the assumption that the data are themselves a set of independent identically distributed observations (see [14] for a complete description).

However, where there does exist serial association in the successive observations of the pairs , as will typically be the case in practice, then some modification of the bootstrap procedure is required. One option is to resample from the original data in blocks, where each such block is sufficiently large that the successive blocks may be treated as at least approximately independent.

4 Data for Examples

The examples in this paper are based on National Grid’s ‘Gone Green 2013’ (GG) scenario [19] for the GB power system in Winter 2013/14 (National Grid is the GB Transmission System Operator). As not all fine detail of the GG scenario can be shared by National Grid, the generating unit capacities used here are adjusted slightly from those in the original GG scenario; the scenario used here is thus referred to as ‘Adjusted Gone Green’ (AGG). It is thus generally representative of GB system scenarios, and will serve well to illustrate the methodological points made in this paper. All other historical data used as inputs to the calculations are also supplied by National Grid.

4.1 Demand Data

Coincident Great Britain wind resource and demand data are available for the seven winters 2005-12. The demand data are based on the historical metered demand available publicly at [20]; an estimate of historical distribution-connected wind output is added on to each transmission-metered demand record, allowing distribution- and transmission-connected wind to be treated on a common basis when studying future scenarios.

Historical demand data may be rescaled to a required underlying level using each winter’s average cold spell (ACS) peak demand, which for the 2013/14 AGG scenario is 55.55 GW. ACS peak demand is the standard measure of underlying peak demand level in Great Britain; conditional on a given underlying demand pattern, it is the median out-turn winter peak demand [21].

The historical metered demand data are on a half-hourly time resolution. However as the wind data used here are on a one-hour resolution, the demand series is converted to hourly observations by taking for each hour the higher of the two half-hourly demands contained therein.

In order to account for the operator’s practice of taking emergency measures such as demand reduction in preference to eroding the frequency response which protects the system against sudden losses of infeed, 700 MW is added to all demand values to balance the capacity of conventional generation that is used to provide this response. This is consistent with the statutory Capacity Assessment Study [11].

4.2 Wind Data

The GB aggregate wind power historical time series combines wind speed resource data from NASA’s MERRA reanalysis dataset with the AGG scenario for installed wind capacity in 2013/14 (in which aggregate installed capacity is 10120 MW). These data may thus be treated as observations of historical available wind capacity assuming this capacity scenario.

For the examples presented, these wind power data are rescaled to different installed capacities while maintaining the same time series of wind load factor. This permits study of the dependence of results on total installed wind capacity while holding other data constant. The origin of this dataset is described in more detail in [11].

4.3 Conventional Plant Data

The available capacity from each individual unit is assumed to follow a two-state distribution with either zero or maximum capacity available. The unit capacities are taken from the 2013 AGG scenario, and the availability probability for each class of unit is the central estimate from the Great Britain Electricity Capacity Assessment Report [11].

The distribution of available conventional capacity is then constructed assuming that the availabilities of the different units are statistically independent. The result of convolving these distributions is usually referred to in power systems as a capacity outage probability table [1]. For the 2013/14 scenario used, the distribution of available conventional capacity has mean 58820 MW and standard deviation 1950 MW.

As the focus of this paper is on the treatment of wind and demand data, the distribution of will not be discussed further here. Examples of sensitivity of LOLE outputs to the distribution of may be found in [11], and further discussion of statistical issues associated with constructing the distribution of may be found in [22].

4.4 Data Visualisation

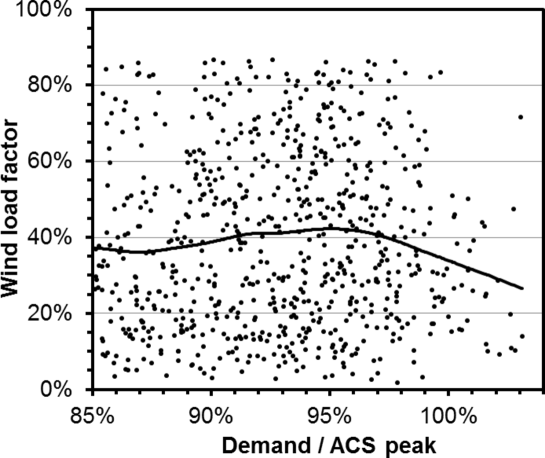

The available demand and wind data from times of high demand are visualised in Fig 1. The plot shows system-wide available wind load factor against demand (each demand data point is normalised by that winter’s ACS peak, and we consider those data points for which the normalised demand exceeds 90%). For clarity, only data points from times of daily peak are plotted. The smooth solid line is an estimate of the mean wind load factor conditional on the daily peak demand. This is fitted using the LOESS local regression method [23], and some experimentation shows that it is robust against varying choices of the width of the smoothing window.

It is clear from this plot that the quantity of data arising from times of truly extreme demand is very small. Indeed, of the 30 days on which ACS peak was exceeded during these seven winters, 23 were in January 2009 and December 2010 and a further 5 in December 2008–January 2009. Due to the serial associations inherent in weather patterns, there is only one completely independent data point provided by each of these periods in 2009 and 2010.

5 Results on Statistical Estimation and Uncertainty Analysis

5.1 Bootstrap Analysis of Uncertainty for LOLE and EFC Results

5.1.1 Bootstrap analysis

This section provides an example application of the parameter estimation and bootstrap uncertainty assessment procedures described in Section 3. The wind and demand data, and the conventional plant distribution, are as described in Section 4. Estimation both of the LOLE and wind EFC (as defined in Section 2) is considered.

The calculations consider only the peak season, which in GB dominates the adequacy risk; a similar bootstrap approach could be applied to wind and demand data in other seasons, in the context of a year-round calculation which models maintenance explicitly. From each of the seven winters, 20 weeks of coincident wind and demand data are used, beginning on the first Sunday in November. In each winter a 2-week Christmas block is defined, giving in the data set as a whole seven 2-week Christmas blocks and 126 1-week ‘normal’ blocks, each block running from Sunday to Saturday.

For each of the statistical approaches described above, once parameter estimates are obtained (e.g. of EFC or LOLE), bootstrap resampling may be used to make to corresponding assessments of uncertainty, as described in Section 3. In each case we use resampling from the original data to generate 1000 bootstrap samples of the same size as that of the original 7-year data set; for each such sample we may readily calculate model outputs such as EFC, LOLE, etc. As noted previously, the variability of these estimates over the bootstrap samples provides the corresponding uncertainty assessments associated with the original central estimates of the model outputs.

For the hindcast approach, each bootstrap sample is obtained by resampling (with replacement) seven 2-week Christmas blocks and 126 1-week ‘normal’ blocks from the bivariate time series of historical wind and demand. Using the alternative approaches of assuming wind-demand independence or rescaling the marginal distribution of wind according to demand level, each bootstrap sample is obtained by sampling (again with replacement) independently from the metered wind and demand time series. For demand, 126 ‘normal’ 1-week blocks and 7 Christmas 2-week blocks are resampled; however for wind, 140 week-long blocks are sampled from the 140 week long blocks in the full time series (unlike demand, wind data from the Christmas period has no special status).

5.1.2 Results

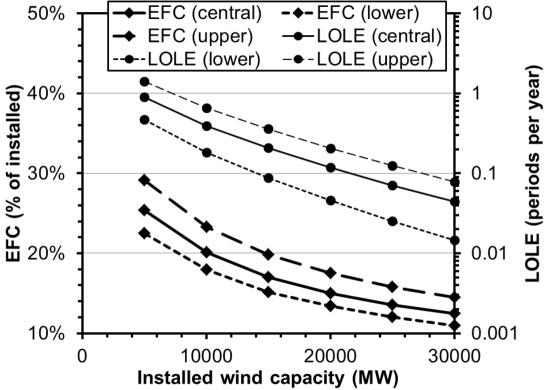

Figures 2 and 3 show LOLE and EFC results derived respectively from hindcast estimation and using the assumption of wind-demand independence, in each case along with 95% confidence intervals derived via bootstrap resampling. EFC is shown as a percentage of installed capacity.

Features of particular note in the plots are:

-

•

In the hindcast calculation, the ratio of the upper and lower ends of the LOLE confidence interval increases very substantially as the installed wind capacity increases, until at 30 GW installed capacity the ratio between the CI’s upper and lower limits is 4.6. This is a consequence of how, in a hindcast calculation, only the very small number of historical records with both high demand and low wind load factor make a substantial contribution.

-

•

In the calculation which assumes wind-demand independence, the ratio of the upper and lower limits of the LOLE CI barely changes as the wind capacity increases. In this case, while data on times of very high demand remain sparse, the quantity of wind data used in estimating the distribution of is comparatively large. The consequences of data sparsity within the EFC and LOLE calculations hence increase only very slightly as the installed wind capacity increases.

-

•

The relative uncertainty in EFC appears much less than that in LOLE. There is some degree of cancellation between the uncertainties in the distributions of demand on each side of the equation defining EFC. Due to the highly nonlinear dependence of LOLE on shifts of the distribution of margin, there is also a tendency for precisely the same uncertainty to appear less substantial when expressed in MW terms through capacity values.

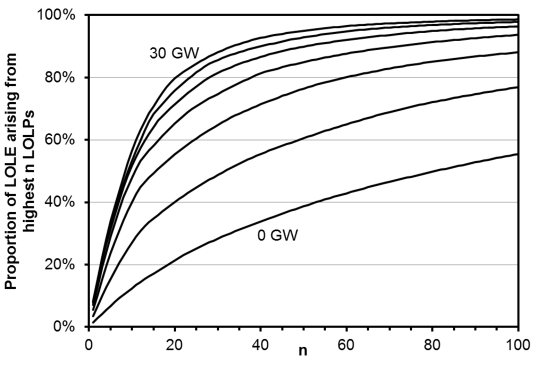

As discussed above, the hindcast results suffer at large wind capacities from such large sampling uncertainty that they are of very little value. The origin of this is explored further in Fig. 4, in which it is seen that at large installed wind capacities in this GB example LOLE results are driven by a very small number of items of historical data combining high demand with low wind resource. Indeed at 30 GW installed wind capacity 2/3 of the calculated LOLE arises from data from just 6 days (1 in each of winters 06-07, 09-10 and 11-12, and 3 in 10-11).

While sampling uncertainty is much reduced in the ‘wind-demand independence’ results, that assumption introduces additional uncertainty, arising from the possibility that there might indeed be some substantial wind-demand statistical relationship which cannot be quantified with the available data. This problem is addressed in the next section.

5.2 Rescaling of Wind Distribution

If the distribution of is to be rescaled by a demand-dependent factor as described in Section 3, then may, for example, be estimated based on a wind v. demand plot and smoothed relationship as in Fig. 1. For the available data, this figure shows a decrease from a mean load factor of around 40% on days of relatively modest demand, to a level of 20–30% at the times of very highest demand. However, as discussed in Section 4.4, the data corresponding to the very high demands almost all arise from just three distinct periods in the three winters 2008-11. The data from these winters cannot be said to provide more than three independent data points, and are thus insufficient to provide a point estimate of with any real confidence.

We can however estimate a range of credible model outputs (i.e. LOLEs and EFCs) by providing credible optimistic and pessimistic bounds on the scaling function corresponding to the highest demands. As there is no evidence to suggest that the wind resource is better at times of very high demand compared to that across the peak season as a whole, a credible upper bound is , i.e. wind-demand independence. We take as a credible lower bound a rescaling function of the form

| (6) |

where , , , and . This is substantially more pessimistic than that suggested by the smoothed relationship in Fig. 1; we do not believe that the data provide a justification for considering a relationship which is more pessimistic still.

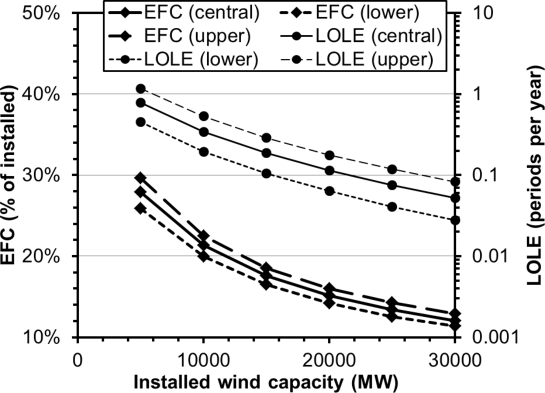

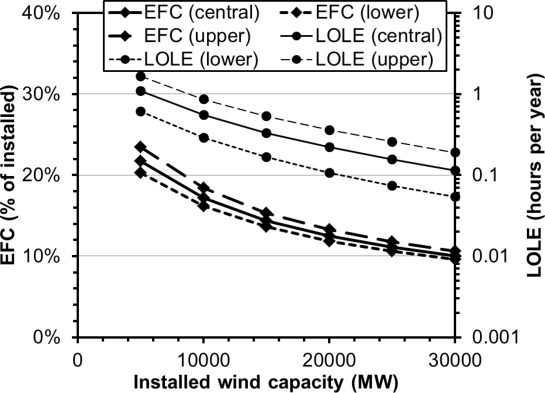

Results for this pessimistic bound on wind’s contribution are displayed in Fig. 5. In this case the extent of the confidence intervals increase very slightly as the installed wind capacity increases, and the ‘rescaled ’ approach has thus achieved its aim (as compared to hindcast) of giving much reduced sampling uncertainty in exchange for an additional natural model structure assumption.

Performing this pessimistic rescaling of the distribution of available wind increases the central estimate of LOLE by a factor which ranges from 1.4 (relative to the wind-demand-independence case) at 5 GW of installed wind capacity, to 2.2 at 30 GW installed capacity. However, the interpretation of the EFC plot is more transparent. The difference between the EFC of the wind with and without the pessimistic rescaling is 6.2% of installed capacity (310 MW) for 5 GW installed wind capacity, and 2.0% of installed capacity (600 MW) at 30 GW installed wind.

It should be remembered that the choice of these optimistic and pessimistic bounds on the scaling function arise from very considerable uncertainty (i.e. very sparse data indeed) regarding the wind resource at the times of the very highest demands. However, the corresponding variation of the EFC result (just MW at 30 GW installed capacity) demonstrates that compared to other uncertainties in inputs the consequences of this uncertainty in the wind-demand relationship are relatively unimportant; examples of such more important uncertainties include

-

•

uncertainty in future ACS peak level is of order 1 GW or more;

-

•

uncertainty over which conventional units will commission or decommission – to leading order, adding or withdrawing a single unit or station shifts the distribution of available capacity by its rated capacity, which may be up to around 1 GW in the case of CCGT or 1.8 GW in the case of nuclear;

-

•

uncertainty in conventional unit availability probabilities – to leading order, a 1 percentage point change in the mean available conventional capacity shifts the distribution of available capacity by around 700 MW.

These are all substantially larger than the range of credible wind EFCs arising from uncertainty in the wind-demand relationship.

6 Conclusions

This paper has described new statistical approaches to the estimation of inputs and assessment of uncertainty in outputs of generation adequacy risk models. Bootstrap analysis provides a generally applicable statistical means of quantifying the consequences of sampling uncertainty; a key observation is that where data on the coincidence of high demand and low VG are very sparse, sampling uncertainty in hindcast calculations may be so great as to render model results quite meaningless. A new approach of rescaling the marginal distribution of available VG according to demand level is thus proposed; this adds an additional – but not unreasonable – model structure assumption, but considerably reduces sampling uncertainty; the use of alternative scaling functions further facilitates analysis of the sensitivity of model outputs to variation in the assumed wind-demand relationship.

In using this bootstrap analysis, one must remember that it only assesses one aspect of uncertainty in these calculations, namely that arising from the use of a finite-size data set within a given statistical estimation process. Other uncertainties which should be considered include that in the distribution of available conventional capacity, how representative historical demand data are of future underlying demand patterns, if synthetic wind data are used how well they represent real wind farm outputs, and possible consequences of natural climate variability and human-induced climate change.

This paper has presented examples for the GB system only, however the methods presented here are generally applicable. The bootstrap approach could be used directly in any system; the rescaling of the VG distribution according to demand level can also be used in any system. Some additional care may need to be taken when, for example, there is a substantial diurnal variability in the VG resource, since demand already has such variation. One possibility is to condition appropriately on the time of day.

It would be interesting to investigate how the statistical analysis and degree of sampling uncertainty might differ between small and large systems, between summer- and winter-peaking systems (in particular there tends to be stronger diurnal variability of the wind resource in summer-peaking systems), and in systems in which solar generation makes a significant contribution.

To conclude, the authors strongly recommend that adequacy studies should include an assessment of statistical uncertainty in model outputs, for instance using the methods in this paper. As emphasised above, without such uncertainty assessment the relationship between model results and the real system is unclear, and thus robust interpretation of modelling results is not possible.

Acknowledgements

The authors express their thanks to colleagues at National Grid and Ofgem for many valuable discussions during the GB Electricity Capacity Assessment project, and express particular thanks to M. Roberts for providing the Adjusted Gone Green Scenario data. They also acknowledge discussions with C. Gibson, the IEEE LOLE Working Group, and colleagues at Durham and Heriot-Watt Universities, EPRI, NREL and University College Dublin.

This work was supported by National Grid, and by the following EPSRC grants: EP/I017054/1, EP/E04011X/1, EP/H500340/1 and EP/I016953/1.

References

- [1] R. Billinton and R. N. Allan, Reliability evaluation of power systems, 2nd edition. Plenum, 1994.

- [2] G. J. Anders, Probability Concepts in Electric Power Systems. Wiley, 1990.

- [3] J. Endrenyi, Reliability Modelling in Electric Power Systems. Wiley, 1978.

- [4] W. Li, Risk Assessment of Power Systems: Models, Methods, and Applications. IEEE/Wiley, 2005.

- [5] A. Keane, M. Milligan, C. J. Dent, B. Hasche, C. D’Annunzio, K. Dragoon, H. Holttinen, N. Samaan, L. Söder, and M. O’Malley, “Capacity Value of Wind Power,” IEEE Trans. Power Syst., vol. 26, no. 2, pp. 564–572, 2011, IEEE PES Task Force report.

- [6] R. Duignan, C. J. Dent, A. Mills, N. Samaan, M. Milligan, A. Keane, and M. O’Malley, “Capacity value of solar power,” in IEEE PES General Meeting, 2012.

- [7] J. Radtke, C. J. Dent, and S. J. Couch, “Capacity Value of Large Tidal Barrages,” IEEE Trans. Power Syst., vol. 26, no. 3, pp. 1697–1704, 2011.

- [8] D. Kavanagh, A. Keane, and D. Flynn, “Capacity Value of Wave Power ,” IEEE Trans. Power Syst., vol. 28, no. 1, pp. 412–420, 2013.

- [9] W. Li and L. Goel, “Foreword: Special Section on Adequacy in Power Systems With Intermittent Sources,” IEEE Trans. Power Syst., vol. 27, no. 4, pp. 2295–2296, 2012.

- [10] R. Billinton, R. Karki, Y. Gao, D. Huang, P. Hu, and W. Wangdee, “Adequacy Assessment Considerations in Wind Integrated Power Systems,” IEEE Trans. Power Syst., vol. 27, no. 4, pp. 2297–2305, 2012.

-

[11]

“Electricity Capacity Assessment Report,” 2013, Ofgem, available at

https://www.ofgem.gov.uk/electricity/wholesale-market/

electricity-security-supply. -

[12]

“PJM Generation Adequacy Analysis: Technical Methods,” 2003, Capacity

Adequacy Planning Department, PJM Interconnection, available at

http://www.pjm.com/planning/resource-adequacy-planning/

reserve-requirement-dev-process.aspx. - [13] B. Hasche, A. Keane, and M. O’Malley, “Capacity Value of Wind Power, Calculation and Data Requirements: the Irish Power System Case,” IEEE Trans. Power Syst., vol. 26, no. 1, pp. 420–430, 2011.

- [14] B. Efron and R. Tibshirani, An introduction to the bootstrap. Chapman and Hall, 1993.

- [15] C. J. Dent and S. Zachary, “Capacity value of additional generation: Probability theory and sampling uncertainty,” in PMAPS, Istanbul, 2012.

-

[16]

IEEE LOLE Working Group meeting notes, available at

http://ewh.ieee.org/cmte/pes/rrpa/RRPA_WG.html. - [17] S. Zachary and C. J. Dent, “Probability theory of capacity value of additional generation,” pp. 33–43, 2012, J. Risk and Reliability (Proc. IMechE pt. O).

- [18] B. Efron, “Bootstrap Methods: Another Look at the Jackknife,” Annals of Statistics, vol. 7, no. 1, pp. 1–26, 1979.

-

[19]

National Grid, “UK Future Energy Scenarios,” 2013, available at

http://www2.nationalgrid.com/uk/industry-information/

future-of-energy/future-energy-scenarios/. -

[20]

“National Grid: Demand Data,” available at

http://www.nationalgrid.com/uk/Electricity/Data/Demand+Data/. -

[21]

“GB NETS Security and Quality of Supply Standard, Issue 2.2,” 2012,

available from

http://www2.nationalgrid.com/UK/

Industry-information/Electricity-codes/SQSS/The-SQSS/. - [22] C. J. Dent and J. W. Bialek, “Non-Iterative Method for Modeling Systematic Data Errors in Power System Risk Assessment,” IEEE Trans. Power Syst., vol. 26, no. 1, pp. 120–127, 2011.

- [23] W. S. Cleveland, E. Grosse, and W. M. Shyu, “Local regression models,” in Statistical Models in S, J. M. Chambers and T. J. Hastie, Eds. Wadsworth & Brooks/Cole, 1992, ch. 8.