Bayesian nonparametric mean residual life regression

SUMMARY

The mean residual life function is a key functional for a survival distribution. It has a practically useful interpretation as the expected remaining lifetime given survival up to a particular time point, and it also characterizes the survival distribution. However, it has received limited attention in terms of inference methods under a probabilistic modeling framework. We seek to provide general inference methodology for mean residual life regression. We employ Dirichlet process mixture modeling for the joint stochastic mechanism of the covariates and the survival response. This density regression approach implies a flexible model structure for the mean residual life of the conditional response distribution, allowing general shapes for mean residual life as a function of covariates given a specific time point, as well as a function of time given particular values of the covariates. We further extend the mixture model to incorporate dependence across experimental groups. This extension is built from a dependent Dirichlet process prior for the group-specific mixing distributions, with common atoms and weights that vary across groups through latent bivariate Beta distributed random variables. We discuss properties of the regression models, and develop methods for posterior inference. The different components of the methodology are illustrated with simulated data examples, and the model is also applied to a data set comprising right censored survival times.

KEYWORDS: Dependent Dirichlet process; Dirichlet process mixture models; Markov chain Monte Carlo;

Mean residual life function; Survival regression analysis.

1 Introduction

The mean residual life (MRL) function of a continuous positive-valued random variable, , provides the expected remaining lifetime given survival up to time , . Its definition requires that has finite mean, which is given by . The MRL function can be defined through the survival function, , in particular, , with when . Conversely, the survival function is defined through the MRL function via (Hall & Wellner, 1981), and thus the MRL function characterizes the survival distribution. Given this property and its useful interpretation, the MRL function is of practical importance in a variety of fields, such as reliability, medicine, and actuarial science.

Often associated with the survival times is a set of covariates, . The MRL regression function at a specified set of covariate values is given by:

| (1) |

provided . In the regression setting, it is of interest to develop modeling that allows flexible MRL function shapes over the covariate space. Note that MRL regression involves study of covariate effects on a function over time. It is of interest to study how MRL regression relationships change across different time points (mean regression corresponds to ), as well as how the MRL function evolves across different covariate values.

Classical estimation methods for MRL regression have been primarily derived from the proportional MRL model, , where and is a baseline MRL function (Oakes & Dasu, 1990). Maguluri & Zhang (1994) extend the proportional MRL model to incorporate covariates, such that the MRL regression function is , where are the regression coefficients. They propose two estimators for under fully observed survival responses. Chen & Cheng (2005), Chen & Wang (2015) and Bai et al. (2016) expand the estimation methods under different forms of censoring. Alternative to the proportional MRL model structure, Chen (2006) and Chen & Cheng (2006) develop additive MRL models with the MRL regression function given by . Sun & Zhang (2009) generalize such models to , where is a pre-specified link function. This model is further extended in Sun et al. (2012) to incorporate time-dependent regression parameters in a linear fashion. Jin et al. (2020) and Ma et al. (2020) consider generalized MRL models under different sampling scenarios. Classical semiparametric estimation methods are restricted by the: proportional or additive form of the MRL regression function; the parametric introduction of covariate effects; and the fact that they are not based on fully probabilistic model settings, thus requiring asymptotic arguments for uncertainty quantification.

Survival analysis is one of the first application areas for nonparametric Bayesian (NPB) modeling and inference methods. The relevant literature includes several prior probability models for cumulative hazard functions, hazard functions, survival functions, or survival densities; see, e.g., Ibrahim et al. (2001), Phadia (2013), and Müller et al. (2015). However, to our knowledge, there is no work in the NPB literature that explores modeling and inference for the MRL function in the presence of covariates.

Our objective is to develop an NPB modeling framework that lends full and flexible inference for MRL regression. To accommodate the regression setting, we extend our earlier work on inference for MRL functions, based on Dirichlet process (DP) mixture priors for the survival distribution (Poynor & Kottas, 2019). To this end, we employ DP mixture modeling for the joint stochastic mechanism of the survival response and the covariates, from which general inference for MRL regression emerges through the implied conditional response distribution. This DP mixture density regression approach was proposed by Müller et al. (1996) for real-valued responses, and it has been applied and elaborated under different settings; see, e.g., DeYoreo & Kottas (2020) for a review and relevant references. In our context, a key modeling choice involves the mixture kernel that corresponds to the survival responses, for which we argue for the gamma density. Even though we do not model directly the MRL function of the response distribution, the implied prior model for the MRL function given the covariates has an appealing structure as a locally weighted mixture of the kernel MRL functions, with weights that depend on both time and the covariates.

For problems with a small to moderate number of random covariates, the density regression modeling approach is attractive in terms of its inferential flexibility. At the same time, survival data typically comprise responses from subjects assigned to different experimental groups, e.g., control and treatment groups. Since the treatment indicator is not a random covariate, we extend the model to allow distinct mixing distributions for the different groups, which are dependent in their nonparametric prior. We develop this extension in the context of two groups, using a dependent Dirichlet process prior (MacEachern, 2000; Quintana et al., 2022) for the group-specific mixing distributions. The general model retains the local weighted mixture structure, with local adjustment provided by weights that depend on time, covariate values, as well as the treatment groups.

The outline of the paper is as follows. Section 2 develops the density regression approach to modeling and inference for MRL regression. In Section 3, we present the model elaboration to incorporate survival data from different experimental groups, including illustrations from two synthetic data examples. In Section 4, we provide a detailed analysis of a standard data set from the literature on right censored survival times for patients with small cell lung cancer. Finally, Section 5 concludes with a summary.

2 Mean residual life regression

2.1 Model formulation

For survival regression problems with a small/moderate number of random covariates, it is meaningful to model the joint distribution of the survival response and covariates. In our context, a key benefit of this modeling strategy involves the implied MRL function of the conditional response distribution. In particular, we obtain general MRL regression relationships across different time points, and flexible MRL functions across different covariate values.

Let be a vector of random covariates and the positive-valued survival response variable. We model the joint response-covariate density using a DP mixture model:

| (2) |

where is the joint kernel density for survival time and covariates, and the mixing distribution, , is assigned a DP prior (Ferguson, 1973). The model is completed with hyperpriors for the DP precision parameter, , and for (some of) the parameters of the baseline (centering) distribution . Under the DP constructive definition (Sethuraman, 1994), a realization from DP is almost surely of the form , where the atoms are independently and identically distributed (i.i.d.) from the baseline distribution, , with the weights constructed through stick-breaking: , and , for , where (independently of the ).

Hence, the density in (2) can be re-written as . Directly from their definitions, the conditional response density can be expressed as , and the conditional survival function as

| (3) |

where . Therefore, the conditional density and survival functions are represented as mixtures of the corresponding kernel functions with covariate-dependent mixture weights. Analogously, the mean regression function is given by (a sufficient condition for the conditional expectation to be finite is given in Section 2.2). The covariate-dependent mixture weights allow for local adjustment over the covariate space, thus enabling general shapes for the conditional response distribution and for the mean regression functional.

Importantly for our objective, this local mixture structure extends to the MRL functional. Using the form for the conditional survival function in (3) and the definition of the MRL regression function from (1), we obtain

| (4) |

where

| (5) |

and is the MRL function of the mixture kernel conditional response distribution. (Implicit here is the assumption that, under the kernel distribution, , for any ). Therefore, our prior model for the MRL regression function admits a representation as a weighted sum of the conditional MRL functions associated with the kernel components, with weights that are dependent on both time and the covariate values. Important to note in the form of the mixture weights in (5) is that there are separate functions controlling the local adjustment over covariate values and time. Aside from the useful interpretation, expressions (4) and (5) suggest the model’s capacity to capture non-standard MRL regression relationships over time, and general MRL function shapes across the covariate space.

2.2 Mixture kernel specification

A key aspect for the model formulation is the choice of the DP mixture kernel, . A structured approach to specifying dependent kernel densities involves a marginal density for the covariates, , and a parametric regression model for , where . For our data illustrations, we use the simpler form for the kernel density with independent components for the survival response and the covariates, . In this case, the prior model in (4) becomes a weighted combination of the marginal kernel MRL functions, , with weights that are still dependent on both time and covariate values through distinct functions, in particular, (replacing in (5)) and , respectively. As can be seen from the model structure, such a kernel density form strikes a useful balance between model flexibility and complexity with respect to the dimensionality of the mixing parameter vector .

Regarding , when all the covariates are continuous, the multivariate normal density is a convenient choice, possibly after transformation for the values of some of the covariates. A normal kernel density can also accommodate ordinal categorical covariates through latent continuous variables (e.g., DeYoreo & Kottas, 2018). Alternatively, categorical covariates (whether ordinal or nominal) can be incorporated by adding a corresponding component to the kernel in a product form, or if relevant, through marginal and conditional densities for the continuous and categorical covariates (e.g., Taddy & Kottas, 2010).

A key consideration for the specification of (or ) is to ensure that the MRL function is well defined, that is, must be (almost surely) finite, for any . The following lemma provides sufficient conditions in that direction.

Lemma. Consider the DP mixture model in (2) with kernel , and with DP baseline distribution . For a generic set of covariate values , assume that: (a) ; and, (b) . Then, , almost surely.

Proof. Based on the DP constructive definition,

where , from assumption (a). Let . Using the monotone convergence theorem, and the independence between the DP atoms and weights, we have , since this expectation is free of as the are i.i.d. (from ). Moreover,

which is finite from assumption (b). Since is a positive-valued random variable with finite expectation, is almost surely finite, and thus, , almost surely.

Note that defining through independent components for and is a natural modeling strategy. Also, under independent kernel components for the response and covariates, simplifies to the expectation of the kernel for survival time, and the second lemma condition becomes . For this model version, it is straightforward to verify the lemma conditions for the gamma density under the choice for discussed below. The gamma choice is unique in this respect among standard lifetime distributions in that it ensures existence of the mixture MRL function without the need for awkward restrictions on the parameter space for . Further support for the gamma kernel choice is provided by the fact that it generates both increasing and decreasing MRL functions (for shape parameter and , respectively), its MRL function can be readily computed (see Section 2.3), as well as by a denseness result for the MRL function of gamma mixture distributions, obtained under the setting without covariates (Poynor & Kottas, 2019).

We use the following parameterization for the gamma density, , with , to facilitate selection of a dependent distribution, taken to be bivariate Gaussian. Finally, we note that the lemma conditions remain generally easy to verify if one wishes to extend the gamma kernel density to depend on covariates, for instance, such that its mean is extended to .

2.3 Posterior inference

We obtain samples from the posterior distribution of the DP mixture model using the blocked Gibbs sampler (Ishwaran & James, 2001). In particular, the Markov chain Monte Carlo (MCMC) posterior simulation method builds from a truncation approximation to the mixing distribution, , with , for , and , for , with . The truncation level can be chosen to any desired level of accuracy, using DP properties. For instance, the prior expectation for the partial sum of the DP weights, , can be averaged over the hyperprior for to estimate for any value of the truncation level. The Appendix B.2 includes details of the MCMC algorithm for the DDP mixture model developed in Section 3, which is a more general version of the density regression model of Section 2.1.

Posterior inference for the density, survival, and mean regression functions can be obtained by evaluating , , and under model (2). Computing proceeds with the posterior samples for , thus involving finite sums at the inference stage. Posterior samples for the MRL regression function can be efficiently computed using expression (4), provided the kernel MRL function can be readily computed. This is the case for the gamma kernel distribution whose MRL function can be expressed in terms of the Gamma function, , and the gamma distribution survival function, (Govilt & Aggarwal, 1983). More specifically, under the gamma density parameterization given in Section 2.2,

This expression suffices for the model built from independent kernel components for the survival response and covariates, and it can be easily extended to accommodate a gamma kernel density that depends on covariates.

The Appendix A includes two synthetic data examples to illustrate the DP mixture density regression model. The two examples correspond to different scenarios regarding the underlying stochastic mechanism that generates the data. The simulation truth in the first example involves a finite mixture for the joint response-covariate distribution, specified such that the MRL function takes on various non-standard shapes at different covariate values. The simulation truth for the second example corresponds to a structured parametric setting, where the survival responses are generated from a three-parameter extension of the Weibull distribution with its parameters defined through specific regression functions.

3 Dependent DP mixture model for MRL regression

3.1 The DDP mixture model formulation

Often in biomedical studies, researchers are interested in modeling survival times of patients under treatment and control groups, where one may expect that the survival distributions for the two groups exhibit some similarity. Modeling groups jointly is thus a natural choice, offering potential learning for the extent of similarity, as well as borrowing inferential strength across groups. We do so by generalizing the DP mixture model of Section 2 to a dependent DP (DDP) mixture model. Since we build on the model structure of DP mixture density regression, we achieve non-standard MRL regression function shapes, which may also differ across groups contingent on the strength of the dependence across experimental groups.

Let represent in general the index of dependence. In our case, this indicates the experimental group, that is, , where is the treatment and is the control group. The model in (2) can be extended to , for , where we now need a nonparametric prior for the group-specific mixing distributions . The DDP prior structure allows for dependence across experimental groups, while maintaining the DP prior marginally for each . The DDP prior builds from the DP constructive definition, and, in its most general form, extends the structure for to , for . Typically, simplified versions are employed with common weights or common atoms. Here, we opt for a common atoms DDP prior model, , with , as in the DP prior, and group-specific dependent weights defined through a bivariate beta distribution for the latent stick-breaking variables. The construction for the weights is detailed later in the section.

A practical advantage of modeling dependence only through the weights is that the construction is not affected by the dimension of the mixture kernel parameter vector, i.e., by the number of covariates. Moreover, the common atoms prior model structure is useful if we expect the group-specific distributions to be comprised of similar components which however exhibit different prevalence across survival time.

Hence, the DDP mixture model can be expressed as

| (6) |

Then, the conditional response density becomes , and the conditional survival function can be written as

| (7) |

where . Likewise, the group-specific mean regression function is . We thus recognize again the local weighted mixture structure with covariate-dependent weights, which now change also with the treatment (group) assignment.

Using (7) with definition (1), the MRL regression function of the general model becomes

| (8) |

where the weights can be written as

| (9) |

Again, the local weighted mixture formulation extends to the MRL regression, with the local adjustment over the covariates, time, and (now) groups controlled by separate components of the mixture weights. Importantly, the model allows flexible MRL functions that can vary in shape across treatment groups at the same covariate values or at the same time points. The practical utility of this model feature is demonstrated in Section 4.2 with relevant results from the analysis of the small cell lung cancer data.

Next, we turn to the construction of the dependent weights of . The stick-breaking method to construct the weights uses latent variables , but one can equivalently work with adjusting accordingly the expression for the weights. Therefore, the weights of the DDP prior for are:

with i.i.d. from a bivariate beta distribution for which the marginals are distributed. This construction incorporates dependence between the two groups (additional to the dependence induced by the common atoms), while maintaining the prior marginally for the group-specific mixing distribution .

We work with a bivariate beta distribution from Nadarajah & Kotz (2005), defined constructively through products of independent beta distributed random variables. In particular, to define the bivariate beta distribution for , start with independent random variables, , , and , subject to the constraint, . Then, define and . The marginals are given by and . We can thus obtain the desired beta marginals for and by setting , and . The DDP prior model is completed with hyperpriors for and , as well as for parameters of the baseline distribution for the common atoms.

For MCMC posterior simulation, we work with the to update , as well as hyperparameters and , thus bypassing the complex form of the bivariate beta density for the . The Appendix B.2 details the blocked Gibbs sampler for the DDP mixture model.

The latent (independent) random variables can also be used to study properties of the bivariate beta distribution. In particular, working with product moments of the bivariate beta distribution for the , we can build the correlation of , and then the correlation of (for any specified measurable set ). The correlation between the group-specific survival times, , , can also be obtained. Details are provided in the Appendix B.1.

3.2 Connections with DDP survival regression models

The model developed in Section 3.1 combines ideas from DP mixture density regression and covariate-dependent DDP mixture models, the two main NPB approaches to fully nonparametric regression. Here, we contrast the MRL regression formulation implied by our model with the one arising from general DDP regression, and from the more structured DDP model in De Iorio et al. (2009), a standard reference on DDP survival regression.

For simpler exposition, we consider the setting with one continuous covariate, , and one binary covariate, (say, a treatment indicator), as in the small cell lung cancer data set of Section 4. Under the DDP mixture approach, the prior model is defined directly for the conditional response density:

with a kernel density on , under which the MRL function of the mixture distribution is well defined. Here, the mixture weights, , and atoms, , depend on both covariates, and the notation takes into account the discrete (binary) nature of . Then the covariate-dependent MRL function can be expressed as

where and are the kernel survival and MRL function, respectively. Hence, the prior model structure is generally similar to the one in (8), although the fashion in which the different weight components control local adjustment over time and the covariates is not as clear as in (9).

The general DDP prior formulation requires group-specific stochastic processes (indexed by the continuous covariate values) for the atoms , and another set of stochastic processes in for the covariate-dependent stick-breaking variables that define the weights . To retain the DP prior marginally at any , the latter stochastic processes must have beta marginals. Evidently, a general DDP prior model becomes more challenging to formulate as the dimension of the covariate space increases, and it is also difficult to estimate with small to moderate amounts of data.

A substantial simplification of the general DDP structure is offered by a linear-DDP formulation, under which only the atoms depend on the covariates through (transformations of) linear regression functions. Consider a two-parameter mixture kernel, , where is a scale parameter, and controls the center of the distribution (say, the mean or median parameter), with and a specified link function. Then, a possible linear-DDP mixture model for the conditional response density can be written as:

where . Examples for the kernel include the gamma density with mean , and the log-normal density with median and corresponding to the standard deviation of the normal whose transformation yields the log-normal. The latter choice essentially yields the linear-DDP regression model in De Iorio et al. (2009).

The MRL regression under the linear-DDP model can be written as

where and are the kernel survival and MRL function, respectively. The linear-DDP structure is restrictive in terms of the implied prior for the MRL function. In contrast to the form in (9), here there is a single function (the kernel survival function) that defines the dependence of the weights on time and the covariates. Lacking the local adjustment over values in the covariate space impedes model flexibility. For instance, under the log-normal kernel, the mean regression function for the control group () and treatment group () is and . Hence, the model can not uncover general non-linear, non-monotonic regression relationships, and furthermore the mean regression function varies across groups in a rigid fashion.

3.3 Synthetic data examples

In this section, we consider two synthetic data examples to investigate the performance of the DDP mixture model without covariates, that is, , where , and the baseline distribution is . The model is completed with the following hyperpriors: , , (gamma distribution with mean ), and .

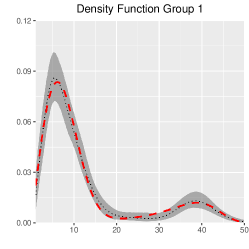

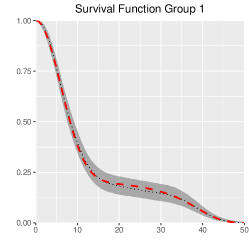

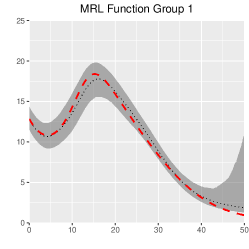

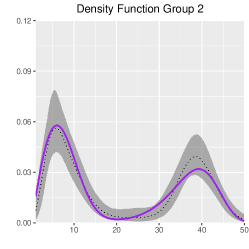

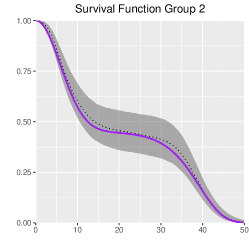

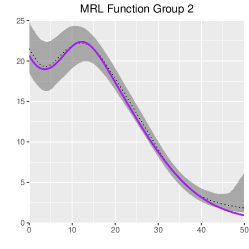

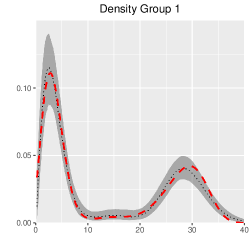

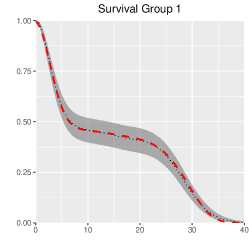

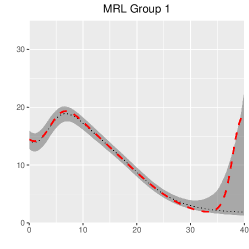

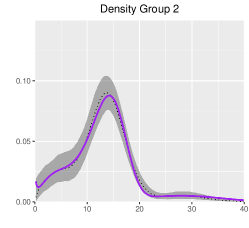

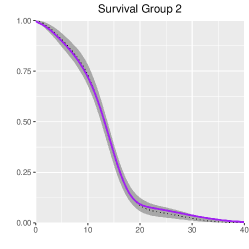

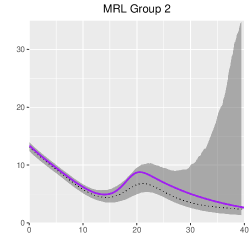

The first simulation scenario involves distributions defined by mixtures of Weibull distributions with the same atoms and different weights. We expect the DDP mixture model to perform well under this scenario since the truth shares the same structure as the DDP prior model. The true density, survival, and MRL functions are shown in Figure 1. Note that the two groups have bimodal densities with modes at essentially the same locations, but with differing prevalence. The second scenario is also based on mixtures of Weibull distributions, but, in this case, with different weights and atoms. The intention is to test the model’s inferential ability for distributions with quite different features. In particular, the second group density exhibits a single mode in between the two modes of the first group density; see Figure 2 for the true density, survival, and MRL functions.

3.3.1 Simulation 1

We work with Weibull mixture distributions that share atoms, but have different weights: and . We sample survival times from the first population and survival times from the second. Regarding the hyperparameters, we set: , , , , and .

Posterior point and interval estimates for the density, survival, and MRL functions are provided in Figure 1. Despite the moderate sample sizes, the model performs well in inference for all functionals, including successfully recovering the non-standard shape of the group-specific MRL functions. As expected from the difference in the sample size for the two groups, the posterior interval bands are wider for the second group estimates.

3.3.2 Simulation 2

Here, the Weibull mixtures have different weights, atoms, and number of components: , and . We generate survival times from each population. The hyperparameters are specified as follows: , , , , and .

As shown in Figure 2, the model is successfully estimating the group-specific density, survival, and MRL functions, even though the simulation truth is now different from the model structure. In particular, the MRL function has non-standard shape which changes in a non-trivial fashion across the two groups. The first group MRL function depicts a rapid increase for survival times at the tail of the corresponding density. Regarding the proportion of data in the tail, only one out of the 250 simulated survival times has value greater than . The MRL function point estimate does not capture the increase in that range of survival times, but the posterior uncertainty bands essentially include the true function.

4 Small cell lung cancer data example

We consider a dataset, provided in Ying et al. (1995), that comprises survival times, in days, of patients with small cell lung cancer. The data has been used as a test case for classical and Bayesian semiparametric regression models, typically, with a linear regression for a central feature (e.g., median) of the log-transformed survival times; see, e.g., Kottas & Krnjajić (2009) and further references therein. The patients were randomly assigned to one of two treatments referred to as Arm A and Arm B. Arm A patients received cisplatin (P) followed by etoposide (E), while Arm B patients received E followed by P. The Arm A group consists of survival times, of which are right censored, whereas the Arm B group consists of survival times, of which are right censored. The age of each patient at entry in the clinical study is also available. We begin the data analysis in Section 4.1 working with treatment as the only covariate, and incorporate the age covariate in Section 4.2.

4.1 Comparative inference for the treatment groups

4.1.1 Results under the DDP mixture model

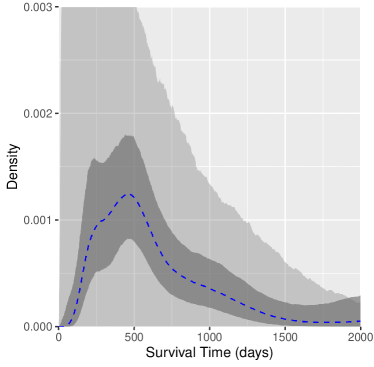

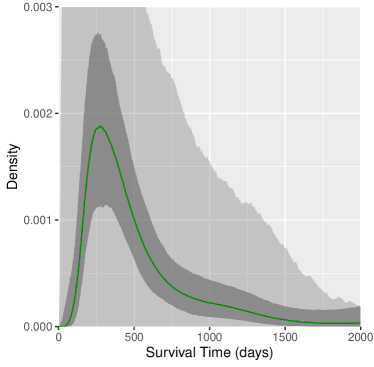

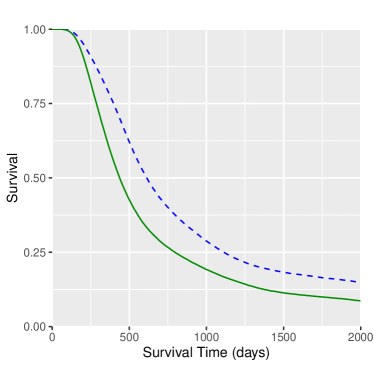

We fit the gamma DDP mixture model, given in Section 3.3, such that indexes the Arm A and Arm B treatment groups. For the hyperparameters, we set: , , , , and . The effect of any particular prior choice can be usefully studied through the implied prior uncertainty for the survival density (or other functionals). The prior interval bands for the Arm A and Arm B density are plotted in Figure 3.

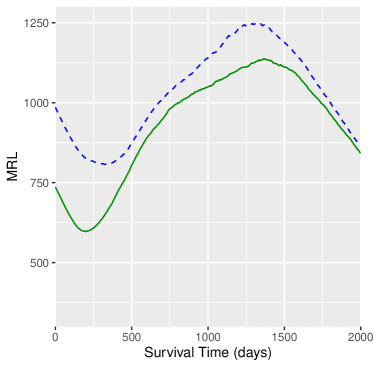

Inference results for the density, survival, and MRL functions are shown in Figure 3. The model estimates heavy tailed densities, with the mode at about 450 days and 350 days for Arm A and Arm B, respectively. Comparing the prior and posterior credible interval bands suggests substantial learning from the data. The survival function point estimates indicate that Arm A has higher survival rate starting from about 200 days. The estimated treatment-specific MRL functions exhibit a non-linear, non-monotonic trend with Arm A having higher mean residual life over the effective range of survival times.

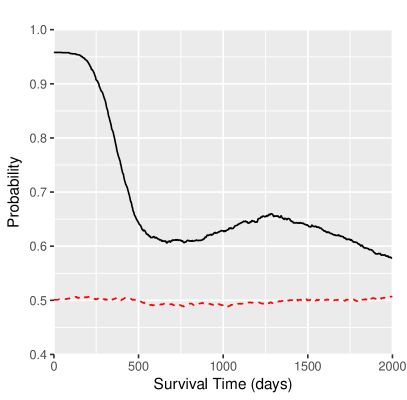

For comparison of the treatment-specific MRL functions that incorporates posterior uncertainty, we work with the posterior probability over a grid of survival times , where and is the MRL function under Arm A and Arm B, respectively. The results are reported in Figure 4, where we also include the prior probability, . Note that the prior does not favor either of the two treatments. The posterior probability is greater than over the entire effective range of survival times; it is fairly large (about ) for the first 200 days, then it decreases to about at around 500 days, from which point on it essentially stabilizes to values that range from to .

4.1.2 Model comparison

Although we are not aware of other NPB models that explore inference for MRL regression, as previously mentioned, the small cell lung cancer data set has been used for illustration of semiparametric survival regression models. In particular, Kottas & Krnjajić (2009) develop a Bayesian semiparametric quantile regression model, based on a linear quantile regression function and a non-parametric scale mixture of uniform densities for the error distribution, and apply it to the log-transformed survival times, using the treatment indicator as the only covariate. We compare the predictive performance of the DDP mixture model through the criterion used in Kottas & Krnjajić (2009), which is based on conditional predictive ordinate (CPO) values.

The CPO for an observed survival time is defined by the value of the posterior predictive density at , given the data with excluded. The definition can be extended to right censored observations replacing the predictive density by the predictive survival function. Large CPO values indicate agreement between the associated observations and the model. Models can be compared by summarizing the CPOs, say, through the average of the log-CPO values, which we refer to as the ALPML criterion. For many hierarchical Bayesian models, CPOs can be computed using posterior samples obtained by fitting the model once to all observations; see, e.g., Chen et al. (2000). This is also possible for the DDP mixture model; the details are provided in Appendix B.3.

The ALPML value for the DDP mixture model is . The ALPML values reported in Kottas & Krnjajić (2009) are for the semiparametric quantile regression model, and for a Weibull proportional hazards model. The semiparametric model provides improvement in predictive performance relative to the parametric proportional hazards regression model. The fully nonparametric DDP mixture model offers further improvement.

4.2 Incorporating the age covariate

Here, we consider the analysis of the data including both available covariates, the treatment indicator () and patient age at entry in the clinical study (). We apply the model in (6) with a product mixture kernel, , where and is the normal density with mean and variance . The baseline distribution comprises independent components: a bivariate normal distribution for ; a normal distribution for ; and an inverse-gamma distribution for . The model is completed with hyperpriors: , , , , , , and . The hyperparameter values are as follows: , , , , , , , , , and .

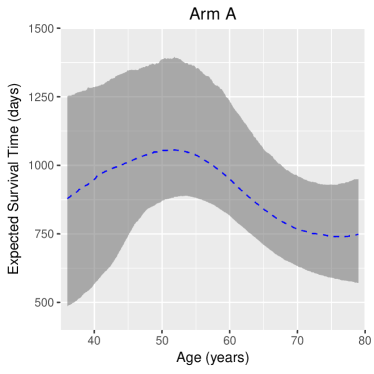

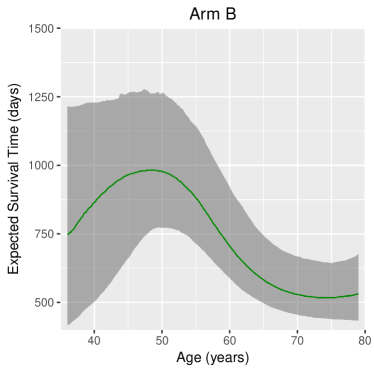

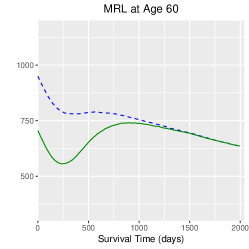

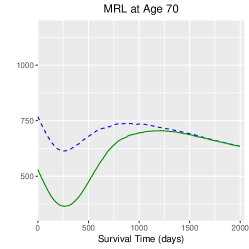

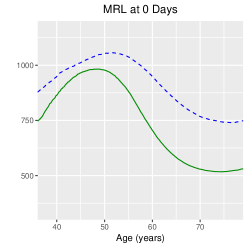

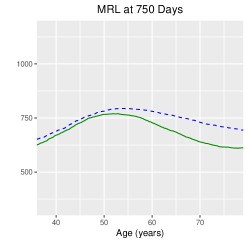

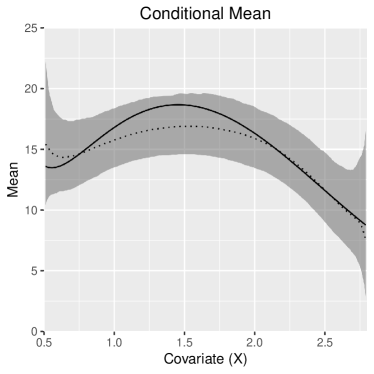

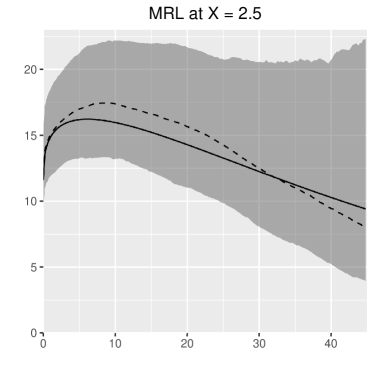

To our knowledge, earlier work that has considered age as a covariate has done so using linear regression. The age-dependent and treatment-dependent weights in the weighted mixture structure for the mean regression, , allow for less standard regression relationships to be uncovered. Indeed, as shown in Figure 5, the model estimates a non-monotonic relationship with age, with an initial increase up to about years followed by a steeper decline, particularly for Arm B. The point estimates for the treatment-specific mean regression are also plotted in Figure 6 (bottom left panel), showing that Arm A achieves higher mean survival across the entire range of age values.

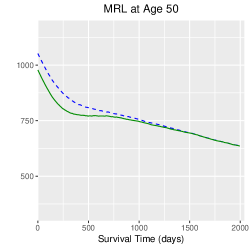

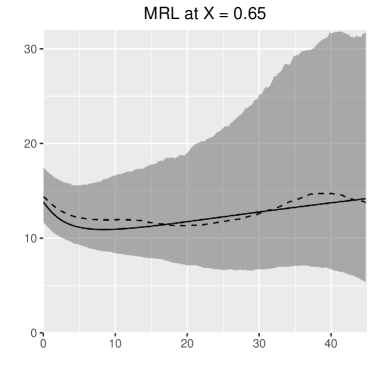

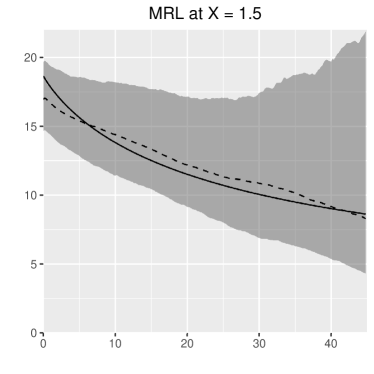

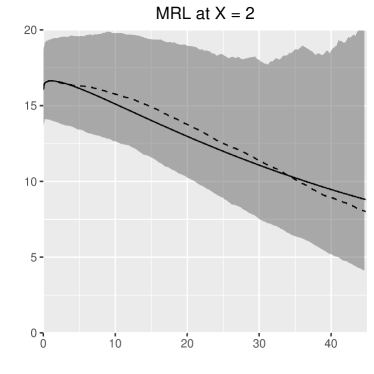

Figure 6 demonstrates the model’s capacity to uncover general MRL function shapes that can change across treatment groups at fixed age values and/or at fixed time points. The top panels compare point estimates for Arm A and Arm B mean residual life as a function of time at age , , and years. At age , the MRL functions are decreasing in time with a small separation between treatments up to days, at which point they become indistinguishable. The Arm B estimate suggests a minor dip at about days. At age , the separation across treatments becomes more apparent in the earlier range of survival times, and the dips are more pronounced, especially for Arm B; here, the estimates become indistinguishable after about days. At age , we observe a similar curvature with the age MRL functions with a dip around days, larger separation for smaller survival times, and essentially identical functions after about days. While the shape of the MRL functions changes in a non-trivial fashion across values of age, Arm A mean residual life remains as high or higher than Arm B. These results provide a picture about the treatment-specific MRL functions, localized in terms of patient’s age at entry in the study. In particular, it is interesting to compare the estimates in the top panels of Figure 6 with the ones in the bottom right panel of Figure 3, based on the model without the age covariate.

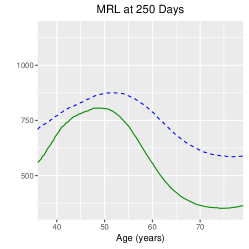

Finally, the bottom panels of Figure 6 compare mean residual life as a function of age at three time points: , , and days. In all three cases, the MRL function is higher for Arm A across the range of age values. Again, the first case corresponds to mean survival as a function of age. Comparing the estimates at and days, we observe a similar non-monotonic relationship with age, including a similar separation between treatments, although there is a decrease in mean residual life at days. The separation between treatment groups and the extent of the non-monotonic trend become less pronounced at days. Overall, the results reinforce the point that Arm A offers a better treatment than Arm B.

5 Summary

We have proposed a nonparametric mixture modeling approach for mean residual life (MRL) regression, a problem that, to our knowledge, has not received attention in the Bayesian nonparametrics literature. The focus has been on developing general inference methodology for MRL functions across different values in the covariate space, as well as for MRL regression relationships across different time points. The modeling approach builds from Dirichlet process mixture density regression, including dependent Dirichlet process priors to accommodate data from different experimental groups. The methodology has been illustrated with both synthetic and real data examples.

Appendix

Appendix A includes simulated data examples for the Dirichlet process mixture model developed in Section 2. Appendix B details the structure and correlation properties of the dependent Dirichlet process prior model of Section 3.1, the MCMC posterior simulation method, and the derivation of the CPO values used in the model comparison of Section 4.1.2.

A. Simulation examples for the density regression model

We provide two simulation examples to demonstrate the capacity of the density regression model (Section 2 of the main paper) to capture a variety of MRL functional shapes.

Both examples involve a single continuous covariate. For the first example, we work with a finite mixture for the joint response-covariate distribution, specified such that the MRL function takes on various non-standard shapes at different parts of the covariate space. In the second example, we consider an exponentiated Weibull distribution (Mudholkar & Strivasta, 1993) for the survival responses. This is a three-parameter extension of the Weibull distribution that achieves more general shapes for the hazard rate and MRL function. The regression model for the simulation truth is built by defining the three response distribution parameters through specific functions of covariate values, which are drawn from a uniform distribution. The two simulation scenarios are designed to correspond to a setting similar to the model structure, as well as a much more structured parametric setting for the data generating stochastic mechanism. We work with relatively large sample sizes ( and for the first and second example) so that the data sets provide reasonably accurate representations of the simulation truth, thus rendering comparison with true MRL functions meaningful. The synthetic data examples of Section 3.2 and the analysis of the real data in Section 4 of the main paper illustrate model inferences under smaller sample sizes.

We apply the same DP mixture model to both synthetic data sets, with a gamma and normal product kernel, . The DP centering distribution is defined by , where denotes the inverse-gamma distribution with mean (provided ). The model is completed with the following hyperpriors: , , , , , and , where denotes the gamma distribution with mean . For both examples, we set , , and for the DP truncation level.

Simulation 1

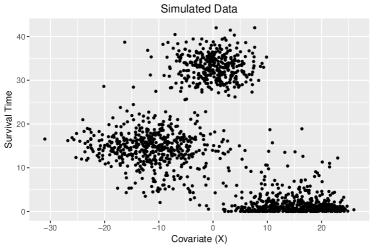

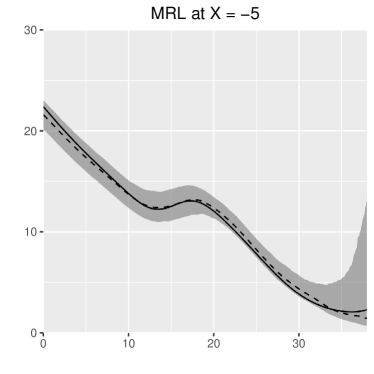

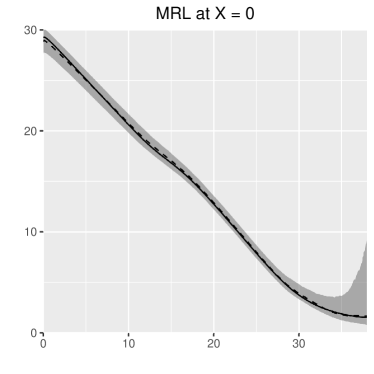

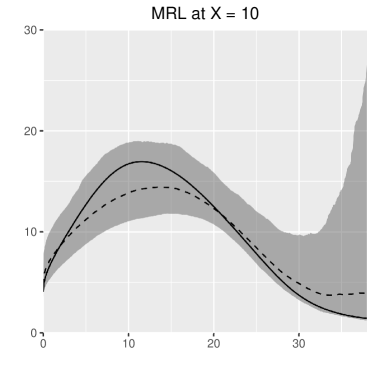

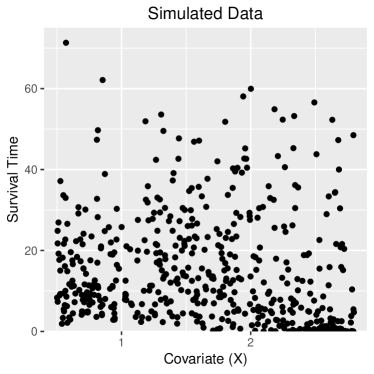

We simulate observations from a population with density: , where , , , , and . The simulated data is shown in the left panel of Figure 7. The following hyper priors were assumed: , , , , , , .

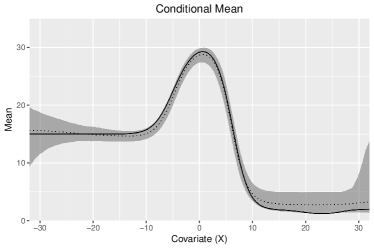

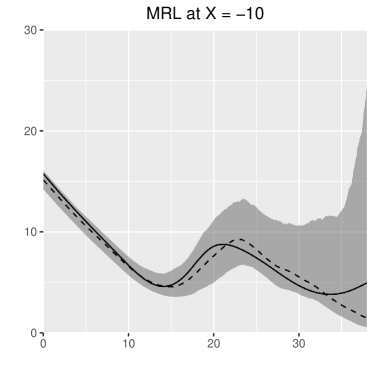

The mean of the survival times across a grid of covariate values is shown in Figure 7 (right panel). In general, the model is able to capture the non-linear trend of the mean over the covariate values. The truth is captured within the interval estimate save for a small sliver barely outside the interval near the right tail of the covariate space where data is sparse. The results for MRL functional inference is shown in Figure 8. We provide point and interval estimates for the MRL function at four different covariate values. The model is able to capture the overall shape of the true MRL functions, despite the variety of and often complexity of the shapes. At covariate values where the data is most dense, such as and , the inference is more precise as is seen in the narrow interval bands. As we move to covariate values where data is more sparse, the wide interval bands reflect the uncertainty of the MRL functional shape.

Simulation 2

The exponentiated Weibull population has survival function, . The MRL function associated with this distribution can take on increasing, decreasing, constant, upside-down bathtub, and bathtub shapes depending on the shape parameters, and , as well as their product ( is a scale parameter). We sample observations from an exponentiated Weibull population with , , and , where . The simulated data is shown in the left panel of Figure 9. The following hyper priors were assumed: , , , , , , .

The mean of the survival times across a grid of covariate values is shown in Figure 9 (right panel). Once again, the true mean regression exhibits a non-linear trend that is increasing until about then decreases. The is captured well within the interval estimate and the parabolic shape is clearly mimicked by the point estimate. The results for MRL functional inference is shown in Figure 10 at four covariate values. In all four scenarios, the truth is captured within the interval bands while the general shapes are mimicked by the point estimates.

B. DDP mixture model

B.1 Properties of the DDP mixture model

Here we study the correlation structure under the dependent Dirichlet process (DDP) mixture model (Section 3.1 of the main paper) that is induced by the bivariate beta distribution in Nadarajah & Kotz (2005). This bivariate beta distribution is based off of the product of independent beta distributions: , , . Letting and provides the bivariate beta distribution on . Generating for under independent and identical processes, the component weights of the DDP mixture model are then defined for group by , , for .

We are interested in obtaining the correlation between the two mixing distributions, and , implied under this bivariate beta distribution. We first begin with examining the correlation between and , . We omit the component subscript in the latent variables, since results are the same for each . The covariance can be written as, . Using the fact that are independent, the covariance becomes . Now, since and have the same marginal distribution, , the covariance and correlation reduces to:

The correlation between and can take values on the interval . As and/or , the correlation goes to . As and/or , the correlation tends to .

We next explore the correlation of the weights, for . When , , which is simply a linear operation, hence the covariance and correlation are the same as before. The and are given above. The case is different for . In this case, the covariance is defined as . Using the fact that are independent across , for each , the covariance, for , can be expressed as

The variance for the weights are independent of group, and can be expressed as . Therefore, the correlation, for , can be obtained by , which is in closed form, but does not reduce. The correlation between the weights for also takes values on the interval and behaves the same in terms of the limits of and as in the case when . The component value, , plays a slight role in the correlation, specifically as get larger, the rate of change for smaller values becomes less extreme.

We now turn to the correlation between the two mixing distributions, and . Let represent a specified (measurable) set in the joint space of the mixing parameters. Recall that the mixing distribution for group has form . Marginally, follows a DP, so the expectation and variance of is and , respectively. The covariance between and is given by , simplifying to, . The infinite series converges under geometric series, and the covariance simplifies to be:

The correlation does not depend on the choice of or ; it is driven by and alone:

| (10) |

The correlation of the mixing distribution lives on the interval . As and/or , the correlation tends to . When the correlation tends to and as the correlation tends to , so when and the correlation goes to . Although this correlation space is limited, it is a typical range seen in the literature (e.g. McKenzie (1985)). It can easily be shown that the correlation of the survival distributions between the two groups given and also live on , which demonstrates the importance of prior knowledge of the relationship between the distributions of the two group survival times.

While the possible values of correlation of the mixing distributions of the two groups is restricted to , the correlation between the survival times (marginal of the covariate(s), see Web Appendix B.3) across the two groups, , takes on values in . The is found by marginalizing over the mixing distributions, and . Starting with the covariance, . Under DDP mixture model without covariates, we have the gamma kernel with bivariate normal . Thus, the covariance is given by the following,

where and . The variance of , for both , conditional on and is given by, where that . Hence, the correlation is given by,

As the the correlation simplifies to . In this case, as the correlation tends to and as the correlation tends to . Also, as the correlation tends to and as the correlation tends to . These results are scaled down as , the expectation of the kernel variance, gets larger.

B.2 MCMC Details

Here we show the posterior sampling algorithm used for the DDP mixture model in the presence of a single random continuous (real-valued) covariate, as applied in Section 4.2 of the main paper. The mixture kernel density comprises a product of the gamma density for the survival response and a normal density for the random covariate. Omitting the model component for the random covariate yields the model applied in Sections 3.3 and 4.1 of the main paper. Assuming a single group, i.e., having only a single index value, will yield the algorithm pertaining to the simulation examples in Web Appendix A. We obtain posterior samples using the blocked Gibbs sampler and working with the latent parameters of the bivariate beta distribution. Posterior samples are based on a truncation approximation, , to : . Specifically, the atoms are defined as , for with corresponding weights for with , and .

Upon introducing the latent configuration variables, , such that if the observation in group is assigned to mixture component , the full hierarchical version of the model is written as,

where and , for , with , , and . We place the following hyperpriors: , , , , , , and .

For subject , let if is observed and if is right censored. Let represent the vector of the most recent iteration of all other parameters. Let be the number of iterations in the MCMC. The posterior samples of can be obtained by the following:

First, we consider updates for ,, and for . If , then draw , , and . If , we have . We use a Metropolis-Hastings step with proposal distribution , where is updated from the average posterior samples of under initial runs, and .

For and , we have and . Thus, we sample via:

where , , and , for .

To obtain samples from we work with . Using slice sampling, we can introduce latent variables and for . The Gibbs steps are given by:

where and

For the update of we have , so we sample from where with and for .

For the update of we have , so we sample where , .

For the update of , we have , so we sample

For the update of we have , so we sample where and .

For the update of we have , so we sample

For the update of , , so we sample .

We do not have conjugacy for and , so we turn to the Metropolis-Hastings algorithm to update these parameters. The Bivariate Beta density of , has a complicated form, however, we can work with the density of the latent variables, : . We sample from the proposal distribution, , where is updated from the average variances and covariance of posterior samples of under initial runs, and is updated from initial runs to optimize mixing.

B.3 Conditional Predictive Ordinate Derivations

Here we provide the details of how we arrived to the expression necessary for computing the CPO values under the DDP mixture model. As our data example in Section 4.1 does not contain any random covariates, we will derive the expression without covariates, however, the derivation can easily be extended to include random covariates in the curve-fitting setting. The hierarchical form of the DDP mixture model without covariates and based on the truncation approximation, , of is given as follows:

with , , , and . Let . The predictive density for a new survival time from group , , is given by:

Let be the experimental group that is not, , and be the normalizing constant for . Namely, . Note, .

The CPO of the survival time in group is defined as, , where is the vector with the member of group removed. Similarly, represents with the member in group removed. Now, consider , which is given by:

Let be the normalizing constant of , specifically:

Then, we can write as:

Thus,

Note, . All that is left is to be able to evaluate :

In summary,

The MCMC approximation of the CPO values is given by:

where is the total number of MCMC iterations.

References

- Bai et al. (2016) Bai, F., Huang, J. & Zhou, Y. (2016). Semiparametric inference for the proportional mean residual life model with right-censored length-biased data. Statistica Sinica 26, 1129–1158.

- Chen et al. (2000) Chen, M.-H., Shao, Q. & Ibrahim, J. (2000). Monte Carlo Methods in Bayesian Computation. Statistics. Springer.

- Chen & Wang (2015) Chen, X. & Wang, Q. (2015). Semiparametric proportional mean residual life model with censoring indicators missing at random. Communications in Statistics 44, 5161–5188.

- Chen (2006) Chen, Y. (2006). Additive regression of expectancy. Journal of the American Statistical Association 102, 153–166.

- Chen & Cheng (2006) Chen, Y. & Cheng, S. (2006). Linear life expectancy regression with censored data. Biometrika 93, 303–313.

- Chen & Cheng (2005) Chen, Y. Q. & Cheng, S. (2005). Semiparametric regression analysis of mean residual life with censored data. Biometrika 92, 19–29.

- De Iorio et al. (2009) De Iorio, M., Johnson, W. O., Müller, P. & Rosner, G. L. (2009). Bayesian nonparametric nonproportional hazards survival modeling. Biometrics 65, 762–771.

- DeYoreo & Kottas (2018) DeYoreo, M. & Kottas, A. (2018). Modeling for dynamic ordinal regression relationships: An application to estimating maturity of rockfish in California. Journal of the American Statistical Association 113, 68–80.

- DeYoreo & Kottas (2020) DeYoreo, M. & Kottas, A. (2020). Bayesian nonparametric density regression for ordinal responses. In Flexible Bayesian Regression Modelling, Eds. Y. Fan, D. Nott, M. S. Smith & J.-L. Dortet-Bernadet, pp. 65–90. Academic Press.

- Ferguson (1973) Ferguson, T. S. (1973). A Bayesian analysis of some nonparametric problems. The Annals of Statistics 1, 209–230.

- Govilt & Aggarwal (1983) Govilt, K. & Aggarwal, K. (1983). Mean residual life function of normal, gamma and lognormal densities. Reliability Engineering 5, 47–51.

- Hall & Wellner (1981) Hall, W. J. & Wellner, J. A. (1981). Mean residual life. In Statistics and Related Topics, Eds. M. Csörgö, D. Dawson, J. Rao & A. Saleh. North-Holland Publishing Company.

- Ibrahim et al. (2001) Ibrahim, J. G., Chen, M. & Sinha, D. (2001). Bayesian Survival Analysis. New York, NY: Springer.

- Ishwaran & James (2001) Ishwaran, H. & James, L. F. (2001). Gibbs sampling methods for stick-breaking priors. Journal of the American Statistical Association 96, 161–173.

- Jin et al. (2020) Jin, P., Zeleniuch-Jacquotte, A. & Liu, M. (2020). Generalized mean residual life models for case-cohort and nested case-control studies. Lifetime Data Analysis 26, 789–819.

- Kottas & Krnjajić (2009) Kottas, A. & Krnjajić, M. (2009). Bayesian semiparametric modeling in quantile regression. Scandinavian Journal of Statistics 36, 297–319.

- Ma et al. (2020) Ma, H., Zhao, W. & Zhou, Y. (2020). Semiparametric model of mean residual life with biased sampling data. Computational Statistics and Data Analysis 142, 106826.

- MacEachern (2000) MacEachern, S. N. (2000). Dependent Dirichlet processes. Technical report, Department of Statistics, Ohio State University.

- Maguluri & Zhang (1994) Maguluri, G. & Zhang, C. (1994). Estimation in the mean residual life regression model. Journal of the Royal Statistical Society, Series B 56, 477–489.

- McKenzie (1985) McKenzie, E. (1985). An autoregessive process for beta random variables. Management Science 31, 988–997.

- Mudholkar & Strivasta (1993) Mudholkar, G. S. & Strivasta, D. K. (1993). Exponentiated Weibull family for analyzing bathtub failure-rate data. IEEE Transactions of Reliability 42, 299–302.

- Müller et al. (1996) Müller, P., Erkanli, A. & West, M. (1996). Bayesian curve fitting using multivariate normal mixtures. Biometrika 83, 67–79.

- Müller et al. (2015) Müller, P., Quintana, F. A., Jara, A. & Hanson, T. (2015). Bayesian Nonparametric Data Analysis. Cham, Switzerland: Springer.

- Nadarajah & Kotz (2005) Nadarajah, S. & Kotz, S. (2005). Some bivariate beta distributions”. Journal of Theoretical and Applied Statistics 39, 457–466.

- Oakes & Dasu (1990) Oakes, D. & Dasu, T. (1990). A note on residual life. Biometrika 77, 409–410.

- Phadia (2013) Phadia, E. G. (2013). Prior Processes and Their Applications. Berlin Heidelberg: Springer.

- Poynor & Kottas (2019) Poynor, V. & Kottas, A. (2019). Nonparametric Bayesian inference for mean residual life functions in survival analysis. Biostatistics 20, 240–255.

- Quintana et al. (2022) Quintana, F. A., Müller, P., Jara, A. & MacEachern, S. N. (2022). The dependent Dirichlet process and related models. Statistical Science 37, 24–41.

- Sethuraman (1994) Sethuraman, J. (1994). A constructive definition of Dirichlet priors. Statistica Sinica 4, 639–650.

- Sun et al. (2012) Sun, L., Song, X. & Zhao, Z. (2012). Mean residual life models with time-dependent coefficients under right censoring. Biometrika 99, 185–197.

- Sun & Zhang (2009) Sun, Z. & Zhang, Z. (2009). A class of transformed mean residual life models with censored survival data. Journal of the American Statistical Association 104, 803–815.

- Taddy & Kottas (2010) Taddy, M. & Kottas, A. (2010). A Bayesian nonparametric approach to inference for quantile regression. Journal of Business and Economic Statistics 28, 357–369.

- Ying et al. (1995) Ying, Z., Jung, S. & Wei, L. (1995). Survival analysis with median regression models. Journal of the American Statistical Association 90, 178–184.