Liquidity Management with Decreasing-returns-to-scale and Secured Credit Line.

Abstract:

This paper examines the dividend and investment policies of a cash constrained firm, assuming a decreasing-returns-to-scale technology and adjustment costs. We extend the literature by allowing the firm to draw on a secured credit line both to hedge against cash-flow shortfalls and to invest/disinvest in productive assets.

We formulate this problem as a bi-dimensional singular control problem and use both a viscosity solution approach and a verification technique to get qualitative properties of the value function. We further solve quasi-explicitly the control problem in two special cases.

Keywords: Investment, dividend policy, singular control, viscosity solution

JEL Classification numbers: C61; G35.

MSC Classification numbers: 60G40; 91G50; 91G80.

1 Introduction

In a world of perfect capital market, firms could finance their operating costs and investments by issuing shares at no cost. As long as the net present value of a project is positive, it will find investors ready to supply funds. This is the central assumption of the Modigliani and Miller theorem [22]. On the other hand, when firms face external financing costs, these costs generate a precautionary demand for holding liquid assets and retaining earnings. This departure from the Modigliani-Miller framework has received a lot of attention in recent years and has given birth to a serie of papers explaining why firms hold liquid assets. Pioneering papers are Jeanblanc and Shiryaev [17], Radner and Shepp [26] while more recent studies include Bolton, Chen and Wang [4], Décamps, Mariotti, Rochet and Villeneuve [7] and Hugonnier, Malamud and Morellec [16]. In all of these papers, it is assumed that firms are all equity financed. Should it runs out of liquidity, the firm either liquidates or raises new funds in order to continue operations by issuing equity. This binary decision only depends on the severity of issuance costs.

The primary objective of our paper is to study a setup where a cash-constrained firm has a mixed capital structure. To do this, we build on the paper by Bolton, Chen and Wang [4] chapter V to allow the firm to access a secured credit line. While [4] assumed a constant-returns-to-scale and homogeneous adjustment costs which allows them to work with the firm’s cash-capital ratio and thus to reduce the dimension of their problem, we rather consider a decreasing-returns-to-scale technology with linear adjustments costs.

Bank credit lines are a major source of liquidity provision in much the same way as holding cash does.

Kashyap, Rajan and Stein [18] found that 70% of bank borrowing by US small firms is through credit line. However, access to credit line is contingent to the solvency of the borrower which makes the use on credit line costly through the interest rate and thus makes it an imperfect substitute for cash (Sufi [28]). From a theoretical viewpoint, the use of credit lines can be justified by moral hazard problems (Holmstrom-Tirole [15]) or from the fact that banks can commit to provide liquidity to firms when capital market cannot because banks have better screening and monitoring skills (Diamond [9])

In this paper, we model credit line as a full commitment lending relationship between a firm and a bank. The lending contract specifies that the firm can draw on a line of credit as long as its outstanding debt, measured as the size of the firm’s line of credit, is below the value of total assets (credit limit). The liability side of the balance sheet of the firm consists in two different types of owners: shareholders and bankers. Should the firm be liquidated, bankers have seniority over shareholders on the total assets.

We assume that the secured line of credit continuously charges a variable spread111The spread may be justified by the cost of equity capital for the bank. Indeed, the full commitment to supply liquidity up to the firm’s credit limit prevents bank’s shareholders to allocate part of their equity capital to more valuable investment opportunities. over the risk-free rate indexed on the firm’s outstanding debt, the higher the size of firm’s line of credit, the higher the spread is. With this assumption, the secured line of credit is somehow similar to the performance-sensitive debt studied in [21] except that the shareholders are here forced to go bankrupt when they are no more able to secure the credit line with their assets.

Many models initiated by Black and Cox [3] and Leland [19] that consider the traditional tradeoff between tax and bankruptcy costs as an explanation for debt issuance study firms liabilities as contingent claims on its underlying assets, and bankruptcy as an endogenous decision of the firm management. On the other hand, these models assume costless equity issuance and thus put aside liquidity problems. As a consequence, the firm’s decision to borrow on the credit market is independent from liquidity needs and investment decisions. A notable exception is a recent paper by Della Seta, Morellec, Zucchi [8] which studies the effects of debt structure and liquid reserves on banks’ insolvency risk. Our model belongs to the class of models that consider endogenous bankruptcy of a firm with mixed capital structure replacing taxes with liquidity constraints.

From a mathematical point of view, problems of cash management have been formulated as singular stochastic optimal control problems. As references for the theory of singular stochastic

control, we may mention the pioneering works of Haussman and Suo [12] and [13] and for application to cash management problems Højgaard and Taksar [14],

Asmussen, Højgaard and Taksar [1], Choulli, Taksar and

Zhou [5], Paulsen [24] among others. To merge corporate liquidity, investment and financing in a tractable model is challenging because it involves a rather difficult three-dimensional singular control problem with stopping where the state variables are the book value of equity, the size of productive asset and the size of the firm credit line while the stopping time is the decision to default. The literature on multi-dimensional control problems relies mainly on the study of leading examples. A seminal example is the so-called finite-fuel problem introduced by Benes, Shepp and Witsenhausen

[2]. This paper provides a rare example of a bi-dimensional optimization problem that combines singular

control and stopping that can be solved explicitly by analytical means. More recently, Federico and Pham [10] have solved a degenerate bi-dimensional singular control problem to study a reversible investment problem where a social planner aims to control its capacity production in order to fit optimally the random demand of a good. Our paper complements the paper by Federico and Pham [10] by introducing firms that are cash-constrained222Ly Vath, Pham and Villeneuve [20] have also studied a reversible investment problem in two alternative technologies for a cash-constrained firm that has no access to external funding. To our knowledge, this is the first time that such a combined approach is used. This makes the problem much more complicated and we do not pretend solving it with full generality, but rather, we pave the way for future developments of these multidimensional singular control models. In particular, we lose the global convexity property of the value function that leads to the necessary smooth-fit property in [10] (see Lemma 8). Instead, we will give properties of the value function (see Proposition 6) and characterize it by means of viscosity solution (see Theorem 2). Furthermore, we will solve explicitly by a standard verification argument the peculiar case of costless reversible investment. A last new result is our characterization of the endogenous bankruptcy in terms of the profitability of the firm and the spread function.

The remainder of the paper is organized as follows. Section 2 introduces the model with a productive asset of fixed size, formalizes the notion of secured line of credit and defines the shareholders value function. Section 3 contains our first main result, it describes the optimal credit line policy and gives the analytical characterization of the value function in terms of a free boundary problem for a fixed size of productive assets. Section 4 is a technical section that builds the value function by solving explicitly the free boundary problem. Section 5 extends the analysis to the case of reversible investment on productive assets and paves the way to a complete characterization of the dividend and investment policies.

2 The No-investment Model

We consider a firm owned by risk-neutral shareholders, with a productive asset of fixed size , whose price is normalized to unity, that has an agreement with a bank for a secured line of credit. The credit line is a source of funds available at any time up to a credit limit defined as the total value of assets. The firm has been able to secure the credit line by posting its productive assets as collateral. Nevertheless, in order to make the credit line attractive for bank’s shareholders that have dedicated part of their equity to this agreement, we will assume that the firm will pay a variable spread over the risk-free rate depending on the size of the used part of the credit line. In this paper, the credit line contract is given and thus the spread is exogenous, see Assumption 1. Finally, building on Diamond’s result [9] we assume that the costs of equity issuance are so high that the firm is unwilling to increase its cash reserves by raising funds in the equity capital market and prefers drawing on the credit line. The firm is characterized at each date by the following balance sheet:

-

•

represents the firm’s productive assets, assumed to be constant333The extension to the case of variable size will be studied in Section 4 and normalized to one.

-

•

represents the amount of cash reserves or liquid assets.

-

•

represents the size of the credit line, i.e. the amount of cash that has been drawn on the line of credit.

-

•

Finally, represents the book value of equity.

The productive asset continuously generates cash-flows over time. The cumulative cash-flows process is modeled as an arithmetic Brownian motion with drift and volatility which is defined over a complete probability space equipped with a filtration . Specifically, the cumulative cash-flows evolve as

where is a standard one-dimensionnal Brownian motion with respect to the filtration .

Credit line requires the firm to make an interest payment that is increasing in the size of the used part of the credit line. We assume that the interest payment is defined by a function where

Assumption 1

is a strictly increasing, continuously differentiable convex function such that

| (1) |

The credit line spread is thus strictly positive and increasing.

The liquid assets earn a rate of interest where represents a carry cost of liquidity444This assumption is standard in models with cash. It captures in a simple way the agency costs, see [7], [16] for more details. Thus, in this framework, the cash reserves evolve as

| (2) |

where is an increasing right-continuous adapted process representing the cumulative dividend payment up to time and is a positive right-continuous adapted process representing the size of the credit line (outstanding debt) at time . Using the accounting relation , we deduce the dynamics for the book value of equity

| (3) |

Finally, we assume the firm is cash-constrained in the following sense:

Assumption 2

The cash reserves must be non negative and the firm management is forced to liquidate when the book value of equity hits zero. Using the accounting relation, this is equivalent to assume bankers get back all the productive assets after bankruptcy.

The goal of the management is to maximize shareholders value which is defined as the expected discounted value of all future dividend payouts. Because shareholders are assumed to be risk-neutral, future cash-flows are discounted at the risk-free rate . The firm can stop its activity at any time by distributing all of its assets to stakeholders. Thus, the objective is to maximize over the admissible control the functional

where

according to Assumption 2. Here (resp. ) is the initial value of equity capital (resp. debt). We denote by the set of admissible control variables and define the shareholders value function by

| (4) |

Remark 1

We suppose that the cash reserves must be non negative (Assumption 2) so to be admissible, a control must satisfy at any time

3 No-investment Model solution

This section derives the shareholders value and the optimal dividend and credit line policies. It relies on a standard HJB characterization of the control problem and a verification procedure.

3.1 Optimal credit line issuance

The shareholders’ optimization problem (4) involves two state variables, the value of equity capital and the size of the credit line , making its resolution difficult. Fortunately, the next proposition will enable us to reduce the dimension and make it tractable the computation of . Proposition 1 shows that credit line issuance is only optimal when the cash reserves are depleted.

Proposition 1

A necessary and sufficient condition to draw on the credit line is that the cash reserves are depleted, that is

Proof: First, by Assumption 2, it is clear that the firm management must draw on the credit line when cash reserves are nonpositive. Conversely, assume that the level of cash reserves is strictly positive. We will show that it is always better off to reduce the level of outstanding debt by using the cash reserves. We will assume that the initial size of the credit line is and denote any admissible strategy. Let us define by the cost of the credit line on the variation of the book value of equity, that is such that the book value of equity dynamics is

| (5) |

Note that is strictly increasing. We first assume that the firm does not draw on the credit line at time 0, . Because , we will built a strategy from as follows:

Note that the credit line issuance strategy consists in always having less debt that under the credit line issuance strategy and because is increasing, the dividend strategy pays more than the dividend strategy . Furthermore, denoting by , equation (5) shows that the bankruptcy time under starting from and the bankruptcy time under starting from have the same distribution. Therefore,

which shows that it is better off to follow than .

So if , it is optimal to set by using units of cash reserves while if , it is optimal to reduce the debt to . In any case, at any time .

Now, if we assume that the firm draw on the credit line at time 0, i.e. , two cases have to be considered.

-

•

which is possible only if . In that case, we set and for .

-

•

. In that case, we take the same strategy with .

According to Proposition 1, we define the value function as . The rest of the section is concerned with the derivation of .

3.2 Analytical Characterization of the firm value

Because the level of capital is assumed to be constant, Proposition 1 makes our control problem one-dimensional. Thus, we will follow a standard verification procedure to characterize the value function in terms of a free boundary problem. In order to focus on the impact of credit line on the liquidity management, we will assume hereafter that . This assumption is without loss of generality but allow us to be more explicit in the analytical derivation of the HJB free boundary problem. We denote by the differential operator:

| (6) |

We start by providing the following standard result which establishes that a smooth solution to a free boundary problem coincides with the value function .

Proposition 2

Assume there exists a and piecewise twice differentiable function on together with a pair of constants such that,

| (7) |

| (8) |

then .

Proof: Fix a policy . Let :

be the dynamic of the book value of equity under the policy . Let us decompose for all where is the continuous part of .

Let the first time when . Using the generalized Itô’s formula, we have :

Because is bounded, the third term is a square integrable martingale. Taking expectation, we obtain

Because , we have therefore the third and the fourth terms are bounded below by

Furthermore is positive because is increasing with and thus the first two terms are positive. Finally,

Letting t and we obtain .

To show the reverse inequality, we will prove that there exists an admissible strategy such that . Let be the solution of

| (9) |

where,

| (10) |

with

whose existence is guaranteed by standard results on the Skorokhod problem (see for example Revuz and Yor [27]). The strategy is admissible. Note also that is continuous on . It is obvious that for . Now suppose . Along the policy , the liquidation time coincides with because . Proceeding analogously as in the first part of the proof, we obtain

where the last two equalities uses, and . Now, because ,

Furthermore, because has at most linear growth and is admissible, we have

Therefore, we have by letting tend to ,

which concludes the proof.

Remark 2

We notice that the proof remains valid when and is infinite by a standard localisation argument which will be the case in section 4.

3.3 Optimal Policies

The verification theorem allows us to characterize the value function. The following theorem summarizes our findings.

Theorem 1

Under Assumption 1 and 2, the following holds:

-

•

If , it is optimal to liquidate the firm, .

-

•

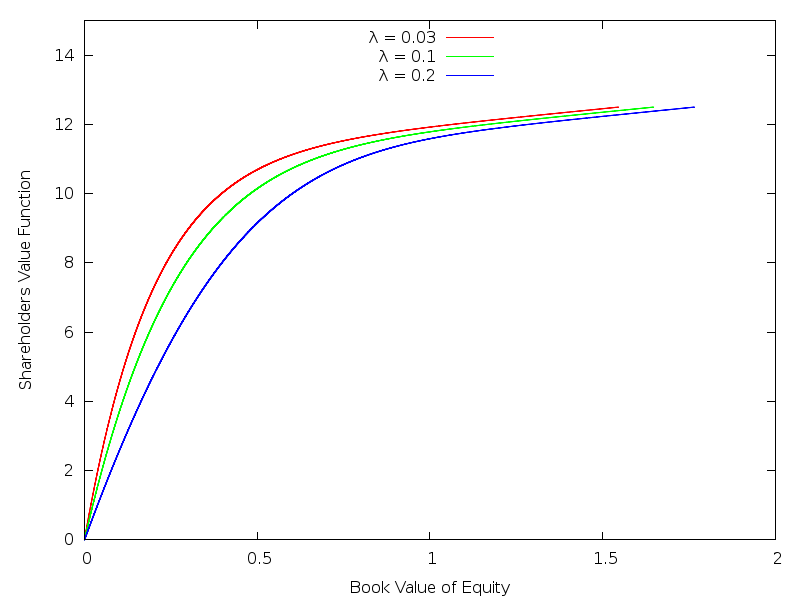

If , the value of the firm is an increasing and concave function of the book value of equity. Any excess of cash above the threshold is paid out to shareholders.(See Figure 1).

-

•

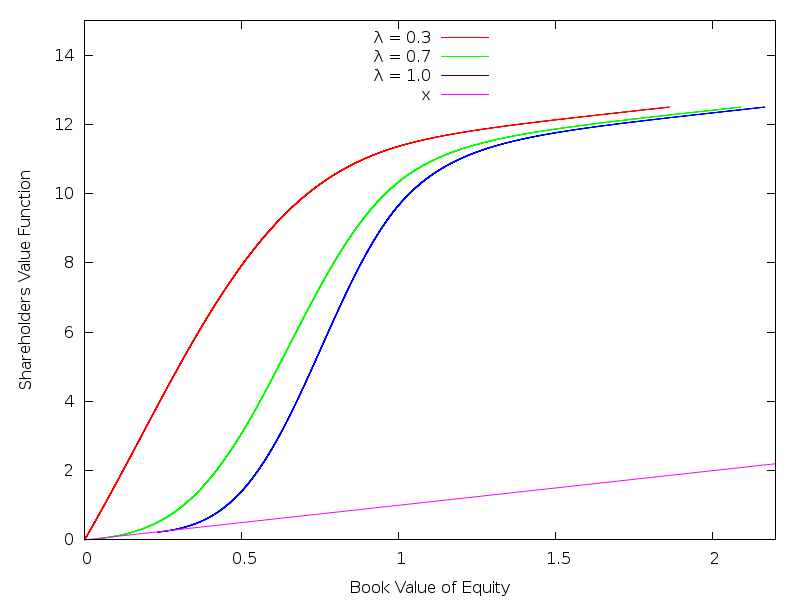

If , the value of the firm is an increasing convex-concave function of the book value of equity. When the book value of equity is below the threshold , it is optimal to liquidate. Any excess of cash above the threshold is paid out to shareholders.(See Figure 2)

It is interesting to compare our results with those obtained in the case of all equity financing. First, because the use of credit line is costly, it is optimal to wait that the cash reserves are depleted to draw on it. Moreover, there exists a target cash level above which it is optimal to pay out dividends. These two first findings are similar to the case of all equity financing. On the other hand, the marginal value of cash may not be monotonic in our case. Indeed, when the cost of the credit line is high, it becomes optimal for shareholders to terminate the lending relationship. This embedded option value makes the shareholder value locally convex in the neighborhood of the liquidation threshold . The higher is the cost, measured by in our simulation, the sooner is the strategic default or equivalently, the value function decreases, while the embedded exit option increases, with the cost of the credit line. The strategic default comes from the fact that the instantaneous firm’s profitability becomes negative for low value of equity capital. This is a key feature of our model that never happens when the firm is all-equity where the marginal value of cash at zero is the only statistic either to trigger the equity issuance or to liquidate.

Figure 1 plots some value functions, when , using a linear function for , with different values of .

Figure 2 plots some value functions, when , using a linear function for , for different values of .

Next section is devoted to the proof of Theorem 1. The proof is based on an explicit construction of a smooth solution of the free boundary problem and necessitates a series of technical lemmas.

4 Solving the free boundary problem

The first statement of Theorem 1 comes from the fact that the function satisfies Proposition 2 when . To see this, we have to show that is nonpositive for any . A straightforward computation gives

Using Equation (1) of Assumption 1, we observe that is nondecreasing for and nonpositive at when .

Hereafter, we will assume that and focus on the existence of a function and a pair of constants satisfying Proposition 2. We will proceed in two steps. First we are going to establish some properties of the solutions of the differential equation . Second, we will consider two different cases- one where the productivity of the firm is always higher than the maximal interest payment , the other where the interest payment of the loan may exceed the productivity of the firm .

Standard existence and uniqueness results for linear second-order differential equations imply that, for each , the Cauchy problem :

| (11) |

has a unique solution over . By construction, this solution satifies . Extending linearly to as , for yields a twice continuously differentiable function over , which is still denoted by .

4.1 Properties of the solution to the Cauchy Problem

We will establish a serie of preliminary results of the smooth solution of (11).

Lemma 1

Assume . If then is increasing and thus positive.

Proof: Because , and , the maximum principle implies on . Let us define

If then . By unicity of the Cauchy problem, this would imply which contradicts . Thus, . If , we would have , and and thus which is a contradiction. Therefore is always positive.

Lemma 2

Assume . We have and on .

Proof: Because is smooth on , we differentiate Equation (11) to obtain,

As and , it follows that , and thus over some interval , where . Now suppose by way of contradiction that for some and let . Then and for , so that for all . Because , this implies that for all ,

which contradicts . Therefore over . Furthermore, using Lemma 1,

The next result gives a sufficient condition on to ensure the concavity of on .

Corollary 1

Assume and , we have and over .

Proof: Proceeding analogously as in the proof of Lemma 2, we define such that and for , so that for all . Because , , we have

Denote by the function

We have by Assumption 1. Because if , we have for which contradicts and by Lemma 2. Therefore over , from which it follows and is concave on . Because Lemma 2 gives the concavity of on , we conclude. The next proposition establishes some results about the regularity of the function for a fixed .

Lemma 3

For any , is an increasing function of b over and strictly decreasing over .

Proof: Consider the solutions and to the linear second-order differential equation over characterized by the initial conditions , , , . We first show that and are strictly positive on . Because and , one has , such that over some interval where . Now suppose by way of contradiction that . Then and . Because , it follows that , which is impossible because and is strictly increasing over . Thus over , as claimed. The proof for is similar, and is therefore omitted.

Next, let be the Wronskian of and . One has and

Because is integrable, the Abel’s identity follows by integration:

Because , and are linearly independent. As a result of this, is a basis of the two-dimensional space of solutions to the equation . It follows in particular that for each , on can represent as :

Using the boundary conditions and , on can solve for as follows:

Using the derivative of the Wronskian along with the fact that is solution to , it is easy to verify that:

So is an increasing function of b over and strictly decreasing over .

Corollary 2

If , then .

4.2 Existence of a solution to the free boundary problem

We are now in a position to characterize the value function and determine the optimal dividend policy. Two cases have to be considered: when the profitability of the firm is always higher than the maximal interest payment () and when the interest payment exceeds the profitability of the firm ().

4.2.1 Case:

The next lemma establishes the existence of a solution to the Cauchy problem (11) such that .

Lemma 4

There exists such that the solution to (11) satisfies .

Proof:

Because , we know from Corollary 1 that is a concave function on .

Moreover, because , . Because is strictly concave over with and , for all . In particular, .

Moreover, we have :

Therefore, Lemma 3 implies . Finally by continuity there is some such that which concludes the proof.

The next lemma establishes the concavity of .

Lemma 5

The function is concave on

Proof:

Because , Lemma 2 implies that is concave on thus .

For , we differentiate the differential equation satisfied by to get,

| (12) |

Because we have .

Now, suppose by a way of contradiction that on some subinterval of . Because is continuous and nonpositive at the boundaries of , there is some such that and . But, this implies

which is a contradiction with Lemma 1.

Proposition 3

If , is the solution of the control problem (9).

Proof:

Because is concave on and , on . Therefore we have a twice continuously differentiable concave function and a pair of constants satisfying the assumptions of Proposition 2 and thus .

When the maximal interest payment is lower than the firm profitability, the value function is concave. This illustrates the shareholders’ fear to liquidate a profitable firm. In particular, the shareholders value is a decreasing function of the volatility.

4.2.2 Case:

We first show that, for all , there exists such that is the solution of the Cauchy Problem (11) with .

Lemma 6

For all , we have .

Proof: Because is continuous with and , there exists such that . Differentiating Equation (11), we observe

using Equation (1). Therefore is convex in a left neighborhood of . If is convex on then for small enough and the result is proved.

If is not convex on then it will exist some such that , and convex on . Differentiating Equation (11) at gives . Therefore is nonincreasing in a neighborhood of . Assume by a way of contradiction that is increasing at some point . This would imply the existence of such that , and which contradicts Equation (11).

Therefore is decreasing on and convex on which implies that for all .

To conclude, for any , we can find small enough to have

which can be extended to by Lemma 3.

Corollary 3

For all , there is an unique such that .

Proof:

By Lemma 1, is concave on , thus .

Suppose that there exists in such that , then there exists such that , , yielding to the standard contradiction with the maximum principle. We thus have for all . Using Lemma 6 and the continuity of the function , it exists for all a threshold such that . The uniqueness of comes from Corollary 2.

We will now study the behavior of the first derivative of .

Lemma 7

There exists such that and .

Proof: Because and , it exists such that

| (13) |

Moreover is strictly concave on by Lemma 2 and thus

Because by Lemma 2, we have on , there exists such that . Let . By Corollary 3, it exists such that . We have and then by Corollary 2.

Let us consider the function , we have , . Moreover, is solution

| (14) |

On , the second member of Equation (14) is negative due to Equation (13). On , it is equal to which is negative because . Assume by a way of contradiction that there is some such that , then it would exist such that and which is in contradiction with Equation (14). Hence, is a positive function on with which implies .

Lemma 8

When , is a convex-concave function.

Proof: According to Corollary 3, there exists such that and by Lemma 1, on . Using Equation (11), we thus have implying that is strictly convex on a right neighborhood of . Because , Lemma 2 implies on . If there is more than one change in the concavity of , it will exist such that , and yielding the standard contradiction.

Proposition 4

If and , is the shareholders value function (4)

Proof: It is straightforward to see that the function satisfies Proposition 2 when .

Now, we will consider the case .

Lemma 9

If , it exists such that and .

Proof: Let . By assumption, we have and by Lemma 7, . By continuity of , there exists such that . By definition, the function satisfies .

Lemma 10

is a convex-concave function on .

Proof: First, we show that is increasing on . Because , we can define . If , we will have , and yielding the standard contradiction. According to Lemma 1, we have over because . Proceeding analogously as in the proof of Lemma 8, we prove that is a convex-concave function because it cannot change of concavity twice.

Lemma 11

We have on with .

Proof: According to Lemma 10, is convex-concave with and , therefore . As a consequence, on and in particular . Remembering that and using Corollary 2, we have .

Proposition 5

Proof: it is straightforward to check that satisfies Proposition 2.

5 The Investment Model

In this section, we enrich the model to allow variable investment in the productive assets. We will assume a decreasing-returns-to-scale technology by introducing an increasing concave function with that impacts the dynamic of the book value of equity as follows:

| (15) |

where (resp. ) is the cumulative capital invested (resp. disinvested) in the productive assets up to time , is an exogenous proportional cost of investment. Assumption (2) thus forces liquidation when the level of outstanding debt reaches the sum of the liquidation value of the productive assets and the liquid assets, . The goal of the management is to maximize over the admissible strategies the risk-neutral shareholders value

| (16) |

where

By definition, we have

| (17) |

5.1 Dynamic programming and free boundary problem

In order to derive a classical analytic characterization of in terms of a free boundary problem, we rely on the dynamic programming principle as follows

Dynamic Programming Principle: For any where , we have

| (18) |

where is any stopping time.

Take the suboptimal control which consists in investing only at time a certain amount . Then, according to the dynamic programming principle, we have with ,

So,

Dividing by , we have

If were smooth enough, we can let tend to to obtain

Likewise, we can prove that

and

where is the second order differential operator

| (19) |

The aim of this section is to characterize via the dynamic programming principle the shareholders value as the unique continuous viscosity solution to the free boundary problem in order to use a numerical procedure to describe the optimal policies.

| (20) |

where

We will first establish the continuity of the shareholders value function which relies on some preliminary well-known results about hitting times we prove below for sake of completeness.

Lemma 12

Let and a sequence of real numbers such that and . Let the solution of the stochastic differential equation

where and satisfy the standard global Lipschitz and linear growth conditions. Moreover, are strictly positive real numbers converging to and is a sequence of bounded functions converging uniformly to . Let us define and . We have

Proof: Let us define the functions , on some bounded interval I containing as

Because converges uniformly to , we note that converges uniformly to where

and

Let , and with and . We first show that is integrable. Because is the scale function of the process , is a local martingale with quadratic variation

Because

the processes and are both martingales. By Optional sampling theorem

which implies

and

thus there is a constant such that

We conclude by dominated convergence that is integrable. The martingale property implies

which yields

by dominated convergence because

This is equivalent to

with . Hence,

Moreover,

Using the uniform convergence of , we have

Lemma 13

Let and a sequence of real numbers such that and . Let the solution to

with the same assumptions as in Lemma 12. There exist constants and such that

| (21) |

Proof: Because are bounded functions, there are two constants and such that for all . We define . By comparison, we have and , with . But the Laplace transform of is explicit and given by

which gives the left inequality of (21). The proof is similar for the right inequality introducing .

Proposition 6

The shareholders value function is jointly continuous.

Proof: Let and let us consider a sequence in converging to . Therefore, for large enough. We consider the following two strategies that are admissible for large enough:

-

•

Strategy : start from , invest if (or disinvest if ) and do nothing up to the minimum between the liquidation time and the hitting time of . Denote the control process associated to strategy .

-

•

Strategy : start from , invest if (or disinvest if ) and do nothing up to the minimum between the liquidation time and the hitting time of . Denote the control process associated to strategy .

To fix the idea, assume . The strategy makes the process jump from to .

![[Uncaptioned image]](/html/1411.7670/assets/strategies_graph.jpg)

Define

and

Dynamic programming principle and on yield

| (22) |

On the other hand, using on

| (23) |

The convergence of implies

from which we deduce using Lemma 12 that

| (24) |

and

| (25) |

Let and . The function is bounded by

thus, according to Lemma 13

with

.

Letting tend to and using

We are now in a position to characterize the shareholders value in terms of viscosity solution of the free boundary problem (20).

Theorem 2

The shareholders value is the unique continuous viscosity solution to (20) on with linear growth.

Proof: The proof is postponed to the Appendix

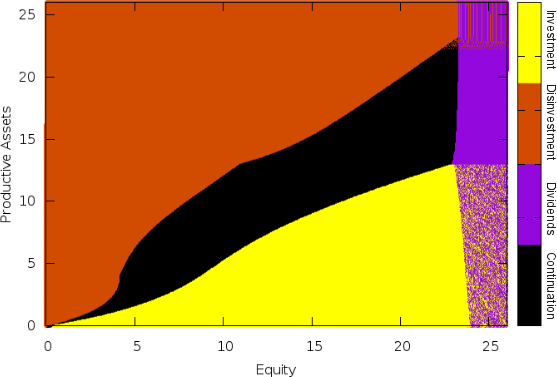

The main interest of Theorem 2 is to guarantee that the standard numerical procedure to solve HJB free boundary problems proposed in [11] will converge to the shareholders value function. We obtain the following description of the control regions (Figure 3). Our numerical analysis demonstrates that

-

•

unlike [4], there exists an optimal level of productive assets (top of the yellow region) and thus an objective measure of managerial overinvestment in our context. This is clearly due to the decreasing-returns-to-scale assumption.

-

•

constrained firms with low cash reserves, that is when equity capital is close to productive asset size, and low equity capital will rather disinvest to offset cash-flows shortfalls.

-

•

constrained firms with low cash reserves and high equity capital will first draw on the credit line to offset cash-flows shortfalls.

-

•

the credit line is never used to invest.

While the numerical results give the above insights about the optimal policies, we have not been able to prove rigorously the shape of the optimal control regions. Nonetheless, making the strong assumption that there is no transaction cost allows us to fully describe the control regions and gives us reasons to believe in Figure 3. This is the object of our last subsection.

5.2 Absence of Investment cost

Using a verification procedure analogous to section 3, we characterize the value function and the optimal policies in terms of a free boundary problem. The following proposition proved in the Appendix summarizes our findings.

Proposition 7

When there is no cost of investment/disinvestment, , the following holds:

-

•

If then it is optimal to liquidate the firm thus .

-

•

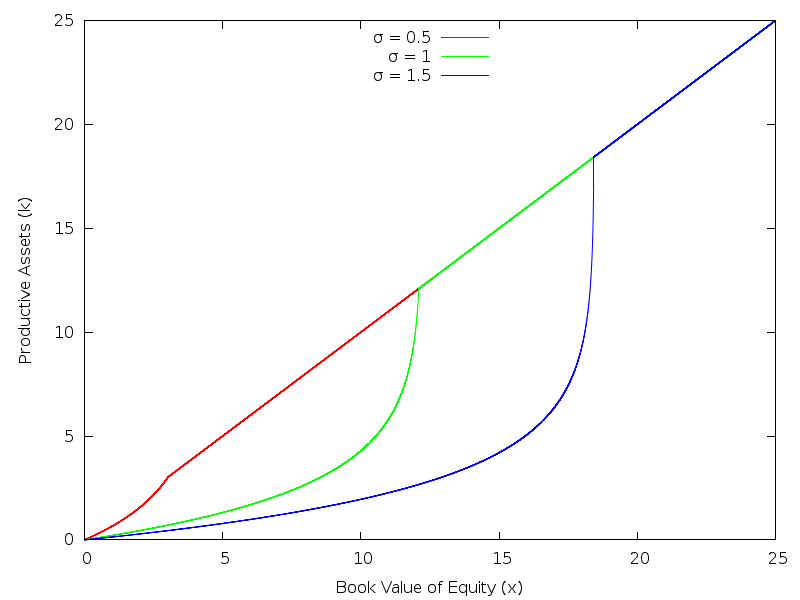

If and , the shareholders value is an increasing and concave function of the book value of equity. Any excess of cash above the threshold is paid out to shareholders (see Figure 4). The optimal size of the productive asset is characterized by a deterministic function of equity capital (see Figure 5) given by

where is the unique nonzero solution of the equation

(27) with

(28) -

•

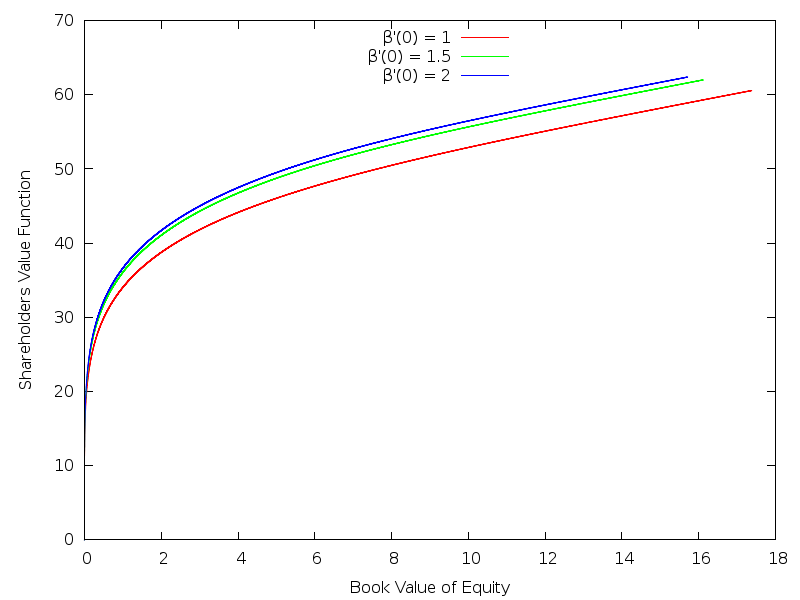

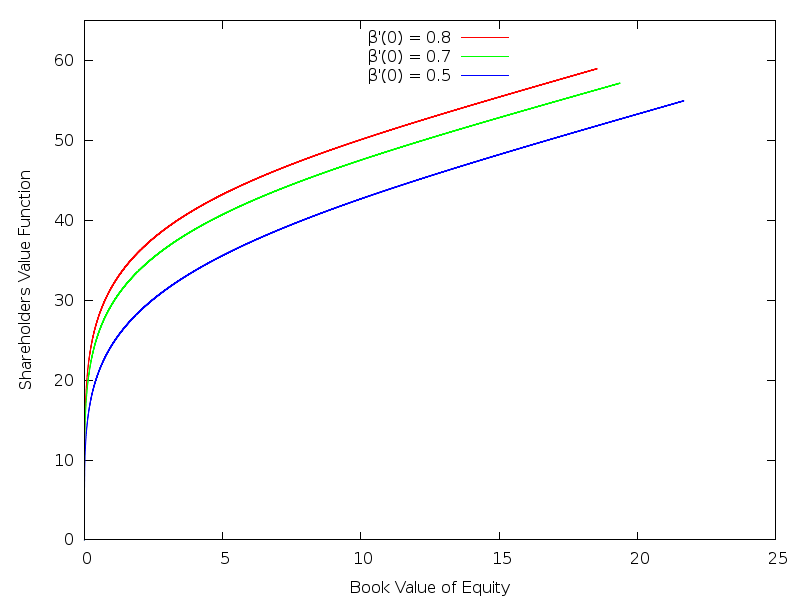

If and , the shareholders value is an increasing and concave function of the book value of equity (see Figure 6). Any excess of cash above the threshold is paid out to shareholders. Moreover, all the cash reserves are invested in the productive assets.

The above proposition has two interesting implications.

-

•

When the volatility of earnings is low , it is optimal to invest all the cash reserves in the productive assets and use it as a complementary substitute for cash which is better off than using a costly credit line.

-

•

Nonetheless, when the volatility of earnings is high, productive assets are not a perfect substitute of cash because it implies a high risk of bankrupcy when the book value of equity is low.

Figure 4 plots the shareholders value functions with and for different values of using :

-

•

a linear function for , .

-

•

an exponential function for , .

Figure 5 plots the optimal level of productive assets for different values of . It shows that, for a given level of the book value of equity, the investment level in productive assets is a decreasing function of the volatility.

Figure 6 plots the shareholders value functions when and for different values of using :

-

•

a linear function for , .

-

•

an exponential function for , .

6 Appendix

6.1 Proof of Theorem 2

Supersolution property. Let and s.t. is a

minimum of in a neighborhood of with small enough to ensure and .

First, let us consider the admissible control

where the shareholders decide

to never invest or disinvest, while the dividend policy is defined by

for , with . Define the exit time . We notice

that for small enough. From the dynamic programming principle, we have

| (29) | |||||

Applying Itô’s formula to the process between and , and taking the expectation, we obtain

| (30) | |||||

Combining relations (29) and (30), we have

| (31) |

-

Take first . We then observe that is continuous on and only the first term of the relation (31) is non zero. By dividing the above inequality by with , we conclude that

-

Take now in (31). We see that jumps only at with size , so that

By sending , and then dividing by and letting , we obtain

Second, let us consider the admissible control

where the shareholders decide

to never payout dividends, while the investment/disinvestment policy is defined by for , with . Define again the exit time .

Proceeding analogously as in the first part and observing that jumps only at , thus

Assuming first , by sending , and then dividing by and letting , we obtain

When , we get in the same manner

This proves the required supersolution property.

Subsolution Property: We prove the subsolution property by contradiction. Suppose that the claim is not true. Then, there exists and a neighbourhood of , included in for small enough, a function with and on , and , s.t. for all we have

| (32) | |||||

| (33) | |||||

| (34) | |||||

| (35) |

For any admissible control , consider the exit time and notice again that . Applying Itô’s formula to the process between and , we have

| (41) | |||||

| (42) | |||||

| (43) | |||||

| (44) | |||||

| (45) |

Note that , and by the Mean Value Theorem, there is some such that,

Therefore,

Notice that while , is either on the boundary or out of . However, there is some random variable valued in such that:

Proceeding analogously as above, we show that

Observe that

Starting from , the strategy that consists in investing or disinvesting depending on the sign of and payout as dividends leads to and therefore,

Using , we deduce

Hence,

| (46) | |||||

We now claim there is such that for any admissible strategy

Let us consider the function, with,

where

satisfies

Applying Itô’s formula, we have

| (48) | |||||

Noting that and , we have

Plugging into (48) with , we obtain

This proves the claim (6.1). Finally, by taking the supremum over and using the dynamic programming principle, (46) implies

, which is a contradiction.

Uniqueness Suppose is a continuous subsolution and a continuous supersolution of (20) on satisfying the boundary conditions

and the linear growth condition

for some positive constants and . We will show by adapting some standard arguments that .

-

Step 1:

(49) and

and define for the continuous function on

Because

and

we have that

which implies that is a strict supersolution of (20). To prove this point, one only needs to take and such that is a minimum of and notice that is also a minimum of with which allows us to use that is a viscosity supersolution of (20).

-

Step 2:

In order to prove the strong comparison result, it suffice to show that for every

Assume by a way of contradiction that there exists such that

(50) Because and have linear growth, we have

Using the boundary conditionsand the linear growth condition, it is always possible to find in Equation (49) such that both expressions above are negative and maximum in Equation (50) is reached inside the domain .

By continuity of the functions and , there exists a pair with such that

For , let us consider the functions

By standard arguments in comparison principle of the viscosity solution theory (see Pham [25] section 4.4.2.), the function attains a maximum in , which converges (up to a subsequence) to when goes to zero. Moreover,

| (51) |

Applying Theorem 3.2 in Crandall Ishii Lions [6] , we get the existence of symmetric square matrices of size 2 , such that:

and

| (54) |

where

and

| (61) |

so

Equation (54) implies

| (62) |

Because and are respectively subsolution and strict supersolution, we have

| (63) |

and

| (64) |

We then distinguish the following four cases:

-

•

Case 1. If then we get from (64), yielding a contradiction when goes to .

-

•

Case 2. If then we get from (64) yielding a contradiction when goes to .

-

•

Case 3. If , then we get from (64) yielding a contradiction when goes to .

-

•

Case 4. If

From

we deduce

Using (62) we get,

By sending to zero and using the continuity of , , and we obtain the required contradiction: .

This ends the proof.

6.2 Proof of the Proposition 7

Because is concave and goes to , the existence of is equivalent to assume

| (65) |

Let us define the function for as the unique solution on of the Cauchy problem

with for and differentiable at .

Remark 3

The Cauchy problem is well defined with the condition differentiable at . Moreover, it is easy to check, using the definition of , that the function is also . Because the cost of debt is high, the shareholders optimally choose not to issue debt but rather adjust costlessly their level of investment.

Lemma 14

For every the function is increasing.

Proof: Clearly, is increasing and thus positive on . Let . because is increasing and positive in a left neighborhood of . Thus, according to the differential equation, we have which implies that is also increasing in a right neighborhood of . Therefore, cannot become negative.

Lemma 15

For every , there is some such that and is a concave function on .

Proof: Assume by a way of contradiction that does not vanish. Using Equations (28) and (27), we have

Therefore, we equivalently assume that . This implies that is stricly decreasing and bounded below by by lemma 14 therefore is an increasing concave function. Therefore, exists and is denoted by . Letting in the differential equation, we obtain, because has a finite limit,

Therefore, either is from which we get a contradiction or finite from which we get by mean value theorem. In the second case, differentiating the differential equation, we have

| (66) |

Proceeding analogously, we obtain that and thus . Coming back to the differential equation, we get

which contradicts that is increasing. Now, define to conclude.

Lemma 16

There exists such that .

Proof: For every , we have

| (67) |

Let . Lemma 14 yields

Therefore, Equation (67) yields .

On the other hand, let . By construction, and thus by concavity of on . Thus, there is some such that

Hereafter, we denote .

Lemma 17

We have .

Proof: Differentiating the differential equation and plugging , we get

Because is increasing in a left neighborhood of , we have implying the result.

Let us define

We are in a position to prove the following proposition

Proposition 8

The shareholders value is .

Proof:

We have to check that satisfies the standard HJB free boundary problem. By construction, is a concave function on satisfying . It remains to check .

For , we have

If , concavity of and Lemma 17 implies

If , we differentiate with respect to and obtain using again concavity of and convexity of ,

Therefore, .

Let , because is concave, the same argument as in the previous lines shows that

and therefore

First order condition gives for

Thus for , we have

which gives,

Therefore the maximum of lies in the interior of the interval and satisfies:

Hence, for , we have by construction

Now, fix . We note that has the same sign as because is strictly increasing. Moreover, because is concave and increasing, we have

Thus, it suffice to prove for or equivalently because is a positive function that the function defined as

is positive. We make a proof by contradiction assuming there is some such that . As by Equation 27 and then there is some such that

Using the differential equation (66) satisfied by , we obtain

from we deduce

But and thus . Moreover, by definition of , we have . Therefore, Equation (28) yields

which is a contradiction.

To complete the characterization of the shareholders value when the cost of debt is high, we have to study the optimal policy when (65) is not fulfilled. We expect that in that case which means that for all , the manager should invest all the cash in productive assets. Thus we are interested in the solutions to

| (68) |

such that .

Proposition 9

Suppose that the functions and are analytic in with a radius of convergence . The solutions to Equation (68) such that are given by

with

where the functions and are

the function is given by

and is the positive root of

The radius of convergence of is at least equal to .

Proof:

This result is given by the Fuchs’ theorem [23].

Note that the solutions of Equation (68) vanishing at zero can be written

If the radius of convergence of the Frobenius series is finite, then the previously defined function can be extended by use of the Cauchy theorem.

Because , we have . As a consequence, we have

Thus, proceeding analogously as in Lemma 15, we prove the existence of such that . Because is linear in , we choose to get a concave solution to (68) with , and . We extend linearly on as usual to obtain a function on .

Proposition 10

The shareholders value is .

Proof: It suffices to check that satisfies the free boundary problem. By construction is a concave function on . Because , we have

and

On , we have

Using concave increasing, convexe, , we have

Then using the concavity of ,

It remains to show that for every

Using concave , convex, and concave increasing, we have

Thus,

Moreover,

We expect

Notice that and

because and is increasing. Thus it is enough to prove for every ,

or equivalently, using ,

for . We make a proof by contradiction assuming the existence of such that . In a neighborhood of , we have

and

From which we deduce because ,

yielding

But thus there is such that

Using the derivative of Equation (68)

from which we deduce :

Now, remember that and thus using the concavity of , we have . Furthermore, when Equation (27) is not fulfilled. Hence,

which yields to a contradiction and ends the proof.

References

- [1] Asmussen, A., Højgaard, B., Taksar, M.: Optimal risk control and dividend distribution policies. Example of excess-of loss reinsurance for an insurance corporation. Finance and Stochastics, 4, 299-324 (2000)

- [2] Benes, V.E., Shepp, L.A., Witsenhausen, H.S.: Some solvable stochastic control problems.Stochastics, 4, 38-83 (1980)

- [3] Black, F., and J. Cox, 1976, Valuing Corporate Securities: Some Effects of Bond Identures Provisions, Journal of Finance, 31, 351-367 (1976)

- [4] Bolton, P., Chen, H., Wang, N.: A unified theory of Tobin’s q, corporate investment, financing, and risk management, Journal of Finance, (2011)

- [5] Choulli, T.,Taksar, M., Zhou, X.Y.: A diffusion model for optimal dividend distribution for a company with constraints on risk control. SIAM Journal of Control and Optimization, 41, 1946-1979 (2003)

- [6] Crandall M.G, Ishii H and Lions P.L: User’s guide to viscosity solutions of second order Partial differential equations, Bull.Amer.Soc. 27, 1-67 (1992).

- [7] Décamps, J.P., Mariotti, T., Rochet, J.C. and Villeneuve, S: Free cash-flows, Issuance Costs, and Stock Prices, Journal of Finance, 66, 1501-1544 (2011).

- [8] Della Sera M., Morellec E. and Zucchi F.: Debt Structure, Rollover Traps and Default Risk, working paper EPFL (2015)

- [9] Diamond, D.: Financial Intermediation and Delegated Monitoring, Review of Economic Studies, 51, 393-414 (1984)

- [10] Federico,S,. Pham, H.: Characterization of the optimal boundaries in reversible investment problems, SIAM Journal of Control and Optimization, 52, 2180–2223 (2014).

- [11] Forsyth, P. and Laban G: Numerical Methods for Controlled Hamilton Jacobi Bellman PDEs in finance,Journal of Computational Finance, 11, pp 1-44 (2007)

- [12] Haussman U.G., Suo W.: Singular optimal stochastic controls I: existence, SIAM Journal of Control and Optimization, 33, 916-936 (1995).

- [13] Haussman U.G., Suo W.: Singular optimal stochastic controls II: dynamic programming, SIAM Journal of Control and Optimization, 33, 937-959 (1995).

- [14] Hojgaard, B., Taksar, M.: Controlling risk exposure and dividends pay-out schemes: Insurance company example, Mathematical Finance 9, 153-182 (1999).

- [15] Holmstrom, B. and Tirole, J.: Private and Public Supply of Liquidity, Journal of Political Economy, 106, pp 1-40

- [16] Hugonnier, J., Malamud, S. and Morellec, E.: Capital supply uncertainty, cash holdings and Investment, Review of Financial Studies, 28, pp 391-445 (2015)

- [17] Jeanblanc-Picqué, M., Shiryaev, A.N.: Optimization of the flow of dividends. Russian Mathematics Surveys, 50, 257-277 (1995)

- [18] Kashyap A., Rajan R. and Stein J.: Banks as Liquidity Providers: An Explanation for the Co-Existence of Lending and Deposit-Taking. Journal of Finance 57 33-73, (2002)

- [19] Leland, H.E.: Corporate debt value, bond covenants, and optimal capital structure. Journal of Finance 49, 1213-1252, (1994)

- [20] Ly Vath V., Pham, H. and Villeneuve, S. :A mixed singular/switching control problem for a dividend policy with reversible technology investment. Annals of Applied Probability, Vol 18 N°3, p1164-1200,(2008).

- [21] Manso, G., Strulovici B. and Tchistyi A.: Performance-sensitive debt,The Review of Financial Studies, 23 1819-1854 (2010)

- [22] Miller, M.H., Modigliani, F.: Dividend policy, growth and the valuation of shares, Journal of Business, 34, 311-433 (1961)

- [23] Nakhlé H. : Partial differential equations with Fourier series and boundary value problems, Upper Saddle River, NJ: Pearson Prentice Hall (2005)

- [24] Paulsen, J.: Optimal dividend payouts for diffusions with solvency constraints. Finance and Stochastics, 7,457-474 (2003)

- [25] Pham H.: Continuous-time Stochastic Control and Optimization with Financial Applications, Springer (2009)

- [26] Radner, R., Shepp, L.: Risk versus profit potential: A model for corporate strategy, Journal of Economic Dynamics and Control 20, 1373-1393 (1996)

- [27] Revuz, D., Yor, M.: Continuous Martingales and Brownian Motion, Springer 3rd ed. (1999).

- [28] Sufi, A.: Bank Lines of Credit in Corporate Finance, Review of Financial Studies, 22, 1057-1088 (2009)