Asymptotic behaviour of the fractional Heston model

Abstract.

We consider the fractional Heston model originally proposed by Comte, Coutin and Renault [12]. Inspired by recent ground-breaking work on rough volatility [2, 6, 24, 26] which showed that models with volatility driven by fractional Brownian motion with short memory allows for better calibration of the volatility surface and more robust estimation of time series of historical volatility, we provide a characterisation of the short- and long-maturity asymptotics of the implied volatility smile. Our analysis reveals that the short-memory property precisely provides a jump-type behaviour of the smile for short maturities, thereby fixing the well-known standard inability of classical stochastic volatility models to fit the short-end of the volatility smile.

Key words and phrases:

Stochastic volatility, implied volatility, asymptotics, fractional Brownian motion, Heston model2010 Mathematics Subject Classification:

60F10, 91G99, 91B251. Introduction

Since the Black-Scholes model was introduced forty years ago, practitioners and academics have been proposing refinements thereof in order to take into account the specific behaviour of market data. In particular, stochastic volatility models, turning the constant Black-Scholes instantaneous volatility of returns into a stochastic process, have been studied and used heavily. Monographs such as [23, 25, 29, 30, 40, 47] are great sources of information regarding this large class of models, both from a theoretical point of view (existence and uniqueness of these processes, asymptotic behaviour), and with practitioner’s insights (how these models actually perform, how they should behave compared to market data). Despite the success of these models, it is now widely understood that calibration of the observed implied volatility surface fails for short maturities, the observed smile being steeper than that generated by diffusions with continuous paths. To remedy this issue, several authors have suggested the addition of jumps, either in the form of an independent Lévy process [5] or within the more general framework of affine processes [33, 39]. Jumps (in the stock price dynamics) imply an explosive behaviour for the implied volatility for short maturities (see [51] for a review of this phenomenon), but are able to capture the observed steepness of the implied volatility. This could be the end of the modelling story; however, this approach has also had (and still has) his share of controversy since the jump part of the process is notoriously difficult to hedge, making its practical implementation a rather delicate (and sometimes philosophical) issue.

From a time series modelling point of view, classical stochastic volatility models, driven by a Brownian motion, have been criticised for not taking into account the long memory of the observed volatility of returns. In ARCH and GARCH models, memory (quantified through the autocorrelation function) decays exponentially fast, whereas it does not decay at all for integrated versions of these. In the discrete-time setting, this has led to the introduction of fractionally integrated models, such as ARFIMA [27] and FIGARCH [3]. In continuous time, this long-memory behaviour has been modelled through fractional Brownian motion [11, 12] with Hurst exponent strictly greater than . Fractional Brownian motion has its pitfalls though, since it is not a semimartingale, and yields arbitrage opportunities [48, 50]. This can be avoided using heavy machinery [10, 19, 28, 32], but as a by-product introduces non-desirable economic features [9]. As documented in [52], these issues are however not relevant when the fractional Brownian motion drives the instantaneous volatility rather than the stock price itself.

These fractional stochastic volatility models, somehow popular in the econometrics and statistics communities, have however received little attention from more classical mathematical finance and stochastic analysis groups. Gatheral, Jaisson and Rosenbaum [26] have recently suggested to consider the Hurst exponent, not as an indicator of the historical memory of the volatility, but as an additional parameter to be calibrated on the volatility surface. Their study reveals that , which seems to indicate short memory of the volatility, thereby contradicting decades of time series analyses. By considering a specific fractional volatility model, directly inspired by the fractional version of the Heston model [12, 31], we provide a theoretical justification of this result. We show in particular that, when , the implied volatility in this model explodes in the jump-sense. Probabilistically speaking, this means that a rescaled (by time) version of the log stock price process converges weakly, but not the process itself, which is reminiscent of what happens in the case of jump-diffusions. In the case , heuristically, long memory does not have time to affect the dynamics of the process and the implied volatility converges to a strictly positive constant. For large maturities, the phenomenon is reversed, in the sense that short memory gets somehow averaged out and the behaviour of the implied volatility is similar to the standard Brownian-driven diffusion case, whereas long memory yields a different asymptotic behaviour. Finally, we comment that recently another fractional version of the Heston model was proposed and analysed in [16, 17, 18], in which the authors defined a different structure for the variance process through fractional integration. In particular, El Euch, Fukasawa and Rosenbaum [18] bridge the connection between market microstructure and rough volatility by proposing a microscopic price model and by showing that it converges to a rough Heston setting in the long term. We also refer interested readers to [1, 6, 7, 22] for more recent developments on fractional volatility modelling.

This paper is structured as follows: in Section 2, we introduce the model and study its main properties. We in particular show that the characteristic function of the stock price is available in closed form. In Section 3, we derive the main, probabilistic and financial, results of the paper, namely large deviations principles for rescaled versions of the log stock price process and the asymptotic behaviour of the implied volatility, both for short and for large maturities. In Section 4 we provide several numerical examples. Section 5 contains the proofs of the main results, and we add a short reminder on large deviations in the appendix.

2. The Model and its properties

2.1. The fractional Heston model

Let be a given filtered probability space supporting two independent standard Brownian motions and . We denote by the stock price process, and let be the unique strong solution to the stochastic differential equation

| (2.1) |

where and the coefficients satisfy . The operator is the classical left fractional Riemann-Liouville integral of order :

valid for any function , where is the standard Gamma function. For more details on these integrals, we refer the interested reader to the monograph [49, Chapter 1, Section 2], and for the application to discretisation schemes, we refer to [12, Section 5]. The couple corresponds to the standard Heston stochastic volatility model [31], which admits a unique strong solution by the Yamada-Watanabe conditions [37, Proposition 2.13, page 291]). The additional parameter , as explained in [12] allows to loosen the tight connection between the mean and the variance of . The process can be written, in integral form, as , and therefore Itô isometry implies that the covariance structure reads, for any ,

The Feller condition [38, Chapter 15], , ensures that the origin is unattainable (otherwise it is regular, hence attainable, and strongly reflecting); under this condition, since the Riemann-Liouville operator preserves positivity, almost surely for all . Now, for any , we have , and, for any

The motivation for such a fractional volatility model comes from the seminal work by Comte and Renault [11] on the Ornstein-Uhlenbeck process. Consider the unique strong solution to the stochastic differential equation starting at zero, with , and a fractional Brownian motion; its fractional derivatives defined via the identity , for all , or

satisfies the SDE , with , where is a standard Brownian motion. Conversely, if satisfies the Ornstein-Uhlenbeck SDE , with , then

Finally, note that the fair strike of a continuously monitored variance swap with maturity reads

| (2.2) |

Note in particular that, when , this representation coincides with the expected variance formula in the standard Heston case, provided in [25, Chapter 11]. Furthermore, for small , Equation (2.1) reads

so that in the rough Heston case the variance swap rate explodes when with a rate of .

2.2. Cumulant generating function

Let , for any and , denote the cumulant generating function of the couple , where is the effective domain of . The following theorem provides a closed-form expression for it:

Theorem 2.1.

For any ,

| (2.3) |

where the functions and satisfy the ordinary differential equations

| (2.4) |

for , with the initial conditions , and where is the usual Gamma function.

It is interesting to note that the couple remains affine in the sense of [15]. As outlined in Remark 2.2, correlation would break the Markovian property of the process, as well as its affine property. When , the Riccati equations (2.4) are the same as in the standard (uncorrelated) Heston model. This in particular implies that, when correlation is null, our model (2.1) and the Heston model have the same marginals. The analysis of the asymptotic behaviour of the implied volatility below will only require the knowledge of the function evaluated at , and we shall write with effective domain .

Proof.

The map is non-negative on a.s., so that, by Tonelli’s theorem,

Since moments of the integrated CIR exist, up to explosion [36, Part I, Chapter 6.3], the Novikov condition then justifies the introduction, for any , of the measure via the Radon-Nikodym derivative

| (2.5) |

The moment generating function can then be written as

Furthermore, under , the process satisfies

| (2.6) |

Set now . We want and solves the following PDE using the Feynman-Kac formula:

for , with terminal condition for . The change of variables yields

for and with initial condition for all . Using the ansatz we find that solve the Ricatti ODEs in (2.4). ∎

Remark 2.2.

For non-zero correlation, the variance dynamics under in (2.6) change to

which is non-Markovian, hence not amenable to Feynman-Kac techniques, and is left for future research.

Remark 2.3.

3. Large deviations and implied volatility asymptotics

3.1. Large deviations of the log stock price process

This section gathers the main results of the paper, namely a large deviations principle for a rescaled version of the log stock price process defined in (2.1) when time becomes large or small. We refer the reader to Appendix A for a brief reminder of large deviations and to [13, 14] for thorough treatments. Before stating (and proving) the main results of the paper, introduce the functions , and :

| (3.1) |

where the real numbers are defined in Theorem 3.3 and

with The expressions and are shorthand notations for, respectively and . Straightforward computations show that the function is smooth on , decreasing and concave on and increasing and concave on , with and

Therefore, is strictly convex and smooth and maps to . Straightforward computations also yield that the function is smooth on the real line. Note that and are nothing else than the Fenchel-Legendre transforms of and . Likewise, the functions and are clearly strictly convex on the whole real line.

Theorem 3.1.

-

(i)

As tends to zero,

-

(a)

if , then satisfies a LDP with good rate function and speed ;

-

(b)

if , then satisfies a LDP with good rate function and speed ;

-

(a)

-

(ii)

As tends to infinity,

-

(a)

if , then satisfies a LDP with good rate function and speed ;

-

(b)

if , then satisfies a partial LDP on with rate function and speed , where are defined in Proposition 3.3.

-

(a)

In practice, the partial LDP in case (ii)(b)is enough here since strikes are of the form , for large maturity and fixed ; furthermore , so that for fixed small , and large enough, even large strikes can be computed, see Theorem 3.6 (ii)(b) for details. For the effective domain of defined in Section 2.2, let , and the effective domain of the pointwise limit as tends to zero (). The proof of Theorem 3.1 relies on the study of the limiting behaviour of the cumulant generating function of (a rescaled version of) the process , which we state in the following two propositions (and defer their proofs to Sections 5.1 and 5.2):

Proposition 3.2.

The following hold as tends to zero:

-

(i)

if , let , then and , for ;

-

(ii)

if , let , then and , for .

Proposition 3.3.

As tends to infinity, we have the following behaviours for the cumulant generating function:

-

(i)

if , then and , for ;

-

(ii)

if , then there exist , such that , for .

Remark 3.4.

The limits above are not continuous in at the origin. In the case (standard Heston), the pointwise limit of the rescaled cumulant generating function was computed in [21] and is such that is a smooth convex function on some interval . In Proposition 3.3, the characterisation of the limiting domain is not fully explicit. However, using comparison principles between the ODEs (2.4) and the corresponding ones in the standard (uncorrelated) Heston model, it is easy to see that the interval is contained in , which is the limiting domain of the rescaled moment generating function in the uncorrelated Heston model (see [21] for details and explicit expressions for ).

Proof of Theorem 3.1.

From Proposition 3.2, the large deviations principle stated in (i)(a)-(b) follows from a direct application of the Gärtner-Ellis theorem (Theorem A.3). Consider now the large-time behaviour, and start with Case (ii)(a), i.e. . From Proposition 3.3, the function is essentially smooth on , but the origin is not in the interior of , and hence the Gärtner-Ellis theorem does not apply directly. However, in the one-dimensional case, one can use the refined version in [45], which relaxes this assumption. Case (ii)(b) is a direct application of the Gärtner-Ellis theorem on the effective domain . ∎

Remark 3.5.

One could prove the lower bound on the whole real line even when the steepness condition is not satisfied, by introducing a well chosen time-dependent change of measure, as in [8] or [34]; however, this requires knowledge of higher orders of the asymptotic behaviour of the cumulant generating function. We leave this for future research.

3.2. Implied volatility asymptotics

We now translate the large deviations principles derived above into asymptotics of the implied volatility. For any , let denote the implied volatility corresponding to European option prices with maturity and strike . The following theorem is proved in Section 5.3 (small time) and in Section 5.4 (large time).

Theorem 3.6.

-

(i)

As tends to zero,

-

(i)

If , then for any , converges to ;

-

(ii)

if , then for any , converges to ;

-

(i)

-

(ii)

as tends to infinity, the implied volatility behaves as follows:

-

(a)

if , then , for all ;

-

(b)

if , then and , for all ;

-

(a)

For large maturities, as approaches zero from above, we recover the standard Heston implied volatility asymptotics derived in [21]; in the long memory case (), the steepness of the implied volatility is more pronounced for very large maturity due to the factor than the standard Heston model. The small-maturity case is especially interesting. In the case of long memory (), the implied volatility converges to a constant at the same speed as Black-Scholes (or for that matter as any diffusion with continuous paths). In the short-memory regime, the implied volatility blows up at the speed . It is well documented [4] that classical stochastic volatility models (driven by standard Brownian motions) are not able to capture the observed steepness of the observed implied volatility smile. Several authors [43, 51] have suggested the addition of jumps in order to fit this steepness. Assume that the martingale stock price is given by , where is a Lévy process with Lévy measure supported on the whole real line. As the maturity tends to zero, the corresponding implied volatility behaves as , for all . The speed of divergence is then to be compared with the () in the fractional framework above: clearly, for small enough , the Lévy implied volatility blows up much faster. Note further that, in the limit as maturity tends to zero, the latter does depend on the strike, but the fractional implied volatility does not. Our results therefore show that fractional Brownian motion (driving the instantaneous volatility) are an alternative to jumps, and provide smiles steeper than standard stochastic volatility, but less steep than Lévy models. They further have the advantage of bypassing the hedging issues in jump-based models. One should also compare this explosion rate to that of the implied volatility in the standard Heston model, where the instantaneous variance is started from an initial distribution. In [34], the authors chose a non-central chi-squared initial distribution and showed that, under some appropriate rescaling, the implied volatility blows up at speed . Jacquier and Shi [35], also inspired by [42], pushed this analysis further by studying the impact of the random initial data on the short-time explosion of the smile.

4. Numerics

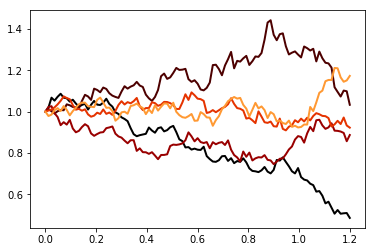

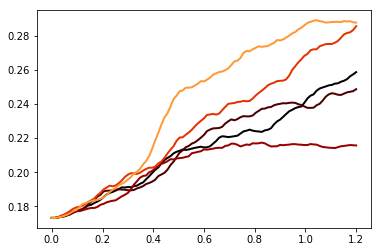

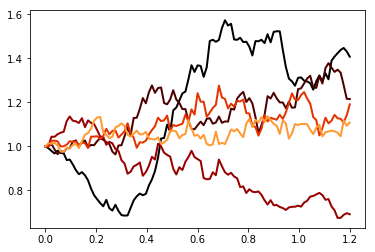

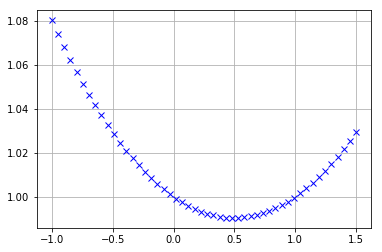

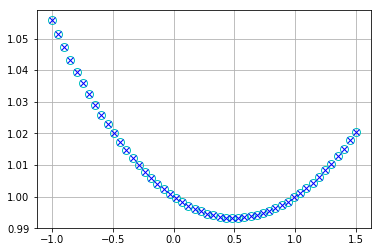

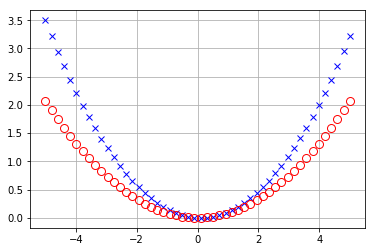

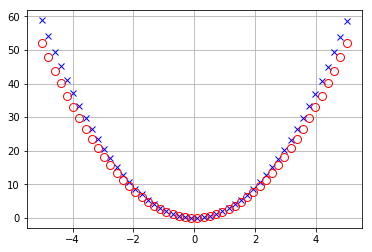

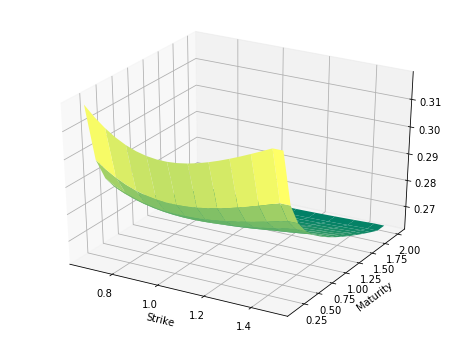

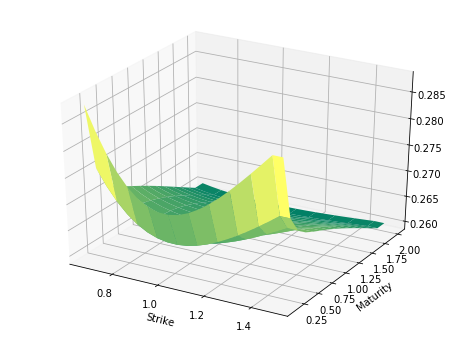

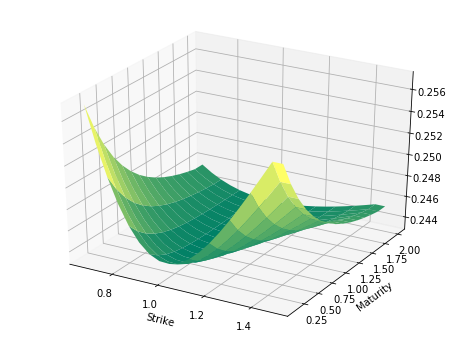

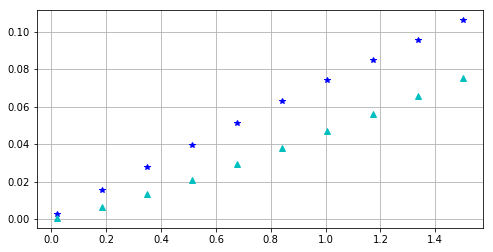

In this section we provide numerical examples describing the behaviour of our model, with parameters . In Figure 4 we provide a comparison of volatility surfaces generated by fractional and standard Heston models. We observe that in the case where the Hurst parameter is less than (), a larger value of pushes up the small-time volatility smile, resonating our small-time analysis in Theorem 3.6. Also notice that with similar parameter choices the at-the-money implied volatilities are higher in the fractional case. This is further confirmed by Figure 5 representing the term structure of the at-the-money total variance.

5. Proofs

5.1. Proof of Proposition 3.2

We separate the and in the proof.

5.1.1. The case

One could use the explicit knowledge of the moment generating function in Remark 2.3 to compute its limiting behaviour. However, we follow a different route here, which we can adapt later to the case. The function is the solution of the ODE

| (5.1) |

with boundary condition . Let , and consider the ansatz , for some sequence of real numbers . Therefore

This polynomial (in ) is null everywhere if and only if and , for . We now make the above derivation rigorous. Consider the map defined by , for . For large enough, , and hence , where the sequence is defined by and , for . Tedious but straightforward computations show that the power series has a radius of convergence , and for all . Therefore, the power series has a radius of convergence greater than and for all . For small enough,

so that . Moreover, using Tonelli’s theorem, for small enough,

is finite. A direct application of Fubini’s theorem then yields , and hence is the solution of 5.1 for small .

We first prove the proposition in the case . The function , solution to (5.1), satisfies:

Moreover, for small enough,

Since for small enough, , then is well defined. Hence the left-hand side converges to zero as tends to zero, and so does to .

In the case , the function , solution to (5.1), satisfies

Moreover, for small enough, . Since the series is well defined for small enough, tends to zero as tends to zero, and so does tends to , which proves the proposition.

5.1.2. The case

Similarly to the case, plugging the ansatz into (2.4) yields

The following statements hold, and are related to the case above:

-

(1)

for any and for ;

-

(2)

for any .

Combining terms of the same order yields . Moreover, for any ,

Then the two statements above can be easily verified by induction, from which , with

| (5.2) |

We show that the series is absolutely convergent. Notice that

| (5.3) |

Following Lemma 5.1, holds for any , and (5.3) then reads

| (5.4) |

We already show that for large enough, then the series has a radius of convergence no less than . Since is strictly positive, then (5.4) implies that the series is absolutely convergent for small such that holds. Therefore the previous ansatz is the solution to the Riccati equation for small . The rest of the proof is essentially the same as the case where , and we therefore omit the details.

Lemma 5.1.

For any , the following estimation for defined in (5.2) holds for any :

Proof.

We prove by induction. In the case where , direct computations yield

Assume that the upper bound holds for for any . Then we have

As a result, for any fixed ,

Plug it into (5.2), and notice that which follows from the fact that all the terms have the same sign for any , then

Iterating the inequality above, we finally obtain

∎

Remark 5.2.

In the case and , the cgf corresponds to the standard Heston model with and mean reversion speed . Here it is well known [20] that . Using the series expansion solution to (5.1) above we find that . Explicitly computing the first few terms we find that , which is in exact agreement with a Taylor expansion of for small .

5.2. Proof of Proposition 3.3

We start with the case . Let be the solution to the ordinary differential equation (2.4), and , , . The function satisfies , for . Define now by

| (5.5) |

We now claim that for any , the following inequalities hold:

| (5.6) |

Note that

| (5.7) |

which implies that , for all , and

Furthermore, note that

| (5.8) |

If is finite, then from monotonicity and continuity of on we have and . As a result, , implying that there exists such that for , hence for , contradicting the finiteness of , and therefore . We now prove that . Define the functions by

where is large enough so that exists as a real number () for . For large , we have

| (5.9) |

For large , and . Since , two cases can occur:

-

•

there exists such that ;

-

•

for all , ;

In the first case, the comparison principle implies that for all , (similarly to the proof of (5.6)). Therefore (5.6) and the definition of yield , which proves the result. In the second case, let us prove first that there exists such that : if for all such that is well defined we have , then

which implies , which contradicts the positivity of (see (5.6) and (5.8)). Thus there exists such that . Therefore, since, for all ,

the comparison principle implies that for all . Therefore is non-decreasing on ; being bounded by , which tends to zero at infinity, it converges to a constant, and .

We now prove that the effective domain converges to as tends to infinity. For any ,

Therefore, , so that

, and hence

.

Since ,

and since is always in , for any (since the process is a martingale),

Part (i) of the proposition follows from Theorem 2.1.

We now move on to part (ii) of the proposition, when . Let us first prove that . Consider the functions as defined in (5.5). As tends to zero, diverges to and to , so that , and hence, from (5.8), is positive in the neighbourhood of the origin. Moreover, for all , Equation (5.7) implies that . Let . If is finite, then because and is positive and increasing in . Therefore, and for all by comparison principle, and hence is decreasing on . Since it is bounded below by , it converges at infinity to some constant . From the Riccati equation (2.4), then converges to , and necessarily . If is infinite, then is increasing and bounded from above by , which tends to at infinity; this yields a contradiction since is increasing, so that . Finally, since is a martingale and the moment generating function is convex, for all and hence .

5.3. Proof of Theorem 3.6(i)

In this section and the next, the process shall denote the unique strong solution starting from the origin to the Black-Scholes stochastic differential equation , for some given , for . In this model, the price of a European Call option with maturity and strike () is given by

where denotes the Gaussian cumulative distribution function. Straightforward computations yield , for all . In [21], the authors proved that the process satisfies a large deviations principle with speed and good rate function , which implies that the following limits hold:

When , from Theorem 3.1(i), we can mimic this proof to obtain

where are defined in (3.1), so that, for any real number , converges to as tends to zero. Likewise, in the case , from Theorem 3.1(i) we obtain

Consider the ansatz , for some ; the Black-Scholes call price then reads

Since as tends to minus infinity, we obtain, after simplifications,

Therefore, taking , we obtain , for all . Similarly, , for all .

5.4. Proof of Theorem 3.6(ii)

Consider a Call option in the Black-Scholes model, with log strike and time-dependent implied volatility . Then

where we used the identity in the second line. Since for large , we obtain

and therefore .

Let us now return to the proof of the theorem, following the lines of [33, Theorem 13]. Let be a function diverging to infinity at infinity such that that the pointwise limit exists for all . Since the stock price is a true positive martingale, we can define a new probability measure via . Under , the limiting cumulant generating function of reads , and clearly for all . Note that if and only if . This identity also shows that the Fenchel-Legendre transforms are related via , for all . Now, if the family satisfies a large deviations principle under both and with speed and good rate functions and , then the following behaviours hold:

| (5.20) |

where and are where the functions and attain their minimum, and satisfy . Furthermore the convergence in (i)-(iii) is uniform in on compact subsets of .

Appendix A The Gärtner Ellis Theorem

We provide here a brief review of large deviations and the Gärtner-Ellis theorem. For a detailed account of these, the interested reader should consult [13]. Let be a sequence of random variables in , with law and cumulant generating function . For a Borel subset of the real line, we shall denote respectively by and its interior and closure (in ).

Definition A.1.

The sequence is said to satisfy a large deviations principle with speed and rate function if for each Borel mesurable set in ,

Furthermore, the rate function is said to be good if it is strictly convex on the whole real line.

Before stating the main theorem, we need one more concept:

Definition A.2.

Let be a convex function, and its effective domain. The function is said to be essentially smooth if

-

•

The interior is non-empty;

-

•

is differentiable throughout ;

-

•

is steep: for any sequence in converging to a boundary point of .

Assume now that the limiting cumulant generating function exists as an extended real number for all , and let denote its effective domain. Let denote its (dual) Fenchel-Legendre transform, via the variational formula . Then the following holds:

Theorem A.3 (Gärtner-Ellis theorem).

If , is lower semicontinuous and essentially smooth, then the sequence satisfies a large deviations principle with rate function .

When partial conditions of the Gärtner-Ellis theorem are satisfied, a full large deviations principle might not be available, but one can define a partial one, as follows:

Definition A.4.

We shall say that the sequence satisfies a partial large deviations principle with speed on some interval with rate function if Definition A.1 holds for all subsets .

It is clear that if and is lower semicontinuous and strictly convex on some interval , then satisfies a partial large deviations principle on with rate function .

References

- [1] E. Alòs, J. Gatheral and R. Radoičić. Exponentiation of conditional expectations under stochastic volatility. ssrn:2983180, 2017.

- [2] E. Alòs, J. León and J. Vives. On the short-time behavior of the implied volatility for jump-diffusion models with stochastic volatility. Finance and Stochastics, 11(4), 571-589, 2007.

- [3] R.T. Baillie, T. Bollerslev and H.O.Mikkelsen. Fractionally integrated generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 74: 3-30, 1996.

- [4] G. Bakshi, C. Cao and Z. Chen. Empirical performance of alternative option pricing models. The Journal of Finance, 52 (5): 2003-2049, 1997.

- [5] D.S. Bates. Jumps and stochastic volatility: exchange rate processes implicit in Deutsche Mark options. Review of Financial Studies, 9:69-107, 1996.

- [6] C. Bayer, P. K. Friz and J. Gatheral. Pricing Under Rough Volatility. Quantitative Finance, 16(6): 887-904, 2016.

- [7] C. Bayer, P. K. Friz, A. Gulisashvili, B. Horvath and B. Stemper. Short-time near-the-money skew in rough fractional volatility models. arXiv:1703.05132, 2017.

- [8] B. Bercu and A. Rouault Sharp large deviations for the Ornstein-Uhlenbeck process. SIAM Theory of Probability and its Applications, 46: 1-19, 2002.

- [9] T. Bjork and H. Hult. A note on Wick products and the fractional Black-Scholes model. Fin. Stoch., 9: 197-209, 2005.

- [10] P. Cheridito. Arbitrage in fractional Brownian motion models. Finance and Stochastics, 7: 533-553, 2003.

- [11] F. Comte and E. Renault. Long memory in continuous-time stochastic volatility models. Math Finance, 8(4): 291-323, 1998.

- [12] F. Comte, L. Coutin and E. Renault. Affine fractional stochastic volatility models. Annals of Finance, 8: 337-378, 2012.

- [13] A. Dembo and O. Zeitouni. Large deviations techniques and applications. Jones and Bartlet publishers, Boston, 1993.

- [14] J.D. Deuschel and D. Stroock. Large Deviations. American Mathematical Society, Volume 342, 2001.

- [15] D. Duffie, D. Filipović and W. Schachermayer. Affine processes and applications in finance. Annals of Applied Probability, 13(3): 984-1053, 2003.

- [16] O. El Euch and M. Rosenbaum. Perfect hedging in rough Heston models. arXiv:1703.05049, 2017.

- [17] O. El Euch and M. Rosenbaum. The characteristic function of rough Heston models. arXiv:1609.02108, 2016.

- [18] O. El Euch, M. Fukasawa and M. Rosenbaum. The microstructural foundations of leverage effect and rough volatility. arXiv:1609.05177, 2016.

- [19] R. Elliott and J. van der Hoek. A general fractional white noise theory and applications to finance. Mathematical Finance, 13: 301-330, 2003.

- [20] M. Forde and A. Jacquier. Small-time asymptotics for implied volatility under the Heston model. IJTAF, 12(6): 861-876, 2009.

- [21] M. Forde and A. Jacquier. The large-maturity smile for the Heston model. Finance and Stochastics, 15(4): 755-780, 2011.

- [22] M. Forde and H. Zhang. Asymptotics for rough stochastic volatility models. SIAM Journal Fin. Math., 8: 114-145, 2017.

- [23] J.P. Fouque, G. Papanicolaou, R. Sircar and K. Solna. Multiscale Stochastic Volatility for Equity, Interest Rate, and Credit Derivatives. CUP, 2011.

- [24] M. Fukasawa. Asymptotic analysis for stochastic volatility: martingale expansion. Finance and Stochastics, 15: 635-654, 2011.

- [25] J. Gatheral. The Volatility Surface: a practitioner’s guide. Wiley, 2006.

- [26] J. Gatheral, T. Jaisson and M. Rosenbaum. Volatility is rough. Preprint, arXiv:1410.3394, 2014.

- [27] C.W.J. Granger and R. Joyeux. An introduction to long memory time series models and fractional differencing. Journal of Time Series Analysis, 1: 15-39, 1980.

- [28] P. Guasoni. No arbitrage under transaction costs, with fractional Brownian motion and beyond. Math. Fin., 16: 569-582, 2006.

- [29] A. Gulisashvili. Analytically tractable stochastic stock price models. Springer Finance, 2012.

- [30] P. Henry-Labordère. Analysis, Geometry, and Modeling in Finance: Advanced Methods in Option Pricing. CRC, 2008.

- [31] S. Heston. A closed-form solution for options with stochastic volatility with applications to bond and currency options. The Review of Financial Studies, 6: 327-342, 1993.

- [32] Y. Hu and B. Oksendal. Fractional white noise calculus and applications to finance. Infinite Dimensional Analysis, Quantum Probability and Related topics, 6: 1-32, 2003.

- [33] A. Jacquier, M. Keller-Ressel and A. Mijatović. Large deviations and stochastic volatility with jumps: asymptotic implied volatility for affine models. Stochastics, 85(2): 321-345, 2013.

- [34] A. Jacquier and P. Roome. The small-maturity Heston forward smile. SIAM Journal Fin. Math., 4(1): 831-856, 2013.

- [35] A. Jacquier and F. Shi. The randomised Heston model. arXiv:1608.07158, 2017.

- [36] M. Jeanblanc, M. Yor and M. Chesney. Mathematical Methods for Financial Markets. Springer, 2009.

- [37] I. Karatzas and S.E. Shreve. Brownian Motion and Stochastic Calculus. Springer-Verlag, 1997.

- [38] S. Karlin and H. Taylor. A Second Course in Stochastic Processes. Academic Press, 1981.

- [39] M. Keller-Ressel. Moment Explosions and Long-Term Behavior of Affine Stochastic Volatility Models. Mathematical Finance, 21(1), 73-98, 2011.

- [40] A. Lewis. Option valuation under stochastic volatility. Finance Press, 2000.

- [41] V. Maric. Regular variation and differential equations. Lecture Notes in Mathematics 1726, Berlin, Springer-Verlag, 2010.

- [42] S. Mechkov. ’Hot-start’ initialization of the Heston model. Risk, November 2016.

- [43] A. Mijatović and P. Tankov A new look at short-term implied volatility in asset price models with jumps. Mathematical Finance, 26(1): 149-183, 2016.

- [44] Y. Mishura. Stochastic Calculus for Fractional Brownian Motion and Related Processes. Springer, 2008.

- [45] G.L. O’Brien and J. Sun. Large deviations on linear spaces. Probability and Mathematics and Statistics, 16(2): 261-273, 1996.

- [46] A. D. Polyanin and V. F. Zaitsev. Handbook of Exact Solutions for Ordinary Differential Equations, Second Edition, Chapman and Hall/CRC, Boca Raton, 2003.

- [47] R. Rebonato. Volatility and Correlation: The Perfect Hedger and the Fox. John Wiley & Sons; Second Edition, 2004.

- [48] L.C.G. Rogers. Arbitrage with fractional Brownian motion. Mathematical Finance, 7: 95-105, 1997.

- [49] S.G. Samko, A.A. Kilbas and O.I. Marichev. Fractional Integrals and Derivatives. Theory and Applications. Gordon and Breach Science Publishers, 1993.

- [50] A. Shiryaev. On arbitrage and replication for fractal models. Research report 20, MaPhySto, Department of Mathematical Sciences, University of Aarhus, Denmark, 1998.

- [51] P. Tankov. Pricing and hedging in exponential Lévy models: review of recent results. Paris-Princeton Lecture Notes in Mathematical Finance, Springer, 2010.

- [52] R. Vilela Mendes, M.J. Oliveira and A.M. Rodrigues. The fractional volatility model: no-arbitrage, leverage and completeness. Physica A: Statistical Mechanics and its Applications, 419(1): 470-478, 2015.