Continuous-Time Perpetuities and Time Reversal of Diffusions

Abstract.

We consider the problem of estimating the joint distribution of a continuous-time perpetuity and the underlying factors which govern the cash flow rate, in an ergodic Markovian model. Two approaches are used to obtain the distribution. The first identifies a partial differential equation for the conditional cumulative distribution function of the perpetuity given the initial factor value, which under certain conditions ensures the existence of a density for the perpetuity. The second (and more general) approach, using techniques of time reversal, identifies the joint law as the stationary distribution of an ergodic multi-dimensional diffusion. This later approach allows for efficient use of Monte-Carlo simulation, as the distribution is obtained by sampling a single path of the reversed process.

Key words and phrases:

Introduction

Discussion

In this article, we consider a continuous-time perpetuity given by the random variable

| (0.1) |

Above, represents the value of an economic factor that determines a cash flow rate . Cash flows are discounted according to ; therefore, represents the whole payment in units of account at time zero. Our main concern is the identification of an efficient means to obtain the joint distribution of , as naive estimation of the distribution by simulating sample paths of and approximating through numerical integration may be prohibitively slow. As is typically observable, the joint distribution of also allows us to obtain the conditional distribution of given .

In order to make the problem tractable, we work in a diffusive, Markovian environment where and are solutions to the respective stochastic differential equations (written in integrated form)111Throughout the text, the prime symbol (′) denotes transposition.

| (0.2) |

| (0.3) |

In the above equations, and are independent Brownian motions of dimension and respectively, while , , , and are given functions. (Precise assumptions on all the model coefficients are given in Section 1.) We assume is stationary and ergodic with invariant density . Equation (0.3) includes in particular the case when is smooth; in other words , where represents a short-rate function. However, the more general form of (0.3) is considered to accommodate a broader range of situations. For example:

-

•

when payment streams are sometimes denominated in units of different account (for example, another currency, or financial assets), in which case discounting has to take into account the “exchange rate”.

-

•

when, for pricing purposes, the payment stream, though denominated in domestic currency, must incorporate both traditional discounting and the density of the pricing kernel.

The two main results of the paper—Theorem 2.1 and Theorem 2.4—identify the distribution of in different ways. First, in the case where in (0.3) is non-degenerate and in (0.1) is sufficiently regular, the conditional cumulative distribution function of given is shown to coincide with the explosion probability of an associated locally elliptic diffusion and, hence, through the Feynman-Kac formula satisfies a partial differential equation (PDE): see Theorem 2.1. Second, for general and , using methods of diffusion time-reversal, we identify an “ergodic” process whose invariant distribution coincides with the joint distribution of . In particular, for any fixed starting point of , the (random) empirical time-average law of on almost surely converges to the joint distribution of in the weak topology: see Theorem 2.4. The time-reversal result has the advantage of leading to an efficient method for obtaining the distribution via simulation, as the ergodic theorem enables estimation of the entire distribution based upon a single realization of ; a numerical example in Section 3 dramatically reinforces this point. However, it must be noted that the invariant distribution for appears in the reversed dynamics, and hence must be known to perform simulation. When is one-dimensional, or more generally, reversing, is given in explicit form with respect to the model parameters. In the general multi-dimensional setup, lack of knowledge of could pose an issue; however, we provide a potential way to amend the situation in the discussion after Theorem 2.4. Note also that in the PDE result in Theorem 2.1, explicit knowledge of is not necessary.

Existing literature and connections

Obtaining the distribution of the perpetuity is of great importance in the areas of finance and actuarial science; for this reason, perpetuities with a form similar to have been extensively studied. For example, [12] deals with the case where

establishing that has an inverse gamma distribution. This fits into the set-up of (0.2), (0.3) by taking , , and . Note that here plays no role. In a similar manner, [32, 10, 11] consider the case

and obtain the first moment, along with bounds for other moments, of . In [17], the perpetuity takes the form

| (0.4) |

Under certain conditions on and , the distribution of is implicitly calculated by identifying the characteristic function and/or Laplace transform for . In fact, the results of [17] are pre-dated (for highly particular and ), in [25, 22]. The Laplace transform method is also used in [27, 26] to treat (0.4) when and is a diffusion. In addition to identifying a degenerate elliptic partial differential equation for the Laplace transform, they propose a candidate recurrent Markov chain whose invariant distribution has the law of . Lastly, the setup of [17] is significantly extended in [7] where, under minimal assumptions on and , the distribution of is shown to coincide with the unique invariant measure for a certain generalized Ornstein-Uhlenbeck process, a relationship that is confirmed in our current setting in Proposition 8.2.

The use of time-reversal to identify the distribution of a discrete-time perpetuity is well known, dating at least back to [13], where takes the form

where the discount factors and cash flows are two independent sequences of independent, identically distributed (iid) random variables. To provide insight, the time-reversal argument in [13] is briefly presented here. With it is clear by the iid property that has the same distribution as . Straightforward calculations show that the reversed process satisfies the recursive equation . Thus, assuming that converges to a random variable in distribution, must solve the distributional equation , where , and are independent, has the same law as and has the same law as . In [31] solutions to the aforementioned distributional equation are obtained based upon the expectation of and . The tails of , as well as convergence of iterative schemes, are studied in [15]; furthermore, [18] gives “almost” if and only if conditions for the convergence of iterative schemes.

In a continuous time setting, we employ an argument similar in spirit, but rather different in execution, to [13]. Specifically, we extend to a whole “forward” process and then, for each define the reversed process on ] by , : see (2.7), (2.8). Using results on time reversal of diffusions from [20] (alternatively, see [24, 3, 8, 14]), as well as additional elementary calculations, we obtain the dynamics for . In fact, Proposition 7.5 shows the generator of does not depend upon and ergodicity can be studied for the process with the given generator. When in and is sufficiently regular, this generator is locally elliptic and the associated process is ergodic with invariant distribution equalling that of : see Proposition 8.2. In the general case a slightly weaker (but still sufficient) form of ergodicity still holds: starting off its invariant distribution and off any starting point , the (random) empirical time-average laws of converge almost surely in the weak topology to the distribution of .

Structure

This paper is organized as follows: in Section 1 we precisely state the given assumptions on the processes and , as well as the function , paying particular attention to deriving sharp conditions under which is almost surely finite or infinite. The main results are then presented in Section 2. First, when in and is sufficiently regular, the conditional cumulative distribution function of given is shown to satisfy a certain partial differential equation. Then, using the method of time reversal, we construct a probability space and diffusion such that with probability one its empirical time-average laws weakly converge to the joint distribution of for all starting points of . Section 2 concludes with a brief discussion how the distribution may be estimated via simulation, in particular proposing a method for obtaining the desired distribution when the invariant density for is not explicitly known. Section 3 provides a numerical example in a specific case where the joint distribution of is explicitly identifiable. Here, we compare the performance of the reversal method versus the direct method for obtaining the distribution of . In particular we show that for a given desired level of accuracy (see Section 3 for a more precise definition), the method of time reversal is approximately to times faster than the direct method. The remaining sections contain the proofs: Section 5 proves the statements regarding the finiteness of ; Section 6 proves the partial differential equation result; Section 7 obtains the dynamics for the time-reversed process ; Section 8 proves the (weak) ergodicity with the correct invariant distribution. Finally, a number of technical supporting results are included in the appendix.

1. Problem Setup

1.1. Well-posedness and ergodicity

The first order of business is to specify precise coefficient assumptions so that in (0.2) and in (0.3), are well-defined. As for , we work in the standard locally elliptic set-up for diffusions: for more information, see [28]. Let be an open, connected region. We assume the existence of such that:

-

(A1)

there exists a sequence of regions such that , each being open, connected, bounded, with being and satisfying for all .

-

(A2)

and , where is the space of symmetric and strictly positive definite -dimensional matrices.

With the provisos in (A1) and (A2), define as the generator associated to :

| (1.1) |

Under (A1) and (A2), one can infer the existence of a solution to the martingale problem for on , with the possibility of explosion to the boundary of : see [28] We wish for something stronger; namely, to construct a filtered probability space on which there is a strong, stationary, ergodic solution to the SDE in (0.2) with invariant density . In (0.2), is a -dimensional Brownian Motion and , the unique positive definite symmetric matrix such that . In order to achieve this, we ask that

-

(A3)

The martingale problem for on is well posed and the corresponding solution is recurrent. Furthermore, there exists a strictly positive with satisfying , where is the formal adjoint of given by

(1.2)

We summarize the situation in the following result: the extra Brownian motion in its statement will be used to define the process via (0.3) later on.

Theorem 1.1.

Under assumptions (A1), (A2) and (A3), there exists a filtered probability space satisfying the usual conditions supporting two independent Brownian motions and , -dimensional and -dimensional respectively, such that satisfies (0.2) and is stationary and ergodic with invariant density .

Remark 1.2.

According to [28, Corollary 5.1.11], in the one-dimensional case, where for , the above assumption (A3) is true if and only if for some

In this case, it holds that

where is a normalizing constant.

In the multi-dimensional case, suppose that there exists a function with the property that , where is the (matrix) divergence defined by333This definition is equivalent to the standard definition of divergence for matrices, where the divergence operator is applied to the columns, by the symmetry of . Also, to differentiate the matrix divergence from its vector counterpart, we will write for symmetric matrices and for vector valued functions . . Then, is a reversing Markov process. Furthermore Assumption (A3) follows if it can be shown that does not explode to the boundary of and . Indeed, by construction satisfies , . Thus, if does not explode, it follows from [28, Theorem 2.8.1, Corollary 4.9.4] that is recurrent. In fact, is ergodic, as shown in [28, Theorems 4.3.3, 4.9.5]. Absent the reversing case, there are many known techniques for checking ergodicity—see [6, 28]. For example, if there exist a smooth function , an integer and constants and such that and on , then (A3) holds.

1.2. Finiteness of

Having the set-up for the existence of and , we proceed to . For the time being, we shall just assume that the function is in 444We define to be those Borel measurable functions on so that . Thus, Borel measurability is implicitly assumed throughout.. For the PDE results of Theorem 2.1 below we require a slightly stronger regularity assumption on , though the time-reversal results of Theorem 2.4 make no additional assumptions. Now, for not necessarily in , it is entirely possible that takes infinite values with positive probability. In this section, conditions are given under which or, conversely, when .

Lemma 1.3.

Let (A1), (A2), (A3) and (A4) hold. For the invariant density of , assume there exists such that

| (1.4) |

Then, the following hold:

-

i)

There exists such that for all , . In particular, a.s..

-

ii)

For any , it holds that .

Remark 1.4.

As a partial converse to Lemma 1.3 we have

Lemma 1.5.

Let (A1), (A2), (A3) and (A4) hold. For the invariant density of , assume there exists such that

| (1.6) |

(If , then assume that and .) If is such that , then .

Remark 1.6.

In view of Lemma 1.3, we ask that

-

(A5)

, , and there exists such that

(1.7)

To recapitulate, for the remainder of the article the following is assumed:

Assumption 1.7.

We enforce throughout all above assumptions (A1), (A2), (A3), (A4) and (A5).

2. Main Results

2.1. The distribution of via a partial differential equation

Define the cumulative distribution function of given by

| (2.1) |

Next, recall that Assumption 1.7 implies that has a density , and define the joint distribution of by

| (2.2) |

Under Assumption 1.7, as well as an additional smoothness requirement on and non-degeneracy requirement on , the first main result (Theorem 2.1 below) shows solves a certain PDE on the state space . This will imply that the joint distribution of has a density (still labeled ) and the law of charges all of .

To motivate the result, as well as to fix notation, for each , consider the process

| (2.3) |

Since Assumption 1.7 implies for all , it is clear that given , on the process tends to . Alternatively, on , will hit at some finite time. What happens on is not immediately clear but it will be shown under the given assumptions there is no probability of this occurring. For fixed , it follows that equals the probability that hits zero, given . According the Feynman-Kac formula, such probabilities “should” solve a PDE. To identify the PDE, note that the joint equations governing and are

Define and by

| (2.4) |

for all . Note that if, in addition to Assumptions 1.7, then is locally elliptic. Let be the second order differential operator associated to , i.e.,

| (2.5) |

Note that for functions of alone. With the previous notation, the first main result now follows.

Theorem 2.1.

Let Assumptions 1.7 hold, and suppose further that a) and b) for all . Then, satisfies with the following “locally uniform” boundary conditions

| (2.6) |

Furthermore, is unique within the class of solutions to taking values in with the above boundary conditions.

Remark 2.2.

The non-degeneracy assumption on is essential for the existence of a density; if it may be that the distribution of has an atom. Indeed, take , , , . Then, with probability one.

Remark 2.3.

Theorem 2.1 implies the law of charges all of , even for those functions which are bounded from above. Theorem 2.1 also implies that has a density without imposing Hormander’s condition [23, Chapter 2] on the coefficients in (2.4). Rather, the infinite horizon combined with the presence of the independent Brownian motion “smooth out” the distribution of .

Theorem 2.1 is certainly important from a theoretical viewpoint. However, it appears to be of limited practical use. Even under the force of the extra non-degeneracy condition , it is unclear how to numerically solve the PDE with the given boundary conditions (2.6), as there are no natural auxiliary boundary conditions in the spatial domain of . In Subsection 2.2 that follows we provide an alternative, more useful method for estimating numerically the law of .

2.2. The distribution of via diffusion time-reversal

The goal here is to show that the distribution of coincides with the invariant distribution of a positive recurrent process . In order to see the connection, extend to a whole process defined via

| (2.7) |

and note that is a stationary process under . Fix , and define the process via time-reversal:

| (2.8) |

It still follows that is stationary under , with the same one-dimensional marginal distribution as . Furthermore, stationarity of clearly implies that the law of the process does not depend on (except for its time-domain of definition). Therefore, one may create a new process such that the law of is the same as the law of for all . If one can establish that is ergodic, then the distribution of may be efficiently estimated via the ergodic theorem.

Towards this end, one needs to understand the behavior of . Standard results (e.g. [20]) in the theory of time-reversal imply that is a diffusion in its own filtration, and identify the corresponding coefficients. In order to deal with , we return to the definition of and define yet one more process via

| (2.9) |

Using all previous definitions, we obtain that

| (2.10) |

As it turns out, one can describe the joint dynamics of in appropriate filtrations (and these dynamics do not depend on , as expected). To ease the presentation, recall from Section 1 that for any valued smooth function on the (matrix) divergence is defined by for . It is then shown in Section 7 that is such that

for independent Brownian motions in an appropriate filtration.

From the joint dynamics of one obtains the joint dynamics of , which again do not depend on . In particular, since is a semimartingale, (2.10) yields that

| (2.11) |

For a generic version with the same generator (which does not depend upon time) as above, ergodicity of implies ergodicity of (see Proposition 7.1 later on in the text). Furthermore, is “mean reverting” as can easily be seen when , and , and continues to be true in the general case. Thus, one expects the empirical laws of to satisfy a certain strong law of large numbers, an intuition that is made precise in the following result.

Theorem 2.4.

Let Assumption 1.7 hold. Then, there exists a probability space supporting independent and dimensional Brownian motions and , as well as process satisfying

where is an -measurable random variable with density .

Define the process as the solution to the linear differential equation

| (2.12) |

and then, for any , define as the solution to the linear differential equation

| (2.13) |

Lastly, let , and set as in (2.1). Define the (random) empirical measure on , the Borel subsets of by

| (2.14) |

With the above notation, there exists a set with such that

| (2.15) |

where is the joint distribution of under given in (2.2).

Remark 2.5.

In the context of Theorem 2.4, note that the processes and can be given in closed form in terms of ; indeed,

Theorem 2.4 provides a way to efficiently estimate the joint distribution of efficiently through Monte-Carlo simulation. Indeed, one need only obtain a single path of the reversed process to recover the distribution . However, the applicability of the result above depends heavily on whether or not the distribution for is known, as it (together with its gradient) appears in the dynamics of . In the case where is one-dimensional, or more generally, reversing, can be expressed in closed form from the model coefficients and in the dynamics for . Furthermore, there are certain cases of non-reversing, multi-dimensional diffusions, where can be (semi-)explicitly computed, as the next example shows.

Example 2.6.

Assume that is a multi-dimensional Ornstein-Uhlenbeck process with dynamics

where , , and . Here, and (A1) clearly holds. Furthermore (A2) is satisfied when is (strictly) positive definite; in fact, we take as the unique positive definite square root of . The process need not be reversing, as can clearly be seen when is the identity matrix, and is not symmetric. However, as will be argued below, the ergodic assumption (A3) holds when all eigenvalues of have strictly positive real part, and one may identify the invariant density “almost” explicitly. To see this, a direct calculation shows that if a symmetric matrix satisfies the Riccati equation

| (2.16) |

then the function

satisfies where is as in (1.2). If is additionally positive definite then, up to a normalizing constant, is the density for a normal random variable with mean and covariance matrix . Thus, is integrable on and (A3) follows from [28, Corollary 4.9.4] which proves recurrence for .

It thus remains to construct a symmetric, positive definite solution to (2.16). From [1, Lemma 2.4.1, Theorem 2.4.25] such a solution (called the “stabilizing solution” therein) exits if a) the pair is stabilizable, in that there exists a matrix such that has eigenvalues with strictly negative real part and b) the eigenvalues of have strictly positive real part. In the present case, each of these statements readily follows: for the first statement, one can take ; for the second statement, note that the eigenvalues of coincide with those of , which by assumption have strictly positive real part. Therefore, even in this non-reversing case one may still identify .

The previous interesting Example 2.6 notwithstanding, for non-reversing, multi-dimensional diffusions, even after verifying the ergodicity of (and hence the existence of ) one does not typically know explicitly. In such cases, the following simulation method is proposed: fix a large enough and first simulate via (0.2), starting from any point (since the invariant density is unknown). If the choice of is large enough, the process will behave as the stationary version in (0.2), since will have approximately density . In that case, defining via for , should behave as it should in the dynamics (7.7), even with having (approximate) density . Now, given , may be defined via the formulas of Remark 2.5; therefore, for large enough , the empirical measure should approximate in the weak sense the joint law .

Note finally that when is known and , and under certain mixing conditions (see [30, 29]), one can also obtain uniform estimates for the speed at which the above convergence takes place.

Remark 2.7.

In the case when and , it is possible to explicitly identify the support of . Such an identification follows from more general ergodic results on “stochastic differential systems” obtained in [5, 4]. To identify the support, note that when , it follows that . A direct calculation using Remark 2.5 shows that has dynamics

| (2.17) |

Hence, the paths of are of bounded variation. Now, define

| (2.18) |

Assumption 1.7 implies for some and thus with if and only if for some constant , for all . In this case, almost surely for all . With this notation, [5] proves:

3. A Numerical Example

We now provide an example which highlights the superiority (in terms of computational efficiency) of the time-reversal method over the naive method for obtaining the distribution of . Consider the case , and

| (3.1) |

Note that the function fails to be non-negative. However, as argued below, the results of Theorem 2.4 still hold. As is a mean-reverting Ornstein Uhlenbeck process, it is straight-forward to verify Assumption (A3) with , so that . We claim that is normally distributed with mean vector and covariance matrix

Indeed, integration by parts shows that for :

The ergodicity of implies almost surely; therefore, it follows that holds almost surely. Next, note that is independent of and normally distributed with mean and variance . Lastly, as a process, is an -bounded martingale and hence almost surely exists, where is independent of , and normally distributed with mean and variance . Thus exists almost surely and

from which the joint distribution follows. Now, even though can take negative values, the time reversal dynamics in (2.17) still hold, taking the form

Lastly, even though Theorem 2.4 no longer directly applies, it is shown in [5, Theorem 3.3, Section 3.D, Proposition 3.15] that is still ergodic555The tightness condition in Proposition 3.15 is straightforward to verify., in that (2.15) holds.

For these dynamics, we performed the following test: for a fixed terminal time and mesh size , we estimated the distribution of in two ways. First, (“Method A”) by sampling and setting , and second (“Method B”) by running the forward process until then setting , . For each simulation we computed the empirical distribution along a single path and then estimated the Kolmogorov-Smirnov distance (, for distribution functions ) between the empirical and true distribution for . The parameter values were , , and .

| Method A | Method B | |

|---|---|---|

| Median Distance | 0.00887 | 0.00882 |

| Standard Deviation | 0.00405 | 0.00413 |

| Percentile | 0.02168 | 0.02255 |

| Percentile | 0.00405 | 0.00290 |

| Median Time (seconds) | 2.694 | 8.766 |

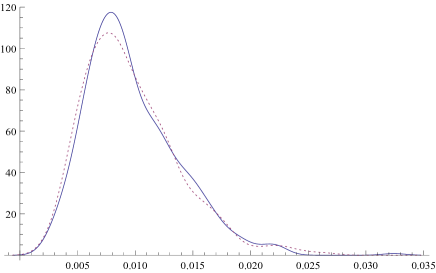

Figure 1 shows the resulting Kolmogorov-Smirnov distances for sample paths. The plot gives a (smoothed) histogram comparing the distances using the two methods described above. As can be seen, the two methods give comparable results: this is not surprising given that rapid convergence of the distribution of to its invariant distribution [9]. Table 1 provides summary statistics regarding the median distances and simulation times, as well as the standard deviation and tail data.

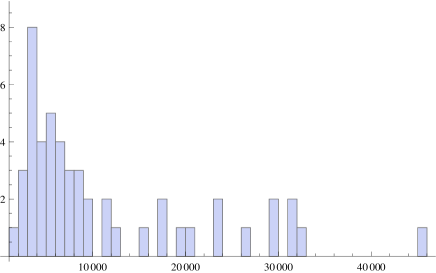

Having obtained Kolmogorov-Smirnov distances using reversal methods, we next compared our results to a naive simulation of , obtained by sampling and computing via (3.1) directly. Here, for the median distance using Method A from Table 1, we sampled stopping at the first instance so that the Kolmogorov-Smirnov distance between the empirical and true distribution for fell below . As can be seen from Figure 2 and the summary statistics in Table 2, the naive simulation performs significantly worse: at the median it took paths and a simulation time of minutes to achieve the same level of accuracy as path ( seconds) of the reversed process. Further, the histogram shows the presence of a significant number of trials where significantly more than the median number of paths were needed to achieve the given accuracy.

| Summary for the Forward Simulation | |

|---|---|

| Median Number of Paths | 7,002 |

| Mean Number of Paths | 11,446 |

| Standard Deviation | 10,165 |

| Minimum Number of Paths | 1,846 |

| Maximum Number of Paths | 45,004 |

| Median Simulation Time (minutes) | 8.66 |

| Mean Simulation Time (minutes) | 14.34 |

4. Conclusion

In this work, using the method of time reversal, an efficient method for simulating the joint distribution of for perpetuities of the form (0.1) is obtained. The joint distribution may be obtained by sampling a single path of the reversed process, as opposed to sampling numerous paths of using the naive method. However, the effectiveness of the proposed method depends on being to obtain analytic representations for the distribution of : an undertaking that, though always possible in the one-dimensional case, is often not possible for non-reversing multi-dimensional diffusions. Furthermore, results are presented for perpetuities with non-negative underlying cash flow rates. As such, more research is needed to identify an effective time reversal method for perpetuities of the form

for general Markovian processes (i.e., not just ) containing both jumps and diffusive terms. Additionally, the performance of the method where is run until a large time and then setting must be thoroughly analyzed: in particular, how fast does the distribution of converge to given a fixed starting point? To answer these questions, one must first analyze the resultant backwards dynamics and associated PDEs for the invariant density, obtaining rates of convergence.

5. Proofs from Section 1.2

Proof of Lemma 1.3.

Let be as in (1.4). Assume first that . Then and (1.4) reads and . Set . Fix and denote by the probability obtained by conditioning upon . The positive recurrence of implies ([28, Theorem 4.9.5]), there exists a -a.s. finite random variable such that implies that and hence the first conclusion of Lemma 1.3 holds. Furthermore, since is stationary, ergodic under , the ergodic theorem implies there is a a.s. finite random variable such that implies . Now, let be such that . We have

where the last inequality follows by the regularity of and the non-explositivity of . Thus

By the stationarity of :

hence , which in turn implies that .

Assume now that , which by continuity of all involved functions implies that . Fix . Positive recurrence of gives that with probability one. On the event , note that

By the Dambis, Dubins and Schwarz theorem and the strong law of large numbers for Brownian motion, it follows that there exists a -a.s. finite random variable such that

therefore,

With , and increasing if necessary (still keeping it -a.s. finite), it follows that implies . Hence the first part of Lemma 1.3 holds true again. Additionally, the ergodic theorem applied with gives a -a.s. finite random variable such that implies . Again, for such that we have

from which follows by the same line of reasoning as above. ∎

Proof of Lemma 1.5.

The proof is nearly identical that if Lemma 1.3. Namely, in each of the cases and , under the given hypothesis there is a constant and a -a.s. finite random variable such that holds for . This gives that

| (5.1) |

where is large enough so that . We thus have

Ergodicity of implies that almost surely

so that , proving the result. ∎

6. Proof of Theorem 2.1

Under the given assumptions there exists a unique solution, to the generalized martingale problem for on , where is from (2.5). Here, the measure space is , where , with being the one-point compactification of . The filtration is the right-continuous enlargement of the filtration generated by the coordinate process on .

Let be an increasing sequence smooth, bounded, open, connected domains of such that . Note that can be obtained by smoothing out the boundary of . By uniqueness of solutions to the generalized martingale problem, for each , the law of of is the same as the law of under (where the latter will always denote a version of the conditional probability) up until the first exit time of . Furthermore, since the process is recurrent, with being the restriction of to the first coordinates, for , the law of under is the same as the law of under . For these reasons, and in order to ease the reading, we abuse notation and still use instead of for the coordinate process on . The underlying space we are working on will be clear from the context.

Denote by the first exit time of from . Assumption 1.7 implies does not explode under and cannot explode to infinity since is strictly positive almost surely under for all . Therefore, the explosion time for is the first hitting time of to and the law of under is the same as the law of the first hitting of to under .

Note that . Assumption 1.7 implies666This follows by the ergodic theorem since .

| (6.1) |

Therefore,

Define

| (6.2) |

Fix and let . Note that . Since holds -a.s., it follows that

| (6.3) |

Therefore, . By definition, is right-continuous in for a fixed and so

Therefore, if is continuous it follows that . It is now shown that in fact is in and satisfies . This gives the desired result for since .

Let be a smooth function such that , . By the classical Feynman-Kac formula

satisfies in with on . Since there exists a pair so that . Using (6.3) this gives

| (6.4) |

Therefore, is transient [28, Chapter 2] and, since is positive recurrent, this implies that for all , with -probability one, either or , where in the latter case, since cannot explode to . This in turn yields that or with -probability one and hence by the dominated convergence theorem

| (6.5) |

For from (6.4), and hence for all [28, Theorem 1.15.1]. But this implies , and so from (6.5) the are converging point-wise to a strictly positive function. Thus, by the interior Schauder estimates and Harnack’s inequality, it follows by “the standard compactness” argument ([28, Page 147]) that there exists a , strictly positive, function such that converges to in the Holder space for all compact . Clearly, this function satisfies in . In fact, since converges to pointwise, and hence .

The boundary conditions for are now considered. Let the integer be given. It suffices to show for each there is some such that

| (6.6) |

The condition near is handled first. By way of contradiction, assume there exists some such that for all integers there exists , such that . Since the are all contained within there is a sub-sequence (still labeled ) such that for .

Let and choose such that implies . Since is increasing in , . Since is continuous, . Since this is true for all , . But, this is a contradiction : for each . To see this, let and choose such that . This is possible in view of (6.1). Thus, for , and hence . Taking gives the result.

The proof for is very similar. Assume by contradiction that there is some such that for all integers there exist , such that . Again, by taking sub-sequences, it is possible to assume . Fix . For , since is increasing in , . Since is continuous, . Since this holds for all , . But, this violates the condition that under , almost surely.

The uniqueness claim is now proved. Let be a solution of such that and such that (2.6) holds. Define the stopping times

| (6.7) |

By Ito’s formula, for any

Since almost surely , taking yields

On , , and hence by and (2.6), for any there is an such that for

Taking thus gives

Taking gives

and hence taking gives . Similarly, for

for all and for some . Note that the set is restricted to include but this is fine since lower bounds are considered. Now, on the event it holds that . Thus, taking

Taking gives

Taking and noting that for large enough on it holds that

where the last equality follows by the definition of in (6.2). Now, in proving it was shown that and hence . Taking gives that , finishing the proof.

7. Dynamics for the Time-Reversed Process

The goal of the next two sections is to prove Theorem 2.4. We keep all notation from Subsection 2.2. We first identify the dynamics for .

Proposition 7.1.

Let Assumptions 1.7 hold. Then, for each , the law of under solves the martingale problem on (for ) for the operator where

| (7.1) |

The operator does not depend upon . Thus, if denotes the solution of the generalized martingale problem for on , then in fact solves the martingale problem for on and is positive recurrent.

Remark 7.2.

If is reversing then satisfies . Thus, in this instance, and, as the name suggests, has the same dynamics as .

Proof.

The first statement regarding the martingale problem is based off the argument in [20]. Since is positive recurrent with invariant measure and has initial distribution under , is stationary with distribution . Since , equation in [20] holds noting that does not depend upon .

For a given and define the function . The Feynman-Kac formula implies satisfies on with : see [21, 19] for an extension of the classical Feynman-Kac formula to the current setup. Therefore, the condition in equation of [20] holds as well. Thus, the formal argument on page of [20] is rigorous and the law of under solves the martingale problem for .

Turning to the statement regarding , set as the formal adjoint to . is given by (1.2) with replacing therein. Using the formula for in (7.1) and for in (1.2) calculation shows that

Since

| (7.2) |

it follows by considering above that . Therefore, is an invariant density for if an only if the diffusion corresponding to the operator does not explode, where is the h-transform of [28, Theorem 4.8.5]. But, by definition of the h-transform [28, pp. 126] and (1.2) with replacing :

where the third equality follows from (7.1). Thus, Assumption 1.7 (specifically the fact that is ergodic and ) implies the diffusion for not only does not explode but also is positive recurrent, finishing the proof. ∎

In preparation for the proof of the main result of this Section, which is Proposition 7.5, it is first needed to define a certain “backwards” filtration and to present two Lemmas. Fix and and let be the -field generated by , , and . Then, let be the usual augmentation of . It is easy to check that is -adapted for all , as well as that the process defined via is a dimensional Brownian motion on , independent of . However, the -adapted process is not necessarily a Brownian motion on .

With this notation, the following two Lemmas are essential for proving Proposition 7.5.

Lemma 7.3.

Let Assumptions 1.7 hold. For locally bounded Borel function and , it holds that

| (7.3) |

Furthermore, if is continuously differentiable, then

| (7.4) |

Proof.

Fix . For each and , let

| (7.5) |

First, assume that is twice continuously differentiable. The standard convergence theorem for stochastic integrals implies that (the following limit is to be understood in measure ):

Since and are independent, by Ito’s formula the last quadratic covariation is zero. Therefore, (7.3) holds for twice continuously differentiable . The fact that (7.3) holds whenever is locally bounded follows from a monotone class argument.

In a similar manner, assume that is twice continuously differentiable. The standard convergence theorem for stochastic integrals implies that

The last quadratic covariation process (without the minus sign) is equal to

where is given by

since . Thus, (7.4) is established in the case where is twice continuously differentiable. The fact that (7.4) holds whenever is continuously differentiable follows form a density argument, noting that there exists a sequence of polynomials such that and both hold, where the convergence is uniform on compact subsets of . ∎

Lemma 7.4.

Proof.

Proposition 7.5.

Let Assumptions 1.7 hold. Then, for each there is a filtration satisfying the usual conditions and and dimensional independent Brownian motions on so that the pair have dynamics

| (7.7) |

Proof of Proposition 7.5.

Proposition 7.1 immediately implies that under , has dynamics:

| (7.8) |

where is a Brownian motion on . In order to specify the dynamics for , recall the definition of from (2.9). Observe that

Then, using the definitions of , and , the above is rewritten as

| (7.9) |

Lemma 7.4 implies is a semimartingale, and hence (7.9) yields

The result now follows by plugging in for from (7.6). ∎

8. Proof of Theorem 2.4

8.1. Preliminaries

We first prove two technical results. The first asserts the existence of a probability space and stationary processes consistent with in Theorem 2.4 in that given , it holds that . The second proposition shows that under the non-degeneracy assumption and regularity assumption it follows that is ergodic.

Lemma 8.1.

Let Assumption 1.7 hold. Then, there is a filtered probability space , supporting independent and dimensional Brownian motions and , measurable random variables with joint distribution , as well as a stationary process with dynamics

| (8.1) |

Furthermore, with defined as in (2.12), (2.13), if the process is defined by (see Remark 2.5) then are stationary with invariant measure and joint dynamics

| (8.2) |

Proof.

This result follows from Proposition 7.1. Indeed, one can start with a probability space supporting independent and dimensional Brownian motions and respectively, as well as a measurable random variable (hence independent of and ). Under the given regularity assumptions, Proposition 7.1 yields a strong, stationary solution satisfying (8.1). Then, defining as in (2.9) and, for , as in (2.13), it follows that and hence satisfy the SDE in (8.2). Under the given regularity assumptions the law under of given coincides with the law under of given that . Since by construction, is an invariant measure for , it follows from the Markov property that is invariant for under and hence is stationary with invariant measure . ∎

Define the measures for via

| (8.3) |

We now consider when on and . According to Theorem 2.1, and hence possesses a density satisfying

| (8.4) |

Additionally, we have the following Proposition:

Proposition 8.2.

Proof of Proposition 8.2.

Recall from (2.4) and define by

| (8.6) |

From (8.2) it is clear that the generator for is . As an abuse of notation, let also denote the solution to the generalized martingale problem for on . Using Theorem 2.1, and the fact that under the given coefficient regularity assumptions, (see [16, Ch. 6]) a lengthy calculation performed in Lemma A.1 below shows that the density from (8.4) solves where is the formal adjoint to . Since by construction, , positive recurrence will follow once it is shown that is recurrent. By Proposition 7.1, the restriction of to the first coordinates (i.e. the part for ) is positive recurrent. Since by (2.13) it is evident that does not hit in finite time, it follows that that does not explode under . Thus, [28, Corollary 4.9.4] shows that is recurrent. Now, that (8.5) holds follows from [28, Theorem 4.9.5].

∎

8.2. Proof of Theorem 2.4

The proof of Theorem 2.4 uses a number of approximations arguments. To make these arguments precise, we first enlarge the original probability space so that it contains a one dimensional Brownian motion which is independent of and . Let be as in (0.3), and for , define . Similarly to (0.1) define

| (8.7) |

Note that takes the form (0.3) for and when the Brownian motion therein is the dimensional Brownian motion . Note that . Denote by the joint distribution of under and by the conditional cdf of given . By Theorem 2.1 it follows that and hence admits a density.

In a similar manner, by enlarging the probability space of Lemma 8.1 to include a Brownian motion (still labeled ) which is independent of , , and and defining the family of processes and for according to

| (8.8) |

it follows that solve the SDE

| (8.9) |

Since , Proposition 8.2 shows for the generator associated to (8.9) is positive recurrent with invariant density and thus for all and all bounded measurable functions on (note that conditioned upon we have ):

| (8.10) |

With all the notation in place, Theorem 2.4 is the culmination of a number of lemmas, which are now presented. The first lemma implies that converges weakly to as .

Proof of Lemma 8.3.

Denote by the sigma-field generated by , and . Set . By the independence of and :

Now, set . Note that is monotone increasing in with . Furthermore,

By assumption, . Since for any , a.s., it thus follows that . The dominated convergence theorem applied path-wise (recall that there exists a so that almost surely) then gives that , which shows that the pair converges in probability to , finishing the proof. ∎

Next, define as the class of (Borel measurable) functions which are bounded and Lipschitz in , uniformly in ; in other words,

| (8.11) |

The next Lemma gives a weak form of the convergence in Theorem 2.4 for regular . Note that the notation stands for the limit in probability as .

Lemma 8.4.

Let Assumption 1.7 hold. Assume additionally that . Then for all and all :

| (8.12) |

Proof of Lemma 8.4.

For ease of presentation we adopt the following notational conventions. First, for any measurable function and probability measure on set

| (8.13) |

Next, similarly to in (2.14), we define to be the empirical measure of on for as in (8.8). Thus, we write

Proposition 8.2 implies for all and that

Indeed, (8.10) gives for all :

| (8.14) |

Thus, the above limit holds almost surely, and hence in probability.

To prove (8.12) we need to show that for any increasing -valued sequence such that , there is a sub-sequence such that

as this implies (8.12) by considering double sub-sequences. To this end, let be any strictly positive sequence that converges to zero, and assume that , where is from Assumption (A5). Next, pick large enough so that and such that

As argued above, this is possible since converges to in probability. Since Lemma 8.3 implies it follows that

Since

it suffices to show

In fact, the claim is that

or the even stronger (recall , ):

| (8.15) |

From (8.11):

| (8.16) |

Furthermore, recall that

where is from (8.8). With it follows that under

With now denoting the field generated by , and , by the independence of and it follows that

| (8.17) |

where for any , is from Lemma 8.3. Since is stationary under , it holds for all that the distribution of under coincides with the distribution of under and the distribution of under is the same as the distribution of under .

We next claim there exists a sequence such that

| (8.18) |

This is shown at the end of the proof. Admitting this fact, and using , it follows that

In the above, the first inequality holds because of (8.17) and the second by (8.18) and the fact that for any r.v. , . The last equality follows by construction of . Recall that was chosen so that , it follows that

which in view of (8.16) implies (8.15), finishing the proof. Thus, it remains to show (8.18). Since for any , the two terms on the right hand side of (8.18) are treated separately. Let . First we have

Now, so on , since . So, for any it follows that

Set . Since goes to in probability, it follows that . Thus, taking to be maximum of and it follows that

Turning to the second term in (8.18), it is clear that

As shown in the proof of Lemma 8.3, goes to as almost surely. Thus by the bounded convergence theorem, as . Since

upon defining it follows that and . This concludes the proof since to combine the two terms one can take to be twice the maximum of the ’s for individual terms.

∎

The next lemma proves the convergence in Lemma 8.4 for , not just .

Lemma 8.5.

Let Assumption 1.7 hold. Then for all and all :

| (8.19) |

Proof of Lemma 8.5.

By mollifying , since is tight in there exists a sequence of functions with such that

| (8.20) |

Note that

Thus, by the Borel-Cantelli lemma it follows that almost surely

For from Assumption 1.7, let . Note that almost surely since for each we can find a almost surely finite random variable so that for , and hence

Since

we see that

| (8.21) |

Thus, with that almost surely and hence if is the joint distribution of then converges to weakly, as . Now, on the same probability space as in Lemma 8.1 define

Note that

and by construction the law of the process on the right hand side above under is the same as the law of under . It thus follows that for

By (8.21) we can find a non-negative sequence such that and . Now, for we have almost surely for :

Therefore, with denoting the empirical law of we have

Since for any and random variable we have it follows that for any

and hence for the given sequence :

| (8.22) |

Now, fix an sequence such that . Since Lemma 8.4 implies for each , for each we can find a so that

It thus follows that

Since it follows by (8.22) that for each that

We have just showed that for any sequence there is a subsequence which converges in probability to which in fact proves that converges in probability to , proving (8.19). ∎

The next lemma strengthens the convergence in Lemma 8.5 to almost sure convergence under , but for almost every , for from (8.11).

Lemma 8.6.

Let Assumption 1.7 hold. Then for all and almost every :

| (8.23) |

Proof of Lemma 8.6.

We again use the notation in (8.13). Recall from Lemma 8.1 and define as the empirical law of on . Given that is stationary under , the ergodic theorem implies that for all bounded measurable functions on that there is a random variable such that

| (8.24) |

By Lemma 8.5 it holds that for , with probability one. Indeed, let and note:

The first of these two terms goes to by (8.24). As for the second, denote by the marginal of with respect to . Then

By Lemma 8.4 the integrand goes to as for all and thus the result follows by the bounded convergence theorem. Next, we have

and thus (8.23) holds for a.e. , finishing the proof. ∎

The last preparatory lemma strengthens Lemma 8.6 to show almost sure convergence for all starting points , not just almost every .

Lemma 8.7.

Let Assumption 1.7 hold. Then for all and all

| (8.25) |

Proof of Lemma 8.7.

Recall from Remark 2.5 that takes the form

| (8.26) |

Let . By Lemma 8.6, there is some such that (8.25) holds. Using the notation in (8.13) and (8.26) it easily follows for any that

We will show below that . Admitting this it holds that almost surely, and hence the result follows since (8.25) holds for .

It remains to prove that . By way of contradiction assume there is some so that . Then, for each it holds that , which in turn implies . By construction, for any fixed the law of on under coincides with the law of under on . It this holds that . But, this gives for all and hence . But this violates Assumptions 1.7 since almost surely for some . Thus, finishing the proof. ∎

With all the above lemmas, the proof of Theorem 2.4 is now given.

Proof of Theorem 2.4.

We again adopt the notation in (8.13). In view of Lemma 8.1 the remaining statement Theorem 2.4 which must be proved is that there is a set with such that (2.15) holds: i.e.

Recall the definition of from (8.11) and let . In view of Lemma 8.7 there is a set such that and

Let the (countable subset) be as in the technical Lemma A.2 below and set . Clearly, . Let and with . Let and for take and as in Lemma A.2 such that (A.11) therein holds. In what follows the will be suppressed, but all evaluations are understood to hold for this .

Let . With from (A.11) equal to it follows that

With from (A.11) equal to one obtains

Putting these two together yields

Since taking gives

Now, from Lemma A.2 we know for fixed that the functions and are increasing and decreasing respectively in and such that a) for and b) for all and . Therefore, taking in the above and using the monotone convergence theorem we obtain

From Lemma A.2 we know that , for all . Thus, by the bounded convergence theorem and the fact that is tight in it follows that by taking :

Taking gives that . Thus, we have just shown for , and that

By applying the above to we see that

which finishes the proof. ∎

Appendix A Some Technical Results

Lemma A.1.

Let Assumptions 1.7 hold, and additionally assume that , . Recall from (2.1) and the invariant density for . Let be given and set

| (A.1) |

Let the operator be as in (2.5) and the operator be as in the proof of Proposition 8.2, where is from (2.4) and is from (8.6). Let be the formal adjoint of . Then . In particular, if then .

Proof.

For notational ease, the arguments will be suppressed when writing functions except for the appearing in the drifts and volatilities of the operators. Now, recall the dynamics for the reversed process in (8.2):

and note, as is mentioned in the proof of Proposition 8.2, that is the generator for . To further simplify the calculations, set

| (A.2) |

and

| (A.3) |

Note that by (7.2) it follows that . With this notation we have that

which in turns yields that

| (A.4) |

along with

| (A.5) |

Lastly, multivariate notation will be used for derivatives with respect to and single variate notation used for derivatives with respect to . Thus, for the given :

Since and is not a function of :

By definition, . Using (A.4):

Calculation shows

so that

This gives where

| (A.6) |

Now, . is treated first. From (A.2) it follows that and hence

For a scalar function and valued function , . Using this

Using that and collecting terms by derivatives of gives

Since , and ,

Plugging this in and factoring out the yields

| (A.7) |

Turning to in (A.6). Using and yields

Since only depends upon ,

Grouping terms by derivatives of and factoring out the yields

| (A.8) | ||||

Putting together (A.7) and (A.8) and using that :

| (A.9) |

Turning now to , since

it follows that (note : only depends upon and )

But, from (A.9) this last term is precisely . ∎

Lemma A.2.

Let Assumption 1.7 hold. Let be as in (8.11). Recall that and let be a family of open, bounded, increasing subsets of with smooth boundary such that . There exists a countable family of functions

| (A.10) |

such that

-

1)

For each , with on and on .

-

2)

For each and , the functions are increasing in and the functions are decreasing in . Furthermore, for any and , for .

Additionally, for any set . Then, for any and any integer there exits an integer such that for all , , . Furthermore, for any Borel measure on :

| (A.11) |

Proof of Lemma A.2.

Fix and let be a countable dense (with respect to the supremum norm) subset of . Now, let and define:

| (A.12) |

As shown in [2, Ch. 3.4], and are a) increasing and decreasing respectively in , and b) Lipschitz continuous in with Lipschitz constant . Furthermore, as , and on .

Next, let be such that , on and on . Clearly, for each . Now, assume and extend and from functions on to all of via

Clearly, and are Lipschitz on and, since is bounded, it also holds that and are in . Note also that and increase and decrease respectively as to a function which is equal to on and that are bounded on all of by and respectively. This proves above.

Now, let with . Let and for choose so that . By construction of in (A.12) it follows for each that

By definition of this gives . Furthermore, since on , we have on . Therefore, for any Borel measure , using the notation in (8.13):

where the last inequality follows since . This gives the lower bound in (A.11). A similar calculation shows for all that

This gives and on . Thus

Therefore, the upper bound in (A.11) is established. ∎

References

- [1] H. Abou-Kandil, G. Freiling, V. Ionescu, and G. Jank, Matrix Riccati equations, Systems & Control: Foundations & Applications, Birkhäuser Verlag, Basel, 2003. In control and systems theory.

- [2] C. D. Aliprantis and K. C. Border, Infinite dimensional analysis, Springer, Berlin, third ed., 2006. A hitchhiker’s guide.

- [3] B. D. O. Anderson, Reverse-time diffusion equation models, Stochastic Process. Appl., 12 (1982), pp. 313–326.

- [4] L. Arnold, Random dynamical systems, Springer Monographs in Mathematics, Springer-Verlag, Berlin, 1998.

- [5] L. Arnold and W. Kliemann, Qualitative theory of stochastic systems, in Probabilistic analysis and related topics, Vol. 3, Academic Press, New York, 1983, pp. 1–79.

- [6] R. N. Bhattacharya, Criteria for recurrence and existence of invariant measures for multidimensional diffusions, Ann. Probab., 6 (1978), pp. 541–553.

- [7] P. Carmona, F. Petit, and M. Yor, Exponential functionals of Lévy processes, in Lévy processes, Birkhäuser Boston, Boston, MA, 2001, pp. 41–55.

- [8] D. A. Castañon, Reverse-time diffusion processes, IEEE Trans. Inform. Theory, 28 (1982), pp. 953–956.

- [9] M. F. Chen and S. F. Li, Coupling methods for multidimensional diffusion processes, Ann. Probab., 17 (1989), pp. 151–177.

- [10] A. De Schepper, M. Goovaerts, and F. Delbaen, The Laplace transform of annuities certain with exponential time distribution, Insurance Math. Econom., 11 (1992), pp. 291–294.

- [11] F. Delbaen, Consols in the cir model, Mathematical Finance, 3 (1993), pp. 125–134.

- [12] D. Dufresne, The distribution of a perpetuity, with applications to risk theory and pension funding, Scand. Actuar. J., (1990), pp. 39–79.

- [13] , Distributions of discounted values, Actuarial Research Clearing House, 1 (1992), pp. 11–24.

- [14] R. J. Elliott and B. D. O. Anderson, Reverse time diffusions, Stochastic Process. Appl., 19 (1985), pp. 327–339.

- [15] P. Embrechts and C. M. Goldie, Perpetuities and random equations, in Asymptotic statistics (Prague, 1993), Contrib. Statist., Physica, Heidelberg, 1994, pp. 75–86.

- [16] D. Gilbarg and N. S. Trudinger, Elliptic partial differential equations of second order, Classics in Mathematics, Springer-Verlag, Berlin, 2001. Reprint of the 1998 edition.

- [17] H. K. Gjessing and J. Paulsen, Present value distributions with applications to ruin theory and stochastic equations, Stochastic Process. Appl., 71 (1997), pp. 123–144.

- [18] C. M. Goldie and R. A. Maller, Stability of perpetuities, Ann. Probab., 28 (2000), pp. 1195–1218.

- [19] P. Guasoni, C. Kardaras, S. Robertson, and H. Xing, Abstract, classic, and explicit turnpikes, Finance Stoch., 18 (2014), pp. 75–114.

- [20] U. G. Haussmann and É. Pardoux, Time reversal of diffusions, Ann. Probab., 14 (1986), pp. 1188–1205.

- [21] D. Heath and M. Schweizer, Martingales versus PDEs in finance: an equivalence result with examples, Journal of Applied Probability, 37 (2000), pp. 947–957.

- [22] T. Nilsen and J. Paulsen, On the distribution of a randomly discounted compound Poisson process, Stochastic Process. Appl., 61 (1996), pp. 305–310.

- [23] D. Nualart, The Malliavin calculus and related topics, Probability and its Applications (New York), Springer-Verlag, Berlin, second ed., 2006.

- [24] É. Pardoux, Smoothing of a diffusion process conditioned at final time, in Stochastic differential systems (Bad Honnef, 1982), vol. 43 of Lecture Notes in Control and Inform. Sci., Springer, Berlin, 1982, pp. 187–196.

- [25] J. Paulsen, Risk theory in a stochastic economic environment, Stochastic Processes and their Applications, 46 (1993), p. 327–361.

- [26] , Present value of some insurance portfolios, Scand. Actuar. J., (1997), pp. 11–37.

- [27] J. Paulsen and A. Hove, Markov chain monte carlo simulation of the distribution of some perpetuities, Advances in Applied Probability, 31 (1999), pp. 112–134.

- [28] R. G. Pinsky, Positive harmonic functions and diffusion, vol. 45 of Cambridge Studies in Advanced Mathematics, Cambridge University Press, Cambridge, 1995.

- [29] A. Y. Veretennikov, Bounds for the mixing rate in the theory of stochastic equations, Theory of Probability and its Applications, 32 (1984), pp. 273–281.

- [30] , Estimates for the mixing rate for Markov processes, Litovsk. Mat. Sb., 31 (1991), pp. 40–49.

- [31] W. Vervaat, On a stochastic difference equation and a representation of nonnegative infinitely divisible random variables, Adv. in Appl. Probab., 11 (1979), pp. 750–783.

- [32] M. Yor, Bessel processes, asian options, and perpetuities, in Exponential Functionals of Brownian Motion and Related Processes, Springer, 2001, pp. 63–92.