Splitstep Milstein methods for multi-channel stiff stochastic differential systems

V. Reshniak

vr2m@mtmail.mtsu.eduA.Q.M. Khaliq

Department of Mathematical Sciences and Center for Computational Science, Middle Tennessee State University, Murfreesboro, TN 37132, USA

Abdul.Khaliq@mtsu.eduD.A. Voss

Professor Emeritus, Department of Mathematics, Western Illinois University, 1 University Circle, Macomb, IL 61455, USA

d-voss1@wiu.eduG. Zhang

Computer Science and Mathematics Division, Oak Ridge National Laboratory, Oak Ridge, TN 37831, USA

zhangg@ornl.gov

Abstract

We consider split-step Milstein methods for the solution of stiff stochastic differential equations with an emphasis on systems driven by multi-channel noise. We show their strong order of convergence and investigate mean-square stability properties for different noise and drift structures. The stability matrices are established in a form convenient for analyzing their impact arising from different deterministic drift integrators. Numerical examples are provided to illustrate the effectiveness and reliability of these methods.

It is hard to overestimate the role which stochastic differential equations play in mathematical modelling of phenomena with uncertainties and random effects which cannot be properly described in terms of classical deterministic models.

For instance, it has been known for a long time that many real-life processes are intrinsically stochastic with multiple sources of randomness. Numerous examples include various applications in electrical circuit engineering [31], neuroscience [26], gene regulatory networks [13], chemistry [15], biology [43] and other fields of science and engineering. Often the dynamical behavior of such systems can be effectively modeled by the system of Itô stochastic differential equations [4]

(1)

where , is a drift vector, is a diffusion matrix and is an -dimensional Wiener process defined on the complete probability space with a filtration satisfying the usual conditions [25].

This paper is concerned with strong solutions of the system in (1). Unfortunately, only a few of such equations can be solved analytically and numerical methods are necessary to obtain approximate solutions. In this paper we use the denotation for the value of numerical approximation of the solution defined at the nodes of equidistant time discretization with a time step . As we consider strong numerical solutions we recall the following

Definition 1.1.

([25])

A discrete approximation converges strongly with order if there exist a finite constant and a positive constant (independent of h) such that for each

(2)

Stability of the scheme represents another important property of a numerical method illustrating its ability to preserve the qualitative behavior of the solution of the original system. There are two main contributors to the stability properties of SDEs: stiffness and geometry of stochastic perturbations. It should be mentioned that, despite their equal importance, most of the research effort in the literature was concentrated on the study of the stiffness property.

This seems to be logical but unfair.

Of course, stiffness has been studied for a long time in the theory of deterministic ODEs and a lot of valuable results have been obtained (see, for example, [20]). Besides, stochastic stiffness is a generalization of its deterministic counterpart in the sense that a deterministically stiff problem is also stochastically stiff.

However, that is where the similarities between deterministic and stochastic systems end. For example, in the above mentioned biological and chemical networks, main issues arise from the multiscale nature of the underlying problem: presence of multiple timescales and the need to include in the simulation both species that are present in relatively small quantities and should be modeled by a discrete stochastic process, and species that are present in larger quantities and are more efficiently modeled by a deterministic differential equation [13]. Moreover, chemical components usually interact in a highly nonlinear way. Therefore, small random fluctuations can significantly influence the behavior of the entire system and change its stiffness with uncertainty.

Stability of stochastic systems also depends on the geometry of random noise and the type of interaction between the drift and diffusion components of SDEs.

It is well known that noise can be used to stabilize or destabilize deterministic systems. The literature on stabilization / destabilization theory is extensive, analysis of the asymptotic stability in almost sure sense can be found in [27, 5, 23, 8] and mean-square stability of systems with stochastic perturbation was discussed in [8, 22].

For instance, it was shown in [22] that under certain conditions imposed on the drift and diffusion geometries even a non-stiff stable deterministic system can be destabilized in the mean-square sense by an infinitesimally small white noise perturbation.

In the following we will use this example in our analysis of the mean-square asymptotic stability of numerical methods which will discussed later.

Additionally, the presence of several independent noise channels by itself might become the source of additional difficulties, both analytical and computational, which are not present in SDEs with a scalar noise. Of course, it is not difficult to extend algorithms for the case of multiple noise channels but it is known that the stability condition of numerical methods might become very restrictive for an increasing number of noise terms [7].

Hence, in view of the above mentioned it should be evident that a novel approach is required for the proper analysis of multi-dimensional stochastic systems.

A classical way to resolve the problem of stiffness is by incorporating implicitness into numerical schemes. However, in the case of SDEs, the straightforward implementation of an implicit approach can lead to unbounded solutions [25]. Various implicit schemes appeared in the literature to overcome this issue. The family of semi-implicit (drift-implicit) methods has been known for a long time [25, 33, 11] and is well adapted to the problems with stiff deterministic part.

For equations where both drift and diffusion parts are stiff, fully implicit schemes can be used at a cost of higher computational complexity [3, 30, 41].

Also, an elegant explicit approach based on a stochastic modification of Chebyshev methods which possess very good stability properties was recently proposed in [1, 2].

Split-step methods represent a class of fully implicit methods which allow the incorporation of implicitness in the stochastic part of the system with relatively little additional cost.

This feature makes them very attractive for solving equations with multi-dimensional noises.

The first method of this type was introduced by Higham in [21] as a modification of the classical Euler-Maruyama method. Then Wang et al. in [39, 40] presented several variants of split-step backward and forward Milstein methods for systems driven by a single noise term. Also, some valuable results for multi-dimensional SDEs with multiplicative multi-channel noise were obtained recently in [18] where convergence properties of split-step methods with one-step ODE solvers possessing at least first order were investigated.

However their stability analysis was restricted to a single noise term only and numerical examples included systems with at most two noise channels.

In this work we explore the trend.

The paper is organized as follows. In section 2, we provide an overview of existing split-step methods and also introduce the new methods. In section 3, we briefly discuss convergence properties of split-step Milstein methods. In section 4, we give the mean-square stability analysis of the proposed methods and apply results to different test systems.

Numerical examples in section 5 are used to confirm theoretical results. Example 1 is a benchmark problem for testing convergence rates of the numerical methods. Example 2 illustrates the influence of stiffness on the stability of the system. Finally, example 3 is an application problem.

All the results were computed in FORTRAN 90 on Intel(R) Core(TM) i7-4930K, 3.4 GHz processor along with 16 GB memory.

2 Split-step methods

In this section we extend existing split-step methods to systems with multi-dimensional noise and introduce the new split-step Adams-Moulton-Milstein method together with its modified analogue.

We start with the first split-step method proposed in the literature - the split-step Euler -method

(3)

Ding et al. [12] investigated the convergence and stability properties of this method under the global Lipschitz condition. The backward Euler variant of this scheme with was first introduced and analyzed by Higham et al. in [21] under one-sided Lipschitz condition.

Though it is known that Euler-type methods always possess bigger stability regions than their Milstein-type counterparts [7], we are interested in the latter because of their higher rate of strong convergence. With respect to the used splitting technique, split-step Milstein methods can be classified into two families. According to this classification we distinguish between the class of split-step composite Milstein methods

(4)

and the class of modified split-step composite Milstein methods

(5)

where is an increment function of the deterministic ODE solver and is a parameter.

The latter scheme is obtained by collecting all deterministic terms in the first splitting step of the method using the fact that .

Remark. In the equations (4) and (5) , and denote stochastic Itô and Stratonovich integrals respectively

(6)

where is a normally distributed random variable. is a differential operator defined as follows

(7)

Computational aspects of the efficient evaluation of triple product sums of the form

will be discussed in Appendix A.

It is obvious that the choice of deterministic solver determines the properties of the above numerical schemes. Here we provide several variants of the first (deterministic) stage which appeared in the literature earlier.

Split-step composite -Milstein method (SSCTM) and modified split-step composite -Milstein method (MSSCTM) were discussed by Guo et al. [17] and correspond to the classical -method used as deterministic solver

(8)

With , the drifting split-step backward Milstein method (DSSBM) and the modified backward Milstein method (MSSBM) are implicit variants of methods (4) and (5), respectively, using

in the deterministic solver (8).

Deterministic solvers with more than one implicit stage have been considered by various authors. In particular, a two-stage Rosenbrock method (RSB) considered in [18] has form

(9)

(10)

with increment function

(11)

where is a Jacobian matrix and the determining parameters are given in [18]. With , method RSB results when in (5) is replaced by

(12)

Finally, we consider a new split-step Adams-Moulton-Milstein (SSAMM) method and its modified analogue (MSSAMM) based on their development in [38] for single channel noise. Their deterministic component is also a two-stage method, but based on the predictor-corrector approach wherein both the predictor and corrector are implicit but share the same Newton iteration matrix, . The method SSAMM replaces in (4) by

(13)

where

(14)

(15)

with . For details on the construction of deterministic solver and choice of values for parameters we refer to [37]. In the following SSAMM+ will be used for SSAMM method with while SSAMM- will be used for SSAMM method with . For method MSSAMM, in (5) is replaced by

(16)

where and are given above.

3 Convergence properties

In this section we provide convergence analysis of methods (4) and (5) with different deterministic integrators. Using the proof similar to that in [18] and [39] we find that these methods have strong order of convergence 1.0. We accomplish our proof under the usual conditions on and .

Assumption 3.1.

The functions , and for all satisfy the global Lipschitz condition for constant and linear growth bound, as follows:

(17)

(18)

It is worth noting that deterministic steps in the schemes (4) and (5) are given by implicit equations and therefore the question of existence and uniqueness of the solution arises. However since the first step in the scheme (4) merely approximates the drift flow of , existence of this solution follows from the properties of the corresponding ODE solver. For instance, using the fixed point theorem and Assumption 3.1 one may show that for the classical -method (8) a unique solution exists, with probability one, for [19, Theorem 7.2]. Moreover, for the same -method global Lipschitz continuity of implies existence of the solution for the deterministic part of (5) if with .

Similar results also hold for more general Runge-Kutta and multistep methods; see, for example, [19, 20, 35].

Now to measure the order of convergence we use the following theorem given by Milstein:

Theorem 3.1.

([29])

Assume for a one-step discrete time approximation that the local mean error and mean square error for all and satisfy the estimates

(19)

and

(20)

with and . Then

(21)

holds for each . Here is independent of but dependent on the length of the time interval .

To prove the convergence of the methods SSCTM, MSSCTM, SSAMM and MSSAMM we need the following Lemma.

Lemma 3.1.

For the methods (4) and (5) under assumption 3.1 we have the following estimate

(22)

where for the methods SSCTM, MSSCTM, SSAMM and MSSAMM we obtain

(23)

Proof.

Based on the Assumption 3.1 we obtain

for SSCTM method:

for MSSCTM method:

for SSAMM method:

Then

and finally

for MSSAMM method:

∎

Then the following theorem establishes convergence of methods (4) and (5).

Theorem 3.2.

Let be the numerical approximation to at the time after steps with step size , .

Then for methods (4) and (5) with an increment function of the selected ODE solver of order at least one under Assumption 3.1 we have

(24)

Proof.

We try to estimate local mean and mean-square errors (19) and (20) first. Denote the local Milstein approximation step as

(25)

Then we arrive at

(26)

Now from Lemma 3.1 we have that

For example, for method SSAMM using the property of Itô integrals we obtain

Hence condition (19) is satisfied with . On the other hand we have

(27)

Therefore using the inequality we get

for some positive constants and . From Lemma 5.7.2 in [25] it is known that and . Thus we obtain the estimate

(28)

This completes the proof.

∎

4 Mean-square stability properties

Similarly to deterministic ODEs, stability analysis of numerical schemes for SDEs has been mainly focused on the ability of the scheme to preserve qualitative behavior of properly designed scalar linear test equation. We have already mentioned that in stochastic theory this approach is in general not justified because it does not capture the role of the diffusion structure.

It is known that stochastic perturbations destabilize deterministic systems in the mean square sense. For stiff and non-normal systems, geometry of the perturbation can be more important factor than intensity of the noise.

This effect cannot happen in one dimension and therefore is not captured by scalar linear stability analysis [22, 8].

Buckwar and Kelly in [8] provided several test systems which can be used to illustrate how the stability of the SDEs depend on the interaction of the drift and diffusion geometries.

Motivated by these results, we will investigate stability of the following linearized multi-channel system [10]

(29)

Definition 4.1.

([24, 10])

The zero solution of system (29) is said to be

1. Mean-square stable, if for each , there exist a such that

whenever .

2. Asymptotically mean-square stable, if it is mean-square stable and, when

where denotes the mean-square norm.

On the other hand the zero solution of system (29) is asymptotically mean-square stable if and only if the zero solution of deterministic differential system of second moments is asymptotically stable [6, 24]

(30)

Applying the vectorization operation to both sides of (30) yields

(31)

with the stability matrix

(32)

Here denotes the Kronecker product.

Stability condition of the system in (30) is given now by the following

Lemma 4.1.

([10])

The zero solution of deterministic system (30) is asymptotically stable if and only if

(33)

where is the spectral abscissa of matrix and is the real part of the eigenvalues of the matrix .

Analogously, for the numerical method written in the form of the recurrence

(34)

with sequence of random matrices , the stability condition is given by

Lemma 4.2.

([10])

The zero solution of deterministic system (34) is asymptotically stable if and only if

(35)

where and is the spectral radius of matrix .

Remark. It is convenient to represent the stability matrix of the numerical method as the sum of two matrices, one corresponding to the deterministic part of the system and the other corresponding to the stochastic part

For multi-channel stochastic systems the major distinction between stability properties of the original differential system and the numerical method is contributed by matrix . For increasing number of noise channels the stability condition of classical numerical methods becomes very restrictive destroying their ability to preserve the qualitative behavior of the differential system and making them absolutely impractical for applied purposes.

In the following we will construct stability matrices for SSCTM, MSSCTM, SSAMM and MSSAMM methods for SDEs with different diffusion and drift structures and show how the splitting technique with proper choice of drift integrator can significantly improve efficiency of the numerical method.

4.1 Stability of Milstein method

Stability of split-step methods depends on the corresponding properties of deterministic and stochastic integrators. In this paper, the stochastic part of SDEs is treated with the Milstein method. Therefore to understand the role of diffusion geometry in the stability of the numerical solution of stochastic systems we have to analyze this method first. In this section we investigate stability of the classical Milstein method applied to systems with commutative and non-commutative noise structures.

The Milstein method applied to the SDE (29) has the form

(36)

Commutative noise

For linear SDE (29) commutativity condition reads as . Together with the identity the Milstein method in (36) converts to

(37)

Non-commutative noise

It is well known that for SDEs with a non-commutative noise it is impossible to build high-order strong schemes which contains Wiener increments only. One also needs to calculate multiple stochastic integrals . Authors of [25] proposed the following representation of the stochastic integrals based on the Karhunen-Loéve expansion

(38)

where , and are normally distributed independent random variables and is the Kronecker delta. It was shown in [25] that by taking terms in the truncated series in (4.1) numerical scheme preserves the strong order 1 of convergence.

Thus, Milstein method applied to the system (29) with non-commutative noise reads

The mean-square stability matrix of the Milstein method applied to the system (29) is given by

(40)

where matrices and are determined by

with

(43)

Proof.

Proof follows from Theorems 3.9 and 3.10 in [10].

∎

Example. ([7]) In 1-dimensional case condition (35) with matrix (40) for commutative noise reads as

This example clearly illustrates that classical Milstein method has extremely poor stability properties and is not able to catch the qualitative behavior of the stochastic systems with multi-dimensional noise.

4.2 Stability of split-step methods

In this section we establish stability matrices in the form convenient for analyzing their impact arising from different deterministic drift solvers.

Split-step Milstein method (4) applied to the linear system (29) reads

(44)

where is defined in (43), is a stability matrix of given deterministic solver and matrix .

Modified split-step Milstein method (5) applied to the linear SDE (29) has the form similar to the above with matrix given by and multiple Itô integrals substituted by Stratonovich integrals.

Theorem 4.2.

The mean-square stability matrix of the split-step and modified split-step Milstein methods in (4.2) applied to the system (29) is given by

and for the modified split-step method (5) we have

(47)

Proof.

Proof follows immediately from Theorem 4.1.

∎

4.3 Deterministic stability matrices of SSCTM, MSSCTM, SSAMM and MSSAMM methods

It is straightforward to verify that deterministic stability matrices of SSCTM, MSSCTM, SSAMM and MSSAMM methods are given as follows

(48)

(49)

(50)

(51)

where , ,

4.4 Application to different test equations

The standard rule of thumb for analysis of stability of numerical methods is to build and compare their stability regions, i.e. the sets of points in the space of system parameters for which the method is stable in some specified sense. Unfortunately, this approach does not allow to visualize stability of general stochastic systems since we are limited to three parameter dimensions only. We cannot hope to consider all possible combinations of drift and diffusion geometries with this number of available parameters. Therefore there is no simple way to choose a universal test equation for system of SDEs.

To illustrate stability properties of the proposed numerical schemes we consider three test systems which, in our opinion, illustrate the most important factors to numerical stability of SDEs.

First test system has simple diagonal drift matrix and two non-commutative destabilizing in the mean-square noise terms:

(52)

Diffusion matrices and act along and orthogonal to the deterministic flow respectively.

This system was proposed in [9] and shows the effect of the discretization of different diffusion structures on the numerical stability of the method.

The form of the second test system is motivated by the study of the pseudospectra of non-normal matrices and operators [36]. It is known that even asymptotically stable non-normal systems may exhibit large transient growth. It was shown in [22, 10] that such systems may be destabilized in the asymptotic mean-square sense by the small amount of noise acting orthogonally to the deterministic flow.

Thus a second test system is used to show interaction between the drift and diffusion structures. It is given by

(53)

where parameter determines the departure from the normality of the matrix.

The aim of the third test equation is to study the impact on the stability of the numerical method arising from the dimension of the noise. In this case we are not interested in the particular structures of the drift and diffusion components and consider a one-dimensional multi-channel SDE of the form:

(54)

In the following we will compute and plot stability regions of the considered methods. All proofs are based on the particular form of the stability matrix and Lemmas 4.1 and 4.2 and hence are omitted.

We start with stability regions of the differential systems in (52)-(53). Applying results of Lemma 4.1 yields

Lemma 4.3.

([10, 9])

1. The zero solution of (52) is asymptotically stable if and only if

(55)

with , , .

2. The zero solution of (53) is asymptotically stable if and only if

(56)

with , , .

(a)

(b)

(c)

(d)

(e)

(f)

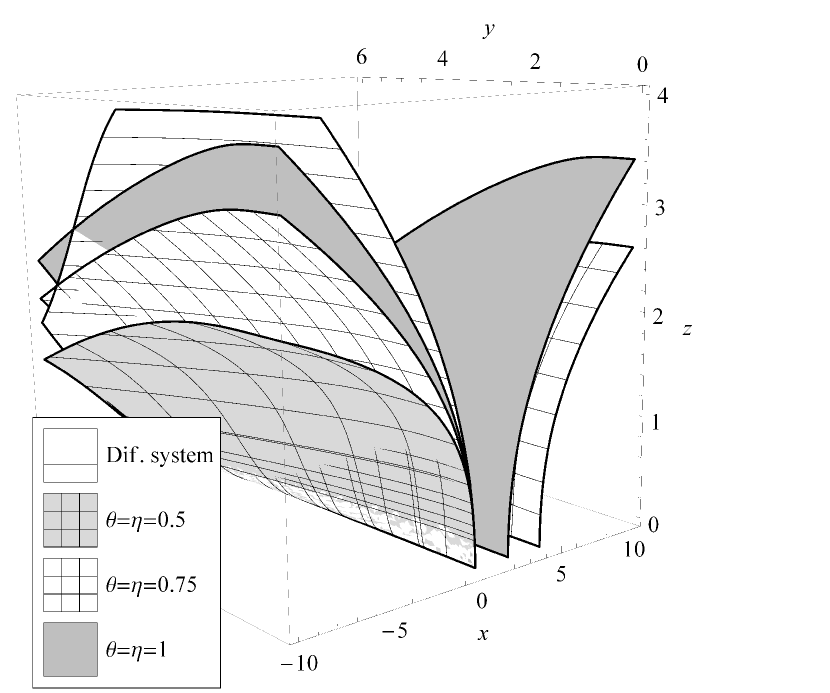

Figure 1: Portions of the mean-square stability regions for the SSCTM (a, c, e) and MSSCTM (b, d, f) method for different values of parameters and applied to the test systems (52)

(a)

(b)

(c)

(d)

(e)

(f)

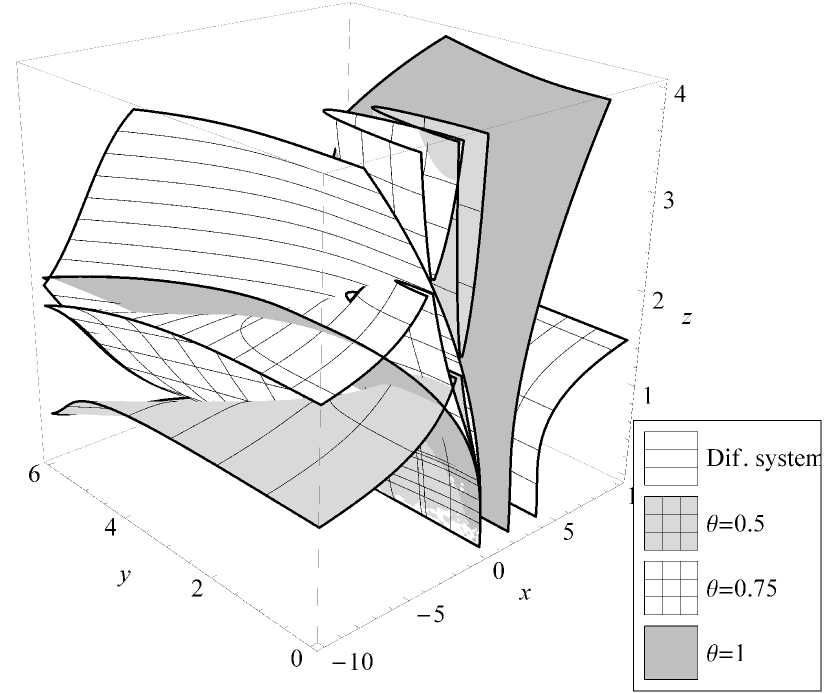

Figure 2: Portions of the mean-square stability regions for the SSCTM (a, c, e) and MSSCTM (b, d, f) method for different values of parameters and applied to the test systems (53)

SSCTM and MSSCTM methods contain two parameters, and , which determine the degree of implicitness of these schemes.

At a first glance it is reasonable to expect better stability properties of the numerical solution for bigger values of and . Figures 1 and 2 show that this is not true in general. One can see that for certain values of the parameters , , and in the test systems (52) and (53) SSCTM / MSSCTM methods possess bigger stability regions for different values of and . A similar result was obtained in [17] for the scalar test equation.

On the other hand it is easy to see that stability properties of the original differential system in the whole stability domain are best recovered for the parameter values .

For the general differential system, the problem of finding the optimal parameters and is very difficult by itself.

Therefore it is reasonable to set unless one knows explicitly how to choose the best parameters.

These values correspond to DSSBM and MSSBM methods which were discussed in Section 2. Therefore in the following we provide stability conditions for these methods only.

Lemma 4.4.

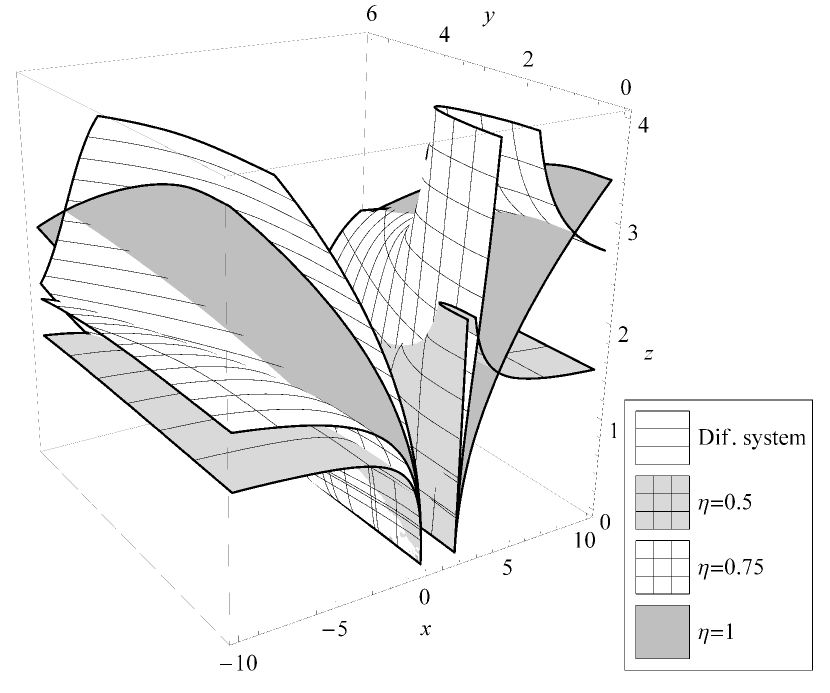

For the test equation (52) the zero solution of stochastic difference equation is asymptotically stable if and only if it satisfies the following conditions:

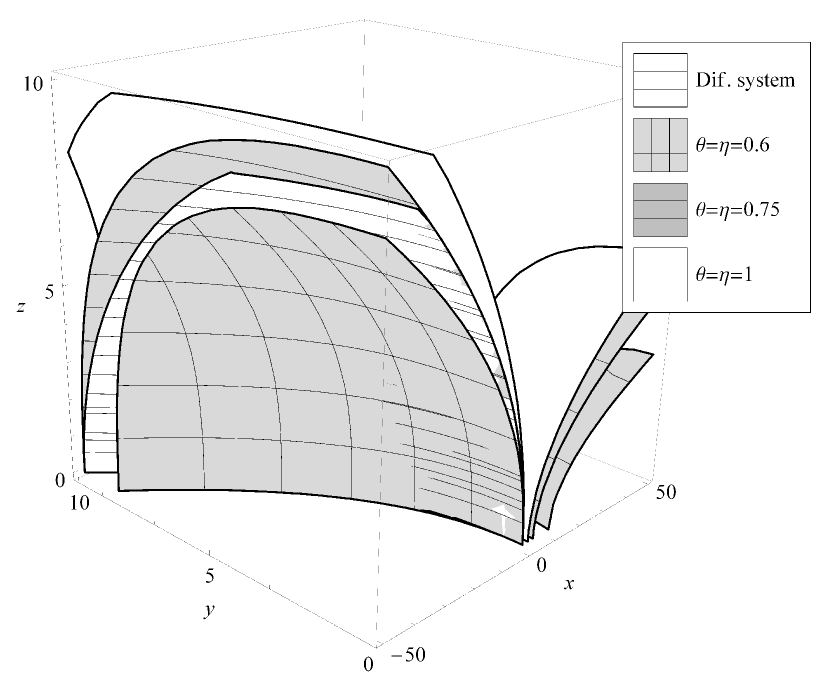

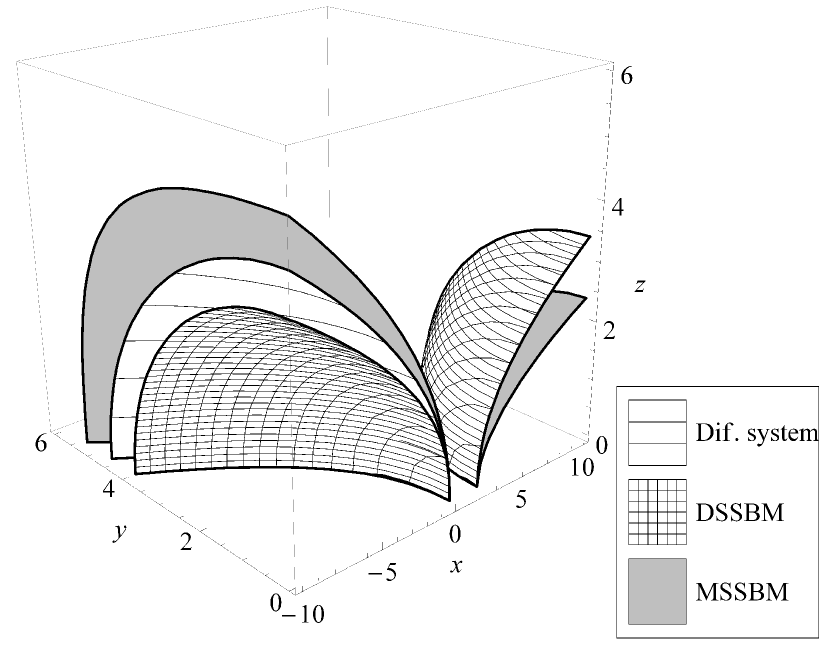

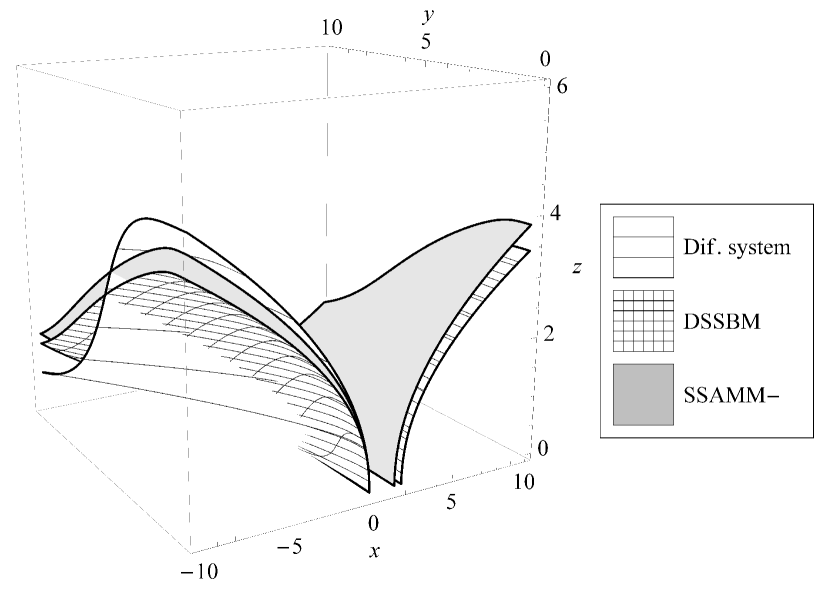

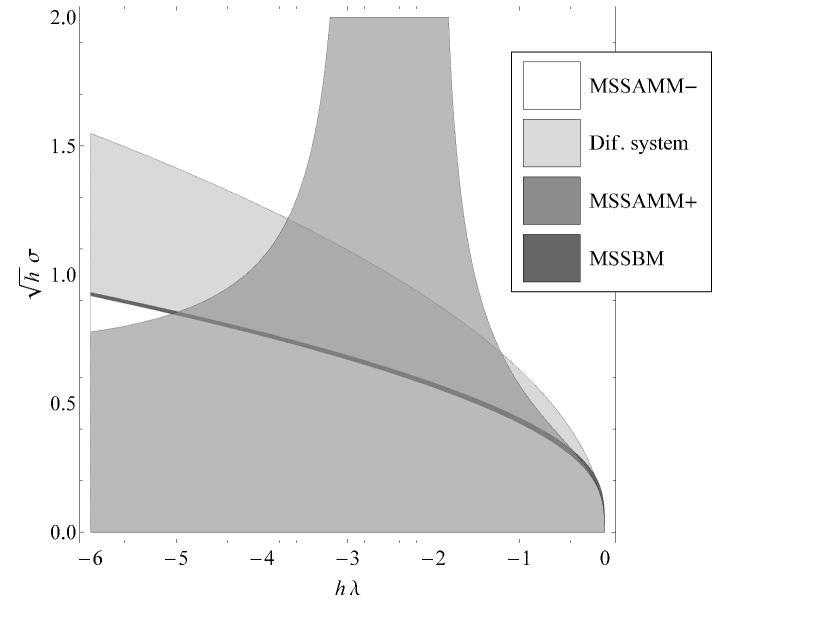

Figure 3: Portions of the mean-square stability regions for the split-step and modified split-step methods applied to test system (52)

.

Figure 3(d) displays the MS-stability regions of the split-step methods (4) and (5) showing better stability properties of the latter when applied to the test system (52). Figure 3 illustrates the impact arising from the choice of the drift integrator. One can see that both regular and modified variants of SSAMM- method are most similar in properties to the original differential system making this method very attractive for practical calculations. On the other hand it is clear that SSAMM+ method is not the best choice for solving systems of this type.

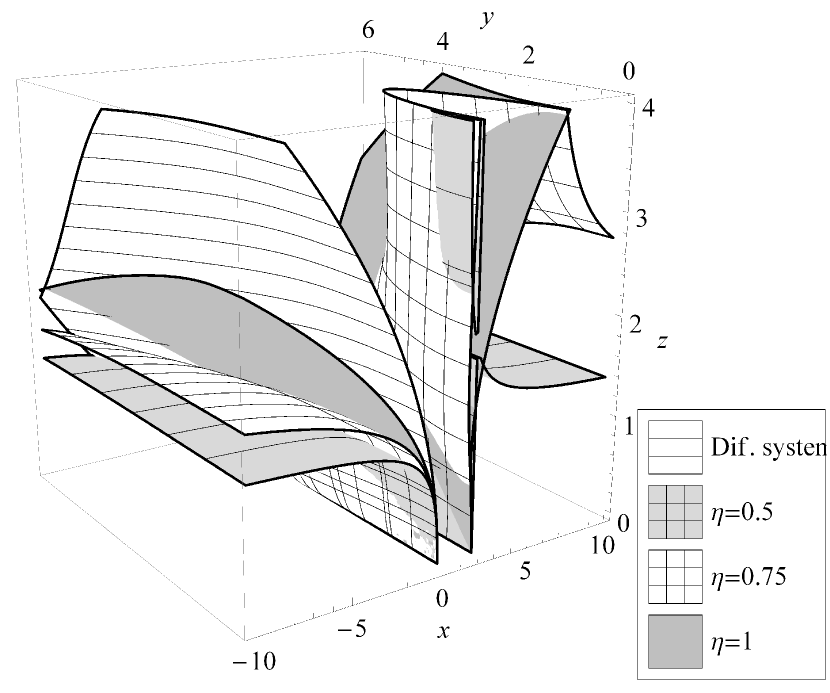

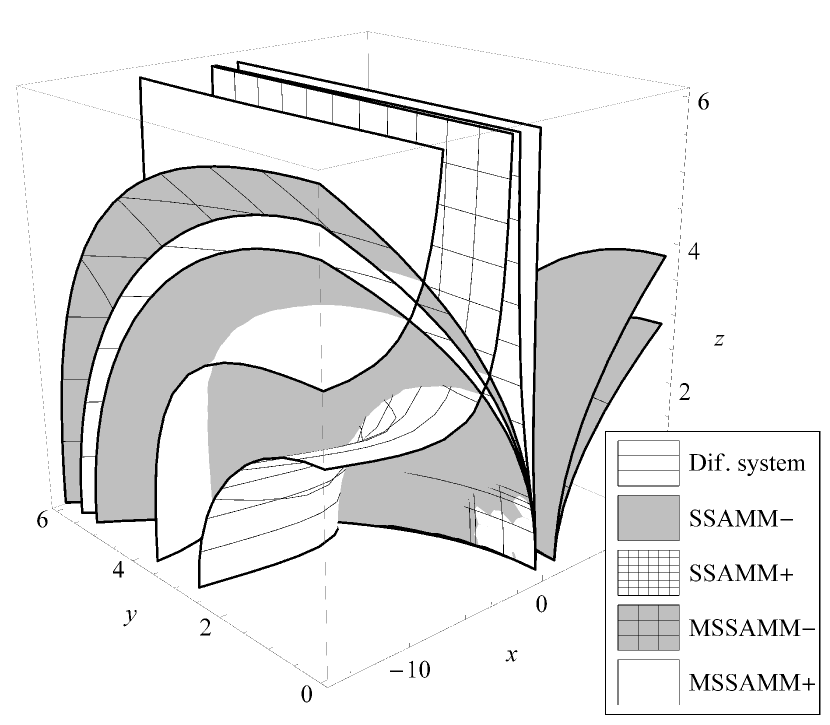

The following Lemma gives the stability conditions for the stochastic difference equations applied to the system with non-normal drift structure.

Lemma 4.5.

For the test system (53) stability condition cannot be written in the closed form and is determined as a spectral radius of the following stability matrix

Parameters for MSSAMM method are omitted due to the space constraints.

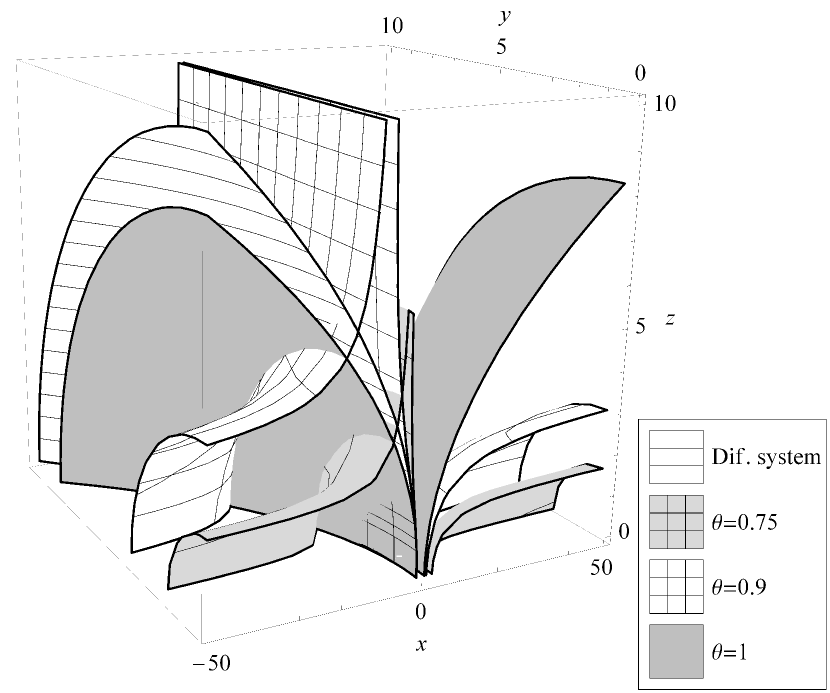

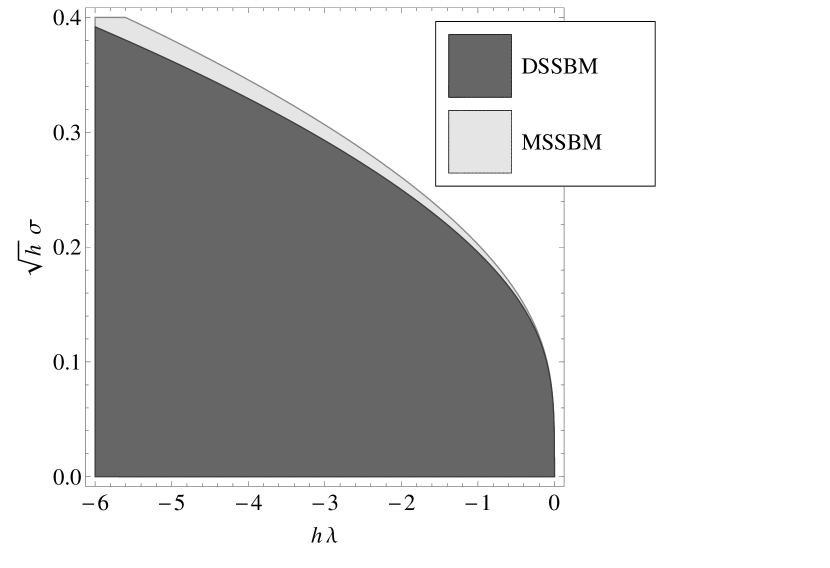

(a)DSSBM and MSSBM

(b)DSSBM and SSAMM-

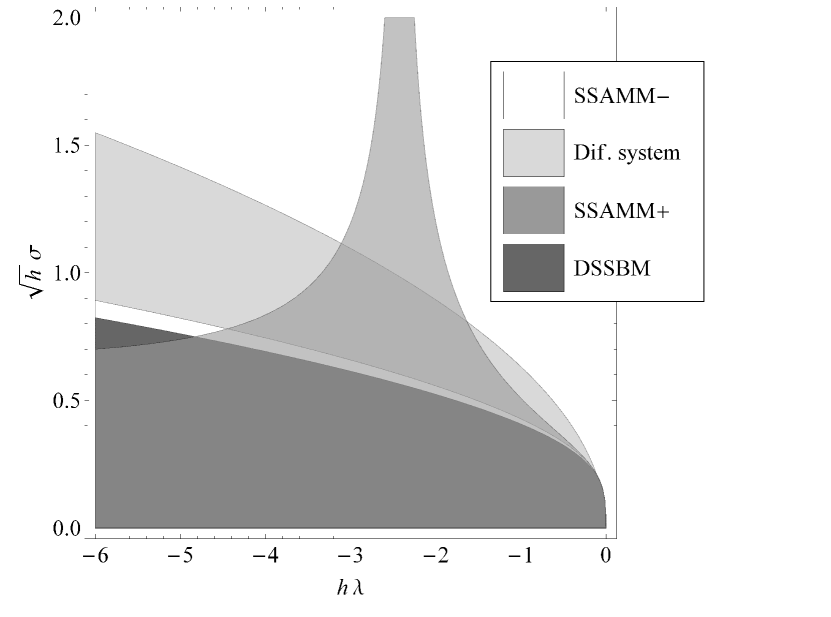

Figure 4: Portions of the mean-square stability regions for the split-step and modified split-step methods applied to test system (53)

.

It is impossible to compute exact eigenvalues for these matrices and therefore we use numerical approximation. Stability regions computed in this way are illustrated in the Figure 4(b). It is easy to see that in contrast to the system (52) for the test system (53) DSSBM method demonstrates better stability properties than MSSBM method. SSAMM and MSSAMM methods behave similarly and hence are not displayed. However it can be seen that SSAMM- still has the best stability properties among considered methods.

The above result is impossible to obtain using the standard stability analysis based on the scalar test equation for which the modified split-step methods always have improved stability properties. This again shows that stability of stochastic differential systems and numerical methods is highly dependent on the structures of the drift and diffusion components and the way they interact with each other.

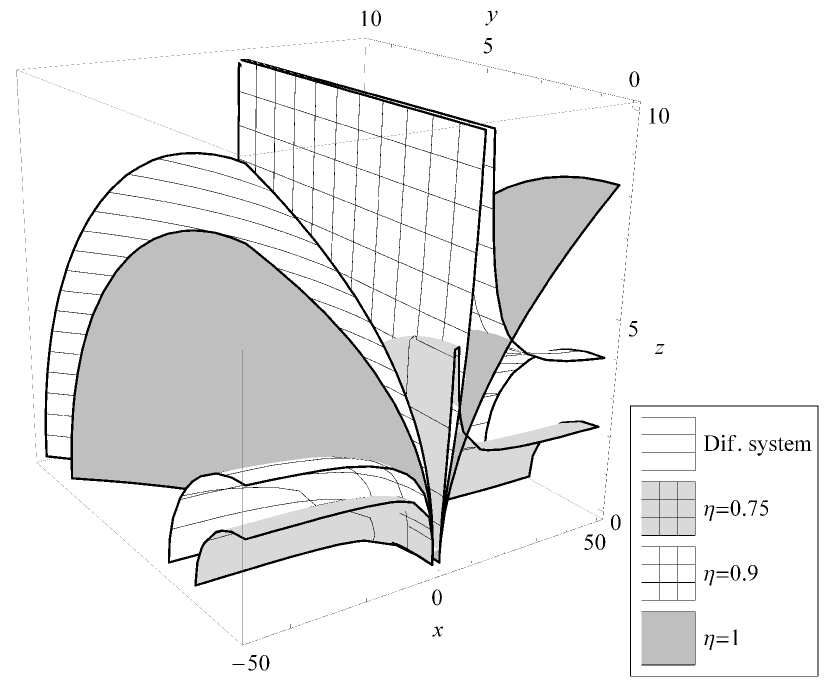

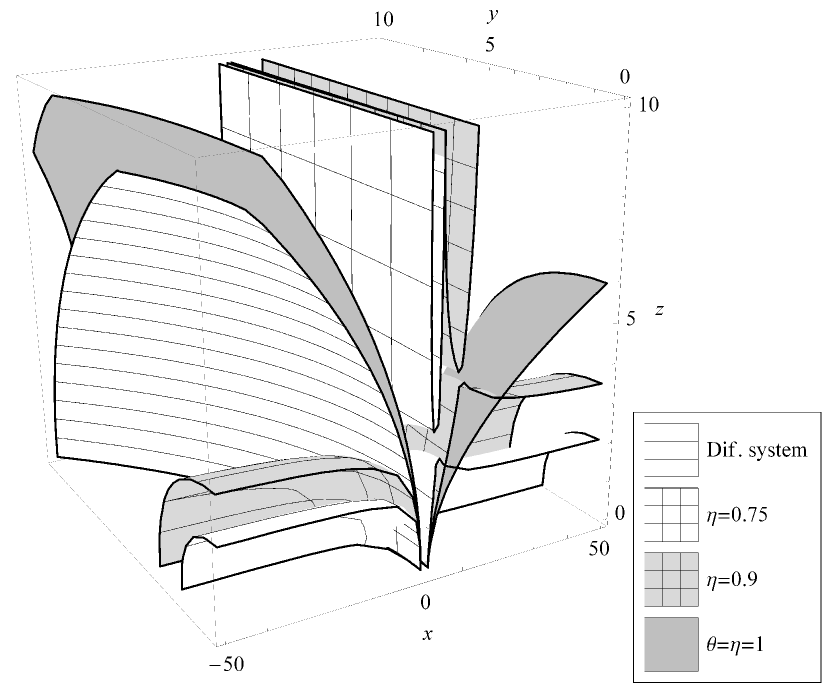

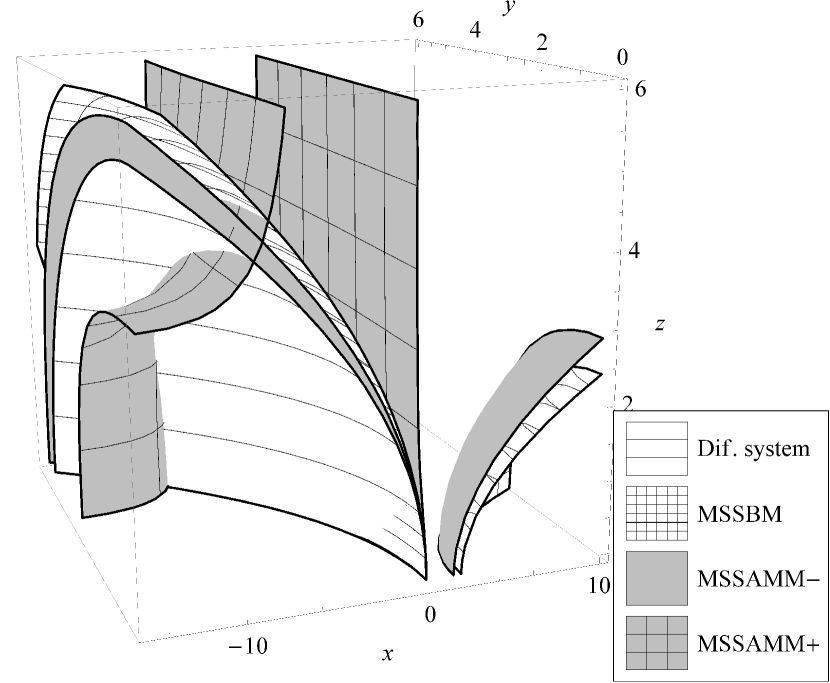

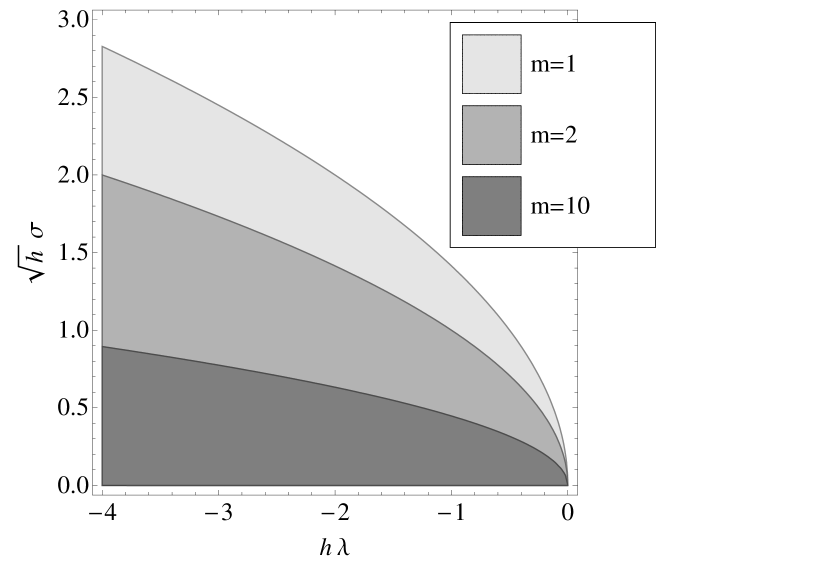

It is easy to obtain stability conditions for the third test equation (54) using Theorem 4.2 and deterministic stability matrices (48)-(51) and therefore this trivial step is omitted. Stability regions for this equation are illustrated on Figure 5(d). Figure 5a shows the influence of the number of noise sources on the stability of the SDE. By comparing stability regions of DSSBM and MSSBM methods from Figure 5(d)b one can see that for the increasing number of noise channels modified methods lose their advantages over the regular methods. Other methods behave similarly. One can also see that for systems with multidimensional noise stability of all the proposed methods deteriorates significantly. However Figures 5(d)c and 5(d)d show that for certain parameter values SSAMM+ and MSSAMM+ methods demonstrate the best stability properties.

(a)Stability regions of the differential system for different numbers of noise channels

(b)Stability regions of DSSBM and MSSBM methods for the system with 10 noise channels

(c)Regular methods

(d)Modified methods

Figure 5: Mean-square stability regions for the test system (54)

.

5 Numerical results

In this section we give four numerical examples to confirm theoretical results from previous sections and illustrate effectiveness of the proposed methods in solving stiff stochastic multi-channel systems.

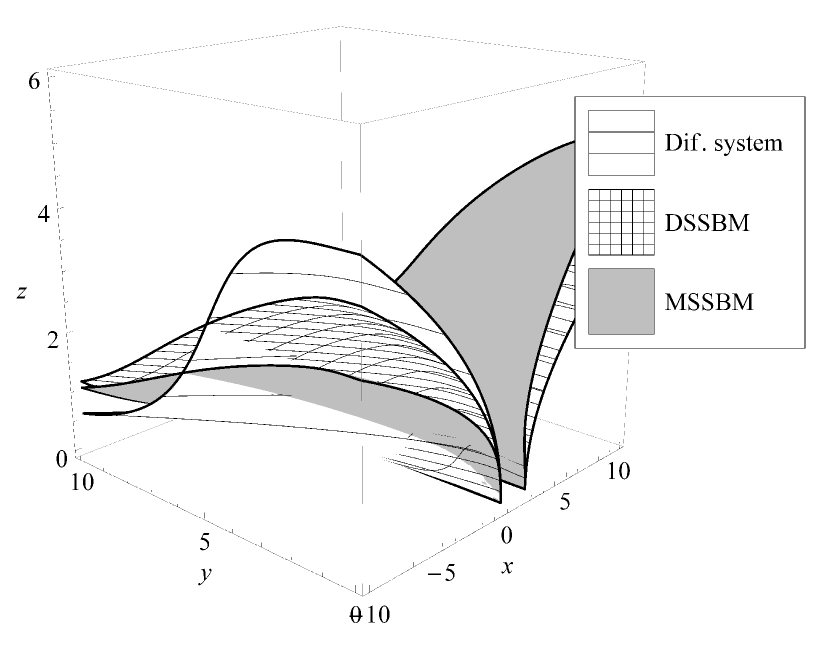

Example 1. To confirm the strong order of convergence of the proposed methods we consider the following multi-dimensional linear stochastic system [32]

(66)

where if , and if , .

Exact solution of the above system is known and given by the expression

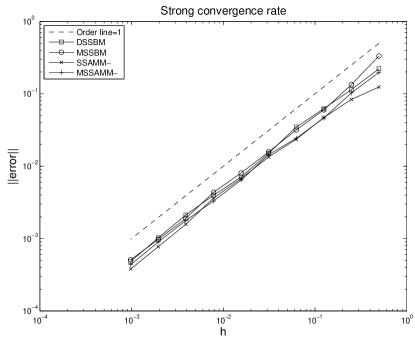

We computed the numerical solution for the case for time steps . Results in the Table 1 and in the Figure 6 show the strong order of convergence 1 for all methods which is in accordance to theoretical results. All schemes have similar level of accuracy.

To study the impact on the stability of the numerical methods arising from the dimension of the noise, we numerically computed spectral radius of the stability matrices for different number of noise channels. We note that the differential system is stable for the considered parameter values. Results from Tables 2-4 clearly illustrate that even for simple linear systems with commutative noise the stability condition can become very restrictive for the increasing number of noise channels. We note that the best result was obtained by the SSAMM+ and MSSAMM+ schemes which is in accordance to the stability analysis performed in the previous section.

h

DSSBM

SSAMM+

SSAMM-

MSSBM

MSSAMM+

MSSAMM-

1.000

1.10 unst.

0.24 stab.

4.48 unst.

0.97 stab.

0.19 stab.

4.18 unst.

0.900

1.05 unst.

0.04 stab.

3.77 unst.

0.94 stab.

0.04 stab.

3.55 unst.

0.800

1.00 unst.

0.07 stab.

3.14 unst.

0.91 stab.

0.07 stab.

2.99 unst.

0.700

0.95 stab.

0.13 stab.

2.58 unst.

0.88 stab.

0.12 stab.

2.49 unst.

0.600

0.90 stab.

0.19 stab.

2.11 unst.

0.85 stab.

0.18 stab.

2.05 unst.

0.500

0.86 stab.

0.31 stab.

1.71 unst.

0.82 stab.

0.28 stab.

1.69 unst.

0.400

0.82 stab.

0.45 stab.

1.39 unst.

0.80 stab.

0.42 stab.

1.38 unst.

0.300

0.80 stab.

0.58 stab.

1.14 unst.

0.79 stab.

0.56 stab.

1.15 unst.

0.200

0.80 stab.

0.70 stab.

0.98 stab.

0.80 stab.

0.69 stab.

0.99 stab.

0.100

0.86 stab.

0.83 stab.

0.91 stab.

0.86 stab.

0.83 stab.

0.92 stab.

Table 2: Values of the spectral radius of the stability matrices for DSSBM, MSSBM, SSAMM and MSSAMM methods for the system (66) with , .

h

DSSBM

SSAMM+

SSAMM-

MSSBM

MSSAMM+

MSSAMM-

1.000

2.21 unst.

0.48 stab.

8.98 unst.

1.80 unst.

0.34 stab.

7.85 unst.

0.900

2.06 unst.

0.09 stab.

7.38 unst.

1.71 unst.

0.06 stab.

6.52 unst.

0.800

1.91 unst.

0.12 stab.

5.96 unst.

1.61 unst.

0.10 stab.

5.33 unst.

0.700

1.75 unst.

0.20 stab.

4.73 unst.

1.50 unst.

0.17 stab.

4.29 unst.

0.600

1.58 unst.

0.30 stab.

3.68 unst.

1.39 unst.

0.26 stab.

3.39 unst.

0.500

1.41 unst.

0.51 stab.

2.80 unst.

1.27 unst.

0.43 stab.

2.62 unst.

0.400

1.24 unst.

0.68 stab.

2.09 unst.

1.15 unst.

0.60 stab.

2.00 unst.

0.300

1.08 unst.

0.79 stab.

1.55 unst.

1.04 unst.

0.73 stab.

1.51 unst.

0.200

0.96 stab.

0.84 stab.

1.17 unst.

0.95 stab.

0.81 stab.

1.17 unst.

0.100

0.91 stab.

0.88 stab.

0.97 stab.

0.91 stab.

0.88 stab.

0.97 stab.

Table 3: Values of the spectral radius of the stability matrices for DSSBM, MSSBM, SSAMM and MSSAMM methods for the system (66) with , .

h

DSSBM

SSAMM+

SSAMM-

MSSBM

MSSAMM+

MSSAMM-

1.000

4.15 unst.

0.90 stab.

16.86 unst.

3.18 unst.

0.58 stab.

14.00 unst.

0.900

3.83 unst.

0.16 stab.

13.70 unst.

2.98 unst.

0.11 stab.

11.49 unst.

0.800

3.49 unst.

0.20 stab.

10.91 unst.

2.77 unst.

0.16 stab.

9.26 unst.

0.700

3.13 unst.

0.32 stab.

8.49 unst.

2.53 unst.

0.27 stab.

7.30 unst.

0.600

2.75 unst.

0.53 stab.

6.42 unst.

2.28 unst.

0.40 stab.

5.62 unst.

0.500

2.36 unst.

0.86 stab.

4.70 unst.

2.02 unst.

0.68 stab.

4.20 unst.

0.400

1.96 unst.

1.08 unst.

3.31 unst.

1.73 unst.

0.90 stab.

3.03 unst.

0.300

1.58 unst.

1.15 unst.

2.25 unst.

1.45 unst.

1.02 unst.

2.12 unst.

0.200

1.23 unst.

1.08 unst.

1.50 unst.

1.18 unst.

1.01 unst.

1.46 unst.

0.100

1.00 unst.

0.97 stab.

1.06 unst.

0.99 stab.

0.95 stab.

1.06 unst.

Table 4: Values of the spectral radius of the stability matrices for DSSBM, MSSBM, SSAMM and MSSAMM methods for the system (66) with , .

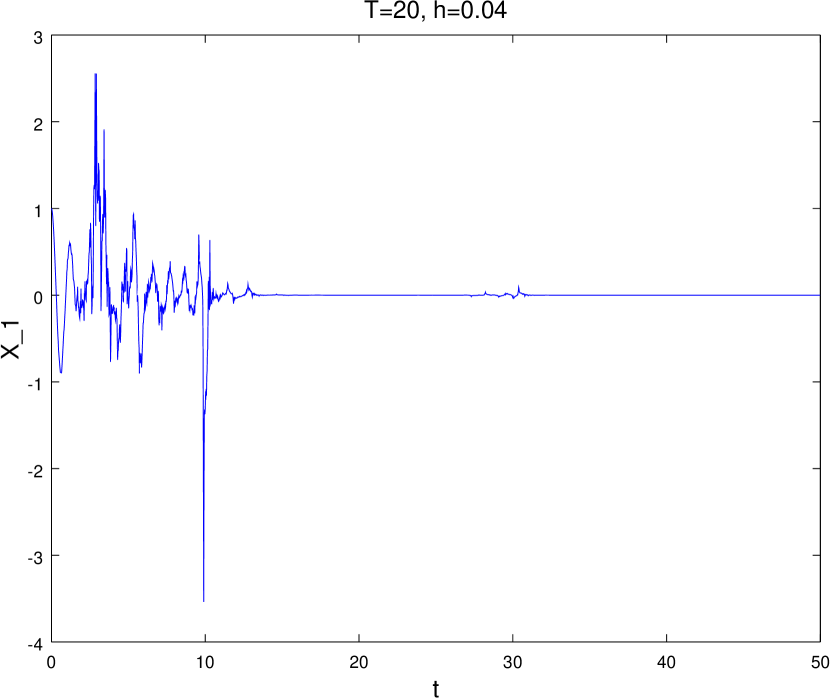

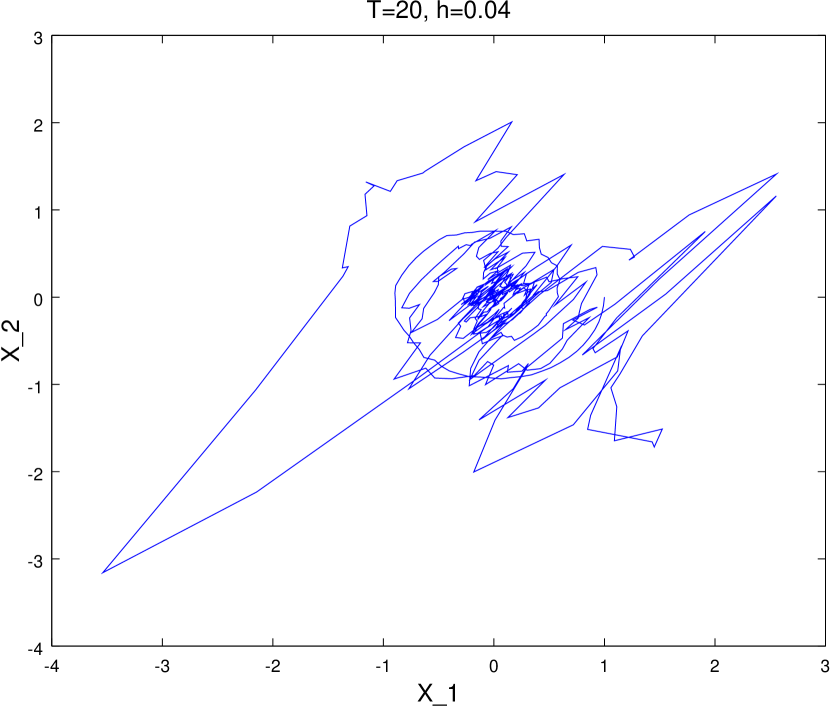

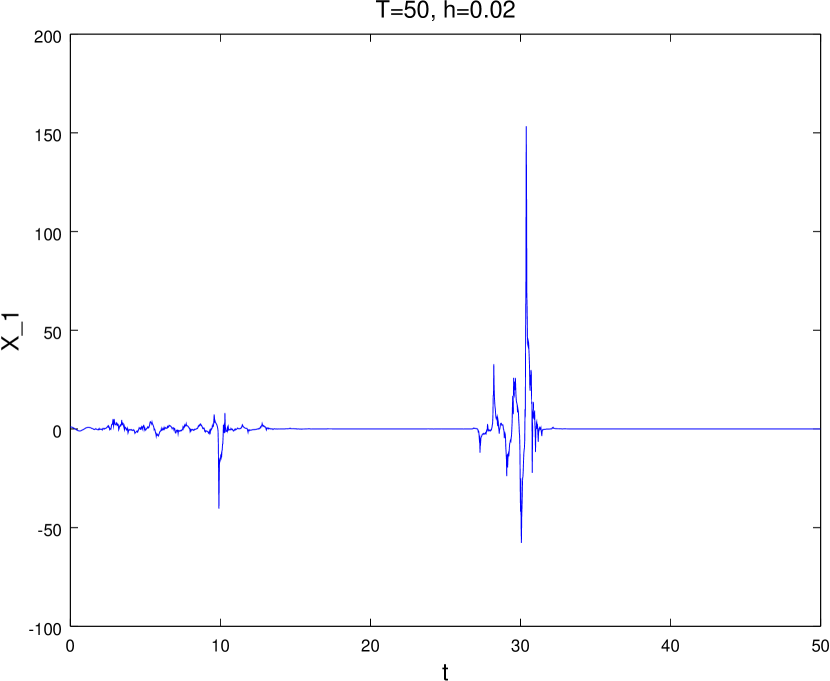

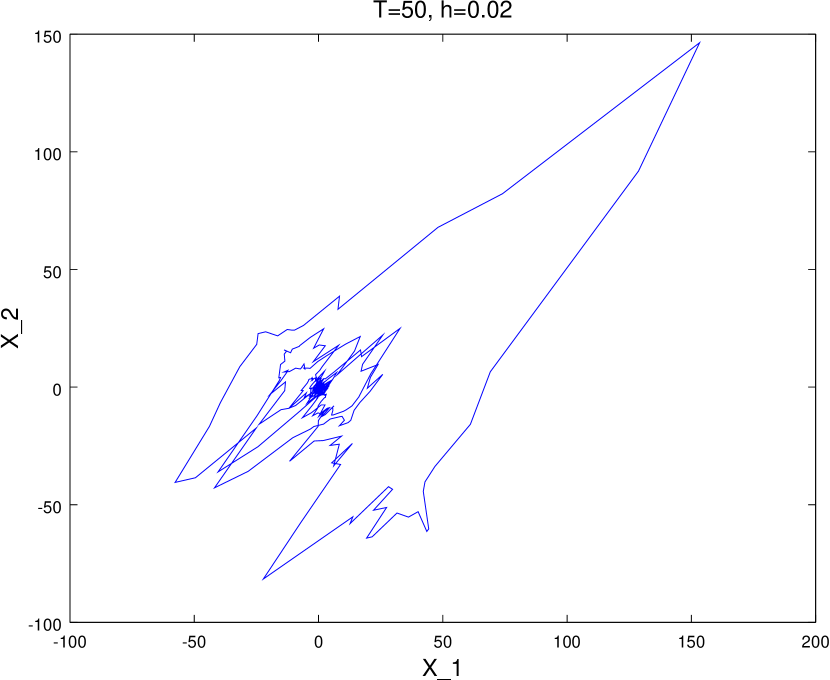

Example 2. Stiff problem.

Second example is a two-dimensional stiff stochastic system [28]

(67)

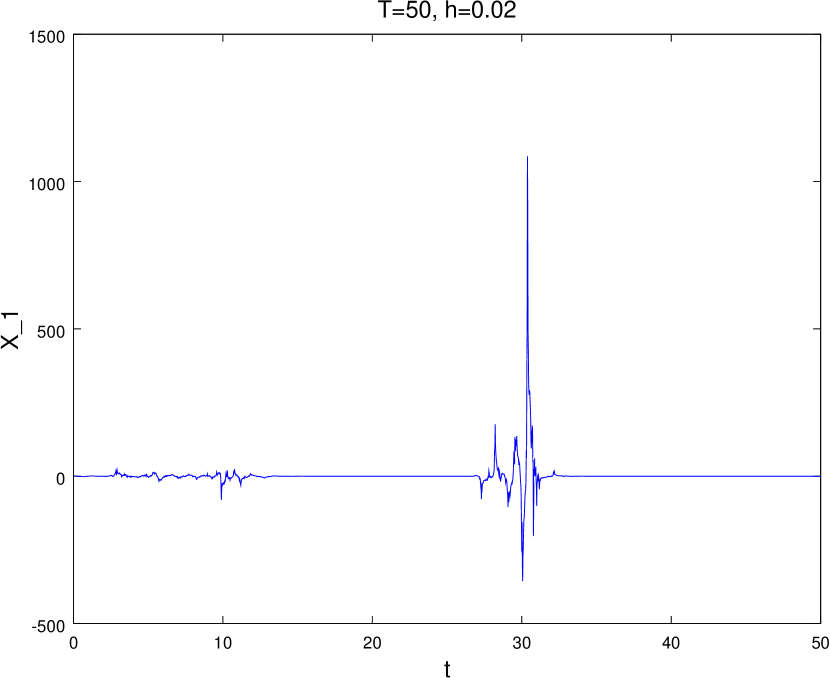

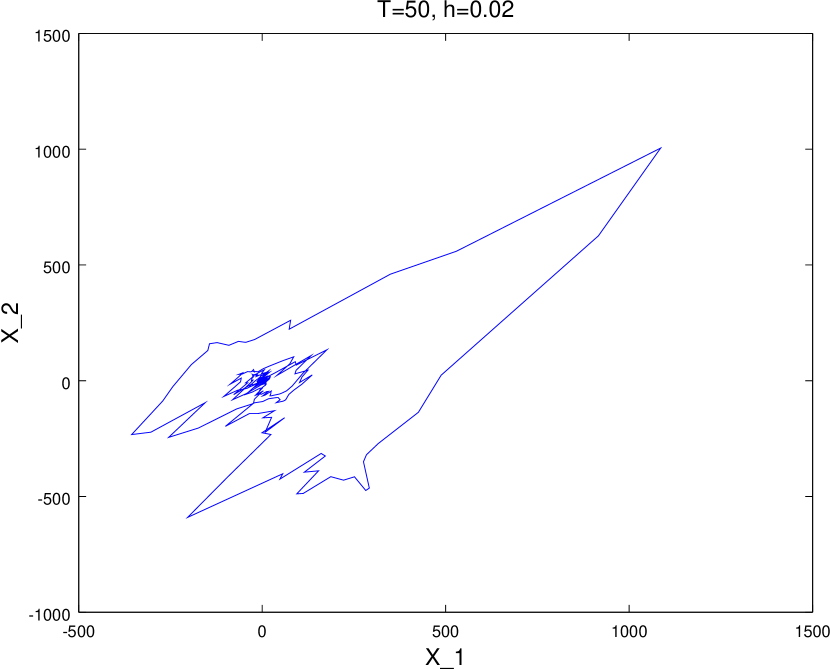

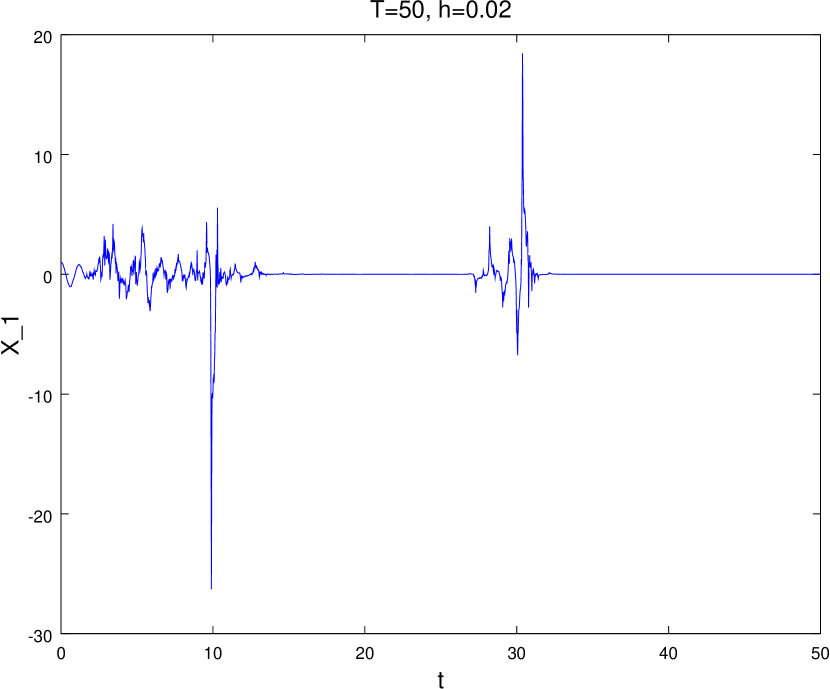

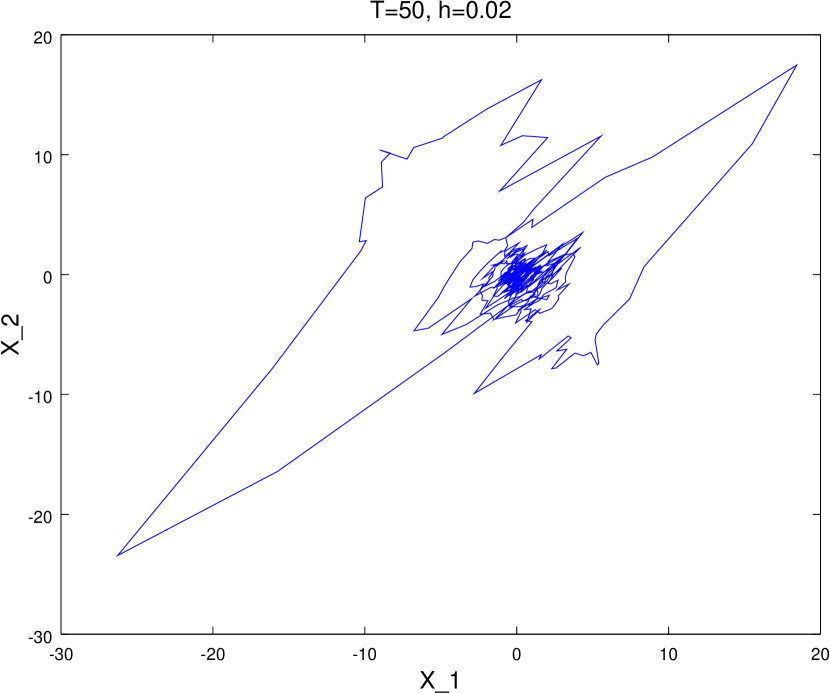

This system was simulated with , and on the interval with initial position at . As it can be seen from Figure 7, all methods have similar dynamics. Their trajectories stay close to the origin which replicates the exact solution. However the methods respond differently to the transients which appear in the long time simulation. These transients are due to the stiffness of the stochastic system in (67). We see that DSSBM and SSAMM methods generate stable solutions while the Milstein method blows up in the vicinity of the transient which is an undesirable behavior for asymptotically stable system.

It is also interesting to compare the behavior of the SSAMM- and the SSCTM () methods since their deterministic parts are geometric integrators of the corresponding rotating deterministic system. Figures 7 e-h show that for the system in (67) SSAMM- method is more stable than SSCTM () method.

Example 3. Application problem: chemical Langevin equations.

When in the well-stirred system of biochemical species interact at a constant temperature through chemical reactions inside some fixed volume in the regime which is far from thermodynamic limit, the state of the system can be modeled by chemical Langevin equations (CLE) [14].

We consider the following 3-species 6-reaction system [34]

with reaction rate constants , , , , and . The initial conditions are , and .

This reaction network can be described by the following system of CLEs

(68)

In the above system is a state vector and denotes the number of molecules of species in the system at time . is a stoichiometric matrix with state-change vectors as columns

Each state-change vector shows the change in the vector of molecular population induced by a single occurrence of a particular reaction.

The propensities of the reaction channels are, respectively,

The product of a propensity function with gives the probability that a particular reaction will occur in the next infinitesimal time .

This system represents an inherently stiff nonlinear system of CLEs, since difference in the scales between propensities has several orders of magnitude.

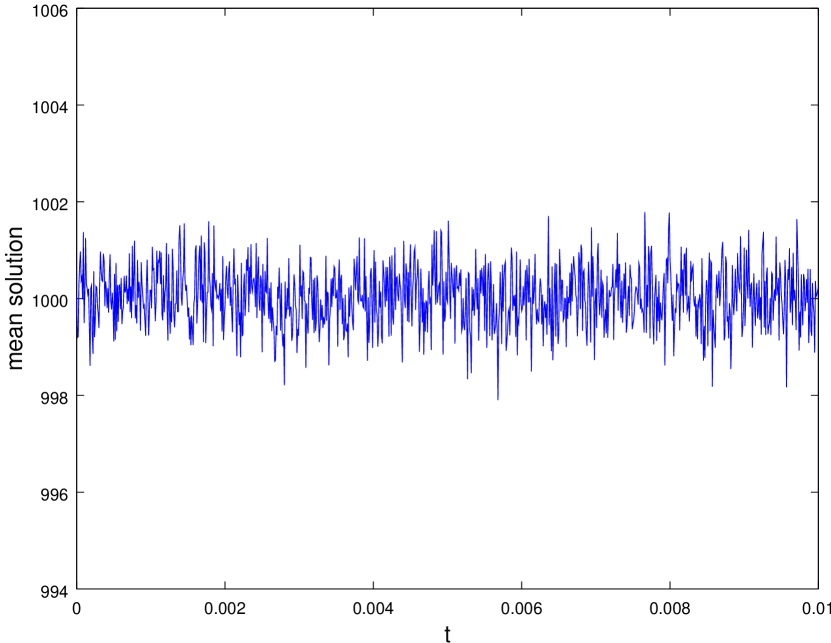

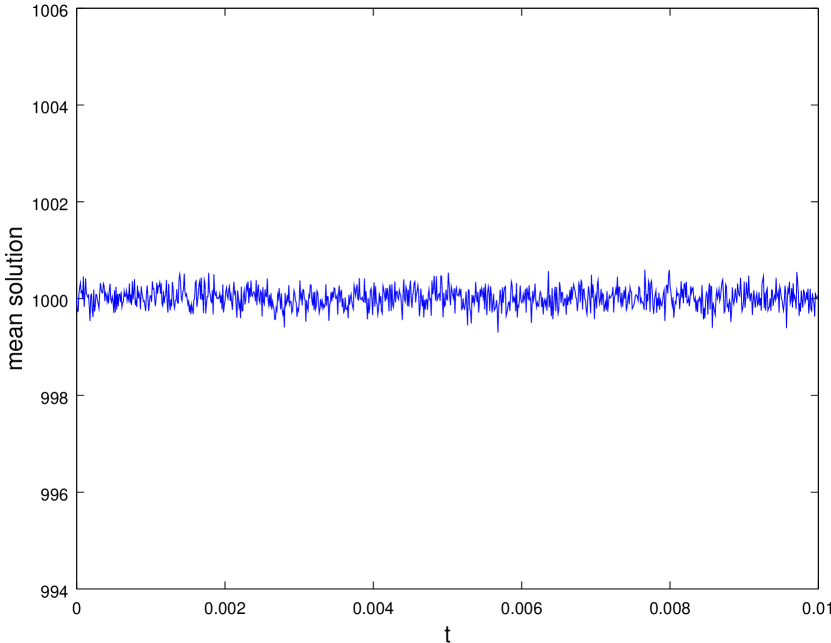

The system in (68) was simulated over the time interval . The tolerance of Newton iterations during the simulation was set to .

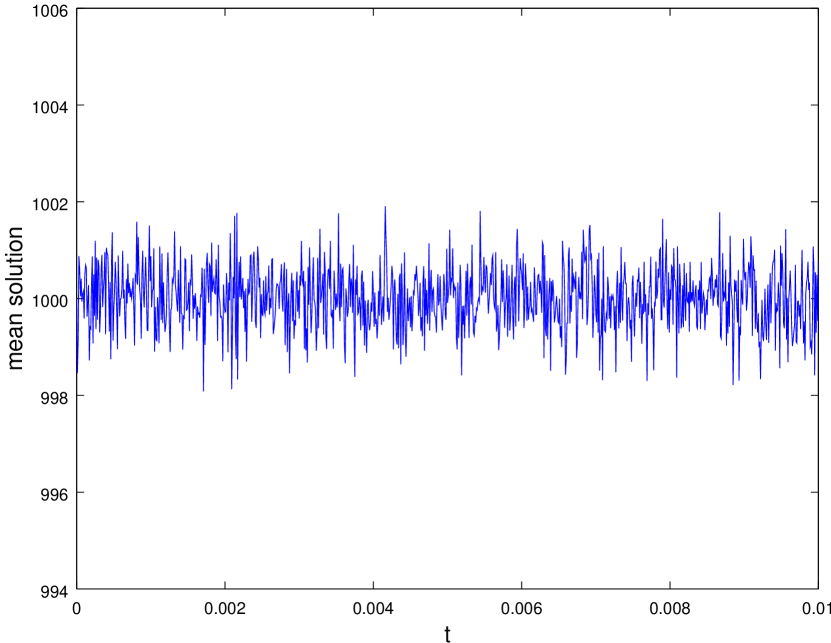

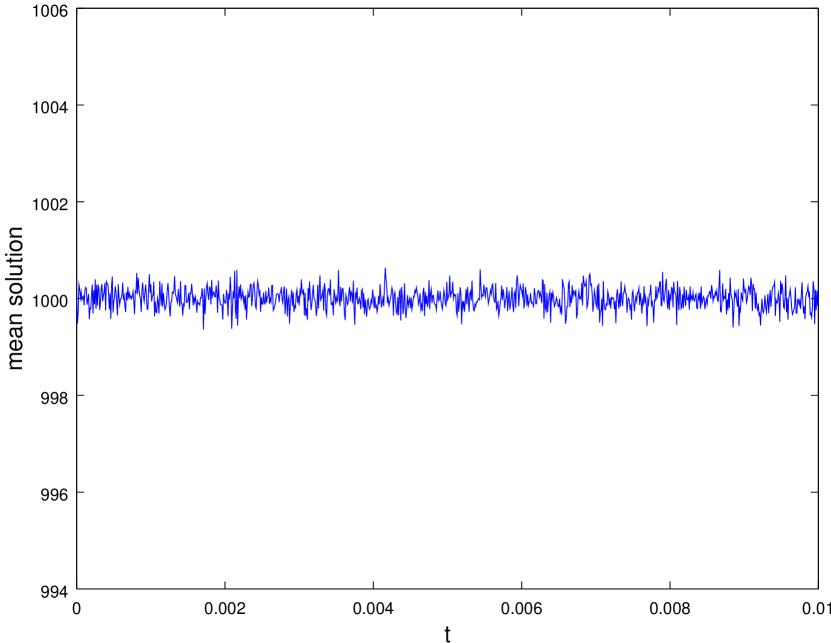

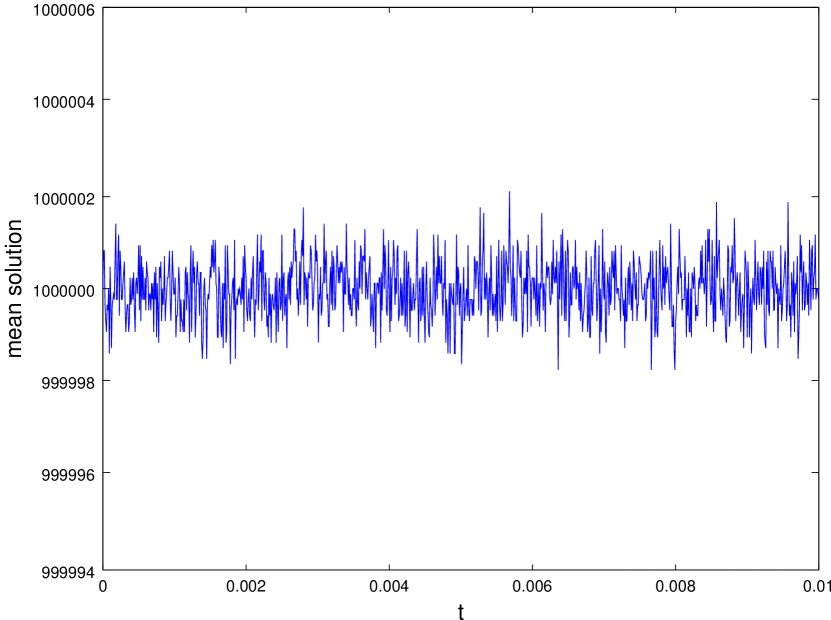

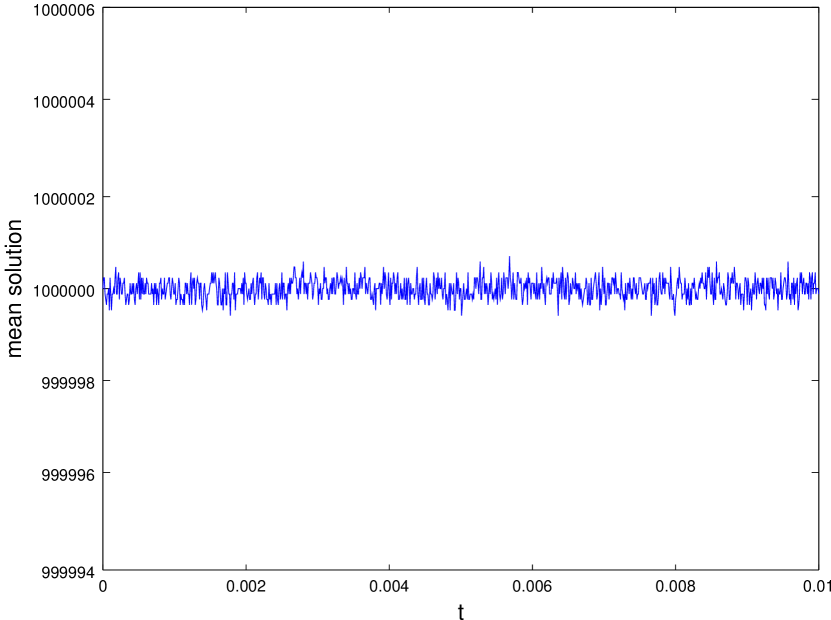

Results of the simulation for different number of sample paths can be seen in Figure 8. We notice that solution oscillates around the initial state of the system which replicates correct behavior of the considered chemical network with given initial state and reaction rate parameters.

The step size has to be chosen carefully since it can destabilize equilibrium of the numerical solution. For instance, for the considered methods it must be smaller than . It has to be noted that the explicit Milstein method cannot generate stable solutions of the system (68) for .

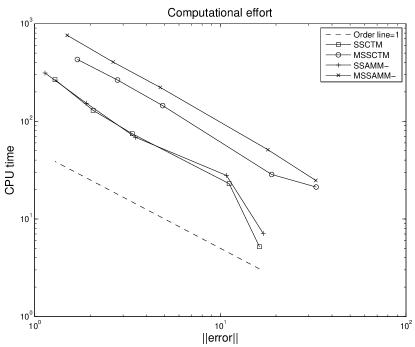

Figure 9 depicts error versus CPU time. It is seen that the computational effort of algorithms grows linearly with respect to the desired tolerance of the solution. Also one can see that modified methods are more expensive than regular methods. Moreover, in the case of the Langevian system in (68) we cannot benefit from the better stability properties of the modified methods because bigger step sizes can destabilize equilibrium of the system.

Additional attention must be paid to positivity preserving of the numerical scheme applied to the system (68) since the number of species cannot be negative. In fact this requirement introduces an even more severe restriction on the time step than it does stiffness. Results reported in [34] show that in order to preserve positivity of the solution using the explicit Milstein scheme time step cannot exceed .

To guarantee positivity of the method we took absolute absolute values in the square roots, which is one of the standard tricks in simulating CLEs. A brief look at the averaged solution (Figure 8) exhibits the acceptability of this approach.

(a)Mean solution for

(b)Mean solution for

(c)Mean solution for

(d)Mean solution for

(e)Mean solution for

(f)Mean solution for

Figure 8: Mean solutions of the equation (68) for (on the left) and (on the right) computed samplesFigure 9: Computational cost of the equation (68)

6 Conclusions.

In this paper, we have investigated split-step Milstein methods for the solution of stiff stochastic differential equations driven by multi-channel noise. We focused on some of the features which are prominent in dealing with systems of SDEs and cannot be captured by scalar stability analysis. The dimension of the noise and geometry of interaction between drift and diffusion components are among the most important factors which influence the numerical stability of stochastic systems. The proposed numerical methods were tested on several problems discussed in the literature, each of these problems has a different nature of stochastic challenges. A linear problem with commutative noise was used as a benchmark for testing the convergence of the methods. From that problem, we also found that the dimension of the noise is a very strong constraint on the stability of the methods. We can make a conjecture that it may be even a stronger constraint on the mean-square stability of the methods than noise geometry.

We have also tested the effectiveness of the methods on a stiff stochastic system of chemical Langevian equations. In addition, we found that for a large number of channels, the computational cost in implementing the modified spit-step methods is higher than the gain in the stability.

7 Acknowledgment.

We appreciate the valuable comments of referees. This helped to improve the quality of the paper.

Appendix A

In the general multi-dimensional case the Milstein scheme takes the form [25]

(69)

Using vector-matrix notation the above expression can be rewritten in more compact and computationally convenient form as

(70)

where are solution and drift vectors respectively, is a diffusion matrix, is an -dimensional vector of Wiener increments and is a product of diffusion matrix and matrix of double stochastic integrals . denotes the -th row of matrix .

In expanded form this reads as

(71)

To derive representation in (71) let take a look at the last term of equation (69)

(72)

If is used to denote the Jacobian matrix of -th row of matrix then the above identity converts to

(73)

Then we obtain

(74)

where denotes the Jacobian matrix of -th column of matrix and is the -th column of matrix .

For efficient calculation of iterated stochastic integrals we refer to [42, 16].

References

Abdulle and Cirilli [2007]

A. Abdulle, S. Cirilli,

Stabilized methods for stiff stochastic systems,

Comptes Rendus Mathematique 345

(2007) 593 – 598.

Abdulle and Cirilli [2008]

A. Abdulle, S. Cirilli,

S-ROCK: Chebyshev methods for stiff stochastic differential

equations, SIAM Journal on Scientific Computing

30 (2008) 997–1014.

Ahmad et al. [2009]

S.S. Ahmad, N.C. Parida,

S. Raha, The fully implicit stochastic

-method for stiff stochastic differential equations,

Journal of Computational Physics 228

(2009) 8263 – 8282.

Allen [2007]

E. Allen, Modeling with Itô Stochastic

Differential Equations, volume 22,

Springer, 2007.

Appleby et al. [2008]

J. Appleby, X. Mao,

A. Rodkina, Stabilization and

destabilization of nonlinear differential equations by noise,

IEEE Transactions on Automatic Control

53 (2008) 683–691.

Arnold [1974]

L. Arnold, Stochastic differential equations:

theory and applications, Wiley-Interscience, New York

(1974).

Buckwar and Berger [2011]

E. Buckwar, S. Berger, A

comparative linear mean-square stability analysis of Maruyama- and

Milstein-type methods, Mathematics and Computers in

Simulation 81 (2011)

1110–1127.

Buckwar and Kelly [2010]

E. Buckwar, C. Kelly,

Towards a systematic linear stability analysis of numerical

methods for systems of stochastic differential equations,

SIAM Journal on Numerical Analysis 48

(2010) 298–321.

Buckwar and Kelly [2012]

E. Buckwar, C. Kelly,

Non-normal drift structures and linear stability analysis of

numerical methods for systems of stochastic differential equations,

Computers & Mathematics with Applications

64 (2012) 2282 – 2293.

Buckwar and Sickenberger [2012]

E. Buckwar, T. Sickenberger,

A structural analysis of asymptotic mean-square stability for

multi-dimensional linear stochastic differential systems,

Applied Numerical Mathematics 62

(2012) 842 – 859.

Buckwar and Winkler [2006]

E. Buckwar, R. Winkler,

Multistep methods for SDEs and their application to

problems with small noise, SIAM Journal on Numerical

Analysis 44 (2006)

779–803.

Ding et al. [2010]

X. Ding, Q. Ma, L. Zhang,

Convergence and stability of the split-step -method

for stochastic differential equations, Computers &

Mathematics with Applications 60 (2010)

1310 – 1321.

El Samad et al. [2005]

H. El Samad, M. Khammash,

L. Petzold, D. Gillespie,

Stochastic modelling of gene regulatory networks,

International Journal of Robust and Nonlinear Control

15 (2005) 691–711.

Gillespie [2000]

D.T. Gillespie, The chemical Langevin

equation, The Journal of Chemical Physics

113 (2000) 297–306.

Gillespie [2007]

D.T. Gillespie, Stochastic simulation of

chemical kinetics, Annual Review of Physical Chemistry

58 (2007) 35–55.

Gilsing and Shardlow [2007]

H. Gilsing, T. Shardlow,

SDElab: A package for solving stochastic differential

equations in MATLAB, Journal of Computational and

Applied Mathematics 205 (2007)

1002 – 1018.

Guo et al. [2014]

Q. Guo, H. Li, Y. Zhu,

The improved split-step methods for stochastic

differential equation, Mathematical Methods in the Applied

Sciences 37 (2014) 2245 –

2256.

Haghighi and Hosseini [2012]

A. Haghighi, S. Hosseini, A

class of split-step balanced methods for stiff stochastic differential

equations, Numerical Algorithms 61

(2012) 141–162.

Hairer et al. [2008]

E. Hairer, S.P. Nørsett,

G. Wanner, Solving Ordinary Differential

Equations I: Nonstiff Problems, Springer-Verlag,

Berlin, 2008.

Hairer and Wanner [1996]

E. Hairer, G. Wanner,

Solving Ordinary Differential Equations II, Stiff and

Differential-Algebraic Systems, Springer-Verlag,

Berlin, 1996.

Higham et al. [2002]

D. Higham, X. Mao,

A. Stuart, Strong convergence of

Euler-type methods for nonlinear stochastic differential equations,

SIAM Journal on Numerical Analysis 40

(2002) 1041–1063.

Higham and Mao [2006]

D.J. Higham, X. Mao,

Nonnormality and stochastic differential equations,

BIT Numerical Mathematics 46

(2006) 525–532.

Huang [2013]

L. Huang, Stochastic stabilization and

destabilization of nonlinear differential equations,

Systems & Control Letters 62

(2013) 163 – 169.

Khasminskii [2012]

R. Khasminskii, Stochastic stability of

differential equations, volume 66,

Springer, 2012.

Kloeden and Platen [1992]

P. Kloeden, E. Platen,

Numerical Solution of Stochastic Differential Equations,

Springer Berlin Heidelberg, 1992.

Laing and Lord [2009]

C. Laing, G.J. Lord,

Stochastic methods in neuroscience,

Oxford University Press, 2009.

Mao [1994]

X. Mao, Stochastic stabilization and

destabilization, Systems & Control Letters

23 (1994) 279 – 290.

Milstein et al. [1998]

G. Milstein, E. Platen,

H. Schurz, Balanced implicit methods for

stiff stochastic systems, SIAM Journal on Numerical

Analysis 35 (1998)

1010–1019.

Omar et al. [2011]

M. Omar, A. Aboul-Hassan,

S. Rabia, The composite Milstein methods

for the numerical solution of Ito stochastic differential equations,

Journal of Computational and Applied Mathematics

235 (2011) 2277 – 2299.

Penski [2000]

C. Penski, A new numerical method for SDEs

and its application in circuit simulation, Journal of

Computational and Applied Mathematics 115

(2000) 461 – 470.

Rößler [2010]

A. Rößler, Strong and weak

approximation methods for stochastic differential equations. some recent

developments, in: L. Devroye,

B. Karasözen, M. Kohler,

R. Korn (Eds.), Recent Developments in

Applied Probability and Statistics, Physica-Verlag HD,

2010, pp. 127–153.

Saito and Mitsui [1996]

Y. Saito, T. Mitsui,

Stability analysis of numerical schemes for stochastic

differential equations, SIAM Journal on Numerical

Analysis 33 (1996)

2254–2267.

Sotiropoulos and Kaznessis [2008]

V. Sotiropoulos, Y.N. Kaznessis,

An adaptive time step scheme for a system of stochastic

differential equations with multiple multiplicative noise: Chemical

Langevin equation, a proof of concept, The Journal of

Chemical Physics 128 (2008).

Stuart and Humphries [1998]

A. Stuart, A.R. Humphries,

Dynamical systems and numerical analysis,

Cambridge University Press, Cambridge, UK,

1998.

Trefethen and Embree [2005]

L.N. Trefethen, M. Embree,

Spectra and pseudospectra: the behavior of nonnormal matrices

and operators, Princeton University Press,

2005.

Voss and Casper [1989]

D. Voss, M. Casper,

Efficient split linear multistep methods for stiff ordinary

differential equations, SIAM Journal on Scientific and

Statistical Computing 10 (1989)

990–999.

Voss and Khaliq [2014]

D.A. Voss, A.Q.M. Khaliq,

Split-step Adams–-Moulton Milstein methods for

systems of stiff stochastic differential equations,

International Journal of Computer Mathematics

(2014) , doi: 10.1080/00207160.2014.915963.

Wang and Han [2009]

P. Wang, Y.C. Han,

Split-step backward Milstein methods for stiff stochastic

systems, Journal of Jilin University (Science Edition)

47 (2009) 1150 – 1154.

Wang and Li [2010]

P. Wang, Y. Li, Split-step

forward methods for stochastic differential equations,

Journal of Computational and Applied Mathematics

233 (2010) 2641 – 2651.

Wang et al. [2012]

X. Wang, S. Gan, D. Wang,

A family of fully implicit Milstein methods for stiff

stochastic differential equations with multiplicative noise,

BIT Numerical Mathematics 52

(2012) 741–772.

Wiktorsson [2001]

M. Wiktorsson, Joint characteristic function

and simultaneous simulation of iterated Ito integrals for multiple

independent Brownian motions, The Annals of Applied

Probability 11 (2001)

470–487.

Wilkinson [2012]

D.J. Wilkinson, Stochastic modelling for

systems biology, volume 44, CRC

press, 2012.