Identifying Multidimensional Adverse Selection Models∗

Abstract.

In this paper, I study the nonparametric identification of a multidimensional adverse selection model.

In particular, I consider the screening model of Rochet and Choné (1998), where products have multiple characteristics and consumers have private information about their multidimensional taste for these characteristics, and determine the data features and additional condition(s) that identify model parameters. The parameters include the nonparametric joint density of consumer taste, the cost function, and the utility function, and the data includes individual-level data on choices and prices paid from one market.

When the utility is nonlinear in product characteristics, however, data from one market is not enough, but with data from at least two markets, or over two periods, with different marginal prices is sufficient for identification as long as these price differences are due to exogenous (and binary) changes in cost and not because the two markets are inherently different.

I also derive all testable conditions for a joint distribution of observed

choices and prices to be rationalized by a model of multidimensional adverse selection.

Keywords: identification, multidimensional adverse selection, rationalizability.

University of Virginia. e-mail: aryalg@virginia.edu

1. Introduction

At least since Akerlof (1970), Spence (1973); and Rothschild and Stiglitz (1976), economists have believed that information asymmetry is a universal phenomenon and that it always results in a significant loss of welfare. This belief has influenced the design of various regulatory policies; see Baron (1989); Joskow and Rose (1989); Laffont and Tirole (1993); and Laffont (1994). However, Chiappori and Salanié (2000) find no evidence of asymmetric information in automobile insurance, and Einav, Finkelstein, and Cullen (2010) estimate the welfare loss due to asymmetric information to be insignificant. One reason for this lack of empirical support for the theory could be that the most widely used theoretical models for asymmetric information assume one-dimensional informational asymmetry, while in reality informational asymmetry is multidimensional and cannot be sorted out in a satisfactory manner according to only one dimension. Ignoring multidimensionality would then lead to incorrect analysis and flawed welfare conclusion(s).111 It is instructive to note that for third-degree price discrimination, the sufficient condition for price discrimination to improve social welfare is known (Varian, 1985). Stiglitz (1977) assumes insurees have private information only about their accident risk, for example, but Finkelstein and McGarry (2006) and Cohen and Einav (2007) have shown that insurers have private information about their risk and risk preferences, and if anything, risk preferences are more likely to be privately known than the risk. Aryal, Perrigne, and Vuong (2015) study the nonparametric identification of insurance markets where insurers have asymmetric information about risk and risk preferences. Most of the literature is focused on insurance and annuities markets; very little is known about other markets where multidimensionality is potentially equally important. In this paper I attempt to contribute to this line of research by studying the identification of a multidimensional adverse selection model, also known as the multidimensional screening model, which lays the foundation for estimating such a model.

In particular, I study an environment where a seller sells a product with multiple characteristics to consumers with heterogeneous taste for each of those characteristics, similar to Lancaster (1971), but where only the consumer is privy to her taste profile. The seller knows only the (market-wide) joint density of the taste profile, and offers a menu of options (product characteristics and prices) to maximize the expected profit. In equilibrium a seller offers a menu of options – a configuration of product characteristics and prices – that maximizes the expected profit, subject to the truth-telling and participation constraints for the consumer. Rochet and Choné (1998) (henceforth, Rochet-Choné) showed that there exists a unique equilibrium, and the (first-order) conditions that characterize the equilibrium provide mappings from the (unobserved) structural parameters to the (observed) choices.

I determine the condition(s) under which I can use data on consumer choices and payments from a single market to nonparametrically identify the joint density of the taste profile, the cost function, and the (common) utility function when product characteristics enter the utility function nonlinearly. Identification is tantamount to showing that the equilibrium mapping implied by Rochet-Choné is invertible. Even though I use the multiple characteristics interpretation, the results can be applied to several other environments, such as a multi-product monopoly and a labor contract for multiple tasks where workers differ in their task-specific skills.

In a sharp contrast with one-dimensional asymmetric information, with multidimensional asymmetric information, bunching (two distinct types of consumers choose the same bundle) is inevitable with possibly very different welfare implications. In equilibrium, the seller partitions the consumers’ types into three categories: the high-types, who are perfectly screened (where each type is offered a unique bundle of qualities); the medium-types, who are further divided into different categories, where all types of the same category are bunched and get the same bundle; and the low-types, who are always excluded or offered the outside option. The identification strategy will depend on whether a type is high-type or medium-type, and since I use both demand and supply-side optimality conditions, I can differentiate which are high-types and which are medium-types. As is pointed out in Subsection 4.1.1, using only the demand side would lead to incorrect estimate of the joint density of consumer types because we would not be able to account for the bunching.222 This problem is moot with one-dimensional consumer heterogeneity with no bunching. Furthermore, using the supply side optimality conditions will be useful to identify general and nonlinear marginal cost function, and not just a constant marginal cost as is typically the case. (It is also important to contrast this with the literature on identification of insurance markets (or insurance-like markets, e.g., annuities) that often use only the demand side. In such markets, the most important cost component are the claims, which are often observed by the econometricians. So supply side is not as important for such markets as it is in this paper.)

I consider these sub-groups sequentially, first when the product characteristics enter the utility function linearly and, then, when they enter nonlinearly. Consider the high-types, who are perfectly screened, which means their incentive compatibility constraints are satisfied, which in turn translates into the restriction that the marginal utility for each characteristic is equal to the marginal price. With linear utility, marginal utility is nothing but the consumers’ type, and the marginal price is the gradient (slope) of the observed price function, which identifies the truncated joint density of high-types. Once we identify the types, I show that we can use the first-order condition that characterizes optimal allocation rule (a map from types to product characteristics) to nonparametrically identify the cost function over an appropriate domain.

This identification strategy does not work for other types because they are bunched. I therefore have to use some other form of exogenous variation. In particular, I show that we can use variation in the observed consumer characteristics. Suppose there are as many consumer characteristics as product characteristics that are independent of the consumer types, then I can identify the truncated joint density of medium-types. The idea behind this strategy is to represent the conditional choice density for a given consumer characteristic as a mixture (Radon transform) of truncated density of consumer types, which is invertible (Helgason, 1999).333 See Gautier and Kitamura (2013) for an application to random coefficient model.

Next, I consider the case when the product characteristics enter the utility function nonlinearly. Then the marginal utility is a product of consumer type and the slope of the nonlinear function. I show that, because of this substitution between the nonlinear function and the type, the model cannot be identified, even for the high-types. I then show that if we have data from either two markets or over two periods where the two markets differ in terms of some exogenous (binary) change in cost, then we can identify the nonlinear utility and the joint density of high-types as long as the cost affects the marginal prices. In particular, if the cost is exogenous and independent of the consumer type then we can compare the multivariate quantiles of choices across these two cost regimes to identify the multivariate quantile (Koltchinskii, 1997) of the high-types. The incentive compatibility constraints for the high-type implies that a median type (among the high-types), say, will choose the median bundle (meant for the high-types) under both costs. Once we have identified the quantiles for the high-types, we can “control” the type and use the consumers’ optimality condition to identify the utility function. This method of matching-quantiles under appropriate exclusion restriction draws insights from Matzkin (2003) and Guerre, Perrigne, and Vuong (2009), and as a result is also related to D’Haultfœuille and Février (2011, 2015) and Torgovitsky (2015).444 See the working paper version D’Haultfœuille and Février (2011). Also see Aryal, Grundl, Kim, and Zhu (2015) for an application to auctions with ambiguity.

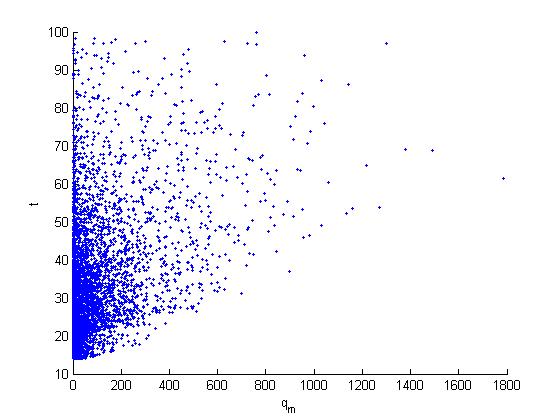

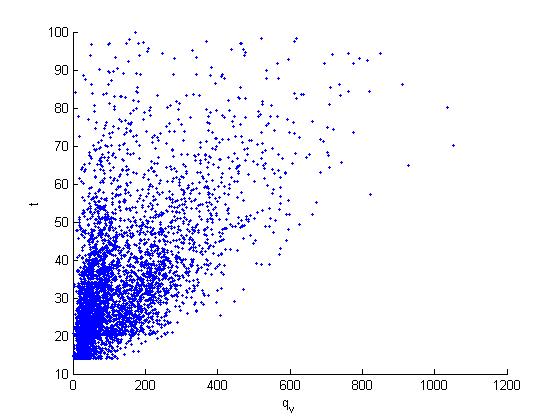

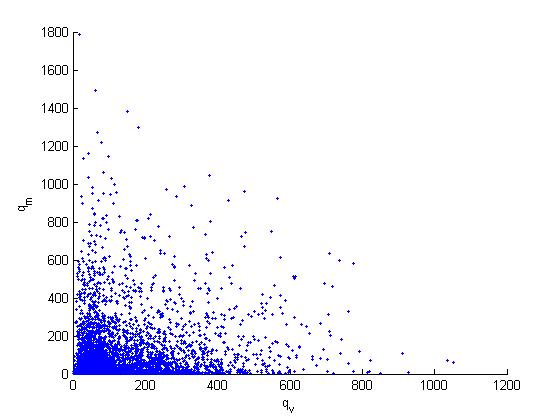

Even though I do not estimate my model, it might be instructive to consider a concrete example of a market where my results would be applicable. Consider the optimal bundling problem faced by a telecommunication company. For example, consider a dominant telecommunication company in a city in China that offers multiple cellphone plans with different rates for talk-time, data, and instant text messaging. For more on this market, see Luo, Perrigne, and Vuong (2012). A scatter plot of the choices and payments are in Figure 1. As can be seen, there is substantial heterogeneity among consumers in terms of their final usage. The payments are not in a ray as a function of either the voice or the messages. Profit for the seller is highest for the plans that are designed for high-type consumers, those who have higher willingness to pay and have higher usage. These high-types, however, cannot be prevented from choosing plans that are meant for the medium-types or the low-types. So a higher profit can only be realized if the seller distorts the product characteristics meant for the latter types in the direction that makes them relatively unattractive for the high-types. But the optimal amount of distortion, and therefore the welfare estimation, depends on the joint density of consumer types. To determine the level of distortion, we have to solve the multidimensional adverse selection (screening) problem, which means that the observed product characteristics or bundles are endogenous. With endogenous product characteristics the approach used in the classic demand estimation, pioneered by Berry (1994); Berry, Levinsohn, and Pakes (1995); and more recently by Berry, Gandhi, and Haile (2013), is inapplicable, not to mention the fact that those models do not allow asymmetric information.555 Fan (2013) considers endogenous product characteristics, but with perfect information.

Next I explore the questions of over identification and rationalizability of the models. Over identification affects both the efficiency of an estimator and the refutability of the model (Koopmans and Riersol, 1950; Romano, 2004). I show that if the truncated joint density of high-types is over identified when the utility is nonlinear and we use data on exogenous consumer characteristics. The logic behind this result is as follows: Since we can identify consumers for every bundle (meant for the high-types), and since this mapping is independent of the consumer characteristics, if the data is generated by the Rochet-Choné equilibrium then it must be the case that this mapping between type and bundle maximizes the correlation between the two for all consumer characteristics. In other words, I ask if there is a way to determine the best way to “transport” the identified types to the observed bundles. The data is an equilibrium outcome if and only if such transport maximizes the correlation between the two, where the correlation is computed with respect to the density of choices and the density of high-types. Such a problem is known as the optimal transport problem and has a long history in economics; see Kantorovich (1960). We know from Brenier (1991) and McCann (1995) that such a mapping exists and is unique, allowing me to conclude that the model is over-identified. I also study the empirical content of the Rochet-Choné model. To that end, I derive all testable conditions for a joint distribution of observed choices and prices to be rationalized by the Rochet-Choné model of multidimensional adverse selection. These conditions can be used in specification tests for model validity, allowing an econometrician to check if multidimensional adverse selection is important, or a model with one-dimension sufficiently rich enough to explain the data.

Pioner (2009) studies the semiparametric identification of the Rochet-Choné model, but he assumes that: a) there is only two dimensions of private information; and b) the econometrician observes one of those types. Between the seller and the econometrician, it is most likely the seller who knows more. These are very strong and restrictive assumptions and my results show neither are necessary. The paper also is related to Perrigne and Vuong (2011) and Gayle and Miller (2014), who study identification of the pure and hybrid moral hazard, respectively; Luo, Perrigne, and Vuong (2012), who study the telecommunication data; Ivaldi and Martimort (1994) and Aryal (2013), who study competitive nonlinear pricing; and Ekeland, Heckman, and Nesheim (2002, 2004); Heckman, Matzkin, and Nesheim (2010); Chernozhukov, Galichon, Henry, and Pass (2014), who study the identification of hedonic models.

The paper is organized as follows. Notations and definitions are in Section 2, Section 3 describes the model, while Section 4 contains the identification results, and Section 5 provides the rationalizability lemmas. Section 6 considers measurement error and unobserved heterogeneity before concluding.

2. Notations and Definitions

I will use the notation to indicate a -dimensional vector with values in the set , and use to denote the boundary values for . If and then denotes the inner product. Let define a dimensional vector of functions

For a scalar function , denotes the gradient of , and denotes the element of the gradient vector. The divergence of a scalar function is defined as

Definition 2.1.

A scalar function is a real analytic function at if there and open ball with such that

One of the properties of analytic functions is that if two real analytic convex functions coincide on an open set, then they coincide on any connected open subset of .

Multivariate Quantiles (Koltchinskii (1997)): Let be a probability space with probability measure . Let be a function such that is integrable function almost everywhere and is strictly convex. Let

be an integral transform of . Let the minimal point of the functional

be called an parameter of with respect to , where is the inner product in . The subdifferential of at a point is denoted by . Since the kernel is strictly convex, is convex and the subdifferential map is well defined. The inverse of this map is the quantile function and is the set of all parameters of . Since is strictly convex, is a single-valued map, and hence we get a unique quantile.666 For example, with one-dimensional case, for any the set of all quantiles of a cdf is exactly the set of all minimal points of .

One can choose any kernel function as long as it satisfies the conditions mentioned above to define a multivariate quantile. Then, from Proposition 2.6 and Corollary 2.9 in Koltchinskii (1997), we know that is a strictly monotone homeomorphism from onto , and for any two probability measures and , the equality implies . For this paper, we choose , so that and

| (1) |

with the inverse as the (unique) quantile function. See Chernozhukov, Galichon, Hallin, and Henry (2015) for an alternative definition.

3. The Model

In this section I will present the model of multidimensional adverse selection of Rochet-Choné. My main goal is to introduce the environment and the conditions that characterize the solution that are essential for identification. I refer readers to the main paper for any missing detail, including the proofs.

A seller offers a menu of options that includes a product line , a set of all feasible characteristics, and a corresponding price function , to consumers who have different tastes for the product characteristics. Let denote this taste profile (or simply type) that is independently and identically distributed (across consumers) as . Let denote the consumer’s observed socioeconomic or demographic characteristics. If a type chooses and pays , let his net utility be given by

Therefore, we assume the utility function is quasilinear in prices. Let be the cost function. The objective of the seller is to choose a (convex) set of product varieties (after suppressing the dependence on ) and a price function that maximizes her expected profit given the cost function and . I begin with the following assumptions:

Assumption 1.

Let

(i) .

(ii) which has a square integrable density a.e. on .

(iii) The net utility be an element of a Sobolev space

with the norm .

(iv) The gross utility function is multiplicative in :

where each is differentiable and strictly increasing, and is either:

(iv-a) linear utility: .

(iv-b) bilinear utility: such that with such that denote those consumer characteristics that interact multiplicatively with the corresponding product characteristics so that for

(iv-c) nonlinear utility: everything is same as the bilinear case, except that where is twice continuously differentiable and strictly quasi concave function, with full rank Jacobian matrix for all and .

(v) is a strongly convex function with parameter , i.e. the minimum eigenvalues of the Hessian matrix is .

Assumption 1-(i) assumes that agents differ in as many dimensions as the attributes of a contract. It means that consumers’ unobserved preference heterogeneity is exactly as rich as the dimension of product characteristics. Assumption 1-(ii)-(iii) are standard assumptions in the literature in mechanism design; for more see Rochet-Choné. Assumption 1-(v) is the standard convexity of cost assumption.

Assumption 1-(iv), however, needs more explanation. The first part of Assumption 1-(iv) assumes that the utility function is multiplicatively separable in consumer type and some function of product characteristics. This multiplicative separability assumption is an important assumption and is widely used in mechanism design literature; see Wilson (1993) and Laffont and Martimort (2001).777 Some exceptions include Carlier (2001) and Figalli, Kim, and McCann (2011). There are typically multiple equilibria, and but it is not unique, but it to argue that at least one solution exists, but the solution is not unique. The second part of the assumption puts more structure on the way the product characteristics enter the utility function (from linear to nonlinear). Assumption 1-(iv-a) assumes that the product characteristics enters linearly and does not depend on consumer characteristics . Assumption 1-(iv-b) assumes that some consumer characteristics might interact with the product characteristics. In particular, it assumes that there are at least as many consumer characteristics as product characteristics, i.e., , such that we can divide the vector into two parts: , a dimensional vector, and , a dimensional vector, depending on whether or not they interact with the product characteristics. The gross utility from a product characteristic is then simply . So, under this specification the product characteristics still enter linearly and are independent of . Assumption 1-(iv-c) generalizes the previous assumption and allows product characteristics to enter the utility function nonlinearly and allows this function to also depend on as long as it is bilinear in and .

It is important to note that for the theoretical model it suffices that the utility function be multiplicatively separable in because we can redefine the units of measurement for the product characteristics and substitute in the place of because the seller observes and knows . Therefore, the only purpose of these three assumptions is from the point of view of an empirical application. Since there is no intrinsic unit of measurement when it comes to the product characteristics, I consider three different cases and study the identification problem for each of them. So, even though assumption 1-(iv-c) allow for the most general functional form, studying the identification of linear and bilinear utility will allow me to isolate the data feature that identifies the model parameter.

For notational ease I will suppress the dependence on until next section. A menu is feasible if there exists an allocation rule that satisfies incentive compatibility (IC) condition,

| (2) |

and individual rationality (IR) condition, . denotes the outside option available to everyone at a fixed price . To ensure the principal’s optimization problem is convex, we assume that , so that the seller will always offer , i.e., . The seller chooses a feasible menu , that maximizes expected profit

| (3) |

where is an indicator function. Let be the social surplus when type is allocated so that

or, equivalently,

Equating these two definitions allows us to express type-specific profit as

Rochet (1987) showed that under Assumption 1, a menu is such that solves Equation (2) (satisfies IC) if and only if (i) and (ii) is convex on . This means that choosing an optimal contract is equivalent to determining the net utility (or the information rent) that each gets by participating. also determines a the corresponding optimal allocation rule as .

Using this result, we can pose the seller’s problem as choosing that maximizes the expected profit

subject to the IC and the IR constraints. As mentioned above, the global IC constraint is equivalent to convexity of , i.e., , and IR is equivalent to for all . Rochet-Choné showed that Assumption 1 is sufficient to guarantee the existence of a unique maximizer . In what follows we will characterize some key properties of the solution.

When there is only one-dimensional asymmetric information (), we can ignore the inequality constraints to find an unconstrained maximizer and verify ex post that these inequality constraints are satisfied. The assumption that the type distribution is regular (the inverse hazard rate is strictly decreasing) was sufficient to guarantee that the constraints were satisfied and equilibrium always had perfect screening. When , however, Rochet-Choné showed that this approach of ex post verification does not work and bunching can never be ruled out. In an important paper, Armstrong (1996) proposes various assumptions that are sufficient to ensure perfect screening. Rochet-Choné has shown that those assumptions are very restrictive and are seldom satisfied. Moreover, it is my opinion that imposing such restrictions to simplify the problem would have been at odds with the nonparametric identification objective of this paper.

One of the key results of Rochet-Choné is that with multidimensional type, the seller will always find it profitable not to perfectly screen consumers and hence bunching (for some subsets of types) was inevitable. And since under bunching two distinct types of consumers choose the same option, it makes identification all that more difficult. In equilibrium the consumers will be divided into three types: the lowest-types who are screened out and offered only , the medium-types who are bunched and offered “medium type” bundles and the high-types who are perfectly screened. The next step is to determine these subsets, which will depend on the model parameters.

If an indirect utility function is optimal then offering any other feasible function , where is non-negative and convex, must lower expected profit for the seller, i.e., . This inequality means the directional derivative of the expected profit, in the direction of , must be nonnegative so is the solution iff: (a) is a convex function and for all convex, non-negative function , ; and (b) with . The Euler-Lagrange condition for the (unconstrained) problem is

| (4) |

Intuitively, measures the marginal loss of the seller when the indirect utility (information rent) of type is increased marginally from to . Alternatively, define , the marginal distortion vector, then is equivalent to , which is the optimal tradeoff between distortion and information rent. Let be the loss of the seller at for the variation . So if the seller increases in the direction of some , then the seller’s marginal loss can be expressed as

| (5) |

where is the Lebesgue measure on the boundary , is an outward normal, and . If we consider those who participate, i.e., , this marginal loss must be zero. Since it means , so that both and must be equal to zero. For those who do not participate, it must mean the loss is positive.

Lemma 1.

Rochet-Choné Proposition 4: The optimal satsifies

| (8) | |||||

| (11) |

The global incentive compatibility condition is important because it determines the optimal bunching in the equilibrium by requiring be convex, and also determines the subset where the optimal allocation rule will be such that some types are allotted the same quantity . Let be the types that gets the same , i.e., . If is convex for all , i.e., if the global incentive compatibility constraint is satisfied, then there is no bunching and would be an empty set. In most of the cases, however, the convexity condition fails and hence there will be non-trivial bunching. So, is affine on all the bunches, and the incentive compatibility constraint is binding for any two types if and only if they both belong to , i.e. if but then .

Theorem 3.1.

Rochet-Choné Theorem 2’: Under Assumptions 1-(i)–(iv-a) and (v) the optimal solution to the problem is characterized by three subsets , and such that:

-

(1)

A positive mass of types do not participate because . This set is characterized by , i.e.,

-

(2)

is a set of “medium types” known as the bunching region, which is further subdivided into subset such that all types in this subset get one type , is affine. restricted to satisfies: and

-

(3)

is the perfect screening region where satisfies the Euler condition , or equivalently , for all , and there is no distortion in the optimal allocation on the boundary, i.e. on .

In summary, the type space is (endogenously) divided into three parts: those who are excluded and get the outside option ; those who are bunched and are allocated some intermediate quality such that all get the same quantity ; and, finally, those who are perfectly screened and are allocated some unique (customized) . An example is shown in Fig. 2. It is also important to note that the allocation rule is continuous.

Corollary 1.

is continuous and .

Proof.

For , since and because it is also continuous. Likewise, for all and hence continuous. Similar arguments show that is continuous for all . ∎

4. Identification

In this section we study the identification of the distribution of types and the cost function from the observables that include the triplet for every consumer. Let . The seller offers to agent with observed characteristics and unobserved type , who then chooses and pays that maximizes the net utility. The seller chooses the menu optimally, which from the revelation principle is equivalent to saying that there exists a direct mechanism, a unique pair of (allocation rule) , and (pricing function) , such that and . Henceforth, will stand for the optimal allocation rule.

Thus assuming that: a) consumers have private information about ; b) the seller only knows the and , and designs a to maximize profit; and c) consumers optimize, leads to the following model:

| (12) |

The model parameters are said to be identified if for any different parameters the implied data distributions are also different, i.e., . Since the equilibrium is unique, there is a unique distribution of the observable for every parameter (Jovanovic, 1989). My objective is to determine some low-level conditions under which the model is globally identified, which is tantamount to showing that Equations in (12) are globally invertible.888 See Rothenberg (1971) and Chen, Chernozhukov, Lee, and Newey (2014) for local identification in parametric and (semi)nonparametric setups, respectively.

Following the equilibrium characterization, I consider the three subsets of types separately. For every let be the set of choices made by consumers with type for , respectively. Since is continuous (Corollary 1), these sets are well defined. In what follows, I will use data from to identify the model parameters restricted to , beginning with the subset . The allocation rule is one-to-one when restricted to , and hence its inverse exists on , but not when restricted to because of bunching, and, as a consequence, the identification strategies are different.999 Since is convex on , the inverse that solves exists (Kachurovksii, 1960). Also see Parthasarathy (1983) and Fujimoto and Herrero (2000) for more details.

In what follows, I suppress the dependence on until it is relevant. Let and be the distribution and density of , respectively. Since the equilibrium indirect utility function is unique, it implies that there is a unique distribution that corresponds to the model structure . Thus the structure is said to be identified if for given there exists a (unique) pair that satisfies Equations (12). Let be the inverse of when restricted on , i.e., . Similarly, let and be the truncated distribution and density of defined, respectively, as:

| (13) |

where is the determinant function. Then the bijection between high-type and high-qualities gives

| (14) |

which will be a key relationship for identification. Before moving on, I introduce new short-hand notations. Let be the CDF restricted to be in the set and let be the set of consumers who buy , for .

4.1. Linear Utility

I begin by showing that without any further restrictions can be identified and can be identified on . When the utility function is linear, consumer optimality for the high-types implies that the marginal utility, which is , is equal to the marginal prices – the gradient of price function. Therefore the type that chooses must satisfy which identifies the (pseudo) type for all . This identification argument uses the demand-side optimality and the price gradients. We lose this identification when either the utility function is nonlinear (Subsection 4.3) or when there are discrete options and we cannot calculate the price gradients (Subsection 6.4).

As restricted to is bijective we can identify the truncated joint distribution of types, or simply the joint distribution of high-types as

Next, I consider identification of the cost function. The equilibrium allocation condition (4) is , or

If we divide both sides by we get

where the second equality follows from Equation (13) and the last equality follows from the definition of the curvature of the pricing function, i.e., . This means the cost function is the solution to the partial differential equation (PDE) with the following boundary condition, on , i.e.,

The cost function is on the convex set identified as the unique solution of this PDE (Evans, 2010). To extend it to the entire domain we need:

Assumption 2.

Cost function is a real analytic function at .

This assumption about being analytic is a technical assumption that assumes is infinitely differentiable and can be expressed (uniquely) as a Taylor series. Hence, it allows for any convex polynomial, trigonometric, and exponential functions. Once the cost function is identified on an open convex set , the analytic extension theorem implies that the function has a unique extension to the entire domain . Since the cost function is completely unspecified, besides convexity, we need to restrict the space of functions to be able to extend it everywhere. Assuming that the cost function is analytic is sufficient. Undoubtedly this is stronger than anything I have assumed thus far, but this assumption has also been used in the literature on nonparametric identification. Newey and Powell (2003) assume that the density belongs to the exponential family, which is analytic (see Liese and Miescke, 2008, Lemma 1.16) and therefore has a unique extension; Fox, il Kim, Ryan, and Bajari (2012) also assume real analyticity to identify a random coefficient logit model; and Fox and Gandhi (2013) assume the utility function is real analytic to identify a random utility model. This result is formalized below.

Theorem 4.1.

It is clear that the monotonicity of is the key to identification, and since we lose monotonicity on we lose identification, as shown in the example below which is taken from Rochet-Choné.

Example 4.1.

Let and the cost function be and types are independent and uniformly distributed on and and . Then, the optimal indirect utility function has different shapes in the three regions: (i) in the non-participation region ; (ii) in the bunching region , depends only on ; and (iii) in the perfect screening region , is strictly convex.

On , which means and on . The boundary that separates and is a linear line , where . On , with . In other words, all consumers with type are treated the same and they get the same . So and on . Sweeping conditions are satisfied if and and on each bunch

which can be used to solve for as Then where is determined by the continuity condition on of , i.e. . Now, define as the inverse of the optimal (bunching) mechanism. Then, identification is to determine the joint cdf of from that of , which is not possible.

To summarize: the seller divides the consumers into three categories and perfectly screens only the top ones. We can then use the distribution of choices made by consumers to determine their types and the cost function. To understand the welfare consequences of asymmetric information, we might also want to understand the heterogeneity in preference of those in the medium categories that are not perfectly screened but are not excluded from the market either. The example above shows that if we restrict the utility function to be linear and independent of the consumer characteristics, then because the bunching is also linear, we cannot identify the types.

4.1.1. Note

This is also a right time to pause and explore the consequence of using only the consumer side optimality condition for identification and ignoring the supply side. To understand the argument it is sufficient to consider discrete types, while keeping aside the problem of identifying the cost function. To that end, let and with probability , respectively. Suppose the optimal allocation is such that is allocated a bundle but the remaining two types are bunched at , and is the pricing function and be the partial derivative with respect to the argument.101010 I am abusing the notation and using partial derivatives to mean inite differences. Suppose the data consists of choice-prices pairs , and let and be the fraction of consumers who choose and , respectively. If we ignore the supply side and only use the demand side, then we will use whenever . We will then conclude that there are only two types of consumer given by with probability , which is not the right parameter.

A natural next step would then be to explore the variation in to identify the model. In particular, I ask: If the utility is also a function of observed characteristics , then can we use the variation in those observed characteristics to identify the medium-types, the types that are bunched? In the following subsection I show that the answer is positive. Under the Assumption 1-(iv-b) that the utility is bilinear, if the observed characteristics are (statistically) independent of the type , and if the dimension of is the same as the dimension of , then we can identify .

4.2. Bilinear Utility

In this subsection I assume that the base utility function satisfies Assumption 1-(iv-b) and is independent of . Recall from assumption 1-(iv) that denotes those characteristics that interact with product characteristics, while do not.

Assumption 3.

Characteristics and are mutually independent.

In particular, suppose that the net utility of choosing by an agent with characteristics and unobserved is

| (15) |

Now, affects the utility, and hence it will also affect the product line and price functions because now they will depend on . However, once we fix the value of (which is observed by the seller) and change the unit of measurement of product quality from to , we can apply Theorem 4.1 to identify . Next, I show that we can also use exogenous variation in to identify the density over the bunching region . So, independent variation in is an important assumption for identification. As will be clear, we will use the notation to make it clear that it is the density of .

In the example above we saw that all agents with type such that selected the same . Now that the agents vary in , agents are bunched according to , in other words, all agents with the same self select , i.e. for all . In other words, acts as a sufficient statistic, and incentive compatibility requires that be monotonic in and hence invertible. So from the observed we can determine the index . Then, the identification problem is to recover from the the joint density of when

Normalize the above equation by multiplying both sides by , which gives

where is an element of a dimensional unit sphere , and .

Then the conditional density of given is

is called the Radon transform (Bracewell, 1990; Helgason, 1999) of . Since the conditional density is identified from , identification of is equivalent to showing that is invertible, for which we need sufficient variation in . For illustration, consider an extreme case where is a vector of constants , then we cannot identify from .

Let denote the Fourier transform of a function , so

are the Fourier transforms of and evaluated at and , for a fixed , respectively. is known from , but is unknown. For identification I use the following property of the Fourier transform of a Randon transform. For a function of two variables , its Fourier transform is , so if we take its projection of on to the axis then we have

For ease of explication, if one slightly abuses the notations and abstracts away from the differences where the functions should be evaluated, one can see that is and is , which means (the unknown) is equal to (the known) , thereby identifying as the Fourier inverse of . The Projection Slice Theorem (Bracewell, 1956) formalizes this intuition and guarantees that for a fixed , , and hence,

Theorem 4.2.

Intuitively, the identification exploits the fact that two consumers with same but different will face different menus and different choices. So if we consider the population with fixed , the variation in the choices must be due to the variation in . But as we change from to , the choices change but variation in remains the same, because . So with continuous variation in , we have infinitely many moment conditions for , which allows us to express the conditional choice density given as a (mixture) Radon transform of the with mixing density being the marginal density of . Hence, even when the equilibrium fails to be bijective, we might be able to use variation in consumer socioeconomic and demographic characteristics for identification. Since the joint density of types in (who were perfectly screened) was identified even without , this result suggests that the model is over identified, which can then be used for specification testing. Even though this intuition is correct, we will postpone the discussion of over identification until the next subsection, when I consider nonlinear utility function. I will show that when utility is nonlinear, and if we have access to a discrete (binary) cost shifter, then to identify the model it is sufficient that the cost shifter causes the gradient of pricing functions to intersect.

Note:

So far I have implicitly assumed that we can divide the observed choices into three subsets. We know the outside option , so the only thing left is to determine the bunching set . As seen in Figure 2, the product line is congruent to one-dimensional , which is the main characteristic of bunching. In a higher dimension, the set will consist of all products that are congruent with the positive real of dimension lower than .

4.3. Nonlinear Utility

In this section I consider the model with nonlinear utility (Assumption 1-(iv-c)), i.e., the (gross) utility function is equal to . To keep the arguments clear, I will ignore , which is tantamount to assuming that , and focus on the identification of on . Once we have understood what variation in the data drives identification, we can introduce and consider the possibility of over-identification.

I begin by first showing that the model cannot be identified because the two optimality conditions Equations (2) and (14) are insufficient. Identification fails because of the substitutability between the type and the curvature of the utility function , as shown below.

Lemma 2.

Under Assumptions 1-(i)–(iv-c) and (v) the model , where the domain of the cost and utility functions are restricted to be and , respectively, are not identified.

Proof.

Since the optimality condition (4) is used to determine the cost function, we can treat the cost function as known. I will suppress the dependence on and let , so . Let the utility function be , and the distribution be and density be . Observed solve the first-order condition

Using the change of variable, the joint (truncated) density of is

Let where with and , be a new model. It is easy to check that solves the first-order condition implied by and the joint (truncated) density of is

∎

As we have seen here, we can increase the type to and decrease the curvature of utility to without changing the observable choices. Therefore, data from only one market is not enough for identification. To that end, let be an exogenous and binary cost shifter that only affects the cost function and is independent of the consumer type and the utility function . For such a shifter to have identification power it must not only change cost but also change the relative prices; however, it is not necessary for us to observe . Such a cost shifter could be either in the form of some exogenous change in law that affects prices over two periods, or different tax or marketing expenses across two independent markets. Either way, as I will show later, it is sufficient for to be binary. This exclusion restriction implies that at different values of the cost shifter: a) the ratio of the types will be equal to the ratio of the slope of the prices at different values of the cost shifter; and b) the (multivariate) quantiles of choices by the high-types are the same.

To see how can help in the identification, consider the non-identification example in Lemma 2. I will use the subscript in to denote the price function and allocation rule when . As in Lemma 2, the utility function is . As before, let us focus only on the high-types and further assume that is also invariant to . Then the demand-side optimality (marginal utility equals the marginal price) can be written as

Solving for for and equating the two gives

i.e., the ratio of types should equal the ratio of marginal prices, or equivalently

| (20) |

Equation (20) captures the fact that a consumer who pays higher marginal price for a when than when must have higher type than . So, if we know s choice when then we can use the curvature of the pricing functions to determine that chooses the same when .

Now, consider the supply side. The allocation rule for the high-types is monotonic (IC constraint), so we know:

where the third equality follows from the monotonicity of and exogeneity of . This relationship is independent of , which gives the following equality

Hence, the (multivariate) quantiles of the choice distribution when are equal to those when

| (21) |

and since is identified, we can identify if we know . Therefore, the difference, , measures the change in when moves from to , while fixing the quantile of at . This variation (21) together with (20) can be used to first identify and then as a (vector valued) function that solves .

The intuition behind identification is as follows: Start with a normalization for some bundle , and determine , the quantile , and from (20).111111 Here, the superscript is an index of the sequence of bundles, and should not be confused with the utility function ; similarly for the superscript on . Using (21), determine with the same quantile under . Then, for determine and , which can determine (inverse of (20)). Then, iterating these steps, we can identify a sequence and the corresponding quantile. If these sequences form a dense subset of then the function is identified everywhere. I formalize this intuition for below, starting with the assumption about exclusion restriction.

Assumption 4.

Let be independent of and .

As before, consumer optimality implies and the general version of Equation (20) can be written as

| (25) | |||||

Next, Assumption 4 and the incentive compatibility condition for high-types imply and hence

| (26) |

Once we determine multivariate quantiles, (26) generalizes (21). Quantiles are the proper inverse of a distribution function, but defining multivariate quantiles is not straightforward because of the lack of a natural order in . One way around this problem is to choose an order (or a rank) function and define the quantiles with respect to that order. I follow the definition of a multivariate quantiles proposed by Koltchinskii (1997); see Section 2. He shows that if we choose a continuously differentiable convex function , then we can define the quantile function as the inverse of some transformation of , denoted as for quantile . For this procedure to make sense, it must be the case that, conditional on the choice of , there is a one-to-one mapping between the quantile function and the joint distribution. In fact, Koltchinskii (1997) shows that for any two distributions and , the corresponding quantile functions are equal, , if and only if . Henceforth, I assume that such a function is chosen and fixed, then (26) and (1) imply

| (27) |

This means we can then use

to identify , for either or . Since for a the probability that is equal to the probability that , i.e., it means

| (28) |

so if we know at some then we can identify at . As mentioned earlier, let us normalize for some so that we know .121212 We can also normalize some quantile of . Then this will allow us to identify where and , which further identifies with and and so on. To complete the identification it must be the case that we can begin with any quantile and identify , possibly by constructing a sequence as above.

To do that we can exploit Assumption 4, which implies that for some the difference measures the resulting change in if we switch from to for a fixed so that we can trace as we move back and forth between and . But for identification it is important that these “tracing” steps come to a halt or, equivalently, for some (fixed point) the mapping . For this it is sufficient that the marginal prices at are equal (). Since this is multidimensional problem, it is also important that the fixed point is attractive (stable), for which it is sufficient that the slope of of all components of (see (25)) depend only on whether or not, irrespective of what is.

Assumption 5.

There exist a such that and is independent of .

Both the components of Assumption 5 are technical assumption, but they are testable, and hence, verifiable from the data. This assumption has been previously used by D’Haultfœuille and Février (2011) to identify a nonseparable model with discrete instrument and multivariate errors.131313 I want to thank Xavier D’Haultfœuille for pointing out the connection zto me. Without loss of generality I assume the initial normalization to be the fixed point , so that is known. In other words, is such that . And from Assumption 4, suppose , whenever . Then, for quantile :

| (29) | |||||

where the first equality is simply the definition, the second equality is the normalization, the third equality follows from (28) with so that , and the fourth equality follows from (25). Repeating this procedure times leads to the seventh equality. The last equality uses the following facts: a) ; b) ; c) is an increasing continuous function so ; and d) . Since the quantile was arbitrary, we identify .

Once the quantile function of is identified, we can identify as before. The optimality condition (Equation (11)) and Equation (13) give

Differentiating with respect to gives

which identifies . Then, substituting in above gives

(a partial differential equation for ), with boundary condition

This PDE has a unique solution , and hence, we have the following result:

To identify the density we can use Theorem 4.2, except now the gross utility function is . Therefore, to account for , we need to be able to extend the utility function from to . For the identification strategy, then, if is a real analytic, like the cost function, then we can extend the domain of to include .

Assumption 6.

Let the utility function be a real analytic function.

4.4. Overidentification

Now that we know identification depends on how many cost shifters we have and whether or not the gradient of the pricing function cross, the next step is analyze the effect of observed characteristics on identification. Before we begin, let us assume that the nonlinear utility model is identified. Then I ask the following question: if the utility function depends on , and is independent of is the model over identified?

Lemma 3.

Consider the optimal allocation rule restricted for high types , where . Suppose and have finite second moments. Then the CDF is over identified.

Proof.

From the previous results and are nonparametrically identified. Since is observed, we can suppress the notation. We want to use the data , the knowledge of , and the truncated distribution to identify . Let be the set of joint distribution with marginals defined as

| (30) |

To that end, consider the following optimization problem:

In other words, given two sets and of equal volume, we want to find the optimal volume-preserving map between them, where optimality is measured against cost function . If the observed were generated under equilibrium, then the solution will map to the right such that , for a fixed . The minimization problem is equivalent to

such that the solution maximizes the (conditional) covariance between and . Either when we minimize the quadratic distance or the covariance, our objective is to find an optimal way to “transport” to . Let be a Dirac measure or a degenerate distribution. Brenier (1991) and McCann (1995) show that that there exists a unique convex function such that is the solution. Therefore for all we can determine its inverse , which identifies . ∎

Therefore we can use to test the validity of the supply-side equilibrium. There are many ways to think of a “specification test.” One way is by verifying that using (instead of ) in Equation (4) leads to the same equilibrium .

5. Model Restrictions

In this section I derive the restrictions imposed by the model on observables under Assumption 1-(iv) –a, b, and c, respectively. These restrictions can be used to test the model validity. For every agent we observe and for the seller we observe . From the model and are given by and . Specifically, suppose a researcher observes a sequence of price and quantity data, and some agents and cost characteristics. Does there exist any possibility to rationalize the data such that the underlying screening model is optimal when the utility function satisfies Assumption 1-(iv-a) (Model 1), Assumption 1-(iv-b) (Model 2), or Assumption 1-(iv-c) (Model 3)? In all three models we ask, in the presence of multidimensional asymmetric information, what are the restrictions on the sequence of data we can test if and only if it is generated by an optimal screening model, without knowing the cost function, the type distribution, and for Model 3 the utility function? We say that a distribution of the observables is rationalized by a model if and only if it satisfies all the restrictions of the model. In other words, a distribution of the observables is rationalized if and only if there is a structure (not necessarily unique) in the model that generates such a distribution.

Let distributed, respectively, as and let

Define the following conditions:

, with density for all .

There is a subset which is a dimensional flat (hyperplane) in .

has non-vanishing gradient and Hessian for all .

Let . Then and let be he density of

Let be the solution of the differential equation

| (31) |

with boundary conditions

5.1. Linear Utility

For every consumer we observe , and the objective is to determine the necessary and sufficient conditions on the joint distribution for it to be rationalized by model .

Lemma 5.1.

If rationalizes then satisfies conditions . Conversely, if and are known and satisfies the then there is a model that generates .

Proof.

If. Since is such that the density everywhere on and the equilibrium allocation rule is onto, and continuous, the CDF is well defined and the density . Moreover, since the equilibrium allocation rule is deterministic, for every there is only one price , hence the Dirac measure, which completes Rochet-Choné shows that in equilibrium the bunching set is nonempty, and hence for all . Moreover, the allocation rule is not bijective, and as a result, as a subset of is flat, which completes . The optimality condition for the types that are perfectly screened is , and incentive compatibility implies the indirect utility function is convex and hence has non-vanishing gradient and Hessian, which completes . Then, , hence . Finally, if we use (13) to replace in with the boundary condition we get .

Only if. Now, we show that if satisfies all conditions listed above then we can determine a model that rationalizes . Let satisfy , then we can determine the cost function . Moreover, it is real analytic so it can be extended uniquely to all . From we can determine the vector , which is also the type , and it satisfies the first-order optimality condition. Thus, the indirect utility of the type that corresponds to the choices is convex and hence satisfies the incentive compatibility constraint. Moreover, since the density and . As far as is concerned, we can simply ignore bunching and define where . ∎

5.2. Bi-Linear Utility

Now I consider the case of bi-linear utility function. Since is redundant information, we can ignore it. The only difference between this and the previous model is now there is . So to save more notations, I slightly abuse notations and use the same conditions , except now they are understood with respect to . For instance, becomes .

Lemma 5.2.

If rationalizes then satisfies conditions . Conversely, if is known, , and satisfies then there is a model that generates .

The proof of this lemma is very similar to that of Lemma 5.2, except in here the menu (allocation and prices) depend on but the cost function and the type CDF do not, and the conditional density can be determined from the data. In view of space I omit the proof.

5.3. Nonlinear Utility

Finally, I consider the case of nonlinear utility.

Before I proceed, I introduce two more conditions.

If is the quantile of then .

The truncated distribution of choices has finite second moment, and for a given (henceforth suppressed) the solution of

where is as defined in (30) is given by a mapping for some convex function such that it solves the optimality condition (4).

So with nonlinear utility, condition replaces condition , and as with the bi-linear utility, the conditions should be interpreted as being conditioned on both and wherever appropriate.

Lemma 5.3.

Let have finite second moment. If rationalizes then satisfies Conversely, if , and a quantile is known, (common support) and satisfies , then there exists a model that rationalizes .

Proof.

If. The CDF is with density everywhere on the support . Moreover, the equilibrium allocation rule is onto and continuous for given . Therefore the CDF is a push forward of given . Since the (truncated) density for all . In equilibrium, for a given the pricing function is deterministic, therefore the distribution is degenerate at , i.e., a Dirac measure. This completes For note that the allocation rule is not bijective, and as a result is a hyperplane. For the high-types, optimality requires the marginal utility is equal to the marginal price , and since has non-vanishing Hessian, also has non-vanishing gradient and Hessian, which completes Since , using Equation (26) gives as desired for The condition follows once we replace and in (31) with and , respectively, and observe that for any pair the equilibrium for high-type is given by . Since is known and is determined, condition follows from Lemma 3.

Only if. We want to show that if satisfies all conditions in the statement, then we can construct a model that rationalizes . For , using condition we can determine two cost functions and . Since (31) is applicable only to , we need to extend the domain of the cost function. Of many ways to extend the domain, the simplest is to assume that the cost is quadratic, i.e., for all . Using the exclusion restriction and (29) for all , we can determine the function along a set for . If the set is a dense subset then there is a unique extension of over all . If not, then, let us linearly extend the function to the entire domain of . Then, define . Finally, to extend the function to , we can assume that each function for all . As far as is concerned, we can simply ignore bunching and define where is such that . Since the probability of and is equal to the probability of and , respectively, we can determine . It is then straightforward to verify that the triplet thus constructed belongs to . ∎

6. Discussion

6.1. Unobserved Taste Shifter

So far I have assumed that consumer’s tastes are completely characterized by a vector . But suppose there is an unobserved market level taste shifter that scales the taste for all consumers, and, as such, is observed by all consumers and the seller but not the econometrician.

Assumption 7.

Let

-

(1)

The random variables are distributed on according to the CDF such that

-

(2)

Let be such that and .

Let denote the types that are perfectly screened. Then, under assumption 7, optimality of these types means , and since we want to identify and from above. Dividing into two parts and reindexing and and taking the log of the above we get

Let be the joint characteristic function of and be the partial derivative of this characteristic function with respect to the first component. Similarly, let and denote characteristic functions of and , which is the shorthand for . Then from Kotlarski (1966):

Then the characteristic function of , which identifies .

Lemma 6.1.

Under Assumption 7, the model with unobserved heterogeneity is identified.

6.2. Measurement Errors

So far, we have assumed that the econometrician observes both the transfers and the contract characteristics without error. Such an assumption could be strong in some environments. Sometimes it is hard to measure the transfers (wages, prices, etc.), and sometimes, it is hard to measure different attributes of contracts. For instance given a monopoly who sells differentiated products, it is possible that some, if not all, of the attributes of the product are measured with error. In this subsection we allow data to be measured with error.

6.2.1. Measurement Error in Prices

I begin by considering the case in which only the transfers are measured with error and subsequently consider the case in which only the contract choices are measured with error. If only the prices are measured with additive error, and if the error is independent of the true price, then the model is still identified. The intuition behind this is simple. When choices are observed without error, but only prices are observed with error, and if this error is additively separable and independent of the true prices, i.e.,

then the observed marginal prices and the true marginal prices are the same, which means the previous identification arguments are still applicable.

Lemma 6.2.

If is observed, where is the price and is the measurement error, then the model parameters are identified.

6.2.2. Measurement Error in Choices

Now consider a case where the choices ’s are observed with error. Furthermore, let’s suppose that there is one (dimensional) error that affects all characteristics. In other words, we envision a situation where there is one for each consumer, and instead of the choice we only measure , where is dimensional vector of ones. Since there is no reason why each component should have a unique measurement error associated with it, having one error unique to each consumer choice seems more natural in this environment. We also assume that and . The data is then pair for every consumer with type . Then implies , which means without correcting for the taste parameter cannot be identified. Following the same logic as Lemma 6.1, we can identify , but that still does not mean we can identify , because we have unknowns and only equation for each consumer.

Lemma 6.3.

If is observed, where is the measurement error then the model cannot be identified.

6.3. Unobserved Product Characteristic

In this section I extend the linear utility model to allow for an unobserved product characteristic. Suppose we observe two bundles and where the former dominates the latter and , with positive demand for both. This pattern suggests that either the model is inappropriate, and hence we can reject the Rochet-Choné model as a good description of the data generating process, or that some product characteristic is missing in the data. Let denote such a characteristic that is observed only by the consumers and the seller, and let be consumer’s taste for this characteristic. The net utility when a (new) type chooses bundle and pays is given by

Introducing can rationalize the above anomaly with and because the consumer is comparing and and not just and , which leads to the following econometrics model:

| (34) |

where are unknown. Since the product characteristics are endogenous, the observed product characteristics are correlated with the unobserved characteristic and hence the model cannot be identified without further restrictions. For example, Bajari and Benkard (2005) allow for one dimensional unobserved product characteristics, as above, but only under the restrictions that: , so all consumers value the missing characteristic the same way; and , so that the missing characteristic is exogenous. As can be seen, both these assumptions are too strong to be useful in the context where the product characteristics are endogenous and consumer preference heterogeneity includes heterogeneity towards the missing characteristics.

6.4. Discrete Options

The identification arguments rely on observing continuous (or a continuum) of many options for the consumers. This is not an assumption I made, but an outcome of the seller ’s maximization problem: the more the seller can discriminate, the better the revenue, as long as it respects incentive compatibility constraints. There can be instances where we observe only discrete (very few) options (Wilson, 1993) but the theory is silent about why a seller would offer fewer (than the optimal number of) options, without imposing arbitrary size restrictions on the consumer type space . If the set is discrete but is continuous, then the identification results do not apply. Without a theory model to rationalize the supply side, I would then have to resort to using some form of exclusion restriction for identification. For instance, it seems safe to conjecture that we can use variation in consumer characteristics to extend Theorem 4.2 to identify and , but not the cost function.

In view of this lacuna in the theory, researchers have started to estimate the loss of payoff from using simpler contracts and find that in some cases the loss is small. For example, Chu, Leslie, and Sorensen (2011) find that the revenue loss of using a two-part tariff instead of a multi-part tariff is small. If the loss of offering simple (or few options) is not too much, but if there is a “menu cost” (for the lack of better term) in offering multiple options, then it stands to reason that offering fewer options could be optimal for the seller. Such menu-cost could be a proxy for the cost of marketing – it is easier and hence cheaper to sell 10 options than 50 options. Although this argument is intuitive, it is not clear how one can make this menu-cost operable in a multidimensional adverse selection environment and achieve point identification. There is so little research in this area that it is not obvious what sort of menu-cost will generate a sharp prediction about the exact number of options in the data.

In the discussion above, finite or discrete options is meant to denote cases where there are indeed very few options. If the seller offers numerous discrete options then we might be able to fit in a continuous function to “fill the gap” and treat the fitted function as if it were a continuous equilibrium outcome and apply the previous results. For example, Aryal (2013) observes more than 200 ad choices and fits a nonlinear tariff function and uses that for identification. Similarly, in the telecommunication market of Figure 1, if we define a product as a bundle of ex-post usage of voice data and SMS then we can make use of heterogeneity in ex-post usage to treat the options as if they were continuous.

The right approach depends on the nature of the market and the data, and whether or not we want to abandon point identification in favor of partial identification. In multi-unit auctions, for example, bidders often submit very few steps, and Kastl (2011), and more recently Cassola, Hortaçsu, and Kastl (2013), posit that it could be because bidders incur an additional cost when submitting a bid having more steps. With bid-submission cost, however, their model can only be partially identified. Studying the failure of point identification of the Rochet-Choné model with cost of offering multiple options is an important and challenging problem and needs a treatment that goes beyond the scope of this paper.

7. Conclusion

In this paper I study the identification of a screening model studied by Rochet and Choné (1998) where consumers have multidimensional private information. I show that if the utility is linear or bi-linear, as is often used in empirical industrial organization literature, then we can use the optimality of both the supply side and the demand side to nonparametrically identify the multidimensional unobserved consumer taste distribution and the cost function of the seller. The key to identification is to exploit equilibrium bijection between the unobserved types and observed choices and the fact that in equilibrium, the consumer will choose a bundle that equates marginal utility to marginal prices. When private information is multidimensional, however, the allocation rule need not be bijective for all types. For those medium-types who are bunched, I show that if we have information about consumers’ socioeconomic and demographic characteristics that are independent of the types, and if there are as many such characteristics as products, the joint density of types can be identified.

When utility is nonlinear, having a binary and exogenous cost shifter is sufficient for identification. I also show that with nonlinear utility if we have independent consumer characteristics then the model is over identified, which can be used to test the validity of supply-side optimality. To the best of my knowledge, this is the first study that provides a way to test optimality of equilibrium in a principal-agent model. Furthermore, I characterize all testable restrictions of the model on the data and extend the identification to consider measurement error and unobserved heterogeneity.

One of the area for future extension would be to allow multiple sellers, for example, the cable television market of Crawford and Yurukoglu (2012) where consumers’ preferences for multiple channels is private information, and as mentioned above, to study the effect of observing discrete options on identification. Much like the problems with discrete options, there are difficulties associated with competition, even with one-dimensional private information; see Epstein and Peters (1999); Martimort and Stole (2002); and Yang and Ye (2008). Laffont, Maskin, and Rochet (1987) propose an aggregation technique that has been used in empirical settings by Ivaldi and Martimort (1994) and Aryal (2013) but can be used only with bi-dimensional types. Another method is to use the generalized Hotelling model (Rochet and Stole, 2002; Bonatti, 2011), which is similar to Bresnahan (1987), if, like Bresnahan (1987), we can find a one-dimensional (hedonic) aggregator of the multidimensional product characteristics.

As far as the estimation is concerned, it is easy to see that the only difficulty arises when the utility function is nonlinear in product quality. When the utility is linear or bi-linear, (nonparametric) estimation is straightforward, as long as one is careful about the asymptotic properties of the estimator, because of multiple steps involved, and bandwidth choice for the Fourier inversion. Having said that, much needs to be done in this field, both in identification and estimation of the nonlinear utility, and my hope is that this paper will provide some useful insights as to how to “take” a seemingly complicated model to data.

References

- (1)

- Akerlof (1970) Akerlof, G. A. (1970): “The Market for “lemons”: Quality uncertainty and the market mechanism,” Quarterly Journal of Economics, 84(3), 488–500.

- Armstrong (1996) Armstrong, M. (1996): “Multiproduct Nonlinear Pricing,” Econometrica, 64, 51–75.

- Aryal (2013) Aryal, G. (2013): “An Empirical Analysis of Competitive Nonlinear Pricing,” Working Paper.

- Aryal, Grundl, Kim, and Zhu (2015) Aryal, G., S. Grundl, D.-H. Kim, and Y. Zhu (2015): “Empirical Relevance of Ambiguity in First Price Auctions,” Working Paper.

- Aryal, Perrigne, and Vuong (2015) Aryal, G., I. Perrigne, and Q. H. Vuong (2015): “Identification of Insurance Models with Multidimensional Screening,” Working Paper.

- Bajari and Benkard (2005) Bajari, P., and C. L. Benkard (2005): “Demand Estimation with Heterogenous Consumers and Unobserved Product Characteristics: A Hedonic Approach,” Journal of Political Economy, 113(6), 1239–1276.

- Baron (1989) Baron, D. (1989): “Design of Regulatory Mechanisms and Institutions,” in Handbook of Industrial Organization, ed. by R. Schlamensee, and R. Willing, vol. II, pp. 1347–1448. Amsterdam-North Holland.

- Berry, Levinsohn, and Pakes (1995) Berry, S., J. Levinsohn, and A. Pakes (1995): “Automobile Prices in Market Equilibrium,” Econometrica, 63(4), 841–890.

- Berry (1994) Berry, S. T. (1994): “Estimation of Discrete-Choice Models of Product Differentiation,” Rand Journal of Economics, 25(2), 242–262.

- Berry, Gandhi, and Haile (2013) Berry, S. T., A. Gandhi, and P. A. Haile (2013): “Connected Substitutes and Invertibility of Demand,” Econometrica, 81(5), 2087–2111.

- Bonatti (2011) Bonatti, A. (2011): “Brand-Specific Tastes for Quality,” International Journal of Industrial Organization, 29(5), 562–575.

- Bracewell (1956) Bracewell, R. N. (1956): “Strip Integration in Radio Astronomy,” Australian Journal of Physics, 9(4), 198–217.

- Bracewell (1990) (1990): “Numerical Transforms,” Science, 248, 697–704.

- Brenier (1991) Brenier, Y. (1991): “Polar Factorization and Monotone Rearrangement of Vector-Valued Functions,” Communication on Pure and Applied Mathematics, 44, 375–417.

- Bresnahan (1987) Bresnahan, T. F. (1987): “Competition and Collusion in the American Automobile Industry: The 1955 Price War,” The Journal of Industrial Economics, 35(4), 457–482.

- Carlier (2001) Carlier, G. (2001): “A General Existence Result for the Principal-Agent Problem with Adverse Selection,” Journal of Mathematical Economics, 35, 129–150.

- Cassola, Hortaçsu, and Kastl (2013) Cassola, N., A. Hortaçsu, and J. Kastl (2013): “The 2007 Subprime Market Crisis Through the Lens of European Central Bank Auctions for Short-Term Funds,” Econometrica, 81(4), 1309–45.

- Chen, Chernozhukov, Lee, and Newey (2014) Chen, X., V. Chernozhukov, S. Lee, and W. K. Newey (2014): “Local Identification of Nonparametric and Semiparametric Models,” Econometrica, 82(2), 785–809.

- Chernozhukov, Galichon, Hallin, and Henry (2015) Chernozhukov, V., A. Galichon, M. Hallin, and M. Henry (2015): “Monge-Kantororvich Depth, Quantiles, Ranks, and Signs,” Working paper.

- Chernozhukov, Galichon, Henry, and Pass (2014) Chernozhukov, V., A. Galichon, M. Henry, and B. Pass (2014): “Single Market Nonparametric Identification of Multi-Attribute Hedonic Equilibrium Models,” Working paper.

- Chiappori and Salanié (2000) Chiappori, P.-A., and B. Salanié (2000): “Testing for Asymmetric Information in Insurance Markets,” Journal of Political Economy, 108(1), 56–78.

- Chu, Leslie, and Sorensen (2011) Chu, S., P. Leslie, and A. Sorensen (2011): “Bundle-Size Pricing as an Approximation to Mixed Bundling,” American Economic Review, 101(1), 263–303.

- Cohen and Einav (2007) Cohen, A., and L. Einav (2007): “Estimating Risk Preferences from Deductible Choices,” American Economic Reveiw, 97(3), 745–788.

- Crawford and Yurukoglu (2012) Crawford, G. S., and A. Yurukoglu (2012): “The Welfare Effects of Bundling in Multichannel Television Markets,” American Economic Review, 102, 301–317.

- D’Haultfœuille and Février (2011) D’Haultfœuille, X., and P. Février (2011): “Identification of Nonseprarable Triangular Models with Discrete Instruments,” CREST Working Paper.

- D’Haultfœuille and Février (2015) (2015): “Identification of Nonseprarable Triangular Models with Discrete Instruments,” Econometrica, 83(3), 1199–1210.

- Einav, Finkelstein, and Cullen (2010) Einav, L., A. Finkelstein, and M. R. Cullen (2010): “Estimating Welfare in Insurance Markets using Variation in Prices,” Quarterly Journal of Economics, 125(3), 877–921.

- Ekeland, Heckman, and Nesheim (2002) Ekeland, I., J. Heckman, and L. Nesheim (2002): “Identifying Hedonic Models,” American Economic Reveiw, 92(2), 304–309.

- Ekeland, Heckman, and Nesheim (2004) (2004): “Identification and Estimation of Hedonic Models,” Journal of Political Economy, 112, 60–109.

- Epstein and Peters (1999) Epstein, L. G., and M. Peters (1999): “A Revelation Principle for Competing Mechanisms,” Journal of Economic Theory, 88, 119–160.

- Evans (2010) Evans, L. C. (2010): Partial Differential Equations. AMS, second edn.

- Fan (2013) Fan, Y. (2013): “Ownership Consolidation and Product Characteristics: A Study of the US Daily Newspaper Market,” American Economic Reveiw, 103(5), 1598–1628.

- Figalli, Kim, and McCann (2011) Figalli, A., Y.-H. Kim, and R. J. McCann (2011): “When is Multidimensional Screening a Convex Program?,” Journal of Economic Theory, 146, 454–478.

- Finkelstein and McGarry (2006) Finkelstein, A., and K. McGarry (2006): “Multiple dimensions of private information: Evidence from the long-term care insurance market,” American Economic Reveiw, 96(4), 938–958.

- Fox and Gandhi (2013) Fox, J. T., and A. Gandhi (2013): “Nonparametric Identification and Estimation of Random Coefficients in Multinomial Choice Models,” Mimeo.

- Fox, il Kim, Ryan, and Bajari (2012) Fox, J. T., K. il Kim, S. P. Ryan, and P. Bajari (2012): “The Random Coefficients Logit Model is Identified,” Journal of Econometrics, 166, 204–212.

- Fujimoto and Herrero (2000) Fujimoto, T., and C. Herrero (2000): “A Univalence Theorem for Nonlinear Mappings: An Elementary Approach,” Okayama Economic Review, 31(4), 277–283.

- Gautier and Kitamura (2013) Gautier, E., and Y. Kitamura (2013): “Nonparametric Estimation in Random Coefficients Binary Choice Models,” Econometrica, 81(2), 581–607.

- Gayle and Miller (2014) Gayle, G.-L., and R. A. Miller (2014): “Identifying and Testing Models of Managerial Compensation,” Review of Economic Studies, forthcoming.

- Guerre, Perrigne, and Vuong (2009) Guerre, E., I. Perrigne, and Q. Vuong (2009): “Nonparametric Identification of Risk Aversion in First-Price Auctions Under Exclusion Restrictions,” Econometrica, 77(4), 1193–1227.

- Heckman, Matzkin, and Nesheim (2010) Heckman, J., R. L. Matzkin, and L. Nesheim (2010): “Nonparametric Identification and Estimation of Nonadditive Hedonic Models,” Econometrica, 78(5), 1569–1591.

- Helgason (1999) Helgason, S. (1999): The Radon Transform. Birkhauser Boston, 2nd edn.

- Ivaldi and Martimort (1994) Ivaldi, M., and D. Martimort (1994): “Competition under Nonlinear Pricing,” Annales d’Économie et de Statistique, 34, 71–114.