Valuation of Variable Annuities with Guaranteed Minimum Withdrawal and Death Benefits via Stochastic Control Optimization

Abstract

In this paper we present a numerical valuation of variable annuities with combined Guaranteed Minimum Withdrawal Benefit (GMWB) and Guaranteed Minimum Death Benefit (GMDB) under optimal policyholder behavior solved as an optimal stochastic control problem. This product simultaneously deals with financial risk, mortality risk and human behavior. We assume that market is complete in financial risk and mortality risk is completely diversified by selling enough policies and thus the annuity price can be expressed as appropriate expectation. The computing engine employed to solve the optimal stochastic control problem is based on a robust and efficient Gauss-Hermite quadrature method with cubic spline. We present results for three different types of death benefit and show that, under the optimal policyholder behavior, adding the premium for the death benefit on top of the GMWB can be problematic for contracts with long maturities if the continuous fee structure is kept, which is ordinarily assumed for a GMWB contract. In fact for some long maturities it can be shown that the fee cannot be charged as any proportion of the account value – there is no solution to match the initial premium with the fair annuity price. On the other hand, the extra fee due to adding the death benefit can be charged upfront or in periodic instalment of fixed amount, and it is cheaper than buying a separate life insurance.

Keywords: Variable Annuity, Optimal Stochastic Control, Guaranteed Minimum Withdrawal Benefit, Guaranteed Minimum Death Benefit, Mortality Risk

1 The Commonwealth Scientific and Industrial Research Organisation, Australia; e-mail: Xiaolin.Luo@csiro.au

2 The Commonwealth Scientific and Industrial Research Organisation, Australia;

e-mail: Pavel.Shevchenko@csiro.au

∗ Corresponding author

1 Introduction

A variable annuity is a fund-linked insurance contract including a variety of financial options on the policy account value; see e.g. Smith, (1982) and Walden, (1985). A recent description of the main features of variable annuity products and the development of their market can be found in Ledlie et al., (2008) and Kalberer2009. The main features of variable annuities are represented by a variety of possible guarantees, which are briefly referred to as GMxB - Guaranteed Minimum ‘x’ Benefit, where ‘x’ stands for accumulation (A), death (D), income (I) or withdrawal (W). All GMxBs provide a protection of the policyholder’s account: GMAB during the accumulation phase and GMDB in case of early death, GMIB and GMWB after retirement, in particular in the face of high longevity. In this study we focus on Guaranteed Minimum Withdrawal Benefit (GMWB) in combination with Guaranteed Minimum Death Benefit (GMDB), overall referred to as GMWDB.

A variable annuity contract with GMWB promises to return the entire initial investment through cash withdrawals during the policy life plus the remaining account balance at maturity, regardless of the portfolio performance. Thus even if the account of the policyholder falls to zero before maturity, GMWB feature will continue to provide the guaranteed cashflows. GMWB allows the policyholder to withdraw funds below or at contractual rate without penalty and above the contractual rate with some penalty. If the policyholder behaves passively and the withdrawal amount at each withdrawal date is predetermined at the beginning of the contract, then the behavior of the policyholder is called static. In this case the paths of the account can be simulated and a standard Monte Carlo simulation method can be used to price the GMWB, though in low dimension problems partial differential equation (PDE) or integration methods are more efficient. On the other hand if the policyholder optimally decide the amount of withdrawal at each withdrawal date, then the behavior of the policyholder is called dynamic. A rational policyholder of GMWB will always choose the optimal withdrawal strategy to maximize the present value of cashflows generated from holding GMWB. Under the optimal withdrawal strategy of a policyholder, the pricing of variable annuities with GMWB becomes an optimal stochastic control problem. There is a rich literature on dynamic programming to deal with optimal stochastic control problems in general, for textbook treatment see e.g. Powell, (2011); Bäuerle & Rieder, (2011). This problem cannot be solved by a simulation based method such as the well known Least-Squares Monte Carlo method introduced in Longstaff & Schwartz, (2001), due to the fact that the paths of the underlying variable are altered by the optimal withdrawal amounts at all pay dates prior to maturity and thus they cannot be simulated. The variable annuities with GMWB feature have been considered in e.g. Milevsky & Salisbury, (2006), Bauer et al., (2008), Dai et al., (2008), Chen & Forsyth, (2008), Bacinello et al., (2011) and Luo & Shevchenko, (2014b).

In the case of a variable annuity contract with Guaranteed Minimum Death Benefit, the beneficiaries obtain a death benefit if the insured dies during the deferment period. When variable annuities were introduced, a very simple form of death benefit was predominant in the market. Since the mid 1990s, insurers started to offer a broad variety of death benefit designs. The basic form of a death benefit is the so-called Return of Premium Death Benefit. Here, the maximum of the current account value at time of death and the single premium is paid. Generally speaking, given a mortality model or a Life Table, the evaluation of GMDB is straightforward - a standard Monte Carlo method will work fine for such a problem and often closed form solutions can be obtained.

The pricing of GMWB is more involved, and it is even more challenging under the dynamic (optimal) policyholder behavior. Milevsky & Salisbury, (2006) developed a variety of methods for pricing GMWB products. In their static approach the GMWB product is decomposed into a Quanto Asian put plus a generic term-certain annuity. In their dynamic approach they assume the policyholder can terminate (surrender) the contract at the optimal time, which leads to an optimal stopping problem akin to pricing an American put option. Bauer et al., (2008) presents valuation framework of variable annuities with multiple guarantees. In their dynamic approach a strategy consists of a numerous possible withdrawal amounts at each payment date. They have developed a multidimensional discretization approach in which the Black-Scholes PDE is transformed to a one-dimensional heat equation and a quasi-analytic solution is obtained through a simple piecewise summation with a linear interpolation on a mesh. Unfortunately the numerical formulation considered in Bauer et al., (2008) has four dimensions and the computation of even a single price of the GMWB contract under the optimal policyholder strategy is very costly. It is mentioned in their paper that it took between 15 and 40 hours on the standard desktop PC to obtain a single price and no results for the dynamic case were shown; also it looks like their methodology in the case of death benefit with dynamic GMWB corresponds to the upper estimator of the price (i.e. corresponds to formula (22) in the next section). Dai et al., (2008) developed an efficient finite difference algorithm using the penalty approximation to solve the singular stochastic control problem for a continuous withdrawal model under the dynamic withdrawal strategy. They have also developed a finite difference algorithm for the more realistic discrete withdrawal formulation. Chen & Forsyth, (2008) present an impulse stochastic control formulation for pricing variable annuities with GMWB under the optimal policyholder behavior, and develop a single numerical scheme for solving the Hamilton-Jacobi-Bellman variational inequality for the continuous withdrawal model as well as for pricing the discrete withdrawal contracts. In Bacinello et al., (2011) the static valuations are performed via ordinary Monte Carlo method, and the mixed valuations, where the policyholder is ‘semiactive’ and can decide to surrender the contract at any time during the life of the GMWB contract, are performed by the Least Squares Monte Carlo method.

Recently we have developed a very efficient new algorithm for pricing variable annuities with GMWB under both static and dynamic policyholder behaviors solving an equivalent stochastic control problem; see Luo & Shevchenko, (2014b). Here the definition of “dynamic” is similar to the one used by Bauer et al., (2008), Dai et al., (2008) and Chen & Forsyth, (2008), i.e. the rational policyholder can decide an optimal amount to withdraw at each payment date (based on information available at this date) to maximize the expected discounted value of the cashflows generated from holding the variable annuity with GMWB. The algorithm is neither based on solving PDEs using finite difference nor on simulations using Monte Carlo. It relies on computing the expected option values in a backward time-stepping between withdrawal dates through Gauss-Hermite integration quadrature applied on a cubic spline interpolation (referred to as GHQC). In Luo & Shevchenko, (2014b) it is demonstrated that in pricing GMWB under the optimal policyholder behavior the GHQC algorithm can achieve similar accuracy as the finite difference method, but it is significantly faster because it requires less number of steps in time. This method can be applied when transition density of the underlying asset between withdrawal dates or it’s moments are known in closed form and required expectations are 1d integrals. It has also been successfully used to price exotic options such as American, Asian, barrier, etc; see Luo & Shevchenko, (2014a).

So far in the literature GMWB and GMDB are mainly considered as two separate contracts and it is implicitly assumed the policyholder of a GMWB contract will always live beyond the maturity date or there is always someone there to make optimal withdrawal decisions for the entire duration of the contract. In reality an elderly policyholder may die before maturity date, especially for a contract with a long maturity. For example, according to the Australian Life Table, Table 6, a male aged 60 will have more than probability to die before the age of 85. So, for a 60 year old male taking up a GMWB contract with a maturity of 25 years; the product design and pricing should certainly consider the probability of death during the contract. Some variable annuity products may have expiry for the death benefit guarantee, e.g. at the age 70 or 75.

In this paper we formulate pricing GMWDB (GMWB combined with GMDB) as a stochastic control problem, where at each withdrawal date the policyholder optimally decides the withdrawal amount based on information available at this date. It is important to note that pricing dynamic GMWDB for a given death time (i.e. conditional on knowing death time) and then averaging over possible death times according to death probabilities will lead to higher price than dynamic GMWDB where decisions are based on information available at withdrawal date (this will be discussed in the next section). We first extend the standard GMWB to allow for termination of the contract due to mortality risk, returning the maximum of the remaining guarantee withdrawal amount and the portfolio account value upon death. In addition, two types of extra death benefits are considered: paying the initial premium or paying the maximum of the initial premium and the portfolio account value upon death. Our recently developed GHQC algorithm in Luo & Shevchenko, (2014b) enables us to perform a comprehensive numerical study on the evaluation of GMWDB.

In the next section we describe the GMWDB product with extra death benefits on top of the usual GMWB features and outline the underlying stochastic model and corresponding optimal stochastic control problem. Section 3 presents the numerical method and algorithm for pricing GMWDB under both static and dynamic policyholder behaviors. In Section 4 we present numerical results for the fair fees of GMWDB under a series of contract conditions. For the case of GMWDB under the optimal policyholder strategy, the inadequacy of the traditional fee structure is revealed in the case of additional death benefit. The fee cannot be charged as any proportion of the account value – there is no solution to match the initial premium with the fair annuity price. An explanation of the inadequacy is given through an example which demonstrates why there is no solution for the fair fee for some long maturities if the death benefit paying at least the initial premium is guaranteed to a rational policyholder. On the other hand, if a fixed upfront fee or periodic instalment is charged, the extra fee of adding life insurance to GMWB is cheaper than holding a separate life insurance. Concluding remarks are given in Section 5.

2 Model and Stochastic Control Formulation

A variable annuity contract with guaranteed minimum withdrawal benefit and death benefit (GMWDB) promises to return the entire initial investment through cash withdrawals during the policy life plus the remaining account balance at the contract maturity , regardless of the portfolio performance. In addition, if policyholder dies before or at the contract maturity, then death benefit is paid to the beneficiaries. We assume (common assumption in the academic research literature on pricing variables annuities) that market is complete in financial risk and mortality risk is completely diversified through selling enough policies and thus the annuity price can be expressed as expectation with respect to appropriate (risk-neutral) probability measure for the risky asset. Below we outline the contract setup, model assumptions and solution via optimal stochastic control method.

2.1 Assumptions and GMWDB contract details

Assume that the annuity policyholder is allowed to take withdrawals at times . The premium paid upfront is invested into risky asset . Denote the value of corresponding wealth account at time as , i.e. upfront premium is . GMWB is the guarantee of the return of the premium via withdrawals allowed at times , . Let denote the number of withdrawals in a year (e.g. for a monthly withdrawal), then the total number of withdrawals , where denotes the ceiling of a float number. The withdrawals cannot exceed the guarantee balance and withdrawals can be different from contractual (guaranteed) withdrawal amount with penalties imposed if . Also denote the annual contractual rate as . Consider the following annuity contract details and model assumptions.

-

•

Risky asset process. Let denote the value of the reference portfolio of assets (mutual fund index, etc.) underlying the variable annuity policy at time that follows the risk neutral process

(1) where is the standard Wiener process, is risk free interest rate and is volatility. Hereafter we assume that the model parameters are piecewise constant functions of time for time discretization , where is today and is annuity contract maturity. Denote corresponding asset values as and risk free interest rate and volatility as and respectively. That is, is the volatility for ; is the volatility for , etc. and similarly for interest rate.

-

•

Wealth account. For clarity, denote the value of the wealth account at time before withdrawal as and after withdrawal as . Then, for the risky asset process (1), the value of wealth account evolves as

(2) (3) where , are independent and identically distributed standard Normal random variables, and is annual fee charged by insurance company. If the wealth account balance becomes zero or negative, then it will stay zero till maturity. For the process (2), the transition density from to is lognormal density, i.e. is from Normal distribution with the mean and variance .

-

•

Guarantee account. Denote the value of guarantee account at time as with , and the value of the account at before withdrawal as and after withdrawal as . The guarantee account evolves as

(4) with and and . Also note that guarantee account is unchanged within , i.e. .

Some real products include “step-up” arrangement that will increase guarantee account balance to on anniversary dates, i.e. in the case of good investment performance. For simplicity we do not consider this feature explicitly but it is not difficult to incorporate this into the algorithm presented in this paper.

-

•

Penalty. The cashflow received by the policyholder at if alive is given by

(5) where is contractual withdrawal amount. That is, penalty is applied if withdrawal exceeds contractual amount , i.e. is the penalty applied to the portion of withdrawal above .

To discourage excessive withdrawals beyond , some contracts may include reset provision on the guarantee level if . We do not consider this explicitly but it is not a problem to incorporate this feature in the pricing algorithm presented in this paper.

-

•

Death process. Denote the time of policyholder death, a random variable, as with conditional death probabilities . It is assumed that death time and asset process are independent. The policyholder age at is needed to find these probabilities from Life Tables. We assume that these probabilities are known and to simplify notation we do not use policyholder age variable explicitly in the formulas. In our numerical examples we assume age 60 for male and female policyholders and use the current Australian Life Table, see Table 6. Consider the corresponding Markov process defined by discrete random variables at

(6) with transition density from at to at specified by probabilities

For example, if death time is between and , then realization of the process for is . Note that this variable is not affected by withdrawal at .

-

•

Death benefit. If death time is after contract maturity , then at the maturity the policyholder takes the maximum between the remaining guarantee withdrawal net of penalty charge and the remaining balance of the personal account, i.e. the final payoff is

(7) If death time occurs before or at contract maturity then the payoff taken by the beneficiary at death time slice (the first time slice larger or equal ) is the death benefit . We consider three types of death benefit denoted as DB0, DB1 and DB2 as follows:

(8) In the above, initial premium is sometimes adjusted for inflation which is a trivial extension.

In some policies the death benefit may change at some age, for example DB2 or DB1 may change to DB0 at the age of 75 years (effectively making the death benefit guarantee expiring at the specified age). If death benefit expiring corresponds to switching to the standard GMWB, then it can be handled by setting death probabilities to zero after death benefit expiry till the contract maturity.

-

•

Payoff. Given withdrawal strategy , the present value of the overall payoff of the annuity contract is a function of state variables corresponding to wealth account , guarantee account and death state . Denote the state vector at time before the withdrawal as and . Then the annuity payoff is

(9) where

(10) is the cashflow at the contract maturity and

(11) is the cashflow at time . Here, is indicator function equals 1 if condition in is true and zero otherwise, and is discounting factor from to

(12) -

•

GMWDB static case. Given the above assumptions and definitions the annuity price under the given static strategy can be calculated as

(13) where denotes expectation with respect to process conditional on information available at time . In the case of static strategy, is deterministic and thus expectation is with respect to and processes.

-

•

GMWDB dynamic case. Under the optimal dynamic strategy the annuity price is

(14) where is a function of state variable at time , i.e. can be different for different realizations of . Note that in this case, process is stochastic via stochasticity in .

-

•

GMWB case. The standard GMWB contract corresponds to the above payoff for GMWDB if death probabilities are set to zero, , i.e. and in GMWDB payoff given in (9) simplify to and . Then static and dynamic GMWB prices are given by (13) and (14) respectively where expectations are calculated with respect to process.

2.2 Solving Optimal Stochastic Control Problem

Given that state variable is Markov process, it is easy to recognize that the annuity valuation under the optimal withdrawal strategy (14) is optimal stochastic control problem for Markov process that can be solved recursively to find annuity value at , via backward induction

| (15) |

starting from final condition . Here is the stochastic kernel representing probability to reach state in at time if the withdrawal (action) is applied in the state at time . For a good textbook treatment of stochastic control problem in finance, see Bäuerle & Rieder, (2011).

Explicitly, this backward recursion can be rewritten as

for starting from maturity condition at

| (16) |

where for clarity we denote and the annuity values at time before and after withdrawal respectively. Taking expectation with respect to death variable and using and , it simplifies to the recursion equations

with jump condition

| (18) |

and maturity condition

| (19) |

Note that expectations in (2.2) are with respect to only because .

2.3 Dynamic GMWDB Upper and Lower Estimators

There are many lower estimators that can be constructed for dynamic GMWDB price given by (14). In particular, any static (deterministic) strategy will produce lower estimator given by equation (13). In Section 4 we will utilize one of such lower estimators.

One of the possible upper estimators of the dynamic GMWDB (14) can be found via calculations of GMWDB conditional on death time (i.e. perfect forecast of the death time). For easier understanding and notational convenience, instead of dealing with the death process in the following we consider the corresponding death time random variable and let be the first withdrawal time equal or exceeding and (if then without loss of generality set ). To avoid confusion, we denote this GMWDB conditional on by . Conditional on (i.e. conditional on ), it is given by

| (20) |

where is expectation with respect to wealth process . It can be solved using backward recursion

for starting from maturity condition at

| (21) |

Then the expectation with respect to death time gives

| (22) | |||||

Note that corresponds to the standard GMWB (i.e. GMWDB conditional on death after contract maturity). Also note that the death probabilities are different from conditional death probabilities in the death process (6); both and are easily found from Life Tables or mortality process models. is the upper estimator for dynamic GMWDB , given by (14), because it is based on optimal strategy conditional on perfect forecast for time of death for each death process realization. Formally,

| (23) |

3 Numerical algorithm

In the literature, the optimal stochastic control problem for pricing GMWB with discrete optimal withdrawals has only been successfully dealt with by solving the one-dimensional PDE equation using a finite difference method presented in Dai et al., (2008) and Chen & Forsyth, (2008). Simulation based method such as the Least Squares Monte Carlo method cannot be applied for such problems due to the dynamic behavior of the policyholder affecting the paths of the underlying wealth account. Recently, Luo & Shevchenko, (2014b) have considered an alternative method without solving PDEs or simulating paths. The new approach relies on computing the expected option values in a backward time-stepping between withdrawal dates through a high order Gauss-Hermite integration quadrature applied on a cubic spline interpolation. In this paper we adopt this method to calculate GMWDB.

3.1 Numerical quadrature to evaluate the expectation

To price variable annuity contract with GMWDB, i.e. to compute , we have to evaluate expectations in (2.2). Assuming the conditional probability density of given is known as , in the case of process (2) it is just lognormal density, (2.2) can be evaluated as

| (24) |

where

We use Gauss-Hermite quadrature for the evaluation of the above integration over an infinite domain. The required continuous function will be approximated by a cubic spline interpolation on a discretized grid in the space.

The wealth account domain is discretized as , where and are the lower and upper boundary, respectively. For pricing GMWDB, because of the finite reduction of at each withdrawal date, we have to consider the possibility of goes to zero, thus the lower bound . The upper bound is set sufficiently far from the spot asset value at time zero W(0). A good choice of such a boundary could be . The idea is to find annuity values at all these grid points at each time step through integration (24), starting at maturity . At each time step we evaluate the integral (24) for every grid point by a high accuracy numerical quadrature.

The annuity value at is known only at grid points , . In order to approximate the continuous function from the values at the discrete grid points, we use the natual cubic spline interpolation which is smooth in the first derivative and continuous in the second derivative; and second derivative is zero for extrapolation region.

The process for between withdrawal dates is a simple process given in (2), the conditional density of given is from a lognormal distribution. To apply Gauss-Hermite numerical quadrature for integration over an infinite domain, we introduce a new variable

| (25) |

and denote the function after this transformation as . Then the integration becomes

| (26) |

For an arbitrary function , the Gauss-Hermite quadrature is

| (27) |

where is the order of the Hermite polynomial, are the roots of the Hermite polynomial , and the associated weights are given by

Applying a change of variable and using the Gauss-Hermite quadrature to (26), we obtain

| (28) |

If we apply the change of variable (25) and the Gauss-Hermite quadrature (26) to every grid point , , i.e. let , then the option values at time for all the grid points can be evaluated through (28). If the transition density function from to is not known in closed form but one can find its moments, then integration can also be done by matching moments as described in Luo & Shevchenko, (2014a, b).

3.2 Jump condition application

Any change of only occurs at withdrawal dates. After the amount is drawn at , the annuity account reduces from to , and the guarantee balance drops from to . The jump condition of across is given by

| (29) |

For the optimal strategy, we chose a value for under the restriction to maximize the function value in (29).

To apply the jump conditions, an auxiliary finite grid is introduced to track the remaining guarantee balance , where is the total number of nodes in the guarantee balance amount coordinate. For each , we associate a continuous solution from (28) and the cubic spline interpolation. We can limit the number of possible discrete withdrawal amounts to be finite by only allowing the guarantee balance to be equal to one of the grid points . This implies that, for a given balance at time , the withdraw amount takes possible values: , and the jump condition (29) takes the following form

| (30) |

For the optimal strategy, we chose a value for to maximize in (30). Note that although the jump amount , is independent of time and account value , the value depends on all variables and the jump amount.

It is worth pointing out that part of the good efficiency of the GHQC algorithm for pricing GMWB or GMWDB under rational policyholder behavior is due to that fact that the same cubic spline interpolation is used for both numerical integration (24) and the application of jump condition (30). A clear advantage of this numerical algorithm over PDE based finite difference approach is that significantly smaller number of time steps are required because the transition density over the finite time period in (24) is known. The finite difference method requires dividing the period between two consecutive withdrawal dates into finer time steps for a good accuracy due to the finite difference approximation to the partial derivatives.

3.3 Death probabilities

Given a Life Table, such as Table 6, estimating the death probabilities and required in (6) and (22) is straightforward. The Life Table tabulates the number of people surviving to the exact age starting with 100,000 at the age zero for each sex and goes beyond 100 years. Denote the number of people still alive at age years as a list , . Denote the age of policyholder at the start of the contract (i.e. at time ) as . To estimate the conditional death probabilities and , we only need to know the number of people alive at time and . Because in the Life Table the number of people is only given at integer number , we estimate the number of people alive for an arbitrary time using linear interpolation, i.e. assuming a uniform distribution for the death time within a year. Of course a more elaborate interpolation is also possible. Then, for , is calculated as

Having obtained and using the above formula (note and may not necessarily fall within the same year), the conditional death probabilities are estimated as

| (31) |

Instead of a Life Table, stochastic mortality models such as frequently used benchmark Lee-Carter model (Lee-Carter) forecasting mortality rate using stochastic process (and typically accounting for systematic mortality risk) can also be used for estimating death probabilities and .

3.4 Overall algorithm description

Starting from a final condition at (just immediately before the final withdrawal), a backward time stepping using (24) gives solution up to time . Applying jump condition (29) to the solution at we obtain the solution at from which further backward time stepping gives us solution at , etc till . The numerical algorithm takes the following key steps

Algorithm 3.1 (GMWDB pricing)

-

•

Step 1. Generate an auxiliary finite grid to track the guarantee account .

-

•

Step 2. Discretize wealth account space as which is a grid for computing (24).

-

•

Step 3. At apply the final condition at each node point , , to get payoff .

-

•

Step 4. Evaluate integration (24) (for each of the ) to obtain .

-

•

Step 5. Apply the jump condition (29) to obtain for all possible jumps and find the jump that maximizes .

-

•

Step 6. Repeat Step 4 and 5 for .

-

•

Step 7. Evaluate integration (24) for the backward time step from to for the single node value to obtain solution and take the value as the annuity price at . Of course if the contract is re-evaluated at some time after it started, one will need to take solution at the node corresponding to and at that time.

We use Gauss-Hermite quadrature integration (28) with cubic spline in Step 4. One can also perform integration using moment matching if the density is not known in closed form but its moments are available. For static case, Step 1 is not needed because only a single solution is required and the jump condition applies to the single solution itself.

4 Numerical Results

The accuracy and efficiency of GHQC method in pricing GMWB under optimal withdraw is well demonstrated in Luo & Shevchenko, (2014a). From numerical point of view, once the problem is correctly formulated, pricing GMWDB (with combined GMWB and GMDB features) uses the same key algorithm components as those for pricing GMWB, such as numerical quadrature integration for the expectations and cubic spline interpolation for applying the jump conditions.

To the best of our knowledge, there is no numerical results available in the literature for variable annuity contracts with combined GMWB and GMDB features under the optimal withdrawal strategy, and only some very limited results are available in the literature for GMWB under the optimal withdrawal strategy, namely from Dai et al., (2008) and Chen & Forsyth, (2008). To validate our implementation for GMWDB, we have made the following efforts:

-

•

Implemented an efficient finite difference (FD) algorithm with the same mathematical formulation and functionality, so GHQC results for GMWDB can always be compared with FD.

-

•

For the limiting case where the death probability is zero, i.e. , the GMQDB price should reduce to the standard GMWB price exactly (still under optimal withdrawal), and we can compare our GMWDB results with GMWB results found in the literature.

-

•

For the static withdraw case, GMWDB contract can be evaluated by Monte Carlo (MC) method, so we can compare our GHQC results for GMWDB with those of MC using a very large number of simulations. The close agreement of results between the two algorithms offers a reassuring validation for both methods.

Below we present and discuss numerical results for GMWDB. In our numerical examples we assume policyholder age 60 for male and female and use the current Australian Life Table, see Table 6, to find corresponding death probabilities.

4.1 Results for dynamic GMWB

Before showing numerical results for GMWDB, we first validate our numerical algorithms by testing the limiting case of zero death probability. In such a case we can compare our GMWDB results with some finite difference results found in the literature for GMWB. In Chen & Forsyth, (2008), the fair fees for the discrete withdrawal model with for the yearly () and half-yearly () withdrawal frequency at and were presented in a carefully performed convergence study, with the same values for other input parameters (, ). Table 1 compares GHQC (Algorithm 3.1) results with those of Chen & Forsyth, (2008). The values of Chen & Forsyth, (2008) quoted in Table 1 correspond to their finest mesh grids and time steps at grid points for coordinate, grid points for coordinate and steps for time, while our GHQC values were obtained using , and with for the number of quadrature points (and the number of time steps is the same as the number of withdrawal dates ). As shown in Table 1, the maximum absolute difference in the fair fee rate between the two numerical studies is only basis point, and the average absolute difference of the four cases in the table is less than 0.2 basis point. As one basis point is , the average difference is in the order of 20 cents for a one thousand dollar account. In relative terms, the maximum difference is less than , and the average magnitude of the relative differences between the two studies is less than . Chen & Forsyth, (2008) did not provide CPU numbers for their calculations of fair fees. In our case each calculation of the fair fee in Table 1, which involves a Newton iterative method of root finding, took about 5 seconds. In Luo & Shevchenko, (2014b), a detailed comparison shows the GHQC algorithm is significantly faster than the FD in pricing dynamic GMWB contract, especially for lower withdrawal frequencies. All our calculations in this study were performed using standard desktop PC (Intel(R) Core(TM) i5-2400 @3.1GHz).

| withdrawal frequency | volatility, | Fair fee, | Fair fee, |

|---|---|---|---|

| Chen & Forsyth, (2008) | GHQC | ||

| yearly | 0.2 | 129.1 | 129.1 |

| half-yearly | 0.2 | 133.5 | 133.7 |

| yearly | 0.3 | 293.3 | 293.5 |

| half-yearly | 0.3 | 302.4 | 302.7 |

4.2 Results for GMWDB

The standard GMWB annuity without consideration of death event assumes that the policyholder will be alive during the contract or there is beneficiary to continue withdrawals until maturity. We refer to this case as GMWDB without death benefit; it is equivalent to GMWDB with death probability set to zero. There are several more or less natural considerations of GMWDB contact payoff in the case of death before or at contract maturity. We consider death benefit types summarised in (8), though many other modifications are possible. A natural contract condition in the case of death event is to pay the maximum of the remaining guaranteed account and the wealth account values (denoted as DB0). An alternative is to payback the initial premium at death (denoted as DB1), which is similar to a term life insurance paying a fixed amount equal to the premium upon death (the amount can be adjust for inflation, etc). On the other hand, the Guaranteed Minimum Death Benefit (GMDB), in its basic form, offers to pay the maximum of the wealth account value and the premium (denoted as DB2). GMWDB contract with DB2 has both features of GMWB and GMDB but requiring only a single premium. All three types of death benefits can be added to either static GMWB or dynamic GMWB. All the following results of GMWDB are based on death probabilities calculated from the Life Table for the male population in Australia, except those in Table 5 which have used the Life Table for the female population in Australia; also see Table 6. We assume that policyholder is 60 years old.

4.2.1 Static GMWDB

Table 2 shows static case results of GMWDB with DB0, DB1 and DB2 death benefits, and standard GMWB (i.e. GMWDB with zero death probability). Here we also present MC and FD results for DB0 case. The number of simulations for MC is 20 million and corresponding standard error in calculation of fair fees is within 0.2 basis point. As shown in Table 2, the maximum difference of fair fee between GHQC and MC methods is 0.2 basis point, and the maximum difference between GHQC and FD methods is 0.1 basis point in the case of DB0. We have also calculated DB1 and DB2 cases using FD and MC methods and the difference between the methods is virtually the same as in the case of DB0 so we do not present these results. The close agreement between MC and GHQC methods is a reassuring validation for both algorithms.

Comparing with results for static GMWB (i.e. GMWDB with death probability set to zero), adding DB0 death benefit requires less than 10 extra basis points in the fair fee. The fair fee increases significantly in the case of DB2 death benefit. As expected, the fair fee for DB2 at all maturities is higher than for DB1 and the difference decreases as maturity increases. At ( years), the fair fee for DB1 is actually negative, meaning the contract is not appropriate. This seems to be odd at first, but it actually makes sense: the withdrawal rate is lower than the expected growth rate of , and returning only the premium at any time of death is a loss to the policyholder, and a possible gain can only be obtained if the policyholder survives beyond the maturity which is not enough to offset the loss due to the probability of death. At , the fair fee for DB1 becomes positive but it is still lower than for DB0, and it is even lower than a static GMWB.

Real product design may impose expiry date for the death benefit guarantee (e.g. at the age 70 or 75) that will reduce the cost of the death benefit guarantee itself and will help avoid the case of negative fee such as in Table 2 for long contract maturity years. If the contract will switch from DB2 or DB1 to DB0 (effectively making the death benefit expiring at the specified age), then it can be handled by the same algorithm described in this paper with adjustment to the death benefit function (8). If the death benefit expiring corresponds to switching to the standard GMWB, then it can be handled by setting death probabilities to zero after death benefit expiry till the contract maturity.

| contractual rate | maturity | GHQC | GHQC | FD | MC | GHQC | GHQC |

|---|---|---|---|---|---|---|---|

| no death | DB0 | DB0 | DB0 | DB1 | DB2 | ||

| 25 | 17.69 | 25.53 | 25.49 | 25.72 | -59.89 | 90.43 | |

| 20 | 28.33 | 35.24 | 35.21 | 35.34 | 23.91 | 99.25 | |

| 16.67 | 40.33 | 46.70 | 46.69 | 46.74 | 64.48 | 111.1 | |

| 14.29 | 53.31 | 59.32 | 59.29 | 59.25 | 92.80 | 125.1 | |

| 12.50 | 66.99 | 72.73 | 72.68 | 72.59 | 116.3 | 140.2 | |

| 11.11 | 81.23 | 86.76 | 86.75 | 86.58 | 137.5 | 155.9 | |

| 10.00 | 95.81 | 101.2 | 101.1 | 101.2 | 157.2 | 172.0 | |

| 6.67 | 171.9 | 176.7 | 176.6 | 176.9 | 249.5 | 256.1 |

4.2.2 Dynamic GMWDB

Table 3 shows results for dynamic GMWDB with DB0, DB1 and DB2 death benefits and dynamic GMWB calculated using GHQC method. Here we also present FD method results for DB0 case. The maximum difference of fees between GHQC and FD methods is 0.4 basis point occurring at the shortest maturity, which has the maximum magnitude in the fee. In relative terms this is less than . For other cases the difference between methods is similar, i.e. very small and we show results calculated using GHQC method only.

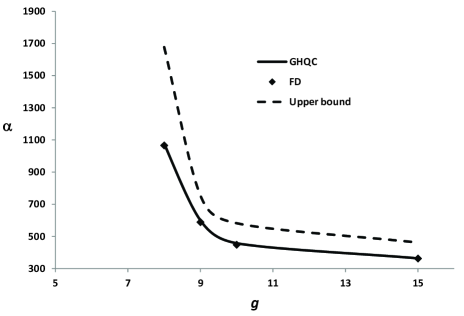

Comparing with results for GMWB, adding DB0 death benefit to a dynamic GMWB only requires a maximum of 10 extra basis points in the fair fee, similar to the static case. As easily seen from the table, adding DB1 or DB2 death benefit (returning at least the initial premium) changes the situation dramatically. At , the shortest maturity, the fair fee of GMWDB with DB1 or DB2 death benefit more than doubled from the value of GMWB. Moreover, the fair fee increases rapidly as the maturity increases, while in all the other cases so far shown in this paper the fair fee is a decreasing function of maturity. This increase in the fair fee is so rapid that no solution for the fair fee exists for (i.e. for ) for either DB1 or DB2 – meaning that even charging fee at is still not enough to cover the risks. The last column in the table is the upper bound of the fair fee corresponding to the upper estimator calculated using equation (22), i.e. estimator calculating GMWDB for given death time (conditional on knowing death time) and then averaging over possible death times with corresponding death probabilities. Figure 1 plots the fair fee of GMWDB with DB2 as a function of the contractual withdrawal rate , showing the rapid increase of fair fee as the contractual rate decreases or the maturity increases. Between DB1 and DB2, the difference in the fair fee is very small, unlike the static case where the difference in the fair fee between DB1 and DB2 is significant. Also shown in Figure 1 (dashed line) is the the upper bound of the fair fee from Table 3. The upper bound of the fee is much higher than the fee corresponding to the optimal withdraw strategy based on information up to the withdrawal date, manifesting the value of ‘knowing the future’.

| contractual rate | maturity | GHQC | GHQC | FD | GHQC | GHQC | GHQC |

|---|---|---|---|---|---|---|---|

| no death | DB0 | DB0 | DB1 | DB2 | DB2∗ | ||

| 25.00 | 56.09 | 66.43 | 66.51 | N/A | N/A | N/A | |

| 20.00 | 70.07 | 77.93 | 77.95 | N/A | N/A | N/A | |

| 16.67 | 83.74 | 90.32 | 90.29 | N/A | N/A | N/A | |

| 14.29 | 97.11 | 102.9 | 102.8 | N/A | N/A | N/A | |

| 12.50 | 110.3 | 115.6 | 115.4 | 1072 | 1076 | 1677 | |

| 11.11 | 123.2 | 128.1 | 127.9 | 597.6 | 599.6 | 754.6 | |

| 10.00 | 136.0 | 140.6 | 140.4 | 455.9 | 457.7 | 582.2 | |

| 6.67 | 199.0 | 203.0 | 202.6 | 362.1 | 363.8 | 461.9 |

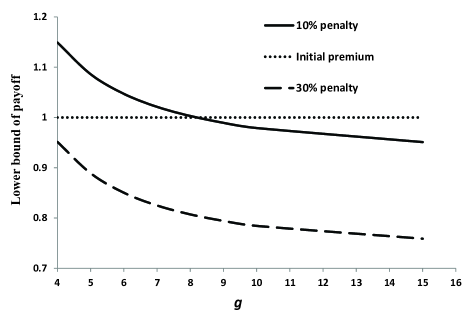

Now let us look at the reason for the non-existence of solution at longer maturity by considering the following simple pre-defined strategy (sufficiently good strategy but not necessarily optimal thus corresponding to the lower price estimator). Assume the policyholder of a dynamic GMWDB with DB2 withdraws all guarantee amount at the first withdrawal date (if surviving the first time period) and waiting for the possible collection of the death benefit. Then wealth account evolves according to (2) with , . The expected present value of payoff (expectation with respect to death time and wealth process ) received by the policyholder using the above strategy is

where is the probability of death occurring during the -th payment period conditional on the policyholder is alive at the beginning of the contract, is the full withdraw amount minus penalty if the policyholder survives the first payment period to execute the strategy, and denotes a lower bound of the expected payoff for this simple strategy. The above estimate of the payoff for the strategy is independent of the fee charged by the insurance company - because the fee only affects the account value, not the guarantee amount, nor the minimum death benefit. Using the same strategy, the above lower bound also applies to DB1. Figure 2 shows the lower bound as a function of the contractual rate . Clearly, at and the strategy always yields a cashflow greater than the initial premium, irrespective of the fee charged, thus explaining why no solution of fair fee exists for . Qualitatively, GMWDB with the minimum death benefit of returning the premium allows a rational policyholder of a long maturity contract to get almost all the initial premium back while having a high probability of collecting the death benefit as well.

One remedy for the above problem of non-existence of solution is simply increasing the penalty rate to discourage excessive withdrawals above the contractual rate. Also shown in Figure 2 is another payoff curve in the case of penalty rate increased to – in this instance the estimated payoff is well below the initial premium at all withdrawal rates and solution for the fair fee exists.

Also, as already mentioned in previous sections, real product design may impose expiry date for the death benefit guarantee (e.g. at the age 70 or 75) that will reduce the cost of the death benefit guarantee itself and will help to avoid the case of non-existence of solution.

4.2.3 Dynamic GMWDB with fixed installment fees for death benefit

The above problem of non-existence of fair fee solution for dynamic GMWDB in some cases, can also be dealt with by a more reasonable fee structure. So far the extra cost of adding DB1 or DB2 death benefit is absorbed in the continuous fee which is linked to the wealth account value , not to the guaranteed premium in the death benefit. As the fund value is reduced by each withdrawal, the charge base is also reduced. A better fee structure is to keep the continuous fee the same as the dynamic GMWB but charge the extra fee due to adding DB1 or DB2 death benefit upfront or in fixed instalments. In practice the later is usually preferred.

Denote the fair fee of a dynamic GMWB (i.e. GMWDB with death probabilities set to zero) as (e.g. column 3 in Table 3), and the fair price of a GMWDB (with either DB1 or DB2) under the same fee as , then obviously and the fair upfront fee is the difference . To work out the constant instalment amount , the probability of death has to be considered. Here we assume each instalment is paid at the beginning of each withdrawal period and no further payment is required upon death. Conditional on death occurring during the period , i.e. , the total sum of instalments received by the issuer of GMWDB is given by , and the expected total sum of instalments is then

where is the probability of surviving beyond maturity , and is the probability of death occurring during the period . Equating with the upfront fee , we obtain the fair instalment fee

| (32) |

Using (32) the calculation of instalment for GMWDB given the fair fee for GMWB is straightforward. Table 4 shows the values of in terms of basis points of the initial premium for the same cases as in Table 3. It is interesting and useful to compare the extra instalment due to adding DB1 or DB2 death benefit to GMWB against the instalment of a separate life insurance with the same term, instalment frequency and the insured amount equal to the initial premium of GMWDB, . In the case of such a life insurance, the instalment is given by

| (33) |

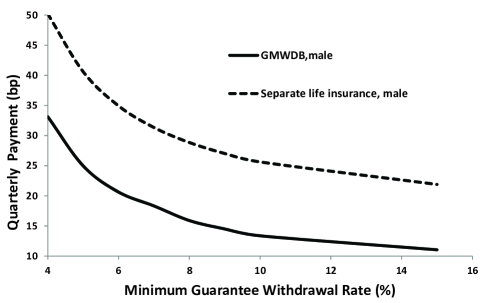

where is the expected payoff of the life insurance. Table 4 also shows the values of in comparison with the values of . Clearly the instalment fee of buying a separate life insurance is higher than the extra instalment fee by adding DB1 (life insurance) or DB2 (GMDB payoff) on top of GMWB, making the combined contract GMWDB an attractive product. The life insurance fee is about higher than the extra fee of GMWDB with DB2 at the longest maturity corresponding to , and this difference increases to at the shortest maturity corresponding to . What is more, upon death the GMWDB contract with DB2 returns the maximum between account value (where is first time slice after the death) and the initial premium , while the life insurance only returns the insured sum . The extra instalment required by DB1 is only very slight smaller than that of DB2. Figure 3 shows the curve of of DB2 in comparison with for the male population. The curve for DB1 (not shown) is hardly distinguishable from those of DB2 in Figure 3.

Instead of buying a separate life insurance, another alternative is to buy a GMDB contract in addition to the GMWB contract, in this case it is very expensive because GMDB requires an additional premium of , while the life insurance does not, nor does the combined GMWDB with either DB1 or DB2 (only a single premium is required). So overall it is better and cheaper to buy a single combined GMWDB contract with either DB1 or DB2 death benefit.

Table 5 is the female counterpart of Table 4. As expected, both the extra instalment fee of the GMWDB on top of the GMWB and the separate life insurance for the female population is much cheaper than for the male population. Depending the maturity, there is also some significant saving on fees of about to for the female population, if the GMWDB is purchased instead of buying a separate life insurance on top of GMWB, although the saving is not as great as for the male population.

| contractual rate, g | maturity | (DB1) | (DB2) | |

|---|---|---|---|---|

| 25.00 | 32.05 | 33.13 | 50.20 | |

| 20.00 | 24.39 | 24.97 | 40.61 | |

| 16.67 | 20.23 | 20.63 | 34.94 | |

| 14.29 | 18.01 | 18.33 | 31.35 | |

| 12.50 | 15.59 | 15.91 | 28.86 | |

| 11.11 | 14.18 | 14.51 | 27.03 | |

| 10.00 | 13.03 | 13.37 | 25.63 | |

| 6.67 | 10.70 | 11.05 | 21.90 |

| contractual rate, g | maturity | (DB1) | (DB2) | |

|---|---|---|---|---|

| 25.00 | 18.90 | 20.14 | 32.55 | |

| 20.00 | 13.34 | 14.14 | 24.85 | |

| 16.67 | 10.84 | 11.46 | 20.96 | |

| 14.29 | 9.67 | 10.23 | 18.62 | |

| 12.50 | 8.23 | 8.82 | 17.01 | |

| 11.11 | 7.49 | 8.06 | 15.82 | |

| 10.00 | 6.89 | 7.43 | 14.97 | |

| 6.67 | 6.02 | 6.35 | 12.86 |

5 Conclusion

In this paper we have presented a numerical valuation of a variable annuity with GMWDB (i.e. with combined GMWB and GMDB features) under both passive (static) and optimal (dynamic) policyholder behaviors. Essentially this contract simultaneously deals financial risk, mortality risk and human behavior in terms of decision under uncertainty. In the case of optimal policyholder behaviour, we formulate and solve the valuation as a stochastic control problem for controlled Markov process, i.e. policyholder performs optimal withdrawals based on account information available at withdrawal date. It is important to note that pricing dynamic GMWDB contract for given death time (i.e. conditional on knowing death time) and then averaging over different death times according to death probabilities will lead to higher price than dynamic GMWDB where decisions are based on information available at withdrawal date.

We presented a series of numerical results for GMWDB with different death benefit types and showed that, in the case of optimal policyholder behavior, adding the premium for the minimum death benefit on top of the GMWB can be problematic for contracts with long maturities if the continuous fee structure is kept, which is ordinarily assumed for a GMWB contract. In fact for some long maturities we observed that the fee cannot be charged as any proportion of the wealth account value – there is no solution to match the initial premium with the fair annuity price. To avoid this problem, the product design may impose expiry for the death benefit guarantee, e.g. at the age of 70 years. On the other hand, the extra fee due to adding the death benefit can be charged upfront or in periodic instalment of fixed amount and it is cheaper than buying a separate life insurance.

6 Acknowledgement

In conclusion, we are grateful to Juri Hinz for useful discussions of the problem. This research was supported by the CSIRO-Monash Superannuation Research Cluster, a collaboration among CSIRO, Monash University, Griffith University, the University of Western Australia, the University of Warwick, and stakeholders of the retirement system in the interest of better outcomes for all.

References

- Bacinello et al., (2011) Bacinello, A.R., Millossovich, P., Olivieri, A., & Pitacco, E. 2011. Variable annuities: a unifying valuation approach. Insurance: Mathematics and Economics, 49(1), 285–297.

- Bauer et al., (2008) Bauer, D., Kling, A., & Russ, J. 2008. A universal pricing framework for guaranteed minimum benefits in variable annuities. ASTIN Bulletin, 38(2), 621–651.

- Bäuerle & Rieder, (2011) Bäuerle, N., & Rieder, U. 2011. Markov Decision Processes with Applications to Finance. Springer, Berlin.

- Chen & Forsyth, (2008) Chen, Z., & Forsyth, P. 2008. A Numerical Scheme for the Impulse Control Formulation for Pricing Variable Annuities with a Guaranteed Minimum Withdrawal Benefit (GMWB). Numerische Mathematik, 109(4), 535–569.

- Dai et al., (2008) Dai, M., Kwok, K. Y., & Zong, J. 2008. Guaranteed minimum withdrawal benefit in variable annuities. Mathematical Finance, 18(4), 595–611.

- Ledlie et al., (2008) Ledlie, M. C., Corry, D. P., Finkelstein, G. S., Ritchie, A. J., Su, K., & Wilson, D. C. E. 2008. Variable annuities. British Actuarial Journal, 14(2), 327 –389.

- Longstaff & Schwartz, (2001) Longstaff, F., & Schwartz, E. 2001. Valuing American options by simulation: a simple lieast-squares approach. Review of Financial Studies, 14, 113–147.

- Luo & Shevchenko, (2014a) Luo, X., & Shevchenko, P. V. 2014a. Fast and Simple Method for Pricing Exotic Options using Gauss-Hermite Quadrature on a Cubic Spline Interpolation. To appear in Journal of Financial Engineering.

- Luo & Shevchenko, (2014b) Luo, X., & Shevchenko, P. V. 2014b. Fast Numerical Method for Pricing of variable annuities with guaranteed minimum withdrawal benefit under optimal withdrawal strategy. Preprint, arxiv 1410.8609 available on http://arxiv.org.

- Milevsky & Salisbury, (2006) Milevsky, M. A., & Salisbury, T. S. 2006. Financial valuation of guaranteed minimum withdrawal benefits. Insurance: Mathematics and Economics, 38(1), 21–38.

- Powell, (2011) Powell, W. B. 2011. Approximate Dynamic Programming. Wiley.

- Smith, (1982) Smith, M. 1982. The life insurance policy as an options package. The Journal of Risk and Insurance, 49(4), 583– 601.

- Walden, (1985) Walden, M. 1985. The whole life insurance policy as an options package: an empirical investigation. The Journal of Risk and Insurance, 52(1), 44 –58.

Appendix A Australian Life Table

| Age | Number of males | Number of females |

|---|---|---|

| surviving to exact age | surviving to exact age | |

| 0 | 100,000 | 100,000 |

| … | … | … |

| 60 | 91,305 | 94,817 |

| 61 | 90,684 | 94,434 |

| 62 | 90,010 | 94,019 |

| 63 | 89,276 | 93,566 |

| 64 | 88,475 | 93,073 |

| 65 | 87,601 | 92,535 |

| 66 | 86,646 | 91,948 |

| 67 | 85,603 | 91,306 |

| 68 | 84,463 | 90,604 |

| 69 | 83,219 | 89,838 |

| 70 | 81,863 | 88,997 |

| 71 | 80,390 | 88,053 |

| 72 | 78,791 | 86,997 |

| 73 | 77,061 | 85,836 |

| 74 | 75,191 | 84,571 |

| 75 | 73,169 | 83,192 |

| 76 | 70,982 | 81,683 |

| 77 | 68,614 | 80,026 |

| 78 | 66,053 | 78,196 |

| 79 | 63,287 | 76,168 |

| 80 | 60,308 | 73,916 |

| 81 | 57,115 | 71,412 |

| 82 | 53,710 | 68,636 |

| 83 | 50,109 | 65,568 |

| 84 | 46,333 | 62,200 |

| 85 | 42,415 | 58,532 |

| … | … | … |