What Teachers Should Know about the Bootstrap: Resampling in the Undergraduate Statistics Curriculum

Abstract

I have three goals in this article: (1) To show the enormous potential of bootstrapping and permutation tests to help students understand statistical concepts including sampling distributions, standard errors, bias, confidence intervals, null distributions, and -values. (2) To dig deeper, understand why these methods work and when they don’t, things to watch out for, and how to deal with these issues when teaching. (3) To change statistical practice—by comparing these methods to common tests and intervals, we see how inaccurate the latter are; we confirm this with asymptotics. isn’t enough—think . Resampling provides diagnostics, and more accurate alternatives. Sadly, the common bootstrap percentile interval badly under-covers in small samples; there are better alternatives. The tone is informal, with a few stories and jokes.

Keywords: Teaching, bootstrap, permutation test, randomization test

1 Overview

I focus in this article on how to use relatively simple bootstrap methods and permutation tests to help students understand statistical concepts, and what instructors should know about these methods. I have Stat 101 and Mathematical Statistics in mind, though the methods can be used elsewhere in the curriculum. For more background on the bootstrap and a broader array of applications, see (Efron and Tibshirani, 1993; Davison and Hinkley, 1997).

Undergraduate textbooks that consistently use resampling as tools in their own right and to motivate classical methods are beginning to appear, including Lock et al. (2013) for Introductory Statistics and Chihara and Hesterberg (2011) for Mathematical Statistics. Other texts incorporate at least some resampling.

Section 2 is an introduction to one- and two-sample bootstraps and two-sample permutation tests, and how to use them to help students understand sampling distributions, standard errors, bias, confidence intervals, hypothesis tests, and -values. We discuss the idea behind the bootstrap, why it works, and principles that guide our application.

In Section 3 we take a visual approach toward understanding when the bootstrap works and when it doesn’t. We compare the effect on bootstrap distributions of two sources of variation—the original sample, and bootstrap sampling.

In Section 4 we look at three things that affect inferences—bias, skewness, and transformations—and something that can cause odd results for bootstrapping, whether a statistic is functional. This section also discusses how inaccurate classical procedures are when the population is skewed. I have a broader goal beyond better pedagogy—to change statistical practice. Resampling provides diagnostics, and alternatives.

This leads to Section 5, on confidence intervals; beginning with a visual approach to how confidence intervals should handle bias and skewness, then a description of different confidence intervals procedures and their merits, and finishing with a discussion of accuracy, using simulation and asymptotics.

In Section 6 we consider sampling methods for different situations, in particular regression, and ways to sample to avoid certain problems.

We return to permutation tests in Section 7, to look beyond the two-sample test to other applications where these tests do or do not apply, and finish with a short discussion of bootstrap tests.

Section 8 summarizes key issues.

Teachers are encouraged to use the examples in this article in their own classes. I’ll include a few bad jokes; you’re welcome to those too. Examples and figures are created in R (R Core Team, 2014), using the resample package (Hesterberg, 2014). I’ll put datasets and scripts at http://www.timhesterberg.net/bootstrap.

I suggest that all readers begin by skimming the paper, reading the boxes and Figures 20 and 21, before returning here for a full pass.

There are sections you may wish to read out of order. If you have experience with resampling you may want to read the summary first, Section 8. To focus on permutation tests read Section 7 after Section 2.2. To see a broader range of bootstrap sampling methods earlier, read Section 6 after Section 2.8. And you may skip the Notation section, and refer to it as needed later.

1.1 Notation

This section is for reference; the notation is explained when it comes up.

We write for a population, with corresponding parameter ; in specific applications we may have e.g. or ; the corresponding sample estimates are , , or .

is an estimate for . Often is the empirical distribution , with probability on each observation in the original sample. When drawing samples from , the corresponding estimates are , , or .

is the usual sample variance, and is the variance of .

When we say “sampling distribution”, we mean the sampling distribution for or when sampling from , unless otherwise noted.

is the number of resamples in a bootstrap or permutation distribution. The mean of the bootstrap distribution is or , and the standard deviation of the bootstrap distribution (the bootstrap standard error) is or .

The interval with bootstrap standard error is .

represents a theoretical bootstrap or permutation distribution, and is the approximation by sampling; the quantile of this distribution is .

The bootstrap percentile interval is , where are quantiles of . The expanded percentile interval is , where . The reverse percentile interval is .

The bootstrap interval is where are quantiles for and is a standard error for .

Johnson’s (skewness-adjusted) statistic is where . The skewness-adjusted interval is .

2 Introduction to the Bootstrap and Permutation Tests

We’ll begin with an example to illustrate the bootstrap and permutation tests procedures, discuss pedagogical advantages of these procedures, and the idea behind bootstrapping.

Student B. R. was annoyed by TV commercials. He suspected that there were more commercials in the “basic” TV channels, the ones that come with a cable TV subscription, than in the “extended” channels you pay extra for. To check this, he collected the data shown in Table 1.

| Basic | 6.95 | 10.013 | 10.62 | 10.15 | 8.583 |

| 7.62 | 8.233 | 10.35 | 11.016 | 8.516 | |

| Extended | 3.383 | 7.8 | 9.416 | 4.66 | 5.36 |

| 7.63 | 4.95 | 8.013 | 7.8 | 9.58 |

He measured an average of 9.21 minutes of commercials per half hour in the basic channels, vs only 6.87 minutes in the extended channels. This seems to support his hypothesis. But there is not much data—perhaps the difference was just random. The poor guy could only stand to watch 20 random half hours of TV. Actually, he didn’t even do that—he got his girlfriend to watch half of it. (Are you as appalled by the deluge of commercials as I am? This is per half-hour!)

2.1 Permutation Test

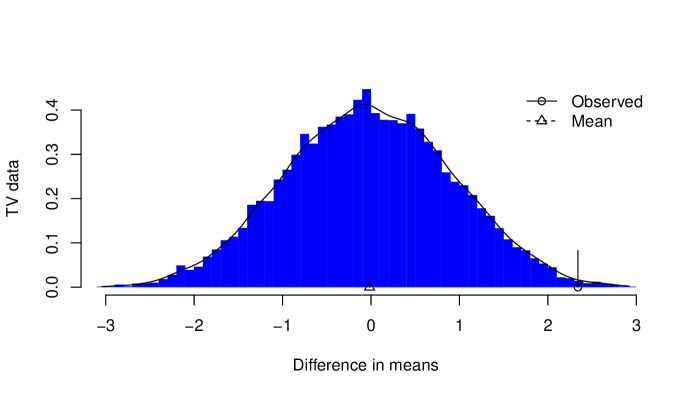

How easy would it be for a difference of 2.34 minutes to occur just by chance? To answer this, we suppose there really is no difference between the two groups, that “basic” and “extended” are just labels. So what would happen if we assign labels randomly? How often would a difference like 2.34 occur?

We’ll pool all twenty observations, randomly pick 10 of them to label “basic” and label the rest “extended”, and compute the difference in means between the two groups. We’ll repeat that many times, say ten thousand, to get the permutation distribution shown in Figure 1. The observed statistic is also shown; the fraction of the distribution to the right of that value () is the probability that random labeling would give a difference that large. In this case, the probability, the -value, is ; it would be rare for a difference this large to occur by chance. Hence we conclude there is a real difference between the groups.

| Two-Sample Permutation Test |

| Pool the values \REPEATX9999 times Draw a resample of size without replacement. Use the remaining observations for the other sample. Calculate the difference in means, or another statistic that compares samples. \ENDREPEATX Plot a histogram of the random statistic values; show the observed statistic. Calculate the -value as the fraction of times the random statistics exceed or equal the observed statistic (add 1 to numerator and denominator); multiply by 2 for a two-sided test. |

We defer some details until Section 7.1, including why we add 1 to numerator and denominator, and why we calculate a two-sided -value this way.

2.2 Pedagogical Value

This procedure provides nice visual representation for what are otherwise abstract concepts—a null distribution, and a -value. Students can use the same tools they previously used for looking at data, like histograms, to inspect the null distribution.

And it makes the convoluted logic of hypothesis testing quite natural. (Suppose the null hypothesis is true, how often we would get a statistic this large or larger?) Students can learn that “statistical significance” means “this result would rarely occur just by chance”.

It has the advantage that students can work directly with the statistic of interest—the difference in means—rather than switching to some other statistic like a statistic.

It generalizes nicely to other statistics. We could work with the difference in medians, for example, or a difference in trimmed means, without needing new formulas.

| Pedagogical Value of Two-Sample Permutation Test |

| Make abstract concepts concrete—null distribution, -value. Use familiar tools, like histograms. Work with the statistic of interest, e.g. difference of means. Generalizes to other statistics, don’t need new formulas. Can check answers obtained using formulas. |

2.3 One-Sample Bootstrap

In addition to using the permutation test to see whether there is a difference, we can also use resampling, in particular the bootstrap, to quantify the random variability in the two sample estimates, and in the estimated difference. We’ll start with one sample at a time.

In the bootstrap, we draw observations with replacement from the original data to create a bootstrap sample or resample, and calculate the mean for this resample. We repeat that many times, say 10000. The bootstrap means comprise the bootstrap distribution.

The bootstrap distribution is a sampling distribution, for (with sampling from the empirical distribution); we’ll talk more below about how it relates to the sampling distribution of (sampling from the population ). (In the sequel, when we say “sampling distribution” we mean the latter, not the bootstrap distribution, unless noted.)

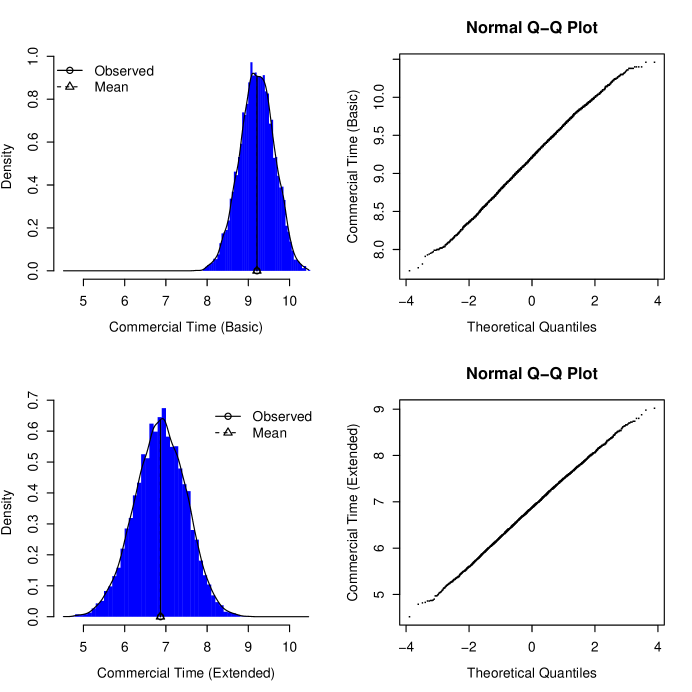

Figure 2 shows the bootstrap distributions for the Basic and Extended data. For each distribution, we look at the center, spread, and shape:

- center:

-

Each distribution is centered approximately at the observed statistic; this indicates that the sample mean is approximately unbiased for the population mean. We discuss bias in Section 4.2.

- spread:

-

The spread of each distribution estimates how much the sample mean varies due to random sampling. The bootstrap standard error is the sample standard deviation of the bootstrap distribution,

- shape:

-

Each distribution is approximately normally distributed.

A quick-and-dirty confidence interval, the bootstrap percentile confidence interval, is the range of the middle 95% of the bootstrap distribution; this is for the Basic channels and for the Extended channels. (Caveat—percentile intervals are too short in samples this small, see Sections 3.2 and 5.2, and Figures 20–22).

Here are the summaries of the bootstrap distributions for basic and extended channels

Summary Statistics:

Observed SE Mean Bias

Basic 9.21 0.4159658 9.207614 -0.002386

Observed SE Mean Bias

Extended 6.87 0.6217893 6.868101 -0.001899

The spread for Extended is larger, due to the larger standard deviation in the original data. Here, and elsewhere unless noted, we use resamples for the bootstrap or for permutation tests.

| One-Sample Bootstrap |

| times Draw a sample of size with replacement from the original data (a bootstrap sample or resample). Compute the sample mean (or other statistic) for the resample. \ENDREPEATX The 10000 bootstrap statistics comprise the bootstrap distribution. Plot the bootstrap distribution. The bootstrap standard error is the standard deviation of the bootstrap distribution, . The bootstrap percentile confidence interval is the range of the middle 95% of the bootstrap distribution. The bootstrap bias estimate is mean of the bootstrap distribution, minus the observed statistic, . \REPEATX |

2.4 Two-Sample Bootstrap

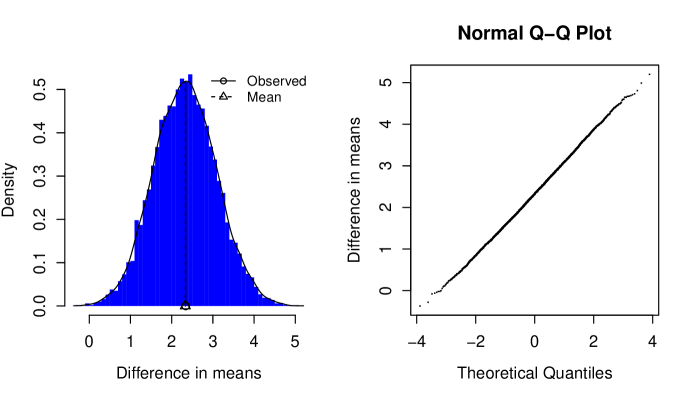

For a two-sample bootstrap, we independently draw bootstrap samples from each sample, and compute the statistic that compares the samples. For the TV commercials data, we draw a sample of size from Basic data, another sample of size from the Extended data, and compute the difference in means. The resulting bootstrap distribution is shown in Figure 3. The mean of the distribution is very close to the observed difference in means, ; the bootstrap standard error is , and the 95% bootstrap percentile confidence interval is . The interval does not include zero, which suggests that the difference between the samples is larger than can be explained by random variation; this is consistent with the permutation test above.

Recall that for the permutation test we resampled in a way that was consistent with the null hypothesis of no difference between populations, and the permutation distribution for the difference in means was centered at zero. Here we make no such assumption, and the bootstrap distribution is centered at the observed statistic; this is used for confidence intervals and standard errors.

2.5 Pedagogical Value

Like permutation tests, the bootstrap makes the abstract concrete. Concepts like sampling distributions, standard errors, bias, central limit theorem, and confidence intervals are abstract, and hard for many students, and this is usually compounded by a scary cookbook of formulas.

The bootstrap process, involving sampling, reinforces the central role that sampling from a population plays in statistics. Sampling variability is visible, and it is natural to measure the variability of the bootstrap distribution using the interquartile range or the standard deviation; the latter is the bootstrap standard error. Students can see if the sampling distribution has a bell-shaped curve. It is natural to use the middle 95% of the distribution as a 95% confidence interval. Students can obtain the confidence interval by working directly with the statistic of interest, rather than using a statistic.

The bootstrap works the same way with a wide variety of statistics. This makes it easy for students to work with a variety of statistics without needing to memorize more formulas.

The bootstrap can also reinforce the understanding of formula methods, and provide a way for students to check their work. Students may know the formula without understanding what it really is; but they can compare it to the bootstrap standard error, and see that it measures how the sample mean varies due to random sampling.

The bootstrap lets us do better statistics. In Stat 101 we talk early on about means and medians for summarizing data, but ignore the median later, like a crazy uncle hidden away in a closet, because there are no easy formulas for confidence intervals. Students can bootstrap the median or trimmed mean as easily as the mean. We can use robust statistics when appropriate, rather than only using the mean.

You do not need to talk about statistics and intervals at all, though you will undoubtedly want to do so later. At that point you may introduce another quick-and-dirty confidence interval, the interval with bootstrap standard error, where is the bootstrap standard error. (This is not to be confused with the bootstrap interval, see Section 5.5.)

| Pedagogical Value of the Bootstrap |

| Make abstract concepts concrete—sampling distribution, standard error, bias, central limit theorem. The process mimics the role of random sampling in real life. Use familiar tools, like histograms and normal quantile plots. Easy, intuitive confidence interval—bootstrap percentile interval. Work with the statistic of interest, e.g. difference of means. Generalizes to other statistics, don’t need new formulas. Can check answers obtained using formulas. |

2.6 Teaching Tips

For both bootstrapping and permutation tests, start small, and let students do some samples by hand. For permutation tests, starting with small groups like 2 and 3 allows students to do all partitions exhaustively.

There is a nice visualization of the process of permutation testing as part of the iNZight package <https://www.stat.auckland.ac.nz/~wild/iNZight>. It demonstrates the whole process: pooling the data, then repeatedly randomly splitting the data and calculating a test statistic, to build up the permutation distribution.

2.7 Practical Value

Resampling is also important in practice, often providing the only practical way to do inference. I’ll give some examples from Google, from my work or others.

In Google Search we estimate the average number of words per query, in every country (Chamandy, 2014). The data is immense, and is “sharded”—stored on tens of thousands of machines. We can count the number of queries in each country, and the total number of words in queries in each country, by counting on each machine and adding across machines, using MapReduce (Dean and Ghemawat, 2008). But we also want to estimate the variance, for users in each country, in words per query per user. The queries for each user are sharded, and it is not feasible to calculate queries and words for every user. But there is a bootstrap procedure we can use. In the ordinary bootstrap, the number of times each observation is included in a bootstrap sample is , which we approximate as . For each user, we generate Poisson values, one for each resample. We don’t actually save these, instead they are generated on the fly, each time the user comes up on any machine, using a random number seed generated from the user’s cookie, so the user gets the same numbers each time. We then compute weighted counts using the Poisson weights, to estimate the variance across users of words per query.

Also in Search, we continually run hundreds of experiments, trying to improve search results, speed, usability, and other factors; each year there are thousands of experiments resulting in hundreds of improvements111http://www.businessweek.com/the_thread/techbeat/archives/2009/10/google_search_g.html (when you search on Google you are probably in a dozen or more experiments). The data are sharded, and we cannot combine results for each user. We split the users into 20 groups, and analyze the variability across these groups using the jackknife (another resampling technique).

In Brand Lift222https://www.thinkwithgoogle.com/products/brand-lift.html. Chan et al. (2010) describe an earlier version. we use designed experiments to estimate the effectiveness of display advertisements. We ask people brand awareness questions such as which brands they are familiar with, to see whether the exposed (treatment) and control groups differ. There are four nested populations:

- (1)

-

people who saw an ad (and control subjects who would have seen one),

- (2)

-

those eligible for solicitation (they visit a website where the survey can be presented),

- (3)

-

those randomly selected for solicitation,

- (4)

-

respondents.

We use two logistic regression models:

- (A)

-

data = (4), Y = actual response,

- (B)

-

data = (4,3), Y = actual response or predictions from (A),

with ’s such as age and gender to correct for random differences in these covariates between exposed and controls. We use predictions from model (A) to extrapolate to (2–3), and predictions from model (B) to extrapolate to (1). The estimated average ad effect is the difference, across exposed people, of , where is the usual prediction, and is the prediction if the person were a control. Formula standard errors for this process are theoretically possible but difficult to derive, and would need updating when we change the model; we bootstrap instead.

For the People Analytics gDNA333http://blogs.hbr.org/2014/03/googles-scientific-approach-to-work-life-balance-and-much-more/ longitudinal survey, we use 5-fold cross-validation (another resampling technique) to evaluate a messy variable selection routine: multiple-imputation followed by backward-elimination in a linear mixed effects model. The models produced within each fold give an indication of the stability of the final result, and we calculate precision, recall, and accuracy on the holdout sets.

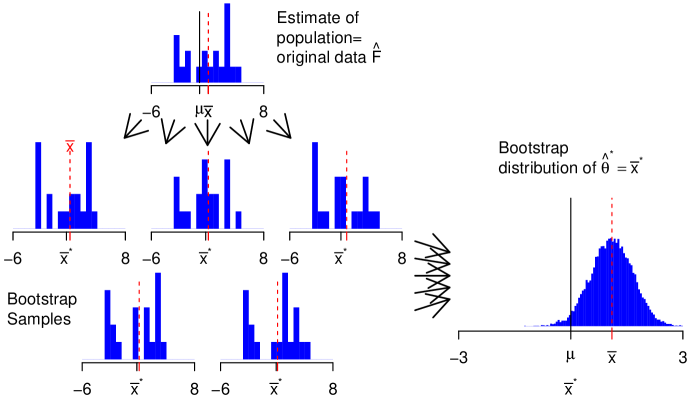

2.8 Idea behind Bootstrapping

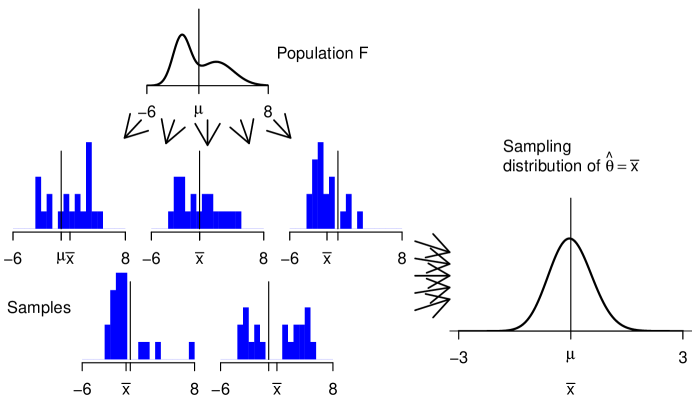

At this point you may have a million questions, but foremost among them is probably: why does this work? We’ll address that next by talking about the key idea behind the bootstrap, saving other questions for later.

Much of inferential statistics requires estimating something about the sampling distribution, e.g. standard error is an estimate of the standard deviation of that distribution. In principle, the sampling distribution is obtained by

-

Draw samples from the population.

-

Compute the statistic of interest for each sample (such as the mean, median, etc.)

-

The distribution of the statistics is the sampling distribution.

This is shown in Figure 4.

The problem with this is that we cannot draw arbitrarily many samples from the population—it is too expensive, or infeasible because we don’t know the population. Instead, we have only one sample. The bootstrap idea is to draw samples from an estimate of the population, in lieu of the population:

-

Draw samples from an estimate of the population.

-

Compute the statistic of interest for each sample.

-

The distribution of the statistics is the bootstrap distribution.

This is shown in Figure 5.

Plug-in Principle

The bootstrap is based on the plug-in principle—if something is unknown, then substitute an estimate for it. This principle is very familiar to statisticians. For example, the variance for the sample mean is ; when is unknown we substitute an estimate , the sample standard deviation. With the bootstrap we take this one step farther—instead of plugging in an estimate for a single parameter, we plug in an estimate for the whole distribution.

What to Substitute

This raises the question of what to substitute for . Possibilities include:

- Nonparametric bootstrap:

-

The common bootstrap procedure, the nonparametric bootstrap, consists of drawing samples from the empirical distribution (with probability on each observation), i.e. drawing samples with replacement from the data. This is the primary focus of this article.

- Smoothed Bootstrap:

-

When we believe the population is continuous, we may draw samples from a smooth population, e.g. from a kernel density estimate of the population.

- Parametric Bootstrap:

-

In parametric situations we may estimate parameters of the distribution(s) from the data, then draw samples from the parametric distribution(s) with those parameters.

We discuss these and other methods below in Section 6.

Fundamental Bootstrap Principle

The fundamental bootstrap principle is that this substitution works. In most cases, the bootstrap distribution tells us something useful about the sampling distribution.

There are some things to watch out for, ways that the bootstrap distribution cannot be used for the sampling distribution. We discuss some of these below, but one is important enough to mention immediately:

Inference, Not Better Estimates

The bootstrap distribution is centered at the observed statistic, not the population parameter, e.g. at , not .

This has two profound implications. First, it means that we do not use the bootstrap to get better estimates444 There are exceptions, where the bootstrap is used to obtain better estimates, for example in random forests. These are typically where a bootstrap-like procedure is used to work around a flaw in the basic procedure. For example, consider estimating where the true relationship is smooth, but you are limited to using a step function with relatively few steps. By taking bootstrap samples and applying the step function estimation procedure to each, the step boundaries vary between samples; by averaging across samples the few large steps are replaced by many smaller ones, giving a smoother estimate. This is bagging (bootstrap aggregating). . For example, we cannot use the bootstrap to improve on ; no matter how many bootstrap samples we take, they are always centered at , not . We’d just be adding random noise to . Instead we use the bootstrap to tell how accurate the original estimate is.

Some people are suspicious of the bootstrap, because they think the bootstrap creates data out of nothing. (The name “bootstrap” doesn’t help, since it implies creating something out of nothing.) The bootstrap doesn’t create all those bootstrap samples and use them as if they were more real data; instead it uses them to tell how accurate the original estimate is.

In this regard it is no different than formula methods that use the data twice—once to compute an estimate, and again to compute a standard error for the estimate. The bootstrap just uses a different approach to estimating the standard error.

The second implication is that we do not use quantiles of the bootstrap distribution of to estimate quantiles of the sampling distribution of . Instead, we use the bootstrap distribution to estimate the standard deviation of the sampling distribution, or the expected value of . Later, in Sections 5.4 and 5.5, we will use the bootstrap to estimate quantiles of and .

Second Bootstrap Principle

The second bootstrap principle is to sample with replacement from the data.

Actually, this isn’t a principle at all, but an implementation detail. We may sample from a parametric distribution, for example. And even for the nonparametric bootstrap, we sometimes avoid random sampling. There are possible samples, or if order doesn’t matter; if is small we could evaluate all of these. In some cases, like binary data, the number of unique samples is smaller. We’ll call this a theoretical bootstrap or exhaustive bootstrap. But more often this is infeasible, so we draw say 10000 random samples instead; we call this the Monte Carlo implementation or sampling implementation.

We talk about how many samples to draw in Section 3.6.

How to Sample

Normally we should draw bootstrap samples the same way the sample was drawn in real life, e.g. simple random sampling, stratified sampling, or finite-population sampling.

There are exceptions to that rule, see Section 6. One is important enough to mention here—to condition on the observed information. For example, when comparing samples of size and , we fix those numbers, even if the original sampling process could have produced different counts.

We can also modify the sampling to answer what-if questions. Suppose the original sample size was 100, but we draw samples of size 200. That estimates what would happen with samples of that size—how large standard errors and bias would be, and how wide confidence intervals would be. (We would not actually use the confidence intervals from this process as real confidence intervals; they would imply more precision than our sample of 100 provides.) Similarly, we can bootstrap with and without stratification and compare the resulting standard errors, to investigate the value of stratification.

Hypothesis testing is another what-if question—if the population satisfies , what would the sampling distribution (the null distribution) look like? We may bootstrap in a way that matches , by modifying the population or the sampling method; see Section 7.4.

| Idea Behind the Bootstrap |

| The idea behind the bootstrap is to estimate the population, then draw samples from that estimate, normally sampling the same way as in real life. The resulting bootstrap distribution is an estimate of the sampling distribution. We use this for inferences, not to obtain better estimates. It is centered at the statistic (e.g. ) not the parameter (). |

3 Variation in Bootstrap Distributions

I claimed above that the bootstrap distribution usually tells us something useful about the sampling distribution, with exceptions. I elaborate on that now with a series of visual examples, starting with one where things generally work well, and three with problems.

The examples illustrate two questions:

-

How accurate is the theoretical (exhaustive) bootstrap?

-

How accurately does the Monte Carlo implementation approximate the theoretical bootstrap?

Both reflect random variation:

-

The original sample is chosen randomly from the population.

-

Bootstrap resamples are chosen randomly from the original sample.

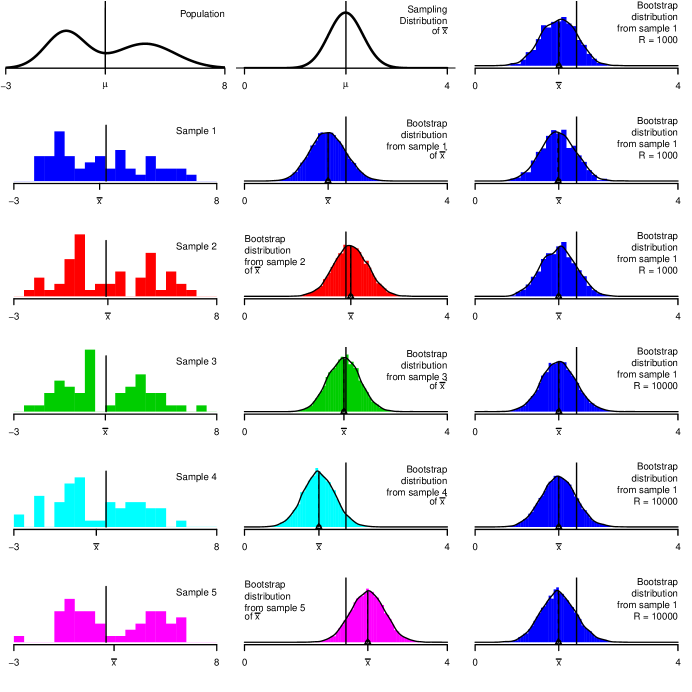

3.1 Sample Mean, Large Sample Size:

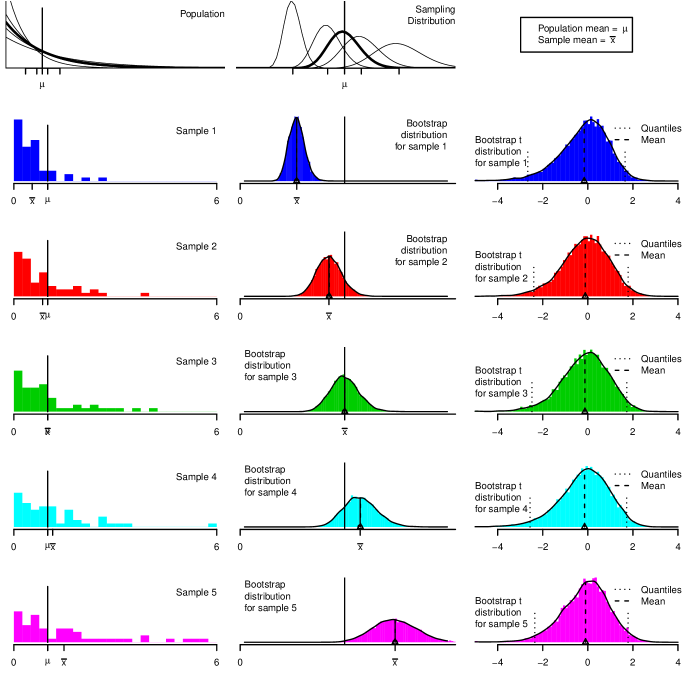

Figure 6 shows a population and five samples of size 50 from the population in the left column. The middle column shows the sampling distribution for the mean and bootstrap distributions from each sample, based on bootstrap samples. Each bootstrap distribution is centered at the statistic () from the corresponding sample rather than being centered at the population mean . The spreads and shapes of the bootstrap distributions vary a bit but not a lot.

This informs what the bootstrap distributions may be used for. The bootstrap does not provide a better estimate of the population parameter, because no matter how many bootstrap samples are used, they are centered at , not . Instead, the bootstrap distributions are useful for estimating the spread and shape of the sampling distribution.

The right column shows additional bootstrap distributions from the first sample, with or resamples. Using more resamples reduces random Monte Carlo variation, but does not fundamentally change the bootstrap distribution—it still has the same approximate center, spread, and shape.

The Monte Carlo variation is much smaller than the variation due to different original samples. For many uses, such as quick-and-dirty estimation of standard errors or approximate confidence intervals, resamples is adequate. However, there is noticeable variability, particularly in the tails of the bootstrap distributions, so when accuracy matters, or more samples should be used.

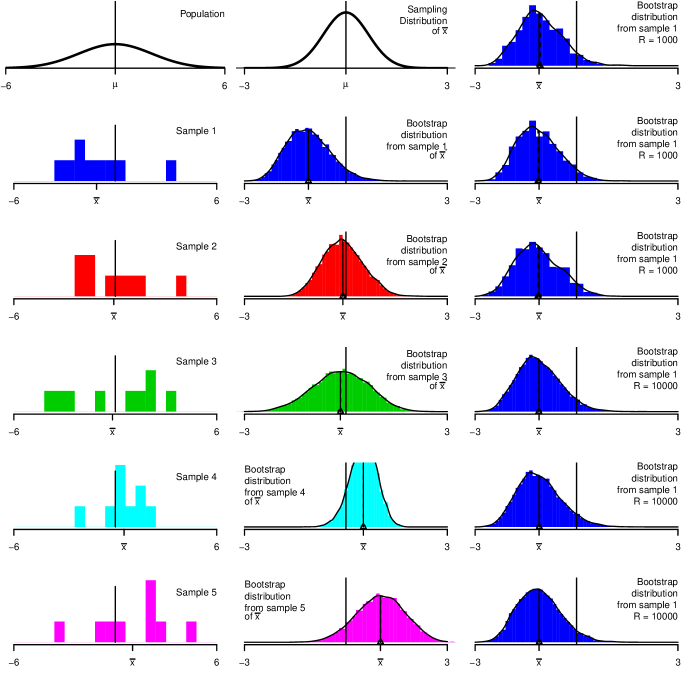

3.2 Sample Mean: Small Sample Size

Figure 7 is similar to Figure 6, but for a smaller sample size, (and a different population). As before, the bootstrap distributions are centered at the corresponding sample means, but now the spreads and shapes of the bootstrap distributions vary substantially, because the spreads and shapes of the samples vary substantially. As a result, bootstrap confidence interval widths vary substantially (this is also true of non-bootstrap confidence intervals). As before, the Monte Carlo variation is small and may be reduced with more samples.

While not apparent in the pictures, bootstrap distributions tend to be too narrow, by a factor of for the mean; the theoretical bootstrap standard error is . The reason for this goes back to the plug-in principle; the empirical distribution has variance , not . For example, the bootstrap standard error for the TV Basic mean is , while .

In two-sample or stratified sampling situations, this narrowness bias depends on the individual sample or strata sizes, not the combined size. This can result in severe narrowness bias. For example, the first bootstrap short course I ever taught was for the U.K. Department of Work and Pensions, who wanted to bootstrap a survey they had performed to estimate welfare cheating. They used a stratified sampling procedure that resulted in two subjects in each stratum—then the bootstrap standard error would be too small by a factor of . There are remedies, see Section 6. For Stat 101 I recommend warning students about the issue; for higher courses you may discuss the remedies.

The narrowness bias and the variability in spread affect confidence interval coverage badly in small samples, see Section 5.2.

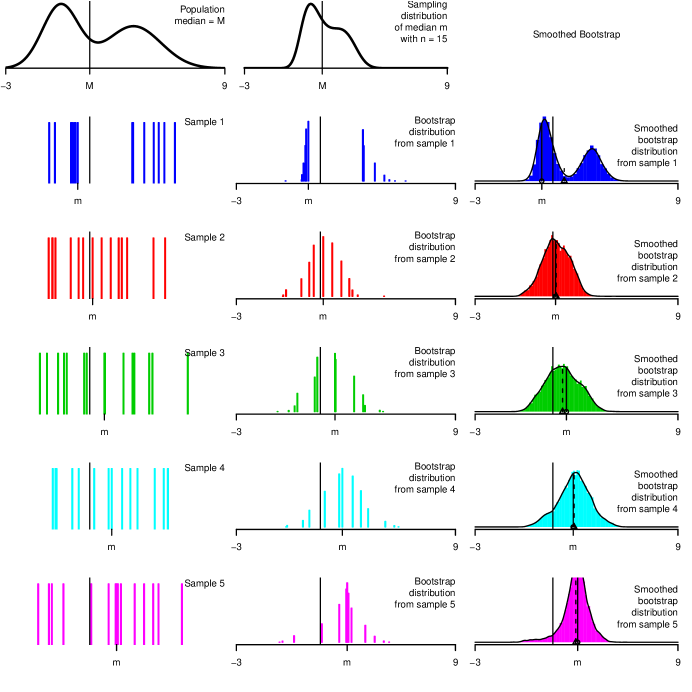

3.3 Sample Median

Now turn to Figure 8 where the statistic is the sample median. Here the bootstrap distributions are poor approximations of the sampling distribution. The sampling distribution is continuous, but the bootstrap distributions are discrete—since is odd, the bootstrap sample median is always one of the original data points. The bootstrap distributions are very sensitive to the sizes of gaps among the observations near the center of the sample.

The ordinary bootstrap tends not to work well for statistics such as the median or other quantiles in small samples, that depend heavily on a small number of observations out of a larger sample; the bootstrap distribution in turn depends heavily on a small number of observations (though different ones in different bootstrap samples, so bootstrapping the median of large samples works OK). The shape and scale of the bootstrap distribution may be very different than the sampling distribution.

Curiously, in spite of the ugly bootstrap distribution, the bootstrap percentile interval for the median is not bad (Efron, 1982). For odd , percentile interval endpoints fall on one of the observed values. Exact interval endpoints also fall on one of the observed values (order statistics), and for a 95% interval those are typically the same or adjacent order statistics as the percentile interval.

The right column shows the use of a smoothed bootstrap (Silverman and Young, 1987; Hall et al., 1989), drawing samples from a density estimate based on the data, rather than drawing from the data itself. See Section 6.3. It improves things somewhat, though it is still not great.

The bootstrap fails altogether for estimating the sampling distribution for .

3.4 Mean-Variance Relationship

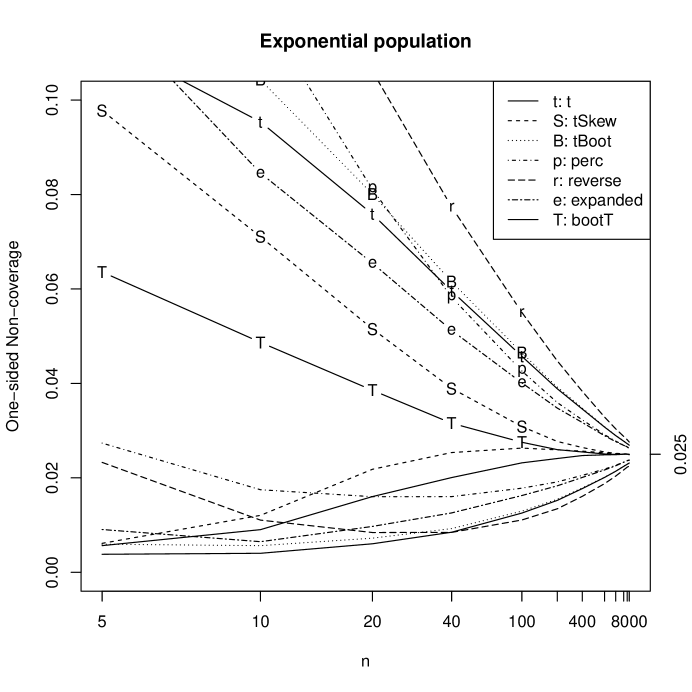

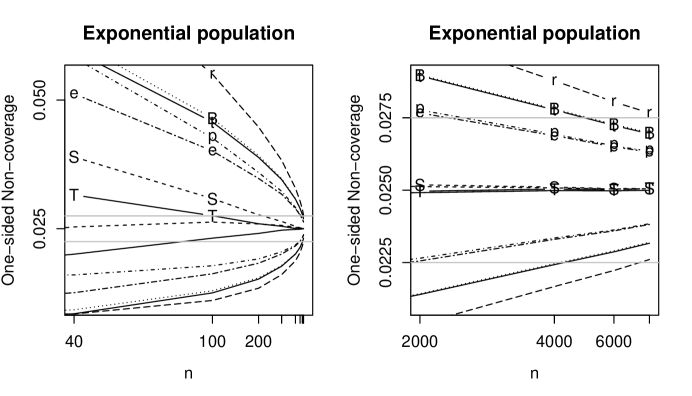

In many applications, the spread or shape of the sampling distribution depends on the parameter of interest. For example, the binomial distribution spread and shape depend on . Similarly, for the mean from an exponential distribution, the standard deviation of the sampling distribution is proportional to the population mean.

This is reflected in bootstrap distributions. Figure 9 shows samples and bootstrap distributions from an exponential population. There is a strong dependence between and the corresponding bootstrap SE.

This has important implications for confidence intervals; good confidence intervals need to reach many (short) SE’s to the right to avoid missing too often in that direction, and should reach fewer (long) SE’s to the left. We discuss this more in Section 5.

This mean-variance relationship in samples normally corresponds to a similar mean-variance relationship between the parameter and variance of the sampling distribution. For example, see the five sampling distributions in the top middle of Figure 9. We call such a relationship acceleration.

The right column of Figure 9 shows bootstrap distributions of the statistic, defined in Section 5.5. These distributions are much less sensitive to the original sample.

There are other applications where sampling distributions depend strongly on the parameter; for example sampling distributions for chi-squared statistics depend on the non-centrality parameter. Similarly for statistics for estimating the number of modes of a population Use caution when bootstrapping in these applications; the bootstrap distribution may be very different than the sampling distribution.

3.5 Summary of Visual Lessons

The bootstrap distribution reflects the original sample. If the sample is narrower than the population, the bootstrap distribution is narrower than the sampling distribution.

Typically for large samples the data represent the population well; for small samples they may not. Bootstrapping does not overcome the weakness of small samples as a basis for inference.

Indeed, for the very smallest samples, you may not want to bootstrap; it may be better to make additional assumptions such as smoothness or a parametric family. When there is a lot of data (sampled randomly from a population) we can trust the data to represent the shape and spread of the population; when there is little data we cannot.

| Visual Lessons about Bootstrap Distributions |

| The bootstrap distribution reflects the data. For large samples the data represent the population well; for small samples they may not. The bootstrap may work poorly when the statistic, and sampling distribution, depend on a small number of observations. Using more bootstrap samples reduces the variability of bootstrap distributions, but does not fundamentally change the center, spread, or shape of the bootstrap distribution. |

Looking ahead, two things matter for accurate inferences:

-

how close the bootstrap distribution is to the sampling distribution (in this regard, the bootstrap has an advantage, judging from Figure 9);

-

some procedures better allow for the fact that there is variation in samples. For example, the usual formula tests and intervals allow for variation in by using in place of ; we discuss a bootstrap analog in Section 5.3.

It appears that the bootstrap resampling process using 1000 or more resamples introduces little additional variation, but for good accuracy use 10000 or more. Let’s consider this issue more carefully.

3.6 How many bootstrap samples?

We suggested above that using 1000 bootstrap samples for rough approximations, or or more for better accuracy. This is about Monte Carlo accuracy—how well the usual random sampling implementation of the bootstrap approximates the theoretical bootstrap distribution.

A bootstrap distribution based on random samples corresponds to drawing observations with replacement from the theoretical bootstrap distribution.

Brad Efron, inventor of the bootstrap, suggested in 1993 that , or even as few as , suffices for estimating standard errors and that is enough for confidence intervals (Efron and Tibshirani, 1993).

We argue that more resamples are appropriate, on two grounds. First, those criteria were developed when computers were much slower; with faster computers it is easier to take more resamples.

Second, those criteria were developed using arguments that combine the random variation due to the original random sample with the extra variation due to the Monte Carlo implementation. We prefer to treat the data as given and look just at the variability due to the implementation. Data is valuable, and computer time is cheap. Two people analyzing the same data should not get substantially different answers due to Monte Carlo variation.

Quantify accuracy by formulas or bootstrapping

We can quantify the Monte Carlo error in two ways—using formulas, or by bootstrapping. For example, in permutation testing we need to estimate the fraction of observations that exceed the observed value; the Monte Carlo standard error is approximately , where is the estimated proportion. (It is a bit more complicated because we add 1 to the numerator and denominator, but this is close.)

In bootstrapping, the bias estimate depends on , a sample average of values; the Monte Carlo standard error for this is where is the sample standard deviation of the bootstrap distribution.

We can also bootstrap the bootstrap! We can treat the bootstrap replicates like any old sample, and bootstrap from that sample. For example, to estimate the Monte Carlo SE for the 97.5% quantile of the bootstrap distribution (the endpoint of a bootstrap percentile interval), we draw samples of size from the observed values in the bootstrap distribution, compute the quantile for each, and take the standard deviation of those quantiles as the Monte Carlo SE.

For example, the 95% percentile interval for the mean of the CLEC data is (from resamples); the Monte Carlo standard errors for those endpoints are and . The syntax for this using the resample package (Hesterberg, 2014) is

bootCLEC <- bootstrap(CLEC, mean, B = 10000)

bootMC <- bootstrap(bootCLEC$replicates,

quantile(data, probs = c(.025, .975), type = 6))

(The resample package uses type=6 when computing quantiles, for more accurate confidence intervals.)

Need to be within 10%

Now, let’s use those methods to determine how large should be for accurate results. We consider two-sided 95% confidence intervals and tests with size 5%.

Consider tests first. We’ll determine the necessary to have a 95% chance that the Monte Carlo estimate of the -value is within 10% when the exhaustive one-sided -value is 2.5%, i.e. 95% chance that the estimated -value is between 2.25% and 2.75%.

For a permutation test, let be the true 2.5% quantile of the permutation distribution. Suppose we observe , so the true (exhaustive) -value is . The standard deviation for the estimated -value is , so we solve , or .

Similar results hold for a bootstrap percentile or bootstrap confidence interval. If is the true 2.5% quantile of the theoretical bootstrap distribution (for or , respectively), for to fall between 2.25% and 2.75% with 95% probability requires .

For a interval with bootstrap SE, should be large enough that variation in has a similar small effect on coverage. This depends on and the shape of the bootstrap distribution, but for a rough approximation we assume that (1) is large and hence we want 95% central probability that where is the standard deviation of the theoretical bootstrap distribution, and (2) the bootstrap distribution is approximately normal, so is approximately chi-squared with degrees of freedom. By the delta method, has approximate variance . For the upper bound, we set ; this requires . The calculation for the lower bound is similar, and a slightly smaller suffices.

Rounding up, we need for simulation variability to have only a small effect on the percentile and bootstrap , and for the with bootstrap SE. While students may not need this level of accuracy, it is good to get in the habit of doing accurate simulations. Hence I recommend for routine use. And, for statistical practice, if the results with are borderline, then increase to reduce the Monte Carlo error. We want decisions to depend on the data, not Monte Carlo variability in the resampling implementation.

We talk below about coverage accuracy of confidence intervals. Note that a large isn’t necessary for an interval to have the right coverage probability. With smaller , sometimes an interval is too short, sometimes too long, and it roughly balances out to give the same coverage as with larger . But that is like flipping a coin—if heads then compute a 96% interval and if tails a 94% interval; while it may have the right overall coverage, the endpoints are variable in a way that does not reflect the data.

| Use 10000 or More Resamples |

| When the true one-sided permutation test -value is 2.5%, we need to have a 95% chance that the estimated -value is between 2.25% and 2.75% (within 10% of the true value). Similarly, we need to reduce Monte Carlo variability in the percentile interval endpoints to 10%, and for a interval with bootstrap SE. We suggest for routine use, and more when accuracy matters. These recommendations are much larger than previous recommendations. Statistical decisions should depend on the data, not Monte Carlo variability. |

4 Transformation, Bias, and Skewness

Three important issues for estimation, confidence intervals, and hypothesis tests are transformations, bias (of the statistic) and skewness (of the population, and the sampling distribution). We’ll look at these in this section, and how they affect the accuracy of permutation tests and tests, and take a first look at how they affect confidence intervals, with a more complete look in the next section. We also discuss functional statistics, and how non-functional statistics can give odd results when bootstrapping.

4.1 Transformations

Table 2 gives rates of cardiovascular disease for subjects with high or low blood pressure. The high-blood pressure group was 2.12 times as likely to develop the disease.

| Blood Pressure | Cardiovascular Disease |

| High | 55/3338 = 0.0165 |

| Low | 21/2676 = 0.0078 |

| Relative risk | 2.12 |

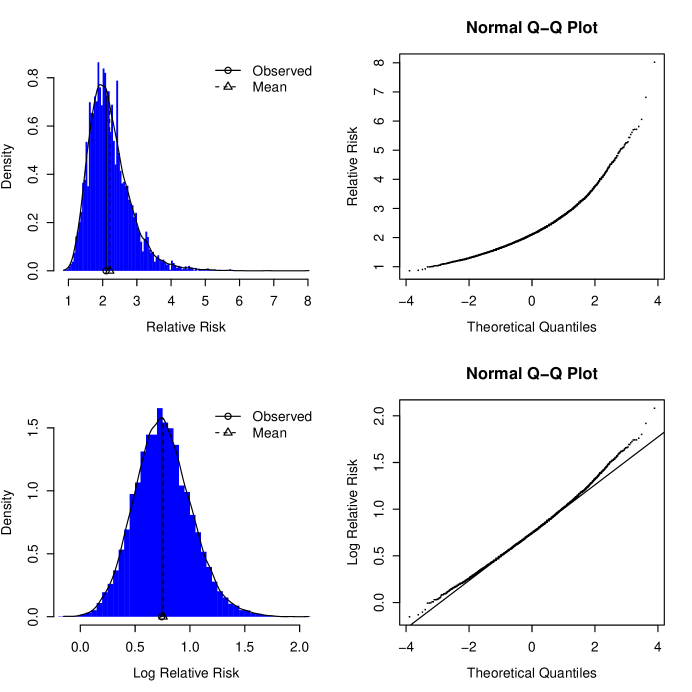

Figure 10 shows the bootstrap distribution for relative risk. The distribution is highly skewed, with a long right tail. Also shown is the bootstrap distribution for log relative risk; this is less skewed. Both distributions exhibit bias; the summary statistics are:

Observed SE Mean Bias

Relative Risk 2.0996 0.6158 2.2066 0.1070

Log Relative Risk 0.7417 0.2625 0.7561 0.0143

One desirable property for confidence intervals is transformation invariance—if is a monotone transformation and , a procedure is transformation invariant if the endpoints of the confidence interval for are and , where is the interval for . Transformation invariance means that people taking different approaches get equivalent results.

The bootstrap percentile interval is transformation invariant. If one student does a confidence interval for relative risk, and another for log relative risk, they get equivalent answers; the percentile interval for relative risk is , and for log-relative-risk is .

In contrast, a interval is not transformation invariant. The interval with bootstrap SE for relative risk is ; taking logs gives . Those differ from endpoints for log relative risk, .

Using an interval that is not transformation invariant means that you can choose the transformation to get the answer you want. Do it one way and the interval includes zero; do it the other way and the interval excludes zero.

4.2 Bias

The bootstrap estimate of bias derives from the plug-in principle. The bias of a statistic is

| (1) |

where indicates sampling from , and is the parameter for population . The bootstrap substitutes for , to give

| (2) |

The bias estimate is the mean of the bootstrap distribution, minus the observed statistic.

The relative risk and log relative risk statistics above are biased (see the summary statistics above).

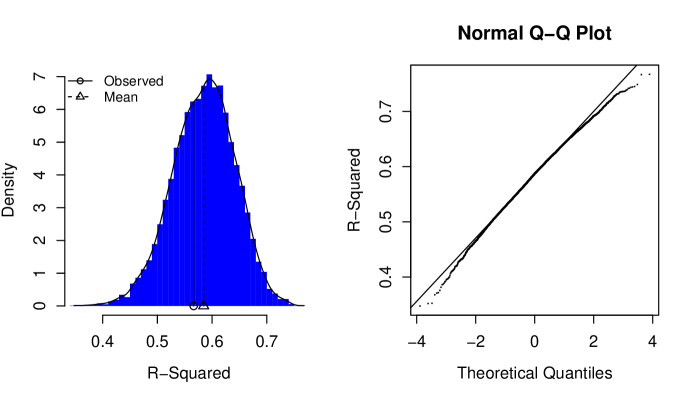

Regression R-Squared

Another example of bias is unadjusted R-squared in regression. Figure 11 shows a bootstrap for unadjusted for an artificial dataset with and . The summary statistics are:

Observed SE Mean Bias

R^2 0.5663851 0.05678944 0.5846771 0.01829191

4.2.1 Bias-Adjusted Estimates

We may use the bias estimate to produce a bias-adjusted estimate, .

We generally do not do this—bias estimates can have high variability, see (Efron and Tibshirani, 1993). Instead, just being aware that a statistic is biased may help us proceed more appropriately.

Bias is another reason that we do not use the bootstrap average in place of —it would have double the bias of .

The bootstrap BCa confidence interval (Efron, 1987) makes use of another kind of bias estimate, the fraction of the bootstrap distribution that is . This is not sensitive to transformations. It is related to median bias—a statistic is median unbiased if the median of the sampling distribution is .

4.2.2 Causes of Bias

There are three common causes of bias. In the first of these bias correction would be harmful, in the second it can be helpful, and in the third the bias would not be apparent to the bootstrap. The differences are also important for confidence intervals.

One cause of bias relates to nonlinear transformations, as in the relative risk example above; . In this case the median bias is near zero, but the mean bias estimate can be large and have high variability, and is strongly dependent on how close the denominator is to zero. Similarly, .

Similarly, is unbiased but is not; .

Another cause is bias due by optimization—when one or more parameters are chosen to optimize some measure, then the estimate of that measure is biased. The example falls into this category, where the regression parameters are chosen to maximize ; the estimated is higher than if we used the true unknown parameters, and the unadjusted is biased upward. Another example is sample variance. The population variance is . An unbiased estimate of that is . Replacing with the value that minimizes that quantity, , gives a biased estimate .

The optimization bias can be large in stepwise regression, where both the variable selection and parameter estimates optimize.

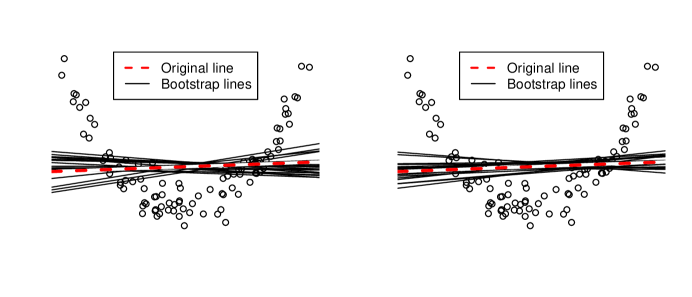

The third cause of bias is lack of model fit. Here the bootstrap may not even show that there is bias. It can only quantify the performance of the procedure you actually used, not what you should have used. For example, Figure 12 shows the result of fitting a line to data with obvious curvature. The bootstrap finds no bias—for any , the bootstrap lines are centered vertically around the original fit. We discuss this further when we consider regression, in Section 6.1.

| The Bootstrap Does Not Find Bias Due to Lack of Fit |

| The bootstrap does not show bias due to a poor model fit. Bootstrap bias estimates for non-functional statistics may be wrong. |

4.3 Functional Statistics

There is a subtle point in the bootstrap bias estimate (equation 2)—it assumes that and —in other words, that the statistic is functional, that it depends solely on the empirical distribution, not on other factors such as sample size. A functional statistic gives the same answer if each observation is repeated twice (because that does not change the empirical distribution). We can get odd results if not careful when bootstrapping non-functional statistics.

For example, the sample variance is not functional, while is. If is the variance of the population , then , the variance of the empirical distribution , with probability on each of the . is times the functional statistic.

Say the sample size is 10; then to the bootstrap, looks like , which it treats as an estimate for . The bootstrap doesn’t question why we want to analyze such an odd statistic; it just does it. Here is the result of bootstrapping for the Basic TV data:

Observed SE Mean Bias

stat1 1.947667 0.5058148 1.762771 -0.1848956

The observed value is , while the average of the bootstrap values of is ; the bias is negative. It concludes that is negatively biased for , i.e. that is downward biased for . If we’re not aware of what happened, we might think that the bootstrap says that is biased for .

Other non-functional statistics include adjusted R-squared in regression, scatterplot smoothing procedures, stepwise regression, and regularized regression.

Bootstrap SE estimates are not affected the same way as bias estimates, because they are calculated solely from the bootstrap statistics, whereas the bias estimate compares the bootstrap statistics to the observed statistic. Confidence intervals are affected—bootstrap procedures typically provide confidence bounds for functional statistics.

4.4 Skewness

Another important issue for the bootstrap, and inference in general, is skewness—skewness of the data for the mean, or more generally skewness of the empirical influence of the observations (Efron and Tibshirani, 1993).

Verizon Example

I consulted on a case before the New York Public Utilities Commission (PUC). Verizon was an Incumbent Local Exchange Carrier (ILEC), responsible for maintaining land-line phone service in certain areas. Verizon also sold long-distance service, as did a number of competitors, termed Competitive Local Exchange Carrier (CLEC). When something would go wrong, Verizon was responsible for repairs, and was supposed to make repairs as quickly for CLEC long-distance customers as for their own. The PUC monitored this by comparing repair times for Verizon and the various CLECs, for many different classes of repairs, and many different time periods. In each case a hypothesis test was performed at the 1% significance level, to determine whether repairs for a CLEC’s customers were significantly slower than for Verizon’s customers. There were hundreds of such tests. If substantially more than 1% of the tests were significant, then Verizon would pay a large penalty. These tests were performed using tests; Verizon proposed using permutation tests instead.

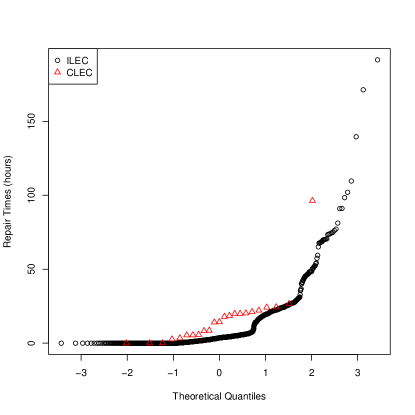

The data for one combination of period, class of service, and CLEC is shown in Table 3, and Figure 13. Both datasets are positively skewed. There are odd bends in the normal quantile plot, due to 24-hour periods (few repairs are made outside of normal working hours).

| n | mean | sd | |

|---|---|---|---|

| ILEC | 1664 | 8.41 | 16.5 |

| CLEC | 23 | 16.69 | 19.5 |

The mean CLEC repair time is nearly double that for ILEC—surely this must be evidence of discrimination? Well maybe not—the CLEC distribution contains one clear outlier, the difference would be less striking without the outlier. But even aside from the outlier, the CLEC repair times tend to be larger than comparable quantiles of the ILEC distribution.

Permutation Test

The permutation distribution for the difference in means is shown in Figure 14. The one-sided -value is , well above the 1% cutoff for these tests, see Table 4. In comparison, the pooled test -value is , about four times smaller. The unpooled -value is . Under the null hypothesis that the two distributions are the same, pooling is appropriate. In fact, the PUC mandated the use of a statistic with standard error calculated solely from the ILEC sample, to prevent large CLEC repair times from contaminating the denominator; this -value is even smaller.

| -value | ||

|---|---|---|

| Permutation test | 0.0171 | |

| Pooled test | 2.61 | 0.0045 |

| Welch test | 1.98 | 0.0300 |

| PUC test | 2.63 | 0.0044 |

So, given the discrepancy between the permutation test result and the various tests, which one is right? Absolutely, definitely, the permutation test. Sir Ronald Fisher originally argued for tests by describing them as a computationally-feasible approximation to permutation tests (known to be the right answer), given the computers of the time.We should not be bound by that limitation.

| Permutation and tests |

| Permutation tests are accurate. tests are a computationally feasible approximation to permutation tests, given the computers of the 1920’s—young women. |

tests assume normal populations, and are quite sensitive to skewness unless the two sample sizes are nearly equal. Permutation test make no distributional assumptions, and don’t care about biased statistics. Permutation test are “exact”—when populations are the same, the -value is very close to uniformly distributed; if there are no ties (different samples that give the same value of the statistic), then the exhaustive permutation distribution has mass on each of the possible values of the statistic, given the combined data. With random sampling the test is not quite exact, but with large is close.

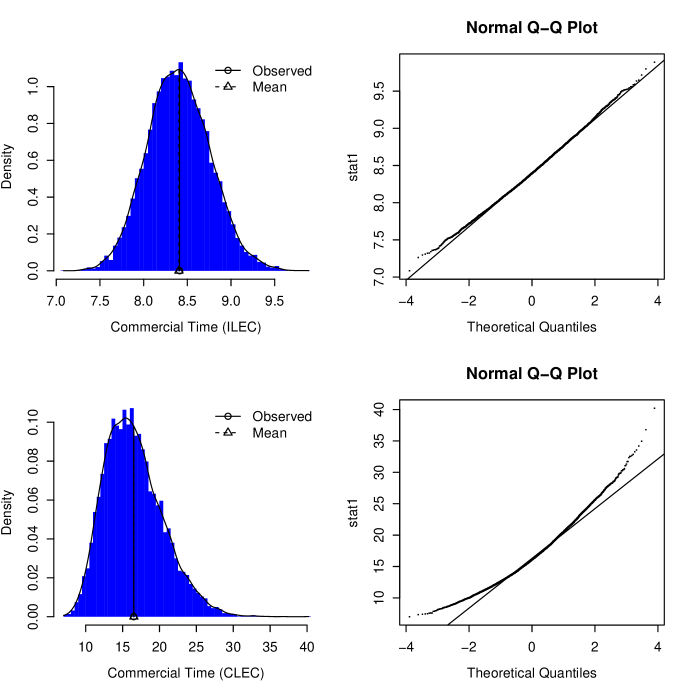

Bootstrap

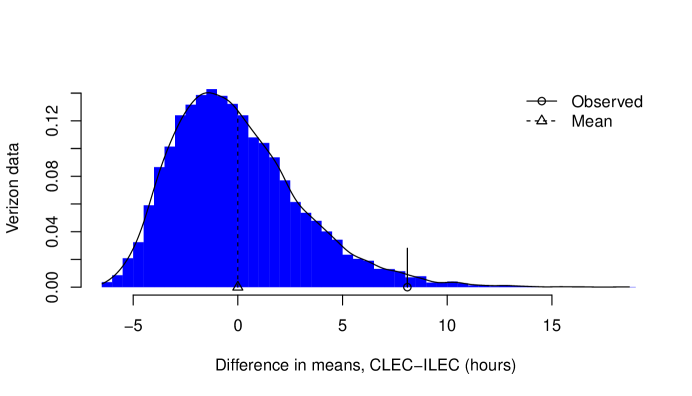

Figure 15 shows the bootstrap distributions for the ILEC and CLEC data. Each is centered at the corresponding observed mean. The CLEC distribution is much wider, reflecting primarily the much smaller sample size (a valuable lesson for students), and the larger sample standard deviation.

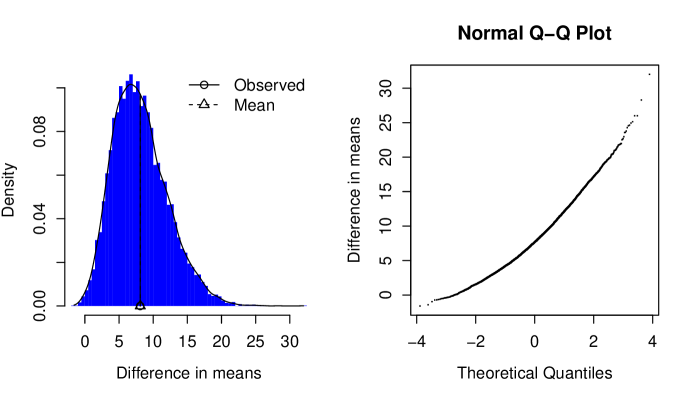

Figure 16 shows the bootstrap distributions for difference of means, CLEC - ILEC. This is centered at the observed difference in means. The SE reflects the contributions to the SE from both samples.

There is skewness apparent in the bootstrap distribution for the difference in means. Does that amount of skewness matter?

Before answering, I’ll share a story. I co-authored (Hesterberg et al., 2003)555A resampling chapter for an introductory statistics text; this and similar chapters can be freely downloaded, see http://www.timhesterberg.net/bootstrap. ; one homework question included a bootstrap distribution similar to Figure 16, and asked if the skewness mattered. The publisher had someone else write the first draft of the solutions, and his answer was that it did not.

That is dead wrong. His answer was based on his experience, using normal quantile plots to look at data. But this is a sampling distribution, not raw data. The Central Limit Theorem has already had its one chance to make things more normal. At this point, any deviations from normality will have bad effects on any procedure that assumes normal sampling distributions.

He’s not alone. I often ask that question during talks and courses, and typically over half of the audience answers that it is no problem.

That points out a common flaw in statistical practice—that we don’t often use effective ways to judge whether the CLT is really working, and how far off it is. To some extent the bootstrap distributions above provide this; the bootstrap distributions below are even more effective.

Even the skewness in the ILEC distribution, with 1664 observations, has a measurable effect on the accuracy of a interval for that data. A 95% interval misses by being too low about 39% too often (3.5% instead of 2.5%). Similarly, a percentile interval is too low about 28% too often. To reduce the 39% to a more reasonable 10% would require about 16 times as many observations. The Central Limit Theorem operates on glacial time scales. We return to this issue below.

Permutation test, not Pooled Bootstrap

We could perform a permutation test by pooling the data, then drawing bootstrap samples of size and with replacement from the pooled data. This sampling would be consistent with the null hypothesis.

It is not as accurate as the permutation test. Suppose, for example, that the data contain three outliers. The permutation test tells how common the observed statistic is, given that there are a total of three outliers. With a pooled bootstrap the number of outliers would vary, and the -value would not as accurately reflect the data we have.

4.5 Accuracy of the CLT and t Statistics

In the Verizon example the two-sample pooled-variance test was off by a factor of four, and the one-sample interval with missed 39% too often on one side. These are not isolated examples.

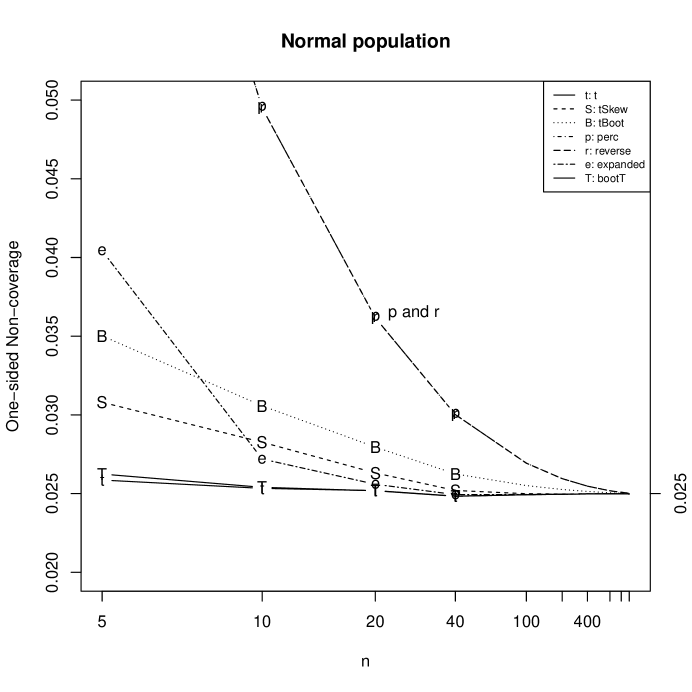

When there is skewness, the standard test and interval converge to the correct size and coverage very slowly, at the rate , with a large constant. (The corresponding constant for the percentile interval is about as large.) We can demonstrate this using simulation or asymptotic methods, see Figures 20–22 and Section 5.6.1.

| The CLT requires for a moderately skewed population |

| For tests and confidence intervals to be reasonably accurate (off by no more than 10% on each side) requires for a 95% interval or two-sided test, for an exponential population. The central limit theorem acts over glacial time scales, when skewness is present. |

The inaccuracy of procedures when there is skewness has been known since at least 1928 (Sutton, 1993), and a number of more accurate alternatives have been proposed, see e.g. (Johnson, 1978; Kleijnen et al., 1986; Sutton, 1993; Meeden, 1999), a number of bootstrap procedures discussed below, and undoubtedly others. Unfortunately, these have had little impact on statistical practice.

I think the reason is a combination of historical practicality and momentum. The simulations needed to accurately estimate error probabilities used to be too costly. Kleijnen et al. (1986) noted

Unfortunately, Monte Carlo experimentation requires much computer time. Obviously the number of replications needed to estimate the actual -error within 10% with 90% probability, is . Hence if is 0.1, 0.05, 0.01 then is 2435, 5140, 26786 respectively. Such high values are prohibitive, given our computer budget

I once estimated that some simulations I did related to confidence interval coverage would have taken about 20000 hours of computer time in 1981.

Then, there is momentum—the statistics profession got in the habit of using tests, with each person following the example of their instructors, and only perform what is provided in software. I plead guilty to that same inertia—it was not until I developed examples for (Hesterberg et al., 2003) that I started to pay attention to this issue.

The usual rule in statistics, of using classical methods if and the data are not too skewed, is imprecise and inadequate. For a start, we should look at normal (or ) quantile plots for bootstrap distributions; next, look at bootstrap distributions rather than , because is twice as skewed in the opposite direction and is biased. Finally, our eye can’t accurately judge effects on coverage probabilities from quantile plots, so we need to calculate rather than eyeball the effect on coverage or -values.

5 Confidence Intervals

We begin with some introductory material, then turn in Section 5.1 to a pair of pictures that help explain how confidence intervals should behave in the easy case (normal with no bias), and in harder cases (bias, and skewness/acceleration).

We then discuss different intervals. In Section 5.2 we recommend two easy intervals for Stat 101, the bootstrap percentile interval and the interval with bootstrap standard error.

Section 5.3 has an adjusted version of the percentile interval, to correct for too-low coverage.

In Sections 5.4 and 5.5 we turn to intervals for other courses and for practice, starting with an interval with a natural derivation for statisticians—that turns out to be terrible but with pedagogical value—then a better interval. We summarize in Section 5.6, including simulation and asymptotic results showing how well the intervals actually perform.

Accurate Confidence Intervals

A accurate confidence interval procedure includes the true value 95% of the time, and misses 2.5% of the time on each side. Different intervals, both formula and bootstrap, have trouble achieving this or even coming close, in different applications and with different sample sizes.

It is not correct for a 95% interval to miss 4% of the time on one side and 1% of the time on the other—in practice almost all statistical findings are ultimately one-sided, so making an error on one side does not compensate for an error on the other. It would be rare indeed to find a report that says, “my new way of teaching was significantly different in effectiveness than the control” without also reporting the direction!

Say that the right endpoint of an interval is too low, so the interval misses 4% of the time on that side. I’d rather have an interval that is correct on the other side than one that is too low—because the combination of being too low on both sides gives an even more biased picture about the location of . A biased confidence interval has endpoints that are too low, or too high, on both sides.

I am not arguing against two-sided tests, or two-sided confidence intervals. In most cases we should be receptive to what the data tell us, in either direction. My point is that those two-sided procedures should have the correct probabilities on both sides, so that we correctly understand what the data says.

As for so-called “shortest intervals”, that intentionally trade under-coverage on one side for over-coverage on the other, to reduce the length—that is statistical malpractice, and anyone who uses such intervals should be disbarred from Statistics and sentenced to 5 years of listening to Justin Bieber crooning.

| Accurate Confidence Intervals |

| An accurate 95% confidence interval misses 2.5% of the time on each side. An interval that under-covers on one side and over-covers on the other is biased. |

First and Second Order Accurate

A hypothesis test or confidence interval is first-order accurate if the one-sided actual rejection probabilities or one-sided non-coverage probabilities differ from the nominal values by . They are second-order accurate if the differences are .

The usual intervals and tests, percentile, and interval with bootstrap standard errors are first-order accurate. The bootstrap and skewness-adjusted interval (see Section 5.6.2) are second-order accurate.

These statements assume certain regularity conditions, and apply to many common statistics, e.g. smooth functions of sample moments (for example, the correlation coefficient can be written as a function of ), smooth functions of solutions to smooth estimating equations (including most maximum likelihood estimators), and generalized linear models. For details see (Efron and Tibshirani, 1993; Davison and Hinkley, 1997; DiCiccio and Romano, 1988; Hall, 1988, 1992).

There are many other bootstrap confidence intervals; in the early days of the bootstrap there was quite a cottage industry, developing second-order accurate or even higher order intervals. Some are described in (Efron and Tibshirani, 1993; Davison and Hinkley, 1997); for a review see DiCiccio and Efron (1996).

To be second-order accurate, a procedure needs to handle bias, skewness, and transformations.

But just being second-order accurate isn’t enough in practice; an interval should also have good small-sample performance. A first-order accurate interval can be better in small samples than a second-order accurate interval, if it handles the “little things” better—things that have an effect on coverage, with little effect for large , but that matter for small . We’ll see below that the bootstrap percentile interval is poor in this regard, and has poor accuracy in small samples.

| First and Second-Order Accurate Inferences |

| A hypothesis test or confidence interval is first-order accurate if the one-sided actual rejection probabilities or one-sided non-coverage probabilities differ from the nominal values by . They are second-order accurate if the differences are . To be second-order accurate, a procedure needs to handle bias, skewness, and transformations. |

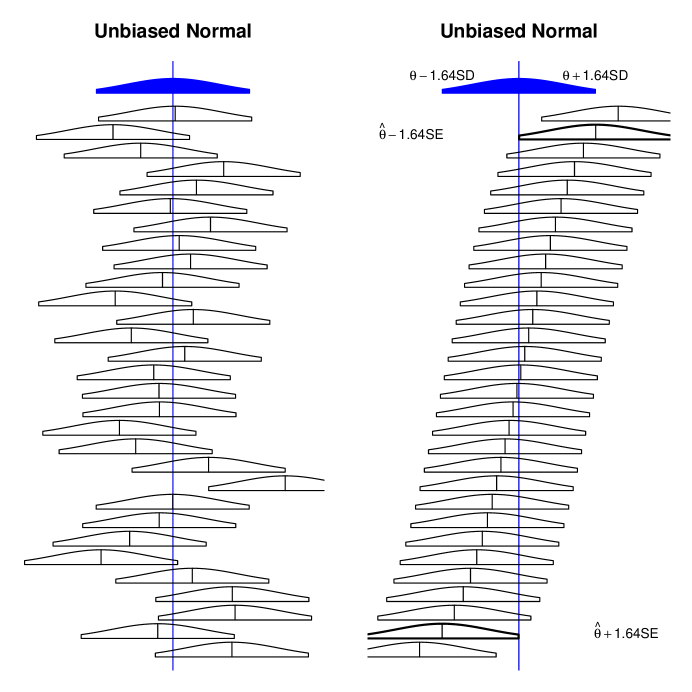

5.1 Confidence Interval Pictures

Here are some pictures that show how confidence intervals should behave in different circumstances.

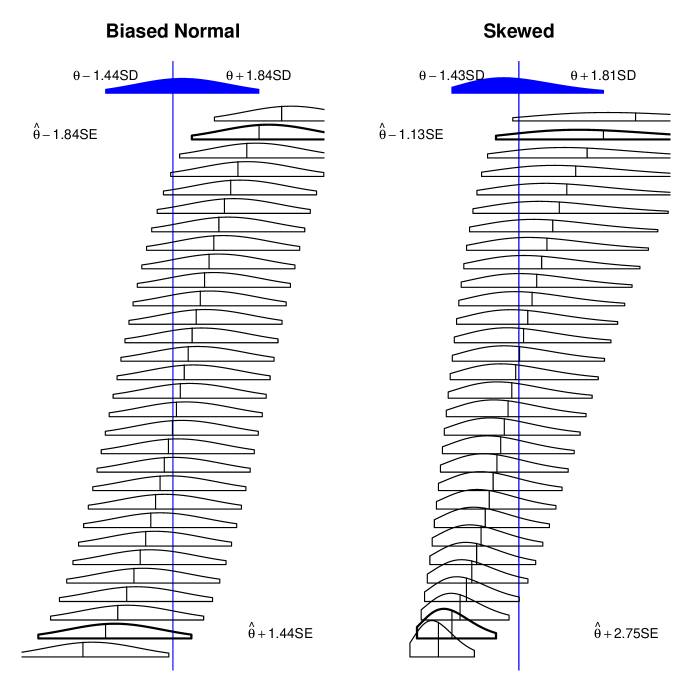

In all cases the parameter is shown with a vertical line, the sampling distribution is on the top, and below that are bootstrap distributions. In the right side of Figure 17 and both sides of Figure 18, the confidence intervals for the samples that are second from top and from bottom should just touch the parameter, those in between should include the parameter, and the top and bottom ones should miss the parameter.

Figure 17 shows what happens in the nice case, of normally-distributed sampling distributions with no bias (and to make things simple, with known variance). Each bootstrap distribution is centered about the statistic for its sample. The bootstrap percentile interval and -interval coincide, and each misses exactly the right fraction of the time on each side.

Simple Bias

The left side of Figure 18 shows what happens when there is simple bias, similar to that of unadjusted R-squared. The statistic is positively biased; the bootstrap distributions are similarly biased. The bias is where . A correct interval would be , or .

intervals are symmetric about the corresponding statistic, so end up with one copy of the bias (from the bias in the original statistic). The intervals miss too often by being above , and not often enough below .

Bootstrap percentile intervals are even worse, because they get a second copy of the bias (the original bias, and bootstrap bias). A bias-corrected percentile interval would subtract twice the bias from the percentile interval endpoints.

Skewness

The right side of Figure 18 shows what happens for unbiased statistics when the distribution is skewed; in this case, the mean of a gamma distribution with shape 9. The sampling distribution has roughly the same asymmetry as in the bias example.

The bootstrap distributions show the same asymmetry; the middle 90% (the 90% bootstrap percentile interval) is .

A correct interval is (see the text beside the bold curves). A correct interval needs to reach many (short) standard errors to the right to avoid missing too often when and standard errors are small.

This time the bootstrap percentile misses too often by being below , and not often enough by being above. Even though the interval is asymmetrical, it is not asymmetrical enough.

A interval is even worse.

See Section 5.6.2 below for a skewness-corrected interval obtained using asymptotic methods; the percentile interval has only about one-third the asymmetry of this interval (asymptotically, for 95% intervals).

| Confidence Intervals for Skewed Data |

| When the data are skewed, a correct interval is even more asymmetrical than the bootstrap percentile interval—reaching farther toward the long tail. |

Failure of intuition

This runs counter to our intuition. If we observe data with large observations on the right, our intuition may be to downweight those observations, and have the confidence interval reach farther left, because the sample mean may be much larger than the true mean. In fact, when the data show that the population has a long right tail, a good confidence interval must protect against the possibility that we observed fewer than average observations from that tail, and especially from the far right tail. If we’re missing those observations, then is too small, and is also too small, so the interval must reach many standard errors to the right.

Conversely, we may have gotten more observations from the right tail than average, and the observed mean is too large—but in that case the standard error is inflated, so we don’t need to reach so many standard errors to reach the parameter.

Transformations

The 90% endpoints of the bootstrap distributions had roughly the same asymmetry in the bias and skewness examples: vs . We could get the same asymmetry by applying a nonlinear transformation to the case of normal with no bias, with . This gives sampling distributions and bootstrap distributions with the same asymmetry as the bias example, . In this case a bootstrap percentile interval would be correct, and a interval would not.

Need more information

We can’t tell just from the asymmetry of the endpoints whether a correct interval should be asymmetrical to the right or left. The correct behavior depends on whether the asymmetry is caused by bias, skewness, transformations, or a combination. We need more information—and second-order accurate bootstrap confidence interval procedures collect and use that information, explicitly or implicitly.

But lacking that information, the percentile interval is a good compromise, with transformation invariance and a partial skewness correction.

| Need More Information for Accurate Intervals |

| Asymmetric bootstrap distributions could be caused by bias, skewness, transformations, or a combination. The asymmetry of a correct confidence interval differs, depending on the cause. Second-order accurate bootstrap confidence intervals are based on additional information. In the absence of more information, a percentile interval is a reasonable compromise. |

5.2 Statistics 101—Percentile, and T with Bootstrap SE

For Stat 101 I would stick with the two quick-and-dirty intervals mentioned earlier: the bootstrap percentile interval, and the interval with bootstrap standard error . If using software that provides it, you may also use the expanded bootstrap percentile interval, see Section 5.3.

The percentile interval will be more intuitive for students. The with bootstrap standard error helps them learn formula methods.

Students can compute both and compare. If they are similar, then both are probably OK. Otherwise, if their software computes a more accurate interval they could use that. If the data are skewed, the percentile interval has an advantage. If is small, the interval has an advantage.

Both intervals are poor in small samples—they tend to be too narrow. The bootstrap standard error is too small, by a factor so the interval with bootstrap SE is too narrow by that factor; this is the narrowness bias discussed in Section 3.2.

The percentile interval suffers the same narrowness and more—for symmetric data it is like using in place of . It is also subject to random variability in how skewed the data is. This adds random variability to the interval endpoints, similar to the effect of randomness in the sample variance , and reduces coverage.

These effects are (effect on coverage probability) or smaller, so they become negligible fairly quickly as increases. For larger , these effects are overwhelmed by the effect of skewness, bias, and transformations. But they matter for small , see Table 5, and the confidence interval coverage in Figures 20 and 21.

| size | ||||

|---|---|---|---|---|

In practice, the with bootstrap standard error offers no advantage over a standard procedure, for the sample mean. Its advantages are pedagogical, and that it can be used for statistics where there are no easy standard error formulas.

In Stat 101 it may be best to avoid the small-sample problems by using examples with larger .

Alternately, you could use software that corrects for the small-sample problems. See the next section.

| Simple Intervals for Stat 101; Poor Coverage for Small |

| I recommend two intervals for Stat 101—the bootstrap percentile interval provides an intuitive introduction to confidence intervals, and the interval with bootstrap standard error as a bridge to formula intervals. However, these intervals are too short in small samples, especially the percentile interval. It is like using as a confidence interval for . People think of the bootstrap (and bootstrap percentile interval) for small samples, and classical methods for large samples. That is backward, because the percentile interval is too narrow for small samples. The interval is more accurate than the percentile interval for , for exponential populations. |

5.3 Expanded Percentile Interval

The bootstrap percentile interval performs poorly in small samples, because of the narrowness bias, and because it lacks a fudge factor to allow for variation in the standard error. The standard interval handles both, using in place of to avoid narrowness bias, and in place of as a fudge factor to allow for variation in . We can interpret the interval as multiplying the length of a reasonable interval, , by , to provide better coverage. This multiplier is the inverse of the product of columns 2–3 of Table 5.

The fact that the interval is exact for normal populations is a bit of a red herring—real populations are never exactly normal, and the multiplier isn’t correct for other populations. Yet we continue to use it, because it helps in practice. Even for long-tailed distributions, where the fudge factor should be larger, using at least a partial fudge factor helps. (For binomial data we do use instead of , because given there is zero uncertainty in the variance.)

Similarly, we may take a sensible interval, the percentile interval, and adjust it to provide better coverage for normal populations, and this will also help for other populations.

A simple adjustment is to multiply both sides of a percentile interval by . But that would not be transformation invariant.

We can achieve the same effect, while not losing transformation invariance, by adjusting the percentiles. If the bootstrap distribution is approximately normal then ^G^-1(α/2) ≈^θ- z_α/2^σ/n. We want to find an adjusted value with

This gives , or . The values of are given in Table 5. For a nominal one-sided level of , the adjusted values range from at to for .

Coverage using the adjusted levels is dramatically better, see (Hesterberg, 1999) and Figure 20, though is still poor with .

This adjustment has no terms for bias or skewness; it only counteracts the narrowness bias and provides a fudge factor for uncertain width. Still, we see in Figure 21 that it also helps for skewness.

This technique of using modified quantiles of the bootstrap distribution is motivated by the bootstrap BCa confidence interval (Efron, 1987), that uses modified quantiles to handle skewness and median bias. However it has no adjustment for narrowness or variation in SE, though these could be added.

I plan to make expansion the default for both percentile intervals and BCa intervals in a future version of the resample package (Hesterberg, 2014).

| Expanded Percentile Interval |

| The expanded percentile interval corrects for the poor coverage of the common percentile interval using adjusted quantiles of the bootstrap distribution. This gives much better coverage in small samples. For exponential populations, this is better than the interval for . |

5.4 Reverse Bootstrap Percentile Interval

The bootstrap percentile interval has no particular derivation—it just works. This is uncomfortable for a mathematically-trained statistician, and unsatisfying for a mathematical statistics course.

The natural next step is the reverse bootstrap percentile interval, called “basic bootstrap confidence limits” in (Davison and Hinkley, 1997). We assume that the bootstrap distribution of can be used to approximate the distribution of . For comparison, in the bootstrap estimate of bias we used to estimate .

We estimate the CDF for using the bootstrap distribution of . Let be the quantile of the bootstrap distribution, i.e. . Then

Hence the confidence interval is of the form

This is the mirror image of the bootstrap percentile interval; it reaches as far above as the bootstrap percentile interval reaches below. For example, for the CLEC mean, the sample mean is , the percentile interval is , and the reverse percentile interval is .

For applications with simple bias, like the left side of Figure 18, this interval behaves well. But when there is skewness, like for the CLEC data or the right side of Figure 18, it does exactly the wrong thing.

The reason is worth discussing in a Mathematical Statistics class—that the sampling distribution is not one constant thing, but depends very strongly on the parameter, and the bootstrap distribution on the observed statistic. When sampling from a skewed population, the distribution of depends strongly on ; similarly the bootstrap distribution of is strongly dependent on . Hence the bootstrap distribution of is a good approximation for the distribution of only when . That isn’t very useful for a confidence interval.