Solving finite time horizon Dynkin games by optimal switching111This research was partially supported by EPSRC grant EP/K00557X/1.

Abstract

This paper uses recent results on continuous-time finite-horizon optimal switching problems with negative switching costs to prove the existence of a saddle point in an optimal stopping (Dynkin) game. Sufficient conditions for the game’s value to be continuous with respect to the time horizon are obtained using recent results on norm estimates for doubly reflected backward stochastic differential equations. This theory is then demonstrated numerically for the special cases of cancellable call and put options in a Black-Scholes market.

MSC2010 Classification: 91A55, 91A05, 93E20, 60G40, 91B99, 62P20, 91A15, 91G60.

Key words: optimal switching, stopping times, optimal stopping problems, Snell envelope.

1 Introduction

Recent papers such as [7, 9, 25] have shown a connection between Dynkin games and optimal switching problems with two modes. In particular, letting denote the horizon, the results of [7, 9] show that the value process of a Dynkin game in continuous time (Section 2.1 below) exists and satisfies , where and are the respective value processes for the optimal switching problem with initial mode and . Separately, the papers [2, 13] have shown how to construct two non-negative supermartingales that solve a Dynkin game on a finite time horizon. Furthermore, appropriate debut times of these supermartingales can be used to form a saddle point strategy for the game.

It is therefore apparent that classical two-player Dynkin games and two-mode optimal switching problems are strongly coupled in the following sense: starting with either the Dynkin game or optimal switching problem, one can use its parameters and solution to formulate and solve the other problem. This paper complements these findings by proving, under appropriate conditions, that the solution to a two-mode optimal switching problem furnishes the existence of a saddle point for the corresponding Dynkin game. This is accomplished by the method of Snell envelopes which appears in [1] for optimal switching problems on one hand, and in [2, 13] for Dynkin games on the other hand. In the process, we relate the solution pair to the two-mode optimal switching problem to a pair of supermartingales which lie between the early exit values of the game. This condition is referred to in some contexts as Mokobodski’s hypothesis.

The content of this paper is as follows. Section 2 introduces the Dynkin game and its auxiliary optimal switching problem. Section 3 then outlines some notation and standing assumptions. The main result on the existence of equilibria in the Dynkin game is presented in Section 4. Additional results on the dependence of the game’s solution on the time horizon are discussed in Section 5. Numerics which showcase this theory can be found in Section 6, followed by the conclusion, acknowledgements and references.

2 Preliminaries

2.1 The Dynkin game

Optimal stopping games, also referred to as stochastic games of timing or Dynkin games, were introduced by Eugene Dynkin sometime during the 1960s. These games have been studied extensively since then and have garnered renewed interest due to the introduction of Game Contingent Claims (also known as Israeli Options) in [11]. The particular variant of the Dynkin game which is described below was studied in recent papers such as [2, 7, 8].

We work on a given complete probability space which is equipped with a filtration satisfying and the usual conditions of right-continuity and completeness. We use to represent the indicator function of a set (event) . The shorthand notation a.s. means “almost surely”. For set , and for each let denote the set of -stopping times which satisfy -a.s. For a given , we write . Let denote the corresponding expectation operator. For notational convenience the dependence on is often suppressed. A horizon is fixed for the discussion which follows and for the majority of this paper. However, we often emphasise the dependence on since the horizon is varied below in Section 5.

Let be given and associate with two players and the stopping times and . The game between and is played from time until , where . During this time pays at a (random) rate of per unit time. If exits the game prior to and either before or at the same time that exits, and , pays the amount . Alternatively, if exits the game first, , then pays to the amount . If neither player exits the game before time , we set and pays the amount . We define this payoff for the Dynkin game on in terms of the conditional expected cost to player :

| (2.1) |

This is a zero-sum game since costs (gains) for are the gains (costs) for . For a given , Player chooses the strategy to minimise whereas plays the strategy to maximise it. This leads to upper and lower values for the game on , which are denoted by and respectively:

| (2.2) |

Definition 2.1 (Game Value).

The Dynkin game on is said to be “fair” if there is equality between the time- upper and lower values,

| (2.3) |

The common value, denoted by , is also referred to as the solution or value of the game on .

When studying Dynkin games, the first course of action is to verify that the game is fair. Afterwards, one searches for strategies for the players which give the game’s value or approximates it closely. This leads to the concept of a Nash equilibrium.

Definition 2.2 (Nash equilibrium).

A pair of stopping times is said to constitute a Nash equilibrium or a saddle point for the game on if for any :

| (2.4) |

It is not difficult to verify that the existence of a saddle point implies the game on is fair and its value is given by:

| (2.5) |

Under quite mild integrability and regularity assumptions on and , it is known (for example [3]) that there exists a càdlàg -adapted process such that for each the random variable gives the fair value of the Dynkin game on . Furthermore, if the stopping costs are sufficiently regular then the debut times and defined by

form a saddle point for the Dynkin game on . We arrive at a similar conclusion in this paper using two-mode optimal switching.

2.2 Two-mode optimal switching

The two-mode optimal switching or “starting and stopping” problem has been studied in a variety of contexts as the papers [7, 9] and the references therein can attest. Following convention, we denote the two modes by and . For there is a random profit rate and time reward . For each there is a cost for switching from to determined by the mapping .

Definition 2.3 (Auxiliary two-mode switching problem parameters).

Define parameters for the optimal switching problem from the payoff (2.1) of the Dynkin game as follows:

- Switching costs:

-

For , set , .

- Profit rate:

-

Set and .

- Terminal reward:

-

Set and .

Definition 2.4 (Admissible switching controls).

For a fixed time and initial mode , an admissible switching control consists of:

-

1.

a non-decreasing sequence with -a.s.

-

2.

a sequence , where is the fixed initial value, is -measurable and satisfies and for .

-

3.

The stopping times are finite in the following sense:

-

4.

The (double) sequence satisfies

where is the total cost of the first switches under :

Let denote the set of admissible switching controls. We write when and drop the superscript when the initial mode is not important for the discussion.

Associated with each is a (random) function referred to as the mode indicator function:

The objective function for the switching control problem associated with the Dynkin game on is given by,

| (2.6) |

Together with appropriate integrability assumptions on and , the objective function is well-defined for any . For given and fixed, the goal is to find a control that maximises the performance index:

Remark 2.5.

Processes or functions with super(sub)-scripts in terms of the random mode indicators are interpreted in the following way:

3 Notation and assumptions

3.1 Notation

In this paper we frequently refer to concepts such as “predictable” and “quasi-left-continuous” from the general theory of the stochastic processes. The reader may consult reference texts such as [10, 24] for further details. We note that we follow the convention of [23, 24] for predictable times and processes (defined on the parameter set ).

-

1.

For , let denote the set of random variables satisfying .

-

2.

For , let denote the set of -progressively measurable, real-valued processes satisfying,

-

3.

For , let denote the set of -progressively measurable processes satisfying:

-

4.

Let denote the set of -adapted, càdlàg processes which are quasi-left-continuous (left-continuous over stopping times).

For a given we use the analogous notation , and for the finite time horizon .

3.2 Assumptions

In this section is arbitrary.

Assumption 3.1.

We impose the following integrability, measurability and regularity assumptions:

-

•

The filtration satisfies the usual conditions and is quasi-left-continuous;

-

•

The instantaneous payoff rate satisfies ;

-

•

The early-exit stopping costs for the game satisfy ;

-

•

The terminal payoff satisfies and is -measurable.

Assumption 3.2.

Stopping costs assumptions:

| (3.1) | ||||

| (3.2) |

4 Existence of a Nash equilibrium via optimal switching

In this section we use martingale methods to prove for every that there exists a saddle point for the Dynkin game on with payoff (2.1).

4.1 The Snell envelope

Remember that an -progressively measurable process is said to belong to class if the set of random variables is uniformly integrable.

Proposition 4.1.

Let be an adapted, -valued, càdlàg process that belongs to class . Then there exists a unique (up to indistinguishability), adapted -valued càdlàg process such that is the smallest supermartingale which dominates . The process is called the Snell envelope of and it enjoys the following properties.

-

1.

For any we have:

(4.1) -

2.

Meyer decomposition: There exist a uniformly integrable càdlàg martingale and a predictable integrable increasing process such that for all ,

(4.2) -

3.

Let be given and be an increasing sequence of stopping times tending to a limit and such that for . Suppose the following condition is satisfied for any such sequence,

Then defined by

(4.3) is optimal after in the sense that:

-

4.

For every , if is the stopping time defined in equation (4.3), then the stopped process is a (uniformly integrable) càdlàg martingale.

4.2 The martingale approach to optimal switching problems

Under Assumptions 3.1 and 3.2, we can prove that there exists a unique pair of processes such that for , solves the optimal switching problem in a probabilistic sense. This can be accomplished using the theory of Snell envelopes and the details can be found in a separate paper [17].

Theorem 4.2.

There exists a unique pair of processes belonging to satisfying ,

| (4.4) |

where and . Furthermore, for every , there exists a control such that

4.3 Existence of a Nash Equilibrium

Let and be the processes in Theorem 4.2 and define , , by:

| (4.5) |

The process is càdlàg and in . By Proposition 4.1 above, the process is the Snell envelope of . By Assumptions 3.1 and 3.2, and as for , is quasi-left-continuous on with a possible positive jump at . We can therefore apply property 3 of Proposition 4.1 to verify that for any , the stopping time defined by

| (4.6) |

is the optimal first switching time on when starting in mode . For each , use (4.6) to define a pair of stopping times by

| (4.7) |

We will prove that is a saddle point for the Dynkin game on . In order to do so, we first establish the following lemma which relates the pair to Mokobodski’s hypothesis.

Lemma 4.3.

The processes and of Theorem 4.2 satisfy the following condition:

| (4.8) |

Proof.

For , let be defined as in equation (4.5). Remember that is the Snell envelope of on . Let be arbitrary. By the dominating property of the (right-continuous) Snell envelope, holds -a.s. and this shows

From this we obtain

On the other hand, we have on the event . Using this with equation (3.1) gives

and the claim (4.8) holds. ∎

Theorem 4.4.

Proof.

The claim is trivially satisfied for , so henceforth let be a given but arbitrary time. For , let be defined as in equation (4.5). Define a process by . By Theorem II.77.4 of [23], a stopped supermartingale is also a supermartingale. For every the stopped Snell envelopes and are therefore supermartingales. Additionally using the martingale property of the stopped Snell envelope in Proposition 4.1, we see that satisfies the following:

-

1.

;

-

2.

for any , ;

-

3.

for any , .

This characterisation enables us to prove both (4.9) and (4.10). The arguments used to establish (4.10) are essentially the same as which we use to show (4.9), modulo straightforward changes from equalities to inequalities based on Assumption 3.2 and Lemma 4.3. We therefore only prove (4.9).

The martingale property of on allows us to deduce the following:

| (4.11) |

The term involving the pair inside of the conditional expectation may be rewritten as:

| (4.12) |

By equation (4.7) and conditional on the event , optimality of the stopping time gives the following:

| (4.13) |

Furthermore, since and -a.s., and we can use equation (4.13) to verify the following: -a.s.,

| (4.14) |

By equation (4.7) and conditional on the event , optimality of the stopping time gives:

which is used to deduce:

| (4.15) |

Since -a.s. we have , and using and a.s., we get:

| (4.16) |

Remark 4.5.

The results of Theorem 4.4 were obtained in a similar fashion to several other papers in the literature which have used probabilistic approaches. For instance, [19] (particularly Theorem 1) which uses martingale methods for Dynkin games; [20] (particularly Theorem 2.1) which has a semi-harmonic characterisation of the value function for the Dynkin game in a Markovian setting; and [2, 8] which use the concept of doubly reflected backward stochastic differential equations.

Remark 4.6.

Although we started with a Dynkin game and subsequently formulated an optimal switching problem, we could have derived these results by doing the reverse. More precisely, take any two-mode optimal switching problem (satisfying the assumptions in Section 3) with terminal reward data , and instantaneous profit processes . We then formulate the corresponding Dynkin game by setting , and using the switching cost function to identify the stopping costs for the game as in Definition 2.3.

5 Dependence of the game’s solution on the time horizon

We suppose in this section and the next that there exists a standard Brownian motion defined on , and furthermore that is the completed natural filtration of . It is well known that in this case all -stopping times are predictable. Therefore, all -adapted processes belonging to have paths which are -almost surely continuous.

Suppose that and of Section 2.1 are defined on all of with and ( still satisfying Assumption 3.2). Additionally, for simplicity and ease of notation in what follows, we suppose and define two processes and by and .

For and , we define the following payoff for a Dynkin game: for ,

| (5.1) |

where is -measurable. In the case we assume and satisfies either or as appropriate.

Under appropriate conditions in both finite and infinite horizon settings, it is known (for example [3], or this paper for the finite horizon case) that there is a càdlàg -adapted process such that the random variable is the value of the game with payoff (5.1). In this section we prove that the deterministic (since is trivial) mapping is continuous on . This will be obtained as a straightforward consequence of recent results in [22] on norm estimates for doubly reflected backward stochastic differential equations (DRBSDEs).

5.1 Doubly reflected backward stochastic differential equations

In order to motivate the discussion on DRBSDEs we make the following observations. By Theorem 4.2, we know that for each given and fixed that there exist processes and belonging to satisfying (4.4). Moreover, since it is also true that and are Snell envelopes of appropriate processes and are therefore supermartingales. Let denote the Meyer decomposition for , (cf. (4.2)). We note that both and belong to since and the filtration is quasi-left-continuous. Using this decomposition, and Brownian martingale representation for , we have for all :

| (5.2) |

where is predictable. Furthermore, one can also show (for example, Proposition B.11 of [12]) that

| (5.3) |

Recall from Theorem 4.4 that the process defined by solves the Dynkin game with payoff (5.1). Recalling Definition 2.3, Lemma 4.3 and using (5.2)–(5.3) above, we see that on the process satisfies

| (5.4) |

We now introduce some notation and recall some results from [22]. For and -adapted càdlàg processes and :

-

•

-

•

For , denotes the total variation of over

-

•

, where (resp. ) is the positive (resp.) negative part of (resp. ).

-

•

Letting , :

where the supremum is taken over all stopping time partitions .

Definition 5.1.

Following [22, p. 10], a (global) solution to the DRBSDE associated with a coefficient (or driver) , an -measurable terminal value , and respective lower and upper barriers, and , is a triple of -progressively measurable processes satisfying

| (5.5) |

where is càdlàg, is a process of finite variation with orthogonal decomposition , and

Recalling equation (5.4) above and the properties of , we see that the triple is a solution to the DRBSDE (5.4) in the sense of Definition 5.1. Moreover, using Lemma 4.3 (Mokobodski’s hypothesis) and Theorem 3.4 of [22] for instance, we also know that is, modulo indistinguishability, the unique solution to (5.4) in this instance.

5.2 Dependence of solutions to DRBSDEs on the time horizon

Henceforth we only consider solutions to the DRBSDE (5.5) with . Let us fix and let be any sequence monotonically decreasing to : . We extend the unique solution to (5.5) on to defined on in the following way: For each ,

| (5.6) |

Defining the respective lower and upper barriers and on by and , it is straightforward to check that is the unique solution on to the DRBSDE

| (5.7) |

in the sense of Definition 5.1 above.

Assumption 5.2.

Suppose we are given a sequence of random variables satisfying:

-

•

Each is -measurable

-

•

-

•

almost surely as

-

•

Note that the last two conditions imply in as . Let denote the unique solution on to the DRBSDE (5.5). We then extend these solutions to in the same way as before (see (5.6)–(5.7)), with respective lower and upper barriers and . We continue writing to denote these extensions to avoid excessive notation.

Define and similarly for other cases. Theorem 3.5 of [22] proves the following estimate:

| (5.8) |

where is a positive constant.

5.3 Dependence of the value of the Dynkin game on the time horizon

We now return to the theme of this section, which is to show is continuous on . For this it suffices to show that for every and arbitrary sequence satisfying , that with (resp. ) denoting the unique solution to (5.5) with and time horizon (resp. ), and where convergence takes place in the usual Euclidean sense. We argue by showing is right-continuous and left-continuous at each point in , noting further that it is sufficient to prove this sequential convergence for monotone sequences . We only show that is right-continuous since the other case follows by similar reasoning.

Theorem 5.3.

Let be arbitrary and be any sequence satisfying . Let (resp. ) be the payoff (5.1) for the Dynkin game with horizon (resp. ). Suppose the terminal values and in these respective payoffs satisfy Assumption 5.2. Then, letting and denote the values for these games (which exist by Theorem 4.4), we have

| (5.9) |

and the map is therefore right-continuous on .

Proof.

From the discussion in Section 5.2 above, we can assert that there exists a positive constant such that (cf. (5.2)):

| (5.10) |

Note that is uniformly bounded in since by Assumption 5.2. Theorem 3.4 of [22] verifies that the norm is finite, and it is not difficult to see that for every . Using this in (5.3) shows that we have

| (5.11) |

and the right-hand side of (5.3) is finite for all . We have

which decreases monotonically to almost surely as . By making use of the Monotone Convergence Theorem and by Assumption 5.2, passing to the limit in (5.3) gives

and the claim follows. ∎

6 Numerical examples

6.1 Cancellable call and put options

In this section we use the same probabilistic setup as Section 5 above. We assume a Black-Scholes market with constant risk-free rate of interest and risky asset price process which satisfies

| (6.1) |

where and are constants. A call (resp. put) option on the underlying asset with finite expiration is a contingent claim that gives the holder the right, but not the obligation, to buy (resp. sell) the asset at a predetermined strike price by time . If this option is of “American” style, then the holder can exercise this right at any time . The payoff of the option when exercised at time is given by:

| (6.2) |

A cancellable (game) version of the option grants the writer the ability to cancel it at a premature time . If the writer decides to exercise this right, then the option holder receives the payoff of the standard option plus an additional amount , which is a penalty imposed on the writer for terminating the contract early. The expected value of the cash flow from the writer to the seller at time is given by:

| (6.3) |

The holder of the contract would like to choose the exercise time to maximise the payoff. On the other hand, the writer would like to minimise this payoff by choosing the appropriate cancellation time . We assume that and are chosen from the set of stopping times.

Equation (6.3) is the payoff for a Dynkin game between the option writer and holder (albeit slightly different to (2.1) above). The assumptions listed in Section 3 can be verified for this game, and an inspection of the proof of Theorem 4.4 shows that its conclusion remains valid for the payoff (6.3). The cancellable call/put option can therefore be valued using optimal switching.

6.2 Approximation procedure

Suppose we are additionally given an integer and an increasing sequence of times satisfying and . Set and for each and , let be the subclass of controls where each takes values in and satisfies for . Our discrete-time approximation to the auxiliary optimal switching problem starting in mode at time takes a similar form as (2.6) (with for simplicity): ,

where is the last mode switched to before under the control . The results of [16] show that there exist -adapted sequences , , defined by

| (6.4) |

such that and -a.s.

For each define by and recall the particular parametrization given in Definition 2.3. Recalling Theorem 4.4, we see that the random variable can be used to approximate the value of the continuous-time Dynkin game with payoff (cf. (2.1)). There is, however, a more efficient backward induction formula for . For and define events and as follows:

| (6.5) |

Notice that for every and . It is not difficult to verify (using Assumption 3.2 and optimality arguments – see [16]) that for and this leads to: ,

| (6.6) | ||||

| (6.7) |

Using , equations (6.6) and (6.7), definition (6.5) for the events and , and the backward induction formula (6.4), one can show that satisfies: -a.s.,

In order to account for exponential discounting, assuming that the rewards and costs have not already been discounted, the backward induction formula should be written as:

| (6.8) |

The reader can compare the backward induction formula (6.8) to the one appearing in Theorem 2.1 of [11]. In a Markovian setting, the Least-Squares Monte Carlo regression (LSMC) method (Chapter 8, Section 6 of [6]) can be used to numerically approximate the conditional expectation in (6.8).

6.3 Numerical results for the cancellable call and put options

We now present numerical results for the cancellable call and put options. The backward induction formula (6.8) with the LSMC algorithm was used to this effect, with simple monomials of degree used to approximate the conditional expectations. For each run of the algorithm, sample paths of the geometric Brownian motion (6.1) were simulated using antithetic sampling and the relation:

where is the step size and is a sequence of I.I.D. standard normal random variables. The option’s value was set to the empirical average of the results from 100 runs of the algorithm.

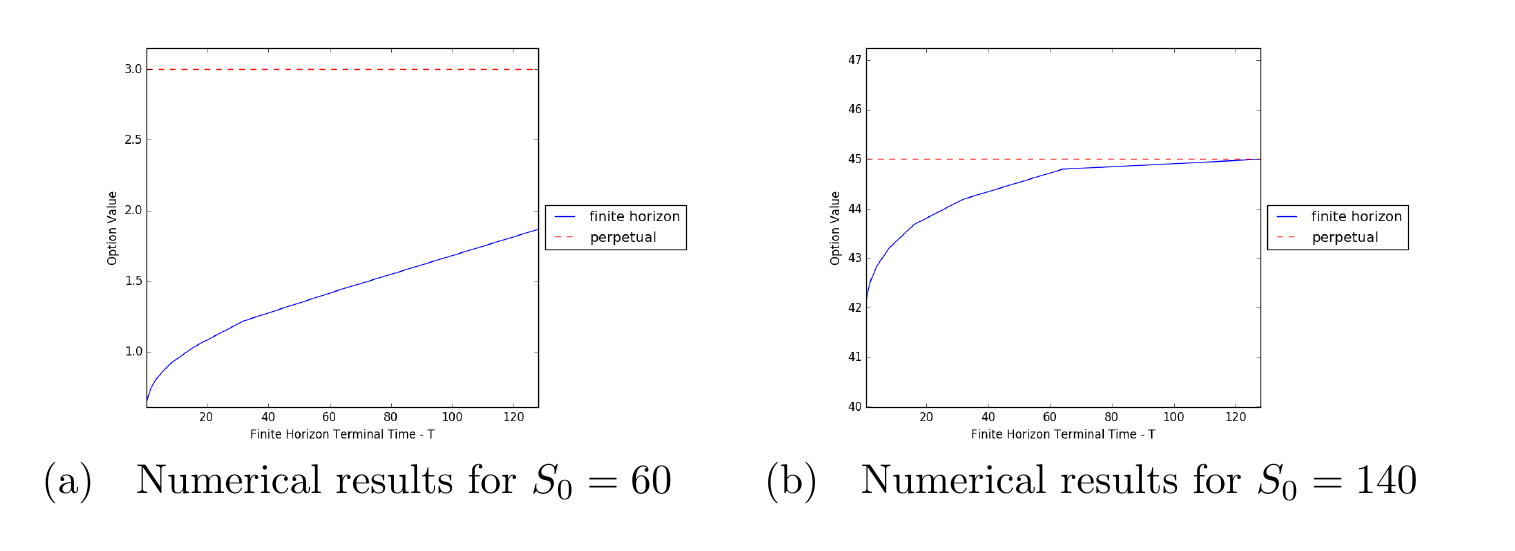

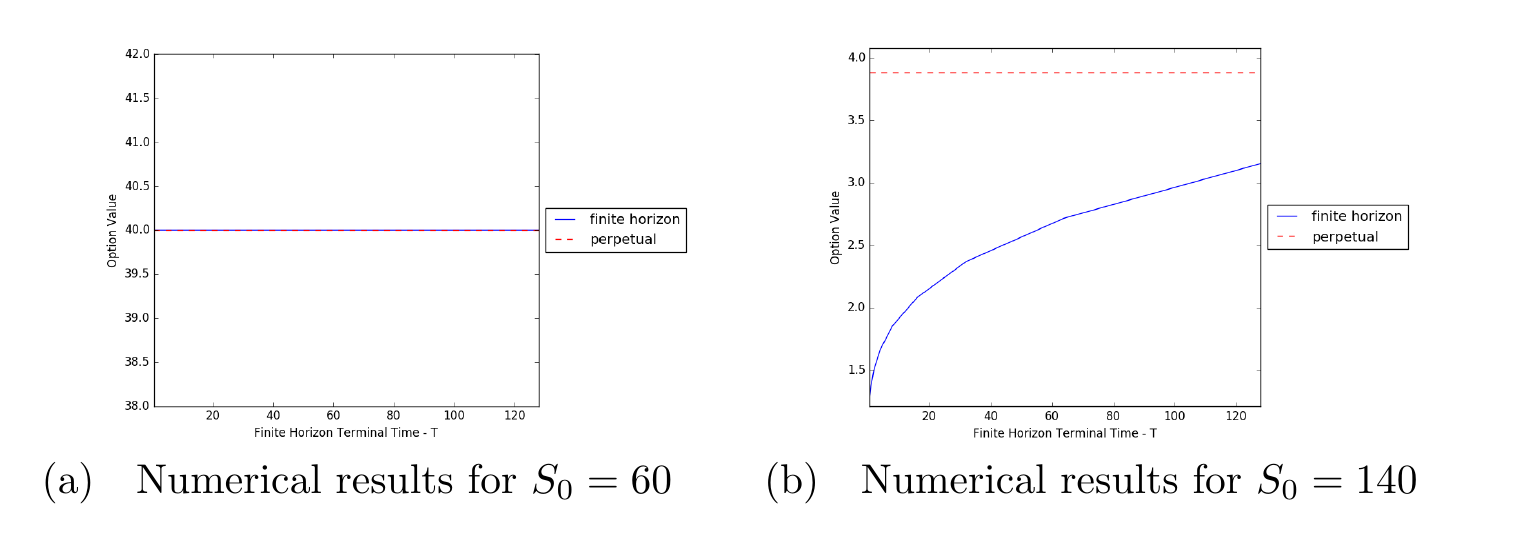

The same model parameters were used to value the cancellable call and put options. These parameters were obtained from [14, p. 128] and are as follows: , , and . We computed option values on a finite time horizon with , , initial spot price , and time steps.

6.3.1 Numerical results for the cancellable call option.

Figure 1 below shows numerical results for the option values for . The solid line shows finite horizon option values whilst the dotted line is the perpetual option’s value. The latter was calculated using the following formula obtained from [4]:

6.3.2 Numerical results for the cancellable put option.

Figure 2 provides the analogous illustrations for the cancellable put option. The perpetual option’s value in this case was calculated using the following formula obtained from [15]:

where , is the time value for the perpetual American put option as a function of the initial asset price, , and is the solution in to the following equation:

For the interested reader, we note that and to one decimal place. This means when and when . In terms of continuity of and possible convergence to the perpetual option value, from Figure 2 one draws similar conclusions to those for the cancellable call option.

7 Conclusion

This paper showed how the solution to a two-mode optimal switching problem can be used to derive the solution to a Dynkin game in continuous-time and on a finite time horizon . Under certain hypotheses, the value of the Dynkin game starting from exists and satisfies , where and are the respective optimal values for the optimal switching problem with initial mode and . Furthermore, and (and therefore ) are right-continuous processes, and a Nash equilibrium solution to the Dynkin game can be constructed using appropriate debut times of . Results on doubly reflected stochastic differential equations were used to prove that the value of the game is a continuous function of the time horizon parameter . This result was confirmed via numerical experiments for cancellable call and put options.

Acknowledgments

This research was partially supported by EPSRC grant EP/K00557X/1. The author would like to thank his PhD supervisor J. Moriarty, colleague T. De Angelis, Prof. S. Hamadène, and all others whose comments which led to an improved draft of the paper.

References

- [1] B. Djehiche, S. Hamadène, and A. Popier, A Finite Horizon Optimal Multiple Switching Problem, SIAM Journal on Control and Optimization, 48 (2009), pp. 2751–2770.

- [2] R. Dumitrescu, M.-c. Quenez, and A. Sulem, Generalized Dynkin Games and Doubly Reflected BSDEs with Jumps, oct 2014, arXiv:1310.2764v2.

- [3] E. Ekström and G. Peskir, Optimal Stopping Games for Markov Processes, SIAM Journal on Control and Optimization, 47 (2008), pp. 684–702.

- [4] E. Ekström and S. Villeneuve, On the value of optimal stopping games, The Annals of Applied Probability, 16 (2006), pp. 1576–1596.

- [5] N. El Karoui, Les aspects probabilistes du contrôle stochastique, Ecole d’Eté de Probabilités de Saint-Flour IX-1979, (1981).

- [6] P. Glasserman, Monte Carlo Methods in Financial Engineering, vol. 53 of Stochastic Modelling and Applied Probability, Springer New York, New York, NY, 2003.

- [7] X. Guo and P. Tomecek, Connections between Singular Control and Optimal Switching, SIAM Journal on Control and Optimization, 47 (2008), pp. 421–443.

- [8] S. Hamadène and M. Hassani, BSDEs with two reflecting barriers driven by a Brownian motion and Poisson noise and related Dynkin game, Electronic Journal of Probability, 11 (2006), pp. 121–145.

- [9] S. Hamadène and M. Jeanblanc, On the Starting and Stopping Problem: Application in Reversible Investments, Mathematics of Operations Research, 32 (2007), pp. 182–192.

- [10] J. Jacod and A. N. Shiryaev, Limit Theorems for Stochastic Processes, vol. 288 of Grundlehren der mathematischen Wissenschaften, Springer Berlin Heidelberg, Berlin, Heidelberg, 2003.

- [11] Y. Kifer, Game options, Finance and Stochastics, 4 (2000), pp. 443–463.

- [12] M. Kobylanski and M.-C. Quenez, Optimal stopping time problem in a general framework, Electronic Journal of Probability, 17 (2012).

- [13] M. Kobylanski, M.-C. Quenez, and M. R. de Campagnolle, Dynkin games in a general framework, Stochastics An International Journal of Probability and Stochastic Processes, 86 (2014), pp. 304–329.

- [14] C. Kühn, A. E. Kyprianou, and K. van Schaik, Pricing Israeli options: a pathwise approach, Stochastics An International Journal of Probability and Stochastic Processes, 79 (2007), pp. 117–137.

- [15] A. E. Kyprianou, Some calculations for Israeli options, Finance and Stochastics, 8 (2004), pp. 73–86.

- [16] R. Martyr, Dynamic programming for discrete-time finite horizon optimal switching problems with negative switching costs, 2015, arXiv:1411.3981.

- [17] , Finite-horizon optimal multiple switching with signed switching costs, 2015, arXiv:1411.3971.

- [18] H. Morimoto, Optimal stopping and a martingale approach to the penalty method, Tohoku Mathematical Journal, 34 (1982), pp. 407–416.

- [19] , Dynkin games and martingale methods, Stochastics, 13 (1984), pp. 213–228.

- [20] G. Peskir, Optimal Stopping Games and Nash Equilibrium, Theory of Probability & Its Applications, 53 (2009), pp. 558–571.

- [21] G. Peskir and A. N. Shiryaev, Optimal Stopping and Free-Boundary Problems, Lectures in Mathematics. ETH Zürich, Birkhäuser Basel, 2006.

- [22] T. Pham and J. Zhang, Some norm estimates for semimartingales, Electronic Journal of Probability, 18 (2013), pp. 1–26.

- [23] L. C. G. Rogers and D. Williams, Diffusions, Markov Processes and Martingales: Volume 1, Foundations, Cambridge University Press, Cambridge, 2nd ed., 2000.

- [24] , Diffusions, Markov Processes and Martingales: Volume 2, Itô Calculus, Cambridge University Press, Cambridge, 2nd ed., 2000.

- [25] A. Yushkevich and E. Gordienko, Average optimal switching of a Markov chain with a Borel state space, Mathematical Methods of Operations Research (ZOR), 55 (2002), pp. 143–159.