Qualitative Robustness in Bayesian Inference

Abstract

The practical implementation of Bayesian inference requires numerical approximation when closed-form expressions are not available. What types of accuracy (convergence) of the numerical approximations guarantee robustness and what types do not? In particular, is the recursive application of Bayes’ rule robust when subsequent data or posteriors are approximated? When the prior is the push forward of a distribution by the map induced by the solution of a PDE, in which norm should that solution be approximated? Motivated by such questions, we investigate the sensitivity of the distribution of posterior distributions (i.e. of posterior distribution-valued random variables, randomized through the data) with respect to perturbations of the prior and data generating distributions in the limit when the number of data points grows towards infinity.

1 Introduction and motivations

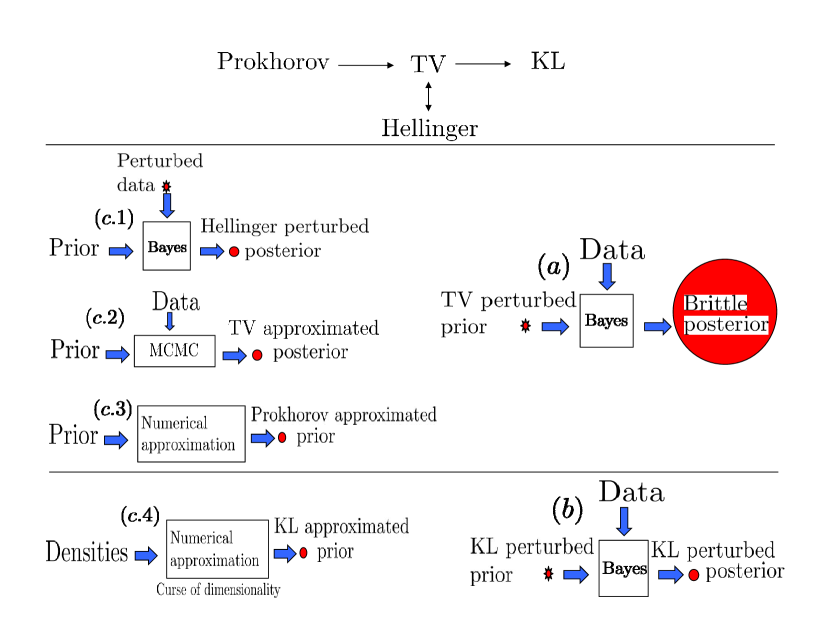

When we apply Bayesian inference with Gaussian priors and linear observations, we do not actually compute Bayes’ rule but solve the linear system whose solution is the conditional expectation, and robustness is guaranteed by that of our linear solver. This paper is motivated by robustness questions that arise in the numerical implementation of Bayes’ rule for continuous systems when closed-form expressions are not available for the computation of posterior values/distributions. For example, what is the sensitivity of posterior values or the sensitivity of the distribution of posterior values to perturbations introduced by the numerical approximation of the prior? When Bayes’ rule is applied in a recursive manner and approximated posterior distributions are used as prior distributions or approximated data is used in the conditioning process, do we have robustness guarantees on subsequent posterior distributions/values? Is it possible to numerically approximate the optimal prior/mixed strategy of a decision theory problem (arising in the continuous setting under the complete class theorem [42]) when closed form expressions are not available, and if it is, in which metric should we do so?

Figure 1.1 provides an illustration of partial answers to such questions, which, when combined, can be used as a map to navigate robustness/non-robustness questions/issues arising from numerical approximations. To begin, (a) [34, 33, 35] shows that the range of posterior values of the quantity of interest under perturbations of the prior in Prokhorov or TV metrics is the deterministic range of the quantity of interest (we will refer to this maximal sensitivity property as brittleness). Moreover, (c.1) [41] shows that the posterior distributions are controlled by the Hellinger metric under the application of the Bayes rule with an exact prior under the perturbation of a finite number of finite dimensional samples (see also [11]). Since the Hellinger and TV metrics are equivalent [23], (c.1) and (a) suggest that, without specific restrictions, it is, in general, not possible to offer guarantees on the robustness of recursive Bayes under perturbations of the data. Similarly (c.2) the convergence of Markov chains (on continuous state spaces) used in MCMC algorithms (such as the Metropolis algorithm) is generallly analyzed with respect to the TV topology [38, 22]. However it should be noted that, according to Roberts and Rosenthal [37, Pg. 10], Gibbs [22], Gelman [20, Intro] and Madras and Sezer [30, Intro], convergence in TV is in general not guaranteed, so that one might say in general that convergence of MCMC is at best in TV. Therefore combining (c.2) and (a) suggests that, without further restrictions, it is, in general, not possible to offer guarantees on the robustness of recursive Bayes if posteriors are approximated using MCMC. Moreover, in many cases, the prior may need to undergo a numerical approximation/discretization step prior to conditioning. For example, in popular applications of Bayes’ rule to stochastic PDEs [44, 16] one pushes forward the prior from the space of coefficients of the PDE to the solution space where it is conditioned. Consequently, if the PDE is numerically approximated this implies an approximation of the pushed-forward prior. Therefore (c.3) representing numerical discretization/approximation as a continuous map between two Polish spaces, it is known that the push forward of a measure under such maps is continuous in the weak topology, which is metrized by the Prokhorov distance. Therefore, combining (c.3) and (a) suggests that, without further restrictions, it is, in general, not possible to offer robustness guarantees to perturbations caused by the numerical discretization of the prior.

For positive results on the other hand, observe that (b) [24] shows that posterior values (given a finite number of data points) are robust to approximation errors of the prior measured in Kullback-Leibler divergence. Therefore if (c.4) the numerical approximation map is continuous in Kullback-Leibler divergence then posterior values (given a finite number of data points) are robust to that numerical discretization step. However observe that unless closed form expressions are available, one must keep track of densities to achieve the continuity of the numerical approximation map in Kullback-Leibler divergence, which is a task plagued by the curse of dimensionality.

Since the brittleness of posterior distributions and values with respect perturbations of the prior defined in TV or Prokhorov metrics is an obstacle to obtaining robustness guarantees to numerical approximation errors when closed form expressions are unavailable, it is natural to ask whether robustness could be guaranteed by considering the distribution of posterior distributions or posterior values generated by the random generation of the data. To answer this question we develop a framework for quantifying the sensitivity of the distribution of posterior distributions with respect to perturbations of the prior and data generating distributions in the limit when the number of data points grows towards infinity. In this generalization of Cuevas’ [13] extension of Hampel’s [27] notion of qualitative robustness to Bayesian inference to include both perturbations of the prior and the data generating distribution, posterior distributions are analyzed as measure-valued random variables (measures randomized through the data) and their robustness is quantified using the total variation, Prokhorov, and Ky Fan metrics. Our results show that (1) the assumption that the prior has Kullback-Leibler support at the parameter value generating the data, classically used to prove consistency, can also be used to prove the non-robustness of posterior distributions with respect to infinitesimal perturbations (in TV) of the class of priors satisfying that assumption, (2) for a prior which has global Kullback-Leibler support on a space which is not totally bounded, we can establish non-robustness and (3) consistency, and the unstable nature of the conditions which generate it, produces non-robustness, and a careful selection of the prior is important if both properties (or their approximations) are to be achieved. The mechanisms supporting our results are different and complementary to those discovered by Hampel and developed by Cuevas. To obtain them, we derive in Section 3 a corollary to Schwartz’ consistency Theorem that leads to robustness or non-robustness results depending on the topology defining the continuity of the numerical approximation map (Kullback-Leibler, TV or Prokhorov). Moreover, this corrollary is further developed in Proposition 7.1 to analyze the convergence of random measures in the qualitative robustness framework. More precisely, although in [24] it is shown that the Fréchet derivatives of posterior values to Kullback-Leibler perturbations of the prior may diverge to infinity with the number of data points, a simple application of Proposition 7.1 implies the robustness of the distribution of posterior distributions/values under Kullback-Leibler perturbations of the prior in the limit where the number of data points goes to infinity. On the other hand, application of Proposition 7.1 also suggest the lack of robustness of the distribution of posterior distributions/values to TV or Prokhorov perturbations of the prior, where we note that Prokhorov perturbations include classes of perturbations defined by generalized moment constraints, as in [8, 6, 7, 5, 34, 33, 35].

2 Qualitative Robustness for Bayesian Inference

Hable and Christmann [25] have recently established qualitative robustness for support vector machines. Consequently, it appears natural to inquire into the qualitative robustness of Bayesian inference. Hampel [27] introduced the notion of the qualitative robustness of a sequence of estimators and Cuevas [13] has extended Hampel’s definition and his basic structural results to Polish spaces. Since the space of priors and posteriors equipped with the weak topology is Polish whenever is, Cuevas’ extension has direct applications to Bayesian inference. Boente et al. [10] have developed qualitative robustness for stochastic processes, Nasser et al. [32] for estimation, and Basu et al.[3] for Bayesian inference with a single sample. The notion of qualitative robustness introduce in this paper is a straightforward generalization of that introduced by Hampel [27] and developed by Cuevas [13], see also Cuevas [15]. Indeed, this version requires no introduction of loss and risk functions and concerns itself with not just expected values but with the full distribution of the effects of the randomness of the observations. It considers a fixed model so is not concerned with robustness with respect to model specification, although such considerations can easily be included. Moreover, since it is formulated with respect to classic notions in probability, it appears to us as simple, natural, flexible, without calibration issues, and easy to interpret statistically.

Metrics on spaces of measures and random variables will be important in its formulation. Fortunately, this is a well studied field, see e.g. Rachev et al. [36] and Gibbs and Su [23], but to keep the presentation simple, here we will restrict our attention to the total variation, Prokhorov and Ky Fan metrics (we refer to [8, 6, 7, 5] for motivations for considering classes of priors defined in the Prokhorov metric). For measurable spaces and , we write and for the set of probability distributions on and respectively. In this general setting, we can metrize the spaces of measures and using total variation. This latter metrization makes into a topological space whose Borel structure can be used to define the space of probability measures on , which can also be metrized using the total variation. However, the separability of these spaces will be extremely useful for us and, in general, these spaces will not be separable under the total variation metric. Recall that for a metric space , the Prokhorov metric on the space of Borel probability measures is defined by

| (2.1) |

where

According to Dudley [18, Thm. 11.3.1], the Prokhorov metric is a metric on . Consequently, when and are metric, , we can also metrize the spaces of measures and with the Prokhorov metrics, and having done so we can define the space of Borel probability measures on the metric space of Borel probability measures on and metrize it with the Prokhorov metric . Furthermore, when is a separable metric space, Dudley [18, Thm. 11.3.3] asserts that the Prokhorov metric metrizes weak convergence and Aliprantis and Border [1, Thm. 15.12] asserts that the metric space is separable.

Therefore, when and are separable metric spaces, the Prokhorov metrics and metrize weak convergence in and respectively and both metric spaces and are separable. Consequently, when is a separable metric space, is a separable metric space and therefore is a separable metric space.

The separability of is sufficient to define the Ky Fan metric on a space of -valued random variables. Indeed, for a separable metric space , probability space , and two -valued random variables and , the Ky Fan distance between and , see e.g. Dudley [18, Pg. 289], is defined as

| (2.2) |

By Dudley [18, Thm. 9.2.2], the Ky Fan metric is a metric on the space of -valued random variables from and metrizes convergence in probability for them. Consequently, when is a separable metric space and is metrized with the Prokhorov metric , the Ky Fan metric of (2.2) metrizes the space of -valued random variables for each . Since this family of metrics depends on the measure we indicate this dependence by writing . Moreover, when and are separable metric spaces, their Borel -algebras are countably generated, which is required to apply Doob’s Theorem to assert that a domninated measurable model has a jointly measurable family of densities, which is required in the consistency theorem of Schwartz which we will need.

When and are Borel subsets of Polish metric spaces, they are separable metric spaces so the above applies. Let us now show that the assumption also facilitates the measurability of Bayesian conditioning that will be needed to define its qualitative robustness. To that end, from now on let us place as default the weak topologies on , and and metrize them with the Prokhorov metrics , and . This is primarly to obtain well-defined Bayesesian conditioning while at the same time applicability of Schwartz’s consistency theorem. We will also place other metric structures on , and to quantify the size of perturbations and indicate them with the notation , and . Consider a measurable model . Since Aliprantis and Border [1, Thm. 15.13] implies that the map defined by is Borel measurable for all , it follows that corresponds to a Markov kernel. Consider a prior . Then since is assumed to be a Borel subset of a Polish space, it follows from Schervish [39, Thm. B.46] that there exists a family of conditional probability measures generated by the model such that the map is -measurable for all bounded and measurable functions . Note that after the proof Schervish mentions that such a family of conditional measures is not unique. Since both and are separable and metrizable, it then follows from Aliprantis and Border [1, Thm. 19.7] that the resulting map from to is measurable. For multiple samples, it is clear that is a Borel subset of the -th power of the ambient Polish space of . By Billingsly’s [9, Thm. 2.8] characterization of weak convergence on product spaces it follows that the injection defined by is continuous, so that it follows that , defined by , is measurable and therefore, by the same arguments as above, we obtain a family of multisample conditional measures such that the resulting map

defined by the determination of the posteriors

| (2.3) |

is measurable. Therefore, its corresponding pushforward operator

is well-defined, where we have removed the bar over in the notation to emphasize that this pushforward operator corresponds to the prior . Then to consider how the posteriors vary as a function of the sample data when it is generated by i.i.d. sampling from , since it follows that so we can utilize the pushforward operator to define

the sampling distribution of the posterior distribution when .

For a fixed prior , we say that the Bayesian inference is qualitatively robust at a data generating distribution with respect to an admissible set containing , and metrics and on and , if for any , there exists a such that

for large enough . On the other hand, when the data generating distribution is fixed and we vary the prior , we consider the sequence of maps

defined by

| (2.4) |

Since the projection is continuous and , it follows from the measurability of , that is measurable, and therefore the resulting sequence

is a sequence of -valued random variables. For each , let be a metric on the space of -valued random variables whose domain is the probability space . Then, for a prior , we say that the Bayesian inference is qualitatively robust at with respect to an admissible set containing and metrics and on if given , there exists a such that

for large enough .

These two definitions can be combined in a straightforward manner to define robustness corresponding to a single prior/data generating pair. However, to consider a larger class of distributions than a single pair, we let denote the admissible set of prior-data generating distribution pairs such that is an admissible candidate for robustness and is an admissible candidate for its perturbation. In particular, the projection denotes the set of admissible prior-data generating pairs. Now combining in a straightforward manner we obtain:

Definition 2.1.

Let and be Borel subsets of Polish metric spaces and let and be equipped with the weak topology metrized by the Prokhorov metrics and . Let be the space of Borel probability measures on the metric space of Borel probability measures on equipped with its weak topology metrized by its Prokhorov metric . Consider perturbation pseudometrics , and on , and respectively and for each , let be a pseudometric on the space of -valued random variables on the probability space . Let denote the admissible set of prior-data generating distribution pairs and suppose that is measurable. Then the Bayesian inference is qualitatively robust with respect to , if given , there exists such that

for large enough .

Finite sample versions, as introduced in Hable and Christmann [26, Def. 2], are also available. Note that unlike Hampel and Cuevas who require “for all ” in their definitions, we follow Huber [28] and Mizera [31] in only requiring closeness “for large enough ”. The results of this paper are applicable to both versions. Of course the relevance of the specific notion of qualitative robustness used depends on the perturbation metrics used. The results of this paper apply to the case when is the Ky Fan metric, metrizing convergence in probability on the space of -valued random variables with domain the probability space and the is any metric weaker than the total variation.

3 Lorraine Schwartz’ Theorem

The fundamental mechanism generating non robustness for Bayesian inference will be its consistency. The breakthrough in consistency for Bayesian inference is considered to be Schwartz’ theorem [40, Thm. 6.1], so we use it as a model for consistency and the conditions sufficient to generate it. Stated in Barron, Schervish and Wasserman [2, Intro], Wasserman [43, Pg. 3] and Ghosal, Ghosh and Ramamoorthi [21, Cor. 1] for the nonparametric case, for the parametric case we will operate in Borel subsets of Polish metric spaces. By Schervish [39, Thm. B.32], regular conditional probabilities exist for conditioning random variables with values in such a space. Moreover, when the parametric model is a Markov kernel and is dominated by a -finite measure, then by the Bayes’ Theorem for densities Schervish [39, Thm. 1.31] we have, in addition, that the Bayes’ rule for densities determines a valid family of densities for the regular conditional distributions. We say that a model is dominated if there exists a -finite Borel measure on such that .

Recall the Kullback-Leibler divergence between two measures and defined by

where is any measure such that both and are absolutely continuous with respect to . It is well known that is nonnegative, and that it is finite only if , and in that case From this we can define the Kullback-Leibler ball of radius about by . For a model , there is the pullback to a function on defined by and when the model is dominated by a -finite measure , if we let be a realization of the Radon-Nikodym derivative, then the pullback has the form

From this we define a Kullback-Leibler neighborhood of a point by

Let us define the set of priors which have Kullback-Leibler support at by

| (3.1) |

which implicitly requires that be measurable111 Note the change from the standard definition to ours does not affect which measures have Kullback-Leibler support, but is more convenient since then is closed, simplifying the proof that is measurable. for all . Also let denote those measures with global Kullback-Leibler support, that is,

is the set of priors which have Kullback-Leibler support at all , and let , defined by

| (3.2) |

denote the set of priors with almost global Kullback-Leibler support.

Let us address the measurability of the Kullback-Leibler neighborhoods . For the nonparametric case, Barron, Schervish and Wasserman [2, Lem. 11] demonstrate that the Kullback-Leibler neighborhoods are measurable with respect to the strong topology restricted to the subspace of measures which are absolutely continuous with respect to a common -finite reference measure. For the parametric case, Dupuis and Ellis [19, Lem. 1.4.3] assert that on a Polish space that K is lower semicontinuous in both arguments. Since the subset embedding of a subset of a metric space is isometric, when is a Borel subset of a separable metric space , it can be shown that the induced pushforward map is isometric in the Prokhorov metrics, in particular it is continuous. Since the composition of a continuous and a lower semicontinuous function is lower semicontinuous, it follows from Dupuis and Ellis [19, Lem. 1.4.3] that on any realization of a standard Borel space that the Kullback-Leibler divergence is lower semicontinuous in each of its arguments separately, in particular, fixing the first, it is lower semicontinuous. Therefore is closed, and therefore measurable for . Consequently, when is measurable, it follows that is measurable for .

The following corollary to Schwartz’ Theorem, and its implications in Proposition 7.1, gives us the form of consistency that we will use in the robustness analysis. Since the -algebra of a Borel subset of a Polish space is countably generated, Doob’s Theorem in Dellacherie and Meyer [17, Thm. V.58] and the measurability of the dominated model implies that a family of densities can be chosen to be measurable, so that this assumption of Schwartz’ Theorem [40, Thm. 6.1] is satisfied. We note that Dellacherie and Meyer emphasize that the countably generated condition is indispensable for Doob’s Theorem to apply. Note the assumption that the map be open.

Corollary 3.1 (Schwartz).

Let and be Borel subsets of Polish metric spaces and equip and with the Prokhorov metrics. Consider an injective measurable dominated model such that is open. Then for every with Kullback-Leibler support at and for every measurable neighborhood of , we have

4 Main Results

Now that we have defined qualitative robustness for Bayesian inference and presented the consistency conditions of Schwartz’ Corollary 3.1, we are now prepared for our main results. Indeed, the brittleness results of [34, 33, 35] and the non qualitative robustness results of Cuevas [13, Thm. 7] suggest that we may obtain non qualitative robustness according to Definition 2.1 by fixing the prior and varying the data generating distribution. However, according to Berk [4], in the misspecified case, although “there need be no convergence (in any sense)”, in the limit the posterior becomes confined to a carrier set consisting of those points which are closest in terms of the Kullback-Leibler divergence. Consequently, it appears possible that a generalization of the results of Hampel [27, Lem. 3] and Cuevas [13, Thm. 1] which allows such a set-valued notion of consistency may be sufficient. Certainly it will require the more sophisticated notions of the continuity, or semi-continuity, of the Kullback-Leibler set-valued information projection and its dependence on the geometry of the model class . Although this path will certainly be instructive and appears feasible, we instead find it simpler to obtain non qualitative robustness by fixing the data generating distribution to be in the model class and varying the prior. In particular, we show that the inference is not robust according to Definition 2.1 when the metric is the the Ky Fan metric and the metric is any that is weaker than the total variation metric. It is important to note that these results do not require any misspecification. Moreover, it appears that Bayesian Inference’s dependence on both the data generating distribution and the prior leads to two complementary mechanisms generating non qualitative robustness; whereas Cuevas’ result [13, Thm. 7] utilizes consistency and the discontinuity of the infinite sample limit, this other component utilizes the non-robustness of consistency, namely that the set of consistency priors, those with Kullback-Leibler support at the data generating distribution, is not robust.

Now let us return to our main results. For , let us recall from (3.1) the set of priors with Kullback-Leibler support at and, for , define a total variation uniformity by

of prior pairs where the first component has Kullback-Leibler support at and the second component is within of the first in the total variation metric. For , we define an admissible set of prior-data generating distribution pairs by

| (4.1) |

using the identification of with .

Our Main Theorem shows, under the conditions of Schwartz’ Corollary, that the Bayesian inference is not robust under the assumption that the prior has Kullback-Leibler support at the parameter value generating the data. This result, along with those that follow, supports Cuevas’ [14] statement that “his results suggest the possibility of proving the instability (i.e. the lack of qualitative robustness) for a wide class of usual Bayesian models.”

Theorem 4.1.

Remark 4.2.

Actually the proof shows more; let denote the diameter of , then for , there does not exist a such that robustness is satisfied. Since is large, either half the diameter of the space or larger than , we say the inference is brittle.

Theorem 4.1 does not assert that the Bayesian inference is not robust at any specified prior, only that it is not robust under the assumption that the prior has Kullback-Leibler support at the parameter value generating the data. To establish non-robustness at specific priors we include variation in the data-generating distribution in the model class as follows. Let , defined by

denote the fact that we allow the data generating distribution to vary throughout the model class but do not allow any perturbations to it. Then, for , define the admissible set by

where is the open ball in the total variation metric.

Since the following theorem is a corollary to the theorem after it, Theorem 4.4, we do not include its proof. However, we state it here because it is the more fundamental result.

Theorem 4.3.

Consider the sitiuation of Theorem 4.1 with not totally bounded. Then if the prior has Kullback-Leibler support for all , the Bayesian inference is not qualitatively robust with respect to for all .

Since a metric space is totally bounded if and only if its completion is compact, when is totally bounded, we assume that it is a Borel subset of a compact metric space. In this case, although Theorem 4.3 does not apply, utilizing the covering number and packing number inequalities of Kolmogorov and Tikhomirov [29], we can provide a natural quantification of qualitative robustness. To that end, we define covering and packing numbers. For a finite subset , the finite collection of open balls is said to constitute a covering of if . For a finite set we denote its size by . The covering numbers are defined by

that is, is the smallest number of open balls of radius centered on points in which covers . On the other hand, a set of points is said to constitute an -packing if . The packing numbers are then defined by

Since the Kolmogorov and Tikhomirov [29, Thm. IV] inequalities

| (4.2) |

are valid in the not totally bounded case, if we allow values of , the following theorem has Theorem 4.3 as its corollary.

Theorem 4.4.

Given the conditions of Theorem 4.3 with totally bounded. If the Bayesian inference is qualitatively robust with respect to for some , then given , we must have

5 Mechanisms generating non-robustness

For the clarity of the paper, in this subsection, we illustrate some of the mechanisms generating non qualitative robustness in Bayesian inference, which complement the mechanism discovered by Hampel [27, Lem. 3] and Cuevas [13, Thm. 1]. These mechanisms do not utilize misspecification. Those which do are discussed in Subsection 5.1. The core mechanism is derived from the nature of both the assumptions and assertions of results supporting consistency. More precisely, Corollary 3.1 states that if the data generating distribution is and if the prior attributes positive mass to every Kullback-Leibler neighborhood of , then the posterior distribution converges towards as .

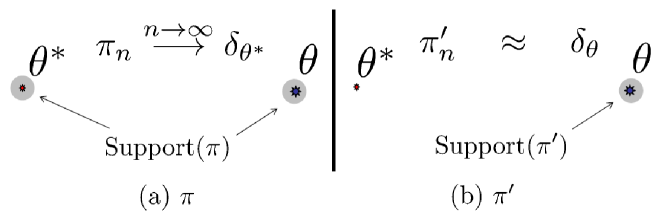

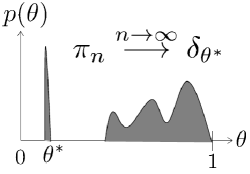

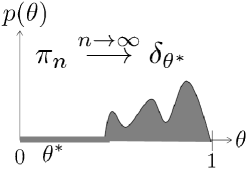

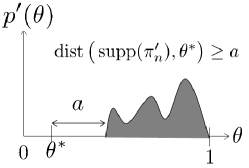

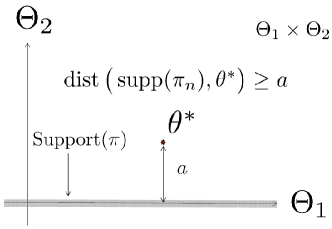

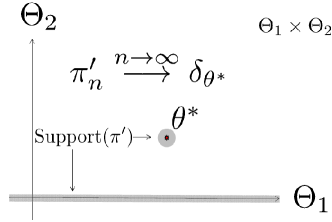

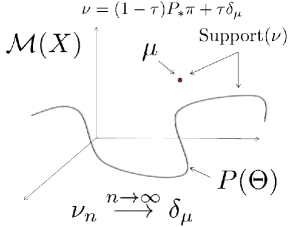

The assumption that attributes positive mass to every Kullback-Leibler neighborhood of does not require to place a significant amount of mass around , but instead can be satisfied with an arbitrarily small amount. Therefore, if, as in Figure 5.1, is a prior distribution with support centered around , but with a very small amount of mass about , so that it satisfies the assumptions of Corollary 3.1 at , then can be slightly perturbed into a with support also centered around , but with no mass about . In this situation, although and can be made arbitrarily close in total variation distance, the posterior distribution of converges towards as , whereas that of remains close to .

Figure 5.2 gives an illustration of the same phenomenon when the parameter space is the interval and the probability density functions of and are and with respect to the uniform measure.

Note that the mechanism illustrated in Figures 5.1 and 5.2 does not generate non qualitative robustness at all priors but instead for the full class of consistency priors, defined by the assumption of having positive mass on every Kullback-Leibler neighborhood of . One may wonder whether this non qualitative robustness can be avoided by selecting the prior to satisfy Cromwell’s rule (that is, the assumption that gives strictly positive mass to every nontrivial open subset of the parameter space ). Theorem 4.3 shows that this is not the case if the parameter space is not totally bounded. For example, when , for all one can find such that the mass that places on the ball of center and radius one is smaller than , and by displacing this small amount of mass one obtains a perturbed prior whose posterior distribution remains asymptotically bounded away from that of when the data-generating distribution is . Similarly if is totally bounded then Theorem 4.4 places an upper bound on the size of the perturbation of the prior that would be required as a function of the covering complexity of . Note that these observations suggest that a maximally qualitatively robust prior should place as much mass as possible near all possible candidates for the parameter of the data generating distribution, thereby reinforcing the notion that a maximally robust prior should have its mass spread as uniformly as possible over the parameter space.

5.1 Robustness under misspecification

Although the main results of Section 4 do not utilize any model misspecification, the brittleness results of [34] suggest that misspecification should also generate non qualitative robustness. Indeed, although, one may find a prior that is both consistent and qualitatively robust when is totally bounded and the model is well-specified, we now show how extensions of the mechanism illustrated in Figures 5.1 and 5.2 suggest that misspecification implies non qualitative robustness. Consider the example illustrated in Figure 5.3. In this example the model is the restriction of a well specified larger model to . Assume that the data generating distribution is where , so that the restricted model is misspecified. Let be any prior distribution on . Although may satisfy Cromwell’s rule the mechanisms presented in this paper suggest that is not qualitatively robust with respect to perturbed priors having support on . Indeed, let be an arbitrarily small perturbation of obtained by removing some mass from the support of and adding that mass around . Note that can be chosen arbitrarily close to while satisfying the local consistency assumption of Corollary 3.1, which implies that the posterior distributions of concentrate on while the posterior distributions of remain supported on . Note that if is interpreted as an extension of the model , then this mechanism suggests that we can establish conditions under which Bayesian inference is not qualitatively robust under model extension.

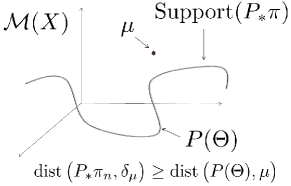

Figure 5.4 represents a non-parametric generalization of the mechanism of Figure 5.3. Assume that the data generating distribution is , so that the model is misspecified. Let be an arbitrary prior distribution and its corresponding non-parametric prior. By removing an arbitrarily small amount of mass from and placing it on one obtains an arbitrarily close prior distribution that is consistent with respect to the data generating distribution . Therefore although and may be made arbitrarily close, their posterior distributions would remain asymptotically separated by a distance corresponding to the degree of misspecification of the model (the distance from to ).

6 Proofs

6.1 Proof of Corollary 3.1

We seek to apply Schwartz’ theorem [40, Thm. 6.1]. Since and are separable metric spaces, their Borel -algebras are countably generated, so Doob’s Theorem [17, Thm. V.58] and the measurability of the dominated model implies that a family of densities can be chosen to be measurable, thus satisfying this requirement of [40, Thm. 6.1]. Since is a neighborhood it follows that it contains an open neighborhood of . Since is open and is open, it follows that is open in , and therefore there is an open set such that . Moreover, is an open neighborhood of . Since is a separable metric space, it follows that metrizes the weak topology, and since is open, it is well known (see e.g. [2, 43, 21]) that there exists a uniformly consistent test of against , see Schwartz [40] for the definition of uniformly consistent test. It follows trivially that there exists a uniformly consistent test of against . Moreover, since is injective it follows that . Therefore, there exists a uniformly consistent test of against .

Since is open, it also follows that there is a Prokhorov metric ball of radius about such that . Now consider the Kullback-Leibler ball for . It follows from Csiszar, Kemperman and Kullback’s [12] improvement of Pinsker’s inequality and the inequality , that . Since then it follows that

Consider now the Kullback-Leibler neighborhood of defined by pulling back to by the model :

Then the previous inequality states that

Since the Kullback-Leibler neighborhoods are measurable in the weak topology and is assumed measurable, it follows that is measurable.

6.2 Proof of Theorem 4.1

Let us prove the assertion for a weaker pseudometric derived from the Prokhorov metric on on . Since it is weaker the assertion follows. To that end, consider . Then for two random variables it follows that , so we can define a pseudometric by

| (6.1) |

Since Dudley [18, Thm. 11.3.5] asserts that

| (6.2) |

we conclude that

| (6.3) |

For fixed and and , the -valued random variable

defined by in (2.4) satisfies

| (6.4) |

where is the pushforward operator corresponding to the map defined by in (2.3). Consequently, we obtain

| (6.5) |

for and fixed. From the triangle inequality we then obtain

bounding the simple single term in terms of the sum of two terms and of qualitative robustness in Definition 2.1. Conseuquently, the assumption of the pseudometric amounts to Definition 2.1 with one epsilon instead of two corresponding to the metric

| (6.6) |

Moreover, non qualitative robustness with respect to this definition implies non qualitative robustness with respect to the original Definition 2.1 with the Ky Fan metric.

Now lets turn to the proof that the inference is non qualitatively robust with respect to the objective metric (6.6). Fix and consider another point and the Dirac mass situated at . For , the convex combination

is a probability measure with Kullback-Leibler support, that is, and

| (6.7) |

Therefore, it follows that

and therefore

where is the admissible set defined in (4.1).

For the prior , let , defined by , denote the corresponding sequence of posterior random variables, and let denote its induced sequence of laws. On the other hand, for the prior , it is easy to see that , so that if we denote the corresponding sequence of posterior random variables by , then .

Since the assumptions of Schwartz’ Corollary 3.1 are satisfied and has Kullback-Leibler support at , we can apply the assertion (7.1) of Proposition 7.1

for . To complete the proof we simply use the fact that convergence in law to a Dirac mass is equivalent to convergence in probability to a constant random variable, that is use the equivalent assertion (7.2) of Proposition 7.1

| (6.8) |

Now the proof is very simple. Indeed, from the triangle inequality we have

and, by two applications of Proposition 7.4, we have

Therefore, since , the convergence (6.8) implies that

Finally, since , it follows from (6.7) that

Then, for any , if we restrict so that , it follows that and so that

| (6.9) |

| (6.10) |

Let denote the diameter of . Then it follows from the triangle inequality that, for any , there exists a such that . Consequently, for any , no matter how small is, there is an such that, in addition to (6.9) and (6.10), we have

for large enough . Consequently, the assertion is proved.

6.3 Proof of Theorem 4.4

As in the proof of Theorem 4.1, we establish the assertion with respect to the modified form of qualitative robustness defined by (6.6), and since this form is weaker it implies the assertion. It follows from the definition of the packing numbers that, for , there is a packing and therefore the collection of open balls is a disjoint union. Denoting and , we therefore obtain

Consequently, since (4.2) implies , there exists a point such that

| (6.11) |

Let denote the open ball about and let denote its complement. Let , defined by

denote the normalization of the restriction of to which, by the inequality (6.11), is well defined. Since it follows that so that we obtain

from which we obtain

| (6.12) |

In particular, when , we obtain

and therefore

That is, when , the point .

For the prior , let , defined by , denote the corresponding sequence of posterior random variables, and let denote its induced sequence of laws. Since the assumptions of Schwartz’ Corollary 3.1 are satisfied and has Kullback-Leibler support at , we can apply the assertion (7.2) of Proposition 7.1 to the sequence of posterior laws corresponding to :

| (6.13) |

From the triangle inequality we have

| (6.14) |

so to lower bound the lefthand side it is sufficient in the limit to lower bound the first term on the right. To that end, we use a quantitative version of the partial converse [18, Thm. 11.3.5] of convergence in probability implies convergence in law, valid when the convergence in law is to a Dirac mass. Indeed, if we denote the Ky Fan metric determined from the measure by , Lemma 7.3 asserts that

| (6.15) |

To evaluate the Ky Fan distance on the righthand side, first observe that since has support contained in the closed set , it follows from Schervish [39, Thm. 1.31] that also has support contained in a.e . Therefore, if we define and , it follows that , so that

and

It follows from Lemma 7.2 that

and, since , we obtain

Therefore, by the definition (2.2) of the Ky Fan metric, we obtain and, by the identity (6.15), we conclude that

Consequently, from the triangle inequality (6.14) and the convergence (6.13), we conclude, for any , that for large enough we have

| (6.16) |

Consequently, if this Bayesian inference is qualitatively robust, then for , it follows from (6.16) and (6.12) that . The requirement that perturbations be admissible, that is determine members in , implies that .

7 Appendix

7.1 Schwartz’ Theorem and the convergence of random measures

It will be useful to express the assertion of Corollary 3.1 and some of its consequences in terms of the convergence of measures and random measures. To that end, recall the notation , and consider the corresponding sequence of random variables , defined by , and its induced sequence of laws . Note especially that is the Dirac mass in situated at the Dirac mass in situated at .

Proposition 7.1.

The assertion of Corollary 3.1 is equivalent to

where is weak convergence. This in turn implies that

| (7.1) |

for , which is equivalent to

| (7.2) |

where is the Prokhorov metric on defined with respect to the Prokhorov metric on .

Proof.

Let denote the open sets in and denote the open neighborhoods of . Then, under the conditions of Corollary 3.1, for , it follows that

Since and it easily follows that

which, by the Portmanteau theorem [18, Thm. 11.1.1], is equivalent to

where denotes weak convergence.

Now consider the corresponding sequence of random variables , defined by , and its induced sequence of laws . Then is equivalent to

Since is a separable metric space it follows that equipped with the Prokhorov metric is a separable metric space. Since a.s. convergence implies convergence in probability for random variables with values in a separable metric space, it follows that

that is,

Since is a separable metric space it follows that equipped with the Prokhorov metric is also a separable metric space. Therefore, since on separable metric spaces convergence in probability to a constant valued random variable is equivalent to the weak convergence of the corresponding set of laws to the Dirac mass situated at that value, see e.g. Dudley [18, Prop. 11.1.3], it follows that the convergence in probability, , is equivalent to the corresponding convergence of laws

Finally, since the Proprokhorov metric on metrizes the weak topology on , it follows that the latter is equivalent to

∎

7.2 Some Prokhorov Geometry

We establish a basic mechanism to bound from below the Prokhorov distance between two measures based on the values of the measures on the neighborhood of a single set.

Lemma 7.2.

Let be a metric space and consider the space of Borel probability measures equipped with the Prokhorov metric. Consider and suppose that there exists a set and such that

Then, for any , we have

Proof.

If the assertion is proved, so let us assume that . Then, denoting , it follows from the assumption that , so that

from which we conclude that . Therefore, either or , proving the assertion. ∎

Lemma 7.3.

Let be a separable metric space. Then, for an -valued random variable we have

where is the Ky Fan metric and denotes the random variable with constant value .

Proof.

Let us denote and . Define the set and and observe that . Therefore, by the definition of we have

and since we obtain

from which we obtain Since this implies that

we conclude that . Since Dudley [18, Thm. 11.3.5] asserts that , the assertion follows. ∎

Proposition 7.4.

Proof.

Consider the set . Then since , it follows that for that . Consequently, since , the inequality

requires either or which implies that . Consequently, . To obtain equality, suppose that . Then, for any which satisfies there exists a measurable set such that

Consequently, , but implies that , which implies the contradiction . ∎

Acknowledgments

The authors gratefully acknowledges this work supported by the Air Force Office of Scientific Research and the DARPA EQUiPS Program under awards number FA9550-12-1-0389 (Scientific Computation of Optimal Statistical Estimators) and number FA9550-16-1-0054 (Computational Information Games).

References

- [1] C. D. Aliprantis and K. C. Border. Infinite Dimensional Analysis: A Hitchhiker’s Guide. Springer, Berlin, third edition, 2006.

- [2] A. Barron, M. J. Schervish, and L. Wasserman. The consistency of posterior distributions in nonparametric problems. Ann. Statist., 27(2):536–561, 1999.

- [3] S. Basu, S. R. Jammalamadaka, and W. Liu. Stability and infinitesimal robustness of posterior distributions and posterior quantities. Journal of statistical planning and inference, 71(1):151–162, 1998.

- [4] R. H. Berk. Limiting behavior of posterior distributions when the model is incorrect. Ann. Math. Statist. 37 (1966), 51–58; correction, ibid, 37:745–746, 1966.

- [5] B. Betrò. Numerical treatment of Bayesian robustness problems. Internat. J. Approx. Reason., 50(2):279–288, 2009.

- [6] B. Betrò and A. Guglielmi. Numerical robust Bayesian analysis under generalized moment conditions. In Bayesian robustness (Rimini, 1995), volume 29 of IMS Lecture Notes Monogr. Ser., pages 3–20. Inst. Math. Statist., Hayward, CA, 1996. With a discussion by Elías Moreno and a rejoinder by the authors.

- [7] B. Betrò and A. Guglielmi. Methods for global prior robustness under generalized moment conditions. In Robust Bayesian analysis, volume 152 of Lecture Notes in Statist., pages 273–293. Springer, New York, 2000.

-

[8]

B. Betrò, F. Ruggeri, and M. M

czarski. Robust Bayesian analysis under generalized moments conditions. J. Statist. Plann. Inference, 41(3):257–266, 1994.‘ e - [9] P. Billingsley. Convergence of Probability Measures. Wiley, New York, second edition, 1999.

- [10] G. Boente, R. Fraiman, and V. J. Yohai. Qualitative robustness for stochastic processes. The Annals of Statistics, pages 1293–1312, 1987.

- [11] T. Bui-Thanh and O. Ghattas. An analysis of infinite dimensional Bayesian inverse shape acoustic scattering and its numerical approximation. SIAM/ASA J. Uncertain. Quantif., 2(1):203–222, 2014.

- [12] I. Csiszár. I-divergence geometry of probability distributions and minimization problems. The Annals of Probability, pages 146–158, 1975.

- [13] A. Cuevas. Qualitative robustness in abstract inference. Journal of Statistical Planning and Inference, 18(3):277–289, 1988.

- [14] A. Cuevas. Comment on ‘Bounds on posterior expectations for density bounded class with constant bandwidth’ by Sivaganesan. Journal of Statistical Planning and Inference, 40(2):340–343, 1994.

- [15] A. Cuevas González. Una definición de robustez cualitativa en inferencia Bayesiana. Trabajos de Estadística y de Investigación Operativa, 35(2):170–186, 1984.

- [16] M. Dashti and A. M. Stuart. Uncertainty quantification and weak approximation of an elliptic inverse problem. SIAM J. Numer. Anal., 49(6):2524–2542, 2011.

- [17] C. Dellacherie and P.-A. Meyer. Probabilities and Potential. B, Vol. 72 of North-Holland Mathematics Studies. North-Holland Publishing Co., Amsterdam, 1982.

- [18] R. M. Dudley. Real Analysis and Probability, volume 74 of Cambridge Studies in Advanced Mathematics. Cambridge University Press, Cambridge, 2002. Revised reprint of the 1989 original.

- [19] P. Dupuis and R. S. Ellis. A Weak Convergence Approach to the Theory of Large Deviations, volume 902. John Wiley & Sons, 2011.

- [20] A. Gelman. Inference and monitoring convergence. In Markov chain Monte Carlo in practice, pages 131–143. Springer, 1996.

- [21] S. Ghosal, J. K. Ghosh, and R. V. Ramamoorthi. Consistency issues in Bayesian nonparametrics. Statistics Textbooks and Monographs, 158:639–668, 1999.

- [22] A. L. Gibbs. Convergence in the Wasserstein metric for Markov chain Monte Carlo algorithms with applications to image restoration. Stoch. Models, 20(4):473–492, 2004.

- [23] A. L. Gibbs and F. E. Su. On choosing and bounding probability metrics. International Statistical Review, 70(3):419–435, 2002.

- [24] P. Gustafson and L. Wasserman. Local sensitivity diagnostics for Bayesian inference. The Annals of Statistics, 23(6):2153–2167, 1995.

- [25] R. Hable and A. Christmann. On qualitative robustness of support vector machines. Journal of Multivariate Analysis, 102(6):993–1007, 2011.

- [26] R. Hable and A. Christmann. Robustness versus consistency in ill-posed classification and regression problems. In Classification and Data Mining, pages 27–35. Springer, 2013.

- [27] F. R. Hampel. A general qualitative definition of robustness. The Annals of Mathematical Statistics, pages 1887–1896, 1971.

- [28] P. J. Huber and E. M. Ronchetti. Robust Statistics. Wiley Series in Probability and Statistics. John Wiley & Sons Inc., Hoboken, NJ, second edition, 2009.

- [29] A. N. Kolmogorov and V. M. Tikhomirov. -entropy and -capacity of sets in function spaces. Trans. Amer. Math. Soc, 17:277–364, 1961.

- [30] N. Madras and D. Sezer. Quantitative bounds for Markov chain convergence: Wasserstein and total variation distances. Bernoulli, 16(3):882–908, 2010.

- [31] I. Mizera. Qualitative robustness and weak continuity: the extreme unction. Nonparametrics and Robustness in Modern Statistical Inference and Time Series Analysis: A Festschrift in honor of Professor Jana Jurecková, 1:169, 2010.

- [32] M. Nasser, N. A. Hamzah, and Md. A. Alam. Qualitative robustness in estimation. Pakistan Journal of Statistics and Operation Research, 8(3):619–634, 2012.

- [33] H. Owhadi and C. Scovel. Brittleness of Bayesian inference and new Selberg formulas. Commun. Math. Sci., 13(75), 2013.

- [34] H. Owhadi, C. Scovel, and T. J. Sullivan. Brittleness of Bayesian inference under finite information in a continuous world. Electron. J. Statist., 9:1–79, 2015.

- [35] H. Owhadi, C. Scovel, and T. J. Sullivan. On the brittleness of Bayesian inference. SIAM Review, 57(4):566–582, 2015.

- [36] S. T. Rachev, L. B. Klebakov, S. V. Stoyanov, and F. J. Fabozzi. The Methods of Distances in the Theory of Probability and Statistics. Springer, New York, 2013.

- [37] G. O. Roberts and J. S. Rosenthal. Markov-chain Monte Carlo: Some practical implications of theoretical results. Canadian Journal of Statistics, 26(1):5–20, 1998.

- [38] G. O. Roberts and J. S. Rosenthal. General state space Markov chains and MCMC algorithms. Probability Surveys, 1:20–71, 2004.

- [39] M. J. Schervish. Theory of Statistics. Springer, 1995.

- [40] L. Schwartz. On Bayes procedures. Z. Wahrscheinlichkeitstheorie und Verw. Gebiete, 4:10–26, 1965.

- [41] A. M. Stuart. Inverse problems: a Bayesian perspective. Acta Numer., 19:451–559, 2010.

- [42] A. Wald. Statistical Decision Functions. John Wiley & Sons Inc., New York, NY, 1950.

- [43] L. Wasserman. Asymptotic properties of nonparametric Bayesian procedures. In Practical nonparametric and semiparametric Bayesian statistics, pages 293–304. Springer, 1998.

- [44] A. D. Woodbury and T. J. Ulrych. A full-bayesian approach to the groundwater inverse problem for steady state flow. Water Resources Research, 36(8):2081–2093, 2000.