Berk-Nash Equilibrium: A Framework for Modeling Agents with Misspecified

Models††thanks: We thank Vladimir Asriyan, Pierpaolo Battigalli, Larry Blume, Aaron

Bodoh-Creed, Sylvain Chassang, Emilio Espino, Erik Eyster, Drew Fudenberg,

Yuriy Gorodnichenko, Stephan Lauermann, Natalia Lazzati, Kristóf Madarász,

Matthew Rabin, Ariel Rubinstein, Joel Sobel, Jörg Stoye, several seminar

participants, and especially a co-editor and four anonymous referees

for very helpful comments. Esponda: Olin Business School, Washington

University in St. Louis, 1 Brookings Drive, Campus Box 1133, St. Louis,

MO 63130, iesponda@wustl.edu; Pouzo: Department of Economics, UC Berkeley,

530-1 Evans Hall #3880, Berkeley, CA 94720, dpouzo@econ.berkeley.edu.

Abstract

We develop an equilibrium framework that relaxes the standard assumption that people have a correctly-specified view of their environment. Each player is characterized by a (possibly misspecified) subjective model, which describes the set of feasible beliefs over payoff-relevant consequences as a function of actions. We introduce the notion of a Berk-Nash equilibrium: Each player follows a strategy that is optimal given her belief, and her belief is restricted to be the best fit among the set of beliefs she considers possible. The notion of best fit is formalized in terms of minimizing the Kullback-Leibler divergence, which is endogenous and depends on the equilibrium strategy profile. Standard solution concepts such as Nash equilibrium and self-confirming equilibrium constitute special cases where players have correctly-specified models. We provide a learning foundation for Berk-Nash equilibrium by extending and combining results from the statistics literature on misspecified learning and the economics literature on learning in games.

1 Introduction

Most economists recognize that the simplifying assumptions underlying their models are often wrong. But, despite recognizing that models are likely to be misspecified, the standard approach (with exceptions noted below) assumes that economic agents have a correctly specified view of their environment. We present an equilibrium framework that relaxes this standard assumption and allows the modeler to postulate that economic agents have a subjective and possibly incorrect view of their world.

An objective game represents the true environment faced by the agent (or players, in the case of several interacting agents). Payoff relevant states and privately observed signals are drawn from an objective probability distribution. Each player observes her own private signal and then players simultaneously choose actions. The action profile and the realized state determine consequences, and consequences determine payoffs.

In addition, each player has a subjective model representing her own view of the environment. Formally, a subjective model is a set of probability distributions over own consequences as a function of a player’s own action and information. Crucially, we allow the subjective model of one or more players to be misspecified, which roughly means that the set of subjective distributions does not include the true, objective distribution. For example, a consumer might perceive a nonlinear price schedule to be linear and, therefore, respond to average, not marginal, prices. Or traders might not realize that the value of trade is partly determined by the terms of trade.

A Berk-Nash equilibrium is a strategy profile such that, for each player, there exists a belief with support in her subjective model satisfying two conditions. First, the strategy is optimal given the belief. Second, the belief puts probability one on the set of subjective distributions over consequences that are “closest” to the true distribution, where the true distribution is determined by the objective game and the actual strategy profile. The notion of “closest” is given by a weighted version of the Kullback-Leibler divergence, also known as relative entropy.

Berk-Nash equilibrium includes standard and boundedly rational solution concepts in a common framework, such as Nash, self-confirming (e.g., Battigalli (1987), Fudenberg and Levine (1993a), Dekel et al. (2004)), fully cursed (Eyster and Rabin, 2005), and analogy-based expectation equilibrium (Jehiel (2005), Jehiel and Koessler (2008)). For example, suppose that the game is correctly specified (i.e., the support of each player’s prior contains the true distribution) and that the game is strongly identified (i.e., there is a unique distribution—whether or not correct—that matches the observed data). Then Berk-Nash equilibrium is equivalent to Nash equilibrium. If the strong identification assumption is dropped, then Berk-Nash is a self-confirming equilibrium. In addition to unifying previous work, our framework provides a systematic approach for extending previous cases and exploring new types of misspecifications.

We provide a foundation for Berk-Nash equilibrium (and the use of Kullback-Leibler divergence as a measure of “distance”) by studying a dynamic setup with a fixed number of players playing the objective game repeatedly. Each player believes that the environment is stationary and starts with a prior over her subjective model. In each period, players use the observed consequences to update their beliefs according to Bayes’ rule. The main objective is to characterize limiting behavior when players behave optimally but learn with a possibly misspecified subjective model.111In the case of multiple agents, the environment need not be stationary, and so we are ignoring repeated game considerations where players take into account how their actions affect others’ future play. We discuss the extension to a population model with a continuum of agents in Section 5.

The main result is that, if players’ behavior converges, then it converges to a Berk-Nash equilibrium. A converse result, showing that we can converge to any Berk-Nash equilibrium of the game for some initial (non-doctrinaire) prior, does not hold. But we obtain a positive convergence result by relaxing the assumption that players exactly optimize. For any given Berk-Nash equilibrium, we show that convergence to that equilibrium occurs if agents are myopic and make asymptotically optimal choices (i.e., optimization mistakes vanish with time).

There is a longstanding interest in studying the behavior of agents who hold misspecified views of the world. Examples come from diverse fields including industrial organization, mechanism design, information economics, macroeconomics, and psychology and economics (e.g., Arrow and Green (1973), Kirman (1975), Sobel (1984), Kagel and Levin (1986), Nyarko (1991), Sargent (1999), Rabin (2002)), although there is often no explicit reference to misspecified learning. Most of the literature, however, focuses on particular settings, and there has been little progress in developing a unified framework. Our treatment unifies both “rational” and “boundedly rational” approaches, thus emphasizing that modeling the behavior of misspecified players does not constitute a large departure from the standard framework.

Arrow and Green (1973) provide a general treatment and make a distinction between objective and subjective games. Their framework, though, is more restrictive than ours in terms of the types of misspecifications that players are allowed to have. Moreover, they do not establish existence or provide a learning foundation for equilibrium. Recently, Spiegler (2014) introduced a framework that uses Bayesian networks to analyze decision making under imperfect understanding of correlation structures.222Some explanations for why players may have misspecified models include the use of heuristics (Tversky and Kahneman, 1973), complexity (Aragones et al., 2005), the desire to avoid over-fitting the data (Al-Najjar (2009), Al-Najjar and Pai (2013)), and costly attention (Schwartzstein, 2009).

Our paper is also related to the bandit (e.g., Rothschild (1974), McLennan (1984), Easley and Kiefer (1988)) and self-confirming equilibrium (SCE) literatures, which highlight that agents might optimally end up with incorrect beliefs if experimentation is costly.333In the macroeconomics literature, the term SCE is sometimes used in a broader sense to include cases where agents have misspecified models (e.g., Sargent, 1999). We also allow beliefs to be incorrect due to insufficient feedback, but our main contribution is to allow for misspecified learning. When players have misspecified models, beliefs may be incorrect and endogenously depend on own actions even if there is persistent experimentation; thus, an equilibrium framework is needed to characterize steady-state behavior even in single-agent settings.444Two extensions of SCE are also potentially applicable: restrictions on beliefs based on introspection (e.g., Rubinstein and Wolinsky, 1994), and ambiguity aversion (Battigalli et al., 2012).

From a technical perspective, we extend and combine results from two literatures. First, the idea that equilibrium is a result of a learning process comes from the literature on learning in games. This literature studies explicit learning models to justify Nash and SCE (e.g., Fudenberg and Kreps (1988), Fudenberg and Kreps (1993), Fudenberg and Kreps (1995), Fudenberg and Levine (1993b), Kalai and Lehrer (1993)).555See Fudenberg and Levine (1998, 2009) for a survey of this literature. We extend this literature by allowing players to learn with models of the world that are misspecified even in steady state.

Second, we rely on and contribute to the literature studying the limiting behavior of Bayesian posteriors. The results from this literature have been applied to decision problems with correctly specified agents (e.g., Easley and Kiefer, 1988). In particular, an application of the martingale convergence theorem implies that beliefs converge almost surely under the agent’s subjective prior. This result, however, does not guarantee convergence of beliefs according to the true distribution if the agent has a misspecified model and the support of her prior does not include the true distribution. Thus, we take a different route and follow the statistics literature on misspecified learning. This literature characterizes limiting beliefs in terms of the Kullback-Leibler divergence (e.g., Berk (1966), Bunke and Milhaud (1998)).666White (1982) shows that the Kullback-Leibler divergence also characterizes the limiting behavior of the maximum quasi-likelihood estimator. We extend the statistics literature on misspecified learning to the case where agents are not only passively learning about their environment but are also actively learning by taking actions.

2 The framework

2.1 The environment

A (simultaneous-move) game is composed of a (simultaneous-move) objective game and a subjective model .

Objective game. A (simultaneous-move) objective game is a tuple

where: is the set of players; is the set of payoff-relevant states; is the set of profiles of signals, where is the set of signals of player ; is a probability distribution over , and, for simplicity, it is assumed to have marginals with full support; we use standard notation to denote marginal and conditional distributions, e.g., denotes the conditional distribution over given ; is a set of profiles of actions, where is the set of actions of player ; is a set of profiles of (observable) consequences, where is the set of consequences of player ; is a profile of feedback or consequence functions, where maps outcomes in into consequences of player ; and , where is the payoff function of player .777The concept of a feedback function is borrowed from the SCE literature. Also, while it is redundant to have depend on , it simplifies the notation in applications. For simplicity, we prove the results for the case where all of the above sets are finite.888In the working paper version (Esponda and Pouzo, 2014), we provide technical conditions under which the results extend to nonfinite and .

The timing of the objective game is as follows: First, a state and a profile of signals are drawn according to . Second, each player privately observes her own signal. Third, players simultaneously choose actions. Finally, each player observes her consequence and obtains a payoff. We implicitly assume that players observe at least their own actions and payoffs.999See Online Appendix E for the case where players do not observe own payoffs.

A strategy of player is a mapping . The probability that player chooses action after observing signal is denoted by . A strategy profile is a vector of strategies ; let denote the space of all strategy profiles.

Fix an objective game. For each strategy profile , there is an objective distribution over player ’s consequences, , where

| (1) |

for all .101010As usual, the superscript denotes a profile where the ’th component is excluded The objective distribution represents the true distribution over consequences, conditional on a player’s own action and signal, given the objective game and a strategy profile followed by the players.

Subjective model. The subjective model represents the set of distributions over consequences that players consider possible a priori. For a fixed objective game, a subjective model is a tuple

where and is player ’s parameter set; and , where is the conditional distribution over player ’s consequences parameterized by ; we denote the conditional distribution by .111111For simplicity, we assume that players know the distribution over own signals.

While the objective game represents the true environment, the subjective model represents the players’ perception of their environment. This separation between objective and subjective models is crucial in this paper.

Remark 1.

A special case of a subjective model is one where each player understands the objective game being played but is uncertain about the distribution over states, the consequence function, and (in the case of multiple players) the strategies of other players. In this special case, player ’s uncertainty about , , and can be described by a parametric model , , where . A subjective distribution is then derived by replacing , , and with , in equation (1).121212In this case, a player understands that other players mix independently but, due to uncertainty over the parameter that indexes , she may have correlated beliefs about her opponents’ strategies, as in Fudenberg and Levine (1993a).

By defining as a primitive, we stress two points. First, this object is sufficient to characterize behavior. Second, working with general subjective distributions allows for more general types of misspecifications, where players do not even have to understand the structural elements that determine their payoff relevant consequences.

We maintain the following assumptions about the subjective model.

Assumption 1. For all : (i) is a compact subset of an Euclidean space, (ii) is continuous as a function of for all , (iii) For all , there exists a sequence in such that and such that, for all , for all , , and .

Conditions (i) and (ii) are the standard conditions used to define a parametric model in statistics (e.g., Bickel et al. (1993)). Condition (iii) plays two roles. First, it guarantees that there exists at least one parameter value that attaches positive probability to every feasible observation. In particular, it rules out what can be viewed as a stark misspecification in which every element of the subjective model attaches zero probability to an event that occurs with positive true probability. Second, it imposes a “richness” condition on the subjective model: If a feasible event is deemed impossible by some parameter value, then that parameter value is not isolated in the sense that there are nearby parameter values that consider every feasible event to be possible. In Section 5, we show that equilibrium may fail to exist and steady-state behavior need not be characterized by equilibrium without this assumption.

2.2 Examples

We illustrate the environment by presenting several examples that had previously not been integrated into a common framework.131313Nyarko (1991) studies a special case of Example 2.1 and shows that a steady state does not exist in pure strategies; Sobel (1984) considers a misspecification similar to Example 2.2; Tversky and Kahneman’s (1973) story motivates Example 2.3; Sargent (1999, Chapter 7) studies Example 2.4; and Kagel and Levin (1986), Eyster and Rabin (2005), Jehiel and Koessler (2008), and Esponda (2008) study Example 2.5. See Esponda and Pouzo (2014) for additional examples. In examples with a single agent, we drop the subscript from the notation.

Example 2.1. Monopolist with unknown demand. A monopolist faces demand , where is the price chosen by the monopolist and is a mean-zero shock with distribution . The monopolist observes sales , but not the shock. The monopolist does not observe any signal, and so we omit signals from the notation. The monopolist’s payoff is (i.e., there are no costs). The monopolist’s uncertainty about and is described by a parametric model , where is the demand function, is a parameter vector, and (i.e., is a standard normal distribution for all ). In particular, this example corresponds to the special case discussed in Remark 1, and is a normal density with mean and unit variance.

Example 2.2. Nonlinear taxation. An agent chooses effort at cost and obtains income , where is a zero-mean shock with distribution . The agent pays taxes , where is a nonlinear tax schedule. The agent does not observe any signal, and so we omit them. The agent observes and obtains payoff .141414Formally, , where and . She understands how effort translates into income but fails to realize that the marginal tax rate depends on income. We compare two models that capture this misspecification. In model A, the agent believes in a random coefficient model, , in which the marginal and average tax rates are both equal to , where . In model B, the agent believes that , where is the constant marginal tax rate and .151515It is not necessary to assume that and are compact for an equilibrium to exist; the same comment applies to Examples 2.3 and 2.4 In both models, measures uncertain aspects of the schedule (e.g., variations in tax rates or credits). Thus, , where is a normal density with mean and variance in model and mean and unit variance in model .

Example 2.3. Regression to the mean. An instructor observes the initial performance of a student and decides to praise or criticize him, . The student then performs again and the instructor observes his final performance, . The truth is that performances are independent, standard normal random variables. The instructor’s payoff is , where if either or , and, in all other cases, .161616Formally, , is the product of standard normal distributions, and . The function represents a (reputation) cost from lying (i.e., criticizing above-average performances or praising below-average ones) that increases in the size of the lie. Because the instructor cannot influence performance, it is optimal to praise if and to criticize if . The instructor, however, does not admit the possibility of regression to the mean and believes that , where , and parameterizes her perceived influence on performance.171717A model that allows for regression to the mean is ; in this case, the agent would correctly learn that and for all . Rabin and Vayanos (2010) study a related setup in which the agent believes that shocks are autoregressive when in fact they are i.i.d. Thus, letting be the a normal density with mean and unit variance, it follows that if and otherwise.

Example 2.4. Monetary policy. Two players, the government (G) and the public (P), i.e., , choose monetary policy and inflation forecasts , respectively. They do not observe signals, and so we omit them. Inflation, , and unemployment, , are determined by181818Formally, and is given by equations (2) and (3).

| (2) | |||||

| (3) |

where , and are shocks with a full support distribution and . The public and the government observe realized inflation and unemployment, but not the error terms. The government’s payoff is . For simplicity, we focus on the government’s problem and assume that the public has correct beliefs and chooses . The government understands how its policy affects inflation, but does not realize that unemployment is affected by surprise inflation:

| (4) |

The subjective model is parameterized by , and it follows that is the density implied by the equations (2) and (4).

Example 2.5. Trade with adverse selection. A buyer with valuation and a seller submit a (bid) price and an ask price , respectively. The seller’s ask price and the buyer’s value are drawn from , so that is the state space. Thus, the buyer is the only decision maker.191919The typical story is that there is a population of sellers each of whom follows the weakly dominant strategy of asking for her valuation; thus, the ask price is a function of the seller’s valuation and, if buyer and seller valuations are correlated, then the ask price and buyer valuation are also correlated. After submitting a price, the buyer observes and gets payoff if and zero otherwise. In other words, the buyer observes perfect feedback, gets if there is trade, and otherwise. When making an offer, she does not know her value or the seller’s ask price. She also does not observe any signals, and so we omit them. Finally, suppose that and are correlated but that the buyer believes they are independent. This is captured by letting and .

2.3 Definition of equilibrium

In equilibrium, we will require players’ beliefs to put probability one on the set of subjective distributions over consequences that are “closest” to the objective distribution. The following function, which we call the weighted Kullback-Leibler divergence (wKLD) function of player , is a weighted version of the standard Kullback-Leibler divergence in statistics (Kullback and Leibler, 1951). It represents a “distance” between the objective distribution over ’s consequences given a strategy profile and the distribution as parameterized by :202020The notation denotes expectation with respect to the probability distribution . Also, we use the convention that and .

| (5) |

The set of closest parameter values of player given is the set

The interpretation is that is the set of parameter values that player can believe to be possible after observing feedback consistent with strategy profile .

Remark 2.

We show in Section 4 that wKLD is the right notion of distance in a learning model with Bayesian players. Here, we provide an heuristic argument for a Bayesian agent (we drop subscripts for clarity) with parameter set who observes data over periods, , that comes from repeated play of the objective game under strategy . Let denote the agent’s ratio of priors. Applying Bayes’ rule and simple algebra, the posterior probability over after periods is

where the second equality follows by multiplying and dividing by . By a law of large numbers argument and the fact that the true joint distribution over is given by , the difference in the log-likelihood ratios converges to . Suppose that . Then, for sufficiently large , the posterior belief is approximately equal to , which converges to 0. Therefore, the posterior eventually assigns zero probability to . On the other hand, if , then the posterior eventually assigns zero probability to . Thus, the posterior eventually assigns zero probability to parameter values that do not minimize .

Remark 3.

Because the wKLD function is weighted by a player’s own strategy, it places no restrictions on beliefs about outcomes that only arise following out-of-equilibrium actions (beyond the restrictions imposed by ).

The next result collects some useful properties of the wKLD function.

Lemma 1.

(i) For all , , and , , with equality holding if and only if for all such that . (ii) For all , is nonempty, upper hemicontinuous, and compact valued.

Proof.

See the Appendix. ∎

The upper-hemicontinuity of would follow from the Theorem of the Maximum had we assumed to be positive for all feasible events and , since the wKLD function would then be finite and continuous. But this assumption may be strong in some cases.212121For example, it rules out cases where a player believes others follow pure strategies. Assumption 1(iii) weakens this assumption by requiring that it holds for a dense subset of , and still guarantees that is upper hemicontinuous.

Optimality. In equilibrium, we will require each player to choose a strategy that is optimal given her beliefs. A strategy for player is optimal given if implies that

| (6) |

where is the distribution over consequences of player , conditional on , induced by .

Definition of equilibrium. We propose the following solution concept.

Definition 1.

A strategy profile is a Berk-Nash equilibrium of game if, for all players , there exists such that

(i) is optimal given , and

(ii) , i.e., if is in the support of , then

Definition 1 places two restrictions on equilibrium behavior: (i) optimization given beliefs, and (ii) endogenous restrictions on beliefs. For comparison, note that the definition of Nash equilibrium is identical to Definition 1 except that condition (ii) is replaced with the condition that players have correct beliefs, i.e., .

existence of equilibrium. The standard existence proof of Nash equilibrium cannot be used here because the analogous version of a best response correspondence is not necessarily convex valued. To prove existence, we first perturb payoffs and establish that equilibrium exists in the perturbed game. We then consider a sequence of equilibria of perturbed games, where perturbations go to zero, and establish that the limit is a Berk-Nash equilibrium of the (unperturbed) game.222222The idea of perturbations and the strategy of the existence proof date back to Harsanyi (1973); Selten (1975) and Kreps and Wilson (1982) also used these ideas to prove existence of perfect and sequential equilibrium, respectively. The nonstandard part of the proof is to prove existence of equilibrium in the perturbed game. The perturbed best response correspondence is still not necessarily convex valued. Our approach is to characterize equilibrium as a fixed point of a belief correspondence and show that it satisfies the requirements of a generalized version of Kakutani’s fixed point theorem.

Theorem 1.

Every game has at least one Berk-Nash equilibrium.

Proof.

See the Appendix. ∎

2.4 Examples: Finding a Berk-Nash equilibrium

Example 2.1, continued from pg. 2.2. Monopolist with unknown demand. Let denote a strategy, where is the probability of choosing price . Because this is a single-agent problem, the objective distribution does not depend on ; hence, we denote it by , which is a normal density with mean and unit variance. Similarly, is a normal density with mean and unit variance. It follows from equation (5) that

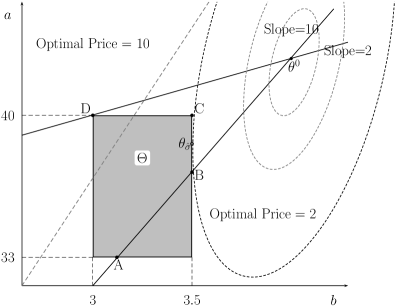

For concreteness, let , and , and .232323In particular, the deterministic part of the demand function can have any functional form provided it passes through and . Let provide a perfect fit for demand, i.e., for all . In this example, and, therefore, we say that the monopolist has a misspecified model. The dashed line in Figure 1 depicts optimal behavior: the optimal price is 10 to the left, it is 2 to the right, and the monopolist is indifferent for parameter values on the dashed line.

To solve for equilibrium, we first consider pure strategies. If (i.e., the price is ), the first order conditions imply , and any on the segment in Figure 1 minimizes . These minimizers, however, lie to the right of the dashed line, where it is not optimal to set a price of 10. Thus, is not an equilibrium. A similar argument establishes that is not an equilibrium: If it were, the minimizer would be at , where it is in fact not optimal to choose a price of 2.

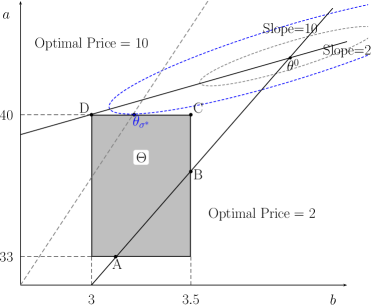

Left panel: the parameter value that minimizes the wKLD function given strategy is . Right panel: is a Berk-Nash equilibrium ( is optimal given —because lies on the indifference line—and minimizes the wKLD function given ).

Finally, consider mixed strategies. Because both first order conditions cannot hold simultaneously, the parameter value that minimizes lies on the boundary of . A bit of algebra shows that, for any totally mixed , there is a unique minimizer characterized as follows. If , the minimizer is on the segment : and solves . The left panel of Figure 1 depicts an example where the unique minimizer under strategy is given by the tangency between the contour lines of and the feasible set .242424It can be shown that , where is a weighting matrix that depends on . In particular, the contour lines of are ellipses. If , then is the northeast vertex of . Finally, if , the minimizer is on the segment : and solves .

Because the monopolist mixes, optimality requires that the equilibrium belief lies on the dashed line. The unique Berk-Nash equilibrium is , and its supporting belief, , is given by the intersection of the dashed line and the segment , as depicted in the right panel of Figure 1. It is not the case, however, that the equilibrium belief about the mean of is correct. Thus, an approach that had focused on fitting the mean, rather than minimizing , would have led to the wrong conclusion.252525The example also illustrates the importance of mixed strategies for existence of Berk-Nash equilibrium, even in single-agent settings. As an antecedent, Esponda and Pouzo (2011) argue that this is the reason why mixed strategy equilibrium cannot be purified in a voting application.

Example 2.2, continued from pg. 2.2. Nonlinear taxation. For any pure strategy and parameter value (model A) or (model B), the wKLD function for model equals

where denotes the true conditional expectation and and are constants.

For model A, is the unique parameter that minimizes .262626We use to denote the random variable that takes on realizations . Intuitively, the agent believes that the expected marginal tax rate is equal to the true expected average tax rate. For model B,

where the second equality follows from Stein’s lemma (Stein (1972)), provided that is differentiable. Intuitively, the agent believes that the marginal tax rate is constant and given by the true expected marginal tax rate.272727By linearity and normality, the minimizers of coincide with the OLS estimands. We assume normality for tractability, although the framework allows for general distributional assumptions. There are other tractable distributions; for example, the minimizer of wKLD under the Laplace distribution corresponds to the estimates of a median (not a linear) regression.

We now compare equilibrium under these two models with the case in which the agent has correct beliefs and chooses an optimal strategy that maximizes . In contrast, a strategy is a Berk-Nash equilibrium of model if and only if maximizes .

For example, suppose that the cost of effort and true tax schedule are both smooth functions, increasing and convex (e.g., taxes are progressive) and that is a compact interval. Then first order conditions are sufficient for optimality, and is the unique solution to . Moreover, the unique Berk-Nash equilibrium solves for model A and for model B. In particular, effort in model B is optimal, . Intuitively, the agent has correct beliefs about the true expected marginal tax rate at her equilibrium choice of effort, and so she has the right incentives on the margin, despite believing incorrectly that the marginal tax rate is constant. In contrast, effort is higher than optimal in model A, . Intuitively, the agent believes that the expected marginal tax rate equals the true expected average tax rate, which is lower than the true expected marginal tax rate in a progressive system.

Example 2.3, continued from pg. 2.2. Regression to the mean. Since optimal strategies are characterized by a cutoff, we let represent the strategy where the instructor praises an initial performance if it is above and criticizes it otherwise. The wKLD function for any is

where is the density of and denotes the true expectation. For each , the unique parameter vector that minimizes is

and, similarly, . Intuitively, the instructor is critical for performances below a threshold and, therefore, the mean performance conditional on a student being criticized is lower than the unconditional mean performance; thus, a student who is criticized delivers a better next performance in expectation. Similarly, a student who is praised delivers a worse next performance in expectation.

The instructor who follows a strategy cutoff believes, after observing initial performance , that her expected payoff is if she criticizes and if she praises. By optimality, the cutoff makes her indifferent between praising and criticizing. Thus, is the unique equilibrium cutoff. An instructor who ignores regression to the mean has incorrect beliefs about the influence of her feedback on the student’s performance: She is excessively critical in equilibrium because she incorrectly believes that criticizing a student improves performance and that praising a student worsens it. Moreover, as the reputation cost , meaning that instructors care only about performance and not about lying, : instructors only criticize (as in Tversky and Kahneman’s (1973) story).

3 Relationship to other solution concepts

We show that Berk-Nash equilibrium includes several solution concepts (both standard and boundedly rational) as special cases.

3.1 Properties of games

In Bayesian statistics, a model is correctly specified if the support of the prior includes the true data generating process. The extension to single-agent decision problems is straightforward. In games, however, we must account for the fact that the objective distribution over consequences (i.e., the true model) depends on the strategy profile.282828It would be more precise to say that the game is correctly specified in steady state.

Definition 2.

A game is correctly specified given if, for all , there exists such that for all for all ; otherwise, the game is misspecified given . A game is correctly specified if it is correctly specified for all ; otherwise, it is misspecified.

identification. From the player’s perspective, what matters is identification of the distribution over consequences , not the parameter . If the model is correctly specified, then the true is trivially identified. Of course, this is not true if the model is misspecified, because the true distribution will never be learned. But we want a definition that captures the same spirit: If two distributions are judged to be equally a best fit (given the true distribution), then we want these two distributions to be identical; otherwise, we cannot identify which distribution is a best fit. The fact that players take actions introduces an additional nuance to the definition of identification. We can ask for identification of the distribution over consequences either for those actions that are taken by the player (i.e., on the path of play) or for all actions (i.e., on and off the path).

Definition 3.

A game is weakly identified given if, for all : if , then for all such that (recall that has full support). If the condition is satisfied for all , then we say that the game is strongly identified given . A game is [weakly or strongly] identified if it is [weakly or strongly] identified for all .

A correctly specified game is weakly identified. Also, two games that are identical except for their feedback may differ in terms of being correctly specified or identified.

3.2 Relationship to Nash and self-confirming equilibrium

The next result shows that Berk-Nash equilibrium is equivalent to Nash equilibrium when the game is both correctly specified and strongly identified.

Proposition 1.

(i) Suppose that the game is correctly specified given and that is a Nash equilibrium of its objective game. Then is a Berk-Nash equilibrium of the (objective and subjective) game; (ii) Suppose that is a Berk-Nash equilibrium of a game that is correctly specified and strongly identified given . Then is a Nash equilibrium of the corresponding objective game.

Proof.

(i) Let be a Nash equilibrium and fix any . Then is optimal given . Because the game is correctly specified given , there exists such that and, therefore, by Lemma 1, . Thus, is also optimal given and , so that is a Berk-Nash equilibrium. (ii) Let be a Berk-Nash equilibrium and fix any . Then is optimal given , for some . Because the game is correctly specified given , there exists such that and, therefore, by Lemma 1, . Moreover, because the game is strongly identified given , any satisfies . Then is also optimal given . Thus, is a Nash equilibrium. ∎

Example 2.4, continued from pg. 2.2. Monetary policy. Fix a strategy for the public. Note that , whereas the government believes . Thus, by choosing such that and , it follows that the distribution over parameterized by coincides with the objective distribution given . So, despite appearances, the game is correctly specified given . Moreover, since , is the unique minimizer of the wKLD function given . Because there is a unique minimizer, then the game is strongly identified given . Since these properties hold for all , Proposition 1 implies that Berk-Nash equilibrium is equivalent to Nash equilibrium. Thus, the equilibrium policies are the same whether or not the government realizes that unemployment is driven by surprise, not actual, inflation.292929Sargent (1999) derived this result for a government doing OLS-based learning (a special case of our example when errors are normal). We assumed linearity for simplicity, but the result is true for the more general case with true unemployment and subjective model if, for all , there exists such that for all .

The next result shows that a Berk-Nash equilibrium is a self-confirming equilibrium (SCE) in games that are correctly specified, but not necessarily strongly identified.303030A strategy profile is a SCE if, for all players , is optimal given , where for all such that . This definition is slightly more general than the typical one, e.g., Dekel et al. (2004), because it does not restrict players to believe that consequences are driven by other players’ strategies.

Proposition 2.

Suppose that the game is correctly specified given , and that is a Berk-Nash equilibrium. Then is also a self-confirming equilibrium.313131A converse does not necessarily hold for a fixed game. The reason is that the definition of SCE does not impose any restrictions on off-equilibrium beliefs, while a particular subjective game may impose ex-ante restrictions on beliefs. The following converse, however, does hold: For any that is an SCE, there exists a game that is correctly specified for which is a Berk-Nash equilibrium.

Proof.

Fix any and let be in the support of , where is player ’s belief supporting the Berk-Nash equilibrium strategy . Because the game is correctly specified given , there exists such that and, therefore, by Lemma 1, . Thus, it must also be that . By Lemma 1, it follows that for all such that . In particular, is optimal given , and satisfies the desired self-confirming restriction. ∎

For games that are not correctly specified, beliefs can be incorrect on the equilibrium path, and so a Berk-Nash equilibrium is not necessarily Nash or SCE.

3.3 Relationship to fully cursed and ABEE

An analogy-based game satisfies the following four properties: (i) States and information structure: The state space is finite with distribution . In addition, for each , there is a partition of , and the element of that contains (i.e., the signal of player in state ) is denoted by ;323232This assumption is made to facilitate comparison with Jehiel and Koessler’s (2008) ABEE. (ii) Perfect feedback: For each , for all ; (iii) Analogy partition: For each , there exists a partition of , denoted by , and the element of that contains is denoted by ; (iv) Conditional independence: is the set of all joint probability distributions over that satisfy

In other words, every player believes that and are independent conditional on the analogy partition. For example, if for all , then each player believes that the actions of other players are independent of the state, conditional on their own private information.

Definition 4.

(Jehiel and Koessler, 2008) A strategy profile is an analogy-based expectation equilibrium (ABEE) if for all , , and such that , , where .

Proposition 3.

In an analogy-based game, is a Berk-Nash equilibrium if and only if it is an ABEE.

Proof.

See the Appendix. ∎

As mentioned by Jehiel and Koessler (2008), ABEE is equivalent to Eyster and Rabin’s (2005) fully cursed equilibrium in the special case where for all . In particular, Proposition 3 provides a misspecified-learning foundation for these two solution concepts. Jehiel and Koessler (2008) discuss an alternative foundation for ABEE, where players receive coarse feedback aggregated over past play and multiple beliefs are consistent with this feedback. Under this different feedback structure, ABEE can be viewed as a natural selection of the set of SCE.

Example 2.5, continued from pg. 2.2. Trade with adverse selection. In Online Appendix A, we show that is a Berk-Nash equilibrium price if and only if maximizes an equilibrium belief function which represents the belief about expected profit from choosing any price under a steady-state . The equilibrium belief function depends on the feedback/misspecification assumptions, and we discuss the following four cases:

The first case, , is the benchmark case in which beliefs are correct. The second case, , corresponds to perfect feedback and subjective model , as described in page 2.2. This is an example of an analogy-based game with single analogy class . The buyer learns the true marginal distributions of and and believes the joint distribution equals the product of the marginal distributions. Berk-Nash coincides with fully cursed equilibrium. The third case, , has the same misspecified model as the second case, but assumes partial feedback, in the sense that the ask price is always observed but the valuation is only observed if there is trade. The equilibrium price affects the sample of valuations observed by the buyer and, therefore, her beliefs. Berk-Nash coincides with naive behavioral equilibrium.

The last case, , corresponds to perfect feedback and the following misspecification: Consider a partition of into “analogy classes” . The buyer believes that are independent conditional on , for each . The parameter set is , where, for a value , parameterizes the marginal distribution over and, for each , parameterizes the distribution over conditional on . Berk-Nash coincides with the ABEE of the game with analogy classes .333333In Online Appendix A, we also consider the case of ABEE with partial feedback.

4 Equilibrium foundation

We provide a learning foundation for equilibrium. We follow Fudenberg and Kreps (1993) in considering games with (slightly) perturbed payoffs because, as they highlight in the context of providing a learning foundation for mixed-strategy Nash equilibrium, behavior need not be continuous in beliefs without perturbations. Thus, even if beliefs were to converge, behavior need not settle down in the unperturbed game. Perturbations guarantee that if beliefs converge, then behavior also converges.

4.1 Perturbed game

A perturbation structure is a tuple , where: and is a set of payoff perturbations for each action of player ; , where is a distribution over payoff perturbations of player that is absolutely continuous with respect to the Lebesgue measure, satisfies , and is independent from the perturbations of other players. A perturbed game is composed of a game and a perturbation structure . The timing of a perturbed game coincides with the timing of , except for two differences. First, before taking an action, each player not only observes her signal but also privately observes a vector of own-payoff perturbations , where denotes the perturbation for action . Second, her payoff given action and consequence is .

A strategy for player is optimal in the perturbed game given if, for all , , where

In other words, if is an optimal strategy, then is the probability that is optimal when the state is and the perturbation is , taken over all possible realizations of . The definition of Berk-Nash equilibrium of a perturbed game is analogous to Definition 1, with the only difference that optimality must be required with respect to the perturbed game.

4.2 Learning foundation

We fix a perturbed game and assume that players repeatedly play the corresponding objective game at each , where the time- state and signals, , and perturbations , are independently drawn every period from the same distribution and , respectively. In addition, each player has a prior with full support over her (finite-dimensional) parameter set, .343434We restrict attention to parametric models (i.e., finite-dimensional parameter spaces) because, otherwise, Bayesian updating need not converge to the truth for most priors and parameter values even in correctly specified statistical settings (Freedman (1963), Diaconis and Freedman (1986)). At the end of every period , each player uses Bayes’ rule and the information obtained in all past periods (her own signals, actions, and consequences) to update beliefs. Players believe that they face a stationary environment and myopically maximize the current period’s expected payoff.

Let denote the set of probability distributions on with full support. Let denote the Bayesian operator of player : for all Borel measurable and all ,

Bayesian updating is well defined by Assumption 1.353535By Assumption 1(ii)-(iii), there exists and an open ball containing it, such that for any in the ball. Thus the Bayesian operator is well-defined for any . Moreover, by Assumption 1(iii), such ’s are dense in , so the Bayesian operator maps into itself. Because players believe they face a stationary environment with i.i.d. perturbations, it is without loss of generality to restrict player ’s behavior at time to depend on .

Definition 5.

A policy of player is a sequence of functions , where . A policy is optimal if for all . A policy profile is optimal if is optimal for all .

Let denote the set of histories, where any history satisfies the feasibility restriction: for all , for some for all . Let denote the probability distribution over that is induced by the priors , and the policy profiles . Let denote the sequence of beliefs such that, for all and all , is the posterior at time defined recursively by for all , where is player ’s signal at given history , and similarly for and .

Definition 6.

The sequence of intended strategy profiles given policy profile is the sequence of random variables such that, for all , all , and all ,

| (7) |

An intended strategy profile describes how each player would behave at time for each possible signal; it is a random variable because it depends on the players’ beliefs at time , , which in turn depend on the past history.

One reasonable criteria to claim that the players’ behavior stabilizes is that their intended behavior stabilizes with positive probability (cf. Fudenberg and Kreps, 1993).

Definition 7.

A strategy profile is stable [or strongly stable] under policy profile if the sequence of intended strategies, , converges to with positive probability [or with probability one], i.e.,

Lemma 2 says that, if behavior stabilizes to a strategy profile , then, for each player , beliefs become increasingly concentrated on . This result extends findings from the statistics of misspecified learning (Berk (1966), Bunke and Milhaud (1998)) to a setting with active learning (i.e., players learn from data that is endogenously generated by their own actions). Three new issues arise: (i) Previous results need to be extended to the case of non-i.i.d. and endogenous data; (ii) It is not obvious that steady-state beliefs can be characterized based on steady-state behavior, independently of the path of play (Assumption 1 plays an important role here; See Section 5 for an example); (iii) We allow the wKLD function to be nonfinite so that players can believe that other players follow pure strategies.363636For example, if player 1 believes that player 2 plays with probability and with , then the wKLD function is infinity at if player 2 plays with positive probability.

Lemma 2.

Suppose that, for a policy profile , the sequence of intended strategies, , converges to for all histories in a set such that . Then, for all open sets , , a.s.- in .

Proof.

See the Appendix. ∎

The sketch of the proof of Lemma 2 is as follows (we omit the subscript to ease the notational burden). Consider an arbitrary and an open set defined as the points which are within distance of . The time posterior over the complement of , , can be expressed as

where equals minus the log-likelihood ratio, . This expression and straightforward algebra implies that

for any and and taken to be “small”. Roughy speaking, the integral in the numerator in the RHS is taken over points which are “-separated” from , whereas the integral in the denominator is taken over points which are “-close” to .

Intuitively, if behaves asymptotically like , there exist sufficiently small and such that is negative for all which are “-separated” from , and positive for all which are “-close” to . Thus, the numerator converges to zero, whereas the denominator diverges to infinity, provided that has positive measure under the prior.

The nonstandard part of the proof consists of establishing that has positive measure under the prior, which relies on Assumption 1, and that indeed behaves asymptotically like . By virtue of Fatou’s lemma, for it suffices to show almost sure pointwise convergence of to ; this is done in Claim B(i) in the Appendix and relies on a LLN argument for non-iid variables. On the other hand, over , we need to control the asymptotic behavior of uniformly to be able to interchange the limit and integral. In Claims B(ii) and B(iii) in the Appendix, we establish that there exists such that asymptotically and over , .

While Lemma 2 implies that the support of posteriors converges, posteriors need not converge. We can always find, however, a subsequence of posteriors that converges. By continuity of behavior in beliefs and the assumption that players are myopic, the stable strategy profile must be statically optimal. Thus, we obtain the following characterization of the set of stable strategy profiles when players follow optimal policies.

Theorem 2.

Suppose that a strategy profile is stable under an optimal policy profile for a perturbed game. Then is a Berk-Nash equilibrium of the perturbed game.

Proof.

Let denote the optimal policy function under which is stable. By Lemma 2, there exists with such that, for all , and for all and all open sets ; for the remainder of the proof, fix any . For all , compactness of implies the existence of a subsequence, which we denote as , such that converges (weakly) to (the limit could depend on ). We conclude by showing, for all :

(i) : Suppose not, so that there exists such that . Then, since is closed (by Lemma 1), there exists an open set with closure such that . Then , but this contradicts the fact that , where the first inequality holds because is closed and converges (weakly) to .

(ii) is optimal for the perturbed game given :

where the second equality follows because is optimal and is single-valued, a.s.- ,373737 is single-valued a.s.- because the set of such that is of dimension lower than and, by absolute continuity of , this set has measure zero. and the third equality follows from a standard continuity argument. ∎

4.3 A converse result

Theorem 2 provides our main justification for Berk-Nash equilibria: any strategy profile that is not an equilibrium cannot represent limiting behavior of optimizing players. Theorem 2, however, does not imply that behavior stabilizes. It is well known that convergence is not guaranteed for Nash equilibrium, which is a special case of Berk-Nash equilibrium.383838Jordan (1993) shows that non-convergence is robust to the choice of initial conditions; Benaim and Hirsch (1999) replicate this finding for the perturbed version of Jordan’s game. In the game-theory literature, general global convergence results have only been obtained in special classes of games—e.g. zero-sum, potential, and supermodular games (Hofbauer and Sandholm, 2002). Thus, some assumption needs to be relaxed to prove convergence for general games. Fudenberg and Kreps (1993) show that a converse for the case of Nash equilibrium can be obtained by relaxing optimality and allowing players to make vanishing optimization mistakes.

Definition 8.

A policy profile is asymptotically optimal if there exists a positive real-valued sequence with such that, for all , all , all , and all ,

where .

Fudenberg and Kreps’ (1993) insight is to suppose that players are convinced early on that the equilibrium strategy is the right one to play, and continue to play this strategy unless they have strong enough evidence to think otherwise. And, as they continue to play the equilibrium strategy, the evidence increasingly convinces them that it is the right thing to do. This idea, however, need not work for Berk-Nash equilibrium because beliefs may not converge if the model is misspecified (see Berk (1966) for an example). If the game is weakly identified, however, Lemma 2 and Fudenberg and Kreps’ (1993) insight can be combined to obtain the following converse of Theorem 2.

Erratum (11/19/2019): We thank Yuichi Yamamoto for pointing out that the statement of Theorem 3 should be corrected as follows:

Theorem 3.

Suppose that is a Berk-Nash equilibrium of a perturbed game that is weakly identified given and let be a belief profile that supports as an equilibrium. Then, for any profile of priors satisfying for all and for any , there exists an asymptotically optimal policy profile such that .

Proof.

See Online Appendix B.393939The statement about the prior highlights that we are not choosing the prior to be degenerate in a way that would make the result trivial. ∎

5 Discussion

importance of assumption 1. The following example illustrates that equilibrium may not exist and Lemma 2 fails if Assumption 1 does not hold. A single agent chooses action and obtains outcome . The agent’s model is parameterized by , where and . The true model is . The agent, however, is misspecified and considers only and to be possible, i.e., . In particular, Assumption 1(iii) fails for parameter value .404040Assumption 1(iii) would hold if, for some , were also in for all . Suppose that is uniquely optimal for parameter value and is uniquely optimal for (further details about payoffs are not needed).

A Berk-Nash equilibrium does not exist: If is played with positive probability, then the wKLD is infinity at (i.e., cannot rationalize given ) and is the best fit; but then is not optimal. If is played with probability 1, then is the best fit; but then is not optimal. In addition, Lemma 2 fails: Suppose that the path of play converges to pure strategy . The best fit given is , but the posterior need not converge weakly to a degenerate probability distribution on ; it is possible that, along the path of play, the agent tried action and observed , in which case the posterior would immediately assign probability 1 to .

forward-looking agents. In the dynamic model, we assumed that players are myopic. In Online Appendix C, we extend Theorem 2 to the case of non-myopic players who solve a dynamic optimization problem with beliefs as a state variable. A key fact used in the proof of Theorem 2 is that myopically optimal behavior is continuous in beliefs. Non-myopic optimal behavior is also continuous in beliefs, but the issue is that it may not coincide with myopic behavior in the steady state if players still have incentives to experiment. We prove the extension by requiring that the game is weakly identified, which guarantees that players have no incentives to experiment in steady state.

large population models. The framework assumes that there is a fixed number of players but, by focusing on stationary subjective models, rules out aspects of “repeated games” where players attempt to influence each others’ play. In Online Appendix D, we adapt the equilibrium concept to settings in which there is a population of a large number of agents in the role of each player, so that agents have negligible incentives to influence each other’s play.

extensive-form games. Our results hold for an alternative timing where player commits to a signal-contingent plan of action (i.e., a strategy) and observes both the realized signal and the consequence ex post. In particular, Berk-Nash equilibrium is applicable to extensive-form games provided that players compete by choosing contingent plan of actions and know the extensive form. But the right approach is less clear if players have a misspecified view of the extensive form (for example, they may not even know the set of strategies available to them) or if players play the game sequentially (for example, we would need to define and update beliefs at each information set). The extension to extensive-form games is left for future work.414141Jehiel (1995) considers the class of repeated alternating-move games and assumes that players only forecast a limited number of time periods into the future; see Jehiel (1998) for a learning foundation. Jehiel and Samet (2007) consider the general class of extensive form games with perfect information and assume that players simplify the game by partitioning the nodes into similarity classes. In both cases, players are required to have correct beliefs, given their limited or simplified view of the game.

relationship to bounded rationality literature. By providing a language that makes the underlying misspecification explicit, we offer some guidance for choosing between different models of bounded rationality. For example, we could model the observed behavior of an instructor in Example 2.3 by directly assuming that she believes criticism improves performance and praise worsens it.424242This assumption corresponds to a singleton set , thus fixing beliefs at the outset and leaving no space for learning. This approach is common in past work that assumes that agents have a misspecified model but there is no learning about parameter values, e.g., Barberis et al. (1998). But extrapolating this observed belief to other contexts may lead to erroneous conclusions. Instead, we postulate what we think is a plausible misspecification (i.e., failure to account for regression to the mean) and then derive beliefs endogenously, as a function of the context.

We mentioned in the paper several instances of bounded rationality that can be formalized via misspecified, endogenous learning. Other examples in the literature can also be viewed as restricting beliefs using the wKLD measure, but fall outside the scope of our paper either because interactions are mediated by a price or because the problem is dynamic (we focus on the repetition of a static problem). For example, Blume and Easley (1982) and Rabin and Vayanos (2010) explicitly characterize beliefs using the limit of a likelihood function, while Bray (1982), Radner (1982), Sargent (1993), and Evans and Honkapohja (2001) focus specifically on OLS learning with misspecified models. Piccione and Rubinstein (2003), Eyster and Piccione (2013), and Spiegler (2013) study pattern recognition in dynamic settings and impose consistency requirements on beliefs that could be interpreted as minimizing the wKLD measure. In the sampling equilibrium of Osborne and Rubinstein (1998) and Spiegler (2006), beliefs may be incorrect due to learning from a limited sample, rather than from misspecified learning. Other instances of bounded rationality that do not seem naturally fitted to misspecified learning, include biases in information processing due to computational complexity (e.g., Rubinstein (1986), Salant (2011)), bounded memory (e.g., Wilson, 2003), self-deception (e.g., Bénabou and Tirole (2002), Compte and Postlewaite (2004)), or sparsity-based optimization (Gabaix (2014)).

References

- (1)

- Al-Najjar (2009) Al-Najjar, N., “Decision Makers as Statisticians: Diversity, Ambiguity and Learning,” Econometrica, 2009, 77 (5), 1371–1401.

- Al-Najjar and Pai (2013) and M. Pai, “Coarse decision making and overfitting,” Journal of Economic Theory, forthcoming, 2013.

- Aliprantis and Border (2006) Aliprantis, C.D. and K.C. Border, Infinite dimensional analysis: a hitchhiker’s guide, Springer Verlag, 2006.

- Aragones et al. (2005) Aragones, E., I. Gilboa, A. Postlewaite, and D. Schmeidler, “Fact-Free Learning,” American Economic Review, 2005, 95 (5), 1355–1368.

- Arrow and Green (1973) Arrow, K. and J. Green, “Notes on Expectations Equilibria in Bayesian Settings,” Institute for Mathematical Studies in the Social Sciences Working Paper No. 33, 1973.

- Barberis et al. (1998) Barberis, N., A. Shleifer, and R. Vishny, “A model of investor sentiment,” Journal of financial economics, 1998, 49 (3), 307–343.

- Battigalli (1987) Battigalli, P., Comportamento razionale ed equilibrio nei giochi e nelle situazioni sociali, Universita Bocconi, Milano, 1987.

- Battigalli et al. (2012) , S. Cerreia-Vioglio, F. Maccheroni, and M. Marinacci, “Selfconfirming equilibrium and model uncertainty,” Technical Report 2012.

- Bénabou and Tirole (2002) Bénabou, Roland and Jean Tirole, “Self-confidence and personal motivation,” The Quarterly Journal of Economics, 2002, 117 (3), 871–915.

- Benaim and Hirsch (1999) Benaim, M. and M.W. Hirsch, “Mixed equilibria and dynamical systems arising from fictitious play in perturbed games,” Games and Economic Behavior, 1999, 29 (1-2), 36–72.

- Benaim (1999) Benaim, Michel, “Dynamics of stochastic approximation algorithms,” in “Seminaire de Probabilites XXXIII,” Vol. 1709 of Lecture Notes in Mathematics, Springer Berlin Heidelberg, 1999, pp. 1–68.

- Berk (1966) Berk, R.H., “Limiting behavior of posterior distributions when the model is incorrect,” The Annals of Mathematical Statistics, 1966, 37 (1), 51–58.

- Bickel et al. (1993) Bickel, Peter J, Chris AJ Klaassen, Peter J Bickel, Y Ritov, J Klaassen, Jon A Wellner, and YA’Acov Ritov, Efficient and adaptive estimation for semiparametric models, Johns Hopkins University Press Baltimore, 1993.

- Billingsley (1995) Billingsley, P., Probability and Measure, Wiley, 1995.

- Blume and Easley (1982) Blume, L.E. and D. Easley, “Learning to be Rational,” Journal of Economic Theory, 1982, 26 (2), 340–351.

- Bray (1982) Bray, M., “Learning, estimation, and the stability of rational expectations,” Journal of economic theory, 1982, 26 (2), 318–339.

- Bunke and Milhaud (1998) Bunke, O. and X. Milhaud, “Asymptotic behavior of Bayes estimates under possibly incorrect models,” The Annals of Statistics, 1998, 26 (2), 617–644.

- Compte and Postlewaite (2004) Compte, Olivier and Andrew Postlewaite, “Confidence-enhanced performance,” American Economic Review, 2004, pp. 1536–1557.

- Dekel et al. (2004) Dekel, E., D. Fudenberg, and D.K. Levine, “Learning to play Bayesian games,” Games and Economic Behavior, 2004, 46 (2), 282–303.

- Diaconis and Freedman (1986) Diaconis, P. and D. Freedman, “On the consistency of Bayes estimates,” The Annals of Statistics, 1986, pp. 1–26.

- Doraszelski and Escobar (2010) Doraszelski, Ulrich and Juan F Escobar, “A theory of regular Markov perfect equilibria in dynamic stochastic games: Genericity, stability, and purification,” Theoretical Economics, 2010, 5 (3), 369–402.

- Durrett (2010) Durrett, R., Probability: Theory and Examples, Cambridge University Press, 2010.

- Easley and Kiefer (1988) Easley, D. and N.M. Kiefer, “Controlling a stochastic process with unknown parameters,” Econometrica, 1988, pp. 1045–1064.

- Esponda (2008) Esponda, I., “Behavioral equilibrium in economies with adverse selection,” The American Economic Review, 2008, 98 (4), 1269–1291.

- Esponda and Pouzo (2011) and D. Pouzo, “Learning Foundation for Equilibrium in Voting Environments with Private Information,” working paper, 2011.

- Esponda and Pouzo (2014) Esponda, I. and D. Pouzo, “Berk-Nash Equilibrium: A Framework for Modeling Agents with Misspecified Models,” ArXiv 1411.1152, November 2014.

- Evans and Honkapohja (2001) Evans, G. W. and S. Honkapohja, Learning and Expectations in Macroeconomics, Princeton University Press, 2001.

- Eyster and Rabin (2005) Eyster, E. and M. Rabin, “Cursed equilibrium,” Econometrica, 2005, 73 (5), 1623–1672.

- Eyster and Piccione (2013) Eyster, Erik and Michele Piccione, “An approach to asset-pricing under incomplete and diverse perceptions,” Econometrica, 2013, 81 (4), 1483–1506.

- Freedman (1963) Freedman, D.A., “On the asymptotic behavior of Bayes’ estimates in the discrete case,” The Annals of Mathematical Statistics, 1963, 34 (4), 1386–1403.

- Fudenberg and Kreps (1993) Fudenberg, D. and D. Kreps, “Learning Mixed Equilibria,” Games and Economic Behavior, 1993, 5, 320–367.

- Fudenberg and Levine (1993a) and D.K. Levine, “Self-confirming equilibrium,” Econometrica, 1993, pp. 523–545.

- Fudenberg and Levine (1993b) and , “Steady state learning and Nash equilibrium,” Econometrica, 1993, pp. 547–573.

- Fudenberg and Levine (1998) and , The theory of learning in games, Vol. 2, The MIT press, 1998.

- Fudenberg and Levine (2009) and , “Learning and Equilibrium,” Annual Review of Economics, 2009, 1, 385–420.

- Fudenberg and Kreps (1988) and D.M. Kreps, “A Theory of Learning, Experimentation, and Equilibrium in Games,” Technical Report, mimeo 1988.

- Fudenberg and Kreps (1995) and , “Learning in extensive-form games I. Self-confirming equilibria,” Games and Economic Behavior, 1995, 8 (1), 20–55.

- Gabaix (2014) Gabaix, Xavier, “A sparsity-based model of bounded rationality,” The Quarterly Journal of Economics, 2014, 129 (4), 1661–1710.

- Harsanyi (1973) Harsanyi, J.C., “Games with randomly disturbed payoffs: A new rationale for mixed-strategy equilibrium points,” International Journal of Game Theory, 1973, 2 (1), 1–23.

- Hirsch et al. (2004) Hirsch, M. W., S. Smale, and R. L. Devaney, Differential Equations, Dynamical Systems and An Introduction to Chaos, Elsevier Academic Press, 2004.

- Hofbauer and Sandholm (2002) Hofbauer, J. and W.H. Sandholm, “On the global convergence of stochastic fictitious play,” Econometrica, 2002, 70 (6), 2265–2294.

- Jehiel (2005) Jehiel, P., “Analogy-based expectation equilibrium,” Journal of Economic theory, 2005, 123 (2), 81–104.

- Jehiel and Samet (2007) and D. Samet, “Valuation equilibrium,” Theoretical Economics, 2007, 2 (2), 163–185.

- Jehiel and Koessler (2008) and F. Koessler, “Revisiting games of incomplete information with analogy-based expectations,” Games and Economic Behavior, 2008, 62 (2), 533–557.

- Jehiel (1998) Jehiel, Philippe, “Learning to play limited forecast equilibria,” Games and Economic Behavior, 1998, 22 (2), 274–298.

- Jehiel (1995) Jehiel, Phillippe, “Limited horizon forecast in repeated alternate games,” Journal of Economic Theory, 1995, 67 (2), 497–519.

- Jordan (1993) Jordan, J. S., “Three problems in learning mixed-strategy Nash equilibria,” Games and Economic Behavior, 1993, 5 (3), 368–386.

- Kagel and Levin (1986) Kagel, J.H. and D. Levin, “The winner’s curse and public information in common value auctions,” The American Economic Review, 1986, pp. 894–920.

- Kalai and Lehrer (1993) Kalai, E. and E. Lehrer, “Rational learning leads to Nash equilibrium,” Econometrica, 1993, pp. 1019–1045.

- Kirman (1975) Kirman, A. P., “Learning by firms about demand conditions,” in R. H. Day and T. Groves, eds., Adaptive economic models, Academic Press 1975, pp. 137–156.

- Kreps and Wilson (1982) Kreps, D. M. and R. Wilson, “Sequential equilibria,” Econometrica, 1982, pp. 863–894.

- Kullback and Leibler (1951) Kullback, S. and R. A. Leibler, “On Information and Sufficiency,” Annals of Mathematical Statistics, 1951, 22 (1), 79–86.

- Kushner and Yin (2003) Kushner, H. J. and G. G. Yin, Stochastic Approximation and Recursive Algorithms and Applications, Springer Verlag, 2003.

- McLennan (1984) McLennan, A., “Price dispersion and incomplete learning in the long run,” Journal of Economic Dynamics and Control, 1984, 7 (3), 331–347.

- Nyarko (1991) Nyarko, Y., “Learning in mis-specified models and the possibility of cycles,” Journal of Economic Theory, 1991, 55 (2), 416–427.

- Nyarko (1994) , “On the convexity of the value function in Bayesian optimal control problems,” Economic Theory, 1994, 4 (2), 303–309.

- Osborne and Rubinstein (1998) Osborne, M.J. and A. Rubinstein, “Games with procedurally rational players,” American Economic Review, 1998, 88, 834–849.

- Piccione and Rubinstein (2003) Piccione, M. and A. Rubinstein, “Modeling the economic interaction of agents with diverse abilities to recognize equilibrium patterns,” Journal of the European economic association, 2003, 1 (1), 212–223.

- Pollard (2001) Pollard, D., A User’s Guide to Measure Theoretic Probability, Cambridge University Press, 2001.

- Rabin (2002) Rabin, M., “Inference by Believers in the Law of Small Numbers,” Quarterly Journal of Economics, 2002, 117 (3), 775–816.

- Rabin and Vayanos (2010) and D. Vayanos, “The gambler’s and hot-hand fallacies: Theory and applications,” The Review of Economic Studies, 2010, 77 (2), 730–778.

- Radner (1982) Radner, R., Equilibrium Under Uncertainty, Vol. II of Handbook of Mathematical Economies, North-Holland Publishing Company, 1982.

- Rothschild (1974) Rothschild, M., “A two-armed bandit theory of market pricing,” Journal of Economic Theory, 1974, 9 (2), 185–202.

- Rubinstein and Wolinsky (1994) Rubinstein, A. and A. Wolinsky, “Rationalizable conjectural equilibrium: between Nash and rationalizability,” Games and Economic Behavior, 1994, 6 (2), 299–311.

- Rubinstein (1986) Rubinstein, Ariel, “Finite automata play the repeated prisoner’s dilemma,” Journal of economic theory, 1986, 39 (1), 83–96.

- Salant (2011) Salant, Y., “Procedural analysis of choice rules with applications to bounded rationality,” The American Economic Review, 2011, 101 (2), 724–748.

- Sargent (1993) Sargent, T. J., Bounded rationality in macroeconomics, Oxford University Press, 1993.

- Sargent (1999) , The Conquest of American Inflation, Princeton University Press, 1999.

- Schwartzstein (2009) Schwartzstein, J., “Selective Attention and Learning,” working paper, 2009.

- Selten (1975) Selten, R., “Reexamination of the perfectness concept for equilibrium points in extensive games,” International journal of game theory, 1975, 4 (1), 25–55.

- Sobel (1984) Sobel, J., “Non-linear prices and price-taking behavior,” Journal of Economic Behavior & Organization, 1984, 5 (3), 387–396.

- Spiegler (2006) Spiegler, R., “The Market for Quacks,” Review of Economic Studies, 2006, 73, 1113–1131.

- Spiegler (2013) , “Placebo reforms,” The American Economic Review, 2013, 103 (4), 1490–1506.

- Spiegler (2014) , “Bayesian Networks and Boundedly Rational Expectations,” Working Paper, 2014.

- Stein (1972) Stein, Charles, “A bound for the error in the normal approximation to the distribution of a sum of dependent random variables,” in “Proceedings of the Sixth Berkeley Symposium on Mathematical Statistics and Probability, Volume 2: Probability Theory” University of California Press Berkeley, Calif. 1972, pp. 583–602.

- Tversky and Kahneman (1973) Tversky, T. and D. Kahneman, “Availability: A heuristic for judging frequency and probability,” Cognitive Psychology, 1973, 5, 207–232.

- White (1982) White, Halbert, “Maximum likelihood estimation of misspecified models,” Econometrica: Journal of the Econometric Society, 1982, pp. 1–25.

- Wilson (2003) Wilson, A., “Bounded Memory and Biases in Information Processing,” Working Paper, 2003.

Appendix

Let . For all , define . We sometimes abuse notation and write , and similarly for . The following claim is used in the proofs below.

Claim A. For all : (i) There exists and such that, , ; (ii) Fix any and such that and . Then ; (iii) is (jointly) lower semicontinuous: Fix any and such that , . Then ; (iv) Let be a random vector in with absolutely continuous probability distribution . Then, , is continuous.

Proof. (i) By Assumption 1 and finiteness of , there exist and such that . Thus, , .

(ii) . The first term in the RHS converges to 0 because , is continuous, and is continuous . The second term converges to 0 because , is continuous, and .

(iii) . The first term in the RHS converges to 0 (same argument as in part (ii)). The proof concludes by showing that, ,

| (8) |

Suppose (if not, (8) holds trivially). Then either (i) , in which case (8) holds with equality (by continuity of ), or (ii) , in which case (8) holds because its RHS is 0 (by convention that ) and its LHS is always nonnegative.

(iv) The proof is standard and, therefore, omitted.

Proof of Lemma 1. Part (i). Note that

where the inequality follows from Jensen’s inequality and the strict concavity of , and it holds with equality if and only if such that (recall that, by assumption, ).

Part (ii). is nonempty: By Claim A(i), such that the minimizers are in the constraint set . Because is continuous over a compact set, a minimum exists.

is upper hemicontinuous (uhc): Fix any and such that , , and . We show that (so that has a closed graph and, by compactness of , is uhc). Suppose, to obtain a contradiction, that . By Claim A(i), there exist and such that and . By Assumption 1, with and, , . We show that there is an element of the sequence, , that “does better” than given , which is a contradiction. Because , continuity of implies that there exists large enough such that . Moreover, Claim A(ii) applied to implies that there exists such that, , . Thus, , . Therefore,

| (9) |

Suppose . By Claim A(iii), such that . This result and expression (9), imply . But this contradicts . Finally, if , Claim A(iii) implies that such that , where is the bound defined in Claim A(i). But this also contradicts .

is compact: As shown above, has a closed graph, and so is a closed set. Compactness of follows from compactness of .

Proof of Theorem 1. We prove the result in two parts. Part 1. We show existence of equilibrium in the perturbed game (defined in Section 4.1). Let be a correspondence such that, , where and is defined as

| (10) |

. Note that if such that , then is an equilibrium of the perturbed game. We show that such exists by checking the conditions of the Kakutani-Fan-Glicksberg fixed-point theorem: (i) is compact, convex and locally convex Hausdorff: The set is convex, and since is compact is also compact under the weak topology (Aliprantis and Border (2006), Theorem 15.11). By Tychonoff’s theorem, is compact too. Finally, the set is also locally convex under the weak topology;434343This last claim follows since the weak topology is induced by a family of semi-norms of the form: for continuous and bounded for any and in . (ii) has convex, nonempty images: It is clear that is convex valued . Also, by Lemma 1, is nonempty ; (iii) has a closed graph: Let be such that and and (under the weak topology). By Claim A(iv), is continuous. Thus, . By Lemma 1, is uhc; thus, by Theorem 17.13 in Aliprantis and Border (2006), is also uhc. Therefore, .

Part 2. Fix a sequence of perturbed games indexed by the probability of perturbations . By Part 1, there is a corresponding sequence of fixed points , such that , where (see equation (10), where we now explicitly account for dependance on ). By compactness, there exist subsequences of and that converge to and , respectively. Since is uhc, then . We now show that if we choose such that, , , then is optimal given in the unperturbed game—this establishes existence of equilibrium in the unperturbed game. Suppose not, so that there exist and such that and . By continuity of and the fact that , such that, , . It then follows from (10) and that . But this contradicts .

Proof of Proposition 3. In the next paragraph, we prove the following result: For all and , (a) for all and (b) for all . Equivalence between Berk-Nash and ABEE follows immediately from (a), (b), and the fact that expected utility of player with signal and beliefs equals .

Proof of (a) and (b): equals, up to a constant,

It is straightforward to check that any parameter value that maximizes the above expression satisfies (a) and (b).

Proof of Lemma 2. The proof uses Claim B, which is stated and proven after this proof. It is sufficient to establish that a.s. in , where . Fix and . Then, by Bayes’ rule,

where the first equality is well-defined by Assumption 1, full support of , and the fact that implies that all the terms are positive, and where we define for the second equality.444444If, for some , for some then we define and . For any , define . Then, for all and , , where (because is bounded) and where and .The proof concludes by showing that, for all (sufficiently small) , such that . This result is achieved in several steps. First, , define and , where . By continuity of , there exist and such that, , . Henceforth, let . It follows that

| (11) |

such that . Also, by continuity of , such that, ,

| (12) |

Second, let and . We now show that . By Lemma 1, is nonempty. Pick any . By Assumption 1, in such that and and all . In particular, such that and, by continuity of , there exists an open set around such that . By full support, . Next, note that,

| (13) |

a.s. in , where the first inequality follows because and is a positive function, the second inequality follows from Fatou’s Lemma and a LLN for non-iid random variables that implies , a.s. in (see Claim B(i) below), and the last equality follows from (12) and the fact that .

Next, we consider the term . Claims B(ii) and B(iii) (see below) imply that such that, , , a.s. in . Thus,

a.s. in . The above expression and equation (13) imply that a.s.-.

We state and prove Claim B used in the proof above. For any , define to be the set such that if and only if for all such that .