Utility maximization in jump models driven by marked point processes and nonlinear wealth dynamics

Abstract

We explore martingale and convex duality techniques to study optimal investment strategies that maximize expected risk-averse utility from consumption and terminal wealth. We consider a market model with jumps driven by (multivariate) marked point processes and so-called non-linear wealth dynamics which allows to take account of relaxed assumptions such as differential borrowing and lending interest rates or short positions with cash collateral and negative rebate rates. We give sufficient conditions for existence of optimal policies for agents with logarithmic and CRRA power utility and present numerical examples. We provide closed-form solutions for the optimal value function in the case of pure-jump models with jump-size distributions modulated by a two-state Markov chain.

1 Introduction

The object of this paper is to find sufficient conditions for existence of investment and consumption strategies that maximize expected risk-averse utility from consumption and terminal wealth for an investor trading in a pure-jump incomplete market model that consists of a money market account and a risky asset with price dynamics driven by a (multivariate) marked point process. The investor faces convex trading constraints and additional cash outflow due to market frictions such as differential rates for money borrowing and lending or short positions with negative rebate rates as a result of stock borrowing fees exceeding the interest rate on cash paid as collateral, see Examples 2.1 and 2.2 below. This is modelled by adding in a margin payment function that depends on the portfolio proportion process to the investor’s wealth equation arising from the self-financing condition.

Marked point processes have gained considerable ground in asset price modelling in the past 15 years, particularly in the modelling of high-frequency financial data and nonlinear filtering for volatility estimation, see e.g. Ceci [4, 5], Ceci and Gerardi [6, 7], Cvitanić et al [10], Frey [13], Frey and Runggaldier [14, 15], Geman et al [16], Prigent [29], Rydberg and Shephard [30].

Indeed, the random times and marks of the underlying marked point process can be used to model the times of occurrence and the magnitude of different market events such as large trades, limit orders or changes in credit ratings. Market makers update their quotes in reaction to these events, which in turn generates variations and jumps in the stock prices. These jumps can be incorporated in the prices dynamics using the (random) counting measure associated with the underlying marked point process, see the formulation of the asset price model in Section 2.

These processes have also been used for modelling of term structure and forward rates in bond markets, see e.g. Björk et al [1] and Jarrow and Madan [20].

Our approach to the utility maximization problem follows closely the convex duality method started by He and Pearson [18], Karatzas et al. [23], Cvitanić and Karatzas [9], and generalized by Kramkov and Schachermayer [25] to the general semi-martingale setting. The method consists in formulating an associated dual minimization problem and finding conditions for absence of duality gap, and has been remarkably effective in dealing with utility maximization with convex portfolio constraints.

For jump-diffusion market models, Goll and Kallsen [17], Kallsen [22] and more recently Michelbrink and Le [28] use the martingale approach to obtain explicit solutions for agents with logarithmic and power utility functions and linear wealth equations. Callegaro and Vargiolu [3] obtain similar results in jump-diffusion models with Poisson-type jumps. In the diffusion setting, the convex duality approach was significantly extended by Cuoco and Liu [8] and Klein and Rogers [24] in order to incorporate non-linear wealth dynamics.

In this paper, we consider the same utility maximization as in Cuoco and Liu [8] but with a marked point process, instead of a Brownian motion, as the main driving process. Our main assumption throughout is that the counting measure of the underlying marked point process has local characteristics of the form . Of particular interest is the case in which these local characteristics depend on an (possibly exogenous) Markovian state process which may describe intra-day trading activity, macroeconomics factors, microstructure rules that drive the market, or simply changes in the economy or business cycle, see Examples 3.1 and 3.2 below. See also Frey and Runggaldier [15].

The main result of this paper is a sufficient condition for existence of an optimal portfolio-consumption pair in terms of the convex dual of the margin payment function and the solution pair of a linear backward SDE driven by the counting measure Although the optimality condition in the main result seems rather restrictive, in the last section we show that it simplifies significantly in the case of logarithmic and power utility functions as well as premium payments due to higher borrowing interest rates or short selling.

As our main example, we consider the regime-switching pure-jump asset price model proposed by López and Ratanov [26] in which the jump-size distributions alternate according to a continuous-time two-state Markov chain, see also the recent papers by Elliot and Siu [12] and López and Serrano [27]. We find explicit formulae for the optimal value functions for this model in the case of logarithmic utility.

Finally, it is worthwhile mentioning that our market model and formulation of the utility maximization problem can be seen as particular case of the more general problem studied by Schroder and Skiadas [31] as they consider a jump-diffusion model driven by a Brownian motion and a marked point process as well as recursive utility functions. However, their main approach is the scale/translation-invariant formulation of the utility maximization problem, although they do relate their results to the dual formulation in the appendix of [31].

Let us briefly describe the contents of this paper. In Section 1 we outline the stochastic setting and information structure for marked point processes, introduce the market model and non-linear wealth equation with margin payment functions and define the optimal investment/consumption problem. In Section 3 we formulate the main assumption on existence of local characteristics for the underlying marked point process. In Section 4 we introduce convex duality techniques from Cuoco and Liu [8] and establish our main result on a sufficient condition for existence of an optimal investment/consumption policy. In Section 5 we illustrate the main result by considering (CRRA) logarithmic and power utility functions combined with margin payments for differential borrowing and lending interest rates as well as short positions with negative rebate rates. We present some numerical examples and, using recent results in López and Serrano [27], provide explicit closed-form solutions for the optimal value function in the case of Markov-modulated jump-size distributions.

2 Market model, non-linear wealth dynamics and risk-averse utility maximization problem

Let be a complete probability space endowed with a filtration and let be Borel subset of an Euclidean space with algebra Let be a marked (or multivariate) point process with mark space , that is, is a sequence of valued random variables and is an increasing sequence of positive random variables satisfying

We define the random counting measure associated with the marked point process as follows

| (2.1) |

see e.g. Jacod and Shiryaev [19, Chapter III, Definition 1.23] or Jeanblanc et al [21, Section 8.8]. For each the counting process counts the number of marks with values in up to time

Let denote the natural filtration related to these counting processes, that is

Throughout we assume Recall that a real-valued process is predictable if the random function is measurable with respect to the algebra on generated by adapted left-continuous processes. Similarly, a map is said to be a -predictable if it is measurable with respect to the product -algebra

We consider a financial market model with a money account with continuously compounded force of interest

and a risky asset or stock with price process defined as the stochastic exponential process with and

The processes and the map are assumed uniformly bounded and -predictable. Here denotes the stochastic (Doléans-Dade) exponential, see e.g. Jeanblanc et al [21, Section 9.4.3].

In this model, the discrete random times can be interpreted as time points at which significant market events occur such as large trades, limit orders or changes in credit ratings, or simply times at which market makers update their quotes in reaction to new information. The marks describe the magnitude of these events, and both times and marks create jumps and variations in the stock prices through the map

Notice that and satisfy

| (2.2) |

We also assume a.s. for every Thus, the solution to equation (2.2) is given by the predictable process

For an agent willing to invest in this market, we denote with the fraction of wealth invested in the risky asset, so that the fraction of wealth invested in the riskless asset is Recall that a positive value for represents a long position in the risky asset, whereas a negative stands for a short position. The process is called portfolio proportion process, or simply portfolio process, and we always assume it is -predictable.

We fix an finite investment horizon and a non-empty closed convex of portfolio constraints with We introduce a margin payment function which is -measurable and satisfies, for each

-

(i)

-

(ii)

is concave and continuous on

During the time interval the investor is allowed to consume at an instantaneous consumption rate Then, under the self-financing condition, the wealth of the investor at time is subject to the following dynamic budget constraint

| (2.3) |

where is a fixed initial wealth and is a pair of -predictable portfolio-consumption processes satisfying

-

(i)

is bounded below and a.s. for all

-

(ii)

a.s.

The stochastic differential equation (2.3) is linear with respect to the wealth process but possibly non-linear in the portfolio policy and, in turn, with respect to the actual amounts invested in both the risky and non-risky asset.

We define the class of admissible pairs for initial wealth as the set of portfolio-consumption pairs for which wealth equation (2.3) possesses an unique strong solution satisfying a.s. for all

We denote with the solution to equation (2.3). In particular, if there is no consumption i.e. for all equation (2.3) is linear in and homogeneous, with solution

| (2.4) |

This is always positive if, for instance, short-selling is not allowed for any of the assets i.e. if for all We can use (2.4) to find an expression for the wealth process in terms of the wealth process with initial wealth and portfolio-consumption pair as follows: define the process

In differential form, we have Then

Since by uniqueness of solution to equation (2.3), the wealth process is a modification of the process

| (2.5) |

Notice that the portfolio-consumption pair leads to positive wealth at time if, almost surely

Example 2.1 (Different borrowing and lending rates).

Consider the case of a financial market in which the interest rate that an investor pays for borrowing is higher than the bank rate the investor earns for lending.

More concretely, let the borrowing rate be a -predictable uniformly bounded process satisfying a.s. for all The margin payment function for this case is

Notice that the wealth equation (2.3) is nonlinear in the portfolio process, although it is piecewise linear. The term in the equation that involves the portfolio and the interest rates reads

Example 2.2 (Short selling with cash collateral and negative rebate rates).

In a short sale transaction, an investor borrows stock shares –typically from a broker-dealer or an institutional investor– and sells them on the market, and at some point in the future must buy the shares back to return them to the lender in the hope of making a profit if the share price decreases.

In order to borrow the stock shares, the short-seller must engage in a security-lending agreement and pay a loan fee to the lender. This fee depends mostly on the difficulty to locate and borrow the security. The short-seller must also put up collateral to better insure that the borrowed shares will be returned to the lender. Acceptable collateral includes cash, government bonds or a letter of credit from a bank. If the collateral is cash, the lender “rebates” interest on the collateral to the borrower, which usually offsets the stock loan fee.

However, if there is a large demand for the security, the stock loan fee might exceed the cash collateral interest rate, and the rebate rate will be negative. We assume this is the case for the risky asset Moreover, we assume that the cash proceeds from the short-sale are held as collateral and earn interests at the money account rate

More concretely, let the stock loan fee be a -predictable uniformly bounded process satisfying a.s. for all Then, the margin payment function is

Here denotes the negative part of We refer the reader to the paper by D’Avolio [11] for a comprehensive description of the market for borrowing and lending stocks, short selling as well as empirical evidence on negative rebate rates.

We now introduce the risk-averse utility maximization problem for optimal choice of portfolio and consumption processes. Let and denote consumption and investment risk-averse utility functions respectively, satisfying the following conditions

-

(i)

and for all and

-

(ii)

for each the mappings and are strictly increasing, strictly concave, of class on such that

-

(iii)

and are continuous on .

Let denote the class of admissible portfolio-consumption strategies such that

We define the utility functional

Our main object of study is the following risk-averse utility maximization problem

| (2.6) |

3 Main assumption: local characteristics

Let denote the random counting measure (2.1). Recall that the compensator or -predictable projection of is the unique (possibly, up to a null set) positive random measure such that, for every -predictable real-valued map the two following conditions hold

-

i.

The process

is -predictable.

-

ii.

If the process

is increasing and locally integrable, then

is -local martingale (see e.g. Jeanblanc et al [21, Definition 8.8.2.1]). Equivalently, for all

The following is the main standing assumption for the rest of this paper: the compensator of the counting measure satisfies

| (A) |

where is a positive -predictable process and is a predictable probability transition kernel, that is, a -predictable process with values in the set probability measures on In this case are called the -local characteristics of the marked point process see e.g. Brémaud [2, Chapter VIII].

Under this assumption, for each the counting process is an inhomogeneous Poisson process with stochastic intensity This can be interpreted as it is possible to separate the probability that an event occurs from the conditional distribution of the mark, given that the event has occurred. Thus, is the conditional distribution of the mark at time and gives the probability of an event occurring in the next infinitesimal time step

Below we present two examples that satisfy the main assumption (A). In both cases, the -local characteristics depend on an (possibly exogenous) Markovian state process with RCLL paths which may be used to describe intra-day market activity, macroeconomics factors, microstructure rules that drive the market or changes in the the economy or business cycle, see e.g [15]. In the first example, the state process is a two-state continuous time Markov-chain. In the second example, it is a jump-diffusion process, possibly having common jumps with the risky asset

Example 3.1 (Markov-modulated marked point process).

Let be a two-state continuous-time Markov chain with values in and infinitesimal generator (intensity matrix)

For each , let be a sequence of independent valued random variables with distributions

Suppose the two distributions and are independent as well as independent of the Markov chain Let denote the jump times of and let denote the state of the Markov chain right before the th jump.

Example 3.2.

Let be a finite measure on a measurable space Let denote a -Poisson random measure on with mean measure and let be a -Brownian motion.

Let denote the solution of the system of Itô-Levy type stochastic differential equations

We assume the Poisson measure is independent of and the coefficients and are measurable functions of their arguments satisfying the usual linear growth and Lipschitz conditions.

Define the sequence of random times as the jump times of the process that is

For each the mark (with mark space is the jump of the process at time

For and we define the sets

Then, if

the predictable projection of the counting measure associated with satisfies condition (A) with local characteristics

For the proof see Proposition 2.2 in Ceci [4].

4 Convex duality approach and main result

In this section we introduce some of the convex duality techniques from Cuoco and Liu [8] and establish our main result on a sufficient condition for existence of an optimal investment/consumption policy. Let

denote the indicator function (in the sense of convex analysis) of the portfolio constraint set and let

The function is upper semi-continuous and concave with a.s., for all We denote by

the convex conjugate of Since it is clear from the definition that Moreover, is lower semi-continuous, convex and

| (4.1) |

If we denote simply with We define the effective domain of denoted with as

Finally, let denote the set of -progressively measurable processes satisfying

Example 4.1.

Consider the margin payment function of Example 2.1, under the portfolio constraint of prohibition of short-selling of the risky asset, that is For fixed, the map

attains a finite maximum value if and only if This maximum value is attained at if and at if Hence, we have

| (4.2) |

with effective domain

Example 4.2.

Consider now the margin payment function of Example 2.2, with portfolio constraint of prohibition of borrowing from the money account, that is For fixed, the map

attains a (finite) maximum value if and only if Again, this maximum value is attained at if and at if Then, we have

| (4.3) |

with effective domain

Let denote the set of locally bounded -predictable marked processes satisfying

-

(i)

a.s. for almost every

-

(ii)

The process defined as

belongs to

Let denote the compensated martingale measure of the counting measure For each let denote the solution of the linear SDE

| (4.4) |

Lemma 4.3.

For each and we have

| (4.5) |

Proof.

Using the product rule for jump processes, we obtain

Integrating from to and using the definition of we get

The stochastic integral in the right hand side of the last inequality is a -local martingale which is bounded below, hence a super martingale, and (4.5) follows. ∎

We now introduce an auxiliary functional related to the convex dual of the utility functions. Let denote either or with fixed. Let denote the inverse of so that

Then, satisfies

In particular,

| (4.6) |

Notice that where is the Legendre-Fenchel transform of the map The map is known as the convex dual of the utility function

For each we define the map

Let For each we denote and define the process and random variable as follows

| (4.7) |

Finally, we define the auxiliary functional

Lemma 4.4.

for all and

Proof.

Let denote the optimal value function of the minimization problem

| (4.8) |

From Lemma 4.4 we have Our aim now is to find a sufficient condition for absence of duality gap and and existence of an optimal portfolio-consumption process for a fixed initial wealth

For each define the processes

and

Observe that satisfies

| (4.9) |

That is, the process is a -martingale. Let denote the essentially unique martingale representation coefficient of with respect to the compensated measure

| (4.10) |

Notice that and for all Moreover, the pair satisfies the linear backward SDE

| (4.11) |

with final condition The following is main result of this paper

Theorem 4.5.

For fixed, suppose there exist and a -predictable portfolio proportion process with values in satisfying

| (4.12) |

and

| (4.13) |

Assume further (2.3) has a solution for where . Then the following assertions hold

Proof.

We first prove part (b). Since it suffices to show that satisfies the wealth equation (2.3) for the pair Recall that satisfies the linear stochastic equation

Using Ito’s formula for jump processes, the differential of is given by

From (4.11), the differential of is given by

Using the product rule for jump processes, we have

We multiply and divide the last bracket by and use to obtain

From (4.13), for the integrand in the stochastic integral, we have

and (4.13) in conjunction with (4.12) yields

and part (b) follows. This in turn implies that a.s. In particular, we get

| (4.14) |

and part (a) follows from Lemma 4.4. Part (c) follows easily since

∎

Remark 4.6.

5 Examples

5.1 Logarithmic utility

We illustrate the main result first by considering logarithmic utility functions

Lemma 5.1.

For all and we have a.s. for -a.e.

Proof.

In this case, we have and for Then, for and

| (5.1) | ||||

Hence, for all and the desired result follows. ∎

Theorem 5.2.

Let be fixed. Suppose there exists a predictable portfolio process with values in satisfying

-

(i)

a.s. for -a.e.

-

(ii)

The process

(5.2) belongs to and satisfies

(5.3)

Then the pair is optimal, where is the consumption process defined by

and is the wealth process with initial wealth and portfolio-consumption pair Moreover, the optimal wealth process satisfies

Proof.

5.2 Regime-switching model with Markov-modulated jump-size distributions

Here we consider the pure-jump model with Markov-modulated jump-size distributions from López and Ratanov [26] (see also López and Serrano [27]) and logarithmic utility.

Let be the marked point process from Example 3.1 with The random times are defined as the jump times of a the two-state continuous-time Markov chain with intensity matrix

For each is the state right before the th jump of and the mark is a random variable with distribution

For each let and denote the continuously compounded interest rate and stock appreciation rate in the regime respectively. Let denote the default-free money-market account with Markov-modulated force of interest that is

The risky asset or stock follows the exponential model with and

Observe that satisfies the linear equation (2.2) with

We assume that for each regime there exists a margin payment function with portfolio constraint set For instance, in the case of different interest rates for borrowing and lending, and prohibition of short-selling, it is given by

where denotes the borrowing rate in regime , which is assumed greater than the lending rate In the case of short selling with cash collateral and negative rebate rates, and prohibition of borrowing from money account,

where is the stock loan fee in regime Finally, for each we define

and Using Theorem 5.2 and the results in Section 4 from [27], we obtain the following

Corollary 5.3.

Let Suppose for each there exists such that for all Suppose further the following conditions hold

-

(i)

-

(ii)

-

(iii)

Let denote the optimal value for the initial wealth and initial regime Then, we have

and

where

5.3 Power utility

We now consider CRRA (fractional) power utility functions of the form with fixed. We suppose that all coefficients in the model the -local characteristics and the margin payment function are non-random.

Lemma 5.4.

For all and deterministic, we have

| (5.4) |

Proof.

Notice that where is the deterministic function

and is the -martingale

Then

with It follows that

and

| (5.5) | ||||

Hence

and

The differential of satisfies

and (5.4) follows. ∎

For simplicity suppose consumption is not allowed i.e. for all

Theorem 5.5.

Let be a (deterministic) portfolio process with values in satisfying

-

(i)

for all

-

(ii)

The map

belongs to and satisfies

Then the portfolio process is optimal.

Proof.

Example 5.6.

Consider the margin payment function of Example 2.1

which models differential interest rates, under the portfolio constraint of prohibition of short-selling of the stock. As seen in Example 4.1, the effective domain of is

Assume further that for all and and the map

| (5.6) |

is well-defined for each and The case corresponds to logarithmic utility, in which case we allow and the -local characteristics to be -predictable processes. It follows that

belongs to iff Using (4.2), condition reads

| (5.7) |

Now, observe that is strictly decreasing for each since

The range of is the interval If also holds, it can be easily checked that the following portfolio weight

| (5.8) |

satisfies and (5.7). Hence, it is optimal. Observe that under the condition the optimal portfolio does not depend on the risk aversion exponent .

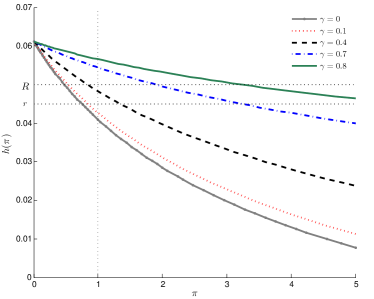

Notice also that and can be given explicitly in terms of the moment generating function of the distribution Indeed, and

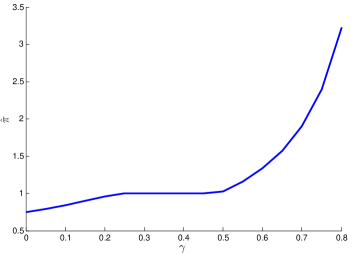

Figure 1 contains plots of for a given and different values of Figure 2 below shows the behaviour of the optimal portfolio as a function of Observe that we can obtain each one of the three last cases in (5.8) by taking different values of

Example 5.7.

Finally, consider the margin payment function of Example 2.2

with which models short-selling with negative rebate rates and prohibition of borrowing from money account. The effective domain of is

Hence, iff and condition reads

| (5.9) |

If also holds, it can be easily checked that the following portfolio weight

| (5.10) |

satisfies and (5.9). Therefore, it is optimal. Observe that, under condition the optimal portfolio does not depend on the risk aversion exponent .

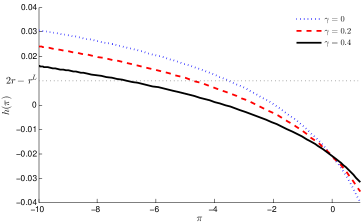

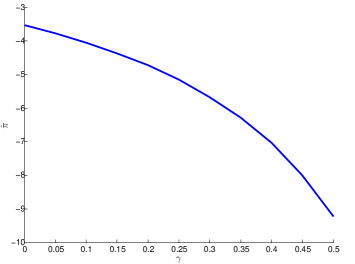

Figures 3 and 4 contain plots of for different values of and of the optimal portfolio as a function of

References

- [1] Tomas Björk, Yuri Kabanov, and Wolfgang Runggaldier, Bond market structure in the presence of marked point processes, Math. Finance 7 (1997), no. 2, 211–239.

- [2] Pierre Brémaud, Point processes and queues, Springer Series in Statistics, Springer-Verlag, New York-Berlin, 1981.

- [3] Giorgia Callegaro and Tiziano Vargiolu, Optimal portfolio for hara utility functions in a pure jump multidimensional incomplete market, Int. J. Risk Assessment and Management 11 (2009), no. 1/2, 180–200.

- [4] Claudia Ceci, Risk minimizing hedging for a partially observed high frequency data model, Stochastics 78 (2006), no. 1, 13–31.

- [5] , Optimal investment problems with marked point processes, Seminar on Stochastic Analysis, Random Fields and Applications VI, Progr. Probab., vol. 63, Birkhäuser/Springer Basel AG, Basel, 2011, pp. 385–412.

- [6] Claudia Ceci and Anna Gerardi, A mode for high frequency data under partial information: a filtering approach, Int. J. Theor. Appl. Finance 9 (2006), no. 4, 555–576.

- [7] , Pricing for geometric marked point processes under partial information: entropy approach, Int. J. Theor. Appl. Finance 12 (2009), no. 2, 179–207.

- [8] Domenico Cuoco and Hong Liu, A martingale characterization of consumption choices and hedging costs with margin requirements, Math. Finance 10 (2000), no. 3, 355–385.

- [9] Jakša Cvitanić and Ioannis Karatzas, Convex duality in constrained portfolio optimization, Ann. Appl. Probab. 2 (1992), no. 4, 767–818.

- [10] Jakša Cvitanić, Robert Liptser, and Boris Rozovskii, A filtering approach to tracking volatility from prices observed at random times, Ann. Appl. Probab. 16 (2006), no. 3, 1633–1652.

- [11] Gene D’Avolio, The marjet for borrowing stock, Journal of Financial Economics 66 (2002), no. 2-3, 271–306.

- [12] Robert J. Elliott and Tak Kuen Siu, Option pricing and filtering with hidden Markov-modulated pure-jump processes, Appl. Math. Finance 20 (2013), no. 1, 1–25.

- [13] Rüdiger Frey, Risk minimization with incomplete information in a model for high-frequency data, Math. Finance 10 (2000), no. 2, 215–225, INFORMS Applied Probability Conference (Ulm, 1999).

- [14] Rüdiger Frey and Wolfgang J. Runggaldier, Risk-minimizing hedging strategies under restricted information: the case of stochastic volatility models observable only at discrete random times, Math. Methods Oper. Res. 50 (1999), no. 2, 339–350.

- [15] , A nonlinear filtering approach to volatility estimation with a view towards high frequency data, Int. J. Theor. Appl. Finance 4 (2001), no. 2, 199–210, Information modeling in finance (Évry, 2000).

- [16] Helyette Geman, Dilip B. Madan, and Marc Yor, Asset prices are Brownian motion: only in business time, Quantitative analysis in financial markets, World Sci. Publ., River Edge, NJ, 2001, pp. 103–146.

- [17] Thomas Goll and Jan Kallsen, Optimal portfolios for logarithmic utility, Stochastic Process. Appl. 89 (2000), no. 1, 31–48.

- [18] Hua He and Neil D. Pearson, Consumption and portfolio policies with incomplete markets and short-sale constraints: the infinite-dimensional case, J. Econom. Theory 54 (1991), no. 2, 259–304.

- [19] Jean Jacod and Albert Shiryaev, Limit theorems for stochastic processes, Grundlehren der mathematischen Wissenschaften (Book 288), Springer, 2002.

- [20] Robert Jarrow and Dilip Madan, Option pricing using the term structure of interest rates to hedge systematic discontinuities in asset returns, Math. Finance 5 (1995), no. 4, 311–336.

- [21] Monique Jeanblanc, Marc Yor, and Marc Chesney, Mathematical methods for financial markets, Springer Finance, Springer, London, UK, 2009.

- [22] Jan Kallsen, Optimal portfolios for exponential Lévy processes, Math. Methods Oper. Res. 51 (2000), no. 3, 357–374.

- [23] Ioannis Karatzas, John P. Lehoczky, Steven E. Shreve, and Gan-Lin Xu, Martingale and duality methods for utility maximization in an incomplete market, SIAM J. Control Optim. 29 (1991), no. 3, 702–730.

- [24] I. Klein and L. C. G. Rogers, Duality in optimal investment and consumption problems with market frictions, Math. Finance 17 (2007), no. 2, 225–247.

- [25] D. Kramkov and W. Schachermayer, The asymptotic elasticity of utility functions and optimal investment in incomplete markets, Ann. Appl. Probab. 9 (1999), no. 3, 904–950.

- [26] Oscar López and Nikita Ratanov, Option pricing driven by a telegraph process with random jumps, J. Appl. Probab. 49 (2012), no. 3, 838–849.

- [27] Oscar López and Rafael Serrano, Martingale approach to optimal portfolio-consumption problems in markov-modulated pure-jump models, Stochastic Models 31 (2015), no. 2, 261––291.

- [28] Daniel Michelbrink and Huiling Le, A martingale approach to optimal portfolios with jump-diffusions, SIAM J. Control Optim. 50 (2012), no. 1, 583–599.

- [29] Jean-Luc Prigent, Option pricing with a general marked point process, Math. Oper. Res. 26 (2001), no. 1, 50–66.

- [30] Tina Hviid Rydberg and Neil Shephard, Dynamics of trade-by-trade price movements: Decomposition and models, Journal of Financial Econometrics 1 (2003), no. 1, 2–25.

- [31] Mark Schroder and Costis Skiadas, Optimality and state pricing in constrained financial markets with recursive utility under continuous and discontinuous information, Math. Finance 18 (2008), no. 2, 199–238.