Nonparametric estimation of extremal dependence

Abstract

There is an increasing interest to understand the dependence structure of a random vector not only in the center of its distribution but also in the tails. Extreme-value theory tackles the problem of modelling the joint tail of a multivariate distribution by modelling the marginal distributions and the dependence structure separately. For estimating dependence at high levels, the stable tail dependence function and the spectral measure are particularly convenient. These objects also lie at the basis of nonparametric techniques for modelling the dependence among extremes in the max-domain of attraction setting. In case of asymptotic independence, this setting is inadequate, and more refined tail dependence coefficients exist, serving, among others, to discriminate between asymptotic dependence and independence. Throughout, the methods are illustrated on financial data.

1 Introduction

Consider a financial portfolio containing three stocks: JP Morgan, Citibank and IBM. We download stock prices from http://finance.yahoo.com between January 1, 2000, and December 31, 2013, and convert them to weekly negative log-returns: if is a series of stock prices, the negative log-returns are

These three series of negative log-returns will be denoted by the vectors for . By taking negative log-returns we force (extreme) losses to be in the upper tails of the distribution functions. It is such extreme values, and in particular their simultaneous occurrence, that are the focus of this chapter.

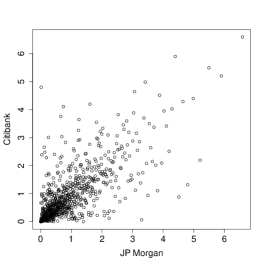

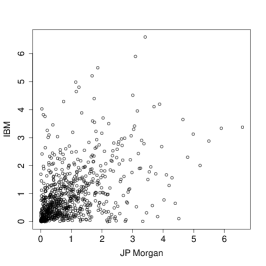

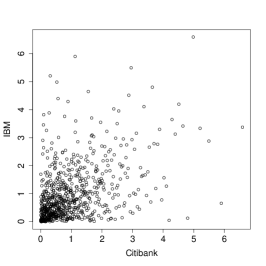

Figure 1 shows the scatterplots of the three possible pairs of negative log-returns on the exponential scale. Specifically, we transformed the negative log-returns to unit-Pareto margins through

| (1) |

(with ) and plotted them on the logarithmic scale; the empirical distribution functions evaluated at the data are defined as

| (2) |

where is the rank of among , i.e., .

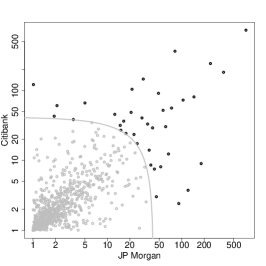

From Figure 1, we observe that joint occurrences of large losses are more frequent for JP Morgan and Citibank (left) than for JP Morgan and IBM (middle) or for Citibank and IBM (right). Given the fact that JP Morgan and Citibank are financial institutions while IBM is an IT company, this is no surprise. In statistical parlance, the pair JP Morgan versus Citibank exhibits the strongest degree of upper tail dependence.

The purpose of this chapter is to describe a statistical framework for modelling such tail dependence. Specifically, we wish to model the tail dependence structure of a -variate random variable , with continuous marginal distribution functions and joint distribution function .

Preliminary marginal transformations of the variables or changes in the measurement unit should not affect the dependence model. Such invariance is obtained by the probability integral transform, producing random variables that are uniformly distributed on the interval . Large values of correspond to being close to unity, whatever the original scale in which was measured. In order to magnify large values, it is sometimes convenient to consider a further transformation to unit-Pareto margins via ; note that for .

In practice, the marginal distributions are unknown and need to be estimated. A simple, robust way to do so is via the empirical distribution functions. The data are then reduced to the vectors of ranks as in (1) and (2).

Starting point of the methodology is a mathematical description of the upper tail dependence of the vector of standardized variables. There is a close connection with the classical theory on vectors of componentwise maxima, the multivariate version of the Fisher–Tippett–Gnedenko theorem (Fisher and Tippett, 1928; Gnedenko, 1943). In the literature, there is a plethora of objects available for describing the dependence component of the limiting multivariate extreme-value distribution. Out of these, we have singled out the stable tail dependence function and the spectral measure (Section 2). The former is convenient as it yields a direct approximation of the joint tail of the distribution function of and thus of ; see (6) below. The latter has the advantage of representing tail dependence as the distribution of the relative magnitudes of the components of given that the vector itself is ‘large’; see (11) below.

Nonparametric inference on tail dependence can then be based on the stable tail dependence function and the spectral measure (Section 3). For convenience and in line with most of the literature, the description of the spectral measure estimators is limited to the bivariate case, although the generalization to the general, multivariate case is straightforward.

A weak point of the classical theory is its treatment of asymptotic independence, that is, when the tail dependence coefficient in (25) is equal to zero. Classically, this case is assimilated to the situation where the variables are exactly independent. Such a reduction applying to all bivariate normal distributions with pairwise correlation less than unity, it is clearly inadequate. More refined tail dependence coefficients as well as tests to distinguish asymptotic dependence from asymptotic independence are presented in Section 4.

The present chapter can serve as an introduction to nonparametric multivariate extreme value analysis. Readers looking for in-depth treatments of multivariate extreme-value distributions and their max-domains of attraction can consult, for instance, Chapter 5 in Resnick (1987) or Chapter 6 in de Haan and Ferreira (2006). Some other accessible introductions are the expository papers by de Haan and de Ronde (1998) and Segers (2012), Chapter 8 in Beirlant et al. (2004), and Part II in Falk et al. (2011). The material on asymptotic independence is inspired on Coles et al. (1999).

2 Tail dependence

2.1 The stable tail dependence function

Let be a random vector with continuous marginal distribution functions and joint distribution function . To study tail dependence, we zoom in on the joint distribution of in the neighbourhood of its upper endpoint . That is, we look at

| (3) |

where is small and where the numbers parametrize the relative distances to the upper endpoints of the variables. The above probability converges to zero as and is in fact proportional to :

The stable tail dependence function, , is then defined by

| (4) |

for (Huang, 1992; Drees and Huang, 1998). The existence of the limit in (4) is an assumption that can be tested (Einmahl et al., 2006).

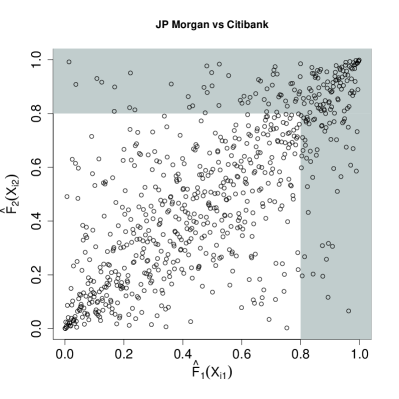

The probability in (3) represents the situation where at least one of the variables is large: for instance, the sea level exceeds a critical height at one or more locations. Alternatively, we might be interested in the situation where all variables are large simultaneously. Think of the prices of all stocks in a financial portfolio going down together. The tail copula, , is defined by

| (5) |

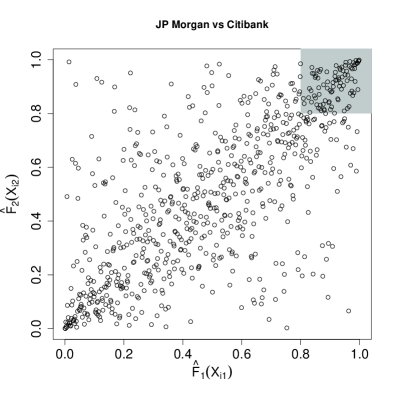

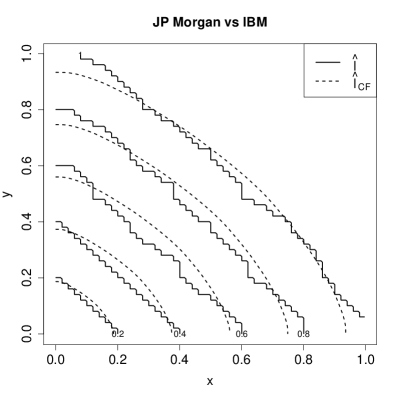

for . Again, existence of the limit is an assumption. In the bivariate case (), the functions and are directly related by . The difference between and is visualized in Figure 2 for the log-returns of the stock prices of JP Morgan versus Citibank. From now on, we will focus on the function because of its direct link to the joint distribution function; see (6).

It is convenient to transform the random variables to have the unit-Pareto distribution via the transformations for . The existence of in (4) is equivalent to the statement that the joint distribution function, , of the random vector is in the max-domain of attraction of a -variate extreme-value distribution, say , with unit-Fréchet margins, i.e., for . The link between and is given by

so that . Since, for “large” we have

| (6) |

we see that estimating the stable tail dependence function is key to estimation of the tail of , and thus, after marginal transformation, of . If, in addition, the marginal distributions are in the max-domains of attraction of the univariate extreme-value distributions , then is in the max-domain of attraction of the -variate extreme-value distribution .

Every stable tail dependence function has the following properties:

-

1.

, and in particular for ;

-

2.

convexity, that is, , for ;

-

3.

order-one homogeneity: , for ;

(Beirlant et al., 2004, page 257). When , these three properties characterize the class of stable tail dependence functions. When , a function satisfying these properties is not necessarily a stable tail dependence function.

The two boundary cases are complete dependence, , and independence, . Another example is the logistic model,

| (7) |

As , extremes become independent and as , extremes become completely dependent. The copula of the extreme-value distribution with this stable tail dependence function is the Gumbel–Hougaard copula.

2.2 The angular or spectral measure

Another insightful approach for modelling extremal dependence of a -dimensional random vector is to look at the contribution of each of the components to their sum conditionally on the sum being large.

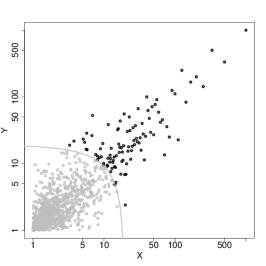

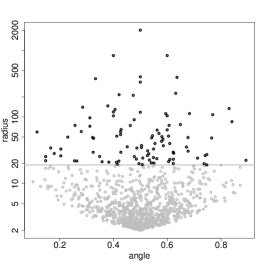

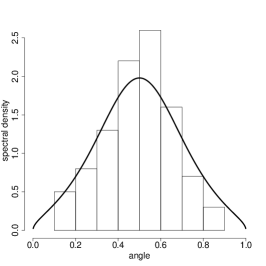

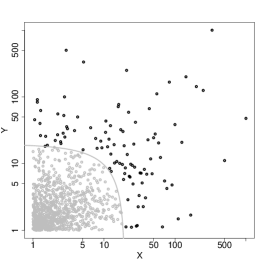

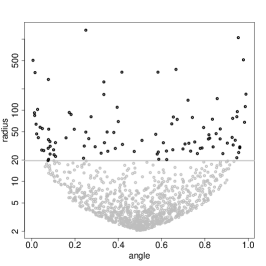

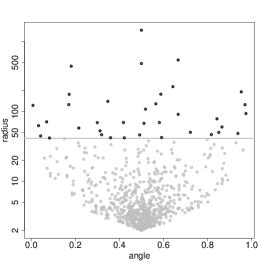

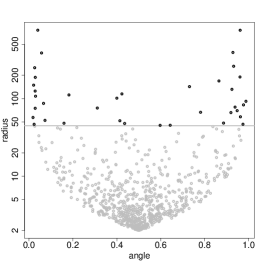

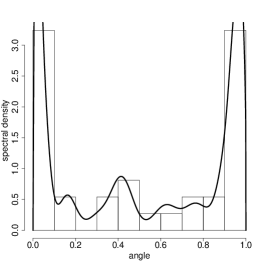

Consider first the bivariate case. In Figure 3 we show pseudo-random samples from the Gumbel copula, which is related to the logistic model (7), at two different values of the dependence parameter : strong dependence () at the top and weak dependence () at the bottom. For convenience, the axes in the scatter plots on the left are on the logarithmic scale. The points for which the sum of the coordinates belong to the top-10% are shown in black. In the middle panels we plot the ratio of the first component to the sum (horizontal axis) against the sum itself (vertical axis). On the right, finally, histograms are given of these ratios for those points for which the sum exceeded the threshold in the plots on the left and in the middle. Strong extremal dependence leads to the ratios being close to (top), whereas low extremal dependence leads to the ratios being close to either or (bottom).

We learn that the distribution of the ratios of the components to their sum, given that the sum is large, carries information about dependence between large values. This distribution is called the angular or spectral measure (de Haan and Resnick, 1977) and is denoted here by . The reference lines in Figure 3 represent the spectral density associated with the Gumbel copula with parameter , that is,

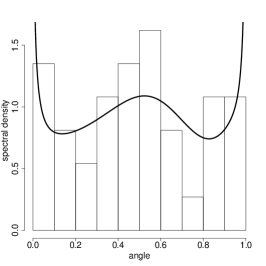

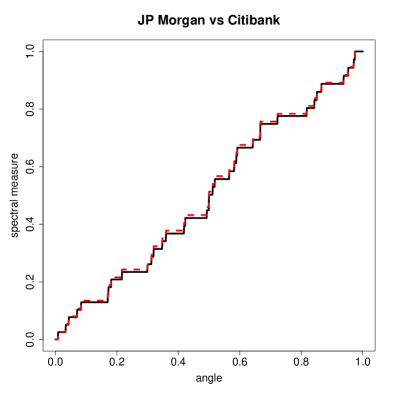

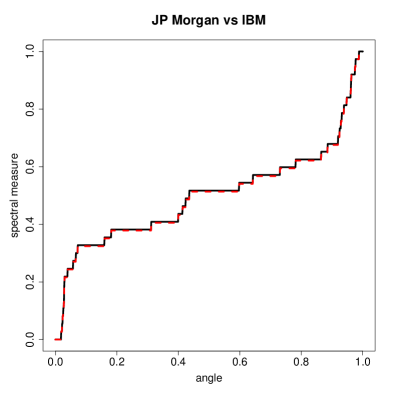

In Figure 4 we show the same plots as in Figure 3 but now for the pairs of negative log-returns of the stock prices of JP Morgan versus Citibank (top) and JP Morgan versus IBM (bottom). For each of the two pairs we do the following. Let , , denote a bivariate sample. First, we transform the data to the unit-Pareto scale using and (1) and (2), i.e.,

| (8) |

Here is the rank of among and is the rank of among . Next, we construct an approximate sample from the spectral measure by setting

| (9) |

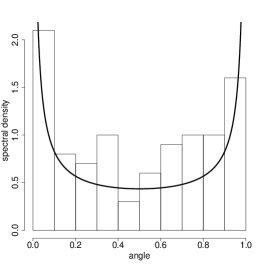

The data in the pseudo-polar representation (9) are shown in the middle plots. The histograms of the ratios for those points for which the sum is above the sample quantile are displayed on the right-hand side. The solid black lines show the smoothed spectral density estimator in (21) below.

For JP Morgan versus Citibank, the ratios are spread equally across the unit interval, suggesting extremal dependence. In contrast, for JP Morgan versus IBM, the spectral density has peaks at the boundaries and , suggesting weak extremal dependence.

In the general, -dimensional setting we transform the random vector as follows:

| (10) |

The spectral measure is defined as the asymptotic distribution of the vector of ratios given that the sum is large:

| (11) |

The support of is included in the unit simplex . In case of asymptotic independence, the spectral measure is concentrated on the vertices of , whereas in case of complete asymptotic dependence it reduces to a unit point mass at the center of .

The spectral measure is related to the stable tail dependence function via

| (12) |

The property that implies the moment constraints

| (13) |

Taking these constraints into account helps to improve the efficiency of nonparametric estimators of (Section 3.1).

3 Estimation

3.1 Estimating the spectral measure

Let , , be independent copies of a random vector with distribution function and continuous marginal distribution functions and . Assume that has a stable tail dependence function as in (24). The function can be represented by the spectral measure via (12), which in the bivariate case specializes to

| (14) |

the unit simplex in being identified with the unit interval, . The moment constraints in (13) simplify to

| (15) |

The aim here is to estimate the spectral measure . The starting point is the limit relation (11). Standardize the margins to the unit-Pareto distribution via and and write

Equation (11) then becomes

| (16) |

The spectral measure can be interpreted as the limit distribution of the angular component, , given that the radial component, , is large.

Mimicking the transformation from via to in a given data-set, it is convenient to standardize the data to the unit-Pareto distribution via (8) and then switch to pseudo-polar coordinates using (9). Different choices for the angular components are possible; for example, Einmahl and Segers (2009) use . For the radial component one can take in general the norm, ; Einmahl et al. (2001) take the norm and de Carvalho et al. (2013) take the norm. Note however that different normalizations lead to different spectral measures.

For estimation purposes, transform pairs into as in (8) and (9). Set the threshold in (16) to , where is an intermediate sequence such that and as . Let denote the set of indices that correspond to the observations with pseudo-radial component above a high threshold, and let denote its cardinality. Here we specify as the quantile of .

In the literature, three nonparametric estimators of the spectral measure have been proposed. All three are of the form

| (17) |

The estimators distinguish themselves in the way the weights are defined.

For the empirical spectral measure (Einmahl et al., 2001), the weights are set to be constant, i.e., . The estimator (17) becomes an empirical version of (16). However, this estimator does not necessarily satisfy the moment constraints in (15). This is a motivation for the two other estimators where the moment constraint is enforced by requiring that .

The maximum empirical likelihood estimator (Einmahl and Segers, 2009), , has probability masses solving the optimization problem

| (18) |

By construction, the weights satisfy the moment constraints. The optimization problem in (18) can be solved by the method of Lagrange multipliers. In the nontrivial case where is in the convex hull of , the solution is given by

where is the Lagrange multiplier associated to the second equality constraint in (18), defined implicitly as the solution to the equation

Note that in (18), it is implicitly assumed that .

Another estimator that satisfies the moment constraints is the maximum Euclidean likelihood estimator (de Carvalho et al., 2013). The probability masses solve the following optimization problem:

| (19) |

This quadratic optimization problem with linear constraints can be solved explicitly with the method of Lagrange multipliers, yielding

| (20) |

where and denote the sample mean and sample variance of , , respectively, that is,

The weights could be negative, but this does usually not occur as the weights are all nonnegative with probability tending to one.

It is shown in Einmahl and Segers (2009) and de Carvalho et al. (2013) that and are more efficient than . Moreover, asymptotically there is no difference between the maximum empirical likelihood or maximum Euclidean likelihood estimators. The maximum Euclidean likelihood estimator is especially convenient as the weights are given explicitly.

For the stock market data from JP Morgan, Citibank and IBM, Figure 5 shows the empirical spectral measure and the maximum Euclidean estimator for the two pairs involving JP Morgan. In each case, the threshold is set to be the quantile of the sample of radii . Enforcing the moment constraints makes a small but noticeable difference. Tail dependence is strongest for the pair JP Morgan versus Citibank, with spectral mass distributed approximately uniformly over . For the pair JP Morgan versus IBM, tail dependence is weaker, the spectral measure being concentrated mainly near the two endpoints, and .

The nonparametric estimators of the spectral probability measure can be smoothed in such a way that the smoothed versions still obey the moment constraints. This can be done using kernel smoothing techniques, although some care is needed since the spectral measure is defined on a compact interval. In de Carvalho et al. (2013) the estimator is constructed by combining Beta distributions with the weights, , of the maximum Euclidean likelihood estimate. To ensure that the estimated measure obeys the marginal moment constraints, it is imposed that the mean of each smoother equals the observed pseudo-angle. The Euclidean spectral density estimator is defined as

| (21) |

where is the smoothing parameter, to be chosen via cross-validation, and

is the Beta density with parameters .

For the financial data, the realized spectral density estimator is plotted on the right-hand panel of Figure 4. The picture is in agreement with the one in Figure 5. The distribution of the spectral mass points to asymptotic dependence for JP Morgan versus Citibank and to weaker asymptotic dependence for JP Morgan versus IBM.

Integrating out the estimated spectral density yields a smoothed version of the empirical spectral measure or its variants: for the maximum Euclidean likelihood estimator, we get

| (22) |

with the regularized incomplete beta function. As

| (23) |

the moment constraint (15) is satisfied.

3.2 Estimating the stable tail dependence function

Consider again the general, multivariate case. Given a random sample , , the aim is to estimate the stable tail dependence function in (4) of the common distribution with continuous margins . A straightforward nonparametric estimator can be defined as follows. Let be such that and as . By replacing by the empirical distribution function, by , and by as defined in (2), we obtain the empirical tail dependence function (Huang, 1992; Drees and Huang, 1998)

Under minimal assumptions, the estimator is consistent and asymptotically normal with a convergence rate of (Einmahl et al., 2012; Bücher et al., 2014). Alternatively, the marginal distributions might be estimated by or , resulting in estimators that are asymptotically equivalent to .

Another estimator of can be defined by estimating the spectral measure, , and applying the transformation in (12), an idea going back to Capéraà and Fougères (2000). In the bivariate case, we can replace in (14) by one of the three nonparametric estimators studied in Section 3.1. Recall the notations in (8) and (9). If we modify the definition of the index set to , where denotes the -th largest observation of the ’s, then there are exactly elements in the set . Starting from the empirical spectral measure , we obtain the estimator

For the maximum empirical or Euclidean likelihood estimators and , one needs to replace the factor by the weights and , respectively.

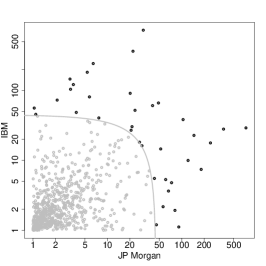

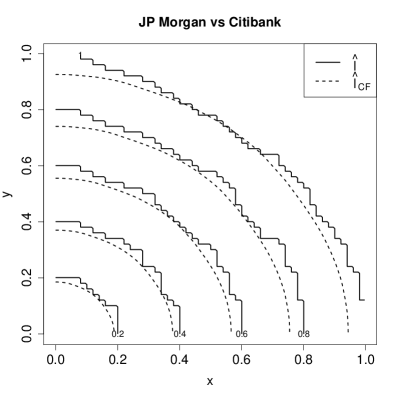

A way to visualize the function or an estimator thereof is via the level sets for a range of value of . Note that the level sets are equal to the lines in case of asymptotic independence and to the elbow curves in case of complete asymptotic dependence. Likewise, a plot of the level sets of an estimator of can be used as a graphical diagnostic of asymptotic (in)dependence; see de Haan and de Ronde (1998) or de Haan and Ferreira (2006, Section 7.2).

We plot the lines for and of and for the weekly log-returns of JP Morgan versus Citibank and JP Morgan versus IBM in Figure 6. The level sets for JP Morgan versus IBM resemble the straight lines much more closely than the level sets for JP Morgan versus Citibank do. The estimator based on the spectral measure, , acts as a smooth version of the empirical tail dependence function .

Nonparametric estimators for can also serve as stepping stone for semiparametric inference. Assume that , a finite-dimensional parametric family. Then one could estimate by minimizing a distance or discrepancy measure between and members of the parametric family (Einmahl et al., 2012; Einmahl et al., 2014).

4 Asymptotic independence

In this section we will focus on the bivariate case. Let , , be independent copies of a random vector , with distribution function having continuous margins and . Recall from (4) that the stable tail dependence function (provided it exists) is given by

| (24) |

After marginal standardization, the pair of component-wise sample maxima converges weakly to the bivariate max-stable distribution given by for ; see (6). Asymptotic independence of the sample maxima, for all , is equivalent to for all . The opposite case, for some , is referred to as asymptotic dependence.

Sibuya (1960) already observed that bivariate normally distributed vectors are asymptotically independent as soon as the correlation is less than unity. We find that in case of asymptotic independence, we cannot rely on the function to quantify the amount of dependence left above high but finite thresholds.

Tail dependence coefficients serve to quantify the amount of tail dependence and to distinguish between asymptotic dependence versus independence (Subsection 4.1). To decide which of the two situations applies for a data set, a number of testing procedures are available (Subsection 4.2).

4.1 Tail dependence coefficients

A first measure for the strength of asymptotic dependence is the tail dependence coefficient

| (25) |

(Coles et al., 1999). By the properties of (Section 2.1), we have for all if and only if . That is, asymptotic independence is equivalent to , whereas asymptotic dependence is equivalent to .

To estimate , we will first write it as the limit of a function , so that ; the function is defined as

To estimate from a sample , simply replace and by their empirical counterparts in (2):

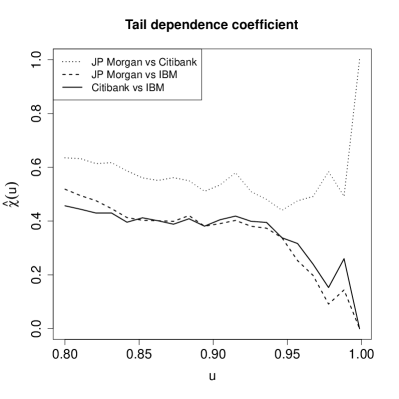

For the stock price log-returns of JP Morgan, Citibank, and IBM, the estimated tail dependence coefficients of the three possible pairs are shown in Figure 7 as a function of . The plot confirms the earlier finding that tail dependence is stronger between the two banking stocks, JP Morgan and Citibank, than between either of the two banks and IBM.

If the variables are asymptotically independent, , we need a second measure quantifying the extremal dependence. The coefficient of tail dependence, , can be motivated as follows (Ledford and Tawn, 1996). Since for , we have

A model that links these two situations is given by the assumption that the joint survival function above is regularly varying at with index , i.e.,

| (26) |

where is a slowly varying function, that is, as for fixed ; see for example Resnick (1987).

For large , if we treat as constant, there are three cases of non-negative extremal association to distinguish:

-

1.

and : asymptotic dependence;

-

2.

: positive association within asymptotic independence;

-

3.

: (near) perfect independence.

Values of occur when there is negative association between the two random variables at extreme levels.

In order to estimate , we first define the structure variable

| (27) |

For a high threshold and for , we have, by slow variation of ,

On the right-hand side we recognize a generalized Pareto distribution with shape parameter . Given the sample , we can estimate with techniques from univariate extreme value theory applied to the variables

One possibility consists of fitting the generalized Pareto distribution to the sample of excesses for those for which (Ledford and Tawn, 1996, page 180). Alternatively, one can use the Hill estimator (Hill, 1975)

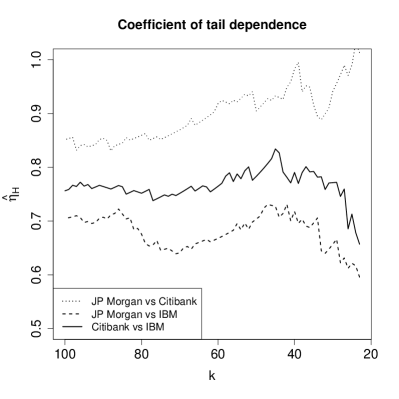

where denote the order statistics of . Figure 7 shows the estimators of the coefficient of tail dependence between JP Morgan and Citibank, JP Morgan and IBM, and Citibank and IBM for a decreasing number of order statistics. The estimators suggest asymptotic dependence for the log-returns of JP Morgan versus Citibank.

Another frequently used measure in case of asymptotic independence can be obtained from (26). Taking logarithms on both sides and using slow variation of , we obtain

Coles et al. (1999) proposed the coefficient

As , we have . For a bivariate normal dependence structure, is equal to the correlation coefficient . Together, the two coefficients and contain complementary information on the amount of tail dependence:

-

•

If and , the variables and are asymptotically independent and quantifies the degree of dependence. The cases , , and correspond to positive association, near independence, and negative association, respectively.

-

•

If and , the variables are asymptotically dependent, and quantifies the degree of dependence.

Although the graphical procedures in this section are easy to use, it is difficult to draw a conclusion from the plots, and it might be better to consider formal tests of asymptotic independence (Section 4.2). For an overview of more recent and advanced techniques in asymptotic independence, see for example de Carvalho and Ramos (2012) or Bacro and Toulemonde (2013).

4.2 Testing for asymptotic (in)dependence

Above we have called the variables and asymptotically independent if . A sufficient condition for asymptotic independence is that the coefficient of tail dependence, , in (26) is less than unity.

These observations yield two possible approaches to test for asymptotic (in)dependence, depending on the choice of the null hypothesis. Suppose the function in (26) converges to a positive constant.

-

•

Testing versus amounts to choosing asymptotic dependence as the null hypothesis.

-

•

Testing versus means that asymptotic independence is taken as the null hypothesis.

Asymptotic dependence as the null hypothesis.

In order to test for versus , the idea is to estimate and to reject if the estimated value of is below some critical value. The estimator chosen in Draisma et al. (2004) is the maximum likelihood estimator, , obtained by fitting a generalized Pareto distribution to the highest order statistics of the sample in (27). The effective sample size, , tends to infinity at a slower rate than .

In order to derive the asymptotic distribution of , condition (26) needs to be refined. Consider the function

Note that the tail dependence coefficient in (25) is given by . Equation (26) implies that the function is regularly varying at zero with index , i.e., for . In Draisma et al. (2004), this relation is refined to bivariate regular variation: it is assumed that

| (28) |

The limit function is homogeneous of order , i.e., for . Clearly, . To control the bias of , a second-order refinement of (28) is needed: assume the existence of the limit

for all with . Here, as , while the limit function is neither constant nor a multiple of . The convergence is assumed to be uniform on .

Suppose that the function has partial derivatives and . Let be a sequence such that as , where if and only if . Then is asymptotically normal,

the asymptotic variance being

Under the null hypothesis , consistent estimators of and are given by

where and is the th largest observation of

The estimator is defined analogously to . The null hypothesis is rejected at significance level if

| (29) |

where or .

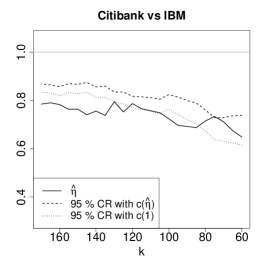

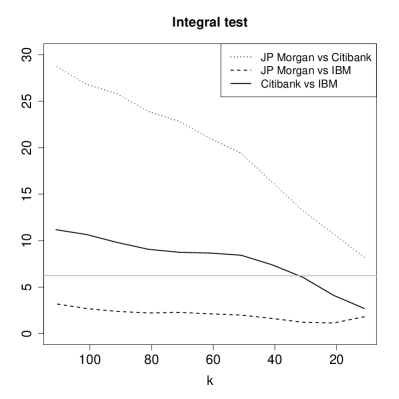

Figure 8 shows the estimates of for a varying number of order statistics , together with the lines defining the critical regions for the two tests in (29). We used the function gpd.fit from the ismev package (Heffernan and Stephenson, 2012). We see clearly that for JP Morgan versus Citibank, for every threshold, asymptotic dependence cannot be rejected; for JP Morgan versus IBM, asymptotic dependence is rejected at every threshold; and for Citibank versus IBM, results vary depending on the value of .

Asymptotic independence as the null hypothesis.

Another approach for deciding between asymptotic dependence and asymptotic independence is to assume a null hypothesis of asymptotic independence, i.e., . Recall the nonparametric estimator in Section 3.2. A natural approach would be to reject as soon as the difference between and the function is too large. However, from Einmahl et al. (2006) it follows that, under ,

The limit being degenerate, it is not possible to compute critical values.

In Hüsler and Li (2009) another estimator of is proposed, based on a division of the sample into two sub-samples. Note first that we can write as

For convenience, assume that is even. The first sub-sample is compared with the -th largest order statistics of the second sub-sample ; in other words, we use the estimator

where for denotes the rank of among . Under , the estimator converges in probability to , for fixed . Define

Then under , assuming certain regularity conditions on and (Hüsler and Li, 2009, page 992), if as ,

where and are two independent Brownian motions. By the continuous mapping theorem,

We reject the null hypothesis of asymptotic independence at significance level if or if , where and represent the quantile functions of and respectively. Hüsler and Li (2009) compute and .

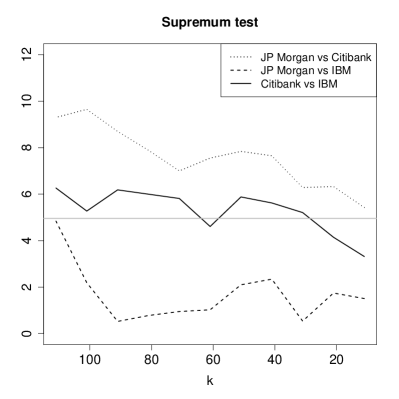

Figure 9 shows the values of the test statistics and for the three pairs of stock returns, together with the pointwise critical regions for a range of -values. The results are in agreement with Figure 8: asymptotic independence is rejected for JP Morgan versus Citibank, asymptotic independence cannot be rejected for JP Morgan versus IBM, and conclusions for Citibank versus IBM depend on the value of .

Acknowledgments

The authors gratefully acknowledge funding by contract “Projet d’Actions de Recherche Concertées” No. 12/17-045 of the “Communauté française de Belgique” and by IAP research network Grant P7/06 of the Belgian government (Belgian Science Policy). Anna Kiriliouk and Michał Warchoł gratefully acknowledge funding from the Belgian Fund for Scientific Research (F.R.S. - FNRS).

REFERENCES

- Bacro and Toulemonde (2013) Bacro, J.-N. and G. Toulemonde (2013). Measuring and modelling multivariate and spatial dependence of extremes. Journal de la Société Française de Statistique 154(2), 139–155.

- Beirlant et al. (2004) Beirlant, J., Y. Goegebeur, J. Segers, and J. Teugels (2004). Statistics of Extremes: Theory and Applications. Wiley.

- Bücher et al. (2014) Bücher, A., J. Segers, and S. Volgushev (2014). When uniform weak convergence fails: empirical processes for dependence functions and residuals using epi- and hypographs. The Annals of Statistics (to appear), http://arxiv.org/abs/1305.6408.

- Capéraà and Fougères (2000) Capéraà, P. and A.-L. Fougères (2000). Estimation of a bivariate extreme value distribution. Extremes 3(4), 311–329.

- Coles et al. (1999) Coles, S., J. Heffernan, and J. Tawn (1999). Dependence measures for extreme value analyses. Extremes 2(4), 339–365.

- Coles and Tawn (1991) Coles, S. and J. Tawn (1991). Modelling extreme multivariate events. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 53, 377–392.

- de Carvalho et al. (2013) de Carvalho, M., B. Oumow, J. Segers, and M. Warchoł (2013). A euclidean likelihood estimator for bivariate tail dependence. Communications in Statistics - Theory and Methods 42(7), 1176–1192.

- de Carvalho and Ramos (2012) de Carvalho, M. and A. Ramos (2012). Bivariate extreme statistics, ii. REVSTAT - Statistical Journal 11(1), 83–107.

- de Haan and de Ronde (1998) de Haan, L. and J. de Ronde (1998). Sea and wind: Multivariate extremes at work. Extremes 1, 7–45.

- de Haan and Ferreira (2006) de Haan, L. and A. Ferreira (2006). Extreme Value Theory: an Introduction. Springer-Verlag Inc.

- de Haan and Resnick (1977) de Haan, L. and S. I. Resnick (1977). Limit theory for multivariate sample extremes. Z. Wahrscheinlichkeitstheorie und Verw. Gebiete 40(4), 317–337.

- Draisma et al. (2004) Draisma, G., H. Drees, A. Ferreira, and L. De Haan (2004). Bivariate tail estimation: dependence in asymptotic independence. Bernoulli 10(2), 251–280.

- Drees and Huang (1998) Drees, H. and X. Huang (1998). Best attainable rates of convergence for estimators of the stable tail dependence function. Journal of Multivariate Analysis 64(1), 25–47.

- Einmahl et al. (2006) Einmahl, J., L. de Haan, and D. Li (2006). Weighted approximations of tail copula processes with application to testing the bivariate extreme value condition. The Annals of Statistics 34, 1987–2014.

- Einmahl et al. (2014) Einmahl, J., A. Kiriliouk, A. Krajina, and J. Segers (2014). An M-estimator of spatial tail dependence. Available on http://arxiv.org/abs/1403.1975.

- Einmahl et al. (2012) Einmahl, J., A. Krajina, and J. Segers (2012). An M-estimator for tail dependence in arbitrary dimensions. The Annals of Statistics 40, 1764–1793.

- Einmahl et al. (2001) Einmahl, J. H., L. de Haan, and V. I. Piterbarg (2001). Nonparametric estimation of the spectral measure of an extreme value distribution. The Annals of Statistics 29(5), 1401–1423.

- Einmahl and Segers (2009) Einmahl, J. H. J. and J. Segers (2009). Maximum empirical likelihood estimation of the spectral measure of an extreme-value distribution. The Annals of Statistics 37(5B), 2953–2989.

- Falk et al. (2011) Falk, M., J. Hüsler, and R.-D. Reiss (2011). Laws of small numbers: extremes and rare events (extended ed.). Birkhäuser/Springer Basel AG, Basel.

- Fisher and Tippett (1928) Fisher, R. A. and L. H. C. Tippett (1928). Limiting forms of the frequency distribution of the largest or smallest member of a sample. In Mathematical Proceedings of the Cambridge Philosophical Society, Volume 24, pp. 180–190. Cambridge Univ Press.

- Gnedenko (1943) Gnedenko, B. (1943). Sur la distribution limite du terme maximum d’une serie aleatoire. Annals of mathematics, 423–453.

- Heffernan and Stephenson (2012) Heffernan, J. E. and A. G. Stephenson (2012). ismev: An Introduction to Statistical Modeling of Extreme Values. R package version 1.38.

- Hill (1975) Hill, B. M. (1975). A simple general approach to inference about the tail of a distribution. The Annals of Statistics 3, 1163–1174.

- Huang (1992) Huang, X. (1992). Statistics of bivariate extreme values. Ph. D. thesis, Tinbergen Institute Research Series.

- Hüsler and Li (2009) Hüsler, J. and D. Li (2009). Testing asymptotic independence in bivariate extremes. Journal of Statistical Planning and Inference 139, 990–998.

- Ledford and Tawn (1996) Ledford, A. W. and J. A. Tawn (1996). Statistics for near independence in multivariate extreme values. Biometrika 83, 169–187.

- Pickands (1981) Pickands, J. (1981). Multivariate extreme value distributions. In Bulletin of the International Statistical Institute, pp. 859–878.

- Resnick (1987) Resnick, S. I. (1987). Extreme Values, Regular Variation, and Point Processes. Springer, New York.

- Segers (2012) Segers, J. (2012). Max-stable models for multivariate extremes. REVSTAT Statistical Journal 10, 61–82.

- Sibuya (1960) Sibuya, M. (1960). Bivariate extreme statistics, I. Annals of the Institute of Statistical Mathematics 11(2), 195–210.