A two-component copula with links to insurance

Abstract.

This paper presents a new copula to model dependencies between insurance entities, by considering how insurance entities are affected by both macro and micro factors. The model used to build the copula assumes that the insurance losses of two companies or lines of business are related through a random common loss factor which is then multiplied by an individual random company factor to get the total loss amounts. The new two-component copula is not Archimedean and it extends the toolkit of copulas for the insurance industry.

Key words and phrases:

Copula, Two-Component model, insurance.2010 Mathematics Subject Classification:

62H05, 62P05.1. Introduction

There are many copulas used in the insurance industry to model dependencies between different lines of businesses within or between insurance companies. Many of these copulas are not built with insurance scenarios in mind and often their assumptions break down when modelling a full insurance distribution curve. For example, the Gaussian copula, which is one of the most commonly used copulas in the insurance industry, does not have any upper tail dependence. Thus, this copula cannot model tail correlation within lines of businesses or between insurance entities which are believed to have tail correlation, such as what would be expected between two lines of business which are heavily affected by the same catastrophic event.

To provide a better copula solution than what is currently in-use, this paper proposes and analyses a new copula, coined the Two-component (model) copula. This copula is based on an insurance model where a dependence structure is formulated between two insurance entities by considering the effects of both macro and micro economic factors. The underlying model of the copula is as follows;

where and are the losses experienced by two insurance companies or lines of businesses. is the macro (common) loss factor and has an exponential distribution with parameter 1 and and are the micro (company specific loss) factors modelled to have inverse gamma distributions with shape parameter and respectively and rate parameter 1; and are constants, and , and are assumed to be independent random variables. From this model the Two-component copula is derived; it is given in Theorem 3.1. In this paper, as well as analysing the derivation model of the copula, simulated data is generated under the two-componend model and fitted to several different copulas to gauge how different it is to copulas already available.

The paper is structured as follows. Chapter 2 contains a background on copulas and provides an outline of the goodness-of-fit (GoF) tests used on the simulated data. In Chapter 3 the Two-component model is derived, analysed and goodness-of-fit tests are preformed on simulated data generated from the the derivation model of the copula.The Appendix contains a detailed algorithm for the GoF test used for the copulas, as well as the colour palette used in the plots.

2. Background

2.1. Copulas

A copula connects the one-dimensional marginal distributions of several random variables to the multivariate distribution function of the variables. Here we concentrate on bivariate distributions. Below is a short overview; for reference and more details see Nelsen (2006).

For each of the following definitions we consider functions with domain where are nonempty; is the range of . We let .

Definition 2.1.

Let be a rectangle whose vertices are in , then the H-volume of is given by

is 2-increasing if , for all rectangles whose vertices are in . Suppose is the least element of . Then is grounded if , for all .

Definition 2.2.

A two-dimensional copula is a function such that is grounded and 2-increasing, and and for all .

Nelsen (2006) states in Lemma 2.1.4 that if defined above is grounded and 2-increasing, then is non-decreasing in each argument. This lemma can be used to show that .

A key theorem for copulas is Sklar’s Theorem, which uses the notion of margins, or marginal distributions. If is the greatest element of , , then the margins of are the functions and where and for all whereas and for all

Theorem 2.3.

[Sklar’s Theorem] (Thm 2.3.3 Nelsen (2006)) If is a joint (cumulative) distribution function with margins and , then there exists a copula such that ,

| (2.1) |

If and are continuous, then is unique; otherwise, is uniquely determined on . Conversely, if is a copula and F and G are distribution functions, then defined by (2.1) is a joint distribution function with margins and .

Sklar’s Theorem shows that a joint distribution can be split into two parts; the respective marginal distributions of the random variables and a dependence relation, given by the copula. Thus, a copula disentangles the dependence structure of random variables from their marginal distributions. Further, since if is the margin of a uniform distribution, the set of copulas is the set of joint distribution functions of two random variables evaluated on .

An advantage copulas have over joint distribution functions is that they act predictably under strictly monotone transformations of continuous random variables, see Thm 2.4.3 and 2.4.4 in Nelsen (2006). In particular we have that if and are continuous random variables, with copula and if and be strictly decreasing transformations on and , respectively, then

| (2.2) |

If and are strictly increasing,then

| (2.3) |

Lastly, since in insurance we are concerned with dependence in extreme events (i.e. one-in-two hundred years event), we use a notion of upper tail dependence and show how it relates to copulas.

Definition 2.4.

Let and be continuous random variables with distributions and , respectively. The upper tail dependence parameter is the limit (if it exists) of the conditional probability that is greater than the 100tth percentile of given that is greater than the 100tth percentile of as approaches 1, i.e.

| (2.4) |

Theorem 2.5.

If , then has upper tail dependence, otherwise it does not have upper tail dependence.

2.2. Dependence measures

The most commonly used dependence measure is Pearson’s Correlation, which is not a copula based measure. Pearson’s Correlation can give misleading answers if the joint distribution linking two random variables does not have an elliptical distribution and is also not defined for some heavy-tailed distributions as it requires finite variances. Here, following Embrechts et al. (2003), Definition 5.1, we say that a random dimensional real vector has an elliptical distribution with parameters and a nonnegative definite, symmetric matrix if the characteristic function of is of the form

| (2.5) |

Since it is commonly seen that insurance data comes from a heavy-tailed distribution, in this article we will instead use Kendall’s tau to measure dependence. Kendall’s tau is in a class of copula-based dependence measures called concordance measures, see Embrechts et al. (2003), which is defined for a random vector

where is an independent copy of . The next theorem links Kendall’s tau to Pearson’s correlation, which is useful for Gaussian copulas, see Subsection 2.3.1.

2.3. Types of copulas

In this section we discuss the Gaussian copula and the Gumbel copula as a special case of an Archimedean copula, as well as the class of Extreme-value copulas. For reference on the Gaussian, Gumbel or Archimedean copulas see Embrechts et al. (2003). For reference on Extreme-value copulas see Gudendorf and Segers (2010) and Ben Ghorbal et al. (2009). All copulas are understood to be bivariate copulas.

2.3.1. The Gaussian Copula

The Gaussian copula with linear correlation matrix with is given by

Gaussian copulas do not have upper tail dependence (Embrechts et al. (2003)), which suggests that even though they are one of the most common copulas used in insurance, they are not suited to this purpose as the one-in-two hundred year events (important for regulation purposes) are modelled incorrectly.

The linear correlation matrix is usually estimated by Pearson’s correlation taken from the data, but particularly for right heavy tailed distributions this could be skewed by a few large observations. Further, as Pearson’s correlation is not invariant under strictly increasing transformations of the random variables and the copula is, we can have , but . A better estimator for , can be derived from Theorem 2.6 for elliptical distributions to be , where is the estimate of Kendall’s tau estimated from the data. This estimator is more robust than as Kendall’s tau is invariant under monotone transformations of the data. Embrechts et al. (2003) recommends this estimator of for both elliptical and non-elliptical distributions with elliptical copulas. Thus, in later chapters when we compare the Two Component Copula with the Gaussian copula on simulated data we will use this estimator. We note that the estimate for is a valid Gaussian copula parameter only if . So a Gaussian copula can only be fitted to by this method if .

2.3.2. The Gumbel Copula

The family of Archimedean copulas is defined using the following two definitions:

Definition 2.7.

Let be a continuous, strictly decreasing function from to such that . The pseudo-inverse of is the function given by

In particular, if , then .

Theorem 2.8.

Copulas of the form (2.6) are called Archimedean copulas and is called the generator of the copula. From the formula it can be seen that Archimedean copulas are symmetric ( for all ).

The Gumbel copula is an Archimedean copula with

Gumbel copulas have an upper tail dependence coefficient of (Embrechts et al. (2003)). Using Theorem 6.5 in Embrechts et al. (2003), if and are random variables with a Gumbel copula with parameter , then . This expression is a valid Gumbel parameter only if and . So if is Kendall’s tau for and estimated from the data, a Gumbel copula can only be fitted if .

2.3.3. Extreme-Value Copulas

Extreme-value copulas occur naturally in extreme event situations, and in contrast to Gaussian or Gumbel copulas do not have to be symmetric (Gudendorf and Segers (2010)). Comparing the Two-component copula to the class of Extreme-value copulas will compliment our tool kit.

Definition 2.9.

(Thm 6.2.3 Gudendorf and Segers (2010)) A bivariate copula is an Extreme-value copula if and only if

where is convex and satisfies for all .

The upper and lower bounds of correspond to perfect independence and dependence, respectively. If and have an Extreme-value copula then the conditional probability of given is an increasing function of and vice versa for given . Kendall’s tau of an Extreme-value copula is non-negative and is given by

The coefficient of upper tail dependence of an Extreme-value copula simplifies to

which is a decreasing function of A(1/2).

The Gumbel copula is the only Archimedean copula that is also an Extreme-value copula, with (Genest et al. (2011)).

2.4. Goodness-of-fit tests for copulas

Weiß (2011) assesses the robustness of three goodness-of-fit tests for copulas which are based on the empirical copula process, Kendall’s dependence function and the Rosenblatt’s transform, respectively. His findings do not specifically show that one test was better than the other. In this study we focus on the goodness-of-fit test based on the empirical copula process because it is the most intuitive test out of the three. This test is based on comparing the best parametric copula under the null hypothesis with Deheuvels’ empirical copula, which is defined as follows.

Definition 2.10.

Let be a vector of any two uniform random variables. Let for be an i.i.d. sample of U of size n. Then Deheuvels’ bivariate empirical copula for U is defined as

| (2.7) |

The empirical copula is similar to the well-known empirical cumulative distribution function (c.d.f.) and converges uniformly to the true underlying copula (Weiß (2011)), making it a (discontinuous) approximation of the true copula.

To describe the goodness-of-fit test, suppose we have a random vector containing two random variables, and suppose we have i.i.d. samples of this vector, for . in order to avoid problems on the boundary we define a transformed sample as

| (2.8) |

where is the empirical one-dimensional c.d.f. at . Then, the fit of a parametric copula is assessed using a Cramér-von-Mises statistic; where is Deheuvels’s bivariate empirical copula and is the best fitting parametric copula from the parametric copula family that contains the true copula under . The parameter of this copula () is estimated using the transformed sample (). In this study the test statistic is approximated empirically by

| (2.9) |

As the distribution of this test statistic is unknown, the -values of the goodness-of-fit test are approximated using a bootstrap method that can be found in Section 3.10 of Berg (2009); see Appendix A. This test performed well in the power study conducted in Berg (2009), where the power of nine goodness-of-fit tests for copulas were compared. Note that the test is independent of the assumption on the marginal distributions.

2.5. The distribution of large insurance losses

This subsection explains the properties generally attributed to and a distribution used to describe large insurance losses that help to derive the model in Chapter 3.

2.5.1. The heavy-tailed property of large insurance

For the five biggest insurance losses from , the range of the loss figures is $57.5 billion, approximately of the largest loss figure, which is $72.3 billion (Hurricane Katrina). Further, the second largest loss, $35.0 billion (Tohoku earthquake and tsunami) is less than of the largest loss, according to http://www.businessinsider.com/the-11-most-expensive-insurance-losses-in-recent-history-2012-2. This is a property of right-heavy tailed distributions. There are several definitions for a heavy-tail distribution (see Theorem 2.6 in Foss et al. (2011)); in this paper we use the following definition:

Definition 2.11.

(Adapted from Thm 2.6 and Def 2.4 Foss et al. (2011)) The distribution function F is a (right) heavy-tailed distribution if and only if

Thus, a distribution is heavy-tailed if extreme right-tail events are more likely to occur in the distribution relative to any exponential distribution.

2.5.2. The Generalised Pareto Distribution

The Generalised Pareto Distribution (GPD) is commonly used to model large insurance losses; for reference see Chotikapanich (2008).

Definition 2.12.

(Embrechts et al. (1997)) A random variable has a Generalised Pareto Distribution with location parameter , scale parameter and shape parameter (denoted by ) if

for when , and when . In particular a random variable has a Type II Pareto distribution with location parameter , scale parameter and shape parameter (denoted by ) if its c.d.f. is

Depending on , the GPD is related to one of three distributions.

-

(1)

If then ;

-

(2)

if then ;

-

(3)

if then is a scaled beta distribution.

Since the Exponential and Beta distributions are not heavy-tailed distributions, the rest of this section focuses on the case .

Comparing the survival distribution of the Type II Pareto distribution with for any , we see that it is a heavy-tailed distribution.

A construction of Pareto distributions from other distributions, is a Feller-Pareto distribution, given in Theorem 2.13.

Theorem 2.13.

(Chotikapanich (2008)) Let and . Let and be two independent Gamma distributions. Then

has a Feller-Pareto distribution, denoted by . Further, .

3. The Two-component copula

In this section we hypothesise how insurance losses (losses) are dependent and derive and analyse a new copula (Two-component model copula) that models these hypotheses. The copula is derived by; first building a model (Two-component model) of an insurance scenario from the hypotheses, then applying Sklar’s theorem to find the copula of this model. Lastly, we see how well our GoF tests perform on data generated from the Two-component model.

3.1. The two-component model

Preliminary to hypothesising about the dependence structure, we make the following assumptions about the marginal distributions of large insurance losses which are based on well-accepted beliefs.

-

(1)

The marginal distributions are GPDs. This assumption is recommended in Embrechts et al. (1997) as it is an Extreme-Value theory distribution.

-

(2)

The GPDs have , hence are Type II Pareto distributions. This assumption arises as it is a common belief that losses are heavy tailed.

-

(3)

The GPDs have . This assumption is plausible as it translates to the assumption that no profit can be made from an insurance payout.

The hypotheses of how losses are dependent are derived by breaking down the problem for why they would occur. Losses occurs if two conditions hold; firstly, a loss event occurred, and secondly, the loss event was underwritten by the company. For simplicity we assume these are the only two factors affecting a payout (other factors like the possibility of default are ignored). The size of the payout should be proportional to both the size of the event, which should not depend on the company because they occur on a macro level, and the level of business underwritten. So suppose that the insurance losses of two companies or lines of business, 1 and 2, in any given year are represented by the random variables and respectively. Let be a random variable representing the size of aggregate loss events in a given year, and as the amount of business written which can be affected by loss events differs between syndicates, define two more variables and which represent the amount of affected business underwritten in the two loss functions, 1 and 2, respectively. Then we assume that as well as

Lastly, as a companies write business before loss events happen, we assume is independent of and , and further for simplicity we also assume is independent of .

To construct for such that; and is proportional to and , which are independent, we use the Feller-Pareto construction (Theorem 2.13). Since the shape parameter () differs between loss functions we take (in the Theorem) and . Our Two-component model is summarised as follows;

Two-component model summary

Let represent the size of the loss events that occurs in a given year and , where , represent the level of underwritten business that can affect the loss function in a given year, for . Suppose that , and are independent. Define

| (3.1) | |||

| (3.2) |

where . Then, and models the loss functions , for .

The assumption that has an inverse-gamma distribution is plausible as it leads to an arc shaped hazard function () with limits 0 (as and ) Cox et al. (2007), as used in survival analysis and some mixture models Glen (2011). Arc shaped hazard functions can be justified in this context as the total amount of business available for underwriting is a limited resource. For small , there is plenty of business for underwriting, so its easy for an insurance company to underwrite more, hence increases. For large , due to competition, it is difficult to find new business to underwrite so decreases. The assumption that is exponential is made partly for convenience, but it is plausible to assume that the loss sizes follow a memoryless distribution.

3.2. The Two-component model copula derivation

Now we derive the Two-component (model) copula and some of its properties.

Theorem 3.1.

The copula for the Two-component model is

where and .

Proof.

Let and be defined by equations 3.1 and 3.2 and let be their joint distribution function, then by conditioning on we have for

where the last line follows from the independence of , and . It is straightforward to calculate that for

and hence

Thus,

For or , we have for and

If and ,

Similarly, if and , then for all With as in the statement of the theorem, and with the parameters and from the marginal distributions of and respectively,

| (3.3) |

By Sklar’s theorem (Theorem 2.3), we see that as is continuous with , is the uniquely determined function on such that Equation (3.3) holds, the function is a copula and further, is the copula of the Two-component model random variables defined in (3.1) and (3.2). ∎

Before we discuss the properties of this copula there are three points to mention. Firstly, the only method we know to estimate and is to assume the dataset has Pareto Type II marginal distributions, and to fit these margins. Hence, the use of this copula is limited to when this assumption holds and further, this method increases the error in the GoF test for the copula. Secondly, the copula requires . Lastly, even though the Two-component model variables, and , are dependent on the parameters and , these parameters do not feature in the copula, hence these parameters do not need to be estimated when fitting the copula.

3.3. Properties of the two-component copula

To limit the notation we first look at the copula , which we denote by the function , and use this function to find the behaviour of the Two-component copula using the equations below, which were inferred from (2.2). Let

| (3.4) | ||||

where . So for

Direct verification shows that

| (3.5) |

where is the probability density function (p.d.f.) of and is the Beta function. Using (3.5) and (3.4) it is straight-forward to calculate that if is as defined in 3.4, then such that

| (3.6) | ||||

where is the probability density function of and is the Beta function. Now using Sklar’s theorem, on we know that is equal to the joint density function of two uniform random variables which have copula .

Remark 3.2.

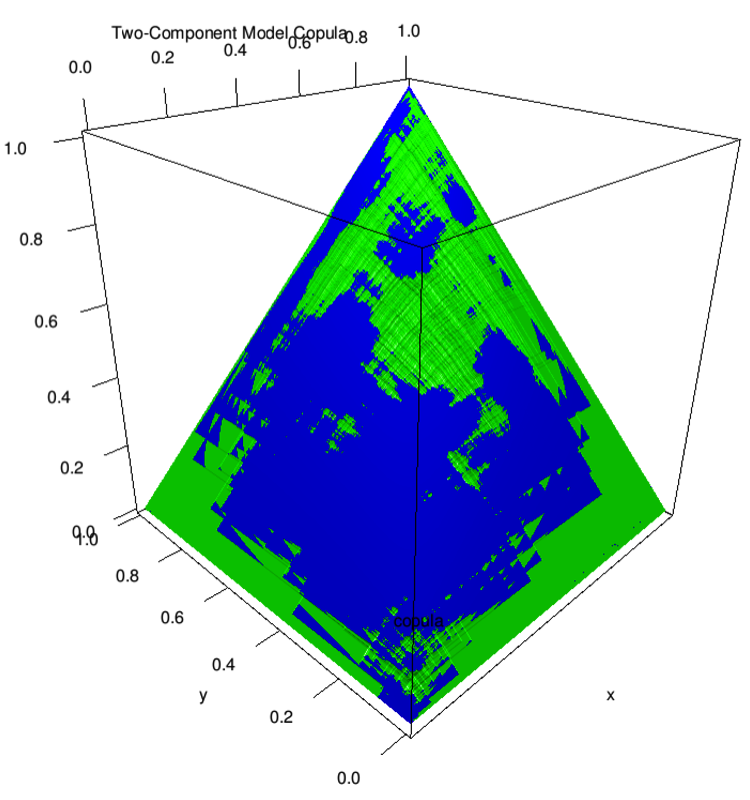

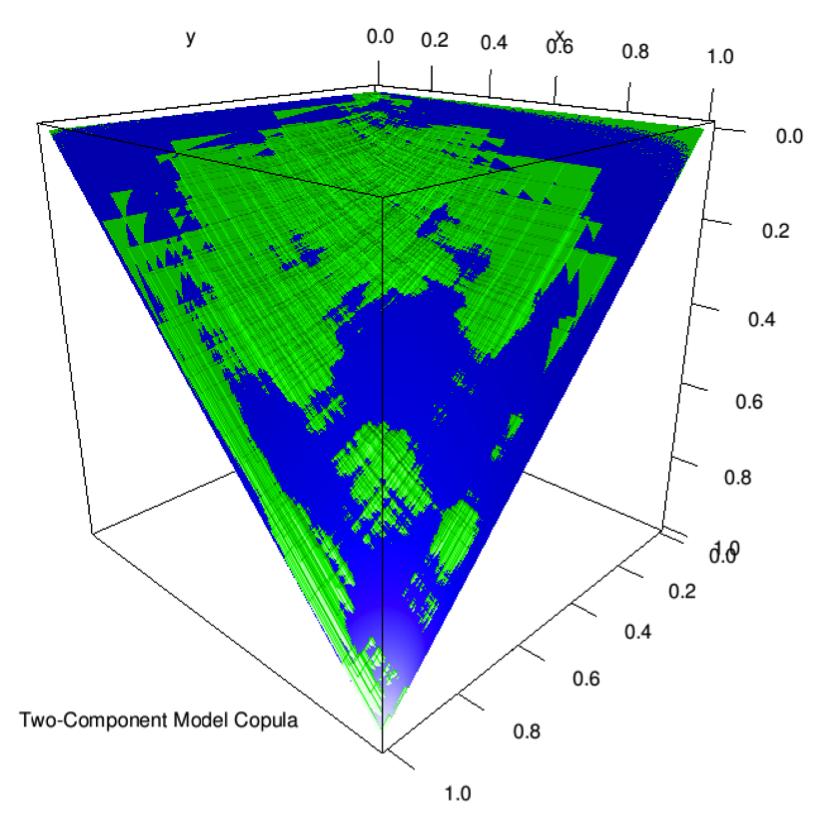

Figures 3.1 and 3.2 show for five different values of namely; , and . There are two plots for each pair; one plot showing the whole graph and the other just showing the part of the graph which falls in the unit cube. The plots illustrate that the more similar and are, the more symmetric the copula; this can be confirmed by looking at Theorem 3.1. Figure 2(d) shows that if is larger than then in the unit cube the density increases more sharply for points where for than for points where for . Comparing the rest of the right-hand figures shows that for larger values of both and the density in the unit cube rises more steeply on both sides of the line . These observations are evidence that the increase in as the line is approached is affected by both and , with steepness increasing on both sides of the line as , or both increase.

Additionally, looking at all the plots it is seen that increases as we approach the the line . Looking at Equation (2.1) this shows that and are more likely to take values where .

Lastly, the figures show that for low and the density clearly differs on the line , with events with u and v being low/high being more likely than events with u and v close to 0.5. This is not seen when where the density is more evenly spread on the line , with all the values in this region having a higher density when compared to the rest of the plane.

3.4. Upper tail dependency

Direct verification shows that the upper tail dependence of (as defined in Theorem 3.1) is

| (3.7) | ||||

In particular, if or if , we have .

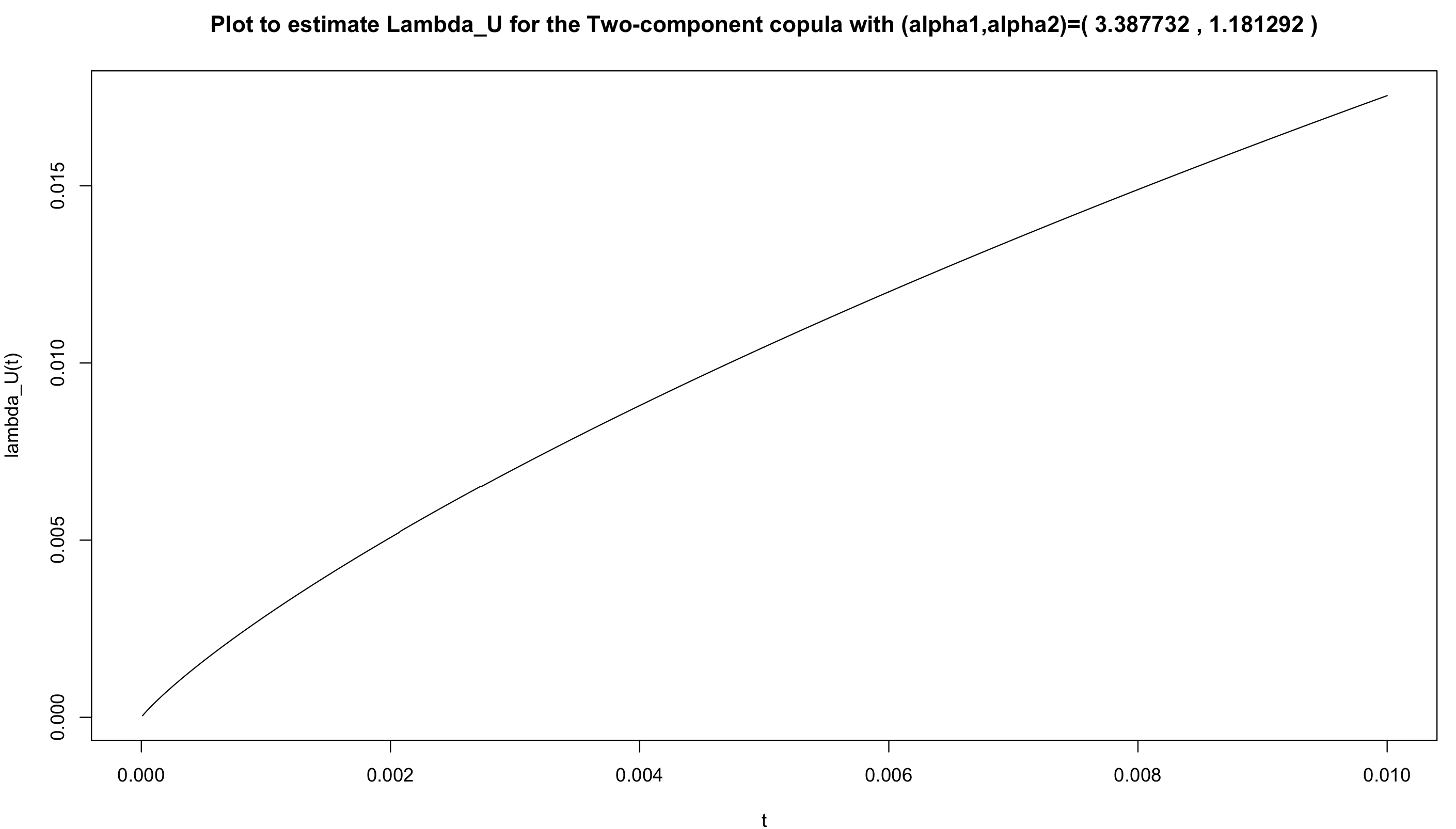

A simple expression for when was not found, so it is estimated by plotting the function (Equation (3.7) without the limit), for the given and , in a range close to 0 and looking at the behaviour of the graph. These plots will not be mentioned again when the estimated values are given, but they can be found in Appendix B.

3.5. Comparisons to other copulas

Tthe Two-component copula is not a Gaussian or Archimedean copula as it does not have the symmetry property if and have different parameters. Further, this copula is not an Extreme-value copula as it does not fit the form given in 2.9.

However, while our copula is new to our knowledge, it has a resemblance to the Clayton copula. The Clayton copula is an Archimedean copula with generator , where to enforce , , see Schmidt (2007).

Proposition 3.3.

If and are generated by

where and are independent with and , then U and V have a Clayton copula with parameter .

Proof.

Schmidt (2007) gives that if and are independent with and , then

have a Clayton copula with parameter . Now,

Hence and are i.i.d. Exp(1) as required. ∎

Proposition 3.4.

If U and V are given by

where and are independent with and , then U and V have the Two-component model copula which is given in Theorem 3.1, with parameters and .

Proof.

Define and as in equations (3.1) and (3.2), then and have a Two-component copula with parameters and . Define

Then in distribution,

where , and are independent with and . Further, and take values on [0,1) as . Now, as and are strictly increasing transformations of and , and have a Two-component copula with parameters and by (2.3). Define and , then again, by (2.3), and are strictly increasing transformations of , , so and also have a Two-component copula with parameters and . ∎

Hence in the Two-component copula the Exponential distribution is fixed and the Gamma distribution and parameter varies between and , while in the Clayton copula the Exponential distribution varies and the Gamma distribution and parameter are fixed between and .

3.6. Goodness-of-fit testing on simulated data

Tosee how well our goodness-of-fit tests preform on data simulated from the Two-component model, we first simulate 1000 i.i.d. observations of from (3.1) and (3.2). We assume that loss function 1 has the larger propensity for loss, and normalise both loss function’s scale parameters according to loss functions 1’s scale parameter; hence we choose . For simplicity we assume loss function 2’s propensity for loss is in the ratio of 9:10 when compared to loss function 1; hence . As copulas are invariant under monotone increasing transformations of random variables, this simplification does not affect any of our copula fits or GoF tests. Moreover from our assumptions we have lies in . As we do not have any other assumptions regarding this parameter we pick its value uniformly in the interval ; for the same reason we pick uniformly in the interval as well.

Then we fit the best Gaussian, Gumbel and Two-component copulas to the data and perform a goodness-of-fit test in each case, as well as the more general goodness-of-fit test, which tests whether the data comes from an Extreme-value copula, as discussed in Section 2. For the Two-component copula the parameters are estimated by the maximum likelihood estimated shape parameters of the marginal GPDs of and . We then apply the tests from Section 2. As we carry out GoF tests we apply the generalised Benjamini-Hochberg procedure (Theorem Benjamini and Yekutieli (2001)): for a test at level we reject the hypothesis () if .

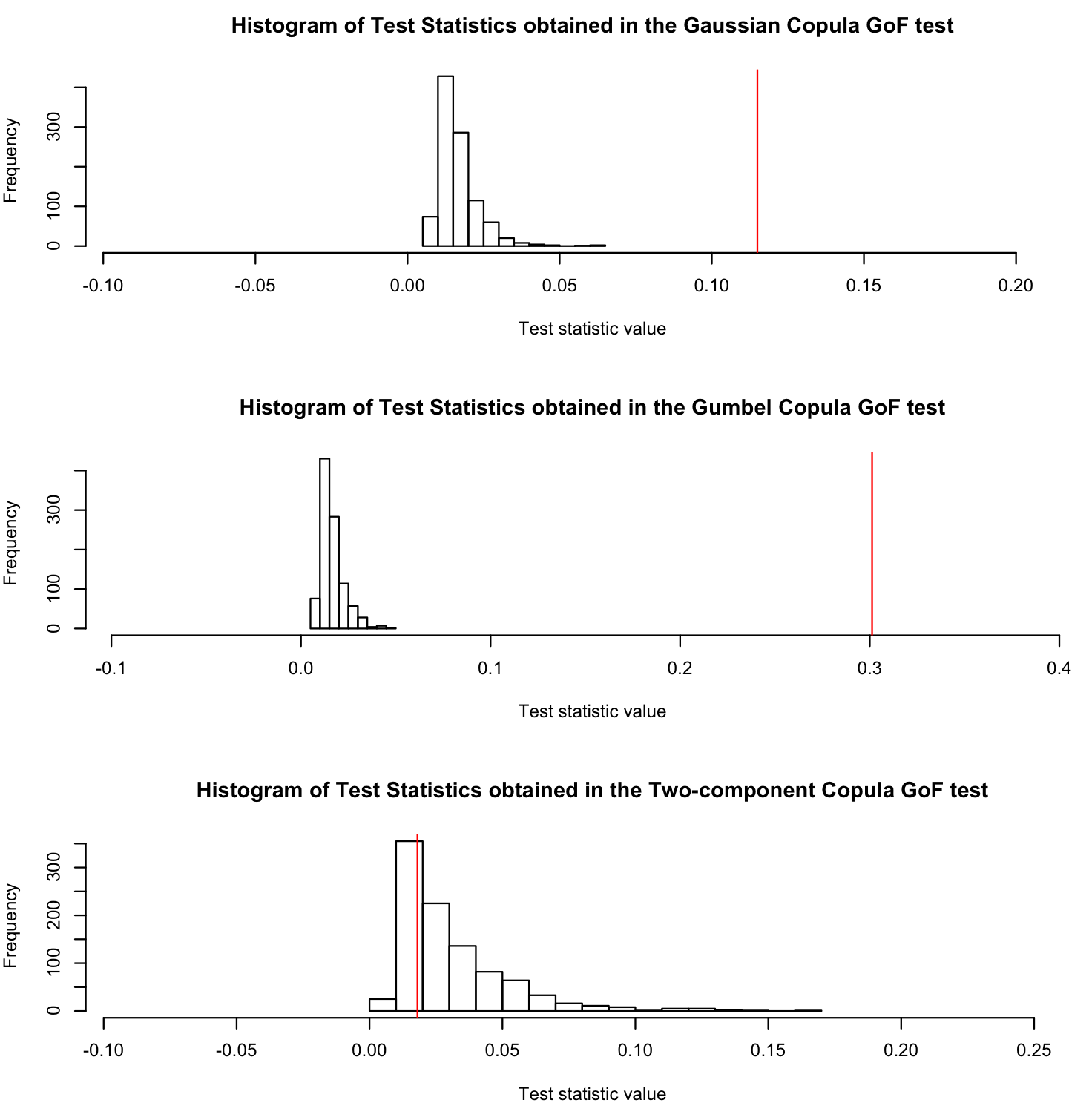

Table 3.1 shows that the Gaussian, Gumbel and Extreme-value copula tests provided statistically significant -values at the 5% significance level.

| Fitted model parameters (3 s.f.) | |

|---|---|

| Gaussian | 0.645 |

| Gumbel | 1.81 |

| Two-component | (3.05,1.18) |

| Estimated (3 s.f.) | |

| Gaussian | 0 |

| Gumbel | 0.533 |

| Two-component | 0 |

| -values for GoF (3 s.f.) | |

| Gaussian | 0 |

| Gumbel | 0 |

| Two-component (-value, valid iterations) | (0.689,1000) |

| Extreme-value copula | |

There is evidence to reject the hypotheses that the dataset has a Gaussian, Gumbel or Extreme-value copula. Since the data did come from a Two-component copula, this result suggests that the Two-component copula is very different to both the Gaussian and Gumbel copulas and illustrates that is not an Extreme-value copula. This result for the Gaussian and Gumbel copula is emphasised in Figure A.4 in Appendix A, which shows that the observed test statistics for the Gaussian and Gumbel tests fell in the extreme tail of the bootstrap simulated distribution of the test statistic under the respected null hypotheses (see Step 5 in Appendix A for the simulation method). The Two-component copula goodness-of-fit test did not provide significant results and the estimated Two-component copula parameters were close to the real values. This is reassuring as we know the dataset is indeed generated from a Two-component copula.

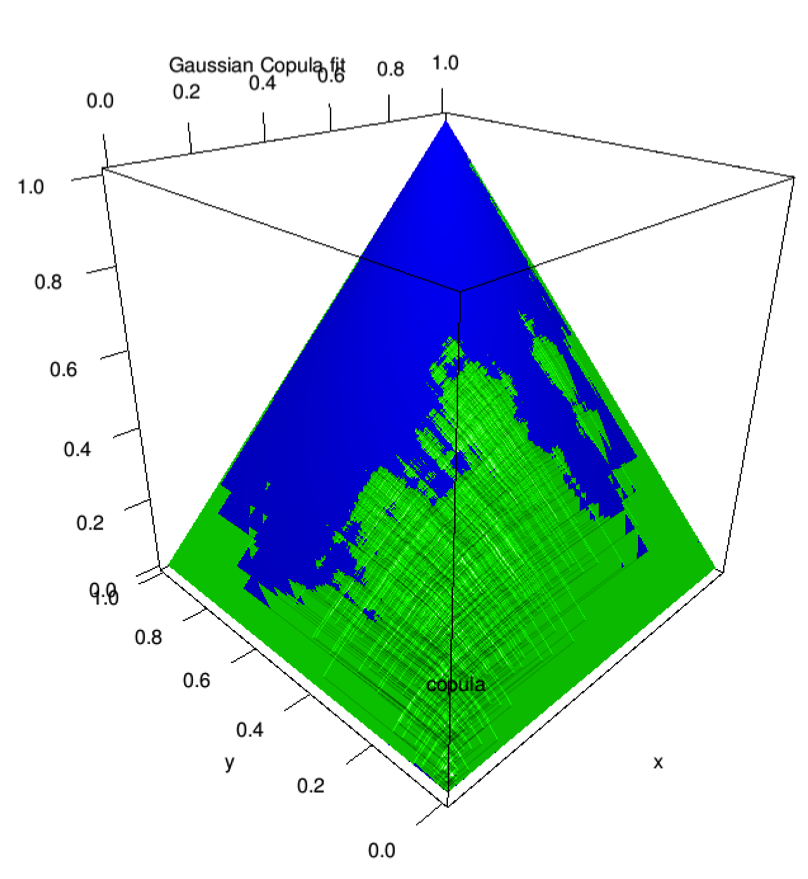

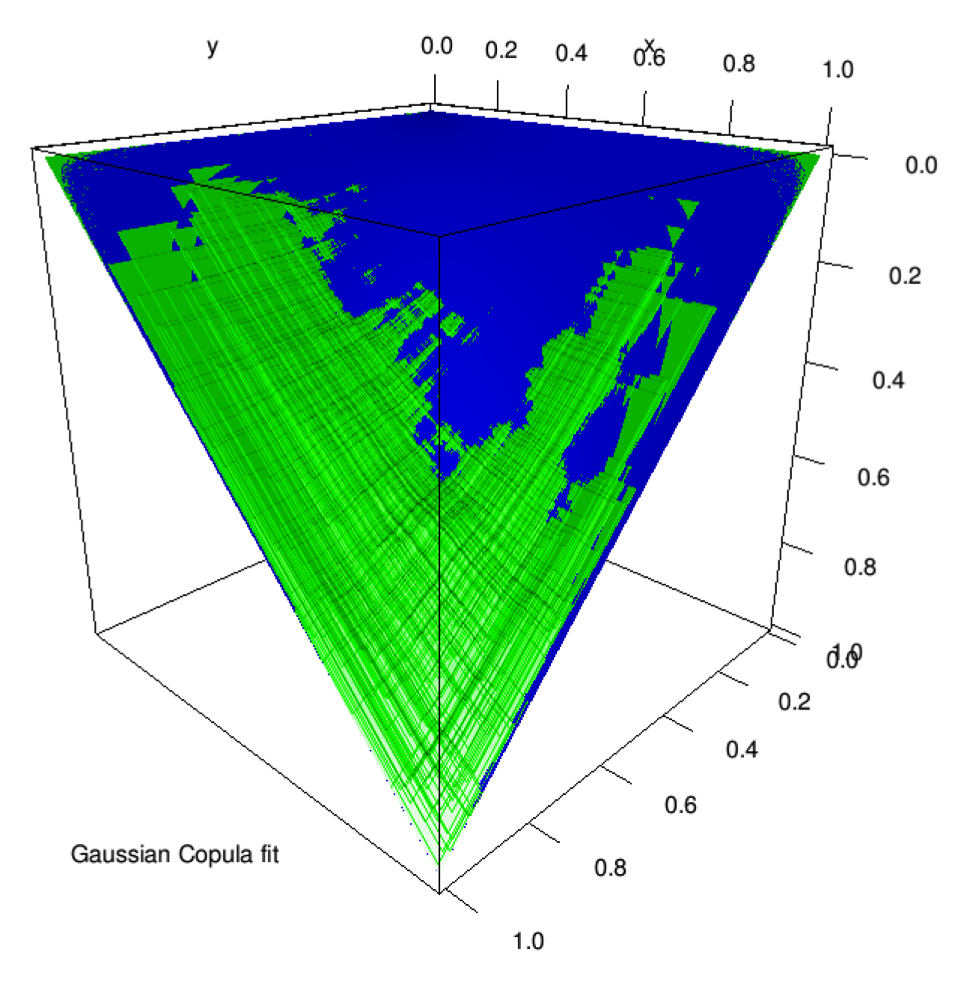

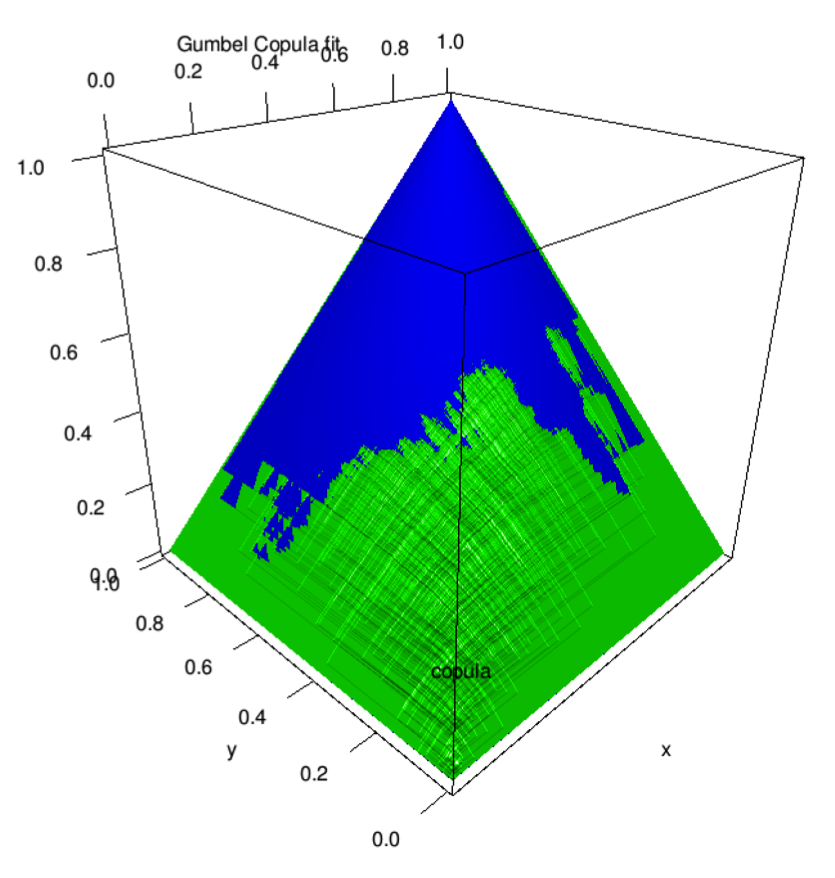

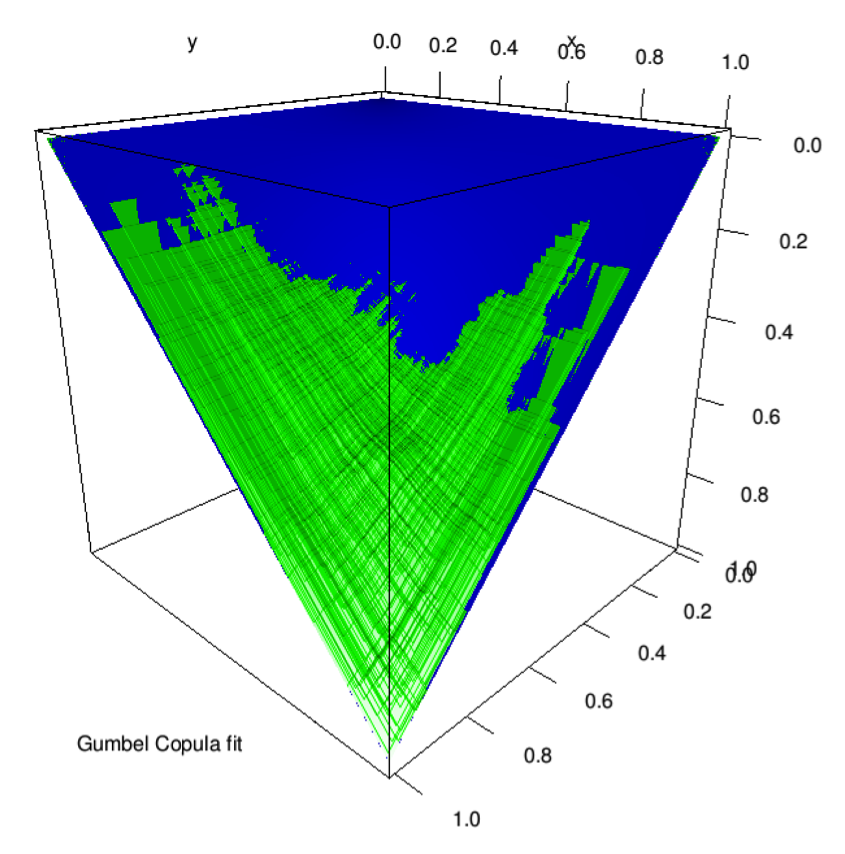

Figure 3.3 shows that the Two-component copula was the best fitting copula of the simulated Two-component model data, as it has the most overlap with the empirical copula while the other copulas show a bias (over-approximate the copula for lower values of and , while under-approximate the copula for higher values of and ).

Thus, the Two-component copula is unlike some of the most commonly used copulas in the insurance field to-date. Consequently, it fills a gap in the literature on copulas for insurance applications.

References

- Ben Ghorbal et al. (2009) N. Ben Ghorbal, C. Genest and J. Nešlehová. On the Ghoudi, Khoudraji, and Rivest test for extreme-value dependence. Canadian Journal of Statistics 37 (4), 534–552 (2009).

- Benjamini and Yekutieli (2001) Y. Benjamini and D. Yekutieli. The Control of the False Discovery Rate in Multiple Testing under Dependency. The Annals of Statistics 29 (4), 1165–1188 (2001).

- Berg (2009) D. Berg. Copula goodness-of-fit testing: an overview and power comparison. The European Journal of Finance 15 (7-8), 675–701 (2009).

- Chotikapanich (2008) D. Chotikapanich. Modeling Income Distributions and Lorenz Curves. Economic Studies in Inequality, Social Exclusion and Well-Being. Springer-Verlag New York (2008).

- Cox et al. (2007) C. Cox, H. Chu, M.F. Schneider and A. Muñoz. Parametric survival analysis and taxonomy of hazard functions for the generalized gamma distribution. Statistics in Medicine 26 (23), 4352–4374 (2007).

- Embrechts et al. (1997) P. Embrechts, C. Klüppelberg and T. Mikosch. Modelling Extremal Events: For Insurance and Finance. Applications of Mathematics, 33. Springer (1997).

- Embrechts et al. (2003) P. Embrechts, F. Lindskog and A. McNeil. Modelling Dependence with Copulas and Applications to Risk Management. In S.T. Rachev, editor, Handbook of Heavy Tailed Distributions in Finance, Handbooks in Finance, pages 329–384. Elsevier Science (2003).

- Foss et al. (2011) S. Foss, D. Korshunov and S. Zachary. An Introduction to Heavy-Tailed and Subexponential Distributions. Springer (2011).

- Genest et al. (2011) C. Genest, I. Kojadinovic, J. Nešlehová and J. Yan. A goodness-of-fit test for bivariate extreme-value copulas. Bernoulli 17 (1), 253–275 (2011).

- Glen (2011) A.G. Glen. On the Inverse Gamma as a Survival Distribution. Journal of Quality Technology 43 (2), 158–166 (2011).

- Gudendorf and Segers (2010) G. Gudendorf and J. Segers. Extreme-Value Copulas. In P. Jaworski, F. Durante, W.K. Härdle and T. Rychlik, editors, Copula Theory and Its Applications, volume 198 of Lecture Notes in Statistics, pages 127–145. Springer Berlin Heidelberg (2010).

- Nelsen (2006) R. B. Nelsen. An Introduction to Copulas. Springer, 2nd edition (2006).

- Schmidt (2007) T. Schmidt. Coping with Copulas. In J Rank, editor, Copulas - From Theory to Applications in Finance, Bloomberg Professional Series, pages 3–34. John Wiley & Sons (2007).

- Weiß (2011) G.N.F. Weiß. On the robustness of goodness-of-fit tests for copulas (2011). Discussion paper 40,2011, SFB 823.

Appendix A Bootstrap method and test results

First we describe the bootstrap method used to obtain a -value in the copula goodness-of-fit test based on the empirical copula. For reference of this method, see section 3.10 of Berg (2009).

-

(1)

Using Equation (2.8), generate the transformed sample () from the sample data ().

-

(2)

Estimate the parameters of the parametric copula, , from the transformed sample, and ensure they satisfy any requirements needed to make the parametric copula valid. If not, no valid parametric copula fits the data and the test fails.

-

(3)

Compute the empirical copula, , using Equation (2.7).

-

(4)

Estimate the test statistic by plugging , and () into Equation (2.9).

-

(5)

For some large integer K, repeat the following steps for every (parametric bootstrap):

-

(i)

Generate a random sample from the null hypothesis copula and using (2.8) calculate the associated transformed sample ().

-

(ii)

Estimate the parameters of the parametric copula, , from the transformed sample (), and ensure they satisfy any requirements needed to make the parametric copula valid. If not pass over this iteration.

- (iii)

-

(i)

-

(6)

Approximate the -value of the test by , where V is the number of valid iterations and the sum only goes over the valid iterations.

In this study, K is chosen to be 1000.

Note. Steps 4 and 5iii only work as there is an analytical expression for each of the copulas. If this was not the case then we would carry out the bootstrap method explained in Berg (2009) to estimate and respectively.

Next we give more details on the results for the comparison with the Gaussian, Gumbel and extreme-value copula. Figure A.4 shows that the observed test statistics for the Gaussian and Gumbel tests fell in the extreme tail of the bootstrap simulated distribution of the test statistic under the respected null hypotheses. It is re-assuring that the simulated values are plausible for a two-component copula, as that is how they were generated.

Appendix B Plots used to estimate for the Two-component copula

This graph was used in Table 3.1 to estimate the upper tail dependence of a Two-component copula with parameters and . The graph was constructed by plotting equation 3.7 (without the limit) for small . If the graph looked to be convergent close to zero, then the upper-tail dependence of the copula was estimated by picking this convergent value. In this case a value of 0 was picked as it can be seen that the curve monotonically decreases towards 0 as decreases, and for small the curve is within 0.001 units of 0.

Appendix C Colour Palette

This colour palette was used to shade the plots in Figures 3.1 and 3.2 to allow the shape of the graph to be seen more clearly. Areas of the graph with larger z-values were shaded using higher ranking colours. The colour palette is the standard rainbow colour palette used in R.