A Fourier interpolation method for numerical solution of FBSDEs: Global convergence, stability, and higher order discretizations 111A previous version of this paper was titled “Global convergence and stability of a convolution method for numerical solution of BSDEs” arXiv:1410.8595v1

Abstract

The convolution method for the numerical solution of forward-backward stochastic differential equations (FBSDEs), introduced in [21], uses a uniform space grid. In this paper we utilize a tree-like spatial discretization that approximates the BSDE on the tree, so that no spatial interpolation procedure is necessary. In addition to suppressing extrapolation error, leading to a globally convergent numerical solution for the FBSDE, we provide explicit convergence rates. On this alternative grid the conditional expectations involved in the time discretization of the BSDE are computed using Fourier analysis and the fast Fourier transform (FFT) algorithm. The method is then extended to higher-order time discretizations of FBSDEs. Numerical results demonstrating convergence are presented using a commodity price model, incorporating seasonality, and forward prices.

Keywords: Forward-backward stochastic differential equations; numerical solutions; fast Fourier transform

Mathematics Subject Classification (2000): Primary: 60H10, 65C30; Secondary: 60H30

1 Introduction

A variety of numerical methods for backward stochastic differential equations (BSDEs) and forward-backward stochastic differential equations (FBSDEs) have been developed recently. Different applications call for innovative techniques for the efficient resolution of these systems. In finance and economics BSDEs are used for option pricing and hedging [17], reflected BSDEs are used for modeling American options [16], and quadratic BSDEs play an important role in continuous-time recursive utility [15] and other utility maximization problems.

Following the establishment of the well-posedness of BSDEs by [27] the first numerical procedures to emerge were partial differential equation (PDE) based methods such as the finite difference approach of [14]. The PDE method is mainly devoted to coupled problems as is the spectral method of [25]. More recent numerical methods based on machine learning [3, 35, 33, 34, 19] have been applied to the numerical solution of BSDEs which, given the connections between the theory of PDE and their represeantations as BSDEs, in turn provides solutions to high dimensional PDEs. Spatial discretization methods were initiated by [9] with a quantization approach to conditional expectations. However, it is only since [36] and [6] that a sound time discretization of (decoupled) FBSDEs is available. The quantization approach was then used in the multidimensional framework of [1, 2] and the coupled FBSDE case of [13]. The theoretical basis for a multinomial approach for BSDEs was introduced by [7] and [24] and followed in practice by [28]. Monte Carlo methods are the most prolific approach for numerical solutions of (F)BSDEs. They include the backward scheme of [36], the Malliavin approach of [6] and [12], the least-square regression approach of [18] and the iterative schemes [4] and [5].

Additional approachs to numerical solution of BSDEs include, include the cubature method [10, 11], Fourier-cosine expansions [29, 20, 30], and the convolution method [21]. In introducing the convolution method, [21] developed a local discretization error which includes an extrapolation error. The extrapolation error component is exclusively produced by the fast Fourier transform (FFT) algorithm and the underlying trigonometric interpolation used to compute conditional expectations. To improve the performance of the convolution method it is desirable to eliminate the extrapolation error, and improve the error bound, with an alternative implementation of the FFT algorithm.

In this paper we propose an alternative space grid for the convolution method, instead of the rectangular grid in [21], which eliminates the extrapolation error, leads to a globally convergent numerical solution for the (F)BSDE, and provides explicit convergence rates. We also apply the numerical method to the Runge-Kutta schemes for FBSDEs proposed by [8]. The tree-like nature of the alternative grid avoids extrapolations and leads to a global error bound for the BSDE approximate solutions. Further, the implementation of the convolution method originally presented in [21] is simplified by using an alternative parametric transformation to enforce the necessary periodic boundary conditions.

The paper is organized as follows. Section 2 reviews the explicit Euler time discretization of BSDEs, recalls the convolution method of [21] for computing the necessary conditional expectations, gives a description of an alternative spatial discretization, and provides a generic implementation of the convolution method on this grid using the discrete Fourier transform. The section ends with a global error analysis. Section 3 extends the Fourier interpolation method to higher order time discretizations of FBSDEs and includes the related global error analysis. Finally, Section 4 presents a numerical implementation, in the context of a commodity price model, that illustrate the theoretical results. Section 5 concludes.

2 The Fourier interpolation method

In this section, we introduce an alternative grid that remove extrapolation error of [21], after a quick presentation of the Euler scheme for FBSDEs. Section 2.4 presents a global error analysis of the Fourier interpolation method on this alternative grid and under the Euler scheme.

2.1 Time Discretization

Let be a complete filtered probability space generated by a dimensional Wiener process . We seek a numerical solution to the FBSDE

| (2.1) |

The forward drift , the forward volatility , the driver are deterministic functions. The initial condition and the terminal condition take the Markovian form where . The FBSDE coefficients satisfy Assumption 2.1 so that existence and uniqueness of the FBSDE solution is assured.

Assumption 2.1.

There exist positive constants , , and such that the coefficients of the FBSDE (2.1) satisfy

| (2.2) | ||||

| (2.3) | ||||

| (2.4) | ||||

| (2.5) | ||||

| (2.6) |

for any , , , .

Moreover is (uniformly) invertible, continuous and bounded

| (2.7) |

for any , .

In addition, the terminal value is square integrable

| (2.8) |

Remark 2.1.

Assumption 2.1 makes no explicit assumption on except square integrability. More restrictive assumptions on , namely that is twice continuously differentiable, shall be specified in the main results of Section 2 and 3 which provide explicit rates of convergence for the Fourier interpolation algorithms. However, similar to [10], see also [31], it should be possible to consider non-differentiable using a mollification argument on the terminal condition.444This approach was suggested by an anonymous referee of an earlier version of this paper. However, we shall not follow this approach in this paper so as to keep the focus on the main contributions which are the overall approach, implementation of the convolution method on the tree-like grid, developing the Runge-Kutta discretization schemes, and explicit convergence rates.

The time discretization of the FBSDE (2.1) on the time partition consists of the explicit Euler scheme given by

| (2.9) |

with and . Under an additional Lipschitz condition on the function we have, from [36] and [6], that the quadratic discretization error

| (2.10) |

is of first-order in time, i.e

| (2.11) |

where

| (2.12) |

Following [21] and [26], the approximate solution and the approximate gradient at time node , , are given by

| (2.13) | ||||

| (2.14) |

where the intermediate solution is given by

| (2.15) |

and is a Gaussian density

| (2.16) |

and where with characteristic function

| (2.17) |

Let and denote the Fourier transform operator and the inverse Fourier transform operator respectively,

| (2.18) | ||||

| (2.19) |

Using the relationships between the characteristic function and the density function leads to the representation

| (2.20) | ||||

| (2.21) |

for equations (2.14) and (2.15) under integrability condition on the approximate solution . In the sequel, we restrict the analysis to the one-dimensional case with .

2.2 Space discretization

The space discretization is performed on a tree-like grid using three parameters: the increment length , the even number of space steps on the increment length, and the initial number of increment intervals. Hence, the space step is constant and uniform on the grid

| (2.22) |

At the time node , , the space domain is restricted on an interval of length centred at and discretized uniformly with space steps where

| (2.23) |

giving the nodes

| (2.24) |

In particular, the relation

| (2.25) |

holds since the restricted interval at each time node is obtained by evenly increasing the previous one with an interval of length . If then the space grid at mesh time is compose by the single point

| (2.26) |

Figure 1 gives examples of alternative grids.

The convolution relations of equations (2.20) and (2.21) call for a discretization of the Fourier space as well. At each mesh time , , the Fourier space is restricted on an interval of length centred at zero and discretized with space steps. The equidistant nodes are thus of the form

| (2.27) |

where . The Nyquist relation555The minimum sampling rate to avoid aliasing. holds whenever is such that

| (2.28) |

2.3 Implementation

In order to compute numerical approximations of equations (2.20) and (2.21) at time node , , we introduce the generic functions , and such that

| (2.29) |

We assume that the function satisfies the periodicity boundary value equalities of Assumption 2.2.

Assumption 2.2.

The generic function satisfies

| (2.30) | ||||

| (2.31) |

Hence, the Fourier integral

| (2.32) |

is restricted on the interval and discretized using the grid points with a quadrature rule with weights . As to the inverse Fourier integral of equation (2.29) we restrict it on the interval and discretize it with lower Riemann sums at the Fourier space grid point .

Let and denote the discrete Fourier transform and the inverse discrete Fourier transform respectively

| (2.33) | ||||

| (2.34) |

Then the discretization procedure leads to the approximation

| (2.35) |

where

| (2.36) |

and the weights are given by

| (2.37) |

where stands for the Kronecker delta. The relation of equation (2.25) allows us to write

| (2.38) |

for .

In equation (2.38), the generic function depends on the space node . If the relation generalizes for all space nodes , , the function values , , can not be computed with a single direct FFT procedure. Instead, a separate FFT procedure using the values of the generic function at is needed to compute the function value . Nonetheless, the vector-matrix representation of the FFT procedure in equation (2.38) allows the computation of all function values with a matrix multiplication. In the vector-matrix representation, equation (2.38) is

where is the th row of the dimension inverse FFT matrix and is the dimension diagonal matrix built with the values . Let be the dimension vector of the function values such that

| (2.39) |

for . The matrix representation gives

| (2.40) |

where is the matrix such that

| (2.41) |

with , and .

The requirements of Assumption 2.2 can easily be satisfied. Given a function and , if we consider the transformation

| (2.42) |

then the parameters and can be chosen such that the transform function and its derivative have equal values at the boundaries of any interval. The following lemma gives a method to select the coefficients and for the transform of equation (2.42) such that Assumption 2.2 holds in general.

Lemma 2.1.

Suppose the real function is differentiable and let be its transformed function as defined in equation (2.42). Then

| (2.43) | ||||

| (2.44) |

solve the system of linear equations defined by

| (2.45) |

Proof.

Hence, the numerical discretization may be applied on the transformation at time node but a correction must be performed so to recover the values of the intermediate solution and the approximate gradient . The next theorem gives the representation under the transform of equation (2.42).

Theorem 2.1.

Proof.

Algorithm 2.1 details the numerical procedure on the space grid and produces numerical solutions , and for the approximate solution , the intermediate solution and the approximate gradient respectively, . We next consider error estimates under the alternative discretization.

Algorithm 2.1.

Fourier Interpolation Method on Alternative Grid

-

1.

Discretize the restricted real space and the restricted Fourier space with space steps so to have the real space nodes and

-

2.

Value

-

3.

For any from to

- (a)

- (b)

- (c)

- (d)

-

(e)

Update the real space grid with equation (2.25) and the Fourier space grid by discretizing the interval with space steps so to have the real space nodes and .

2.4 Spatial discretization error analysis

Let , and denote the numerical solutions obtained from the convolution method at time node given the solution at time . For the Fourier interpolation method on the alternative grid, we defined the local discretization error as

| (2.54) |

for and .

Theorem 2.2.

Suppose that the driver is , the terminal condition is , and Assumption 2.1 is satisfied. Then the convolution method yields a local discretization error of the form

| (2.55) |

for some constant on the alternative grid and under the trapezoidal quadrature rule with weights

Proof.

We suppose the solution at time is known. The solution is twice differentiable since and . Also, is square integrable with respect to the Gaussian density.

By Theorem 2.1, we limit ourselves to the case where

so that the coefficients of the transform are . Let be the Fourier polynomial interpolating on . Then

| (2.56) | ||||

| (2.57) |

where

| (2.58) |

when using the trapezoidal quadrature rule. We have that

where

for some constant which is inversely proportional to by Cauchy-Schwarz and Chernoff inequalities since the solution is square integrable. Hence

| (by equation 2.57) | |||

| (by Chernoff inequality, since is bounded) | |||

| (by equation 2.58 when using the trapezoidal quadrature rule) | |||

Similar techniques show that

| (2.59) |

where is inversely proportional to . The Lipschitz property of the driver completes the proof. ∎

As expected, the alternative discretization improves the local error bound by eliminating extrapolation errors in [21]. The result of Theorem 2.2 establishes the consistency of the convolution method with respect to the approximate functions and gradients . Furthermore, the absence of extrapolation errors in the local discretization allows us to develop a tighter bound for the global discretization error. The following corollary proves helpful when deriving the global discretization error bound.

Corollary 2.1.

Under the conditions of Theorem 2.2, there is such that

| (2.60) |

We define the global error as

| (2.61) |

where

| (2.62) | ||||

| (2.63) |

for with . The next theorem describes the stability and convergence properties of the convolution method.

Theorem 2.3.

Proof.

Let’s first notice that

| (2.66) |

where is the Lipschitz constant of the driver . Also, we have that

| (2.67) |

Furthermore, the construction of the Fourier interpolation method gives

| (2.68) |

where the last inequality holds by Assumption 2.1. Similarly,

| (2.69) |

The inequalities of equations (2.66), (2.68) and (2.69) lead to

where and is the Lipschitz constant of the driver . Consequently,

| (2.70) |

since

and the Gronwall’s Lemma yields

| (2.71) |

from the inequality of equation (2.70) for knowing that . The last equation establishes the stability of the Fourier interpolation method for the approximate solution since its error at any time step is absolutely bounded.

The inequalities of equations (2.67), (2.69) and (2.71) lead to

| (2.72) |

for a positive constant . Hence, the convolution method is also stable for the approximate gradient . The result of equation (2.65) follows by taking the supremum on the left hand sides of equations (2.71) and (2.72) other time steps and applying Corollary 2.1.

∎

As for most explicit methods for PDEs, the convolution method requires a stability condition as described in equation (2.64). In general, Theorem 2.3 shows that the convolution method converges when the space discretization is relatively as fine as the time discretization. Other numerical methods for BSDEs, and particularly Monte Carlo based methods, have a stability and convergence condition. Indeed, error explosion occurs for fine time discretizations in the backward methods of [18] and [6]. In order to maintain stability and convergence, the space discretization has to be refined by increasing the number of simulated paths.

3 Higher order time discretization for FBSDEs

In this section, we discuss further extensions of the Fourier interpolation method on the alternative grid. In particular, we apply the Fourier interpolation method to Runge-Kutta schemes for FBSDEs proposed by [8].

3.1 Runge-Kutta schemes

The FBSDE of equation (2.1) is discretized on the time partition . Let , we consider the -stage Runge-Kutta scheme giving the following numerical solution at mesh time

| (3.1) | ||||

| (3.2) |

for a set positive coefficients such that . The intermediate solutions take the form

| (3.4) |

where

| (3.5) |

with , and terminal condition

| (3.6) |

The coefficients , , and are all positive and satisfy

| (3.7) | ||||

| (3.8) | ||||

| (3.9) |

Let denote the set of continuous and bounded functions on such that

| (3.10) |

The stochastic coefficient with and is defined as

| (3.11) |

with for some .

The global error of the stage Runge-Kutta scheme is defined as

| (3.12) |

and is hence weaker than the error considered for the Euler scheme. Nonetheless, the global error is easier to handle since it is strongly related to the local time discretization error which simplifies the theoretical study in [8].

The scheme can be represented by the following tableau

| … | … | ||||||||

| … | … | ||||||||

| … | … | ||||||||

| … | … |

One can observe that if and , , then the -stage Runge-Kutta scheme is explicit. Otherwise, the scheme is implicit. For instance, the Runge-Kutta schemes with tableau

and the scheme with tableau

known as the Crank-Nicolson scheme constitute stage implicit Runge-Kutta schemes. The only stage explicit Runge-Kutta scheme admits the tableau

In [8] the implicit and the explicit stage Runge-Kutta schemes are shown to be at least one-half order convergent. The Crank-Nicolson scheme, already studied in [11], presents a first-order of convergence. Notice that the Euler schemes used in the previous chapters are not stage Runge-Kutta schemes since they do not lead to any consistent tableau. Nonetheless, their structure is equivalent to the explicit stage Runge-Kutta scheme and both schemes display the same half order of convergence. The following tableau gives a example of explicit -stage Runge-Kutta schemes of first-order of convergence for and .

3.2 Further simplification

From the -stage Runge-Kutta scheme for BSDEs, one notices that we have at least conditional expectations to compute at each time step. These conditional expectations can be simplified and made more suitable for numerical implementation if we consider a reasonable time discretization of the forward SDE. Hence, we make the following assumption.

Assumption 3.1 (Forward process discretization).

The following are assumed throughout this section.

-

1.

The forward SDE is discretized with the piecewise constant process such that for we have pathwise.

-

2.

The forward SDE time discretization with global error is of order i.e

(3.13) -

3.

The forward SDE time discretization admits the conditional characteristic functions

(3.14) and

(3.15) for and with .

-

4.

There are positive constants , , , and such that

(3.16) , hence the discrete version of the forward process has conditional exponential moments. In addition,

(3.17)

Itô-Taylor expansion based schemes are an example of SDE discretization satisfying the conditions of Assumption 3.1. A more complete presentation of these schemes can be found in [22]. The next theorem gives a simplification of the BSDE time discretization expressions.

Theorem 3.1.

Under Assumption 3.1 (1), the solution of the -stage Runge-Kutta scheme satisfies

| (3.18) |

for . Consequently, we can write

| (3.19) | ||||

| (3.20) |

for and where , and .

Proof.

As a consequence of Assumption 3.1, if the stage Runge-Kutta scheme and the forward SDE time discretization are of order then error of the FBSDE numerical solution defined as is of order . We must hence choose the Runge-Kutta scheme and the SDE scheme accordingly.

3.3 Fourier representation

Following Theorem 3.1, the intermediate solutions at mesh time , , are given by

| (3.22) | ||||

| (3.23) |

for with , and . The approximate solution and approximate gradient at mesh time , , are then

| (3.24) | |||

| (3.25) |

with

| (3.26) |

and

| (3.27) | ||||

| (3.28) |

In this setting, we have that

| (3.29) |

Note that

| (using Fubini’s theorem) | |||

| (3.30) |

Therefore, by (3.29) and (3.29), we have

| (3.31) |

whenever is Lebesgue integrable.

As to the intermediate solutions , and , we have

| (3.32) |

for an integrable function .

Even if the expressions in equations (3.31) and (3.32) appear too general, they are implementable with the Fourier interpolation method for in various particular cases. One can retrieve the characteristics and and also perform the corrections due to the transform of equation (2.42) for many SDE time discretizations. The following lemma helps in retrieving the conditional characteristics.

Lemma 3.1.

The conditional characteristics write

| (3.33) |

with

| (3.34) |

where is the Malliavin derivative of given

Proof.

The lemma is proved by applying the duality formula and the chain rule successively to equation (3.15). ∎

3.3.1 Half-order Itô-Taylor schemes

The Euler scheme constitutes the main example of half-order Itô-Taylor scheme with step

In addition, we have that and for where and are the zero matrix and the identity matrix respectively. Hence,

so we get, from equation (3.33), that

| (3.35) |

The conditional characteristic function is explicitly given by

| (3.36) |

since the increment has a Gaussian distribution.

Equations (3.31) and (3.32) along with the characteristics of equations (3.36) and (3.35) define the Fourier method under half-order Itô-Taylor schemes and the method is implementable in one dimension () with the procedure given in section 2.3. The following theorem generalizes the result of Theorem 2.1 to Runge-Kutta schemes under half-order Itô-Taylor schemes.

3.3.2 First-order Itô-Taylor schemes

Consider the first-order scheme

Then knowing that

| (3.39) |

using the fundamental theorem of calculus where is the diagonal matrix composed with the elements of , for , the Malliavin derivative of the discretized forward process is given by

| (3.40) |

Equation (3.33) leads to

| (3.41) |

since

using the duality formula, so that

with

| (3.42) |

As to the conditional characteristic , it can be easily derived as

| (3.43) |

where

knowing that , given , is an affine function of a multivariate non-central random variable with degree of freedom and non-centrality parameters .

Equations (3.31) and (3.32) along with the expressions in equations (3.41) and (3.43) characterize the method under first order discretizations on the forward process. The procedure introduced in Section 2.3 allows us to do the necessary computations given the characteristics and and using the following theorem.

Theorem 3.3.

Proof.

By the definition of the alternative transform, we must have that

| (3.46) |

Notice that

| (3.47) |

and

| (3.48) |

Equations (3.46), (3.47) and (3.48) lead to the expression for in equation (3.44).

The definition of the alternative transform also requires

| (3.49) |

using the duality formula once again. ∎

The implementation of higher order time discretization for FBSDEs on the alternative grid is described in the following algorithm. Algorithm 3.1 produces the numerical intermediate solutions , and at time step , and stage , for the approximate solution , the intermediate solution and the approximate gradient respectively, .

Algorithm 3.1.

Fourier Interpolation Method on Alternative Grid for -stage Runge-Kutta schemes

-

1.

Discretize the restricted real space and the restricted Fourier space with space steps so to have the real space nodes and

-

2.

Value

-

3.

For any from to

-

(a)

For any j,

- i.

-

ii.

Compute through equation (2.38) for with

(3.51) and retrieve the values with the appropriate correction.

- iii.

-

iv.

Compute through equation (2.38) for with

(3.53) and retrieve the values with the appropriate correction.

- v.

-

vi.

Update the real space grid with equation (2.25) and the Fourier space grid by discretizing the interval with space steps so to have the real space nodes and .

-

(b)

Set and

-

(a)

3.4 Spatial discretization error analysis

We denote by and the intermediate numerical solutions obtained at time step , and stage , , from the Fourier interpolation method on the alternative grid when using a stage Runge-Kutta scheme. In addition, and are the intermediate numerical solutions obtained at the intermediate stage , , of time step given the exact solutions and at . We have from the notation previously used that the numerical solutions at write

| (3.55) | ||||

| (3.56) |

and are computed from the intermediate solutions , where . When the exact solutions and are known at , we also write

| (3.57) | ||||

| (3.58) |

The local (space) discretization error has the form

| (3.59) |

for and . The next theorem gives a description of the local (space) discretization error bound.

Theorem 3.4.

Suppose that the driver and the terminal condition and Assumptions 2.1 and 3.1 are satisfied, then the Fourier interpolation method yields a local space discretization error of the form

| (3.60) |

for some constant on the alternative grid and under the trapezoidal quadrature rule for any explicit -stage Runge-Kutta scheme.

Proof.

We follow the steps in the proof of Theorem 2.2. The truncation error when computing the numerical solutions is

| (using Cauchy-Schwarz inequality twice since is sq. int.) | ||||

| (since is of Gaussian distribution) | ||||

| (by Chernoff’s inequality) | ||||

| (by Assumptions 3.1) | ||||

The Fourier interpolation leads to a first-order space discretization error when computing the numerical solutions since the driver and the terminal condition are twice differentiable.

The same statements hold for the numerical solutions using similar arguments. By recursion and using the Lipschitz property of the driver , the statements hold for , . Since the time step and the space node are arbitrary, the space truncation and discretization error bounds hold for any and . ∎

Locally, the truncation error remains spectral. Nonetheless, it is of a unspecified index in this general setting where the conditional characteristic function is itself unspecified. For higher order time discretizations, one can expect since the forward process increment has a heavy tail distribution. Indeed, the Gaussian distribution of forward process increments and the quadratic exponential form of their characteristic functions were the main reason for the spectral convergence of index of the truncation error in Section 2.4. The space discretization error though is unchanged with first-order due to the second-order differentiability of the BSDE coefficients. However, the Fourier interpolation produces a space discretization error with a higher order when the driver and the terminal function have the required smoothness. In general, if and , we can expect a space discretization error of order which is the convergence order of the underlying Fourier interpolation.

We now turn to the global space discretization error defined as in equation (2.61). The next theorem gives its error bound.

Theorem 3.5.

Suppose the conditions of Theorem 3.4 are satisfied. If the discretization is such that

| (3.61) |

then the Fourier interpolation method is stable and yields a global discretization error of the form

| (3.62) |

where for any explicit -stage Runge-Kutta scheme.

Proof.

From the definition of the global space discretization error, we may write

| (3.63) | ||||

| (3.64) |

Assume that the boundary values of the function and the sequence are matched on the alternative grid so that we don’t have to treat the alternative transform. Under an explicit stage Runge-Kutta scheme, we have

| (3.65) |

Similarly, we get

| (using Assumption 3.1) | |||

so that we get

| (3.66) |

recursively for using the Lipschitz property of the driver and the boundedness of the Runge-Kutta coefficients. Equations (3.63) and (3.64) combined with equations (3.66) and (3.65) lead to

where

Gronwall’s Lemma then yields

| (3.67) |

so that the scheme is stable. The result of equation (3.62) follows by taking the supremum on the left hand side of equation (3.67) other time steps and applying Theorem 3.4. ∎

In this general case, the global discretization error maintains the structure of the local discretization error under a stability condition. Equation (3.61) indicates that the space discretization has to be relatively as fine as the time discretization to ensure stability. Hence, stability can always be reached for any time discretization by refining the space discretization. However, the structure of the characteristic functions and determines the relative refinement needed for the space discretization.

4 Numerical Results

We test the convergence properties of the Fourier interpolation method on Runge-Kutta schemes with a problem of commodity derivative pricing under a model proposed by [23]. We shall test the method’s convergence and behaviour on smooth and unbounded FBSDE coefficients.

The commodity spot price is defined by

| (4.1) |

where the deterministic function represents the seasonality component of the commodity and is the price diffusion following an Ornstein-Uhlenbeck process according to the Vašíček [32] model

| (4.2) |

As indicated by [23], the commodity spot price satisfies the stochastic differential equation

| (4.3) |

where

| (4.4) |

We consider the commodity price as our forward process through equation (4.3).

When the risk-free rate and the market price of risk are both constant, the forward (or future) price with maturity at time is given by

| (4.5) |

with

| (4.6) |

where the expectation is taken under the equivalent risk measure . It can be shown that the forward price solves a BSDE with linear driver

| (4.7) |

and terminal condition

| (4.8) |

Options on forward contracts can also be represented in form of BSDEs in this spot price model but we limit our analysis to forward price estimation. From equation (4.5) the control process (or equivalently the forward price delta) is given by

| (4.9) |

The adjustment speed of the diffusion process is and the volatility of the diffusion is set to be . The seasonality component is given by

| (4.10) |

and the initial spot price by

| (4.11) |

where we normalize the real value666The real value can be considered as the production cost (per unit) of the commodity. of the commodity . Also, the maturity of the forward contract is and we suppose a market price of risk of .

The FBSDE is solved on an alternative grid centred at with a uniform time mesh. For a given number of time steps and the initial number of intervals, the length of an increment interval is set as

| (4.12) |

so that the truncated interval at time has length . This restriction keeps the space nodes in the upper half plane knowing that the commodity price is a positive process. Moreover, the number of space steps on an increment interval is .

We numerically solve the BSDE with the explicit stage Runge-Kutta scheme of half-order and an explicit stage Runge-Kutta scheme of first-order. Under the explicit stage scheme, the commodity price is discretized with an Euler scheme whereas a Milstein scheme is used for the forward process under the explicit stage Runge-Kutta scheme. In addition, we use an explicit stage Runge-Kutta scheme with tableau

Under both FBSDE discretizations, we compute two different types of error. The first error evaluates the maximal absolute error of the numerical solution with respect to the true solution

| (4.13) |

where

| (4.14) |

The second error is a simulation error. Given the numerical solution , with simulated paths for the forward process, we compute the numerical solution of the backward processes by linearly interpolating the simulated paths through the BSDE numerical solutions and at each time step . The error can be written as

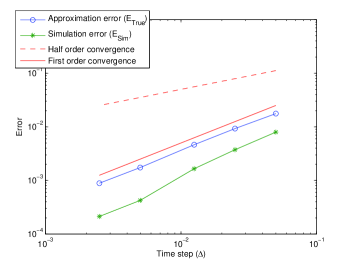

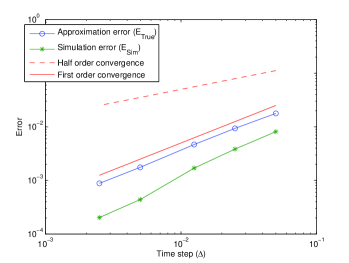

We systematically use paths. Even if the errors and may be of the same order, they are interpreted differently. The error gives the behaviour of the maximal approximation error on the grid whereas gives the behaviour of the error on the relevant part of grid when solving the FBSDE numerically. Figure 2 displays the errors under the explicit stage Runge-Kutta scheme with and Figure 3 shows the errors under the explicit stage scheme.

The sample standard deviation of the error was less than for all time discretizations.

The sample standard deviation of the error was less than for all time discretizations.

The error graphs of Figures 2 and 3 look almost identical and confirm that the stage scheme is of first order and the stage scheme of (at least) half-order. The extra-efficiency of the stage scheme may be attributed in this particular case to the simplicity of the driver and the terminal condition .

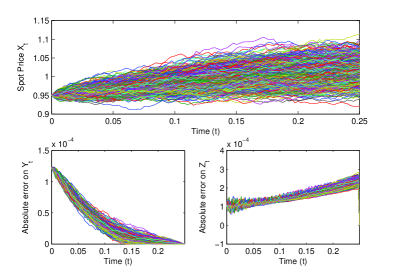

The numerical solution is obtained on a time mesh with time steps and returns an forward price of and initial value of for the control process. The exact values are and respectively.

The numerical solution is obtained on a time mesh with time steps and returns an forward price of and initial value of for the control process. The exact values are and respectively.

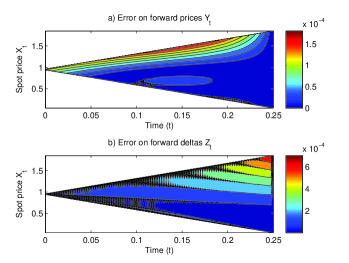

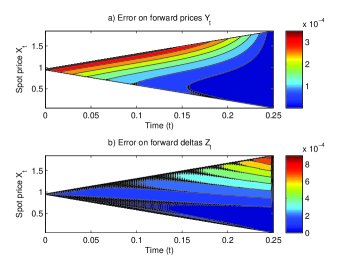

In Figure 4, we present the absolute errors along the simulated paths for the BSDE solution. One notices that the maximal errors occur at the initial time for the forward price () and at maturity for the control process (). Nonetheless, the simulation errors are of the same order () for both processes. This information is confirmed by the contour plot of Figure 5 not only along the simulated paths but on the entire grid.

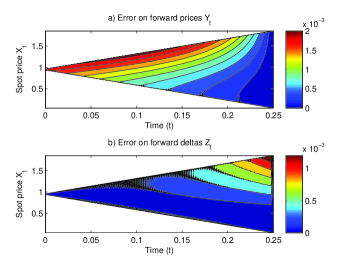

Moreover, the contour plot gives indication on the source of errors. Indeed, Figure 5 shows that the maximal errors mainly occur for the upper space node values on the alternative grid and they decrease for lower space node values. This is due to the unbounded nature of the spot price process coefficients. Since the volatility of the spot price is a positive and increasing function of the spot price777See equation (4.3)., higher spot price values lead to higher local volatility. Hence, the fixed length of increment interval may not be sufficiently large to ensure accuracy for higher space node values. In general, the phenomenon is amplified with the magnitude of the forward process coefficients as illustrated in the contour plot of Figure 6 where we choose a higher value for the volatility and keep the other parameters unchanged. Similar results can be obtained by selecting a higher value for the speed of adjustment as shown in Figure 7 .

The numerical solution is obtained on a time mesh with time steps and returns an forward price of and initial value of for the control process. The exact values are and respectively.

The numerical solution is obtained on a time mesh with time steps and returns an forward price of and initial value of for the control process. The exact values are and respectively.

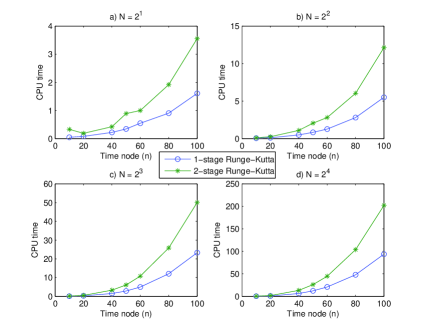

We end this section with an efficiency study of our schemes. Using the parameters initially given, the BSDE is solved on a uniform time grid with time steps and space steps and value the computation time. Figure 8 displays the results. First note that since the Fourier interpolation method performs matrix multiplications, it is much slower than the convolution method of [21].

As shown in Figure 8, the computation time of Fourier interpolation method increases with the number of time steps leading to a trade-off between computation speed and accuracy. The exponential nature of the curves suggests that preference has to be given to the coarsest time discretization providing a satisfactory level of accuracy. Similarly, the computation time also increase drastically with the number of space steps. Coarse space grids insuring accuracy are hence also preferable. Since a total number of conditional expectations are computed under a -stage Runge-Kutta scheme, we can expect the -stage scheme to run twice as fast as the -stage scheme. This is confirmed on Figure 8, especially when looking at the computation times for .

5 Conclusion

In order to solve the problem of extrapolation errors in the initial implementation of the convolution method, we proposed an alternative space discretization. The new tree-like space grid naturally allows the usage of the FFT algorithm when computing the conditional expectation included in the underlying explicit Euler scheme. The error analysis shows that both the alternative grid and the (alternative) transform suit the periodic nature of the FFT algorithm and help in producing a stable, consistent and globally convergent numerical procedure for the FBSDE approximate solutions. The second part of the paper deals with the implementation of the Fourier interpolation method with higher order time discretizations of FBSDEs. When the forward process increments admit conditional characteristic functions satisfying certain regularity conditions, it was shown that the method is also consistent, conditionally stable and globally convergent under Runge-Kutta schemes for FBSDEs. A challenging area of research is the implementation of the methods of this paper in multidimensional and jump cases.

Acknowledgements

This research was supported by the Natural Sciences and Engineering Research Council of Canada (NSERC).

References

- Bally and Pages [2003] V. Bally and G. Pages. A quantization algorithm for solving multidimensional discrete-time optimal stopping problems. Bernoulli, 9(6):1003–1049, 2003.

- Bally et al. [2005] V. Bally, G. Pages, and J. Printems. A quantization tree method for pricing and hedging multidimensional American options. Math. Finance, 15(1):119–168, 2005.

- Beck et al. [2019] C. Beck, E. Weinan, and A. Jentzen. Machine learning approximation algorithms for high-dimensional fully nonlinear partial differential equations and second-order backward stochastic differential equations. Journal of Nonlinear Science, 29(4):1563–1619, 2019.

- Bender and Denk [2007] C. Bender and R. Denk. A forward scheme for backward SDEs. Stochastic Process. Appl., 117(12):1793–1812, 2007.

- Bender and Zhang [2008] C. Bender and J. Zhang. Time discretization and Markovian iteration for coupled FBSDEs. Ann. Appl. Probab., 18(1):143–177, 2008.

- Bouchard and Touzi [2004] B. Bouchard and N. Touzi. Discrete-time approximation and Monte-Carlo simulation of backward stochastic differential equations. Stochastic Process. Appl., 111(2):175–206, 2004.

- Briand et al. [2001] P. Briand, B. Delyon, and J. Memin. Donsker-type theorem for BSDEs. Elect. Comm. in Probab., 6:1–14, 2001.

- Chassagneux and Crisan [2014] J. Chassagneux and D. Crisan. Runge-Kutta schemes for BSDEs. Ann. Appl. Probab., 24(2):679–720, 2014.

- Chevance [1997] D. Chevance. Numerical methods for backward stochastic differential equations. In L. C. G. Rogers and D. Talay, editors, Numerical Methods in Finance, Publ. Newton Inst., pages 232–244. Cambridge University Press, Cambridge, 1997.

- Crisan and Manolarakis [2012] D. Crisan and K. Manolarakis. Solving backward stochastic differential equations using the cubature method: application to nonlinear pricing. SIAM J. Financ. Math., 3(1):534–571, 2012.

- Crisan and Manolarakis [2014] D. Crisan and K. Manolarakis. Second order discretization of backward SDEs and simulation with the cubature method. Ann. Appl. Probab., 24(2):652–678, 2014.

- Crisan et al. [2010] D. Crisan, K. Manolarakis, and N. Touzi. On the Monte Carlo simulation of BSDEs: An improvement on the Malliavin weights. Stochastic Process. Appl., 120(7):1133–1158, 2010.

- Delarue and Menozzi [2006] F. Delarue and S. Menozzi. A forward-backward stochastic algorithm for quasi-linear PDEs. Ann. Appl. Probab., 16(1):140–184, 2006.

- Douglas JR. et al. [1996] J. Douglas JR., J. Ma, and P. Protter. Numerical methods for forward-backward stochastic differential equations. Ann. Appl. Probab., 6:940–968, 1996.

- Duffie and Epstein [1992] D. Duffie and L. G. Epstein. Stochastic differential utility. Econometrica, 60(2):353–394, 1992.

- El Karoui et al. [1997a] N. El Karoui, E. Pardoux, and M. Quenez. Reflected backward SDEs and American options. In L. C. G. Rogers and D. Talay, editors, Numerical Methods in Finance, Publ. Newton Inst., pages 215–231. Cambridge University Press, Cambridge, 1997a.

- El Karoui et al. [1997b] N. El Karoui, S. Peng, and M.-C. Quenez. Backward stochastic differential equations in finance. Math. Finance, 7 (1):1–71, 1997b.

- Gobet et al. [2005] E. Gobet, J.-P. Lemor, and X. Warin. A regression-based Monte Carlo method to solve backward stochastic differential equations. Ann. Appl. Probab., 15(3):2172–2202, 2005.

- Han and Long [2020] J. Han and J. Long. Convergence of the deep BSDE method for coupled FBSDEs. Probability, Uncertainty and Quantitative Risk, 5(1):5, 2020.

- Huijskens et al. [2016] T. Huijskens, M. Ruijter, and C. Oosterlee. Efficient numerical Fourier methods for coupled forward-backward SDEs. J. Comput. Appl. Math., 296:593–612, 2016.

- Hyndman and Oyono Ngou [2017] C. B. Hyndman and P. Oyono Ngou. A convolution method for numerical solution of backward stochastic differential equations. Methodol. Comput. Appl. Probab., 19:1–29, 2017.

- Kloeden and Platen [1992] P. Kloeden and E. Platen. Numerical Solution of Stochastic Differential Equations, volume 23 of Applications of Mathematics (New York). Springer-Verlag, Berlin, 1992.

- Lucia and Schwartz [2002] J. Lucia and E. Schwartz. Electricity prices and power derivatives: Evidence from the nordic power exchange. Rev. Derivatives Res., 5:5–50, 2002.

- Ma et al. [2002] J. Ma, P. Protter, J. S. Martin, and S. Torres. Numerical method for backward stochastic differential equations. Ann. Appl. Probab., 12 (1):302–316, 2002.

- Ma et al. [2008] J. Ma, J. Shen, and Y. Zhao. On numerical approximations of forward-backward stochastic differential equations. SIAM J. Numer. Anal., 46(5):2636–2661, 2008.

- Oyono Ngou [2014] P. Oyono Ngou. Fourier methods for numerical solution of FBSDEs with applications in mathematical finance. PhD thesis, Concordia University, Montréal, Canada, January 2014.

- Pardoux and Peng [1992] E. Pardoux and S. Peng. Backward stochastic differential equations and quasilinear parabolic partial differential equations. In Stochastic partial differential equations and their applications (Charlotte, NC, 1991), volume 176 of Lec. Notes Control and Inform. Sci., pages 200–217. Springer, Berlin, 1992.

- Peng and Xu [2011] S. Peng and M. Xu. Numerical algorithms for backward stochastic differential equations with 1-d Brownian motion: Convergence and simulations. ESAIM Math. Model. Numer. Anal., 45:335–360, 2011.

- Ruijter and Oosterlee [2015] M. Ruijter and C. W. Oosterlee. A Fourier-cosine method for an efficient computation of solutions to BSDEs. SIAM J. Sci. Comput., 37(2):A859–A889, 2015.

- Ruijter and Oosterlee [2016] M. J. Ruijter and C. W. Oosterlee. Numerical Fourier method and second-order Taylor scheme for backward SDEs in finance. Appl. Numer. Math., 103:1 – 26, 2016.

- Turkedjiev [2015] P. Turkedjiev. Two algorithms for the discrete time approximation of Markovian backward stochastic differential equations under local conditions. Electronic Journal of Probability, 20:1 – 49, 2015.

- Vašíček [1977] O. Vašíček. An equilibrium characterization of the term structure. J. Financ. Econ., 5(2), 1977.

- Weinan E et al. [2017] Weinan E, J. Han, and A. Jentzen. Deep learning-based numerical methods for high-dimensional parabolic partial differential equations and backward stochastic differential equations. Communications in Mathematics and Statistics, 5(4):349–380, 2017.

- Weinan E et al. [2019] Weinan E, M. Hutzenthaler, A. Jentzen, and T. Kruse. On multilevel Picard numerical approximations for high-dimensional nonlinear parabolic partial differential equations and high-dimensional nonlinear backward stochastic differential equations. Journal of Scientific Computing, 79(3):1534–1571, 2019.

- Weinan E et al. [2022] Weinan E, J. Han, and A. Jentzen. Algorithms for solving high dimensional PDEs: From nonlinear Monte Carlo to machine learning. Nonlinearity, pages 278–310, 2022.

- Zhang [2004] J. Zhang. A numerical scheme for BSDEs. Ann. Appl. Probab., 14:459–488, 2004.