Inequalities for the false discovery rate (FDR) under dependence

Abstract

Inequalities are key tools to prove FDR control of a multiple test. The present paper studies upper and lower bounds for the FDR under various dependence structures of -values, namely independence, reverse martingale dependence and positive regression dependence on the subset (PRDS) of true null hypotheses. The inequalities are based on exact finite sample formulas which are also of interest for independent uniformly distributed -values under the null. As applications the asymptotic worst case FDR of step up and step down tests coming from an non-decreasing rejection curve is established. In addition, new step up tests are established and necessary conditions for the FDR control are discussed. The reverse martingale models yield sharper FDR results than the PRDS models. Already in certain multivariate normal dependence models the familywise error rate of the Benjamini Hochberg step up test can be different from the desired level . The second part of the paper is devoted to adaptive step up tests under dependence. The well-known Storey estimator is modified so that the corresponding step up test has finite sample control for various block wise dependent -values. These results may be applied to dependent genome data. Within each chromosome the -values may be reverse martingale dependent while the chromosomes are independent.

doi:

10.1214/154957804100000000keywords:

[class=AMS]keywords:

and

1 Introduction

High dimensional testing problems given by hypotheses and corresponding ordered -values of the -value vector are frequently judged by multiple tests, like step up and step down tests. These tests rely on the component wise comparison of the ordered -values with a family of critical values , see [1-3, 7-11,17 23-25] for instance. The overall control of the error probability of first kind is often too restrictive and leads to very conservative multiple tests. Therefore, Benjamini and Hochberg [1] promoted the false discovery rate (FDR) as error measure to control. The FDR is the expected ratio of the number of falsely rejected null hypotheses among the total number of rejections.

Starting with the famous choice of critical values by Benjamini and Hochberg [1], quite a lot of authors studied finite sample or asymptotic FDR control (by some given level ) under various assumptions. Roughly speaking the finite sample research can be derived in two categories. When the critical values are deterministic, then different sufficient conditions and dependence concepts for the -values were established in order to ensure FDR control at level , i.e. , see Benjamini and Hochberg [1], Benjamini and Yekutieli [2], Blanchard and Roquain [5] and Finner et al. [9] among others. In case of data dependent critical values , which lead to adaptive multiple tests, typically the i.i.d. structure of the -values of true null hypotheses is assumed to achieve FDR control, see Storey et al. [24] and Sarkar [21] for instance. They include an estimation of the number of true null hypotheses in the critical values in order to exhaust the predetermined FDR level better. Another branch is the asymptotic FDR control, where milder assumptions like weak dependency may be considered.

In this paper we will again revisit FDR inequalities for step up and step down tests. The results depend on three dependence structures for the -values, namely the most restrictive basic independence (BI) model, the reverse martingale model and the positive regression dependence on a subset (PRDS) model, respectively, which are introduced in Section 2 beside the basic notation. Martingale arguments were used in Chapter 3 of the dissertation of Scheer [22] for the comparison of the FDR and the expected number of false rejections. Reverse martingale models naturally show up for instance for measurements under restrictions or in multivariate extreme value theory, see Example 3.3 which include a Marshall/Olkin type dependence structure. Section 3 gives some construction methods of reverse martingales and it is pointed out that the FDR of the classical Benjamini Hochberg step up test can exactly be calculated for the reverse martingale structure, whereas already strict inequalities hold under multivariate normal PRDS models, see Example 3.1. Section 4 discusses FDR inequalities for all these models which include inequalities for the FDR and inequalities for the critical values of FDR controlling step up tests. New necessary and sufficient conditions for finite sample FDR control at level are derived. In particular, critical values considered earlier by Finner et al. [9] and Gavrilov et al. [11] are discussed, see also Section 5.1. The inequalities can be used to modify the critical values of Gavrilov et al. [11] for step up tests, confer Example 5.1 for improved new tests. Theorem 5.1 establishes an exact asymptotic formula for the worst case FDR of step up tests which come from an increasing rejection curve. Observe that our inequalities allow to treat the difficult case when the expected portion of true null hypotheses becomes maximal. That result can be compared with the asymptotic optimal rejection curve (AORC) of Finner et al. [9] which compares concave rejection curves. For concave rejection curves, it is remarkable that the asymptotic worst case FDR value here is the same for the corresponding step up and step down tests, see Section 5.2.

Section 6 deals with adaptive SU tests under dependence which has often been neglected in the past. The adaptive step up tests rely on conservative estimators of the expected number of true null hypotheses. Mostly the basic independence model is assumed in the literature when the FDR of the adaptive test is shown to be controlled. We will point out that finite sample FDR control of adaptive step up tests is a difficult affair and can not be expected in general under dependence. Recall that the well-known Storey multiple test does not work under positive regression dependence on the subset of true null hypotheses, see Example 6.1 for instance. We will give a simple condition which ensures asymptotic FDR control under different dependence structures, see Theorem 6.1 and 6.2. For fixed sequence of estimators these conditions may also be regarded as conditions for the possible dependence structures. Furthermore, finite sample control can be obtained for various adaptive step up tests under the reverse martingale model. Also necessary conditions for finite sample control will be presented. It is shown that under additional conditions some modified Storey estimators work for dependent but block wise independent -values, see Theorem 6.3. Under the general assumptions these results are sharp and can not be improved, see Example 6.1. However, when all -values are independent then the new blockwise test is conservative.

2 Basic notation and dependence models

Throughout, we investigate models with different dependence structures. All of these models are based on the following basic model with random number of true null hypotheses. Let be a probability space and let

| (2.1) |

be a multivariate random variable where codes the occurrence of a -value of a false null hypothesis, for short false -value, and the occurrence of a -value of a true null hypothesis, for short true -value, whose marginal distribution is the uniform distribution on . Then the model of the -values is given by

| (2.2) |

where is the random number of true p-values. This model includes the well studied mixture model of Efron et al. [6], where , and are i.i.d. and jointly independent. Observe that here is naturally random. Throughout, true or false null hypotheses are identified with their -values and for short the corresponding -values are called “true” or “false”, respectively. Since our multiple tests only rely on -values this identification may be justified. Moreover, we define and . Below, further assumptions about the dependence structure of the vector (2.1) are introduced. To avoid trivial cases let be always positive and let us assume that our observations are the order statistics of the -values, which are introduced as

| (2.3) |

Moreover, let , , be the empirical cumulative distribution function of the -values.

Let denote the Borel sets of . A set is said to be decreasing iff, and component-by-component imply .

Definition 2.1 (Dependence structures).

(a) Let , be independent. Then we call this submodel for the -values

(2.2) to be the basic independence (BI) model. Note that

is considered as one random variable whereas are considered as individual random variables in terms of

independence.

(b) Let

| (2.4) |

be non-increasing for every decreasing set , and all

with . Then -value model (2.2) is called the PRDS model (positive regression

dependent on the subset of true null hypotheses).

(c) Conditioned under let

| (2.5) |

be a reverse martingale with respect to the reverse filtration . Then -value model (2.2) is called reverse martingale model.

Remark 2.1.

(a) The assumptions for the PRDS model in Definition 2.1 (b) are a little bit weaker than the usual

PRDS assumptions, see Finner et al. [9] for instance. In the literature it is sometimes called

weak PRDS. Nevertheless, we will call it PRDS model for brevity.

(b) The BI model is a submodel of the PRDS and reverse martingale model. Furthermore, the intersection of the PRDS and

reverse martingale models is at least greater than the BI model. To see this regard independent disjoint blocks of

with maximal dependence in each block given here by the same uniformly distributed random variable.

We will see that the reverse martingale models yield sharper FDR results than the PRDS concept. A comparison of these models is included in Section 3.

In the past literature usually conditional versions of the BI and PRDS model with deterministic have been considered, see Benjamini and Hochberg [1], Benjamini and Yekutieli [2], Blanchard and Roquain [5], Finner et al. [9] and Finner and Roters [10] for instance. In all models defined above these conditional versions are included as special case.

In this paper we mainly focus on step up tests (SU tests), which we briefly recall. Suppose that

| (2.6) |

denote possibly data dependent critical values and set for convenience. The corresponding SU test is based on the number of rejections

| (2.7) |

and rejects the null hypotheses corresponding to the set of -values . When the condition in (2.7) is empty no hypothesis is rejected and holds. Then equivalently all null hypotheses with -values

| (2.8) |

are rejected. Let

| (2.9) |

be the unobservable number of falsely rejected true null hypotheses. The judgment of multiple tests is often done via the control of the celebrated “false discovery rate” (FDR) which is given by (with . More generally we introduce the conditional false discovery rate

| (2.10) |

as conditional expectation given . The conditional quantity (2.10) is a special case since constant are included.

Benjamini and Hochberg [1] promoted the FDR as new error criterion competing against the well known familywise error rate (FWER) and provided a multiple test procedure controlling the FDR under certain assumptions. The so-called Benjamini Hochberg test (BH test) is the linear SU test with fixed critical values

| (2.11) |

In our setting and notation it was shown by Benjamini and Yekutieli [2] and Finner and Roters [10] that

| (2.12) |

holds for the conditional expectation in the BI model. Benjamini and Hochberg [1] previously showed that “” holds in (2.12) for the BI model. Moreover, Benjamini and Yekutieli [2] proved that “” holds in (2.12) for the PRDS model. In the same work, they also introduced a new SU test based on more conservative critical values

| (2.13) |

Benjamini and Yekutieli [2] pointed out that “” again holds in (2.12) for this SU test under the basic model with arbitrary dependence structure of . Blanchard and Roquain [5] showed that the critical values (2.13) may also be replaced by

| (2.14) |

where is an arbitrary probability measure on . For , , the critical values correspond to (2.13). Adaptive versions based on (2.13) and (2.14) are presented in Theorem 6.2 under arbitrary dependence.

We will particularly focus on critical values coming from a continuous non-decreasing function

| (2.15) |

for some . We refer to as rejection curve. Moreover, let denote the left continuous inverse of and let the deterministic critical values be generated via

| (2.16) |

We refer to as critical value curve. Note that the BH test is based on the Simes line , , see Finner et al. [9] for instance.

Finner et al. [9] introduced the Asymptotic Optimal Rejection Curve (AORC) which is constructed to have FDR control by in an asymptotic Dirac uniform (DU) setting given by , . The AORC is given by

| (2.17) |

but since , the above assumptions for rejection curves for SU tests are not fulfilled. There are several modifications of the AORC and corresponding SU tests to overcome this problem. For further details we refer to Finner et al. [9].

3 Examples of reverse martingale models and a comparison with PRDS

At the beginning it is shown that there exist positive dependent multivariate normal models which are PRDS without the martingale property. To prove this we will consider the following example.

Example 3.1.

Let and be i.i.d. standard normal random variables with distribution function .

(a) Consider the PRDS model

and related -values . Then the familywise error rate of the BH step up test

with critical values (2.11) at level and is , cf.

(2.12), i.e. less than .

(b) For the negative dependence model

the familywise error rate of the BH step up test is and hence greater than .

The proof is given in Section 7. Note that Gavrilov et al. [11], p. 625, already derived Monte Carlo results showing that the FWER of the BH step up test may be strictly below under PRDS. In contrast to PRDS the reverse martingale models allow sharper FDR results, see Section 4 and Lemma 7.1. The next remark summarizes this.

Remark 3.1.

In conclusion we see that reverse martingale models allow sharper FDR formulas as under PRDS. However, we do not know whether every reverse martingale model is PRDS.

The reverse martingale structure yields a rich class of -values. The next example shows how to construct new reverse martingale models from known ones. In particular, reverse martingale measures on product spaces of are preserved under a lot of operations.

Example 3.2.

Let , and be fixed with . Define -values via the canonical projections . Then

is the set of reverse martingale measures.

(a) is closed under mixtures including convex combinations.

(b) (Independent coupling of reverse martingale regimes) Suppose that there are partitions and

with for all but is allowed to be empty. Whenever

holds for all , then the product measure belongs to .

(c) (Optional switching of reverse martingales) It is well known that two independent reverse martingale models

given by and may be combined as follows. Let

denote a reverse stopping time w.r.t. model . Whenever holds, that -value for the index comes from

the model. In case , consider the -value of and take the renormalized value

as new -value for these coordinates.

(d) Let be any random variables such that

| (3.1) |

is a reverse martingale. Suppose that denotes a uniformly distributed permutation of jointly independent of the ’s. Then the family of -values has the reverse martingale property (2.5) for each component.

Part (d) of that example is easy to prove and grew out of a discussion with Julia Benditkis which is kindly acknowledged.

The subsequent example gives an explicit example which may have the following practical meaning. The statistician can only observe a concentration above a joint random ground level . It also occurs in multivariate extreme value theory and risk analysis when the have a joint risk component .

Example 3.3.

(Marshall and Olkin type dependence, see Marshall and Olkin [18]) Let denote continuous, independent, real random variables, where are i.i.d.. Consider for . The transformed true -values , given by have the reverse martingale property, see Section 7 for a proof. It is easy to verify, that the present model is also PRDS since it is based on a comonotone transformation of the i.i.d. model . Notice that in case the negative variables correspond to the bivariate Marshall and Olkin [18] model.

Reverse martingale models can also be obtained allowing some dependence between “true and false” -values.

Example 3.4.

(Dependence between the null and alternatives) The following models may be used as ingredients for Example 3.2 (b). Consider a distribution on , where

-

(i)

the marginal distribution of the “trues“ belongs to .

-

(ii)

Suppose holds almost everywhere.

Then holds. The proof follows the same line as in Example 3.3.

4 Inequalities for the FDR

In this section new inequalities are derived which are used in the proceeding chapters. We start with arbitrary non-decreasing deterministic critical values and the following question.

-

•

What can be said about the FDR of the corresponding SU test given by a fixed model (2.2)?

The next inequalities rely on more technical results given in Section 7, in particular in Lemma 7.1.

Proposition 4.1.

(a) Assume the reverse martingale model (including the BI model) and consider the SU test with arbitrary deterministic critical values (2.6). Then we have

| (4.1) |

(b) Suppose that holds.

-

(i)

The inequality implies the strict inequality

| (4.2) |

-

(ii)

Conversely, implies

| (4.3) |

(c) Under the PRDS model we still obtain

| (4.4) |

Observe that Example 3.1 gives a counterexample that the lower bound in (4.1) does not hold under PRDS.

With different methods Guo and Rao [13] already showed that the upper bound in (4.1) holds under the PRDS property. Moreover, Sarkar [20] derived several inequalities and exact expressions for the FDR for so-called generalized step-up-down tests. These inequalities are then used as key tools to prove FDR control of an step-up-down test basically with Benjamini Hochberg critical values (2.11) under the PRDS assumption and a further step-down test under multivariate total positivity of order 2 (MTP2).

Under regularity assumptions the inequalities are asymptotically sharp. We refer to Section 7 and Lemma 7.4.

For deterministic critical values let us discuss the assumption

| (4.5) |

It is easy to verify that (4.5) holds for the critical values (2.16) which come from a concave rejection curve. Under (4.5) Benjamini and Yekutieli [2] showed that Dirac uniform (DU) configurations (i.e. ) are least favorable parameter configurations for the FDR in the BI model for fixed . Let us assume that the critical values with (4.5) lead to overall finite sample FDR control for the BI model, the PRDS model or the martingale model, respectively. Then the subsequent results investigate necessary conditions for the critical values itself and the following question can be treated.

-

•

What can be said about the critical values when the FDR is controlled by for all distributions given by a specified class of submodels for fixed ?

Lemma 4.1.

Corollary 4.1.

Consider the assumptions of Lemma 4.1.

(a) The inequality always holds.

(b) If then the SU test is already a BH test at level .

Otherwise, holds.

(c) If for some , then always follows.

Remark 4.1.

(a) Consider the Dirac uniform configuration DU with and , , for the reverse martingale model. Under (4.5) the lower bound in (4.1) can then be improved following the lines of Proposition 4.1 for by

| (4.6) |

(b) The statements of Lemma 4.1 and Corollary 4.1 naturally hold if holds for all szenarios described by the PRDS or reverse martingale model, since the BI model is a submodel of both models.

The next example demonstrates an application of our inequalities.

Example 4.1 (about necessary conditions for the BI model).

(a) SU tests with critical values

| (4.7) |

are frequently

discussed in the literature. The requirement for all implies . A necessary

condition for is then by Lemma 4.1 the additional condition . If

is positive then is necessary.

(b) Consider some fixed integer and the adjusted critical values

| (4.8) |

of the Asymptotic Optimal Rejection Curve (AORC) (2.17) of Finner et al. [9] which are first only specified for . There are several possibilities for the choice of , , for the extension of (4.8) such that (4.5) remains true and holds, see (5.2) below and confer also Finner et al. [9] and Gontscharuk [12]. It is well-known by Finner et al. [9] that the SU tests with adjusted critical values (4.8) do not have finite sample FDR control but asymptotic FDR control. Since and we directly observe by (a) that finite sample FDR control can not hold. Even the first critical value is too large to allow FDR control.

5 Applications under independence

5.1 FDR control

Our inequalities include a device for the choice of adequate parameters for the critical values (4.7). Below, we restrict ourselves to the FDR adjustment under the BI model. Some technical inequalities presented in Section 7 also work under dependence.

Proposition 5.1.

Sharper inequalities for the range of the parameter of (5.1) are included in Proposition 7.1 which may be of computational interest in practice. However, the exact value should be calculated by numerical calculations, see Lemma 7.3 (a) of the proof section. For the step up test with critical values (4.7), , and we have for instance which is not far away from the upper bound .

In the next step we establish another FDR adjustment as in (5.1) of critical values which may have some advantage in practice. The new proposal relies on the following observation. Typically the largest coefficients of (2.6) are responsible for a worst case FDR value with , cf. Finner et al. [7]. For these reasons we propose to bound the largest critical values as follows.

Proposition 5.2.

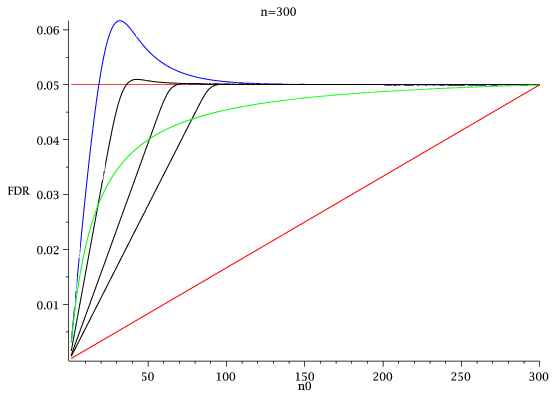

The modification (5.2) of the critical values has also been considered by Finner et al. [9] Example 3.2 for the special case of critical values coming from the AORC. Moreover, for this type of modification Finner et al. [7] propose to increase the parameter in a further step in order to decrease the FDR below . In contrast to earlier work Proposition 5.2 works for general critical values with (4.5). In principal, Proposition 5.2 also works for . For practical purposes a choice of a very small value can be recommended, see Figure 1 in Example 5.1.

Example 5.1.

(Under the BI model)

(a) Let us consider the step down critical values

| (5.4) |

of Gavrilov et al. [11]. It is well-known that the corresponding SD test, see Section

5.1 for the notation, yields

finite sample FDR control, whereas the corresponding SU test has no finite sample FDR control. On the other hand

the necessary conditions for finite sample FDR control of Lemma 4.1 (a) are fulfilled.

In this case our results do not exclude this procedure but we get a meaningful lower bound based on (4.6)

for the worst case of FDR and a hint how the critical values (5.4) can be modified.

(b) Figure 1 shows the FDR of the SU test for and for the least favorable DU configurations

for different values of with , given by the critical values (5.4).

The lower bound in (4.1) is based on

| (5.5) |

Thus, this lower bound is close to the FDR for fixed for this example.

Moreover, Figure 1 shows the FDRDU plot for different choices given by

(5.2) based on the critical values (5.4) with graphs decreasing in .

The straight line represents the FDR of the BH test and the green curve is the lower bound (4.6).

Numerical results yield the value for and for given by

(5.3), see Table 1. Here, leads to a BH test and is the only

with .

(c) In practice the statistician can accept the enlarged FDR value or he can reduce the critical values

(5.4) by a minor reduction of .

5.2 Asymptotic worst FDR case

Our technique applies to the worst case FDR asymptotics for SU tests given by rejection curves .

Theorem 5.1.

Let be the set of all possible distributions of the BI model for fixed . Consider a non-decreasing continuous rejection curve for some with , . Assume also that is left-sided differentiable on and let for all and some . For the sequence of SU tests based on the critical values (2.16) the asymptotic worst SU case FDR is

| (5.6) |

Moreover, holds.

Remark 5.1.

(a) Note that the AORC curve (2.17) yields

| (5.7) |

which again supports the optimality of .

(b) Suppose that holds for some rejection curve treated in Theorem 5.1. The proof of Theorem

5.1 implies on with the upper bound for

the critical values of the SU tests.

(c) The question about the limiting FDR for was addressed in Remark 5.1 of

Finner et al. [9]. Our approach contributes to this open problem.

For concave rejection curves we briefly point out that the asymptotic bound of Theorem 5.1 is the same for step down (SD) tests. Consider again the critical values (2.16). The step down critical index is given by the number of SD rejections

| (5.8) |

The modification of (2.7) and (2.8) for SD tests requires that all null hypotheses with -values

| (5.9) |

are rejected. When the condition in (5.8) is empty no hypothesis is rejected and holds. Similarly to (2.9) put to be the number of false positive rejections.

Theorem 5.2.

Remark 5.2.

Consider a sequence of SD tests with critical values given by (2.16) based on a concave rejection curve (2.15) and which has finite sample FDR control by for all in the BI model. Then the same holds asymptotically for the corresponding sequence of SU tests. This technique does not apply for the sequence of SU tests based on the Gavrilov et al. [11] critical values (5.4), since the critical values are not generated by one rejection curve, but by the sequence of rejection curves based on the AORC.

6 Applications to adaptive control under dependence

In contrast to the preceding sections now data driven critical values are considered in order to exhaust the FDR level of given SU tests. Much effort was done in order to establish adaptive SU tests which are based on the linear SU test of Benjamini and Hochberg [1]. These tests are typically based on conservatively biased estimators of in order to exploit the FDR level better. The approach is motivated by the substitution of by which leads to the heuristic for consistent and to data dependent BH type critical values

| (6.1) |

We refer to the well-known and frequently applied so called Storey type estimators given by the empirical distribution function of the -values

| (6.2) |

where is often chosen to be close to , see Storey et al.[24] and Storey[23] for the choice of . There are several estimators and conditions for FDR control in the literature, for example see Benjamini et al. [3], Sarkar [21] and Zeisel et al. [25].

The finite sample FDR control of the adaptive SU test of Storey based on the critical values (6.1) and estimator (6.2) with seems to be restricted to the BI model. Even for the reverse martingale model, which allows that some -values coincide, further assumptions are required, see Example 6.1 below for instance.

The aim of this section is twofold for the reverse martingale model.

-

•

In Section 6.1 sufficient conditions for estimators of are introduced which ensure asymptotic FDR control.

-

•

In Section 6.3 modified Storey SU tests are introduced which have finite sample FDR control for various block wise dependence models.

Moreover, we propose an adaptive multiple test for arbitrary dependent data and we also give a sufficient condition for the estimator and dependence structure, respectively, which again ensures asymptotic FDR control, compare with (2.13) and (2.14).

The estimators and multiple tests are based on various assumptions. Let and divide into two areas, the rejection area and the estimation area . Let us specify different assumptions.

-

(A1)

The unknown value is estimated by an estimator

| (6.3) |

-

via the empirical cumulative distribution function on the estimation area and a measurable function .

-

(A2)

The unknown value is estimated by

| (6.4) |

-

(A3)

The multiple test is applied to the rejection area with data dependent critical values

| (6.5) |

-

(A4)

The multiple test is applied to the rejection area with the following data dependent critical values

| (6.6) |

-

where is an arbitrary probability measure on .

Taking the minimum in (6.5) goes back to Storey et al. [24] and ensures that one does not reject -values greater than , therefore the name rejection area. Statisticians often do not like to reject a hypothesis when the -value is too high. The estimated critical values (6.6) are based on the deterministic family of critical values (2.14) of Blanchard and Roquain [5] which also include the critical values (2.13) of Benjamini and Yekutieli [2].

6.1 Asymptotic results

The central Lemma 7.1 now establishes sufficient conditions for asymptotic FDR control of adaptive SU tests under different dependence structures.

Theorem 6.1.

Let be the set of all possible distributions of the reverse martingale models for fixed and let be a sequence of distributions with . Moreover, let be a sequence of estimators for which fulfill (A1). If

| (6.7) |

holds for all , where for , then

| (6.8) |

holds for the sequence of adaptive SU tests given by (A3).

Finner and Gontscharuk [8] and Gontscharuk [12] already used condition (6.7) to show asymptotic FWER control of a specific sequence of adaptive Bonferroni tests and adaptive SD tests, respectively. Under mild regularity assumptions, Liang and Nettleton [17] showed that the FDR of the adaptive SU test of Storey with altered estimator and critical values is asymptotically controlled at level for every arbitrary and data dependent selection of the tuning parameter out of a candidate set . This result may also be proved by application of Theorem 6.1, but note that Theorem 6.1 works for a much broader class of estimators and also under the reverse martingale model. The conservative consistency (6.7) is a very weak condition. Under mild regularity assumptions the crucial assumption (6.7) is also necessary for (6.8) for Storey type estimators (6.2).

Proposition 6.1.

Remark 6.1 (About asymptotic FDR of Storey type SU tests).

Consider the reverse martingale model. As long as enough variability of the variables is present condition (6.7) can be verified. Let be the estimator (6.2) for some positive sequence . Let

| (6.9) |

be the cumulative distribution function of true -values. Then a sufficient condition to ensure (6.7) is (6.10), where the conditional variances

| (6.10) |

tends to zero in probability as . The corresponding SU tests then have asymptotic FDR control.

At this point, Theorem 6.1 can be extended to treat arbitrary -values. Like Benjamini and Yekutieli [2] and Blanchard and Roquain [5], who considered non data dependent SU tests for arbitrary dependence structures. Therefore we have to consider more conservative test procedures. The adaptive SU test (A4) is based on the critical values (2.14) of Blanchard and Roquain [5] and yields asymptotic FDR control if (6.7) is satisfied.

Theorem 6.2.

Let be the set of all possible distributions of the -value model (2.2) for fixed , where each is distributed according to the uniform distribution on . No further distributional assumption and no dependence structure is assumed. Again, let be a sequence of distributions with and be a sequence of estimators for which fulfill (A2). If (6.7) is fulfilled, then (6.8) holds for the sequence of adaptive SU tests given by (A4).

6.2 Finite sample results

Let us now come back to finite sample FDR control. We will give a condition for FDR control for the reverse martingale model and the next very useful Lemma offers an exact formula for the FDR of our adaptive tests.

Lemma 6.1.

Let denote the number of true null hypotheses with -values . Under the reverse martingale model, the adaptive SU test with critical values (A3) and estimator (A1) fulfills

| (6.11) |

This result generalizes Lemma 3.1 of Heesen and Janssen [15], where the BI model is treated only. For the control of the FDR by one merely has to show

| (6.12) |

For example the benchmark result of Liang and Nettleton [17, Theorem 7] works for estimators with almost surely with defined in (6.2) with and for some . In comparison to that, Lemma 6.1 works for the class of estimators (A1) and also for the reverse martingale model. Some interesting estimators which do not satisfy are given Heesen and Janssen [15].

The following negative result explains first that the use of adaptive SU tests is limited under dependence and further results are needed for finite sample FDR control.

Proposition 6.2.

Consider an adaptive SU test based on (A1), (A3) and . Assume that the estimator is non-decreasing for each coordinate . If we have for all reverse martingale models then holds and the adaptive critical values are dominated by the BH critical values.

The adaptive step up test of Storey does not yield FDR control in the reverse martingale and PRDS model. For instance Blanchard and Roquain [4, Theorem 17] proved that in case of and , for a uniform distributed on ,

holds for the Storey estimator (6.2) with . This result corresponds to Lemma 6.1. Note that condition (6.7) is violated since holds on for the Storey estimator (6.2).

6.3 Case of a block model

Finally the following modified adaptive SU test is considered when mild additional dependence assumptions are present. Suppose that the -values can be divided by

| (6.13) |

in disjoint blocks or groups . Suppose the reverse martingale condition for . Assume in addition that for each group the subset corresponds to uniformly distributed -values given by true null hypotheses. Below let the groups , , be conditionally independent given the signs whereas within group a reverse martingale dependence structure is allowed.

Remark 6.2.

In practice the model may have the following meaning for genome data. may stand for independent portions of true -values which may come from different chromosomes. The -values of may be reverse martingale dependent, for instance some of them may be equal.

Consider the maximal size of the groups

| (6.14) |

with a remainder . Furthermore, let us assume that the number of true -values is almost surely lower bounded by . For the tuning parameters and the modified Storey estimator

| (6.15) |

with is introduced. Again (6.15) can be improved by the factor , i.e. also will work. We show that the step up test with estimated critical values

| (6.16) |

yields FDR control , , under the present block wise dependence model for all . If the groups are balanced, i.e. holds, then vanishes and the best fit is expected. Of course may happen for large in the unbalanced case and there would then be no advantage in comparison with the BH test when the -values are all independent.

Theorem 6.3.

Consider the reverse martingale model for the -values. Assume that the -values can be divided in disjoint groups, see (6.13) and (6.14) above. Moreover, assume that holds almost surely for a lower bound . Let conditionally on the signs the groups of the true -values be independent. If holds, then the modified adaptive SU test with critical values (6.16) and estimator (6.15) has finite sample FDR control, i.e. , and (6.12) holds.

Gontscharuk [12] considered a similar block model which leads to dependent -values and an adaptive Bonferroni type procedure with asymptotic FWER control. Theorem 6.3 works for finite .

If the group structure is known and balanced with , then Guo and Sarkar [14] propose an adaptive multiple test with FDR control under PRDS within each group. The ingredients are based on the Storey type estimator (6.2), where depends on the number of blocks and . However, every rejected -values has to be less than or equal to in comparison to for the adaptive SU test considered in Theorem 6.3.

As mentioned above the estimator (6.15) may produce very conservative SU tests for independent -values. However, Theorem 6.3 is designed for block dependent -values and we will see by the inspection of the FWER that this procedure can not always be improved. The necessary calculations for Example 6.1 are included in the proof of Theorem 6.3.

Example 6.1.

Consider blocks of size with true -values. Suppose that for each block all -values coincide with the same uniformly distributed random variable whereas the blocks are independent. The model has both the PRDS and the reverse martingale property. When holds then the choice for the procedures (6.15) and (6.16) yields

| (6.17) |

Here the modified estimator attains the FWER bound and we obtain a sharp result for the block model.

We conducted a small Monte-Carlo simulation with 100.000 repetitions to explore the situation beyond the case of Example 6.1 for the adaptive SU test with critical values (6.16) and estimator (6.15) with at size . All false -values are set to . Consider a setting of groups with -values and 16 equal true -values in each group. The choices of lead to . Furthermore, the group frequencies 25,25,20,15,15 with 20,20,16,12,12 equal true -values within theses groups and the choices of lead to . Since the number of true -values within each group is unknown, the simulation and Example 6.1 indicate that here is an appropriate tuning parameter for the adaptive SU test. Moreover, a simulation with equal group frequencies under the global intersection hypothesis shows that slightly smaller than already yields . For groups of equal size with and only true -values in each group, the choice of yields .

7 Technical results and proofs

Lemma 7.1.

(a) Let be data dependent critical values

| (7.1) |

given by measurable functions and introduce . Moreover define . Then

| (7.2) |

holds for the corresponding adaptive SU tests under the reverse martingale model (including the BI model).

(b) Let , , be non-decreasing in and let

. Moreover, assume that is a probability measure on and define the

data dependent critical values via

| (7.3) |

Then ”“ holds in (7.2) for the corresponding adaptive SU test with critical values (7.3) for arbitrary dependent variables .

Remark 7.1.

(a) Lemma 7.1 (a) also applies to deterministic critical values

if we put . In this case, the reverse martingale assumption (2.5) can be weakened

in order to prove (7.2). It is only necessary to assume that (2.5) is a reverse martingale

w.r.t. the discrete parameter set and .

(b) Storey et al. [24] already used martingale arguments which have been outlined by

Scheer [22].

(c) In case of deterministic critical values we obtain the inequality ”“

in (7.2) under the PRDS model. The proof follows straightforward classical lines, see Heesen [16]

and Meskaldji et al. [19].

Proof of Lemma 7.1. (a) Observe that the SU test can be represented by the reverse stopping time

which is adapted to the reverse Filtration and where . Then every -value is rejected. For and for we have . Conditioned under the critical values are fixed and therefore, is a discrete stopping time w.r.t. the reverse martingale (2.5) for the periode . Furthermore, observe that holds if since . Thus by (2.5) and the discrete version of the optional stopping theorem

holds and integration yields

(b) Applying the technique of the proof of Lemma 3.2 of Blanchard and Roquain [4] yields

There, the technique is formulated for deterministic critical values, but observe that it also works for data dependent critical values.

When the proof was finished we came across the early paper of Meskaldji et al. [19] which covers the special non-adaptive case of our technical Lemma 7.1 (b). For deterministic critical values their proof also follows the lines of Blanchard and Roquain [5].

7.1 Proofs of Section 3

Proof of Example 3.1. Below the proof of part (a) is sketched. The calculations for (b) are similar. Recall from Finner et al. [9], p. 604, the FDR formula for

| (7.4) |

since holds for the normal sample . For we have by conditioning w.r.t.

where . Similarly,

| (7.5) |

Notice that

| (7.6) |

follows. Thus, and holds which implies the result.

Proof of Example 3.3. Part (b) and (c) are obvious. To prove (a) define

In case it is well known that is a reverse martingale w.r.t. . In case let us prove that is a reverse martingale w.r.t. . Obviously, holds if . Otherwise, implies and . Thus holds for and all . Let be a possible path of , . If holds we have

Above we used that and are independent. Observe that the time change

by the inverse distribution function preserves the reverse martingale.

7.2 Proofs of Section 4

Lemma 7.2.

(a) Assume the PRDS model or reverse martingale model (which include the BI model). Consider the SU test with deterministic critical values (2.6) and suppose that there exist some and with for all .

-

(i)

Then holds.

-

(ii)

Suppose that the assumption holds for . If in addition holds for a fixed with , then follows for the BI model.

(b) Assume the reverse martingale model, consider the SU test with critical values (2.6) and suppose that holds for all .

-

(i)

Then holds.

-

(ii)

If in addition holds for some with , then holds at least under the BI model.

Proof.

(a)(i) Let and observe that holds for all . Then Lemma 7.1 (a) and Remark 7.1 (c) imply

for the PRDS and reverse martingale model, respectively.

(ii) By (i) we already know and in case of equality we have .

But observe that holds. Thus,

| (7.7) |

follows by our assumptions, a contradiction.

(b)(i) Observe that holds for all . Thus Lemma 7.1 implies

for the reverse martingale model.

(ii) Observe that and hold and

the assertion follows in the same way as in (a) (ii).

∎

Proof of Proposition 4.1. The proposition is a direct application of Lemma 7.1 (a) and Remark 7.1 (c) with deterministic critical values. Again let , . For the reverse martingale and PRDS models we have

| (7.8) |

by Lemma 7.1 (a) and Remark 7.1 (c). Under the assumptions of (b)(i) the first inequality in (7.8) is actually a strict inequality ”“. The other inequalities follow analogously.

Proof of Lemma 4.1. (a) In this proof we may always choose the Dirac uniform case for the false -values. Let be deterministic. Thus by Lemma 7.1 (a)

since holds when is positive and

is non-increasing. By our assumption the inequality proves the result.

(b) In that case we have for .

Obviously, holds for with . Thus we have strict inequality in the proof of

part (a) and follows.

Proof of Corollary 4.1.

(a) is a special case of Lemma 4.1.

(b) Assume the multiple test is not a BH test. Take the first value with

Then Lemma 4.1 (b) implies which contradicts our assumption.

(c) On the other hand implies and

by Lemma 7.2 (b).

Lemma 7.3.

Consider SU tests based on the critical values (4.7) with with fixed value

and an adjustment of .

(a) Under the reverse martingale model and the Dirac uniform configuration DU the FDR is given by

| (7.9) |

with ”“ under PRDS. Then

| (7.10) |

holds.

(b) The following inequality holds for the expected number of false rejections under DU

Note that this statement holds without any dependence assumption on .

Proof.

Remark 7.2.

Proof of the Recursion (7.11) of Remark 7.2. Consider a true -value, say , of . Put and let be the number of rejections. Simple calculations show that holds on the set . Observe, when is rejected, then could also be zero. Moreover, we have in any case for SU tests which implies

| (7.13) |

by Fubini’s theorem and . Under DU we obtain

| (7.14) |

and the recursion. Formula (7.12) follows by induction.

Remark 7.3.

Under the BI model the proof of statement (7.2) can be simplified as follows. Consider deterministic critical values. Using the proof of Remark 7.2 above we may again conclude by Fubini’s Theorem

The method of proof can be used to prove the discussion about least favorable ”false p-values“ given by Benjamini and Yekutieli [2] Theorem 5.3.

7.3 Proofs of Section 5.1

Proof of Proposition 5.1. By (7.10) we may concentrate on the DU case for the BI model. Note also that is strictly increasing in since the critical values are ordered. On the other hand expression (7.10) converges to for . Thus, the solution of (5.1) is unique and it is easy to see that holds.

Proposition 7.1.

Consider the assumptions of Proposition 5.1. Introduce as the unique positive solution of

| (7.15) |

where . Then the crucial parameter satisfies .

Proof.

Observe first, that the coefficients dominate the BH critical values for the choice of . Thus we have and

Hence, it is easy to see that the solution of (5.1) satisfies . ∎

Proof of Proposition 5.2. The requirements (4.5) remain true for the new coefficients (5.2) and we may restrict ourselves to the worst DU case. Here we have

We see that FDR is ordered by ”“ when the critical values and thus the ’s are ordered since increases. Observe that yield a BH test with FDR and the proof is finished.

7.4 Proofs of Section 5.2

In regular cases the inequalities (4.1) are asymptotically sharp. For this purpose assume that the critical values are generated by a function via

| (7.16) |

At this stage we require that is a non-decreasing function with , and . Then under regularity assumptions these bounds (4.1) are asymptotically sharp in the sense that for there exist sequences of BI distributions so that

| (7.17) |

Lemma 7.4.

Consider the SU test with critical values (7.16) given by a continuous function . Suppose that converges in probability for some and suppose that exists. Then .

Suppose that as well as are attained for some . Furthermore, assume that there exist sequences of distributions with , , in probability, respectively, and . Then Lemma 7.4 can be applied in order to get sharp bounds in (4.1).

Proof of Lemma 7.4. Let be an open neighborhood of with on . Then

holds. Introduce

which is a tight sequence of random variables. On the other hand the bounded sequence of random variables

converges in probability. Turning to distributional convergent subsequences of we finally obtain

since holds by Lemma 7.1.

Proof of Theorem 5.1. The present proof is given by several steps. Below the following elementary geometric property of the AORC is used. Consider for the function for in the plain. Then

-

1.

iff belongs to the graph of , i.e. .

-

2.

iff is below the graph of , i.e. .

-

3.

iff lies above the graph of , i.e. .

(I) We claim . We first show . Therefore, choose and a Dirac uniform configuration. Then holds. Hence every -value will be rejected and in particular every -value . Thus

for this sequence of Dirac uniform models. Let us next show . Therefore, let be arbitrary and observe that lies above the Benjamini Hochberg rejection curve of the BH test. By Lemma 7.2 (a)(i) we always have

(II) The statement (5.6) of the Theorem is first proved for concave rejection curves . Therefore, observe that under the distribution of

for all , since the Dirac uniform configuration is least favorable for the FDR for SU tests with critical values fulfilling (4.5). Hence we get

| (7.18) |

since belongs to and thus there exists a subsequence , again denoted by , with

| (7.19) |

and some . Now we determine the limit of for every sequence .

1. For observe that

and by a similar argument it follows that the limit of is continuous in at .

2. Let us consider with positive and introduce the straight line which runs through the points and and has the unique crossing point , , with . Observe that

holds. Now let be a weak accumulation point of . Since is continuous and converges uniformly to with probability 1 the equation

follows. There is only one crossing point and thus is constant for each weak accumulation point. From we now deduce

| (7.20) |

at least along subsequences. Similar arguments were used by Scheer [22], Lemma 2.9, in his set up in order to prove that converges to the crossing point .

A simple geometric argument for the gradient of yields

and hence

| (7.21) |

By Lemma 7.4 and subsequence arguments

| (7.22) |

holds for all sequences .

3. Now consider . Again in distribution. This follows from (7.20) by the monotonicity of in since holds for . Observe next that for every we have and hence by (4.5)

holds for . By Lemma 7.2 (a)(i)

holds and hence

when since .

(III) Let now be the general rejection curve of Theorem 5.1. Introduce

.

(a) Claim: . The geometric arguments 1.-3. at the beginning of the proof imply for the AORC with parameter . Next is modified as follows. Let be the tangent straight line attached at at the point . Then

| (7.23) |

defines a concave rejection curve with for some . By Lemma 7.5, given below, the is always an upper bound of the . By step (II) the asymptotic worst case FDR of equals

| (7.24) |

It is easy to see that the left hand side is just .

(b) The proof will be completed by showing . The inequality follows from the next special construction of mixture models, where now in contrast to part (II) of this proof the DU configuration is no longer least favorable. Introduce for each the straight line and the intersection set . Note that is a compact set bounded away from and with and

| (7.25) |

Thus, there exists some maximal element with for all . In the next step we will introduce for each set a mixture model with appropriate distribution function

| (7.26) |

The non-uniform part will have the following properties:

-

(i)

, which implies for all and .

-

(ii)

for all .

In order to do so, let be a straigt line through with sufficiently large slope such that for all . Here the left-sided differentiability of is used. Put now

| (7.27) |

This is the only cut point of and . Consider now a mixture model with distribution function . Similarly as in (II) we have and via the cut point consideration we arrive at

| (7.28) |

at least along suitable subsequences. A comparison of the line segment with the AORC yields for each if we take 1.-3. into account. This construction can be done for each set . Thus, the proof of the inequality is complete.

The next lemma is used in the last proof and may be of separate interest.

Lemma 7.5.

Let be a non-decreasing rejection curve with , for some and for some . Moreover, let be a concave rejection curve and a lower bound of . Under the BI Model for fixed and we have

| (7.29) |

for the FDR of the SU tests based on and via (2.16).

Proof.

Let and be the critical values of the rejection curves and , respectively, defined by (2.16). Define and as the number of rejections of the SU test based on and , respectively. It is easy to see that and hence almost surely holds. Using the technique of Remark 7.3 we obtain

since is non-decreasing and the configuration is least favorable for the FDR, cf. Benjamini and Yekutieli [2]. ∎

Remark 7.4.

Consider the BI Model and let the false -values be independent and stochastically smaller than the uniform distribution. Let denote the FDR under uniformly distributed false -values. If we replace in Lemma 7.5 by a convex rejection curve which is a upper bound of , it is easy to see by similar arguments that

| (7.30) |

holds for the FDR of the SU tests based on and , since is non-increasing for the critical values corresponding to the rejection curve . According to Benjamini and Yekutieli [2], here the uniform distribution is least favorable for the FDR under stochastically smaller -values.

If (2.4) is non-increasing, then the -values are called to be negative regression dependent on the subset of true null hypotheses (NRDS). Under this assumption the lower bound in (4.1) and Lemma 7.2 (b)(i) stay true, see Heesen [16] for instance.

Proof of Theorem 5.2. By Gontscharuk [12, Theorem 3.10] it is well known that

holds for tests with critical values (4.5), see also Heesen [16] Lemma 2.29. The inequality also follows from the technique used in Remark 7.3. Hence

| (7.31) |

In the proof of Theorem 5.1 we already showed that is attained by for some . Thus, to show ”” on the left hand side in (7.31) it suffices to show that for all such there is some sequence of distributions so that converges to . Therefore, let us now consider sequences of configurations with . Along the lines of the proof of Theorem 5.1 we have

| (7.32) |

Observe that holds since . Moreover, holds since for all for some . Now with and as in (7.20) and (7.21) in the proof of Theorem 5.1 we have

by dominated convergence. Hence we have “=” in (7.31) since the above formula holds for all and the representation (5.6).

7.5 Proofs of Section 6

Proof of Theorem 6.1. First observe that obviously holds if . Thus, without loss of generality let almost surely for all . Conditioned under we obtain by Lemma 7.1 (a) and (6.5)

| (7.33) |

for the reverse martingale model since the conditional case is also included. Thus by integration

holds for every and the statement follows by (6.7).

Proof of Proposition 6.1. Introduce the set . An inspection of the proof of Lemma 6.1 (given below) yields

restricted on . Define , then

follows. First, let us consider case (ii). For each we have

| (7.34) |

Observe next that is tight and we consider an arbitrary distributional cluster point of . The appertaining subsequence is for convenience also denoted by , i.e. in distribution. Note that and

hold. Now Jensen’s inequality implies

when . Since is strictly convex we have a.e. Since was an arbitrary cluster point we conclude in -probability. This statement implies the result

In case (i) the proof is similar. Note that the assumption then implies

and we may proceed as in (7.34)

Proof of Remark 6.1. Observe that

holds, where the right hand side converges by (6.10) in probability w.r.t. the conditional convergence.

Proof of Theorem 6.2. Conditioned under we directly obtain by Lemma 7.1 (b) and (6.6) that

| (7.35) |

holds and the statement follows by the same arguments as in the proof of Theorem 6.1.

Proof of Lemma 6.1. Conditioned under , and we have exactly true -values smaller or equal to where is a fixed number. Without restriction we assume since everything is obviously fine for the excluded cases. Let us now consider new rescaled -values , defined by

When a new -values corresponds to a true null hypothesis it is again uniformly distributed on and is a reverse martingale with respect to the reverse filtration under the above conditional assumption. The exact positions of the true -values in does not matter for our considerations. We now apply Lemma 7.1 (a) for the SU multiple test with critical values

on the ’s. The data dependent level only depends by assumption (A1) on the information given by . Conditionally under we have a regular non data dependent SU procedure on the ’s. Let and denote the number of rejections and false rejections respectively by the above SU test. Observe that

| (7.36) |

Now observe that

and hence since both tests, belonging to and , are rejecting the same hypotheses. Thus by (7.36) we get

Proof of Proposition 6.2. Choose and for all . Thus and . The exact FDR formula (6.11) yields

where stands for the value of the estimator when for all . Thus holds. By our assumption we have .

We need the following “balayage“ lemma for the proof of Theorem 6.3.

Lemma 7.6.

Let be a convex function and let be a distribution on , where denotes the Dirac distribution on . Then and hold for the distribution

Proof.

obviously holds by the definition of . Then by the convexity of we have

∎

Proof of Theorem 6.3. Throughout the condition (6.12) will be verified. For the portion of true -values introduce the quantities

| (7.37) |

with . Whenever holds select one true -value . Observe that the are conditionally independent given . Under that condition we have for (6.14)

In the next step we are going to condition under . Note that then is a distributed random variable. By Lemma 7.6, can be substituted by the worst case random variable , i.e.

If we proceed times we arrive at the upper bound

since is increasing for and holds. Moreover, holds and the last inequality follows by the well known result for Binomial variables

| (7.38) |

Proof of Example 6.1. The proof for the FWER is mostly included in the proof of Theorem 6.3. Notice first that

| (7.39) |

always holds under our assumptions, where is a binomial variable. Thus, we have equality in (6.11). By an inspection of the proof above we arrive at a sequence of equality with

| (7.40) |

and (7.38) can be applied.

Acknowledgements

The authors are grateful to Helmut Finner and Julia Benditkis for many stimulating discussions and to Veronika Gontscharuk who provided a program for the exact computation of the SU FDR for arbitrary critical values in a DU setting, see Figure 1. Furthermore, the authors gratefully acknowledge the helpful suggestions of the referees, who also referred to [14], the associate editor and editor. The authors also wishes to thank the Deutsche Forschungsgemeinschaft, DFG, for financial support.

References

- [1] Benjamini, Y. and Hochberg, Y. (1995). Controlling the false discovery rate: A practical and powerful approach in multiple testing. J. Roy. Stat. Soc. B 57 289-300.

- [2] Benjamini, Y. and Yekutieli, D. (2001). The control of the false discovery rate in multiple testing under dependency. Ann. Stat. 10 1165-1188.

- [3] Benjamini, Y. and Krieger, A. M. and Yekutieli, D. (2006). Adaptive linear step-up procedures that control the false discovery rate. Biometrika 93, (3) 491-507.

- [4] Blanchard, G. and Roquain, E. (2009). Adaptive False Discovery Rate Control under Independence and Dependence. J. Mach. Learn. Res. 29 2837-2871.

- [5] Blanchard, G. and Roquain, E. (2008). Two simple sufficient conditions for FDR control. Electron. J. Stat. 2 963-992.

- [6] Efron, B., Tibshirani, R. and Storey, D. (2001). Empirical Bayes Analysis of a Microarray Experiment. J. Am. Stat. Soc. 96 1151-1160.

- [7] Finner, H., Gontscharuk, V., Dickhaus, T. (2012). False discovery rate control of step-up-down tests with special emphasis on the asymptotically optimal rejections curve. Scand. J. Stat. 39 382-397.

- [8] Finner, H., and Gontscharuk, V. (2009). Controlling the familywise error rate with plug-in estimator for the proportion of true null hypotheses. J. R. Stat. Soc. B 71 1031-1048.

- [9] Finner, H., Dickhaus, T. and Roters, M. (2009). On the false discovery rate and an asymptotically optimal rejection curve. Ann. Stat. 37 596-618.

- [10] Finner, H. and Roters, M. (2001). On the false discovery rate and expected type I errors. Biometrical J. 43 985-1005.

- [11] Gavrilov, Y., Benjamini, Y. and Sarkar, S.K. (2009). An adaptive step-down procedure with proven FDR control under independence. Ann. Stat. 37 619-629.

-

[12]

Gontscharuk, V. (2010).

Asymptotic and exact results on FWER and FDR in multiple hypothesis testing.

Diss. PhD thesis, Heinrich-Heine-Universität Düsseldorf.

http://docserv.uni-duesseldorf.de/servlets/DocumentServlet?id=16990 - [13] Guo, W., Rao, M. B. (2008). On optimality of the Benjamini-Hochberg procedure for the false discovery rate. Statist. Probab. Lett. 78, (14) 2024-2030.

- [14] Guo, W. and Sarkar, S. K. (2013). Adaptive Controls of FWER and FDR Under Block Dependence. Unpublished manuskript web.njit.edu/wguo/Guo%20&%20Sarkar%202012.pdf

- [15] Heesen, P. and Janssen, A. (2014). Dynamic adaptive multiple tests with finite sample FDR control. arXiv:1410.6296v1, October 2014.

- [16] Heesen, P. (2014). Adaptive step up tests for the false discovery rate (FDR) under independence and dependence Ph.D. thesis, Heinrich-Heine-Universität Düsseldorf, Germany.

- [17] Liang, K. and Nettleton, D. (2012). Adaptive and dynamic adaptive procedures for false discovery rate control and estimation. J. Roy. Stat. Soc. B 74(1) 163-182.

- [18] Marshall, A. W. and Olkin, I. (1967). A multivariate exponential distribution. J. Amer. Stat. Assoc. 62 (317) 30-44.

- [19] Meskaldji, D. E., Thiran, J.-P. and Morgenthaler, S. (2013). A comprehensive error rate for multiple testing. arXiv:1112.4519v4, July 2013.

- [20] Sarkar, S. K. (2002). Some results on false discovery rate in stepwise multiple testing procedures. Ann. Statist. 30 239-257.

- [21] Sarkar, S. K. (2008). On Methods controlling the False Discovery Rate Sankhya Series A, 70 135-168.

-

[22]

Scheer, M. (2013).

Controlling the Number of False Rejections in Multiple Hypotheses Testing.

Diss. PhD thesis, Heinrich-Heine-Universität Düsseldorf.

http://docserv.uni-duesseldorf.de/servlets/DocumentServlet?id=23691 - [23] Storey, J. D. (2002). A direct approach to false discovery rates. J. Roy. Stat. Soc. B 64 479-498.

- [24] Storey, J. D., Taylor, J. E. and Siegmund, D. (2004). Strong control, conservative point estimation and simultaneous conservative consistency of false discovery rates: a unified approach. J. Roy. Stat. Soc. B 66 187-205.

- [25] Zeisel, A. and Zuk, O. and Domany, E. (2011). FDR control with adaptive procedures and FDR monotonicity. Ann. Appl. Stat. 5 (2A) 943-968.