Selecting the number of principal components: estimation of the true rank of a noisy matrix

Abstract

Principal component analysis (PCA) is a well-known tool in multivariate statistics. One significant challenge in using PCA is the choice of the number of components. In order to address this challenge, we propose an exact distribution-based method for hypothesis testing and construction of confidence intervals for signals in a noisy matrix. Assuming Gaussian noise, we use the conditional distribution of the singular values of a Wishart matrix and derive exact hypothesis tests and confidence intervals for the true signals. Our paper is based on the approach of Taylor, Loftus and Tibshirani (2013) for testing the global null: we generalize it to test for any number of principal components, and derive an integrated version with greater power. In simulation studies we find that our proposed methods compare well to existing approaches.

keywords:

[class=MSC]keywords:

arXiv:1410.8260 \startlocaldefs \endlocaldefs

, and

t1Supported by NSF Grant DMS-12-08857 and AFOSR Grant 113039. t2Supported by NSF Grant DMS-99-71405 and NIH Contract N01-HV-28183.

1 Introduction

1.1 Overview

Principal component analysis (PCA) is a commonly used method in multivariate statistics. It can be used for a variety of purposes including as a descriptive tool for examining the structure of a data matrix, as a pre-processing step for reducing the dimension of the column space of the matrix (Josse and Husson, 2012), or for matrix completion (Cai, Candès and Shen, 2010).

One important challenge in PCA is how to determine the number of components to retain. Jolliffe (2002) provides an excellent summary of existing approaches to determining the number of components, grouping them into three branches: subjective methods (e.g., the scree plot), distribution-based test tools (e.g., Bartlett’s test), and computational procedures (e.g., cross-validation). Each branch has advantages as well as disadvantages, and no single method has emerged as the community standard.

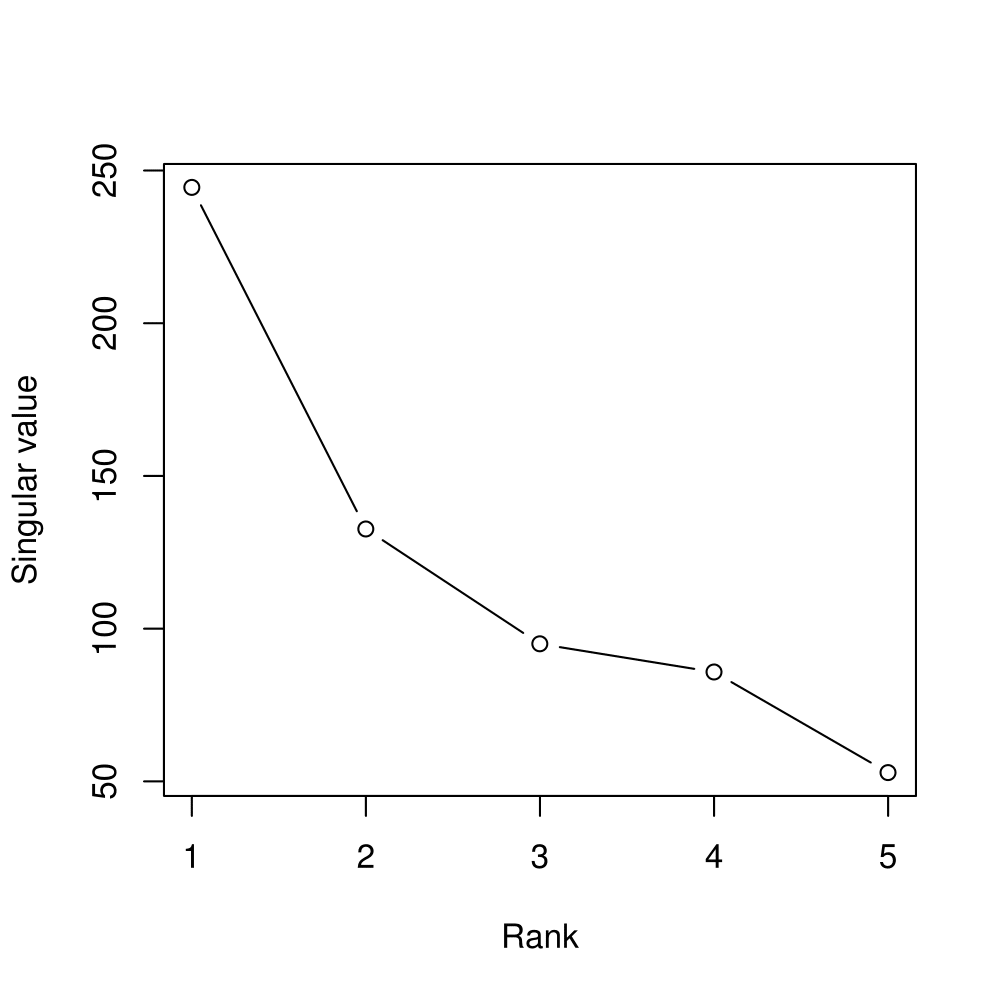

Figure 1 offers a scree plot as an example. The data are five test scores from 88 students (taken from Mardia, Kent and Bibby (1979)); the figure shows the five singular values in decreasing order.

The “elbow” in this plot seems to occur at rank two or three, but it is not clearly visible. We revisit this example with our proposed approach in Section 5.3.

In this paper, we propose a statistical method for determining the rank of the signal matrix in a noisy matrix model. The estimated rank here corresponds to the number of components to retain in PCA. This method is derived from the conditional Gaussian-based distribution of the singular values, and yields exact p-values and confidence intervals.

1.2 Related work

Our method is motivated by the Kac-Rice test (Taylor, Loftus and Tibshirani, 2013), an exact method for testing and constructing confidence intervals for signals under the global null hypothesis in adaptive regression. Our work corresponds to the Kac-Rice test under the global null scenario, in a penalized regression minimizing the Frobenius norm with a nuclear norm penalty. In this paper, we extend the test and confidence intervals to the general case with improved power. The resulting statistic uses the survival function of the conditional distribution of the eigenvalues of a Wishart matrix.

In the context of inference based on the distribution of eigenvalues, Muirhead (1982) and, more recently, Kritchman and Nadler (2008) have proposed methods for testing essentially the same hypothesis as in this paper. Both Muirhead (1982) and Kritchman and Nadler (2008) benefit from an asymptotic distribution of the test statistic: Muirhead (1982) forms a likelihood ratio test with the asymptotic Chi-square distribution. Kritchman and Nadler (2008) use the Tracy-Widom law, which is the asymptotic distribution of the largest eigenvalue of a Wishart matrix, incorporating the result of Johnstone (2001). We provide a method for constructing confidence intervals in addition to hypothesis testing, with the procedures being exact.

1.3 Organization of the paper

The rest of the paper is organized as follows. In Section 2, we propose methods based on the distribution of eigenvalues of a Wishart matrix. Section 2.1 introduces the main points of the Kac-Rice test (Taylor, Loftus and Tibshirani, 2013) from which we derive our proposals. Then, we suggest a procedure for hypothesis testing of the true rank of a signal matrix in Section 2.2. Our method for constructing exact confidence intervals of signals is described in Section 2.3.

In Section 3, we propose a method for estimating the rank of a signal matrix from the hypothesis tests. We illustrate sequential hypothesis testing procedure for determining the matrix rank, based on a proposal of G Sell et al. (2013).

Section 4 introduces a data-driven method for estimating the noise level. Our suggested method is analogous to cross-validation. In order to apply cross-validation to a data matrix, we use a method suggested by Mazumder, Hastie and Tibshirani (2010).

Section 5 provides additional examples of the suggested methods. In Section 5.1, simulation results with estimated noise level are presented. Section 5.2 shows simulation results with non-Gaussian noise to check for robustness. We revisit the real data example introduced in Figure 1 in Section 5.3. The paper concludes with a brief discussion in Section 6.

2 A Distribution-Based Method

Throughout this paper, we assume that the observed data matrix is the sum of a low-rank signal matrix and a Gaussian noise matrix as follows:

that is,

| (2.1) |

In this paper, without loss of generality, we assume that . We focus on the estimation of , the rank of the signal matrix , and the construction of confidence intervals for the signals in .

We first review the global null test and confidence interval construction of the first signal of Taylor, Loftus and Tibshirani (2013) and its application in matrix denoising problem in Section 2.1. Then we extend the global null test to a general test procedure for testing in Section 2.2 and describe how to construct confidence intervals for the largest signal parameters in Section 2.3.

2.1 Review of the Kac-Rice test

We briefly discuss the framework of Taylor, Loftus and Tibshirani (2013) and its application to a matrix denoising problem, which we extend further later in this paper. Section 2.1.1 covers the testing procedure for a class of null hypothesis. This null hypothesis corresponds to the global null in our matrix denoising problem. In Section 2.1.2, we construct a confidence interval for the largest signal.

2.1.1 Global null hypothesis testing

Taylor, Loftus and Tibshirani (2013) derived the Kac-Rice test, an exact test for a class of regularized regression problems of the following form:

| (2.2) |

with an outcome , a predictor matrix and a penalty term with a regularization parameter . Assuming that the outcome is generated from

the Kac-Rice test (Taylor, Loftus and Tibshirani, 2013) provides an exact method for testing

| (2.3) |

under the assumption that the penalty function is a support function of a convex set . i.e.,

When applied to a matrix denoising problem of a popular form, (2.3) becomes a global null hypothesis:

| (2.4) |

where denote the singular values of . Here are the details. For an observed data matrix , a widely used method to recover the signal matrix in (2.1) is to solve the following criterion:

| (2.5) |

where and denote a Frobenius norm and a nuclear norm respectively. The nuclear norm plays an analogous role as an penalty term in lasso regression (Tibshirani, 1996). The objective function (2.5) falls into the class of regression problems described in (2.2), with the predictor matrix being and the penalty function being

with where denotes a spectral norm. We can therefore directly apply the Kac-Rice test with the resulting test statistic as follows, under the assumed model discussed in the beginning of Section 2:

| (2.6) |

where denote the observed singular values of . The test statistic in (2.6) is uniformly distributed under the null hypothesis (2.4) and provides a p-value for testing the global null hypothesis: the value represents the probability of observing more extreme values than under the null hypothesis.

Viewed differently, the test statistic corresponds to a conditional survival function of the largest observed singular value conditioned on all the other observed singular values . The integrand of coincides with the conditional distribution of the largest singular value of a central Wishart matrix up to a constant (James, 1964). Its denominator acts as a normalizing constant because the domain of the largest singular value is . A small magnitude of implies large compared to and thus supports .

2.1.2 Confidence intervals for the largest signal

Along with the Kac-Rice test mentioned in Section 2.1.1, a procedure for constructing an exact confidence interval for the leading signal in adaptive regression is suggested in Taylor, Loftus and Tibshirani (2013). As in Section 2.1.1, by applying the result of Taylor, Loftus and Tibshirani (2013) to our matrix denoising setting, we can generate an exact confidence interval for which is defined as follows:

where is a singular value decomposition of with for , and and are the first column vectors of and respectively. It is desirable to directly find the confidence interval for instead of , however, as is unobservable, is the “best guess” of the unit vector associated with in its direction.

To discuss the procedure in detail, in the matrix denoising problem of (2.5), the result from Taylor, Loftus and Tibshirani (2013) yields an exact conditional survival function of around as follows:

| (2.7) |

The test statistic for testing in Section 2.1.1 conforms to (2.7) when it is true that . The suggested procedure for constructing the level confidence interval is as follows:

| (2.8) |

Since in (2.7) is uniformly distributed, we observe that

and thus (2.8) generates an exact level confidence interval.

2.2 General hypothesis testing

In this section, we extend the test for the global null in Section 2.1.1 to a general test which investigates whether there exists the largest signal in .

Suppose that we want to test the hypothesis

| (2.9) | |||||

for . For , the null hypothesis in (2.9) corresponds to a global null as in Section 2.1.1. With the signal matrix is full rank under the alternative hypothesis, and the test becomes unidentifiable from a low rank signal matrix with higher noise level problem. Thus, we do not consider the case of .

One of the most straightforward approaches for extending the global test (2.6) to testing (2.9) for would be to apply it sequentially. That is, we can remove the first observed singular values of and then apply the test to the remaining singular values, in analogy to other methods dealing with essentially the same hypothesis testing (Muirhead, 1982; Kritchman and Nadler, 2008).

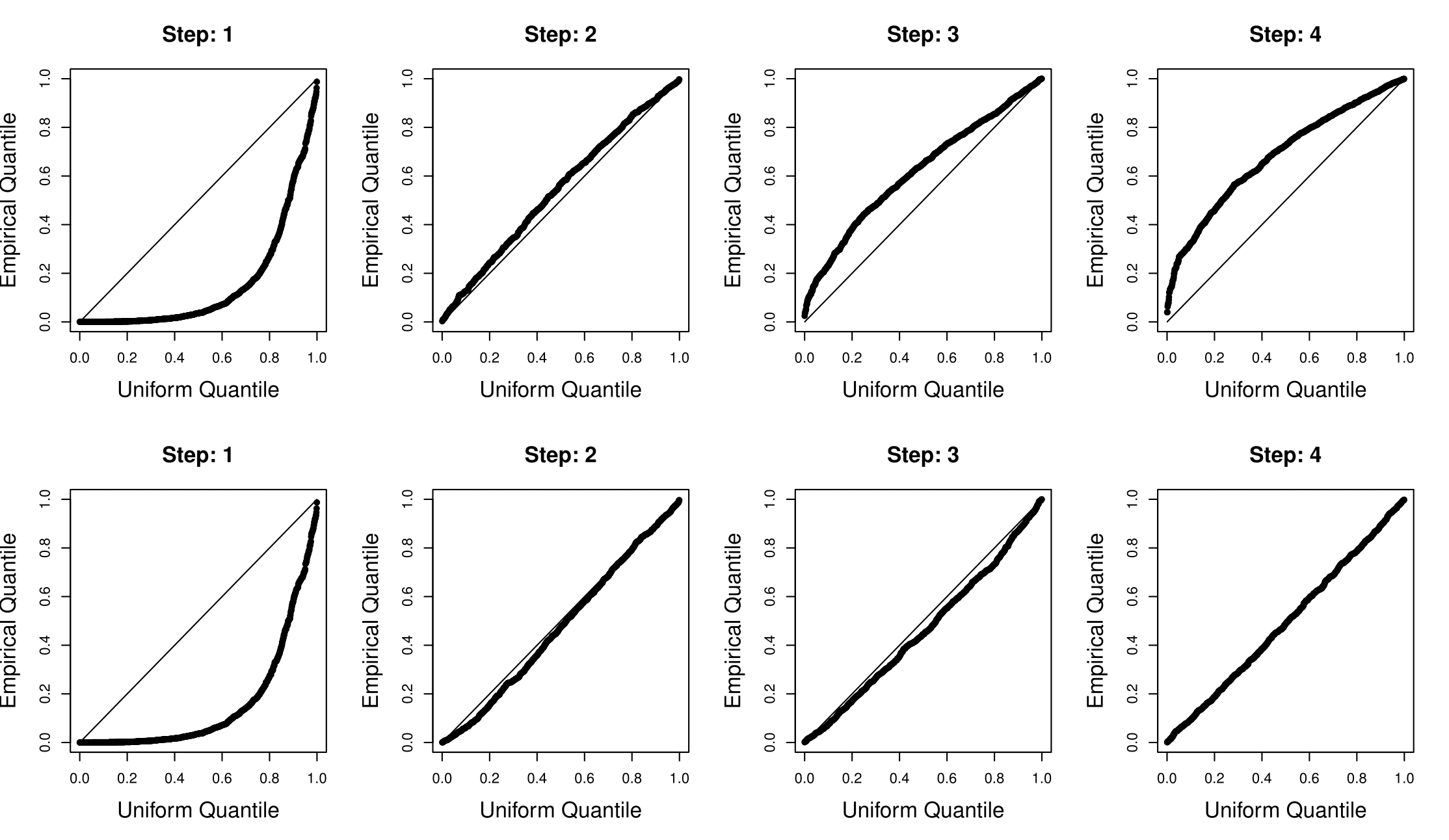

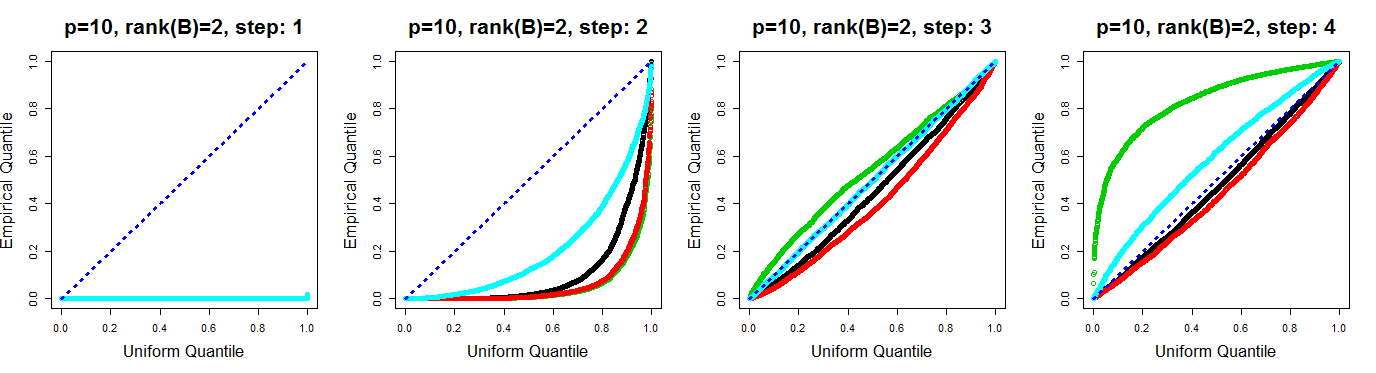

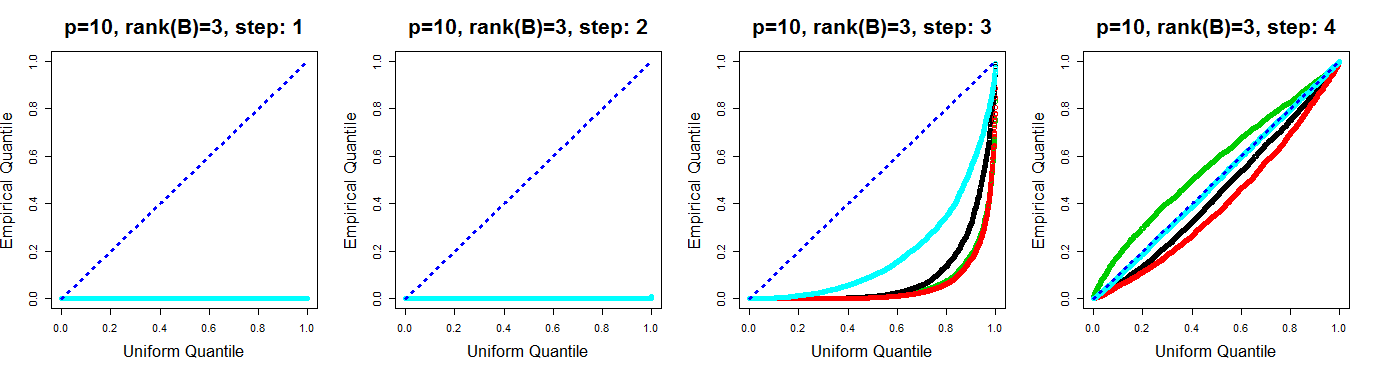

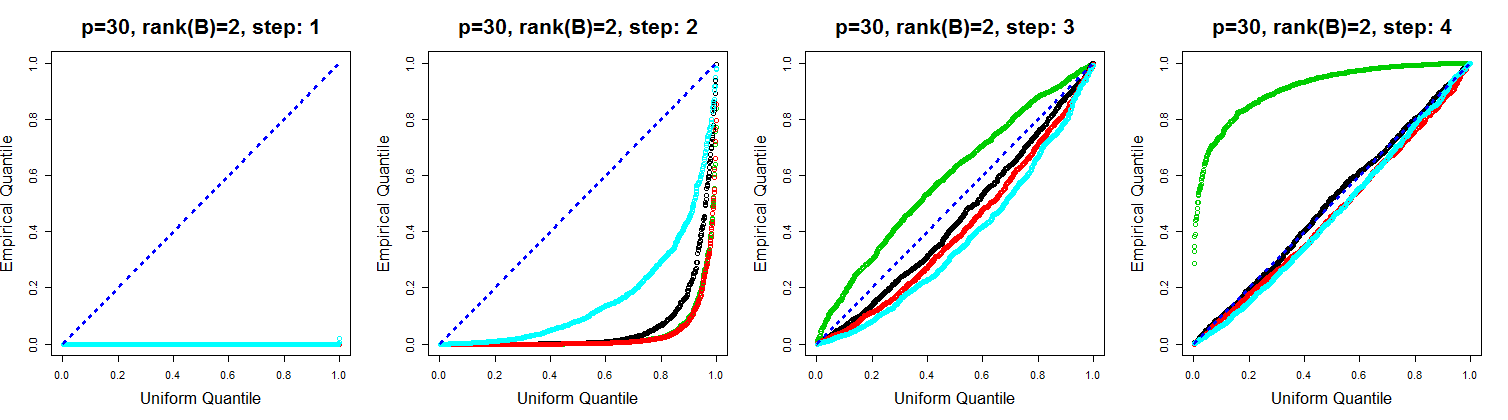

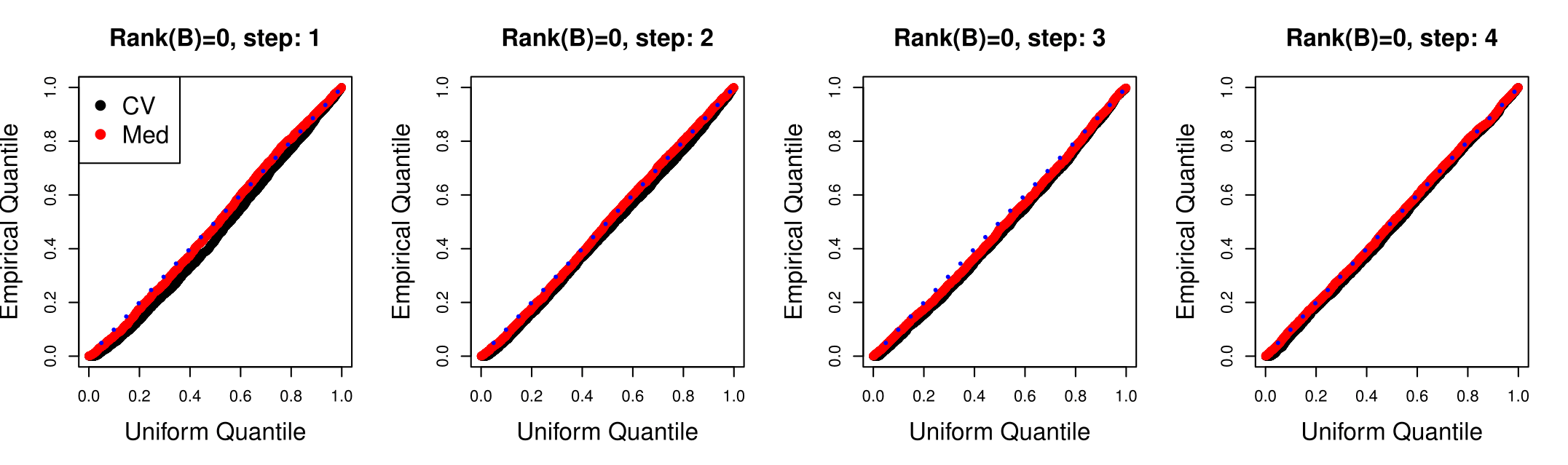

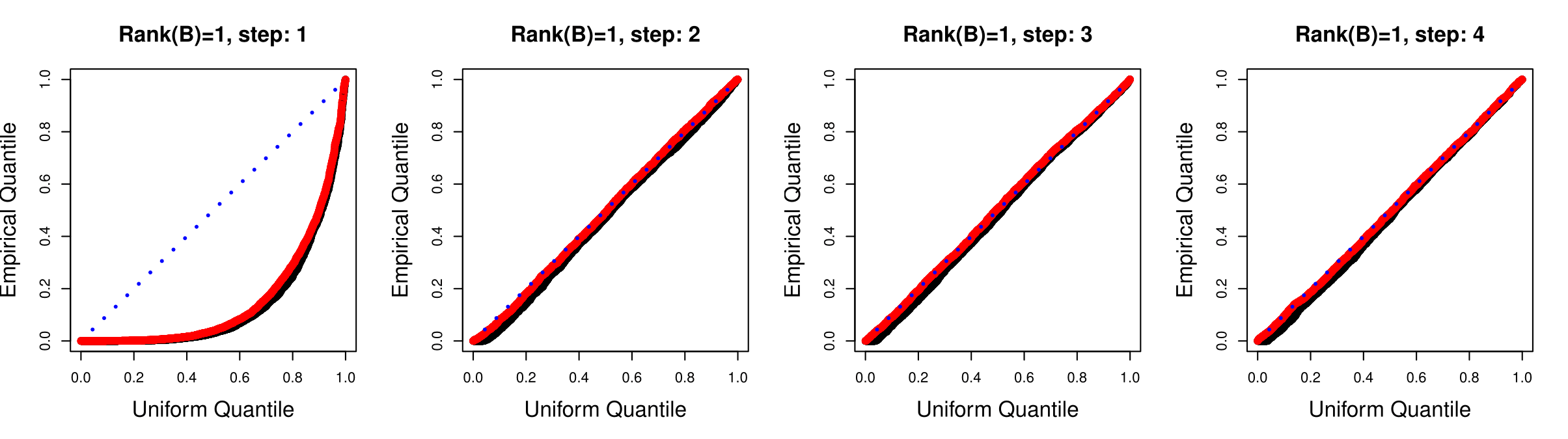

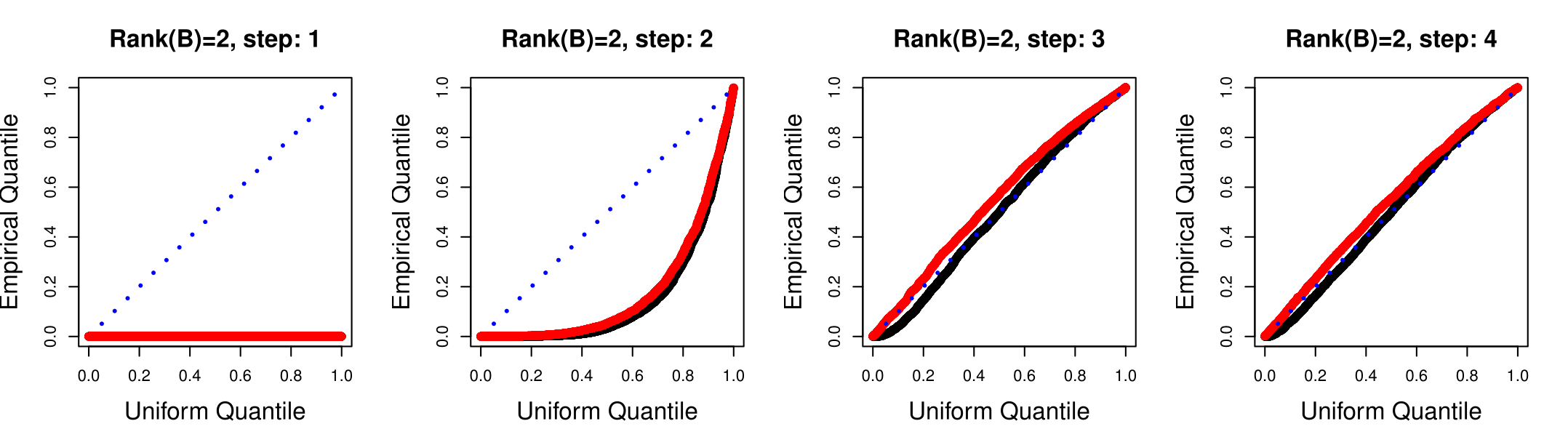

How well does this work? Figure 2 shows an example. Here , and there is a rank one signal of moderate size. The top panels show quantile-quantile plots of the p-values for the sequential Kac-Rice test versus the uniform distribution. We see that the p-values are small when the alternative hypothesis is true (step 1), and then fairly uniform for testing rank versus (step 2) as desired, which is the first case in which the null hypothesis is true. However the test becomes more and more conservative for higher steps, although the p-values are generated under the null distributions. The conservativeness of these p-values can lead to potential loss of power. One of the reasons for this conservativeness is that, at step , for example, the test does not consider that the two largest singular values have been removed. The test instead plugs the 3rd largest singular value into the place of the 1st largest singular value. As the 1st and the 3rd largest singular values do not have the same distribution, the sequential Kac-Rice test at is no longer uniformly distributed, and so results in conservative p-values.

The plots in the bottom panel come from our proposed conditional singular value (CSV) test, to be described in Section 2.2.1. It follows the uniform distribution quite well for all null steps. For testing at the step, the CSV method takes it into account that our interest is the signal by conditioning on the first singular values in its test statistic.

Section 2.2.1 presents the CSV test procedure in detail. In Section 2.2.2, we propose an integrated version of the CSV which has better power. Simulation results of the proposed procedures are illustrated in Section 2.2.3.

2.2.1 The Conditional Singular Value test

In this section, we introduce a test in which the test statistic has an “almost exact” null distribution under in (2.9) for . Writing the singular value decomposition of a signal matrix as , and submatrices of a matrix by where and , the test of (2.9) can be rewritten as

| (2.10) |

since .

As an alternative to (2.9) or (2.2.1), we derive an exact test statistic for the following hypothesis:

| (2.11) | |||

where we write the singular value decomposition of the data matrix as . The test (2.11) investigates whether there remains signals in the residual space of of which the first singular values are removed. Under of (2.2.1), when we have strong signals in , approaches as in (2.11).

The proposed test procedure is as follows:

Test 2.1 (Conditional Singular Value test).

With a given level , and the following test statistic,

| (2.12) |

where , we reject if and accept otherwise.

Analogous to (2.6), plays the role of a p-value. It compares the relative size of ranging between , and a small value of implies a large value of , supporting the hypothesis . We refer to this procedure as the conditional singular value test (CSV). Theorem 2.1 shows that this test is exact under (2.11). The test statistic is a conditional survival function of the singular value under : the probability of observing larger values of the singular value than the actually observed , given and all the other singular values. The proofs of this and other results are given in the Appendix.

Theorem 2.1.

then

The bottom panels of Figure 2 confirm the claimed Type I error property of the procedure. After the true rank of one, the p-values are all close to uniform.

2.2.2 The Integrated Conditional Singular Value test

As a potential improvement of the CSV, we introduce an integrated version of . Our aim is to achieve higher power in detecting signals in compared to the ordinary CSV. Here we integrate out with respect to small singular values (). The resulting statistic becomes a function of , only the first singular values of , while the ordinary CSV test statistic is a function of all the singular values of . The idea is that conditioning on less can lead to greater power. The suggested test statistic is as follows:

| (2.13) |

where

| (2.14) | |||

Our proposed Integrated Conditional Singular Value (ICSV) test is as follows:

Test 2.2 (ICSV test).

With a given level , we reject if and accept otherwise, where is as defined in (2.13).

As in the test, works as a p-value for the test, and also it is an exact test for (2.11), as is shown in Theorem 2.2. It is a survival function of the singular value given and the first singular values under .

Theorem 2.2.

then

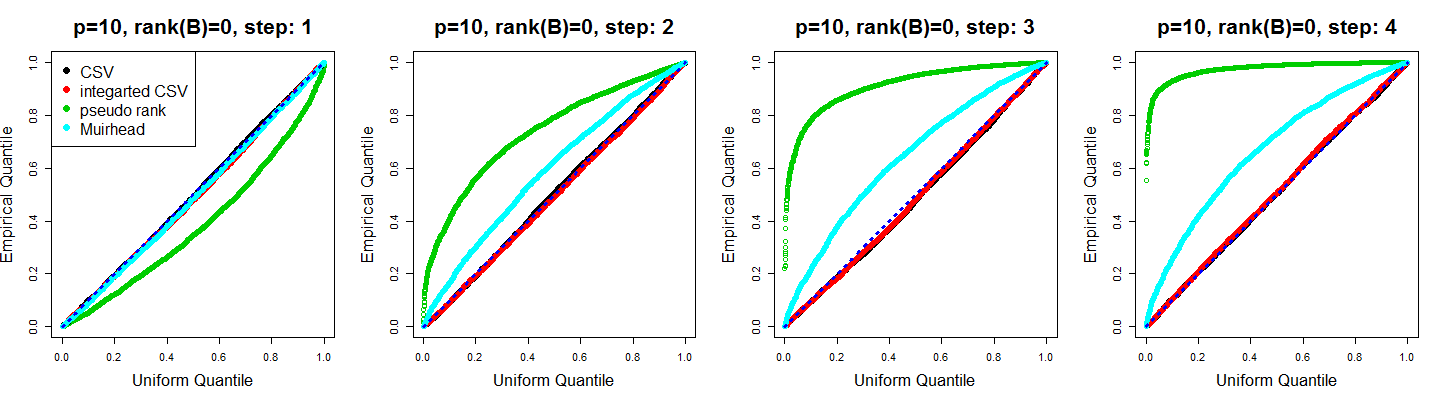

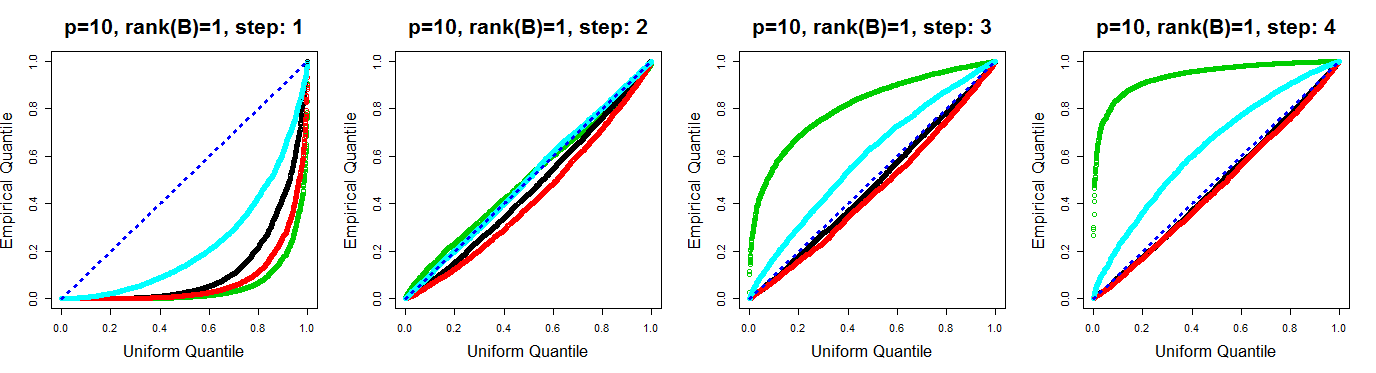

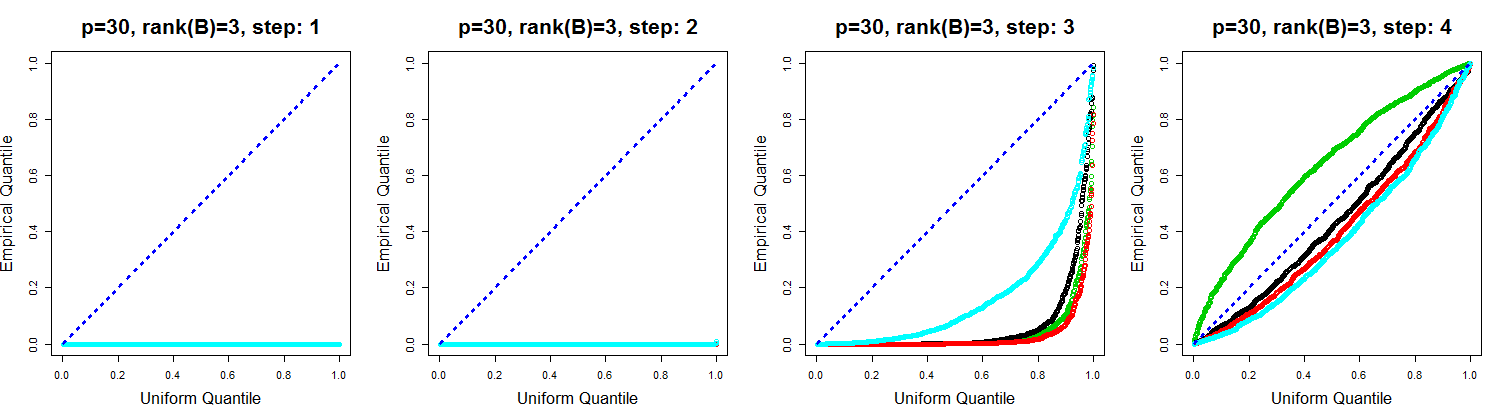

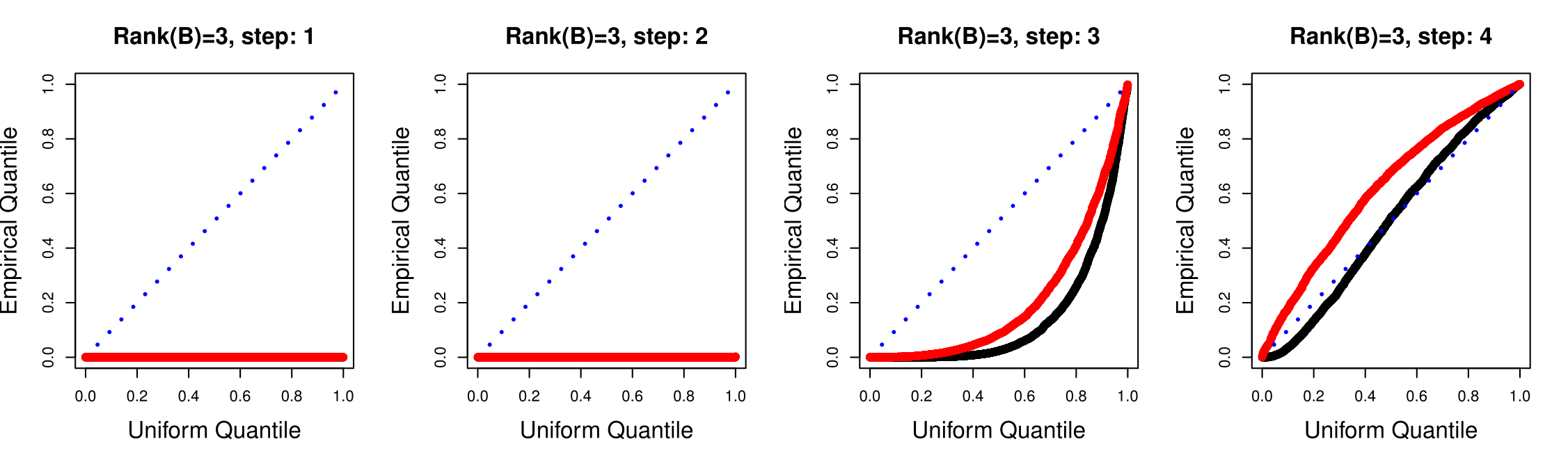

Figure 3 demonstrates that the ICSV procedure achieves higher power than the ordinary CSV.

In this paper, we use importance sampling to evaluate the integral in (2.13) with samples drawn from the eigenvalues of a Wishart matrix. As the computational cost increases sharply with large , we are currently unable to compute this test for beyond say 30 or 40. An interesting open problem is the numerical approximation of this integral, in order to scale the test to larger problems. We leave this as future work.

2.2.3 Simulation Examples

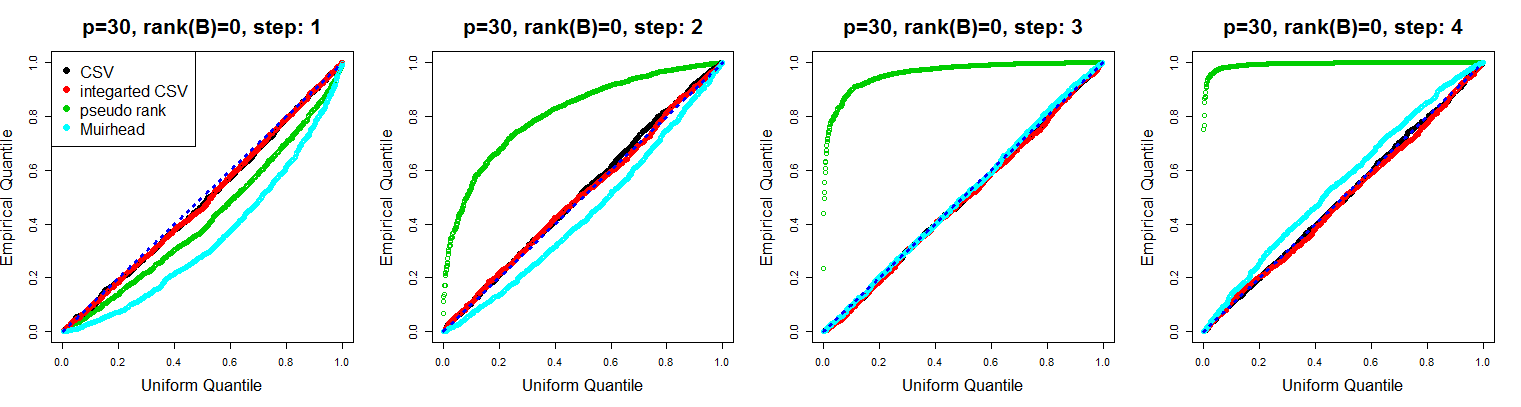

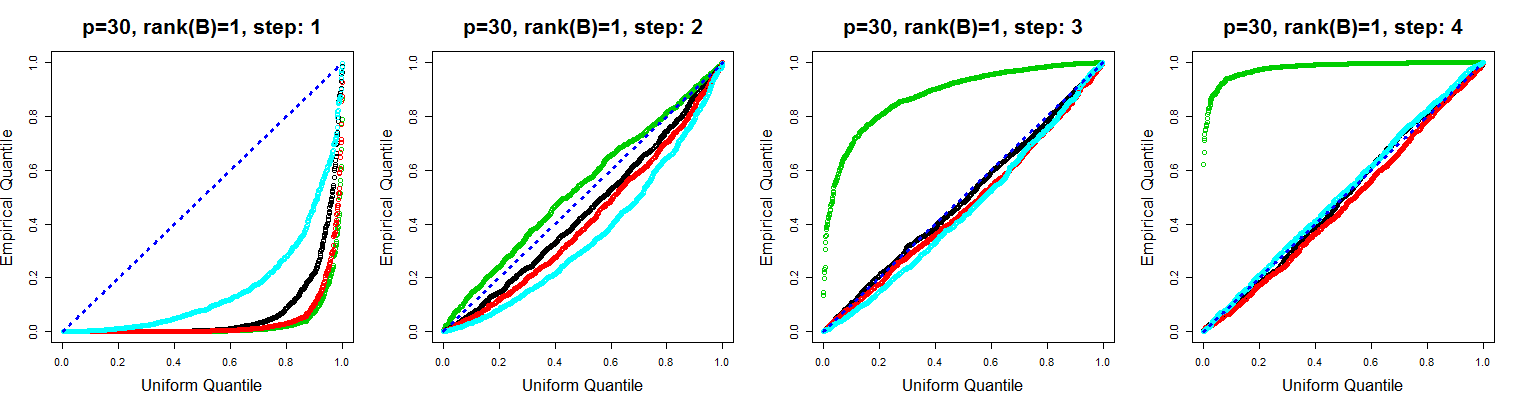

In this section, we present results of the CSV and the ICSV on simulated examples. We compare the performance of these proposed methods with those in Kritchman and Nadler (2008) and Muirhead (1982)[Theorem 9.6.2] mentioned in Section 1.2, which we refer as the pseudorank and the Muirhead’s method respectively:

Test 2.3 (Pseudorank).

With a given level , and following and ,

we reject if

where is the upper -quantile of the Tracy-Widom distribution.

Test 2.4 (Muirhead’s method).

With a given level , and defined as

we reject if

where , and denotes the upper quantile of the distribution with degree .

We investigate cases with i.i.d Gaussian noise entries with . The observed data matrix has the signal matrix formed as follows:

| (2.15) |

where with , and , are rotation operators generated from a singular value decomposition of random Gaussian matrix with entries. The signals of increase linearly. The constant determines the magnitude of the signals. From , a phase transition phenomenon is observed when in which the expectation of the largest singular value of starts to reflect the signal (Nadler, 2008).

We illustrate two cases of and with fixed to . For both cases, we set and . For and , we evaluate the procedure through and repetitions respectively. The true value of the noise level is used for all testing procedures.

Figures 3 and 4 present quantile-quantile plots of the expected (uniform) quantiles versus the observed quantiles of p-values. Under , the ICSV test shows improved power compared to the CSV, and close to that of pseudorank. Both the CSV and the ICSV show stronger power than Muirhead’s test. Under , both the CSV and the ICSV quantiles nearly agree with the expected quantiles and provide almost exact p-value, as the theory predicts. Pseudorank estimation becomes strongly conservative for further steps, and the results of Muirhead’s test depend on the size of and .

|

|

|

|

|

|

|

|

2.3 Confidence interval construction

Here we generalize the exact confidence interval construction procedure of the largest singular value in (2.8) to the signal parameter for any .

We define the signal parameter as follows:

| (2.16) |

where and are the column vector of and respectively. We propose an approach to construct an exact level confidence interval of . Our proposed procedure is as follows:

| (2.17) |

where

We can find the boundary points of using bisection. Theorem 2.3 below shows that is an exact level confidence interval. This procedure addresses the general case of (2.12): tests whether .

Theorem 2.3.

is uniformly distributed when .

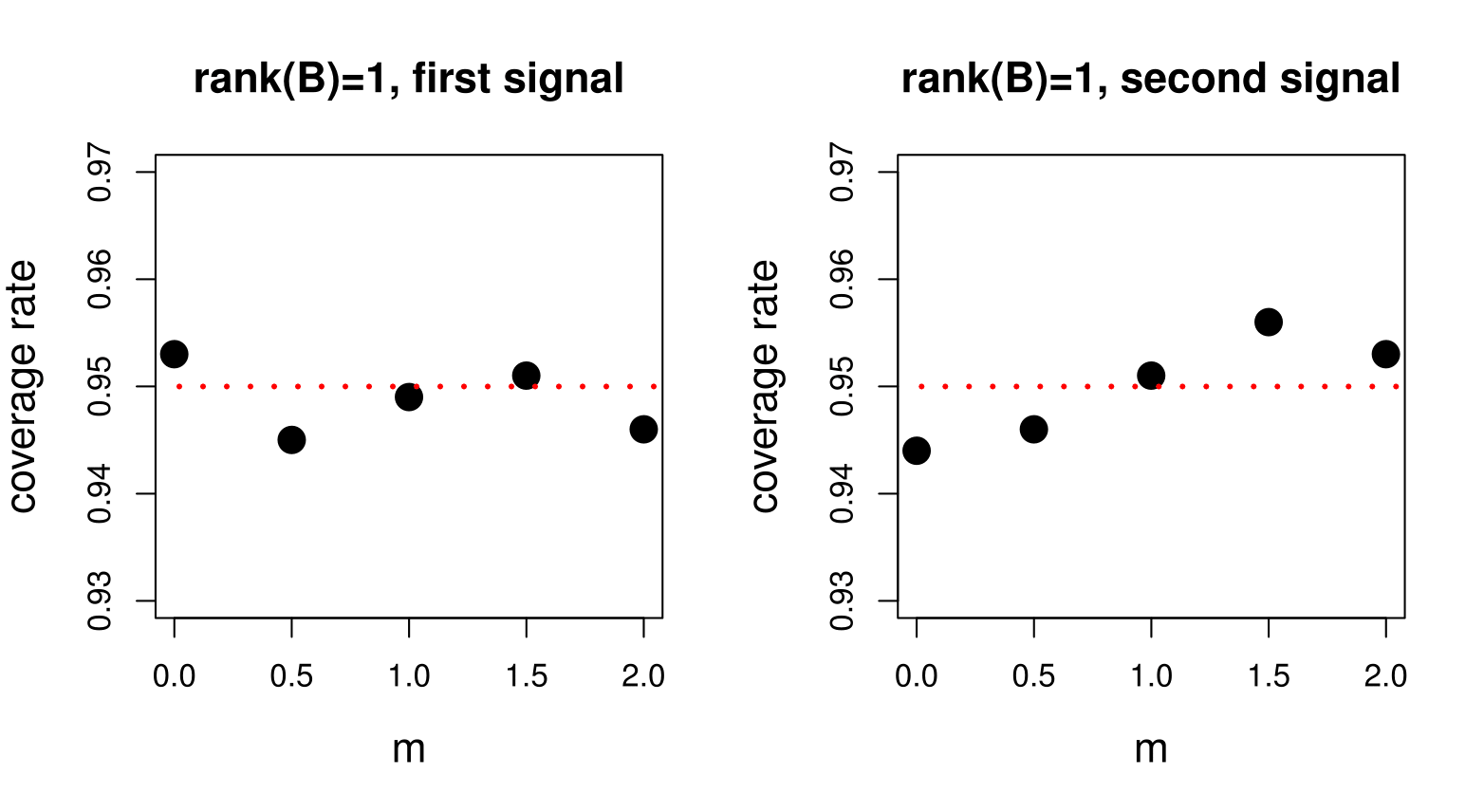

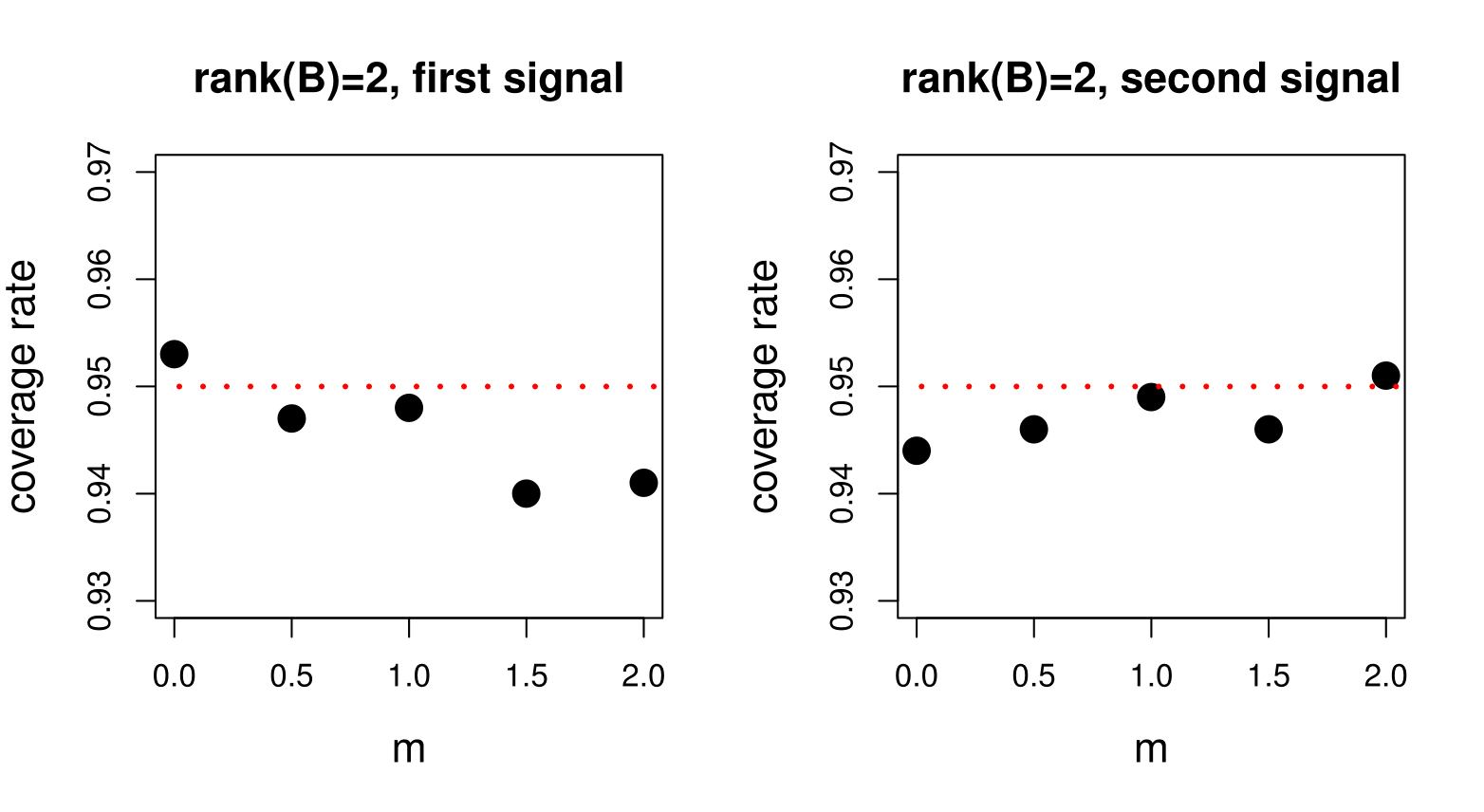

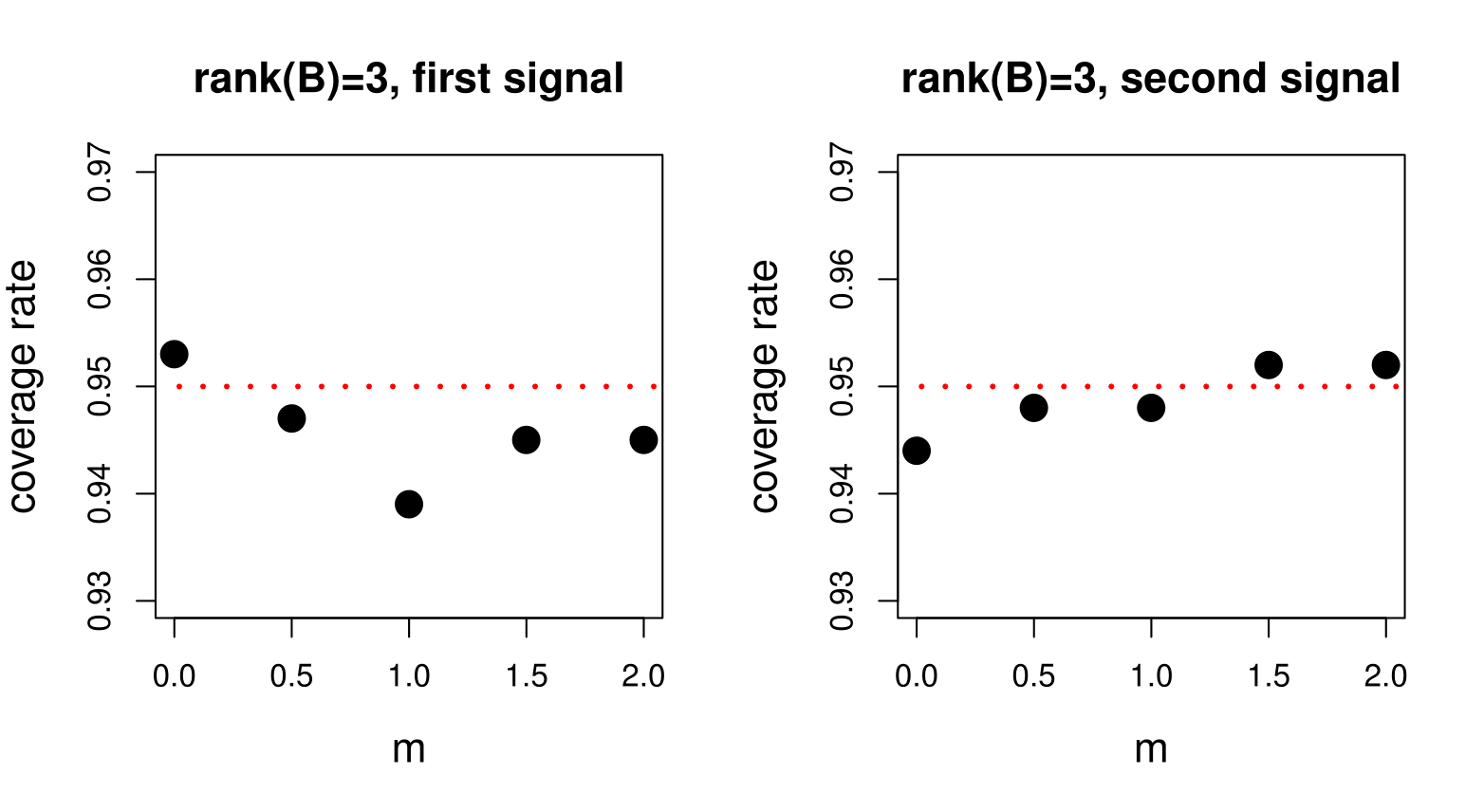

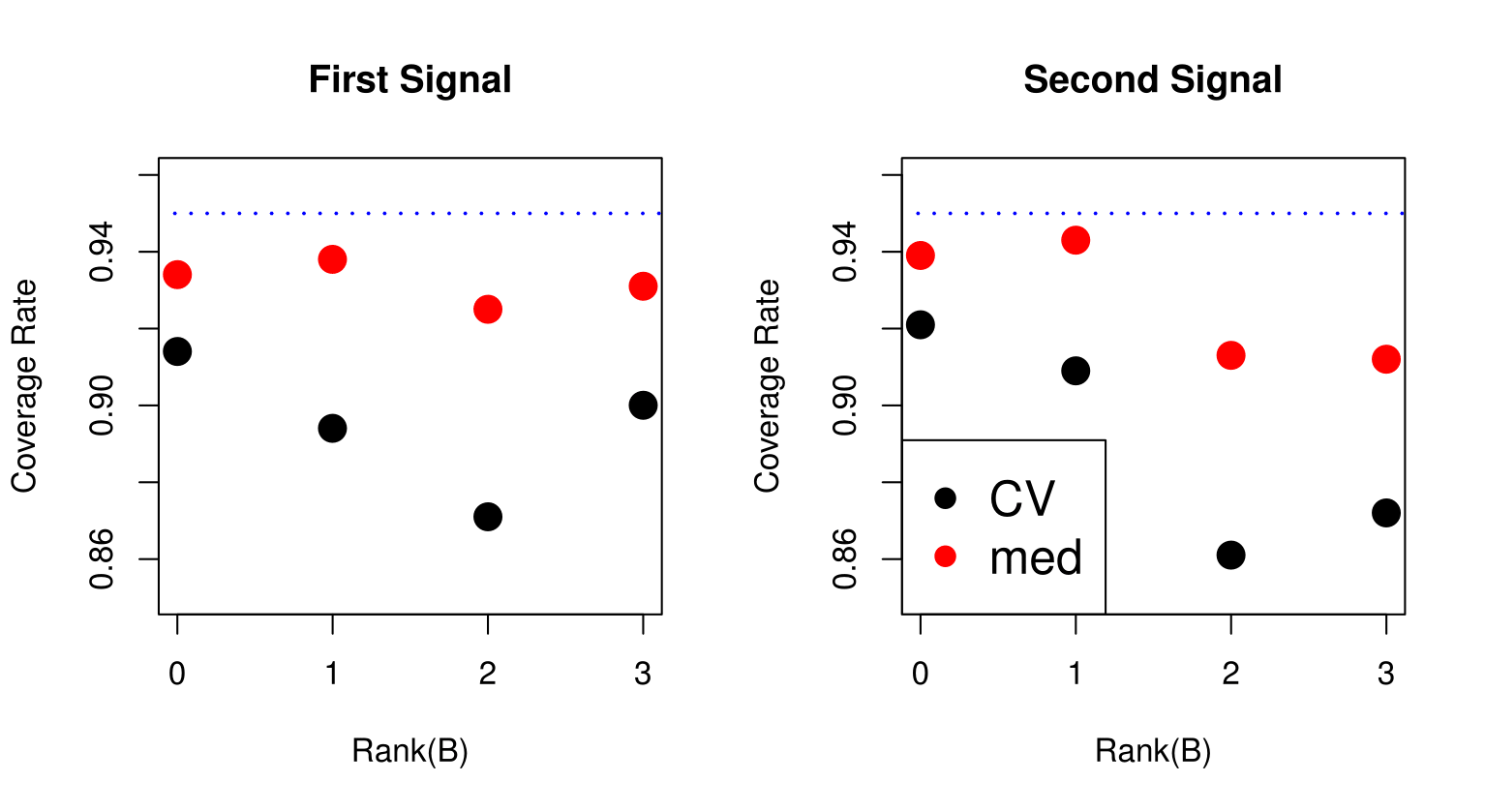

Figure 5 shows that the coverage rate of . As expected, the coverage rate of the true parameter is close to the target .

2.3.1 Simulation studies of the confidence interval construction

We illustrate the coverage rates of in (2.17) on simulated data. The simulation settings are the same as in Section 2.2.3 with and . Figure 5 shows the coverage rate of the confidence intervals for the first two signal parameters and in (2.16). Here, we vary in (2.15) from to . Large leads to large magnitude of true and .

Figure 5 shows that regardless of , true , or the size of , the constructed confidence intervals cover the parameters at the desired level.

|

|

|

3 Rank Estimation

This section discusses the selection of the number of principal components, or equivalently, the estimation of the true rank of under our model assumptions. For determining the rank of , here we investigate the StrongStop procedure (G Sell et al., 2013), applying it to the tests developed in Section 2.2 (CSV and ICSV).

We determine the rank of based on our testing results on , since explicitly tests the range of the true rank. Given the sequence of hypothesis with , the rejection of these must be carried out in a sequential fashion such that once is rejected, all for should be rejected as well. Under such sequential testing framework of this kind, it is natural to choose to be the largest that rejects . The question here is how to choose the ‘stopping point’ for rejection.

One of the simplest methods is to choose the value at which is rejected for the last time with a given level :

which we refer as SimpleStop.

In this paper, instead of SimpleStop, we use StrongStop. This procedure takes sequential p-values as its input and controls family-wise error rate. When the p-values of the sequential tests are uniformly and independently distributed under the null, the StrongStop procedure controls the family-wise error rate under a given level of (G Sell et al., 2013)[Theorem 3]. For rank determination, by the nature of our hypothesis, being true implies also being true for all . The family-wise error rate control property in rank determination, therefore, becomes control of rank over-estimation with level as follows:

where denotes the selected . The resulting procedure is as follows:

Here, denotes the value of either of the CSV or of the ICSV, and conventionally . The independence of p-values from our proposed testing procedures for with has yet been established; however StrongStop shows good performance for strong signals on simulated data.

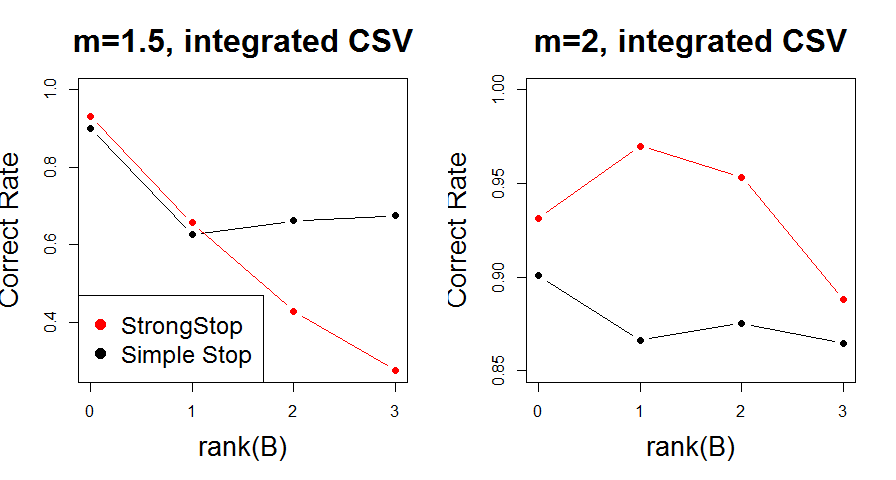

Figure 6 illustrates the simulation results of StrongStop on p-values from the ICSV procedure with . The simulation setting is the same as in Section 2.2.3 with and . We compare StrongStop with SimpleStop. From Figure 6, we observe that for smaller signals, SimpleStop tends to choose the correct rank of better than StrongStop. This can be explained by the strict overestimation control property of StrongStop which might lead to underestimation in low signal case. For strong signals, StrongStop is better at avoiding overfitting.

|

4 Estimating the Noise Level

For the testing procedures CSV and ICSV, and confidence interval , we have assumed that the noise level is known. In case the prior information of is unavailable, the value of needs to be estimated. In this section, we introduce a data-driven method for estimating .

For the estimation of , it is popular to assume that the rank of is known. One of the simplest methods estimates using mean of sum of squared residuals by

with known .

Instead of using the rank of , Gavish and Donoho (2014) use the median of the singular values of as a robust estimator of as follows:

| (4.1) |

where is a median of the singular values of and is a median of a Marčenko-Pastur distribution with . This estimator works under the assumption that .

In this paper, we suggest three estimators, all of which make few assumptions. Our approach uses cross-validation and the sum of squared residuals as an extension of classical noise level estimator. For a fixed value of , we define our estimators , and as follows:

| (4.2) |

with

where denotes the singular value of . The estimators and correspond to the ordinary mean squared residual, with the latter accounting for the degrees of freedom (Reid, Tibshirani and Friedman, 2013). With , the estimator lies between and . We use cross-validation for choosing the appropriate value of the regularization parameter .

For these estimators, choosing an appropriate value for the regularization parameter is important, since depends on . In penalized regression, it is common to use cross-validation for this purpose, examining a grid of values. Unlike the regression setting, however, here there is no outcome variable and thus it is not clear how to make predictions on left-out data points.

In this paper, we use softImpute algorithm (Mazumder, Hastie and Tibshirani, 2010). In the presence of missing values in a given data matrix, softImpute carries out matrix completion with the following criterion:

| (4.3) |

where is an index set of observed data point with a function such that if and otherwise. We define the prediction error of the unobserved values as follows:

where denotes the estimator of acquired from (4.3) and denotes the index set of unobserved values (). Using this prediction error, we carry out k-fold cross-validation, randomly generating non-overlapping leave-out sets of size from . For a grid of values, we compute the average of for each over the left-out data. We choose our to be the minimizer of the average as in usual cross-validation (see e.g. Hastie, Tibshirani and Friedman (2009)).

4.1 A study of noise level estimation

We illustrate simulation examples of noise level estimation of the proposed methods , and in (4) compared to in (4.1). For the estimator , we use in ad-hoc. These approaches do not require predetermined knowledge of .

Simulation settings are the same as in Section 2.2.3 with and . The true value of the noise level is and for choosing , 20-fold cross-validation is used. Table 1 illustrates the simulation results for the three proposed estimators.

| m | Est | se | Est | se | Est | se | Est | se |

| 0.0 | 0.863 | 0.230 | 0.990 | 0.230 | 0.926 | 0.210 | 0.996 | 0.084 |

| 0.5 | 0.869 | 0.236 | 1.000 | 0.238 | 0.934 | 0.216 | 1.006 | 0.085 |

| 1.0 | 0.869 | 0.254 | 1.039 | 0.263 | 0.954 | 0.234 | 1.027 | 0.088 |

| 1.5 | 0.823 | 0.271 | 1.127 | 0.318 | 0.969 | 0.254 | 1.044 | 0.090 |

| 2.0 | 0.789 | 0.246 | 1.245 | 0.324 | 0.999 | 0.224 | 1.052 | 0.091 |

| 0.5 | 0.871 | 0.260 | 1.061 | 0.280 | 0.962 | 0.237 | 1.039 | 0.089 |

| 1.0 | 0.784 | 0.262 | 1.321 | 0.355 | 1.025 | 0.244 | 1.093 | 0.096 |

| 1.5 | 0.700 | 0.288 | 1.611 | 0.431 | 1.052 | 0.201 | 1.121 | 0.100 |

| 2.0 | 0.646 | 0.211 | 1.762 | 0.471 | 1.047 | 0.196 | 1.134 | 0.102 |

| 0.5 | 0.827 | 0.303 | 1.206 | 0.365 | 1.002 | 0.288 | 1.098 | 0.095 |

| 1.0 | 0.674 | 0.235 | 1.771 | 0.459 | 1.076 | 0.231 | 1.186 | 0.107 |

| 1.5 | 0.585 | 0.202 | 2.135 | 0.623 | 1.062 | 0.228 | 1.226 | 0.113 |

| 2.0 | 0.549 | 0.180 | 2.324 | 0.711 | 1.057 | 0.224 | 1.242 | 0.116 |

In this setting, decreases with larger and signals while and increases. For large and signals, shows good results, as compared to other methods. The poor performance of may be caused by the use of an improper definition of , the degrees of freedom. Following the definition of degrees of freedom by Efron et al. (2004), our simulation result shows that the number of non-zero singular values does not coincide with degrees of freedom under our setting. Further investigation into the degrees of freedom is needed in future work.

The competing method consistently shows a small standard deviation. However, with large , especially when , the procedures over-estimates due to the effect of the signals.

5 Additional Examples

We discuss additional examples in this section. Section 5.1 presents results of the proposed methods when the estimated noise level is used. In Section 5.2, hypothesis testing results with non-Gaussian noise are illustrated. Section 5.3 shows results on some real data.

5.1 Simulation examples with unknown noise level

In this section, we illustrate the results when estimated value is used on simulated data. For the estimation of the noise level, we use and which showed good performance in Section 4.1. As in Section 4.1, for the estimator , 20-fold cross-validation and is used. The simulation settings are the same as in Section 2.2.3 with and . We investigate the case of .

|

|

|

|

| Est | se | Est | se | |

|---|---|---|---|---|

| 0 | 0.926 | 0.210 | 0.996 | 0.084 |

| 1 | 0.969 | 0.254 | 1.044 | 0.090 |

| 2 | 1.052 | 0.201 | 1.121 | 0.100 |

| 3 | 1.062 | 0.228 | 1.226 | 0.113 |

Table 2 illustrates the estimated values we used for the testing procedure. Figure 7 shows quantile-quantile plots of observed p-values obtained from using the estimated versus the expected (uniform) quantiles. In quantile-quantile plots, both estimators of show reasonable results in general, and for large , shows better result than . In terms of coverage rate of confidence interval, we can see from Figure 8 that dominates for all cases, which might be due to small standard deviation of estimator. The estimation of is presented in Table 3. For the estimation, StrongStop is applied to the CSV p-values with level . The estimation performance seems to vary with the quality of the estimate of .

| Rate | MSE | Rate | MSE | |

|---|---|---|---|---|

| 0 | 0.894 | 3.704 | 0.948 | 0.063 |

| 1 | 0.455 | 4.243 | 0.486 | 0.514 |

| 2 | 0.231 | 1.080 | 0.157 | 0.853 |

| 3 | 0.181 | 0.845 | 0.026 | 0.975 |

5.2 Simulation example with non-Gaussian noise

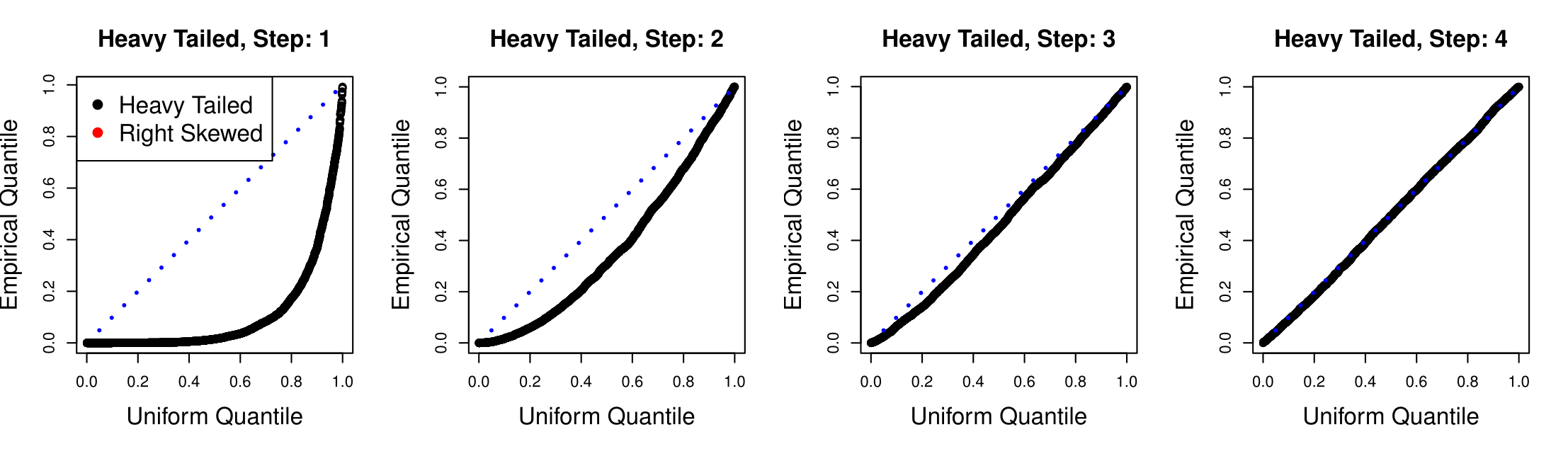

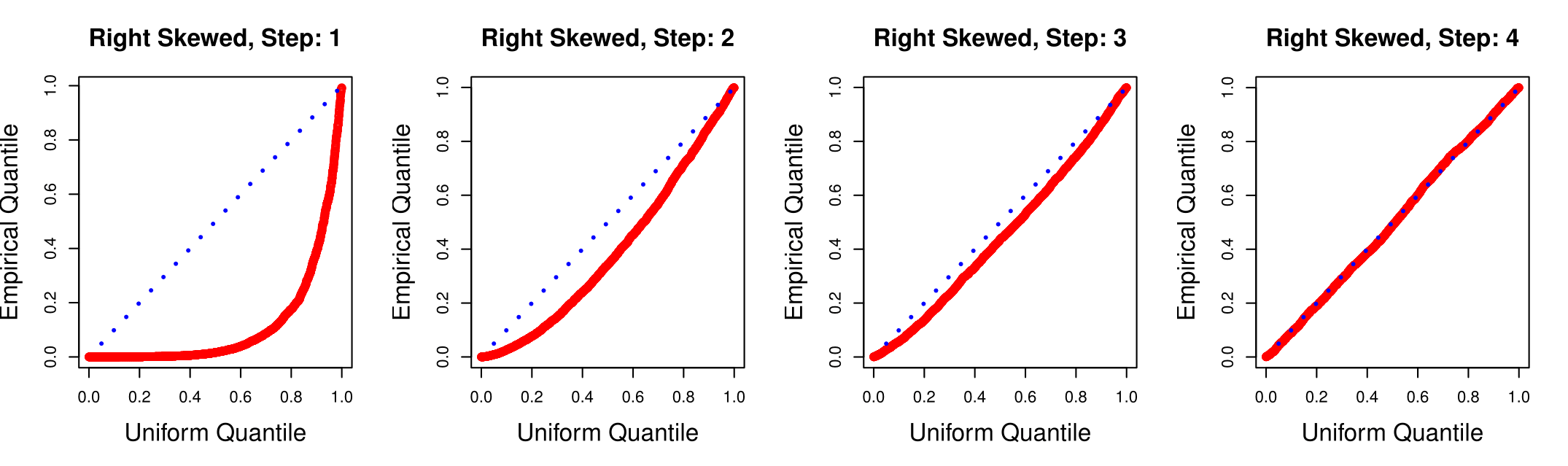

Our testing procedure is based on an assumption of Gaussian noise. Here we investigate the performance of the CSV test on simulated examples with the normality assumption of noise violated. Simulation settings are the same as in Section 2.2.3 with and except for the noise distribution. We study the case of with along with two sorts of noise distribution: heavy tailed and right skewed. The heavy tailed noise is drawn from where denotes t-distribution with degrees of freedom=5, and the right skewed noises are drawn from where denotes the exponential distribution with mean=1. In each case, noise entries are drawn i.i.d., and known value of is used.

|

|

Figure 9 shows quantile-quantile plots of the observed p-values versus expected (uniform) quantiles. The top panels correspond to the heavy tailed noise from and the bottom panels correspond to the right skewed noise from . Quantile-quantile plots from both types of noise show that the p-values deviate slightly from a uniform distribution under the null . For further steps, p-values lie closer to the reference line.

The nonconformity shown in early steps under the null hypothesis is not surprising considering the construction of the CSV procedure based on Gaussian noise. In future work, we will investigate whether the procedures introduced here can be extended to a method robust to non-normality using data-oriented method such as bootstrap.

5.3 Real data example

In this section, we revisit the real data example mentioned in Figure 1. We apply the CSV test to the data of examination marks of 88 students on 5 different topics of Mechanics, Vectors, Algebra, Analysis and Statistics (Mardia, Kent and Bibby, 1979, p. 3-4), and determine the number of principal components to retain for PCA.

In this data, Mechanics and Vectors were closed book exams while the other topics were open book exam. We use and for the estimated noise level. For , 20-fold cross-validation is used with . The CSV test results are presented in Table 4. The estimated is 2 with estimator and 1 with with level using StrongStop. Thus, in PCA we may use one or two principal components depending on our choice of the noise level. In this example, one or two principal components makes sense as these 5 topics cover closely related areas.

| Step | ||

|---|---|---|

| 1 | 0.000 | 0.000 |

| 2 | 0.000 | 0.015 |

| 3 | 0.001 | 0.573 |

| 4 | 0.093 | 0.940 |

| Selected | 2 | 1 |

6 Conclusions

In this paper, we have proposed distribution-based methods for choosing the number of principal components of a data matrix. We have suggested novel methods both for hypothesis testing and the construction of confidence intervals of the signals. The methods have exact type I error control and show promising results in simulated examples. We have also introduced data-based methods for estimating the noise level.

There are many topics that deserve further investigation. In following studies, the analysis of power of the suggested tests and the width of the constructed confidence interval will be investigated. Also, application of the methods to high dimensional data using numerical approximations will be explored. For multiple hypothesis testing corrections to be properly applied, we will study the dependence structure of the p-values in different steps. In addition, for robustness to non-Gaussian noise, bootstrap versions of this procedure will be investigated. Future work may involve a notion of degrees of freedom of the spectral estimator of the signal matrix. These extensions may lead to improvement in noise level estimation.

Variations of these procedures can potentially be applied to canonical correlation analysis (CCA) and linear discriminant analysis (LDA), and these are topics for future work.

Appendix

.1 Lemma 1 and Proof

Lemma 1.

For where , we write the singular value decomposition of by where with . Without loss of generality we assume . As in Section 2.2.1, and denote submatrices of and . Writing the law by , the density of by , by , and by , we have

Proof.

Without loss of generality, we assume . Writing the density function of as , when , we have

| (.1) |

where

| (.2) |

denotes the density of singular values of a Gaussian matrix from with a normalizing constant , is the Jacobian of mapping , denotes Haar probability measure on under the map , and denotes Haar probability measure on . Here, denotes an orthogonal group of matrices.

Note that, can be alternatively derived from , and . and have Haar probability measure on under mapping and on respectively, since the distribution of and are rotation invariant. The determinant of the Jacobian can be calculated either explicitly or from this relation.

As in the case of , for general we have,

| (.3) | |||||

Therefore, with given , , and , we have

since , and thus

| (.4) |

and equivalently,

∎

.2 Proof of Theorem 2.1

Proof.

We follow the notations in Lemma 1. Without loss of generality we assume . When , then . Thus, from Lemma 1 and (.1), we have

where denotes the density of singular values of a Gaussian matrix from as in (.2). Therefore, we have

| (.5) |

Note that (.2) is the integrand of the CSV test statistic with some cancellation from the fraction, and thus is the probability of having the singular value that is bigger than the observed one given all the other singular values, and .

Thus, if the observation is actually generated under

, then the density of the singular value becomes (.2) up to a constant. Consequently, when writing the observed singular values by , and the observed singular value decomposition of by without confusion,

The denominator of works as a normalizing constant. ∎

.3 Proof of Theorem 2.2

Proof.

We follow the notation of Lemma 1 and without loss of generality, assume . Under , we have . Then, as in Theorem 2.1, we have

and therefore,

| (.6) |

where is defined in (2.14). Note that (.3) is the integrand of the ICSV test statistic , and is the conditional survival function of the singular value given and .

Thus, if the observation is under , then its singular value has the conditional density of (.3) upto a constant. Consequently, when writing the observed singular value by , and the observed singular value decomposition of by without confusion,

The denominator of works as a normalizing constant. ∎

.4 Proof of Theorem 2.3

Proof.

We follow the notations in Lemma 1 and without loss of generality, assume . From (.3), we have

where as defined in (2.16). Therefore, we have

| (.7) |

As (.4) is the integrand of , when writing the observed singular values by , and the observed singular value decomposition of by without confusion, we have

Here, the denominator of works as a normalizing constant. ∎

Acknowledgements

We would like to thank Boaz Nadler and Iain Johnstone for helpful conversations. Robert Tibshirani was supported by NSF grant DMS-9971405 and NIH grant N01-HV-28183.

References

- Cai, Candès and Shen (2010) {barticle}[author] \bauthor\bsnmCai, \bfnmJian-Feng\binitsJ.-F., \bauthor\bsnmCandès, \bfnmEmmanuel J.\binitsE. J. and \bauthor\bsnmShen, \bfnmZuowei\binitsZ. (\byear2010). \btitleA singular value thresholding algorithm for matrix completion. \bjournalSIAM J. Optim. \bvolume20 \bpages1956–1982. \bdoi10.1137/080738970 \bmrnumber2600248 (2011c:90065) \endbibitem

- Efron et al. (2004) {barticle}[author] \bauthor\bsnmEfron, \bfnmBradley\binitsB., \bauthor\bsnmHastie, \bfnmTrevor\binitsT., \bauthor\bsnmJohnstone, \bfnmIain\binitsI. and \bauthor\bsnmTibshirani, \bfnmRobert\binitsR. (\byear2004). \btitleLeast angle regression. \bjournalAnn. Statist. \bvolume32 \bpages407–499. \bnoteWith discussion, and a rejoinder by the authors. \bdoi10.1214/009053604000000067 \bmrnumber2060166 (2005d:62116) \endbibitem

- Gavish and Donoho (2014) {barticle}[author] \bauthor\bsnmGavish, \bfnmMatan\binitsM. and \bauthor\bsnmDonoho, \bfnmDavid L.\binitsD. L. (\byear2014). \btitleThe optimal hard threshold for singular values is . \bjournalIEEE Trans. Inform. Theory \bvolume60 \bpages5040–5053. \bdoi10.1109/TIT.2014.2323359 \bmrnumber3245370 \endbibitem

- G Sell et al. (2013) {barticle}[author] \bauthor\bsnmG Sell, \bfnmMax Grazier\binitsM. G., \bauthor\bsnmWager, \bfnmStefan\binitsS., \bauthor\bsnmChouldechova, \bfnmAlexandra\binitsA. and \bauthor\bsnmTibshirani, \bfnmRobert\binitsR. (\byear2013). \btitleSequential Selection Procedures And False Discovery Rate Control. \bnotePreprint. Available at arXiv:1309.5352. \endbibitem

- Hastie, Tibshirani and Friedman (2009) {bbook}[author] \bauthor\bsnmHastie, \bfnmTrevor\binitsT., \bauthor\bsnmTibshirani, \bfnmRobert\binitsR. and \bauthor\bsnmFriedman, \bfnmJerome\binitsJ. (\byear2009). \btitleThe elements of statistical learning, \beditionsecond ed. \bseriesSpringer Series in Statistics. \bpublisherSpringer, New York \bnoteData mining, inference, and prediction. \bdoi10.1007/978-0-387-84858-7 \bmrnumber2722294 (2012d:62081) \endbibitem

- James (1964) {barticle}[author] \bauthor\bsnmJames, \bfnmAlan T.\binitsA. T. (\byear1964). \btitleDistributions of matrix variates and latent roots derived from normal samples. \bjournalAnn. Math. Statist. \bvolume35 \bpages475–501. \bmrnumber0181057 (31 #5286) \endbibitem

- Johnstone (2001) {barticle}[author] \bauthor\bsnmJohnstone, \bfnmIain M.\binitsI. M. (\byear2001). \btitleOn the distribution of the largest eigenvalue in principal components analysis. \bjournalAnn. Statist. \bvolume29 \bpages295–327. \bdoi10.1214/aos/1009210544 \bmrnumber1863961 (2002i:62115) \endbibitem

- Jolliffe (2002) {bbook}[author] \bauthor\bsnmJolliffe, \bfnmI. T.\binitsI. T. (\byear2002). \btitlePrincipal component analysis, \beditionsecond ed. \bseriesSpringer Series in Statistics. \bpublisherSpringer-Verlag, New York. \bmrnumber2036084 (2004k:62010) \endbibitem

- Josse and Husson (2012) {barticle}[author] \bauthor\bsnmJosse, \bfnmJulie\binitsJ. and \bauthor\bsnmHusson, \bfnmFrançois\binitsF. (\byear2012). \btitleSelecting the number of components in principal component analysis using cross-validation approximations. \bjournalComput. Statist. Data Anal. \bvolume56 \bpages1869–1879. \bdoi10.1016/j.csda.2011.11.012 \bmrnumber2892383 \endbibitem

- Kritchman and Nadler (2008) {barticle}[author] \bauthor\bsnmKritchman, \bfnmShira\binitsS. and \bauthor\bsnmNadler, \bfnmBoaz\binitsB. (\byear2008). \btitleDetermining the number of components in a factor model from limited noisy data. \bjournalChemometrics and Intelligent Laboratory Systems \bvolume94 \bpages19–32. \endbibitem

- Mardia, Kent and Bibby (1979) {bbook}[author] \bauthor\bsnmMardia, \bfnmKantilal Varichand\binitsK. V., \bauthor\bsnmKent, \bfnmJohn T.\binitsJ. T. and \bauthor\bsnmBibby, \bfnmJohn M.\binitsJ. M. (\byear1979). \btitleMultivariate analysis. \bpublisherAcademic Press [Harcourt Brace Jovanovich, Publishers], London-New York-Toronto, Ont. \bnoteProbability and Mathematical Statistics: A Series of Monographs and Textbooks. \bmrnumber560319 (81h:62003) \endbibitem

- Mazumder, Hastie and Tibshirani (2010) {barticle}[author] \bauthor\bsnmMazumder, \bfnmRahul\binitsR., \bauthor\bsnmHastie, \bfnmTrevor\binitsT. and \bauthor\bsnmTibshirani, \bfnmRobert\binitsR. (\byear2010). \btitleSpectral regularization algorithms for learning large incomplete matrices. \bjournalJ. Mach. Learn. Res. \bvolume11 \bpages2287–2322. \bmrnumber2719857 (2011m:62184) \endbibitem

- Muirhead (1982) {bbook}[author] \bauthor\bsnmMuirhead, \bfnmRobb J.\binitsR. J. (\byear1982). \btitleAspects of multivariate statistical theory. \bpublisherJohn Wiley & Sons, Inc., New York \bnoteWiley Series in Probability and Mathematical Statistics. \bmrnumber652932 (84c:62073) \endbibitem

- Nadler (2008) {barticle}[author] \bauthor\bsnmNadler, \bfnmBoaz\binitsB. (\byear2008). \btitleFinite sample approximation results for principal component analysis: a matrix perturbation approach. \bjournalAnn. Statist. \bvolume36 \bpages2791–2817. \bdoi10.1214/08-AOS618 \bmrnumber2485013 (2010g:62190) \endbibitem

- Reid, Tibshirani and Friedman (2013) {barticle}[author] \bauthor\bsnmReid, \bfnmStephen\binitsS., \bauthor\bsnmTibshirani, \bfnmRobert\binitsR. and \bauthor\bsnmFriedman, \bfnmJerome\binitsJ. (\byear2013). \btitleA study of error variance estimation in lasso regression. \bnotePreprint. Available at arXiv:1311.5274. \endbibitem

- Taylor, Loftus and Tibshirani, Ryan (2013) {barticle}[author] \bauthor\bsnmTaylor, \bfnmJonathan\binitsJ., \bauthor\bsnmLoftus, \bfnmJoshua\binitsJ. and \bauthor\bsnmTibshirani, Ryan (\byear2013). \btitleTests in adaptive regression via the Kac-Rice formula. \bnotePreprint. Available at arXiv:1308.3020. \endbibitem

- Tibshirani (1996) {barticle}[author] \bauthor\bsnmTibshirani, \bfnmRobert\binitsR. (\byear1996). \btitleRegression shrinkage and selection via the lasso. \bjournalJ. Roy. Statist. Soc. Ser. B \bvolume58 \bpages267–288. \bmrnumber1379242 (96j:62134) \endbibitem