Large-Maturity Regimes of the Heston Forward Smile

Abstract.

We provide a full characterisation of the large-maturity forward implied volatility smile in the Heston model. Although the leading decay is provided by a fairly classical large deviations behaviour, the algebraic expansion providing the higher-order terms highly depends on the parameters, and different powers of the maturity come into play. As a by-product of the analysis we provide new implied volatility asymptotics, both in the forward case and in the spot case, as well as extended SVI-type formulae. The proofs are based on extensions and refinements of sharp large deviations theory, in particular in cases where standard convexity arguments fail.

Key words and phrases:

Stochastic volatility, Heston, forward implied volatility, asymptotic expansion, sharp large deviations2010 Mathematics Subject Classification:

60F10, 91G99, 91G601. Introduction

Consider an asset price process with , paying no dividend, defined on a complete filtered probability space with a given risk-neutral measure , and assume that interest rates are zero. In the Black-Scholes-Merton (BSM) model, the dynamics of the logarithm of the asset price are given by , where represents the instantaneous volatility and is a standard Brownian motion. The no-arbitrage price of the call option at time zero is then given by the famous BSM formula [14, 58]: , with , where is the standard normal distribution function. For a given market price of the option at strike and maturity , the spot implied volatility is the unique solution to the equation .

For any and , we define as in [13, 56] a forward-start option with forward-start date , maturity and strike as a European option with payoff where pathwise. By the stationary increment property, its value is simply in the BSM model. For a given market price of the option at strike , forward-start date and maturity , the forward implied volatility smile is then defined (see also [13]) as the unique solution to . The forward smile is a generalisation of the spot implied volatility smile, and the two are equal when .

The literature on implied volatility asymptotics is extensive and has drawn upon a wide range of mathematical techniques. Small-maturity asymptotics have received wide attention using heat kernel expansion results [8]. More recently, they have been studied using PDE methods [12, 42, 61], large deviations [23, 26], saddlepoint methods [28], Malliavin calculus [9, 53] and differential geometry [35, 43]. Roger Lee [55] was the first to study extreme strike asymptotics, and further works on this have been carried out by Benaim and Friz [6, 7] and in [39, 40, 41, 31, 23, 19]. Large-maturity asymptotics have only been studied in [67, 27, 46, 45, 29] using large deviations and saddlepoint methods. Fouque et al. [30] have also successfully introduced perturbation techniques in order to study slow and fast mean-reverting stochastic volatility models. Models with jumps (including Lévy processes), studied in the above references for large maturities and extreme strikes, ‘explode’ in small time, in a precise sense investigated in [1, 2, 66, 60, 59, 24].

On the other hand the literature on asymptotics of forward-start options and the forward smile is sparse. Glasserman and Wu [37] use different notions of forward volatilities to assess their predictive values in determining future option prices and future implied volatility. Keller-Ressel [52] studies the forward smile asymptotic when the forward-start date becomes large ( fixed). Bompis [15] produces an expansion for the forward smile in local volatility models with bounded diffusion coefficient. In [47] the authors compute small and large-maturity asymptotics for the forward smile in a general class of models (including stochastic volatility and time-changed exponential Lévy models) where the forward characteristic function satisfies certain properties (in particular essential smoothness of the re-scaled limit). In [48] the authors prove that for fixed the Heston forward smile explodes as tends to zero. Finally, empirical results on the forward smile have been carried out by practitioners in Balland [5], Bergomi [13], Bühler [17] and Gatheral [34].

Under some conditions on the parameters, it was shown in [47] that the smooth behaviour of the pointwise limit yielded an asymptotic behaviour for the forward smile as where and are continuous functions on . In particular for (spot smiles), they recovered the result in [27] (also under some restrictions on the parameters). Interestingly, the limiting large-maturity forward smile does not depend on the forward-start date . A number of practitioners (see eg. Balland[5]) have made the natural conjecture that the large-maturity forward smile should be the same as the large-maturity spot smile. The result above rigorously shows us that this indeed holds if and only if the Heston correlation is close enough to zero.

It is natural to ask what happens when the parameter restrictions are violated. We identify a number of regimes depending on the correlation and derive asymptotics in each regime. The main results (Theorems 3.1 and 4.1) state the following, as tends to infinity:

for any , where is some indicator function related to the intrinsic value of the option price, and , , strictly positive constants, depending on the level of the correlation. The remainder decays to zero as tends to infinity. If (spot smiles) we recover and extend the results in [27].

The paper is structured as follows. In Section 2 we introduce the different large-maturity regimes for the Heston model, which will drive the asymptotic behaviour of forward option prices and forward implied volatilities. In Section 3 we derive large-maturity forward-start option asymptotics in each regime and in Section 4 we translate these results into forward smile asymptotics, including extended SVI-type formulae (Section 4.1). Section 6 provides numerics supporting the asymptotics developed in the paper and Section 7 gathers the proofs of the main results.

Notations: shall always denote expectation under a risk-neutral measure given a priori. We shall refer to the standard (as opposed to the forward) implied volatility as the spot smile and denote it . The forward implied volatility will be denoted as above and we let and . For a sequence of sets in , we may, for convenience, use the notation , by which we mean the following (whenever both sides are equal): Finally, for a given set , we let and denote its interior and closure (in ), and the real and imaginary parts of a complex number , and if and otherwise.

2. Large-maturity regimes

In this section we introduce the large-maturity regimes that will be used throughout the paper. Each regime is determined by the Heston correlation and yields fundamentally different asymptotic behaviours for large-maturity forward-start options and the corresponding forward smile. This is due to the distinct behaviour of the moment explosions of the forward price process in each regime . In the Heston model, the (log) stock price process is the unique strong solution to the following SDEs:

| (2.1) |

with , , and and and are two standard Brownian motions. We also introduce the notation . The Feller SDE for the variance process has a unique strong solution by the Yamada-Watanabe conditions [50, Proposition 2.13, page 291]). The process is a stochastic integral of and is therefore well-defined. The Feller condition, (or ), ensures that the origin is unattainable. Otherwise the origin is regular (hence attainable) and strongly reflecting (see [51, Chapter 15]). We however do not require the Feller condition in our analysis since we work with the forward moment generating function (mgf) of . Define the real numbers and by

| (2.2) |

and note that with if and only if . We now define the large-maturity regimes:

| (2.3) |

In the standard case , corresponds to and is its complement. We now define the following quantities:

| (2.4) |

with

| (2.5) |

as well as the interval by

Note that for , if and if Also defined in (2.5) is a well-defined real number for all . Furthermore we always have and with if and only if . We define the real-valued functions and from to by

| (2.6) |

with , and defined in (7.3). It is clear (see also [27] and [45]) that the function is infinitely differentiable, strictly convex and essentially smooth on the open interval and that . Furthermore if and only if . For any the (saddlepoint) equation has a unique solution :

| (2.7) |

Further let denote the Fenchel-Legendre transform of :

| (2.8) |

The following lemma characterises and can be proved using straightforward calculus. As we will see in Section 3.1, the function can be interpreted as a large deviations rate function for our problem.

Lemma 2.1.

Define the function for any . Then

-

•

: on ;

-

•

: on and on ;

-

•

: on and on ;

-

•

:

-

•

: on and on .

3. Forward-start option asymptotics

In order to specify the forward-start option asymptotics we need to introduce some functions and constants. As outlined in Theorem 3.1, each of them is defined in a specific regime and strike region where it is well defined and real valued. In the formulae below, , are defined in (7.3), in (2.4) and in (2.6).

| (3.1) |

where

| (3.2) |

| (3.3) |

| (3.4) |

| (3.5) |

| (3.6) |

| (3.7) |

Since and , we always have and . Furthermore, and one can show that ; therefore all the functions and constants in (3.1), (3.2), (3.3), (3.4) and (3.5) are well-defined and real-valued. is well-defined since and and the constant are well-defined since . Finally define the following combinations and the function :

| (3.8) |

| (3.9) |

We are now in a position to state the main result of the paper, namely an asymptotic expansion for forward-start option prices in all regimes for all (log) strikes on the real line. The proof is obtained using Lemma 7.6 in conjunction with the asymptotics in Lemmas 7.13, 7.15, 7.18 and 7.17.

Theorem 3.1.

The following expansion holds for forward-start call options for all as tends to infinity:

where the functions , and the constants , and are given by the following combinations111whenever is in force, the case is excluded if , with defined in (7.33), for .:

-

•

: for ;

-

•

: for ; for ; for ;

-

•

: for ; for ; for ;

-

•

: for ; for ; for ; at ; for ;

-

•

: for ; for ; for ;

In order to highlight the symmetries appearing in the asymptotics, we shall at times identify an interval with the corresponding regime and combination in force. This slight abuse of notations should not however be harmful to the comprehension.

Remark 3.2.

-

(i)

Under , asymptotics for the large-maturity forward smile (for ) have been derived in [47, Proposition 3.8].

- (ii)

-

(iii)

All asymptotic expansions are given in closed form and can in principle be extended to arbitrary order.

-

(iv)

When and are in force then is linear in as opposed to being strictly convex as in .

-

(v)

If then with equality if and only if . If then . Since , the leading order decay term is given by .

-

(vi)

Under (which only occur when for log-strikes strictly greater than ), forward-start call option prices decay to one as tends to infinity. This is fundamentally different than the large-strike behaviour in other regimes and in the BSM model, where call option prices decay to zero. This seemingly contradictory behaviour is explained as follows: as the maturity increases there is a positive effect on the price by an increase in the time value of the option and a negative effect on the price by increasing the strike of the forward-start call option. In standard regimes and for sufficiently large strikes the strike effect is more prominent than the time value effect in the large-maturity limit. Here, because of the large correlation, this effect is opposite: as the asset price increases, the volatility tends to increase driving the asset price to potentially higher levels. This gamma or time value effect outweighs the increase in the strike of the option.

-

(vii)

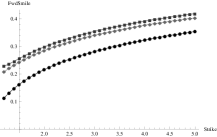

In , the decay rate has a very different behaviour: the minimum achieved at is not zero and is constant for . There is limited information in the leading-order behaviour and important distinctions must therefore occur in higher-order terms. This is illustrated in Figures 5 and 6 where the first-order asymptotic is vastly superior to the leading order.

-

(viii)

It is important to note that and depend on the forward-start date through (2.4) and the regime choice. However, in the uncorrelated case , always applies and does not depend on . The non-stationarity of the forward smile over the spot smile (at leading order) depends critically on how far the correlation is away from zero.

In order to translate these results into forward smile asymptotics (in the next section), we require a similar expansion for the Black-Scholes model, where the log stock price process satisfies , with . Define the functions and by and

so that the following holds (see [47, Corollary 2.11]):

Lemma 3.3.

Let , and set for large enough so that . In the BSM model the following expansion then holds for any as tends to infinity (the function is defined in(3.9)):

3.1. Connection with large deviations

Although clear from Theorem 3.1, we have so far not mentioned the notion of large deviations at all. The leading-order decay of the option price as the maturity tends to infinity gives rise to estimates for large-time probabilities; more precisely, by formally differentiating both sides with respect to the log-strike, one can prove, following a completely analogous proof to [48, Corollary 3.3], that

for any Borel subset of the real line, namely that satisfies a large deviations principle under with speed and good rate function as tends to infinity. We refer the reader to the excellent monograph [20] for more details on large deviations. The theorem actually states a much stronger result here since it provides higher-order estimates, coined ‘sharp large deviations’ in [11] (see also [10, Definition 1.1]). Now, classical methods to prove large deviations, when the the moment generating function is known rely on the Gärtner-Ellis theorem. In mathematical finance, one can consult for instance [26], [27] or [46] for the small-and large-time behaviour of stochastic volatility models, and [62] for an insightful overview. The Gärtner-Ellis theorem requires, in particular, the limiting logarithmic moment generating function to be steep at the boundaries of its effective domain. This is indeed the case in Regime , but fails to hold in other regimes. The standard proof of this theorem (as detailed in [20, Chapter 2, Theorem 2.3.6]) clearly holds in the open intervals of the real line where the function is strictly convex, encompassing basically all occurrences of . The other cases, when becomes linear, and the turning points and , however have to be handled with care and solved case by case. Proving sharp large deviations essentially relies on finding a new probability measure under which a rescaled version of the original process converges weakly to some random variable (often Gaussian, but not always); in layman terms, under this new probability measure, the rare events / large deviations of the rescaled variable are not rare any longer. More precisely, fix some log-moneyness ; we determine a process , and a probability measure via

where is the unique solution to the equation , with denoting the (rescaled) logarithmic moment generating function of (See Section 7.1). The characteristic function has some expansion as tends to infinity. Once this pair has been found, the final part of the proof is to express call prices (or probabilities) as inverse Fourier transforms of the characteristic function multiplied by some kernel, and to use the expansion of to determine the desired asymptotics. The main technical issues, and where the different regimes come into play, arise in the properties of the asymptotic behaviour of and as tends to infinity (and on the value one has to choose). More precise details about the main steps of the proofs are provided at the beginning of Section 7 and in Section 7.3.

Sharp large deviations, or more generally speaking, probabilistic asymptotic expansions, à la Bahadur-Rao [4], can also be proved via other routes. In particular, the framework developed by Benarous [8] (and applied to the financial context in [22, 23]) is an extremely powerful tool to handle Laplace methods on Wiener space and heat kernel expansions. However, the singularity of the square root diffusion (in the SDE (2.1) for the variance) at the origin falls outside the scope of this theory. Incidentally, Conforti, Deuschel and De Marco [18] recently proved a (sample path) large deviations principle for the square root diffusion, giving hope for an alternative proof to ours. As explained in [48, 49], the forward-start framework on the couple , solution to (2.1), starting at , can be seen as a standard option pricing problem on the forward couple , solution to the same stochastic differential equation (2.1), albeit starting at the point , namely with random initial variance. This additional layer of complexity arising from starting the SDE at a random starting point makes the application of the Benarous framework as well as the Conforti-Deuschel-De Marco result, a fascinating, yet challenging, exercise to consider.

4. Forward smile asymptotics

We now translate the forward-start option asymptotics obtained above into asymptotics of the forward implied volatility smile. Let us first define the function by

| (4.1) |

with defined by and given in Lemma 2.1. Define the following combinations:

Here and are given in (3.4) and (3.5) and is defined by

| (4.2) |

with and given in (2.6) and in (2.7). We now state the main result of the section, namely an expansion for the forward smile in all regimes and (log) strikes on the real line. The proof is given in Section 7.6.

Theorem 4.1.

The following expansion holds for the forward smile as tends to infinity:

where is defined by

with the functions , the remainder and the constant given by the following combinations222whenever is in force, the case is excluded if , with defined in (7.33), for .:

-

•

: for ;

-

•

: for ; for ; for ;

-

•

: for ; for ; for ;

-

•

: for ; for ; for ; for ;

-

•

: for ; for .

Remark 4.2.

-

(i)

In the standard spot case , the large-maturity asymptotics of the implied volatility smile was derived in [29] for only (i.e. assuming ). In the complementary case, , the behaviour of the smile for large strikes become more degenerate, and one cannot specify higher-order asymptotics for .

- (ii)

-

(iii)

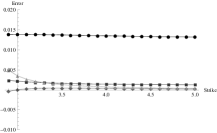

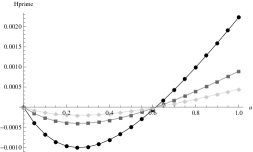

Straightforward computations show that for , and for , so that is well defined on . On , , so that in Regimes on and in on , is always a positive adjustment to the zero-order term ; see Figure 1 for an example of this ’convexity effect’.

Theorem 4.1 displays varying levels of degeneration for high-order forward smile asymptotics. In one can in principle obtain arbitrarily high-order asymptotics. In , and one can only specify the forward smile to arbitrary order if . If this is not the case then we can only specify the forward smile to first order. Now the dynamics of the Heston volatility is given by with . If then the volatility becomes Gaussian, which this corresponds to a specific case of the Schöbel-Zhu stochastic volatility model. So as the Heston volatility dynamics deviate from Gaussian volatility dynamics a certain degeneracy occurs such that one cannot specify high order forward smile asymptotics. Interestingly, a similar degeneracy occurs in [48] for exploding small-maturity Heston forward smile asymptotics and in [23] when studying the tail probability of the stock price. As proved in [23], the square-root behaviour of the variance process induces some singularity and hence a fundamentally different behaviour when . In , and at the boundary points one cannot specify the forward smile beyond first order for any parameter configurations. This could be because these asymptotic regimes are extreme in the sense that they are transition points between standard and degenerate behaviours and therefore difficult to match with BSM forward volatility. Finally in and for we obtain the most extreme behaviour, in the sense that one cannot specify the forward smile beyond zeroth order. This is however not that surprising since the large correlation regime has fundamentally different behaviour to the BSM model (see also Remark 3.2(iii)).

4.1. SVI-type limits

The so-called ’Stochastic Volatility Inspired’ (SVI) parametrisation of the spot implied volatility smile was proposed in [33]. As proved in [36], under the assumption , the SVI parametrisation turn out to be the true large-maturity limit for the Heston (spot) smile. We now extend these results to the large-maturity forward implied volatility smile. Define the following extended SVI parametrisation

for all and the constants

where is defined in (2.4) and in (7.3). Define the following combinations:

| (4.3) |

The proof of the following result follows from simple manipulations of the zeroth-order forward smile in Theorem 4.1 using the characterisation of in Lemma 2.1.

Corollary 4.3.

The pointwise continuous limit exists for with constants and given by333whenever is in force, the case is excluded if , with defined in (7.33), for .:

-

•

: for ;

-

•

: for ; for ;

-

•

: for ; for ;

-

•

: for ; for ; for ;

-

•

: for ; for .

5. Financial Interpretation of the large-maturity regimes

The large-maturity regimes in (2.3) were identified with specific properties of the limiting forward logarithmic moment generating function. Each regime uncovers fundamental properties of the large-maturity forward smile, some of which having been empirically observed by practitioners. These regimes are not merely mathematical curiosities, but their studies reveal particular behaviours and oddities of the model. An intuitive question is how different the large-maturity forward smile and the large-maturity spot smile are. This is a metric that a trader would have a view on and can be analysed using historical data. Because of the ergodic properties of the variance process, at first sight it seems natural to conjecture that the large-maturity spot and forward smiles should be the same at leading order. More specifically, if denotes the Black-Scholes implied volatility observed at time , i.e. the unique positive solution to the equation , then by definition the forward implied volatility solves the equation . If we suppose that , where the function is independent of (this is the case in Heston — it does not depend on ) then it seems reasonable to suppose that and hence that . It is therefore natural to conjecture (see for example [5]) that the limiting forward smile is the same as the limiting spot smile . Theorem 4.1 shows us that this only holds under the good correlation regime , i.e. for correlations ‘close’ to zero. Deviations of the correlation from zero therefore effect how different the large-maturity forward smile is to the large-maturity spot smile.

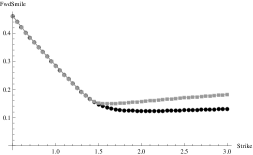

Consider now the practically relevant (on Equity markets) case of large negative correlation (). In Figure 1 we compare the two limiting smiles using the zero-order asymptotics in Corollary 4.3 when . At the critical log-strike , the forward smile becomes more convex than the corresponding spot smile. Interestingly this asymmetric feature has been empirically observed by practitioners [13] and is a fundamental property of the model—not only for large-maturities. Quoting Bergomi [13] from an empirical analysis: ”…the increased convexity (of the forward smile) with respect to today’s smile is larger for than for …this is specific to the Heston model.”

It is natural to wonder about the origin of this effect. Consider a standard European option with large strike . A large number of sample paths of the stock price approach , but, because of the negative correlation, the corresponding variance tends to be low (the so-called ‘leverage effect’). For a delta-hedged long position this is exactly where we want the variance to be the highest (maximum gamma and vega). Hence there is a tendency for the (spot) implied volatility to be downward sloping for high strikes. On the other hand, consider a forward-start option with large strike . Suppose that the variance is large at the forward-start date, . Because of the negative correlation, the stock price will tend to be low here. But this is irrelevant since the stock price is always re-normalised to at this point. Hence there will be a greater number of paths where the re-normalised stock for is close to and the variance is high relative to the (spot) case discussed above. The relative nature of this effect induces this ‘convexity effect’. When there is large positive correlation (), then the large-maturity forward smile is more convex then the large-maturity spot smile for low strikes, . This is the ‘mirror image’ effect of and follows from similar intuition to above.

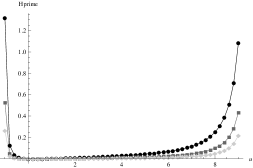

When ( and ) there is a transition point for large strikes where the smile is upward sloping and possibly concave (See Figures 5 and 6). It is important to note that this effect materialises for both the large-maturity spot and forward smile and is due to the fact that paths where the stock price are high will tend to be accompanied by periods of very high variance because of the positive correlation.

The intuitive arguments given above for each regime are not specific to Heston. A natural conjecture is that all stochastic volatility models where the variance process has a stationary distribution will exhibit similar large-maturity regimes. However, the location of the transition points and the magnitude of the ‘convexity corrections’ may be quite different and model specific.

6. Numerics

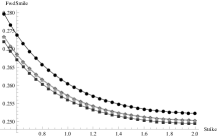

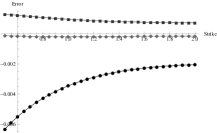

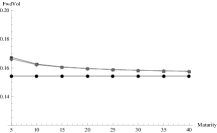

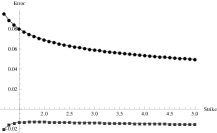

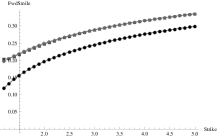

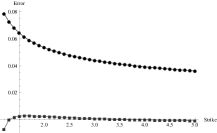

We first compare the true Heston forward smile and the asymptotics developed in the paper. We calculate forward-start option prices using the inverse Fourier transform representation in [54, Theorem 5.1] and a global adaptive Gauss-Kronrod quadrature scheme. We then compute the forward smile with a simple root-finding algorithm. In Figure 2 we compare the true forward smile using Fourier inversion and the asymptotic in Theorem 4.1(i) for the good correlation regime, which was derived in [47]. In Figure 3 we compare the true forward smile using Fourier inversion and the asymptotic in Theorem 4.1(ii) for the asymmetric negative correlation regime. Higher-order terms are computed using the theoretical results above; these can in principle be extended to higher order, but the formulae become rather cumbersome; numerically, these higher-order computations seem to add little value to the accuracy anyway. In Figure 4 we compare the asymptotic in Theorem 4.1(ii) for the transition strike . Results are all in line with expectations.

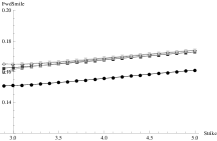

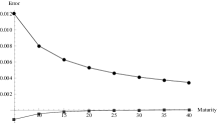

In the large correlation regime , we find it more accurate to use Theorem 3.1 and then numerically invert the price to get the corresponding forward smile (Figures 5 and 6), rather than use the forward smile asymptotic in Theorem 4.1. As explained in Remark 3.2(iv) the leading-order accuracy of option prices in this regime is poor and higher-order terms embed important distinctions that need to be included. This also explains the poor accuracy of the forward smile asymptotic in Theorem 4.1 for the large correlation regime. As seen in the proof (Section 7.6), the leading-order behaviour of option prices is used to line up strike domains in the BSM and Heston model and then forward smile asymptotics are matched between the models. If the leading-order behaviour is poor, then regardless of the order of the forward smile asymptotic, there will always be a mismatch between the asymptotic forms and the forward smile asymptotic will be poor. Using the approach above bypasses this effect and is extremely accurate already at first order (Figures 5 and 6).

In all but , higher-order terms can approach zero or infinity as the strike approaches the critical values ( or ), separating the asymptotic regimes, and forward smile (and forward-start option price) asymptotics are not continuous there (apart from the zeroth-order term), see also Remark 4.2(i). Numerically this implies that the asymptotic formula may break down for strikes in a region around the the critical strike. Similar features have been observed in [48] where degenerate asymptotics were derived for the exploding small-maturity Heston forward smile.

7. Proof of Theorems 3.1 and 4.1

This section is devoted to the proofs of the option price and implied volatility expansions in Theorems 3.1 and 4.1. We first start (Section 7.1) with some preliminary results of the behaviour of the moment generating function of the forward process , on which the proofs will rely. The remainder of the section is devoted to the different cases, as follows:

- •

- •

-

•

Section 7.6 translates the expansions for the option price into expansions for the implied volatility.

7.1. Forward logarithmic moment generating function (lmgf) expansion and limiting domain

For any , , define the re-normalised lmgf of and its effective domain by

| (7.1) |

A straightforward application of the tower property for expectations yields:

| (7.2) |

where

| (7.3) |

The first step is to characterise the effective domain for fixed as tends to infinity. Recall that the large-maturity regimes are defined in (2.3) with and given in (2.4).

Lemma 7.1.

For fixed , converges (in the set sense) to defined in Table 2, as tends to infinity.

Proof.

Recall the following facts from [47, Lemma 5.11 and Proposition 5.12] and [45, Proposition 2.3], with the convention that when :

-

(i)

for all if ;

-

(ii)

for all if ;

-

(iii)

for all if ;

-

(iv)

for all if ;

-

(v)

if and only if and if and only if . We always have and . In the latter case it is possible that in which case .

Then for fixed , the lemma follows directly from (i)-(iv) in combination with property (v). ∎

The following lemma provides the asymptotic behaviour of as tends to infinity. The proof follows the same steps as [47, Lemma 5.13], using the fact that the asset price process is a true martingale [3, Proposition 2.5], and is therefore omitted.

Lemma 7.2.

Remark 7.3.

-

(i)

When ( and ), we have , so that the limit is not continuous at the right boundary . For we always have and .

-

(ii)

For all , , so that the remainder goes to zero exponentially fast as tends to infinity.

7.2. The strictly convex case

Let and . When , an analogous analysis to [47, Theorem 2.4, Propositions 2.12 and 3.5], essentially based on the strict convexity of on , can be carried out and we immediately obtain the following results for forward-start option prices and forward implied volatilities (hence proving Theorems 3.1 and 4.1 when holds):

Lemma 7.4.

Proof.

We sketch here a quick outline of the proof. For any , the equation has a unique solution by strict convexity arguments. Define the random variable ; using Fourier transform methods analogous to [47, Theorem 2.4, Proposition 2.12]) the option price reads, for large enough ,

where is the characteristic function of under the new measure defined by . Using Lemma 7.2, the proofs of the option price and the forward smile expansions are similar to those of [47, Theorem 2.4 and Proposition 2.12] and [47, Proposition 3.5]. The exact representation of the set follows from the definition of in Table 2 and the properties of . ∎

7.3. Other cases: general methodology

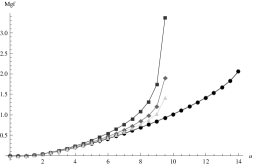

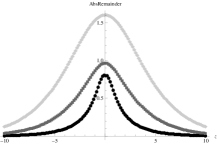

Suppose that (defined in Section 7.2) is finite with . We cannot define a change of measure (as in the proof of Lemma 7.4) by simply replacing for since the forward lmgf explodes at these points as tends to infinity (see Figure 7).

One of the objectives of the analysis is to understand the explosion rate of the forward lmgf at these boundary points. The key observation is that just before infinity, the forward lmgf is still steep on , and an analogous measure change to the one above can be constructed. We therefore introduce the time-dependent change of measure

| (7.5) |

where is the unique solution to the equation for . We shall also require that there exists such that for all and ; therefore Lemma 7.2 holds, and we can ignore the exponential remainder ( for all ) so that the equation reduces to 444A similar analysis can be conducted even if is not eventually in the interior of the limiting domain, but then one will need to use the full lmgf (not just the expansion) in (7.6).

| (7.6) |

In the analysis below, we will also require to solve (7.6) and to converge to other points in the domain (not only boundary points). This will be required to derive asymptotics under for the strikes and , where there are no moment explosion issues but rather issues with the non-existence of the limiting Fourier transform (see Section 7.5 for details). We therefore make the following assumption:

Assumption 7.5.

There exists and a set such that for all and , Equation (7.6) admits a unique solution on satisfying .

Under this assumption is finite for and . Also is almost surely strictly positive and by definition . Therefore (7.5) is a valid measure change for sufficiently large and all .

Our next objective is to prove weak convergence of a rescaled version of the forward price process under this new measure. To this end define the random variable for and some , with characteristic function under :

| (7.7) |

Define now the functions and by

| (7.8) |

where denotes the complex conjugate of in (A.1), namely:

| (7.9) |

The main result here (proved in Appendix A) is an asymptotic representation for forward-start option prices:

Lemma 7.6.

Under Assumption 7.5, there exists such that for all , as :

| (7.10) |

We shall also need the following result on the behaviour of the characteristic function of

Lemma 7.7.

Proof.

Fix . Analogous arguments to Lemma B.2(iii) yield that for any . Assumption 7.5 implies that for all , . It also implies that , and hence there exists and such that for all . Now, since is strictly positive and concave on and , we obtain . This implies that the quantities and are all equal to for all . Using the definition of , the change of measure (7.5) and Lemmas 7.2 and B.2, we can write

Since the remainder tends to zero exponentially fast as tends to infinity. The uniformity of the remainder follows from tedious, yet non-technical, computations showing that the absolute value of the difference between and its approximation is bounded by a constant independent of as tends to infinity. ∎

7.4. Asymptotics in the case of extreme limiting moment explosions

We consider now the cases , and , corresponding to the limiting lmgf being linear.

Lemma 7.8.

Assumption 7.5 is verified in the following cases:

-

(i)

with and ;

-

(ii)

and with and .

-

(iii)

and with and .

Proof.

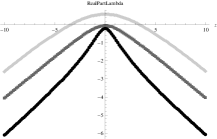

Consider Case (i) and re-write (7.6) as . Let ; since is strictly convex on , we have . We now show that has the necessary properties to prove the lemma. The following statements can be proven in a tedious yet straightforward manner (Figure 8 provides a visual help):

-

(i)

On there exists a unique such that ;

-

(ii)

is strictly increasing and tends to infinity at .

Therefore (i) and (ii) imply that a unique solution to (7.6) exists satisfying the conditions of the lemma with . The function is strictly positive on , and hence for large enough , is strictly increasing and bounded above by , and therefore converges to a limit . If , then the continuity of and and the strict convexity of implies that , which is a contradiction. Therefore , which proves Case (i). Cases (ii) and (iii) are analogous, and the lemma follows. ∎

In the following lemma we derive an asymptotic expansion for . This key result will allow us to derive asymptotics for the characteristic function as well as other auxiliary quantities needed in the analysis.

Lemma 7.9.

Proof.

Consider Regime when is in force, i.e. , and fix such a . Existence and uniqueness was proved in Lemma 7.8 and so we assume the result as an ansatz. This implies the following asymptotics as tends to infinity:

| (7.11) |

We substitute this into (7.6) and solve at each order. At the order we obtain which is well-defined since and . We choose the negative root since we require for large enough. In a tedious yet straightforward manner we continue the procedure and iteratively solve at each order (the next equation is linear in ) to derive the asymptotic expansion in the lemma. The other cases follow from analogous arguments. ∎

We now derive asymptotic expansions for . The expansions will be used in the next section to derive asymptotics for the function in (7.8).

Lemma 7.10.

The following expansions hold as tends to infinity:

-

(i)

In Regimes , and ,

-

(a)

under :

-

(b)

under :

-

(a)

-

(ii)

In Regimes and ,

-

(a)

For :

-

(b)

For :

-

(a)

for some integer different from one line to the other. Recall that is defined in (7.7) and in (3.2). Furthermore, as tends to infinity the remainders in (i) and (ii)(b) are uniform in for and the remainder in (ii)(a) is uniform in for .

Remark 7.11.

-

(i)

In Case (i)(a), converges weakly to a centred Gaussian with variance when holds.

-

(ii)

In Case (i)(b), converges weakly a centred Gaussian with variance when holds.

-

(iii)

In Case(ii)(a), converges weakly to the zero-mean random variable , where and is a Gamma random variable with shape parameter and scale parameter . Lemma 7.14 implies that the limiting characteristic function satisfies for any .

-

(iv)

In Case(ii)(b), converges weakly to the zero-mean random variable , where is Gaussian with mean and variance and is Gamma-distributed with shape and scale .

We now prove Case (i)(a) in Regime , as the proofs in all other cases are similar. In the forthcoming analysis we will be interested in the asymptotics of the function defined by

| (7.12) |

Under , in Case (i)(a), tends to zero as tends to infinity, so that it is not immediately clear what happens to for large . But the asymptotic behaviour of in (7.11) and the definition (7.12) yield the following result:

Lemma 7.12.

Proof of Lemma 7.10.

Consider Regime when is in force, i.e. , and fix such a , and for ease of notation drop the superscripts and -dependence. Lemma 7.7 yields

| (7.13) |

Using Lemma 7.9, we have the Taylor expansion (similar to (7.11))

| (7.14) |

as tends to infinity, where , and are evaluated at . Using (7.11) we further have

| (7.15) | ||||

| (7.16) |

We now study the behaviour of , where is defined in (2.6). Using Lemma 7.12 and the expansion (7.15) for large , we first note that

| (7.17) |

with defined in (7.12). Together with (7.14), this implies

| (7.18) |

with defined in (3.2). Substituting in (3.3) into the second term in (7.4) we find

| (7.19) |

Following a similar procedure using we establish for large that

| (7.20) |

and combining (7.4), (7.19) and (7.20) we find that

| (7.21) |

We now analyse the second term of . We first re-write this term as

| (7.22) | |||

and deal with each of the multiplicative terms separately. For the first term we re-write it as

| (7.23) |

and then we use the asymptotics of in 7.12 and equation (7.17) to find that as tends to infinity,

| (7.24) |

For the second term we use the asymptotics in (7.11) and (7.16) to find that for large

It then follows that for the second term of that for large we have

| (7.25) |

Further as tends to infinity, the equality (7.15) implies

| (7.26) |

Combining (7.21), (7.25) and (7.26) into (7.13) completes the proof. The proof of the uniformity of the remainders and the existence of the integer follow the same lines as the proof of [11, Lemmas 7.1, 7.2]. ∎

In order to derive complete asymptotic expansions we still need to derive expansions for and in (7.8). This is the purpose of this section. We first derive an expansion for which gives the leading-order decay of large-maturity out-of-the-money options:

Lemma 7.13.

Proof.

Consider Regime in Case(i)(a) (namely when holds), and again for ease of notation drop the superscripts and -dependence. We now use Lemma 7.9 and (7.11) to write for large :

| (7.27) | ||||

with and where we have used the characterisation of given in Lemma 2.1. We now study the asymptotics of . Using the definition of in (7.12) we write

| (7.28) |

and deal with each of these terms in turn. Now by (7.20) we have, as tends to infinity,

| (7.29) |

Using the asymptotics of given in Lemma 7.12 and those of in (7.11) we find

| (7.30) |

Using the definition of in (3.3), note the simplification . Combining this, (7.27), (7.28), (7.29) and (7.30) we find that

with , and in (3.4). All other cases follows in an analogous fashion and this completes the proof. ∎

In Lemma 7.15 below we provide asymptotic expansions for the function in (7.8). However, we first need the following technical result, the proof of which can be found in [11, Lemma 7.3]. Let denote the density of a Gamma random variable with shape and scale , and the corresponding characteristic function:

| (7.31) |

Lemma 7.14.

The following expansion holds as tends to infinity:

with , , and denoting the -th derivative of the Gamma density .

Lemma 7.15.

Proof.

Again, we only consider here Regime under in Case (i)(a). Using the asymptotics of given in Lemma 7.9, we can Taylor expand for large to obtain where the remainder is uniform in as soon as . Combining this with the characteristic function asymptotics in Lemma 7.10 we find that for large , Using Lemma B.1, there exists such that as tends to infinity we can write this integral as

The second line follows from Lemma 7.10 and in the third line we have used that the tail estimate for the Gaussian integral is exponentially small and absorbed this into the remainder . By extending the analysis to higher order the term is actually zero and the next non-trivial term is . For brevity we omit the analysis and we give the remainder as in the lemma. Case (i)(b) follows from analogous arguments to above and we now move onto Case (ii)(a). Using the asymptotics of in Lemma 7.9 we have where we set and the remainder is uniform in as soon as . Using the characteristic function asymptotics in Lemma 7.10 and Lemma B.1, there exists such that as tends to infinity:

| (7.32) |

The second line follows from Lemma 7.10 and Remark 7.11(iii). Further we note that

for some as tends to infinity. Combining this with (7.32) we can write

where we have absorbed the exponential remainder into , and where the second line follows from Lemma 7.14. We now prove (ii)(b). Using the asymptotics of for large in Lemma 7.9, we obtain , with and where the remainder is uniform in as soon as . Using the characteristic function asymptotics in Lemma 7.10 and analogous arguments as above we have the following expansion for large :

Let and denote the Gaussian density and characteristic function with zero mean and variance . Using (7.31), we have

so that

This integral can now be computed in closed form and the result follows after simplification using the definition of and the duplication formula for the Gamma function. ∎

7.5. Asymptotics in the case of non-existence of the limiting Fourier transform

In this section, we are interested in the cases where whenever is in force, which corresponds to all the regimes except and at . In these cases, the limiting Fourier transform is undefined at these points. We show here however that the methodology of Section 7.3 can still be applied, and we start by verifying Assumption 7.5. The following quantity will be of primary importance:

| (7.33) |

for , and it is straightforward to check that is well defined whenever is in force.

Lemma 7.16.

Let and assume that . Then, whenever holds, Assumption 7.5 is satisfied with and . Additionally, if , then there exists such that if and if for all , and if , then there exists such that for all ;

Proof.

Recall that the function is defined in (2.6). We first prove the lemma in the case , in which case . Note that if and only if and if and only if . Now let and and consider the equation . Since is continuous is strictly positive in some neighbourhood of zero. In order for the right-hand side to be positive we require our solution to be in for some since is strictly convex. So let . With the right-hand side locked at we then adjust accordingly so that . We then set . It is clear that for there always exists a unique solution to this equation and furthermore is strictly increasing and bounded above by zero. The limit has to be zero otherwise the continuity of and implies , a contradiction. A similar analysis holds for and in this case converges to zero from above. When then for all (i.e. it is a fixed point). Analogous arguments hold for : if and only if () and if and only if . If () then converges to from below (above) and when , for all . ∎

We now provide expansions for and the characteristic function . Define the following quantities:

| (7.34) |

The proofs are analogous to Lemma 7.9 and 7.10 and omitted. Note that the asymptotics are in agreement with the properties of in Lemma 7.16.

Lemma 7.17.

Let and assume that . When , the following expansions hold as tends to infinity (for some integer ):

We now define the following functions from to and then provide expansions for in (7.8):

| (7.35) |

Lemma 7.18.

Let and assume that . Then the following expansions hold as tends to infinity (with given in (7.34)):

Proof.

Consider the case . Set and note that . Using Lemma 7.17 and the definition of in (7.8):

| (7.36) |

We cannot now simply Taylor expand for small and integrate term by term since in the limit is not . This was the reason for introducing the time dependent term so that the Fourier transform exists for any . Indeed, we easily see that . We therefore integrate these terms directly and then compute the asymptotics as tends to infinity. Note first that since , then . Further for any , , and . Now using the definition of in (7.35) and exchanging the integrals and the asymptotic (an analogous justification to the proof of Lemma 7.15(i)) in (7.36) we obtain

Using Lemma 7.17 and asymptotics of the cumulative normal distribution function we compute:

The case is analogous using and the lemma follows. ∎

Remark 7.19.

Consider and with in Section 7.4. Here also tends to and it is natural to wonder why we did not encounter the same issues with the limiting Fourier transform as we did in the present section. The reason this was not a concern was that the speed of convergence () of to was the same as that of the random variable to its limiting value. Intuitively the lack of steepness of the limiting lmgf was more important than any issues with the limiting Fourier transform. In the present section steepness is not a concern, but again in the limit the Fourier transform is not defined. This becomes the dominant effect since converges to at a rate of while the re-scaled random variable converges to its limit at the rate .

7.6. Forward smile asymptotics: Theorem 4.1

The general machinery to translate option price asymptotics into implied volatility asymptotics has been fully developed by Gao and Lee [32]. We simply outline the main steps here. There are two main steps to determine forward smile asymptotics: (i) choose the correct root for the zeroth-order term in order to line up the domains (and hence functional forms) in Theorem 4.1 and Corollary 3.3; (ii) match the asymptotics.

We illustrate this with a few cases from Theorem 4.1. Consider and with . We have asymptotics for forward-start call option prices for in Theorem 4.1. The only BSM regime in Corollary 3.3 where this holds is where . We now substitute our asymptotics for and at leading order we have the requirement: implies that . We then need to check that this holds only for the correct root used in the theorem. Note that we only use the leading order condition here since if then there will always exist a such that , for . Suppose now that we choose the root not as given in Theorem 4.1. Then for the upper bound we get the condition . Since we require and then this only holds for . This already contradicts but let’s continue since it may be true for a more limited range of . The lower bound gives the condition . But the upper bound implied that we needed and so further . Therefore but this can never hold since simple computations show that . Now let’s choose the root according to the theorem. For the upper bound we get the condition and this is always true. For the lower bound we get the condition and this is always true for since . This shows that we have chosen the correct root for the zeroth-order term and we then simply match asymptotics for higher order terms.

As a second example consider and in Theorem 4.1. Substituting the ansatz into the BSM asymptotics for forward-start call options in Corollary 3.3, we find

where , and and is a constant, the exact value does not matter here. We now equate orders with Theorem 3.1. At the zeroth order we get two solutions and since , we choose the negative root such that matches the domains in Corollary 3.3 and Theorem 3.1 for large (using similar arguments as above). At the first order we solve for . But now at the second order, we can only solve for higher order terms if due to the term in the forward-start option asymptotics in Theorem 3.1. All other cases follow analogously.

Appendix A Proof of Lemma 7.6

Lemma A.1.

There exists such that for all , , .

Proof.

We compute:

| (A.2) |

where the inequality follows from the simple bounds

Finally (A.2) is finite since , . ∎

We denote the convolution of two functions by , and recall that . For , we denote its Fourier transform by and the inverse Fourier transform by For , define the functions by

and define by . Recall the -measure defined in (7.5) and the random variable defined on page 7.3. We now have the following result:

Lemma A.2.

There exists such that for all and :

| (A.3) |

Proof.

Assuming (for now) that , we have for any , for . For we can write

which is valid for with in (A.1). For we can write

which is valid for . Finally, for we have

which is valid for . From the definition of the -measure in (7.5) and the random variable on page 7.3 we have

with and denoting the density of . On the strips of regularity derived above we know there exists such that for . Since is a density, , and therefore

| (A.4) |

We note that and hence

| (A.5) |

Thus by Lemma A.1 there exists such that for . By the inversion theorem [63, Theorem 9.11] this then implies from (A.4) and (A.5) that for :

∎

We now move onto the proof of Lemma 7.6. We use our time-dependent change of measure defined in (7.5) to write our forward-start option price for as

with defined on page 7.3. We now apply Lemma A.2 and then convert to forward-start call option prices using Put-Call parity and that in the Heston model is a true martingale [3, Proposition 2.5]. Finally the expansion for follows from Lemma 7.2.

Appendix B Tail Estimates

Lemma B.1.

There exists such that the following tail estimate holds for all and as tends to infinity:

Proof.

By the definition of in (7.7) we have For we have the simple estimate and therefore

for all . We deal with the case . Analogous arguments hold for the case . Lemma B.2(i) implies that there exists such that for :

Using Lemma B.2(ii) we compute

for any . Now using that and are continuous and Assumption 7.5 we have that and as tends to infinity. Lemma B.2(iii) implies that and the lemma follows. ∎

Lemma B.2.

-

(i)

The expansion holds as tends to infinity where for some and is uniform in .

-

(ii)

There exists such that for all and .

-

(iii)

For all the function has a unique maximum at zero.

Proof.

- (i)

- (ii)

-

(iii)

The proof of (iii) is straightforward and follows the same steps as [47, Appendix C]. We omit it for brevity.

∎

References

- [1] E. Alòs, J. León and J. Vives. On the short-time behavior of the implied volatility for jump-diffusion models with stochastic volatility. Finance and Stochastics, 11: 571-589, 2007.

- [2] L.B.G. Andersen and A. Lipton. Asymptotics for exponential Lévy processes and their volatility smile: survey and new results. International Journal of Theoretical and Applied Finance, 16(1): 1-98, 2013.

- [3] L. Andersen and V.P. Piterbarg. Moment Explosions in Stochastic Volatility Models. Finance and Stochastics, 11(1): 29-50, 2007.

- [4] R. Bahadur and R. Rao. On deviations of the sample mean. Annals of Mathematical Statistics, 31: 1015-1027, 1960.

- [5] P. Balland. Forward Smile. Global Derivatives Conference, 2006.

- [6] S. Benaim and P. Friz. Smile asymptotics II: models with known moment generating functions. Journal of Applied Probability, 45: 16-32, 2008.

- [7] S. Benaim and P. Friz. Regular Variation and Smile Asymptotics. Mathematical Finance, 19(1): 1-12, 2009.

- [8] G. Ben Arous. Développement asymptotique du noyau de la chaleur hypoelliptique hors du cut-locus. Annales Scientifiques de l’Ecole Normale Supérieure, 4(21): 307-331, 1988.

- [9] E. Benhamou, E. Gobet and M. Miri. Smart expansions and fast calibration for jump diffusions. Finance and Stochastics, 13: 563-589, 2009.

- [10] B. Bercu, F. Gamboa and M. Lavielle. Sharp large deviations for Gaussian quadratic forms with applications. ESAIM PS, 4: 1-24, 2000.

- [11] B. Bercu and A. Rouault. Sharp large deviations for the Ornstein-Uhlenbeck process. Theory Probab. Appl., 46(1): 1-19, 2002.

- [12] H. Berestycki, J. Busca, and I. Florent. Computing the implied volatility in stochastic volatility models. Communications on Pure and Applied Mathematics, 57(10): 1352-1373, 2004.

- [13] L. Bergomi. Smile Dynamics I. Risk, September, 2004.

- [14] F. Black and M. Scholes. The Pricing of Options and Corporate Liabilities. Journal of Political Economy, 81(3): 637-659, 1973.

- [15] R. Bompis. Stochastic expansion for the diffusion processes and applications to option pricing. PhD thesis, Ecole Polytechnique, pastel-00921808, 2013.

- [16] W. Bryc and A. Dembo. Large deviations for quadratic functionals of Gaussian processes. J.Theoret. Probab., 10: 307-332, 1997.

- [17] H. Bühler. Applying Stochastic Volatility Models for Pricing and Hedging Derivatives. Available at quantitative-research.de/dl/021118SV.pdf, 2002.

- [18] G. Conforti, J.D. Deuschel and S. De Marco. On small-noise equations with degenerate limiting system arising from volatility models. Large Deviations and Asymptotic Methods in Finance, Springer Proceedings in Mathematics and Statistics, 110, 2015.

- [19] S. De Marco, C. Hillairet and A. Jacquier. Shapes of implied volatility with positive mass at zero. Preprint, http://arxiv.org/abs/1310.1020, 2013.

- [20] A. Dembo and O. Zeitouni. Large deviations techniques and applications. Jones and Bartlet Publishers, Boston, 1993.

- [21] A. Dembo and O. Zeitouni. Large deviations via parameter dependent change of measure and an application to the lower tail of Gaussian processes, Progr. Probab., 36: 111-121, 1995.

- [22] J.D. Deuschel, P.K. Friz, A. Jacquier and and S. Violante. Marginal density expansions for diffusions and stochastic volatility, Part I: Theoretical foundations. Communications on Pure and Applied Mathematics, 67(1): 40-82, 2014.

- [23] J.D. Deuschel, P.K. Friz, A. Jacquier and and S. Violante. Marginal density expansions for diffusions and stochastic volatility, Part II: Applications. Communications on Pure and Applied Mathematics, 67(2): 321-350, 2014.

- [24] J. Figueroa-López, R. Gong and C. Houdré. Small-time expansions of the distributions, densities, and option prices of stochastic volatility models with Lévy jumps. Stochastic Processes and their Applications, 122: 1808-1839, 2012.

- [25] D. Florens-Landais and H. Pham. Large deviations in estimation of Ornstein-Uhlenbeck model. J.Appl. Prob., 36: 60-77, 1999.

- [26] M. Forde and A. Jacquier. Small-time asymptotics for implied volatility under the Heston model. International Journal of Theoretical and Applied Finance, 12(6), 861-876, 2009.

- [27] M. Forde and A. Jacquier. The large-maturity smile for the Heston model. Finance and Stochastics, 15(4): 755-780, 2011.

- [28] M. Forde, A. Jacquier and R. Lee. The small-time smile and term structure of implied volatility under the Heston model. SIAM Journal of Financial Mathematics, 3(1): 690-708, 2012..

- [29] M. Forde, A. Jacquier and A. Mijatović. Asymptotic formulae for implied volatility in the Heston model. Proceedings of the Royal Society A, 466(2124): 3593-3620, 2010.

- [30] J.P. Fouque, G. Papanicolaou, R. Sircar and K. Solna. Multiscale Stochastic Volatility for Equity, Interest Rate, and Credit Derivatives. CUP, 2011.

- [31] P. Friz, S. Gerhold, A. Gulisashvili and S. Sturm. Refined implied volatility expansions in the Heston model. Quantitative Finance, 11 (8): 1151-1164, 2011.

- [32] K. Gao and R. Lee. Asymptotics of Implied Volatility to Arbitrary Order. Finance and Stochastics, 18(2): 349-392, 2014.

- [33] J. Gatheral. A parsimonious arbitrage-free implied volatility parameterization with application to the valuation of volatility derivatives. madrid2004.pdf, 2004.

- [34] J. Gatheral. The Volatility Surface: A Practitioner’s Guide. John Wiley & Sons, 2006.

- [35] J. Gatheral, E.P Hsu, P. Laurence, C. Ouyang, T-H. Wong. Asymptotics of implied volatility in local volatility models. Mathematical Finance, 22: 591-620, 2012.

- [36] J. Gatheral and A. Jacquier. Convergence of Heston to SVI. Quantitative Finance, 11(8): 1129-1132, 2011.

- [37] P. Glasserman and Q. Wu. Forward and Future Implied Volatility. Internat. Journ. of Theor. and App. Fin., 14(3), 2011.

- [38] R.R. Goldberg. Fourier Transforms. CUP, 1970.

- [39] A. Gulisashvili. Asymptotic formulas with error estimates for call pricing functions and the implied volatility at extreme strikes. SIAM Journal on Financial Mathematics, 1: 609-641, 2010.

- [40] A. Gulisashvili. Left-wing asymptotics of the implied volatility in the presence of atoms. International Journal of Theoretical and Applied Finance, 18(2), 2015.

- [41] A. Gulisashvili and E. Stein. Asymptotic Behavior of the Stock Price Distribution Density and Implied Volatility in Stochastic Volatility Models. Applied Mathematics & Optimization, 61 (3): 287-315, 2010.

- [42] P. Hagan and D. Woodward. Equivalent Black volatilities. Applied Mathematical Finance, 6: 147-159, 1999.

- [43] P. Henry-Labordère. Analysis, geometry and modeling in finance. Chapman and Hill/CRC, 2008.

- [44] S. Heston. A closed-form solution for options with stochastic volatility with applications to bond and currency options. The Review of Financial Studies, 6(2): 327-342, 1993.

- [45] A. Jacquier and A. Mijatović. Large deviations for the extended Heston model: the large-time case. Asia-Pacific Financial Markets, 21(3): 263-280, 2014.

- [46] A. Jacquier, M. Keller-Ressel and A. Mijatović. Implied volatility asymptotics of affine stochastic volatility models with jumps. Stochastics, 85(2): 321-345, 2013.

- [47] A. Jacquier and P. Roome. Asymptotics of forward implied volatility. SIAM J. on Financial Mathematics, 6(1): 307-351, 2015.

- [48] A. Jacquier and P. Roome. The small-maturity Heston forward smile. SIAM J. on Financial Mathematics, 4(1): 831-856, 2013.

- [49] A. Jacquier and P. Roome. Black-Scholes in a CEV random environment: a new approach to smile modelling. Preprint available at arXiv:1503.08082, July 2015.

- [50] I. Karatzas and S.E. Shreve. Brownian Motion and Stochastic Calculus. Springer-Verlag, 1997.

- [51] S. Karlin and H. Taylor. A Second Course in Stochastic Processes. Academic Press, 1981.

- [52] M. Keller-Ressel. Moment Explosions and Long-Term Behavior of Affine Stochastic Volatility Models. Mathematical Finance, 21(1): 73-98, 2011.

- [53] N. Kunitomo and A. Takahashi. Applications of the Asymptotic Expansion Approach based on Malliavin-Watanabe Calculus in Financial Problems. Stochastic Processes and Applications to Mathematical Finance, World Scientific, 195-232, 2004.

- [54] R.W. Lee. Option Pricing by Transform Methods: Extensions, Unification and Error Control. Journal of Computational Finance, 7(3): 51-86, 2004.

- [55] R.W. Lee. The Moment Formula for Implied Volatility at Extreme Strikes. Mathematical Finance, 14(3): 469-480, 2004.

- [56] V. Lucic. Forward-start options in stochastic volatility models. Wilmott Magazine, September, 2003.

- [57] E. Lukacs. Characteristic Functions. Griffin, Second Edition, 1970.

- [58] R. Merton. The Theory of Rational Option Pricing. Bell Journal of Economics and Management Science, 4(1): 141-183, 1973.

- [59] A. Mijatović and P. Tankov. A new look at short-term implied volatility in asset price models with jumps. Forthcoming in Mathematical Finance, 2013.

- [60] J. Muhle-Karbe and M. Nutz. Small-time asymptotics of option prices and first absolute moments. Journal of Applied Probability, 48: 1003-1020, 2011.

- [61] S. Pagliarani, A. Pascucci and C. Riga. Adjoint expansions in local Lévy models. SIAM Journal on Financial Mathematics, 4(1): 265-296, 2013.

- [62] H. Pham. Some methods and applications of large deviations in finance and insurance. Paris-Princeton Lecture notes in mathematical Finance, Springer Verlag, 2007.

- [63] W. Rudin. Real and complex analysis, third edition. McGraw-Hill, 1987.

- [64] R. Schöbel and J. Zhu. Stochastic volatility with an Ornstein-Uhlenbeck process: an extension. European Finance Review, 3(1): 23-46, 1999.

- [65] E. Stein and J. Stein. Stock-price distributions with stochastic volatility - an analytic approach. Review of Financial studies, 4(4): 727-752, 1991.

- [66] P. Tankov. Pricing and hedging in exponential Lévy models: review of recent results. Paris-Princeton Lecture Notes in Mathematical Finance, Springer, 2010.

- [67] M. R. Tehranchi. Asymptotics of implied volatility far from maturity. Journal of Applied Probability, 46: 629-650, 2009.

- [68] D. Williams. Probability With Martingales. CUP, 1991.