Convergence rate analysis of the forward-Douglas-Rachford splitting scheme††thanks: This work is partially supported by grants NSF DGE-0707424 (graduate research fellowship program) and NSF DMS-1317602.

Damek Davis

Department of Mathematics, University of California, Los Angeles

Los Angeles, CA 90025, USA

damek@math.ucla.edu

Abstract

Operator splitting schemes are a class of powerful algorithms that solve complicated monotone inclusion and convex optimization problems that are built from many simpler pieces. They give rise to algorithms in which all simple pieces of the decomposition are processed individually. This leads to easily implementable and highly parallelizable or distributed algorithms, which often obtain nearly state-of-the-art performance.

In this paper, we analyze the convergence rate of the forward-Douglas-Rachford splitting (FDRS) algorithm, which is a generalization of the forward-backward splitting (FBS) and Douglas-Rachford splitting (DRS) algorithms. Under general convexity assumptions, we derive the ergodic and nonergodic convergence rates of the FDRS algorithm, and show that these rates are the best possible. Under Lipschitz differentiability assumptions, we show that the best iterate of FDRS converges as quickly as the last iterate of the FBS algorithm. Under strong convexity assumptions, we derive convergence rates for a sequence that strongly converges to a minimizer. Under strong convexity and Lipschitz differentiability assumptions, we show that FDRS converges linearly. We also provide examples where the objective is strongly convex, yet FDRS converges arbitrarily slowly. Finally, we relate the FDRS algorithm to a primal-dual forward-backward splitting scheme and clarify its place among existing splitting methods. Our results show that the FDRS algorithm automatically adapts to the regularity of the objective functions and achieves rates that improve upon the sharp worst case rates that hold in the absence of smoothness and strong convexity.

Operator-splitting schemes are algorithms for splitting complicated problems arising in PDE, monotone inclusions, optimization, and control into many simpler subproblems. The achieved decomposition can give rise to inherently parallel and, in some cases, distributed algorithms. These characteristics are particularly desirable for large-scale problems that arise in machine learning, finance, control, image processing, and PDE [5].

In optimization, the Douglas-Rachford splitting (DRS) algorithm [21] minimizes sums of (possibly) nonsmooth functions on a Hilbert space :

(1)

During each step of the algorithm, DRS applies the proximal operator, which is the basic subproblem in nonsmooth minimization, to and individually rather than to the sum . Thus, the key assumption in DRS is that and are easy to minimize independently, but the sum is difficult to minimize. We note that many complex objectives arising in machine learning [5] and signal processing [11] are the sum of nonsmooth terms with simple or closed-form proximal operators.

The forward-backward splitting (FBS) algorithm [23] is another technique for solving (1) when is known to be smooth. In this case, the proximal operator of is never evaluated. Instead, FBS combines gradient (forward) steps with respect to and proximal (backward) steps with respect to . FBS is especially useful when the proximal operator of is complex and its gradient is simple to compute.

Recently, the forward-Douglas-Rachford splitting (FDRS) algorithm [7] was proposed to combine DRS and FBS and extend their applicability (see Algorithm 1). More specifically, let be a closed vector space and suppose is smooth. Then FDRS applies to the following constrained problem:

(2)

Throughout the course of the algorithm, the proximal operator of , the gradient of , and the projection operator onto are all employed separately.

The FDRS algorithm can also apply to affinely constrained problems. Indeed, if for a closed vector subspace and a vector , then Problem (2) can be reformulated as

(3)

For simplicity, we only consider linearly constrained problems.

The FDRS algorithm is a generalization of the generalized forward-backward splitting (GFBS) algorithm [24], which solves the problem where are closed, proper, convex and (possibly) nonsmooth. In the GFBS algorithm, the proximal mapping of each function is evaluated in parallel. We note that GFBS can be derived as an application of FDRS to the equivalent problem:

(4)

In this case, the vector space is the diagonal set of and the function is separable in the components of .

The FDRS algorithm is the only primal operator-splitting method capable of using all structure in Equation (2).

In order to achieve good practical performance, the other primal splitting methods require stringent assumptions on and . Primal DRS cannot use the smooth structure of , so the proximal operator of must be simple. On the other hand, primal FBS and forward-backward-forward splitting (FBFS) [25] cannot separate the coupled nonsmooth structure of and , so minimizing subject to must be simple. In contrast, FDRS achieves good practical performance if it is simple to minimize , evaluate , and project onto .

Modern primal-dual splitting methods [8, 18, 13, 26, 6, 19] can also decompose problem (2), but they introduce extra variables and are, thus, less memory efficient. It is unclear whether FDRS will perform better than primal-dual methods when memory is not a concern. However, it is easier to choose algorithm parameters for FDRS and, hence, it can be more convenient to use in practice.

Application: constrained quadratic programming and support vector machines

Let and be natural numbers. Suppose that is a symmetric positive semi-definite matrix, is a vector, is a constraint set, is a linear map, and is a vector. Consider the problem:

(5)

subject to:

Problem (5) arises in the dual form soft-margin kernelized support vector machine classifier [14] in which is a box constraint, is , and has rank one. Note that by the argument in (3), we can always assume that .

Define the smooth function , the indicator function (which is on and elsewhere), and the vector space . With this notation, (5) is in the form (2) and, thus, FDRS can be applied. This splitting is nice because is simple whereas the proximal operator of requires a matrix inversion which is expensive for large-scale problems.

1.1 Goals, challenges, and approaches

This work seeks to characterize the convergence rate of the FDRS algorithm applied to Problem (2). Recently, [16] has shown that the sharp convergence rate of the fixed-point residual (FPR) (see Equation (21)) of the FDRS algorithm is . To the best of our knowledge, nothing is else is known about the convergence rate of FDRS. Furthermore, it is unclear how the FDRS algorithm relates to other algorithms. We seek to fill this gap.

The techniques used in this paper are based on [15, 16, 17]. These techniques are quite different from those used in classical objective error convergence rate analysis. The classical techniques do not apply because the FDRS algorithm is driven by the fixed-point iteration of a nonexpansive operator, not by the minimization of a model function. Thus, we must explicitly use the properties of nonexpansive operators in order to derive convergence rates for the objective error.

We summarize our contributions and techniques as follows:

1.

We analyze the objective error convergence rates (Theorems 12 and 15) of the FDRS algorithm under general convexity assumptions. We show that FDRS is, in the worst case,

nearly as slow as the subgradient method yet nearly as fast as the proximal point algorithm (PPA) in the ergodic sense. Our nonergodic rates are shown by relating the objective error to the FPR through a fundamental inequality. We also show that the derived rates are sharp through counterexamples (Remarks 4 and 5).

2.

We show that if or is strongly convex, then a natural sequence of points converges strongly to a minimizer. Furthermore, the

best iterate converges with rate , the ergodic iterate converges with rate , and the nonergodic iterate converges with rate . The results follow by showing that a certain sequence of squared norms is summable. We also show that some of the derived rates are sharp by constructing a novel counterexample (Theorem 25).

3.

We show that if is differentiable and is Lipschitz, then the best iterate of the FDRS algorithm has objective error of order (Theorem 19). This rate is an improvement over the sharp convergence rate for nonsmooth . The result follows by showing that the objective error is summable.

4.

We establish scenarios under which FDRS converges linearly (Theorem 20) and show that linear convergence is impossible under other scenarios (Theorem 25).

5.

We show that even if and are strongly convex, the FDRS algorithm can converge arbitrarily slowly (Theorem 24).

6.

We show that the FDRS algorithm is the limiting case of a recently developed primal-dual forward-backward splitting algorithm (Section 7) and, thus, clarify how FDRS relates to existing algorithms.

Our analysis builds on the techniques and results of [7, 16, 17]. The rest of this section contains a brief review of these results.

1.2 Notation and facts

Most of the definitions and notation that we use in this paper are standard and can be found in [3]. Throughout this paper, we use to denote (a possibly infinite dimensional) Hilbert space. In fixed-point iterations, will denote a sequence of relaxation parameters, and

(6)

is its th partial sum.

For any subset , we define the distance function:

(7)

In addition, we define the indicator function of : for all and , we have and .

Given a closed, proper, and convex function , the set denotes its subdifferential at and

denotes a subgradient. (This notation was used in [4, Eq. (1.10)].) If is Gâteaux differentiable at , we have [3, Proposition 17.26].

Let be the identity map on . For any and , we let

which are known as the proximal and reflection operators, respectively.

The subdifferential of the indicator function where is a closed vector subspace is defined as follows: for all ,

(8)

where is the orthogonal complement of . Evidently, if is the projection onto , then

and these operators are independent of .

Let , let , and let be a map. The map is called -Lipschitz continuous if for all . The map is called nonexpansive if it is -Lipschitz. We also use the notation:

(9)

If and is nonexpansive, then is called -averaged [3, Definition 4.23].

We call the following identity the cosine rule:

(10)

Young’s inequality is the following: for all and , we have

(11)

1.3 Assumptions

Assumption 1(Convexity).

and are closed, proper, and convex.

We also assume the existence of a particular solution to (2)

Assumption 2(Solution existence).

Finally we assume that is sufficiently nice.

Assumption 3(Differentiability).

The function is differentiable, is -Lipschitz, and is -Lipschitz.

For now, we do not specify the stepsize parameters. See section 1.6 for choices that ensure convergence and, see Lemma 6 and Figure 1 for intuition.

Evidently, Algorithm 1 has the form: for all , where

(12)

Because is nonexpansive (Part 7 of Proposition 1), it follows that the FDRS algorithm is a special case of the Krasnosel’skiĭ-Mann (KM) iteration [20, 22, 10].

By choosing particular and , we recover several other splitting algorithms:

For general and , the primal DRS and FBS algorithms are not capable splitting Problem (2) in the same way as (12). Indeed, the DRS algorithm cannot use the smooth structure of , and the FBS algorithm requires the evaluation of The FDRS algorithm eliminates these difficult problems and replaces them with (possibly) more tractable ones.

1.5 Proximal, averaged, and FDRS operators

We briefly review some operator-theoretic properties.

Proposition 1.

Let , let , let , and let be closed, proper, and convex.

1.

Optimality conditions of : Let . Then if, and only if,

2.

Optimality conditions of : Let . Then if, and only if,

Also, .

3.

Averaged operator contraction property: A map is -averaged (see (9)) if, and only if, for all ,

(13)

4.

Composition of averaged operators: Let . Suppose and are and -averaged operators, respectively. Then for all , the map is averaged with parameter

(14)

5.

Wider relaxations: A map is -averaged if, and only if, (see (9)) is -averaged for all .

6.

Proximal operators are -averaged: The operator is -averaged and, hence, the operator is nonexpansive.

7.

Averaged property of the FDRS operator: Suppose that . Then the operator (see (12)) is averaged.

Proof.

Parts 1, 2, 3, 5, and 6 can be found in [3]. Part 4 can be found in [12]. Part 7 follows from two facts: The operator is -averaged by Part 6, and is -averaged by [7, Proposition 4.1 (ii)]. Thus, Part 4 proves Part 7.

∎

Remark 1.

Later we require so we hope that is small. Note that the expression for is new and improves upon the previous constant: See also [12, Remark 2.7 (i)].

The proof of the following Proposition is essentially contained in [12, Theorem 2.4]. We reproduce it in Appendix B.1 in order to derive a bound. The reader should note the following inequality before reading the proof.

Remark 2.

Let . Then it is easy to show that

(15)

Proposition 2.

Let . Suppose that and are and -averaged operators, respectively, and that is a fixed-point of . Define as in (14). Let , let , and consider a sequence . Let be generated by the following iteration: for all , let Then

1.6 Convergence properties of FDRS

The paper [7] assumed the stepsize constraint in order to guarantee convergence of Algorithm 1. We now show that the parameter can (possibly) be increased beyond , which can result in faster practical performance. The proof follows by constructing a new Lipschitz differentiable function so that the triple generates the same FDRS operator, , as . This result was not included in [7].

Lemma 3.

Define a function

(16)

Then the FDRS operator associated to is identical to the FDRS operator associated to . Let be the Lipschitz constant of . Then . In addition, let . Then is -averaged where

(17)

Proof.

The averaged property of and the equivalence of FDRS operators follows from Part 7 of Proposition 1. The bound follows because for all ,

There are cases where is significantly larger than . For instance, in the quadratic programming example in (5), is the reciprocal of the Lipschitz constant of , which is the maximal eigenvalue of . On the other hand, the gradient has rank at most . Thus, unless the eigenvectors of with eigenvalue lie in the -dimensional space , the constant is larger than . See Appendix A for experimental evidence.

Most of our results do not require that converges. However, for completeness we include the following weak convergence result.

Proposition 4.

Let , let , and suppose that Then (from Algorithm 1) weakly converges to a fixed-point of .

Proof.

Apply [7, Proposition 3.1] with the new averaged parameter .

∎

The following theorem recalls several results on convergence rates for the iteration of averaged operators [16]. In addition, we show that is a summable sequence [7] whenever is chosen properly.

Theorem 5.

Suppose that is generated by Algorithm 1 with and , and let be a fixed-point of . Then

1.

Fejér monotonicity: the sequence is nonincreasing. In addition, for all and , we have

2.

Summable fixed-point residual: The sum is finite:

3.

Convergence rates of fixed-point residual: For all , let . Suppose that . Then for and ,

(18)

4.

Gradient summability: Let and suppose that

(19)

Then the following gradient sum is finite:

(20)

Proof.

Parts 1, 2, and 3 are a direct consequence of [16, Theorem 1] applied to the -averaged operator . Part 4 is a direct consequence of Proposition 2 applied to the -averaged operator (see Part 6 of Proposition 1) and the -averaged operator (from the Baillon-Haddad Theorem [1] and [3, Proposition 4.33]).

∎

We call the following term the fixed-point residual (FPR):

(21)

Remark 3.

Note that the convergence rate proved for in (18) is sharp for the operator [16, Section 6.1.1].

2 Subgradients and fundamental inequalities

In this section, we prove several algebraic identities of the FDRS algorithm. In addition, we prove a relationship between the FPR and the objective error (Propositions 9 and 10).

In first-order optimization algorithms, we only have access to (sub)gradients and function values. Consequently, the FPR is usually the squared norm of a linear combination of (sub)gradients of the objective functions. For example, the gradient descent algorithm for a smooth function generates a sequence of iterates by using forward gradient steps: ; the FPR is

In splitting algorithms, the FPR is more complex because the subgradients are generated via forward-gradient or proximal (backward) steps (see Part 1 of Proposition 1) at different points. Thus, unlike the gradient descent algorithm where the objective error can be bounded with the subgradient inequality, splitting algorithms for two or more functions can only bound the objective error when some or all of the functions are evaluated at separate points — unless a Lipschitz assumption is imposed. In order to use this Lipschitz assumption, we enforce consensus among the variables, which is why the FPR rate is useful.

2.1 A subgradient representation of FDRS

Fig. 1: A single FDRS iteration, from to (see Lemma 6). Both occurrences of represent the same subgradient .

Figure 1 pictures one iteration of Algorithm 1: FDRS projects onto to get . The reflection of across is . Then FDRS takes a forward-gradient with respect to from the reflected point and a proximal (backward) step with respect to to get . Finally, we move from to by traveling along the positive subgradient .

where and is uniquely defined by Part 1 of Proposition 1.

In addition, each FDRS step has the following form:

(24)

In particular, .

Definition 7(Ergodic iterates).

Let be generated by Algorithm 1 and define and as in (22) (with ). Then define ergodic iterates:

and

(25)

2.2 Optimality conditions of FDRS

The following lemma characterizes the zeros of in terms of the fixed-points of the FDRS operator. The intuition is the following: If is a fixed-point of , then the base of the rectangle in Figure 1 has length zero. Thus, , and if we travel around the perimeter of the rectangle, we will start and begin at . This argument shows that , i.e., .

That is, if is a fixed-point of , then is a minimizer of (2), and

2.3 Fundamental inequalities

In this section, we prove two fundamental inequalities that relate the FPR (see (21)) to the objective error.

Throughout the rest of the paper, we use the following notation: The functions and are and -strongly convex, respectively, where we allow or to be zero (i.e., no strong convexity). In addition, we assume that is -Lipschitz differentiable, where we allow . If , then . With these assumptions, we get the following lower bounds [3, Theorem 18.15]:

(26)

(27)

where , and for any ,

(28)

(29)

See Appendices B.4, B.5, and B.6 for the proofs of the following inequalities:

Proposition 9(Upper fundamental inequality).

Let , let , and let . Then for all , we have the following inequality:

Let be a fixed-point of , and let . Choose subgradients and with (see Lemma 8). Then for all and , we have

(31)

Corollary 11.

Let , let , and let . Let be a fixed-point of , and let . Then with and from Lemma 6,

(32)

3 Objective convergence rates

In this section, we analyze the ergodic and nonergodic convergence rates of the FDRS algorithm applied to (2).

Throughout the rest of the paper, will denote an arbitrary fixed-point of , and we define a minimizer of (2) using Lemma 8:

All of our bounds will be produced on objective errors of the form:

(33)

The objective error on the left hand side of (33) can be negative. Thus, we bound its absolute value. In addition, we bound . Because , the objective error on the right hand size of (33) is positive. Consequently, is the natural point at which to measure the convergence rate. To derive such a bound, we assume is Lipschitz. Note that in both cases, we have the identity .

3.1 Ergodic convergence rates

In this section, we analyze the ergodic convergence rate of the FDRS algorithm. The key idea is to use the telescoping property of the upper and lower fundamental inequalities, together with the summability of the difference of gradients shown in Part 4 of Theorem 5. See Section 1.2 for the distinction between ergodic and nonergodic convergence rates.

Theorem 12(Ergodic convergence of FDRS).

Let , let , and suppose that satisfies (19). Define and as in (25). Then we have the following convergence rate: for all ,

In addition the following feasibility bound holds:

Proof.

Fix . The feasibility bound follows from Part 1 of Theorem 5:

(34)

Now we prove the objective convergence rates. For all , let . Note that by (15) because we have and . Thus, by Cauchy-Schwarz and (11), we have

(35)

Therefore, by Jensen’s inequality, the Cauchy-Schwarz inequality, (30), and the bound (see (34)), we have

The lower bound in Proposition 10 and the Cauchy-Schwarz inequality show that

In general, and are not in . However, the conclusion of Theorem 12 can be improved if is Lipschitz continuous. The following proposition gives a sufficient condition for Lipschitz continuity on a ball.

Proposition 13(Lipschitz continuity on a ball [3, Proposition 8.28]).

Suppose that is proper and convex. Let , and let . If , then is -Lipschitz on .

To use this fact, we need to show that the sequences , and are bounded. Recall that and for . Proximal, reflection, and forward-gradient maps are nonexpansive (see Proposition 1, the Baillon-Haddad Theorem [1], and [3, Proposition 4.33]), so we have for all . Thus, The ball is convex, so

Corollary 14(Ergodic convergence with Lipschitz ).

Let the notation be as in Theorem 12. Let and suppose is -Lipschitz on . Then

Proof.

The proof follows from by combining the upper bound in Theorem 12 with the following bound:

In this section, we analyze the nonergodic convergence rate of FDRS when is bounded away from and . The proof bounds the inequalities in Propositions 9 and 10 with Theorem 5.

The lower bound follows from (31) and Part 3 of Theorem 5:

(38)

The rates follow from (37) and (38), and the corresponding rates for the FPR in (18). The bounds on follow from .

∎

If is Lipschitz continuous, we can evaluate the entire objective function at . The proof of the following corollary is analogous to Corollary 14. We ask the reader to recall from Section 3.1 that

Corollary 16(Nonergodic convergence with Lipschitz ).

Let the notation be as in Theorem 15. Let and suppose is -Lipschitz on . Then

and .

Proof.

Combine the upper bound in Theorem 15 with the following bound: The rate follows because (see (24) and (18)) and (see Theorem 15).

∎

In this section, we show that , , and their ergodic variants converge strongly whenever or is strongly convex. The techniques in this section are similar to those in Section 3, so we defer the proof to Appedix B.7

Theorem 17(Auxiliary term bound).

Let , let let , and suppose that is generated by Algorithm 1. Then

1.

“Best” iterate convergence: Let and suppose that satisfies (19). If , then

and and .

2.

Ergodic convergence:

If , and satisfies (19), then

3.

Nonergodic convergence:

If , then and

Remark 6.

See Section 6.1 for a proof that the nonergodic “best” rates are sharp. It is not clear if we can improve the general nonergodic rates to .

5 Lipschitz differentiability

In this section, we assume is smooth:

Assumption 4.

is differentiable and is -Lipschitz where .

Under Assumption 4, we will show that the objective value

is summable. Therefore, by [16, Lemma 3] the minimal objective error after iterations is of order . We will need the following upper bound to prove this. See Appendix B.8 for the proof.

Proposition 18(Fundamental inequality under Assumption 4).

If , , , , is a fixed-point of , and , then

(39)

The next theorem shows that the upper bound in Proposition 18 is summable and, as a consequence, we will have convergence.

In addition, by the Cauchy-Schwarz inequality and (11), we have

Therefore, for all ,

Recall that we assume and .

Now suppose that . The following identity follows from from Lemma 6:

This identity results from tracing the perimeter of Figure 1 from to to to . Likewise, we have .

Note that

(41)

Now, fix , and let By the convexity of , we have

Therefore,

Now assume that . Observe that:

where we use the identity (see (24)). The proof of this case is similar to the case except that we use the above identity for , the bound , and the constant

in place of . Then the contraction follows.

In both cases, the linear rate for follows by unfolding (40).

∎

Remark 8.

Note that smaller lead to larger and smaller , while larger lead to smaller and larger .

6.1 Arbitrarily slow convergence for strongly convex problems

In general, we cannot expect linear convergence of FDRS when is not differentiable—even if and are strongly convex. In this section, we construct an example to prove this claim. The following example is based on [2, Section 7] and [16, Example 1].

A family of slow examples

Let . Let denote counterclockwise rotation in by degrees. Let denote the standard unit vector, and let . Let be a sequence of angles in such that as . For all , let . We let

(42)

Note that [2, Section 7] proves the projection identities

We now begin our extension of this example. Choose and set and Note that and . In addition, for , we have Thus, is -Lipschitz, and, hence, and we can choose . Therefore, , so we can choose . We also note that .

Define on each 2-dimensional component of as follows: for all ,

where the second equality follows by direct expansion. Therefore, we have

(43)

Note that for all , the operator has eigenvector

(44)

with eigenvalue . Each component also has the eigenvector with eigenvalue . Thus, the only fixed-point of is . Finally,

(45)

Slow convergence proofs

We know that from (18). Therefore, because is linear, [3, Proposition 5.27] proves the following lemma.

Lemma 21(Strong convergence for linear operators).

Any sequence generated by the operator in (43) converges strongly to . Consequently, the sequences and converge strongly to zero.

Suppose that is a function that is strictly decreasing to zero such that Then there exists a monotonic sequence such that as and an increasing sequence such that for all ,

Let the notation be as in Lemma 22. Then for all , we can find a sequence that satisfies the conditions of the lemma.

Proof.

For any , replace the sequence in Lemma 22 with .

∎

We are now ready to show that FDRS can converge arbitrarily slowly.

Theorem 24(Arbitrarily slow FDRS).

For every function that strictly decreases to zero and satisfies , there is a point and two closed subspaces and with zero intersection, , such that the FDRS sequence generated with the functions and and parameters and strongly converges to zero, but for all , we have

Proof.

For all , define with as in (44). Then and is an eigenvector of with eigenvalue . Define the concatenated vector . Note that because . Thus, for all , we let .

Now, recall that . Thus, for all and , we have

Thus, . Choose and the sequence using Corollary 23 with . Then solve

∎

Remark 9.

Theorems 24 and 17 show that the sequence can converge arbitrarily slowly even if and converge with rate .

The following theorem shows that and do not converge linearly. See Appendix B.9 for the proof.

Theorem 25.

There exists a sequence so that and converge strongly, but not linearly. In particular, for any , there is an initial point so that for all ,

and

Thus, the nonergodic “best” convergence rates in Part 3 of Theorem 17 are sharp.

7 Primal-dual splittings

In this section, we reformulate FDRS as a primal-dual algorithm applied to the dual of the following problem: .

Lemma 26(FDRS is a primal-dual algorithm).

Let , and suppose that is generated by the FDRS algorithm with . For all , let Then for all , we have the recursive update rule:

(46)

Proof.

Fix . By Lemma 6, , so . Thus, the formula for follows from .

Now observe that

Furthermore, . Thus,

The algorithm in (46) is the primal-dual forward-backward algorithm of Vũ and Condat [26, 13] applied to the following dual problem: where is the Legendre-Fenchel transform of [3, Definition 13.1].

For convergence, [26, Theorem 3.1] requires and whereas FDRS requires (and ).

Thus, the FDRS algorithm is a limiting case of Vũ and Condat’s algorithm, much like the DRS algorithm [21] is a limiting case of Chambolle and Pock’s primal-dual algorithm [8]. In addition, the convergence rate analysis in Section 3 cannot be subsumed by the recent convergence rate analysis of the primal-dual gap of Vũ and Condat’s algorithm [15], which only applies when . The original FDRS paper did not show this connection [7, Remark 6.3 (iii)].

8 Conclusion

In this paper, we provided a comprehensive convergence rate analysis of the FDRS algorithm under general convexity, strong convexity, and Lipschitz differentiability assumptions. In almost all cases, the derived convergence rates are shown to be sharp. In addition, we showed that the FDRS algorithm is the limiting case of a recently developed primal-dual forward-backward operator splitting algorithm and, thus, clarify how it relates to existing algorithms. Future work on FDRS might evaluate the performance of the algorithm on realistic problems.

Acknowledgement

We thank Prof. Wotao Yin and the anonymous reviewers for helpful comments. We also thank the two anonymous referees for their insightful and detailed comments.

Appendix A Performance improvement: versus

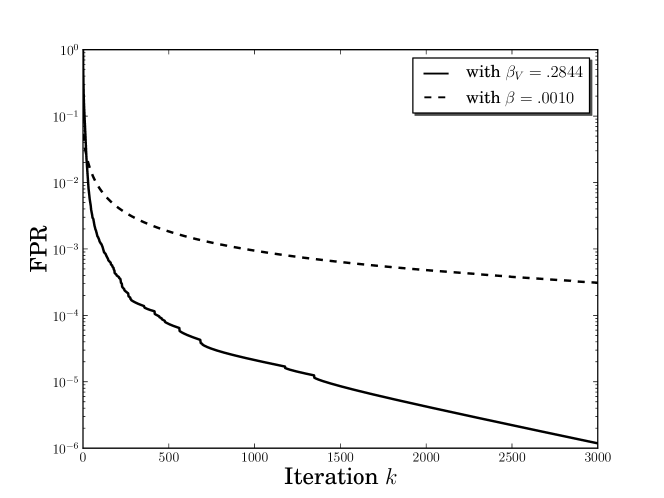

Fig. 2: We plot the normalized FPR, , in a dual SVM example. See Appendix A for the details.

In this section, we briefly illustrate the benefits of using in place of on a Kernelized SVM problem, which is discussed in Section 1; see (5) for notation. In Figure 2 we plot the FPR associated to the FDRS algorithm applied to a 1000-dimensional quadratic program. To generate the quadratic program, we use a random 1000-element subset of the the “a7a” dataset (available from the LIBSVM website [9]) denoted by where for each , is a data point and is a class label. We use the matrix with entry given by the formula for (i.e., we use the radial basis function kernel). The matrix is the row vector , and the set is the box . In this case, has rank , but the maximal eigenvalue of is approximately times smaller than the maximal eigenvalue of . Figure 2 shows that choosing results in a tremendous speedup. (In both examples, we chose .)

The identity for follows from Part 1 of Proposition 1. Note that by the Moreau identity , we have . Note that by definition, and . Thus, we get the identity for :

Finally, given the identity , (24) will follow as soon as we show :

Hence, for all , we have (using as in (35) and (15))

The “best” convergence rates now follow by taking and using [16, Lemma 3]. In addition, we apply Jensen’s inequality to in the first term to get

We now fix . For all , define . Observe that and do not depend on the value of . Therefore, we use (32) to get

(49)

where (49) uses the ()-Lipschitz continuity of and the identity , and the last line uses the Fejér property (see Part 1 of Theorem 5). The rates follow from (49) and the corresponding rates for the FPR in (18).

where the first inequality follows from [3, Theorem 18.15(iii)]. By applying the identity , the cosine rule (10), and the identity (see (24)) multiple times, we have

For all , let . Let , and let Then and, hence, . Now for all , we have

(54)

because . In addition, for all , we have

where the third equality follows because .

Now, for all , let . Again, for all , let be the eigenvalue of associated to . Note that whenever (hint: use the bound , and note that is increasing in for fixed ). Therefore, for all , we have

(55)

where we use and the lower integral approximation of the sum.

Now we prove the bound for . For all , (see (6)). In addition, for all ,

Thus, for all , we have

where the last inequality follows because and . Note that for all , we have because . Therefore, for all , we have

where we use similar arguments to those used in (55).

References

[1]J.-B. Baillon and G. Haddad, Quelques propriétés des

opérateurs angle-bornés et -cycliquement monotones, Israel

Journal of Mathematics, 26 (1977), pp. 137–150.

[2]H. H. Bauschke, J. Y. Bello Cruz, T. T. A. Nghia, H. M. Phan,

and X. Wang, The rate of linear convergence of the Douglas-Rachford

algorithm for subspaces is the cosine of the friedrichs angle, Journal of

Approximation Theory, 185 (2014), pp. 63–79.

[3]H. H. Bauschke and P. L. Combettes, Convex analysis and monotone

operator theory in Hilbert spaces, Springer, 2011.

[4]D. P. Bertsekas, Incremental gradient, subgradient, and proximal

methods for convex optimization: A survey, Optimization for Machine

Learning, (2010), pp. 1–38.

[5]S. Boyd, N. Parikh, E. Chu, B. Peleato, and J. Eckstein, Distributed

optimization and statistical learning via the alternating direction method of

multipliers, Foundations and Trends in Machine Learning, 3 (2011),

pp. 1–122.

[6]L. M. Briceño-Arias and P. L. Combettes, A monotone+skew

splitting model for composite monotone inclusions in duality, SIAM Journal

on Optimization, 21 (2011), pp. 1230–1250.

[7]L. M. Briceño-Arias, Forward-Douglas-Rachford splitting and

forward-partial inverse method for solving monotone inclusions,

Optimization, 64 (2015), pp. 1239–1261.

[8]A. Chambolle and T. Pock, A first-order primal-dual algorithm for

convex problems with applications to imaging, Journal of Mathematical

Imaging and Vision, 40 (2011), pp. 120–145.

[9]C.-C. Chang and C.-J. Lin, LIBSVM: A library for support vector

machines, ACM Transactions on Intelligent Systems and Technology, 2 (2011),

pp. 27:1–27:27.

Software available at \urlhttp://www.csie.ntu.edu.tw/ cjlin/libsvm.

[10]P. L. Combettes, Solving monotone inclusions via compositions of

nonexpansive averaged operators, Optimization, 53 (2004), pp. 475–504.

[11]P. L. Combettes and J.-C. Pesquet, Proximal splitting methods in

signal processing, in Fixed-point algorithms for inverse problems in science

and engineering, Springer, 2011, pp. 185–212.

[12]P. L. Combettes and I. Yamada, Compositions and convex combinations

of averaged nonexpansive operators, Journal of Mathematical Analysis and

Applications, 425 (2015), pp. 55 – 70.

[13]L. Condat, A Primal–Dual Splitting Method for Convex Optimization

Involving Lipschitzian, Proximable and Linear Composite Terms, Journal of

Optimization Theory and Applications, 158 (2013), pp. 460–479.

[14]C. Cortes and V. Vapnik, Support-vector networks, Machine learning,

20 (1995), pp. 273–297.

[16]D. Davis and W. Yin, Convergence rate analysis of several splitting

schemes, arXiv preprint arXiv:1406.4834v2, (2014).

[17], Faster convergence

rates of relaxed Peaceman-Rachford and ADMM under regularity

assumptions, arXiv preprint arXiv:1407.5210v2, (2014).

[18]E. Esser, X. Zhang, and T. Chan, A General Framework for a Class of

First Order Primal-Dual Algorithms for Convex Optimization in Imaging

Science, SIAM Journal on Imaging Sciences, 3 (2010), pp. 1015–1046.

[19]N. Komodakis and J.-C. Pesquet, Playing with Duality: An Overview

of Recent Primal-Dual Approaches for Solving Large-Scale Optimization

Problems, arXiv preprint arXiv:1406.5429v2, (2014).

[20]M. Krasnosel’skiĭ, Zwei Bemerkungen über die Methode der

sukzessiven Approximationen., Usp. Mat. Nauk, 10 (1955), pp. 123–127.

[21]P. Lions and B. Mercier, Splitting Algorithms for the Sum of Two

Nonlinear Operators, SIAM Journal on Numerical Analysis, 16 (1979),

pp. 964–979.

[22]W. R. Mann, Mean Value Methods in Iteration, Proceedings of the

American Mathematical Society, 4 (1953), pp. pp. 506–510.

[23]G. B. Passty, Ergodic convergence to a zero of the sum of monotone

operators in Hilbert space, Journal of Mathematical Analysis and

Applications, 72 (1979), pp. 383 – 390.

[24]H. Raguet, J. Fadili, and G. Peyré, A Generalized

Forward-Backward Splitting, SIAM Journal on Imaging Sciences, 6 (2013),

pp. 1199–1226.

[25]P. Tseng, A Modified Forward-Backward Splitting Method for Maximal

Monotone Mappings, SIAM Journal on Control and Optimization, 38 (2000),

pp. 431–446.

[26]B. C. Vũ, A splitting algorithm for dual monotone inclusions

involving cocoercive operators, Advances in Computational Mathematics, 38

(2013), pp. 667–681.