Optimal Monitoring and Mitigation of Systemic Risk in Financial Networks111We would like to thank Ben Craig, David Marshall, Celso Brunetti, and seminar participants at the Federal Reserve (Washington, DC), Federal Reserve Bank of Chicago, Federal Reserve Bank of Cleveland, and Northwestern University for helpful comments and suggestions.

Abstract

This paper studies the problem of optimally allocating a cash injection into a financial system in distress. Given a one-period borrower-lender network in which all debts are due at the same time and have the same seniority, we address the problem of allocating a fixed amount of cash among the nodes to minimize the weighted sum of unpaid liabilities. Assuming all the loan amounts and asset values are fixed and that there are no bankruptcy costs, we show that this problem is equivalent to a linear program. We develop a duality-based distributed algorithm to solve it which is useful for applications where it is desirable to avoid centralized data gathering and computation. Since some applications require forecasting and planning for a wide variety of different contingencies, we also consider the problem of minimizing the expectation of the weighted sum of unpaid liabilities under the assumption that the net external asset holdings of all institutions are stochastic. We show that this problem is a two-stage stochastic linear program. To solve it, we develop two algorithms based on Monte Carlo sampling: Benders decomposition algorithm and projected stochastic gradient descent. We show that if the defaulting nodes never pay anything, the deterministic optimal cash injection allocation problem is an NP-hard mixed-integer linear program. However, modern optimization software enables the computation of very accurate solutions to this problem on a personal computer in a few seconds for network sizes comparable with the size of the US banking system. In addition, we address the problem of allocating the cash injection amount so as to minimize the number of nodes in default. For this problem, we develop two heuristic algorithms: a reweighted minimization algorithm and a greedy algorithm. We illustrate these two algorithms using three synthetic network structures for which the optimal solution can be calculated exactly. We also compare these two algorithms on three types random networks which are more complex.

1 Introduction

The events of the last several years revealed an acute need for tools to systematically model, analyze, monitor, and control large financial networks. Motivated by this need, we propose to address the problem of optimizing the amount and structure of liquidity assistance in a distressed financial network, under a variety of modeling assumptions and implementation scenarios.

Two broad applications motivate our work: day-to-day monitoring of financial systems and decision making during an imminent crisis. Examples of the latter include the decision in September 1998 by a group of financial institutions to rescue Long-Term Capital Management, and the decisions by the Treasury and the Fed in September 2008 to rescue AIG and to let Lehman Brothers fail. The deliberations leading to these and other similar actions have been extensively covered in the press. These reports suggest that the decision making processes could have benefited from quantitative methods for analyzing potential policies and their likely outcomes. In addition, such methods could help avoid systemic crises in the first place, by informing day-to-day actions of financial institutions, regulators, supervisory authorities, and legislative bodies.

Given a financial network model, we are interested in addressing the following problem.

-

Problem I: Allocate a fixed amount of cash assistance among the nodes in a financial network in order to minimize the (possibly weighted) sum of unpaid liabilities in the system.

An alternative, Lagrangian, formulation of the same problem, is to both select the amount of injected cash and determine how to distribute it among the nodes in order to minimize the overall cost equal to a linear combination of the weighted sum of unpaid liabilities and the amount of injected cash.

We consider a static model with a single maturity date, and with a known network structure. At first, we assume that we know both the amounts owed by every node in the network to every other node, and the net asset amounts available to every node from sources external to the network. Even for this relatively simple model, Problem I is far from straightforward, because of a nonlinear relationship between the cash injection amounts and the loan repayment amounts. Building upon the results from [20], we construct algorithms for computing exact solutions for Problem I and its Lagrangian variant, by showing in Section 3 that both formulations are equivalent to linear programs under the payment scheme assumed in [20].

Because of this equivalence to linear programs, these problems can be solved for any network topology by any standard LP solver. In some scenarios, however, this approach may be impractical or undesirable, as it requires the solver to know the entire network structure, namely, the net external assets of every institution, as well as the amount owed by each institution to each other institution. In Section 6, we adapt our framework to avoid centralized data gathering and computation. We propose a distributed algorithm to solve our linear program. While the algorithm is slower than standard centralized LP solvers, simulations suggest its practicality for the US banking system.

Some applications, such as stress testing, require forecasting and planning for a wide variety of different contingencies. Such applications call for the use of stochastic models for the nodes’ external asset values. In this case, we aim to solve a stochastic version of Problem I.

-

Problem I-stochastic: Allocate a fixed amount of cash assistance among the nodes in a financial network in order to minimize the expectation of the (possibly weighted) sum of unpaid liabilities in the system.

We prove in Section 5 that, under the payment scheme assumed in [20]—whereby each defaulting bank uses all its available funds to pay all its creditors in proportion to the amounts it owes them—this problem is equivalent to a stochastic linear program. To solve this problem we develop two algorithms based on Monte Carlo sampling: a Benders decomposition algorithm described in Section 5.1 and a projected stochastic gradient descent algorithm described in Section 5.2. Both algorithms are centralized (non-distributed) and assume that we are able to efficiently obtain independent samples of the external asset vector.

We show in Section 4 that under the all-or-nothing payment scheme where the defaulting nodes do not pay at all, Problem I is an NP-hard mixed-integer linear program. However, we show through simulations that use optimization package CVX [33, 32] that this problem can be accurately solved in a few seconds on a personal computer for a network size comparable to the size of the US banking network.

We also consider another problem where the objective is to minimize the number of defaulting nodes rather than the weighted sum of unpaid liabilities:

-

Problem II: Allocate a fixed amount of cash assistance among the nodes in a financial network in order to minimize the number of nodes in default.

For Problem II, we develop two heuristic algorithms: a reweighted minimization approach inspired by [12] and a greedy algorithm. We illustrate our algorithms using examples with synthetic data for which the optimal solution can be calculated exactly. We show through numerical simulations that the solutions calculated by the reweighted algorithm are close to optimal, and the performance of the greedy algorithm highly depends on the network topology. We also compare these two algorithms using three types of random networks for which the optimal solution is not available. In one of these three examples the performance of these two algorithms is statistically indistinguishable; in the second example the greedy algorithm outperforms the reweighted algorithm; and in the third example the reweighted algorithm outperforms the greedy algorithm.

While Problem II is unlikely to be of direct practical importance (indeed, it is difficult to imagine a situation where a regulator would consider the failures of a small local bank and Citi to be equally bad), it serves as a stepping stone to a more practical and more difficult scenario where the optimization objective is a linear combination of the weighted unpaid liabilities (as in Problem I) and the sum of weights over the defaulted nodes (an extension of Problem II).

-

Problem III: Given a fixed amount of cash to be injected into the system, we consider an objective function which is a linear combination of the sum of weights over the defaulted nodes and the weighted sum of unpaid liabilities.

We show that this problem is equivalent to a mixed-integer linear program.

1.1 Related Literature

Contagion in financial networks has been frequently studied in the past, especially after the financial crisis in 2007-2008. Notable examples of network topology analysis based on real data are [10, 51, 16, 37]. Real data informs the new approaches for assessing systemic financial stability of banking systems developed in [27, 22, 23, 52, 34, 17, 47, 13, 45, 28, 4, 35, 26, 3].

Often, systemic failures are caused by an epidemic of defaults whereby a group of nodes unable to meet their obligations trigger the insolvency of their lenders, leading to the defaults of lenders’ lenders, etc, until this spread of defaults infects a large part of the system. For this reason, many studies have been devoted to discovering network structures conducive to default contagion [1, 15, 44, 29, 2, 9, 5]. The relationships between the probability of a systemic failure and the average connectivity in the network are investigated in [29, 5, 1]. Other features, such as as the distribution of degrees and the structure of the subgraphs of contagious links, are examined in [2].

While potentially useful in policymaking, most of these references do not provide specific policy recipes. One strand of literature on quantitative models for optimizing policy decisions has focused on analyzing the efficacy of bailouts and understanding the behavior of firms in response to bailouts. To this end, game-theoretic models are proposed in [46] and [7] that have two agents: the government and a single private sector entity. The focus of another set of research efforts has been on the setting of capital and liquidity requirements [15, 36, 30] in order to reduce systemic risk.

Our work contributes to the literature by taking a network-level view of optimal policies and proposing optimal cash injection strategies for networks in distress. Our present paper extends our earlier work reported in [40, 41, 39]. In addition to ours, several other papers have recently considered cash injection policies for lending networks [18, 19, 48, 49, 14], all based on the framework proposed in [20].

A cash injection targeting policy is developed in [18, 19] for an infinitesimally small amount of injected cash. The basic idea of the policy is to inject the cash into the node with the largest threat index, which is defined as the derivative of the unpaid liability with respect to the current asset value. However, extending this idea to construct an optimal cash injection policy for non-infinitesimal cash amounts produces an inefficient algorithm, as we show in Section 3.2. We show that our own method proposed in Section 3.1 is both more efficient and more flexible, as it can be extended to a more complex stochastic model described in Section 5.

In [48, 49], bankruptcy costs are incorporated into the model of [20]. The main contribution of that work is showing that because of the bankruptcy costs, it is sometimes beneficial for some solvent banks to form bailout consortia and rescue failing banks. However, it may happen that the solvent banks do not have enough means to effect a bailout, and in this case external intervention may still be needed.

A multi-period stochastic clearing framework based on [20] is proposed in [14], where a lender of last resort monitors the network and may provide liquidity assistance loans to failing nodes. The paper proposes several strategies that the lender of last resort might follow in making its decisions. One of these strategies, the so-called max-liquidity policy, aims to solve our Problem I during each period. However, [14] does not describe an algorithm for solving this problem.

1.2 Outline of the Paper

The paper is organized as follows. Section 2 describes the model of financial networks, the clearing payment mechanism, and the notation. Section 3 shows that if each defaulting node pays its creditors in proportion to the owed amounts, then Problem I and its Lagrangian formulation are equivalent to linear programs. A reweighted minimization algorithm to solve Problem II is also developed in Section 3. Section 4 considers Problem I under the assumption that the defaulting nodes do not pay anything. We prove that it is then an NP-hard problem and can be formulated as a mixed-integer linear program that can be efficiently solved using modern optimization software for network sizes comparable to the size of the US banking system. Section 5 extends Problem I to the situation where the capital of each institution is random. Section 6 proposes a duality-based distributed algorithm to solve Problem I and its Lagrangian formulation.

2 Model and Notation

| vector | -th component |

|---|---|

| 0 | 0 |

| 1 | 1 |

| net external assets at node before cash injection | |

| external cash injection to node | |

| the amount node owes to all its creditors | |

| the total amount node actually repays all its creditors on the due date of the loans | |

| node ’s total unpaid liabilities | |

| remaining cash of node after clearing payment | |

| the weight of $1 of unpaid liability at node | |

| the weight of node ’s default | |

| indicator variable of whether node defaults, i.e., if node defaults; otherwise |

Our network model is a directed graph with nodes where a directed edge from node to node with weight signifies that owes to . This is a one-period model with no dynamics—i.e., we assume that all the loans are due on the same date and all the payments occur on that date. We use the following notation:

-

•

any inequality whose both sides are vectors is component-wise;

-

•

, , , , , , , , , and are all vectors in defined in Table 1;

-

•

is the weighted sum of unpaid liabilities in the system;

-

•

is the number of nodes in default, i.e., the number of nodes whose payments are below their liabilities, ;

-

•

is what node owes to node , as a fraction of the total amount owed by node ,

-

•

and are the matrices whose entries are and , respectively.

Given the above financial system, we consider the proportional payment mechanism and

the all-or-nothing payment mechanism. The latter can be alternatively interpreted as

the proportional payment mechanism with 100% bankruptcy costs.

As proposed in [20], the proportional payment mechanism without bankruptcy costs

is defined as follows.

Proportional payment mechanism with no bankruptcy costs:

-

•

If ’s total funds are at least as large as its liabilities, then all ’s creditors get paid in full.

-

•

If ’s total funds are smaller than its liabilities, then pays all its funds to its creditors.

-

•

All ’s debts have the same seniority. This means that, if ’s liabilities exceed its total funds then each creditor gets paid in proportion to what it is owed. This guarantees that the amount actually received by node from node is always . Therefore, the total amount received by any node from all its borrowers is .

Under these assumptions, a node will pay all the available funds proportionally to its creditors,

up to the amount of its liabilities. The payment vector can lie anywhere in the rectangle

. Under the all-or-nothing payment scenario,

the defaulting nodes do not pay at all.

All-or-nothing payment mechanism:

-

•

If ’s total funds are at least as large as its liabilities (i.e., ) then all ’s creditors get paid in full.

-

•

If ’s total funds are smaller than its liabilities, then pays nothing.

As defined in [20], a clearing payment vector is a vector of borrower-to-lender payments that is consistent with the conditions of the payment mechanism. Several algorithms for computing the clearing payment vector are discussed and compared in Appendix A.

In this paper, we are mostly concerned with Problems I and II under the proportional payment scenario with no bankruptcy costs. We also prove that the all-or-nothing payment scenario makes Problem I NP-hard. In this case, Problem I can be formulated as a mixed-integer linear program that can be efficiently solved on a personal computer using modern optimization software for network sizes comparable to the size of the US banking system.

3 Centralized Algorithms for Problems I, II, III under the Proportional Payment Mechanism

3.1 Minimizing the Weighted Sum of Unpaid Liabilities is an LP

Consider a network with a known structure of liabilities and a known vector of net assets before cash injection. Using the notation established in the preceding section, Problem I seeks a cash injection allocation vector to minimize the following weighted sum of unpaid liabilities,

subject to the constraint that the total amount of cash injection does not exceed some given number :

In this section, we assume proportional payments with no bankruptcy costs. We first prove that, for any cash injection vector , there exists a unique clearing payment vector that maximizes the cost .

Lemma 1.

Given a financial system , a cash injection vector and a weight vector , there exists a unique clearing payment vector minimizing the weighted sum .

Proof.

Method 1: First, note that since and do not depend on or , minimizing is equivalent to maximizing . With a fixed cash injection vector , the financial system is equivalent to . Since , we have that is a strictly increasing function of . By Lemma 4 in [20], the clearing payment vector can be obtained by solving the following linear program:

| (1) | |||

| subject to | |||

| (2) | |||

| (3) |

From Theorem 1 in [20], there exists a greatest clearing payment vector . Since is a strictly increasing function of , is a solution of LP (1-3). For any other , we have for and at least one of these inequalities is strict. Thus, . Therefore is the unique solution of LP (1-3). This completes the proof of Lemma 1.

Method 2: Here is another method to prove Lemma 1 without using Theorem 1 in [20]. It is clear that LP (1-3) is feasible and bounded so the solution always exists. Assume there are two different solutions and , and define as for . Then , for . Here the inequality is strict because .

For each , by definition, or . Since and are both solutions of the LP, they both satisfy constraint (2), i.e., and for all . Therefore, we also have for all , which means that also satisfies constraint (2). In addition, both and satisfy constraint (3), which, along with the fact that all entries of are nonnegative, implies that and for all , and therefore also for all . Therefore, also satisfies constraint (3). Thus, is in the feasible region of LP (1-3) and achieves a larger value of the objective function than do and , which contradicts the fact that and are solutions of LP (1-3). This completes the proof of Lemma 1.

We now establish the equivalence of Problem I and a linear programming problem.

Theorem 1.

Assume that the liabilities matrix , the asset vector , the weight vector , and the total cash injection amount are fixed and known. Assume that the system utilizes the proportional payment mechanism with no bankruptcy costs. Consider Problem I, i.e., the problem of calculating a cash injection allocation to minimize the weighted sum of unpaid liabilities subject to the budget constraint . A solution to this problem can be obtained by solving the following linear program:

| (4) | |||

| subject to | |||

| (5) | |||

| (6) |

Proof.

Since the constraints on and in LP (4-6) form a closed and bounded set in , a solution exists. Moreover, for any fixed , it follows from our Lemma 1 and Lemma 4 in [20] that the linear program has a unique solution for which is the clearing payment vector for the system.

Let be a solution to (4-6). Suppose that there exists a cash injection allocation that leads to a smaller cost than does . In other words, suppose that there exists , with , such that the corresponding clearing payment vector satisfies or, equivalently,

| (7) |

Note that satisfies the first two constraints of (4-6). Moreover, since is the corresponding clearing payment vector, the last two constraints are satisfied as well. The pair is thus in the constraint set of our linear program. Therefore, Eq. (7) contradicts the assumption that is a solution to (4-6). This completes the proof that is the allocation of that achieves the smallest possible cost .

In the Lagrangian formulation of Problem I, we are given a weight and must choose the total cash injection amount and its allocation to minimize . This is equivalent to the following linear program:

| (8) | |||

| subject to | |||

This equivalence follows from Theorem 1: denoting a solution to (8) by , we see that the pair must be a solution to (4-6) for . At the same time, the fact that maximizes the objective function in (8) means that it minimizes , since is a fixed constant.

3.2 Comparison with Demange’s Algorithm

A cash injection targeting policy is developed in [18, 19] for an infinitesimally small amount of the injected cash. The basic idea of Proposition 4 in [19] is to inject the cash into the node with the largest threat index, which is defined as the derivative of the sum of the unpaid liabilities with respect to the current asset value. Moreover, as small amounts of cash are gradually injected, the target remains the same until at least one bank is fully rescued (i.e., changes from defaulting to solvent), so the optimal policy for non-infinitesimal amounts of cash would be to keep injecting cash into the same node until one node changes its state. While no algorithm for the injection of a non-infinitesimal amount of cash (i.e., for our Problem I) is proposed in [18, 19], we construct such an algorithm based on the ideas from [18, 19].

Algorithm for Problem I based on [18, 19]:

-

1.

Initialization: set cash injection vector and the remaining cash still to be allocated .

-

2.

Compute the clearing payment vector for system .

-

3.

Compute the threat index for system by solving the linear program (13) in [19]. Select the one with the largest threat index, denoted as node .

-

4.

Inject a small amount of cash into node and update the clearing payment vector . Define as the increase of the payment vector after injecting into node .

-

5.

Compute for . Select the smallest one, denoted as node . Then node will be the first node that changes from defaulting to being solvent when we keep injecting cash into node .

-

6.

Set . Set . If , stop; otherwise, go to Step 2.

Each iteration of this algorithm computes the clearing payment vector twice: in Steps 2 and 4. Step 3 moreover involves solving a linear program to obtain the threat index. In the worst case, the algorithm will stop after iterations since at each iteration, only one defaulting node is guaranteed to be rescued. Thus, we would need to solve LPs and compute the clearing payment vector times in the worst case—much less computationally efficient than our approach of Theorem 1 which requires solving a single LP. Note that the above algorithm makes a simplifying assumption in Step 4 that a small number can be found in advance such that the injection of in Step 4 does not lead to the rescue of any banks. Our algorithm based on Theorem 1 does not require this simplifying assumption. In addition, unlike our LP method, the above algorithm has limited applications. For example, it is not easy to extend this algorithm to solve Problem I-stochastic.

3.3 Minimizing the Number of Defaults

Given that the total amount of cash injection is , Problem II seeks to find a cash injection allocation vector to minimize the number of defaults , i.e., the number of nonzero entries in the vector .

In this section, we propose two heuristic algorithms to solve Problem II approximately. First, we adapt the reweighted minimization strategy approach from Section 2.2 of [12]. Our algorithm solves a sequence of weighted versions of the linear program (4-6), with the weights designed to encourage sparsity of . In the following pseudocode of our algorithm, is the weight vector during the -th iteration.

Reweighted minimization algorithm:

-

1.

.

-

2.

Select (e.g., ).

- 3.

-

4.

Update the weights: for each ,

where is constant, and is the clearing payment vector obtained in Step 3.

-

5.

If , where is a constant, stop; else, increment and go to Step 3.

Note that nodes for which is very small require very little additional resources to avoid default. This is why Step 4 is designed to give more weight to such nodes, thereby encouraging larger cash injections into them. On the other hand, nodes for which is very large require a lot of cash to become solvent. The algorithm essentially “gives up” on such nodes by assigning them small weights.

The second heuristic algorithm we develop is a greedy algorithm. At each iteration of the greedy algorithm, we calculate the clearing payment vector and select the node with the smallest unpaid liability among all the defaulting nodes. We inject cash into that node to rescue it so that during each iteration, we save the one node that requires the smallest cash expenditure. In this procedure, we inject the cash sequentially, bailing out some nodes completely before they fully receive the payments from their borrowers. These nodes may subsequently receive some more cash from their borrowers if their borrowers are rescued several steps later. Because of this, a rescued node may end up with a surplus. If this happens, the node would use its surplus to repay its cash injection. Such repayments can then be used to assist other nodes. The algorithm terminates either when there are no defaults in the system or when the injected cash reaches the total amount and no rescued node has a surplus.

Greedy algorithm:

-

1.

, , .

- 2.

-

3.

Calculate the surplus of each node after clearing: .

-

4.

Update the remaining cash to be injected into the system after the rescued nodes repay their cash injections: , for .

-

5.

If or there are no defaults in the system, stop.

-

6.

Find node with the minimum unpaid liability among all defaulting nodes.

-

7.

, , go to Step 2.

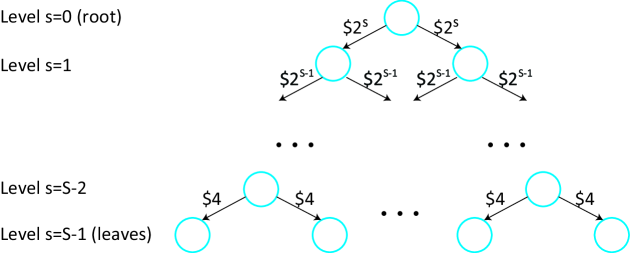

3.3.1 Example: A Binary Tree Network

First, we use a full binary tree with levels and nodes. As shown in Fig. 1, levels 0 and correspond to the root and the leaves, respectively. Every node at level owes to each of its two creditors (children). We set .

If , then all non-leaf nodes are in default, and the leaves are not in default. In aggregate, the nodes at any level owe the nodes at level . Therefore, if , then can be achieved by allocating the entire amount to the root node.

For , we first observe that if for some integer , then the optimal solution is to allocate the entire amount to a node at level . This would prevent the defaults of this node and all its non-leaf descendants, leading to defaults. If is not a power of two, we can represent it as a sum of powers of two and apply the same argument recursively, to yield the following optimal number of defaults:

where is the number of non-leaf nodes in an -level complete binary tree, is the -th bit in the binary representation of (right to left) and is the number of bits. To summarize, the smallest number of defaults , as a function of the cash injection amount , is:

| (9) |

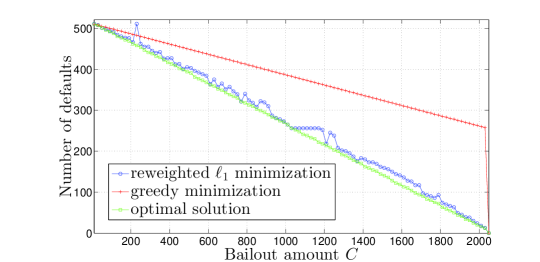

In our test, we set . The green line in Fig. 2 is a plot of the minimum number of defaults as a function of from Eq. (9). The blue line is the solution calculated by the reweighted minimization algorithm with and . The algorithm was run using six different initializations: five random ones and . Among the six solutions, the one with the smallest number of defaults was selected. The red line is the solution calculated by the greedy algorithm. As evident from Fig. 2, the results of the reweighted minimization algorithm are very close to the optimal for the entire range of . The performance of the greedy algorithm is poor. The greedy algorithm always injects cash into the nodes at level which have the smallest unpaid liabilities. For , this strategy is inefficient since spending $16 on a node at level rescues both that node and its two children, whereas spending $16 on two nodes at level only rescues those two nodes.

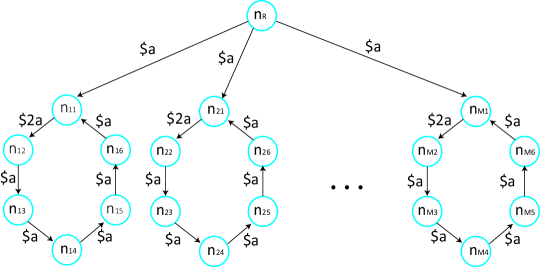

3.3.2 Example: A Network with Cycles

Second, we test our algorithms on a network with cycles shown in Fig. 3. The network contains cycles with six nodes each. The nodes in the -th cycle are denoted . Node owes to . Node owes to . For , owes to . The root node, denoted as , owes to , for every . We set .

If , then the root node and all nodes connected to the root, ), are in default. The remaining nodes are not in default.

If , then allocating the entire amount to the root yields zero defaults.

If , then giving to node will prevent it from defaulting. Thus, the total number of defaults in this case is .

Summarizing, for this network structure, the smallest number of defaults , as a function of the cash injection amount , is:

| (10) |

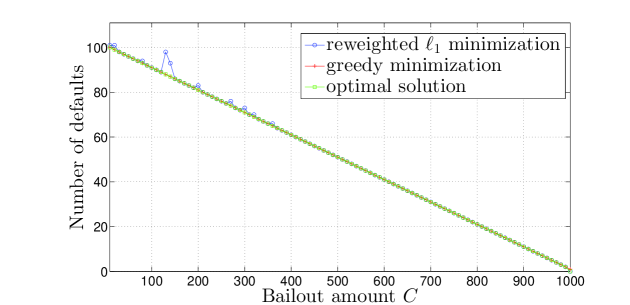

In our test, we set and . In Fig. 4, the green line is a plot of the minimum number of defaults as a function of . The blue line is the solution calculated by the reweighted minimization algorithm with and . The algorithm was run using six different initializations: five random ones and . Among the six solutions, the one with the smallest number of defaults was selected. The red line is the solution calculated by the greedy algorithm. As evident from Fig. 4, the results produced by both algorithms are very close to the optimal ones. The greedy algorithm achieves the optimal for the entire range of except the point . When , the optimal strategy is to inject into the root node whereas the greedy algorithm injects into for .

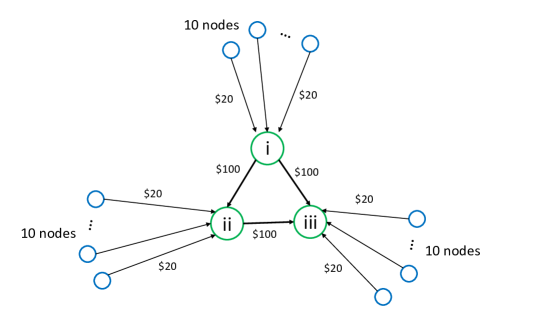

3.3.3 Example: A Core-Periphery Network

Third, we test our algorithm on a simple core-periphery network, since core-periphery models are widely used to model banking systems [21, 24, 37, 16]. In Fig. 5, i, ii, and iii are the three core nodes. Node i owes $100 each to nodes ii and iii, and node ii owes $100 to iii. Ten periphery nodes are attached to each core node, and each periphery node owes $20 to its core node. There are no external assets in the system and therefore in the absence of an external injection of cash, all the nodes are in default except node iii.

If the cash injection amount is , the optimal solution is to select any periphery nodes and give $20 to each of them. This reduces the number of defaults by .

If , we first select any five periphery nodes of core node ii and give $20 to each of them, because this saves both node ii and these five periphery nodes. Then we select any other periphery nodes and give $20 to each. This decreases the number of defaults by .

If , we first use $200 to rescue all 10 periphery nodes of core node i, saving i, ii, and these 10 periphery nodes. Then we select any other periphery nodes and give $20 to each. This decreases the number of defaults by .

If , then all the nodes can be rescued by giving $20 to each periphery node.

To sum up, for this core-periphery network structure, the smallest number of defaults , as a function of the cash injection amount , is:

| (11) |

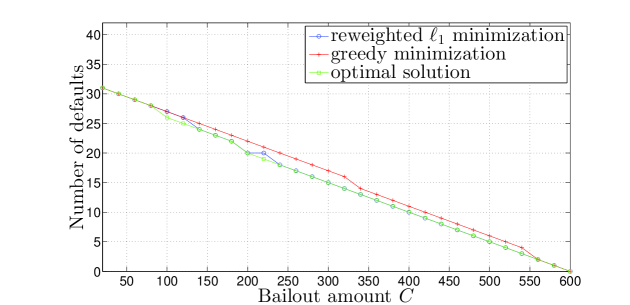

In Fig. 6, the green line is a plot of this minimum number of defaults as a function of . The blue line is the solution calculated by our reweighted minimization algorithm with and . The algorithm was run using six different initializations: five random ones and . Among the six solutions, the one with the smallest number of defaults was selected. The red line is the solution calculated by the greedy algorithm. As evident from Fig. 6, the results produced by the reweighted algorithm are very close to the optimal ones for the entire range of . Note that for the greedy algorithm, the performance depends on the order of rescuing nodes with the same unpaid liability amounts. For example, if the greedy algorithms rescue the periphery nodes of core node iii first, the performance would be poor.

3.3.4 Example: Three Random Networks

We now compare the reweighted minimization algorithm to the greedy algorithm using more complex network topologies in which the optimal solution is difficult to calculate directly.

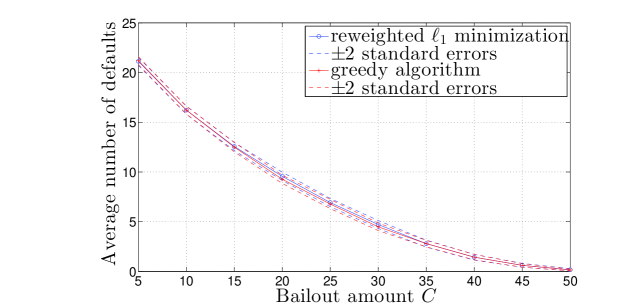

We construct three types of random networks, all having external asset vector . The first one is a random graph with 30 nodes. For any pair of nodes and , is zero with probability 0.8 and is uniformly distributed in with probability 0.2.

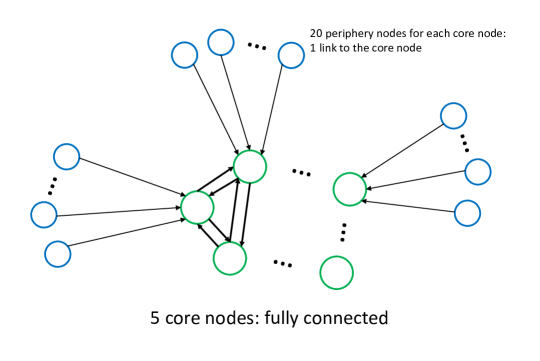

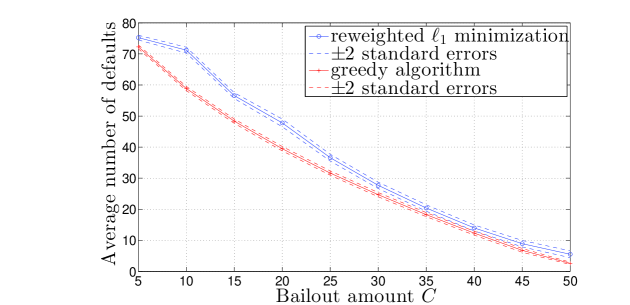

The second one is a random core-periphery network which is illustrated in Fig. 7. The core contains five nodes which are fully connected. The liability from one core node to every other core node is uniformly distributed in . Each core node has 20 periphery nodes. Each periphery node owes money only to its core node. This amount of money is uniformly distributed in .

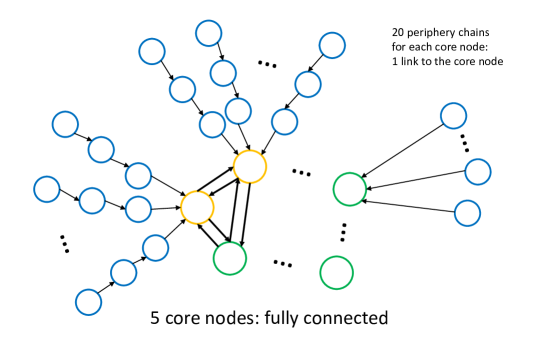

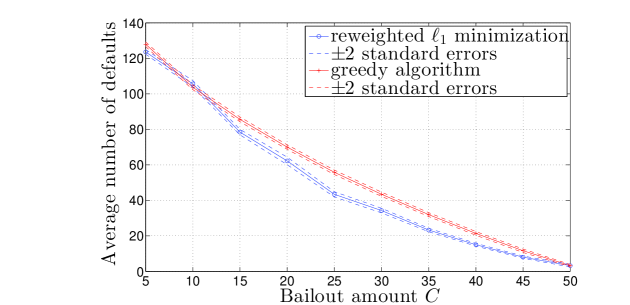

The third one is a random core-periphery network with chains of periphery nodes. As shown in Fig. 8, the core contains five nodes which are fully connected. The liability from one core node to every other core node is uniformly distributed in [0,20]. Each core node has 20 periphery chains connected to it, each chain consisting of either a single periphery node (short chains) or 3 periphery nodes (long chains). Each core node has either only short periphery chains connected to it or only long periphery chains connected to it. There are two core nodes with long periphery chains. The liability amounts along each long chain are the same, and are uniformly distributed in [0,1]. The liability amounts along each short chain are also uniformly distributed in [0,1].

For each of these three random networks, we generate 100 samples from the distribution and run both the reweighted minimization algorithm and the greedy algorithm on each sample network. In the reweighted minimization algorithm, we set , . We run the algorithm using six different initializations: five random ones and . Among the six solutions, the one with the smallest number of defaults is selected.

The results are shown in Figs. 9, 10, and 11. The blue and red solid lines represent the average numbers of defaulting nodes after the cash injection allocated by the two algorithms: blue for the reweighted minimization and red for the greedy algorithm. The dashed lines show the error bars for the estimates of the average. Each error bar is two standard errors.

From Fig. 9, we see the performance of the reweighted algorithm is close to the greedy algorithm on the random networks. From Fig. 10 and Fig. 11, we see that on random core-periphery networks, the greedy algorithm performs better than the reweighted algorithm, while on random core-periphery networks with chains, the reweighted algorithm is better.

3.4 Minimizing a Linear Combination of Weighted Unpaid Liabilities and Sum of Weights over Defaulting Nodes

We now investigate Problem III which is a combination of Problem I and Problem II. Instead of just minimizing the weighted sum of unpaid liabilities or the number of defaulting nodes, we consider an objective function which is a linear combination of the sum of weights over the defaulted nodes and the weighted sum of unpaid liabilities:

As defined in Table 1, is a binary variable indicating whether node defaults, and is the weight of node ’s default.

Since is strictly decreasing with respect to , Lemma 4 in [20] implies that minimizing will yield a clearing payment vector. In light of this fact, we prove that minimizing subject to a fixed injected cash amount is equivalent to a mixed-integer linear program.

Theorem 2.

Assume that the liabilities matrix , the external asset vector , the weight vectors and and the total cash injection amount are fixed and known. Assume that the system utilizes the proportional payment mechanism with no bankruptcy costs. Define as in Table 1. Then the optimal cash allocation policy to minimize the cost function can be obtained by solving the following mixed-integer linear program:

| (12) | |||

| subject to | |||

| (13) | |||

| (14) | |||

| (15) | |||

| (16) | |||

| (17) | |||

| (18) |

Proof.

Let (, , ) be a solution of the mixed-integer linear program (12–18). We first show that is a clearing payment vector, i.e., that for each , we have or . Assume that this is not the case for some node , i.e., that and . We construct a vector which is equal to in all components except the -th component. We set the -th component of to be , where is small enough to ensure that and . Since is a matrix with non-negative entries, for any , we have:

In addition, . Thus, (, , ) is also in the feasible region of (12–18) and achieves a larger value of the objective function than (, , ). This contradicts the fact that (, , ) is a solution of (12–18). Hence, is a clearing payment vector.

Second, we show that . If , then due to constraints (17) and (18). If , then constraint (17) is always true. In this case the fact that implies that, in order to maximize the objective function, must be zero. Thus, .

So far, we have proved that and are the clearing payment vector and default indicator vector, respectively, for cash injection vector . We now prove by contradiction that is the optimal cash injection allocation. Assume leads to a strictly smaller value of the cost function than does . In other words, suppose that satisfies the constraints (13) and (14), and that the corresponding clearing payment vector and default indicator vector satisfy , which is equivalent to:

Since is the corresponding clearing payment vector, constraint (15) and (16) are satisfied. Moreover, is the corresponding default indicator vector satisfying constraint (17) and (18) for . So (,,) is in the feasible region of (12–18) and achieves a larger objective function than (, , ), which contradicts the fact that (, , ) is the solution of (12–18).

4 All-or-Nothing Payment Mechanism

We now show that under the all-or-nothing payment mechanism, Problem I is NP-hard. Despite this fact, we show through simulations that for network sizes comparable to the size of the US banking system, this problem can be solved in a few seconds on a personal computer using modern optimization software.

Theorem 3.

With the all-or-nothing payment mechanism, Problem I can be reduced to a knapsack problem, which means that Problem I is NP-hard.

Proof.

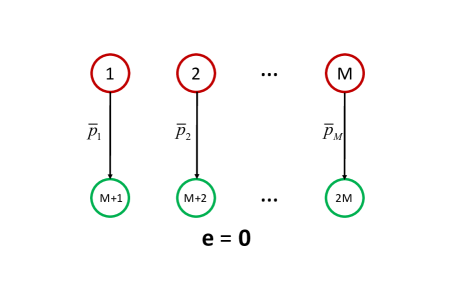

Consider the network depicted in Fig. 12. The network has nodes where is a positive integer. We let for ; for all other pairs , we set . We set the external asset vector to zero: . We set all the weights to 1: . We let be the rescue indicator variable for node , i.e., if is in default and if is fully rescued, for .

Note that under the all-or-nothing payment mechanism, fully rescuing node for any in Fig. 12 means injecting . On the other hand, injecting any other nonzero amount is wasteful, as it does not reduce the total amount of unpaid liabilities in the system. Therefore, for each defaulting node we have , , and , and for each rescued node we have , , and . The reduction in the total amount of unpaid obligations due to the cash injection is

We must select to maximize this amount, subject to the budget constraint that says that the total amount of cash injection spent on fully rescued nodes must not exceed :

| (19) | |||

| subject to | |||

If any cash remains, it can be arbitrarily allocated among the remaining nodes or not spent at all, because partially rescuing a node does not lead to any improvement of the objective function. Program (19) is a knapsack problem, a well-known NP-hard problem. Thus, Problem I under the all-or-nothing payment mechanism for the network of Fig. 12, which can be reduced to (19), is an NP-hard problem.

We now establish a mixed-integer linear program to solve Problem I with the all-or-nothing payment mechanism.

Theorem 4.

Assume that the liabilities matrix , the external asset vector , the weight vector and the total cash injection amount are fixed and known. Assume the all-or-nothing payment mechanism. Then Problem I is equivalent to the following mixed-integer linear program:

| (20) | |||

| subject to | |||

| (21) | |||

| (22) | |||

| (23) | |||

| (24) | |||

| (25) |

Proof.

Let () be a solution of the mixed-integer linear program (20–25). We first show that is the clearing payment vector corresponding to . For node , if , then from constraints (24) and (25) it follows that so that . If , then constraint (24) is satisfied for both and . In this case, in order to maximize the objective function, it must be that and . This completes the proof that is the clearing payment vector corresponding to under the all-or-nothing payment mechanism.

Second, we prove by contradiction that is the optimal allocation. Assume that leads to a smaller weighted sum of unpaid liabilities, or equivalently, a larger value of , where is the clearing payment vector corresponding to . Since is a clearing payment vector, we have that if then ; and if then . We define vector as for and otherwise. Then () is located in the feasible region of MILP (20–25) but leads to a larger value of the objective function than (). This contradicts the fact that () is a solution of (20–25).

4.1 Numerical Simulations

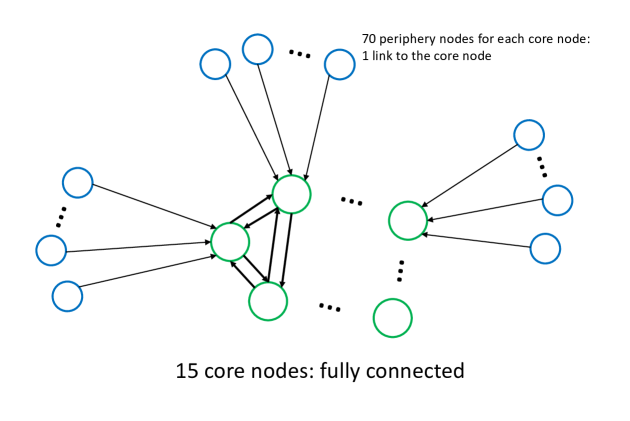

To solve MILP (20), we use CVX, a package for specifying and solving convex programs [33, 32]. A variety of prior literature, e.g. [51], suggests that the US interbank network is well modeled as a core-periphery network that consists of a core of about 15 highly interconnected banks to which most other banks connect. Therefore, we test the running time on a core-periphery network shown in Fig. 13. It contains 15 fully connected core nodes. Each core node has 70 periphery nodes. Each periphery node has a single link pointing to the corresponding core node. Every node has zero external assets: . All the obligation amounts are independent uniform random variables. For each pair of core nodes and the obligation amount is uniformly distributed in . For a core node and its periphery node , the obligation amount is uniformly distributed in . For a core node , we set the weight ; for a periphery node , we set the weight . For this core-periphery network, we generate 100 samples. We run the CVX code on a personal computer with a 2.66GHz Intel Core2 Duo Processor P8800. The average running time is and the sample standard deviation is . The relative gap between the objective of the solution and the optimal objective is less than . (This bound is obtained by calculating the optimal value of the objective for the corresponding linear program, which is an upper bound for the optimal objective value of the MILP.) We can see that for the core-periphery network, MILP (20) can be solved by CVX efficiently and accurately. The CVX code is given in Appendix B.

5 Random Capital Model

In the previous sections, we assume that the external asset vector is a deterministic vector known by the regulator. However, some applications, such as stress testing, require forecasting and planning for a wide variety of different contingencies. Such applications call for the use of stochastic models for the nodes’ asset amounts. In this case, we aim to solve a stochastic version of Problem I where is modeled as a random vector. It is assumed that we are able to efficiently obtain independent samples of this vector. The remaining parameters—, and —are still assumed to be deterministic and known, and are defined as in the previous section. According to Lemma 1, the clearing payment vector that minimizes the weighted sum of unpaid liabilities is a function of and , which we denote as . If is a random vector, so is . We use to denote the corresponding minimum value of the weighted sum of unpaid liabilities. If is a random vector, then is a random variable. Given a total amount of cash , our aim is to find the optimal cash allocation strategy to minimize the expectation of the weighted sum of unpaid liabilities. This can be formulated as the following two-stage stochastic LP:

| (26) | |||

| subject to | |||

where

| (27) | ||||

| subject to | ||||

Even if the joint distribution of is known, the distributions of and cannot be computed in closed form. In order to solve (26), we take independent samples of the asset vector, denoted as , and use to approximate . By the weak law of large numbers, when is large enough, the sample average is a good estimate of . This motivates approximating Eq. (26) as follows:

| (28) | |||

| subject to | |||

Similar to Theorem 1, the optimization problems (27) and (28) can be combined into one single LP:

| (29) | |||

| subject to | |||

Since and for are all -dimensional vectors, LP (29) contains variables. The computational complexity of solving an LP with variables is [53]. To achieve a high accuracy, needs to be a large number. Then the computational burden is large if we want to solve LP (29) directly. The memory complexity, which is , may also be prohibitive for large and . Hence, efficient algorithms to solve LP (29) are needed.

5.1 Benders Decomposition

If the cash injection vector is fixed, then the LP (29) can be split into smaller independent LPs—one for each sample —each of which can be solved independently for each . In this case, instead of solving an LP with variables, we solve LPs with variables each, which significantly reduces the computational complexity. Inspired by this idea, we apply Benders decomposition to the LP (29). Benders decomposition, which is described in [6, 50, 38], makes a partition of and () and allows us to find iteratively with fixed in each step. In fact, for our problem, Benders decomposition can be further simplified due to some special properties of (29).

From the proof of Lemma 1, we know that for any fixed , the feasible region of is non-empty. Thus, (29) is equivalent to the following problem:

| (30) | |||

| subject to | |||

where

| (31) | ||||

| subject to | ||||

| (32) | ||||

| (33) |

We let be the dual variables for the constraints (32), and we let be the dual variables for the constraints (33). Then can be obtained from the following dual problem:

| (34) | ||||

| subject to | ||||

Note that, since minimizes the objective function of LP (34) subject to the constraints of LP (34), we have that is the greatest lower bound of this objective function, subject to these constraints. Therefore, LP (30) is equivalently rewritten as the maximization of the lower bound to the objective function of LP (34), subject to the constraints of both LP (30) and LP (34):

| (35) | |||

| subject to | |||

| (36) | |||

LP (35), the equivalent version of (29), has an infinite number of constraints in the form of (36), because constraint (36) must be satisfied by every pair from the feasible region of LP (34). The key idea is solving a relaxed version of (35) by ignoring all but a few of the constraints (36). Assume the optimal solution of this relaxed program is . If the solution satisfies all the ignored constraints, the optimal solution has been found; otherwise, we generate a new constraint by solving (34) with fixed and add it to the relaxed problem. Here is the summary of the Benders decomposition algorithm:

-

1.

Initialization: set , , , .

-

2.

Fix , solve the following sub-programs for :

subject to Denote the solution as , for .

-

3.

If , terminate and is the optimal.

-

4.

Set , , , for .

-

5.

Solve the following master problem:

(37) subject to Denote the solution as . Set , . Then go to Step 2.

In this algorithm, at each iteration, we solve LPs with variables instead of one LP with variables, which saves both computational complexity and memory cost. Note that, comparing to the general form of Benders decomposition (Section 2.3 in [50]), the above algorithm is simpler. Since LP (31) is always feasible and bounded, it is not necessary to consider constraint (22b) in [50]. Step (2’) in [50] can also be removed since (37) is always bounded.

5.2 Projected Stochastic Gradient Descent

In this section, we introduce the projected stochastic gradient descent method to solve (26). This is an online algorithm, which allows us to handle one sample at a time, without building a huge linear program. The basic idea is that for each sample , we move the solution along the direction of the negative gradient of with respect to and then project the result onto the set defined by the constraints of (26). This procedure will converge to the optimal solution if the step size is selected properly [11]. The algorithm proceeds as follows. At iteration ,

-

1.

Sample an asset vector .

-

2.

Move along the negative gradient of according to the following equation:

(38) -

3.

Set as the projection of onto the set .

According to [11], step size should satisfy the condition that and . Thus, a proper choice could be .

Note that , where

| (39) | ||||

| subject to | ||||

To obtain the gradient of in Step 2, we consider the dual problem of LP (39):

| (40) | ||||

| subject to | ||||

Assuming that is a solution of (40), we have .

In Step 3, we find the projection of using the following quadratic program:

| (41) | ||||

| subject to | ||||

Thus, at each iteration in this projected stochastic gradient descent method, instead of solving LP (29) which contains variables, we solve one -variable LP and one -variable quadratic program. This algorithm is memory efficient because it requires no storage except the current solution of .

6 Distributed Algorithms for Problem I with Proportional Payment Mechanism

We showed in Theorem 1 that Problem I without bankruptcy costs is equivalent to a linear program, and therefore can be solved exactly, for any network topology, using standard LP solvers. In some scenarios, however, this approach may be impractical or undesirable, as it requires the solver to know the entire network structure, namely, the net external assets of every institution, as well as the amounts owed by each institution to each other institution. We now adapt our framework to applications where it is necessary to avoid centralized data gathering and computation. We propose a distributed algorithm to solve our linear program. The algorithm is iterative and is based on message passing between each node and its neighbors. During each iteration of the algorithm, each node only needs to receive a small amount of data from its neighbors, perform simple calculations, and transmit a small amount of data to its neighbors. During the message passing, no node will reveal to any other node any proprietary information on its asset values, the amounts owed to other nodes, or the amounts owed by other nodes.

Our algorithm can be used both to monitor financial networks and to simulate stress-testing scenarios. The integrity of the process can be enforced by the supervisory authorities through auditing.

While the algorithm is slower than standard centralized LP solvers, simulations suggest its practicality for the US banking system which we model as a core-periphery network with 15 core nodes and 1050 periphery nodes.

6.1 Problem I

6.1.1 A Distributed Algorithm

To develop a distributed algorithm for LP (4-6), we formulate its dual problem and solve it via gradient descent because the dual problem has simpler constraints which are easily decomposable. It turns out that every iteration of the gradient descent involves only local computations, which enables a distributed implementation.

In order to apply the gradient descent method to the dual problem, we need the objective function in (4) to be strictly concave, which would guarantee that the dual problem is differentiable at any point [25]. However, the objective function of LP (4) is not strictly concave and so we apply the Proximal Optimization Algorithm [43, 8]. The basic idea is to add quadratic terms to the objective function. The quadratic terms will converge to zero so that we make the objective function strictly concave without changing the optimal solution.

We introduce two vectors and and add two quadratic terms

to (4). Then we proceed as follows.

Algorithm :

At the -th iteration,

-

•

P1) Fix and and maximize the objective function with respect to and :

(42) subject to (43) (44) Note that since the objective function is strictly concave, a unique solution exists. Denote it as and .

-

•

P2) Set , .

6.1.2 Implementation of Algorithm

In Step P1, for fixed and , the objective function of (42) is strictly concave so that the dual problem is differentiable at any point [25]. Hence, we can solve the dual problem using gradient descent, as follows.

Let a scalar and an vector be Lagrange multipliers for constraints (43) and (44), respectively. We define the Lagrangian as follows:

| (45) |

where and are non-negative and is an identity matrix. We further expand (45):

| (46) | ||||

| (47) |

To obtain Eq. (47) from Eq. (46), we use the following equation: . Then the objective function of the dual problem is:

| (48) |

In Eq. (47), the term is 0 if node is not a borrower of . Thus, if node receives all the from its lenders, it can determine and to achieve the maximum of the Lagrangian .

The dual problem is differentiable at any point since the objective function of the primal is strictly concave [25]. Hence, gradient descent iterations can be applied to solve the dual.

At iteration , and . Then the gradients of with respect to and at this point are:

where and solve (48) for and :

| (50) |

where , and

| (51) |

Therefore, taking into account the non-negativity of and , the gradient descent equations are:

| (52) |

| (53) |

where and are the step sizes, and . For fixed and , the dual update will converge to the minimizer of as , if the step size is small enough [8].

From (52), we notice that in order to update , is required from all the nodes. It means at each iteration , each node should send to a central node so that the central node could update and send it back to every node in the system.

If node is not a borrower of node , then ; otherwise, represents the amount of money that node pays to node at -th iteration. Hence, with the information of from all its borrowers, node is able to update based on (53).

6.1.3 A More Efficient Algorithm

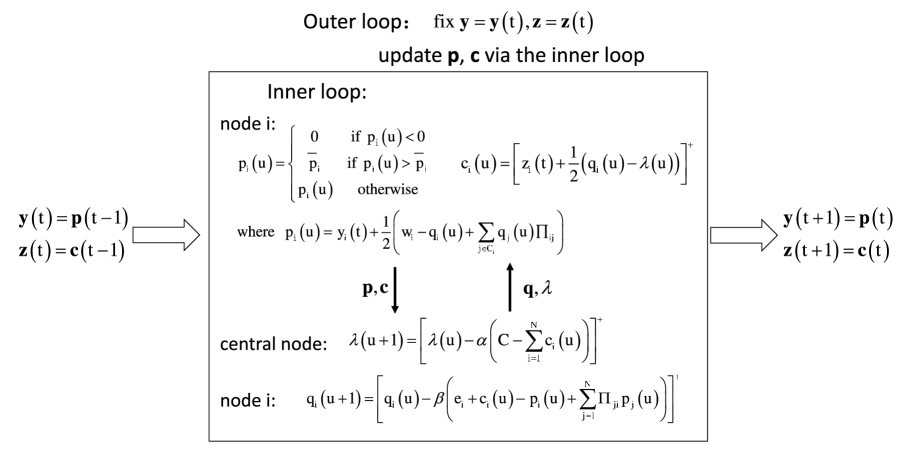

As shown in Fig. 14, in the algorithm, we first fix and and solve (42)

by updating , and , iteratively until they converge.

Then we update and . This is a two-stage iteration, which is likely to slow down

the convergence of the entire algorithm as too many dual updates are wasted for each

fixed and [43].

To avoid the two-stage iteration structure, we consider the following algorithm.

Algorithm :

At the -th iteration,

-

•

A1) Fix and , maximize with respect to p and c,

-

•

A2) Update Lagrange multipliers and by

(54) (55) -

•

A3) Update y and z with

In algorithm , instead of an infinite number of dual updates, we only update Lagrange multipliers and once for each fixed and . The following theorem guarantees the convergence of algorithm .

Theorem 5.

6.1.4 Implementation of Algorithm

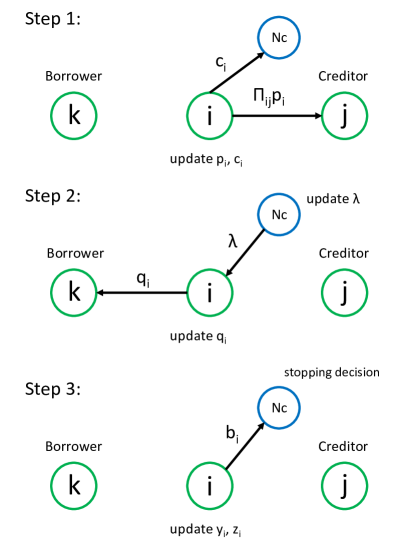

Assume and are the sets of borrowers and creditors of node

respectively. Then the -th iteration of algorithm is as follows.

-

1.

For each node , fix , , and , and calculate and :

where , and

Then send to every node , and send the updated to node .

-

2.

Each node receives from every and updates :

Then each node sends the updated to every node .

Node receives from all nodes and updates :

Then node send the updated to every node .

-

3.

Every node receives from each and receives from node , then updates and :

where , and

where .

Every node then checks the conditions and . If both conditions hold, node sets ; otherwise it sets . It then sends to the central node . If for all , then directs all nodes to terminate the algorithm.

These steps are illustrated in Fig. 15.

In Step 3, and are the stopping tolerances, which are usually set as small positive numbers according to the accuracy requirement. We utilize and rather than their projections and in the stopping criterion because the convergence of and implies the convergence of the Lagrange multipliers and , whereas the convergence of and does not.

In the implementation of algorithm , we include a central node. At each iteration the central node has two functions. One is to sum the and calculate in Step 2; the other is to test whether for all nodes in Step 3. For both functions, the central node only collects a small amount of data and performs simple calculations. We could entirely exclude the central node by calculating the sum of and communicating the stopping sign in a distributed way, at the cost of added computational burden during each iteration.

6.2 Lagrange Formulation of Problem I

We now apply the duality-based distributed algorithm to LP (8), the Lagrange formulation of Problem I. Note that now represents the importance of the injected cash amount in the overall cost function. The algorithm is similar to Section 6.1 except for the fact that is not updated at each iteration because is fixed and given. Similar to (45), we define the Lagrangian as:

| (56) |

The objective function of dual problem is:

Then the dual problem is:

The Lagrange multipliers are updated by (55), where and maximize Lagrangian (56).

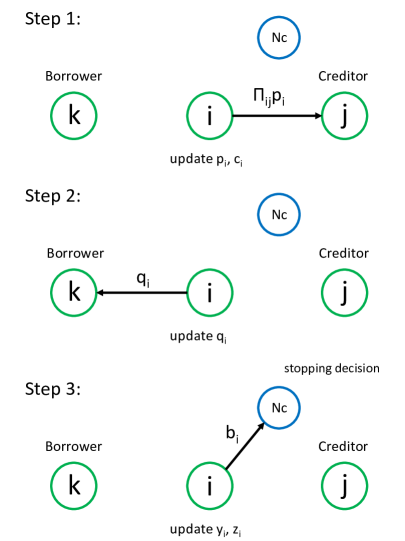

6.2.1 Implementation of Algorithm

Our algorithm for this problem is a simple modification of Algorithm . We call it Algorithm . Its -th iteration is as follows.

-

1.

Each node fixes , , and , and calculates and :

where , and

Then each node sends to every node .

-

2.

Each node receives from every and updates :

Then each node sends the updated to every .

-

3.

Each node receives from every and updates and :

where , and

where .

Each node checks the conditions and . If both conditions hold, it sets ; otherwise, it sets . It then sends to the central node . If for all then asks all nodes to terminate the algorithm.

These steps are illustrated in Fig. 16.

6.3 Numerical Results

6.3.1 Example 1: A Four-Node Network

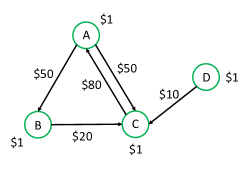

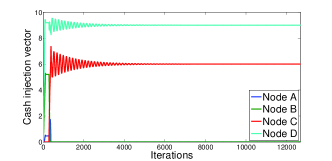

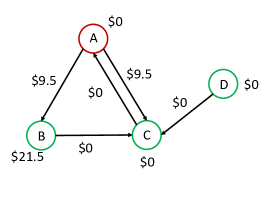

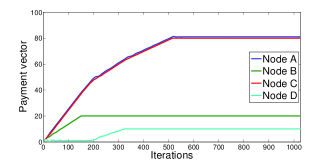

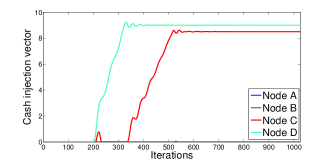

In this section, we illustrate the convergence of our distributed algorithm to the optimal solution. We use a four-node network shown in Fig. 17(a). Node owes $ to and , node owes $ to , node owes $ to , and node owes $ to . Each node has $ on hand. After all the clearing payments, the borrower-lender network reduces to Fig. 17(b). Without any external financial support, nodes , , and are in default, and the total amount of unpaid liability is $. Assume that for in LP (4), i.e., that each dollar of unpaid liability contributes to the cost. Without any external cash injection, the value of the cost function is .

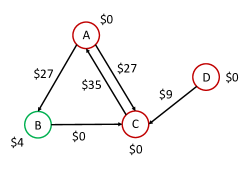

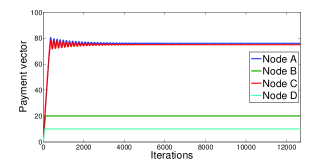

We first study Problem I, the case with a fixed maximum total amount of injected cash. We assume that we can inject at most into the system. We run our algorithm with initial and . The step size is , and the stopping tolerance is . Figs. 19(a) and 19(b) illustrate the evolution of payment vector and cash injection vector , respectively, as a function of the number of iterations of the proposed distributed algorithm. The payment vector converges to ; the cash injection vector converges to . These are optimal, as verified by solving the LP (4-6) directly. With external cash injection, the borrower-lender network reduces to Fig. 19 after all the payments. Now the total unpaid liability is $. Thus the value of the cost due to unpaid liability after the optimal bailout is .

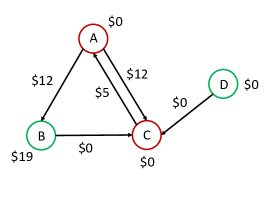

Second, we test our algorithm on the Lagrange formulation of Problem I. In this example, the initial settings are the same as in the previous example. In addition, we fix the Lagrange multiplier . As shown in Fig. 21(a) and Fig. 21(b), the payment vector converges to , and the cash injection vector converges to . These are optimal, as verified by solving the LP (8) directly. With external cash injection, the borrower-lender network reduces to Fig. 21 after all the payments. Now the total unpaid liability is $, and the cash injection amount is $. Thus the value of the cost function after the optimal bailout is . By injecting $17.5, we reduce the total unpaid liability by $35.55, and we reduce the total cost by .

We see from Fig. 21 that although is still in default, in the optimal bailout strategy we choose not to inject any cash in . The reason is that if we inject some cash $ into in Fig. 21, the total unpaid liability will decrease by $ so that the unpaid liability term of the cost function will be reduced by , i.e., the value of the overall cost function will actually increase by .

6.3.2 Example 2: A Core-Periphery Network

In this section, we examine the practicality of our distributed algorithm. As in Section 4, we assume that the US interbank network is well modeled as a core-periphery network that consists of a core of 15 highly interconnected banks to which most other banks connect [51]. We test the distributed algorithm for LP (8) on a simulated core-periphery network illustrated in Fig. 13. The core network consists of 15 fully connected core nodes. Each core node has 70 corresponding periphery nodes which owe money only to this core node. For each pair of two core nodes and , we set as a random number uniformly distributed in . For a core node and its periphery node , is set to be uniformly distributed in . All these obligation amounts are statistically independent. The asset vector is . In addition, we assume for , and in LP (8). We generate 100 independent samples of a core-periphery network drawn from this distribution. These samples thus all have the same topology but different amounts of liabilities. We run the distributed algorithm of Section 6.2.1 with initial conditions . The step size is .

The stopping criterion for the distributed algorithm is . Let be the value of the total cost function calculated by our distributed algorithm, and let be the corresponding value obtained by solving the linear program directly, in a centralized fashion. Under this stopping criterion, the relative error, defined as , is less than for each sample in our simulations.

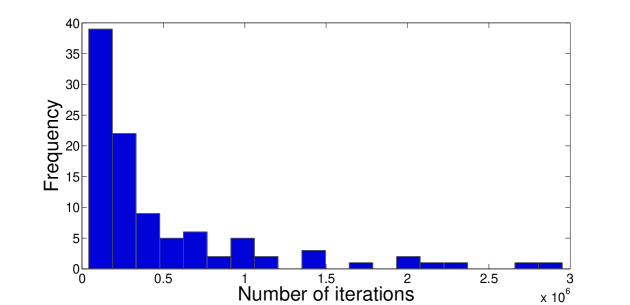

The number of iterations is shown in Fig. 22. The average number of iterations is . Moreover, from Fig. 22, we can see that for most cases, the algorithm terminates within iterations.

The time spent on each iteration consists of two parts: the computing time and the time it takes to convey messages between the nodes. During each iteration, a node needs to transmit information to a set of neighbors twice: in Steps 1 and 2. Note that in Step 3, the stopping sign is transmitted to the central node. However, it is not necessary for a node to wait for the response before next iteration. Therefore, we do not count it towards the communication delay during one iteration. It takes light 13.2ms to travel from LA to NYC, which is the longest possible distance between two financial institutions within the continental US. So the propagation delay in one iteration could be roughly estimated as . Hence, for most cases, the algorithm would terminate within , and the average running time would be below . These running times would be acceptable in applications where these computations are run overnight or during a weekend. Note that the computation time at each node is negligible compared to these communication times, and therefore we ignore it in these estimates.

Another possible set-up is that each institution provides a client-end computer and we colocate these computers in one room. Assuming that the longest network cable in this room is 100 meters, the propagation delay per iteration would be around . For the computing time, we just analyze the core nodes because the periphery nodes have no borrowers and only one creditor so that the computing time for the periphery nodes is much smaller than for the core nodes. Usually, multiplications dominate the computing time. At each iteration, a core node calculates , , and for all its creditors . Since the core network is a fully connected network with 15 core nodes, a core node has 14 creditors so that it does less than 50 multiplications per iteration. Assuming that each multiplication takes 500 cpu cycles and the cpu on the client-end computer is 3GHz, then the computing time per iteration is around . Thus, for most cases, the algorithm terminates within . By colocating the client-end computers of all the financial institutions in the system, we can significantly reduce the running time of our distributed algorithm so that it can be easily run many times during a day.

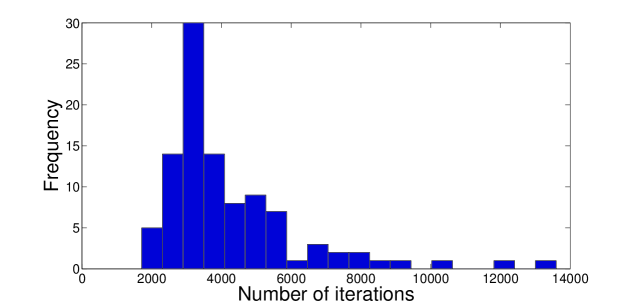

In a monitoring application, our aim might be to calculate the payments approximately rather than exactly. In this case, the running time can be reduced by relaxing the termination tolerance. We set the stopping criterion as . Under this stopping criterion, the relative error, , is around for each sample in our simulations. Fig. 23 illustrates the number of iterations. The average number is . The number of iterations is less than 10000 for most cases. By similar analysis, the average running time for the non-colocated scenario is . For most cases, the algorithm will be terminated within . If we colocate the client-end computers of all the financial institutions, the algorithm will terminate within .

The above running time analysis is for the Lagrangian formulation of Problem I, in which is a constant. In Problem I, is a dual variable that also needs to converge. So the running time of the distributed algorithm for Problem I will be larger than the time for its Lagrangian formulation. From Fig. 19 and Fig. 21, we observe that with the same stopping tolerance, the number of iterations of the distributed algorithm for Problem I is around 10 times the number of iterations for its Lagrangian formulation. Therefore, for Problem I, to calculate the exact payment vector, the algorithm will terminate within around for the non-colocated scenario and within for the colocated scenario. To obtain the payments within 1% error, the algorithm will terminate within around and for the non-colocated and colocated scenarios.

7 Conclusions

In this work, we have developed a linear program to obtain the optimal cash injection policy, minimizing the weighted sum of unpaid liabilities, in a one-period, non-dynamic financial system. We have further proposed a reweighted minimization algorithm based on this linear program and a greedy algorithm to find the cash injection allocation strategy which minimizes the number of defaults in the system. By constructing three topologies in which the optimal solution can be calculated directly, we have tested both two algorithms and shown through simulation that the results of the reweighted minimization algorithm are close to optimal, and the performance of the greedy algorithm highly depends on the network topology. We also compare these two algorithms using three types of random networks for which the optimal solution is not available. Moreover, we have proposed a duality-based distributed algorithm to solve the linear program. The distributed algorithm is iterative and is based on message passing between each node and its neighbors. No centralized gathering of large amounts of data is required, and each participating institution avoids revealing its proprietary book information to other institutions. The convergence and the practicality of the distributed algorithm are both supported by our simulations. We have also considered the situation where the capital of institutions at maturity is a random vector with known distribution. We have developed a stochastic linear program to find the optimal cash injection policy to minimize the expectation of the weighted sum of unpaid liabilities. To solve it, we have proposed two algorithms based on Monte Carlo sampling: Benders decomposition algorithm and projected stochastic gradient descent. In addition, we show that the introduction of the all-or-nothing payment mechanism turns the optimal cash injection allocation problem into an NP-hard mixed-integer linear program. However, we show through simulations that use optimization package CVX [33, 32] that this problem can be accurately solved in a few seconds for a network size comparable to the size of the US banking network.

Appendix A Comparison of Three Algorithms for Computing the Clearing Payment Vector

A.1 Proportional Payment Mechanism

In [20], zero bankruptcy costs are assumed, and three methods of finding the clearing payment vector are proposed: a fixed-point algorithm, the fictitious default algorithm and an optimization method. In this section, we first introduce and analyze these three methods and then compare their computation times under different network topologies.

A.1.1 Fixed-Point Algorithm

By definition, the clearing payment vector is a fixed point of the following map:

where the minimum of the two vectors is component-wise. Under certain mild assumptions

specified in [20], the fixed point is unique. It can be found

iteratively via the following algorithm [20].

Fixed-point algorithm:

-

1.

Initialization: set , , and set the stopping tolerance to a small positive number based on the accuracy requirement.

-

2.

.

-

3.

If , stop and output the clearing payment vector ; else, set and go to Step 2.

At each iteration, the computational complexity is dominated by , which is . The number of iterations is highly dependent on the network topology and the amounts of liabilities.

A.1.2 Fictitious Default Algorithm

The fictitious default algorithm is proposed in Section 3.1 in [20]. The basic idea

is to first assume that all the nodes pay their liabilities in full. If, under this assumption,

every node has enough funds to pay in full, then the algorithm terminates. If some nodes do not

have enough funds to pay in full, it means that these nodes would default even if all the other

nodes pay in full. Such defaults that are identified during the first iteration of the algorithm

are called first-order defaults. In the second iteration, we assume that only the first-order

defaults occur. Every non-defaulting node pays in full, i.e., ; every defaulting

node pays all its available funds, i.e., .

If there is

no new defaulting nodes during this second iteration, then the algorithm is terminated. Otherwise,

the new defaulting nodes are called second-order defaults, and we proceed to the third iteration.

In the third iteration we assume that both the first-order and second-order defaults occur. We

calculate the new payment vector and again check the set of defaulting nodes. We keep iterating

until no new defaults occur. Since there are nodes in the system, this algorithm is guaranteed

to terminate within iterations. The specifics of the fictitious default algorithm are as follows.

Fictitious default algorithm:

-

1.

Initialization: , , and .

-

2.

For all nodes , compute the difference between their incoming payments and their obligations:

-

3.

Define as the set of defaulting nodes:

-

4.

If , terminate.

-

5.

Otherwise, set for all . For all , compute the payments by solving the following system of equations:

-

6.

Set and go to Step 2.

At each iteration of the fictitious default algorithm, the computational complexity is dominated by solving the linear equations in Step 5. The number of unknowns in these equations and the number of equations are both equal to the number of elements in . In the worst case, the number of defaulting nodes in the system is of the same order as . In this case the computational complexity per iteration is [53]. Compared to the fixed-point algorithm, the fictitious default algorithm has a larger computational complexity per iteration, and, as shown below in Section A.1.4, larger running times on several network topologies. However, the advantage of the fictitious default algorithm is that it is guaranteed to terminate within iterations. Moreover, the fictitious default algorithm will produce the exact value of clearing payment, unlike the fixed-point algorithm which produces an approximation.

A.1.3 Linear Programming Method

Define , which is a strictly increasing function of . By Lemma 4 in [20], the clearing payment vector can be obtained via the following linear program:

| (57) | |||

| subject to | |||

The computational complexity of solving an LP is [53].

| Fixed-point algorithm | Fictitious default algorithm | LP method | ||||

| ave (s) | stdev | ave (s) | stdev | ave (s) | stdev | |

| fully connected | 0.9128 | 0.1045 | 10.7341 | 0.7182 | 53.1725 | 11.8947 |

| core-periphery | 0.0869 | 0.0342 | 7.8213 | 1.2843 | 0.1964 | 0.0507 |

| linear chain | 0.0462 | 0.0170 | 10.2574 | 1.0211 | 0.1610 | 0.0449 |

A.1.4 Comparison of Running Times on Three Different Topologies

We calculate the clearing payment vector via the above three methods on three different network topologies and compare the running times. The first network topology is a fully connected network with 1000 nodes. All the obligation amounts and asset amounts are independent random variables, uniformly distributed in . The second network topology is a core-periphery network shown in Fig. 13. It contains 15 fully connected core nodes. Each core node has 70 periphery nodes. Each periphery node has a single link pointing to the corresponding core node. All the obligation amounts are independent uniform random variables. For each pair of core nodes and the obligation amount is uniformly distributed in . For a core node and its periphery node , the obligation amount is uniformly distributed in . The asset amounts are uniformly distributed in . The third network topology is a long linear chain network with 1000 nodes. For , the obligation amount is uniformly distributed in , and for other pairs of and , . The asset amounts are uniformly distributed in .

For each type of network, we generate 100 samples. We run the Matlab code on a personal computer with a 2.66GHz Intel Core2 Duo Processor P8800. The average running times and the sample standard deviations of the running times for the three methods are shown in Table 2. For all three types of networks, the fixed-point algorithm is the most efficient one. Note that the computation time of linear program method is highly variable because simpler topologies result in being a sparse matrix, reducing the running time.

A.2 All-or-Nothing Payment Mechanism

A.2.1 Fixed-Point Algorithm and Fictitious Default Algorithm

We now assume the all-or-nothing payment mechanism where node pays if it is solvent and pays nothing if it defaults. Therefore, the clearing payment vector is a fixed point of the map defined as follows:

We find the fixed point of iteratively via the following algorithm.

Fixed-point algorithm:

-

1.

Initialization: set , .

-

2.

.

-

3.

If , stop and output the clearing payment vector ; else, set and go to Step 2.

In fact, under the all-or-nothing payment mechanism, this fixed-point algorithm can be interpreted as the following fictitious default algorithm. We initially assume that all the nodes pay their liabilities in full, i.e., . If, under this assumption, every node has enough funds to pay in full, then the algorithm terminates. If some nodes do not have enough funds to pay in full, it means that these nodes would default even if all the other nodes pay in full. We define these nodes as first-order defaults. With function , we identify the first-order defaults and set their payments to zero. In the second iteration, we assume that only the first-order defaults occur. Every non-defaulting node pays in full, i.e., ; every defaulting node pays 0, i.e., . Again, with function , we identify the new defaulting nodes, which are called second-order defaults, and set their payments to zero. If there are no such new defaulting nodes, the algorithm terminates; otherwise, we proceed to the third iteration. We keep iterating until no new defaults occur, i.e., .

Since there are nodes in the system, this algorithm is guaranteed to terminate within iterations. At each iteration, the computational complexity is dominated by , which is . Therefore, the computational complexity of the fixed-point algorithm (fictitious default algorithm) is .

A.2.2 Mixed-Integer Linear Programming Method

A.2.3 Comparison of Running Times on Three Different Topologies

We calculate the clearing payment vector under the all-or-nothing payment mechanism via the above two methods on three network topologies described in Section A.1.4, and compare the running times.