On volatility smile and an investment strategy with out-of-the-money calls

Abstract.

A motivating question in this paper is whether a sensible investment strategy may systematically contain long positions in out-of-the-money European calls with short expiry. Here we consider a very simple trading strategy for calls. The main points of this note are the following. First, the presented trading strategy appears very lucrative in the Black-Scholes-Merton (BSM) framework. In fact, it is such even to the extent that the BSM model turns out to be, in a sense, incompatible with the CAPM. Second, if one wishes to adapt these models together, then the adjustment of the consistent pricing rule (i.e. modifying state price densities) inevitably leads to some form of volatility smile and this is the main point of the paper. Moreover, these observations arise from purely structural considerations.

1. Introduction

In this note we make some simple observations about the prices of European call options in the Black-Scholes-Merton (BSM) model. We suspect that many scholars and practitioners find the conclusion somewhat counter-intuitive111For example in [Haug 2007] pp. 54-65 the compatibility of CAPM and BSM models is discussed in several occurrences.. The main observation of this note is that in the confinements of the BSM model it is in some sense a very lucrative strategy to keep buying cheap out-of-the-money calls with short time horizons in successive instances. In fact, the strategy appears to be ’too good to be true’. We will work inside the BSM framework with hardly any empirical information, so the findings are structural in nature.

The author came across the key observation here by an (unsuccessful) attempt to apply the BSM framework in pricing catastrophe bonds. Namely, it would appear like a sound approach to model a CAT bond by means of digital options, which are triggered by an extreme behavior of the underlying, or a ‘tail event’. The author tried to find a kind of asymptotic price of risk for an extremely rare but expensive event. The idea was to analyze European calls, with eventually extreme parameters, in such a way that the probability of the the portfolio yields being non-zero would diminish but the expected value of the yields would be kept constant, say . This approach somewhat resembles ’renormalization’ techniques in physics.

Here is what went wrong. Suppose that and are the physical and the risk-neutral probability measures, respectively, appearing in the standard BSM model. Let us recall that provides the modeled real probabilities of events, whereas is applied in calculating the prices of derivatives. We will later recall how to calculate the Radon-Nikodym derivative (a.k.a. stochastic discount factor) for a given equity value at the time horizon . The following simple observation is promoted here; namely that the measures and , although equivalent in the measure theoretic sense222Perhaps the most common name for is the equivalent martingale measure., are in a sense not well comparable financially. That is, the ratio tends to as and tends to as . Therefore the above mentioned attempt in pricing CAT bonds was bound to fail, since selecting either of the tails results in a trivial asymptotic price of risk, either or , depending on which tail is chosen.

The fact that the above ratio strongly biases small values of is intuitive from the point of view of a risk averse agent. Still, it enables one to device an interesting trading strategy. The key idea in forming this strategy is that according to the asymptotics of the ratio it is possible to buy ’lottery tickets’ at a price, which is very small compared to the expected payoff.

As the result, we will device a rather simple trading strategy which shares some characteristics of high-frequency trading strategies, such as a large number of relatively small, restricted bets and a very high Sharpe ratio.

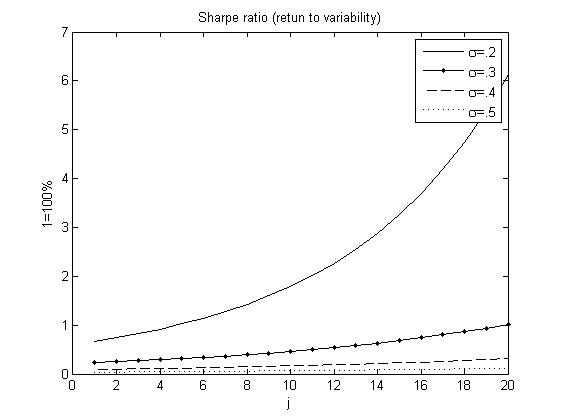

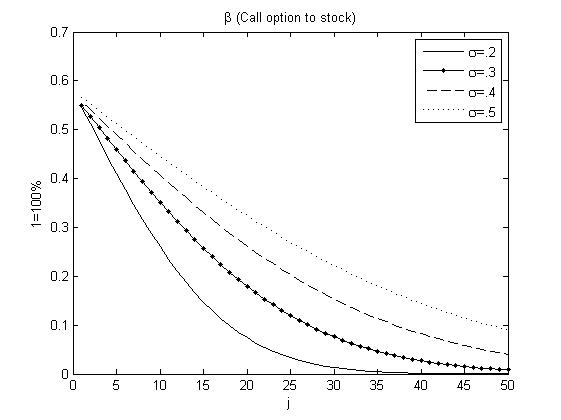

One theoretically intriguing phenomenon here is that the outcome of the trading strategy is not well in harmony with Modern Portfolio Theory (MPT) or Capital Asset Pricing Model (CAPM) and it produces unrealistically high Sharpe ratios, as already mentioned. It is also quite easy to see how moderately out-of-the-money calls have a low beta with respect to the underlying asset. The compatibility question of the BSM and CAPM has been addressed in previous literature, see e.g. [Bick 1987], [Benninga&Mayshar 2000]. This is of course a natural problem since BSM and CAPM are typical representatives of the two most commonly applied financial valuation schemata, risk-neutral (RN) pricing and equilibrium pricing, respectively. Also, Black and Scholes applied CAPM in their seminal paper to give an alternative derivation for their option valuation formula. This, per se, does not guarantee the general compatibility of these pricing frameworks. It is also well-known that the actuarial value of derivatives may easily differ from the risk-neutral pricing based value.333Actually, starting from the fact that the treatment of risk premia sometimes varies, the actuarial value is not even completely uniquely defined throughout the literature.

To reiterate, it turns out that the investigated investment strategy, taken to the extreme, produces in the BSM framework Sharpe ratios tending to the infinity, a state non-maintainable in view of the philosophy of the Modern Portfolio Theory (MPT), so that apparently the BSM model and the MPT are not fully compatible. The same conclusion is valid for BSM and CAPM, since the strategy simultaneously produces low betas as well.

We conclude by discussing an interesting connection to volatility smile. Our findings suggest how some form of volatility smile can be actually an expected phenomenon by looking at structural properties of common valuation models with rather minimal empirical information; we mainly rely on the fact that the market price of risk is positive. In particular, we are not required to invoke further asset dynamics considerations (e.g. fat tails), empirical or stylized facts, preference structure considerations, behavioral finance issues, etc. The volatility smile here is of formal nature and we are by no means claiming that it fully explains the one witnessed empirically.

We have tried to make the discussion accessible to an audience as general as possible.

1.1. Preliminaries

We will make rather casually references to the Arbitrage Pricing Theory (APT), Black-Scholes-Merton model (BSM), Capital Asset Pricing Model (CAPM) and Modern Portfolio Theory (MPT). We refer to the list of monographs in the references for notations and suitable background information.

The Sharpe ratio appears here very frequently, so let us recall it for convenience:

| (1.1) |

where is the stochastic rate of return of an asset in question and is the rate of return of a benchmark risk-free asset, both annual.

Let us recall some well-known formulas relevant to the discussion for the sake of convenience. Let us calculate the ratio discussed in the introduction. First, let us recall the density functions of the physical measure and risk neutral measure in the BSM model. Here we are particularly interested in the relative increments in the value of the equity where is deterministic. The -density is given by

that is, considered with respect to measure has the law

.

The risk neutral density is similar, only the center of the distribution is shifted downwards:

(see e.g. [Fölmer&Schied 2011, p. 269]), that is, considered with respect to measure has the law .

The price of a European call at time having payoff at maturity is denoted by . The following equation holds:

| (1.2) |

for all constants by change of variable . Similarly we obtain that

| (1.3) |

Denote the above expectation by . Then we may write the -standard deviation of the call payoff as follows:

2. The mechanism described

2.1. The ratio

Recall that the state price density and stochastic deflator can be written by means of the Radon-Nikodym derivative which can be computed as follows:

| (2.1) |

and straight forward algebraic manipulations yield that (2.1) equals

| (2.2) |

Recall that (typically). This can be seen rather a structural property than empirical fact, since in reasonable models the expected rate of returns of risky assets are higher than that of the risk-free assets.

We see immediately that (2.2) tends to as and tends to as . Since (typically), we have that

| (2.3) |

as . This quantity has the same asymptotics with respect to as (2.2) and decays exponentially as grows. By definition, the right hand side of (2.3) equals to when , that is, the critical point where physical probability and the risk-neutral one asymptotically coincide, is at-the-money. The role of in this context will be discussed subsequently. In that connection we will apply the short time scale ratio , since it is convenient to work with.

2.2. The trading strategy

An essential feature of the trading strategy discussed shortly is that we would like to buy very cheap, out-of-the-money European style ’plain vanilla’ calls with short horizon. Then we wait to the end of the horizon, and, regardless of the outcome, we buy the next patch, wait, and keep doing this, say, to the end of the year. In practice the lengths of intervals between expiration dates of traded European style options are bounded from below, for example for index options on S&P 500 it is one month. We are also required to trade very small amounts of calls.

However, in the BSM model there is no structural constraint preventing us from buying and selling options every second worth a cent. We will follow the BSM framework in other aspects too. Thus, we will assume that there are no transaction costs, liquidity concerns, or any other such market imperfections. We will assume that when cash is not invested in calls, it is invested in risk-free bonds recognized by the BSM model. We will assume that the parameters of the BSM model remain constant during the whole time. In the next section we will analyze a yet simpler situation for the sake of transparency of the ideas present.

The downside of the theoretical considerations proposed here, of course, is that were are dealing with phenomena appearing only in micro scale when we push the BSM model to the limit. This happens in the model when buying extremely deep out-of-the-money calls.

Although the assumptions made are very strong with potential practical applications in mind and the situations arising can be considered as marginal, we suspect that the fact that ’the odds are not against’ the proposed strategy could potentially pave way for some suitable automated options trader detecting bargains. This is to say, we believe the idea presented here could be combined with some other high-frequency trading functions. The practical problem with finding extremely deep out-of-the-money options and the limited number of expiries could be somewhat relaxed by internationally diversifying to all the European type calls. In fact, as it turns out in the next section, the high Sharpe ratio resulting from running the investment strategy is not restricted to using plain vanilla calls.

Next we will describe our trading strategy. In order to make sure it is self-financing, we will first fix the amount to be invested, say units of numeraire during year. We will divide the year equally to time intervals . Since the model parameters and are constant over time, an inspection of the option price formula (1.2) reveals that there exists a unique constant such that

| (2.4) |

regardless of what the realized values shall be. This is a crucial fact and it makes the strategy simple to implement and to analyze.

The algorithm of the investment strategy is as follows:

-

(i)

At time we have units of numeraire is at our disposal.

-

(ii)

At time we buy -many European calls maturing at time with strike . Here is the constant appearing in (2.4).

-

(iii)

At time we invest the possible proceeds of the maturing call to risk-free bonds.

-

(iv)

At time we buy -many European calls maturing at time with strike .

-

(v)

We continue in this manner to the end of the year , at which point we have the yield of the tradings invested in risk-free bonds.

Because of the -to- correspondence (for a fixed ) of and we may alternatively describe the strategy by first choosing the constant and then solve the initial capital to be invested accordingly.

Since we buy a portfolio of -many calls with strike at time we observe similarly as in (1.2) and (1.3) that the yield of such a call portfolio has essentially the same risk-neutral and physical distributions as the yield of one call with parameters , and the same running time interval. Thus, since the increments are independent in the BSM model, we are only required to analyze the expected value, variance and the price of one call only, it is convenient by virtue of (1.2) and the preceding formulas to assume that

| (2.5) |

2.3. Numerical illustrations

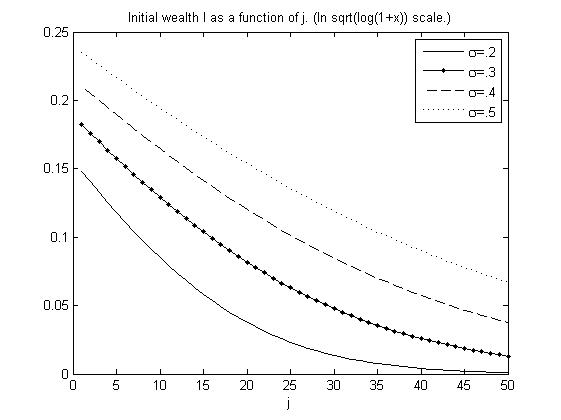

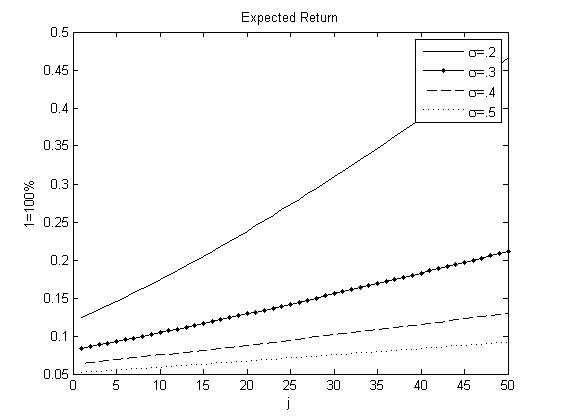

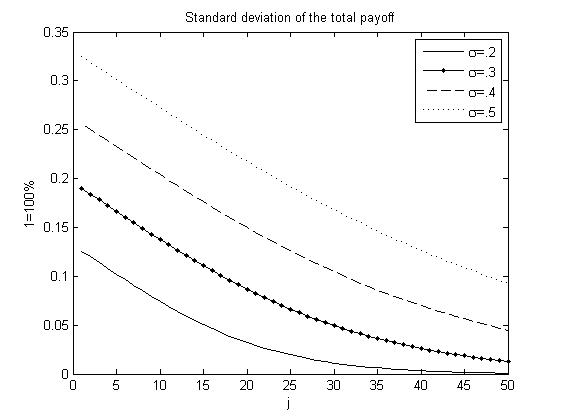

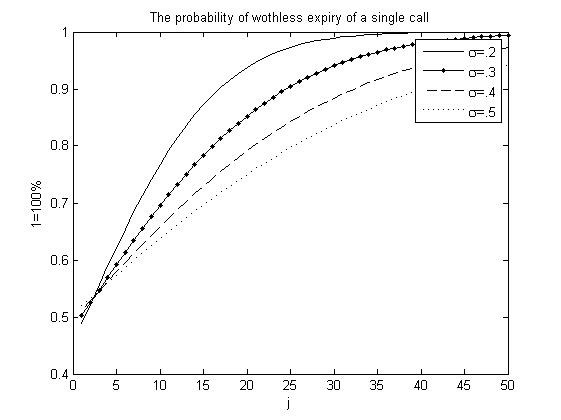

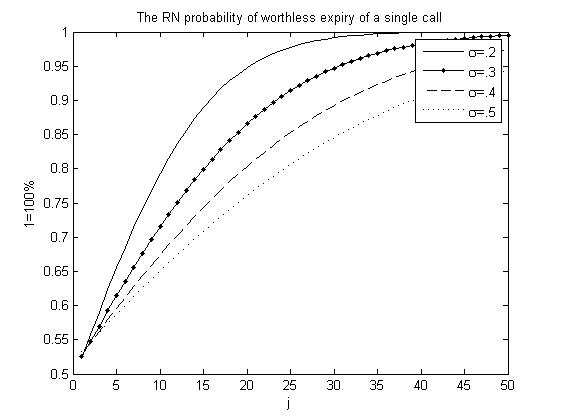

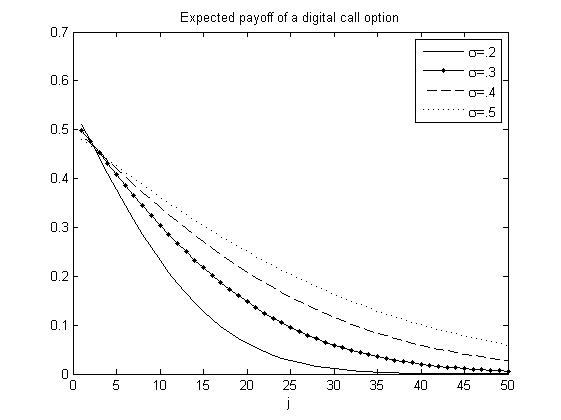

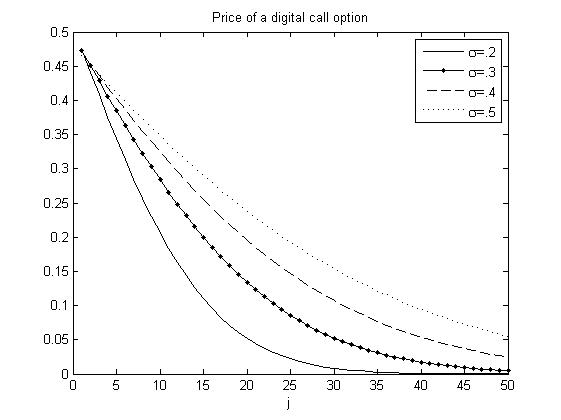

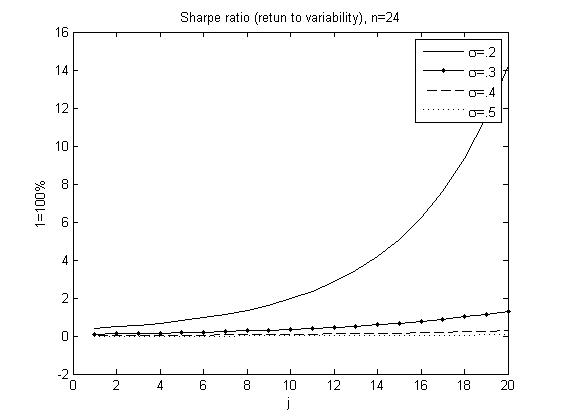

Some relevant values of the cash flows resulting from running the strategy are presented below. For the sake of simplicity we will begin by choosing different values for the constant , instead of choosing the initial wealth level in the investment strategy. The computations are done by using Matlab with the BSM model parameters (trend), (short rate), (implied volatility) and strike prices with ( nominally by (2.5)) , (number of steps above at-the-money) and (months). The following figures illustrate the fact that the trading strategy is most lucrative (on paper) and is sensitive to the availability of deep out-of-the-money calls and large number of holding periods.

These computations suggest that if one is to expect BSM type conditions on the market for a year (e.g. constant volatility, no autocorrelation on the equity returns, normally distributed increments and no volatility smile), then buying a cheap call every month already results in high Sharpe ratios and low beta.

3. Theoretical considerations

3.1. Digital options

We will take a look at digital options since they are easy to analyze and yet they capture the essential phenomenon discussed here. Since the analysis is transparent and even rather elementary with these options, the upside is that we do not require any numerical computations. Thus we will revisit the trading strategy by using digital options in place of the plain calls.

Let us consider the price of a European style digital option, which pays unit of numeraire at the time of maturity if the underlying security satisfies . This kind of digital option can be approximated, both in payoff and price, by buying many European options with strike price and shorting many options with strike price , see [Breeden&Litzenberger 1987] and [Jarrow 1986]. Here the time to maturity for all the options mentioned is the same and the approximation improves as increases.444It is useful to think of the definition of differential and put , being a large natural number.

In the BSM model the value of the digital option at time is

where the current value of is deterministic. The risk-neutral probability on the right hand side equals

In contrast, this should be compared to the physical probability that the option is triggered:

In the investment strategy of the previous section we kept cash invested in risk-free bonds when not invested in calls. However, the accumulation of interest does not play a significant role in this paper. Therefore, in what follows we will instead consider cash being invested in a bank account with zero interest for the sake of simplicity, and, similarly, we will treat the discount factor as by convention. Indeed, this causes no problem as we are not running any kind of replication strategy to synthesize derivatives and therefore we may separate the short rates appearing in the BSM model and in the bank account. The Sharpe ratio (1.1) is invariant under positive scaling of cash flows, therefore in calculations it does not matter what is the initial capital to be invested.

The expected rate of return for a digital option is easy to formulate:

| (3.1) |

The above ratio reads as follows: the potential payment of the option (i.e. ) times the probability of the option being triggered divided by the purchase price of the option. Since (2.2) is decreasing in , it is easy to check that the fraction in (3.1) satisfies

| (3.2) |

where is the length of each holding period. In particular, the expected return on investment (3.1) tends to infinity as increases.

Now, suppose that we will use digital options in a similar fashion as in the previously introduced trading strategy. Then the outcome is easy to understand. Namely, for holding periods we will buy in the beginning of each period digital options with horizon and strike such that the total worth is . Then the payoff is binomially distributed, since we are essentially dealing with an i.i.d. sequence of binary random variables. The expected payoff of each of the independent bets is given by

where is the unique solution to the equation

Above we applied the change of variable . We observe that as . In the appendix we will show that the latter holds as .

The expected payoff resulting from running the above strategy with binary options is clearly and the standard deviation of the payoff is . The Sharpe ratio is then

We note that choosing high and results in low and , and high , in (3.2). In the above trading strategy we let the parameter (and thus ) vary in order to circumvent some technical calculations involving (3.2).

We note that it is essential above that we let and tend to infinity. Namely, for a fixed the corresponding binomial payoff process Sharpe ratio tends to .

3.2. Double digital options

The above considerations also apply if one uses double digital options, instead of simple digital ones. Recall that a double digital option is a European style derivative which pays of unit of numeraire if the value of the underlying asset hits a closed interval at maturity.

The above strategy implemented with double digital options also results in binomially distributed cash flow. For short intervals, where the option is triggered, the ratio will be close to (2.2), hence easy to understand.

For infinitesimal intervals the double digital options can be viewed as theoretical Arrow-Debreu securities and in this case the ratio (2.2) holds exactly for .

3.3. Incompatibility of the BSM model and the CAPM

The existence of the described (theoretical) investment opportunities appears not to align well with the Modern Portfolio Theory, since the Sharpe ratio of the investment opportunity grows unrealistically high.

The presented trading strategy has also some convenient linear statistical properties following from the simple feature that most of the time the European calls bought expire worthless. Namely, because of this reason and the basic properties of linear correlation the yield of the strategy has beta close to zero for large . Roughly speaking, in most holding periods the payoff is completely uncorrelated with the market. This remains true even if the underlying asset was a large base equity index corresponding to the market portfolio. The picture is, however, complicated by the fact that the investment strategy payoff process moves with large increases of the underlying asset. See appendix for information about the application of the central limit theorem to analyze the beta.

In the BSM framework the successively held options are non-autocorrelated and even independent. According to (1.3) and the fact that we buy -many calls, the payoffs resulting from each of the holding periods are identically distributed. Therefore the total proceeds of the investment strategy are roughly normally distributed by the Central Limit Theorem for a large number of holding periods555The obvious distortions in distributions resulting e.g. from the limited losses are shared by models of equity value.

Since the beta can be made very small, the theoretical investment opportunity is a fortiori incompatible with CAPM. The BSM model suggests singularly lucrative investment opportunities which cannot be fitted in the CAPM framework, i.e. simultaneously low beta and high Sharpe ratio. Thus the models appear structurally incompatible. Essentially same considerations apply to the APT model, since it is difficult to predict very specific short-term fluctuations of the stock prices or equity index by macroeconomic factors.

It is not clear how this mismatch should be interpreted. Perhaps these findings suggest that the equilibrium valuation models (e.g. CAPM and APT) prone to cancellations of risk, and, on the other side, the hedging-based valuation, represent different paradigms of financial economics. For example, the term ’arbitrage’ is a very different notion in the context of risk-neutral pricing, compared to its occurrence in the APT where the term rather stands for statistical arbitrage. In the risk-neutral pricing one identifies the values of cash flows which coincide with probability . On the other hand, in APT one identifies values of cash flows having only the same distribution, in fact only certain same parameters (factors) describing the distribution.

3.4. Volatility smile

As we already pointed out in the introduction, the investment strategies are based on the key observation that the physical and risk-neutral densities are not asymptotically comparable. We have so far discussed strategies in which one buys successively European vanilla or digital calls but the non-comparability of the densities at the lower tail suggests an analogous investment strategy where one successively shorts puts instead.

Suppose that the proposed investment strategy type were viable in practice. Then a wide adoption of these trading strategies should adjust upward the market prices of calls out-of-the-money and with a short horizon. Similarly, the market prices of short-horizon puts with low strikes should adjust downward, compared to the benchmark provided by the BSM model.666Intuitively, this appears to result in lower implied volatility but the following formal reasoning suggests the opposite. If the volume of the underlying security is outnumbered by the quantity of liquid options traded, then our attention in pricing the options shifts from hedging arguments to the law of supply and demand, cf. [Fengler 2005, p.45].

Next we will see what happens when the state price density curve is adapted into a shape such that the proposed investment strategy ceases to exist. Let us analyze the asymptotic ratio (2.3), since it involves a simple relationship between the strike price and the volatility. Namely, the situation where

tends to (respectively ), as (respectively ) results in option prices incompatible with some equilibrium valuation models, like CAPM. One consistent remedy to this situation is to change the underlying state price density (see also [Fengler 2005]). Let us replace the constant in (2.3) by a function . Our heuristic rationale is that should be chosen in such a way that

| (3.3) |

for some reasonable (finite) bounds . This means that the BSM state price density could by adjusted by varying continuously in such a way that at-the-money no change occurs (see remarks after (2.3)) and in the above inequality the bounds are obtained asymptotically.

We leave the exploration of these bounds for future research but we suggest that studying the Sharpe ratios of the resulting investment strategies’ payoffs should be a good starting point.

The above inequalities suggest the following asymptotics for in adjusting the state price density, which also involves the volatility smile:

| (3.4) |

Next we will give as an example an ad hoc formula for volatility smile curve. We choose and apply a suitable logistic-like function to model the above asymptotics. Put

and consider

where . We obtain the following heuristic volatility smile formula for :

| (3.5) |

This approach, although being ad hoc and not producing a completely satisfying volatility smile curve, is rather transparent in what comes to describing the tails.

We have discussed a trading strategy with short time intervals, which then amplifies the phenomenon under investigation. This suggests that the above explanation of the volatility smile should be most relevant for options having short time to maturity and low base volatility. The constant above appears like a market smile factor which should be calibrated from the market data.

In fact, the factor has a clear interpretation in our setting. Namely, since was chosen to be the supremum of the absolute value of the inverse of the right hand side of (2.3), the quantity can be described as the least upper bound for the expected rate of return for all European style derivatives in the model with short horizon. In the above framework the feature that markets ’tolerate’ high corresponds to weak volatility smile.

4. Discussion

We have used structural assumptions of the BSM model to argue that some form of volatility smile is an expected phenomenon. Surely we are not claiming here that fat tails of return distributions and jumps do not contribute to volatility smile.

We make next some remarks. The latter example with digital options produces expected returns growing slower because in treating regular calls the integration of the function (instead of ) against both physical and risk-neutral probabilities puts more weight on the upper tail where the ratio increases rapidly. Thus the discussed phenomenon amplifies in the case with the European plain vanilla calls (instead of digital options).

We argued the beta of the payoff of the investment strategy is small since most of the time the calls bought expire worthless. This intuitively means that in most holding periods the payoff happens to be completely uncorrelated with the market. Similarly, the autocorrelation of the payoff process is close to zero, even if the underlying were strongly autocorrelated. Also, according to the same reasoning the correlation of the yield process with macro economic indicators employed by the APT model is close to zero.

4.1. Extensions

The basic phenomenon discussed does not change considerably if the parameters , and change over time. Therefore the strategy should run similarly with similar conclusions even if the model is updated with new parameter values in between the holding periods.

There are of course issues not considered here related to deviation form the BSM framework, such as the non-normality of the yield distribution. Perhaps the issue with the distributions is not crucial here because we essentially applied only the very rudimentary property of the pricing system, namely that tends to as . Therefore the strategy should be successfully executable in any pricing systems with this key feature. Immediately two questions arise next:

-

(1)

What happens if one uses other than European style of options in the investment strategy?

-

(2)

What happens if one trades European calls with similar logic but does not wait to maturity?

These problems are related to the fact that the times to expiry of issued options are bounded from below so that in practice one cannot take to be very large annually.

There are two more serious issues in the real markets that appear to impair the functioning of the described strategy. One is market information implicit in the prices of derivatives and the other is autocorrelation of the securities.

Often the prices of derivatives are considered to contain information (or at least market sentiment) about the future values of the underlying. Therefore one could argue that the described strategy fails because the markets anticipate the future rise/drop of the security value in the derivative price and thus the effect of true randomness strongly exploited here vanishes. Moreover, one could argue that even though in the long run the future values of the market are hard to predict, the market has disproportionately good insight about the near future. This could appear to be a plausible worry, especially in the sense that we would possibly end up betting against well-informed agents. Also, the markets could react to such consistent trading by making deep-out-of-the-money calls less cheap. We do not only restrict our concern to a ‘spontaneous’ response of the markets due to the law of supply and demand but possibly by a strategic decision of some agents as well. This was already discussed in connection to volatility smile.

Another possible critique involves autocorrelated securities returns. Namely, keeping betting (up, in our setting) in a bearish trend could have similar consequences as betting against well-informed investors. We admit that the presented strategy is probably not such a good idea in a bearish market.

Still, there appears to be a possible remedy to these suggested problems. In both the examples the problem was a severe failure of the models resulting from a kind of lack of of randomness. The idea is to cultivate the strategy further in order to forcibly randomize events, in a sense.

Let us first try to deal with the informed markets effect. We claim that even if some agents participating in the markets have information about the future values of the underlying security or index, it is not easy to predict the exact value of the underlying. Therefore we can circumvent the proposed problem by trading double digital options instead of plain vanilla calls. The payoff function of a double digital option can be regarded as an indicator function on possible short interval . The shorter the interval, the more difficult it is obviously for anyone, no matter how informed, to predict if the underlying is going to hit the interval at the date of maturity or not. The interval can be placed far in the upper tail, so that the expected returns tend high according to (2.2).

In what comes to the problem with the autocorrelation, one possible, rather theoretical approach is to attempt a similar randomization method by making the step sizes ultra-short and then executing trades only in every tenth interval, or so.

We already discussed how the trading strategy works with digital options. These can be regarded as power options of power under the conventions if and . Since the limit (2.3) decays exponentially, we could instead use power options of any power in the trading strategy. Note that for and large values of the upper tail values have relatively higher weight than in the case with regular calls and therefore the effect on expected returns becomes more pronounced.

Expected returns are more sensitive to the choice of the constant , compared to the number of holding periods . For low levels of implied volatility one can choose the constant closer to compared to the case with higher volatilities. In (2.3) we considered the case where

It could easily happen that the above quotient is as well, for example in our case with the constants , and . The critical volatility can be seen as an inversion level where the effect of the time span on the ratio (2.3) changes its direction (). Interestingly, for this critical volatility the short time scale ratio is the correct value for (2.2), i.e. the ratio remains the same in all time scales.

Let us consider the extreme cases in (2.3) involving the value far away from the inversions level, that is, low implied volatility and high implied volatility, e.g. , respectively. The above observation about the change of the effect of the time scale suggests the following, in principle testable hypothesis involving volatility smiles. Namely, for shortening the expiry of out-of-the-money calls increases the expected return of the call in the case of low overall implied volatility, ceteris paribus, whereas it decreases the expected return of the call in case of high overall implied volatility.

Appendix

The strike to spot ratio of the trading strategy

Recall the formula

Write

We wish to check that as .

Note that

Observe that must be a unique function which is also strictly increasing and continuous.

Assume first that is continuously differentiable. Then

Actually, from this form one can deduce easily a continuously differentiable solution , thus it is continuously differentiable by uniqueness. From the above form we observe that for all . We obtain

for large . If approaches a real number asymptotically, then

thus

which means that , . This contradicts the assumption that has an asymptotic value. Therefore as .

Zero-beta of the investment opportunity with digital options

According to the Central Limit Theorem the average of the i.i.d realized payoffs converge in probability to the expected payoff. However, in using the normal approximation for the average payoffs one has to address the problem arising from the fact that for different values of the distributions of the payoffs from running the bets are different. Therefore one may apply a stronger result, namely Berry-Esseen theorem which gives a quantitative control of the convergence speed for the normal approximation of the distribution in terms of and the third moment. It suffices to verify that sample correlation between the payoff and the underlying converges to in probability with respect to as because then the same holds for also by the equivalence of the measures.

References

- [Benninga&Mayshar 2000] S. Benninga, J. Mayshar, Heterogeneity and Option Pricing, Review of Derivatives Research 4 (2000), 7-27.

- [Bick 1987] A. Bick, On the Consistency of the Black-Scholes Model with a General Equilibrium Framework, Journal of Financial and Quantitative Analysis, (1987), 259-275.

- [Björk 2004] T. Björk, Arbitrage theory in continuous time, Oxford University Press, 2004.

- [Brealey&Myers&Allen 2011] R. Brealey, S. C. Myers, F. Allen, Principles of Corporate Finance, McGraw-Hill/Irwin, 2011.

- [Breeden&Litzenberger 1987] D. T. Breeden, R. H. Litzenberger, Prices of State-Contingent Claims Implicit in Option Prices, The Journal of Business, 51, (1978), pp. 621-651.

- [Fengler 2005] M. Fengler, Semiparametric modeling of Implied Volatility, Springer 2005.

- [Fölmer&Schied 2011] H. Föllmer, A. Schied, Stochastic finance : an introduction in discrete time, De Gruyter, 2011.

- [Haug 2007] E. Haug, Derivatives Models on Models, The Wiley Finance Series.

- [Hull 2003] J.C. Hull, Options, futures, and other derivatives, Prentice-Hall, 2003.

- [Jarrow 1986] R. A. Jarrow, A characterization theorem for unique risk neutral probability measures, Economics Letters, Volume 22 (1986), 61-65

- [Shriyaev 1999] A. N. Shiryaev, Essentials of stochastic finance : facts, models, theory, Advanced series on statistical science & applied probability, 3, World Scientific, 1999.