Price Competition in Networked Markets: How do Monopolies Impact Social Welfare?

Abstract

We study the efficiency of allocations in large markets with a network structure where every seller owns an edge in a graph and every buyer desires a path connecting some nodes. While it is known that stable allocations in such settings can be very inefficient, the exact properties of equilibria in markets with multiple sellers are not fully understood even in single-source single-sink networks. In this work, we show that for a large class of natural buyer demand functions, we are guaranteed the existence of an equilibrium with several desirable properties. The crucial insight that we gain into the equilibrium structure allows us to obtain tight bounds on efficiency in terms of the various parameters governing the market, especially the number of monopolies . All of our efficiency results extend to markets without the network structure.

While it is known that monopolies can cause large inefficiencies in general, our main results for single-source single-sink networks indicate that for several natural demand functions the efficiency only drops linearly with . For example, for concave demand we prove that the efficiency loss is at most a factor from the optimum, for demand with monotone hazard rate it is at most , and for polynomial demand the efficiency decreases logarithmically with . In contrast to previous work that showed that monopolies may adversely affect welfare, our main contribution is showing that monopolies may not be as ‘evil’ as they are made out to be; the loss in efficiency is bounded in many natural markets. Finally, we consider more general, multiple-source networks and show that in the absence of monopolies, mild assumptions on the network topology guarantee an equilibrium that maximizes social welfare.

1 Introduction

The mechanism governing large decentralized markets is often straightforward: sellers post prices for their goods and buyers buy bundles that meet their requirements. Given this framework, the challenge faced by researchers has been to characterize the equilibrium states at which these markets operate. More concretely, consider a market with multiple sellers that can be represented by a network as follows:

-

Every seller owns an item, which is a link in the network.

-

Every infinitesimal buyer seeks to purchase a path in the network (set of items) connecting some pair of nodes.

In addition to actual bandwidth markets where users purchase capacity on links for routing traffic, networks are commonly used in the literature to model combinatorial markets where the items are a mix of substitutes and complements [3, 18, 32, 34]. As an illustrative example, consider the (sample) sandwich market of substitutes and complements in Figure LABEL:fig_examplemarket; the prices of different sandwich ingredients are controlled by different sellers, and every buyer wants to purchase a set of ingredients to make a full sandwich. Our goal in this paper is to analyze the effects of price competition in such networked markets, i.e., the pricing strategies employed by competing sellers and their effect on equilibrium welfare.

In this paper, we are interested in the following question: “How efficient are the equilibrium allocations in such markets and how do they depend on buyer demand and network structure?”. Our interest stems in part, from the fact that a vast majority of literature has focused exclusively on Walrasian Equilibrium as the market operating point. There is limited understanding of efficiency beyond the Walrasian framework. Walrasian Equilibria are indeed attractive: they always exist in large markets [6] and they are guaranteed to be optimal. However, the idea that prices are just ‘handed out’ to buyers and sellers so that the market clears may not always be applicable in a decentralized market. As [25] remarks,

“…an embarrassing lacuna in the theory of walrasian equilibrium is the failure to explain where the prices come from.”

In contrast, we take the view that the sellers control their own prices in order to maximize revenue and not just clear the market, i.e., they act as price-setters and not price-takers. In such a setting, it does not make sense to consider Walrasian Equilibrium as the notion of stability. Our objective therefore, is to quantify the inefficiency as compared to Walrasian Equilibrium due to the strategic behavior of agents. A large body of work in Computer Science has attempted to bound this inefficiency [7, 19, 29], albeit with a focus on the strategic behavior of buyers who can misreport their preferences, in settings with a single central seller. On the other hand, we consider a market with many strategic sellers and a continuum of buyers. In such a model, it is reasonable to assume that buyers behave as price-taking agents since their individual demand is small compared to the market size. Moreover, in large markets, the seller does not need to know every buyer’s value as long as they can anticipate the aggregate demand at any given price.

Our Model and Equilibrium Concept

We model the interaction between buyers and sellers as a two-stage pricing game in a networked market. Each seller controls a single good or link in the network; he can produce any quantity of this good incurring a production cost of . Every non-atomic buyer in the market wants to purchase infinitesimal amount of some path (bundle of edges) connecting a source and a sink node for which she receives a value . For the majority of this work, we will focus on single-source, single-sink networks, i.e., markets where every buyer wants to purchase a path between the same source and sink node although they may hold different values for the same.

We consider a full information game where sellers can estimate the aggregate demand at any given price. In the first stage of the game, sellers set prices on the edges and in the second stage buyers buy edges along a path. For any seller , if at a price of per unit amount of the good, a population of buyers purchase the good, then the profit is . The buyer’s utility is minus the total price paid. A solution is said to be a Nash Equilibrium if (i) Every buyer receives a utility maximizing bundle, i.e, she purchases the cheapest available path as long as its price is at most , (ii) No seller can unilaterally change his price and improve his profit at the new allocation (which depends on how many buyers purchase the good at the new prices).

Bertrand Competition with Monopolies

Our two-stage game is essentially a generalization of the classic model of competition proposed by Bertrand where sellers fix prices and buyers choose quantities to purchase. Bertrand’s model has been extensively studied in settings where all the items are substitutes[10, 22, 27]), a common theme being that perfect competition leads to socially optimal outcomes.

In combinatorial markets such as ours, however, inefficiencies arise mainly due to the monopolizing power held by some sellers, i.e., their items are not substitutable. In fact, as we show in Example D, even a monopoly in a single-link market can improve its profit from the Walrasian outcome by raising prices, leading to a loss in social welfare. Our contribution is breaking down the dependence of efficiency on network topology into a single parameter : the number of monopolies simultaneously operating in the market.

Our work is most closely related to the model of Bertrand Competition in Networks with supply limited sellers studied in [18] and later in [17]. Our model is more general as the convex production costs that we consider strictly generalize limited supply. The behavior of Bertrand Networks with seller costs was posed as an open question in [18]. We address this question by extensively applying techniques from the theory of minimum-cost flows. The above paper also considered the efficiency of such markets and showed that in the worst case the equilibrium solution can be arbitrarily worse than the social optimum. We provide a more nuanced understanding of efficiency and characterize the loss in welfare as a function of the number of monopolies () for a wide spectrum of demand functions. Our main result is that for a large class of reasonable demand functions, the loss in efficiency is at most a factor from the optimum solution. We interpret this as a positive result for two reasons,

- 1.

-

2.

Although a market may consist of a large number of distinct goods, it is reasonable to expect that the number of sellers independently monopolizing the market may be limited. Our bound depends only on such sellers; it is one of very few results interpolating between perfect competition and complete monopoly structure.

The Inverse Demand Function In this work, our primary focus will be on single-source single-sink networks where every buyer has a different value , although we do look at more general models in Sections 5 and 6. In large markets, it is reasonable to assume that sellers know exactly how many buyers value the - path at or more. Formally, we define an inverse demand function such that for any , implies that exactly amount of buyers value the path at or larger. Inverse demand functions are extremely common in Economics literature and provide a direct method to relate buyer demand and welfare in large markets, i.e., total value derived when buyers receive the good is .

1.1 Our contributions

Our objective in this paper is to characterize the quality of equilibrium in terms of the demand and network structure, and specifically show the effect of monopolies on efficiency. Therefore, all our efficiency bounds depend only on the number of monopolies which is equivalent to the number of edges present in all - paths. Note that we define efficiency to be the ratio of the optimum social welfare of the market to that at equilibrium. We make no assumptions on the graph structure and sellers’ cost functions other than convexity, which is the standard way to model production costs in literature.

Single-Source Single-Sink Networks

Our first results concern existence and uniqueness. We show that:

-

1.

There exists a Nash Equilibrium Pricing in every market where the inverse demand has a monotone ‘price elasticity’. (MPE functions, see Appendix A for details). This is a very natural assumption, which is obeyed by most of the demand functions considered in the literature.

-

2.

Our existence proof is constructive: we characterize both the equilibrium prices and the allocation and show how to compute it efficiently.

-

3.

The equilibrium that we construct satisfies several desirable properties including fairness and Pareto-optimality, and it is reasonable to expect this equilibrium to arise in practice. In fact, although there may exist multiple equilibria, ours is the unique equilibrium that is robust or resilient to small perturbations, i.e., it strictly dominates all neighboring solutions.

Therefore, we bound the efficiency of this solution.

Efficiency for general classes of demand functions

Our main contribution is showing that for a large class of demand functions, the efficiency drops only linearly as the number of monopolies increases. In particular, we prove the following

-

When all buyers have symmetric valuations (uniform demand), there exists Nash Equilibrium Pricing maximizing social welfare.

-

If the inverse demand function has a monotone hazard rate (MHR), the loss in efficiency at equilibrium is bounded by a factor of .

-

When is concave (a subset class of MHR functions), the efficiency loss is .

These efficiency bounds are all tight. Both concave and MHR inverse demand assumptions are quite general and include many popular demand functions (see Section A for details and examples).

Filling the gaps: Efficiency for specific demand functions

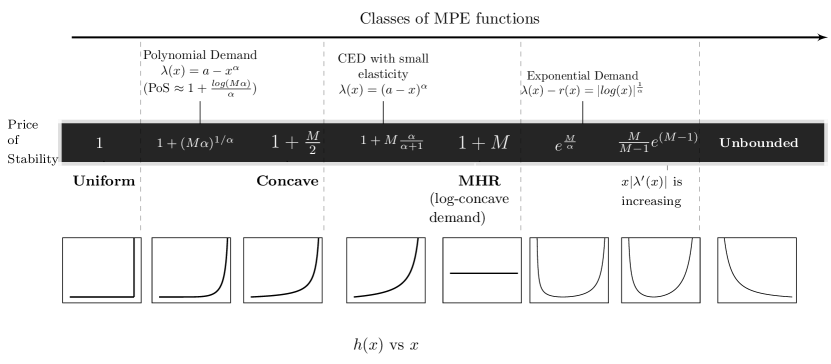

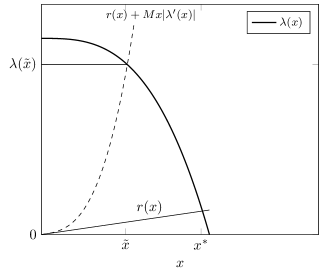

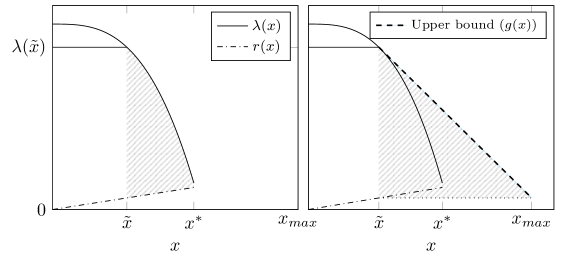

We also come close to characterizing the efficiency for all demand functions obeying the MPE condition. This characterization is summarized in Figure 1. This result is also useful because some of the special classes of functions considered here capture buyer demand in some specific applications in the real world. For instance, in highly inelastic markets (eg. electricity market), the efficiency is close to and in settings with concave but polynomial demand, the efficiency only drops logarithmically with .

The main conclusion to draw from this is that the presence of monopolies does not completely destroy efficiency: it crucially depends on the properties of the demand curve and the number of these monopolies. We supplement this result by showing that in several settings without any monopolies, there exist welfare-maximizing Nash Equilibrium. This generalizes Bertrand’s classic maxim of ‘competition causes efficiency’ to combinatorial markets. Finally, we also generalize our results to markets that do not have a graph structure, i.e, buyers may desire arbitrary bundles. All our results extend to this setting with one difference: is the number of sellers with ‘monopoly-like’ power at equilibrium. This may include sellers who are not monopolies in the traditional sense as their items do not belong to all bundles.

Multiple-Source Networks We provide a first step towards understanding efficiency in multiple-source networked markets by tackling a question of special interest: what conditions cause equilibrium to be fully efficient in such markets? We show that even when buyers desire different paths, as long as the network has a series-parallel structure and no monopolies, equilibrium is efficient. In contrast, without the series-parallel topology, even simple networks with no monopolies may have inefficient equilibria. We also show that the equilibrium is optimal if the buyer demand is fully elastic, or if every buyer has a ‘last-mile monopoly’ (See Section 6).

1.2 Related Work

Price Competition with Multiple Sellers. As mentioned earlier, our model generalizes previous papers on Bertrand competition in networks, especially [18] and [17], which showed worst case bounds on efficiency. As our model is more general than theirs, we cannot hope to do better over all instances, however we show that for many important demand functions this inefficiency is bounded. Nevertheless some of our results (specifically Theorem 4.4) are essentially generalizations of results from [17]. Moreover, the behavior in markets with production costs may be quite different from that in supply-limited markets as illustrated in Claim 6.1.

Another closely related model that also considers price competition was studied in [8]. They show that when there are multiple sellers but a single buyer, equilibrium allocations are efficient. Although we consider large markets, our Theorem 5.2 is similar in spirit to their result. Our main results, however, are for more complex demand functions, which are not considered in that paper.

The negative results in [18] and [17] have led some researchers to consider more sophisticated pricing mechanisms and other notions of equilibrium: see [32, 21, 34]. For example, [32] and [21] consider non-linear pricing, where the unit price of a good increases with demand. While complex pricing mechanisms do sometimes lead to improvement in efficiency, it imposes additional complications on the buyers as they now have to anticipate the change in price due to the behavior of other buyers. Thus even though fixed pricing (as we consider) is more natural, its effects are not really well-understood beyond the fact that competition leads to better outcomes and monopolies cause a loss in welfare. Our work captures both these maxims, but attempts to provide additional insight on the structure and quality of equilibrium.

Work such as [3, 2] has also considered two-sided markets where buyers pay the price on each edge, but also incur a cost due to the congestion on the edge; such settings are essentially a combination of the type of market we consider and the classic selfish routing games [37]. Unfortunately, most of the results in this settings are only known for simple structures such as parallel links or parallel paths. One exception is [36], which considers a unique one-sided model where the routing decisions are taken locally by sellers and not buyers as in our paper. They show that in the absence of monopolies, local decisions by sellers can result in efficient solutions.

Combinatorial Auctions with a Single Seller. Algorithmic Game Theory has also focused on Nash Equilibria of games derived from market mechanisms with strategic buyers and a single centralized seller [7, 19, 29]. The motivation in such papers is complementary to ours, to bound the efficiency loss due to non-price taking buyers. In addition, there has been a surge in the field of envy-free monopoly pricing [12, 26], two-stage games where all the items are owned by a single seller.

Finally, our two-stage game bears some similarity to first price procurement or path auctions (see [30, 35] and the references therein). Such auctions are very useful for modeling competition between sellers, but usually ignore the buyer side of the market by assuming that there is a single buyer who wants to purchase exactly one bundle (instead of having some price-dependent demand). Contrary to our setting, path auctions become uninteresting in the presence of monopolies; existing work has mostly focused on concepts like frugality [30, 35] and not social welfare.

2 Definitions and Preliminaries

An instance of our two-stage game is specified by a directed graph , a source and a sink , an inverse demand function and a cost on each edge. There is a population of infinitesimal buyers; every buyer wants to purchase edges on some - path and amount of buyers hold a value of or more for these paths. A buyer is satisfied if she purchases all the edges on some path connecting and and is indifferent among the different paths.

Equivalently, we could consider a single atomic buyer with demand for units such that is her value for a total of units of the bundles corresponding to - paths. We define to be the number of monopolies in the market: an edge is a monopoly if removing it disconnects the source and sink. We make the following standard assumptions on the demand and the cost functions.

-

1.

The inverse-demand function is continuous on and non-increasing. The latter assumption simply means that the total demand should not increase if sellers increase their price.

-

2.

is non-decreasing and convex , a standard assumption for production or congestion costs. Moreover, is continuous, twice differentiable, and its derivative satisfies . We relax these assumptions in Section 5.

Nash Equilibrium Pricing. A solution of our two-stage game is a vector of prices on each item and an allocation or flow of the amount of each - path purchased, representing the strategies of the sellers and buyers respectively. The total flow or market demand is equal to the number of buyers with non-zero allocation , where is the set of - paths. We can also decompose this flow into the amount of each edge purchased by the buyers (). Given such a solution, the total utility of the sellers is and the aggregate utility of the buyers is . The total social welfare is simply , i.e., prices are intrinsic to the system and do not appear in the welfare.

We now formally define the equilibrium states of our game. An allocation is said to be a best-response by the buyers to prices if buyers only buy the cheapest paths and for any cheapest path , . That is, buyers act as price-takers and any buyer whose value is at least the price of the cheapest path will purchase some such path. A solution is a Nash Equilibrium if is a best-response allocation to the prices and, if the seller unilaterally changes his price from to , then for every feasible best-response flow for the new prices, seller ’s profit cannot increase, i.e., . Our notion of equilibrium is quite strong as the seller does not have to predict exactly the resulting flow: for every best-response by the buyers, the seller’s profit should not increase.

Classes of inverse demand functions that we are interested in

We now define some classes of demand functions that we consider in this paper. For the sake of notational convenience, we assume that the inverse demand function is continuously differentiable, and thus is well-defined (and not positive as is non-increasing). However, all our results hold exactly even without this assumption (see Section 5). The reader is asked to refer to Appendix A for additional discussion and interpretation of each class of functions and other related economic concepts.

- Uniform buyers:

-

for . In other words, a population of buyers all have the same value for the bundles.

- Concave Demand:

- Monotone Hazard Rate (MHR) Demand:

-

is non-increasing or is non-decreasing in . This is equivalent to the class of log-concave functions [4] where is concave, and essentially captures inverse demand functions without a heavy tail. Example function: .

- Monotone Price Elasticity (MPE):

-

is a non-decreasing function of which tends to zero as . This is equivalent to functions where the price elasticity of demand is non-decreasing as the price increases. Price elasticity measures the responsiveness of the market demand over its sensitivity to price, and exactly equals using our notation.

Each class of demand function defined above strictly contains all the classes defined previously, i.e., Uniform Demand Concave MHR MPE.

Min-Cost Flows and the Social Optimum: Since an allocation vector on a graph is equivalent to a - flow, we briefly dwell upon minimum cost flows. Formally, we define to be the cost of the min-cost flow of magnitude and , its derivative, i.e., . Both the flow and its cost can be computed via a simple convex program given a graph and cost functions. Clearly, is non-decreasing since increasing the amount of flow can only lead to an increase in cost, as the production costs are non-decreasing. We prove in the Appendix that:

Proposition 2.1.

is continuous, differentiable, and convex for all .

It is also easy to see from the KKT conditions that for a min-cost flow , we have for any path with non-zero flow (for a full proof see the Appendix). Given an instance of our game, the optimum solution is an allocation or flow which maximizes the social welfare . Since the buyers’ utility depends only on the magnitude of the flow, welfare is maximized when the flow is of minimal cost. The optimum solution therefore maximizes and must satisfy the following condition:

Proposition 2.2.

The solution maximizing social welfare is a min-cost flow of magnitude satisfying . Moreover, unless .

3 Existence, Uniqueness, and Computation of Equilibrium Prices

In this section, we show that for a large class of demand functions, we are always guaranteed the existence of Nash Equilibrium. Although there may be multiple equilibria in general, we show that some of these are highly unrealistic. The equilibrium that we consider, on the other hand, satisfies several desirable properties and is the unique solution that is resilient to small perturbations. Finally, we show how to efficiently compute this unique equilibrium.

We now show our first result that reinforces the fact that even in arbitrarily large networks (not necessarily parallel links), competition results in efficiency. This result is only a starting point for us since it is the addition of monopolies that leads to interesting behavior. We only sketch our proofs here, full proofs are located in the Appendix.

Claim 3.1.

In any network with no monopolies (i.e, you cannot disconnect , by removing any one edge), there exists a Nash Equilibrium maximizing social welfare.

(Proof Sketch) Consider the optimum solution and price every edge at . Notice that if any edge increases its price, it stands to lose all of its flow since buyers will have other cheaper paths. No edge can improve profits by pricing below marginal cost because . ∎

We remark that our notion of a “no monopoly” graph is weaker than what has been considered in some other papers [21, 36] and therefore, our result is stronger. We are now in a position to prove our main existence result. Unlike [18], our results do not depend on how much the buyers value the goods (no assumption on how large can be). The result is also constructive, we are able to characterize the equilibrium prices and properties of the demand function at equilibrium.

Theorem 3.2.

For any MPE demand function , there exists a Nash equilibrium.

(Proof Sketch) We define a simple pricing rule for a min-cost flow of any given magnitude and an instance with monopolies. The rule is fair from the monopolies’ perspective: first every edge is priced at its marginal and then the remaining slack is divided among the monopolies. The rest of the proof lies in showing that that obeys the conditions of Corollary 3.3 and that no seller can increase or decrease his price to improve profits when the following prices are used.

Corollary 3.3.

For any inverse demand function belonging to the class MPE, we are guaranteed the existence of a Nash Equilibrium with a min-cost flow of size such that,

-

1.

The prices obey the pricing rule above.

-

2.

Either or , the optimum solution.

Before analyzing the efficiency of equilibrium, it is important to address the question of what equilibria are likely to be formed. In markets such as ours, it does not make sense to provide a blanket bound on all stable solutions since some of these are highly unrealistic. In contrast, the solution obeying Corollary 3.3 is the unique solution that satisfies useful desiderata, motivating us to study its efficiency in the following sections. We begin by illustrating some of the “unreasonable” equilibria that exist even in the simplest of markets.

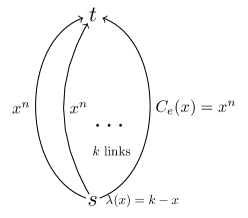

-

Trivial Equilibrium [17]: In any instance where all paths have length at least , we can easily show the existence of a Nash Equilibrium with zero flow. Suppose that in the example of Figure 2(a), every seller sets a really high price (say larger than ). No buyer can afford the bundle, moreover, no seller can unilaterally lower his price and induce any flow.

-

Non-Competitive Equilibrium: Consider the parallel network shown in Figure 2(b). There exists an equilibrium that has non-zero flow but closely mirrors trivial equilibria. Assume for concreteness that and . Consider the solution where each edge is priced at (say) and receives units of flow. No edge can lower its price because then it would receive the entire 2 units of flow, which is too expensive to transit. This solution is Pareto-dominated by the optimum equilibrium in Claim 3.1 since every seller’s profit is larger in the latter. As , this violates the well-established idea that perfect competition causes efficiency [28, 20].

Motivated by these, we now define some natural properties that one desires from market equilibrium. All of these are obeyed by the equilibrium from Corollary 3.3. We formally prove this fact in the Appendix.

-

1.

(Non-Trivial Pricing): Every edge that does not admit flow must be priced at , or more generally .

-

2.

(Recovery of Production Costs): Given an equilibrium , every item’s price is at least .

This property induces a basic fairness criteria for the seller: the seller’s price for any item is at least the cost of producing it.

-

3.

(Pareto-Optimality): A Pareto-optimal solution over the space of equilibria is an equilibrium solution such that for any other equilibrium, at least one agent prefers the former solution to the latter. Pareto-Optimality is often an important criterion in games with multiple equilibria; research suggests that in Bertrand Markets, Pareto optimal equilibria are the solutions that arise in practice [14].

-

4.

(Local Dominance): Given an equilibrium , no seller’s profit should strictly increase when a small fraction of buyers shift their flow from one path to another. The essence of this property is that the solution is resilient against small buyer perturbations. By definition of an equilibrium, no seller can change his price. However, at the same price, a seller may be able to attract a small fraction of buyers towards his item. If the resulting solution is strictly preferred by the seller, then it indicates that the original equilibrium is not robust. Local dominance provides a strong guarantee: that an equilibrium dominates all neighboring solution along every single component.

We now show that for any given instance with strictly monotone demand and non-zero production costs, either all equilibria are optimal or the equilibrium in Corollary 3.3 is the unique non-trivial equilibrium with that satisfies local dominance. From the perspective of efficiency, this means that we only have to bound the welfare of a single equilibrium solution. In cases where this is not true, all equilibrium solutions are optimal. In addition to uniqueness, we also show that the above solution can be computed efficiently by means of a simple binary search followed by a single min-cost flow computation. As always in the case of real-valued settings (e.g., for convex programming, other equilibrium concepts, etc), “computing” a solution means getting within arbitrary precision of the desired solution; the exact solution may not be computable efficiently or even be irrational.

Theorem 3.4.

For any given instance with strictly monotone MPE demand and non-zero production costs, we are guaranteed that one of the following is always true,

-

1.

There is a unique equilibrium that obeys Local Dominance and Non-Trivial Pricing, or

-

2.

All equilibria that satisfy Local Dominance and Non-Trivial Pricing maximize welfare.

As is the case with our uniqueness result, in most systems, a certain degree of strong monotonicity is essential to show uniqueness. We now focus on understanding the quality of these equilibrium solutions, in comparison with the social optimum.

4 Effects of Demand Curves and Monopolies on Efficiency of Nash Equilibrium

In this paper, we are interested in settings where approximately efficient outcomes are reached despite the presence of self-interested sellers with monopolizing power over the market. While for general functions belonging to the class MPE, the efficiency can be arbitrarily bad, we show that for many natural classes of functions it is relatively small, even in the presence of a limited number of monopolies. The proofs can be found in Appendix D.

We begin with the special case of buyers with uniform demand, i.e., every buyer in the continuum values the - paths at the same value . In this case, the inverse demand function becomes for and otherwise. We show that for buyers with uniform demand, an equilibrium maximizing social welfare. It is however, interesting to note that this solution may not necessarily coincide with the Walrasian Equilibrium, an example of the same is provided in the Appendix.

Theorem 4.1.

Every instance with uniform demand buyers admits an efficient Nash Equilibrium.

(Proof Sketch) The essence of the proof lies in computing the socially optimal flow, pricing every edge at the marginal and dividing the slack evenly on the monopolies. This way the total price is and no edge can increase its price and as long as , reducing the price serves no purpose. When , from Proposition 2.2, there is no slack so every edge is priced at its marginal cost.∎

Main Result: MHR Demand and Concave Demand

We now show our main result that the efficiency drop is a factor when the inverse demand function has a monotone hazard rate. As mentioned previously, these correspond exactly to the case when the inverse demand function is log-concave, i.e., is concave. Log-concavity is a very natural assumption on the inverse demand function and it is not surprising to see that such functions have received considerable attention in Economics literature [4, 9, 33]. Finally, note that being concave is a special case of log-concavity. For this class of functions, we obtain an improved bound of on the efficiency. The extremely popular linear inverse demand function falls under this class.

Theorem 4.2.

The social welfare of Nash equilibrium from Section 3 is always within a factor of:

-

of the optimum for concave .

-

of the optimum for Log-concave (i.e., MHR) .

Both these bounds are tight, i.e., there exist instances where the optimum solution has a welfare that is exactly times the Nash Equilibrium for MHR demand and times that of the equilibrium for concave demand.

(Proof Sketch for the bound on MHR functions)

The proof relies crucially on our characterization of equilibria. Showing that an equilibrium satisfying several nice properties and Corollary 3.3 was the hard part. Armed with these results, the rest of the efficiency proof becomes extremely intuitive. For MHR functions, the proof hinges on an interesting claim (that may be of independent interest) linking the welfare loss at equilibrium to the profit made by all sellers. Specifically, our key claim is that ‘the loss in welfare is at most a factor times the total profit in the market at equilibrium’. In addition, it is also not hard to see that in any market, the profit cannot exceed the total social welfare of a solution.

Why is this property useful? Using profit as an intermediary, we can now compare the welfare lost at equilibrium to the welfare retained. This implies that the welfare loss cannot be too high because that would mean that the profit and hence the welfare retained is also high. But then, the sum of welfare lost retained is the optimum welfare and is bounded. Therefore, once we bound the welfare lost at equilibrium, we can immediately bound the overall efficiency. Our key claim is,

where is the payment made by every buyer, is the amount of buyers in the equilibrium solution and , in the optimum. The integral in the LHS can be rewritten as . Now, we apply some fundamental properties of MHR functions () and show in the appendix that for all , the following is true,

The final equality comes from our equilibrium characterization in Corollary 3.3. Therefore, we have,

| ( is non-increasing and ) | ||||

The total payment on any path must exactly equal (See Equilibrium Def.).

We reiterate here that both the results in the theorem make no assumption on the graph structure or cost functions other than the ones mentioned in Section 2. It is reasonable to assume that even in multi-item markets where consumers may desire large bundles, the number of purely monopolizing goods is not too large: in such cases the equilibrium quality is high.

Filling the gaps: Other classes of Demand Functions

The above classes of inverse demand functions encapsulate many different types of functions, but there is a large gap between an efficiency factor of 1 and that of , for example. We attempt to interpolate between our bounds above by considering two very specific (but important and commonly studied) classes of functions defined below, and obtain the following results (see Appendix D.3 for proofs).

Theorem 4.3.

-

1.

Let denote functions of the form for any and . For , the efficiency is at most . When , this quantity is approximately .

-

2.

Let denote functions of the form for any and . For , the efficiency is at most for .

Discussion

-

1.

Polynomially decreasing inverse demand functions such as the ones in are extremely common in papers that assume concave demand, e.g, in [13]; the special case when is popularly referred to as “linear inverse demand functions” in the literature [1]. It is interesting to note that the efficiency drops only logarithmically with for these functions as opposed to linearly in the general case.

-

2.

CED stands for constant elastic demand (see for Appendix A), where the elasticity of demand is and denotes how much the demand changes with the changes in price. The main application of our result is showing that when the demand is relatively inelastic, the efficiency can still be much better than . It is well-known that several essential commodities have such a relatively inelastic demand: only a large increase in price can lead to a lot of consumers dropping out. For instance, the elasticity of the market for electricity is believed to be somewhere around [24]; our results would guarantee a Nash equilibrium within a factor of of optimum for such functions.

By varying in all the functions above, we can interpolate between our results in Theorem 4.2, and quantify how the quality of equilibrium changes as the functions become less concave. For the sake of completeness, we also consider functions that do not have a monotone hazard rate but still fall under the class MPE. Perhaps most important among these seem to be the class of MPE functions where the quantity is non-decreasing. This class of functions was considered in [17], where it was shown that the efficiency loss can be as bad as . We generalize their results to markets with cost functions, and further are able to slightly improve upon the bound in that paper.

Claim 4.4.

If has non-decreasing, then the loss in efficiency for any instance is at most .

Finally, we are also able to characterize the efficiency spectrum between linear and exponential. Our next result shows that for an interesting class of functions with logarithmic inverse demand, the efficiency is . Such demand functions are reasonably popular (see [13, 39]) and are considered to represented actual buyer demand in the transportation industry [23].

Claim 4.5.

Let denote the demand and cost functions which can be represented as for , and . Then the efficiency is at most for .

5 Looking beyond Graphical Markets: More General Models

All the results above hold for the somewhat limited case in which the market structure is that of a graph. However, what if all the buyers still have an identical set of valid bundles (with each buyer possibly having different valuations), but this set did not correspond to the set of - paths in a graph? This case can become a lot more intractable, since there can be sellers which are not true monopolies (they do not belong to all bundles in ), but still hold much more power than other sellers. Similar to [18], this can be formalized through the notion of virtual monopolies: a seller is a virtual monopoly for an allocation if is part of every bundle which is allocated a non-zero amount in .

Formally, consider a market with a set of goods. Every buyer desires one bundle from a subset of valid and is indifferent as to which bundle she gets. In addition, we also drop the requirement that for every edge. In a sense, this assumption helped maintain competition. Consider a market with two parallel links and but is much larger than . It is clear that if the demand is not too high, then has the power of a monopoly here as the entry cost for is just too high. Now, we can generalize our results as follows:

Theorem 5.1.

The proof is non-trivial and does not follow from our previous techniques in Section 3. In fact we consider a new ascending price algorithm that generalizes the pricing rule mentioned in the proof of Theorem 3.2. The algorithm for setting prices at equilibrium may be of independent interest.

Discussion. While in the worst case, the number of virtual monopolies can be as large as the number of sellers, for markets with reasonable (but not perfect) competition it is likely to be a lot less.

Uniform Demand Buyers with General Combinatorial Valuations

So far the buyer valuation functions have all had a certain structure: the buyer has a set of desired bundles and cares only about these bundles. What if instead all buyers had a single monotone valuation function that captures how much they value the set of items . We generalize both our Theorem 4.1 and a result in [8] and show that for uniform demand buyers with arbitrary combinatorial valuations, there exists an efficient Nash Equilibrium.

Formally, consider a monotone valuation function defined for every . Every buyer in the continuous population of receives a value of from set . Then we show the following,

Theorem 5.2.

In any setting where uniform buyers have arbitrary combinatorial valuations, there exists an efficient Nash Equilibrium.

6 Multiple-Source Networks and Efficient Equilibrium

6.1 Single-Source Networks: When does competition lead to complete efficiency?

We conclude our findings for single-source single-sink networks by showing that when the demand is ‘somewhat elastic’ and sellers are limited in supply, there exists an efficient Nash Equilibrium. This is an interesting special case for capacitated networks not considered in [18] and [17]. Surprisingly, for the exact same demand but with production costs, we show in the Appendix (Claim D.6) that the equilibrium can be arbitrarily inefficient. Therefore, this result reiterates our claim that the behavior in networks with general production costs can be quite different from the special case with capacities.

Formally, consider a networked market where every edge has a capacity of . This is a special convex cost function where if and otherwise. The ‘somewhat elastic’ demand functions that we consider have the form where and . The exact value of depends on .

Claim 6.1.

For any single-source single-sink network with edge capacities, monopolies, and demand function , there exists an efficient Nash Equilibrium as long as .

6.2 Multiple-Source Networks

We now move on to more general networks where different buyers have different - paths that they wish to connect and the demand function can be different for different sources. Unfortunately, our intuition from the previous sections does not carry over. As we show in Appendix F.1, Nash equilibrium may not exist even for instances with two sources and a single sink. Perhaps more surprisingly, we give relatively simple examples in which perfect efficiency is no longer achieved, even with complete absence of monopolies! Nevertheless, we prove that for some interesting special cases, fully efficient Nash equilibrium still exists even when buyers desire different sets of bundles. In particular, we believe that our result on series-parallel networks is an important starting point for truly understanding multiple-source networks.

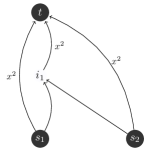

We begin by showing that even in a simple network with two sources, a common sink and no monopolies, there is no equilibrium maximizing social welfare.

Claim 6.2.

There exists an instance with two sources, one sink, and no monopoly edges for either source, where all equilibria are inefficient.

(Proof Sketch)

Consider the instance shown in the figure, where the cost function on each edge is given as the edge weight. Suppose that has demand and has . At the unique optimum point sends a flow of on its direct link (edge ) to the sink and sends units of flow, one on each of its paths.

Assume by contradiction that prices stabilizing the optimum flow. For , and so this must be the price on . On the other hand, is carrying unit of flow at a cost of and therefore, for non-zero profit, its price must be at least one. But this means that is virtually a monopoly for . Therefore, if increases its price to , its profit will also strictly improve. This contradicts the assumption that the original solution is stable. ∎

Despite this discouraging result, we show that there are important special cases where equilibrium allocations do maximize social welfare. We first consider the case when all the buyers desiring to connect a given source-sink pair have uniform demand, i.e., we consider a multiple-source, multiple-sink network where every pair has a buyer demand for and zero otherwise. For this, we show conditions on both the demand and network topology that lead to efficient equilibria.

Claim 6.3.

There exists efficient equilibrium in multiple-source multiple-sink networks with uniform demand buyers at each source if one of the following is true

-

1.

Buyers have a large demand and production costs are strictly convex.

-

2.

Every source node is a leaf in the network.

The second case commonly arises in several real-world networks including Internet, postal, and transportation networks [38]. The commonality between these physical networks is that there exists a well-connected, easily-accessible central network that links major hubs, but the last-mile between the hub and the final user is often controlled by a local monopoly and thus the source is a leaf. It is not feasible for firms to compete at the last-mile due to the heavy infrastructure costs and minimal returns.

Multiple-Source Single-Sink Series-Parallel Networks In some sense, Claim 3.1 embodies the very essence of the Bertrand Paradox, the fact that competition drives prices to their marginal cost. So it is perhaps surprising that this does not hold in general networks as illustrated by Claim 6.2. However, we now show that for a large class of markets which have the series-parallel structure, the absence of monopolies still gives us efficient equilibria. Series-Parallel networks have been commonly used [21, 32] to model the substitute and complementary relationship that exists between various products in arbitrary combinatorial markets. We conjecture that this result is tight in the sense that no larger class of graphs without monopolies have this property.

We define a multiple-source single-sink graph to be a series-parallel graph if the super graph of the given network obtained by adding a super-source and connecting it to all the sources has the series-parallel structure. The notion of “no-monopolies” for a complex network has the same idea as a single-source network: there is no edge in the graph such that its removal would disconnect any source from the sink. We are now in a position to show our main result extending the Bertrand Paradox to arbitrary series-parallel graphs.

Theorem 6.4.

A multiple-source single-sink series-parallel network with no monopolies admits a Nash Equilibrium that has the same social welfare as the optimum solution for any given instance where all edges have .

7 Conclusions and Future Work

In this work, we considered large, decentralized markets with production costs, where Walrasian Equilibrium may not be an appropriate solution concept. Our main focus is on single-source single-sink network markets where our results provide significant understanding of how monopolies affect the efficiency of the market equilibrium. In particular, our main contribution is that as long as the inverse demand obeys a natural condition (monotone hazard rate), the efficiency is at most . This result relies crucially on the characterization of the equilibrium prices and allocation that we provide. Our results also hint that studying the inverse demand as opposed to direct demand provides a better understanding of welfare properties. In particular Figure 1 indicates that efficiency seems to depend on the hazard rate of the inverse demand. A deeper understanding of welfare as a function of a single parameter that captures most demand functions is an obvious future step.

We also generalize our model in two directions: non-networked markets where buyers desire arbitrary bundles and multiple-source markets where different buyers desire different bundles. For the latter case, our results provide a modest but important first step in understanding the factors controlling efficiency in more complex networks. The study of general multiple-source networks with some structure (trees, series-parallel networks) that builds on existing work appears to be the most promising future direction.

References

- [1] Melika Abolhassani, Mohammad Hossein Bateni, MohammadTaghi Hajiaghayi, Hamid Mahini, and Anshul Sawant. Network cournot competition. In Proceedings of the 10th Conference on Web and Internet Economics (WINE), pages 15–29. Springer, 2014.

- [2] Daron Acemoglu and Asuman Ozdaglar. Competition and efficiency in congested markets. Mathematics of Operations Research, 32(1):1–31, 2007.

- [3] Daron Acemoglu and Asuman Ozdaglar. Competition in parallel-serial networks. IEEE Journal on Selected Areas in Communications, 25(6):1180–1192, 2007.

- [4] Rabah Amir. Cournot oligopoly and the theory of supermodular games. Games and Economic Behavior, 15(2):132–148, 1996.

- [5] Simon P Anderson and Régis Renault. Efficiency and surplus bounds in cournot competition. Journal of Economic Theory, 113(2):253–264, 2003.

- [6] Eduardo M Azevedo, E Glen Weyl, and Alexander White. Walrasian equilibrium in large, quasilinear markets. Theoretical Economics, 8(2):281–290, 2013.

- [7] Moshe Babaioff, Brendan Lucier, Noam Nisan, and Renato Paes Leme. On the efficiency of the walrasian mechanism. In Proceedings of the fifteenth ACM Conference on Economics and Computation (EC), pages 783–800. ACM, 2014.

- [8] Moshe Babaioff, Noam Nisan, and Renato Paes Leme. Price competition in online combinatorial markets. In Proceedings of the 23rd international conference on World wide web (WWW), pages 711–722. International World Wide Web Conferences Steering Committee, 2014.

- [9] Tim Baldenius and Stefan Reichelstein. Comparative statics of monopoly pricing. Economic Theory, 16(2):465–469, 2000.

- [10] Michael R Baye and John Morgan. A folk theorem for one-shot bertrand games. Economics Letters, 65(1):59–65, 1999.

- [11] Kostas Bimpikis, Shayan Ehsani, and Rahmi Ilkiliç. Cournot competition in networked markets. In Proceedings of the fifteenth ACM Conference on Economics and Computation (EC), page 733, 2014.

- [12] Patrick Briest and Piotr Krysta. Buying cheap is expensive: Approximability of combinatorial pricing problems. SIAM Journal on Computing, 40(6):1554–1586, 2011.

- [13] Jeremy I Bulow and Paul Pfleiderer. A note on the effect of cost changes on prices. The Journal of Political Economy, pages 182–185, 1983.

- [14] Marie-Laure Cabon-Dhersin and Nicolas Drouhin. Tacit collusion in a one-shot game of price competition with soft capacity constraints. Journal of Economics & Management Strategy, 23(2):427–442, 2014.

- [15] Andrew Caplin and Barry Nalebuff. Aggregation and imperfect competition: On the existence of equilibrium. Econometrica: Journal of the Econometric Society, pages 25–59, 1991.

- [16] XM Chang, DZ Du, and FK Hwang. Characterization for series-parallel channel graphs. Bell System Technical Journal, The, 60(6):887–891, 1981.

- [17] Shuchi Chawla and Feng Niu. The price of anarchy in bertrand games. In Proceedings of the 10th ACM conference on Electronic Commerce (EC), pages 305–314. ACM, 2009.

- [18] Shuchi Chawla and Tim Roughgarden. Bertrand competition in networks. In Proceedings of the 1st International Symposium on Algorithmic Game Theory (SAGT), pages 70–82. Springer, 2008.

- [19] Ning Chen, Xiaotie Deng, Hongyang Zhang, and Jie Zhang. Incentive ratios of fisher markets. In Automata, Languages, and Programming - 39th International Colloquium, ICALP 2012, Warwick, UK, July 9-13, 2012, Proceedings, Part II, pages 464–475, 2012.

- [20] Prabal Roy Chowdhury and Kunal Sengupta. Coalition-proof bertrand equilibria. Economic Theory, 24(2):307–324, 2004.

- [21] José R Correa, Nicolás Figueroa, Roger Lederman, and Nicolás E Stier-Moses. Pricing with markups in industries with increasing marginal costs. Mathematical Programming, pages 1–42, 2008.

- [22] Krishnendu Ghosh Dastidar. On the existence of pure strategy bertrand equilibrium. Economic Theory, 5(1):19–32, 1995.

- [23] Andrew Evans. A theoretical comparison of competition with other economic regimes for bus services. Journal of Transport Economics and Policy, pages 7–36, 1987.

- [24] Massimo Filippini. Swiss residential demand for electricity. Applied Economics Letters, 6(8):533–538, 1999.

- [25] Douglas Gale. Strategic foundations of general equilibrium: dynamic matching and bargaining games. Cambridge University Press, 2000.

- [26] Venkatesan Guruswami, Jason D Hartline, Anna R Karlin, David Kempe, Claire Kenyon, and Frank McSherry. On profit-maximizing envy-free pricing. In Proceedings of the Sixteenth Snnual ACM-SIAM Symposium on Discrete algorithms (SODA), pages 1164–1173. Society for Industrial and Applied Mathematics, 2005.

- [27] Carlos Lever Guzmán. Price competition on network. Technical Report Working Papers 2011-04, July 2011.

- [28] Joseph E Harrington. A re-evaluation of perfect competition as the solution to the bertrand price game. Mathematical Social Sciences, 17(3):315–328, 1989.

- [29] Avinatan Hassidim, Haim Kaplan, Yishay Mansour, and Noam Nisan. Non-price equilibria in markets of discrete goods. In Proceedings of the 12th ACM Conference on Electronic Commerce (EC), pages 295–296, 2011.

- [30] Nicole Immorlica, David Karger, Evdokia Nikolova, and Rahul Sami. First-price path auctions. In Proceedings of the 6th ACM conference on Electronic Commerce (EC), pages 203–212. ACM, 2005.

- [31] Ramesh Johari and John N Tsitsiklis. Efficiency loss in cournot games. Cambridge, MA: MIT Lab. Inf. Decision Syst., 2005. Publication 2639., 2005.

- [32] Volodymyr Kuleshov and Gordon T. Wilfong. On the efficiency of the simplest pricing mechanisms in two-sided markets. In Proceedings of the 8th International Workshop on Internet and Network Economics (WINE), pages 284–297, 2012.

- [33] Tae-Ho Lyoo, Jongwook Jeong, Hyun-Jung Lee, and Jeong-Dong Lee. Efficient spectrum policy using real options and game theoretic methods. In The Economics of Online Markets and ICT Networks, pages 157–166. Springer, 2006.

- [34] Emerson Melo. Price competition, free entry, and welfare in congested markets. Games and Economic Behavior, 83:53–72, 2014.

- [35] Hervé Moulin and Rodrigo A Velez. The price of imperfect competition for a spanning network. Games and Economic Behavior, 2013.

- [36] Christos H. Papadimitriou and Gregory Valiant. A new look at selfish routing. In Innovations in Computer Science (ICS) 2010, Tsinghua University, Beijing, China, January 5-7, 2010. Proceedings, pages 178–187, 2010.

- [37] Tim Roughgarden. Selfish routing and the price of anarchy. MIT press, 2005.

- [38] Laurie A Schintler, Sean P Gorman, Aura Reggiani, Roberto Patuelli, Andy Gillespie, Peter Nijkamp, and Jonathan Rutherford. Complex network phenomena in telecommunication systems. Networks and Spatial Economics, 5(4):351–370, 2005.

- [39] John N Tsitsiklis and Yunjian Xu. Efficiency loss in a cournot oligopoly with convex market demand. Journal of Mathematical Economics, 53:46–58, 2014.

Appendix A The Inverse Demand Function

Our main aim in this paper is to understand the efficiency of equilibrium allocations for different types of demand. In order to characterize the structure of demand in the market, we used an inverse demand function . Intuitively, the inverse demand function gives us a value such that exactly of the non-atomic buyers hold a value of or more for the desired bundles. It is not hard to see that the total value derived by the buyers when buyers buy the desired bundles is the integral of from to . Alternatively, we could define the inverse demand function for a market with one atomic buyer with a large demand.

Atomic buyers: While we defined the model above with non-atomic buyers who each desire an infinitesimal amount of any bundle in , we could equivalently have defined the market as consisting of a single buyer with a large demand, so that this buyer’s utility is for obtaining amount of any combination of bundles in . Note that this is very different from simply assuming a single buyer who wants one unit of a good at a fixed value; properties of the utility function can greatly change the properties of the system.

Direct Demand The inverse demand function captures the price that the market can pay as a function of the total demand. Such functions are very commonly used in Economics while studying the efficiency of markets with divisible goods as they provide a simple way to relate social welfare and prices. On the other hand, in markets with several atomic buyers, it is also natural to model the distribution of demand using a ‘direct demand function’, which is essentially the inverse of the inverse demand function. Mathematically, we can represent the direct demand by a non-increasing function , such that exactly buyers hold a value of or more for the bundles.

Let us also define a quantity , which in some sense tells us the amount of buyers who who hold a value of exactly for the bundles.

We now define some commonly used quantities in terms of the direct and inverse demand functions.

-

1.

The value is the change in the value or ‘lowest-valued’ buyers when you add or remove some buyers. It is not hard to see that this is equal to at some value of . Similarly, the quantity .

-

2.

Elasticity of Demand Informally, this is the relative ‘responsiveness’ of the market over the sensitivity to price. Mathematically . The elasticity can be rewritten as a function of demand () as because as a function of is exactly equal to . The elasticity of demand is negative for the vast majority of goods.

-

3.

Constant Elasticity of Demand (CED) This represents the class of (inverse demand functions) such that the elasticity of demand is constant, i.e., for all . It known that these functions can be represented in the form of where is referred to as the elasticity of demand. When , the demand is said to highly inelastic. As , the demand becomes more and more elastic. Using some simple algebra, the same inverse demand functions for the CED case are

Relatively inelastic demand Monotone Hazard Rate Elastic Demand Usually the demand for essential commodities (food, electricity) are considered to be inelastic whereas the demand for non-essentials are somewhat elastic depending on the case.

We defined several classes of demand functions in the paper and show bounds on the efficiency for many of these classes. We now discuss each of these demand functions, their interpretations and give examples. Although for ease of presentation, we assume that is continuously differentiable, this assumption is not necessary for any of our results, as we argue in Section 5.

- Uniform buyers

-

for . In other words, a population of buyers all have the same value for the bundles. Alternatively, one or more atomic buyers exist in the market and the total amount demanded by all atomic buyers is . And each atomic buyer receives a value of for every unit of the good(s).

From a traditional Economics point of view, the quantity for .

- Concave Demand

-

is a non-increasing function of . Informally, is decreasing faster and faster as increases. This means that if it so happens that the buyers are in agreement over the value of the bundles, then more buyers are clustered around a higher price than a lower price.

This includes the popular linear inverse demand case () [1, 39] where the demand drops linearly as price increases. In this case is a constant and so changing the price always leads to the same (addition) or removal of buyers. That is buyers at every price are equally senstive to a change in price. Another example function that we examine later is concave and polynomially decreasing, i.e., for .

The classic way of representing such functions would be to consider is non-decreasing with .

- Monotone Hazard Rate (MHR) Demand

-

This is a strict generalization of Concave Demand. Mathematically, it is the class of functions where is non-increasing or is non-decreasing in . This is equivalent to the class of log-concave functions [4, 9] and essentially captures inverse demand functions without a heavy tail.

While uniformly decreasing demand (linear inverse demand, ) has been assumed more commonly due to its tractable nature, it is more likely that the elasticity of demand is not constant across different prices. Indeed different segments of the market may react differently to a change in price. MHR functions capture a very interesting class of such functions where the responsiveness of a market relative to the value of the buyers is non-decreasing. More concretely if at some price , an increase of in the price leads to a reduction in number of buyers. Then at a price , in order to make the same number of consumers () drop out, the increase in price has to be at least . In simple terms, the market cannot be ‘overly sensitive’ at smaller prices compared to its sensitivity at a larger price. Example function: .

Such functions denote the case where is non-decreasing with .

- Monotone Price Elasticity (MPE)

-

is a non-decreasing function of which tends to zero as . This is equivalent to functions where the price elasticity of demand is non-decreasing as the price increases. Notice that . So since is non-decreasing, this means that is also non-decreasing with . If we look at the absolute value of , it is decreasing in , which means that the market cannot be too elastic at a lower price as compared to a higher price. Or buyers who value the item more are more sensitive.

While uniformly decreasing demand (linear inverse demand, ) has been assumed more commonly due to its tractable nature, it is more likely that the elasticity of demand is not constant across different prices. Indeed different segments of the market may react differently to a change in price. MHR functions capture a very interesting class of such functions where the responsiveness of a market relative to the value of the buyers is non-decreasing. More concretely if at some price , an increase of in the price leads to a reduction in number of buyers. Then at a price , in order to make the same number of consumers () drop out, the increase in price has to be at least . In simple terms, the market cannot be ‘overly sensitive’ at smaller prices compared to its sensitivity at a larger price.

Each class of demand functions contains all the previously defined classes, i.e., Uniform Concave MHR MPE. We also extend these definitions to functions which may not be differentiable everywhere. However, it is well known that if the is monotone, then its derivative exists ‘almost everywhere’. In this case, we define the MPE class to be obey monotonicity where the derivative is defined and at any where it is not defined, we require

We also consider specific demand functions that have more specific forms. for which are concave but essentially more ‘concave’ than simple linear inverse demand. , which belong to the class MHR but are relatively more inelastic. Notice that linear inverse demand functions form some sort of a border between these two classes.

Finally, we look at functions of the form where . Ignoring the structure of the cost function, this essentially means that the direct demand is exponentially decreasing.

Appendix B Min-Cost Flows

In this section we prove Proposition 2.1, establishing the properties of the min-cost flow value .

Flow Allocations: We now discuss flow allocations, which we use only in our proofs. Given a flow whose total magnitude is , we represent the flow by an allocation vector , such that the flow on edge is for . Then, we can define the total cost as a function of just , i.e., for a fixed allocation rule . We also define a total differential cost function, the marginal cost of sending additional flow according to a given allocation.

We are now in a position to prove some properties of the min-cost function . Intuitively, it also seems like must be continuous since increasing the flow by a small amount should not lead to a large increase in the cost. We begin by showing this formally.

Proposition B.1.

is continuous .

Proof.

Since is a non-decreasing function, we know the following inequality must hold: . Let , i.e., is the optimal allocation for the min-cost flow of value . Then for any , , simply because is the cost of the best allocation, which includes the allocation . Taking the limit on both sides as tends to zero, we get that cannot be any larger than . Thus we get that for all .

Moving on to the other limit, suppose that . For some sufficiently small , let be the min-cost flow corresponding to and be the flow corresponding to . Consider the flow . Clearly, this is a feasible flow of magnitude . Moreover, since is convex, we know that . The last inequality holds because for some sufficiently small , the convex combination lies in between and . This is a contradiction since is the minimum cost of a flow of magnitude . Thus is continuous at . ∎

Recall the derivative of the min-cost flow . Although is continuous, it is not clear that it is differentiable, so we define the appropriate left and right hand derivatives , according to the first principles. We now show that these two are the same. Then, we show that the derivative is continuous and non-decreasing in .

Proposition B.2.

is differentiable for all .

Proof.

Recall the differential cost function for a fixed allocation . Since is differentiable, then is continuous. More precisely, .

Let denote the optimal flow allocation for a flow of size (i.e., ). Then, we know that

From the above definitions, we see that is always greater than . This is true because since the former is the min-cost flow of that magnitude, and the latter may be using a suboptimal allocation. Similarly, , so we have . This gives us our first bound,

Now, suppose that . This would imply that

Thus there exists a sufficiently small such that which implies .

Let the flows corresponding to and be and respectively. Once again, take the average flow . This flow has a magnitude of and its cost . However, this is a contradiction since no feasible flow of magnitude can have a cost less than . So we conclude that . So finally, we have

Moreover, since all are differentiable, then is always finite, thus proving the desired claim that always exists and is continuous. ∎

Proposition B.3.

is convex.

Proof.

Consider arbitrary flow values and , and let . Suppose to the contrary that . Now consider the flow vector where are the flow vectors corresponding to the minimum cost flows at , respectively. Clearly has magnitude . Moreover since is convex, This is a contradiction as no flow of magnitude can have a cost less than , and so must be convex. ∎

Now that we have a good understanding of the min-cost function , we show that if we take the min-cost flow at any value , the cost of sending an additional infinitesimal flow equals the marginal cost of any one path with flow on it. First we show some simple lemmas that yield some insight on the allocation on the min-cost flow.

Lemma B.4.

For any given , let be the minimum cost flow vector and be any two paths with non-zero flow in . Then, . If is a path with no flow and has non-zero flow in the minimum cost flow, then .

Proof.

The lemma can be formally proved using the Karush-Kuhn-Tucker conditions for the min-cost flow optimization program. However, observe any cost minimizing flow must also be a local optimum (for a convex program, the local and global optima coincide). If the above lemma were not true, and for two such paths suppose that , without loss of generality. Then, consider a new flow with the flow on reduced by some sufficiently small and the flow on increased by the same amount. If the cost of the old flow is , then the cost of the new flow is

which is a contradiction because is minimum cost among all feasible flows supporting a flow magnitude of . The same argument works for switching a small amount of flow to a path with zero flow. ∎

Lemma B.5.

For a minimum cost flow vector of magnitude , and for any path with , we have .

Proof.

From the proof of being differentiable, we know that if is the min-cost allocation for a flow of magnitude , then . So we just have to prove that for any path with non-zero flow.

For every path with non-zero flow, we know by Lemma B.4 that is the same. Let the value of this quantity by . We also know that for any given edge , by definition. So if is the set of paths with non-zero flow, we have

∎

Appendix C Proofs from Section 3: Existence and Computation of Equilibrium Prices

C.1 Our Pricing rule:

We redefine our pricing rule which we will use for both the existence and uniqueness proofs. Let be the set of edges and be the differential cost function on each edge. Throughout this section will refer to a valid flow and to the magnitude of this flow. Consider any instance with monopolies. For any given minimum cost flow of magnitude , we will use the following pricing rule:

| (1) |

It is easy to verify (from the properties of minimum cost flows) that every flow carrying path has a price of exactly . Indeed, we already know that the total marginal cost of every flow carrying path is . According to the pricing rule, edges are first priced at their marginal cost. In addition, for any flow is the total available slack or surplus, which is divided equally among all the monopolies. For example, if all edges are monopolies having the same cost function, then and . Our first simple lemma shows that any edge priced at its marginal cost has no incentive to lower its price.

Lemma C.1.

At any flow , an edge priced at can never increase its profit by lowering its price.

Proof.

Suppose an edge decreases its price from to and its flow increases from to , then we need to show that . Consider the function . For a fixed , its derivative is negative for . Therefore, for any , we have . But since , we know . This completes the proof. ∎

Claim 3.1. In any network with no monopolies (i.e, you cannot disconnect , by removing any one edge), there exists a Nash Equilibrium maximizing social welfare.

Proof.

The solution is quite straight-forward. We compute the optimum solution and price edges according to our pricing rule above, which translates to each edge being priced at since the instance has no monopolies. By Lemma B.4 and Proposition 2.2, we know that for every flow carrying path , . So all flow carrying paths have the same total price, call it . We claim that sending a flow of magnitude is a best-response by the buyers to this price. First consider the case when . According to Proposition 2.2, is the total flow available in the market. Thus all the buyers have a value of at least for the paths and since the price is not larger than this, all of them purchase one of the paths. When , it means that exactly of the buyers value the paths at or more, so these many buyers send the flow. In both cases, buyer behavior is indeed a best-response to the prices.

Now we show that sellers cannot change their price unilaterally and increase their profit. We claim that for every edge with flow, if the edge is removed from the graph, then there exists at least one path with a total price of . Then, no edge would wish to unilaterally increase its price as the flow would switch to the alternative path. Since the graph has no monopolies, there exists at least one path not containing for every edge . Let be a flow carrying path with where and . If the flow on is , then there exists at least one flow carrying path without and the price of this path is , so we are done. If not, then for some and some , there must exist a path between and that only passes through edges with no flow on them. The price on these edges without flow must be . Consider the new path . The price of this path is no larger than , since the price of edges in is zero. So the price of this path must be exactly . Therefore, we conclude that no single edge can increase its price and still retain some flow.

By Lemma C.1, we already know that no edge can priced at its marginal can decrease its price and make more profit, no matter how much the flow increases by. For the case, the whole market demand is satisfied so decreasing the price has no additional impact anyway. The edges without flow are already priced at , so they cannot decrease their price. This completes the proof. ∎

C.2 Proof of Existence

Theorem 3.2. For any MPE demand function , there exists a Nash equilibrium Pricing.

Proof.

Recall that a solution of our game is given by . Clearly, once prices are fixed, buyers always buy best-response bundles so we only consider solutions of this form. Finally for any edge, we define to be the increase in the price of an edge from its marginal cost. That is, given a solution, . We will now show some sufficient conditions that this ‘increased’ price must obey in an equilibrium.

Lemma C.2.

Given a solution with a best-response flow to prices , with and , we have that no seller can increase his price and improve profits as long as either one of the following conditions hold,

-

1.

The good is tight, i..e, some - path that does not contain the edge and has the same total price as the flow-carrying paths that do contain (or)

-

2.

Proof.

The first part of the lemma is fairly trivial: let be any flow-carrying path that contains and be a path not containing but having the same overall price as . Since buyers always buy the best-response bundles, if seller increases his price, the price of (or any other flow carrying path containing ) would become strictly larger than that of . All the buyers that originally purchased from this seller would now shift to using or any other path not containing , and seller ’s profit would become zero which cannot be strictly larger than his original profit.

Suppose an edge is not tight and a seller who obeys can increase his price (perhaps to some extent) and still have the cheapest paths pass through this edge. In this case, it is necessary that the entire flow must be using this edge. To see why, suppose if the flow on this edge , then there must be atleast one other - path not containing with non-zero flow on it. Since all the paths with non-zero flow must have the same price (, this boils down to our first condition of being tight since there is an alternative path with the same price. Therefore, and every flow carrying path contains .

Now suppose that seller increases his price from to and the resulting flow on the edge is . Then, it is not hard to see that , because the price of every flow carrying path has increased by a non-zero amount () and if the flow remained the same, then it would mean that is not uniquely defined at . We first establish the relation between and , namely that . To see why, notice that the flow of size is a best-response flow to the prices in our original solution, except with price on edge . As we argued above, all cheapest paths in our given solution have cost ; thus all cheapest paths in this new pricing have cost . Since this pricing results in a flow of size , it must be that : the buyers who purchase the cheapest bundles are exactly the ones who value them more than . Thus, we know that .

Now consider seller ’s original profit, . After changes its price to , this profit become , which by the above argument equals . We want to show that this new profit is at most the old profit as long as Condition (2) is obeyed. Define . We will prove that in the domain , is maximized when , thus implying that no matter what amount the seller increases his price by, at the resulting flow of magnitude , his profit cannot be strictly larger than the original profit.

We now proceed to prove that is maximized at . Specifically, we look at the derivative of and show that it is non negative for . Recall that the seller obeys Condition (2) which implies,

Since

Thus the derivative of is equal to

Since the last term in the parenthesis, is non-negative ( is non-decreasing), in order to show that for all , it suffices if we show the first terms are non-negative. The following proposition implies that for MPE functions, this is indeed true.

Proposition C.3.

For and , we have that for .

Proof.

First suppose that . Let and ; we want to show that . Suppose to the contrary that . is non-negative since is non-increasing, and is nonnegative since . We know by the property of MPE functions that

| (2) |

Let and , and consider how compares with . First, notice that we have at ,

Therefore, . Thus we know that , and thus . By our assumption that , this implies that , i.e.,

This contradicts Inequality (2) above, thus proving that .

What if ? Since MPE functions must have non-decreasing , we can only conclude that for all , . In this case, it is not hard to see that the proposition trivially holds since and the RHS is zero as well. ∎

We have therefore shown that for all , is non-negative. This means that is non-decreasing in this region and therefore maximized at in the domain . Therefore, no ‘monopoly edge’ can benefit by changing its price, as desired. Also notice that if , then has to be finite if the prices are finite; the above argument works for this case as well. ∎ ∎

We now show sufficient conditions on the other half of seller behavior, namely give conditions on when a seller cannot decrease his price.

Lemma C.4.

Given a solution with a best-response flow to prices , satisfying , no seller can decrease his price and improve profits as long as any one of the following conditions hold,

-

1.

or

-

2.

or

-

3.

and

Proof.

Once again the first two conditions are easy to prove. If , it just means that there are no more buyers left in the market. So for any such seller, a decrease in price is not going to lead to any additional flow. In the second case, simply means that a seller is priced at its marginal price and so by Lemma C.1 no such seller would wish to decrease his price. For the final condition, suppose that and .

Notice that as with the previous proof, any decrease in price from to will result in a flow of magnitude . As we argued previously, since buyers will only indulge in best-response behavior, it is necessary that .