Classical mechanics of economic networks

Abstract

Financial networks are dynamic. To assess their systemic importance to the world-wide economic network and avert losses we need models that take the time variations of the links and nodes into account. Using the methodology of classical mechanics and Laplacian determinism we develop a model that can predict the response of the financial network to a shock. We also propose a way of measuring the systemic importance of the banks, which we call BankRank. Using European Bank Authority 2011 stress test exposure data, we apply our model to the bipartite network connecting the largest institutional debt holders of the troubled European countries (Greece, Italy, Portugal, Spain, and Ireland). From simulating our model we can determine whether a network is in a “stable” state in which shocks do not cause major losses, or a “unstable” state in which devastating damages occur. Fitting the parameters of the model, which play the role of physical coupling constants, to Eurozone crisis data shows that before the Eurozone crisis the system was mostly in a “stable” regime, and that during the crisis it transitioned into an “unstable” regime. The numerical solutions produced by our model match closely the actual time-line of events of the crisis. We also find that, while the largest holders are usually more important, in the unstable regime smaller holders also exhibit systemic importance. Our model also proves useful for determining the vulnerability of banks and assets to shocks. This suggests that our model may be a useful tool for simulating the response dynamics of shared portfolio networks.

keywords:

Financial Crisis — Stress Test — Systemic Risk — Linear Response — Phase Transition — Bipartite NetworkSignificance

We propose a simple yet powerful deterministic model for a fully dynamical bipartite network of banks and assets and apply it to the Eurozone sovereign debt crisis. The results closely match real-world events (e.g., the high risk of Greek sovereign bonds and the failure of Greek banks). The model can be used to conduct “systemic stress tests” to determine the vulnerability of banks and assets in time-dependent networks. It also provides a simple way of assessing the stability of a system by using the ratio of the log returns of sovereign bonds and the stocks of major holders. We also propose a “systemic importance” ranking, BankRank, for these dynamic bipartite networks.

Recent financial crises have motivated the scientific community to seek new interdisciplinary approaches to modeling the dynamics of global economic systems. Many of the existing economic models assume a mean-field approach, and although they do include noise and fluctuations, the detailed structure of the economic network is generally not taken into account. Over the past decade there has been heightened interest in analyzing the “pathways of financial contagion.” The seminal papers were by Allen and Gale [1, 2] and these were following by many other studies [3, 4, 5, 6, 7, 8]. Economists have recently become aware that econometrics has traditionally paid insufficient attention to two factors: (i) the structure of economic networks and (ii) their dynamics. Studies indicate that a more thorough approach to the examination of economic systems must necessarily take network structure into consideration [9, 10, 11, 12, 13, 14, 15, 16].

One example of this approach is the work of Battiston et al. [17]. They study the 2008 banking crisis and use network analysis to develop a measure of bank importance. By defining a dynamic centrality measurement called DebtRank that measures interbank lending relationships and their importance in propagating network distress, they show that the banks that must be rescued if a crash is to be avoided (those that are “too big too fail”) are the ones that are more “central” in terms of their DebtRank.

Another recent event that has motivated and provided the focus for our study reported here is the 2011 European Sovereign Debt Crisis. It began in 2010 when the yield on the Greek sovereign debt started to diverge from the sovereign debt yield of other European countries, and this led to a Greek government bailout [18]. The nature of the sovereign debt crisis and resulting network behavior that we analyze here differs somewhat from that of the US banking crisis. Here we focus on the funds that several Eurozone countries—Greece, Italy, Ireland, Portugal, and Spain (GIIPS)—had borrowed from the banking system through the issuing of bonds. When these governments faced fiscal difficulties, the banks holding their sovereign debt faced a dilemma: should they divest some of their holdings at reduced values or should they wait out the crisis. The bank/sovereign-debt network that we analyze in this study is a bilayer network. Although DebtRank has also been used to study bipartite networks, e.g., to describe the lending relationships between banks and firms in Japan [19], it does not take into account that link weights exhibit a dynamic behavior.

Huang et al. [20] and Caccioli et al. [21] analyzed a similar problem, that of cascading failure in a bipartite network of banks vs assets in which risk propagates among banks through overlapping portfolios (see also Ref. [22]). Although network connections in real-world financial systems, e.g., interbank lending networks or stock markets, are dynamic, neither of the above models [20, 21] take this into account. Other models by Hałaj and Kok [23], which use simulated networks similar to real systems, or by Battiston et al. [24] allow the nodes to be dynamic but not the links (see, however, Ref. [25], in which dynamic behavior occurs when a financial network attempts to optimize “risk adjusted” assets [26]). Our approach differs from both of these because by introducing only two parameters which play the role of coupling constants in physics we can enable all network variables to be dynamic. Our model is related to Caccioli et al. [21] and Battiston et al. [17] but differs in that we allow both nodes and links to be dynamic.

We use a time-slice of the GIIPS sovereign debt holders network from the end of 2011 to focus on a simplified version of the network structure and use it to set the initial conditions for our model.111To assess the robustness of our model, we use what we learn about the GIIPS network structure and apply it to simulations of other networks of varying sizes and distributions. These results are available in the supporting materials.

We start by proposing, solely on phenomenological grounds, a set of dynamical equations. Based on our analysis we observe that:

-

1.

When we model how a system responds to an individual bank experiencing a shock, our analysis is in accordance with real-world results, e.g., in our simulations Greek debt is clearly the most vulnerable.

-

2.

The dynamics arising from our model produces different end states for the system depending on the values of the parameters.

In order to determine which banks play a systemically dominant role in this bipartite network, we adjust the equity of each bank until it goes bankrupt and then quantify the impact (the BankRank) of the bank’s failure on the system. We simulate the dynamics for different parameter values and observe that the system exhibits at least two distinctive phases, one in which a new equilibrium is reached without much damage and one in which the monetary damage is quite significant, even devastating.

1 The GIIPS problem

Governments borrow money by issuing sovereign (national) bonds that trade in a bond market (which is similar to a stock market222The entity that issues a bond (e.g., the government in case of sovereign bond) promises to pay interest. Governments also promise to return the face value of the loan at the “maturity” date. Bonds, unlike stocks, have maturities and interest payments. A detailed description of some of these bond characteristics can be found in Ref. [27]. As is the case with stocks, the value of these sovereign bonds increases when countries are doing well, and supply and demand ultimately determine the value of the bonds. If, however, the country becomes troubled and the market perceives that the government will not be able to pay back the debt, the price of the bond can crash, which was the case of Greece.).

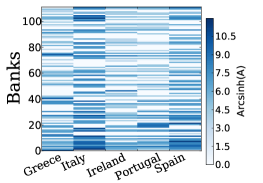

Our GIIPS data are from the 137 banks, investment funds, and insurance companies that were the top holders in the GIIPS sovereign bond-holder network in 2011. (Hereafter we will use “banks” to refer to all these financial institutions.) Table 1 shows the percentages of the sovereign bonds issued by each GIIPS country owned by these banks. Since our model requires knowing the equity of each bank, we reduce our dataset to the 121 banks whose equity value was obtainable. By the end of 2011, two important Greek banks—the National Bank of Greece and Piraeus Bank—had negative equities. Because our model only considers banks that can execute trades based on positive capital, we also had to eliminate these two banks from our analysis. Figure 1 shows the weighted adjacency matrix of this network.333The intensity of the color is proportional to Arcsinh() for better visibility. For large , arcsinh.

| Greece | Italy | Portugal | Spain | Ireland | |

|---|---|---|---|---|---|

| Total (bnEu) | 64.85 | 330.38 | 30.63 | 151.15 | 18.41 |

| % in Banks | 23.67 | 20.13 | 23.81 | 21.81 | 20.55 |

When a country defaults on sovereign debt (or stops paying interest as it comes due) the consequences are usually grave. To prevent cascading sovereign defaults, the European Union, the European Central Bank, and the International Monetary Fund jointly established financial programs to provide funding to troubled European countries. Funding was conditional on implementing austerity measures and stabilizing the financial system in order to promote growth and increase productivity. We use our sovereign debt data as the initial condition for a model of cascading distress propagating through a bipartite bank network in which banks only affect each other through shared portfolios. In order to develop a framework for analyzing these problems that goes beyond simply determining how distress propagates through the links, we construct a model in which dynamic change affects both the weights of links and the attributes of nodes. Figure 1 shows the weighted adjacency matrix of this network in log format.

2 Model

The system that we study is a bipartite network as shown in Fig. 1. On one side we have the GIIPS sovereign bonds, which we call “assets,” and on the other we have the “banks” that own the GIIPS bonds. The nodes on the “asset” side are labeled using Greek indices . To each asset we assign a “price,” at time . The “bank” nodes are labeled using Roman indices . Each bank node has an “equity” , a time , and an initial value of asset . Each bank in the network can have differing amounts of holdings in each of the asset types. The amount of asset that bank holds is denoted by , which is essentially an entry of the weighted adjacency matrix of the network. In our model we begin with a set of phenomenological equations describing how each of the variables , and evolve over time. A key feature of our model is that the weights of links are time-dependent, and this introduces dynamics into our network.

2.1 Assumptions, simplifications and the GIIPS system

The key assumptions that differentiate our model from other banking system or dynamic network models are:

-

1.

The banks do not exclusively trade with each other. They may trade with an external entity, which may be the European Central Bank (ECB) or other, smaller investors. 444This is appropriate in the case of GIIPS sovereign debt because, in addition to the ECB (which buys some of the bonds if there is a need to stabilize the system), a large number of investors hold GIIPS sovereign debt. This is important to keep in mind because in most problems associated with banking or financial networks agents are assumed to be trading with each another.

-

2.

When there is no change in equity, price, or bond holdings, nothing happens and there is no intrinsic dynamic activity in our financial network.

-

3.

The model describes the short time response of the system and disregards slow, long-term driving forces of the market.

-

4.

We assume the agents in the system will copy each other’s actions, producing the so-called “herding effect.” This is why we assume the “coupling constants” (the free parameters) are the same for all agents.

3 Notations and Definitions

We denote by the weighted adjacency matrix, the components of which are the amount of exposure of bank to asset . The equity of a bank is defined as

Here is the “price ratio” of asset at a given time to its price at , is the bank’s cash, and is bank’s liability. These parameters evolve in time. Bank will fail if its equity goes to zero,

We assume that the liabilities are independent of the part of the market we are considering and are constant. For convenience we define

Two other dependent variables that we use are the “bank asset value” and the total GIIPS sovereign bonds on the market . In our model we assume that and are constant. Everything else is time-dependent.

3.1 The time evolution of GIIPS holdings and their price

For changes in equity we have

Here we assume that the cash minus liability changes according to the amount of money earned through the sale of GIIPS holdings,

where the minus sign indicates that a sale means and this should add positive cash to the equity of bank . is the cash made from transactions outside of the network of . The first term in cancels one term in and we get (all at time )

In the secondary market for the bonds (where issued bonds are traded in a manner similar to stocks) the prices are primarily determined by supply and demand. We use a simple model for the pricing that should hold as a first-order approximation. We assume the price changes to be

Here the coupling constant is essentially the “inverse of the market depth,” i.e. the fraction of sales ( required to reduce the price by one unit () is equal to . We are assuming that the market is “liquid” meaning that any amount of assets can be sold or bought without a problem. We have defined is the change in price from the previous step, the net trading (number of purchases minus sales) of asset , and the “response time of the market.” We choose the same “inverse market depth” for all GIIPS holdings , assuming that they belong to the same class of assets. We then define how the GIIPS holdings are sold or bought, i.e., we define . We also include a “panic factor” that indicates how abruptly distress propagates when a loss is incurred, and a “market sensitivity” factor that indicates how quickly the price of an asset drops when part of it is sold. These variables are summarized in Table 2.

| symbol | denotes |

|---|---|

| Holdings of bank in asset at time | |

| Normalized price of asset at time () | |

| Equity of bank at time . | |

| Banks’ “Panic” factor. | |

| “Inverse market depth” factor of price to a sale. |

We assume that if a bank’s equity shrinks it will start selling GIIPS holdings in order to continue meeting its liability obligations, and that if a bank’s equity shrinks because of asset value deterioration it will sell a fraction of its entire portfolio to ensure meeting those obligations. The amount of GIIPS holdings sold will depend on how panicked the bank is, i.e., on the value of “panic factor” . A bank thus determines what fraction of its equity has been lost in the previous step and sells according to

where is the “response time of the banks.” Here we assume that banks purchase using the same protocol as when selling and sell the same fraction of all their GIIPS assets. The above equations can be converted to differential equations by simply replacing . If we assume that the time lags are small, we can expand the equations with to first-order and get

For brevity, we define . The three equations become:

| (1) | ||||

| (2) | ||||

| (3) |

where has the meaning of external force. where is the time-scale in which Banks respond to the change, and is the time-scale of market’s response.555Without a time lag, these equations would be primarily constraint equations relating the first-order time derivatives of to each other. Note however that in simulating this dynamic system the order in which we update the variables matters because most of the nontrivial dynamic behavior follows from this time lag between updates.

In our simulations we use these differential equations and choose . One of them can always be chosen as a time unit and set to one, but setting them equal is an assumption and may not be true in reality. Our analysis showed that the choice of does not affect the stability of the system and that the stability only depends on , and the shock. The , which are changes in the equity from what banks own outside of this network, can be thought of as external noise or driving force. We use to shock the banks and make them go bankrupt. We shock a single bank, say bank , at a time by reducing its equity 10% by putting666Note that the magnitude of the shock only rescales time, according to Eq. (3) because is the same as and thus .777 is the kronecker delta, or the identity matrix elements, and is the Dirac distribution or impulse function. Starting with , plugging into (1) and integrating over a small interval yields

| (4) |

This and are the initial conditions we start with. In addition, we require during the simulations.

4 Application to European Sovereign Debt Crisis

We apply our model to the GIIPS data mentioned above. Before looking at the simulations of Eqs. (1)–(3), we estimate the values of our parameters in the case of the GIIPS sovereign debt crisis.

4.1 Estimating values of

We use approximate versions of Eqs. (1)–(3) to estimate the product of parameters and (details of the approximation and the assumptions are discussed in the SI). The distribution of the assets is roughly log-normal, so a small number banks hold a significant portion of each GIIPS country’s debt. Thus using only the equity of the dominant holders and denoting their sum by for country will give us a good estimate of . We estimate that the response times are at most on the order of several days. Thus we will calculate over a period of four months to allow the system to reach its new final state, and we can discard the second-order derivatives. This allows us to write

where denotes the equity of the dominant bank for asset . Using this approximation we can relate the first two equations888 The equity of the banks is mostly comprised of the shareholders’ equity, or common stocks. These banks usually have multiple stock tickers, but there is generally one or two main stock tickers where most of the equity is. We can use the movements in these main stocks to estimate . For this approximation we use the following formula: where is the stock price at the beginning of the period and is at the end of it. ,

Thus we can approximate as

| (5) |

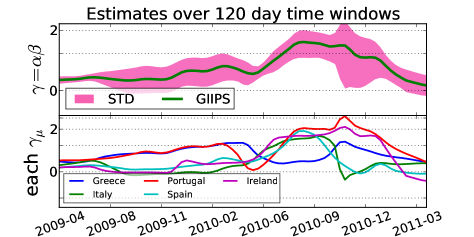

We evaluate for each country . If the values are similar for different values it may indicate that the “herding effect” is a factor. This both supports our model and suggests that it is applicable to this problem. We evaluate for the time period between early 2009, when the crisis was just beginning, and early 2011, when most government bailouts had either been paid or scheduled.

If we assume that the number of shares issued by our banks were roughly constant over the period in question, the movements in stock prices may be used as a proxy for the changes in the equity of banks. Many of the major movements (or slope changes) in each country’s values seem to coincide with bailout payment times.

Figure 2 shows the average values during this period with standard deviation error-bars. The bottom of the figure gives estimates for and assuming . A more detailed plot with individual values of obtained using each country is also shown in Fig. 2.

Figure 2 shows that before the crisis and at its height . Below we will explore the phase space in terms of different values of and . An important finding is that our model predicts that is an unstable phase in which a negative shock to the equity of any bank will cause most asset prices to fall dramatically to nearly zero. Similarly, a positive shock will cause the formation of bubbles. When , on the other hand, after a shock the system smoothly transitions into a new equilibrium and, although some banks may fail, no asset prices will fall to zero.

5 Simulations

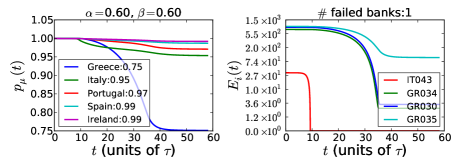

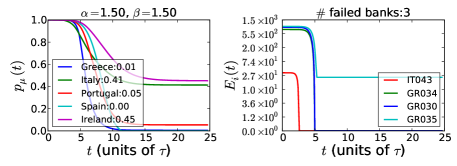

We find that when values of and are small, e.g., , shocking any of the banks in the network will result in the same final state (see Fig. S2). This is a new stable equilibrium. If we shock the system a second time the prices do not change significantly, i.e., less than 0.1%). Figure 3 shows a sample of the time evolution of the asset prices and the equity of the banks that incurred the largest losses.

Figure 3 shows results that seem in line with what actually happened during the European debt crisis, although the damage shown for Ireland is less than what actually occurred. In this figure, bailouts are disregarded. Three of the four most vulnerable banks (MVB) shown in Figs. 3 and 4 are holders of Greek debt. In this simulation, Greek debt is the asset that loses the most value. Note that the loss prediction produced by the model is based solely on the network of banks holding GIIPS sovereign debt and provides information about the economies of these countries, with Greece experiencing the largest loss, followed by Portugal (real-world data indicates that Ireland’s loss was as severe as Portugal’s).

Note that the new equilibrium depends on and . Returning to the real data, Fig. 2 shows that before the onset of the crisis the system responds to a shock by achieving a new equilibrium similar its initial equilibrium (behavior similar to that shown in Fig. 3). At the height of the crisis, however, when , even a small shock can have a devastating effect and precipitate a crisis (see Fig. 4). Although many banks incur significant losses when and values are at their highest, the same four banks fail.

In the SI we show the effect of rewiring the banks who lend to each country, meaning we take and take random permutations of index so that the equities of banks connected to each country changes randomly. Interestingly, such a rewiring changes the damages suffered by GIIPS bonds entirely, meaning that Greece will no longer be the most vulnerable. This shows that in our model, while qualitative behavior of the system only depends on and , the final prices and equities depend strongly on the network structure.

6 Systemic Risk and BankRank

We thus take a different approach. We find that a bank can cause a large amount of systemic damage when its equity level is at the bare minimum necessary to survive a shock. Banks with very low equity fail rapidly, no longer trade, and thus no longer transmit damage to the system. Banks with equity sufficient to survive for a significant period of time, on the other hand, continue to transmit damage into the system and thus cause more damage than extremely weak banks. Based on this observation we rank the banks using a “survival equity ratio” (SER), i.e., the fraction of actual equity a bank needs in order to survive systemic shock. The total damage done to the system varies significantly from bank to bank. To rank the systemic importance of each bank we measure the effect their failure has on the system. Since normally no banks other than the four mentioned above fail, we modify the data slightly. The steps we take are as follows:

-

1.

We increase the equity of the four failing banks to to keep them from failing and significantly damaging the system. Then when , the system becomes resilient to shocks and the drop in prices falls below 1% (the system has reached a stable phase). When the system continues to incur significant losses.

-

2.

To assess the systemic importance of bank , we run separate simulations with initial conditions changed to , until we find the threshold of survival under a small shock to any other bank ().

-

3.

We calculate the total GIIPS holdings left in the system.

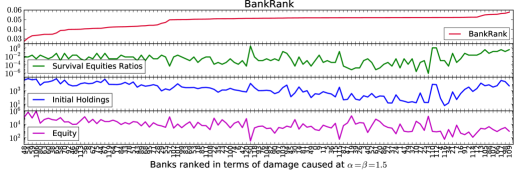

We define “BankRank” of to be the ratio of the final holdings to initial holdings if bank fails, i.e. BankRank of is equal to the amount of monetary damage the system would take if bank fails:

| (6) |

The smaller the value of , the greater the systemic importance of bank .

Fig. 5 on the left shows the BankRank in the unstable regime at and how it compares to the initial holdings, minimum ratio of equity required for survival, and initial equities. We observe some correlation between BankRank and each of these variables, but for many banks BankRank does not seem to follow any of these variables. On the right of Fig. 5, on the top left we see that BankRank in the stable regime at has very high correlation with the initial holdings. In the other three plots on the right we see that BankRank changes significantly when we transition from the stable to the unstable regime. This again indicates that, while in the stable regime holding almost completely determine the systemic importance of a bank, in the unstable regime this is no longer the case and many small holders will have high systemic importance.

7 Conclusion and Remarks

We study the systemic importance of large institutional holders of GIIPS sovereign debt and propose a simple, dynamic “systemic risk measurement,” which we call BankRank. We do not find any definitive correlation between BankRank and diversification, but there is a strong correlation between BankRank and total GIIPS holdingsq. Our model describes the response of the GIIPS system to shocks well enough to reveal a “herding effect,” i.e., its presence is indicated whenever a single value for the parameters can be used for the whole system. Our methodology (i) can be used to model “systemic risk propagation” through a bi-partite network of banks and assets, i.e., it can serve as a “systemic stress testing” tool for complex financial systems, and (ii) it can be used to identify the “state” or “phase” in which a financial network resides, i.e., if a banking system is in a fragile state we can quantify it and determine how to transition the system into a more stable state.

We suggest that our model could be useful as a monitoring and simulation tool that allows policy makers to identify systemically important financial institutions and to assess systemic risk build-up in the financial network.

Acknowledgements.

We thank the European Commission FET Open Project “FOC” 255987 and “FOC-INCO” 297149, NSF (Grant SES-1452061), ONR (Grant N00014-09-1-0380, Grant N00014-12-1-0548),DTRA (Grant HDTRA-1-10-1-0014, Grant HDTRA-1-09-1-0035), NSF (Grant CMMI 1125290), the European MULTIPLEX and LINC projects for financial support. We also thank Stefano Battiston for useful discussions and providing us with part of the data. The authors also wish to thank Matthias Randant and others for helpful comments and discussions, and especially Fotios Siokis for sharing important points about the data and the Eurozone crisis.References

- [1] Allen, F., & Gale, D. (2000). “Financial contagion.” Journal of political economy, 108(1), 1-33.

- [2] Allen, F., & Gale, D. (2007). “Systemic risk and regulation. In The Risks of Financial Institutions” (pp. 341-376). University of Chicago Press.

- [3] Furfine, C. H. “Interbank exposures: quantifying the risk of contagion.” Journal of Money, Credit and Banking 35, 111-128 (2003).

- [4] Wells, S. “UK interbank exposures: systemic risk implications.” Bank of England Financial Stability Review December, 175-182 (2002).

- [5] Upper, C. & Worms, A. “Estimating bilateral exposures in the German interbank market: is there a danger of contagion?” European Economic Review 48, 827-49 (2004).

- [6] Elsinger, H., Lehar, A. & Summer, M. “Risk assessment for banking systems.” Management Science 52, 1301 (2006).

- [7] Nier, E., Yang, J., Yorulmazer, T. & Alentorn, A. “Network models and financial stability.” J. Econ. Dyn. Control 31, 2033 (2007).

- [8] Cifuentes, R., Ferrucci, G. & Shin, H. S.“Liquidity risk and contagion.” Journal of the European Economic Association 3, 556 (2005).

- [9] Haldane, A. G. & May, R. M. “Systemic risk in banking ecosystems.” Nature 469, 351-355 (2011).

- [10] Rodríguez-Moreno M., Peña J. I., Systemic risk measures: The simpler the better?, Journal of Banking & Finance, Volume 37, Issue 6, June 2013, Pages 1817-1831

- [11] Johnson, N. & Lux, T. “Financial systems: Ecology and economics.” Nature 469, 302-303 (2011).

- [12] Schweitzer, F. et al. “Economic networks: the new challenges.” Science 325, 422-425 (2012).

- [13] Watts D. , “A simple model of global cascades on random networks.” PNAS, no. 99, pp. 5766-5771, 2002.

- [14] Buldyrev, S. V., Parshani, R., Paul, G., Stanley, H. E., & Havlin, S. (2010). “Catastrophic cascade of failures in interdependent networks.” Nature, 464(7291), 1025-1028.

- [15] Levy Carciente, S., Kenett, D. Y., Avakian, A., Stanley, H. E. & Havlin, S., “Dynamical Macro-Prudential Stress Testing Using Network Theory.” (August 18, 2014). Available at SSRN: http://ssrn.com/abstract=2482742

- [16] Ranking the Economic Importance of Countries and Industries Li, W., Kenett, D. Y., Yamasaki, K., Stanley H. E. & Havlin, S., “Ranking the Economic Importance of Countries and Industries.” http://arxiv.org/abs/1408.0443

- [17] Battiston, S. , Puliga, M. , Kaushik, R. , Tasca, P., & Caldarelli, G. “DebtRank: Too Central to Fail? Financial Networks, the FED and Systemic Risk.” , Nature, Scientific Reports, Published 02 August 2012

- [18] Lane, P.R. “The European Sovereign Debt Crisis.” The Journal of Economic Perspectives, Vol. 26, No. 3, Pages: 49-67 Published: Summer 2012

- [19] Aoyama H. , Battiston S. , Fujiwara Y. “DebtRank Analysis of the Japanese Credit N.” RIETI Discussion Paper Series 13-E-087, October 2013

- [20] Huang, X. , Vodenska, I. , Havlin, S. , Stanley, H.E. “Cascading Failures in Bi-partite Graphs: Model for Systemic Risk Propagation.” , Nature, Scientific Reports, Published 05 February 2013

- [21] Caccioli, F. , Shrestha, M., Moore, C., & Farmer, J. D. “Stability analysis of financial contagion due to overlapping portfolios.”

- [22] Tsatskis, I. “Systemic losses in banking networks: indirect interaction of nodes via asset prices.” arXiv,1203.6778v1 (2012).

- [23] Hałaj, G., & Kok, C. “Assessing interbank contagion using simulated networks.” Computational Management Science (2013): 1-30.

- [24] Battiston, S., Delli Gatti, D., Gallegati, M., Greenwald, B., & Stiglitz, J. E. (2012). Liaisons dangereuses: “Increasing connectivity, risk sharing, and systemic risk.” Journal of Economic Dynamics and Control 36(8) (2012): 1121-1141.

- [25] Hałlaj, G., & Kok, C. (2013). “Modeling Emergence of the Interbank Networks.” ECB Working Paper, forthcoming.

- [26] Montagna, M., & Kok, C. (2013) “Multi-layered interbank model for assessing systemic risk.” No. 1873. Kiel Working Paper.

- [27] Battiston, S., Gatti, D. D., Gallegati, M., Greenwald, B., & Stiglitz, J. E. (2012). “Default cascades: When does risk diversification increase stability?.” Journal of Financial Stability, 8(3), 138-149.

Supporting Information

8 Testing the Role of the Network

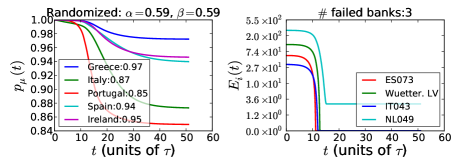

Our goal is to determine how much of the above behavior is caused by the network structure and how much by the value of the outstanding debts. To examine the dependence of the results on network structure, i.e., to determine which banks hold which country’s debt and how much bank equities matter, we randomize the network and redo our analysis. We do not change the value of the total GIIPS sovereign debt held by the banks. We only rewire the links in the network, changing the amount of debt held by each bank and the countries to which each bank lends money.

Figure S1 shows an example of this randomization and how dramatically it changes the end result, and it demonstrates two important features of the model: (i) system dynamics are strongly affected by network structure, i.e., knowing such global variables as the equity and exposure of individual banks is not sufficient, and (ii) real-world data seems to indicate that it was the structure of the network of lenders to Greece that caused Greek sovereign bonds to become the most vulnerable. This suggests that our model may be useful as a stress testing tool for banking networks, or any network of investors with shared portfolios.

9 Shocking different banks

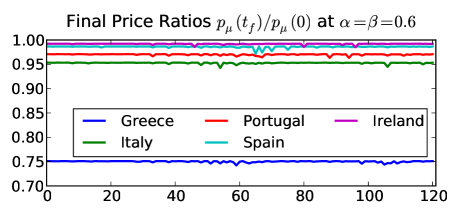

Fig. S2 shows the final prices found from shocking different banks. They are all almost identical. However, the small variation and the variations in the can be used to construct BankRank and find that different banks have different mounts of influence.

10 The Banks

The listed banks, insurance companies, and funds in the order of largest holders of the GIIPS holdings is given in table 3.

| Name | Code Name | Holdings | Equity | Greece | Italy | Portugal | Spain | Ireland | |

|---|---|---|---|---|---|---|---|---|---|

| 0 | GESPASTOR | Gespastor | 3.5e+02 | 1.6e+03 | 0 | 0 | 0 | 3.5e+02 | 0 |

| 1 | M&G | M&G | 37 | 1.1e+04 | 0 | 0 | 37 | 0 | 0 |

| 2 | UNION INVESTMENT | Union Inv. | 3.4e+03 | 7e+02 | 1.6e+02 | 2e+03 | 77 | 1e+03 | 1.5e+02 |

| 3 | ATTICA BANK | Attica | 1.8e+02 | 1.5e+04 | 1.8e+02 | 0 | 0 | 0 | 0 |

| 4 | MILANO ASSICURAZIONI | Milano Assic. | 74 | 9.3e+02 | 23 | 0 | 0.71 | 49 | 2.1 |

| 5 | GROUPAMA | Groupama | 4.4e+02 | 4.3e+03 | 0 | 4.2e+02 | 19 | 0 | 0 |

| 6 | AEGON NV | Aegon | 1.1e+03 | 2.6e+04 | 2 | 65 | 9 | 9.8e+02 | 26 |

| 7 | RIVERSOURCE | River Source | 48 | 7.4e+03 | 48 | 0 | 0 | 0 | 0 |

| 8 | AVIVA PLC | Aviva | 1.1e+04 | 1.8e+04 | 1.5e+02 | 8.4e+03 | 2.3e+02 | 1.4e+03 | 7.2e+02 |

| 9 | EMPORIKI BANK | Emporiki | 2.9e+02 | 1.2e+03 | 2.9e+02 | 0 | 0 | 0 | 0 |

| 10 | MELLON GLOBAL | Mellon | 16 | 2.8e+04 | 0 | 0 | 0 | 0 | 16 |

| 11 | DAIWA | Daiwa | 7.1e+02 | 7.3e+03 | 0 | 5e+02 | 0 | 2e+02 | 0 |

| 12 | FIDEURAM | Fideuram | 2e+03 | 5.5e+02 | 0 | 2e+03 | 0 | 0 | 0 |

| 13 | UNIPOL | Unipol | 1.3e+04 | 2.5e+03 | 26 | 1.2e+04 | 1.5e+02 | 1.1e+03 | 2.4e+02 |

| 14 | WGZ BANK AG WESTDT. GENO. | DE029 | 3.6e+03 | 1.9e+03 | 3.2e+02 | 1.4e+03 | 4.6e+02 | 1.2e+03 | 2.2e+02 |

| 15 | JYSKE BANK | DK009 | 1.2e+02 | 1.4e+04 | 64 | 0 | 19 | 15 | 22 |

| 16 | OESTERREICHISCHE VOLKSBANK AG | AT003 | 3.7e+02 | 4.8e+02 | 1.1e+02 | 1.5e+02 | 29 | 66 | 13 |

| 17 | CAIXA PORTUGAL | Caixa (PT) | 8.1e+03 | 2.4e+04 | 35 | 4.6e+02 | 30 | 7.5e+03 | 44 |

| 18 | BLACKROCK | Blackrock | 2e+03 | 2e+04 | 1.2e+02 | 1.1e+03 | 29 | 7.1e+02 | 30 |

| 19 | BANK OF AMERICA | BofA | 3.8e+02 | 1.8e+05 | 13 | 2.5e+02 | 5.4 | 83 | 29 |

| 20 | NORDEA BANK AB (PUBL) | SE084 | 1.6e+02 | 2.6e+04 | 0 | 97 | 0 | 64 | 1.4 |

| 21 | CAJA DE AHORROS Y M.P. | ES077 | 1.5e+03 | - | 0 | 0 | 0 | 1.5e+03 | 0 |

| 22 | SELLA GESTIONI | Sella | 6.6e+02 | 1.3e+02 | 0 | 6.6e+02 | 0 | 0 | 0 |

| 23 | MITSUBISHI UFJ | Mitsubishi | 1.6e+03 | 8.1e+04 | 0 | 9.2e+02 | 71 | 5.2e+02 | 62 |

| 24 | UBS | UBS | 1.3e+03 | 4.8e+04 | 53 | 6.8e+02 | 55 | 4.4e+02 | 42 |

| 25 | OPPENHEIMER | Oppenheimer | 2.4e+02 | 3.8e+02 | 15 | 0 | 0 | 2.2e+02 | 0 |

| 26 | VONTOBEL | Vontobel | 18 | 1.2e+03 | 18 | 0 | 0 | 0 | 0 |

| 27 | NOMURA | Nomura | 39 | 1.8e+04 | 0 | 0 | 20 | 0 | 19 |

| 28 | MACKENZIE | MacKenzie | 15 | 3.4e+03 | 15 | 0 | 0 | 0 | 0 |

| 29 | AGEAS | Ageas | 5.3e+03 | 7.8e+03 | 6.4e+02 | 2e+03 | 1e+03 | 1.1e+03 | 5.1e+02 |

| 30 | DEUTSCHE POSTBANK | De.Postbank | 9.2e+02 | 5.7e+03 | 9.2e+02 | 0 | 0 | 0 | 0 |

| 31 | MORGAN STANLEY | Morgan Sta. | 4.6e+02 | 5e+04 | 0 | 4.6e+02 | 0 | 0 | 0 |

| 32 | HELVETIA HOLDING | Helvetia | 1e+03 | 3.6e+03 | 7.6 | 7.2e+02 | 18 | 2.4e+02 | 15 |

| 33 | HWANG-DBS | Hwang | 23 | 8.7e+02 | 23 | 0 | 0 | 0 | 0 |

| 34 | ASSICURAZIONI GENERALI | Generali | 1.7e+04 | 1.8e+04 | 1.3e+03 | 5.4e+03 | 3.1e+03 | 5.7e+03 | 1.7e+03 |

| 35 | AMLIN PLC | Amlin | 15 | 1.6e+03 | 0 | 0 | 0 | 15 | 0 |

| 36 | SWISS LIFE HOLDING | Swiss Life | 5.9e+02 | 7.5e+03 | 30 | 1.7e+02 | 77 | 1.8e+02 | 1.3e+02 |

| 37 | PHOENIX GROUP | Phoenix | 3.2e+02 | 2.8e+03 | 0 | 2.3e+02 | 11 | 76 | 2.2 |

| 38 | PRICE T ROWE | PT Rowe | 15 | 2.6e+03 | 0 | 0 | 0 | 0 | 15 |

| 39 | AXA | Axa | 2.9e+04 | 4.9e+04 | 7.6e+02 | 1.7e+04 | 1.5e+03 | 9.4e+03 | 7.5e+02 |

| 40 | TOKIO MARINE | Tokio Marine | 56 | 1e+04 | 0 | 0 | 30 | 0 | 26 |

| 41 | ROTHSCHILD | Rothschild | 1.1e+02 | 6e+02 | 61 | 0 | 52 | 0 | 0 |

| 42 | TT ELTA AEDAK | TT Elta Aedak | 27 | 9.3e+02 | 27 | 0 | 0 | 0 | 0 |

| 43 | BALOISE | Baloise | 7.9e+02 | 3.2e+03 | 84 | 2.7e+02 | 98 | 2.3e+02 | 1.1e+02 |

| 44 | NATIXIS | Netaxis | 3.3e+03 | 2.1e+04 | 4.3e+02 | 1.3e+03 | 3.9e+02 | 8.6e+02 | 3.9e+02 |

| 45 | CREDIT AGRICOLE | FR014 | 1.7e+04 | 4.9e+04 | 6.6e+02 | 1.1e+04 | 1.2e+03 | 3.9e+03 | 1.6e+02 |

| 46 | JULIUS BAER | Jul. Baer | 1.2e+02 | 3.5e+03 | 68 | 0 | 0 | 0 | 57 |

| 47 | FRANKLIN TEMPLETON | Franklin Temp. | 5.1e+03 | 9.7e+03 | 0 | 0 | 0 | 0 | 5.1e+03 |

| 48 | NOVA LJUBLJANSKA BANKA | SI057 | 1.7e+02 | - | 20 | 96 | 15 | 26 | 15 |

| 49 | STATE STREET | State St. | 51 | 1.6e+04 | 0 | 0 | 27 | 0 | 24 |

| 50 | ALLIANZ | Allianz | 3.8e+04 | 1e+05 | 6.2e+02 | 2.9e+04 | 7.5e+02 | 7.1e+03 | 4.9e+02 |

| 51 | VIENNA INSURANCE | Vienna | 93 | 5e+03 | 21 | 13 | 0 | 7 | 52 |

| 52 | BANCO POPOLARE - S.C. | IT043 | 1.2e+04 | 33 | 87 | 1.2e+04 | 0 | 2e+02 | 0 |

| 53 | COMMERZBANK AG | DE018 | 2e+04 | 2.5e+04 | 3.1e+03 | 1.2e+04 | 9.9e+02 | 4e+03 | 32 |

| 54 | LEGAL & GENERAL | L&G | 3.8e+02 | 6.3e+03 | 1.1 | 3.3e+02 | 6.6 | 35 | 4.4 |

| 55 | EFFIBANK | ES063 | 3e+03 | 2.7e+03 | 37 | 0 | 16 | 2.9e+03 | 0 |

| 56 | INTESA SANPAOLO S.P.A | IT040 | 6.2e+04 | 6.4e+05 | 6.2e+02 | 6e+04 | 73 | 8.1e+02 | 1.1e+02 |

| 57 | IRISH LIFE AND PERMANENT | IE039 | 1.9e+03 | 3.5e+03 | 0 | 0 | 0 | 0 | 1.9e+03 |

| 58 | HSBC HOLDINGS PLC | GB089 | 1.5e+04 | 1.3e+05 | 1.3e+03 | 9.9e+03 | 1e+03 | 2e+03 | 2.9e+02 |

| 59 | DANSKE BANK | DK008 | 1.2e+03 | 1.3e+05 | 1 | 5.8e+02 | 1.1e+02 | 1.2e+02 | 4.1e+02 |

| 60 | ROYAL BANK OF SCOTLAND | GB088 | 1e+04 | 9.6e+04 | 1.2e+03 | 7e+03 | 2.9e+02 | 1.5e+03 | 4.5e+02 |

| 61 | BNP PARIBAS | FR013 | 4.1e+04 | 8.6e+04 | 5.2e+03 | 2.8e+04 | 2.3e+03 | 5e+03 | 6.3e+02 |

| 62 | BARCLAYS PLC | GB090 | 2e+04 | 8e+04 | 1.9e+02 | 9.4e+03 | 1.4e+03 | 8.8e+03 | 5.3e+02 |

| 63 | LLOYDS BANKING GROUP PLC | GB091 | 94 | 5.8e+04 | 0 | 32 | 0 | 62 | 0 |

| 64 | DEUTSCHE BANK AG | DE017 | 1.3e+04 | 5.5e+04 | 1.8e+03 | 7.7e+03 | 1.8e+02 | 2.6e+03 | 5.3e+02 |

| 65 | SOCIETE GENERALE | FR016 | 1.8e+04 | 5.1e+04 | 2.8e+03 | 8.8e+03 | 9e+02 | 4.8e+03 | 9.8e+02 |

| 66 | BPCE | FR015 | 8.5e+03 | 4.1e+04 | 1.3e+03 | 5.4e+03 | 3.5e+02 | 1e+03 | 3.4e+02 |

| 67 | BBVA | ES060 | 6.1e+04 | 4e+04 | 1.3e+02 | 4.2e+03 | 6.6e+02 | 5.6e+04 | 0 |

| 68 | BANK OF VALLETTA (BOV) | MT046 | 24 | - | 10 | 3.9 | 2.8 | 0 | 7 |

| 69 | BANCO BPI, SA | PT056 | 5.5e+03 | 8.2e+02 | 3.2e+02 | 9.7e+02 | 3.9e+03 | 0 | 2.8e+02 |

| 70 | BANCO SANTANDER S.A. | ES059 | 5.1e+04 | 2.6e+04 | 1.8e+02 | 7.2e+02 | 3.7e+03 | 4.6e+04 | 0 |

| 71 | CAIXA DE AFORROS DE GALICIA, | ES067 | 4.7e+03 | 2.3e+04 | 0.0022 | 1.6e+02 | 1.3e+02 | 4.4e+03 | 0 |

| 72 | CAIXA D’ESTALVIS DE CATALUNYA | ES066 | 2.8e+03 | 2.3e+04 | 0 | 0 | 0 | 2.8e+03 | 0 |

| 73 | CAJA DE AHORROS Y PENSIONES | ES062 | 3.7e+04 | 2.2e+04 | 0 | 1.3e+03 | 26 | 3.5e+04 | 0 |

| 74 | KBC BANK | BE005 | 7.9e+03 | 1.7e+04 | 4.4e+02 | 5.6e+03 | 1.6e+02 | 1.4e+03 | 2.7e+02 |

| 75 | ERSTE BANK GROUP (EBG) | AT001 | 1.2e+03 | 1.5e+04 | 3.5e+02 | 6e+02 | 1e+02 | 1.4e+02 | 40 |

| 76 | JP MORGAN | JPM | 17 | 1.5e+05 | 0 | 0 | 17 | 0 | 0 |

| 77 | BAYERISCHE LANDESBANK | DE021 | 1.3e+03 | 1.4e+04 | 1.5e+02 | 5.1e+02 | 1.1e-05 | 6.6e+02 | 20 |

| 78 | BFA-BANKIA | ES061 | 2.5e+04 | 1.2e+04 | 55 | 0 | 0 | 2.5e+04 | 0 |

| 79 | SNS BANK NV | NL050 | 1e+03 | 5.4e+03 | 47 | 7.6e+02 | 0 | 57 | 1.6e+02 |

| 80 | RAIFFEISEN BANK (RBI) | AT002 | 4.6e+02 | 1.1e+04 | 1.7 | 4.5e+02 | 2.1 | 3.5 | 0.00016 |

| 81 | DZ BANK AG DT. | DE020 | 8.7e+03 | 1.1e+04 | 7.3e+02 | 2.7e+03 | 1e+03 | 4.2e+03 | 51 |

| 82 | F VAN LANSCHOT | Lanschot | 18 | 7.4e+02 | 0 | 0 | 0 | 0 | 18 |

| 83 | ALLIED IRISH BANKS PLC | IE037 | 6.5e+03 | 1.4e+04 | 40 | 8.2e+02 | 2.4e+02 | 3.3e+02 | 5e+03 |

| 84 | SKANDINAVISKA ENSKILDA BANKEN | SE085 | 6.3e+02 | 1.2e+04 | 1.2e+02 | 2.9e+02 | 1.3e+02 | 86 | 0 |

| 85 | IBERCAJA | Ibercaja | 9.6e+02 | 2.7e+03 | 0 | 0 | 0 | 9.6e+02 | 0 |

| 86 | LANDESBANK BADEN-WURT… | DE019 | 2.8e+03 | 9.5e+03 | 7.8e+02 | 1.4e+03 | 95 | 5.4e+02 | 0 |

| 87 | BANCO POPULAR ESPANOL, S.A. | ES064 | 9.7e+03 | 9.1e+03 | 0 | 2.1e+02 | 6.4e+02 | 8.9e+03 | 0 |

| 88 | CAJA ESP. DE INVER. SALAMANCA | ES070 | 7.6e+03 | - | 0 | 0 | 27 | 7.6e+03 | 0 |

| 89 | NORDDEUTSCHE LANDESBANK | DE022 | 2.8e+03 | 6.5e+03 | 1.5e+02 | 1.9e+03 | 2.6e+02 | 5e+02 | 41 |

| 90 | BANCA MARCH, S.A. | ES079 | 1.5e+02 | 6.5e+03 | 0 | 0 | 0 | 1.5e+02 | 0 |

| 91 | OP-POHJOLA GROUP | FI012 | 43 | 6.2e+03 | 3.1 | 0.36 | 0.00093 | 0.07 | 40 |

| 92 | BANCO COMERCIAL PORTUGUES, | PT054 | 7.4e+03 | 4.4e+03 | 7.3e+02 | 50 | 6.5e+03 | 0 | 2.1e+02 |

| 93 | BANCO DE SABADELL, S.A. | ES065 | 7.4e+03 | 5.9e+03 | 0 | 0 | 91 | 7.3e+03 | 38 |

| 94 | HYPO REAL ESTATE HOLDING AG, | DE023 | 1.1e+04 | - | 0 | 7.1e+03 | 4.9e+02 | 3.4e+03 | 44 |

| 95 | FRANKLIN ADVISERS INC | Franklin Adv. | 3.6e+02 | 4.7e+02 | 0 | 0 | 0 | 0 | 3.6e+02 |

| 96 | ABN AMRO BANK NV | NL049 | 1.5e+03 | 2.8e+02 | 0 | 1.3e+03 | 0 | 1.1e+02 | 1.3e+02 |

| 97 | MUENCHENER RV | Munich RV | 8.2e+03 | 2.3e+04 | 5.8e+02 | 3.6e+03 | 4.2e+02 | 1.9e+03 | 1.8e+03 |

| 98 | HSH NORDBANK AG, HAMBURG | DE025 | 1e+03 | 4.8e+03 | 1e+02 | 6.6e+02 | 62 | 1.8e+02 | 0 |

| 99 | GRUPO BANCA CIVICA | ES071 | 4.8e+03 | - | 5.4 | 0 | 0 | 4.7e+03 | 0 |

| 100 | CAIXA GERAL DE DEPOSITOS, SA | PT053 | 6.8e+03 | 5.3e+03 | 51 | 0 | 6.5e+03 | 2e+02 | 23 |

| 101 | CAJA DE AHORROS DEL MEDITER… | ES083 | 5.6e+03 | 3.8e+03 | 0 | 20 | 4.8 | 5.6e+03 | 15 |

| 102 | GRUPO BMN | ES068 | 3.7e+03 | - | 0 | 0 | 88 | 3.6e+03 | 0 |

| 103 | BANK OF IRELAND | IE038 | 5.6e+03 | 1e+04 | 0 | 30 | 0 | 0 | 5.6e+03 |

| 104 | DEKABANK | DE028 | 6e+02 | 3.3e+03 | 87 | 2.7e+02 | 32 | 1.8e+02 | 30 |

| 105 | DEXIA | BE004 | 2.3e+04 | 3.3e+03 | 3.5e+03 | 1.6e+04 | 1.9e+03 | 1.5e+03 | 0.34 |

| 106 | GRUPO BBK | ES075 | 3.1e+03 | - | 0 | 0 | 3 | 3.1e+03 | 4 |

| 107 | BANKINTER, S.A. | ES069 | 3.6e+03 | 3.1e+03 | 0 | 1.2 | 0 | 3.6e+03 | 0 |

| 108 | WESTLB AG, DUSSELDORF | DE024 | 2.2e+03 | 3e+03 | 3.4e+02 | 1.1e+03 | 0 | 7.5e+02 | 35 |

| 109 | UNIONE DI BANCHE ITALIANE SCPA | IT044 | 1.1e+04 | 1.1e+04 | 25 | 1.1e+04 | 0 | 0 | 0 |

| 110 | CAJA DE AHORROS Y M.P. | ES072 | 3.3e+03 | 2.7e+03 | 0 | 3.8e+02 | 0 | 2.9e+03 | 0 |

| 111 | CAIXA D’ESTALVIS UNIO DE CAIXES | ES076 | 2.6e+03 | - | 0 | 11 | 0 | 2.6e+03 | 13 |

| 112 | BANK OF CYPRUS PUBLIC CO | CY007 | 2.8e+03 | 2.4e+03 | 2.4e+03 | 36 | 0 | 58 | 3.2e+02 |

| 113 | LANDESBANK BERLIN AG | DE027 | 1.1e+03 | 2.3e+03 | 4.5e+02 | 3.3e+02 | 0 | 3.7e+02 | 0.075 |

| 114 | ALPHA BANK | GR032 | 5.5e+03 | 2e+03 | 5.5e+03 | 0 | 0 | 0 | 0 |

| 115 | UNICREDIT S.P.A | IT041 | 5.2e+04 | 9.3e+05 | 6.7e+02 | 4.9e+04 | 94 | 1.9e+03 | 58 |

| 116 | MARFIN POPULAR BANK PUBLIC CO | CY006 | 3.4e+03 | 1.7e+03 | 3.4e+03 | 0 | 0 | 0 | 39 |

| 117 | BANCO PASTOR, S.A. | ES074 | 2.6e+03 | 1.6e+03 | 41 | 1e+02 | 1.2e+02 | 2.3e+03 | 0 |

| 118 | GRUPO CAJA3 | ES078 | 1.5e+03 | - | 0 | 0 | 0 | 1.5e+03 | 8.4 |

| 119 | TT HELLENIC POSTBANK S.A. | GR035 | 5.3e+03 | 9.3e+02 | 5.3e+03 | 0 | 0 | 0 | 0 |

| 120 | EFG EUROBANK ERGASIAS S.A. | GR030 | 8.9e+03 | 8.8e+02 | 8.8e+03 | 1e+02 | 0 | 0 | 0 |

| 121 | ESPIRITO SANTO GROUP, | PT055 | 3.1e+03 | 6.2e+03 | 3.1e+02 | 0 | 2.7e+03 | 55 | 0 |

| 122 | AGRICULTURAL BANK OF GREECE | GR034 | 7.9e+03 | 7.5e+02 | 7.9e+03 | 0 | 0 | 0 | 0 |

| 123 | CAJA DE AHORROS DE VITORIA | ES080 | 6e+02 | - | 0 | 0 | 0 | 6e+02 | 0 |

| 124 | ING BANK NV | NL047 | 1.1e+04 | 3.5e+04 | 7.5e+02 | 7.7e+03 | 7.6e+02 | 1.9e+03 | 92 |

| 125 | RABOBANK NEDERLAND | NL048 | 1.1e+03 | - | 3.8e+02 | 4.4e+02 | 82 | 1.6e+02 | 60 |

| 126 | WUERTTEMBERGISCHE LV | Wuetter. LV | 7.7e+02 | 1.2e+02 | 85 | 4.5e+02 | 52 | 1.8e+02 | 8 |

| 127 | NYKREDIT | DK011 | 1.1e+02 | - | 22 | 88 | 0 | 0 | 0 |

| 128 | MONTE DE PIEDAD Y CAJA | ES073 | 3.3e+03 | 58 | 6 | 3.1e+02 | 0 | 2.9e+03 | 0 |

| 129 | CAJA DE AHORROS Y M.P. | ES081 | 6 | 58 | 0 | 0 | 0 | 6 | 0 |

| 130 | BANCA MONTE DEI PASCHI DI | IT042 | 3.3e+04 | 1.9e+03 | 8.1 | 3.2e+04 | 2e+02 | 2.8e+02 | 0 |

| 131 | COLONYA - CAIXA D’ESTALVIS DE | ES082 | 26 | - | 0 | 0 | 0 | 26 | 0 |

| 132 | BANQUE ET CAISSE D’EPARGNE DE | LU045 | 2.8e+03 | 2.9e+03 | 85 | 2.4e+03 | 1.8e+02 | 1.7e+02 | 0 |

| 133 | PIRAEUS BANK GROUP | GR033 | 8.2e+03 | -1.9e+03 | 8.2e+03 | 0 | 0 | 0 | 0 |

| 134 | NATIONAL BANK OF GREECE | GR031 | 1.9e+04 | -4.3e+03 | 1.9e+04 | 0 | 0 | 0 | 18 |

| 135 | ZURICH FINANCIAL | Zurich | 8.7e+03 | 2.5e+04 | 0 | 4.2e+03 | 3.7e+02 | 3.7e+03 | 3.7e+02 |

| 136 | MITSUI | Mitsui | 6.4e+02 | 6.9e+04 | 0 | 3.7e+02 | 25 | 1.7e+02 | 76 |