A backward dual representation for the quantile hedging of Bermudan options

Abstract

Within a Markovian complete financial market, we consider the problem of hedging a Bermudan option with a given probability. Using stochastic target and duality arguments, we derive a backward algorithm for the Fenchel transform of the pricing function. This algorithm is similar to the usual American backward induction, except that it requires two additional Fenchel transformations at each exercise date. We provide numerical illustrations.

Keywords: stochastic target problems, quantile hedging, Bermudan options.

AMS 2010 Subject Classification Primary, 91G20, 91G60 ; Secondary, 60J60, 49L20.

1 Introduction

We study the problem of hedging a claim of Bermudan style with a given probability . More precisely, we want to characterize the minimal initial value of an hedging portfolio for which we can find a financial strategy such that, with a probability , it remains above the exercise value of the Bermudan option at any possible exercise date.

This problem is referred to quantile hedging, and it was popularized by Föllmer et al. [12, 13] . For claims of European type, they explained how the so-called quantile hedging price can be computed explicitly when the market is complete, by using duality arguments or the Neyman-Pearson lemma. A similar question was studied in Bouchard et al. [6] but in a Markovian setting. They showed that, even in incomplete markets and for general loss functions, one can characterize the pricing function as the solution of a non-linear parabolic second order differential equation, by using tools developed in the context of stochastic target problems by Soner and Touzi [17]-[18]. When the market is complete, they also observed that taking a Legendre-Fenchel transform in the equation reduces the computation of the price to the resolution of a linear parabolic second order differential equation, which can be solved explicitly by using the Feynman-Kac formula.

As far as super-hedging is concerned, the pricing of a Bermudan option reduces to a backward sequence of pricing problems for European claims. It is therefore natural to ask whether a similar result holds for the quantile hedging price, and whether one can extend the closed-form solutions of [12] and [6] to Bermudan options.

This paper answers to the positive. Namely, we provide a backward induction algorithm for the Fenchel transform of the quantile hedging price , with respect to the parameter which prescribes the probability of hedging, see (2.27) and Theorem 2.1. The algorithm (2.27) is in a sense very similar to the one used for the pricing of Bermudan options. It is however written on the Fenchel transform , rather than , and it involves two additional Fenchel transformations at each exercise date.

To derive this, we first build on the original idea of [6] which consists in increasing the state space in order to reduce to a stochastic target problem of American type, as studied in Bouchard and Vu [8]. We then follow a very different route. Instead of appealing to stochastic target technics, we derive from this formulation a first dynamic programming algorithm for , see Proposition 2.3, which relates to a series of optimal control of martingale problems. This dynamic programming principle suggests a backward algorithm for the computation of the Fenchel transform. It is defined in (2.27). We analyze it in details in Section 3.2. The main difficulty consists in controlling the propagation of the differentiability and growth properties of the corresponding value function, backward in time. Then, as in [6, 12], a martingale representation argument allows us to show, by backward induction, that the algorithm in (2.27) and Proposition 2.3 provides the Fenchel transform of one another.

Before concluding this introduction, we would like to point out that a similar problem has been studied recently by Jiao et al. [14] in the form of general lookback-style contraints. They provide an alternative formulation in terms of an optimal control of martingale problems. This has to be compared with [5] and our Proposition 2.3. No Markovian structure is required, but they do not provide an explicit scheme as we do. Moreover, the smoothness conditions they impose on their loss functions are not satisfied in the quantile hedging case. They also study the case of several constraints in expectation set (independently) at the different exercise times, which is close to the P&L matching problems of Bouchard and Vu [7].

Finally, in this paper, we focus on the quantile hedging problem for sake of simplicity. It is an archetype of an irregular loss function, and it should be clear that a similar analysis can be carried out for a wide class of (more regular) loss functions. Also note that to obtain the dual algorithm, we only use probabilistic arguments which opens the door to the study of more general non-Markovian settings.

Notations: Let be a positive integer. Any vector of is seen as a column vector. Its norm and transpose are denoted by and . We set and denote by the transpose of , while is its trace. For ease of notations, we set .

We fix a finite time horizon . Let . If it is smooth enough, we denote by and its derivative with respect and , and by its Jacobian matrix with respect to , as a column vector. The Hessian with respect to is , is the second order derivative with respect to , and is the vector of cross second order derivatives. We denote by its Fenchel transform with respect to the last argument,

| (1.1) |

and define

If is convex with respect to its last variable, we denote by and its corresponding right- and left-derivatives. We refer to [15] for the various notions related to convex analysis.

We fix a complete probability space supporting a -dimensional Brownian motion . We denote by the usual augmented Brownian filtration. All over the paper, inequalities between random variables have to be understood in the -a.s. sense.

2 Problem formulation and main results

2.1 Financial market and hedging problem

Our financial market consists in a non-risky asset, whose price process is normalized to unity, and risky assets whose dynamics are given by

| (2.1) |

given the initial data . To ensure that the above is well-defined, we assume that

| (2.2) |

and that the unique strong solution to (2.1) takes its values in when the original data lies in .

In order to enforce the absence of arbitrage and the completeness of the financial market, we also impose that

| (2.3) | ||||

The Lipschitz continuity condition is not required to define the risk neutral measure111 denotes here the Doléans-Dade exponential.

| (2.4) |

but will be used in some of our forthcoming arguments.

In this model, an admissible financial strategy is a -dimensional predictable process such that

| (2.5) |

and the corresponding wealth process remains non-negative

given the initial data of the market and the initial dotation . We denote by the collection of admissible financial strategies. As usual, each should be interpreted as the number of units of asset in the portfolio at time .

We now fix a finite collection of times

together with payoff functions

| (2.6) |

Our quantile hedging problem consists in finding the minimal initial wealth which ensures that the stream of Bermudan payoffs can be hedged with a given probability ,

| (2.7) |

where

Observe that must be interpreted as a continuation value, i.e. the price at time knowing that the option has not been exercised on . In particular, . For , coincides with the continuation value of the super-hedging price of the Bermudan option. In this complete market, it satisfies the usual dynamic programming principle

| (2.9) |

see [16]. Above and in the following, we use the notation

Note that can also be formulated in terms of stopping times, see the Appendix for the proof.

Proposition 2.1.

For ,

| (2.12) |

in which is the set of stopping times with values in , and .

Remark 2.1.

The function is non-decreasing. It takes the value if where

| (2.13) |

with the convention . To avoid trivial statements, we assume that , for , which implies

| (2.14) |

Moreover, it follows from (2.6) that we can find such that , for , . This implies that we can restrict to strategies such that

| (2.15) |

by possibly adopting a buy-and-hold strategy after the first time at which the wealth process hits the right-hand side term, recall that has positive components. In particular,

| (2.16) |

2.2 Equivalent formulation as a stochastic target problem

The first step in our analysis consists in reducing the problem to a stochastic target problem of American type as studied in [8]. As in [6], we first increase the dimension of the controlled process by introducing the family of martingales

where is a square integrable predictable process. The process will be later on interpreted as the conditional probability of success. It is therefore natural to restrict to the class of controls such that

We denote by the set of predictable square integrable processes such that the above holds, and set .

Proposition 2.2.

Fix , then

| (2.17) |

Proof. At time both sets are by definition of . We now fix . Let denote the right-hand side in (2.17) and let be one of his elements. Fix such that on . Then, on . Since and therefore , this implies

The process being a martingale, , . Hence

Therefore, and this argument proves that .

We now fix and choose such that . By the martingale representation theorem, we can find such that

By possibly replacing by the constant process after the first time after at which reaches the level , we can assume that . Moreover, the above implies

which by taking the conditional expectation and using the fact that is a martingale leads to on . The latter is equivalent to on . Hence, .

2.3 Dynamic programming and dual backward algorithm

With the formulation obtained in Proposition 2.2 at hand, one can now derive a first dynamic programming algorithm. Its proof is postponed to the Appendix.

Proposition 2.3.

Fix and ,

| (2.18) |

As a consequence, there exists such that

| (2.19) |

for all and .

Remark 2.2.

Note that this provides a first way to compute the value function . Indeed, standard arguments (see [6]) should lead to a characterization of on each interval , and on as a viscosity solution of

| (2.20) |

with the boundary conditions

| (2.21) | |||

| (2.22) |

However, the fact that the control in the above is not bounded (as it comes from the martingale representation theorem) makes the associated Hamilton-Jacobi-Bellman operator in (2.20) discontinuous. More precisely it is lower semi-continuous but not upper semi-continuous and a precise statement would then require a relaxation of the operator in (2.20). This discontinuity makes the proof of a comparison result very difficult and the latter is necessary to build convergent numerical schemes. One way to overcome this problem is to consider instead the Fenchel transform of , see (1.1) in the notations section.

Indeed, heuristically, as already observed in [6] in the case , a change of variable argument in (2.20) and the exploitation of the boundary conditions in (2.22) suggests that the dual function should be at least a viscosity sub-solution of the linear partial differential equation

| (2.23) |

on the different time steps, and of the following boundary condition obtained by taking the Fenchel transform in (2.21)

| (2.24) |

By the Feynman-Kac representation this corresponds to the following representation

The aim of this paper is actually to prove by using probabilistic arguments only that on

| (2.27) |

with defined in (2.4), is the proper algorithm to compute the value function and thus .

Indeed our main result is given by the following theorem.

Theorem 2.1.

on .

The proof of this result is the object of the subsequent sections. Although it is in the spirit of [6], our proof is different and more involved. The main difficulty comes from the induction. At each time step, we have to verify that behaves in a sufficiently nice way. In the one step case, [6] had only to consider the terminal payoff . Moreover, we only use probabilistic arguments as opposed to PDE arguments.

Clearly, the algorithm (2.27) provides a way to compute the value function easily. One can for instance use the fact that is the unique viscosity solution of (2.23) with the boundary condition (2.24). Let us make this statement more precise.

Definition 2.1.

We say that a lower-semicontinuous function is a viscosity super-solution of the system () if, on each , , it is a viscosity super-solution of (2.23) with the boundary conditions

We define accordingly the notion of sub-solution for upper-semicontinuous functions. A function is a viscosity solution if its lower- (resp. upper-) semicontinuous envelope is a viscosity super- (resp. sub-) solution.

Note that in the above definition we have to understand as being on to compute the Fenchel transforms involved in the time boundary conditions.

We now provide a version of the comparison principle for () which pertains for the usual extensions of the Black and Scholes model. The assumptions used below are here to avoid the boundary of - when this is not the case, one has to specify additional boundary conditions.

Proposition 2.4.

The function is continuous on , non-negative, has linear growth in its last variable and is a viscosity solution of (). Moreover, if there exists two functions and such that and , then on whenever and are respectively a super- and a sub-solution of (), which are non-negative and have linear growth in their last variable on .

The proof is postponed to the Appendix. Given the latter, it is not difficult to follow the arguments of [3] to construct a convergent finite difference scheme for the resolution of . Alternatively, one could also use quantization methods to tackle the approximation of , see [1, 2], or a regression based Monte-Carlo method, see the survey paper [9] and the references therein.

2.4 Examples of application

In this section, we present two examples of application. The numerical results

are obtained using the following procedure which is based on the above

algorithm to compute : for ,

1) compute the value of by

approximating the Fenchel-Legendre transform numerically,

2) solve the PDE (2.23)-(2.24) for ,

using e.g. finite difference methods, on .

We now fix and . We work in a Black-Scholes setting with market parameters: , , .

For our first numerical application, we consider a put option, i.e. , with strike .

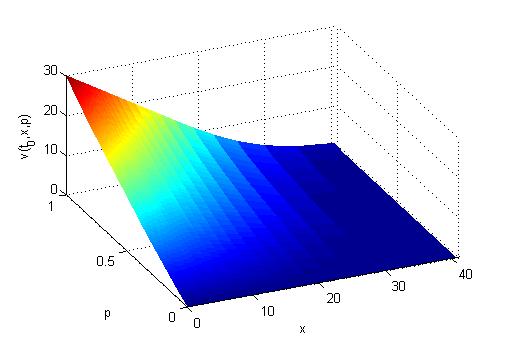

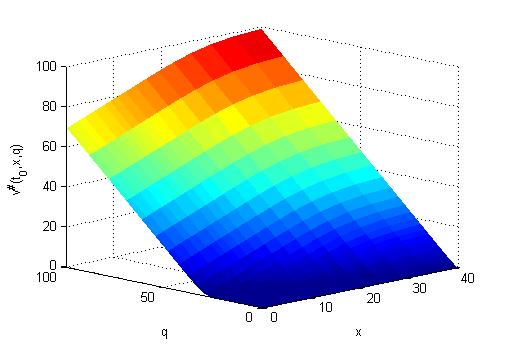

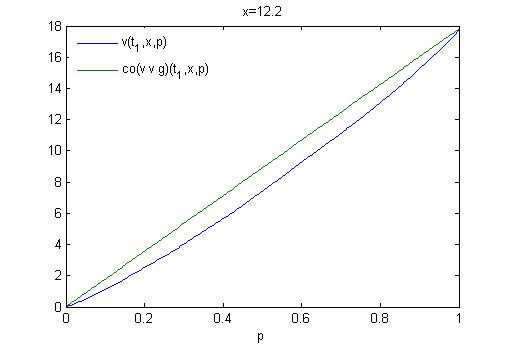

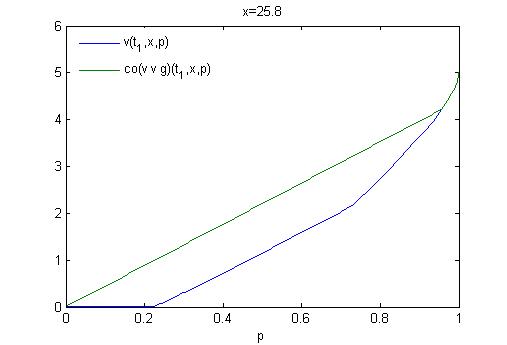

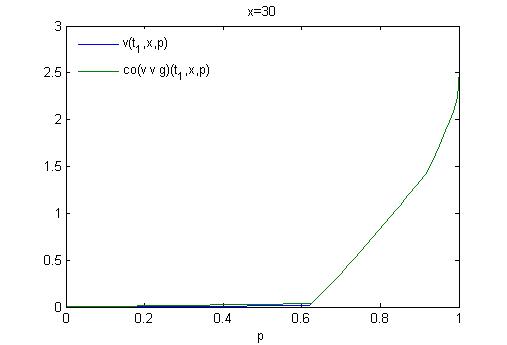

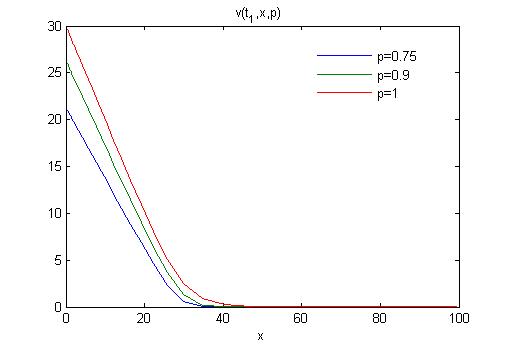

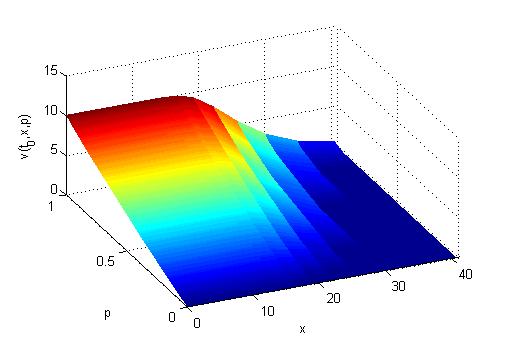

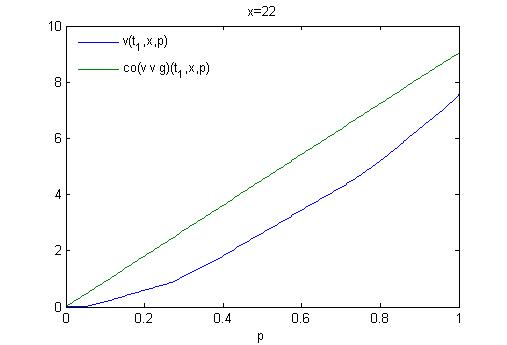

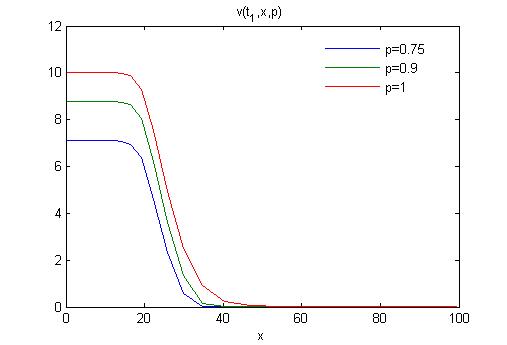

In figure 1, we plot the functions and at . In figure 2(a-b-c), we plot for different values of the function and . This shows the rather complicated behavior of the transformation , as predicted by Proposition 3.3(b) below. With the notation of this proposition, figure 2(a) corresponds to the case , figure 2(b) corresponds to the case and figure 2(c) corresponds to the case . Because of the interest rate being set to and the payoff being convex, we always have . Figure 2(d) shows the decrease of value for , when decreases.

|

|

| (a) | (b) |

|

|

| (a) | (b) |

|

|

| (c) | (d) |

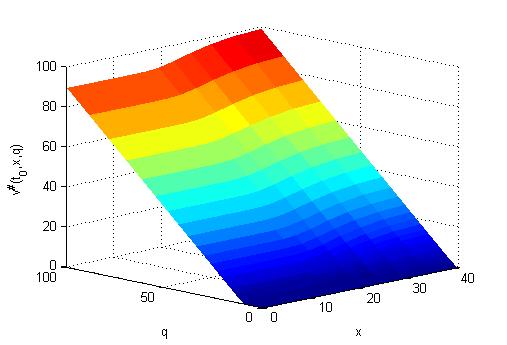

In our second example, we consider a put spread option with strikes and , i.e. . The numerical results are displayed in Figure 3 and 4. It may happen here that , see figure 4(a).

|

|

| (a) | (b) |

|

|

| (a) | (b) |

We conclude this section with the following remark on the behavior of near .

3 Proof of the backward dual representation

From now on, we extend to by setting

| (3.1) |

Using the convention , this extension is consistent with (2.7).

3.1 The backward algorithm as a lower bound

We first show that the backward algorithm (2.27) actually provides a lower bound for the value function .

Proposition 3.1.

on .

Proof. First note that , by definition. Thus, . We now assume that on for some . Then, and therefore

Fix . Taking the expectation on both sides and recalling (2.27), we obtain

Taking first the supremum over in the right-hand side and then the infimum over in the left-hand side, we get from Proposition 2.3 that .

3.2 Representation and differentiability of the backward dual algorithm

This section is devoted to the study of the function which appears in the dual algorithm (2.27) and of its Fenchel transform . We first provide a decomposition in simple terms in Proposition 3.3. They only contain and auxiliary functions that are easy to handle, see (3.3)-(3.4) below. In view of (2.27), this will then allow us to study the subdifferential of in terms of the subdifferential of . This analysis is reported in Lemma 3.2. These results will be of important use in the final proof of Theorem 2.1 as it will require to find a particular value in the subdifferential of and then to apply a martingale representation argument between elements of the subdifferential of at and at , see the proof of Theorem 3.1.

We start with properties that stem directly from the definition of and standard results in convex analysis. The proof is postponed to the Appendix.

Proposition 3.2.

The following holds for all .

(a) The functions is a proper convex non-decreasing and non-negative function. Moreover, and for .

(b) The function and are convex, non-negative, non-decreasing and continuous on their respective domains. Moreover, and for .

The next result is key to get the representation of and . Recall that .

Lemma 3.1.

Let and be a non-decreasing convex function such that ,

on , on

.

(a) The convex envelope of is given by

with .

(b) Moreover, we have

which is a closed proper convex function. In particular, it is continuous at when .

Proof.

1. The left-hand side identity in (a) follows from [15, Theorem

12.2].

We set , which is

convex.

By assumption, we already know that for .

Since and , we have by convexity that

, , which implies , for .

Since for and , we compute that

. By convexity, we also have

for and then

. In particular, we observe that

. It is straightforward to check that any candidate for

the convex envelope of is below . The above shows also that whenever .

2. Let us now observe that , for , since for . It follows that the subdifferential of at non-negative is non empty. The

proof of (b) follows from calculations based on the following results from

convex analysis, see e.g. [11, Chapter I Proposition 5.1]. Let

be a proper function on , then

is in the subdifferential of at if and only if

| (3.2) |

(i) At , the subdifferential of is equal to . This follows directly from the characterization of the convex envelope of given in (a). Using the above equality with , we then have for

since by our assumption,

namely and .

(ii) The subdifferential of at

is equal to if

or otherwise. This follows again

directly from (a). We recall from the step 1. that . Then,

using (3.2) with and (a), we

have for

(iii) If , an element of the subdifferential of at satisfies

We first note that necessarily. Indeed, by [11, Chapter I Corollary 5.2], while . Recall that on . We then deduce from the previous equality that

Observing that the reverse inequality follows from , we get for .

We are now in position to provide the decomposition of and . It basically follows from the application of the previous Lemma to .

Proposition 3.3.

For , we define the following ‘facelift’ of

with

Then,

-

(a)

The function is continuous on its domain and

(3.3) -

(b)

For all :

(3.4) where

with and the subsets of : , , .

Remark 3.1.

Proof of Proposition 3.3. The identities in (3.3) are immediate consequences of Lemma 3.1(a), Proposition 3.2(b) and of the definition of . We now prove (3.4). For , we have and therefore on . For , we have that by Proposition 3.2(b) and the result follows directly. On , the expression is exactly the one given by Lemma 3.1(b).

We can now turn to the study of the subdifferential of . Recall the definition of in (2.13).

Lemma 3.2.

Fix and . Then:

(a) if and

if ,

(b) ,

(c) .

Moreover,

| (3.5) | ||||

| (3.6) |

Proof. The proof is based on an induction argument. Our assumptions guarantee that (a)-(b)-(c) are valid at . Let us assume that it holds true on for some .

We have by induction , which ensures that . By the convexity of , this implies that . In view of (2.27), a dominated convergence argument then leads to (3.5)-(3.6) and .

We now use our induction hypothesis again to observe from the decomposition above that

3.3 The backward algorithm as an upper-bound

Our final proof will proceed by backward induction on the time steps. Fix . Part of the induction hypothesis is:

Hypothesis ().

The following holds

-

(i)

The functions and are continuous on .

-

(ii)

and .

-

(iii)

For all , the map is non-decreasing, continuous and converges to as .

Before turning to the final argument, we provide three additional results that hold at any time whenever is in force.

3.3.1 Bounds and limits for

Our first additional result concerns the behavior of . It shows that . The last assertion will be used in the proof of Lemma 3.4 below to show that (iii) of holds if (iii) of does.

Lemma 3.3.

Let iii of hold. Fix . Then, is non-negative, continuous on its domain and

Moreover, the map is non-decreasing, continuous on and converges to as .

Proof. The continuity and non-negativity of are stated in (b) of Proposition 3.2. We now observe that (2.27) implies that

which shows that is non-decreasing since (iii) of holds. Applying the monotone convergence Theorem, iii of and (2.9), we obtain that is continuous and that

This implies that , while for . The fact that has been proved in Proposition 3.1.

3.3.2 Convexification in the dynamic programming algorithms

As already mentioned in Remark 2.2, one can expect that can be replaced by its convex envelope, with respect to , in (2.18). The Hypotheses i-ii of ensure this, see Proposition 3.4 below. We shall prove a similar result for later on in Theorem 3.1. Note that the two identities (3.7) and (3.11) below already suggest that the equality at should iterate at , since we already know from Proposition 3.1 that .

Proposition 3.4.

Proof. We fix . Assuming that (3.7) is true, we deduce that ii of holds, since for and therefore for . By ii of , the same argument combined with Proposition 2.3 implies that (3.7) is valid for .

It remains to prove (3.7) for . In view of Proposition 2.3, this reduces to showing that

the reverse inequality being trivial. We argue as in [5, Proof of Proposition 3.3]. It follows from the Caratheodory theorem that we can find two maps , , such that

| (3.10) |

We claim that they can be chosen in a measurable way. More precisely, i of and [4, Proposition 7.49] imply that they can be chosen to be analytically measurable. We can then appeal to [4, Lemma 7.27] to obtain a Borel-measurable version which coincides a.e. for the pull-back measure of , for and fixed. This is this version that we use in the following.

We now let be a -measurable random variable such that

Then, by the above construction, and we can then find such that and . Recalling (3.10), we obtain

with

recall (2.6), (2.16) and (2.19). Moreover, since , using i of , we can pass to the limit to obtain

Since our final result is , the same convexification should appear in the dual algorithm. As already mentioned, it will actually allow us to show that at if this true at .

Theorem 3.1.

Let iii of hold. Fix . Then, there exists such that

| (3.11) |

Proof. Recall the definition of in (2.13).

1. We first assume that . We know from Lemma 3.2(b)-(c) that there exists a such that lies in the subdifferential of at . Then, we can find such that . In view of (3.5)-(3.6), this implies that

| (3.12) |

It follows from Lemma 3.2 and its proof that the random variable in the expectation is valued in . By the martingale representation theorem, we can find such that

For later use, note that the above implies

| (3.13) |

where we used (3.2) with . On the other hand, we also have, again by (3.2) with ,

| (3.14) |

and, by (2.27),

| (3.15) |

Thus, inserting (3.12) and (3.15) into (3.14), and using (3.13), leads to

We conclude by appealing to (3.3).

3.4 Conclusion of the proof

To conclude the proof of Theorem 2.1, we need to prove the inequality .

Proposition 3.5.

on .

Proof. We use a backward induction argument. We assume that holds and that and on for some . Since it is true for by construction, the proof will be completed if one can show that this implies that holds and that on .

Let us fix . Then, our induction hypothesis implies that

for all . It then follows from Theorem 3.1 and Proposition 3.4 that . But, the reverse inequality is proved in Proposition 3.1. This shows that on . Then (i) of is a consequence of Proposition 3.3 and Proposition 3.2. Proposition 3.4 implies (ii) of . Regarding the validity of (iii) of , it is proved in Lemma 3.4 below.

Lemma 3.4.

The hypothesis implies iii of .

Proof. It follows from (3.4) that

| (3.16) |

in which

By Lemma 3.3, so that , recall (2.14). In particular, we observe that on . The fact that the right-hand side in (3.4) converges to as is then a consequence of Lemma 3.3 and the definition of the .

It remains to show that each term in (3.4) is non-decreasing and continuous. From Lemma 3.3, we know that is continuous and non-decreasing. The second term in the right-hand side of (3.4) is continuous and non-decreasing as well. As for the last term, we know that is continuous, so that it suffices to check the monotony on each sub-interval and distinctly. On the second interval, we have that is non-decreasing by Lemma 3.3. This is also true on first interval since .

4 Appendix

We provide here the proofs of some technical results that were used in the proof of Theorem 2.1.

Proof of Proposition 2.1 For the sets in (2.12) are by definition of and . For , the definition of implies , while , for any . Hence, for ,

where, in the last implication, we used the fact that . This proves (2.12) for .

Proof of Proposition 2.3. 1. We first show that (2.18) holds. Let denote the right-hand side of (2.18) and set

Fix and such that Then, it follows from the martingale representation theorem that we can find such that

In particular, . Since, we also have , it follows from the same arguments as in the proof of [8, Lemma 2.2] that we can find a predictable process which coincides with on , in the -sense, and such that

These processes are elements of whenever is square integrable in the sense of (2.5) and is such that . The latter can be modified so that is restricted to live in the interval while can be modified so that (2.15) holds. By the Itô isometry, this induces the required square integrability property of the financial strategy, recall (2.2)-(2.3). Combining the above with Proposition 2.2 shows that .

Conversely, let us fix . Then, it follows from the geometric dynamic programming principle of [8, Theorem 2.1] that there exists such that

Since is a super-martingale under , this implies that . The fact that then follows from the arbitrariness of .

2. We now prove the Lipschitz continuity property. Note that it is true for , since by construction. Let us assume that (2.19) holds on for some and show that it is then also true on . Let us fix and . We have that for all

Using first (2.6), the linear growth of (see (2.16)) together with the fact that (2.19) holds for , and using then (2.18), we deduce that there exists such that is bounded by

In view of (2.2)-(2.3), this is controlled by up to a multiplicative constant.

Proof of Proposition 2.4. The growth property on follows from Proposition 3.2 (which will be proved just below), Theorem 2.1, (3.1) and (2.16),

Note that Theorem 2.1 implies that . The fact that the lower- (resp. upper-) semicontinuous envelope of is a viscosity super- (resp. sub-) solution of () is standard and we omit the proof. Continuity will then follow from the comparison principle. The comparison can be proved by backward induction. It is well-known that (2.23) admits a comparison principle in the class of functions with polynomial growth, see e.g. [10]. Hence, the comparison holds on . Assume that it holds on and that has polynomial growth, for , then it holds on too since implies . Hence, we just have to prove that has polynomial growth. By [15, Theorem 16.5], we have . Since and the later has polynomial growth, the required property holds.

Proof of Proposition 3.2. We proceed by backward induction on . Our claims are straightforward from (2.27) at time . Indeed, direct computations show that . Hence, . The properties (a) and (b) hold.

We now assume that (a) and (b) are satisfied on for some and fix . Then, the definition of in (2.27) implies that is non-negative, non-decreasing, convex and that (it is in particular proper). It takes the value for , by (2.27) and the fact that for . Hence (a) holds on . These two last assertions imply that and for . We know from [15, Theorem 12.2] that it is closed, convex and continuous on the interior of its domain. Since is non-decreasing, by definition, we get from its closeness that it is continuous on its domain. The fact that also implies that is non-negative; moreover, . For , we then compute . For , we get . Moreover, non-decreasing on . By definition, is closed, convex and continuous on the interior of its domain. Being non-decreasing and closed, it is in fact continuous on its domain.

References

- [1] Vlad Bally and Gilles Pagès. Error analysis of the quantization algorithm for obstacle problems. Stochastic Processes and their Applications, 106(1):1–40, 2003.

- [2] Vlad Bally and Gilles Pagès. A quantization method for pricing and hedging multidimensional american style options. Mathematical finance, 15(1):119–168, 2005.

- [3] Guy Barles and Panagiotis E Souganidis. Convergence of approximation schemes for fully nonlinear second order equations. Asymptotic analysis, 4(3):271–283, 1991.

- [4] Dimitri P Bertsekas and Steven E Shreve. Stochastic optimal control: The discrete time case, volume 139. Academic Press New York, 1978.

- [5] Bruno Bouchard, Romuald Elie, and Anthony Réveillac. Bsdes with weak terminal condition. The Annals of Probability, 43(2):572–604, 2015.

- [6] Bruno Bouchard, Romuald Elie, and Nizar Touzi. Stochastic target problems with controlled loss. SIAM Journal on Control and Optimization, 48(5):3123–3150, 2009.

- [7] Bruno Bouchard and Thanh Nam Vu. A stochastic target approach for p&l matching problems. Mathematics of Operations Research, 37(3):526–558, 2012.

- [8] Bruno Bouchard and Thanh Nam Vu. The obstacle version of the geometric dynamic programming principle: Application to the pricing of american options under constraints. Applied Mathematics and Optimization, 61(2):235–265, 2010.

- [9] Bruno Bouchard and Xavier Warin. Monte-carlo valuation of american options: facts and new algorithms to improve existing methods. In Numerical methods in finance, pages 215–255. Springer, 2012.

- [10] M.G. Crandall, H. Ishii, and P.L. Lions. User’s guide to viscosity solutions of second order partial differential equations. Amer. Math. Soc., 27:1–67, 1992.

- [11] Ivar Ekeland and Roger Temam. Convex analysis and variational problems, volume 1. North-Holland American Elsevier, 1976.

- [12] Hans Föllmer and Peter Leukert. Quantile hedging. Finance and Stochastics, 3(3):251–273, 1999.

- [13] Hans Föllmer and Peter Leukert. Efficient hedging: cost versus shortfall risk. Finance and Stochastics, 4(2):117–146, 2000.

- [14] Ying Jiao, Olivier Klopfenstein, and Peter Tankov. Hedging under multiple risk constraints. arXiv preprint arXiv:1309.5094, 2013.

- [15] R Tyrrell Rockafellar. Convex analysis. Number 28. Princeton university press, 1997.

- [16] Martin Schweizer. On Bermudan options. In Advances in Finance and Stochastics, 257–270, Springer, 2002.

- [17] H Mete Soner and Nizar Touzi. Stochastic target problems, dynamic programming, and viscosity solutions. SIAM Journal on Control and Optimization, 41(2):404–424, 2002.

- [18] H Mete Soner and Nizar Touzi. A stochastic representation for mean curvature type geometric flows. Annals of probability, 31(3):1145–1165, 2003.