Non–Implementability of Arrow–Debreu Equilibria by Continuous Trading under Knightian Uncertainty

Abstract

Under risk, Arrow–Debreu equilibria can be implemented as Radner equilibria by continuous trading of few long–lived securities. We show that this result generically fails if there is Knightian uncertainty in the volatility. Implementation is only possible if all discounted net trades of the equilibrium allocation are mean ambiguity–free.

Key words and phrases: Knightian Uncertainty, Ambiguity, general Equilibrium, Asset Pricing, Radner Equilibrium

JEL subject classification: D81, C61, G11

1 Introduction

A celebrated and fundamental result of financial economics characterizes the situations in which all contingent consumption plans can be financed by trading few long–lived assets; in diffusion models, asset markets are dynamically complete if the number of risky assets corresponds to the number of independent sources of uncertainty. When information is generated by a –dimensional Brownian motion, risky assets consequently suffice to span a dynamically complete market.

In such a setting, one can thus expect an equivalence between the rather heroic equilibria of the Arrow–Debreu type – where all trade takes place on a perfect market for contingent claims at time zero, and no trade ever takes place afterwards, – and the more realistic Radner equilibra where agents trade long–lived assets dynamically over time.

Such equivalence of static and dynamic equilibria for diffusion models has been established in different settings and at different levels of generality by Duffie and Huang (1985), Duffie and Zame (1989), Karatzas, Lehoczky, and Shreve (1990), Anderson and Raimondo (2008), Riedel and Herzberg (2013), Hugonnier, Malamud, and Trubowitz (2012).

In this paper, we show that this celebrated equivalence generically breaks down under Knightian uncertainty about volatility. We place ourselves in a framework which makes it as easy as possible for the market to span the equilibrium allocations. Even then, we claim, Arrow–Debreu equilibria will usually not be implementable by a dynamic market if there is Knightian uncertainty in individual endowments.

In which sense do we make it easy? First, we consider a model in which a –dimensional Brownian motion with ambiguous volatility generates the economy’s information flow. Second, as in the Duffie–Huang–approach, we consider nominal asset markets. The nominal asset structure allows for an exogenously chosen asset structure. If there is no spanning in this setting, one cannot expect spanning in the more demanding real asset setting considered by Anderson and Raimondo (2008), Riedel and Herzberg (2013), and Hugonnier, Malamud, and Trubowitz (2012) where security prices and consumption prices are endogenously determined in equilibrium and linked via the real dividend structure. Third, we consider a setting where aggregate endowment is ambiguity–free. This is the ideal starting point for an economic analysis of insurance properties of competitive markets. In this setting, a “good” economic institution should lead to an ambiguity–free allocation for all (ambiguity–averse) individuals. Indeed, we show that the efficient (and thus, Arrow–Debreu equilibrium) allocations in this Knightian economy provide full insurance against uncertainty. This generalizes the results of Billot, Chateauneuf, Gilboa, and Tallon (2000), Dana (2002), Tallon (1998) and De Castro and Chateauneuf (2011) to the continuous–time setting with non–dominated sets of priors.

We study the possibility of implementation in the so–called Bachelier model where the risky (or, in this Knigtian setting, maybe better: uncertain) asset is given by the Brownian motion itself because this case is particularly transparent. Indeed, in the classic case, one can then immediately apply the martingale representation theorem to find the portfolio strategies that finance the Arrow–Debreu (net) consumption plans. We study under what condition this result holds in an uncertain world. Under Knightian uncertainty about volatility, the martingale representation theorem changes in several aspects. Implementation is possible if and only if the value of net trades is mean ambiguity–free, or in other words, if the expected value of net trades is the same for all priors.

We thus completely clarify under what conditions one can implement Arrow–Debreu as Radner equilibria. Clearly, being free of ambiguity in the mean is weaker than being free of ambiguity in the strong sense of having the same probability distribution under all priors. Nevertheless, our result implies that “generically”, implementation will be impossible under Knightian uncertainty about volatility. We show this explicitly in the case when there is no aggregate uncertainty in the economy. The set of all endowments for which implementation fails is prevalent.333In infinite–dimensional settings, there is no obvious notion of genericity. We use the concept of prevalence (or shyness) introduced into theoretical economics by Anderson and Zame (2001) who show that it is a reasonable measure–theoretic generalization to infinite–dimensional spaces of the usual “almost everywhere”–concept in finite–dimensional contexts. Compare also Hunt, Sauer, and Yorke (1992).

An additional contribution of our paper concerns the existence of Arrow–Debreu equilibria; without existence, the question of implementation would be void. Existence is not a trivial application of the well–known results on existence of general equilibrium for Banach lattices as the informed reader might think (and the authors used to think as well). Under volatility uncertainty, the natural commodity space combines the well–known –space with some degree of continuity. In fact, the right commodity space consists of contingent claims that are suitably integrable or even bounded almost surely for all priors, and are quasi–continuous. A mapping is quasi–continuous if it is continuous in nearly all its domain. The property of quasi–continuity comes for free in the probabilistic setting: Lusin’s theorem establishes the fact that any measurable function on a nice topological space is quasi–continuous. Under volatility uncertainty, this equivalence between measurability and quasi–continuity no longer holds true. We are thus led to study a new commodity space which has not been studied so far in general equilibrium theory. Compare also the discussion of this space in the recent papers Epstein and Ji (2013), Epstein and Ji (2014) and Beißner (2014).

For this commodity space, the available existence theorems do not immediately apply. The abstract question of existence must thus be dealt with separately, but we leave the general question of existence for the future as it is not the main concern of this paper. In this paper, we use a different approach to establish existence. In our homogenous framework, one can show that the efficient allocations coincide with the efficient allocations under risk (compare the related results of Dana (2002) in a static setting). When all agents share the same prior, it is well known that the efficient allocations are independent of the prior and can be determined by maximizing a suitable weighted sum of utilities pointwise. As a consequence, the efficient allocations are continuous functions of aggregate endowment; they are quasi–continuous if aggregate endowment is quasi–continuous. This allows us to establish existence in our new commodity space where quasi–continuity is required. One can just fix any prior and choose an Arrow–Debreu equilibrium in the expected utility economy where all agents use this prior. These equilibria are also equilibria under Knightian uncertainty. As a by–product, we obtain indeterminacy of equilibria, as in related Knightian settings, such as Tallon (1998), Dana (2002), Rigotti and Shannon (2005), or Dana and Riedel (2013).

The paper is set up as follows. The next section describes the economy. Section 3 studies efficient allocations and Arrow–Debreu equilibria. Section 4 contains our main results on (generic non–)implementability. Section 5 concludes. The appendix contains additional material on Knightian uncertainty in continuous time.

2 The Economy under Knightian Uncertainty

We consider an economy over the time interval with Knightian uncertainty.

There is a finite set of agents agents in the economy who care only about consumption at terminal time . The agents share a common view of the uncertainty in their world in the sense that they all agree on the same set of priors on the state space of possible trajectories for the canonical –dimensional Brownian motion .

Quite general specifications are possible here, and we discuss some of them in the last section. To have a concrete model, we start here with volatility uncertainty for independent Brownian motions. Let for . models the possible values of the volatilities of our ambiguous Brownian motion . The set of priors consists of all probability measures that make a martingale such that the covariation between any and satisfies for all –a.s. In our concrete case, this means that the covariation between two different Brownian motions vanishes and the variation of a Brownian motion satisfies for all .

The set of priors is not dominated by a single probability measure. In such a context, sets that are conceived as null by the agents cannot be identified with null set under one probability measure. Indeed, as possible scenarios are described by a whole class of potentially singular priors, an event can only be considered as negligible or null when it is a null sets under all priors simultaneously. Such sets are called polar sets; the corresponding sure events, those that have probability one under all priors, are called quasi–sure events.

These issues require a reconsideration of some measure theoretic results. Under risk, a measurable function is “almost” continuous in the sense that for every there is an open set with probability at least such that the function is continuous on ; this is Lusin’s theorem. Under non–dominated Knightian uncertainty, this Lusin property, or quasi–continuity, does not come for free from measurability, and one needs to impose it. We refer to Epstein and Ji (2013) and Denis, Hu, and Peng (2011) for the financial and measure–theoretic background.

A proper commodity space under non–dominated Knightian uncertainty then consists of all bounded quasi–continuous functions; it is denoted by . The boundedness assumption of endowments is made for ease of exposition and to keep the arguments as concise as possible for our aims; it can be relaxed, of course, as we discuss later on. The consumption set, denoted by , consists of quasi-surely positive functions in .

Agents’ preferences are given by Gilboa–Schmeidler–type expected utility functionals of the form

for nonnegative consumption plans and a Bernoulli utility function

which is concave, strictly increasing, sufficiently smooth, and satisfies the Inada condition

In the following, we will denote by the economy we just described and refer to it as the Knightian economy to distinguish it from expected utility economies later on. In the economy , agents use expected utility for a particular common prior ; otherwise, the economy has the same structure as .

Agents have an endowment which is bounded and bounded away from zero quasi–surely.

In the following, we consider a situation where the market can potentially insure individuals against their idiosyncratic ambiguity because ambiguity washes out in the aggregate. We explicitly do allow for aggregate (and individual) risk.

Definition 2.1

is ambiguity–free (in the strong sense) if has the same probability distribution under all priors .

We assume throughout this paper that aggregate endowment is ambiguity–free in the strong sense. We thus make it as easy as possible for the market to provide insurance.

3 Efficient Allocations and Arrow–Debreu Equilibria with No Aggregate Ambiguity

Before considering the possibility or impossibility of implementing Arrow–Debreu equilibria by trading few long-lived assets, we need to study existence and properties of equilibria in our context. It will turn out that efficient allocations, and a fortiori Arrow–Debreu equilibrium allocations are ambiguity–free. If we allow for a complete set of forward markets at time zero, the market is thus able to ensure all individuals against their idiosyncratic Knightian uncertainty.

We recall the structure of efficient allocations in the homogenous expected utility case. If all agents agree on one particular probability , the efficient allocations are independent of that ; indeed, they are characterized by the equality of marginal rates of substitution. For weights , the efficient allocation maximizes pointwise the sum

over all vectors with . It is characterized by the first–order conditions

for all agents with strictly positive weights ; the agents with weight zero consume zero, of course. Due to our assumptions, one can then write the efficient allocations as a continuous function

of aggregate endowment. In the following, we denote by the simplex of weights that sum up to and by the set of efficient allocations in homogenous expected utility economies.

Theorem 3.1

-

1.

Every efficient allocation in is ambiguity–free.

-

2.

The efficient allocations in the Knightian economy coincide with the efficient allocations in homogenous expected utility economies and are independent of a particular prior .

Proof: Note that the efficient allocations in homogenous expected utility economies are ambiguity–free as they can be written as monotone functions of aggregate endowment. As these functions are continuous, they are also quasi–continuous in the state variable and thus do belong to our commodity space.

We first show that these allocations are also efficient in our Knightian economy. Fix some weights and fix some . Let be a feasible allocation. Then we have

As maximizes the weighted sum of utilities pointwise, we continue with

Now is ambiguity–free, hence we have for all and thus . We conclude that maximizes the weighted sum of Gilboa–Schmeidler utilities. It is thus efficient.

Now let be another efficient allocation. By the usual separation theorem, it maximizes the weighted sum of utilities

for some . Set

Due to our strict concavity assumptions, we have

for all . Now assume that is not a polar set. Then there is with . Therefore, we have

Since is ambiguity–free, . On the other hand, by ambiguity–aversion,

and we obtain a contradiction. We thus conclude that is a polar set and thus quasi–surely.

The preceding theorem obtains the same characterization of efficient allocations in our Knightian case as Dana (2002) does for Choquet expected utility economies. The argument is different, though: as our set of priors does not lead to a convex capacity, one cannot use the comonotonicity of efficient allocations to identify a unique worst–case measure for the agents. Instead, we rely on aggregate endowment being ambiguity–free to reach the conclusion that all efficient allocations are ambiguity–free and coincide with the efficient allocations of any expected utility economy in which all agents share the same prior. Moreover, we do not have a dominating measure here.

As a consequence of the theorem we obtain the following generalization of Billot, Chateauneuf, Gilboa, and Tallon (2000) to our non–dominated setting.

Corollary 3.2

If there is no aggregate uncertainty, i.e. quasi–surely, then all efficient allocations are full insurance allocations.

Let us now turn to Arrow–Debreu equilibria. In the first step, it is important to clarify the structure of price functionals. A price is a positive and continuous linear price functional on the commodity space . A typical representative of these price functionals has the form of a pair where is the state–price density as in the expected utility case and is some particular prior in . Knightian uncertainty adds the new feature that the market also chooses the measure .

An Arrow–Debreu equilibrium consists then of a feasible allocation and a price such that for all the strict inequality implies .

We are going to show that Arrow–Debreu equilibria exist and equilibrium prices are indeterminate. Recall that is the economy in which agents have standard expected utility preferences for the same prior and the same endowments as in our original economy. Bewley (Theorem 2 in Bewley (1972)) has shown that Arrow–Debreu equilibria exist with state–price densities in for the economy . By the first welfare theorem, an equilibrium allocation in can be identified with some for a vector of weights and the corresponding equilibrium state–price density with . Due to our assumption that endowments are in the interior of the consumption set, all weights are strictly positive.

We are now ready to characterize the equilibria of our Knightian economy.

Theorem 3.3

-

1.

Let be an equilibrium of for some and . Then is an Arrow–Debreu equilibrium of the Knightian economy.

-

2.

If is an Arrow–Debreu equilibrium of , then there exists and such that and with

In particular, Arrow–Debreu equilibria

-

•

exist,

-

•

their price is indeterminate,

-

•

and the allocation is ambiguity–free.

Proof: Let be an equilibrium of . obviously clears the market and is budget–feasible in the Knightian economy because we use the same pricing functional as in the economy . It remains to show that maximizes utility in the Knightian economy subject to the budget constraint.

In the first place, we need to verify that belongs to our commodity space (which is smaller than the commodity space considered by Bewley (1972) as it contains only quasi–continuous elements). But we have already noted above that the are quasi–continuous, and thus elements of , because they can be written as continuous functions of .

Let be budget–feasible for agent . As is an Arrow–Debreu equilibrium in the expected utility economy , we have . As is ambiguity–free by Theorem 3.1, we have . Therefore,

and we are done.

For the converse, let be an Arrow–Debreu equilibrium of . By the first welfare theorem and Theorem 3.1, there exist with . All as individual endowments are strictly positive. (Otherwise, which is dominated by .) Due to utility maximization, has to be a supergradient of at . The set of supergradients consists of linear functionals of the form , where is a minimizer in the set of priors. Since is ambiguity–free, is constant on and hence every element in is a minimizer of the Gilba–Schmeidler–type expected utility.

4 (Non–)Implementability by Continuous Trading of Few Long–Lived Securities

We now tackle the question if the efficient allocations of Arrow–Debreu equilibria can be implemented by trading a few long–lived assets dynamically over time. Under risk, the answer is (essentially) affirmative. If we allow the market to select the asset structure, Duffie and Huang (1985) establish implementability. In this case, we have purely nominal assets whose dividends are not directly related to commodities. One can thus choose their prices independently of consumption prices. In general, of course, the asset price structure with real assets is endogenous. In that case, the question of Radner implementability is much more complex and was only recently solved by Anderson and Raimondo (2008), Riedel and Herzberg (2013) and Hugonnier, Malamud, and Trubowitz (2012). If the asset market is potentially complete in the sense that sufficiently many independent dividend streams are traded, then one can obtain endogenously dynamically complete asset markets in sufficiently smooth Markovian economies. For non–smooth economies and non–Markovian state variables, the question is still open.

As we focus on the intrinisic limit of implementability which is created by Knightian uncertainty, we make here the life as easy as possible for the financial market: as in Duffie and Huang (1985), we consider the case with nominal assets freely chosen by the market. Since the equivalence between Arrow–Debreu and Radner equilibria usually breaks down, the result is stronger if we allow the market to choose the asset structure for nominal assets. If one cannot even implement the Arrow–Debreu equilibrium in the nominal case, one cannot do so with real assets either.

The Bachelier Market

We consider first the simplest case of a so–called Bachelier market. There is a riskless asset . Moreover, the price of the other assets is given by our -dimensional ambiguous (or )–Brownian motion . A trading strategy then consists of a process , the space of admissible integrands for (Knightian) Brownian motion (see Appendix A.2, Epstein and Ji (2013) or Denis, Hu, and Peng (2011) on details for the admissible integrands). The agents start with wealth zero (as there is no endowment nor consumption at time zero). Their gains from trade at time are then

| (1) |

They can afford to consume with where is the spot consumption price at time , a nonnegative –measurable function. A budget–feasible consumption–portfolio plan is a pair of a consumption plan and a trading strategy that satisfy the above budget constraint.

A Radner equilibrium consist of a spot consumption price and portfolio–consumption plans such that markets clear, i.e. , , and agents maximize their utility over all portfolio–consumption plans that satisfy the budget constraint.

Theorem 4.1

In the Bachelier model with asset prices , an Arrow–Debreu equilibrium of the form can be implemented as a Radner equilibrium if and only if the value of the net trades are mean ambiguity–free, i.e. for all

Proof: Let be an Arrow-Debreu Equilibrium as in Theorem 3.3.

Suppose we have an implementation in the Bachelier model with trading strategies . The Radner budget constraint gives

Stochastic integrals are symmetric –martingales, i.e. for all . Consequently the value of each net trade is mean ambiguity–free.

We show now that implementation is possible if net trades are mean ambiguity–free. We divide the proof into three steps. First, we introduce the candidate trading strategies for agent and show market clearing in the second step. Finally we show that these strategies are maximal in the budget sets.

Let the value of the net trade be mean ambiguity–free for all agents . The Arrow–Debreu budget constraint gives . Consequently by Corollary A.7, the process is a symmetric -martingale, so by the martingale representation theorem A.6

and

Hence, the trading strategies are candidates for trading strategies in a Radner equilibrium with allocation and spot consumption price .

By market–clearing in an Arrow–Debreu equilibrium, we have

As stochastic integrals that are zero have a zero integrand (even under Knightian uncertainty; see Proposition 3.3 in Soner, Touzi, and Zhang (2011)), we conclude that the portfolios clear, .

It remains to check that the consumption–portfolio strategy is optimal for agent under the Radner–budget constraint. Suppose there is a trading strategy with

We then have

and is thus budget–feasible in the Arrow–Debreu model. We conclude that .

To illustrate the theorem, we consider a concrete example.

Example 4.2

Let , , , and for . Assume and . By Corollary 3.2 and Theorem 3.3, equilibrium allocations are full insurance; therefore, the state price density is deterministic, so that we may take without loss of generality .

In this case, the expected value of net trades depends on the particular measure . For example, if has constant volatility under , then

where is the standard normal distribution. Radner implementation is therefore impossible.

The previous example suggests that Radner implementation might not be expected, in general. In the next step, we clarify this question in a world without aggregate uncertainty. We know from our analysis in the previous section that all Arrow–Debreu equilibria fully insure all agents in such a setting. We claim that “for almost all” economies, or “generically”, Radner implementation is impossible.

While the notion of “almost all” has a natural meaning in the finite–dimensional context because one can use Lebesgue measure to define negligible sets as null sets under that measure, the notion of “almost all” does not generalize immediately to infinite–dimensional Banach spaces because there is no translation–invariant measure that assigns positive measure to all open sets on such spaces. Anderson and Zame (2001) develop the notion of prevalence which coincides with the usual notion of full Lebesgue measure in finite–dimensional contexts and is thus an appropriate generalization to infinite–dimensional settings.

In the following, we fix aggregate endowment with no uncertainty and consider the class of economies parametrized by individual endowments

We say that an economy with endowments does not allow for implementation if there is no Arrow–Debreu equilibrium which can be implemented as a Radner equilibrium. Let be the subset of economies in which do not allow for implementation.

In Theorem 4.1, we introduced the notion mean ambiguity–free random variables in . The collection of all such elements is denoted by and set . For an alternative characterization of , see Corollary A.7.

Theorem 4.3

With no aggregate uncertainty, implementation of Arrow–Debreu equilibrium via a Bachelier Model is generically impossible: is prevalent in .

Proof: Let be an equilibrium and let without loss of generality. By Corollary 3.2, is the only non–constant within the value of each net trade . Consequently by Theorem 4.1 implementability fails if there is a with .

From this observation, we may focus on the prevalence of the property “mean ambiguity–free” within the space of initial endowments . The following claim is crucial; its proof is below. The order relation induced by the cone .

Claim: is a prevalent set in of .

In the case , one endowment within determines a distribution of endowments via , hence

is a shy subset of . Therefore the claim implies that is prevalent in .

For an arbitrary , we have is a prevalent subset in of . This follow by the the same arguments as in the proof of the claim, by choosing the subspace of as the finite dimensional test space. Hence, is a shy set in . The result then follows by an analogous argument as in the case .

We come now to the proof of the claim made above. The proof relies on the Martingale representation Theorem A.6. The Corollary A.7 implies , where is the completion of piecewise constant process, see (2) in Appendix A.3.

Let denote the Banach space of progressive–measurable processes with continuous paths and of bounded variation on , so that

where denotes all processes such that and .444Akin to (3), set .

The main step is to define a tractable “test–space” (to check prevalence) via a concrete : By Remark A.8 and setting , fix given by

The process is again an increasing –martingale since preserves constants. Positive homogeneity of implies that is an -martingale if . A rescaling of into yields .555This is possible since as discussed in the Appendix for the the case .

Fix the following one dimensional test space

of and denote the Lebesgue measure on by ; we have to check:

-

1.

There is a with :

The arbitrary translation of is performed by . Since only a positive makes an –martingale, we derive .

-

2.

For all we have :

This follows directly from the definition of and , since at most one lies in . The condition follows, since for every .

By Fact 6 of Anderson and Zame (2001) every finitely shy set in is also a shy set in , and therefore is a prevalent subset of .

Remark 4.4

The proof of Theorem 4.3 also establishes the general fact that is a shy subset in .

4.1 General Asset Structures

The Bachelier model we presented allows for negative values of the price process. Theorem 4.1 is still valid, when our -Brownian motion of the Bachelier model is decomposed into the positive and negative part . The trading strategies are then given by and where denotes the fractions invested in the uncertain assets of Theorem 4.1. In the same fashion, as mentioned in Section 5 of Duffie and Huang (1985), the number of assets becomes .

On the other it is also possible to implement the Arrow-Debreu equilibrium with an arbitrary symmetric –martingale. A canonical example is a symmetric –martingale of exponential form:

The strictly positive process is the unique solution of the following linear stochastic differential equation with respect to the –Brownian motion ,666 See Section 5 in Peng (2010) for details and especially Remark 1.3 therein.

From a general perspective, we aim to enlarge the scope of Theorem 4.1 by allowing a large family of symmetric -martingales as feasible substitutes of the Bachelier Model. The following result takes a leaf out of Duffie (1986), where the notion of “martingale generator” points to the implementability of an Arrow–Debreu Equilibrium under some classical probability space.

Proposition 4.5

Theorem 4.1. is still valid if we replace the implementing with a symmetric –martingale , such that –q.s. and .

Proof: We show that every can be written as a .

By Proposition 3.3 in Soner, Touzi, and Zhang (2011) states that under every , the Itô integral with respect to some , coincides -almost surely with the stochastic integral under .

By using the representation of from Proposition A.2, we have -almost surely, where denotes the quadratic variation of the -Brownian motion under , since is an -martingale under every . Since is bounded, we have if and only if

Consequently, a stochastic integral with respect to the present symmetric –martingale can then be written as where , see (2) for the exact of . The equations hold -almost surely for every .

From the conditions on it follows that may represent payoffs in similarly to , since for every (with ), we have

and this yields .

5 Conclusion

This paper establishes a crucial difference of risk and Knightian uncertainty. Under risk, dynamic trading of few long–lived assets suffices to implement the efficient allocations of Arrow–Debreu equilibria as dynamic Radner equilibria if the number of traded assets is equal to the number of sources of uncertainty. This result generically fails under Knightian uncertainty even in the stylized framework of no aggregate uncertainty and for nominal asset structures.

All results of the paper are formulated in terms of Peng’s sub–linear expectation space . As stated in Proposition A.2, the Knightian expectation can be represented by a set priors that corresponds to different volatility processes that live within constant bounds . A further extension refers to the possibility to extend results when the Knightian expectation is induced by time–dependent and stochastic volatility bounds. For instance, Epstein and Ji (2014) introduce a more general family of time–consistent conditional Knightian expectations. Since most results of the paper are heavily based on the Martingale representation Theorem A.6, extensions to more general volatility specifications crucially depend on the availability of an analogous martingale Representation.

Appendix A Knightian Uncertainty in Continuous Time

We fix a time horizon . Our state space consists of all continuous trajectories on the time interval that start in zero:

The coordinate process

will describe the information flow of our economy as in the usual continuous–time diffusion model. As agents live in a Knightian world, we do not assume that the distribution of the process is commonly known. Instead, we just use a nonlinear expectation which is defined on a suitably rich space of functions on in the sense of the following definition.

Definition A.1

Let be a vector lattice of functions from to that contains the constant functions. We call an uncertainty space if the mapping

satisfies the following properties:

-

1.

preserves constants: for all ,

-

2.

monotone: for all ,

-

3.

sub-additive: ,

-

4.

homogeneous: .

We call a (Knightian) expectation.

We start here with the notion of an uncertainty space rather than modeling the set of priors because we want to stress that one can build a whole new theory of uncertainty (rather than probability theory) by starting with the notion of an uncertainty space rather than a probability space, as the work of Peng (2006) demonstrates. Peng calls such spaces sublinear expectation spaces, but from a philosophical point of view, the name “uncertainty space” seems quite fitting to us.

Distributions under and -Brownian Motion

Of particular importance to us is the fact that one can develop the notion of Brownian motion in this Knightian setup. We assume throughout the paper that is an -Brownian motion777Again, we slightly deviate from Peng’s nomenclature where this object is called –Brownian motion - no exists at this point., the ambiguous version of classic Brownian motion on Wiener space.

We would like to take a second to explain how such an ambiguous Brownian motion is to be understood. With regard to the concept of ambiguity free (in the strong sense) from Definition 2.1, we start how one can define the notion of a “distribution” of a function in our setting. When is sufficiently rich (what we assume), then for every continuous and bounded function , as well. We can then define a new operator

on the space of continuous, bounded real functions by setting

We call the operator the (uncertain) distribution of . We consequently say that have identical uncertainty, or , if .

The notion of independence is crucial for probability theory. We follow Peng again in letting be (-)independent of if for all continuous bounded functions we have

One can thus first fix the value of , take the expectation with respect to , and then take the expectation with respect to . This is one way to generalize the notion of independence to the Knightian case. Without going into the philosophical issues involved here, we just take this approach. In the same vein, we call independent of if for all continuous bounded functions we have

The class of (normalized) normal distributions is infinitely divisible. In particular, if we have two independent standard normal distributions, then for positive numbers and , the new variable is again normally distributed with variance . This property is well known to characterize the class of normal distributions. One can take this characterization of normal distributions to call –normal if for any which has identical uncertainty and is independent of , the uncertain variable has the same uncertainty as .

We have now the tools at hand to define uncertain -Brownian motion. is called an –Brownian motion if all increments are independent of the past and identically –normal: for all and all the increment is independent of .

It is, of course, a completely nontrivial question whether such an ambiguous Brownian motion exists. This has been shown by Shige Peng (Peng (2006)) with the help of the theory of viscosity solutions of nonlinear partial differential equations. An alternative route proceeds via the construction of a suitable set of multiple priors. Indeed, readers familiar with the literature on ambiguity aversion in decision theory or the theory of risk measures in mathematical finance might immediately anticipate a representation of our Knightian expectation in terms of a set of probability measures. For the case of Knightian Brownian motion, the set of probability measures has a special structure that we now describe.

A.1 Representing Priors and Volatility Uncertainty

We start with the simpler one–dimensional case. Fix two bounds . The set consists of all probability measures on endowed with the Borel –field that make a martingale whose quadratic variation is –almost surely between the following two bounds:

In general, the set of priors can be parametrized by a subset of ; this set describes the possible volatility structures of the dimensional Knightian Brownian motion. Theorem 52 in Denis, Hu, and Peng (2011) implies the next results.

Proposition A.2

For any , we have the representation

where is the probabilistic expectation of under the probability measure . is a weakly–compact set, with respect to the topology induced .

Wwe give a more detailed description of the lattice of payoffs we are working with and set for the rest of the appendix . Peng constructs the –Brownian motion first on the set of all locally Lipschitz functions of that satisfy a polynomial growth constraint. The space is obtained by closing this space under the norm

where -q.s. refers to -almost surely for every . As indicated in the introduction and Section 2, we may formulate the uniform version of Luisin’s property: A mapping is said to be quasi-continuous (q.c.) if for all there exists an open set with such that is continuous.

Similarly to Lebesgue spaces based on a probability space, we restrict attention to equivalent classes. Under , as shown in Denis, Hu, and Peng (2011), we have the following representation of our commodity space

where denotes the space of -equivalence classes of measurable payoffs and are the trivial payoffs with respect to that do not charge any . We say that has a -q.c. version if there is a quasi–continuous function with q.s.

A.2 Conditional Knightian Expectation

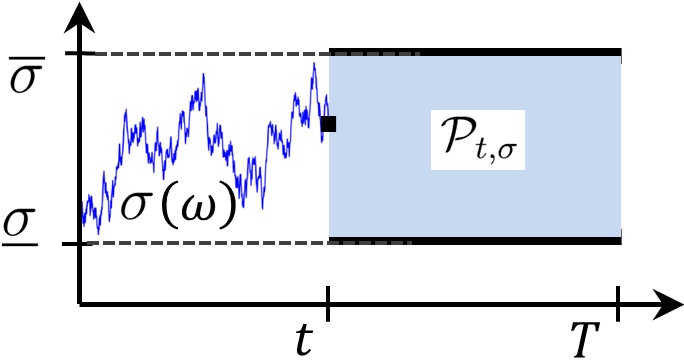

For the purpose of a martingale representation theorem we need a well–defined conditional expectation. In accordance with the representation of in Proposition A.2, we denote for each , the conditional probability by . Fix a volatility regime and denote the resulting martingale law by . The set of priors with a time–depending restriction on the related information set , generated by , is given by

This set of priors consists of all extensions of from to within . All priors in agree with in the events up to time , as illustrated in Figure 1.

As we are seeking for a rational–updating principle, we note, the following formulation of conditiong is closely related to dynamic consistency or rectangularity of Epstein and Schneider (2003).

The efficient use of information is commonly formalized by the concept of conditional expectations and depends on the underlying uncertainty model. We introduce a universal conditional expectation, that is under every prior almost surely equal to the maximum of relevant conditional expectations. This concept is formulated in the following.

Let denote the subspace of –measurable payoffs. For all there exists an -measurable random variable such that

The linear conditional expectation under some has strong connections to a positive linear projection operator. In the presence of multiple priors, the conditional updating in an ambiguous environment involves a sub–linear projection . In this regard the conditional Knightian expectations satisfies a rational–updating principle, with .

Lemma A.4

meet the law of iterated expectation: , .

A.3 Spanning and Martingales

We proceed similarly to the single prior case, where the Radner implementation in continuous time is based on a classical martingale representation. As indicated in Proposition A.2, the multiple prior model enforces a conditional sub–linear expectation and spawns an elaborated martingale representation.

We start with a notion of martingales under the conditional expectation . Fix a random variable . As stated in Lemma A.4, the time consistency of the conditional Knightian expectation allows to define a martingale similarly to the single prior setting, as being its own estimator.

Definition A.5

An -adapted process is an -martingale if

We call a symmetric -martingale if and are both -martingales.

The nonlinearity of the conditional expectation implies that if is an –martingale, then is not necessarily an –martingale. Intuitively, the negation let become super–additive.

We come now to the representation of -martingales and specify the space of admissible integrands taking values in . All processes we consider are -progressively measurable.888The filtration , deviates from the well–known two–step augmentation procedure from the stochastic analysis literature, i.e. including the null–sets and taking the right continuous version. Usually this new filtration is said to satisfy the “usual conditions”. As mentioned in Section 2 of Soner, Touzi, and Zhang (2011), this assumption is no longer required. Consequently, the usually questionable assumption of a too rich information structure at time can be dropped. We begin with the space of well–defined integrands when the Bachelier model builds up the integrator:

| (2) |

where is closure of piecewise constant progressively measurable processes with , under the norm , see Remark A.3

Condition (1) states the self–financing property of an adapted and -integrable . For the arguments in Theorem 4.1, it is crucial if a payoff can be represented or replicated in terms of a stochastic integral. To formulate Theorem A.6, set

| (3) |

The following Theorem clarifies this issue, see Soner, Touzi, and Zhang (2011) for a proof.

Theorem A.6

For every , there exist a unique pair , where is a –martingale, such that for all

The increasing –martingale refers a correction term for the “overshooting” of the sub–linear expectation . Specifically, the conditional Knightian expectation enforces to be a supermartingale under every . For some effective priors , is an -martingale. Foreclosing Corollary A.7, these two possible cases, can be distinguished, by the fact if and only if .

The following corollary illustrates which random variables have the replication property in terms of a stochastic integral. In this connection, a fair game against nature refers to the symmetric –martingale property. Apparently, in this situation the process is equivalently an -martingale under every .

Corollary A.7

The space of mean ambiguous–free contingent claims is a closed subspace of . More precisely, we have

The notion of perfect replication is associated to the situation when . Elements in generate symmetric martingales, via the successive application of the conditional Knightian expectation along the augmented filtration .

Remark A.8

When is contained in a subset of , including all with Lipschitz continuous, then the –martingale admits an explicit representation,

where is an endogenous output of the martingale representation, so that becomes a function of . If , the function is given by . As such it is an open problem, if every can be represented in this complete form. We refer to Peng, Song, and Zhang (2013) for the latest discussion.

References

- (1)

- Anderson and Raimondo (2008) Anderson, R., and R. Raimondo (2008): “Equilibrium in Continuous-Time Financial Markets: Endogenously Dynamically Complete Markets,” Econometrica, 76, 841–907.

- Anderson and Zame (2001) Anderson, R., and W. Zame (2001): “Genericity with Infinitely Many Parameters,” Advances in Microeconomic Theory, 1(1), 1–64.

- Beißner (2014) Beißner, P. (2014): “Equilibrium Prices under Ambiguous Volatility,” Mimeo, IMW Bielefeld.

- Bewley (1972) Bewley, T. (1972): “Existence of Equilibria in Economies with Infinitely Many Commodities,” Journal of Economic Theory, 4, 514–540.

- Billot, Chateauneuf, Gilboa, and Tallon (2000) Billot, A., A. Chateauneuf, I. Gilboa, and J. Tallon (2000): “Sharing Beliefs: Between Agreeing and Disagreeing,” Econometrica, 68, 685–694.

- Dana (2002) Dana, R. (2002): “On Equilibria when Agents Have Multiple Priors,” Annals of Operations Research, 114, 105–112.

- Dana and Riedel (2013) Dana, R., and F. Riedel (2013): “Intertemporal Equilibria with Knightian Uncertainty,” Journal of Economic Theory, 148(2013), 1582–1605.

- De Castro and Chateauneuf (2011) De Castro, L. I., and A. Chateauneuf (2011): “Ambiguity aversion and trade,” Economic Theory, 48(2-3), 243–273.

- Denis, Hu, and Peng (2011) Denis, L., M. Hu, and S. Peng (2011): “Function Spaces and Capacity Related to a Sublinear Expectation: Application to G-Brownian Motion Paths,” Potential Analysis, 34, 139–161.

- Duffie (1986) Duffie, D. (1986): “Stochastic Equilibria: Existence, Spanning Number, and the No Expected Financial Gain from Trade Hypothesis,” Econometrica, 54(5), 1161–1184.

- Duffie and Huang (1985) Duffie, D., and C. Huang (1985): “Implementing Arrow-Debreu Equilibria by Continuous Trading of Few Long-Lived Securities,” Econometrica, 53, 1337–1356.

- Duffie and Zame (1989) Duffie, D., and W. Zame (1989): “The Consumption-Based Capital Asset Pricing Model,” Econometrica, 57, 1274–1298.

- Epstein and Ji (2013) Epstein, L., and S. Ji (2013): “Ambiguous Volatility and Asset Pricing in Continuous Time,” Review of Financial Studies, 26(7), 1740–1786.

- Epstein and Ji (2014) Epstein, L., and S. Ji (2014): “Ambiguous Volatility, Possibility, and Utility in Continuous Time,” Journal of Matthematical Economics, 50, 269–282.

- Epstein and Schneider (2003) Epstein, L., and M. Schneider (2003): “Recursive Multiple Priors,” Journal of Economic Theory, 113, 1–31.

- Hugonnier, Malamud, and Trubowitz (2012) Hugonnier, J., S. Malamud, and E. Trubowitz (2012): “Endogenous Completeness of Diffusion Driven Equilibrium Markets,” Econometrica, 80(3), 1249–1270.

- Hunt, Sauer, and Yorke (1992) Hunt, B., T. Sauer, and J. Yorke (1992): “Prevalence: A Translation–Invariant ’Almost Everywhere’ on Infinite–Dimensional Spaces,” Bulletin (New Series) of the American Mathematical Society, 27, 217–238.

- Karatzas, Lehoczky, and Shreve (1990) Karatzas, I., J. P. Lehoczky, and S. E. Shreve (1990): “Existence and Uniqueness of Multi-Agent Equilibrium in a Stochastic, Dynamic Consumption / Investment Model,” Mathematics of Operations Research, 15(1), 80–128.

- Peng (2006) Peng, S. (2006): “G-expectation, G-Brownian Motion and Related Stochastic Calculus of Itô Type,” Stochastic analysis and applications, The Abel Symposium 2005, 541–567.

- Peng (2010) Peng, S. (2010): “Nonlinear expectations and stochastic calculus under uncertainty,” Arxiv preprint arXiv:1002.4546.

- Peng, Song, and Zhang (2013) Peng, S., Y. Song, and J. Zhang (2013): “A complete representation theorem for -martingales,” arXiv preprint arXiv:1201.2629v2.

- Riedel and Herzberg (2013) Riedel, F., and F. Herzberg (2013): “Existence of Financial Equilibria in Continuous Time with Potentially Complete Markets,” Journal of Mathematical Economics, 49(5), 398–404.

- Rigotti and Shannon (2005) Rigotti, L., and C. Shannon (2005): “Uncertainty and Risk in Financial Markets,” Econometrica, 73(1), 203–243.

- Soner, Touzi, and Zhang (2011) Soner, M., N. Touzi, and J. Zhang (2011): “Martingale representation theorem for the G-expectation,” Stochastic Processes and their Applications, 121(2), 265–287.

- Tallon (1998) Tallon, J. (1998): “Do Sunspots Matter When Agents are Choquet–Expected-Utility Maximizers,” Journal of Economic Dynamics and Control, 22(3), 357–368.