On the inference about the spectra of high-dimensional covariance matrix based on noisy observations

Abstract

In practice, observations are often contaminated by noise, making the resulting sample covariance matrix to be an information-plus-noise-type covariance matrix. Aiming to make inferences about the spectra of the underlying true covariance matrix under such a situation, we establish an asymptotic relationship that describes how the limiting spectral distribution of (true) sample covariance matrices depends on that of information-plus-noise-type sample covariance matrices. As an application, we consider the inference about the spectra of integrated covolatility (ICV) matrices of high-dimensional diffusion processes based on high-frequency data with microstructure noise. The (slightly modified) pre-averaging estimator is an information-plus-noise-type covariance matrix, and the aforementioned result, together with a (generalized) connection between the spectral distribution of true sample covariance matrices and that of the population covariance matrix, enables us to propose a two-step procedure to estimate the spectral distribution of ICV for a class of diffusion processes. An alternative estimator is further proposed, which possesses two desirable properties: it eliminates the impact of microstructure noise, and its limiting spectral distribution depends only on that of the ICV through the standard Marčenko-Pastur equation. Numerical studies demonstrate that our proposed methods can be used to estimate the spectra of the underlying covariance matrix based on noisy observations.

keywords:

[class=AMS]keywords:

–with applications to integrated covolatility matrix inference in the presence of microstructure noise

and

t1Research partially supported by NSFC 11501348 and Shanghai Pujiang Program 15PJ1402300. t2Research partially supported by DAG (HKUST) and GRF 606811 of the HKSAR.

1 Introduction and Main Results

1.1 Motivation

Covariance structure is of fundamental importance in multivariate analysis and all kinds of applications. While in classical low-dimensional setting, a usually unknown covariance structure can be estimated by the sample covariance matrix, in the high-dimensional setting, it is now well understood that the sample covariance matrix is not a consistent estimator. What is even worse, in many applications the observations are contaminated, and below we explain one such setting that motivates this work. Similar situations certainly arise in many other settings.

Our motivating question arises in the context of estimating the so-called integrated covariance matrix of high-dimensional diffusion process, with applications towards the study of stock price processes. More specifically, suppose that we have stocks whose (efficient) log price processes are denoted by for . Let . A widely used model for is

| (1.1) |

where is a -dimensional drift process, is a matrix for any , and is called the covolatility process, and is a -dimensional standard Brownian motion. The interval stands for the time period of interest, say, one day. The integrated covariance (ICV) matrix refers to

The ICV matrix, in particular, its spectrum (i.e., its set of eigenvalues) plays an important role in financial applications such as factor analysis and risk management.

A classical estimator of the ICV matrix is the so-called realized covariance (RCV) matrix, which relies on the assumption that one could observe at high frequency. More specifically, suppose that could be observed at time points for . Then, the RCV matrix is defined as

| (1.2) |

where

stands for the vector of log returns over the period . Consistency as well as central limit theorems for RCV matrix under such a setting and when the dimension is fixed is well unknown, see, for example, Andersen and Bollerslev (1998), Andersen et al. (2001), Barndorff-Nielsen and Shephard (2002), Jacod and Protter (1998), Mykland and Zhang (2006), among others.

However, in practice, the observed prices are always contaminated by the market microstructure noise. The market microstructure noise is induced by various frictions in the trading process such as the bid-ask spread, asymmetric information of traders, the discreteness of price, etc. Despite the small size, market microstructure noise accumulates at high frequency and affects badly the inferences about the efficient price processes. In practice, as is pointed out in Liu et al. (2015) where a careful comparison between various volatility estimators and the 5-min realized volatility is carried out, when the sampling frequency is higher than one observation per five minutes, the microstructure noise is usually no longer negligible, and the following additive model has been widely adopted in recent studies on volatility estimation:

| (1.3) |

where denote the observations, denote the noise, which are i.i.d., independent of , with and certain covariance matrix .

Observe that under (1.3), the observed log-returns relates to the true log-returns by the following equation

| (1.4) |

where, as usual, . We are therefore in a noisy observation setting where the observations are contaminated by additive noise. Such a setting forms the basis of the current work.

Besides microstructure noise, there is another issue which is due to asynchronous trading. In practice, different stocks are traded at different times, consequently, the tick-by-tick data are not observed synchronously. There are several existing methods for synchronizing data, like the refresh times (Barndorff-Nielsen et al. (2011)) and previous tick method (Zhang (2011)). Compared with microstructure noise, asynchronicity is less an issue. For example, as is pointed out in Zhang (2011), asynchronicity does not induce bias in the two-scales estimator, and even the asymptotic variance is the same as if there is no asynchronicity. While we do not seek a rigorous proof to avoid the paper being unnecessarily lengthy, we believe our methods to be introduced below work just as well for asynchronous data. The reason, roughly speaking, is as follows. Take the previous tick method for example. Here we choose a (usually equally spaced) grid of time points , and for each stock , for each time , let be the latest transaction time before . One then acts as if one observes at time for stock . With the original additive model at time :

we have at time ,

In other words, the asynchronicity induces an additional error . The error is however diminishingly small as the sampling frequency since . To sum up, even though asynchronicity induces an additional error, the error is of negligible order compared with the microstructure noise . Henceforth we shall stick to the model (1.4).

One striking feature in (1.4) that differs from most noisy observation settings is that as the observation frequency goes to infinity, the signal, namely, the true log-return becomes diminishingly small, while the noise remains of the same order of magnitude, and therefore the signal-to-noise ratio goes to 0. In the next section we will explain a method that fixes this issue. Our first main result, Theorem 1.1, applies to a general setting where the signal and noise are of a same order of magnitude.

1.2 Pre-averaging approach

The pre-averaging (PAV) approach is introduced in Jacod et al. (2009), Podolskij and Vetter (2009) and Christensen, Kinnebrock and Podolskij (2010) to deal with microstructure noise. Other approaches include the two-scales estimator (Zhang, Mykland and Aït-Sahalia (2005),Zhang (2011)), realized kernel (Barndorff-Nielsen et al. (2008),Barndorff-Nielsen et al. (2011)) and quasi-maximum likelihood method (Xiu (2010),Aït-Sahalia et al. (2010)). We shall use a slight variant of the PAV approach in this work. First, choose a window length . Then, group the intervals , into pairs of non-overlapping windows, each of width , where denotes rounding down to the nearest integer. Introduce the following notation for any process ,

With such notation, the observed return based on the pre-averaged price becomes

| (1.5) |

One key observation is that if is chosen to be of order (which is the order chosen in Jacod et al. (2009), Podolskij and Vetter (2009) and Christensen, Kinnebrock and Podolskij (2010)), then in (1.5) the “signal” and “noise” can be shown to be of the same order of magnitude. Our version of PAV matrix is then just the sample covariance matrix based on these returns:

| PAV | (1.6) |

1.3 From signal to signal-plus-noise and back

We first recall some concepts in multivariate analysis. For any symmetric matrix , suppose that its eigenvalues are , then its empirical spectral distribution (ESD) is defined as

The limit of ESD as , if exists, is referred to as the limiting spectral distribution, or LSD for short.

The matrix PAV can be viewed as the sample covariance matrix based on observations , which model the situation of information vector being contaminated by additive noise . Dozier and Silverstein (2007a) consider such information-plus-noise-type sample covariance matrices as

where is independent of , and consists of i.i.d. entries with zero mean and unit variance. Write . The authors show that if converges, then so does . They further show how the LSD of depends on that of (see equation (1.1) therein).

In this article, we investigate the problem from a different angle. We shall show how the LSD of depends on that of . Our motivation for seeking such a relationship is that, in practice, we are usually interested in making inferences about signals based on noisy observations . Therefore, a more practically relevant result is a relationship that describes how the LSD of depends on that of . Let us mention that inverting the aforementioned relationships is in general notoriously difficult. For example, the Marčenko-Pastur equation, which is very similar to equation (1.1) in Dozier and Silverstein (2007a) and describes how the LSD of the sample covariance matrix depends on that of the population covariance matrix, is long-established, but it was only a few years ago that researchers [El Karoui (2008); Mestre (2008); Bai, Chen and Yao (2010) etc.] realized how the (unobservable) LSD of the population covariance matrix can be recovered based on the (observable) LSD of the sample covariance matrix. Our first result, Theorem 1.1 below, provides an approach that allows one to derive the LSD of based on that of .

We first collect some notation that will be used throughout the article. For any real matrix , denotes its spectral norm, where is the transpose of , and denotes the largest eigenvalue. For any nonnegative definite matrix , denotes its square root matrix. For any , write and as its real and imaginary parts, respectively, and as its complex conjugate. For any distribution , denotes its Stieltjes transform defined as

In particular, for any Hermitian matrix with eigenvalues , the Stieltjes transform of its ESD, denoted by , is given by

where is the identity matrix. For any vector , stands for its Euclidean norm. Finally, “” stands for “equal in distribution”, denotes weak convergence, means convergence in probability, means that the sequence is tight, and means that .

We now present our first result about how the LSD of depends on that of .

Theorem 1.1.

Suppose that , where

-

-

(A.i)

is , independent of , and with , we have , where is a probability distribution with Stieltjes transform denoted by ;

-

(A.ii)

with ;

-

(A.iii)

is with the entries being i.i.d. and centered with unit variance; and

-

(A.iv)

with as .

-

(A.i)

Then, almost surely, the ESD of converges in distribution to a probability distribution . Moreover, if is supported by a finite interval with and possibly has a point mass at 0, then for all such that the integral on the right hand side of (1.7) below is well-defined, is determined by in that it uniquely solves the following equation

| (1.7) |

in the set

| (1.8) |

Remark 1.1.

Since and as , the imaginary part of the denominator of the integrand on the right hand side of (1.7) is asymptotically equivalent to as , and so the integral is well-defined for all with sufficiently large. Note further that by the uniqueness theorem for analytic functions, knowing the values of for with sufficiently large is sufficient to determine for all

In practice, as the ESD of is observable, we can replace with and solve equation (1.7) for . Since fully characterizes the ESD of , this allows us to make inferences about the covariance structure of the underlying signals . In the simulation studies we explain in detail about how to implement this procedure in practice.

1.4 Applications to PAV

The term can be written in a more clear form by using the triangular kernel:

| (1.9) | ||||

Based on this, one can show that if dimension is fixed, then

| (1.10) |

It is also easy to verify that

where ’s are i.i.d. random vectors with zero mean and covariance matrix .

The following Corollary is a direct consequence of Theorem 1.1.

Corollary 1.1.

Suppose that

-

-

(B.i)

for all , is a -dimensional process for some drift process and covolatility process defined in (1.1);

-

(B.ii)

the ESD of converges to a probability distribution with Stieltjes transform denoted by ;

-

(B.iii)

the noise are independent of , and are i.i.d. with zero mean and covariance matrix for some and as ;

-

(B.iv)

for some , and satisfy that .

-

(B.i)

Then, almost surely, the ESD of PAV defined in (1.6) converges in distribution of a probability distribution . Moreover, if is supported by a finite interval with and possibly has a point mass at 0, then for all such that the integral on the right hand side of (1.11) below is well-defined, is determined by in that it uniquely solves the following equation

| (1.11) |

in the set

Remark 1.2.

Although Corollary 1.1 is stated for the case when noise components have the same standard deviations, it can readily be applied to the case when the covariance matrix is a general diagonal matrix, say . To see this, let . We can then artificially add additional to the original observations, where are independent of , and are i.i.d. with zero mean and covariance matrix . The noise components in the modified observations then have the same standard deviation , and Corollary 1.1 can be applied. Note that the variances, , can be consistently estimated, see, for example, Theorem A.1 in Zhang, Mykland and Aït-Sahalia (2005). A similar remark applies to Theorem 1.1.

1.5 Further inference about ICV

Corollary 1.1 allows us to estimate the ESD of . In light of the convergence (1.10), this would have been sufficient for us to make inferences about the ICV if the convergence (1.10) held as well in the high-dimensional case. Unfortunately, it is not the case, and a further step to go from to ICV is needed. Such an inference is generally impossible, as can be seen as follows. ICV is an integral . In the simple situation where and is deterministic, the building blocks in defining , , are multivariate normals with mean 0 and covariance matrices The bottom line is, all the covariance matrices, for , could be very different from the ICV! We can easily change the covariance matrices and hence the distributions of without changing ICV. And as both the dimension and observation frequency go to infinity, there are just too much freedom in the underlying distributions which makes the inference about ICV impossible. Certain structural assumptions are necessary to turn the impossible into the possible. The simplest one is to assume , in which case are i.i.d. The apparent shortcoming about this assumption is that it could not capture stochastic volatility which is a stylized feature in financial data. The following class of processes, introduced in Zheng and Li (2011), accommodates both stochastic volatility and leverage effect and in the meanwhile makes the inference about ICV still possible (and as we will see soon that the theory is already much more complicated than the i.i.d. setting).

Definition 1.1.

Suppose that is a -dimensional process satisfying (1.1). We say that belongs to Class if, almost surely, there exist and a matrix satisfying tr such that

| (1.12) |

where stands for the space of càdlàg functions from to .

Remark 1.3.

The convention that tr is made to resolve the non-identifiability built in the formulation (1.12), in which one can multiply and divide by a same constant without modifying the process . It is thus not a restriction.

Class incorporates some widely used models as special cases:

-

•

The simplest case is when the drift and , in which case the returns are i.i.d. .

-

•

More generally, again when the drift while is independent of the underlying Brownian motion , the returns follow mixed normal distributions.

-

–

Mixed normal distributions, or their asymptotic equivalent form in the high-dimensional setting111See Section 2 of El Karoui (2013) for the asymptotic equivalence between the mixed normal distributions and the elliptic distributions in the high-dimensional setting., elliptic distributions have been widely used in financial applications. McNeil, Frey and Embrechts (2005) state that “elliptical distributions … provided far superior models to the multivariate normal for daily and weekly US stock-return data”, and “multivariate return data for groups of returns of a similar type often look roughly elliptical.”

- –

-

–

-

•

Furthermore, Class allows the drift to be non-zero, and more importantly, the process to be stochastic and even dependent on the Brownian motion that drives the price process, thus featuring the so-called leverage effect in financial econometrics, which is an important stylized fact of financial returns and has drawn a lot of attention recent years, see, for example, Aït-Sahalia, Fan and Li (2013) and Wang and Mykland (2014).

Observe that if belongs to Class , then the ICV matrix

| (1.13) |

Furthermore, if the drift process and is independent of , then, conditional on and using (1.9), we have

where consists of independent standard normals, and

| (1.14) |

It follows that

1.5.1 Further inference based on

Using Corollary 1.1 and Theorem 1 in Zheng and Li (2011) we establish the following result concerning the LSD of .

We put the following assumptions on the underlying process. They are inherited from Proposition 5 of Zheng and Li (2011), and we refer the readers to that article for some further background and explanations. Observe in particular that Assumption (C.v) allows the covolatility process to be dependent on the Brownian motion that drives the price processes. Such a dependence allows us to capture the so-called leverage effect in financial econometrics. Assumptions (C.iv) and (C.vi) are about the spectral norm of the ICV matrix. We do not require the norm to be bounded, allowing, for example, spike eigenvalues.

Assumption C:

-

-

(C.i)

For all , is a -dimensional process in Class for some drift process and covolatility process ;

-

(C.ii)

there exists a such that for all and all , for all almost surely;

-

(C.iii)

as , the ESD of converges in distribution to a probability distribution ;

-

(C.iv)

there exist and such that for all , almost surely;

-

(C.v)

there exists a sequence of index sets satisfying and such that may depend on but only on ;

-

(C.vi)

there exists a such that for all and for all , almost surely, and additionally, almost surely, converges uniformly to a nonzero process that is piecewise continuous with finitely many jumps.

-

(C.i)

Theorem 1.2.

Remark 1.4.

Based on Corollary 1.1 and Theorem 1.2, we obtain the following two-step procedure to estimate the ESD of ICV:

- (i)

- (ii)

See the simulation studies for more detailed explanations about the estimation procedure.

1.5.2 An alternative estimator

The aforementioned two-step procedure involves the which needs to be estimated in practice. Moreover, equations (1.16) and (1.17) involves three unknowns ( and ) and the numerical solutions of these equations may be unstable. Motivated by this consideration, we draw ideas from Zheng and Li (2011) and propose an alternative estimator that overcomes these challenges. It is also worth mentioning that the alternative estimator allows for rather general dependence structures in the noise process, both cross-sectional and temporal. The temporal dependence between the microstructure noise has been documented in recent studies, see, for example, Hansen and Lunde (2006), Ukabata and Oya (2009) and Jocod et al. (2014).

Our alternative estimator is an extension of the time-variation adjusted RCV matrix introduced in Zheng and Li (2011) to our noisy setting. To start, we fix an and , and let and . The time-variation adjusted PAV matrix is then defined as

| (1.18) |

where

| (1.19) |

Note that here window length has a higher order than in Theorem 1.2. The reason is that, after pre-averaging, the underlying returns are and the noises are . In Theorem 1.2, we balance the orders of the two terms by choosing to achieve the optimal convergence rate. In Theorem 1.3 below, we take for some to eliminate the impact of noise.

We first recall the concept of -mixing coefficients.

Definition 1.2.

Suppose that is a stationary time series. For , let be the -field generated by the random variables . The -mixing coefficients are defined as

where for any probability space , refers to the space of square-integrable, -measurable random variables.

We now introduce a number of assumptions. Observe that Assumption (D.i) says that we allow for rather general dependence structures in the noise process, both cross-sectional and temporal. We actually do not put any restrictions on the cross-sectional dependence, and even the dependence between the microstructure noise and the price process is allowed. Note also that Jocod et al. (2014) provides an approach to estimate the decay rate of the -mixing coefficients. Assumption (D.ii) is again about the dependence between the covolatility process and the Brownian motion that drives the price processes. Assumption (D.iv) is about the boundedness of individual volatilities.

-

-

(D.i)

For all , the noises is stationary, have mean 0 and bounded th moments and with -mixing coefficients satisfying for some integer as ;

-

(D.ii)

there exists a and a sequence of index sets satisfying and such that may depend on but only on ;

-

(D.iii)

there exists a such that for all , for all almost surely;

-

(D.iv)

there exists a such that for all and all , the individual volatilities for all almost surely;

-

(D.v)

there exist and such that for all , almost surely;

- (D.vi)

-

(D.vii)

for some and , and satisfy that , where is the integer in Assumption (D.i).

-

(D.i)

Remark 1.5.

Careful readers may have noticed that Assumptions (B.iv) and (D.vii) are mathematically incompatible as Assumption (B.iv) requires while Assumption (D.vii) requires for some . The two assumptions are, however, perfectly compatible in practice when we deal with finite samples. In fact, take the choices of in the simulation studies (Section 2 below) for example. There we take . When applying Corollary 1.1 and Theorem 1.2, we take , which leads to in Assumption (B.iv); while when applying Theorem 1.3 below, we take , which gives in Assumption (D.vii).

We have the following convergence result regarding the ESD of the alternative estimator.

Theorem 1.3.

Suppose that for all , is a -dimensional process in Class for some drift process and covolatility process . Suppose also that Assumptions (C.ii), (C.iii) and (C.vi) in Theorem 1.2 hold. Under Assumptions (D.i)-(D.vii), we have as , the ESDs of ICV and converge almost surely to probability distributions and , respectively, where satisfies (1.15), and is determined by in that the Stieltjes transform of , denoted by , satisfies the following (standard) Marčenko-Pastur equation

| (1.20) |

Remark 1.6.

Theorem 1.3 says that the LSDs of ICV and are related via the Marčenko-Pastur equation. Several algorithms have been developed to recover by inverting the Marčenko-Pastur equation, see, for example, El Karoui (2008); Mestre (2008); Bai, Chen and Yao (2010) etc. We can therefore readily estimate the ESD of ICV by using these existing algorithms.

The rest of the paper is organized as follows. Section 2 demonstrates how to implement both the two-step procedure introduced in Remark 1.4 and the more direct method in Remark 1.6 to estimate the spectral distribution of underlying covariance matrix based on noisy observations. The proof of Theorem 1.1 is given in Section 3. Section 4 concludes. The proofs of some lemmas and Theorems 1.2 and 1.3 are given in the Appendix A.

2 Simulation studies

In this section, we illustrate how to make inferences using Corollary 1.1, Theorems 1.2 and 1.3. In particular, we will show how to estimate the ESD of ICV by using (1) Corollary 1.1 and Theorem 1.2 based on PAV, and (2) Theorem 1.3 based on the alternative estimator .

We consider a stochastic U-shaped process as follows:

where , ,

and with being the th component of the Brownian motion that drives the price process. Observe that such a formulation makes to be dependent on all the component of the underlying Brownian motion, hence Assumptions (C.v) and (D.ii) are actually both violated. However, we shall see soon that our methods still work well. A sample path of is given below.

Next, the matrix is taken to be where is a random orthogonal matrix and is a diagonal matrix whose diagonal entries are drawn independently from Beta distribution. With such and , the individual daily volatilities are around , which is similar to what one observes in practice. The latent log price process follows

Finally, the noise are drawn from i.i.d. .

In the studies below, the dimension, i.e., the number of assets is taken to be 100, and the observation frequency is set to be 23,400 which corresponds to one observation per second on a regular trading day.

2.1 Applications of Corollary 1.1 and Theorem 1.2

In this subsection, we illustrate how to estimate the ESD of ICV based on PAV matrix by using the two-step procedure that we introduced in Remark 1.4.

In the first step, we replace in equation (1.11) with the ESD of PAV and solve for . The window length in defining PAV is set to be . As to to be solved, we choose a set of ’s whose real and imaginary parts are equally spaced in the intervals and respectively. Denote these ’s by , and the estimated by . We then need to estimate the ESD of based on , which is done as follows.

Inspired by the nonparametric estimation method proposed in El Karoui (2008), we approximate with a weighted sum of point masses

| (2.1) |

where is a grid of points to be specified, and ’s are weights to be estimated. To choose the grid , naturally we would like to cover the support of which, however, is unknown. To overcome such a difficulty, note that by the Marčenko-Pastur theorem, the support of ESD of sample covariance matrix always covers that of the population covariance matrix, and since by Theorem 1.3, our alternative estimator, , satisfies the same Marčenko-Pastur equation as the sample covariance matrix, inherits such a property with a support covering that of ICV. (Such a feature can be clearly seen in the first plot in Figure 5.) Thanks to this property, we choose ’s be equally spaced between 0 and the largest eigenvalue of , and we are guaranteed that will cover the support of .

Next we discuss how to estimate the weights . Observe that the discretization (2.1) gives an approximated Stieltjes transform of as Let

be the approximation errors. The weights are then estimated by minimizing the approximation errors:

| (2.2) |

We move on the estimation of the ESD of ICV by using Theorem 1.2. We first need to estimate two unknowns, and , which we do as follows. First note that multiplying and on both sides of the first and second equations in (1.17) respectively yields

and

where the last step is due to equation (1.16). It follows that

| (2.3) |

and Substituting the last expression of into equation (2.3) yields

| (2.4) |

By plugging the obtained in the first step and solving equation (2.4) we get .

We are now ready to estimate the ESD of ICV. Similarly as in the first step, discretize as

| (2.5) |

where ’s are weights to be estimated. By equation (1.16) we expect that

to be small. The ’s are then estimated by minimizing the approximation errors just as in (2.2).

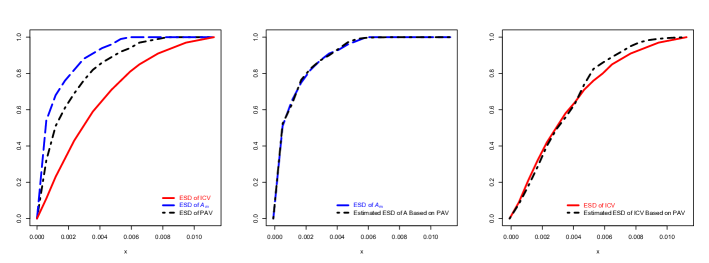

Figure 4 below illustrates the estimation procedure. The left plot shows three ESDs, those of ICV, and PAV respectively. The three curves are clearly different from each. Keep in mind that we only observe that of PAV, whereas the ESDs of both ICV and are underlying and need to estimated. The estimation of the ESD of is conducted in the first step, and the result is shown in the middle plot. The second step estimates the ESD of ICV, given in the right plot. We see in both plots that the estimated ESDs roughly match with their respective targets, showing that our proposed two-step procedure indeed works in practice.

2.2 Application of Theorem 1.3

In this subsection we illustrate how to use our alternative estimator and Theorem 1.3 to estimate the ESD of ICV. According to Theorem 1.3, asymptotically, the ESD of is related to that of ICV through the standard Marčenko-Pastur equation. Several algorithms have been developed to estimate the spectra of the population covariance matrices by inverting the Marčenko-Pastur equation, and in the below we adopt the algorithm proposed in El Karoui (2008). Set the window length in defining to be . Discretize the ESD of ICV as (2.5). According to Theorem 1.3, the Stieltjes transform of the ESD of , denoted by , should approximately satisfy equation (1.20) with replaced with the ESD of ICV. In other words, we again expect the approximation errors

to be small. So again, we estimate the weights ’s by minimizing the approximation errors as in (2.2).

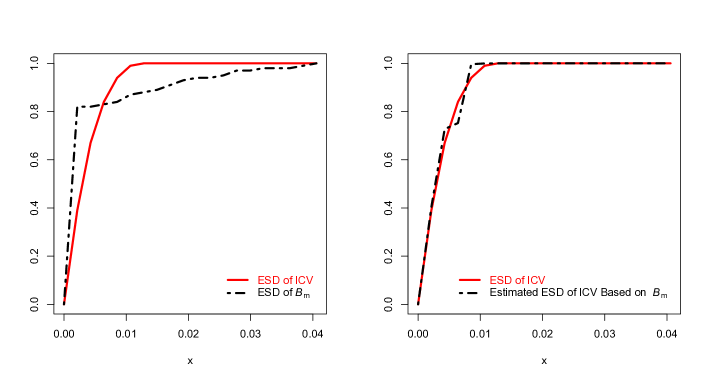

The estimation results are given in Figure 5. Observe that the left plot shows clearly that the ESD of differs from the (latent unobserved) ESD of ICV, yet the right plot shows that we can estimate this latent distribution.

3 Proofs

3.1 Proof of Theorem 1.1

Theorem 1.1 is a consequence of the following proposition.

Proposition 3.1.

Under the assumptions of Theorem 1.1, there exists a constant such that almost surely, for all

we have

| (3.1) |

where for all large enough, is the unique solution to the equation

| (3.2) |

in the set

| (3.3) |

and

| (3.4) |

The proof of Proposition 3.1 is given in Section 3.1.3 after some preparation works have been done in Sections 3.1.1 and 3.1.2. In Section 3.1.4 we show how to establish Theorem 1.1 based on Proposition 3.1.

To prove Proposition 3.1, we shall use the following results from Dozier and Silverstein (2007a). By Theorem 1.1 therein, the sequence converges weakly to a probability distribution . Moreover, by using the same truncation and centralization technique as in Dozier and Silverstein (2007a), we may assume that

-

-

(E.i)

for some ,

-

(E.ii)

, , and

-

(E.iii)

.

-

(E.i)

In addition to equation (3.2), we shall also study its limiting equation

| (3.5) |

where is the Stieltjes transform of the probability distribution .

It is shown in Dozier and Silverstein (2007b) that the distribution admits a continuous density on . Since we assume that is supported by a finite interval with and possibly has a point mass at 0, we conclude that admits a bounded density supported by a finite interval and possibly a point mass at zero.

3.1.1 Properties of and

Lemma 3.1.

There exists a constant such that for all , for all large enough, equation (3.2) admits a unique solution in .

Lemma 3.2.

Suppose that solves equation (3.5) for . Write and . Then ; moreover, as , uniformly in , one has and .

Lemma 3.3.

There exists a constant such that for any , equation (3.5) admits a unique solution.

Lemma 3.4.

There exists a constant such that the solution to (3.5) is analytic on .

Lemma 3.5.

3.1.2 Some further preliminary results

Let and , , be the th column of and , and let . Denote so that . For any complex number such that , define

| (3.6) | |||

According to equation (2.2) in Silverstein and Bai (1995), we have

| (3.7) |

Thus using the identity we obtain that

| (3.8) |

Next we introduce another definition of , as the solution to the following equation

| (3.9) |

We claim that the definition of in (3.9) is equivalent to the earlier definition of defining to be the solution to equation (3.2). In fact, write

Right-multiplying both sides by and using (3.7) yield

Taking trace on both sides and dividing by one gets that

| (3.10) | |||||

This shows that if satisfies (3.9), then satisfies equation (3.2). On the other hand, if satisfies equation (3.2), from (3.10) we have

namely, satisfies (3.9).

Recall the definitions of , , and in (3.6). Using (3.8) we have

Define

| (3.15) |

Certainly , but introducing makes the computations below more clear.

Recall that , and so . We can then rewrite as

where

| (3.16) | ||||

where in the last equality we used the equivalent definition (3.9) of .

Lemma 3.6.

Suppose that solves equation (3.2) for , then for all , is bounded by .

Lemma 3.7.

Suppose that solves equation (3.2) for , then is bounded by .

Lemma 3.8.

Lemma 3.9.

Suppose that solves equation (3.2) for , then the random variables and satisfy

3.1.3 Proof of Proposition 3.1

Proof.

Recall the defined in (3.1.2). The proof will be completed if we show almost surely for all .

By (A.10), (E.iii) and Lemma 3.7, there exists a constant such that

| (3.17) |

Moreover, by Lemmas 3.2, 3.5 and the convergence of , we have as ,

| (3.18) |

and . In particular, for all large enough, we have

| (3.19) |

We now show that almost surely. Using Markov’s inequality and Hölder’s inequality, for any , we have

where the last step follows from Lemmas 3.6 and 3.9. Thus almost surely by Lemmas 3.5, 3.2 and the Borel-Cantelli Lemma.

Similarly we can prove that almost surely for by using Lemmas 3.6, 3.7, 3.8, 3.9 and inequalities (3.17), (3.19).

∎

3.1.4 Proof of Theorem 1.1

Proof.

We first show that equation (1.1) in Dozier and Silverstein (2007a) can be derived from Proposition 3.1.

For any fixed , by Proposition 3.1, Lemmas 3.5, 3.2, 3.7, and the dominated convergence theorem we obtain that

| (3.20) |

where is the unique solution to equation (3.5) and . Moreover, if we let , then by the definition (3.5) of and the convergence (3.18) we have

and

Substituting the expressions of , and in terms of into equation (3.20) yields

| (3.21) |

where .

Next we show that (3.21) holds for all . In fact, by Lemma 3.4, is analytic on . In particular, for any convergent sequence such that as , we have , all in ; moreover, and all satisfy equation (3.21). Noting that equation (3.21) is well-defined for all , by the analyticity of on and the uniqueness theorem for analytic functions, we conclude that equation (3.21) holds for every , in other words, equation (1.1) in Dozier and Silverstein (2007a) holds.

For any , denote , where, recall that, and . We further define

We will show the following facts:

-

-

(F.i)

,

-

(F.ii)

, or .

-

(F.i)

We now show (F.ii). Let . Then

| (3.22) |

By substituting (3.22) and into equation (3.5), we obtain

That is,

Therefore,

namely, (F.ii) holds.

Next, by (3.21) and the definitions of and and (F.ii), we have

Using the facts (F.i) and (F.ii) we obtain that

| (3.23) | ||||

By plugging in the expression of , we see that for all , satisfies

It follows from the uniqueness theorem for analytic functions that the above equation holds for all such that the integral on the right hand side is well-defined.

It remains to show that the solution to equation (1.7) is unique in the set defined in (1.8). In fact, suppose otherwise that both satisfy equation (1.7). Define for

| (3.24) |

By (1.7) and (3.24), we have Hence

| (3.25) |

which implies that

| (3.26) |

Using (3.24) and (3.26) we can rewrite as

| (3.27) | |||||

Observing that the Stieltjes transforms and are uniquely determined by equation (3.21) at points and respectively, together with (3.27), we obtain

Therefore

which implies that . It then follows from (3.25) that , a contradiction. ∎

4 Conclusion

Motivated by the inference about the spectra of the ICVmatrix based on high-frequency noisy data,

-

•

we establish an asymptotic relationship that describes how the spectral distribution of (true) sample covariance matrices depends on that of sample covariance matrices constructed from noisy observations;

-

•

using further a (generalized) connection between the spectral distribution of true sample covariance matrices and that of the population covariance matrix, we propose a two-step procedure to estimate the spectral distribution of ICV for a class of diffusion processes;

-

•

we further develop an alternative estimator which possesses two desirable properties: it eliminates the impact of microstructure noise, and its limiting spectral distribution depends only on that of the ICV through the standard Marčenko-Pastur equation;

-

•

numerical studies demonstrate that our proposed methods can be used to estimate the spectra of the underlying covariance matrix based on noisy observations.

Appendix A Proofs

A.1 Proof of Lemmas 3.1 – 3.9

Proof of Lemma 3.1.

Rewrite equation (3.2) as

| (A.1) | ||||

Firstly, under the assumptions of Theorem 1.1, by Theorem 1.1 in Bai and Silverstein (2012), if we let be an interval containing the support of , then we may assume that for all large , . Let , and . Since and , we have for all large and for all ,

| (A.2) |

Define

We will apply the Banach fixed point theorem to show that for all large enough, there exists a unique point such that . The desired conclusion then follows.

Step (i): we prove that the mapping is defined from to . From the definition of and that , we have

and hence for all large enough,

where the last inequality follows from the fact that for any ,

Step (ii): we shall show that is a contraction mapping. In fact, for any two points , ,

Using Cauchy-Schwartz inequality we get that almost surely for all large enough, for all ,

which is strictly smaller than 1 when . Therefore the mapping is contractive in , and the Banach fixed point theorem guarantees the existence of a unique solution to equation (3.2). ∎

Proof of Lemma 3.2.

Taking imaginary parts on both sides of equation (3.5) yields

| (A.3) |

It is then straightforward to verify that and . Furthermore, since

| (A.4) | ||||

when , we have

| (A.5) |

Proof of Lemma 3.3.

Firstly, by the same proof as for Lemma 3.1, one can show that for all with , equation (3.5) admits a unique solution in defined in (3.3). Moreover, by Lemma 3.2, if solves (3.5), then ; furthermore, we can find a constant such that if solves (3.5) for with then we must have . The latter two properties imply that for all with the solution to (3.5) must lie in . Redefining if necessary, we see that for all , (3.5) admits a unique solution. ∎

Proof of Lemma 3.4.

Define a function as

That solves (3.5) is equivalent to . Write and . By taking the partial derivative with respect to we get

Note that

which, by (A.7), goes to zero as . Thus there exists a constant such that for all , . It follows from the implicit function theorem and Lemma 3.2 that is analytic on . ∎

Proof of Lemma 3.5.

Write and . Similar to the proof of Lemma 3.2, taking imaginary parts on both sides of equation (3.2), one can easily show that and .

Next we show that is tight, in other words, for any , there exists , such that for all large enough, . Since , it suffices to show that is tight.

Let , and let be the Stieltjes transform of the ESD . The spectra of and differ by number of zero eigenvalues, hence and

| (A.8) |

Thus equation (3.2) can also be expressed as

Taking real parts on both sides yields

Solving for yields

| (A.9) |

Now suppose that is not tight, then with positive probability, there exists a subsequence such that . By (A.9), we have

However, as goes to infinity, if , since is tight and , one gets that the RHS goes to 1. This contradicts the supposition that .

Next, for any convergent subsequence in set , by (A.2), for all large enough, we have . We can then apply the dominated convergence theorem to conclude that the limit point of must satisfy equation (3.5). By Lemma 3.3, the solution is unique, hence the whole sequence converges to the unique solution to equation (3.5). ∎

Proof of Lemma 3.7.

Any eigenvalue of can be expressed as , where is an eigenvalue of . We have

where the last step follows from the fact that thanks to Lemma 3.5. ∎

A.2 Proof of Theorem 1.2

Proof of Theorem 1.2.

The convergence of follows easily from Assumption (C.iii) and the fact that

Next, by Theorem 3.2 in Dozier and Silverstein (2007b), the assumption that has a bounded support implies that has a bounded support as well. Thus Assumption (A.iii′) in Zheng and Li (2011) that has a finite second moment is satisfied.

We proceed to show the convergence of . As discussed in Subsection 1.5.1, if the diffusion process belongs to Class , the drift process , and is independent of , then conditional on , we have

| (A.11) |

where is as in (1.14) and is independent of , and consists of independent standard normals. Hence, has the same distribution as defined as

| (A.12) |

Claim 1. Without loss of generality, we can assume that the drift process and is independent of .

In fact, firstly whether the drift term vanishes or not does not affect the LSD of . To see this, note that , where

| (A.13) |

and

| (A.14) |

Since all the entries of are of order , by Lemma B.2 in Appendix B, and have the same LSD.

Next, by the same argument as in the beginning of Proof of Theorem 1 in Zheng and Li (2011), we can assume without loss of generality that is independent of . It follows that and have the same LSD.

Claim 2. is bounded, and there exists a piecewise continuous process with finitely many jumps such that

| (A.15) |

In fact, using the boundedness of assumed in (C.vi) and that , one can easily show that is bounded.

Next we show that (A.15) is satisfied for . Define

Suppose that has jumps for . For each , there exists an such that the th jump falls in the interval . Then

Since and are both bounded, for any and for large enough, we have

For the second term , since is continuous in when , and by (A.vi), uniformly converges to , for any and for large enough, we have

Moreover, since , for all large we have

This completes the proof of (A.15).

Since and for , using Claim 2 and applying Theorem 1 in Zheng and Li (2011) we conclude that the ESD of converges to whose Stieltjes transform satisfies

| (A.16) | |||||

where , together with another function , uniquely solve the following equations in

| (A.17) |

∎

A.3 Proof of Theorem 1.3

Note that the convergence of the ESD of ICV has been proved in Theorem 1.2. The rest of Theorem 1.3 is a direct consequence of the following two convergence results.

Lemma A.1.

Under the assumptions of Theorem 1.3, we have

Proposition A.1.

Under the assumptions of Theorem 1.3, converge almost surely, and the limit is determined by in that its Stieltjes transform satisfies the following equation

| (A.18) |

Proof of Proposition A.1.

We now show the convergence of . The main reason that we choose in such a way that is to make the noise term negligible. To be more specific, by choosing for some where is the integer as in Assumption (D.i), we shall show that

have the same LSD. This will follow if we can show that

| (A.19) |

and

| (A.20) |

We start with (A.19). Since

in order to prove (A.19), it suffices to show

Below we shall prove the following slightly stronger result:

| (A.21) |

where for any vector , denotes its th entry.

Notice further that for (A.20), using Lemma B.2 in Appendix B, to prove (A.20), it also suffices to show (A.21).

We now prove (A.21). We start with the denominator term . We have for and defined in (A.13) and (A.14) respectively. Write as , where is defined in (1.14) and

By Assumption (D.ii), for all , are i.i.d. . By using the same trick as the proof of (3.34) in Zheng and Li (2011), we have

| (A.22) |

Note that

Assumption (D.iii) implies that for all , there exist such that

Therefore by Assumption (D.vii), there exists such that

which, together with (A.22), implies that there exists such that for all large enough,

Moreover, by Assumption (C.ii), for all , hence , which, by Assumption (D.vii), is . Therefore, there exists a constant such that, almost surely, for all large enough,

| (A.23) |

It remains to prove that

| (A.24) |

Observe that if we can show there exists such that

| (A.25) |

where is the integer satisfying as in Assumption (D.vii), then for any , by Markov’s inequality, we have

where the last equation is due to Assumption (D.vii). Since , we have , hence by the Borel-Cantelli Lemma, (A.24) holds.

We now show (A.25), which is a Marcinkiewicz-Zygmund type inequality. We will use Theorem 1 in Doukhan and Louhichi (1999) to prove (A.25). For that we need to verify , where

where

We now verify that . For any and for any , using the definition of -mixing coefficients we have

By Hölder’s inequality, we have

and similarly for . Since ’s have bounded th moments according to Assumption (D.i) and , we get .

Finally, by using a similar argument as in the last part of the proof of Proposition 8 in Zheng and Li (2011) (see pp.3142–3143), we have that has the same LSD as

where consists of independent standard normals. It is well known that the LSD of is determined by (A.18), hence by the previous arguments, so does that of . ∎

Now we prove Lemma A.1.

Proof of Lemma A.1.

We have

The convergence (A.24) and that imply that almost surely. To prove the lemma, it then suffices to show that

| (A.26) |

and

| (A.27) |

We start with (A.26). Write as in the proof of Proposition A.1. The convergence (A.22) implies that

where the error term converges to 0 almost surely. By Riemann integration and Assumption (C.vi) it is easy to show that , so we get

Furthermore by using the bound that one can easily show that

We therefore get (A.26).

Appendix B Two lemmas

Lemma B.1.

(Lemma 2.7 in Bai and Silverstein (1998) ). Let be a vector where the ’s are centered i.i.d. random variables with unit variance. Let be an deterministic complex matrix. Then, for any ,

Lemma B.2.

(Lemma 1 in Zheng and Li (2011)). Suppose that for each , and , , are all -dimensional vectors. Define

If the following conditions are satisfied:

-

•

with ;

-

•

there exists a sequence such that for all and all , all the entries of are bounded by in absolute value;

-

•

almost surely.

Then almost surely, where for any two probability distribution functions and , denotes the Levy distance between them.

References

- Andersen and Bollerslev (1998) {barticle}[author] \bauthor\bsnmAndersen, \binitsT. G, and \bauthor\bsnmBollerslev, \binitsT. (\byear1998). \btitleAnswering the Skeptics: Yes, Standard Volatility Models Do Provide Accurate Forecasts. \bjournalInternational Economic Review \bvolume39 \bpages885–905. \endbibitem

- Andersen et al. (2001) {barticle}[author] \bauthor\bsnmAndersen, \binitsT. G., \bauthor\bsnmBollerslev, \binitsT., \bauthor\bsnmDiebold, \binitsF. X. and \bauthor\bsnmLabys, \binitsP. (\byear2000). \btitleThe Distribution of Realized Exchange Rate Volatility. \bjournalJournal of the American Statistical Association \bvolume96 \bpages42–55. \endbibitem

- Aït-Sahalia, Fan and Li (2013) {barticle}[author] \bauthor\bsnmAït-Sahalia, \bfnmYacine\binitsY., \bauthor\bsnmFan, \bfnmJianqing\binitsJ. and \bauthor\bsnmLi, \bfnmYingying\binitsY. (\byear2010). \btitleThe leverage effect puzzle: Disentangling sources of bias at high frequency. \bjournalJournal of Financial Economics \bvolume109 \bpages224–249. \endbibitem

- Aït-Sahalia et al. (2010) Aït-Sahalia, Y., Fan, J. Xiu, D. (2010). High Frequency Covariance Estimates with Noisy and Asynchronous Financial Data, Journal of the American Statistical Association, 105, 1504-1517.

- Bai, Chen and Yao (2010) {barticle}[author] \bauthor\bsnmBai, \bfnmZhidong\binitsZ., \bauthor\bsnmChen, \bfnmJiaqi\binitsJ. and \bauthor\bsnmYao, \bfnmJianfeng\binitsJ. (\byear2010). \btitleOn estimation of the population spectral distribution from a high-dimensional sample covariance matrix. \bjournalAust. N. Z. J. Stat. \bvolume52 \bpages423–437. \bdoi10.1111/j.1467-842X.2010.00590.x. \bmrnumber2791528 (2012c:62157) \endbibitem

- Bai and Silverstein (1998) {barticle}[author] \bauthor\bsnmBai, \bfnmZ. D.\binitsZ. D. and \bauthor\bsnmSilverstein, \bfnmJack W.\binitsJ. W. (\byear1998). \btitleNo eigenvalues outside the support of the limiting spectral distribution of large-dimensional sample covariance matrices. \bjournalAnn. Probab. \bvolume26 \bpages316–345. \bdoi10.1214/aop/1022855421. \bmrnumber1617051 \endbibitem

- Bai and Silverstein (2012) {barticle}[author] \bauthor\bsnmBai, \bfnmZhidong\binitsZ. and \bauthor\bsnmSilverstein, \bfnmJack W.\binitsJ. W. (\byear2012). \btitleNo eigenvalues outside the support of the limiting spectral distribution of information-plus-noise type matrices. \bjournalRandom Matrices Theory Appl. \bvolume1 \bpages1150004, 44. \bdoi10.1142/S2010326311500043. \bmrnumber2930382 \endbibitem

- Barndorff-Nielsen et al. (2008) Barndorff-Nielsen, O. E., Hansen, P. R., Lunde A. and Shephard N. (2008). Designing Realized Kernels to Measure Ex-post Variation of Equity Prices in the Presence of Noise, Econometrica, 76, 1481-1536.

- Barndorff-Nielsen and Shephard (2002) {barticle}[author] \bauthor\bsnmBarndorff-Nielsen, \bfnmOle E.\binitsO. E., and \bauthor\bsnmShephard, \bfnmNeil\binitsN. (\byear2002). \btitleEconometric Analysis of Realized Volatility and its use in Estimating Stochastic Volatility Models. \bjournalJournal of the Royal Statistical Society. Series B. Statistical Methodology \bvolume64 \bpages253–280. \endbibitem

- Barndorff-Nielsen et al. (2011) {barticle}[author] \bauthor\bsnmBarndorff-Nielsen, \bfnmOle E.\binitsO. E., \bauthor\bsnmHansen, \bfnmPeter Reinhard\binitsP. R., \bauthor\bsnmLunde, \bfnmAsger\binitsA. and \bauthor\bsnmShephard, \bfnmNeil\binitsN. (\byear2011). \btitleMultivariate Realised Kernels: Consistent Positive Semi-Definite Estimators of the Covariation of Equity Prices with Noise and Non-Synchronous Trading. \bjournalJournal of Econometrics \bvolume162 \bpages149-169. \endbibitem

- Christensen, Kinnebrock and Podolskij (2010) {barticle}[author] \bauthor\bsnmChristensen, \bfnmKim\binitsK., \bauthor\bsnmKinnebrock, \bfnmSilja\binitsS. and \bauthor\bsnmPodolskij, \bfnmMark\binitsM. (\byear2010). \btitlePre-averaging estimators of the ex-post covariance matrix in noisy diffusion models with non-synchronous data. \bjournalJ. Econometrics \bvolume159 \bpages116–133. \bdoi10.1016/j.jeconom.2010.05.001. \endbibitem

- Doukhan and Louhichi (1999) {barticle}[author] \bauthor\bsnmDoukhan, \bfnmPaul\binitsP. and \bauthor\bsnmLouhichi, \bfnmSana\binitsS. (\byear1999). \btitleA new weak dependence condition and applications to moment inequalities. \bjournalStochastic Processes and their Applications \bvolume84 \bpages313–342 \bdoi10.1016/S0304-4149(99)00055-1. \bmrnumber1719345 \endbibitem

- Dozier and Silverstein (2007a) {barticle}[author] \bauthor\bsnmDozier, \bfnmR. Brent\binitsR. B. and \bauthor\bsnmSilverstein, \bfnmJack W.\binitsJ. W. (\byear2007a). \btitleOn the empirical distribution of eigenvalues of large dimensional information-plus-noise-type matrices. \bjournalJ. Multivariate Anal. \bvolume98 \bpages678–694. \bdoi10.1016/j.jmva.2006.09.006. \bmrnumber2322123 \endbibitem

- Dozier and Silverstein (2007b) {barticle}[author] \bauthor\bsnmDozier, \bfnmR. Brent\binitsR. B. and \bauthor\bsnmSilverstein, \bfnmJack W.\binitsJ. W. (\byear2007b). \btitleAnalysis of the limiting spectral distribution of large dimensional information-plus-noise type matrices. \bjournalJ. Multivariate Anal. \bvolume98 \bpages1099–1122. \bdoi10.1016/j.jmva.2006.12.005. \bmrnumber2326242 \endbibitem

- El Karoui (2008) {barticle}[author] \bauthor\bsnmEl Karoui, \bfnmNoureddine\binitsN. (\byear2008). \btitleSpectrum estimation for large dimensional covariance matrices using random matrix theory. \bjournalAnn. Statist. \bvolume36 \bpages2757–2790. \bdoi10.1214/07-AOS581. \bmrnumber2485012 \endbibitem

- El Karoui (2009) {barticle}[author] \bauthor\bsnmEl Karoui, \bfnmNoureddine\binitsN. (\byear2009). \btitleConcentration of measure and spectra of random matrices: applications to correlation matrices, elliptical distributions and beyond. \bjournalAnn. Appl. Probab. \bvolume19 \bpages2362–2405. \bdoi10.1214/08-AAP548. \bmrnumber2588248 \endbibitem

- El Karoui (2010) {barticle}[author] \bauthor\bsnmEl Karoui, \bfnmNoureddine\binitsN. (\byear2010). \btitleHigh-dimensionality effects in the Markowitz problem and other quadratic programs with linear constraints: risk underestimation. \bjournalAnn. Statist. \bvolume38 \bpages3487–3566. \bdoi10.1214/10-AOS795. \bmrnumber2766860 \endbibitem

- El Karoui (2013) {barticle}[author] \bauthor\bsnmEl Karoui, \bfnmNoureddine\binitsN. (\byear2013). \btitleOn the realized risk of high-dimensional Markowitz portfolios. \bjournalSIAM J. Financial Math. \bvolume4 \bpages737–783. \bdoi10.1137/090774926. \bmrnumber3118251 \endbibitem

- Hansen and Lunde (2006) Hansen, P. R. and Lunde, A.(2006), Realized Variance and Market Microstructure Noise, Journal of Business and Economic Statistics, 24, 127–161.

- Jacod et al. (2009) {barticle}[author] \bauthor\bsnmJacod, \bfnmJean\binitsJ., \bauthor\bsnmLi, \bfnmYingying\binitsY., \bauthor\bsnmMykland, \bfnmPer A.\binitsP. A., \bauthor\bsnmPodolskij, \bfnmMark\binitsM. and \bauthor\bsnmVetter, \bfnmMathias\binitsM. (\byear2009). \btitleMicrostructure noise in the continuous case: the pre-averaging approach. \bjournalStochastic Process. Appl. \bvolume119 \bpages2249–2276. \bdoi10.1016/j.spa.2008.11.004. \bmrnumber2531091 \endbibitem

- Jacod and Protter (1998) {barticle}[author] \bauthor\bsnmJacod, \binitsJ. and \bauthor\bsnmProtter, \binitsP. (\byear1998). \btitleAsymptotic Error Distributions for the Euler Method for Stochastic Differential Equations. \bjournalAnnals of Probability \bvolume26 \bpages267–307. \endbibitem

- Jocod et al. (2014) Jacod J., Y. Li, and X. Zheng (2014). Statistical Properties of Microstructure Noise: II. Available at SSRN: http://ssrn.com/abstract=2212119.

- Liu et al. (2015) {barticle}[author] \bauthor\bsnmLiu, \bfnmLily Y.\binitsL.Y., \bauthor\bsnmPatton, \bfnmAndrew J.\binitsA.J. and \bauthor\bsnmSheppard, \bfnmKevin\binitsK. (\byear2015). \btitleDoes Anything Beat 5-Minute RV? A Comparison of Realized Measures Across Multiple Asset Classes. \bjournalJournal of Econometrics. \bvolume187 \bpages293–311. \bdoi10.1016/j.jeconom.2015.02.008. \bmrnumber3347308 \endbibitem

- McNeil, Frey and Embrechts (2005) {barticle}[author] \bauthor\bsnmMcNeil, \bfnmAlexander J.\binitsA.J., \bauthor\bsnmFrey, \bfnmRudiger\binitsR. and \bauthor\bsnmEmbrechts, \bfnmPaul\binitsP. (\byear2005). \btitleQuantitative Risk Management: Concepts, Techniques, and Tools.. \bjournalPrinceton University Press. \endbibitem

- Mestre (2008) {barticle}[author] \bauthor\bsnmMestre, \bfnmXavier\binitsX. (\byear2008). \btitleImproved estimation of eigenvalues and eigenvectors of covariance matrices using their sample estimates. \bjournalIEEE Trans. Inform. Theory \bvolume54 \bpages5113–5129. \bdoi10.1109/TIT.2008.929938. \bmrnumber2589886 (2010h:62174) \endbibitem

- Mykland and Zhang (2006) {barticle}[author] \bauthor\bsnmMykland, \binitsP. A. and \bauthor\bsnmZhang, \binitsL. (\byear2006). \btitleANOVA for Diffusions and Ito Processes. \bjournalAnnals of Statistics \bvolume34 \bpages1931-1963. \endbibitem

- Podolskij and Vetter (2009) {barticle}[author] \bauthor\bsnmPodolskij, \bfnmMark\binitsM. and \bauthor\bsnmVetter, \bfnmMathias\binitsM. (\byear2009). \btitleEstimation of volatility functionals in the simultaneous presence of microstructure noise and jumps. \bjournalBernoulli \bvolume15 \bpages634–658. \bdoi10.3150/08-BEJ167. \bmrnumber2555193 (2011b:62081) \endbibitem

- Silverstein and Bai (1995) {barticle}[author] \bauthor\bsnmSilverstein, \bfnmJack W.\binitsJ. W. and \bauthor\bsnmBai, \bfnmZ. D.\binitsZ. D. (\byear1995). \btitleOn the empirical distribution of eigenvalues of a class of large-dimensional random matrices. \bjournalJ. Multivariate Anal. \bvolume54 \bpages175–192. \bdoi10.1006/jmvB.1995.1051. \bmrnumber1345534 \endbibitem

- Ukabata and Oya (2009) Ukabata, M. and K. Oya (2009). Estimation and Testing for Dependence in Market Microstructure Noise. J. Financial Econometrics, 7, 106-151.

- Wang and Mykland (2014) {barticle}[author] \bauthor\bsnmWang, \bfnmChristina D.\binitsC.D. and \bauthor\bsnmMykland, \bfnmPer A.\binitsP.A. (\byear2014). \btitleThe Estimation of Leverage Effect With High-Frequency Data. \bjournalJ. Amer. Statist. Assoc. \bvolume109 \bpages197–215. \bdoi10.1080/01621459.2013.864189. \bmrnumber3180557 \endbibitem

- Xiu (2010) {barticle}[author] \bauthor\bsnmXiu, \bfnmDacheng\binitsD. (\byear2010). \btitleQuasi-maximum likelihood estimation of volatility with high frequency data. \bjournalJ. Econometrics \bvolume159 \bpages235–250. \bdoi10.1016/j.jeconom.2010.07.002. \bmrnumber2720855 (2011f:62036) \endbibitem

- Zhang et al. (2005) Zhang, L., Mykland, P. A. and Aït-Sahalia, Y. (2005). A Tale of Two Time Scales: Determining Integrated Volatility with Noisy High-Frequency Data,” Journal of the American Statistical Association, 100, 1394-1411.

- Zhang (2011) {barticle}[author] \bauthor\bsnmZhang, \bfnmLan\binitsL. (\byear2011). \btitleEstimating covariation: Epps effect, microstructure noise. \bjournalJournal of Econometrics \bvolume160 \bpages33–47. \bdoi10.1016/j.jeconom.2010.03.012. \bmrnumber2745865 (2012b:62345) \endbibitem

- Zhang, Mykland and Aït-Sahalia (2005) {barticle}[author] \bauthor\bsnmZhang, \bfnmLan\binitsL., \bauthor\bsnmMykland, \bfnmPer A.\binitsP. A. and \bauthor\bsnmAït-Sahalia, \bfnmYacine\binitsY. (\byear2005). \btitleA tale of two time scales: determining integrated volatility with noisy high-frequency data. \bjournalJ. Amer. Statist. Assoc. \bvolume100 \bpages1394–1411. \bdoi10.1198/016214505000000169. \bmrnumber2236450 (2007h:62079) \endbibitem

- Zheng and Li (2011) {barticle}[author] \bauthor\bsnmZheng, \bfnmXinghua\binitsX. and \bauthor\bsnmLi, \bfnmYingying\binitsY. (\byear2011). \btitleOn the estimation of integrated covariance matrices of high dimensional diffusion processes. \bjournalAnn. Statist. \bvolume39 \bpages3121–3151. \bdoi10.1214/11-AOS939. \bmrnumber3012403 \endbibitem