Iteration complexity analysis of dual first order methods for

conic convex programming

\nameI. Necoaraa∗

and A. Patrascua∗Corresponding author. Email:

ion.necoara@acse.pub.ro.

a Automatic Control and Systems

Engineering Department, University Politehnica Bucharest, 060042

Bucharest, Romania

(January 2015)

Abstract

In this paper we provide a detailed analysis of the iteration

complexity of dual first order methods for solving conic convex

problems. When it is difficult to project on the primal feasible set

described by convex constraints, we use the Lagrangian relaxation to

handle the complicated constraints and then, we apply dual first

order algorithms for solving the corresponding dual problem. We give

convergence analysis for dual first order algorithms (dual gradient

and fast gradient algorithms): we provide sublinear or linear

estimates on the primal suboptimality and feasibility violation of

the generated approximate primal solutions. Our analysis relies on

the Lipschitz property of the gradient of the dual function or an

error bound property of the dual. Furthermore, the iteration

complexity analysis is based on two types of approximate primal

solutions: the last primal iterate or an average primal sequence.

keywords:

conic convex problem, smooth optimization, dual first order methods,

approximate primal solutions, rate of convergence.

††articletype: RESEARCH ARTICLE

{classcode}

90C25; 90C46; 49N15; 65K05.

1 Introduction

Nowadays, many engineering applications can

be posed as conic convex problems. Several

important applications that can be modeled in this framework, the

network utility maximization problem

[1, 4, 26], the resource allocation

problem [27], the optimal power flow problem for a power

system [28] or model predictive control problem for a

dynamical system [11, 14, 20], have

attracted great attention lately.

When it is difficult to project on the primal feasible set

of the convex problem, we use the Lagrangian relaxation to handle

the complicated constraints and then solve the corresponding dual.

First order methods for solving the corresponding dual of

constrained convex problems have been extensively studied in the

literature. Dual subgradient methods based on averaging (so called

ergodic sequence), that produce primal solutions in the limit, can

be found e.g. in [2, 5, 7]. Convergence

rate analysis for the dual subgradient method has been studied e.g.

in [15], where estimates for suboptimality and feasibility

violation of an average primal sequence are provided.

In [12] the authors have combined a

dual fast gradient algorithm and a smoothing technique for solving

non-smooth dual problems and derived rate of convergence of order

, with denoting the

iteration counter, for primal suboptimality and

feasibility violation for an average primal sequence. Also, in

[11] the authors proposed inexact dual (fast) gradient

algorithms for solving dual problems and estimates of order

() in

an average primal sequence are provided for primal suboptimality

and feasibility violation. Convergence properties of a dual fast

gradient algorithm were also analyzed in [20] in the

context of predictive control. However, most of the papers

enumerated above provide an approximate primal solution for convex

problems based on averaging.

There are very few papers deriving the iteration

complexity of dual first order methods using as an approximate

primal solution the last iterate of the algorithm (see e.g.

[9, 10, 1, 22]),

although from our practical experience we have observed that usually these methods are

converging faster in the primal last iterate than in a primal

average sequence. For example, for a dual fast gradient method, rate

of convergence of order in the last

iterate is provided in [1] under the assumptions of

Lipschitz continuity and strong convexity of the primal objective

function and primal linear constraints. From our knowledge first

result on the linear convergence of dual gradient method in the last

iterate was provided in [9] under a local

error bound property of the dual. However, in [9]

linear convergence is proved only locally and for dual gradient

method. Recently, in [10] the authors show that, for

linearly constrained smooth convex problems satisfying a Slater type

condition, the dual problem has a global error

bound property. Moreover, in [24] Tseng posed the question whether there

exist fast gradient schemes that converge linearly on convex

problems having an error bound property.

Another strand of this literature uses augmented

Lagrangian based methods [3, 6, 14] or

Newton methods [26, 13]. For example,

[3] established a linear convergence rate of

alternating direction method of multipliers using an error bound

condition that holds under specific assumptions on the primal

problem. In [6, 14] the iteration complexity of

inexact augmented Lagrangian methods is analyzed, where the inner

problems are solved approximately and the dual variables are updated

using dual (fast) gradient schemes. In [26, 13]

dual Newton algorithms are derived under the assumption that the

primal objective function is self-concordant.

In conclusion, despite the fact that there are attempts to

analyze the convergence properties of dual first order methods, the

results are dispersed, incomplete and many aspects have not been

fully studied. In particular, in practical applications the main

interest is in finding approximate primal solutions. Moreover, we

need to characterize the convergence rate for these near-feasible

and near-optimal primal solutions. Finally, we are interested in

providing schemes with fast convergence rate. These issues motivate

our work here, which provides a detailed convergence analyzes of dual first order methods for

solving conic convex problems.

Contributions. In this paper we provide a

convergence analysis of dual first order methods producing

approximate primal feasible and suboptimal solutions for conic

convex problems. Our analysis is based on the Lipschitz gradient

property of the dual function or an error bound property of the dual

problem. Further, the iteration complexity analysis is based on two

types of approximate primal solutions: the last primal iterate or

an average primal sequence. We prove that first order algorithms for

solving the dual problem have the following iteration complexity in

terms of primal suboptimality and infeasibility:

(i) for strongly convex primal objective functions we

prove: for dual gradient method a sublinear convergence rate in

both, an average primal sequence (convergence rate of order

), or the last primal iterate sequence

(convergence rate )); for dual fast

gradient method a sublinear convergence rate in an average primal

sequence (convergence rate ), or the last primal

iterate sequence (convergence rate ).

(ii) if we use regularization techniques we prove that

the convergence estimates of dual fast gradient method for both

primal sequences (the last iterate and an average of iterates) have

the same order (up to a logarithmic factor).

(iii) if additionally the dual problem has an error bound

property, then we prove that dual first order methods (including a

fast gradient scheme with restart) converge globally with linear rate

in the last primal iterate sequence (convergence rate

, with ), a result which appears to

be new in this area.

(iv) finally, if the conic constraints are linear

constraints, then based on the properties of dual first order

methods and regularization techniques we improve the previous

convergence rates of dual first order methods in the last iterate

with one order of magnitude.

An important feature of our results is that these rates of

convergence are not only for the average of iterates but also for

the latest iterate. This feature is of practical importance since

usually the last iterates are employed in practical applications

and the present paper provides computational complexity certificates

for them.

Notations: We work in the space

composed by column vectors. For we denote the

standard Euclidean inner product , the

Euclidean norm and

the projection of onto the convex set as . Further, denotes the distance from

to the convex set , i.e. . Moreover, for a matrix we use

the notation for the spectral norm.

2 Problem formulation

We consider the following conic convex optimization problem:

(1)

where is convex function, , is a proper cone and is a closed convex set. Moreover, we assume that

both sets and are simple, i.e. the projection on these

sets is easy. Many engineering applications can be posed as

constrained convex problems (1) (e.g. network utility maximization

problem [1, 27]: is function and

is a box set; optimal power flow problem [28]:

is quadratic function and is a box set; model predictive

control problem [11, 14, 20]: is quadratic

function and is a set described by linear equality constraints).

Thus, we are interested in deriving tight convergence estimates

of dual first order methods for this optimization model. We denote with

the corresponding dual cone of ,

i.e. . Further, for simplicity of the exposition we use the short

notation:

Throughout the paper, we make the following assumption on

optimization problem (1):

Assumption 2.1.

The function is -strongly

convex w.r.t. the Euclidean norm and there exists a finite optimal

Lagrange multiplier for the conic constraints of

(1). ∎

Note that if the objective function is not strongly

convex, we can apply smoothing techniques by adding a

regularization term to the convex function in order to obtain a

strongly convex approximation of it and a corresponding smooth

approximation of the dual function. Then, we can use a dual fast

gradient method for maximizing the smooth approximation of the dual

function and then we can recover an approximate primal solution for

the original problem (see e.g. [12] for more details

regarding the iteration complexity estimates for this approach).

Furthermore, we can always guarantee the existence of a finite

optimal Lagrange multiplier provided that e.g. Slater

condition holds: there exists such

that .

Since there exists a finite optimal Lagrange

multiplier , strong duality holds for optimization problem

(1) (see [21]). In particular, we

have:

We denote by the set of optimal

solutions of dual problem (2), which is nonempty

and convex according to Assumption 2.1. Since is

strongly convex function, the Lagrangian function is also strongly convex. Then, the inner

problem has always a unique finite

optimal solution for any fixed . In conclusion, the

dual function has the effective domain the entire Euclidean

space , i.e. . Moreover, since

the minimizer of (3) for any fixed

is unique, from Danskin’s theorem [21] we get that the

dual function is differentiable everywhere and its gradient is

given by the following expression:

where denotes the unique optimal solution of the inner

problem (3), i.e.:

(4)

Moreover, from Theorem 1 in [17] it follows immediately

that the dual gradient is Lipschitz continuous on

with constant , i.e.:

(5)

From Lipschitz continuity of the dual gradient (5) the

following inequality (so-called descent lemma) is valid

[16, 17]:

(6)

In this paper we analyze several dual first order

methods for solving problem (1) and derive convergence

estimates for dual and primal suboptimality and also for primal feasibility

violation, i.e. finding an -primal-dual pair

such that:

(7)

where is a given accuracy and is the unique minimizer of problem (1). Thus, we introduce the

following definition:

Definition 1.

We say that is an -primal solution for

the original convex problem (1) if we have the

following relations for primal infeasibility and suboptimality:

(8)

2.1 Preliminary results

In this section we derive first some relations between the

optimal solution of the inner problem and the dual function

. Then, we also derive some properties of the gradient map.

These results will be used in the subsequent sections.

In the next lemma we derive some relations between the optimal solution of the

inner problem and the dual function . These relations

have been proven in [1, 22] for

(non-negative orthant). For completeness, we also give a short

proof:

Lemma 2.2.

Under Assumption 2.1, the following

inequality holds:

(9)

and the primal feasibility violation can be expressed in terms of

as:

(10)

Proof.

First, let us recall that and the

following relations:

Since is -strongly

convex, it follows that is also

-strongly convex in the variable for

any fixed , which gives the following inequality:

(11)

Taking now in the previous inequality (11) and

using that for any

and that for any ,

we have:

valid for all . We now express the primal

feasibility violation in terms of for any . Indeed, using that and that we get:

These relations prove the statements of the lemma.

∎

We now express the primal suboptimality in terms of , a result which appears to be new:

Lemma 2.3.

Under Assumption 2.1, the following inequality holds:

(12)

Proof.

Firstly, using the complementarity condition

we get:

which leads to the following relation:

Using the Cauchy-Schwartz inequality we derive:

(13)

Secondly, from the definition of the dual function we have:

Subtracting from both sides and

using the complementarity condition we get:

(14)

valid for all , where in the first inequality we used

concavity of dual function , in the second inequality the

relation and Cauchy-Schwartz

inequality and in the third inequality a property of the Euclidean

norm. In conclusion, using the triangle inequality for vector norms,

we obtain the following inequality:

(15)

Combining (13) and (15) we obtain the

bound on primal suboptimality (12).

∎

Note that, based on our derivations from above, we are

able to characterize primal suboptimality (12) without

assuming any Lipschitz property on as opposed to the results in

[1], where the authors had to require Lipschitz

continuity of for providing estimates on primal suboptimality.

However, for many applications is unbounded set and is quadratic function

(e.g. in model predictive control is quadratic and might be a set described by linear equality constraints [11, 20]) and thus it is not Lipschitz continuous, so that our theory covers this important case.

Further, let us introduce the notion of gradient map

denoted and the gradient step from denoted

(see also [16]):

(16)

Clearly, if and only if and

. Next lemma proves that the norm of the

gradient map is decreasing along a gradient step, i.e.:

Lemma 2.4.

Under Assumption 2.1 the following

inequality holds:

(17)

Proof.

Since the dual function has -Lipschitz gradient on

(see (5)) and is concave, the following relation

holds [16]:

If we replace in the previous inequality with a

gradient step in , i.e. , and arranging the terms we get:

Grouping the terms

appropriately we obtain:

Using now the triangle inequality

for a norm we get:

Finally, since the projection is non-expansive we obtain:

Combining the previous inequality with the definitions of and of , we obtain the statement of the lemma.

∎

Finally we show a relation between the dual gradient and

the gradient map:

Lemma 2.5.

Under Assumption 2.1 the following

inequality holds:

(18)

Proof.

First, we derive a property of the projection, namely:

(19)

Indeed, if and

only if for

all . Hence for all .

Since the left hand side of the last inequality is bounded below

for all , it follows that .

Then, we have:

Since , we also obtain a bound for

primal infeasibility:

(20)

∎

2.2 Dual first order algorithms

In this section we present a general framework for dual first order

methods generating approximate primal feasible and primal optimal

solutions for the convex problem (1). This

general framework covers important particular algorithms [16, 22]:

e.g. dual gradient algorithm, dual fast gradient algorithm,

hybrid fast gradient/gradient algorithm or restart fast gradient algorithm,

as we will see in the next sections. Thus, we will analyze the iteration complexity of some particular cases of the following general dual first order method that updates two dual sequences and one primal sequence as follows:

Algorithm (DFO) Given , for compute:1.2.,3..

where and are the parameters of the method

and in the next sections we show how we can choose them in an

appropriate way. Recall also the following relations:

and . Note that if we cannot solve the inner problem (step 1 in Algorithm (DFO)) exactly, but approximatively with some inner accuracy, then our framework allows us to use

approximate solutions and inexact dual gradients. This is

beyond the scope of the present paper, but for more details see e.g.

[11, 14, 25].

3 Rate of convergence of dual gradient algorithm

In this section we consider a variant of

Algorithm (DFO), where for all . Under

this choice for the parameter we have that and thus we obtain the following dual gradient algorithm

with variable step size :

Algorithm (DG) Given , for compute:1.2.,

where such

that and recall that . Let us now derive some important properties of the

dual gradient method that will be useful in the following sections.

Lemma 3.1.

Let Assumption 2.1 hold and the

sequence be generated by Algorithm

(DG). Then, the following inequalities are valid:

Proof.

Based on the update rule for the gradient method we get:

where the first inequality follows from the definition of

, i.e. from the property of the projection operator

for any , and . In conclusion, for all and we

obtain:

(21)

Now, if we take in (21) and use

concavity of , we get that:

Thus, we obtain:

(22)

Moreover, if we take in (21) and use , then we get that the dual gradient algorithm is

an ascent method:

(23)

Finally, if we take in (21), using that

and that , then we get:

(24)

Relations (22), (23) and (24) prove

the statements of the lemma.

∎

Furthermore, for any we can define the

following finite quantity:

(25)

From Assumption 2.1 it follows that there exists a

finite optimal Lagrange multiplier and thus , i.e. it is finite, for any finite . The

well-known sublinear convergence rate of Algorithm (DG) in

terms of dual suboptimality is given in the next lemma (see Theorem

4 in [19]):

Lemma 3.2.

[19]

Let Assumption 2.1 hold and the

sequence be generated by Algorithm (DG). Then, defining , a sublinear

estimate on dual suboptimality for dual problem

(2) is given by:

(26)

Proof.

Although the convergence rate is given for constant step size in

[19], it is easy to show that for variable step size

the convergence rate is similar. Therefore, we omit the proof and we

refer e.g. to Theorem 4 in [19] for details.

∎

In the sequel we use and thus

. Our iteration complexity

analysis for Algorithm (DG) is based on two types of

approximate primal solutions: the last primal iterate sequence

or an average primal sequence of the form:

(27)

3.1 Sublinear convergence in the last primal iterate

In this section we derive

sublinear estimates for primal feasibility and primal

suboptimality for the last primal iterate sequence generated by Algorithm (DG). Let us notice that from

the definition of Algorithm (DG) we have .

Theorem 3.3.

Let Assumption 2.1 hold and the

sequences be generated by Algorithm

(DG). Then, for a given accuracy we get an

-primal solution for (1) in the last

primal iterate of Algorithm (DG) after iterations.

Proof.

Firstly, combining (9) and

(26) we obtain the following important

relation characterizing the distance from the last iterate to

the unique optimal solution of our original problem

(1):

(28)

Secondly, combining the previous relation (28) and

(10) we obtain a sublinear estimate for feasibility

violation of the last iterate for Algorithm (DG):

(29)

where we used that and

. Finally, we derive a sublinear estimate for

primal suboptimality of the last iterate . Combining

(22), (12) and (28) we

obtain:

(30)

where in the second inequality we used the definition of the

finite constants and

. In conclusion, we have

obtained sublinear estimates of order

for primal infeasibility

(inequality (29)) and primal suboptimality (inequality

(3.1)) for the last primal iterate sequence generated by Algorithm (DG). Now, it is

straightforward to see that if we want to get an -primal

solution in we need to perform iterations.

∎

3.2 Sublinear convergence in an average primal sequence

In this section we derive sublinear

convergence estimates for primal infeasibility and primal

suboptimality for the average primal sequence defined in (27).

Theorem 3.4.

Let Assumption 2.1 hold and the

sequences be generated by Algorithm

(DG). Then, for a given accuracy we get an

-primal solution for (1) in the average

primal sequence of Algorithm (DG) after iterations.

Proof.

Our proof follows similar lines as in

[15, Proposition 1] given for the dual subgradient

method. However, in our case, by taking into account that the dual

is smooth and the nice properties of gradient method (see Lemma

3.1) and of the projection on cones (19),

we get better convergence estimates than in [15]. First,

given the definition of in Algorithm (DG) we get:

Subtracting from both sides, adding up the above inequality

for to , we get:

Denoting and dividing by

we get:

Since , then also .

Moreover, from the definition of and the relation , we obtain . Using the definition of the

distance and the previous facts we obtain:

(31)

It remains to bound . Using the

inequality (22) we get:

Using this bound in (31) and the fact that , we get the following

estimate on feasibility violation:

(32)

In order to derive estimates for primal suboptimality we

use the definition of dual cone and that ,

which imply:

Using the definition of and the previous

inequality we get:

Using the definition of and the convexity of we get:

(34)

Combining (33) and (34) we obtain the

following bounds on primal suboptimality:

(35)

In conclusion, we have obtained sublinear estimates of order

for primal infeasibility (inequality

(32)) and primal suboptimality (inequality (35))

for the average primal sequence generated

by Algorithm (DG). Now, if we want to get an

-primal solution in we need to perform iterations.

∎

We can also characterize the distance from to

the unique primal solution of problem (1).

Indeed, taking and in (11) and

using that , we have:

Note that if we assume constant step size , then . Thus, this choice for the

step size provides us the best convergence estimates. Further, the

iteration complexity estimates of order

in the last primal iterate

sequence (see Section 3.1) are inferior to

those estimates of order corresponding to

an average of primal iterates (see this section).

However, in Section 6 we show that for the particular

case of linearly constrained convex problems the convergence

estimates for both sequences, the last iterate and an average of

iterates, have the same order.

4 Rate of convergence of dual fast gradient algorithm

In this section we consider a variant of

Algorithm (DFO), where the step size is chosen

constant, i.e. for all

and is updated iteratively as shown below. In this case

we obtain the following dual fast gradient algorithm, which is an

extension of Nesterov’s optimal gradient method [16] (see

[22, 23, 24]):

Algorithm (DFG) Given , for compute:1.2.,3., and .

where we recall that and . Since is strongly convex, the Lagrangian is also strongly convex for any

fixed . Therefore, the minimizer of (3) for any fixed is unique and from Danskin’s theorem [21] we get that the

dual function is differentiable everywhere and thus is well defined even for . It can be easily seen that and the

step size sequence satisfies: . Therefore, we obtain the following

bound:

(37)

Rearranging the terms in the step size update , we

have the relation: .

Summing on the history and defining , we also obtain:

(38)

Denoting and

, we

now state the following auxiliary result (for a similar result

corresponding to another formulation of Algorithm (DFG) see

[23]).

Theorem 4.1.

Let Assumption 2.1 hold and the sequences

be generated by Algorithm (DFG), then

for any Lagrange multiplier and we

have the following relation:

(39)

Proof.

From the Lipschitz gradient relation and the strong convexity

property of the corresponding quadratic approximation of

(6), we have:

Taking now , then and we have:

where in the last inequality we used concavity of . Subtracting

now and multiplying with both hand sides, we

obtain:

Further, note that the choice in Algorithm (DFG)

implies that . On the other hand, using the iteration of

Algorithm (DFG) we have . Then, summing on the history, we obtain our result.

∎

The sublinear convergence rate of Algorithm (DFG) in

terms of dual suboptimality is given in the next lemma.

Lemma 4.2.

[22, 23]

Let Assumption 2.1 hold and the

sequences be generated by

Algorithm (DFG). Then, a sublinear estimate on dual

suboptimality for dual problem (2) is given by

(recall that ):

(40)

Our iteration complexity analysis for Algorithm (DFG) is based on two types of approximate primal solutions: the

last primal iterate sequence defined as

(41)

or an average primal sequence of the form

(42)

4.1 Sublinear convergence in the last primal iterate

In this section we derive sublinear

convergence estimates for primal infeasibility and suboptimality

for the last primal iterate sequence as defined

in (41) of Algorithm (DFG).

Theorem 4.3.

Let Assumption 2.1 hold and the

sequences be generated by

Algorithm (DFG). Then, for a given accuracy we

get an -primal solution for (1) in the

last primal iterate of Algorithm (DFG)

after iterations.

Proof.

Let us notice that (see (41)). Firstly,

combining (9) and (40) we obtain

the following important relation characterizing the distance from

the last iterate to the unique optimal solution of our

original problem (1):

(43)

Secondly, combining the previous relation (43)

and (10) we obtain a sublinear estimate for

feasibility violation of the last iterate for Algorithm

(DFG):

(44)

where we again used . Finally,

we derive a sublinear estimate for primal suboptimality of the last

iterate . We first prove that . Indeed, taking in Theorem 4.1

and using that the terms and

are positive we

have:

Using the triangle inequality and dividing by

, we further have:

Using an inductive argument, we can conclude that:

(45)

Combining (45) with relations (12) and

(43) and using the definition of

we obtain:

(46)

In conclusion, we have obtained sublinear estimates of

order for primal infeasibility

(inequality (4.1)) and primal suboptimality

(inequality (4.1)) for the last primal iterate

sequence generated by Algorithm (DFG).

Now, if we want to get an -primal solution in we

need to perform iterations.

∎

In [1] estimates of order

have been given for primal infeasibility

and suboptimality for the last primal iterate generated by

Algorithm (DFG). However, those derivations are based on

the assumption of Lipschitz continuity of the objective function

, while in our derivations we do not need to impose this

additional condition, since our proofs make use explicitly of the

properties of the algorithm as given in Theorem 4.1 and the

inequality (45). Note that for some applications the

assumption of Lipschitz continuity of objective function may be

conservative: e.g. quadratic objective function and unbounded

set .

Finally, we consider the application of dual fast

gradient Algorithm (DFG) for the regularization of the dual

problem of (1), i.e.:

(47)

Note that regularization strategies have been also used in other

papers, e.g. in order to make the norm of the gradient of some

objective function small by using first order methods

[18, 6]. We show in the sequel that by

regularization we can improve substantially the convergence rate of

dual fast gradient method in the last iterate. Denoting

the optimal solution of (47), its

optimality conditions are given by:

(48)

Note that the regularized dual objective function

in (47) is strongly concave with

and has Lipschitz gradient with

. Then, if we replace in

Step 3 of Algorithm (DFG) the term with the constant term , i.e.:

the modified dual fast gradient algorithm achieves linear

convergence [16]. More precisely, for solving the

regularized dual problem (47) with the modified

Algorithm (DFG) described above we have the convergence

rate:

We want to find first an upper bound on in terms of . Since

is -strongly concave function and

, we have:

Based on the previous inequality we can bound as follows:

Thus, the number of iterations we need in order to

attain accuracy, i.e. , is given by:

(49)

Since and , we get that after the number of iterations

(49) we have from that:

Let us assume for simplicity that and

choose:

(50)

Then, we get an estimate on dual suboptimality for the dual problem

of (1):

We are now ready to prove one the main results of this

paper:

Theorem 4.4.

Let Assumption 2.1 hold and the

sequences be generated by the

modified Algorithm (DFG). Then, for a given accuracy

we get an -primal solution for

(1) in the last primal iterate of

modified Algorithm (DFG) after

iterations.

Proof.

First, we determine a bound on .

Since is -strongly concave function and

, we have:

(51)

Moreover, since the dual gradient is Lipschitz,

it satisfies [16]:

Using that in the

previous inequality we obtain:

Now using the previous bound on , the fact that and the expressions of

and we get an estimate on primal infeasibility in

the last primal iterate :

In order to derive a convergence estimate on primal

suboptimality, we observe that for any , the

optimality conditions of the inner subproblem are given by:

(52)

Since is concave and has Lipschitz continuous

gradient, it satisfies [16]:

Taking into account the expression for , using in the previous inequality and the optimality

conditions for , we have:

(53)

On the other hand, using the strong convexity of the

function and taking in

(52), we obtain:

Adding in both sides the term , we get:

Taking in (48), using (53),

Lipschitz gradient property of ,the fact that

, the Cauchy-Schwartz inequality and previous

inequality, we obtain:

On the other hand, we have:

Therefore, using (50) and the facts that

and , we derive the

convergence rate for primal suboptimality from the previous

estimates on suboptimality and infeasibility:

where .

Now, if we replace the expression for from

(50) in the expression of from (49)

it follows that we obtain -accuracy for primal

suboptimality and infeasibility in the last primal iterate for

the modified Algorithm (DFG) after

iterations.

∎

From Theorem 4.4 it follows that we

obtain -accuracy for primal suboptimality and

infeasibility for the modified Algorithm (DFG) in the last

primal iterate after

iterations which is better than

iterations obtained in Theorem 4.3 for the last primal

iterate or in [1]. From our knowledge Theorem

4.4 provides the best convergence rate for dual

fast gradient method in the last iterate. However, the modified

algorithm needs to know the parameter , that according to

(50), is depending on . In

practice, we need to know an estimate of .

4.2 Sublinear convergence in an average primal sequence

In this section we derive sublinear

estimates for primal infeasibility and suboptimality of the average

primal sequence as defined in (42)

for Algorithm (DFG).

Theorem 4.5.

Let Assumption 2.1 hold and the

sequences be generated by

Algorithm (DFG). Then, for a given accuracy we

get an -primal solution for (1) in the

average primal iterate of Algorithm (DFG) after

iterations.

Proof.

For any we have Let us denote . Then, we can write as follows:

(54)

Note that . Further, summing on the history, multiplying by the previous relation and using the definition of , we obtain:

Since (according to (19)), we have . In conclusion, using the definition of the distance, we obtain:

Taking in (39) and using

that the two terms and are positive,

we get for all . Moreover, we have . Thus, we can further bound the primal infeasibility as follows:

(55)

Further, we derive sublinear estimates

for primal suboptimality. First, note that:

Summing on the history and using the convexity of

, we get:

(56)

Using (56) in (39), and dropping

the term , we have:

(57)

Taking in the previous inequality, we get:

Taking in account that , then we have:

(58)

On the other hand, we have:

(59)

From (58) and (59) we obtain an

estimate on primal suboptimality:

(60)

Thus, we have obtained sublinear estimates of order

for primal infeasibility (inequality

(55)) and primal suboptimality (inequality

(60)) for the average primal sequence generated by Algorithm (DFG). Now, if we want to

get an -primal solution in we need to

perform iterations.

∎

Based on (36), we can also characterize the

distance from to the unique primal optimal solution

. Using (55) and (58), we get:

In Theorem 4.4 we obtained an

-primal solution for the modified Algorithm (DFG)

in the last primal iterate after

iterations, which is of the same order (up to a logarithmic term)

as for the primal average sequence from previous Theorem

4.5. Moreover, the reader should also notice that all our

previous convergence estimates depend only on three constants: the

Lipschitz constant , the initial starting dual point

and its distance to the dual optimal set denoted

. Moreover, if , then , i.e. the function values in the primal average

sequences are always below the optimal value for Algorithms

(DG) and (DFG).

5 Dual error bound property and linear convergence of dual first order methods

In this section, we show that if the dual problem has an error bound type property we can get an -primal solution for problem (1) with the previous dual first order methods in iterations. Thus, in this section we assume that the dual problem of (1) has an error bound property. More precisely, we assume that for any there exists a constant depending on and the data of problem (1) such that the following

error bound property holds for the corresponding dual problem of (1):

(61)

where (i.e. the Euclidean projection

of onto the optimal dual set ) and recall that denotes the gradient map: .

Remark 1.

For example, if we consider a linearly constrained convex problem ():

(62)

where we assume that is -strongly convex

function and has -Lipschitz continuous

gradient, and , then in [8, 10, 25] it has been

proved that the corresponding dual problem satisfies an error bound type property. Indeed, for the convex function , we denote its conjugate by [21]: . According to Proposition 12.60 in [21], under the previous assumptions, function is strongly

convex w.r.t. Euclidean norm, with constant

and has

Lipschitz continuous gradient with constant . Note that in these settings our

dual function of (62) can be written as: . Since is strongly convex, the dual gradient is Lipschitz continuous with constant

[17]. Furthermore, if has full row rank, then it

follows immediately that the dual function is strongly convex.

Therefore, we consider the nontrivial case when is rank

deficient. In [8, 10, 25] it has been proved that

for convex problem (62) with

function being -strongly convex and having

-Lipschitz gradient and , for any there exists a constant depending

on and the data of problem (62) such that an

error bound property of the form (61) holds for the corresponding dual problem. ∎

Next, we derive a strong convex like inequality that will be used in the sequel.

Theorem 5.1.

Under Assumption (2.1) and the error bound property (61) for the corresponding dual of convex problem (1) the following inequality holds:

(63)

Proof.

Let us define so that . Note that is the optimal solution of the following convex problem:

(64)

From (6) and the optimality conditions of

(64) we get the following increase in terms of the objective

function :

Firstly, we consider Algorithm (DG)). For simplicity, we assume

constant step size . Since

Algorithm (DG) is an ascent method according to

(23), we can take . Thus, the error bound

property (61) holds for the sequence generated by Algorithm (DG), i.e. there exists

such that:

(66)

where . The following theorem

provides an estimate on the dual suboptimality for Algorithm (DG) with constant step size.

Theorem 5.2.

Under Assumption (2.1) and the error bound property (61) for the corresponding dual of problem (1), the sequence generated

by Algorithm (DG) converges linearly in terms of the distance to the dual optimal set and of the dual objective function values:

Taking now in the previous relations and using

and the strong convex like inequality (63), we get:

or equivalently

(68)

Thus, we obtain linear convergence rate in terms of distance to the optimal set :

(69)

We can also derive linear convergence in terms of dual

function values:

∎

Note that our proof from Theorem

5.2 is different from Tseng’s proof

[24] for linear convergence of gradient method under an

error bound property. More precisely, in our proof we make use

explicitly of the strong convex like inequality (63) which

allows us to get for better convergence rate

than in [24].

We now derive linear estimates for primal infeasibility and

primal suboptimality for the last iterate sequence generated by our Algorithm (DG) with constant step size

. For simplicity of the exposition

let us denote:

Under the assumptions of Theorem 5.2,

let the sequences be generated by

Algorithm (DG). Then, for a given accuracy we get

an -primal solution for (1) in the last primal

iterate of Algorithm (DG) after iterations.

Proof.

Combining (9) and (70) we obtain the

following relation:

(71)

Then, combining the previous relation

(71) and (10) we obtain a linear

estimate for feasibility violation of the last iterate :

(72)

where we used the definitions of and . Finally, we derive linear

estimates for primal suboptimality of the last iterate .

Combining (71) and (12) we obtain:

(73)

In conclusion, we have obtained linear estimates of order

, with , for primal infeasibility

(inequality (72)) and suboptimality (inequality

(5)) for the last iterate sequence generated by Algorithm (DG). Now, if we want to get an

-primal solution in we need to perform iterations.

∎

Secondly, we show that under Assumption (2.1)

and the error bound property (61) for the

corresponding dual of problem (1), a restarting

version of Algorithm (DFG) has linear convergence. Similar to

Algorithm (DG), we can also take in this case and thus the error bound property (61)

holds for the sequence generated by a restarting

version of Algorithm (DFG). Indeed, combining

(40) and (63) we get:

where we choose a positive constant such that

Then, for fixed , the number of iterations that we need to

perform in order to obtain

is given by:

Note that if the optimal value is known in advance, then we just need to

restart Algorithm (R-DFG) at iteration when the following condition holds:

which can be practically verified. After each steps of Algorithm (DFG) we

restart it obtaining the following scheme:

Algorithm (R-DFG) Given and restart interval . For do:1.Run Algorithm (DFG) for iterations to get 2.Restart: , and

.

Then, after restarts of Algorithm (R-DFG) we obtain linear

convergence in terms of dual suboptimality:

Theorem 5.4.

Under Assumption (2.1) and

the error bound property (61) for the

corresponding dual of problem (1), the

sequence generated by

Algorithm (R-DFG) converges linearly in terms of the dual

objective function values, i.e.:

(74)

Proof.

After restarts of Algorithm (R-DFG) we have:

Thus, the total number of iterations is . Since it

follows that is the gradient step from and thus

. Therefore, we may assume for simplicity that . For we have:

provided that we perform number of iterations.

∎

Next theorem shows linear convergence in terms of primal suboptimality and infeasibility of the last primal iterate generated by Algorithm (R-DFG).

Theorem 5.5.

Under the assumptions of Theorem 5.4, we get

an -primal solution for (1) in the last primal

iterate of Algorithm (R-DFG) after iterations.

Proof.

Combining (9) and (74) we obtain the

following relation:

(75)

Then, combining the previous relation

(75) and (10) we obtain a linear

estimate for feasibility violation of the last iterate :

(76)

where we used the definition of . Finally, we derive linear estimates for

primal suboptimality of the last iterate . Combining

(75) with (45) we get:

(77)

In conclusion, we get an

-primal solution in the last primal iterate provided that we perform iterations of Algorithm (R-DFG).

∎

From our knowledge, the results stated in Theorems

5.4 and 5.5 answer for the

first time to a question posed by Tseng [24] related to

whether there exist fast gradient schemes that converge linearly

on convex problems having an error bound property.

6 Better convergence rates for dual

first order methods in the last primal iterate for

linearly constrained convex problems

In this section we prove that for linearly constrained convex

problems () we can get better iteration complexity estimates for dual first order methods corresponding to the last primal iterate sequence. More precisely, we prove

that we can improve substantially the convergence rate of dual

first order methods (DG) and (DFG)) in the last

iterate when the optimization problem (1) has

linear equality constraints: i.e. instead of . Therefore, in this section we consider a particular case for the optimization

problem (1), namely a linearly constrained

convex optimization problem of the form:

(78)

For (78) we still require Assumption (2.1) to hold: i.e. is -strongly convex function,

a simple convex set and there exists a finite optimal Lagrange multiplier .

Since is strongly convex and , the dual gradient is Lipschitz continuous with constant (see e.g. [17]). We

analyze below the convergence behavior of dual first order methods

for solving the linearly constrained convex problem

(78). Note that since we have linear constraints in

(78), i.e. , the corresponding dual problem is unconstrained, i.e. .

Case 1: We first consider applying steps of Algorithm (DG). For simplicity, let us assume constant step size for solving the corresponding dual of problem

(78).

Theorem 6.1.

For problem (78) let be

-strongly convex function, be simple convex set

and the set of optimal multipliers be nonempty. Further, let the

sequences be generated by Algorithm

(DG) with . Then, for a given

accuracy we get an -primal solution for

(78) in the last primal iterate of Algorithm

(DG) after

iterations.

Proof.

We have proved in (23) that gradient algorithm is an ascent method, i.e.:

Adding for to and using that the gradient map sequence is decreasing along the iterations of Algorithm (DG) (see Lemma 2.5), we get:

(79)

Since , we obtain:

From we obtain a sublinear estimate for feasibility violation

of the last primal iterate of Algorithm

(DG):

(80)

We can also characterize primal suboptimality in the last

iterate for Algorithm (DG) using that , the estimate on infeasibility (80) and the

inequalities (13)–(14):

(81)

Therefore, we have obtained sublinear estimates of order

for primal infeasibility (inequality

(80)) and primal suboptimality (inequality (81))

for the last primal iterate sequence generated by

Algorithm (DG). Now, it is straightforward to see that if

we want to get an -primal solution in we need to

perform iterations.

∎

In conclusion, from Theorem 6.1 it

follows that we obtain -accuracy for primal suboptimality

and infeasibility for Algorithm (DG) in the last primal

iterate after

iterations. This is better than

iterations obtained in Theorem 3.3 for the last primal

iterate and it is of the same order as for the primal average

sequence from Theorem 3.4. However, this

better result is obtained for the particular linearly constrained

convex problem (78). Note that an immediate consequence of

Lemma 2.5 for this case is that the

sequence is decreasing, i.e.:

Case 2: We now consider an hybrid algorithm

that applies steps of Algorithm (DFG) and then

steps of Algorithm (DG) for solving the corresponding

dual of problem (78).

Theorem 6.2.

Under the assumptions of Theorem

6.1 let the sequences be generated by applying steps of

Algorithm (DFG) and then steps of Algorithm

(DG) with . Then, for a given

accuracy we get an -primal solution for

(78) in the last primal iterate of this algorithm

after iterations.

Proof.

Since the gradient algorithm is an ascent method (see (23)), we have:

Adding for to and using the decrease of the gradient map, we get:

Since , we obtain:

. From we obtain a sublinear estimate for feasibility

violation of the last primal iterate of this

hybrid algorithm:

(82)

We can also characterize primal suboptimality in the last

iterate for this hybrid algorithm using that , the estimate (82) and the

inequalities (13)–(14):

(83)

Therefore, we have obtained sublinear estimates of order

for primal infeasibility

(inequality (82)) and primal suboptimality (inequality

(83)) for the last primal iterate sequence generated by an algorithm applying steps of (DFG)

and then steps of (DG). Now, it is straightforward to

see that if we want to get an -primal solution in

we need to perform

iterations.

∎

For the linear constrained problem (78) in

[22] convergence rate was

derived for the last primal iterate of Algorithm (DFG)

(see also our Theorem 4.3 that gives the same

convergence rate for conic problems). However, Theorem

6.2 shows that applying further gradient

steps we can improve the convergence rate to

for problem (78).

In conclusion, in this paper we obtained the following

estimates for the convergence rate of dual first order methods:

•

in a primal average sequence we have

for Algorithm (DG) and

for Algorithm

(DFG)

•

in the last iterate they are are summarized in Table 1.

Table 1: Rate of convergence estimates of dual first

order methods in the last primal iterate.

7 Better convergence rates for dual first order methods

in the last primal iterate for conic convex problems

In this section we prove that some of the results of the previous

section can be extended to conic convex problem

(1). More precisely, we prove that we can improve

substantially the convergence estimates for primal infeasibility and

left hand side suboptimality of dual first order methods in the last iterate for the general problem (1).

Case 1: We first consider applying steps

of Algorithm (DG). For simplicity, let us assume

constant step size for solving the

corresponding dual of problem (1). Indeed, we

have proved in (23) that gradient algorithm is an ascent

method, i.e.:

Adding for to and using that the gradient

map sequence is decreasing along the iterations of Algorithm (DG) (see Lemma 2.5), we get:

(84)

Since , we obtain:

From we obtain a sublinear estimate for feasibility violation

of the last primal iterate of Algorithm

(DG):

(85)

We can also characterize primal suboptimality in the last

iterate for Algorithm (DG). On one hand, using

the estimate on infeasibility (85) and the definition

of the dual cone , we have:

Therefore, we have obtained sublinear estimates of order

for primal infeasibility (inequality

(85)) and left hand side suboptimality (inequality

(7)) and of order

for right hand side primal suboptimality (inequality

(7)) for the last primal iterate sequence

generated by Algorithm (DG).

Case 2: We now consider an hybrid algorithm

that applies steps of Algorithm (DFG) and then

steps of Algorithm (DG) for solving the corresponding

dual of problem (1). Since the gradient

algorithm is an ascent method (see (23)), we have:

Adding for to and using the decrease of the gradient map, we get:

Since , we obtain:

. From we obtain a sublinear estimate for feasibility

violation of the last primal iterate of this

hybrid algorithm:

(88)

We can also characterize primal suboptimality in the last

iterate for this hybrid algorithm. Using the estimate

(88), a similar reasoning as in the relations

(7) leads to:

Therefore, we have obtained sublinear estimates of order

for primal infeasibility

(inequality (88)) and for left hand side primal

suboptimality (inequality (89)) and of order

for right hand side primal suboptimality

(inequality (7)) for the last primal iterate

sequence generated by Algorithm (DG).

8 Numerical simulations

For numerical experiments we consider random

problems of the following form:

where is positive definite matrix with

, , and . We need

to remark that the objective function is not convex for , but it is convex e.g. when on

or when on .

Note that this type of problems arises in many practical

applications: in network utility maximization [1]

; in resource allocation problems

[27] ; in optimal power

flow or model predictive control [11] (). All

the data of the problem are generated randomly and is sparse

having tens of nonzeros () on each row for large

problems (). We have considered the accuracy

, the value for and the

stopping criteria in the tables below were chosen as follows:

where is either the last primal iterate () or average

of primal iterates () and we allow at most number

of iterations for each algorithm.

8.1 Case 1:

In the first set of experiments we choose

and simple constraints (e.g. network utility

maximization problems [1] can be recast in this form).

In this type of applications the complicating constraints are related to the capacity of the links and we need to also

impose simple constraints , since represents the

source rates. Note that the objective function is strongly convex

and with Lipschitz gradient on . However, the presence of simple

constraints makes the dual function degenerate (i.e. does not

satisfy an error bound property).

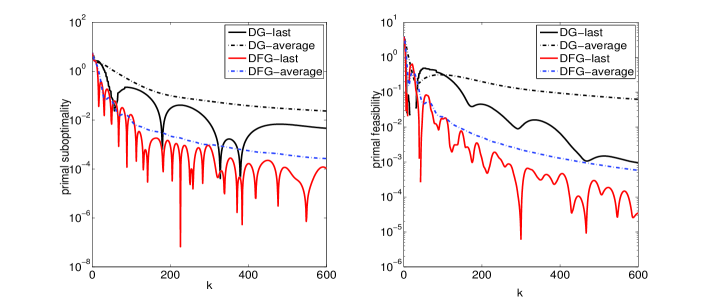

Typically, the performance in terms of primal

suboptimality and infeasibility of Algorithms (DG) and

(DFG) in the primal last iterate or in the average of

primal iterates is oscillating as Fig. 1 shows. However, these

algorithms have a smoother behavior in the average of iterates than

in the last iterate. Moreover, from our numerical experience we

have observed that for our dual first order methods we usually have

a better behavior in the last iterate than in the average of

iterates as we can also see from Fig. 1 and Table 1 (in the table we

display the average number of iterations for random problems

for each dimension ranging from to ). On the other

hand, our worst case convergence analysis says differently, i.e.

we have obtained better theoretical estimates in the primal average

sequence than in the last primal iterate sequence. This does not

mean that our analysis is weak, since we can also construct

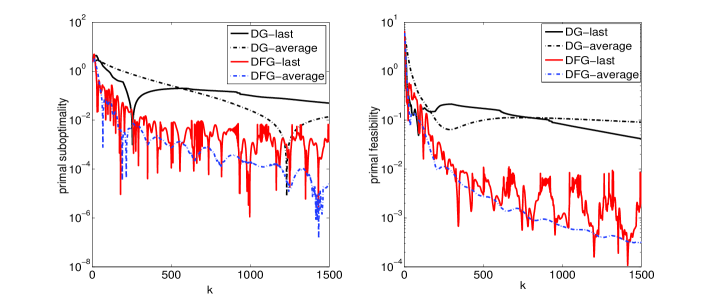

problems which show the behavior predicted by our theory, see e.g.

Fig. 2 where indeed we have a better behavior in the average of

iterates than in the last iterate.

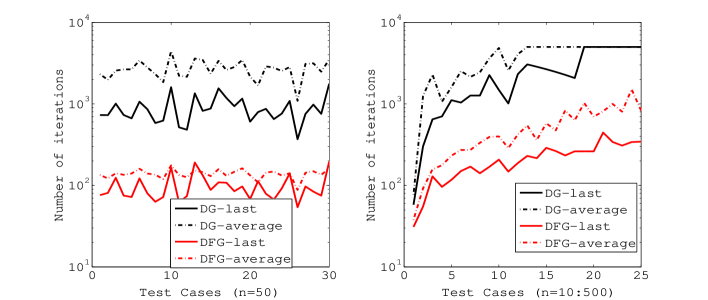

Finally, in Fig. 3 we plot the practical number of

iterations of Algorithms (DG) and (DFG) for

different test cases of the same dimension (left) and for

different test cases of variable dimension ranging from to

(right). From this figure we observe that the number of

iterations are not varying much for different test cases and also

that the number of iterations are mildly dependent of problem’s

dimension.

Figure 1: Typical performance in terms of

primal suboptimality and infeasibility of

Algorithms (DG) in the last iterate (DG-last), (DG) in average (DG-average),

(DFG) in the last iterate (DFG-last) and (DFG) in average (DFG-average) for .

Table 2: Average number of iterations

for random problems for each dimension for Algorithms

(DG) and (DFG) in the last iterate and in the

average of iterates. We observe that dual first order methods perform

better in the primal last iterate than in the average of iterates.

Alg./n

Figure 2: Practical performance comparable with the

theoretical estimates for primal suboptimality and infeasibility of

Algorithms (DG) in the last iterate (DG-last),

(DG) in average (DG-average), (DFG) in the last

iterate (DFG-last) and (DFG) in average (DFG-average) for

.

Figure 3: Practical number of iterations of

Algorithms (DG) in the last iterate (DG-last),

(DG) in average (DG-average), (DFG) in the last

iterate (DFG-last) and (DFG) in average (DFG-average) for

random test cases of fixed dimension (left) or variable

dimension ranging from to (right).

8.2 Case 2:

In the second set of experiments we choose and simple box constraints defining the set (e.g. this optimization model, in separable form, was

considered in [27] for resource allocation problems).

In this case the objective function is strongly convex and has

Lipschitz gradient on . Therefore, if the simple box constraints are

missing, then according to our theory given in Section

5 Algorithm (DG) is converging linearly.

We first consider box constraints

and the results (average number of iterations) are shown in Table 2

for random problems for each dimension ranging from to

. We can again observe that dual first order methods perform

better in the primal last iterate than in the average of iterates. Further, we can notice

that the behavior of Algorithm (DG) in the last iterate is

comparable to that of Algorithm (DFG) in average. However,

the inner problem has to be solved with higher accuracy in Algorithm

(DFG) than in (DG) since the first one is more

sensitive to errors, such as inexact first order information, than

the last one (see [11] for a more in depth discussion on inexact dual

first order methods).

Table 3: Average number of iterations

for random problems for each dimension for Algorithms

(DG) and (DFG) in the last iterate and in the

average of iterates. We can again observe that dual first order methods perform

better in the primal last iterate than in the average of iterates.

Alg./n

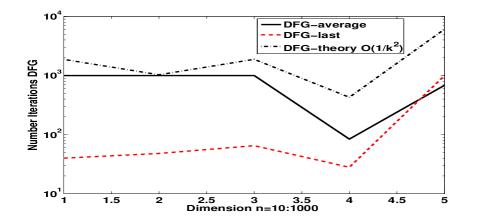

Then, we also take and we solve the corresponding QP problems over an

increasing dimension to . In Fig. 4 we compare for Algorithm (DFG) the real number of iterates in the primal latest iterate and average of iterates and the estimated number of iterates for a primal suboptimality and infeasibility level of . We observe from Fig. 4

that our theoretical estimates are quite close to the practical ones for the

dual fast gradient method.

Figure 4: Real number of iterates in the primal latest iterate and average of iterates

and the estimated number of iterates for Algorithm (DFG).

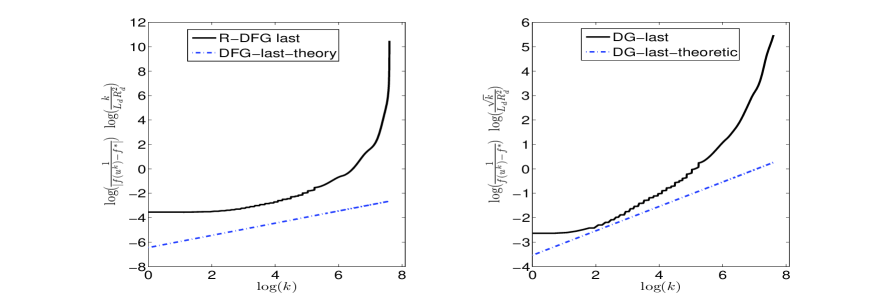

Finally, we drop the simple box constraints (i.e. now ) and for dimension we plot in Fig. 5

the behavior of Algorithm (DG) in the last iterate along

iterations, starting from . From our results (see Section

5) we have linear convergence, which is also seen in

practice from this figure (in logarithmic scale). In the same figure

we also plot the theoretical sublinear estimates for the

convergence rate of Algorithm (DG) in the last iterate as

given in Section 3.1 (see (29) and

(3.1)). The plot clearly confirms our theoretical

findings, i.e. linear convergence of Algorithm (DG) in the

last iterate, provided that .

Figure 5: Linear convergence of Algorithms

(DG) and (R-DFG) in the last iterate for : logarithmic

scale of primal suboptimality. We also compare

with the theoretical sublinear estimates (dot lines) for the

convergence rate in the last iterate. The plot clearly shows our theoretical

findings, i.e. linear convergence.

References

[1]

A. Beck, A. Nedic, A. Ozdaglar, and M. Teboulle,

Optimal distributed gradient methods for network resource allocation problems,

IEEE Transactions on Control of Network Systems, 1(1):1–10, 2014.

[2]

E. Gustavsson, M. Patriksson, and A.B. Stromberg,

Primal convergence from dual subgradient methods for convex optimization,

Mathematical Programming, Ser. A, 2014.

[3]

M. Hong and Z.Q. Luo,

On the linear convergence of the alternating direction method of

multipliers,

Technical report, University of Minnesota, arxiv.org/abs/1208.3922,

2012.

[4]

F. P. Kelly, A.K. Maulloo, and D.K.H. Tan,

Rate control in communication networks: shadow prices, proportional

fairness and stability,

Journal of the Operational Research Society, 49:237–252, 1998.

[5]

K.C. Kiwiel, T. Larsson, and P.O. Lindberg,

Lagrangian relaxation via ballstep subgradient methods,

Mathematics of Operations Research, 32(3):669–686, 2007.

[6]

G. Lan and R.D.C. Monteiro,

Iteration-complexity of first-order augmented lagrangian methods for convex programming,

Mathematical Programming, 2015.

[7]

T. Larsson, M. Patriksson, and A.B. Stromberg,

Ergodic convergence in subgradient optimization,

Optimization Methods and Software, 9(1–3):93–120, 1998.

[8]

Z.Q. Luo and P. Tseng,

On the convergence of coordinate descent method for convex

differentiable minimization,

Journal of Optimization Theory and Applications, 72(1):7–35, 1992.

[9]

Z.Q. Luo and P. Tseng,

On the convergence rate of dual ascent methods for

linearly constrained convex minimization,

Mathematics of Operations Research, 18(4):846–867, 1993.

[10]

I. Necoara and V. Nedelcu,

On linear convergence of a distributed dual gradient algorithm for

linearly constrained separable convex problems,

Automatica, in press:1–9, 2015.

[11]

I. Necoara and V. Nedelcu,

Rate analysis of inexact dual first order methods: application to dual decomposition,

IEEE Transactions on Automatic Control, 59(5):1232 –1243, 2014.

[12]

I. Necoara and J.A.K. Suykens,

Application of a smoothing technique to decomposition in convex optimization,

IEEE Transactions on Automatic Control, 53(11):2674–2679, 2008.

[13]

I. Necoara and J.A.K. Suykens,

An interior-point lagrangian decomposition method for separable convex optimization,

Journal of Optimization Theory and Applications, 143(3):567–588, 2009.

[14]

V. Nedelcu, I. Necoara, and Q. Tran Dinh,

Computational complexity of inexact gradient augmented lagrangian methods: application to constrained MPC,

SIAM Journal on Control and Optimization, 52(5):3109–3134, 2014.

[15]

A. Nedic and A. Ozdaglar,

Approximate primal solutions and rate analysis for dual subgradient methods,

SIAM Journal on Optimization, 19(4):1757–1780, 2009.

[16]

Y. Nesterov,

Introductory Lectures on Convex Optimization: A Basic Course,

Kluwer, Boston, USA, 2004.

[17]

Y. Nesterov,

Smooth minimization of non-smooth functions,

Mathematical Programming, 103(1):127–152, 2005.

[18]

Y. Nesterov,

How to make the gradients small,

Optima, 88:10–11, 2012.

[19]

Y. Nesterov,

Gradient methods for minimizing composite functions,

Mathematical Programming,

140(1):125–161, 2013.

[20]

P. Patrinos and A. Bemporad,

An accelerated dual gradient-projection algorithm for embedded linear model predictive control,

IEEE Transactions on Automatic Control, 59(1):18–33, 2014.

[21]

R.T. Rockafellar and R.J. Wets,

Variational Analysis,

Springer-Verlag, New York, 1998.

[22]

A. Beck and M. Teboulle,

A fast dual proximal gradient algorithm for convex minimization and applications,

Operations Research Letters, 42(1):1–6, 2014.

[23]

P. Tseng,

On accelerated proximal gradient methods for convex-concave optimization,

SIAM Journal of Optimization, submitted:1–20, 2008.

[24]

P. Tseng,

Approximation accuracy, gradient methods and error bound for structured convex optimization,

Mathematical Programming, 125(2):263–295, 2010.

[25]

P.W. Wang and C.J. Lin,

Iteration complexity of feasible descent methods for convex optimization,

Journal of Machine Learning Research, 15:1523–1548, 2014.

[26]

E. Wei, A. Ozdaglar, and A. Jadbabaie,

A distributed newton method for network utility maximization –

Part I and II,

IEEE Transactions on Automatic Control, 58(9), 2013.

[27]

L. Xiao and S. Boyd,

Optimal scaling of a gradient method for distributed resource allocation,

Journal of Optimization Theory and Applications, 129(3), 2006.

[28]

R.D. Zimmerman, C.E. Murillo-Sanchez, and R.J. Thomas,

Matpower: Steady-state operations, planning, and analysis tools for power systems research and education,

IEEE Transactions on Power Systems, 26(1):12–19, 2011.