Letter to the Editor

arXiv:0000.0000 \startlocaldefs \endlocaldefs

and ,

1 Dedication

This Letter is dedicated to the 50th anniversary of unexpected death of Samuel Stanley Wilks. To exact distribution of His, Wilks’s, statistics first author devoted his ”Lambert W research” in 2000-2003.

2 Introduction

In 1938, Samuel Stanley Wilks proved the -asymptotics of , where is the likelihood ratio statistics in regular exponential family (see Wilks S.S. (1938) [30]). But how does the exact CDF of look like? Stehlík M. (2003) [23], derived the exact cumulative distribution function of and decomposition of Kullback-Leibler-divergence (I-divergence) in the sense of Pázman A. (1993) [21], by substantial usage of Lambert W function, firstly introduced by Johann Heinrich Lambert in 1758 (see [20]), a contemporary of Euler. The paper by Goerg G. M. (2011) [13], ”Lambert W random variables-a new family of generalized skewed distributions with applications to risk estimation”, introduced a class of so called Lambert W F random variables,

| (2.1) |

where is skewness parameter and is continuous random variable. Stehlík M. (2003) [23] derived the exact distribution of Wilks statistics to test for the scale hypothesis in the regular Gamma family and proven that Wilks statistics is a function of a random variable

| (2.2) |

where is random variable from exponential family. Here, notice that

| (2.3) |

where of Goerg G. M. (2011) [13] is defined by (2.1) and The statistical application of the class (2.1) and ”Lambert W function” is intrinsically related to I-divergence decompositions and the importance they play in statistical inference. Stehlík M. (2003) [23] derived that Kullback-Leibler divergence in the sense of Pázman (1993) [21] has the form

| (2.4) |

Notice, that is the ”basic” information of LR test, based on just a single random variable , directly relating nonlinearly transformed of Goerg G. M. (2011) [13] to of Stehlík M. (2003) [23] (see (2.3)). In Stehlík M. (2006) [24] and Stehlík M. (2008) [25] extension of results to Weibull and generalized Gamma distributions (Ggds) was made. Considered Ggd covers for various choices of parameters of one-sided normal, Weibull and in the limit a log-normal distribution. The LW function approach based on transformation was used for exact inference for Pareto heavy tailed distribution in Stehlík M. et al. (2010) [26]. The LW function approach and transformation was used fundamentally in Balakrishnan and Stehlík (2008) [2] for extension of results also to cases of Type I and Type II censored samples and missing data.

In this letter we discuss several important methodological and practical aspects of Lambert W variable. According Goerg G. M. (2011) [13] the Lambert W framework is a new generalized way to analyze skewed, heavy-tailed data. In the next two sections we discuss both, heavy-tails and skewness perspectives of this Lambert W framework.

In the next section ”Heavy Tails: On three regimes of IGMM-algorithm”, based on heavy-tailedness we define three Regimes of Goerg G. M. (2011)’s Algorithm 3, and its implementation IGMM in R-package LambertW. However, current implementation of algorithm 3 cannot work in all three Regimes. In Regime III, where no moments of financial data exist, we show that IGMM is not working. Based on simple graphical method we give a practical guidelines how to discriminate between regimes. Also we introduce a robust tests for normality against heavy tails to enable a formal statistical procedure for the better linking of a given data to Regimes. The introduced methodology is illustrated on LATAM data, used by Goerg G. M. (2011). Also suggestion for correction of Algorithm 3 in Regime III is provided.

In the section ”Skewness: On asset Returns and t-distribution” we discussed difficulties with symmetrization of data, based on transformation introduced by Goerg G. M. (2011) [13].

3 Heavy Tails: On three regimes of IGMM-algorithm

In this section we describe three regimes of iterative method of moments introduced by Goerg G. M. (2011) [13] (IGMM-Method). The description is based on approximations by random walk, respectively to heavy-tailedness of input variable Such a description is important, in particular for applicability of Algorithm 3 to any financial data, e.g. LATAM data. The three regimes are defined as follows:

-

1.

Regime I: distributions with finite mean and finite variance (here belongs e.g. student--distribution with )

-

2.

Regime II: distributions with finite mean but infinite variance (here belongs e.g. student--distribution with )

-

3.

Regime III: distributions with and infinite variance (here belongs e.g. student--distribution with ).

We are showing that algorithm which works in Regime I (because of Strong-Law of Large Numbers) cannot work well in Regime III, since statistical learning in Regime I is related to arithmetic mean, whereas in Regime III to harmonic mean (see Beran, Schell, and Stehlík (2014) [3]). Before any further methodological discussion we provide illustration of computation with IGMM-method for the three regimes. Since in subexponential family Pareto tail is well fitting to student- (used also in Goerg G. M. (2011) [13]), we simulate samples of 1000 observations of student--distribution with degrees of freedom, to represent all three regimes. The same sample size has been used for the computations on the basis of Pareto distribution. In these regimes we study sensitivity of parameter estimation of , and of implemented function IGMM. The procedure for this sensitivity check is conducted as follows:

-

1.

Simulating a sample from student or Pareto distribution for all three regimes

-

2.

Transformation of for all samples U

-

3.

Estimation of parameters for transformed samples by usage of IGMM.

-

4.

Repeat steps 2.-3. for a different values of .

The calculated differences between the true values and their estimators are shown in Table 1. Higher degrees of freedom lead to better approximations of the parameters. Deviations are higher for increasing and lower degrees of freedom. Due to increasing deviations for smaller it can be assumed that IGMM-method works acceptably for student-t-distribution of Regime I, deviations are larger for Regime II and astronomical deviations are received in Regime III. The similar results are obtained for Pareto distribution. Astronomical deviations of estimation with heavy-tailed distributions are similar to those of student distributions of Regime II and III.

| Student -distribution | Pareto- distribution | ||||||

|---|---|---|---|---|---|---|---|

| 5 | 0.0201 | 0.0182 | 1.2535 | 5 | 1.9479 | 0.3433 | 0.2331 |

| 1.5 | 0.6061 | 0.3993 | 5.5353 | 1.5 | -5.25 | 11.53 | 4.29 |

| 1 | -1.51 | 11.6649 | 0.0000 | 1 | 5.24 | 0.1504 | 1.12 |

| 5 | 0.0449 | 0.0531 | 1.2054 | 5 | 2.1923 | -0.2561 | 2.9713 |

| 1.5 | 1.58 | -0.0494 | 3.36 | 1.5 | 4.49 | 0.0501 | 9.54 |

| 1 | 2.84 | -0.0496 | 6.04 | 1 | 7.74 | 0.0504 | 1.64 |

| 5 | 0.1151 | 0.0445 | 1.2027 | 5 | 2.3260 | 0.2121 | 0.3343 |

| 1.5 | 1.29 | -0.2494 | 2.74 | 1.5 | 3.71 | 0.0004 | 7.89 |

| 1 | 8.99 | -0.2497 | 1.91 | 1 | 9.38 | 0.0005 | 1.99 |

The astronomical discrepancies in Regime III (the case where no finite expectation exists), i.e. are theoretically explained by law of large numbers. Goerg G. M. (2011) [13] has used in his algorithm IGMM intuitively scaled score function, i.e. of the normal distribution

| (3.1) |

where mean is taken as a parameter of interest and is nuisance. Such an algorithm is working when both mean and variance are finite, i.e. for However, when only mean is finite (), the effect of nuisance is well visible (see Table 1). In the case of heavy tailed student (), where both mean and variance are infinite, the error converges in probability to infinity. This can be obtained by usage of e.g. Kolmogorov’s Strong Law of Large Numbers (LLN) (see e.g. [29]). If we have a sample from distribution with infinite mean (e.g. ), i.e. Lebesgue integral then will have a finite limit for with probability zero. Such random walk is introduced in step 8 (among others) of Algorithm 3 of Goerg G. M. (2011) [13], where sample mean and sample deviation updates scale and location parameters. Therefore we shall expect astronomical numbers in both differences of location parameters and ratios of scales with probability 1 (see e.g. rows for Student and rows for Pareto() in Table 1). Such a divergence is not avoided by step 4, namely , in Algorithm 3 of Goerg G. M. (2011) [13].

Random walk of normal scores (3.1) is the reason for this behavior and it explains the astronomical errors of magnitude for distribution. Indeed, especially in financial returns (like Asset returns, discussed in section 7.2 of Goerg G. M. (2011) [13]) we shall expect heavy tailed data. Naturally following questions arise: What should be done in such cases? Can we define some procedure how to check when we can apply IGMM? The answer to this questions is given in the next Sections 3.1 and 3.2.

3.1 Robust testing for normality against Pareto tail

First, we shall testify for the range of Pareto tail parameter against light tailed normal distribution: for this purpose we need to apply a test for normality against Pareto tails. A consistent and robust test developed as a robust version of Jarque-Bera (JB) test based on the location functional is given by Stehlík et al (2012) [27]. This procedure recognizes in which regime we have our data. The developed test also works for arbitrary sample size, which is very practical for financial applications. For a specific alternatives, also robustified directed Lin-Mudholkar tests (see Stehlík, Thulin and Střelec (2014) [28]) have a good trade-off between power and robustness. Before using such a test one shall check for homogeneity in Pareto tail within our financial time series (this is a practical problem, because tail parameters typically varies during the series). Such testing procedure is developed, jointly with likelihood ratio test for simple hypothesis of the Pareto tail in Stehlík et al (2010) [26] by a substantial usage of Lambert W-random variable. We applied robustified JB test of Stehlík et al (2012) [27] for simulated data from Regime II and III, and received p-values 0. Thus it is not recommended to apply IGMM to these two regimes.

To explain this fact from the point of view of finance, we shall realize that LATAM data contains daily log-returns (in percent) of an equity fund investing in Latin America (LATAM) from January 1, 2002 until May 31, 2007. Emerging markets in Latin America (see e.g. [12]) can have different properties on left and right tails. It was shown that e.g. Argentina and Brazil have higher estimates of the right tail index than of the left tail index. Therefore, high positive returns are more likely than similar losses in these growing economies. In 2004 it was observed that positive stock return distribution in e.g. Brazil may not have a finite second moment since the estimated extreme value index was around 0.5. There is (even from 1988) an empirical evidence of non-existence of first moment (see page 9 of [1]). Another increase of heavy tailedness of the right tail has been introduced in the years 2004-2015, where high-frequency trading became more present in Latin America. Analogously, in electric markets less credibility has been given to analysis using empirical means, often quickly replaced by median based techniques (see e.g. [19]).

3.2 A graphical screening between regimes of IGMM

In the following, we show how the three Regimes of IGMM can be recognized based on t-Hill plots. t-Hill estimator is a robust but consistent Pareto tail estimator introduced in Fabián and Stehlík (2009) [7] and its consistency for iid sample was proven in Stehlík et al (2012) [28], whereas for dependent data in Jordanova, Dušek and Stehlík (2013) [18]. We base our regimes discrimination on robust t-Hill, so that regime boundaries are not influenced by possible outliers. However, to decrease variability (and increase efficiency) of specification of type of regime for a given data, we use flexible Harmonic mean estimator introduced in Beran, Schell and Stehlík (2014) [3].

To recall the Harmonic mean estimator, the next definition follows.

Definition 1.

We suppose that are possibly dependent copies of with d.f. , upper order statistics

Let us denote the class of regularly varying functions at infinity, with an index of regular variation equal to , i.e. positive measurable functions such that for all , , as .

| (3.2) |

Harmonic Moment tail Index Estimator has the form

where is tuning parameter.

For we obtain t-Hill, for we have Hill estimator (see Hill (1975) [16]). The tuning parameter is regulating the trade-off between efficiency and robustness. For the effect of large contaminations is bounded, since the Harmonic Moment Tail Index Estimator benefits from the properties of the harmonic mean. However, a larger value of also implies an increased variance. For the Harmonic Moment Tail Index Estimator also has a higher variance than Hill’s estimator.

Remark 1.

Remark on VAR for LATAM returns

As the second example, Goerg G. M. (2011) [13] reexamines the LATAM returns. He assures that ”a comparison of risk estimators (Value at Risk, VAR) demonstrates the suitability of the Lambert W F distributions to model financial data.” From the perspective of minimal mean square error, a Mean-of-order-p (MOP) class of VAR estimators can have a mean square error smaller than that of classical extreme value index (EVI) estimators, not only around optimal levels, but for other levels too (see Gomes, Brilhante and Pestana (2014) [14]). MOP EVI-estimator was introduced in Brilhante, Gomes and Pestana (2012) [8]. Note that if we consider a generalization (motivated by robustness) to of the MOP functionals , we get the t-Hill estimator . This is a VAR-justification of why to use t-Hill estimator for specification of boundaries of the Regimes. Such setup is also of interest for BASEL II (and higher) initiative in banking and audit.

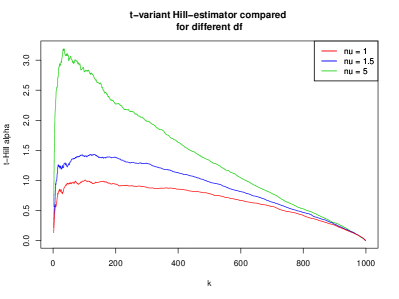

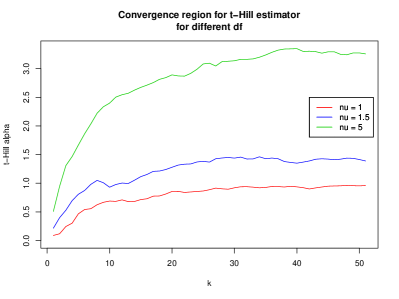

Let be fixed as sample size. Analogously to the Hill plot we consider the set of points with coordinates

Further on we call this plot ”modified Hill plot”. Our graphical procedure is illustrated on discrimination between and in Figure 1.

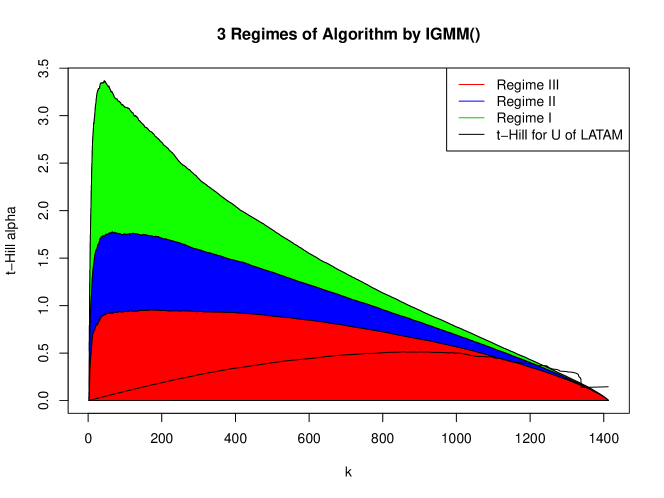

The three colored areas representing Regimes are displayed in Figure 2. Therein also the reciprocal of the harmonic moment tail index estimator (almost Hill-estimator) for unskewed LATAM data (by IGMM and get.input of [13]) is plotted as an estimate for (see [3]). Simulations have shown that using unskewed or original LATAM data yields approximately the same results (not provided here), however, they differ slightly in the upper bound of k due to the occurrences of zeros leading to infinite values in the computations (division by zero). Therefore, we have provided the result for the skewed data, indeed, one way to correct for this obstacle can be to replace zeros by simulated values of uniform distribution between zero and the following order statistics of the returns, which is unequal to zero. Another way would be to use only values unequal to zero in order to avoid this problem.

A sample of length equal to the number of observations of the aforementioned data (n = 1421) has been simulated from Student distribution with degrees of freedom. Following to that the harmonic moment tail index estimator has been computed on the basis of the ordered absolute values by setting in Definition 1 on page 196 in [3]. This has been conducted for each degree of freedom in order to define the area of each Regime. These steps were repeated 100 times (Figure 1 shows the result for 10 repetitions for the sake of comparison) for every setup and the reciprocal of the averages of these Hill estimators (in order to receive ) were plotted against the values of k, whereby . Recall that the almost Hill-estimator visualizes a single run of the algorithm, because it is based on the transformed absolute values of LATAM instead of simulated data.

It is well visible, that LATAM data tail is substantially overlapping with Regime III, thus it is not recommended to process these data with IGMM. To explain this fact from the point of view of finance, we shall realize that LATAM data contains daily log-returns (in percent) of an equity fund investing in Latin America (LATAM) from January 1, 2002 until May 31, 2007. Emerging markets in Latin America (see e.g. [12]) can have different properties on left and right tails. It was shown that e.g. Argentina and Brazil have higher estimates of the right tail index than of the left tail index. Therefore, high positive returns are more likely than similar losses in these growing economies. In 2004 it was observed that positive stock return distribution in e.g. Brazil may not have a finite second moment since the estimated extreme value index was around 0.5. There is (even from 1988) an empirical evidence of non-existence of first moment (see page 9 of [1]). Another increase of heavy tailedness of the right tail has been introduced in the years 2004-2015, where high-frequency trading became more present in Latin America. Analogously, in electric markets less credibility has been given to analysis using empirical means, often quickly replaced by median based techniques (see e.g. [19]).

3.3 On Regime III of IGMM

As mentioned above, Normal score is working in Regime I, but not in Regime III. The classical score function as an indicator of the sensitivity of likelihood , has been built for distributions with support on real line, having all moments (see Fisher (1925) [10]). In case of Regime 3 (no finite moments), we shall not only transform a random variable, but also appropriately transform its inference function. For classical transformed t-score results see Fabián (2001) [6] and Stehlík et al (2010) [26]. In this letter we consider only a semi-parametric setup. For a nonparametric analogy see Dobrovidov, Koshkin and Vasiliev (2012) [4] where scores are defined for a conditionally exponential family in the linear model where are known constants, is Gaussian noise, is a two-component Markov process, is an observable process and is an unobservable useful process.

In our setup, let be the support of the distribution with density , continuously differentiable according to and let be given by Johnson (1949) [17] and Then the transformation-based score or shortly the t-score (see Fabián (2001) [6]) is defined by

which expresses a relative change of a ”basic component of the density”, i.e., density divided by the Jacobian of mapping

It is clear that for Normal distribution, which is an archetypical distribution, we have and , with MLE standing for maximum likelihood estimator, which is the solution of

However, for the Pareto distribution we can consider two recently implemented approaches, namely:

-

•

MLE, which is related to the “standard score” estimation with and and

-

•

-score estimation with (see Stehlík M. et al. (2010) [26]). Notice that the MLE is not robust wrt right outliers, i.e. if , then For -estimation we have t-score

Thus standard estimation gives us (where is harmonic mean) which is an estimator apparently robust against right-outliers.

Thus transformation of the data (e.g. by machinery of Lambert W variable), accompanied with a construction of proper score function transformation is the reasonable further research direction to regularize Algorithm 3 in Regime III.

4 Skewness: On asset Returns and t-distribution

Skewness and symmetry are fundamental objects of statistics and it is interesting to study their transformations. Symmetry itself is related to the nature of the problem and its permutation invariance, and cannot be obtained just by a simple transformation. Thus symmetry is one of the fundamental notions of nonparametric statistics and is fundament for typical value of Hartigan (1969) [15], studied in perspective of reflection groups in Francis, Stehlík and Wynn (2014) [11].

Goerg G. M. (2011) [13] defines a transformation where is skewed output and is symmetrical input. It is true, that having a symmetric zero-mean regulates the skewness. However, the inverse problem is much more delicate, as is demonstrated by the following simulations. In Section 7.2, ”Asset returns”, Goerg G. M. (2011) [13] used Kolmogorov-Smirnov (KS) test, and stated ”As a KS test cannot reject a student t-distribution..”. KS test implementation in R[22], (as function ks.test()) was also used in the function ks.test.t() which was introduced in Goerg G. M. (2011) [13] and in his package LambertW. However, parameters are estimated and thus, classical KS test cannot be used. There exist some more refined distribution theory for the KS test with estimated parameters (see Durbin (1973) [5]), but this is not implemented in ks.test(), used in the function ks.test.t(). The undesirable parameter dependence of such implementation can influence one of the goals of the paper: having a symmetric -distribution input and being a skewed output.

The following example shows, that estimation of parameters affects this aim in an undesirable way. First, we simulated input variable as a skewed t-distribution (see Fernandez and Steel (1998) [9]) with skew parameter . Data was simulated with function rskt(n, df, ) of package skewt. The values for parameter and resulting skewness with four degrees of freedom can be found in left part of Table 2. Then we transformed data to where and have been chosen from grids Finally we estimated and parameters by IGMM and conducted ks.test.t() from this package LambertW. This shows the effect of usage of ks.test.t() jointly with parameter estimation, which led to acceptance of skewed distributions as symmetric student distribution.

For equal to 0.9 or 0.75 we received p-values of 0.502 and 0.269 , and thus skewed distribution (skewness = -0.93 and -1.37) is accepted as symmetric student. First line of Table 2 presents simulation of t-distribution (skewness = -0.3415) and resulting p-value is correctly higher than 0.05. The same comparison was done for skewed normal distribution, which was simulated with rsn(n, xi , omega , alpha ) from package sn. is in this setting skewing parameter and its values can be seen in the first column of the right side of Table 2. Location (xi) and scaling parameters (omega), which are equivalent to mean and standard deviation, were chosen to be and . Skewness was compared for different and p-values resulting from ks.test.t() are presented as before. For all listed cases we received p-values and therefore skewed normal distributions were falsely assumed as symmetric t-distributions. Obviously p-values are decreasing for higher , but for all symmetric t-distribution cannot be rejected for simulated skewed normal distribution.

| Skewed t- and t-distribution | Skewed normal and normal distribution | ||||

|---|---|---|---|---|---|

| skewness | p-value | skewness | p-value | ||

| -0.3415 | 0.2872 | 0.0130 | 0.7731 | ||

| -2.8894 | 0.0001 | 0.20 | -0.0892 | 0.0569 | 0.10 |

| -1.6850 | 0.0000 | 0.40 | 0.0277 | 0.5323 | 0.50 |

| -1.3785 | 0.2693 | 0.75 | 0.0810 | 0.6801 | 1.00 |

| -0.9304 | 0.5017 | 0.90 | 0.8108 | 0.5035 | 2.50 |

| 0.8054 | 0.0924 | 5.00 | |||

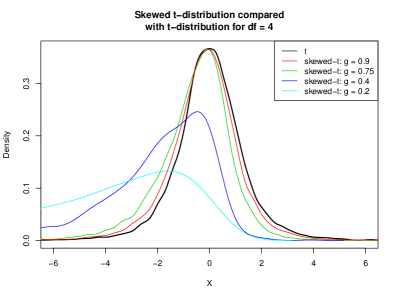

| 0.9391 | 0.0527 | 8.00 | |||

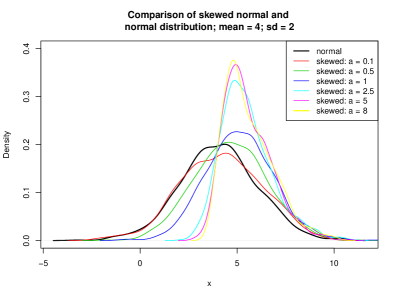

In order to check graphically for impact of and on skewed distributions, kernel density estimations were plotted in R [22]. This density estimation comparison in Figure 3(a) shows stronger skewed distributions for decreasing values of . Distributions were simulated with negative skewness in this example. Black density corresponds to student distribution and the others are computed with previously defined values and show skewed t-distributions. A graphical comparison between skewed normal distributions and normal distribution is done in Figure 3(b). Increasing skewing parameter leads to stronger skewness of the data and a shift to the right. In contrast to the previous examples skewness is except for positive and increasing with .

4.0.1 Auto-Correlation Rising from IGMM and LATAM data

We also checked auto-correlations resulting from estimation by Algorithm 3 for different distributions in a following simulation setup. We simulated standard Normal distribution, Weibull, Exponential and student-t distributions. In the next step IGMM was used to estimate parameters and as a consequence back-transformation with get.input was applied with estimated and . We observed significant auto-correlation for all 4 distributions. Also auto-correlation function of back-transformed series of LATAM has been observed to be significant (e.g. at lags 2, 7, 8, 13 and 30).

References

- Akgiray et al. [2014] Akgiray, V., Booth, G.G., Seifert, B. (1988) Distribution properties of Latin American black market exchange rates. Journal of International Money and Finance, 7(1), 37-48

- Balakrishnan and Stehlík [2008] Balakrishnan N. and Stehlík M. (2008), Exact likelihood ratio test of the scale for censored Weibull sample. Ifas Res.Report 35, online at http://www.jku.at/ifas/

- Beran et al. [2014] Beran J., Schell D., Stehlík M. (2014) The harmonic moment tail index estimator: asymptotic distribution and robustness, Annals of the Institute of Statistical Mathematics 66(1); 193-220.

- Dobrovidov et al. [2012] Dobrovidov A.V., Koshkin G.M. and Vasiliev V.A (2012) Non-Parametric State Space Models. Kendrick Press. USA

- Durbin, J. [1973] Durbin, J. (1973) Distribution theory for tests based on the sample distribution function. SIAM.

- Fabián [2001] Fabián Z (2001). Induced cores and their use in robust parametric estimation. Communications in Statistics—Theory Methods 30 537–556

- Fabián and Stehlík [2009] Fabian, Z. and Stehlík, M. (2009). On robust and distribution sensitive Hill like method. IFAS Research Paper Series , online at http://www.jku.at/ifas/

- Fabián and Stehlík [2009] Brilhante, M.F., Gomes, M.I., Pestana, D. (2013), A simple generalization of the Hill estimator, Computational Statistics & Data Analysis 57, 518–535

- Fernandez, C. and Steel, M. F. J. [1998] Fernandez, C. and Steel, M. F. J. (1998). On Bayesian modeling of fat tails and skewness, J. Am. Statist. Assoc. 93 359-371.

- Fisher [1925] Fisher R. A. (1925). Theory of statistical estimation, Proceedings of the Cambridge Philosophical Society 22 700-725, doi:10.1017/S0305004100009580

- Francis et al. [2014] Francis, R.A., Stehlík, M. and Wynn, H.P. (2014) Exact confidence nets based on finite reflection groups, arXiv:1407.8375 [math.ST]

- Gençay and Selçuk [2004] Gençay, R. and Selçuk, F. (2004). Extreme value theory and Value-at-Risk: Relative performance in emerging markets. International Journal of Forecasting, 20(2), 287-303.

- Goerg [2011] Goerg G. M. (2011). Lambert W Random Variables - A New Family Of Generalized Skewed Distributions With Applications To Risk Estimation. The Annals of Applied Statistics. 5(3) 2197-2230.

- Gomes et al. [2014] Gomes, M.I., Brilhante, F. and Pestana, D.(2014). A mean-of-order-p class of value-at-risk estimators. Theory and Practice of Risk Assessment, Springer Proceedings in Mathematics and Statistics, In Kitsos, C., Oliveira, T., Rigas, A. and Gulati, S. (eds.), p. 1-16,

- Hartigan [1969] Hartigan, J. A.(1969) Using subsample values as typical values. Journal of the American Statistical Association 64, 328, 1303-1317.

- Hill [1975] Hill, B.(1975) A simple general approach to inference about the tail of a distribution, Annals of Statistics 3:5, 1163–1174

- Johnson [1949] Johnson N. L. (1949). Systems of frequency curves generated by methods of translations. Biometrika 36 149-176.

- Jordanova et al. [2013] Jordanova P., Dušek J. and Stehlík M. (2013), Modeling methane emission by the infinite moving average process, Chemometrics and Intelligent Laboratory Systems, 122, 40-49

- Kim et al. [2011] Kim, J. H., Powell, W. B., and Collado, R. A. (2011). Quantile optimization for heavy-tailed distribution using asymmetric signum functions. Princeton University.

- Lambert [1758] Lambert JH(1758). Observationes variae in mathesin puram. Acta Helveticae physico-mathematico-anatomico-botanico-medica, Band III, 128–168.

- Pázman [1993] Pázman A,(1993). Nonlinear statistical Models. Kluwer Acad. Publ. Dordrecht. chapters 9.1 and 9.2

- R [2008] R Core Development Team (2008): A Language and Environment for Statistical Computing. R Foundation for Statistical Computing. Vienna, Austria. ISBN 3-900051-07-0

- Stehlík [2003] Stehlík, M. (2003). Distributions of exact tests in the exponential family. Metrika 57 145–164.

- Stehlík [2006] Stehlík M. (2006). Exact likelihood ratio scale and homogeneity testing of some loss processes. Statistics and Probability Letters 76 19-26.

- Stehlík [2008] Stehlík, M. (2008). Homogeneity and scale testing of generalized gamma distribution. Reliability Engineering & System Safety 93 1809–1813.

- Stehlík et al. [2010] Stehlík M., Potocký R., Waldl, H. and Fabian, Z. (2010). On the favourable estimation of fitting heavy tailed data. Computational Statistics 25 485-503

- Stehlík et al. [2012] Stehlík M., Fabián Z. and Střelec L. (2012). Small sample robust testing for Normality against Pareto tails. Communications in Statistics - Simulation and Computation 41(7) 1167-1194

- Stehlík et al. [2014] Stehlík, M. Thulin, M., Střelec, L. (2014). On robust testing for normality in chemometrics. Chemometrics and Intelligent Laboratory Systems 130 98-108

- Sung [2013] Sung S.H. (2013). On the strong law of large numbers for pairwise i.i.d. random variables with general moment conditions, Statistics and Probability Letters 83 1963-1968

- Wilks [1938] Wilks S. S. (1938). The Large-Sample Distribution of the Likelihood Ratio for Testing Composite Hypotheses. Ann. Math. Statist. 9(1) 60-62.