Multinomial and empirical likelihood under convex constraints: directions of recession, Fenchel duality, perturbations

Abstract

The primal problem of multinomial likelihood maximization restricted to a convex closed subset of the probability simplex is studied. Contrary to widely held belief, a solution of this problem may assign a positive mass to an outcome with zero count. Related flaws in the simplified Lagrange and Fenchel dual problems, which arise because the recession directions are ignored, are identified and corrected.

A solution of the primal problem can be obtained by the PP (perturbed primal) algorithm, that is, as the limit of a sequence of solutions of perturbed primal problems. The PP algorithm may be implemented by the simplified Fenchel dual.

The results permit us to specify linear sets and data such that the empirical likelihood-maximizing distribution exists and is the same as the multinomial likelihood-maximizing distribution. The multinomial likelihood ratio reaches, in general, a different conclusion than the empirical likelihood ratio.

Implications for minimum discrimination information, compositional data analysis, Lindsay geometry, bootstrap with auxiliary information, and Lagrange multiplier test are discussed.

Keywords and phrases: closed multinomial distribution, maximum likelihood, convex set, estimating equations, zero counts, Fenchel dual, El Barmi Dykstra dual, Smith dual, perturbed primal, PP algorithm, epi-convergence, empirical likelihood, Fisher likelihood

AMS 2010 subject classifications: Primary , ; secondary

1 Introduction

Zero counts are a source of difficulties in the maximization of the multinomial likelihood for log-linear models. A considerable literature has been devoted to this issue, culminating in the recent papers by Fienberg and Rinaldo [12] and Geyer [14]. In these studies, convex analysis considerations play a key role.

Less well recognized is that the zero counts also cause difficulties in the maximization of the multinomial likelihood under linear constraints, or, in general, when the cell probabilities are restricted to a convex closed subset of the probability simplex; see Section 2 for a formal statement of the considered primal optimization problem . Though in this case the nature of the difficulties is different than in the log-linear case, the convex analysis considerations are important here as well, because they permit developing a correct solution of – one of the main objectives of the present work.

The problem of finding the maximum multinomial likelihood under linear constraints dates back to, at least, Smith [41], and continues through the work of Aitchison and Silvey [4], Gokhale [16], Klotz [26], Haber [19], Stirling [42], Pelz and Good [33], Little and Wu [30], El Barmi and Dykstra [10, 11], to the recent studies by Agresti and Coull [2], Lang [27], and Bergsma et al. [8], among others. Linear constraints on the cell probabilities appear naturally in marginal homogeneity models, isotonic cone models, mean response models, multinomial-Poisson homogeneous models, and many others; cf. Agresti [1], Bergsma et al. [8]. They also arise in the context of estimating equations.

Contrary to widely-held belief, a solution of may assign a positive weight to an outcome with zero count; cf. Theorem 2, Examples 3 and 4, as well as the examples in Section 5. This fact also affects the Lagrange and Fenchel dual problems to .

The restricted maximum of the multinomial likelihood defined through the primal problem is not amenable to asymptotic analysis, and the primal form is not ideal for numerical optimization. Thus, it is common to consider the Lagrange dual problem instead of the primal problem. This permits the asymptotic analysis (cf. Aitchison and Silvey [4]), and reduces the dimension of the optimization problem, because the number of linear constraints is usually much smaller than the cardinality of the sample space. Smith [41, Sects. 6, 7] has developed a solution of the Lagrange dual problem, under the hidden assumption that every outcome from the sample space appears in the sample at least once; that is, , where is the vector of the observed relative frequency of outcomes. The same solution was later considered by several authors; see, in particular, Haber [19, p. 3], Little and Wu [30, p. 88], Lang [27, Sect. 7.1], Bergsma et al. [8, p. 65]. It remained unnoticed that, if the assumption is not satisfied, then the solution of Smith’s Lagrange dual problem does not necessarily lead to a solution of the primal problem .

El Barmi and Dykstra [10] studied the maximization of the multinomial likelihood under more general, convex set constraints, where it is natural to replace the Lagrange duality with the Fenchel duality. When the feasible set is defined by the linear constraints, El Barmi and Dykstra’s (BD) dual reduces to Smith’s Lagrange dual. The BD-dual leads to a solution of the primal if . The authors overlooked that this is not necessarily the case if a zero count occurs.

Taken together, the decisions obtained from El Barmi and Dykstra’s simplified Fenchel dual can be severely compromised. It is thus important to know the correct Fenchel dual to . This is provided by Theorem 6, which also characterizes the solution set of . It is equally important to know the conditions under which the BD-dual leads to a solution of . The answer is provided by Theorem 16. An analysis of directions of recession is crucial for establishing the theorem.

Since obtaining a solution of the Fenchel dual is numerically demanding, a simple algorithm for solving the primal is proposed. The PP algorithm forms a sequence of perturbed primal problems. Theorem 21 demonstrates that the PP algorithm epi-converges to a solution of . Even stronger, pointwise convergence can be established for a linear constraint set; see Theorem 22. The convergence theorems imply that the common practice of replacing the zero counts by a small, arbitrary value can be supplanted by a sequence of perturbed primal problems, where the perturbed relative frequency vectors are such that . Because each is strictly positive, the PP algorithm can be implemented through the BD-dual to the perturbed primal, by the Fisher scoring algorithm, Gokhale’s algorithm [16], or similar methods.

The findings have implications for the empirical likelihood. Recall that ‘in most settings, empirical likelihood is a multinomial likelihood on the sample’; cf. Owen [32, p. 15]. As the empirical likelihood inner problem (cf. Section 9) is a convex optimization problem, it has its Fenchel dual formulation. If the feasible set is linear, then the Fenchel dual to is equivalent to El Barmi and Dykstra’s dual to . Thanks to this connection, Theorem 16 provides conditions under which the solution set of the multinomial likelihood primal problem and the solution set of the empirical likelihood inner problem are the same, and the maximum of the multinomial likelihood is equal to the maximum of the empirical likelihood. Consequently:

-

•

If is an H-set or a Z-set with respect to the type (for the definition, see Section 6), the maximum empirical likelihood does not exist, though the maximum multinomial likelihood exists. The notion of H-set corresponds to the convex hull problem (cf. Owen [31, Sect. 10.4]) and the notion of Z-set corresponds to the zero likelihood problem (cf. Bergsma et al. [7]). By Theorem 16, these are the only ways the empirical likelihood inner problem may fail to have a solution; cf. Section 9.

-

•

If any of conditions (i)–(iv) in Theorem 16(b) are not satisfied, then , and the empirical likelihood may lead to different inferential and evidential conclusions than those suggested by the multinomial likelihood.

Fisher’s [13] original concept of the likelihood carries the discordances between the multinomial and empirical likelihoods also into the continuous iid setting; cf. Section 9.1.

The findings also affect other methods, such as the minimum discrimination information, compositional data analysis, Lindsay geometry of multinomial mixtures, bootstrap with auxiliary information, and Lagrange multiplier test, which explicitly or implicitly ignore information about the support and are restricted to the observed outcomes.

1.1 Organization of the paper

The multinomial likelihood primal problem and its characterization (cf. Theorem 2) are presented in Section 2. The Fenchel dual problem to is introduced in Section 3. A Lagrange dual formulation of the convex conjugate (cf. Theorem 5) serves as a ground for Theorem 6, one of the main results, which provides a relation between the solutions of and . If the feasible set is polyhedral, a solution of can be obtained also from a different Lagrange dual to ; cf. Section 3.1. A special case of the single inequality constraint is discussed in detail in Section 3.2, where a flaw in Klotz’s [26] Theorem 1 is noted. In Section 4, El Barmi and Dykstra’s [10] dual is recalled; Section 4.1 introduces its special case, the Smith dual problem. Theorem 2.1 of El Barmi and Dykstra [10], and its flaws are presented in Section 5, where they are also illustrated by simple examples. Section 6 studies the scope of validity of the BD-dual ; cf. Theorem 16. Sequential, active-passive dualization is proposed and analyzed in Section 7. Perturbed primal problem is introduced in Section 8, where the epi-convergence of a sequence of the perturbed primals for a general, convex , and the pointwise convergence for the linear are formulated (cf. Theorems 21, 22) and illustrated. Implications of the results for the empirical likelihood method are discussed in Section 9. A brief discussion of implications of the findings for the minimum discrimination information, compositional data analysis, Lindsay geometry of multinomial mixtures, bootstrap with auxiliary information and Lagrange multiplier test is contained in Section 10. Finally, Section 11 comprises detailed proofs of the results.

An R code and data to reproduce the numerical examples can be found in [18].

2 Multinomial likelihood primal problem

Let denote a finite alphabet (sample space) consisting of letters (outcomes) and denote the probability simplex

identify with . Suppose that is a realization of the closed multinomial distribution with parameters and . Then the multinomial likelihood kernel , where , Kerridge’s inaccuracy [25], is

| (2.1) |

and is the type (the vector of the relative frequency of outcomes). The conventions , apply; denotes the extended real line and is the scalar product of , . Functions and relations on vectors are taken component-wise; for example, . For , is a shorthand for .

Consider the problem of minimization of , restricted to a convex closed set :

| () |

The goal is to find the solution set as well as the infimum of the objective function over . The problem will be called the multinomial likelihood primal problem, or primal, for short.

Special attention is paid to the class of polyhedral feasible sets

| (2.2) |

or to its subclass of sets given by (a finite number of) linear equality constraints

| (2.3) |

where are vectors from . These feasible sets are particularly interesting from the applied point of view and permit to establish stronger results.

Without loss of generality it is assumed that is the support of , that is, for every there is with ; in other words, the structural zeros (cf. Baker et al. [6, p. 34]) are excluded. Due to the convexity of this is equivalent to the existence of with . Under this assumption, Theorem 2 gives a basic characterization of the solution set of . Before stating it, some useful notions are introduced.

Definition 1.

For a type (or, more generally, for any ), the active and passive alphabets are

The elements of are called active, passive letters, respectively.

Put , . Let , be the natural projections; identify with and with . Note that if then and . For , and are the shorthands for and , respectively. (If no ambiguity can occur, the elements of will be denoted also by .) Identify with , so that it is possible to write for every . Finally, for a subset of and let

be the active projection and the -slice of ; analogously define and .

Theorem 2 (Primal problem).

Let be from . Let be a convex closed subset of with support . Then is finite, is compact and there is , , such that

Moreover,

-

(a)

If then and is a singleton.

-

(b)

If then , and is a singleton if and only if the -slice of is a singleton.

Thus the primal has always a solution . Its active coordinates are unique and the passive coordinates are arbitrary such that . It is worth stressing that need not be equal to , that is, a solution of may put positive mass to passive letter(s). The following couple of simple examples illustrates the points; see also the examples in Section 5. Hereafter denotes a random variable supported on .

Example 3.

Take and . Let , so that and . Then , the minimum of over is , and . Here, is (trivially) unique and .

Example 4.

Motivated by Wets [43, p. 88], let , and . Then , . Since , the positive weight is assigned to the passive, unobserved letter .

The Fisher scoring algorithm which is commonly used to solve when is a linear set may fail to converge when the zero counts are present; cf. Stirling [42]. Other numerical methods, such as the augmented Lagrange multiplier methods, which are used to solve the convex optimization problem under polyhedral and/or linear may have difficulties to cope with large . Thus, it is desirable to approach also from another direction.

3 Fenchel dual problem to

Consider the Fenchel dual problem to the primal :

| () |

where

is the polar cone of and

is the convex conjugate of (in fact, the convex conjugate of given by for and otherwise).

The Fenchel dual is often more tractable than the primal , in particular when is given by linear equality and/or inequality constraints. This is the case of the models for contingency tables, mentioned in Introduction. Also an estimating equations model leads to a linear feasible set , when is fixed. The model is , where

| (3.1) |

and , , are the estimating functions. There and need not be equal to . Since is usually much smaller than , may be easier to solve numerically than .

Observe that the convex conjugate itself is defined through an optimization problem, the convex conjugate primal problem (cc-primal, for short), whose solution set is

| (3.2) |

The structure of is described by Proposition 40. The conjugate can be evaluated by means of the Lagrange duality, where the Lagrange function is

It holds that (cf. Lemma 38)

For every and , , , define

Theorem 5 (Convex conjugate by Lagrange duality).

Let and . Then

where

| (3.3) |

and is the unique solution of

| (3.4) |

The key point is that the , which solves (3.4), is not always the which minimizes . They are the same if and only if . As it will be seen in Theorem 6, if then this inequality decides whether the solution of primal is supported only on the active letters, or some probability mass is placed also to the passive letter(s).

Theorem 5 serves as a foundation for Theorem 6, which states the relation between the Fenchel dual and the primal.

Theorem 6 (Relation between and ).

Let be as in Theorem 2. Then

is a nonempty convex compact set and for every . Moreover, if we put

| (3.5) |

then and the following hold:

-

(a)

If then and

-

(b)

If then and

Thus, in the active coordinates, the solution of is unique and is related to by (3.5). Together with Theorem 2 this yields

In the case (a), , and the passive projections of the solutions satisfy . Then it suffices to solve the primal solely in the active letters and is a singleton. This happens for instance if .

In the case (b), , and satisfy . Then every solution of the primal assigns the positive probability to at least one passive letter.

To sum up, the Fenchel dual problem, once solved, permits to find through (3.5) and this way it incorporates into . In the case of linear or polyhedral the dual may reduce dimensionality of the optimization problem, yet the numerical solution of is somewhat hampered by the need to obey (3.3). Moreover, remains to be found; in this respect see Proposition 51.

3.1 Polyhedral and linear

In the polyhedral case (2.2)

a solution of the Fenchel dual can also be obtained from the saddle points of the following Lagrange function

Indeed, it holds that

Hence is a saddle point of if and only if and ; cf. Bertsekas [9, Prop. 2.6.1].

The vectors from of the form will be called the base solutions of . From the Farkas lemma (cf. Bertsekas [9, Prop. 3.2.1]) and the monotonicity of (Lemma 41) it follows that, for a polyhedral , there always exists a base solution, and every solution of is a sum of a base solution and a vector from ; that is,

There may exist many base solutions. However, if are linearly independent then the base solution is unique, since then the system of equations has a unique solution .

Analogous claim holds for a linear (cf. (2.3)), just in this case , by the Farkas lemma.

3.2 Single inequality constraint and Klotz’s Theorem 1

To illustrate the base solution in connection with Theorem 6, consider

given by a single inequality constraint. By the Farkas lemma, . If the case (a) of Theorem 6 applies (for if not, there is a base solution and, by Theorem 6(b), should be ; this is not possible since ).

Assume that and the case (b) of Theorem 6 applies. Take any base solution . Then, by Theorem 6(b), ; so

| (3.6) |

Further, by Theorem 2, is arbitrary from . If attains the minimum at a single letter, then the solution of the primal is always unique.

To sum up, the case (b) of Theorem 6 happens if and only if

| (3.7) |

The primal problem with this was considered by Klotz [26]. Theorem 1 of [26] asserts that the solution of takes the form

if and ; see Klotz’s condition (3.1b). There, is the unique root of

Thus, under Klotz’s condition (3.1b), the solution of should assign zero weight to any passive letter. This is not the case, as the following example demonstrates.

In a similar way it is possible to analyze a single equality constraint. For more than one equality/inequality constraint the condition guaranteeing that cannot be given in such a simple form as (3.7).

4 El Barmi-Dykstra dual problem to

El Barmi and Dykstra [10] consider a simplified Fenchel dual problem (the BD-dual, for short)

| () |

where

will be called the BD conjugate of . Note that the BD-dual is easier to solve than , as in the former is fixed to .

If is polyhedral then, in analogy with the concept of the base solution of , the vectors from of the form are called the base solutions of . As above, every solution of can in this case be written as a sum of a base solution and a vector from .

4.1 Smith dual problem

By the Farkas lemma, for the feasible set given by linear equality constraints, the polar cone is . Then the BD-dual becomes

| (4.1) |

which is (equivalent to) the simplified Lagrange dual problem (the Smith dual, for short) considered by Smith [41, Sect. 6] and many other authors; see, in particular, Haber [19, p. 3], Little and Wu [30, p. 88], Lang [27, Sect. 7.1], and Bergsma et al. [8, p. 65]. It is worth noting that (4.2) is an unconstrained optimization problem.

5 Flaws of BD-dual

In [10, Thm. 2.1] El Barmi and Dykstra state the following relationship between and .

Theorem 8 (Theorem 2.1 of [10]).

Let be a convex closed subset of .

-

(): If is finite, then is nonempty and . Moreover, for every , belongs to .

-

(): If is finite, then . Moreover, if , then belongs to . (There, convention applies).

Though is always finite, may be infinite, leaving the solution set inaccessible through () of [10, Thm. 2.1]. Moreover, the claims () and () of the theorem are not always true. In fact, there are three possibilities:

-

1.

;

-

2.

is finite, but there is a BD-duality gap, that is, ;

-

3.

(no BD-duality gap).

To illustrate them, we give below six simple examples: one where the BD-duality works and the other five where it fails. In Examples 9, LABEL:E:E, LABEL:E:Z, LABEL:E:gap the set is linear, whereas Example 11 presents a nonlinear , and in Example 12 the set is defined by linear inequalities.

Example 9 (No BD-duality gap).

Example 10 (name=H-set, label=E:E).

Example 11 (nonlinear , H-set).

Let , , and . Thus , , and .

- •

- •

Example 12 (monotonicity, H-set).

Example 13 (name=Z-set, label=E:Z).

Observe that Theorem 2.1 of [10] implies that , provided that is finite. However, may be different than ; in such a case has a strictly positive coordinate and the BD-duality gap occurs.

Example 14 (name=BD-duality gap, label=E:gap).

Let , , so that , and . Thus , , and .

- •

-

•

: Since , the base solution of is and . From (3.5), it follows that .

- •

- •

6 Scope of validity of BD-dual

The correct relation of the BD-dual to the primal is stated in Theorem 16. In order to formulate the conditions under which is infinite (cf. Theorem 16(a)) the notions of H-set and Z-set are introduced. They are implied by the recession cone considerations of .

Definition 15.

If a nonempty convex closed set and a type are such that , then we say that is an H-set with respect to . The set is called a Z-set with respect to if is nonempty but its support is strictly smaller than .

Note that comprises those which are supported on the active letters. Thus, is neither an H-set nor a Z-set if and only if there is with , .

Clearly, in Example LABEL:E:E, is an H-set with respect to the . The same set becomes a Z-set with respect to the considered in Example LABEL:E:Z. And it is neither an H-set nor a Z-set with respect to the studied in Example 9. Further, the feasible set considered in Example LABEL:E:gap is neither an H-set nor a Z-set with respect to the particular . In Examples 11 and 12, is an H-set with respect to the .

Theorem 16 (Relation between and ).

Let be as in Theorems 2 and 6.

-

(a)

If is either an H-set or a Z-set with respect to then

-

(b)

If is neither an H-set nor a Z-set then is finite, , and there is such that and

Moreover, there is no BD-duality gap, that is,

if and only if any of the following (equivalent) conditions hold:

-

(i)

(that is, );

-

(ii)

(that is, );

-

(iii)

(extremality relation) for some , where

-

(iv)

.

-

(i)

Informally put, Theorem 16(a) demonstrates that the BD-dual breaks down if is either an H-set or a Z-set with respect to the observed type . Then the ( ) part of Theorem 8 does not apply. At the same time the ( ) part of Theorem 8 does not hold, as , yet . This is illustrated by Examples LABEL:E:E–LABEL:E:Z.

Part (b) of Theorem 16 captures the other discomforting fact about the BD-dual: if the solution of exists, it may not solve the primal problem . By (i) this happens whenever the solution of assigns a positive weight to at least one of the passive letters (provided that ). See Example LABEL:E:gap.

At least, for the BD-dual works well.

Corollary 17.

If then are singletons,

The corollary justifies the use of the BD-dual for solving when . Recall that in the case of linear the BD-dual is just Smith’s simplified Lagrange dual problem (4.1), which is an unconstrained optimization problem. It can be solved numerically by standard methods for unconstrained optimization or by El Barmi & Dykstra’s [10] cyclic ascent algorithm.

Finally, it is worth noting that the solution sets and are always compact but , if nonempty, is compact if and only if , that is, there is no passive letter. If and , then is unbounded from below.

6.1 Base solution of and no BD-duality gap

The case (iv) of Theorem 16(b) provides a way to find out whether a solution of assigns the zero weights to the passive letters or not. First, determine whether is neither an H-set nor a Z-set with respect to . Then, solve the BD-dual and find a solution of it. Finally, verify that belongs to the polar cone . For example, if then this is satisfied automatically.

On the other hand, in order to have (that is, to have no BD-duality gap), must be satisfied by some . In the case when is polyhedral, there must exist a base solution of with . The next example illustrates the point.

Example 18 (Base solution of ).

Let , where . Let , so that . Let ; hence , , and . For what values of the solution of assigns zero weights to the passive letters? First, solves , where . This gives . Thus, when . Then, in order to have , the condition gives that . In the other case () the condition is not binding, hence for . Taken together, for it holds that , since has a positive coordinate and . To give a numeric illustration, let , , and . Then , that is, a positive weight is assigned to a passive letter. For , which is above the threshold, .

To sum up, El Barmi and Dykstra’s dual may fail to lead to the solution of the multinomial likelihood primal in different ways. For a particular type the feasible set may be an H-set or a Z-set, and then the BD-dual fails to attain finite infimum. Even if this is not the case may fail to provide a solution of , due to the BD-duality gap. Theorem 16(b) states equivalent conditions under which the BD-dual is in the extremality relation with and leads to a solution of ; see also Lemma 62.

7 Active-passive dualization

The active-passive dualization is based on a reformulation of the primal as a sequence of partial minimizations

Assume that is such that the slice has support (this is not a restriction, since otherwise the inner infimum is ). Since , Corollary 17 gives that a solution of the inner (active) primal problem

| () |

can be obtained from its BD-dual problem

| () |

where .

Theorem 19 (Relation between and ).

Let be such that the support of is . Then there is a unique solution of , and

| (7.1) |

is the unique member of . Moreover, and .

Thanks to (7.1) and the extremality relation between and , the active-passive (AP) dual form of the active-passive primal is

The active-passive dualization is illustrated by the following example.

Example 20 (continues=E:Z).

Here and the AP dual can be written in the form

where . The inner optimization gives

This , plugged into , yields

which has to be maximized over . The maximum is attained at . Thus , , , and ; since by (7.1), and . Hence, .

In the outer, passive optimization, it is possible to exploit the structure of (cf. Theorem 2), and this way reduce the dimension of the problem. This is the case, for instance, when is polyhedral.

8 Perturbed primal and PP algorithm

For let be a perturbation of the type ; we assume that

| (8.1) |

The perturbation activates passive, unobserved letters. For every consider the perturbed primal problem

| () |

where .

Since the activated type has no passive coordinate, the perturbed primal problem can be solved, for instance, via the BD-dualization; recall Corollary 17. Thus, for every ,

| (8.2) |

How is related to , and to ? Theorem 21 asserts that epi-converges to when . (There, for a map and a set , the map is given by if , and if .) The epi-convergence (cf. Rockafellar and Wets [39, Chap. 7]) is used in convex analysis to study a limiting behavior of perturbed optimization problems. It is an important modification of the uniform convergence (cf. Kall [24], Wets [43]).

Theorem 21 (Epi-convergence of to ).

Assume that is a convex closed subset of with support , , and is such that (8.1) is true. Then

Consequently,

and the active coordinates of solutions of converge to the unique point of :

Moreover, if is a singleton (particularly, if ) then also the passive coordinates converge and

Thus, if is small enough, the (unique) solution of the perturbed primal is close to a solution of the primal problem . Theorem 21 also states that in the active coordinates the convergence is pointwise, to the unique of . The next theorem demonstrates that if is given by linear constraints and is defined in a ‘uniform’ way in , also the passive coordinates of converge pointwise.

Notice that the condition (8.3) is satisfied if for every ; for example if

| (8.4) |

where is the vector with if and if . This corresponds to the case when every passive coordinate is ‘activated’ by equal weight.

The following example demonstrates that without the assumption (8.3) the convergence in passive letters need not occur.

Example 23 (Divergent ).

Consider the setting of Example 3. That is, and

where . For , . Define the perturbed types in such a way that

and is on . Then, for every ,

so the limit does not exist. Note that in this case the condition (8.3) is violated. Indeed, and for every ; hence, by the mean value theorem, for every there is such that . Since , .

In Examples LABEL:E:E, LABEL:E:Z, LABEL:E:gap, with given by (8.4), the pointwise convergence can be demonstrated analytically.

Example 24 (continues=E:E).

Here , where . So, and .

Example 25 (continues=E:Z).

First, and

this leads to . Thus, and, since , .

Example 26 (continues=E:gap).

Here with . Thus, , and .

The next example provides a numeric illustration of the pointwise convergence of a sequence of perturbed primals to . The perturbed primal solutions are obtained through their BD-duals. It is worth stressing that to is, for a linear , an unconstrained optimization problem; cf. Section 4.1.

Example 27 (Qin and Lawless [35], Ex. 1).

Consider a discrete-case analogue of Example 1 from Qin and Lawless [35]. Let and

where . Then is the estimating equations model; cf. (3.1). Clearly, and . Let .

For a fixed and a perturbed type , the BD-dual to the perturbed primal is (equivalent to)

and the corresponding . For and given by (8.4) with (, Table 1 illustrates the pointwise convergence of to , to .

The optimal ’s were computed by optim of R [36]. The rightmost three columns in Table 1 state orders of the precision of satisfaction of the constraints , , and . The solution of , obtained by solnp from the R library Rsolnp (cf. Ghalanos and Theussl [15]; based on Ye [44]), is and .

3 0.161439 0.001013 0.528326 0.294553 0.014669 0.823788 7 7 8 5 0.162488 0.000010 0.525041 0.299936 0.012525 0.812404 7 7 6 7 0.162501 1e-7 0.525000 0.299999 0.012500 0.812242 6 6 6 9 0.162501 1e-8 0.525000 0.300000 0.012502 0.812242 5 5 6

For the numerical effects become noticeable. For instance, for , the precision of the constraints satisfaction is of the order .

As an aside, note that for this type the BD-dual to the original, unperturbed primal breaks down, since is an H-set. In fact, it is an H-set with respect to this for any ; cf. the empty set problem in Grendár and Judge [17].

The convergence theorems suggest that the practice of replacing the zero counts by an ‘ad hoc’ value can be superseded by the PP algorithm; i.e., by a sequence of the perturbed primal problems, for such that . Since each , the PP algorithm can be implemented through the BD-dual to , by the Fisher scoring algorithm, or by the Gokhale algorithm [16], among other methods.

9 Implications for empirical likelihood

Let us point out some of the consequences of the presented results for the empirical likelihood (EL) method; cf. Owen [31]. In most settings, including the discrete one, empirical likelihood is ‘a multinomial likelihood on the sample’, Owen [32, p. 15]. It is usually applied to an empirical estimating equations model, which is in the discrete setting defined as , where

and are the empirical estimating functions. The empirical likelihood estimator is defined through

| (9.1) |

For a fixed the data-supported feasible set is a convex set and the inner optimization in (9.1) is the empirical likelihood inner problem

| () |

Since is just the -slice of (given by (3.1)), the EL inner problem can equivalently be expressed as

Its dual is

| (9.2) |

Note that (9.2) is just Smith’s simplified Lagrangean (4.1), that is, the BD-dual to the multinomial likelihood primal problem , for the linear set . This connection implies, through Theorem 16, that the maximum of empirical likelihood does not exist if is either an H-set or a Z-set with respect to . The two possibilities are recognized in the literature on EL, where an H-set is referred to as the convex hull condition (cf. Owen [32, Sect. 10.4]), and a Z-set is known as the zero likelihood problem (cf. Bergsma et al. [7]). Theorem 16 also implies that these are the only ways the EL inner problem may fail to have a solution. Note that the inner empirical likelihood problem may fail to have a solution for any ; cf. the empty set problem, Grendár and Judge [17].

In addition, Theorem 16 implies that, besides failing to exist, the empirical likelihood inner problem may have different solution than the multinomial likelihood primal problem. If is neither an H-set nor a Z-set then, by Theorem 16(b), it is possible that

-

1.

either (no BD-duality gap), or

-

2.

(BD-duality gap).

Since , in the latter case and . This happens when any of the conditions (i)–(iv) from Theorem 16(b) is not satisfied. Then the distribution that maximizes empirical likelihood differs from the distribution that maximizes multinomial likelihood. Moreover, the multinomial likelihood ratio may lead to different inferential and evidential conclusions than the empirical likelihood ratio. The next example illustrates the points.

Example 28 (LR vs. ELR).

Let , with and . Let . Clearly, for . Let .

-

•

, for ,

-

•

, for .

As the two solutions are very close, the multinomial likelihood ratio is

-

•

,

which indicates inconclusive evidence.

However, the empirical likelihood ratio leads to a very different conclusion. Note that the active letters are , and is neither an H-set nor a Z-set with respect to the observed type , for the considered (). Hence for both ’s the solution of exists and it is

-

•

, for ,

-

•

, for .

The weights given by EL to are very different in the two models; the same holds for . The empirical likelihood ratio is

-

•

,

which indicates decisive support for ; cf. Zhang [46].

The BD-duality gap thus implies that in the discrete iid setting, when is linear, EL-based inferences from finite samples may be grossly misleading.

9.1 Continuous case and Fisher likelihood

As far as the continuous random variables are concerned, due to the finite precision of any measurement ‘all actual sample spaces are discrete, and all observable random variables have discrete distributions’, Pitman [34, p. 1]. Already Fisher’s original notion of the likelihood [13] (see also Lindsey [29, p. 75]) reflects the finiteness of the sample space. For an iid sample and a finite partition of a sample space , the Fisher likelihood which the data provide to a pmf is

where is the number of observations in that belong to . Thus, this view carries the discordances between the multinomial and empirical likelihoods also to the continuous iid setting.

Example 29 (FL with estimating equations).

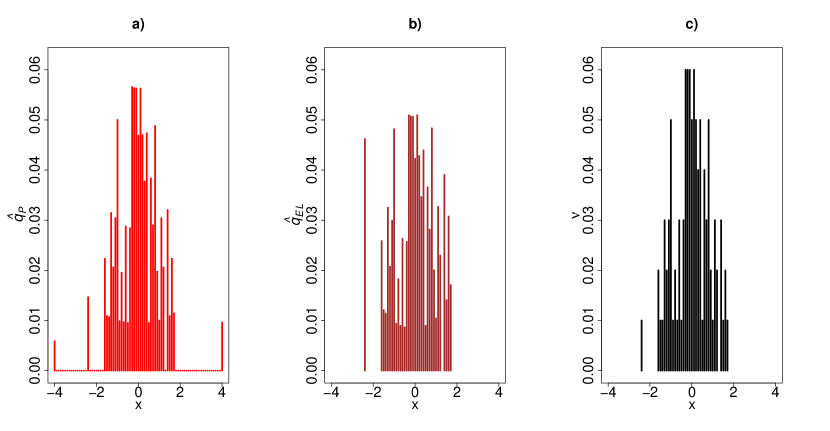

To give an illustration of the Fisher likelihood as well as yet another example that may be different than , consider the setting of Example 27 with and . The letters of the alphabet are taken to be the representative points of the partition , , , , of . This way the alphabet captures the finite precision of measurements of a continuous random variable. The type exhibited at the panel c) of Figure 1 is induced by a random sample of size from the -quantized standard normal distribution. The EL estimate of is and the associated EL-maximizing distribution is different than the multinomial likelihood maximizing distribution , which is associated with the estimated value and assigns a positive weight also to the passive letters and .

10 Implications for other methods

Besides the empirical likelihood, the minimum discrimination information, compositional data analysis, Lindsay geometry, bootstrap in the presence of auxiliary information, and Lagrange multiplier test ignore information about the alphabet, and are restricted to the observed data. Thus, they are affected by the above findings.

1) In the analysis of contingency tables with given marginals, the minimum discrimination information (MDI) method (cf. Ireland and Kullback [23]) is more popular than the maximum multinomial likelihood method. This is because the former is more computationally tractable, thanks to the generalized iterative scaling algorithm (cf. Ireland et al. [22]). MDI minimizes over , so that a solution of the MDI problem must assign a zero mass to a passive, unobserved letter. Thus, MDI is effectively an empirical method. This implies that the MDI-minimizing distribution restricted to a convex closed set may not exist; however, the multinomial likelihood-maximizing distribution always exists (cf. Theorem 2), and may assign a positive mass to an unobserved outcome(s).

Example 30 (Contingency table with given marginals).

Consider a contingency table with given marginals. Let , and let the observed bi-variate type have all the mass concentrated to ; the remaining eight possibilities have got zero counts. Let the column and raw marginals be , , respectively. One of the multinomial likelihood maximizing distributions is displayed in Table 2. In the active letter is unique, in the passive letters . The table exhibits the which can also be obtained by the PP algorithm with the uniform activation (8.4). Note that , so that the MDI-minimizing distribution does not exist.

0.100 0.000 0.000 0.094 0.080 0.026 0.306 0.320 0.074

It is worth stressing that the PP algorithm makes the multinomial likelihood primal problem computationally feasible.

2) Multinomial likelihood maximization has the same solution regardless of whether the proportions or the counts are used. Note that the vector of normalized frequencies is an instance of the compositional data. In the analysis of compositional data, it is assumed that the compositional data belong to ; cf. Aitchison [3, Sect. 2.2]. This assumption transforms into . Consequently, the multinomial likelihood problem is replaced by the empirical likelihood problem . However, this replacement is not without consequences, as the solution of the empirical likelihood problem (if it exists) may differ from the solution of ; cf. Section 9.

3) Lindsay [28, Sect. 7.2] discusses multinomial mixtures under linear constraints on the mixture components, and assumes that it is sufficient to consider the distributions supported in the data (i.e., in the active alphabet). Though the objective function in is a ‘single-component’ multinomial likelihood, the present results for the H-set, Z-set, and BD-gap suggest that it would be more appropriate to work with the complete alphabet; see also Anaya-Izquierdo et al. [5, Sect. 5.1].

11 Proofs

11.1 Notation and preliminaries

In this section we introduce notation and recall notions and results which will be used later; it is based mainly on Bertsekas [9] and Rockafellar [38, 37]. We will not repeat the definitions introduced in the previous part of the paper.

We assume that the extended real line is equipped with the order topology; so it is a compact metrizable space homeomorphic to the unit interval. The arithmetic operations on are defined in a usual way; further we put . For we define ; then is continuous.

For put and (recall that, for , ). In the matrix operations, the members of are considered to be column matrices. If no confusion can arise, a vector with constant values is denoted by a scalar.

Let be a nonempty subset of . The convex hull of is denoted by . The polar cone of is the set . This is a nonempty closed convex cone [9, p. 166]. Assume that is convex. The relative interior of is the interior of relative to the affine hull of [9, p. 40]; it is nonempty and convex [9, Prop. 1.4.1].

The recession cone of a convex set is the convex cone

| (11.1) |

[9, p. 50]. Every is called a direction of recession of . Clearly, ; if it is said to be trivial. The lineality space of is defined by [9, p. 54]; it is a linear subspace of . Note that if is a cone then and .

Let be a subset of and be a function. By we denote the directional derivative of at in the direction [9, p. 17]. By and we denote the gradient and the Hessian of at . For a nonempty set , and denote the sets of all minimizing and maximizing points of over , respectively; that is,

The (effective) domain and the epigraph of are the sets [9, p. 25]

A function is

-

•

proper if and there is with [9, p. 25] (this should not be confused with the properness associated with compactness of point preimages);

-

•

closed if is closed in [9, p. 28];

-

•

lower semicontinuous (lsc) if for every and every sequence in converging to [9, p. 27]; analogously for the upper semicontinuity (usc);

-

•

convex if both and are convex [9, Def. 1.2.4];

-

•

concave if is convex.

When dealing with closedness of , we will often use the following simple lemma [9, Prop. 1.2.2 and p. 28].

Lemma 31.

Let be a map defined on a set . Define

Then the following are equivalent:

-

(a)

is closed;

-

(b)

is closed;

-

(c)

is lower semicontinuous;

-

(d)

the level sets are closed for every .

The recession cone of a proper convex closed function is the recession cone of any of its nonempty level sets [9, p. 93]. The lineality space of is, due to the convexity of , the set of directions in which is constant (that is, for every and ); thus is also called the constancy space of [9, p. 97]. If is concave, the corresponding notions for are defined via the convex function .

The fundamental results underlying the importance of recession cones, are the following theorems ([9, Props. 2.3.2 and 2.3.4] or [38, Thm. 27.3]).

Theorem 32.

Let be a nonempty convex closed subset of and be a proper convex closed function such that . Then the following are equivalent:

-

(a)

the set of minimizing points of over is nonempty and compact;

-

(b)

and have no common nonzero direction of recession, that is,

Both conditions are satisfied, in particular, if is bounded.

Theorem 33.

Let be a nonempty convex closed subset of and be a convex closed function such that . If

| (11.2) |

or if

then the set of minimizing points of over is nonempty. Under condition (11.2), can be written as , where is compact.

Standing Assumption.

If not stated otherwise, in the sequel it is assumed that a nonempty convex closed subset of having support , and a type are given.

Since no confusion can arise, by we denote also an extension of the original function (defined in (2.1)) to :

| (11.3) |

the conventions and for every apply.

11.2 Proof of Theorem 2 (Primal problem)

In the next lemma we prove that is a proper convex closed function. Since is compact, has no nonzero direction of recession. From this and Theorem 32, Theorem 2 will follow.

Lemma 34.

If and is given by (11.3), then

-

(a)

for every , and if and only if ; so

-

(b)

is a proper continuous (hence closed) convex function;

-

(c)

the restriction of to its domain is strictly convex if and only if ;

-

(d)

is differentiable on with the gradient given by

the one-sided directional derivative of at in the direction is

-

(e)

the recession cone and the constancy space of are

Proof.

The properties (a) and (d) are trivial and the property (b) follows from the continuity and concavity of the logarithm (extended to the whole real line); closedness of follows from continuity by Lemma 31. For the property (c), use that the Hessian is a diagonal matrix . Hence it is positive definite and is strictly convex if and only if [9, Prop. 1.2.6].

It remains to prove (e). Fix any such that the level set is nonempty. If is such that then there is an active letter with . In such a case, for any there is with and so . Hence, by (11.1), .

Now take any with . Then, for every and , by the monotonicity of the logarithm. That is, and so . The property (e) is proved. ∎

Proposition 35.

Proof.

Since is compact, its recession cone is trivial. Thus the first assertion follows from Theorem 32. The fact that is a singleton provided , follows from the strict convexness of . ∎

Proposition 36.

Let and be a convex closed set having support . Then the -projection of onto active letters is always a singleton and

Consequently, is a singleton if and only if is a singleton.

Proof.

Note that is a nonempty convex closed subset of . Define by for and otherwise. Since

| (11.4) |

it holds that

The map is proper, convex and closed (use Lemma 31 and the fact that the restriction of to the closed set is continuous, hence closed). Since is bounded, Theorem 32 gives that is a nonempty compact set. This set is a subset of and the restriction of to is strictly convex (Lemma 34(c)), so is a singleton. Hence there is a unique point such that . Now, (11.4) gives that if and only if ; so . ∎

11.3 Proof of Theorem 5 (Convex conjugate by Lagrange duality)

In this section we prove Theorem 5 on the convex conjugate , defined by the convex conjugate primal problem (cc-primal, for short)

The proof is based on the following reformulation of the cc-primal

where

is the Lagrangian function; cf. Lemma 38. Then we will show that the map is minimized at ; cf. Section 11.3.2. Structure of the solution set of the cc-primal is described in Section 11.3.3. Additional properties of the convex conjugate, which will be utilized in the proof of Theorem 6, are stated in Section 11.3.4.

For every and put

| (11.5) |

and recall that , where solves . Since

| (11.6) |

is well-defined. We start with a simple lemma.

Lemma 37.

For every and ,

Proof.

The first two equalities follow from the facts that and that . The final one is a trivial consequence of the definition of ; indeed, since for every , . ∎

11.3.1 Lagrange duality for the convex conjugate

Assume that and are given. For put

and define extended-real-valued functions

Lemma 38 (Lagrange duality for the convex conjugate).

For every and ,

Proof.

We follow [37, Sect. 4]. Denote by the subset of . Define and by

Note that, in the definition of , can be replaced by ; indeed, if then for some and hence . The set is closed convex (in fact, polyhedral) and the map , is convex and continuous, hence closed. Since the epigraphs of and coincide,

| (11.7) |

The corresponding optimal value function is defined by (cf. [37, (4.7)])

We are going to show that

| (11.8) |

To this end, take any and with . Assume that . Then

For any ,

Since is continuous at and , there is such that for every . Thus whenever and . This gives

Since if (indeed, for such , for every ), (11.8) is proved.

The Lagrangian function associated with is defined by (cf. [37, (4.2)])

A simple computation yields (cf. [37, (4.4)] with , , and , all restricted to )

(Indeed, fix any and . If then for every , hence . If and , then whenever both are sufficiently large; for such , is not bounded from below (use that or ), hence . Finally, assume that and . If then by the definition of . If then , with the equality if , . Thus .)

If we define (cf. [37, (4.6)])

then [37, Thm. 7], (11.7), and (11.8) imply

By the definition of , ; thus to finish the proof of the lemma it suffices to show that

| (11.9) |

If then ; to see this, take arbitrary and realize that . Fix any . Then, for every , ; hence

Since , we have

Thus (11.9) is established and the proof of the lemma is finished. ∎

11.3.2 Proof of Theorem 5

Proof of Theorem 5.

Keep the notation from Section 11.3.1. By Lemma 38, , and, using partial maximization,

Note that , where does not depend on . Thus

| (11.10) |

The second case immediately gives

| (11.11) |

If and for some , then (use (11.10) and the fact that, for any and , the map is strictly increasing and ). That is

| (11.12) |

Assume now that and . Note that

By (11.10), is differentiable and strictly concave on the open set (use that the Hessian, which is equal to , is negative definite). Thus the basic necessary and sufficient condition for unconstrained optimization [9, p. 258] gives that

where is the unique solution of ; that is,

The above equation immediately yields

and

| (11.13) |

Corollary 39.

If then, for every ,

11.3.3 The structure of the solution set

The structure of the cc-primal solution set , defined by (3.2), is described. First, recall the definition (11.5) of .

Proposition 40.

For every , is a nonempty compact set and

where

In particular, if then is a singleton.

Proof.

Fix and put , ; then, by Theorem 5, . The fact that is nonempty and compact follows from Theorem 32.

Take any . Then and, for every ,

If also then, analogously,

Thus, by combining these two inequalities,

For positive and , , with equality if and only if . Thus, for every ; hence,

| (11.14) |

Distinguish two cases. First assume that and put . Then (use that ) and

Hence and, since , by (11.14).

Assume now that ; then . Take any with and note that . An argument analogous to the first case gives

Hence if and only if . Since , the last condition is equivalent to the fact that for every with . In view of (11.14) this proves the proposition. ∎

11.3.4 Additional properties of the convex conjugate

Some additional properties of the convex conjugate , concerning its monotonicity and differentiability, are summarized in the next lemmas.

Lemma 41.

The following is true for every :

-

(a)

If then , with the equality if and only if .

-

(b)

If then (that is, is nondecreasing), with the equality if and only if and .

Proof.

(a) If then for every ; moreover, for some if and only if . Using (11.6), (a) follows.

(b) Assume that . Then for every , hence . If and then by Theorem 5. It suffices to prove that if or then .

Since the convex conjugate is finite-valued and convex, by [38, Thm. 10.4] it is locally Lipschitz. The following lemma claims that is even globally Lipschitz with the Lipschitz constant equal to . (Here we assume that is equipped with the sup-norm .)

Lemma 42.

The convex conjugate is a (finite-valued) convex function which is Lipschitz with .

Proof.

The fact that is always finite is obvious. To prove that is Lipschitz-, fix any . Then, for any ,

Analogously . Thus . Since by Lemma 37 (use that for ), we have . ∎

Lemma 43.

The map is differentiable (even ) and

The map is continuous.

Proof.

Since , the continuity of follows from the continuity of ; thus it suffices to prove the first part of the lemma.

To this end, we may assume that , that is, and . Put and define by

Note that, for every , is the unique solution of such that . The set is open and connected and is on . Moreover,

By the local implicit function theorem [9, Prop. 1.1.14], is on and is given by . From this the lemma follows. ∎

Lemma 44.

For every , the subgradient and the directional derivative of are given by

In particular, if then is differentiable at and

Proof.

This is a consequence of Danskin’s theorem [9, Prop. 4.5.1]. To see this, fix and take such that . Put and define

The map is continuous and the partial functions are (trivially) convex and differentiable for every with (continuous) . Thus, by Danskin’s theorem,

and

Note that is continuous by Lemma 43 and hence also is continuous. Thus on a neighborhood of , and so on . This proves the first assertion.

If then is a singleton , where . In such a case Danskin’s theorem gives that is differentiable at with . So also the second assertion of the lemma is proved. ∎

The convex conjugate is not strictly convex, even if . This is so because for every constant , cf. Lemma 37. However, the following holds.

Lemma 45.

Let . Then is and, for every ,

where , . Consequently, for every , and

Proof.

We use the notation from the proof of Lemma 43. By Corollary 39 and Lemma 43,

since . Further,

for , and

Thus the first assertion of the lemma is proved.

To prove the second part of the lemma, fix any and put , . Then

(). Since , Jensen’s inequality gives that , and if and only if . The lemma is proved. ∎

11.4 Proof of Theorem 6 (Relation between and )

The proof of Theorem 6 goes through several lemmas. First, in Lemma 47, the extremality relation between and is established using the Primal Fenchel duality theorem. Then the minimax equality for (cf. (11.15)) is proved, see Corollary 49. Proposition 51 gives a relation between the solution set of the primal and the solution set of the convex conjugate for . Lemma 52 provides a key for establishing the second part of Theorem 6. The structure of the solution set is described in Lemma 54.

11.4.1 Extremality relation

In the following denote by the set ; note that neither the primal nor the convex conjugate are affected by restricting to .

Lemma 46.

Let . If then .

Proof.

Take any and . Then, for every ,

Thus . ∎

Lemma 47.

For every convex closed set having support and for every it holds that

Proof.

Write the primal problem in the form

is the convex cone generated by . Since is convex, there is [9, Prop. 1.4.1(b)]. Further, is the support of , so there is satisfying . By [9, Prop. 1.4.1(a)], belongs to . Further, by [38, p. 50],

thus . Since trivially , it holds that

Now the Primal Fenchel duality theorem [9, Prop. 7.2.1, pp. 439–440], applied to the convex set , the convex cone and the real-valued convex function , gives that

and that the supremum in the right-hand side is attained. That is, and . ∎

11.4.2 Minimax equality for

Let be given by

| (11.15) |

Lemma 48.

For every and ,

Proof.

The first equality is immediate since if then . To show the second one, realize that . If then for every , and for ; hence . If , there is with (use that is convex closed, thus [9, Prop. 3.1.1] and ). Since for every ,

Thus provided . ∎

Corollary 49.

We have

Lemma 50.

For every and ,

Recall that is a saddle point of [9, Def. 2.6.1] if, for every and ,

| (11.16) |

11.4.3 Relation between and

Proposition 51.

Let . Then

11.4.4 From to

The proof of the following lemma is inspired by that of [10, Thm. 2.1].

Lemma 52.

Proof.

If then by (11.17). Since , again . As before we obtain and . The lemma is proved. ∎

11.4.5 Structure of

Lemma 53.

Let be as in Theorem 2. Then

Lemma 54.

Let be as in Lemma 52. Then

11.4.6 Proof of Theorem 6

Now we are ready to prove Theorem 6.

Proof of Theorem 6.

The facts that and were proved in Lemma 47. Further, the set is convex and closed due to the fact that the conjugate is convex and closed (even continuous, see Lemma 42). To show compactness of it suffices to prove that it is bounded.

Since , there is with ; put . Take any and put . Then, since and ,

for every . Thus and so is bounded, hence compact.

11.5 Proof of Theorem 16 (Relation between and )

First, basic properties of are proven. Then Lemma 56 provides a preparation for the recession cone considerations of . This leads to Proposition 57 giving the conditions of finiteness of . There is seen as a primal problem and Theorem 33 is applied to it. The solution set is described in Lemma 58. Lemma 59 provides properties of defined via , noting that need not belong to . Conditions equivalent to are stated in Lemma 62. Its proof utilizes also Lemmas 60 and 61.

Let be a type. Recall from Section 4 that the map is for defined by

Since

for every (where is defined on by (11.3)), Lemma 34 yields the following result.

Lemma 55.

If , then

-

(a)

for every , and if and only if ; so

-

(b)

is a proper continuous (hence closed) convex function;

-

(c)

the restriction of to its domain is strictly convex if and only if ;

-

(d)

is differentiable on with the gradient given by

-

(e)

the recession cone and the constancy space of are

11.5.1 Finiteness of the BD-dual

Lemma 56.

Let and be a convex closed subset of having support . Assume that is either an -set or a -set. Then there is an active letter with the following property: For any and

| (11.18) |

Proof.

Assume first that is a -set, that is, and there is an active letter such that whenever satisfies . Fix any , and choose such that . By compactness of we can find such that, for every , implies . (For if not, there is a sequence in with and for every ; by compactness, there is a limit point of this sequence and any such satisfies and , a contradiction.) Finally, take any .

Define by

| (11.19) |

Take arbitrary ; we are going to show that . If then and , so

by the choice of . On the other hand, if then, using ,

by the choice of . Thus .

Now assume that is an -set; that is, . By compactness, there exists such that for every . Continuing as above we obtain that, for any , and , the vector given by (11.19) belongs to . ∎

Proposition 57.

11.5.2 The solution set of the BD-dual

Lemma 58.

Let . Let be a convex closed subset of having support , which is neither an -set nor a -set (with respect to ). Then the solution set is nonempty, and there is such that and

Moreover, is a singleton if and only if .

Proof.

The proof is analogous to that of Proposition 36. Define by if , otherwise. Then for any , hence

| (11.20) |

By Lemma 55, is strictly convex, so contains at most one point. The set is neither an -set nor a -set, so there is with and . Thus, as in the proof of Proposition 57, . Since , Theorem 32 gives that is nonempty, hence a singleton; denote its unique point by . Since trivially , the first assertion of the lemma follows from (11.20). The second assertion follows from the first one and Lemma 46. ∎

11.5.3 No BD-duality gap; proof of Theorem 16

The proof of the following lemma is inspired by that of [10, Thm. 2.1].

Lemma 59 (Relation between and ).

Let . Let be a convex closed subset of having support , which is neither an -set nor a -set (with respect to ). Let be as in Lemma 58 and put

| (11.21) |

Then

Note that need not belong to ; for conditions equivalent to , see Lemma 62.

Proof.

Take any . Then

| (11.22) |

Applying (11.22) to and then to (both belonging to since is a cone) gives

| (11.23) |

Now (11.22) and (11.23) yield for every , that is, (for the last equality use that is convex closed). Further (recall the definition (11.5) of ),

by (11.23) and (11.21). Since , . Moreover, (use that ), and so . Finally,

The lemma is proved. ∎

Lemma 60.

Let and be a convex closed subset of having support . Then

Moreover, if then .

Proof.

Lemma 61.

Let , be a convex closed subset of having support , and be as in Theorem 2. Assume that is neither an -set nor a -set (with respect to ), and that . Then and belongs to .

Proof.

Now we prove that . For this follows from Lemma 60. In the other case put . This is a nonempty convex closed set with (use that is neither an -set nor a -set). Put and

where is defined on . Since we trivially have . Further, . (To see this, take any ; then there is such that for every . Since for any , for every such we have ; that is, .) Hence (for the equality see the definition () of ). By Lemma 60 and Theorem 6, , thus,

Now by the inequality from Lemma 60. To finish the proof it suffices to realize that this fact and (11.24) yield , and so . ∎

Lemma 62.

Keep the assumptions and notation from Lemma 59. Then there is no BD-duality gap, that is,

if and only if any of the following (equivalent) conditions hold:

-

(a)

;

-

(b)

;

-

(c)

;

-

(d)

;

-

(e)

;

-

(f)

;

-

(g)

;

-

(h)

for some ;

-

(i)

for some ;

-

(j)

for some (extremality relation);

-

(k)

.

Proof.

We first prove that the conditions (a)–(k) are equivalent. First, Theorem 2 and Lemma 59 yield that the conditions (a)–(c) are equivalent and that any of them implies (d). By the definitions of and from Theorem 6 and Lemma 59, (a) is equivalent to (e). Theorem 6 and Lemma 58 yield that the conditions (e)–(g) are equivalent. Since (d) implies (f) by Lemma 61, it follows that (a)–(g) are equivalent.

Since for any by Lemmas 58 and 59, (h) is equivalent to (i). Since is nonempty, (g) implies (h). If (h) is true then, for some ,

by Theorem 5; now Lemma 60 gives that . Hence (h) implies (f). Further, (b), (e), and (h) imply (j) by Theorem 5 and Lemma 59. On the other hand, the extremality relation (j) implies that and that ; that is, (j) implies both (b) and (f). So (a)–(j) are equivalent

By Theorem 6, (e) implies (k). By Lemmas 59 and 58, (k) implies that belongs to and that ; thus, (k) implies (h).

We have proved that the conditions (a)–(k) are equivalent. To finish we show that no BD-duality gap is equivalent to the condition (b). If (b) is true (that is, ) then by Lemma 59; hence (b) implies no BD-duality gap. Assume now that . Then Lemma 59 yields . So (b) is satisfied and the proof is finished. ∎

11.6 Proof of Theorem 19 (Active-passive dualization )

Proof of Theorem 19.

Fix with . Then . Recall that and note that is a convex closed subset of . Thus

is a convex closed subset of with . Put , and denote by and the primal problem and its solution set for minimizing over . Then is a singleton by Theorem 2, and ; hence

| (11.25) |

Consider now the BD-dual to . First, and, by Corollary 17,

11.7 Proof of Theorem 21 (Perturbed primal — the general case, epi-convergence)

We start with some notation, which will be used also in Section 11.8. Then we embark on proving the epi-convergence of perturbed primal problems.

11.7.1 Perturbed primal — notation

11.7.2 Epi–convergence

For the definition of epi-convergence, see [39, Chap. 7]. We will use [39, Ex. 7.3, p. 242] stating that, for every sequence of maps and for every ,

| (11.28) |

where is the closed ball with the center and radius . If , we say that the sequence epi-converges to and we write . For a system of maps indexed by real numbers , we say that epi-converges to for and we write , provided for every sequence decreasing to zero.

Before proving the epi-convergence of to , two simple lemmas are presented.

Lemma 63.

Let be a convex closed subset of with . Then there exists a positive real such that

where, for , denotes the unique point of .

Proof.

Fix some from and put . For any and we have ; so, by Lemma 34(d), is differentiable at and the directional derivative is nonnegative. Thus, by the choice of ,

for every . From this the lemma follows. ∎

Lemma 64.

Fix and take the map

defined on

Then is continuous on .

Proof.

Take any sequence from such that , . Then . The sum converges to . Further, for every such that ,

(which is true also in the case when ) and the right-hand side converges to zero. Hence and the lemma is proved. ∎

Note that need not be continuous on . For example, take , , converging to , and . Then , but does not converge to .

Lemma 65.

Let be a convex closed subset of with . Then the maps epi-converge to , that is,

Proof.

Take any sequence decreasing to . To prove that we use (11.28). Take , , and put

If then, since is closed, provided is small enough; hence .

Assume now that . Then, by the monotonicity of the logarithm,

If and , then and , so continuity of at easily gives that . If there is with , then and , so again .

Finally, assume that is such that and there is with . By Theorem 2 (applied to and to the nonempty convex closed subset of ), for every there is unique from such that

Moreover, by Lemma 63 there is such that

| (11.29) |

Take any convergent subsequence of , denoted again by , and let denote its limit. Then, by (11.29) and Lemma 64, converges to . Hence all cluster points of belong to . Since is continuous, . This implies that and the lemma is proved. ∎

Lemma 66.

Let . Then

Proof.

Take any decreasing to . Since epi-converges to and is finite, the result follows from [39, Thm. 7.1, p. 264] (in part (a) take ; use that and that ). ∎

The lemma states that every cluster point of a sequence of solutions of the perturbed primal problems () is a solution of the (unperturbed) primal . Of course, not every solution of can be obtained as a cluster point of a sequence of perturbed solutions. For example, it is shown in the following section that if satisfies the regularity condition (8.3), then the perturbed solutions converge to a unique solution of , regardless of whether is a singleton.

11.8 Proof of Theorem 22 (Perturbed primal — the linear case, pointwise convergence)

Let a model be given by finitely many linear constraints (2.3), that is,

where () are fixed vectors from . Let a type be given and let and be the sets of active and passive coordinates with respect to .

Assume that perturbed types () are such that the conditions (8.1) and (8.3) are true (with replaced by ); that is, is continuously differentiable,

and there is a constant such that, for every ,

The aim of this section is to prove that, under these conditions, solutions of the perturbed primal problems converge to a solution of the unperturbed primal ; that is,

11.8.1 Outline of the proof

The proof is based on the following ‘passive-active’ reformulation of the perturbed primal problem

hence, the passive projection of the optimal solution is

(recall that is the projection of onto the active coordinates and, for , that is the -slice of ). Employing the implicit function theorem, it is then shown that the passive projections can be obtained from the active ones via a uniformly continuous map . Since converges by Theorem 21, the uniform continuity of ensures that also converges.

The above argument is implemented in the following steps:

- 1.

-

2.

Define an open bounded polyhedral set by

(11.30) there stands for and stands for , for brevity. Let denote the projection of onto the first coordinates. For put

(11.31) In Lemma 69, it is proven that, for every , the map

(where and denote the -th rows of and , respectively) has a unique minimizer .

- 3.

- 4.

11.8.2 Parametric expression for

Let be given by (2.3). Denote by the matrix whose first rows are equal to (the passive projections of , ), and the last row is a vector of ’s; analogously define using the active projections of . Let be such that for and . Then

| (11.33) |

Let (of dimension ) be the Moore-Penrose inverse of . By [21, p. 5-12], (11.33) can be written in the following form, where denotes the identity matrix:

where

Put .

If then and uniquely depends on . That is, for every , the set is a singleton. By Theorems 2 and 21, also is a singleton and converges to the unique member of ; so in this case Theorem 22 is proved.

Hereafter, we assume that and, without loss of generality, that the first columns of are linearly independent. Put

(the submatrix of entries that lie in the first rows and the first columns). Since equals , the next lemma follows.

Lemma 67.

Let be given by (2.3) and be as above. Assume that . Then there are , an matrix of rank , an matrix , and a vector such that

There,

and

is a nonempty closed polyhedral subset of .

Note that, for , since has full column rank.

Keep the notation from Lemma 67. Write for , for , and define by (11.30). Let be the natural projection mapping onto . Put

and, for , define by (11.31). Since is the -slice of ,

Note also that, by Lemma 67,

| (11.34) |

for every , , and every . Moreover,

| (11.35) |

Lemma 68.

The following are true:

-

(a)

is a nonempty open bounded polyhedral set;

-

(b)

is a nonempty open bounded set;

-

(c)

() is a nonempty open (closed) bounded polyhedral set for every .

Proof.

(a) The fact that is open and polyhedral is immediate from (11.30). It is nonempty since for every and every such that (such exists since has support ). To finish the proof of (a) it remains to show that is bounded. Since has full column rank, (11.34) and [21, p. 5-12] yield

where is the Moore-Penrose inverse of . Thus is bounded.

(b) Since is the natural projection of , it is open, bounded and nonempty.

(c) Boundedness follows from (a); the rest is trivial. ∎

11.8.3 Global minima of the maps ()

Fix and define a map by

| (11.36) |

(the convention applies), where and denote the -th rows of and , respectively. Since is differentiable on , we can define a map by (11.32); that is,

Easy computation gives (recall that , hence also , is differentiable)

| (11.37) |

where is the transpose of , and are given by

| (11.38) |

Lemma 69.

For every there is a unique minimizer of :

Proof.

Since is open for every , the necessary condition for optimality gives the following result.

Lemma 70.

Let be as in Lemma 69. Then, for every ,

Since is continuously differentiable and is always regular, the local implicit function theorem [9, Prop. 1.1.14] and (11.37) immediately imply the next lemma.

Lemma 71.

11.8.4 Boundedness of

Let denote the spectral matrix norm [21, p. 37-4], that is, the matrix norm induced by the Euclidean vector norm, which is also denoted by . If is a matrix, denotes its transpose. The following result must be known, but the authors are not able to give a reference for it.

Proposition 72.

Let and be an matrix with full column rank . Then there is such that

for every -diagonal matrix with positive entries on the diagonal.

Before proving this proposition we give a formula for the inverse of , which is a simple consequence of the Cauchy-Binet formula; cf. [21, p. 4-4]. To this end some notation is needed. If is an matrix and , are nonempty, by we denote the submatrix of of entries that lie in the rows of indexed by and the columns indexed by . , , , and are shorthands for , , , and , respectively (there, means the complement of ). For , denotes the system of all subsets of of cardinality . Finally, if is an indexed system of numbers and is finite, put

Lemma 73.

Let , be an matrix with full rank , and be a diagonal matrix with every . Put

Then is regular and the following are true:

-

(a)

,

-

(b)

for every ,

-

(c)

,

where , , and for every , , and .

Proof.

Put . By the Cauchy-Binet formula,

thus (a) and the regularity of are proved. Also the property (b) immediately follows from the Cauchy-Binet formula, since . Finally, (c) follows from the formula , where is the adjugate of , and the fact that is symmetric. ∎

Proof of Proposition 72.

The proof is by induction on . If then is a regular square matrix and , so it suffices to put . Assume that and that the assertion is true for every matrix of type . Take any matrix of rank and any diagonal matrix with . Since for any , we may assume that and for every . Put and write in the form

with being an matrix and . Without loss of generality assume that . By the induction hypothesis, there is a constant not depending on such that .

An easy computation gives

By the Sherman-Morrison formula [21, p. 14-15], for any , it holds that

Hence

and

To finish the proof it suffices to show that is bounded by a constant not depending on . (Indeed, if this is true then , which follows from the matrix norm triangle inequality applied to , and from the matrix norm consistency property; cf. [21, p. 37-4].)

11.8.5 Lipschitz property of

The result of the previous section and Lemma 71 yield that is Lipschitz, hence uniformly continuous on .

Lemma 74.

The map is Lipschitz on . Consequently, there exists a continuous extension of to the closure of .

11.8.6 Proof of Theorem 22

The following lemma demonstrates that, for , the passive projection of the solution of can be expressed via and the active projection .

Lemma 75.

Proof.

Acknowledgements

Substantive feedback from Jana Majerová is gratefully acknowledged. This research is an outgrowth of the project “SPAMIA”, MŠ SR-3709/2010-11, supported by the Ministry of Education, Science, Research and Sport of the Slovak Republic, under the heading of the state budget support for research and development. The first author also acknowledges support from VEGA 2/0038/12, APVV-0096-10, and CZ.1.07/2.3.00/20.0170 grants.

References

- [1] A. Agresti. Categorical data analysis. Wiley-Interscience [John Wiley & Sons], New York, second edition, 2002.

- [2] A. Agresti and B. A. Coull. The analysis of contingency tables under inequality constraints. J. Statist. Plann. Inference, 107(1-2):45–73, 2002.

- [3] J. Aitchison. The statistical analysis of compositional data. Chapman & Hall, London, 1986.

- [4] J. Aitchison and S. D. Silvey. Maximum-likelihood estimation of parameters subject to restraints. Ann. Math. Statist., 29:813–828, 1958.

- [5] K. Anaya-Izquierdo, F. Critchley, P. Marriott, and P. W. Vos. Computational information geometry: theory and practice. arXiv preprint arXiv:1209.1988, 2012.

- [6] R. Baker, M. Clarke, and P. Lane. Zero entries in contingency tables. Comput. Statist. Data Anal., 3:33–45, 1985.

- [7] W. Bergsma, M. Croon, and L. A. van der Ark. The empty set and zero likelihood problems in maximum empirical likelihood estimation. Electron. J. Stat., 6:2356–2361, 2012.

- [8] W. Bergsma, M. A. Croon, and J. A. Hagenaars. Marginal models. Springer, 2009.

- [9] D. P. Bertsekas. Convex analysis and optimization. Athena Scientific, Belmont, MA, 2003. With Angelia Nedić and Asuman E. Ozdaglar.

- [10] H. El Barmi and R. L. Dykstra. Restricted multinomial maximum likelihood estimation based upon Fenchel duality. Statist. Probab. Lett., 21(2):121–130, 1994.

- [11] H. El Barmi and R. L. Dykstra. Maximum likelihood estimates via duality for log-convex models when cell probabilities are subject to convex constraints. Ann. Statist., 26(5):1878–1893, 1998.

- [12] S. E. Fienberg and A. Rinaldo. Maximum likelihood estimation in log-linear models. Ann. Statist., 40(2):996–1023, 2012.

- [13] R. A. Fisher. Theory of statistical estimation. Math. Proc. Cambridge Philos. Soc., 22(05):700–725, 1925.

- [14] C. J. Geyer. Likelihood inference in exponential families and directions of recession. Electron. J. Stat., 3:259–289, 2009.

- [15] A. Ghalanos and S. Theussl. Rsolnp: general non-linear optimization using augmented Lagrange multiplier method. 2012. R package version 1.14.

- [16] D. V. Gokhale. Iterative maximum likelihood estimation for discrete distributions. Sankhyā Ser. B, 35(3):293–298, 1973.

- [17] M. Grendár and G. Judge. Empty set problem of maximum empirical likelihood methods. Electron. J. Stat., 3:1542–1555, 2009.

- [18] M. Grendár and V. Špitalský. Source code for “Multinomial and empirical likelihood under convex constraints: directions of recession, Fenchel duality, perturbations”. http://www.savbb.sk/grendar/likelihood/Rcode-arxiv-v1.zip.

- [19] M. Haber. Maximum likelihood methods for linear and log-linear models in categorical data. Comput. Statist. Data Anal., 3(1):1–10, 1985.

- [20] P. Hall and B. Presnell. Intentionally biased bootstrap methods. J. R. Stat. Soc. Ser. B Stat. Methodol., 61(1):143–158, 1999.

- [21] L. Hogben, editor. Handbook of linear algebra. Discrete Mathematics and its Applications (Boca Raton). Chapman & Hall/CRC, Boca Raton, FL, 2007.

- [22] C. T. Ireland, H. H. Ku, and S. Kullback. Symmetry and marginal homogeneity of an contingency table. J. Amer. Statist. Assoc., 64:1323–1341, 1969.

- [23] C. T. Ireland and S. Kullback. Contingency tables with given marginals. Biometrika, 55:179–188, 1968.

- [24] P. Kall. Approximation to optimization problems: an elementary review. Math. Oper. Res., 11(1):9–18, 1986.

- [25] D. F. Kerridge. Inaccuracy and inference. J. Roy. Statist. Soc. Ser. B, 23:184–194, 1961.

- [26] J. H. Klotz. Testing a linear constraint for multinomial cell frequencies and disease screening. Ann. Statist., 6(4):904–909, 1978.

- [27] J. B. Lang. Multinomial-Poisson homogeneous models for contingency tables. Ann. Statist., 32(1):340–383, 2004.

- [28] B. G. Lindsay. Mixture models: theory, geometry and applications. In NSF-CBMS regional conference series in probability and statistics, pages i–163, 1995.

- [29] J. K. Lindsey. Parametric statistical inference. The Clarendon Press, Oxford University Press, New York, 1996.