On the resolution of misspecified convex optimization and monotone variational inequality problems

Abstract

We consider a misspecified optimization problem that requires minimizing a function over a closed and convex set where is an unknown vector of parameters that may be learnt by a parallel learning process. In this context, we examine the development of coupled schemes that generate iterates as , then , a minimizer of over and . In the first part of the paper, we consider the solution of problems where is either smooth or nonsmooth. In smooth strongly convex regimes, we demonstrate that such schemes lead to a quantifiable degradation of the standard linear convergence rate. When strong convexity assumptions are weakened, it can be shown that the convergence in function values sees a modification in the convergence rate of by an additive factor where represents the initial misspecification in and denotes the contractive factor associated with the learning process. In both convex and strongly convex regimes, diminishing steplength schemes are also provided and are less reliant on the knowledge of problem parameters. Finally, we present an averaging-based subgradient scheme and show that the optimal constant steplength leads to a modification in the rate by , implying no effect on the standard rate of . In the second part of the paper, we consider the solution of misspecified monotone variational inequality problems, motivated by the need to contend with more general equilibrium problems as well as the possibility of misspecification in the constraints. In this context, we first present a constant steplength misspecified extragradient scheme and prove its asymptotic convergence. This scheme is reliant on problem parameters (such as Lipschitz constants) and leads us to present a misspecified variant of iterative Tikhonov regularization. Numerics support the asymptotic and rate statements with one important observation: it appears that the rate bound derived for strongly convex problems appears to be slack in that the standard linear rate is again observed, despite the theoretical prediction that learning leads to degradation.

1 Introduction

Traditionally, the field of deterministic optimization has focused on

the problem of minimizing a function over a prescribed set

and it is generally assumed that the decision maker has complete

knowledge of both the function and the set

(cf. [1, 2]). In many settings,

problem data may be uncertain, severely limiting the applicability of

deterministic methods. Initiated through the research by

Dantzig [3] and Beale [4],

stochastic programming has represented a popular avenue for addressing

risk-neutral as well as risk-averse static and adaptive (recourse-based)

decision-making problems [5, 6]

in developing both static as well as adaptive (recourse-based) models.

An alternative approach has found merit by obviating the need for

distributional information and instead focuses on obtaining solutions

that are robust to parametric uncertainty over a prescribed

(uncertainty) set [7, 8]. In

either instance, a subset of parameters is natively uncertain. Our focus

is on a class of problems in which the vector parameters is ,

a fixed but unknown vector, that may be learnt through a

related but distinct learning process. We provide a clearer

understanding of our problem of interest by considering a

motivating problem.

Data-driven stochastic optimization: Standard models for stochastic optimization have required the solution of the following problem [5, 6]:

| (StochOpt) |

where , , is a dimensional random variable, and denotes the probability space. Note that represents the parameters of the distribution . Unfortunately, a key shortcoming in the use of standard models necessitates knowledge of , often a stringent requirement. Instead, suppose may be learnt by a suitably defined maximum likelihood estimation (MLE) problem [9], captured by a metric , and formally defined as follows:

| (MLE) |

Generally, in most practically occurring problems, the MLE problem is

often massive and one avenue lies in generating sequences

such that is an approximate solution of

(StochOpt).

A range of other problems can be cast in a similar regime. For instance, in traffic equilibrium problems [10], a common assumption is that the demand pattern and the travel times are known vectors, assumptions that are often hard to justify in practice. Similarly, in a range of production planning problems, it is routinely assumed that cost and demand information is accurately available when in fact, it needs to be empirically estimated. Consequently, one approach lies in conducting such an estimation through a parallel learning process. Yet another problem that can be cast under this umbrella is the well studied multi-armed bandit problem [11]. In such a problem, a gambler is faced with a choosing from a collection of slot machines at every step without a prior knowledge of the average reward distribution. If one could view the learning problem associated with the reward distributions as a parallel estimation problem, this may be one avenue towards developing algorithmic techniques. Motivated by this new set of decision-making problems, we consider the static misspecified convex optimization problem , defined as follows:

| () |

where , is a convex function in for every . Suppose denotes the solution to a convex learning problem denoted by :

| () |

where is a convex function in and is defined on a closed and convex set Consequently, we consider gradient methods in which sequences and may be generated with the goal that

It should be noted that the second author has examined the counterpart of such problems in stochastic regimes where stochastic approximation schemes are employed [12].

1.1 Alternate and related avenues

Given that the focus lies on solving and simultaneously, at least three approaches assume relevance and are described next.

A sequential approach:

A natural question is whether this problem could indeed be solved in a sequential fashion. For instance, one approach could be to compute in the first stage and subsequently solve (). Yet such an avenue is complicated by several challenges: (i) First, the problem () is often of a large or massive scale and accurate/exact solutions of this problem are needed in finite time to utilize this approach. However, the claim that finite termination schemes are available is a strong one. In fact, even in the rare instance when this requirement is met, the number of steps might be far too large in practice. Consequently, such an approach leads to obtaining an approximation of , given by a vector and cannot provide asymptotically accurate solutions. (ii) Second, if the process is terminated prior to the commencing with the computation of , then the resulting computational effort would be wasted in that we have no guarantees regarding the solution. We consider precisely such an approach in the context of economic dispatch problems, discussed in Section 4. Table 1 shows the importance of terminating the learning problem after a sufficiently large number of iterations via a sequential approach. In particular, for smaller problems with generators, learning steps suffice in getting reasonably accurate estimates of while the same number of iterations prove insufficient for getting accurate solutions for networks with generators. In contrast, our focus lies in developing techniques that can provide asymptotically accurate solutions equipped with global non-asymptotic error bounds.

| Learning steps | Computational steps | number of generators 5 | number of generator 40 | ||

|---|---|---|---|---|---|

| 1000 | 15000 | e | e- | e | e- |

| 5000 | 15000 | e | e- | e | e- |

| 10000 | 15000 | e- | e- | e | e- |

| 15000 | 15000 | e- | e- | e | e- |

A variational approach:

Given that a sequential approach may not always be satisfactory, a partial resolution lies in considering a variational approach where the overall problem is cast as a static variational inequality problem [10]. If and , then it may be recalled that VI requires an such that for all Under convexity assumptions, it can be shown with relative ease that is a solution of VI if and But the solution of VI via projection-based techniques [13] remains a challenge since is generally not a monotone map over the set even if and are convex functions in and , respectively; it may be recalled that a map is monotone over if for every , . But there are no available first-order schemes for computing solutions to non-monotone variational inequality problems, severely limiting the utility of such an approach. Yet, despite the inherently challenging nature of the joint variational problem, our goal remains in deriving non-asymptotic rates of convergence for gradient methods for such problems by leveraging the structure of the problem and ascertaining the impact that learning has on the rates.

A robust optimization approach:

Robust optimization, a subfield of optimization, considers obtaining solutions that are robust to parametric uncertainty [8, 14, 7]. In such problems, rather than a vector , a part of the problem input is the uncertainty set, say . In such a case, the relevant robust optimizaton problem attempts to obtain an that minimizes the worst-case value that takes over :

In contrast, our framework is fundamentally different in that the vector is a deterministic and unknown vector that can be learnt. To provide a clearer comparison, the learning scheme solves the following problem

Learning while doing schemes:

Finally, we note the surge of interest in algorithms which incorporate learning directly into the optimization phase. Early instances of such problems were seen in the form of the multi-armed bandit problem [15, 11] in which a decision-maker simultanelusly acquires new knowledge and leverages existing knowledge in optimizing decisions. In contrast with the current context, the learning problem is no longer static and available a priori; instead, it evolves in time as a consequence of aggregating observations. In response to such challenges, Agarwal et al. have developed techniques in the context on online linear programming [16] as well as stylized counterparts in the context of revenue management [17, 18]. A rather different tack is taken in the work by Jiang et al. [19], where the problem is replaced by a sequence of learning problems , such that the index of represents the number of data points used within the construction of the associated estimation (regression) problem. The solution of the th learning problem is denoted by and under suitable assumptions, , where is a solution to the limiting problem. If is used within the scheme for computing , then probabilistic convergence statements are provided for in the context of distributed projection-based schemes for stochastic Nash games, leading to monotone variational inequality problems. We note that offline schemes provide a benchmark in terms of ascertaining the cost of obtaining observations over time, rather than a priori, allowing us to derive metrics to relate online schemes with their offline counterparts (such as through competitive ratios for instance).

1.2 Contributions and outline

In this paper, we investigate the global convergence and rate analysis of joint first-order gradient methods under a variety of convexity, Lipschitzian, and boundedness requirements. Suppose and denote steplength for optimization and learning at iteration . If denotes the Euclidean projection of a vector on the set , then consider the following prototypical update:

Algorithm 1 (Joint gradient scheme).

Given and and sequences ,

| (Opt) | |||||

| (Learn) |

In our proposed scheme, we take a gradient step in the

-space using an estimate of and a

simultaneous step in the space. Note that instead of using the exact gradient at the th iterate, we employ as the gradient estimate and represents the error in

the gradient at iteration . Recent literature on inexact

gradient schemes has investigated convergence properties and rate

analysis for various schemes using inexact

gradients with bounded

error [20, 21, 22, 23, 24].

Our framework is distinct in that we develop a broader framework of

gradient, extragradient, and regularized schemes for solving both

optimization and variational inequality problems through the

provision of modified algorithmic requirements (such as those on

steplengths), asymptotics, and enhanced rate statements.

The framework is developed under the caveat that the inexactness (in

gradient estimates) decays to zero at a prescribed rate, a

consequence of obtaining increasing accurate estimates of

when taking the gradient step in the space. The main

contributions of this work can be captured as follows:

(i) Convex optimization: In the first part of this

paper, we develop asymptotics and rate statements for misspecified

convex optimization problems in smooth and nonsmooth settings and assume

that the learning problem is strongly convex, unless mentioned

otherwise: (a) Smooth optimization problems: Our first set of results in the smooth regime demonstrate

that constant steplength schemes are convergent but lead to a

quantifiable decay in the linear convergence rate characteristic of

constant steplength gradient methods. Unfortunately, such techniques are

heavily reliant on the knowledge of certain problem parameters, in the

absence of which we show that diminishing steplength sequences are also

convergent. When the strong convexity assumptions are weakened, we note

that the presence of learning leads to modification of the convergence

rate in function values by an additive factor given by

where represents our

initial estimate of , denotes the contractive

constant in the learning problem. Finally, we demonstrate that when

the learning problem loses strong convexity, under a suitably

defined weak-sharpness requirement, global convergence can still be

retained; (b) Nonsmooth optimization problems: When the

optimization problem is nonsmooth, it can be shown that while the

overall convergence rate of the proposed misspecified subgradient

methods is still , a similar additive factor emerges

of the form A summary of the rate statements is provided

in Table 2.

| Computation | Computation & Learning | |

|---|---|---|

| Strongly convex/diff. | Linear | Sublinear |

| convex/diff. | ||

| convex/nonsmooth. |

(ii) Monotone variational inequality problems: Variational

inequality problems represent a broad framework for capturing

optimization and equilibrium problems and assume particular relevance,

given that misspecification may arise in the constraints. In the second

part of this paper, we consider two sets of schemes for resolving

misspecified variational inequality problems. Of these, the first avenue

is a constant steplenth misspecified extragradient scheme for monotone

variational inequality problems. However, this approach requires an

accurate estimate of suitable Lipschitz parameters. Consequently, we

present a misspecified variant of the iterative Tikhonov regularization

framework to misspecified monotone regimes.

(iii) Numerics: We develop a set of test problems based on economic dispatch problems [25] with misspecified cost and demand. The numerics support the asymptotic statements and the validity of the bounds.

2 Misspecified Convex Optimization

In this section, we will consider two settings differentiated by the assumptions on the function in and the function in . In Section 2.1, we examine gradient-based methods where is differentiable in for every while in Section 2.2, we weaken the smoothness requirement on . In each setting, we provide both constant steplength schemes with associated complexity statements as well as diminishing steplength schemes that are less reliant on problem parameters.

2.1 Smooth convex optimization

In this section, we consider regimes where both the optimization and learning problems are differentiable and distinguish the cases based on the convexity assumptions on the problem. Specifically, in subsection 2.1.1, we provide convergence statements and rate analysis when both problems are strongly convex. Next, in subsection 2.1.2, we weaken the strong convexity assumption on the computational problem to mere convexity and provide rate statements in such settings. Finally, in subsection 2.1.3, we relax the strongly convex assumption of the learning function and analyse the case when the solution set of the learning problem satisfies a weak sharpness assumption. We now list several key assumptions used during our analysis. We begin with a differentiability assumption on and .

Assumption 1.

The function is continuously differentiable in for all and function is continuously differentiable in .

Next, we impose a Lipschitzian assumption on in , uniformly in .

Assumption 2.

The gradient map is Lipschitz continuous in with constant uniformly over or

Additionally, the gradient map is Lipschitz continuous in with constant .

Finally, we impose a requirement on steplength sequences for the computational and learning problems required in the diminishing steplength regime.

Assumption 3.

Let and be diminishing nonnegative sequences chosen such that , , , and .

2.1.1 Strongly convex optimization and learning

In this subsection, convergence statements for the iterates produced by Algorithm 1 are provided under the following strong convexity assumption.

Assumption 4.

The function is strongly convex in with constant for all and the function is strongly convex with constant .

We impose an additional Lipschitzian assumption on in .

Assumption 5.

The gradient is Lipschitz continuous in with constant .

Before providing the main results, we introduce the following Lemma from [26]:

Lemma 1.

Let the following hold:

Then, . In particular, if , then .

Our first result provides a convergence statement under a constant steplength assumption.

Proposition 2 (Constant step length scheme).

Proof.

By nonexpansivity of the Euclidean projector and triangle inequality, can be bounded as follows:

| (1) |

The first term in (1) can be further bounded by first writing the following expansion:

| (2) |

Under the assumption of Lipschitz continuity of in , it follows that

By combining the above inequality with (2), we obtain

| (3) |

In addition, under strong convexity of in , it follows that

Thus, inequality (3) becomes

| (4) |

Note that since , then it follows that The second term in is bounded by leveraging the Lipschitz continuity of in :

| (5) |

Now by combining (1), (4), and (5), we obtain the following bound:

| (6) |

where and . To show that as , we may employ Lemma 1. This requires showing the following:

Since , is satisfied. In addition, by the Lipschitz continuity of and choosing such that , as . Consequently, condition is met as well, completing the proof. ∎

In many instances, while we may be able to claim strong convexity or

Lipschitz continuity, the precise bounds may be unavailable. However,

an incorrect choice of a steplength may lead to divergence, motivating

the need for an alternate approach. To this end, we employ a diminishing

steplength sequence that does not necessitate the knowledge of either

the convexity constant or the Lipschitz constant. We outline the proof

of convergence in the next Proposition.

Proposition 3 (Diminishing steplength schemes).

Proof.

We use a similar line of argument as in Proposition 2 to obtain the following bound:

| (7) |

where for sufficiently large , we have that and . By Assumption 3, we have that . Furthermore, we have the following simplification of condition (ii) of Lemma 1:

since and and as . Therefore, the conditions of Lemma 1 are satisfied and as . ∎

It is well known that under strong convexity assumption, the iterates generated from the projected gradient method converge at a geometric rate [27]. However, when learning is incorporated, it is expected that this rate drops. Next, we analyze the impact introduced by learning.

Proposition 4 (Rate analysis in strongly convex regimes).

Proof.

Under the assumption of strong convexity of , the learning algorithm has a globally geometric rate of convergence when employing constant stepsize where ; specifically,

| (8) |

where since . To obtain the convergence rate for the joint scheme, we expand to obtain the following bound:

| (9) |

We may further expand using to simplify the bound as below:

where . Note that condition guarantees that , implying that is less than 1. ∎

Remark: Notably, the presence of learning leads to a degradation in the convergence rate from the standard linear rate to a sub-linear rate. Furthermore, it is easily seen that when we have access to the true , the original rate may be recovered.

2.1.2 Convex optimization with strongly convex learning

In this subsection, we weaken the rather stringent assumptions of strong convexity of in for every .

Assumption 4b. The function is convex in for all and the function is strongly convex with constant .

In addition, we make the following assumptions:

Assumption 6.

-

(a)

The sets and are compact and , where is a constant.

-

(b)

The gradient map is uniformly Lipschitz continuous in with constant :

Assumption 7.

There exists a constant such that

Before presenting the main result, we introduce the following Lemma from [28].

Lemma 5.

Let for all . Furthermore, suppose the following holds for all :

Suppose and . Then and .

In the following proposition, we prove the convergence of the iterates

generated by Algorithm 1 under the convexity requirements on

. We also provide the rate statement.

Proposition 6 (Constant steplength scheme with averaging).

Proof.

(i) Recall the following by the mean-value theorem, the Cauchy-Schwartz inequality, and Lipschitz continuity of the gradient map in :

If we set and and since , we have the following:

| (10) |

where . Under the convexity of in ,

| (11) |

By summing up (10) and (11), we obtain

| (12) |

Next, we bound the term From the property of the projection on a convex set, denoted by , we have that

If we set and in the above inequality and by noting that , we obtain that After rearrangement of the terms, the above inequality is equivalent to

By using this bound in (12), we get that

Since , the above inequality can be written as

Moving to the other side and summing from to , we get the following:

where the second inequality follows from the nonnegativity of . Dividing both sides by ,

| (13) |

By Assumption 6(a), for all . In addition, by Assumption 6(b), we have that . Since the function is strongly convex and , there exists a such that . Therefore, from (13), we obtain the following:

By leveraging the convexity of in , we have that

| (14) |

But, we may derive a bound on as follows:

| (15) |

We leverage the Lipschitz continuity of in uniformly in with constant together with (14) and (15) to complete the proof of (i):

| (16) |

where and

.

(ii) Global convergence

follows by taking limits (16) and by recalling that

to claim that

∎

Remark: Unlike in the case of strongly convex

optimization, there is no degradation in the standard rate of

convergence in function values which is . In particular, the

contribution from learning adds a factor to this rate that is scaled

by , the distance of from . Notably,

this factor has two parts, the first of which is a faster geometric rate

given by and the a second part given by

. In short, the overall rate

changes by a constant factor. Furthermore, if , we

recover the standard rate for convex optimization. However, this scheme

does require knowledge of relevant Lipschitz

constants and we now present diminishing

steplength schemes that do require Lipschitzian properties but do not

require knowing the precise constants.

Proposition 7 (Diminishing steplength scheme).

Proof.

By the nonexpansivity property of the Euclidean projection operator, for all , can be bounded as follows:

| (17) |

where . By leveraging convexity and the gradient inequality, we have that implying that

| (18) |

By substituting (18) in (17) and by noting that , we have the following bound:

| (19) |

By Assumption 6, we have that . In addition, under strong convexity of and choosing , we have that , where . Consequently as . Furthermore, can be further simplified as below:

| (20) |

The requirements of Lemma 5 hold since since Consequently, by leveraging Lemma 5, we observe that since

and , since

and

is bounded, a consequence of the

compactness of and and the continuity of the gradient

map. We may therefore conclude that

and

It suffices to show that .

Since and , it follows that . Since the set is closed, all accumulation points of lie in . Furthermore, since along a subsequence, it follows that has a subsequence converging to some point in . Moreover, since is convergent, then the entire sequence converges to a point in . ∎

2.1.3 Convex optimization with convex learning

A key restriction in the prior subsection is the need for imposing a strong convexity assumption on the learning problem. The need for this assumption arises from noting that we require utilizing a rate estimate in solution iterates in the learning space, rather than merely function iterates. In this subsection, we consider a convex learning problem but impose a weak sharpness requirement [26] which is defined next. Note that an alternative approach is pursued in the next section in a more general variational regime.

Definition 2.1 (Weak sharpness).

The solution set is said to be weak sharp if there exists a positive number such that where and is called modulus of sharpness.

Under a weak sharpness requirement on the solution set, the solution to the learning problem can be obtained in a finite number of iterations. The proof of this Lemma may be found in [26].

Lemma 8 (Finite convergence under constant steplength).

Consider a convex differentiable learning problem in which the solution set is nonempty and satisfies a weak sharpness property. Furthermore, is assumed to be Lipschitz continuous with a constant . Then, the sequence generated by a projected gradient scheme with stepsize converges to in a finite number of iterations, where .

We now consider a constant steplength scheme where and are sufficiently small constants.

Proposition 9 (Constant steplength scheme).

Let Assumptions 1, 2, and 6 hold. In addition, suppose that satisfies a weak sharpness requirement and the stepsize sequences and are fixed at some positive constants and , respectively, where and . Let be the sequence generated by Algorithm 1. Then, converges to a point in and converges to a point in as .

Proof.

Based on Lemma 8, there exist a finite such that for all , we have that . Hence, for all , Algorithm 1, becomes standard projected gradient scheme without learning and thus under Lipschitzian property of gradient of function and by choosing , the sequence converges to . For the proof of convergence of gradient projected scheme, the reader can refer to [26] . ∎

Next, we consider a diminishing steplength sequence for the optimization and learning problems and provide an intermediate result on the summability of the sequence

Lemma 10.

Proof.

Under boundedness of gradient of function and by using diminishing step length

Under the weak sharp property of , we have that . By substituting this expression into the above inequality, we obtain

where . Since , then by using Lemma 5, we conclude that ∎

We now impose a Lipschitzian requirement on the gradient map in uniformly in .

Assumption 8.

There is a constant such that for for all , and .

Theorem 11 (Diminishing steplength scheme).

Proof.

By the nonexpansivity property of the Euclidean projection operator, for all and any , can be bounded as follows:

where . By leveraging convexity and the gradient inequality, we have that

implying that By the previous observation and the Cauchy-Schwartz inequality, we have the following:

| (21) |

where is the constant in Assumption 6(a). By Lemma 10,

In addition,

where . Hence, the conditions of Lemma 5 are satisfied and the sequence is convergent for any and The the latter implies in view of Since the set is closed, all accumulation points of lie in . Furthermore, since along a subsequence, by continuity of it follows that has a subsequence converging to some point in . Moreover, since is a convergent sequence, the entire sequence converges to some point in . Finally, the sequence converges to a , a consequence of Lemma 10. ∎

2.2 Nonsmooth convex optimization

In this section, we derive the global convergence and rate statements for the regime when function is not necessarily differentiable. Note that Assumptions 1, 2 and 4 still hold for function and for clarity, we restate them in the following assumption and proceed to present a subgradient-based analog of Algorithm 1.

Assumption 9.

The function is continuously differentiable in , strongly convex, and the gradient map is Lipschitz continuous in with constant .

Algorithm 2 (Joint subgradient scheme).

Given an and a and sequences , then

| (nsOpt) | |||||

| (Learn) |

where .

We now state two assumptions employed in this subsection, the first of which pertains to subgradient boundedness while the second imposes Lipschitz continuity of in uniformly in .

Assumption 10 (Subgradient boundedness).

There exists an such that for all and for all .

Assumption 11.

There exists a constant such that

The following Lemma will be used subsequently in our convergence analysis.

Lemma 12.

Proof.

By nonexpansivity of the Euclidean projector and triangle inequality, we may bound as follows:

Now, by leveraging convexity of function in for all , we obtain

| (22) |

By Assumption 11, the function is Lipschitz continuous in for every . Consequently, and . It follows that

By combining these two inequalities, we get the following lower bound:

Now by combining above inequality with (22), we have that

| (23) |

∎

By leveraging Lemma 12, we now provide the main convergence result for subgradient-based schemes for resolving misspecified convex optimization problems.

Proposition 13 (Global convergence for diminishing steplength schemes).

Proof.

Using (23) for , where is any point in , we obtain

To prove the convergence, we employ Lemma 5. Since , we have that

Hence, conditions of Lemma 5 are satisfied and as and . Because , we can conclude that . This implies that a subsequence of converges to a point in . But the entire sequence is convergent, implying that the entire sequence converges to a point in . Furthermore, as . ∎

In keeping with the focus of this paper, we now provide derive rate statements for the function iterates where we quantify the impact of learning.

Proposition 14 (Rate analysis with averaging).

Proof.

(i) By letting in (23) and by summing (23) over , we have that the following holds:

By the nonnegativity of , it follows that

| (25) |

From the convexity of in , we have the following:

| (26) |

By combining (25) and (26), we obtain the inequality

Notably, the second term arises from learning and can be further bounded as follows:

Consequently, we may bound as follows:

It follows that may be bounded as follows:

Since , , and

, it

follows that

(ii) Next, if we assume that the steplength is fixed at ,

after iterations, the bound on the error is given by

the following:

If we minimize the right hand side with respect to , we arrive at the best optimal constant stepsize

Using this step length, we have the optimal convergence rate of

where and ∎

Remark: Standard subgradient methods for convex optimization display a convergence rate of in function value [29]. Notably, the joint scheme shows no degradation in the rate, not even in a constant factor sense. More specifically, the modification in the rate is given by , with both terms arising from learning diminishing to zero at a faster rate. This factor is scaled by the distance of from its true value and we recover the original rate if .

3 Misspecified monotone variational inequality problems

In the problem formulation investigated thus far, the misspecified parameter lay in the objective function . Yet in many instances, the misspecification may also arise in the constraint set. In particular, consider the following misspecified problem , defined as

| () |

where , is a convex function in for every . One approach is to relax the constraints that are misspecified and consider a Lagrangian (or an augmented Lagrangian) approach. Another approach lies in leveraging the convexity of the problem and considering the complementarity problem arising from the first-order (sufficient) optimality conditions. It is well known that if the constraints set has an algebraic structure given by

where is a convex function in for every , then the first-order conditions are given by

| (CP)) |

where for every . It is well known [10] that this complementarity problem (CP) is equivalent to VI, where and , defined as

is a monotone map. More generally, variational inequality problems represent a broadly encompassing tool for capturing a range of equilibrium problems arising in economics, engineering, and applied sciences (cf. [13]). This motivates us to extend the realm of computational problems to accommodate the class of misspecified monotone variational inequality problems, which is formally defined later in this section. By doing so, we may not only accommodate the problem , but also we can consider a far broader class of misspecified problems.

Given a set and , a single-valued mapping, then a variational inequality problem VI requires an such that for all More specifically, we consider the misspecifed variational inequality problem VI where :

| () |

In Subsections 3.1 and 3.2, we present extragradient and regularized first-order schemes, respectively, for misspsecified monotone variational inequality problems with strongly convex learning problems. Throughout this section, we make the following assumption on the learning function and map .

Assumption 12.

-

(a)

The function is differentiable, strongly convex with constant , and Lipschitz continuous in gradient with constant .

-

(b)

The map is monotone in and uniformly Lipschitz continuous in and with constants and , respectively:

3.1 Extragradient schemes

The extragradient scheme was first proposed by Korpolevich [30] and such approaches have been enormously useful in the solution of both convex optimization problems and monotone variational inequality problems [13] via constant steplength schemes. Subsequently, Nemirovski [31] proposed a prox-type method with a general distance function with convergence rate of , which is equivalent to extragradient scheme under a Euclidian distance function. In this subsection, we consider whether the extragradient framework can be extended to the regime of interest and propose a misspecified variant of the extragradient scheme:

Algorithm 3 (A joint extragradient scheme).

Given and a steplength ,

| (Extra) | |||||

| (Extra) | |||||

| (Learn) |

Unlike the standard projected gradient framework, the extragradient scheme requires two consecutive gradient steps with the same belief . Note that the proof of convergence follows along the lines of that provided by Facchinei and Pang [32], but with some care required to handle the extra terms arising from learning. We begin by presenting a supporting Lemma.

Lemma 15.

Proof.

By the projection property, we have that for any ,

Using above relation with and , we obtain

By expanding the terms on the right hand side, we have

| (27) | |||

| (28) |

where the second inequality is a consequence of adding and subtracting and is defined as . By the monotonicity of over , it follows that

and since , the above inequality can be simplified to Hence, by adding and subtracting in the above inequality, we obtain that

which implies

Using this relation in (28), we see that

By writing , we can expand as follow:

By combining the terms in the inner product with , we obtain

| (29) |

Through the addition and subtraction of terms, as follows:

Since and , the first term on the right hand side is nonpositive by the projection property. By leveraging this property and the Lipschitz continuity of in , we have

| (30) |

From the Lipschitz continuity of in , it follows that . By employing this bound and by substituting (30) in (29), the result follows.

∎

We now leverage this result in proving the convergence of the iterates produced by Algorithm 3.

Theorem 16 (Convergence of extragradient scheme).

Proof.

From Lemma 15, we have

where is any point in . By writing and using the triangle inequality, we obtain that

from By strong convexity of function , there exist a constant such that . By replacing this bound into the above inequality and then combining the similar terms, we get

| (31) |

To prove that the sequence converges to a point in , we make use of Lemma 5. To check that conditions of Lemma are satisfied, we first see that

In addition, satisfies the following for every :

Consequently, for all . Then, by Lemma 5, we have that (i) is a convergent sequence and (ii) . By (i), as where is not necessarily a point in . Since (ii) holds and by observing that , it follows that Consequently, we have that for some subsequence ,

This implies that is a point in . But since is a convergent sequence, the entire sequence converges to and the result follows. ∎

Remark: It can be observed that if , then we recover the standard bound on the steplength for extragradient schemes. While we do not analyze the rate of extragradient schemes, we believe that analogous rate statements may be possible, akin to those provided by Nemirovski [31].

3.2 Regularized schemes for monotone VIs

Consider a perfectly specified problem VI, where is a monotone map over a set and assume that denotes its least square norm solution. Consider the -regularized problem, denoted by VI, where is a positive constant and is an identity map. Since the map is strongly monotone as a consequence of the regularization, VI admits a unique solution. This motivates the exact Tikhonov regularization method that generates a sequence where solves VI, denotes the regularization at the kth iteration, and as . Under suitable conditions (see [33, 34, 10, Ch.12]) the sequence converges to as The standard structure of the Tikhonov regularization scheme requires obtaining exact or increasingly exact solutions of the subproblems VI, a relatively costly process. An alternative lies in taking a simple projected gradient step on the regularized map [26] and updating the regularization and steplength sequence at appropriate rates. This framework appears to have been first mentioned in [35] and further analyzed in [36] and is often referred to as iterative Tikhonov regularization and defined as follows:

where and are two vanishing sequences satisfying certain requirements. The reader can refer to [36] for more details. Inspired by this framework, we introduce a class of (Tikhonov) regularized schemes for the solution of misspecified monotone variational inequality problems:

Algorithm 4 (A regularized projection scheme).

Given an and and sequences and ,

| (Var) | |||||

| (Learn) |

In our analysis, we consider two auxiliary sequences and , defined as follows:

| (Tik) | ||||

| (Tik) |

Note that denotes the Tikhonov sequence associated with an estimate of , given by , and each iterate represents the solution of the regularized problem VI. The iterate can be viewed as a solution to a fixed-point problem, an alternative avenue for stating that is a solution of VI. Analogously represents a sequence in which each iterate is a solution to the regularized problem VI In what follows, we present a series of Lemmas that will be used to prove the convergence of the sequence to the least-norm solution of problem . The proof sketch is as follows: In Lemma 17, we relate with and show that as converges to , converges to . Lemmas 18, 19 and 20, when combined, show that as , the iterative Tikhonov sequence converges to the sequence , by first deriving the bound on and then showing that this bound goes to zero. Consequently, convergence of to the least norm solution will be immediate since we know that as and converges to the least norm solution of problem . We make the following assumptions on the set and also on the stepsize and regularization sequences:

Assumption 13.

The set is compact and , where M is a constant.

Assumption 14.

The following hold:

-

(a)

for all ;

-

(b)

and ;

-

(c)

;

-

(d)

such that , and , where .

Proof.

By the definition of , we have the following: Similarly, we have the following: By adding the two inequalities, we obtain the following:

By using monotonicity of and Lipschitz continuity of , this inequality can be recast as follows:

It can then be concluded that

where the second inequality is a consequence of the strong convexity of , by which converges to at a geometric rate . Using Assumption 14(d), it follows that ∎

We now develop a bound on in terms of the regularization parameters and and the estimates and .

Lemma 18.

Proof.

We begin by recalling that and satisfy the following inequalities:

Adding both inequalities, we obtain that

By adding and subtracting and , we obtain the following by using the monotonicity of in :

Consequently, by leveraging Cauchy-Schwartz inequality and by invoking the bound , we obtain the following bound:

Furthermore, can be bounded as follows:

The resulting bound on can be further simplified as ∎

Next, we proceed to derive a bound on the difference .

Lemma 19.

Proof.

We begin by bounding by leveraging the nonexpansivity of the Euclidean projector.

The Lipschitzian property of in uniformly in and the strong monotonicity of in uniformly in allows for deriving the following bound.

which can be simplified to where . By using the triangle inequality, the above inequality can be expanded as the following:

| (32) |

By combining (32) and Lemma 18, we obtain the following:

∎

We now leverage this bound to show that as .

Lemma 20.

Proof.

This requires the use of Lemma 19 and Lemma

1.

(i) Under Assumption 14(a), we have that

where the last inequality follows from Assumption 14(b). Hence, we obtain the following:

where the last equality follows from Assumption 14(b).

(ii) Under Assumption 14, we

obtain the following:

where the last inequality follows from Assumption 14(b) (since for all implying ) and the last equality is a consequence of invoking Assumption 14 (d) and (c). Hence, conditions of Lemma 1 are met. This completes the proof. ∎

We now prove the convergence of the regularized gradient schemes by showing that as .

Theorem 21 (Convergence of regularized scheme).

Proof.

A natural question is whether there is indeed a feasible choice of steplength sequences that satisfies the prescribed assumptions. In the next Lemma, we show that there exists a feasible choice of stepsizes that can satisfy requirements of Assumption 14.

Lemma 22.

Let and , where and . Then, conditions of Assumption 14 are satisfied.

Proof.

(a) It can be seen by the choices of and that

(b)

(c) If , we may express the required limitas follows:

Since this limit is of the form of , we may use L’Hôpital’s rule to express the limit as follows:

(d) We have that since the numerator converges to zero at a faster rate than the denominator. In addition, for the same reason. ∎

4 Numerical Results

In this section, we present some numerical results that support the converence and rate analysis provided earlier. In Section 4.1, we describe the economic dispatch problem which will form the basis of our computational investigations. On the basis of this problem, we consider the problem of misspecified costs (Section 4.2) as well as misspecified demand (Section 4.3).

4.1 Economic dispatch problem

A traditional economic dispatch problem [25] requires scheduling of generation to meet demand requirements in a least-cost fashion. The schedule has to abide by a set of capacity and ramping constraints and is given by the following optimization problem:

| (EDisp) | |||||

| subject to | (33) | ||||

| (34) | |||||

| (35) | |||||

| (36) | |||||

where and are number of generators and time periods, respectively. In addition, represents output power of generator at time , and is the generation cost function of generator , denotes load demand at period , is the capacity of generator , and and are the ramp-up and ramp-down limits of generator , respectively. Note that (33) is responsible for balancing generation with demand while (34) ensures that the power output of generators stay within the defined threshold. Constraints (35) and (36) are ramping rate bounds that simply ensure that any change in power output is within a defined limit over consecutive periods.

4.2 Misspecified cost functions

In what follows, we consider a setting where generation cost functions are misspecified quadratic functions modeled as , where is unknown. Suppose that for generator , we have a prior collection of samples denoted by , defined as where is a random variable with mean zero. Then, the misspecified parameter is learnt by solving the following least squares problem:

| Capacity | |||

|---|---|---|---|

In the first set of tests, we examine convergence of the constant and diminishing step length schemes proposed in Section 2.1.1. We consider a set of generators with misspecified generation cost function coefficients. The goal is to schedule the power output over time periods. The generators’ specifications are shown in Table 3. For each generator, a set of samples is collected for constructing the learning problem.

Figure 1 shows the behavior when using a constant steplength scheme, with and . Note that the Lipschitz constants for the gradient of optimization and learning functions are and , respectively, while the strong convexity constant of the optimization problem is . Hence, the prescribed stepsizes satisfy the required conditions. The scheme is also compared to the case when using the optimal in the cost coefficient, requiring no learning. Expectedly, we observe slower convergence when the cost function coefficients are misspecified. The figure on the right displays the trajectories when using diminishing step length scheme with . Figure 2 plots the convergence rate when using constant step size schemes and both the optimization and learning problems are strongly convex.

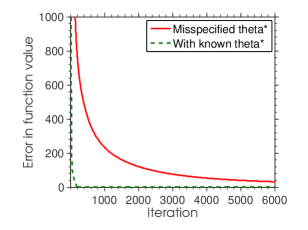

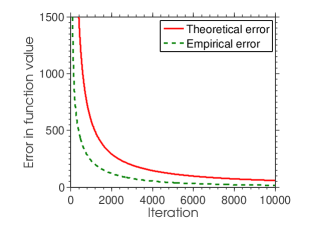

Figure 2 (l) compares the error in solution iterates of optimization problem for the cases of missipecified and known . As would be expected, when no learning is involved, we observe a linear convergence rate as shown in the dashed line. However, when learning is incorporated, the rate drops as shown by solid line. Figure 2 (r) compares the actual error in solution iterates of misspecified optimization problem to the theoretically predicted bound obtained in Proposition 4 and supports the validity of the bound.

| No. of generators | Constant step size, | Diminishing step size, | Averaging scheme, | |||

|---|---|---|---|---|---|---|

| 5 | - | - | - | - | - | - |

| 10 | - | - | - | - | - | - |

| 15 | - | - | - | - | - | - |

| 20 | - | - | - | - | - | - |

In Table 4, we examine the performance of the various schemes as the problem size grows. The implemented schemes are the constant step size scheme proposed in Proposition 2 , diminishing step size scheme proposed in Proposition 3 and averaging scheme stated in proposition 6. We compare the error in both the solution to the learning problem and the error in the function value associated with the optimization problem after a prescribed set of iterations. While constant steplength schemes perform well, the performance appears to be more affected by problem size in comparison with diminishing steplength or averaging schemes. This can be traced to the observation that as problem size grows, the Lipschitz constant of gradient of learn function increases as well and the employed step sizes for constant step size scheme are adjusted accordingly.

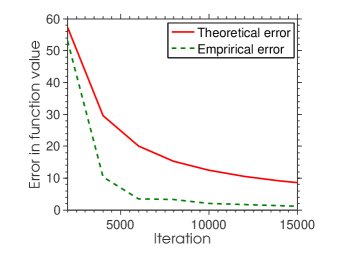

Figure 3 displays the performance when using the averaging schemes proposed in Proposition 6. With known , the rate of convergence in function values is of the order of where is number of steps. In Figure 3 (l), the error in function values is shown as a dashed line when is known and this rate drops by a constant factor when learning is involved as shown by the solid line. Figure 3 (r) compares the theoretical bound in Proposition 6 with the empirical error. As it is confirmed in this figure, the theoretically predicted rate represents an upper bound to the actual convergence rate of averaging scheme. Table 4 displays the errors obtained from running the averaging scheme for iterations with increasing number of generators.

To test the joint subgradient scheme(Algorithm 2), we consider a nonsmooth generation cost function that is the maximum of linear functions and is defined as below:

Figure 4 displays the result using the optimal constant step length scheme proposed in part (ii) of Proposition 14. Given a terminal iteration index , the optimal step length is first calculated using (24) and then the scheme is terminated after number of iterations. Figure 4 compares the resulted empirical error in function value of averaged point versus the theoretical bound. As shown in the figure, the empirical error is within the theoretical bound.

4.3 Misspecified demand

Suppose that demand vector is misspecified and may be learnt through a parallel learning process. We refer to the misspecifed problem as (EDisp) where denotes the misspecified demand. Suppose the linear inequality constraints of (EDisp) are given by

where , , and the cost function is given by . The first order conditions of this problem are necessary and sufficient and are given by

and is a vector of dual variables corresponds to the constraints set . The above conditions can be compactly stated as VI [13] allowing us to consider the use of the regularized and extragradient schemes developed in Section 3 for the solution of misspecified variational inequality problems. We consider a set of generators with known quadratic cost functions while the demand vector is unknown. A set of samples is randomly generated and the optimal demand is the solution to the following learning problem:

and , denote the set of samples. Since the variational problem is merely monotone, the solution set is multi-valued. In such settings, we use the gap function [10] as a metric of progress, which is analogous to the objective function in optimization. Given VI, associated gap function is defined as follows:

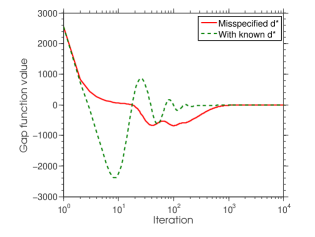

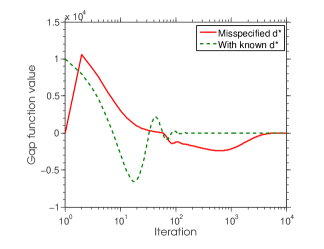

where Recall that solves VI if and only if . To allow for representing the gap function when , we use a modified gap function given by , which could be negative. Figure 5 (l) compares the trajectory of gap function value with learning (solid line) with the trajectory observed when is available. Note that in this problem, and and . In addition, we employ a constant step size of for the learning problem, given that the Lipschitz constant of is estimated to be . Expectedly, learning leads to a degradation in the convergence rate as compared with using the true demand . In Figure 5 (r), we examine the behavior of the misspecified extragradient scheme where and , and , respectively. Hence, the step sizes are fixed at and . Finally, in Table 5, we examine the error when the number of generators increases. We terminate the regularized and extragradient scheme after and iterations and we present the error in solution iterates of learning function as well as the gap function associated with the true problem. Since the extragradient scheme is a constant steplength scheme, its performance appears to be significantly better than the regularized scheme but the latter does not necessitate knowledge of system parameters.

| No. of generators | Extragradient scheme, | Regularization scheme, | ||

|---|---|---|---|---|

| G | G | |||

| 5 | - | - | - | - |

| 10 | - | - | - | - |

| 15 | - | - | - | - |

| 20 | - | - | - | - |

5 Concluding remarks

The field of optimization algorithms has predominantly focused on the resolution of optimization problems when the objective function and the constraint set are known with certainty. However, in settings complicated by large networked systems with streaming data, the resulting optimization problems are often corrupted by a misspecification, either in terms of the model or a prescribed parameter. We focus on the second case and examine how one may resolve this misspecification through a suitably defined learning process. More precisely, we formalize the setting as one where we have two coupled computational problems; of these, the first is a misspecified optimization problem while the second is a learning problem that arises from having access to a learning data set, collected a priori. One avenue for contending with such a problem is through an inherently sequential approach that solves the learning problem and utilizes this solution in subsequently solving the computational problem. Unfortunately, unless accurate solutions of the learning problem are available in finite time, it appears that sequential approaches may not prove advisable.

In this paper, we consider a simultaneous approach that combines learning and computation via gradient-based techniques. We make several contributions in this regard, broadly categorized within the realm of misspecified convex optimization and monotone variational inequality problems: (i) Convex optimization problems: First, in strongly convex regimes, it can be readily shown that constant steplength gradient schemes admit global convergence properties. In regimes where the strong convexity constants are unavailable, we prove that suitably defined diminishing steplength schemes are also shown to be convergent. Furthermore, we provide rate statements that demonstrate a degradation the linear convergence rate, a consequence of incorporating learning. Next, we consider problems where the computational problem is merely convex and observe that both constant steplength gradient and subgradient methods see no change in the overall convergence rate but instead display a similar modification in their rates given by . This term is scaled by the initial misspecification in and comprises of two terms, the first being a term that emerges from learning the true and decays to zero at a geometric rate while the second is an interaction term that takes its rate from the averaging structure. When both the computation and the learning problems are assumed to be merely convex with an additional weak sharpness assumption on the learning problem, both constant steplength and diminshing steplength statements may be provided; (ii) Variational inequality problems: In the context of monotone variational inequality problems, we present two sets of techniques. Of these, the first is a constant steplength extragradient scheme in which the steplength bound is modified to incorporate the initial misspecification, given by . Our second scheme develops an iterative (Tikhonov) regularized scheme that does rely on problem parameters and allows for recovery of the least norm solution of the misspecified variational inequality problem. Finally, preliminary numerical tests support the theoretical findings and remarkably the empirical convergence rates show a significant superiority to theoretical bounds, suggesting that improvements may be available.

Yet much remains to be understood about the realm of such techniques, For instance, to what extent does the introduction of learning affect the convergence rate in gradient methods as arising from Nesterov-type acceleration techniques? Furthermore, can be develop analogous rate statements for proximal and Lagrangian schemes and quantify the impacts from learning? Finally, can we extend this framework to other computational problems such as in the solution of Markov decision-making problems (MDPs)?

References

- [1] P. E. Gill, W. Murray, and M. H. Wright, Practical Optimization. Boston, MA, USA: Academic Press, 1981.

- [2] D. Bertsekas, Nonlinear Programming: 2nd Edition. Athena Scientific, Belmont, MA., 1999.

- [3] G. B. Dantzig, “Linear programming under uncertainty,” Management Sci., vol. 1, pp. 197–206, 1955.

- [4] E. M. L. Beale, “On minimizing a convex function subject to linear inequalities,” J. Roy. Statist. Soc. Ser. B., vol. 17, pp. 173–184; discussion, 194–203, 1955, (Symposium on linear programming.).

- [5] J. R. Birge and F. Louveaux, Introduction to Stochastic Programming: Springer Series in Operations Research. Springer, 1997.

- [6] A. Shapiro, D. Dentcheva, and A. Ruszczyński, Lectures on stochastic programming, ser. MPS/SIAM Series on Optimization. Philadelphia, PA: SIAM, 2009, vol. 9, modeling and theory. [Online]. Available: http://dx.doi.org/10.1137/1.9780898718751

- [7] A. Ben-Tal, L. El Ghaoui, and A. Nemirovski, Robust Optimization, ser. Princeton Series in Applied Mathematics. Princeton University Press, October 2009.

- [8] D. Bertsimas, D. B. Brown, and C. Caramanis, “Theory and applications of robust optimization,” SIAM Rev., vol. 53, no. 3, pp. 464–501, Aug. 2011. [Online]. Available: http://dx.doi.org/10.1137/080734510

- [9] T. Hastie, R. Tibshirani, and J. H. Friedman, The elements of statistical learning: data mining, inference, and prediction: with 200 full-color illustrations. New York: Springer-Verlag, 2001.

- [10] F. Facchinei and J.-S. Pang, Finite-dimensional variational inequalities and complementarity problems. Vol. I, ser. Springer Series in Operations Research. New York: Springer-Verlag, 2003.

- [11] J. C. Gittins, Multi-armed bandit allocation indices. Wiley-Interscience Series in Systems and Optimization, Chichester: John Wiley & Sons, Ltd., 1989.

- [12] H. Jiang and U. V. Shanbhag, “On the solution of stochastic optimization and variational problems in imperfect information regimes,” http://arxiv.org/abs/1402.1457, 2014.

- [13] F. Facchinei and J. S. Pang, Finite-dimensional variational inequalities and complementarity problems. Vol. I, ser. Springer Series in Operations Research. New York: Springer-Verlag, 2003.

- [14] G. C. Calafiore and M. C. Campi, “Uncertain convex programs: Randomized solutions and confidence levels,” Mathematical Programming, vol. 102, pp. 25–46, 2005.

- [15] M. N. Katehakis and A. F. Veinott, “The multi-armed bandit problem: Decomposition and computation,” Mathematics of Operations Research, vol. 12, no. 2, pp. 262–268, 1987. [Online]. Available: http://dx.doi.org/10.1287/moor.12.2.262

- [16] S. Agrawal, Z. Wang, and Y. Ye, “A dynamic near-optimal algorithm for online linear programming,” Operations Research, vol. 62, no. 4, pp. 876–890, 2014.

- [17] S. Agrawal, E. Delage, M. Peters, Z. Wang, and Y. Ye, “A unified framework for dynamic prediction market design,” Operations Research, vol. 59, no. 3, pp. 550–568, 2011.

- [18] Z. Wang, S. Deng, and Y. Ye, “Close the gaps: A learning-while-doing algorithm for single-product revenue management problems,” Operations Research, vol. 62, no. 2, pp. 318–331, 2014.

- [19] H. Jiang, U. V. Shanbhag, and S. P. Meyn, “Distributed computation of equilibria in misspecified convex stochastic Nash games,” http://arxiv.org/abs/1308.5448, 2013.

- [20] D. Bertsekas and J. N. Tsitsiklis, “Gradient convergence in gradient methods with errors,” SIAM J. on Optimization, vol. 10, no. 3, pp. 627–642, Jul. 1999. [Online]. Available: http://dx.doi.org/10.1137/S1052623497331063

- [21] A. d’Aspremont, “Smooth optimization with approximate gradient,” SIAM J. on Optimization, vol. 19, no. 3, pp. 1171–1183, Oct. 2008. [Online]. Available: http://dx.doi.org/10.1137/060676386

- [22] D. Olivier, G. François, and Y. E. Nesterov, “First-order methods of smooth convex optimization with inexact oracle,” Math. Program., Ser. A, 03/2013 2013.

- [23] I. Necoara and V. Nedelcu, “Rate analysis of inexact dual first-order methods application to dual decomposition,” IEEE Transactions on Automatic Control, vol. 59, no. 5, May 2014.

- [24] M. Schmidt, N. L. Roux, and F. R. Bach, “Convergence rates of inexact proximal-gradient methods for convex optimization,” in Advances in Neural Information Processing Systems 24, J. Shawe-Taylor, R. Zemel, P. Bartlett, F. Pereira, and K. Weinberger, Eds. Curran Associates, Inc., 2011, pp. 1458–1466.

- [25] D. S. Kirschen and G. Strbac, Fundamentals of Power System Economics. John Wiley & Sons, 2004.

- [26] B. T. Polyak, Introduction to optimization. New York: Optimization Software, Inc., 1987.

- [27] D. Bertsekas, A. Nedić, and A. E. Ozdaglar, Convex analysis and optimization. Athena Scientific, Belmont, MA, 2003.

- [28] H. Robbins and D. Siegmund, “A convergence theorem for non negative almost supermartingales and some applications,” in Optimizing methods in statistics (Proc. Sympos., Ohio State Univ., Columbus, Ohio, 1971). New York: Academic Press, 1971, pp. 233–257.

- [29] S. Boyd and L. Vandenberghe, Convex Optimization. New York, NY, USA: Cambridge University Press, 2004.

- [30] G. M. Korpelevich, “The extragradient method for finding saddle points and other problems.” Ekonomika i Matematischeskie Metody, vol. 12, p. 747–756, 1976.

- [31] A. Nemirovski, “Prox-method with rate of convergence O(1/T) for variational inequalities with lipschitz continuous monotone operators and smooth convex-concave saddle point problems,” SIAM J. on Optimization, vol. 15, no. 1, pp. 229–251, Jan. 2005.

- [32] F. Facchinei and J. S. Pang, Finite-dimensional variational inequalities and complementarity problems. Vol. II, ser. Springer Series in Operations Research. New York: Springer-Verlag, 2003.

- [33] A. N. Tikhonov, “On the solution of incorrectly put problems and the regularisation method,” in Outlines Joint Sympos. Partial Differential Equations (Novosibirsk, 1963). Acad. Sci. USSR Siberian Branch, Moscow, 1963, pp. 261–265.

- [34] A. N. Tikhonov and V. Arsénine, Méthodes de resolution de problèmes mal posés. Moscow: Éditions Mir, 1976, traduit du russe par Vladimir Kotliar.

- [35] E. G. Golshtein and N. V. Tretyakov, Modified Lagrangians and monotone maps in optimization, ser. Wiley-Interscience Series in Discrete Mathematics and Optimization. New York: John Wiley & Sons Inc., 1996, translated from the 1989 Russian original by Tretyakov, A Wiley-Interscience Publication.

- [36] A. Kannan and U. V. Shanbhag, “Distributed computation of equilibria in monotone Nash games via iterative regularization techniques.” SIAM Journal on Optimization, vol. 22, no. 4, pp. 1177–1205, 2012.