Diversification and Endogenous Financial Networks

Abstract

We test the hypothesis that interconnections across financial institutions can be explained by a diversification motive. This idea stems from the empirical evidence of the existence of long-term exposures that cannot be explained by a liquidity motive (maturity or currency mismatch). We model endogenous interconnections of heterogenous financial institutions facing regulatory constraints using a maximization of their expected utility. Both theoretical and simulation-based results are compared to a stylized genuine financial network. The diversification motive appears to plausibly explain interconnections among key players. Using our model, the impact of regulation on interconnections between banks -currently discussed at the Basel Committee on Banking Supervision- is analyzed.

Key words: Diversification; Financial networks; Regulation; Solvency; Systemic risk.

JEL Code: G22, G28.

The opinions expressed in the paper are only those of the authors and do not necessarily reflect those of the Autorité de Contrôle Prudentiel et de Résolution (ACPR).

1 Introduction

The behavior of financial institutions, namely banks and insurance companies, constitutes a paradox. On the one hand, they oppose one another in a competition to collect deposits as one may expect for firms in a common sector. In this perspective, the distress of one institution seems good news for the others since there is room for increasing market shares. However, on the other hand, financial institutions need to cooperate. For instance, the withdrawal of a bank from the short term interbank market means that a source of liquidity vanishes, triggering setbacks for other banks. In this case, one financial institution’s distress is definitely bad news for the other ones. Thus, even if they are in competition, banks cooperate, insurance companies cooperate and last but not least, banks cooperate with insurance companies. The last point has been ever more significant during the recent years. A support of this cooperation is the interconnections they develop between each other.

In a short-term view, interconnections mirror the resolution of the liquidity needs. As any other firms, banks and insurance companies face asynchronous in-flows and out-flows of cash. One solution is that every institution has its own cash buffer. Alternatively, institutions can create a liquidity pool by sharing their cash to mutualize the liquidity risk (Holmstrom and Tirole,, 1996; Tirole,, 2010; Rochet,, 2004). Allen and Gale, (2000) explicitly link the interconnectedness of banks to liquidity shocks. Besides the asynchronism of in-flows and out-flows, the liquidity risk is particularly salient since banks are exposed to runs (Diamond and Dybvig,, 1983) and operate large gross transactions in payment systems (Rochet and Tirole,, 1996). Indeed flows between institutions are not netted.

However, one may argue that this analysis is not specific to banks and insurance companies since every firm actually faces asynchronous in-flows and out-flows.

Liquidity concerns are not the only cause of interconnections between financial institutions.

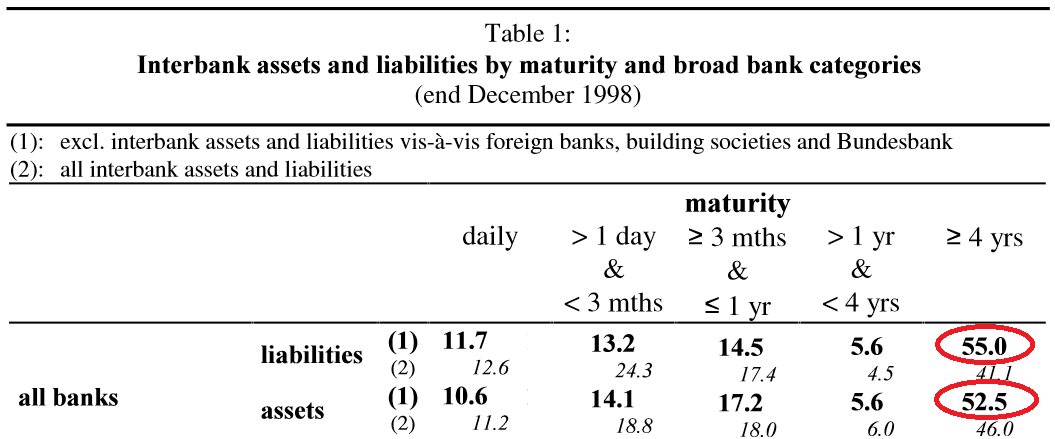

Moreover, there is evidence in the literature that banks are interconnected not only in the short term but also in the long run. For instance, according to Upper and Worms, (2004), half of German interbank lending is composed of loans whose maturity is over 4 years (see Figure 1). According to Table 1 in

Alves et al., (2013), interbank assets with residual maturity larger than one year account for about 50% of total interbank assets at the European level.333The existence of long-term interconnections, through loans or shares, is also reported for other countries such as Canada (see Table 3 in Gauthier et al., (2012)) or France (Fourel et al.,, 2013). These long term exposures cannot be explained by a liquidity motive since liquidity is a short term phenomenon. Other possible reasons are horizontal integration (share of a pool of customers via joint products), vertical integration (e.g. risk transfer between insurance and reinsurance companies), ego of top managers aiming at increasing their control of the market and last but not least diversification. Of course, in practice, the network formation stems from a combination of all these motives. However, for reasons explained further, diversification appears as a very important motive. Therefore, in this paper, we consider that these long-term exposures are accounted for by a diversification principle, in a sense that will be defined in the following.

The diversification principle is supported by the existence of various business models for banks and insurance companies. The diversity of institutions leads to a diversity of debts and shares available for the other institutions as assets. In the case of insurance companies, there is a clear-cut distinction between mutual funds and profit-oriented insurance companies. The banking sector regroups heterogenous institutions from mutual saving banks to commercial banks. Moreover, the bankassurance business model blurs the separation between banking and insurance activities. This variety can be explained by the different preferences of stakeholders or by historical patterns. Investors who have the same risk aversion gather and form an institution. This heterogeneity can also be linked to a specialization process. For instance, a mutual savings bank funded by farmers is very efficient in granting loans to farmers who in turn favor this bank since it provides the fairest interest rate. This auto-selection mechanism leads to a situation close to a local monopoly. We then understand that for a specific bank, getting interconnected to other institutions is a way to get access to their specific markets. Considering specific markets implicitly assumes that these are not perfectly correlated: for example retail differs from trading. Similarly, insurance companies also specialize in specific risk classes.444For instance, in the US health insurance sector, specialized institutions exist. The Federal Employees Health Benefits (FEHB) Program is dedicated to federal employees. Thus being interconnected to other insurance companies allows diversifying one’s risk portfolio. All this supports the fact that the diversification principle may explain long-term interconnections among banks and insurance companies.

In order to properly model banking and insurance activities, one has to keep in mind that

the banking and insurance sectors are characterized by a very specific production process as well as a heavy regulation. The core activity of a bank consists of the selection of profitable loans and in the management of the resulting maturity transformation. Banks screen potential entrepreneurs for reliable projects and fairly price the resulting interest rate charged. At the same time, they manage the maturity gap: loans to entrepreneurs are long-term assets whereas deposits and issued bonds constitute short-term debt on the liability side. Information is also key to the core activity of insurance (e.g. damage insurance): the insurer has to efficiently assess the riskiness of the potential policyholder and to deduce the corresponding premium. Strictly speaking the insurance company does not provide maturity transformation. However, its production cycle is reversed: it first collects premia and cushions losses when claims occur. The regulation of the banking and insurance sectors is crucial to maintain people’s confidence in the system. In order to avoid bank runs, it is necessary that depositors consider their deposit as safe. Likewise, if policy-holders are not confident in the capacity of the insurer to honor its commitments, they will make other insurance choices. A solvency ratio is imposed to banks and insurance companies: in the case of banks, the ratio compares the riskiness of granted loans with own funds, while for insurance companies, the ratio balances the riskiness of insured risks and the collected premia.

Our paper has two main objectives. The first objective is to test whether a diversification motive is a plausible cause for interconnectedness across financial institutions. To do so, we build a model where interconnections are endogenous choices of financial institutions resulting from the maximization of their expected utility. After deriving some theoretical and simulation-based features of the resulting network, we compare these features to those of a stylized financial network (benchmark) based on empirical evidence. The second objective is to fairly assess the impact of regulation on interconnections based on our model.

The cornerstone of this paper is the modeling of the endogenous balance sheet of a financial institution, especially interconnections. Endogenous networks have been intensively analyzed in sociology or socio-economics (for a survey, see Goyal, (2012) or Jackson and Zenou, (2013)). However, finance yields a new field of application. Usually, interconnections among financial institutions are considered as given, especially in applied papers (see among others Cifuentes et al., (2005), Arinaminpathy et al., (2012), or Anand et al., (2013)). Endogenous financial networks stem from the seminal paper by Allen and Gale, (2000). For instance, Babus, (2007) models interconnections across banks as the result of an insurance motive: interconnections represent a means of protection against contagion. More recently, Acemoglu et al., (2013) focus on the short-term interbank market and model the network formation in the case of risk-neutral banks being able to renegotiate their claims in a case of distress. Elliott et al., (2014) make a case of showing the incentives that may drive financial network formations. Important insights are brought by this strand of literature inspired by microeconomics and game theory analysis.555See among others Cohen-Cole et al., (2011), Gofman, (2012), Farboodi, (2014) or Georg, (2014). Nevertheless, in this field, financial institutions only compute their interconnections: the remaining elements of their balance sheet are completely exogenous. This assumption seems suitable in a short-term perspective but not anymore when considering long-term interconnections. Therefore, by including more endogenous balance sheet items than the sole interconnections, we distance ourselves from this strand of research. To the best of our knowledge, the unique paper that considers a complete balance sheet optimization (apart from the debt) is Bluhm et al., (2013). They propose a dynamic network formation with risk-neutral banks. Using a specific "trial and error" process, the authors first compute the volume of interbank assets (that corresponds to the network’s importance) and second its allocation (that corresponds to the network’s shape). The allocation is carried out using a matching algorithm based on the strict indifference of banks. In contrast, our paper considers heterogeneously risk-averse banks which explicitly get interconnected to specific counterparts. Last but not least, almost all papers only consider lending (or debt securities) whereas, based on Gouriéroux et al., (2012), our paper also considers shares. This feature cannot be neglected in a long run perspective since financial institutions can take cross-shareholdings.

The paper is organized as follows. Section 2 falls into two parts. First, the production process of banks and insurance companies and the regulatory constraints are described. Secondly, we introduce the financial network benchmark. Section 3 presents the theoretical results. After describing the optimization program of financial institutions, we show the existence of an equilibrium and discuss the conditions for its uniqueness. We show that interconnections are usually optimal for financial institutions. These theoretical properties allow to characterize the shape of the network stemming from a diversification motive. Therefore, we compare the shape of a genuine interbank network to a diversification-based one. In Section 4, we first present the computational methodology and the calibration choices. Then we show some simulation results which lead us to assess the proximity of the obtained network to the benchmark network both in terms of balance sheet volume and support of interconnections (debt securities or cross-shareholdings). Section 5 provides an analysis of financial interconnections with respect to financial regulation. Elaborating on Repullo and Suarez, (2013), we first show how to fairly analyze interconnectedness and then compare different regulatory frameworks. Section 6 concludes. All proofs are gathered in the Appendix.

2 Balance sheet structure and network benchmark

In this section, we first describe the economic setup which corresponds to the technology of financial institutions. We introduce the different elements of their balance sheet as well as the regulatory constraints. We then present the stylized network to be later used as a benchmark.

2.1 Bank and insurance business

Each bank has access to a specific class of external illiquid assets and each insurance company specializes in one specific class of risk. These classes can be interpreted as main banking (respectively insurance) activities such as, for instance, trading, commercial loans, mortgage loans, sovereign loans (respectively e.g. property insurance, liability insurance, life insurance).

The tight relationship between a specific class of assets (respectively risks) and a specific institution has to be interpreted as a consequence of costly portfolio management by investors followed by a specialization process. By portfolio management, we mean the screening process. For banks, that means selecting promising entrepreneurs to finance and offering a fair interest rate. In the case of insurance companies, it means organizing the mutualization of risks, i.e. finding the adequate premium with respect to the policyholder’s risk profile. The specialization process strengthens the efficiency of managing a specific portfolio. Due to auto-selection of customers, specialization triggers further specialization.

2.1.1 Asset side

Bank ’s specific asset book value is labeled , for (we consider financial institutions). This asset is some illiquid loan and therefore cannot be exchanged on a market. Thus, no market value can be defined and only its book value is considered in the following.

We denote and the net return of and its realization, respectively. The distribution function of the returns is denoted : . The corresponding density is denoted by . Banks have access to another external asset, denoted by . Its return, deterministic and assumed to be common to all institutions, is denoted . Here, is a very liquid and low-risk asset (for instance AAA bonds or S&P 500 shares), the management of which does not require high technical skills. In the following, will be assimilated to cash, which does not require any screening. We assume that insurance companies’ external assets are only composed of . Insurance companies are indeed assumed not to have the same capacity of selecting promising innovators as banks, and therefore do not own any specific asset.

Besides, Institution can buy shares or debt securities issued by Institution in proportions and , respectively.

2.1.2 Liability side

The liability side is composed of equity (that is brought by investors) and nominal debt, whose book values are respectively denoted by and for Institution . Since equity and debt securities will be traded on the the secondary market, it is necessary to introduce their market values, respectively denoted by and .

In the case of banks, includes different types of debts (deposits and bonds of various maturities) considered as homogeneous in terms of seniority.666For various seniority levels, see Gouriéroux et al., (2013). Banks issue debt along a common yield curve. In other words, bank debt securities are considered risky (the interest rate curve is above the risk free yield curve) but have a common degree of risk (the same rating, say). Despite this common feature, Bank chooses its own degree of maturity transformation . Let us denote by the average of maturities of all types of debts and by the maturity of the assets. Then, is defined as . For instance deposits can be seen as every day re-funded overnight loans by households to banks and therefore their maturity is equal to , yielding . On the opposite, a debt whose maturity equals the asset maturity corresponds to . Banks usually assume that their short-term debt will be rolled over. However, it is not always the case, especially during crises. If a bank is only funded by deposits (), it may happen that all depositors suddenly quit, causing a funding liquidity shock. The same can happen in the case of debt issued with bonds if investors decide not to roll over. In the extreme opposite case (), there is no possible liquidity shock (but there is no maturity transformation). Banking activity is precisely profitable due to maturity transformation since the interest rate corresponding to long term lending (asset side) is larger than the one corresponding to short term borrowing. In our model, the interest rate charged on the debt of Bank is deterministic, depends on and is denoted by .

In the case of insurance companies, the nominal debt mostly corresponds to technical provisions relative to the underwritten risks. Therefore, can no longer be interpreted as a degree of maturity transformation but as the mean severity of claims. Thus, we do not have necessarily anymore. Contrary to banks, the liability side of an insurer is stochastic. For instance, in line with standard ruin models (see e.g. Asmussen and Albrecher,, 2010), could be the parameter of the Pareto distribution in a claims model. Of course, the collected premia directly reflect the risk profile of the insurance contracts.

The balance sheet of Bank is represented at the initial date and the end date in Tables 1 and 2, respectively. The dates are represented by an upper-scripted index in parenthesis.

| Asset | Liability | ||||

|---|---|---|---|---|---|

| debt | |||||

| value of the firm | |||||

| external assets | |||||

| cash |

| Asset | Liability | ||||

|---|---|---|---|---|---|

| debt | |||||

| value of the firm | |||||

| external assets | |||||

| cash |

It is important to note that the equity and the debt of the other institutions (on the asset side) must be priced at the market value at . At time , the book value can be considered.

In line with the Value-of-the-Firm model (Merton,, 1974), the value of debt and equity at any date are linked through the following equilibrium equations

| (1) |

| (2) |

These 2 equations define a liquidation equilibrium. Equation (1) corresponds to the simple accounting definition of equity as the net value of assets over debts. Equation (2) is very similar to (1) and directly follows from Merton’s model: the debt value is the minimum between the asset value and the nominal debt.

Proposition 2 in Gouriéroux et al., (2012) states that these equations define a suitable liquidation equilibrium (see Proposition 5 in Appendix B.1). The cornerstone of our approach will consist in optimizing the balance sheet items of the financial institutions (apart from the equity which is exogenous). Proposition 5 states that whatever the balance sheet composition of each institution (whatever the values of , , , and satisfying Assumptions , and in Proposition 5), the network obtained can theoretically exist (under suitable unique values for and , ). In particular, our optimized network exists and thus the approach we develop in this paper can be carried out.

2.2 Regulatory constraints

In line with the usual Basel regulation (see e.g. BCBS,, 2011, Section I)777BCBS means Basel Committee on Banking Supervision., the solvency constraint for Institution is written

| (3) |

where and are regulatory parameters (risk weights) for external assets and inter-financial shareholdings and debtholdings, satisfying . The parameter relative to the external assets is specific to each institution whereas those relative to interfinancial assets are common within a specific sector (banking or insurance business). This constraint means that the equity must be higher than the risk-weighted assets and aims at ensuring the existence of a sufficient capital buffer to avoid losses for creditors in most cases.

Note that in the case of insurance companies, (3) corresponds to the Solvency I regulatory framework (see CEC,, 1979)888CEC means the Council of the European Communities., apart from the term corresponding to interconnections.

Since Solvency II is not implemented so far, we choose not to consider it in our modeling. Moreover, let us emphasize that the weights of banks differ from those of insurance companies. In the case of an insurer, the constraints on and can be relaxed to .

Even if we do not focus on liquidity shocks, we introduce a liquidity constraint:

| (4) |

with being some increasing function with respect to both variables which will be characterized further and satisfying . This constraint aims at ensuring a sufficient liquid assets buffer to face exposure to liquidity risk (maturity transformation in the case of banks and claims in the case of insurance companies) stylized by and . Note that this constraint is similar to the Basel III Liquidity Coverage Ratio (see BCBS,, 2013).

2.3 Summary of the optimization framework

In short, both banks and insurance companies select their balance sheet items under restrictions (class of assets for banks and class of risks for insurance companies) and regulatory constraints. Their business model is reflected through a size variable and an intensity variable: the size is the total credit granted for a bank and the total of individual risks covered for an insurance company, while the intensity is the degree of maturity transformation for a bank and the claims’ severity for an insurance company.

We emphasize that our modeling allows to take the specificities of banks and insurance companies into account in a unified way. The same parameters allow interpretation in terms of banks as well as of insurance companies. However, as we mentioned, the nature of the debt and that of the maturity are different when considering a bank or an insurance company. In the following, we will mainly focus on banks.

2.4 Network Benchmark

Our testing principle is to compare the network obtained through our modeling and a stylized network, so-called benchmark. In this part, we describe this stylized network along three dimensions. First, we provide the main aggregate items of a bank’s balance sheet. Thus, we will be able to check if, apart from interbank assets, the obtained balance sheet composition is close to a real one. Second, we focus on the network shape. This level provides a qualitative assessment of interconnections. Last, the size of interconnections along instruments in a typical banking network is described. This last level provides a quantitative assessment of interconnections. We restrict the analysis to interbank networks in industrial countries, typically the United-States, Canada or Europe. We identify four stylized facts that characterize an interbank network.

2.4.1 Main aggregate items of a bank’s balance sheet

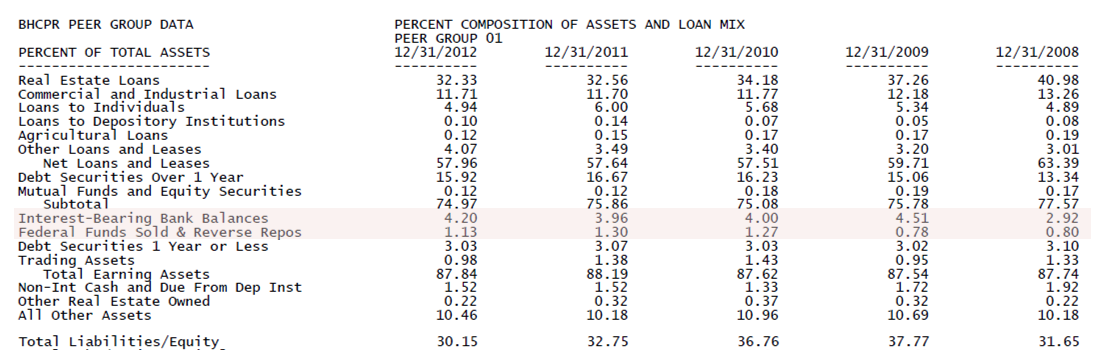

We consider the Bank Holding Company Performance Report Peer Group Data, published by the Federal Financial Institutions Examination Council, that provides the structure of asset and liability sides for banks above $10 billion (from 69 banks in 12/2008 to 90 in 12/2012). Figure 2 provides the composition of the asset side and the leverage for these banks. Corresponding informations are summarized in the following stylized fact:

Stylized fact 1: For a typical bank, the external assets () represent about 95% of its total assets while its equity () represents about 5% of its total assets.

Comment: interbank assets are mostly concentrated in highlighted lines.

2.4.2 Network shape

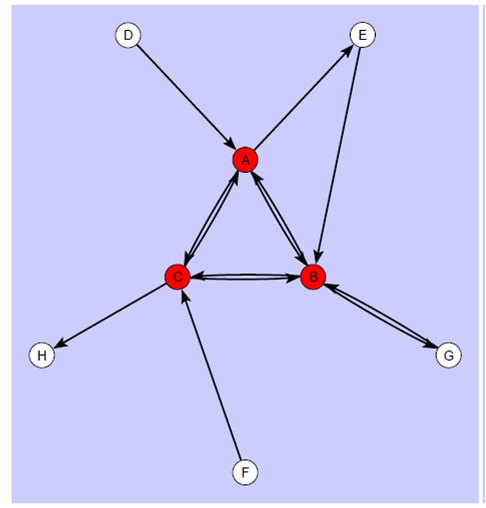

National interbank networks999See Furfine, (2003) for USA, Wells, (2002) for UK, Upper and Worms, (2004) for Germany, Lublóy, (2005) for Hungary, van Lelyveld and Liedorp, (2006) for the Netherlands, Degryse and Nguyen, (2007) for Belgium, Toivanen, (2009) for Finland, Gauthier et al., (2012) for Canada, Mistrulli, (2011) for Italy and Fourel et al., (2013) for France. are usually characterized by a core-periphery structure (Craig and Von Peter,, 2014). The core is composed of large banks highly interconnected. The periphery is composed of smaller banks which are connected to core banks only. Figure 3 represents a typical national interbank network. Note that at the international level, the core-periphery structure is much less clear among major banks (Alves et al.,, 2013). A complete structure seems more representative of the reality. These observations are summarized in the following two stylized facts:

Stylized fact 2: For a network composed of banks heterogeneous in size, a core-periphery structure is ideally expected. In other words, matrices and

present a block structure with a majority of zeros.

Stylized fact 3: For a network composed of large banks homogeneous in size, a complete structure is ideally expected. In other words, and have few zero coefficients.

2.4.3 Interconnections size and support

As mentioned above, total interbank assets account for about 5% of total assets. However, data concerning the relative importance of the different instruments are scarce. At the European level (at the end of 2011), according to Table 1 in Alves et al., (2013), credit claims (direct credit from one bank to another) and debt securities represent 90% of exposures. The remainder is composed of "other assets". For the 6 largest Canadian banks (as at May 2008), there is a factor 4 between exposure through traditional lending and exposure through cross-shareholdings, as reported in Table 3 in Gauthier et al., (2012).

Stylized fact 4: In the case of large banks, lending exposures represent a major part of exposures (between 80% and 90%). In other words, , where , and . However, cross-shareholdings can not be neglected.101010It is paramount to take the relative weight of share securities into account since they are more risky than debt/lending: shareholders lose as soon as the financial institution has losses while a debt holder is only affected if the losses of the financial institution are above its equity. For contagion analysis, cross-shareholdings cannot be neglected.

3 Model, theoretical properties and network shape

We model the network formation in two steps. The first one -dealt with in this section- concerns the modeling of the behavior of one institution, the state of the others being given. The aim is to determine how a financial institution defines its balance sheet and especially the interconnections knowing the main balance sheet elements of the other ones. For instance, how does a new bank get interconnected to previously existing ones? Or how does a bank adapt its balance sheet to modifications of the structure of others? The second step concerns the whole network formation using the modeling of individual behaviors and will be considered in Section 4.

Based on the framework introduced in the previous section, a one-period model is built. Banks are risk-averse agents optimizing their balance sheet structure for the shareholder’s interest at the initial date . The horizon is the final date .

The assumption that interconnections represent a long-term choice is a cornerstone of our analysis. Interconnections are not motivated by any liquidity features: they correspond to optimal choices in the long-run. Including liquidity-motivated interconnections that stem from daily work of Asset Liability managers, as well as the interactions between short-term and long-term interconnections, constitutes an ongoing work of ours.

A very important concern is the problem of reflexivity: how to technically manage the fact that the choices of financial institutions are interdependent? The main issue is that a complete Nash equilibrium modeling of the whole balance sheet structure -interconnections, external assets and debt- is clearly wishful thinking. It triggers difficulties, especially with respect to privately available information and anticipation formation. Note that in models with Nash equilibrium such as in Babus, (2007) or Acemoglu et al., (2013), choices are only taken at the level of interconnections: all the other components of the balance sheet are exogenous. This scope is arguably adapted in a short-term framework but is clearly unsuitable from a long-term perspective. In order to circumvent a complete game theoretic model, we adopt some simplifying assumptions backed up by practical considerations.

3.1 Modeling strategy

We choose an efficient, albeit simple strategy: each financial institution is assuming that the asset side of the other financial institutions is only composed of their external assets. This implies that the institution optimizing its balance sheet is not taking into account the future reactions of the other financial institutions. In this perspective, the optimization program is not strategic. Apart from simplifying the resulting optimization program, this strategy corresponds to sound assumptions for each financial institution and this for several reasons.

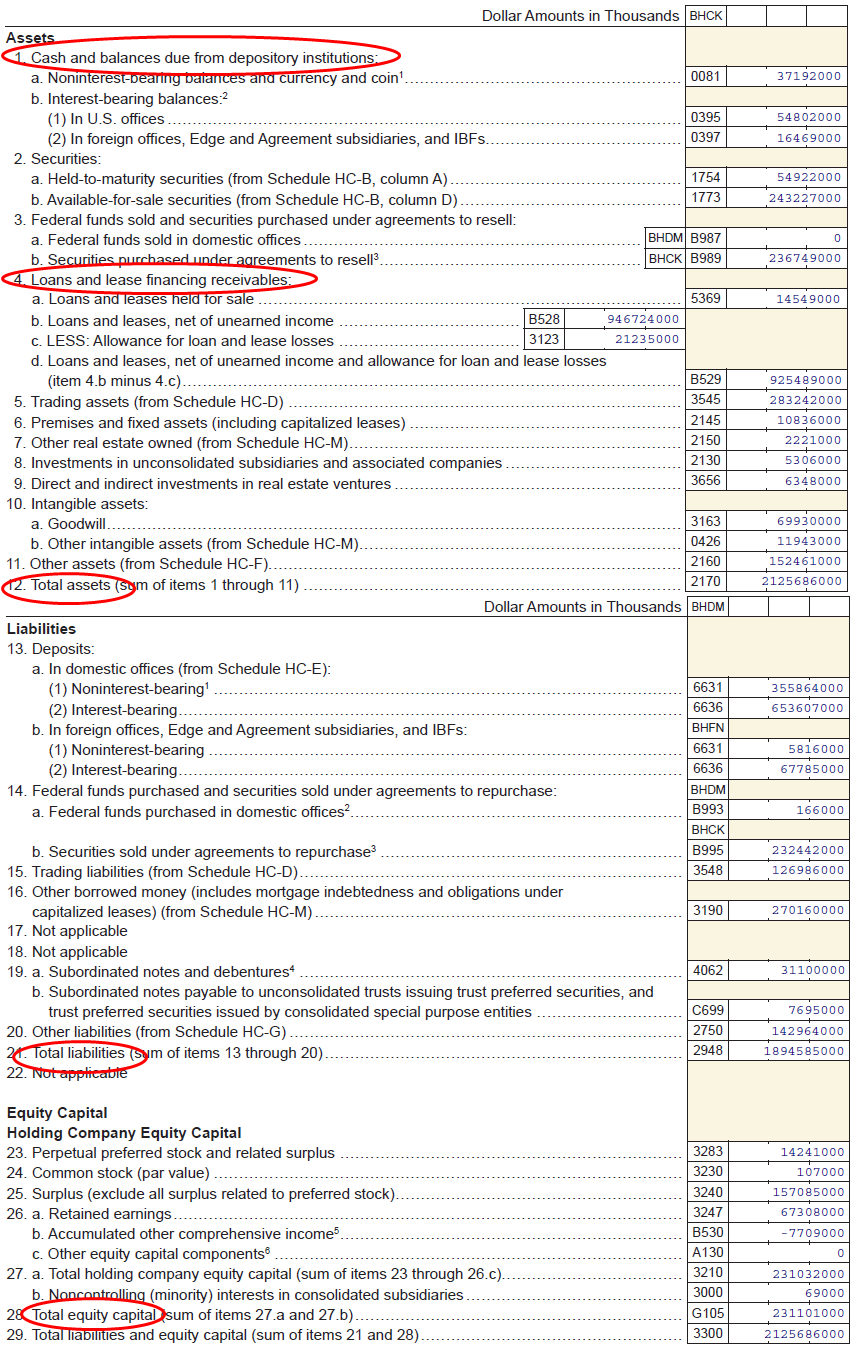

Firstly, the information set used in the optimization program is very close to the genuinely available one. Actually, bilateral exposures are private information. Publicly available information for any major financial institution are the detailed income statement and the balance sheet. For instance, return-on-asset, return-on-equity, cash, total interbank assets, loans on the asset side, debt and equity on the liability side are easily extracted from the public financial communication of firms or published reports (see Appendix A for an excerpt of the Consolidated Financial Statements for Bank Holding Companies (BHCs) of Bank of America published by the Federal Financial Institutions Examination Council111111http://www.ffiec.gov/nicpubweb/content/help/HelpFinancialReport.htm). Secondly, note that a large part of debt securities and shares are traded on the secondary market. Therefore, Bank cannot know exactly who its creditors and shareholders are: Bank knows its asset side but not the repartition of its liability side. The part of tradable shares is called the floating equity. By analogy, we call the floating debt the part of the debt traded on the secondary market.

Lastly, the absence of anticipation of reaction constitutes an approximation. As previously mentioned, there is no information on bilateral exposures. However, total interbank assets represent about 5% or 10% of total assets.121212For instance, on June 30, 2013, the proportion of interbank assets in the total assets is 3.4% for Bank of America, 13% for JPM, 8.40% for Citigroup 8.3% for Wells Fargo, according to the Consolidated Financial Statements for BHCs. Each bilateral exposure should be much smaller: 0.5% of total assets seems a reasonable upper bound. Therefore, when a new bank gets interconnected, the new interconnections do not significantly modify its balance sheet. It may trigger a reaction from its own counterparts but the effects can be neglected by comparison to the risk borne in the external assets for instance. As we will see in the simulation results, the reaction of counterparts only has a light influence on each institution, leading to a rapid stabilization of the network. This provides an indication that this assumption of absence of anticipation can be accepted as a first step towards building more realistic models.

Then this assumption allows us to derive in the next subsection some strong and tractable theoretical results.

3.2 Optimization program

Bank is managed for the benefits of its investors (i.e. shareholders) who are risk-averse and endowed with an initial capital . The risk-aversion of the investors of Bank is represented by a utility function .

We denote (respectively ) the floating equity (respectively debt) of Bank , for .

In line with our modeling strategy, we scale the total assets of Bank by .

These scaling factors compensate for the fact that we consider that the counterparts are not interconnected. Thus, we get the following approximation for the equity of Bank i at time :

| (5) |

If we denote by the expectation computed at time , the optimization program of Bank is

The constraint ensures the balance sheet equilibrium at the initial date. Note that this constraint allows the network resulting from our formation process (see Section 4) to satisfy (1) for each institution. The inequalities and are respectively the regulatory solvency and liquidity constraints presented in Section 2.2. , and stand for Balance sheet Constraint, Solvency Constraint and Liquidity Constraint, respectively.

3.3 Solution analysis

We define the position of Bank as the difference between its total assets (denoted by ) and its nominal debt. Therefore, at time , . If this difference is positive, the position is simply the equity; if the difference is negative, the position is the loss for creditors (while the equity is equal to zero in this situation). can be interpreted as the profit-and-loss.

The uniqueness of the solution usually requires the strict concavity of the objective function. The concavity of (where denotes the composition operator) is not a necessary condition since we could expect that the integration operation makes the expectation strictly concave even if is not strictly concave everywhere (see the Appendix for more details). Moreover, it would impose conditions on . Thus, we look for conditions on . Due to their limited liability, shareholders aim at maximizing the expected utility of the equity. The latter is defined as , making non-differentiable and introducing a level shape. An unfortunate consequence is that for standard utility functions , is not strictly concave and not even concave. Then our strategy is to approximate the real equity by a function to obtain the concavity. From an economic perspective, it is satisfactory to consider a transformation of the equity, as we will see in the following. Therefore, we decompose the analysis of into two steps. Firstly, we show that under mild assumptions there exists a solution (Theorem 1). Secondly, we transform the optimization program into a close one () for which existence and uniqueness are ensured (Theorem 2).

3.3.1 Analysis of the exact optimization program

Contrary to usual optimization programs where the total wealth is exogenous, increasing wealth by issuing debt is allowed in . Therefore, intuitively, the main difficulty in showing the existence of a solution is to show that Bank has no gain in issuing an infinite amount of debt. The argument is as follows. The equity is exogenously fixed. Therefore, implies that the total value of risky assets is bounded. Thus, starting from a specific amount of debt, the funding obtained by issuing more debt is necessarily invested in the risk free liquid asset. But since the interest rate charged on the debt is higher than the risk free rate, it is not profitable to issue debt to invest in liquid assets. In other words, banks are expected to invest in risky assets: granting credit is the core activity of banks.

All this goes to state the following proposition:

Theorem 1 (Existence of a solution to ).

If

-

the investors neglect interconnections among their counterparts;

-

the utility function is continuous and strictly increasing;

-

the distribution function is continuous. Moreover, the density is strictly positive on , for some ;

-

the yield curve, , is continuous and strictly higher than the risk free rate;

then there exists a solution to .

Assumption is both a technical assumption and a way to reflect the restricted information available for each agent. Assumptions , and are very common in the literature and not restrictive.

3.3.2 Analysis of the approximated optimization program

As stressed before, it appears impossible to establish the uniqueness for except in particular cases of simple models for . We therefore consider an optimization problem where the sole difference with is that the objective function is the expected utility of a strictly increasing transformation (denoted by ) of the position of Bank , . Considering the position directly makes things easier. However, it means not taking into account the limited liability which has some important implications. Indeed, it plays the role of a protection against extreme events for the managers: they are impacted by regular shocks but not by extreme ones. Some phenomena cannot be explained by macro-economic models ignoring limited liability. The optimization program is

With this specification, the level aspect of the limited liability is removed and the transformation ensures flexibility. For instance, with , one considers the usual maximization of the expected utility of profits. Alternatively, can be chosen to closely fit the design of the limited liability of shareholders while relaxing their complete indifference for loss magnitude. In the latter case, is very close to .

In short, the argument for the existence of a solution of is similar to the argument for the existence of a solution of . The uniqueness mainly stems from the strict concavity of the objective function we obtain by adjusting . However, the strict convexity of the constraints is necessary, imposing restrictions on the functional form of (see the proof for details). The following theorem provides the result regarding uniqueness:

Theorem 2 (Existence and uniqueness of a solution to ).

Under , , , and the extra assumptions:

-

the composition of the transformation function and the utility function is strictly concave: ;

-

the interest rate on debt is strictly concave: ;

-

the interest rate on debt satisfies ;

-

the function in satisfies

there exists a unique solution to in the following sense. If all control variables appearing on the asset side of Bank are fixed apart from one variable, denoted by , then there is uniqueness of the triplet (, , ).

Note that the result of Theorem 2 is equivalent to saying that the main balance sheet items are unique. Indeed, the value of total assets , the degree of maturity transformation and the debt are unique. Due to the high number of control variables on the asset side and the complexity of the problem, it seems impossible to prove the uniqueness of all control variables (see the Appendix for more details). The uniqueness for all control variables will be verified on simulations.

3.3.3 Approximation properties

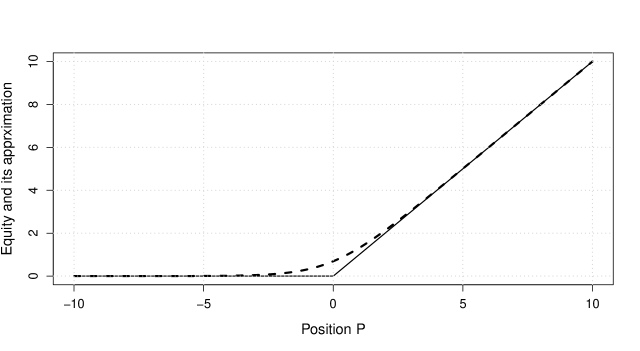

As mentioned before, the transformation function gives room for flexibility. Lemma 1 provides two specifications satisfying , corresponding respectively to the position and a very good approximation of the equity.

Lemma 1 (Some specifications of and ).

-

•

i) If , then reduces to .

-

•

ii) If , then is satisfied for the utility function .

The approximation corresponding to is shown in Figure 4. As we can see, the approximation error is very low. In the perspective of maximizing the utility, this function is probably even more satisfactory than the real equity. Indeed the utility of the equity is equal to zero whatever the position if the position is negative. In reality, one may think that the bank’s managers prefer a light insolvency situation to a large one, for example for the sake of reputation. It is be difficult to find funding to build a new project after letting an institution in a state of large insolvency. Our approximation function is strictly increasing and therefore takes this aspect into account. This is especially true for position values not too far away from the insolvency point.

Lemmas 2 and 3 provide a specification for the interest rate curve and the function appearing in , respectively satisfying and .

Lemma 2 (Specification of function ).

An interest rate curve of the form

| (6) |

satisfies .

Lemma 3 (Specification of function ).

The function defined by

satisfies .

3.3.4 Choice

Previous theoretical results provide different suitable specifications (especially of the function ) leading to a unique solution of the optimization program. In order to clarify the presentation, let us make a clear recommendation of choice. The following result is directly derived from Theorem 2 and Lemmas 1, 3 and 2.

Corollary 1 (Existence and uniqueness to a solution of a specific optimization program).

Additionally to , let us consider:

-

a logarithmic utility function

-

the following approximation of the limited liability of shareholders:

-

the following liquidity constraint:

-

the following interest rate curve:

Then, the associated optimization program has a unique solution.

To conclude this section, let us emphasize that all parameters and variables required to perform the optimization can be obtained via publicly available data.

3.4 Optimal interconnections

Previous theoretical results ensure that the bank’s maximization program has a (unique) solution. However, we did not characterize this solution, in particular the interconnections. In this part, we show that under some conditions, it is optimal for a bank to get interconnected. In this section, in order to simplify the presentation and to explain the main features, we do not take into account the control variables and , as well as the liquidity constraint .

In order to start, let us consider a simplified case of a portfolio composed of a quantity and a quantity of assets having respectively random variables and as gross returns, under a solvency constraint.131313For the sake of simplicity, the product of the complete program has been simplified into . The penalization weights are respectively and . The corresponding optimization program is

The Karush, Kuhn and Tucker (KKT) Theorem (Karush,, 1939; Kuhn and Tucker,, 1951) allows to derive the following proposition.

Proposition 1.

For the sake of simplicity, we denote . Under the condition

the optimal is different from 0.

This shows that under the condition that the derivative of the expected utility with respect to (relative to its corresponding weight) is higher than the one with respect to , the optimal is strictly positive. Proposition 1 does not provide the solution but gives an indication that interconnections can be strictly positive under some conditions. This result can be generalized to a higher number of assets. Note that this illustrative program does not contain any equality constraint. However, such a constraint can be trimmed by replacing one control variable in function of the others. That reduces the problem’s dimension. This point will be further detailed in the following.

Due to the high complexity of our optimization problem (high dimension and high number of constraints), the KKT conditions are very numerous and therefore it seems impossible to derive the solution in a closed form. We decompose the analysis

in different steps. We first consider a risk-neutral agent maximizing the value of its portfolio without limited liability. Secondly, we consider the case of a risk-averse agent and finally the limited liability is taken into account.

Risk-neutral agent without limited liability:

In the risk-neutral case, the utility function is the identity function.

Therefore, we can consider the following optimization program:

where is the equity value (book value) of another institution at time and is the equity value (market value) of this institution at time .

By using the same type of argument as in Proposition 1, it is easy to show that if or , then

-

•

if , the unique solution is ;

-

•

if , the unique solution is ;

-

•

if , the solution is not unique.

Therefore, due to the solvency constraint, a risk-neutral agent only invests in the asset having the highest return with respect to its specific regulatory weight in the solvency constraint.

Let us now consider the case where a limit to the availability is introduced: the constraint is replaced by . In this case, if , . Therefore, if , investing all in does not bind the solvency constraint. In this case (and if ), an investment in completes the portfolio. This result can be easily generalized to the case of institutions and where it is possible to invest in the debt of the other institutions. This is done in the following theorem.

Theorem 3.

Let us consider the following optimization program:

To find this problem’s solution, let us sort in decreasing order the following returns (relative to their penalty weight): , (), (). The optimal solution consists in investing as much as possible in the asset having the highest return with respect to its regulatory weight. When this asset is not available anymore, it is better to invest as much as possible in the second one, and so on. This is repeated until the solvency constrained is binding.

Risk-averse agent without limited liability

A risk-averse agent aims at decreasing the variance of its portfolio. To this purpose, it is necessary to diversify. Therefore, in this case, we can expect an investment in many assets, contrary to the "binary" investment described previously. This is confirmed by numerical experiments.

Agent with limited liability

In the previous considerations, we did not take into account the limited liability as well as the fact that equity and debt have very different features. Therefore, we could not see the implications of the fact that the and the are related to very different instruments. To pinpoint these implications, let us consider a stylized set-up with two banks. One can identify four situations in which Bank 1 (or 2) is either solvent or in default. Table 3 reports these 4 states. Let us focus on the impact of limited liability for Bank 1. We assume that Bank 1 builds interconnections with Bank 2 anyway (for example in order to reduce its variance) and we discuss the distribution among shares and debt securities.

| Bank 2 in default | Bank 2 solvent | |

|---|---|---|

| Bank 1 in default | ||

| Bank 1 solvent |

The expected utility of Bank 1 is written as follows

where is the probability of being in state and the associated payoff for Bank 1. Due to limited liability, . Thus

In the state , Bank 2 defaults, meaning that its equity is equal to zero. It is therefore more interesting to invest in its debt. In the state , Bank 2 is solvent. Thus, if the equity of Bank 2 has a higher return than its debt with respect to their regulatory weights, Bank 1 prefers investing in the share securities of Bank 2, thus increasing the . If the correlation between the external assets of both banks is highly positive, both banks are likely to be solvent and to default simultaneously. That means that is very low, giving: . In this situation, Bank 1 prefers investing in share securities. On the contrary, if the correlation between the external assets of both Banks is highly negative, Bank 2 is likely to default when Bank 1 is solvent. In this case and Bank 1 prefers investing in debt securities.

It is important to understand that the asymmetry between the cases and is due to the limited liability feature. Indeed, let us assume that Bank 1 has no limited liability and thus is not indifferent to losses. If is highly positive, . In state , Bank 2 defaults and it is better to invest in its debt whereas in state , it is better to invest in its shares. Therefore, it can be appropriate to invest in both instruments and thus the asymmetry disappears. The same happens for a highly negative .

However, keep in mind that this set-up is too minimal to show all the implications of the limited liability.

3.5 Cost of funding

In the considerations of Section 3.4, we assumed that the agent owns a sufficient amount of wealth to invest until the solvency constraint is binding. However, the capital is very low compared to the total assets to invest (due to the regulatory weight values). Thus, once the total capital has been used, the institution must raise debt in order to continue to invest. Returns of shares and debt securities must be netted by the cost of funding. To make the investment attractive (in terms of net returns), the cost of raising debt should be lower than the returns of shares and debt securities.

Let us now state some results about the returns of investments in shares and debt securities issued by other institutions, compared to their funding cost. For the sake of simplicity of the interpretation, before stating the result for general functions and , we propose a result in the case where and are the identity functions. It corresponds to the case of a risk-neutral institution maximizing its position .

Proposition 2 (Returns against opportunity cost, in the case of a risk-neutral institution maximizing the expectation of its position).

-

The expected return of a share issued by Bank is larger than the cost of funding of Bank if and only if

(7) where , and is the marginal density of the net return of the external asset of Bank .

-

The expected return of the debt issued by Bank is higher than the cost of funding of Bank if and only if

where

Proposition 3 (Returns against opportunity cost, in the general case of an institution maximizing the expectation of the utility of its equity).

-

•

The expected return of a share issued by Bank is larger than the cost of funding of Bank if and only if

where

where

-

•

The expected return of the debt issued by Bank is higher than the cost of funding of Bank if and only if

where and has been defined above.

Equation (7) corresponds to the fact that . Note that in this formula, the return of only Bank matters. It can be beneficial for Bank to increase its participation in Bank if the return on equity of Bank is higher than the interest rate that Bank must pay for its debt.

In the general case, the same type of inequality as (7) is obtained. However, it takes the marginal utility (up to function ) into account via . For interpretation purpose, let us assume that . For a given value of , the algebraic gain of increasing the participation must be weighted by the marginal utility, which depends on the returns of all institutions. Integrating this marginal utility with respect to all returns apart from yields the term . The risk aversion of Bank is embedded in the term .

The same type of argument applies in the case of the debt.

3.6 Testing of the diversification motive: the network shape

Let us now compare the consequences of Theorem 3 and Stylized Facts 2 and 3 on the network shape, and discuss the impact of risk-aversion and limited liability.

A risk-neutral bank with unlimited liability gets interconnected to others by strict mechanical behaviors: it seeks sequentially for the highest returns until binding the solvency constraint. Consequently, the network shape is very structured and directive since everyone gets interconnected in the same direction. Thus, in such a case, there is no general shape.141414Nevertheless, with a particular set of returns, a star network can occur. In other words, with risk-neutral banks and unlimited liability, the diversification motive cannot provide interesting results.

In the case of risk-averse banks, the interconnections tend to shape a complete network. Institutions carry out a diversification to decrease the variance, in addition to their aim of obtaining higher returns. Note that a diversified portfolio has a lower variance than a concentrated one.151515If and are two random variables with mean , variance and correlation , then

whereas . Therefore, even if all institutions have similar returns, it can be beneficial to get interconnected. To significantly benefit from the diversification, the variance reduction must be high enough: situations where the specific assets are not almost non-risky and/or where the correlation is negative are prone to yield a complete network structure. These findings will be confirmed numerically in the next section. The limited liability feature can modify the balance between shares and debt securities.

When considering risk-averse banks, the diversification motive generates complete financial networks, such as those usually observed among major institutions. Therefore, we cannot rule out diversification as explaining interconnections between key financial players.161616Note that our approach has no clue on the relevance of the other motives mentioned in Introduction. We simply show that diversification provides consistent results with empirical observations.

4 Network formation and simulation results

In this section, we derive simulation results in order to assess the relevance of the diversification motive for the financial network formation. First, we present the specification that we use and our calibration strategy. Second, we develop a network formation process taking advantage of the strong and tractable theoretical results obtained in the previous section. Then, optimal choices for one financial institution and regarding the whole network are analyzed.

4.1 Specifications

For the sake of simplicity, two banks are considered, i.e. . Each institution is endowed with a capital amount of , i.e. . Both institutions have as utility function. An initial capital of implies that the equity value at the optimization horizon is about . Therefore, the objective function is close to be linear over the most likely area, meaning that the banks are only slightly risk-averse.

In order to properly understand the main features of our model, we exclude and from the control variables. The interest rates paid by the two financial institutions, denoted by and are therefore fixed. Moreover, the risk-free interest rate is set to zero: .

Finally, note that the expectations are computed using Monte-Carlo techniques; simulations ensure a good precision.

4.2 Calibration strategy

The gross returns on external assets follow a bivariate log-normal distribution:

| (8) |

In order to calibrate the mean parameter, we consider the income statement in the Consolidated Financial Statements for BHCs (reporting form FR Y-9C) for banks over $10 billion. Between 12/31/2010 and 12/31/2012, the (annual) net income varies from 0.51% to 0.71% of the total assets. We round this value, considering that on average the net income of our banks is equal to 1%. Over the same period, the interest expenses represent between 0.74% and 1.07% of the total assets.171717In this paper, we consider that the total assets are equal to the earning assets and to the average assets. We basically consider that the cost of debt ( and ) varies between 0% and 1%. Finally, the expected return of the external assets for Bank is equal to , where is the Bank ’s ratio of debt over total assets. For the variance parameter, a probability of default of 0.1% is in line with the current rating of major banks. We combine the informations relative to the net income and the probability of default to compute the parameters and (see Appendix E for details). The parameter lies between -0.9 to 0.9. A negative can be interpreted as a sign of competition between the two banks or as the fact that banks operate in different markets (or geographical areas). Meanwhile, a positive could be interpreted as an underlying common factor affecting both banks.

We consider the Basel 2 regulation. This regulation does not provide a unique set of values for the risk weights , and . If the external assets correspond to a retail activity (i.e. loans to households), loans to unrated firms (i.e. small firms) or quoted shares, the required capital is equal to 6%, 8% or 23.2% of the total exposure, respectively. For debt securities issued by banks, the required capital is equal to 1.6% (when AAA or AA rated) or 4% (when A rated). Lastly, as discussed in Repullo and Suarez, (2013), there is a factor between the regulatory capital and the (accounting) equity, that varies from 1 to 2. For the sake of simplicity, we consider that the regulatory capital is either equal to the equity or to a half of the equity. Bottom line, we have 8 possible sets of risk weights.

4.3 Discussion about the pricing of shares and debt securities

Recall that the position of Bank 1 at time is as follows if Bank 2 is solvent:

| (9) |

The terms and are respectively the market values of the share securities and debt securities issued by Bank 2 at time . In a complete market and with the usual assumptions, the price of an asset would be the discounted expected payoff under the risk-neutral probability:

where denotes the available information at time . Since , appears as a call option whose underlying is and whose strike is . However, since is the price of an illiquid asset, it is difficult to argue that there exists a unique probability (the risk-neutral probability) that makes a martingale. Therefore, we choose to consider that the price is the discounted expected payoff under the physical probability. The corresponding prices and are given in the following proposition.

Proposition 4.

If we assume that , then the expected equity and debt values of Bank are

where , and is the distribution function of the standard Gaussian variable.

In order to understand some implications of our pricing choice, consider a situation where all returns are deterministic and . In such a framework, we have

Therefore, injecting these prices in (4.3), we obtain

| (10) |

Generally, we have , meaning that the factors of and are negative and thus that the net yields on shares and debt securities are negative. Therefore, for a risk-neutral agent (i.e. not interested in variance reduction), it would not be optimal to invest in shares and debt securities. That stems partly from the fact that we have priced these instruments using the physical probability. Under the latter probability, the shares and debt securities yield in average the risk-free rate. This feature could of course be challenged. Note that we should pay attention to the interpretations based on (4.3) since (4.3) only gives the expression of the position in a very simplified case. Equation (4.3) must only be considered as an indication.

Contrary to the share and debt security prices, the initial value of does not take the future returns into account. As we already mentioned, is an illiquid asset that cannot be exchanged on the market. Therefore, the assumption of absence of arbitrage is not necessarily satisfied and we price using its book value. Since generally , the specific asset provides a positive return. This is logical since getting positive returns via maturity transformation constitutes the core business of banks. However, in the pricing of , we consider the future returns of . This asymmetry can be discussed but it is difficult to find an ideal solution given the close link between a market asset () and an illiquid asset () in our model.

4.4 Methodology for the network formation

The optimization programs and presented in Section 3 allow computing the balance sheet of an institution, knowing the state of the others. Here the aim is to build a complete network using this individual optimization program. To this purpose, we operate in a sequential way until an equilibrium in the network is reached.

We propose to use an iterative game. At each step, one institution optimizes its balance sheet taking into account the state of the network obtained at the previous step. Thanks to Corollary 1, there exists only one network at each step. The procedure is as follows181818Note that this formation process can be applied in the general framework of Section 3 but is here presented using the previously mentioned specification.:

-

1.

Bank optimizes its balance sheet on and . Quantities and are forced to be equal to zero since at the initialization step, Bank ’s balance sheet is totally unknown;

-

2.

Bank optimizes its balance sheet on , , and given Bank ’s balance sheet from step 1;

-

3.

Bank optimizes its balance sheet on ,, and given Bank ’s balance sheet from step 2. and are optimized for the first time;

-

4.

Bank optimizes its balance sheet on , , and given Bank ’s balance sheet from step 3;

-

5.

Bank optimizes its balance sheet on ,, and given Bank ’s balance sheet from the previous step;

-

6.

and so on.

For further details, see Appendix D.

Theoretically, this procedure may be endless. However, in less than 10 steps, the variations of the control variables from one step to the next are lower than 1% and we consider that the final situation constitutes an equilibrium. Moreover, if we accept the numerical argument for the existence of the limit-network, we can affirm its uniqueness. Indeed, if at each step the network is unique, then its final state is necessarily unique. It is interesting to note that this method is inspired by the classical methodology used to determine a Nash equilibrium (in the sense that no institution has any interest in deviating from its current state). However, further investigations would be required to know if the network obtained by our method effectively corresponds to a Nash equilibrium.

Last but not least, it is important to check that the obtained network is consistent in the sense that it satisfies (1) and (2). Firstly, at time , all banks considered in the network are solvent; otherwise they would disappear from the network. That means that the initial debt equals the contractual one: . Therefore, (2) is automatically satisfied for each institution. Moreover, at each step, being a constraint of the optimization program, (1) is satisfied for the bank optimizing its balance sheet. If preliminary, this step has impacts on the other banks’ balance sheets and (1) is not exactly satisfied anymore for them. Nevertheless, after some iterations, the network does not evolve from one step to the next (due to the convergence), implying that (1) is satisfied for all institutions. These two points show that the obtained network is actually consistent.

This sequential algorithm could appear a little artificial but it is actually close to what happens in reality. An example of a real formation process of a network is as follows:

-

1.

Consider an initial situation where there is no bank;

-

2.

A first bank, denoted by , is created during year . Since there are no other banks, there are no possible interconnections. Thus, optimizes and . On January 1st of year , publishes its balance sheet;

-

3.

Imagine that on January 3rd, a second bank is created. knows and and then can solve the optimization program to determine , , and . Once proportions and have been determined, can buy on the secondary market shares and bonds issued by in these proportions;

-

4.

On June 1st, and publish their balance sheets (apart from interconnections). Since the balance sheet of did not evolve since January 1st, has no new optimization to carry out. On the other hand, discovers for the first time informations relative to : and . Then optimizes its balance sheet and thus obtains , , and . can buy on the secondary market shares and bonds issued by ;

-

5.

On January 1st of year , balance sheets of and are published. The balance sheet of did not change and thus has no optimization to do. On the other hand, must adapt to the new balance sheet of ;

-

6.

and so on.

After such iterations, one may think that there is convergence to an equilibrium in the network. Balance sheets of and do not evolve a lot from one step to the next.

4.5 Simulation results about the optimal choice for one institution

Let us here focus on the second step of the iterative game where Bank 2 optimizes its whole balance sheet (knowing the choice of Bank 1 at step 1). We assume that Bank ’s external assets are equal to 10. We present the sensitivity of the optimal choices of external assets , nominal debt and interconnections and , with respect to the regulatory parameters and correlation . Our computations were carried out under various debt-issuing conditions (not costly with , both costly with and only one costly with ) and we observe that the results are independent of these conditions. In each set-up, we consider the 8 sets of risk-weights and we let the correlation parameter vary between and .

The corresponding results are summarized in Table 4. First, we observe that interconnections based on debt securities are never used. A direct consequence is that the risk weight on debt, , has no impact on the balance sheet and thus does not appear in Table 4. Second, interconnections based on share securities are used only when the correlation is lower than -0.3 (independently of the interest rates) and when the associated risk weight is equal to 23.2%. They linearly decrease from about 45% to 0% between and . Third, the solvency constraint is binding. The optimal external assets represent about . The last row-block displays the ratio of interbank assets over the total assets: when interconnections are present, their proportion in the total assets is in line with the stylized facts.

These results could be interpreted as follows. First, the bank plays its core business: it invests as much as it can in its external assets. Then, if the regulation is not too strict and if the competitor’s results are sufficiently anti-correlated, the bank opts for diversification: it slightly lowers its external assets to buy share securities issued by the competitor. Debt securities are not used since their net returns are negative (as a consequence of the pricing specification described in Section 4.3) and "nearly" deterministic (due to the low probability of default).

| 23.2% | 6% | 14 | 15 | 16 | |

| 23.2% | 8% | 11 | 12 | 11 | |

| 46.4% | 12% | 8 | 8 | 8 | |

| 46.4% | 16% | 6 | 6 | 6 | |

| 23.2% | 6% | 45 | 25 | 0 | |

| (%) | 23.2% | 8% | 45 | 25 | 0 |

| 46.4% | 12% | 0 | 0 | 0 | |

| 46.4% | 16% | 0 | 0 | 0 | |

| 23.2% | 6% | 0 | 0 | 0 | |

| (%) | 23.2% | 8% | 0 | 0 | 0 |

| 46.4% | 12% | 0 | 0 | 0 | |

| 46.4% | 16% | 0 | 0 | 0 | |

| 23.2% | 6% | 3.1 | 1.6 | 0 | |

| (%) | 23.2% | 8% | 3.9 | 2.0 | 0 |

| 46.4% | 12% | 0 | 0 | 0 | |

| 46.4% | 16% | 0 | 0 | 0 |

4.6 Iterative game results

The iterative game reaches an equilibrium in less than 5 steps. The features pictured in the analysis of the behavior of one institution are still present. Especially, results are robust to the debt-issuing conditions.

Both institutions have the same balance sheet, whose composition is given in Table 5. Results are very similar to those for one institution only (Table 4). In particular, the proportion of interbank assets in the total assets is in agreement with the sylized facts. Note that for and , the values of and are close to . However, we have reported since such low values do not have any economic meaning.

Let us state that these results have been obtained using , in order to avoid numerical instability. Indeed, if the values of become too large, it makes no sense anymore to assume that the asset side of the other banks is only composed of their external assets.

| 23.2% | 6% | 15 | 15 | 16 | |

| 23.2% | 8% | 11 | 12 | 12 | |

| 46.4% | 12% | 8 | 8 | 8 | |

| 46.4% | 16% | 6 | 6 | 6 | |

| 23.2% | 6% | 70 | 45 | 16 | |

| (%) | 23.2% | 8% | 60 | 35 | 6 |

| 46.4% | 12% | 0 | 0 | 0 | |

| 46.4% | 16% | 0 | 0 | 0 | |

| 23.2% | 6% | 0 | 0 | 0 | |

| (%) | 23.2% | 8% | 0 | 0 | 0 |

| 46.4% | 12% | 0 | 0 | 0 | |

| 46.4% | 16% | 0 | 0 | 0 | |

| 23.2% | 6% | 3.2 | 2.3 | 1 | |

| (%) | 23.2% | 8% | 3.6 | 2.4 | 0.5 |

| 46.4% | 12% | 0 | 0 | 0 | |

| 46.4% | 16% | 0 | 0 | 0 |

4.7 Testing the diversification motive

Regarding the capacity of the diversification motive to account for interconnections, the previous results provide a quantitative assessment completing the qualitative arguments developed in Section 3. The key result is that when returns on specific assets are anti-correlated, diversification leads to interconnections with reasonable size in terms of proportion of the total assets. However, debt securities are never used, meaning that interconnections are only supported by share securities. This portfolio composition contrasts with empirical findings.

Nevertheless, it is important to emphasize that in our simulation study, the choice of pricing shares and debt securities under the physical probability has large impacts. As explained in Section 4.3, it implies that the net yields of shares and bonds are negative. Therefore, in this framework, interconnections only allow for variance reduction but not for gain opportunity. We can expect this feature to be modified if the pricing is done under the risk-neutral probability. Interconnections in both shares and debt securities could then be observed, even for values of larger than . The study of the risk-neutral specification constitutes an ongoing work. In some sense, these two types of specification for the pricing allow disentangling the two aims of the diversification: variance reduction and opportunity.

The latter discussion shows that our model seems promising but that results are very sensitive to the different possible specifications. Moreover, one feature that is not included in our model for the sake of simplicity may partly explain the discrepancy regarding debt securities. In reality, there are additional constraints -apart from the required capital- imposed to large shareholders, such as mandatory public communication. These constraints could discourage banks to invest in shares and could instead lead to higher investments in debt securities.

5 Application: impact of interconnectedness regulation

The diversification motive has proven an interesting explanation of the bank size (Stylized Fact 1), the network shape (Stylized Facts 2 and 3) and the composition of interconnections (Stylized Fact 4). Previous results concern the initial network resulting from banks’ choices based on their expectations. Due to the endogenous feature of interconnections, we can build some plausible counterfactual scenarios, allowing to analyze the impact of regulation on the welfare at time .

5.1 Assessing interconnections

The interconnectedness across financial institutions has become a key concern of supervisors and regulatory authorities. Currently, long-term interbank exposures are covered by two main requirements. The first one concerns the solvency required capital for the interconnections, as for any other assets. It imposes a constraint on the total interbank exposure. The second one concerns "large" single exposures and imposes the risk-weighted exposure to be lower than a fraction of the equity.191919We do not distinguish equity, own funds and regulatory capital. Currently, the Basel Committee considers that an exposure is large if above 5% (instead of 10%) of the equity and to impose that the risk-weighted exposure ( for the exposition to Bank ) has to be lower than 25% of the equity (see BCBS,, 2014, Section II and Section IV.B). These requirements are valid for any type of exposure (e.g. corporate or sovereign) but the weights can vary with respect to the type. Moreover, the Basel Committee proposes to introduce tighter rules about interbank exposures for the G-SIBs (Global Systematically Important Banks). An upper bound between 10% and 15% instead of 25 % is in discussion (see BCBS,, 2014, Section V). These tighter rules about interbank exposures aim at reducing the risk of contagion.

These different aspects show that interconnectedness is generally assessed in a negative way. Actually, supervisors are primarily concerned with excessive risks and therefore either analyze the effects of interconnections under depressed scenarios (stress-test approach) or build indicators in order to monitor the current fragility of the financial sectors. In both approaches, interconnectedness usually means contagion only. For instance, the seminal papers about network stress-tests -such as Furfine, (2003) on US data or Upper and Worms, (2004) on German data- sequentially consider the effects in their national banking sectors of the default of each bank. From their point of view, interconnected banks are likely to trigger defaults or to go bankrupt due to contagion.

Nevertheless, these analyses are not built on counterfactuals. They certainly give informative insights about what could happen within the current network in the case of defaults of some institutions or difficult macroeconomic conditions. However, since the network reaction is not taken into account, such studies do not really provide any clue on the way to obtain a more resilient network structure. Moreover, note that the question of regulation impact has hardly been addressed quantitatively, even in the case of a crystallized network.

The endogenous nature of interconnections in our model precisely allows us to study how the network reacts to tough macroeconomic conditions or to assess the impact of regulation on interbank exposures, for instance of the regulation in discussion at the Basel Committee. In the following, we focus on the impact of regulatory changes. To do so, we consider our 8 sets of regulatory weights associated to interbank exposure (, and ).202020In reality only 4 since with the specification chosen, has no impact. For each specific set, the initial network is derived using our formation process. This step accounts for the diversification motive. Then we simulate returns of the external assets and examine the network at time . Let us emphasize that the shocks are properly propagated through the real interconnections.212121Contrary to the assumption -used in the individual optimization program- that banks do not consider interconnections of their counterparts. The unique set of values and (see Proposition 5) is determined using the algorithm described in Appendix F. This allows us to carry out a fair assessment of contagion. To do so, we build a welfare indicator including an explicit concern for the real economy and examine its sensitivity to the regulatory set of weights.

5.2 Welfare analysis

We adapt the welfare analysis by Repullo and Suarez, (2013) to assess the impact of the regulatory parameters on the real economy.

The contribution of one bank is either negative or positive. When a bank defaults, its contribution is negative and proportional to the loss on its debt. This feature encompasses the cost of deposit insurance. When a bank is solvent, its contribution is the volume of external assets, i.e. the lendings provided to the real economy. This component captures the capacity to finance the real economy. The contribution of Bank is written

where is the social cost for deposit insurance (in Repullo and Suarez, (2013), varies in ).

Our welfare indicator is the ratio of the contribution of all banks over the initial lending to the real economy:

For , the welfare is given in Table 6. When there are interconnections, the welfare is higher than 1, indicating an increase of the banking capacity to lend to the real economy. In contrast, when there is no interconnection, the value of the external assets decreases. A complete analysis of the impact of interconnections would require further studies. However, these results suggest that the interconnections stemming from diversification are beneficial for the real economy.

| Sum of contributions | 23.2% | 6% | 29.9 | 30.9 | 32.4 |

| 23.2% | 8% | 22.8 | 23.6 | 24.8 | |

| 46.4% | 12% | 15.6 | 15.6 | 15.6 | |

| 46.4% | 16% | 11.9 | 11.9 | 11.9 | |

| Welfare (%) | 23.2% | 6% | 101.0 | 101.0 | 101.0 |

| 23.2% | 8% | 101.0 | 101.0 | 100.8 | |

| 46.4% | 12% | 93.4 | 93.4 | 93.4 | |

| 46.4% | 16% | 95.6 | 95.6 | 95.5 |

6 Concluding remarks

A diversification motive appears as a sound candidate to account for long-term exposures across financial institutions. The first aim of this paper is to test this assumption.

To this purpose, we build a model of financial network in which the balance sheets of all institutions (including interconnections) are totally endogenous apart from the equity. The network formation process involves two components. The first one explains how a bank optimizes its balance sheet knowing the state of the other banks in the network. We prove the existence and partial uniqueness of the solution of this optimization. The second part shows how to form the network using the individual optimization program. The existence and unicity of this network are shown by numerical arguments. An important feature of our model is its ability to account for the main features of the banking and the insurance business with the same set of parameters. Nevertheless, we focus in this paper on the banking business.

Secondly, the characteristics of the resulting network are compared to features usually observed. As to the shape of the network, we theoretically find that the diversification motive leads to a network close to those observed across big banks. Regarding the size and support of the interconnections, we show that a correct magnitude is reached under standard calibration. Moreover, the results are sensitive to some specifications, for example the pricing method of shares and debt securities.

The fact that our network is totally endogenous allows studying how it adapts to regulatory changes. Thus, the second aim is to apply our model to fairly assess the impact of regulation on interbank exposures. To this purpose we study the evolution of the welfare with respect to the regulatory weights and . We observe that the welfare is higher under regulations favoring interconnections.