Estimation of Monotone Treatment Effects in Network Experiments

Abstract

Randomized experiments on social networks pose statistical challenges, due to the possibility of interference between units. We propose new methods for estimating attributable treatment effects in such settings. The methods do not require partial interference, but instead require an identifying assumption that is similar to requiring nonnegative treatment effects. Network or spatial information can be used to customize the test statistic; in principle, this can increase power without making assumptions on the data generating process.

Keywords: causal inference, attributable effect, interference, randomized experiments, network data,

Facebook, peer effects

1 Introduction

Spillover effects, social influence, and the sharing of information are widely believed to be important mechanisms for social and economic systems. To better understand them, researchers may collect network data on relationships between units. In some cases, the data may come from a randomized experiment; past examples include studies in viral marketing [Aral and Walker, 2011], voting behavior [Bond et al., 2012, Nickerson, 2008], online sharing [Kramer et al., 2014], education [Sweet et al., 2013], and health [Miguel and Kremer, 2004].

In such experiments, the outcomes tend to be social in nature, and the treatment of one individual may influence others. This phenomenon, known as interference, often complicates the analysis. For example, [Bond et al., 2012] describes an experiment that was conducted using Facebook, a social network website. On the day of the 2010 US midterm Congressional elections, participants received a banner advertisement on Facebook which encouraged them to vote, with the option to self-report that they had voted by clicking on an “I voted” button. This advertisement was customized for each recipient, so that it displayed the total number of users who had already viewed the advertisement and clicked “I voted”; for a random subset, the advertisement also displayed the profile pictures of up to six of the recipient’s Facebook friends who had already self-reported. The self-reported voting rate for the treatment group (those receiving profile pictures) was 2.08% higher than for the other participants, a difference large enough to reject a sharp null of zero effect. Since the content of the advertisement for each viewer depended on the actions of previous viewers, the presence of peer effects was ensured by the experiment design. Additionally, participants may have influenced each other through conversations caused by viewing the advertisement. Due to this interference, rigorous estimates of the effect size do not necessarily follow from rejection of the sharp null, as estimation methods that assume no interference may not be applicable.

We propose a new approach for these types of experiments, which is based on an identifying assumption that the treatment effect is monotone. This is slightly weaker than requiring the treatment to not have negative effects, either directly or indirectly, on the outcome of any unit. Aside from this assumption, the interference will be allowed to take arbitrary and unknown form. Specifically, we do not assume partial interference or a correctly specified model of social influence.

The outline of the paper is as follows. Section 2 surveys related works. The basic problem formulation is given in Section 3. Three methods for estimation are presented in Section 4. These methods are demonstrated using data and simulation examples in Section 5. Section 6 discusses practical issues and future directions. Further technical details of the methods are presented in the appendices.

2 Related Work

Early discussion of interference in the potential outcomes framework is attributed to [Rubin, 1990, Halloran and Struchiner, 1995]. Current methods can be broadly divided between those which use a distribution-free rank statistic, and those which add identifying assumptions.

Distribution-free rank statistics are considered in [Rosenbaum, 2007, Luo et al., 2012]. In this approach, no assumptions are made on the interference, so that the estimates are highly robust. However, estimation is limited to rank-based quantities, i.e., on whether the treatment caused an overall shift in the ranks of the treated population when ordering the units by outcome. For non-rank quantities of interest, such as the average outcome under a counterfactual treatment, it appears that additional assumptions are required.

The most common identifying assumption is that the units form groups (such as households or villages) that do not interfere with each other; this is termed partial interference [Sobel, 2006]. The paper [Hudgens and Halloran, 2008] derives unbiased point estimates under partial interference, and variance bounds on the estimation error under a stronger condition termed stratified interference. Asymptotically normal estimates are given in [Liu and Hudgens, 2013], again assuming stratified interference, and finite sample error bounds are derived in [Tchetgen and VanderWeele, 2012]. For settings where partial interference does not apply, more general exposure models have been investigated by [Toulis and Kao, 2013, Ugander et al., 2013, Aronow and Samii, 2012, Ogburn and VanderWeele, 2014, Manski, 2013], with rigorous results if one assumes knowledge of the network dynamics, such as who influences whom. As a result, they may not be suitable when the underlying social mechanisms are not well understood. The recent paper [Eckles et al., 2014] also studies biased estimation of treatment effects under weaker assumptions than partial or fully modeled interference, which is similar in spirit to this present work.

3 Setup and notation

Let denote the number of units in the experiment. Let treatments be assigned by sampling units without replacement, and let encode the treatment assignment, where if the th unit was selected for treatment and otherwise. Let denote the observed outcomes, and let denote the counterfactual outcomes under “full control”, i.e., if none of the units had received treatment and for all .

As previously mentioned, we do not require an assumption of partial interference to hold. Instead, we require the following assumption on the treatment effect:

Assumption 1 (Monotonicity).

, for all .

This assumption might not be appropriate for some applications; for example, police interventions might displace crime, so that crime rates would decrease in some areas but increase in others. On the other hand, a vaccination program via “herd immunity” might have a strictly beneficial effect on the risk of infection.

Let denote the attributable effect of the treatment, defined to be the total difference between and :

| (1) |

Our definition for generalizes that of [Rosenbaum, 2001] to allow for interference; if no interference is present, the two definitions are equivalent. Our inferential goal is a one-sided confidence interval lower bounding . If this lower bound on is large, it implies that the observed treatment had a large effect on the outcomes.

Let denote a network of observed pre-treatment social interactions between the units. This snapshot of observed interactions might be only a crude proxy for the actual social dynamics. Hence, we will not use to make explicit assumptions on the influence between units. Instead, will be used to choose a test statistic. Our motivation is robustness to model error. If turns out to be a poor proxy, the method will lose power but not correctness, so that any significant findings will still be valid.

4 Constructing a Confidence Interval for

In this section, we present three methods for estimating one-sided confidence intervals that upper bound , which by (1) is equivalent to a lower bound on the attributable effect . In Section 4.1, a t-test based asymptotic confidence interval is presented for count-valued outcomes, i.e., when and are nonnegative integers. In Section 4.2, a non-asymptotic estimate is presented for the special case of binary outcomes, which is then extended in Section 4.3 to utilize the observed network .

4.1 T-test Based Asymptotic Confidence Interval

Suppose that the entries of are actually observed for the untreated units. Assuming that these units are sampled without replacement, it is well known [Thompson, 2012] that an unbiased point estimate for is given by the sample average ,

Under certain conditions, is asymptotically normal, in which case an asymptotic confidence upper bound for is given by

| (2) |

where is the estimated variance,

and where is the -critical value of a distribution with degrees of freedom.

In our setting, is not actually observed, and hence (2) cannot be evaluated. Let us assume that Assumption 1 holds, and also that is restricted to the set of nonnegative integers, so that and . Then an upper bound to the unknown value of (2) can be found by solving the following optimization problem:

| (3) | ||||

| such that |

which equals the highest value of (2) over all possible values of . A polynomial-time solution method for this optimization problem is described in Appendix A.

Example 1.

It may seem counterintuitive that (3) may be maximized by smaller than . To illustrate that this may be possible, let , , and let the entries of equal for the untreated units. Using (2) while letting gives a 95% upper bound of . On the other hand, letting equal for the untreated units gives an upper bound of , achieving the optimal value of (3).

As with any t-test, by using (3) we are implicitly assuming that satisfies a central limit theorem. Equivalently, we may instead state that one of two alternatives must be true: either (3) gives a correct confidence interval, or the -quantile of (after studentization) is greater than , which for large and roughly equates to having heavy tails.111for example, [Bloznelis, 1999, Th. 1.1] implies that must be large.

We remark that bootstrapping the untreated entries in will not compute a confidence interval for , since in general . However, the bootstrap may be still useful as a distributional check, testing whether (2) is valid for the point hypothesis .

4.2 Non-asymptotic Confidence Interval for Binary Outcomes

For binary-valued outcomes, a non-asymptotic one-sided confidence interval for can be computed. This can be done by a process known as “inverting a test statistic”222In practice, inverting a test statistic to produce a confidence interval can potentially result in unstable behavior when the underlying assumptions are violated [Gelman, 2011]. While we do not recommend our methods when Assumption 1 is violated, they do not suffer from this behavior. This is because (5) will always have at least one feasible solution, .. Let denote a test statistic of that is parameterized by the unknown . Let denote the -quantile of , defined by

| (4) |

While is unknown, we know two constraints on its value. First, we know that , by Assumption 1. Second, we know that with probability , by (4). Hence, to upper bound with probability , we can find the which maximizes while satisfying these constraints. That is, we can solve the optimization problem

| (5) | ||||

| such that | ||||

It can be seen that includes all non-rejected hypotheses, thus finding a one-sided confidence interval for .

We will use the test statistic , defined as

It can be seen that is generated by sampling entries from without replacement, so that is a random variable. As a result, the optimization problem (5) is easily computable for , and we describe a solution method in Appendix B. This method was originally presented in [Rosenbaum, 2001, Appendix], but for the case of no interference.

Weaker Assumption

We present a weaker assumption than Assumption 1, which may be applicable when the treatment effect is not strictly nonnegative:

Assumption 2 (Aggregate Monotonicity for the Untreated).

4.3 Using the observed network

We extend the approach of Section 4.2 to handle a new statistic , which utilizes the observed network . This statistic will have power to detect treatment effects that spill over from treated units to their untreated neighbors.

Let be given by

where is a smoothed version of , so that each entry in is a weighted average of nearby entries in . More precisely, let equal

where the smoothing matrix is given by

| (7) |

where denotes the distance between units and in ; where are shape parameters; and where denotes a normalizing constant

chosen so that the columns sum to one, making each element of a weighted average of elements in .

Because each entry of is a weighted average, units that are close to treated units will have high values in , even if they are not treated themselves. This will give power to detect spillovers. However, unlike , exact solution of (5) is not computationally feasible for . In Appendix C, (25) gives a relaxation of (5) that can be efficiently solved when the outcomes are binary-valued, yielding a asymptotically conservative estimate of under Assumption 1.

5 Data and Simulation Examples

In this section, we present data and simulation examples to exhibit the performance of the methods described in the previous section. In Section 5.1, the estimator (3) is used to analyze a primary school deworming experiment presented in [Miguel and Kremer, 2004]. In Section 5.2, the Facebook election experiment of [Bond et al., 2012] is analyzed using the test statistic . In Section 5.3, simulated experiments are used to evaluate the performance of the test statistic .

5.1 Analysis of [Miguel and Kremer, 2004]

[Miguel and Kremer, 2004] describes a primary school deworming project that was carried out in 1998 in Busia, Kenya, in order to reduce the number of infections by parasitic worms in young children. We restrict analysis to schools in a high infection area of Busia, which were divided into 2 equal-sized groups. Schools in group 1 received free deworming treatments beginning in 1998, while group 2 did not. Students were surveyed in 1999, and substantially fewer infections were found in the treatment-eligible pupils in group 1 compared to group 2, with 141 and 506 infections respectively. It is believed that the number of infections in each schools was affected not only by its own treatment status, but also that of other schools as well. This is because students that received the deworming treatment were susceptible to re-infection by infected students.

To demonstrate the estimator given by (3) on this experiment, we will assume that treatment was assigned by sampling without replacement333Groups 1, 2, and 3 (with group 3 excluded from the 1999 survey) were actually assigned by dividing the schools into administrative subunits, listing them in alphabetical order, and assigning every third school to the same group., and that all missing values in the data are ignorable. We also assume that the deworming treatment never increases the risk of infection, either to its direct recipient or to others. Under these assumptions, we solve a variant of (3) as discussed in Appendix A. The resulting estimates are that with 95% confidence, the number of infections that would have occurred if all schools received deworming is upper bounded by , and the number of infections that would have occurred if no schools received deworming is lower bounded by . These estimates may well be conservative, as no spatial information was used. However, they are not vaccuous; the one-sided confidence intervals are equal to those given by a regular t-test, which requires a much stronger assumption of no interference between schools, and an identical assumption regarding the asymptotic normality of .

5.2 Election Day Facebook Experiment

Using the reported counts for each treatment/outcome combination for the Facebook experiment of [Bond et al., 2012], we may estimate the attributable effect by solving (5) or (6) for . In both cases, the resulting 95% confidence interval for equals , implying that the usage of profile pictures caused at least 1,199,323 users to click “I voted”, when they would not have done so otherwise. This equals 2.0% of the treated population, matching the estimate of [Bond et al., 2012] which assumed no interference.

As the solutions to (5) and (6) are the same, our estimate of is valid under either Assumption 1 or Assumption 2. Possibly, some individuals may have been discouraged from voting by seeing the profile picture of a Facebook friend (for example, perhaps due to a negative relationship), which would violate Assumption 1. Assumption 2 allows for this possibility, since no restrictions are made on the effects of treatment on the treated.

5.3 Simulated Study

In settings where spillover effects are large, the statistic may outperform by identifying clusters of outcomes that were caused by the treatment. To demonstrate this behavior, we ran simulations in which treatments resulted in higher probabilities of positive outcomes not only for the treated units, but also for those nearby as well. We explored a range of scenarios, varying the number of treatments and their spatial separation, the spillover radius of the treatment effect, the counterfactual , and also the choice of kernel matrix . We found that estimates using were most accurate and robust to choice of when the treatments resulted in many well-separated clusters of positive outcomes; in particular, increasing the number of treatments or their potency could could actually decrease accuracy, by causing treatment effects to “run into each other”.

Description of Simulated Experiments

In each simulation, units were placed on a uniformly spaced grid. Sampling with replacement was used to select units for treatment, and auxiliary binary variables were generated with distribution . For , each counterfactual outcome was a random variable, and each observed outcome equaled if , and otherwise equaled a random variable, where the probability of having outcome due to treatment was given by

| (8) |

where denotes a truncated gaussian,

| (9) |

where denotes distance between units and on the grid, and where and are shape parameters. In words, (8)-(9) imply that each treatment has no effect if , and otherwise has an area effect that is independent of other treatments, i.e., each treatment for which has probability of independently causing unit to have outcome .

Simulation Results

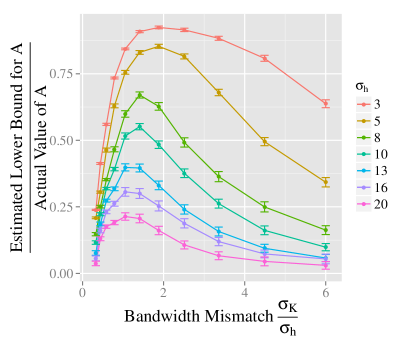

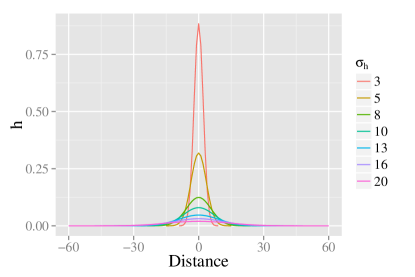

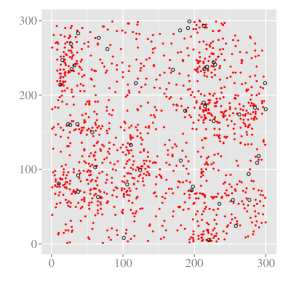

Figure 1(a) shows estimation performance as a function of the generative and the assumed kernel . To construct this figure, 7 different choices for were used, in which and were adjusted so that the degree of localization of the treatment effect was varied while was kept constant in expectation. These choices for are shown in Figure 1(b), with examples of the simulated outcomes shown in Figure 2. The assumed kernel was varied by ranging the bandwidth parameter used in (7) from to . In all cases, performance eventually decreased for large , suggesting that the choice of should reflect knowledge about the anticipated treatment effect. For localized effects (i.e., small ), the estimates were more accurate, and allowed for the bandwidth of to be chosen many times larger than . For diffuse effects (i.e., large ), estimates were highly conservative and more sensitive to the choice of . These results suggest that estimation using may require spatial separation between treated units, so that the effects can be localized to their source.

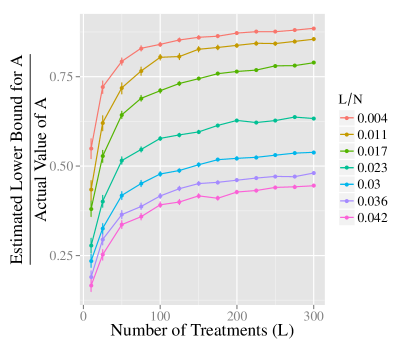

Figure 3 shows average estimation performance as a function of the number of treatments , and also their spatial density , which was controlled by varying the grid size . We found that increasing with the number of treatments improved accuracy, while increasing the spatial density of treatments worsened it. As a result, increasing while keeping fixed could decrease accuracy, due to the diminished spatial separation between the treatments. Examples of the simulations used are shown in Figure 4.

grid)

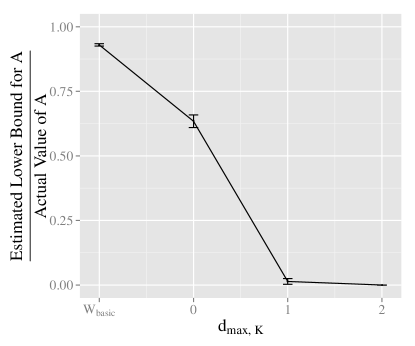

Figure 5 shows the average estimation performance when , meaning that the simulated treatments had no spillovers. The estimated lower bound on was produced either by inverting , or by inverting with ; the parameter can be interpreted as an assumption on the maximum distance between a treated unit and its spillover. Estimation using was most accurate; on average, the estimated lower bound on was of the true value. Estimation using was less accurate, ranging from of the true value when to the trivial lower bound of zero when . These results reinforce that should reflect knowledge of the anticipated treatment effect, and that may perform better when spillovers are at zero or near-zero levels.

As expected, the coverage rates for the estimated 95% one-sided confidence intervals were conservatively high. The highest frequency of violated confidence intervals was 3%, which occurred when . Over all of the simulations, only 0.1% of them resulted in a confidence interval which did not cover the true value of .

6 Discussion

Applicability of

The simulations of Section 5.3 are stylized, and are mainly meant to show that in principle, it is possible to rigorously estimate spillovers without placing strong assumptions on the validity of the observed network . However, the results also suggest that as a practical method, inverting the test statistic may have limitations due to the following requirements:

-

1.

The treatments should result in a large number of well-separated clusters of outcomes. If spillovers are non-existent or very small, should be used instead.

-

2.

The kernel smoothing matrix should be at least somewhat matched to the form of the spillovers.

How practical are these requirements? We would not expect the effects of single physical treatment, such as a coupon or advertisement, to resemble the simulations, in which as many as outcomes were caused per treatment. However, the condition need not represent a single physical treatment. Instead, it could mean administering the physical treatment to a subset of units in the vicinity of . For example, the condition could signify that some percentage of all units within some distance to (or belonging to the same region as ) receive the physical treatment. In this manner, it may be possible to design experiments in which the outcomes tend to be clustered at some desired intensity. Additionally, the treatment vicinities corresponding to each unit may be used to guide the choice of the kernel smoothing matrix .

Cluster-randomized designs, such as the type described above, are likely to be more effective for investigating interference-based effects – not only for , but for any other estimator as well. Assumption 1 allows for a good deal of flexibility in the experiment design. For example, if a unit belonged to multiple vicinities that were selected for treatment, the experiment protocol could give the unit a higher probability of receiving the physical treatment, or limit the unit to the same probability as those units in a single treatment vicinity, or even disqualify the unit from treatment altogether, as all three design options are allowed under Assumption 1.

General Usage

In this paper, we have considered the problem of estimating the attributable effect by a lower bound. Such a lower bound, if it is not vacuously conservative, may help in determining whether an experimental treatment had a practically significant effect. In returning only a lower bound, we are taking a conservative approach to the possibility of errors in the network or spatial model (or the lack of a model in (3) and ). We believe that a conservative approach to model misspecification will be desireable in some applications.

In addition to estimation of , one might consider testing the hypothesis that equals zero. However, under Assumption 1, can equal zero only if , meaning that the treatment must have zero effect on each individual unit. As a definition of “no effect”, this is far more restrictive than the hypothesis of zero average treatment effect, which allows for individual outcomes to change under treatment so long as the totals remain the same. For this reason, we recommend that significance tests should not assume Assumption 1. When interference is present, a better choice for significance testing might be to use the rank-based methods of [Rosenbaum, 2007].

While we have focused on estimation of the attributable effect , our methods can sometimes also be applied to estimate a version of the average treatment effect, which we define as follows. Let denote the counterfactual outcomes under full treatment, i.e., the outcome if all units were treated and for all . Let denote the counterfactual under full control. One definition for the average treatment effect is

which is the difference in outcomes between full treatment and full control, averaged over all units. As an example, in Section 5.1 (and with further details in Appendix A), we report an upper bound on and a lower bound on using (3) for the data of [Miguel and Kremer, 2004], thus inducing a lower bound on the average treatment effect. For binary outcomes, it can be seen that solving (5) for with in place of and in place of is equivalent to estimating a upper bound on , which gives a lower bound on . In principle, (25) for can also be solved with and transformed in the same manner. However, the runtime for inverting for this problem will be prohibitively large if , as was the case in the simulations. As a result, the performance of the relaxation (25) under this transformation has not been investigated.

Future directions and further analysis of [Miguel and Kremer, 2004]

In many settings, an observed network or spatial information might be only a crude proxy to the true underlying social mechanisms. We have shown that it is possible to rigorously use such information to improve estimates, without making unreasonable assumptions on the generative process. However, the proposed method needed high signal-to-noise for good performance, and it was not demonstrated on a real data set. For these reasons, usage of should be regarded as proof-of-concept rather than recommended practice.

As a possible direction for future work, we are investigating how the method of (3) might be applied to the “effective treatment” estimator discussed in [Eckles et al., 2014, Sec. 2.4.3]. This estimator, also discussed in [Aronow and Samii, 2012], was shown in [Eckles et al., 2014, Thm 2.2] to reduce bias under Assumption 1, but currently requires a correctly specified exposure model to compute a confidence interval. As this is a very strong assumption, a conservative estimate similar to (3) may be of interest.

We describe a special case of this estimator for which (3) can be seen to apply, in the context of the deworming experiment of [Miguel and Kremer, 2004]. We grouped of the schools into 16 triplets by order of distance, i.e., the closest three schools were grouped together, then the closest three out of the remaining schools, and so forth. The final 2 schools were removed from the analysis. We declared that a group of schools was treated if at least 2 schools in the group were treated (i.e., if they received the deworming treatment). The treated schools in the treated groups were declared to be selected. In this manner, 18 schools belonging to 8 treated groups were selected. Conditioned on the number of treated groups, and the number of selected schools in each group, the distribution of the 18 selected schools equals a two-stage sample [Thompson, 2012], in which the treated groups are selected by sampling without replacement, and then the selected schools are sampled within the treated groups. It follows by arguments similar to Section 4.1 that the average number of observed infections for the 18 selected schools is a conservatively biased point estimate for the per-school infections under full treatment. This value equaled , implying an point estimate of for the total number of infections under full treatment. This is a reduction from the point estimate of that would result from an assumption of no interference, i.e., if all 24 treated schools were averaged.

To compute a confidence interval, in principle the method of (3) can be applied to the selected schools, using the estimated variance of a two stage sample in place of . While the small sample size of 8 groups likely invalidates the central limit theorem requirements of (3)444We remark that the upper bound found this way for the deworming experiment was . This is somewhat less than the estimate of found in Section 5.1, suggesting at least that the proposed approach will not be vacuously conservative., the approach may be applicable in a larger experiment, such as [Bond et al., 2012]. Also, we observe that the point estimate is reminiscent of a U-statistic, since it can be written as a function of all school triplets and their respective treatments. This suggests further possibilities for new estimators.

In this preliminary analysis, the spatial information in [Miguel and Kremer, 2004] was used to remove treated schools from consideration if they were far from other treated schools. This improved the point estimate because such schools were more susceptible to reinfection. This is quite different from the simulations, where well-separated treatments gave the best estimates. We conjecture that both types of settings can arise in practice.

Appendices

Appendix A T-test Based Asymptotic Confidence Interval

Solution of (3)

It can be seen that the objective function of (3) is a function of and , and is increasing in the latter argument. Hence, the optimal will maximize over some level set of , which is equivalent to solving

| (10) | ||||

| such that | ||||

for some value of . Since must be an integer between and , we can solve (10) for all possible values of , and then choose the solution that maximizes (3).

Variant of (3) used in [Miguel and Kremer, 2004]

To estimate the number of infections that would occur if all of the schools were treated, we define , and as follows. Let denote the number of infections observed in school . Reversing the definition of , let denotes that school receives the deworming treatment. Let denote the counterfactual outcomes that would occur if for all . With , and thus defined, Assumption 1, which states that , means that treating all of the schools would not increase the infection counts over the observed values. A 95% confidence upper bound on can be found by solving (3).

To estimate the number of infections that would occur if none of the schools were treated, let be defined as before; let denote that school receives deworming treatment; and let denote the counterfactual outcome that would occur if no schools receive treatment. In place of Assumption 1, we assume that , meaning that treating no schools would not reduce the infection counts below the observed values, and also that , where is the total number of students at school that were measured in the 1999 survey. By similar reasoning as (3), in order to lower bound we can solve

| (12) | ||||

| such that |

where and are defined as before. Similar to (3), the optimal must maximize along a level set of , so that

| (13) | ||||

| such that | ||||

can be solved for different values of to find the optimal .

The optimization problem (13) can be formulated and solved as a dynamic programming problem. Generically, a simplified version of a dynamic program involves choosing a sequence of discrete decision variables , so as to control a sequence of state variables , where the initial state is given and for and some set of functions which model the state dynamics. A reward is paid for each decision, and an final reward is paid based on the final state. The goal is to choose to maximize , thereby steering towards a high reward final state while also maintaining high rewards for each decision. A canonical algorithm to solve this problem is value iteration [Bertsekas et al., 1995], which is also called backwards induction or Bellman’s equation.

Appendix B Estimation Using

Solution of (5) for

For , the -level critical value of is a function of , since is a random variable. Let denote the -level critical value of . It follows that (5) can be rewritten as

| such that | (14) | |||

| (15) | ||||

| (16) |

where (15) and (16) are consequences of . This optimization problem depends only the quantities and . As these quantities are integer valued and bounded above and below, their optimal values can be easily found by exhaustive search.

Solution of (6) for

Appendix C Estimation Using

For , the solution of of the optimization problem (5) is computationally hard. We present a conservative approximation of (5) that yields a larger confidence interval for . The main steps of the approximation are to bound the critical value using a simpler expression, and to enclose the feasible region of (5) by linear inequalities.

Preliminaries

We will require the following basic identities. It can be seen that equals the average of samples drawn without replacement from the vector . Because the columns of sum to one, it holds that

| (17) |

where we note that the expectation is taken over the random treatment .

Let denote a unit sampled uniformly from . Let denote the indicator function returning for unit and elsewhere. It follows that is equal in distribution to for . For all , it holds that

| (18) | ||||

| (19) |

where (19) follows from basic properties of simple random sampling [Thompson, 2012, Eq. 2.5].

Approximation of (5)

By Chebychev’s inequality, it holds for any choice of that

| (20) |

This is a highly conservative bound, but we use it here for simplicity and defer improvements for later discussion. Analogous to (5), a one-sided confidence interval for is given by

| (21) | ||||

| such that | ||||

To rewrite this problem with a smaller number of decision variables, let denote the vector given by

Let denote the set of all achievable values for . Equating terms and using (17)-(19), the optimization problem (21) can be restated as

| (22) | ||||

| such that | ||||

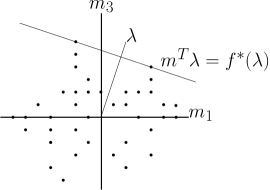

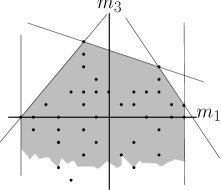

While this optimization problem has only 3 decision variables, it is hard to optimize because the constraint is difficult to check. As a relaxation, we will replace the constraint by a weaker constraint , where is a polyhedron that contains , and which can be represented by a tractable number of linear inequalities. Let denote the maximum inner product between and :

Given a set , let denote the set . Since for all , it follows that contains . Hence the following optimization problem upper bounds (22), yielding a conservative confidence interval:

| (23) | ||||

| such that | ||||

This optimization problem is low dimensional. As a result, it can be practically solved by a grid-based search over the feasible region, provided that is known for all .

Computation of

To solve (23), we must compute for all . For , it holds by the following identities,

that we may write as

| (24) | ||||

For nonnegative and , (24) can be transformed into a canonical optimization problem of finding an “- min cut” in a graph. The transformation, described in Appendix D, was originally proposed in [Greig et al., 1989] for image denoising. After the transformation, the min cut problem can be solved by linear programming or the Ford-Fulkerson algorithm, which runs in time where . [Papadimitriou and Steiglitz, 1998]

Selection of

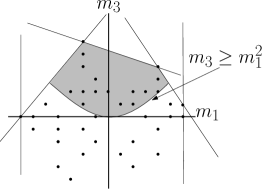

Figure 6 gives a geometric picture of the role of and in determining the feasible region of (23). The set must satisfy for all , since cannot be efficiently computed otherwise. By definition, each half-space equals a supporting hyperplane of the set in the direction . This implies that when is a positive scalar. As a result, a reasonable strategy is to choose to cover the allowable directions as densely as possible, so that approximates the convex hull of in those directions.

Reducing conservativeness

Chebychev’s inequality gives a very conservative approximation to the critical value of the test statistic. Because is a sample average, a normal approximation may yield a better estimate of its critical value. That is, it may hold that

where is the upper critical value of a standard normal. Using this approximation leads to the following optimization problem

| (25) | ||||

| such that | ||||

Summary of method

Given binary observations , treatment assignment , and network information , the method entails the following steps:

-

1.

Choose a smoothing matrix , for example by choosing values of and .

-

2.

Choose a set such that for all . This will ultimately induce the set which relaxes the actual feasible region.

- 3.

-

4.

Solve (23) or (25) to the desired level of precision. This is done by discretizing the feasible region of (23) or (25) along a grid, and checking every grid point. Because the objective is linear and the feasible region is 3-dimensional, the number of grid points that must be checked increases cubically with the desired precision. The best solution is an upper bound on , up to the precision of the grid search.

Appendix D Transformation of to min-cut problem

Given a nonnegative matrix with zero diagonal, and , the s-t min cut problem is

| (26) | ||||

| such that |

The interpretation of (26) is that denotes a weighted adjacency matrix of a network, and divides the nodes into two groups, with and in separate groups, so as to minimize the sum of the weighted edges that are “cut” by the division. This problem is polynomially solvable by the Ford-Fulkerson algorithm and also by linear programming [Papadimitriou and Steiglitz, 1998].

To transform into the form of (26), we observe that

may be rewritten as

for some , , , and nonnegative matrix , where the decision variable corresponds to the free elements in , i.e., those in . Following [Greig et al., 1989], we transform this to a min-cut problem by observing that

| (27) |

Let . Then maximizing (27) is equivalent to

| (28) |

Let , , and let . We can rewrite (28) as

which can be rewritten as (26) for some nonnegative with zero diagonal.

References

- [Aral and Walker, 2011] Aral, S. and Walker, D. (2011). Creating social contagion through viral product design: A randomized trial of peer influence in networks. Management Science, 57(9):1623–1639.

- [Aronow and Samii, 2012] Aronow, P. M. and Samii, C. (2012). Estimating average causal effects under general interference. In Summer Meeting of the Society for Political Methodology, University of North Carolina, Chapel Hill, July, pages 19–21.

- [Bertsekas et al., 1995] Bertsekas, D. P., Bertsekas, D. P., Bertsekas, D. P., and Bertsekas, D. P. (1995). Dynamic programming and optimal control, volume 1. Athena Scientific Belmont, MA.

- [Bloznelis, 1999] Bloznelis, M. (1999). A berry-esseen bound for finite population student’s statistic. Annals of probability, pages 2089–2108.

- [Bond et al., 2012] Bond, R. M., Fariss, C. J., Jones, J. J., Kramer, A. D., Marlow, C., Settle, J. E., and Fowler, J. H. (2012). A 61-million-person experiment in social influence and political mobilization. Nature, 489(7415):295–298.

- [Eckles et al., 2014] Eckles, D., Karrer, B., and Ugander, J. (2014). Design and analysis of experiments in networks: Reducing bias from interference. arXiv preprint arXiv:1404.7530.

- [Gelman, 2011] Gelman, A. (2011). Why it doesn’t make sense in general to form confidence intervals by inverting hypothesis tests. http://andrewgelman.com/2011/08/25/why_it_doesnt_m/. Accessed: 2015-10-02.

- [Greig et al., 1989] Greig, D., Porteous, B., and Seheult, A. H. (1989). Exact maximum a posteriori estimation for binary images. Journal of the Royal Statistical Society. Series B (Methodological), pages 271–279.

- [Halloran and Struchiner, 1995] Halloran, M. E. and Struchiner, C. J. (1995). Causal inference in infectious diseases. Epidemiology, pages 142–151.

- [Hudgens and Halloran, 2008] Hudgens, M. G. and Halloran, M. E. (2008). Toward causal inference with interference. Journal of the American Statistical Association, 103(482).

- [Kramer et al., 2014] Kramer, A. D. I., Guillory, J. E., and Hancock, J. T. (2014). Experimental evidence of massive-scale emotional contagion through social networks. Proceedings of the National Academy of Sciences, 111(24):8788–8790.

- [Liu and Hudgens, 2013] Liu, L. and Hudgens, M. G. (2013). Large sample randomization inference of causal effects in the presence of interference. Journal of the American Statistical Association, (just-accepted).

- [Luo et al., 2012] Luo, X., Small, D. S., Li, C.-S. R., and Rosenbaum, P. R. (2012). Inference with interference between units in an fmri experiment of motor inhibition. Journal of the American Statistical Association, 107(498):530–541.

- [Manski, 2013] Manski, C. F. (2013). Identification of treatment response with social interactions. The Econometrics Journal, 16(1):S1–S23.

- [Miguel and Kremer, 2004] Miguel, E. and Kremer, M. (2004). Worms: identifying impacts on education and health in the presence of treatment externalities. Econometrica, pages 159–217.

- [Nickerson, 2008] Nickerson, D. W. (2008). Is voting contagious? evidence from two field experiments. American Political Science Review, 102(01):49–57.

- [Ogburn and VanderWeele, 2014] Ogburn, E. L. and VanderWeele, T. J. (2014). Vaccines, contagion, and social networks. arXiv preprint arXiv:1403.1241.

- [Papadimitriou and Steiglitz, 1998] Papadimitriou, C. H. and Steiglitz, K. (1998). Combinatorial optimization: algorithms and complexity. Courier Dover Publications.

- [Rosenbaum, 2001] Rosenbaum, P. R. (2001). Effects attributable to treatment: Inference in experiments and observational studies with a discrete pivot. Biometrika, 88(1):219–231.

- [Rosenbaum, 2007] Rosenbaum, P. R. (2007). Interference between units in randomized experiments. Journal of the American Statistical Association, 102(477).

- [Rubin, 1990] Rubin, D. B. (1990). Comment: Neyman (1923) and causal inference in experiments and observational studies. Statistical Science, 5(4):472–480.

- [Sobel, 2006] Sobel, M. E. (2006). What do randomized studies of housing mobility demonstrate? causal inference in the face of interference. Journal of the American Statistical Association, 101(476):1398–1407.

- [Sweet et al., 2013] Sweet, T. M., Thomas, A. C., and Junker, B. W. (2013). Hierarchical network models for education research hierarchical latent space models. Journal of Educational and Behavioral Statistics, 38(3):295–318.

- [Tchetgen and VanderWeele, 2012] Tchetgen, E. J. T. and VanderWeele, T. J. (2012). On causal inference in the presence of interference. Statistical Methods in Medical Research, 21(1):55–75.

- [Thompson, 2012] Thompson, S. K. (2012). Sampling. Wiley.

- [Toulis and Kao, 2013] Toulis, P. and Kao, E. (2013). Estimation of causal peer influence effects. In Proceedings of The 30th International Conference on Machine Learning, pages 1489–1497.

- [Ugander et al., 2013] Ugander, J., Karrer, B., Backstrom, L., and Kleinberg, J. (2013). Graph cluster randomization: network exposure to multiple universes. arXiv preprint arXiv:1305.6979.