Properties and Applications of some Distributions derived from Frullani’s integral

Rose Baker

Centre for Operational Research and Applied Statistics

University of Salford, UK

r.d.baker@salford.ac.uk

Abstract

Frullani’s integral dates from 1821, but a probabilistic interpretation of it has never been made. In this paper, Frullani’s integral formula is shown to result from mixing a lifetime distribution by allowing the logarithm of the scale factor to be uniformly distributed over a finite range. This gives a class of long-tailed distributions related to slash distributions, where the pdf is simply expressed in terms of the survival function of the ‘parent’ distribution. The resulting survival distributions have all moments finite, and can exhibit the bimodal hazard functions sometimes seen in practice. A distribution of this type analogous to the t-distribution is derived, the corresponding multivariate distributions are given, and two skewed versions of this distribution are derived. The use of the mixed distributions for inference is exemplified by fitting them to several datasets. It is expected that there will be many applications, in health, reliability, telecommunications, finance, etc.

Keywords

Bimodal hazard, Frullani integral, hazard function, mixture distribution, survival distribution, two-piece distribution.

1 Introduction

Frullani’s result is that

| (1) |

where , , and where is Lebesgue-integrable in . Arias-De-Renya (1990) gives the fullest account of the history of the discovery of this result, which was first given by Frullani in 1821, and later by Cauchy in 1823 and 1827. Iyengar (1941) gives the first modern analysis, followed by Ostrowski (1949), Agnew (1951), Ostrowski (1976) and Arias-De-Renya (1990). The modern work is largely concerned with replacing the limits and by suitable mean values, and is not directly relevant to this paper.

One’s initial reaction is probably surprise that the integral is determined by and alone. Both terms in the integrand are infinite, and a quick proof of (1) rigorous enough for most proceeds by removing this problem by evaluating for small , and then letting . This is left for the reader’s amusement, as is another loose proof based on integration by parts.

However, the connection with survival distributions follows from a different proof of (1), which is rewritten as

| (2) |

where, without loss of generality, , and where is the distribution function of a survival distribution. The meaning is now that

| (3) |

is a pdf where if is a monotonically increasing function of its argument; naturally, must obey this condition to be a valid distribution function. The pdf then integrates to unity and is everywhere non-negative. As , tends to the pdf of . We can also write (3) in terms of the survival functions , when

| (4) |

To explore the meaning of this pdf, we write

| (5) |

and then note that

| (6) |

Hence (5) becomes

| (7) |

The purpose of this paper is of course not to prove Frullani’s result, but note that (1) follows quickly from (7) on reversing the order of the two integrals.

Equation (7) shows that (3) is the pdf of a mixture distribution generated by allowing the scale of a random variable from a survival distribution to be a random variable in the range , with pdf . These distributions have some attractive properties; for example, the generation of random numbers is simple: one computes , where , and then generates a random number from the distribution with pdf with scale factor .

Regarding notation, it is convenient to refer to as the parent pdf, and as the daughter pdf, and to give daughter distributions names such as the ‘-gamma distribution’. The parent pdfs are written as , where is the scale factor, and the pdf with unit scale is useful. The scale parameters are omitted in daughter pdfs . We write and for simplicity, standard distributions where are given; it is easy to put the scale back in by . . Finally, we use as the r.v. for survival distributions, and for r.v.s defined on the whole real line.

In general, the daughter distributions have longer tails than their parent, and one extra parameter. These pdfs are most attractive when the parent distribution function can be written down explicitly, as is the case for e.g. the exponential, Weibull and log-logistic distributions. For the -gamma distribution, the pdf is expressible only in terms of the incomplete gamma function. When fitting censored survival data, we also need the distribution function corresponding to the pdf , or the survival function , and this is often available as a special function, and if not, can be evaluated as an integral.

The next section gives some properties of the -distributions, then -distributions defined on the whole real line and multivariate -distributions are considered. Finally, some survival data with covariates and two other datasets are fitted to exemplify the use of the new distributions.

2 Properties of the Mixture Distributions

2.1 Moments

As with all mixture distributions, the moments are readily found in terms of those of the parent. Let for the parent distribution with scale factor . Then for the pdf

and reversing the order of integration,

from which . Since , we have that

| (8) |

The coefficient of variation is related to , that of the parent distribution, by

from which .

All moments of the daughter distribution are finite if those of the parent are, and the moment generating function , if it exists, is

where is the moment-generating function of the parent distribution evaluated with unit scale. For example, for an exponential parent distribution, , so .

2.2 Relationship to slash distributions

Tukey (e.g., Mosteller and Tukey, 1977) first introduced slash distributions. The standard slash distribution is the distribution of the ratio , where is uniformly distributed in , and is for example normally distributed. Taking now as uniform in , we have that

Setting we have that

In the limit

and we have the distribution function corresponding to (7). Hence the Frullani distributions are a type of slash distribution.

2.3 Other properties

The survival function is

which leads via integration by parts to

| (9) |

The tail behaviour of the -distributions and some numerical problems arising in inference are discussed in appendix A. It is shown there that the hazard function behaves like that of the parent with smallest scale factor, . This can give hazard functions that decrease in the tail, or bimodal hazard functions can occur.

In the left tail, as , we have

| (10) |

where is the parent pdf with unit scale factor. This value of is intermediate between and .

All daughter distributions examined from unimodal parent distributions have been unimodal. It may be possible to produce bimodal daughter distributions; a proof that daughter distributions from unimodal parents must be unimodal is lacking.

Inference with covariates is straightforward. To model dependence on a vector of covariates , one can use the proportional hazards or additive hazards assumptions as usual, e.g.

where the overall scale is a function of the covariates, but the range of scales is not.

3 The Frullani-Weibull and Frullani-log-logistic distributions

Brief details are given of the -distributions for two of the most important distributions used in survival analysis, the Weibull and log-logistic. The computation of the survival function is necessary when fitting right-censored data by likelihood methods, so this is also given. Moments are trivially derivable from the parent distribution moments using (8).

Substituting the Weibull survival function into (4) gives

| (11) |

The corresponding survival function is needed for likelihood estimation with censored data. We have

where is the exponential integral . Computation can be done more easily using the related function , where . Then

Although cannot be expressed using elementary functions, the exponential integral is a special function for which there are well-established numerical approximations. The -Weibull with has a hazard function that peaks and then rises again in the tail.

Lifetime distributions can be mixed using the gamma density. The exponential distribution then yields the Pareto distribution, so the pdf (11) with is a shorter-tailed version of the Pareto distribution. There is an application to frailty analysis (e.g. Klein and Moeschberger 2003); instead of using a gamma density for the random hazard scaling factor within a group, one can use the pdf for .

For a log-logistic distribution with survival function , the pdf is

and on integrating

This distribution can have a bimodal hazard function, and is used in section 6 to exemplify the methodology.

The Frullani procedure can be repeated more than once, taking (3) as the pdf for a second transformation. Here the effect is to change the weighting of from . The resulting pdfs and distribution functions are complicated, and so this second ‘Frullani-ization’ has in general not been attempted. However, for the log-logistic parent, the th Frullani-ized survival function can be written in terms of the th polylogarithm (for polylogarithms, see e.g., Andrews et al, 1999).

The survival function of the log-logistic distribution is , and from (4) the survival function of the distribution is obtained by

One can take varying scale ratios or keep them all equal. The pdf of the -log-logistic distribution is

This distribution is very long-tailed. The survival function is

where the dilogarithm function is

| (12) |

Further -distributions are given in appendix B; some of these are very tractable.

4 Distributions defined on the whole real line

One way to obtain distributions defined on the whole real line is to transform the random variable to the positive real line, e.g. by taking its exponent, ‘Frullani-ize’ the resulting survival distribution, and then back-transform the result. In terms of the original distribution function , this yields

where the mixing procedure consists simply of making the centre of location a uniform random variable within the range . Applying this to the normal distribution yields a short-tailed distribution, with kurtosis . It becomes uniform as . This distribution was studied by Bhattacharjee et al (1963). One can obtain other distributions using different transformations from to , such as , but the results are messy.

One can also proceed by reflecting (7) about the origin. This gives a smooth distribution iff . For example, from the half-normal distribution we obtain the -Gaussian pdf

| (13) |

where is the standard normal distribution function. From (8), the variance is

and the kurtosis is

an increasing function of . The value of corresponding to a kurtosis can be found by Newton-Raphson iteration. It is best to start at a value , because the slope at , and low slopes can cause the method to diverge.

The pdf at from (10) is .

The moment-generating function is

| (14) |

The distribution function is probably best evaluated as

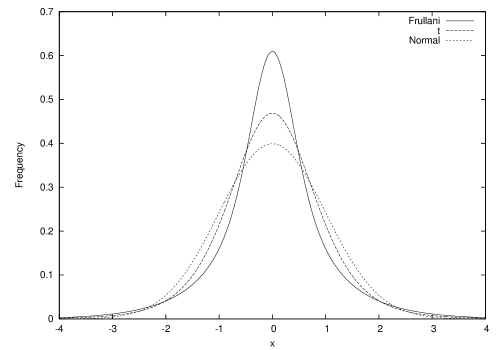

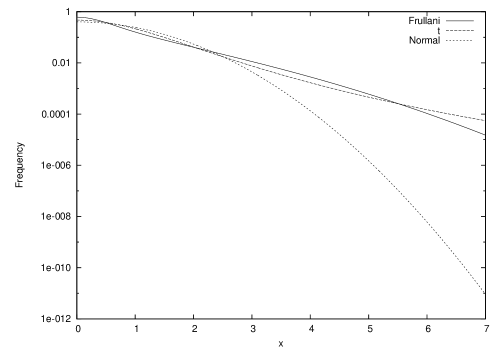

This distribution is long-tailed, with the normal as a special case when . Figure 1 shows this distribution and the t-distribution, both with unit variance and kurtosis . It can be seen that this distribution is heavier in the tail than the t-distribution. Figure 2 shows the tail behaviour, where the t-distribution is heavier in the extreme tail.

Skewness can be introduced by a device used by Azzalini (e.g. Azzalini and Capitanio, 1999, but used earlier by inter alia O’Hagan and Leonard (1976)), when for example

| (15) |

where can be of either sign.

Writing the function of as a mixture, changing the order of integration, applying the method of parts and making the substitution yields the mean

The second moment is that of (13), so that the variance is , and the skewness can then be found from the third moment , obtained like the mean as

The kurtosis can be found from the fourth moment

that of (13).

There is however a more natural way of skewing the -normal distribution, without going beyond the concept of ‘Frullani-ization’. One can generate half-normal pdfs with parameters for and for . The two pdfs are made to be equal at by weighting them, so that

| (16) |

where

This is the probability that exceeds the mode. The pdf (16) is that of a two-piece distribution. As the matching occurs at the mode the first derivative of is also continuous.

The moments are simple if messy functions of and , if the distribution is translated to have its mode at . We have then

and

In particular,

This distribution looks promising in its ability to fit skew and long-tailed data. The moments are finite and easily calculable, and a nice feature for data fitting and inference is that the mode is a parameter of the distribution.

If the distribution is skew to the right, and the probability of exceeding the mode . There is an inferential problem for the skew-t distribution in that the log-likelihood is bimodal as a function of ; there is no such difficulty with the two-piece distribution proposed here.

Two-piece distributions, often based on the normal distribution, appear in the literature occasionally, for example the ‘two-piece normal’ distribution of Gibbons and Mylroie (see e.g. Johnson, Kotz and Balakrishnan (1994), p173). Here the standard deviations differ in each half. Jones (2006) also discusses general two-piece distributions where the scale differs in the two halves. Note that (16) is not of this type, although one could construct such an -distribution from (3).

5 Multivariate distributions

The simple expression (7) for extends simply to the multivariate case. To illustrate with the bivariate case, let the mixture distributions for two time measures and be defined over respectively. Then we define the bivariate pdf

where is a bivariate distribution function. Applying (6), this becomes

so that finally

This by the way gives a bivariate result analogous to the Frullani integral:

| (17) |

The mixing does not induce a correlation between and , but a bivariate survival distribution where and are correlated can be modified in this way to give longer tails, the degree of tail elongation being allowed to differ between the two variables. This property is often required. In terms of copulae, the dependence parameter of the copula is unchanged.

The flexibility to give differing tail lengths is achieved with two extra parameters. Clearly, multivariate extensions are straightforward.

Elliptical distributions (e.g. Johnson and Kotz, 1972) are becomingly increasingly popular, and another possible way to extend the methodology to the multivariate case is to take a mixture of elliptical distributions. For example, the -variable normal pdf, with a scaling factor of is

Allowing to have a gamma distribution yields the multivariate t-distribution (Johnson and Kotz, 1972). The corresponding -multivariate normal distribution has pdf

One parameter is redundant, so we can set e.g. . Hence

where and is the distribution function of the chi-squared distribution with degrees of freedom. For example, when , the bivariate pdf is

The moment-generating function is

where is the mean, analogously to (14).

In general, the moments of the mixed distributions are given by

where is the corresponding moment of the parent distribution.

These distributions can of course be skewed e.g. by Azzalini’s method (Azzalini and Capitanio, 1999, 2003), as is done for the multivariate t-distribution. Some more -distributions are described in appendix B.

6 Results of Data Fitting

To illustrate the use of Frullani-mixed distributions in survival analysis, a dataset from Klein and Moeschberger 2003, section 1.14 was analysed. The times in weeks to weaning of first-born babies from 927 young mothers were found from interview, along with some covariates, such as race (white, black, or other), whether the mother smoked at the birth of the child, years of mother’s schooling, whether the mother lived in poverty, and so on. Censoring is light; some mothers stopped breastfeeding before the baby was weaned (i.e., switched to bottle-feeding, etc). The dataset is available from the authors’ website.

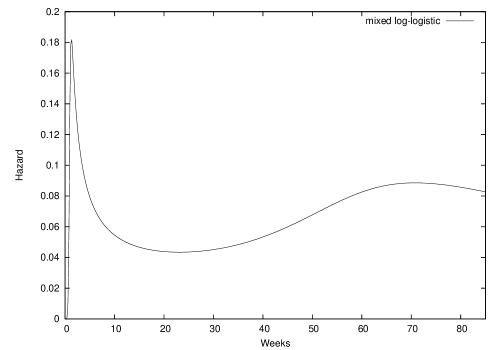

There is considerable evidence of rounding of the number of weeks to weaning, but the data are usable. Table 1 shows minus log-likelihoods () for fits of the models discussed above to the data, with no covariates. It can be seen that the mixture models fit considerably better than conventional models. The scale ratio is high, showing a considerable departure from the parent distribution. Figure 3 shows the hazard function, of the Frullani-mixed log-logistic model (-log-logistic model) , with 95% confidence intervals.

The hazard function decreases and then rises again after about 50 weeks. This was also noted by Klein and Moeschberger, and is the reason why the mixture models perform so well here. After a tail of slow weaning, most mothers still breastfeeding wean the baby after a year, only a very few continuing longer. This type of behaviour, with a long tail which however eventually peters out, is well fitted by these mixture models.

Table 2 shows covariate parameter estimates, standard errors (or coefficient of variation) and 95% confidence intervals, for the mixed log-logistic model. The log-likelihood increased by 7.84 on adding the covariates, some of which are statistically significant. The findings obtained here are similar to those of Klein and Moeschberger.

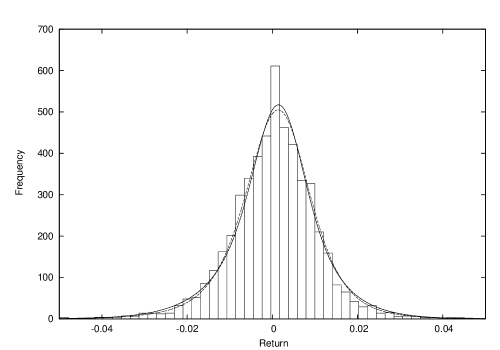

To illustrate the use of (15) and (16), 5106 FTSE-100 returns from 1984 to 2003 were fitted by maximum likelihood estimation. Figure 4 shows the model fit, and that of the Azzalini skew-t distribution. This latter has 4.3 degrees of freedom, corresponding to a long tail. However, (15) and (16) fitted the data with a nearly identical log-likelihood. The fitted ratio a/b was 4.41 for (15). As the skewness is small here, the lines from these two pdfs can not be distinguished.

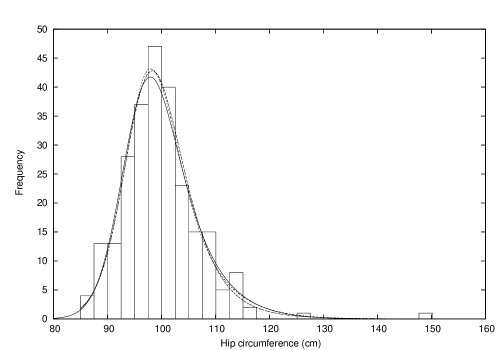

Finally, figure 5 shows the fit of this distribution to some hip circumference data from the Statlib database. The dataset contains estimates of the percentage of body fat determined by underwater weighing and various body circumference measurements for 252 men, and was submitted to Statlib by Roger Johnson.

Here the data are also long-tailed, the skew-t distribution fitting with 5.8 degrees of freedom. The pdf (15) fits with an identical log-likelihood function, and a ratio of 4.84, and the two-piece -normal distribution fitted very similarly.

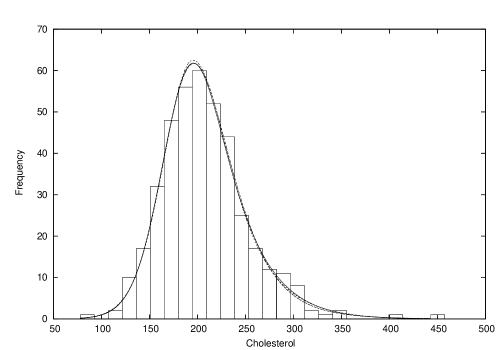

Figure 6 shows fits to cholesterol level of 403 patients interviewed in connection with diabetes, given in Harrell (2001). The Azzalini skew distribution fitetd with degrees of freedom, and all three fits had very similar log-likelihood and overlap on the plot.

7 Conclusions

The Frullani integral (1) has a probabilistic interpretation, i.e. that, given a pdf, a mixture distribution where the logarithm of the scale of the random variable is uniformly distributed within a finite range, is also a pdf. The Frullani integral leads to a class of ‘daughter’ distributions, which are here called ‘-distributions’, whose pdfs are simply expressible in terms of the ‘parent’ distribution functions.

That this is so is theoretically interesting; the mathematical result has been known since 1821, but never applied to ‘distribution-ology’. However, this result will doubtless be of little interest to statisticians, unless the new distributions obtained are practically useful. They are relatively tractable: the moments are simply expressible in terms of the parent distribution moments, and random numbers are readily generated if they can be for the parent distribution.

The most direct application is to survival distributions. Here there is already a wide range of univariate distributions available, with hazard functions capturing most of the behaviour actually observed. Hazards can rise or fall (Weibull model), rise then fall (lognormal and log-logistic models), or fall then rise, the ‘bathtub’ hazard of human mortality and some equipment failure. There are some particular new distributions that might be useful, such as the -exponential and -Weibull (11). But what is unusual about the new class of distributions is the tail behaviour. In the tail, the hazard becomes that of the parent distribution with the smallest scale factor (largest mean). For a parent distribution such as the lognormal, the hazard function can be bimodal. This type of behaviour has been observed, e.g. in breast cancer (Demicheli et al 2008), in bovine foetal survival (Hanson et al 2003), and in the weaning example used in this paper. In general, these distributions can be very long-tailed, but behave like the parent distribution in the extreme tail. For example, if , in the tail , so from (4) , until in the extreme tail .

In finance, this type of behaviour has to be engineered, via the ‘truncated Levy’ distribution. Finite moments are desirable, and to achieve this Ali and Nadarajah (2006) truncated the Pareto distribution, and Nadarajah (2009) has produced truncated versions of five distributions used in finance, telecommunications etc., including the t-distribution, with the aim of achieving finite moments. Hopefully, many more examples of this type of behaviour will come to light; in many instances, distributions can be long tailed or heavy tailed, but often there is eventually some kind of limitation. For example, human weight is ultimately limited by physics and biology.

By exploiting the reflection symmetry of distributions such as the Gaussian, an -Gaussian distribution can be derived. Such distributions, and their multivariate generalisation, provide an alternative to the t-distribution for which all moments exist. The two-piece skewed distribution is one of a useful class of distributions that can be skew and long-tailed, with the normal distribution as a special case.

Acknowledgement

The author is grateful to Prof. Chris Jones for pointing out the connection with slash distributions and for helpful comments on the manuscript.

References

- 1 Agnew, R. P. (1951) Mean Values and Frullani Integrals, Proceedings of the American Mathematical Society, 2, 237-241.

- 2 Ali, M. M. and Nadarajah, S. (2006) A truncated Pareto distribution, Computer Communications 30, 1-4.

- 3 Andrews, G. E., Askey, R., Roy, R. (1999) Special Functions, Cambridge: Cambridge University Press.

- 4 Arias-De-Renya, J. (1990) On the theorem of Frullani, Proceedings of the American mathematical Society 109, 165-175.

- 5 Azzalini, A., Capitanio, A., (1999) Statistical applications of the multivariate skew normal distribution. Journal of the Royal Statistical Society series B, 61 579-602.

- 6 Azzalini, A., Capitanio, A., (2003) Distributions generated by perturbation of symmetry with emphasis on a multivariate skew t-distribution. Journal of the Royal Statistical Society series B, 65, 367-389.

- 7 Bhattarcharjee, G. P., Pandit, S. N. N. and Mohan, R. (1963) Dimensional chains involving rectangular and normal error-distributions, Technometrics 5, 404-406.

- 8 Demicheli, R., Biganzoli, E., Boracchi, P. Greco, M. and Retsky, M. W., (2008) Recurrence dynamics does not depend on the recurrence site, Breast Cancer Research 10, doi:10.1186/bcr2152, http://breast-cancer-research.com/content/10/5/R83.

- 9 Hanson, T., Bedrick, E. J., Johnson, W. O. and Turmond, M. C. (2003) A mixture model for bovine abortion and foetal survival Statist. Med. 22, 1725-1739.

- 10 Harrell, Frank E. Jr. (2001) Regression Modeling Strategies With Applications to Linear Models, Logistic Regression, and Survival Analysis, New York: Springer.

- 11 Iyengar, K. S. K. (1941), On Frullani Integrals, Mathematical Proceedings of the Cambridge Philosophical Society, 37, 9-13.

- 12 Johnson, N. L. and Kotz, S. (1972) Distributions in Statistics: Continuous Multivariate Distributions, New York: Wiley.

- 13 Johnson, N. L., Kotz, S. and Balakrishnan, N., (1994) Continuous Univariate Distributions, 2nd ed., New York: Wiley.

- 14 Jones, M. C. (2006) A note on rescalings, reparametrizations and classes of distributions, Journal of Statistical Planning and Inference 136, 3730 - 3733

- 15 Klein, J. P. and Moeschberger, M. L. (2003) Survival analysis: techniques for censored and truncated data, 2nd ed., USA: Springer.

- 16 Mosteller, F. and Tukey, J. W. (1977) Data analysis and regression: a second course in Statistics, Reading, MA: Addison-Wesley.

- 17 Nadarajah, S. (2009) Some Truncated Distributions, Acta Applicandae Mathematicae, 106, 105-123.

- 18 O’Hagan, A. and Leonard, T. (1976) Bayes estimation subject to uncertainty about parameter constraints. Biometrika, 63, 201-202.

- 19 Ostrowski, A. M. (1949) On some generalizations of the Cauchy-Frullani integral, Proceedings of the National Academy of Sciences of the United States of America, 35, 612-616.

- 20 Ostrowski, A. M. (1976) On Cauchy-Frullani integrals , Journal Commentarii Mathematici Helvetici, 51, 57-91.

Appendix A: Some more properties of the -distributions

Tail behaviour

The hazard function of the pdf is

Writing

we have that

If as , then , because terms with have weight zero. Probabilistically, in the tail, events from distributions with have already occurred, and only the longest-tailed distribution in the mixture can still supply events.

However, if tends to a constant, all components of the mixture contribute with constant weight. The hazard function , derived from is then independent of , so we can again write .

Finally, cannot tend to zero, as we would not then have as . Hence it is always true that . This means that a distribution such as the Weibull with an increasing hazard function gives rise to a mixture distribution where the hazard first increases, then decreases, and finally increases again in the extreme tail.

An example where tends to a constant is the Pareto distribution , so long-tailed that the mean is not defined. Here , and . The hazard function .

Numerical problems

These mixture distributions have scale parameters and , as well as any others intrinsic to the parent distribution, such as the Weibull shape parameter. When maximising likelihood functions, the function minimizer may choose values such that . Although the pdf is invariant under , the log-likelihood function may then contain logarithms of negative argument. One can resolve this problem by using parameters , and taking , , or by taking parameters and . When , computation of the pdf and survival function become numerically unstable, and one simply computes the parent pdf and survival function. For the two-piece skew distribution (16) there are three scale parameters, . It is probably best to take and as parameters, where , . One has to test for and , and revert to the parent pdf if so.

A deeper problem is now identified. Consider (3) when and . Expanding in a McLaurin series in , and writing ,

The log-likelihood of observing an uncensored sample is

where the first term is . Hence

The linear term in vanishes, by virtue of the fact that is a MLE; . This shows that there is a small computational problem for inference, if we maximise the log-likelihood for the parent distribution, and restart a function minimizer at the point . At that point , so some minimizers could ‘stick’ and exit with .

Score tests

Consider (3) when , , and . The central differencing of the distribution function allows us to explore ‘sensible’ hypotheses, where we have a maximum-likelihood fit to data of the parent pdf , with scale parameter , and we consider taking a mixture of scale factors around . Expanding in a McLaurin series in , and writing ,

The log-likelihood on observing an uncensored sample is

where the first term is . Hence

From this the score statistic can be read off as

or

where denotes the second derivative w.r.t. . The variance of the score is

which can be approximated as the sample sum. Asymptotically the standardised score is under .

For the exponential distribution, the score statistic is . The score test is a one-sided test of whether the standard deviation exceeds the mean, this equality being a well-known property of the exponential distribution.

Appendix B: More distributions

The -gamma distribution

The parent pdf is , with distribution function

where is the incomplete gamma function. The daughter distribution is then

with survival function

This can be integrated by parts using (9) to give the single integral

The mean for the general distribution is

variance

The -lognormal distribution

With standard normal, the mixture pdf is

where is the standard normal distribution function.

On using (9) we obtain the survival function

This fortunately requires only the computation of elementary functions and the error function.

The -Pareto distribution

Taking the parent survival function as for , the -Pareto pdf is

The survival function is

The -Cauchy distribution

The distribution function corresponding to the Cauchy pdf is , from which the -Cauchy pdf derived from Frullani-izing the right half of the distribution and reflecting about the origin is

or

The distribution function is

where is the dilogarithm defined by (12).

Figures and Tables

| Model | -Log-likelihood | Shape param. | ||

|---|---|---|---|---|

| Exponential | 3409.29 | 1 | 0.0594826 | n/a |

| Mixed exponential | 3406.36 | 1 | 0.108615 | 0.0359083 |

| Weibull | 3408.56 | 0.970074 | 0.0602816 | n/a |

| Mixed Weibull | 3388.41 | 2.01358 | 0.482310 | 0.0152277 |

| Gamma | 3409.27 | 0.992376 | 0.0590219 | n/a |

| Mixed gamma | 3379.93 | 5.35736 | 3.90543 | 0.0865375 |

| Lognormal | 3402.77 | 1.17603 | 0.106397 | n/a |

| Mixed lognormal | 3374.38 | 0.403807 | 0.856643 | 0.0173032 |

| Log-logistic | 3429.32 | 1.43847 | 0.101974 | n/a |

| Mixed log-logistic | 3372.66 | 7.38682 | 1.06599 | 0.0159815 |

| Parameter | estimate | SE | 95% CI |

|---|---|---|---|

| Shape | 6.60933 | 0.2308 (CV) | (4.204491 10.389665) |

| Scale | 1.70841 | 0.2101 (CV) | (1.131659 2.579107) |

| Scale | 0.027619 | 0.2512 (CV) | (0.016881 0.045187) |

| Race: Black | -.155922 | 0.07564 | (-0.304182 -0.007663) |

| Race: Other | -.0009 | 0.09047 | (-0.178226 0.176426) |

| Smoked at birth | -.109407 | 0.06312 | (-0.233113 0.014300) |

| Years schooling | 0.0440546 | 0.01878 | (0.007238 0.080871) |

| Poverty | 0.196038 | 0.07658 | (0.045936 0.346140) |