Sector-based Factor Models for Asset Returns

Abstract.

Factor analysis is a statistical technique employed to evaluate how observed variables correlate through common factors and unique variables. While it is often used to analyze price movement in the unstable stock market, it does not always yield easily interpretable results. In this study, we develop improved factor models by explicitly incorporating sector information on our studied stocks. We add eleven sectors of stocks as defined by the IBES, represented by respective sector-specific factors, to non-specific market factors to revise the factor model. We then develop an expectation maximization (EM) algorithm to compute our revised model with 15 years’ worth of S&P 500 stocks’ daily close prices. Our results in most sectors show that nearly all of these factor components have the same sign, consistent with the intuitive idea that stocks in the same sector tend to rise and fall in coordination over time. Results obtained by the classic factor model, in contrast, had a homogeneous blend of positive and negative components. We conclude that results produced by our sector-based factor model are more interpretable than those produced by the classic non-sector-based model for at least some stock sectors.

1. Introduction

Suppose we visit a local high school and decide to study the academic performances of a random sample of students. We model each student’s GPA as a random variable. We can expect these GPAs to vary widely. At the same time, though, we can also expect these GPAs to somehow relate to each other through common factors.

To understand how the GPAs vary, we can assume that only a very small number of aspects of students’ lives account for the majority of their GPAs. For how many hours a day do they watch the television, play sports, or socialize with friends? How long do they use their computers to read the news, check their emails, use social networking sites, or finish homework? How much do they sleep?

Each of these aspects is a random variable, and, among the students, we would expect a varied distribution. Yet we would suspect that, with a single student, GPA and the measurements would not all be truly independent; some underlying factors would connect and influence some of these measurements. For example, it would not be a wild guess to assume that a student who spent nine hours a day sprawled in front of the television but only five minutes in front of a book had a lower GPA than average. Socialization could be related to time spent finishing homework or checking email through a common factor.

Of course, students are individuals. They, like the real world, are so infinitely complex that we cannot even dream of precisely finding and calculating the effects of all the factors that influence GPA, no matter how many factors we can think of and express statistically.

Factor analysis is meant to relate observed variables with a small number of common factors and a special random variable unique to each [2, 5, 6, 8, 18, 23]. We seek to explain how the variables are interconnected by these common factors. The unique random variables are included to account for the variability not influenced by any of the common factors. We could perform factor analysis on the hypothetical study mentioned above on high school students to see how factors might impact students’ academic performance.

The common factor model is as follows:

| (1) |

where and are vectors; is an matrix; is an vector; and is an vector. It may be clearer to the reader if we expand equation:

| (2) |

Thus each is represented as a linear combination of random variables (factors), with the components of as coefficients. In the hypothetical academic performance study proposed above, is the current GPA of student , and is his “true” GPA over the course of the study. are latent unobserved random variables meant to interpret up to error . is the factor loading matrix with being the weight of factor , referred to as loading—it indicates the relative importance of to . A low value of , therefore, indicates that its does little in influencing .

In order to successfully run factor analysis, we must make several assumptions. First, all and are normal with mean and mutually independent. We also assume that and have standard deviations of , and , respectively. This implies that is also normal with mean. Factor analysis is easy to use and often provides very useful approximations in practice.

The history of factor analysis is rooted in psychology. In 1904, Charles Spearman published an article in the American Journal of Psychology, trying to find a definitive and completely accurate measure of intelligence [21]. Factors that influenced intelligence, he argued, were the subject’s test scores on pitch, light, weight, classics, French, English, and mathematics; the scores on those tests were weighted. From then on, factor analysis has expanded from psychology to many different fields of study [1, 2, 3, 4, 7, 8, 9, 13, 15, 18, 20, 22, 24], along with broad discussions about how to efficiently compute factor models [2, 10, 11, 14, 16, 17, 19, 23].

In particular, it is a well-established practice to use factor analysis to study price fluctuations in stock prices [2, 6]. The stock market is notable for its seeming randomness and frequent large up and down swings. By studying the daily log return, i.e.,

of stock prices through factor analysis, for example, we can better understand these price swings and potentially design trading strategies that can better handle them.

Nonetheless, factor analysis is not at all perfect and is quite ambiguous [1]. The factor loading matrix is far from unique. In the hypothetical academic performance study example, there is no obvious relationship between and any identifiable aspect of life that might influence academic performance. The motivation for a factor model is not actually built into the factor model. This paradox can often limit the usefulness of factor models. There have been many attempts to improve the factor model for better practical performance [6, 10].

In the stock market, stocks are often divided into sectors depending on the products of the associated companies. According to the Institutional Brokers’ Estimate System (IBES), we have used sectors: finance, health care, consumer non-durables, consumer services, consumer durables, energy, transportation, technology, basic industries, capital goods, and public utilities. For example, Morgan Stanley (stock symbol: MS) is in the financial services sector. Its stock price often moves with other financial services stocks. Google (stock symbol: GOOG) provides internet-related services and is in the technology sector. Its stock price often moves with other technology stocks as well. There are also stocks that do not belong to any of these sectors. When factor models are used to measure variability of stock price fluctuations, such sector-dependent behavior is typically not revealed in the factor model, although some sector association can be seen (see Sections 3 and 4.)

It is the goal of our work to develop factor models that explicitly utilize sector information, to better exploit the real relationships between stocks. We first select our factor-loading matrix to ensure representation of both the whole market and every sector. We assign each sector to a different : represents finance, represents health care, and so on. We choose , such that through are non-specific market factors. We set to be zero when is not in the industry represented by . For example, with , a business in the transportation industry () would be expressed as (compare with equation (2))

or

We then develop an expectation maximization (EM) algorithm to compute the factor model, and use this algorithm to test our factor model using daily close prices of the S&P 500 stocks over the last 15 years. Finally, we drew some interesting conclusions from our tests.

2. Materials and Methods

In the study of daily stock log returns, we will make the typical assumption that stocks have returns over time so that in equation (1). Our goal is to develop a method to identify and , the diagonal covariance matrix of , with sector information specifically built into and by observing over a period of time.

Equation (1) allows us to write out the covariance matrix for explicitly as . To proceed, we first review a simple method to identify and in the standard factor model, which repeatedly improves the estimates for and based on the principle of expectation maximization (EM). More details are in [10, 17].

Given a pair of estimated and , the expected value of the factors is

where , and the second moment of the factors is

Given daily log returns , we then compute a pair of new estimates for and through an Expectation step (E-step) and an Maximization step (M-step):

- E-step:

-

Compute and for all data points .

- M-step:

-

where and .

To build the IBES sector information into the factor model, we will choose so that there are sector factors and market factors in the factor model. The market factors reflect the dependence of individual stocks on a few number of global market parameters, but the sector factors will only reflect inter-dependence of stocks within a given sector. As mentioned in Section 1, we choose to set to if stock is not in sector . This way, there are quite a lot of zeros in the factor-loading matrix , reflecting on the financial intuition that stocks in different sectors have less influence over each other (although they can still exert influence through the global market factors).

Remarkably, only small modifications need to be made to identify this new factor model. For stock , let be the set of non-zero loading indexes. Then,

The formula for remains the same. See details in Appendix 6.2.

3. Results and Discussion

To validate our factor model, we downloaded daily close prices of the S&P 500 stocks over 15 years (from 1996 to 2010). There were actually stocks over this time period due to the frequent changes in the index. We also obtained IBES sector classifications over this same period.

Our mentor provided a MATLAB program, which we used to perform an empirical study of the new factor model on the daily returns computed from these close prices. For this experiment, we choose and convergence is considered reached after EM iterations.

The factor models in Figures 1 through 5 are computed with data in the years 1996–2005. We compare the standard factor model with the new one in terms of the computed factors. Our goal is to demonstrate that the new factor models indeed can generate more informative factors.

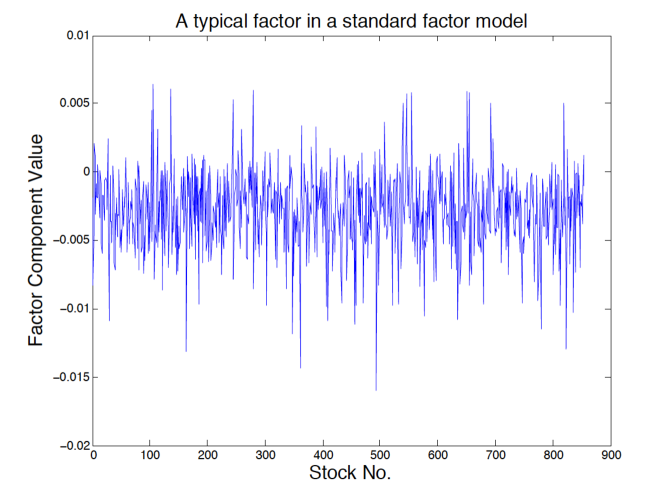

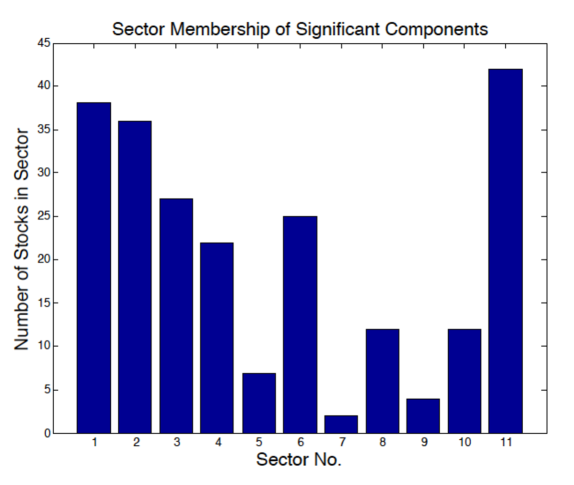

Figure 1 depicts one of the factors computed in the standard factor model. Figure 2 depicts the sector memberships of all the components that are at least 10% of the largest component in absolute value. This factor is dominated by stocks in sectors , and , three sectors that are very different from each other. Since there are as many positive components as there are negative ones, it is difficult to interpret the factor direction. We struggle to analyze the graphs of the stock values or to predict any future values.

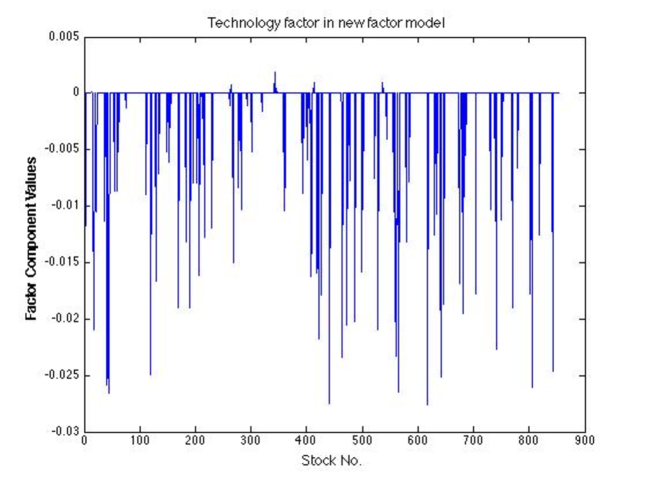

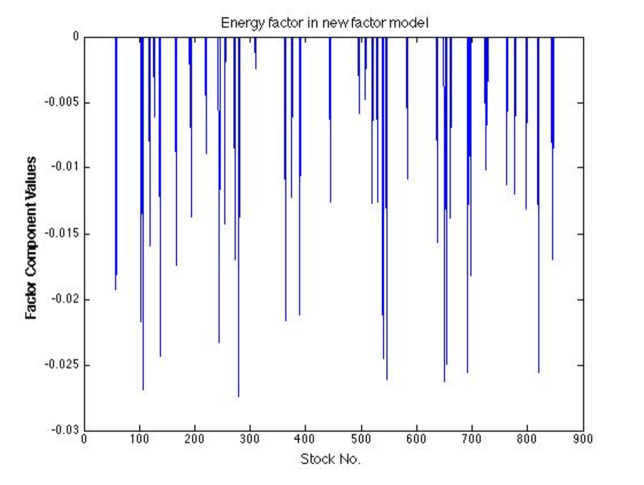

Figure 3 depicts the factor computed in the new factor model that corresponds to the technology sector. Most of the sector components are now negative, indicating the tendency that most technology components move up or down together over time. This is more consistent with financial intuition about the phenomenon that stocks in the same sector often move in tandem. Figure 4 depicts the components in the energy sector. As in Figure 3, the energy factor also indicates the tendency to move up or down together. Instead of the random fluctuations noted in Figures 1 and 2 that don’t regard the sectors of the stocks, we can clearly observe a strong common direction here.

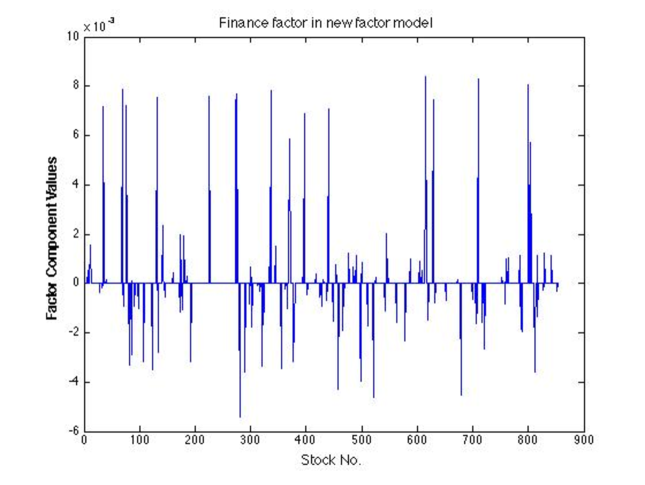

Figure 5 depicts the components in the financial sector. Although our results supported our hypothesis that the motions of stocks in the same sector tend to be contingent upon one another, we see that not all sectors behave the same. In Figure 5, there seem to be as many positive and negative components. Due to the nature of finance, we believe stocks in the financial sector should not all move in the same direction over time.

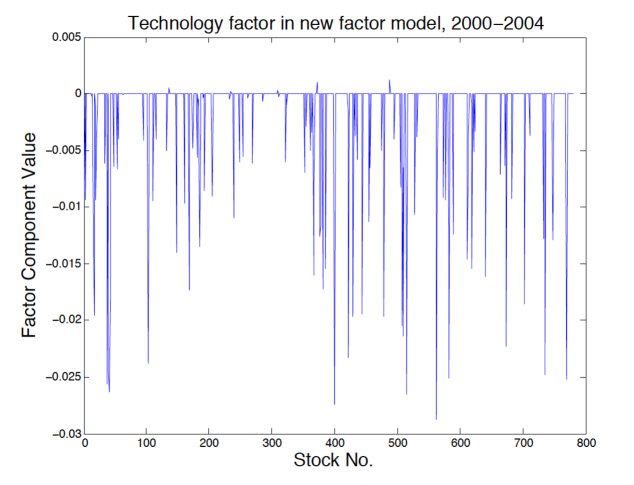

Finally, Figure 6 depicts the components in the technology sector using data during years 2000–2004. While Figure 6 looks quite different from Figure 3, indicating large changes in the technology sector over time, the factor components remain largely negative. This is an indication that stocks in technology sector consistently move in tandem over time. We have observed similar behavior in most other sectors.

4. Illustrations

5. Conclusions and Future Work

We sought to understand if taking a sector-based approach to factor analysis models of the stock market would increase our understanding of stocks and help us study how different stocks interact. Our experiments with the S&P 500 index seem to suggest the possibility of additional information in our computed sector factors. The overwhelming and consistent trends of Figures 3 and 4 do not typically show up in a standard factor model.

We have only provided a simplified model of reality, though. There are two major problems with our sectors. Some large companies expand into more than one sector; Google, for example, is classified as a technology company, but has recently begun to make phones and cars—respectively, public utilities and transportation. Additionally, within each sector there are many subgroups. This is especially an important issue for sectors as large as technology, which encompasses diverse industries such as computer manufacturing and microwave devices. medical equipment, physician associations, and medical training. Future experiments should take these two issues into account.

The goal of any experiment is to apply the results. Our work only focuses on past data. In order to determine how useful our work in sector-based factor analysis is, it would be interesting to evaluate the performance of a stock portfolio where the risk estimation is based on our model in place of a standard factor model.

Stock will forever remain a mystery; there would be no point in the stock market if it could be perfectly figured out. We hope, though, that our work will help unshroud its mysteries just a little more.

6. Appendix

6.1. IBES sector classification

01:FINANCE 02:HEALTH CARE 03:CONSUMER NON-DURABLES 04:CONSUMER SERVICES 05:CONSUMER DURABLES 06:ENERGY 07:TRANSPORTATION 08:TECHNOLOGY 09:BASIC INDUSTRIES 10:CAPITAL GOODS 11:PUBLIC UTILITIES

6.2. EM for factor analysis

The expected likelihood for factor analysis is

where is a constant, and is the trace operator.

The last expression is quadratic in for each . This leads to the best optimal estimate for . It is also quadratic in each diagonal of , which leads to the best optimal estimate for (see [10] for more details.)

Acknowledgments. The authors would like to thank Prof. L.-H. Lim in the Department of Statistics at the University of Chicago for his invaluable mentorship, guidance, and encouragement while the authors were working on this project.

References

- [1] Bandalos, D.L.; Boehm-Kaufman, M.R. (2008). Four common misconceptions in exploratory factor analysis”. Statistical and Methodological Myths and Urban Legends: Doctrine, Verity and Fable in the Organizational and Social Sciences. Taylor & Francis. pp. 61–87.

- [2] Bartholomew, D.J.; Steele, F.; Galbraith, J.; Moustaki, I. (2008). Analysis of Multivariate Social Science Data. Statistics in the Social and Behavioral Sciences Series (2nd ed.). Taylor & Francis.

- [3] Barton, E.S.; Hallbauer, D.K. (1996). ”Trace-element and U–Pb isotope compositions of pyrite types in the Proterozoic Black Reef, Transvaal Sequence, South Africa: Implications on genesis and age”. Chemical Geology 133: 173–199.

- [4] Bregler, C. and Omohundro, S. M. (1994). Surface learning with applications to lip-reading. In Cowan, J. D., Tesauro, G., and Alspector, J., editors, Advances in Neural Information Processing Systems 6, pages 43-50. Morgan Kaufman Publishers, San Francisco, CA.

- [5] Brown, J. D.. ”Principal components analysis and exploratory factor analysis – Definitions, differences and choices.”. Shiken: JALT Testing & Evaluation SIG Newsletter. Retrieved 16 April 2012.

- [6] W. Cheng, Factor Analysis for Stock Performance. Professional Masters thesis, Worcester Polytechinic Institute, May, 2005.

- [7] Duda, R. O. and Hart, P. E. (1973). Pattern Classification and Scene Analysis. Wiley, New York.

- [8] Everitt, B. S. (1984). An Introduction to Latent Variable Models. Chapman and Hall, London.

- [9] Fabrigar et al. (1999). ”Evaluating the use of exploratory factor analysis in psychological research.”. Psychological Methods.

- [10] Ghahramani, Z. and Hinton, G. (1997). The EM Algorithm for Mixtures of Factor Analyzers. Technical Report CRG-TR-96-1, Department of Computer Science, University of Toronto.

- [11] Hochreiter, Sepp; Clevert, Djork-Arné; Obermayer, Klaus (2006). ”A new summarization method for affymetrix probe level data”. Bioinformatics 22 (8): 943–9.

- [12] Ledesma, R.D. and Valero-Mora, P. (2007). ”Determining the Number of Factors to Retain in EFA: An easy-to-use computer program for carrying out Parallel Analysis”. Practical Assessment Research & Evaluation, 12(2), 1–11

- [13] Love, D.; Hallbauer, D.K.; Amos, A.; Hranova, R.K. (2004). ”Factor analysis as a tool in groundwater quality management: two southern African case studies”. Physics and Chemistry of the Earth 29: 1135–43.

- [14] MacCallum, R. (June 1983). ”A comparison of factor analysis programs in SPSS, BMDP, and SAS”. Psychometrika 48 (48).

- [15] Meng, J. (2011). Uncover cooperative gene regulations by microRNAs and transcription factors in glioblastoma using a nonnegative hybrid factor model”. International Conference on Acoustics, Speech and Signal Processing.

- [16] Ritter, N. (2012). A comparison of distribution-free and non-distribution free methods in factor analysis. Paper presented at Southwestern Educational Research Association (SERA) Conference 2012, New Orleans, LA.

- [17] Rubin, D. and Thayer, D. (1982). EM algorithms for ML factor analysis. Psychometrika, 47(1):69–76.

- [18] Russell, D.W. (December 2002). ”In search of underlying dimensions: The use (and abuse) of factor analysis in Personality and Social Psychology Bulletin”. Personality and Social Psychology Bulletin 28 (12): 1629–46.

- [19] SAS Statistics. ”Principal Components Analysis”. SAS Support Textbook.

- [20] Schwenk, H. and Milgram, M. (1995). Transformation invariant autoassociation with application to handwritten character recognition. In Tesauro, G., Touretzky, D., and Leen, T., editors, Advances in Neural Information Processing Systems 7, pages 991-998. MIT Press, Cambridge, MA.

- [21] Spearman, C. (1904). ””General Intelligence,” Objectively Determined and Measured”. The American Journal of Psychology 15 (2): 201–292.

- [22] Sternberg, R.J. (1977). Metaphors of mind: Conceptions of the nature of intelligence. New York: Cambridge. pp. 85–111.

- [23] Suhr, D. (2009). ”Principal component analysis vs. exploratory factor analysis”. SUGI 30 Proceedings. Retrieved 05 April 2012.

- [24] Subbarao, C.; Subbarao, N.V.; Chandu, S.N. (December 1996). ”Characterisation of groundwater contamination using factor analysis”. Environmental Geology 28 (4): 175–180.