Maximum likelihood estimation for

stochastic differential

equations using

sequential kriging-based optimization

Grant Schneider1,3,

Peter F. Craigmile1,2,4 and

Radu Herbei1,5

1 Department of Statistics, The Ohio State University, Columbus, OH 43210, USA

2

School of Mathematics and Statistics,

University of Glasgow,

Glasgow,

Scotland

3schneider.393@osu.edu

4pfc@stat.osu.edu

5herbei@stat.osu.edu

Abstract: Stochastic Differential Equations (SDEs) are used as statistical models in many disciplines. However, intractable likelihood functions for SDEs make inference challenging, and we need to resort to simulation-based techniques to estimate and maximize the likelihood function. While sequential Monte Carlo methods have allowed for the accurate evaluation of likelihoods at fixed parameter values, there is still a question of how to find the maximum likelihood estimate. In this article we propose an efficient Gaussian-process-based method for exploring the parameter space using estimates of the likelihood from a sequential Monte Carlo sampler. Our method accounts for the inherent Monte Carlo variability of the estimated likelihood, and does not require knowledge of gradients. The procedure adds potential parameter values by maximizing the so-called expected improvement, leveraging the fact that the likelihood function is assumed to be smooth. Our simulations demonstrate that our method has significant computational and efficiency gains over existing grid- and gradient-based techniques. Our method is applied to modeling the closing stock price of three technology firms.

Keywords:

Discretely sampled diffusions;

Expected improvement;

Gaussian process;

Sequential Monte Carlo;

Parameter estimation.

1 Introduction

Many phenomena that arise in finance, biology, ecology, and other areas are modeled in continuous time using a real-valued diffusion process, , that is the solution to the stochastic differential equation (SDE)

| (1) |

where is the initial value of the process and is a standard Brownian motion. We assume that the drift and the diffusion functions, and respectively, are known up to the parameter vector , where is some compact set in . We further assume the drift and diffusion functions are locally Lipschitz with linear growth bounds so that a weakly unique solution to (1) exists. Suppose that we observe the process at time points where , and let . In this article we are interested in maximum likelihood estimation of and associated confidence bounds based on the data .

Let represent the conditional probability density of given evaluated at for a given set of parameters . Treating as fixed, we can then use the Markov property to write the likelihood of the data as the product of these individual transition densities

| (2) |

When the transition density is known, likelihood calculation and its maximization with respect to for a given set of data discretely observed from (1) is straightforward. As the transition density does not exist in closed-form except for a handful of cases, approximations are typically necessary; see for example Hurn et al., (2007) for a recent overview. These methods are often separated into four groups: (1) sequential Monte Carlo (SMC) (Pedersen,, 1995; Santa-Clara,, 1997; Elerian et al.,, 2001; Brandt and Santa-Clara, 2002b, ; Durham and Gallant,, 2002; Lin et al.,, 2010), (2) methods based on the exact simulation of diffusions (Beskos et al., 2006b, ), (3) closed-form Hermite expansions of the transition density (Aït-Sahalia,, 2002, 2008), and (4) approximations derived by numerically solving the Kolmogorov forward equation (Lo,, 1988).

Detailed discussions of the benefits of the method on which we choose to focus, SMC, may be found in Durham and Gallant, (2002); Brandt and Santa-Clara, 2002a ; Brandt and Santa-Clara, 2002b and a direct comparison to the Hermite expansion in Stramer and Yan, 2007b . In contrast to the other procedures, it does not require transforming (1) into an SDE of unit diffusion and it can be made arbitrarily accurate at the expense of more computation. One of our goals is to ease this computational burden associated with repeatedly obtaining Monte Carlo estimates of the log-likelihood over the parameter space. Much of the previous work has focused on efficiently estimating the likelihood at a fixed . An approximate MLE can then be obtained by maximizing this estimated likelihood over . In some cases, the derivatives of the log-likelihood with respect to can be obtained from the simulated values used to produce the estimate of the likelihood as in Stramer and Yan, 2007b and gradient ascent optimization is straightforward. Typically, however, these derivatives must be obtained numerically, which adds a significant computational burden. Although the underlying log-likelihood may be smooth as a function of , the Monte Carlo estimates will be subject to variability and thus will be much less amenable to derivative calculation.

We propose an efficient Gaussian-process-based method for exploring which accounts for the inherent Monte Carlo variability of the simulated likelihood method and does not require knowledge of the gradient of the log-likelihood. Our sequential method offers significant computational efficiency over a naive approach based on estimating the likelihood over a grid of possible parameter values. By using a global search criterion from computer experiments called the “expected improvement” (Jones et al.,, 1998; Schonlau et al.,, 1998; Williams et al.,, 2000), we alleviate difficulties with local maxima that may be encountered by gradient ascent methods. We obtain a sequential sample of parameter values, thus avoiding the need to use a regular grid for likelihood evaluation, through a kriging approach which allows for estimation of the MLE of and straightforward quantification of its uncertainty.

The paper is organized as follows. Section 2 introduces and discusses the SMC method for estimating the likelihood at fixed parameter values . Section 3 details our proposed sequential kriging-based optimization method that is used to find the MLE of and to construct confidence bounds for . In Section 4 we evaluate the performance of our MLE method through a simulation study. We apply our methodology to the modeling of the closing price of three technology stocks in Section 5. Conclusions and discussion are given in Section 6. A discussion of our choice of importance sampler is given in Appendix A.

2 Sequential Monte Carlo

Central to our approach is the ability to approximate the transition density , for each . Without loss of generality, it is sufficient to approximate for some . We use the Euler approximation given by

| (3) |

where is the density of a normal random variable with mean and variance evaluated at . In general, for large this approximation is inaccurate. As a remedy, we partition the interval into subintervals with endpoints , such that , and consider the unobserved points . The discretized transition density (see Kloeden and Platen,, 1992) is defined to be

| (4) |

where denotes the Lebesgue measure. We can use importance sampling to calculate (4) by calculating the expectation of the random variable with respect to the importance density , where .

We use a classical Monte Carlo estimator for this expectation, given by

| (5) |

where the variates are calculated based on independent and identically distributed (IID) draws . The construction of the discretized and estimated log-likelihoods is a straightforward application of the Markov property as in (2).

It is clear from (4) and (5) that selecting a good importance sampling density is very important. The optimal is the true joint density of given and (Stramer and Yan, 2007b, ), which is unavailable, as it depends on the transition density that we are trying to estimate. Pedersen, (1995) and Brandt and Santa-Clara, 2002b choose . In that case, simplifies to and (5) can be rewritten as

| (6) |

We note that simulating follows from sequentially simulating , for according to (3). Elerian et al., (2001) criticized (6) for its inefficiency and proposed a computationally intensive method of sampling from a multivariate Normal or distribution based on a second-order Taylor expansion. Exact simulation (Beskos and Roberts,, 2005; Beskos et al., 2006a, ; Beskos et al.,, 2008) presents an opportunity to sample from a that is exactly , but adds another layer of computational complexity (Bladt and Sørensen,, 2014). Similar to Pedersen’s method (6), the exact simulation method ignores , and thus suffers from efficiency issues.

As a compromise between the accuracy and the computational efficiency of estimating the log-likelihood, we choose to be the modified Brownian bridge sampler (Durham and Gallant,, 2002). This sampler produces values of conditional on and , which leads to an efficiency gain over Pedersen’s method and the exact simulation techniques. Further details of this sampler are given in Appendix A. An added benefit of using the modified Brownian bridge sampler is that guidance is available for the somewhat arbitrary choices of and . We set , as Stramer and Yan, 2007a show that this choice is computationally optimal for a fixed large amount of computer time. A recent extension, the guided-resampling version of the Brownian bridge sampler (Lin et al.,, 2010), may be used when depends strongly on or is large. As the original version of the modified Brownian bridge sampler is sufficient for our purposes, we avoid the bit of extra computation and set-up costs associated with the guided-resampling version.

We emphasize that although we choose to use the modified Brownian bridge sampler, the user is free to choose any desired before proceeding with our proposed method. The references above provide guidance for obtaining estimates at a fixed , but exploring the parameter space remains problematic. Although a very important practical issue, exploration methods have been typically ignored in the literature. A notable exception is in Lin et al., (2010), where the authors admit that their rough estimate of the smooth likelihood is not conducive to parameter estimation.

3 Kriging-Based Optimization

Our approach assumes that the discretized log-likelihood function, , is smooth in , but that the estimates of this function obtained via the Brownian bridge sampler (our SMC estimate) are subject to Monte Carlo variability. Rather than attempting to maximize the estimated function using a prohibitively large Monte Carlo sample, we propose a sequential optimization method that explicitly models the underlying smooth discretized log-likelihood using a Gaussian process (GP), while treating Monte Carlo variability as measurement error. Using kriging equations, parameter values are added sequentially by maximizing the so-called expected improvement, which balances the uncertainty in estimating the discretized log-likelihood at unexplored parameter values with the desire to find parameter values near the current maximum that have a higher log-likelihood.

More formally, given data from (1), we start by estimating the discretized log-likelihood at a range of parameters values, , that span the space of possible parameter values. For this purpose let denote the initial parameter values, selected using a space-filling design, such as a Latin hypercube. Letting denote the SMC-based estimate of , we assume for that

| (7) |

where is a set of independent of N(, ) errors.

We model using a GP with mean function and some valid covariance function , where are unknown parameters. There is an extensive literature on the choice of mean and covariance function for the GP (see Cressie and Wikle,, 2011; Santner et al.,, 2003) – richer choices can more accurately emulate the discretized log-likelihood, at a cost of necessitating larger sample sizes, , and more computational resources to faithfully model the features of the GP.

The sequential optimization procedure proceeds as follows. Given , we first find estimates of the parameters defining the GP above. Conditionally on , we predict the discretized log-likelihood for some . By Gaussianity of the GP and data model (7), the best linear unbiased prediction of is the kriging mean

| (8) |

with kriging variance

| (9) |

In the above equations is a mean vector of length with th element , is a covariance vector of length with th element , and is the covariance matrix with element . Let denote the maximum value of the kriging mean over the explored values. Then, the improvement (Jones et al.,, 1998) at is

| (10) |

but since is unknown we replace it by the expected improvement at parameter value , which can be shown to be equal to (Jones et al.,, 1998)

| (11) |

where is the standard Gaussian cumulative distribution function. As explained above, the expected improvement balances the need to maximize the discretized log-likelihood (the first term) and the uncertainty in estimating the log-likelihood (the second term).

Our sequential optimization scheme adds the parameter value that maximizes the expected improvement (11); details are given at the end of this section. We then estimate the discretized log-likelihood using SMC at that new parameter value, yielding and update the data and the GP parameter estimates . After updating the kriging mean (8) and kriging variance (9) using , we search for another parameter value that maximizes the expected improvement. We continue observing new estimated log-likelihood values and optimizing (11) to find more parameter values, until some stopping criteria is met. It is then straightforward to obtain the estimated MLE, , where is the total number of iterations in this procedure.

We can also obtain an approximate joint confidence region for directly from the kriging mean based on the likelihood ratio test:

| (12) |

where is the 1- quantile of a chi-square distribution with degrees of freedom. Given the GP parameters will be will be trivial to compute compared to . However as the dimension of , , grows obtaining the region in (12) may become difficult; in that case we can use a Rao-based confidence region of the form

| (13) |

where we can estimate the Fisher information, using the second derivative of with respect to evaluated at .

Estimating the parameters of the GP.

We now turn to estimating the parameters and conditionally on . These parameters may be updated in a variety of ways, including least squares, maximum likelihood, restricted maximum likelihood, and Bayesian methods. We adopt a Bayesian viewpoint and specify a prior distribution for the GP parameters. Throughout the paper we use the square bracket notation to denote “distribution of”. For notational simplicity, let and . Using Bayes’ rule,

| (14) |

The posterior distribution (3) can be explored and summarized in several ways. In our examples below, we take our estimates to be the mode of (3).

Maximizing the expected improvement.

Maximizing (11) may be done using either an optimization procedure (e.g. Nelder-Mead) or over a grid. If an optimization approach is used, to aid the exploration of over , the derivative of (11) with respect to can be shown to be

| (15) |

The derivatives and will depend on the mean and covariance functions of the chosen GP and may be calculated accordingly. The grid approach may be simpler to implement, but it should be noted that this will become computationally intensive as the dimension of grows. This will be similar to the problem with estimating over a fine grid, but it will occur at a slower rate because the computations involved in calculating expected improvement are simpler than those used to estimate the discretized log-likelihood. If a grid approach is used, adjustments should also be made to allow for replicates at a given .

Choosing a stopping rule.

We choose to stop adding points once we have observed no change to for five consecutive added points. As noted in Williams et al., (2000), expected improvement is not monotonically decreasing as points are added, so choosing a stopping rule may prove difficult. Possible alternative choices for stopping criteria may be based on a fixed number of points or small changes in . Alternatively, consecutively observing the maximum expected improvement over below some threshold is a viable strategy as well.

4 Simulation Results

We now use data simulated from two models to evaluate the performance of the sequential kriging-based optimization (SKBO) compared to naive space-filling designs in terms of accuracy and speed. We consider a “practical” naive space-filling design which estimates at points across . We choose to stop the sequential search when the estimate of changes by less than .01 in each direction for five consecutive iterations, or when we have sampled points, whichever occurs first, to provide a fair comparison to the naive method.

A common rule-of-thumb in the computer experiments literature is to use initial values based on a space-filling design. To investigate the role that the initial number of points plays, we perform SKBO based on and initial values. We also attempted to investigate the alternative strategy of using a large Monte Carlo sample to guide a steepest-ascent search, but even at this value of , in which the estimated values took 1000 times as long to obtain, the log-likelihood is not smooth enough for the optimization to converge.

As the choices of and will affect the shape of and the Monte Carlo variability which we estimate using , we consider two combinations of these values for each model. This practical choice is necessary for any SMC-based estimation, regardless of the strategy used to search . As the difference between and is of order (Bally et al.,, 1995), should be selected to be large enough to reduce this bias to some acceptable level, while keeping computational cost in mind. Once has been selected, we choose , which is the most efficient use of computational resources for the modified Brownian bridge sampler (Stramer and Yan, 2007a, ). We note that when and are specified to be large, it is even more important to carefully explore the parameter space, as each value is more difficult to obtain.

In the following simulations we choose and . We also assume where and . We find that even when these choices do not reflect reality, the sequential kriging-based optimization performs well. We used R (R Core Team,, 2013) for the implementation of SKBO and sped up the matrix calculations involved in calculating the expected improvement using C++ through the R package RcppArmadillo (Eddelbuettel and Sanderson,, 2013). We also used C to quickly obtain the modified Brownian bridge sample based on an adaptation of code in the R package sde (Iacus, 2009a, ), and the latin.hypercube function of the R package emulator (Hankin,, 2005) to obtain the initial grid over .

4.1 Ornstein-Uhlenbeck Process

We first consider the Ornstein-Uhlenbeck (OU) model (Uhlenbeck and Ornstein,, 1930) given by

| (16) |

where is the initial value of the process, and is a standard Brownian motion. Without loss of generality, we have assumed unit diffusion in (16). If this is not the case, (16) may be transformed into a process with unit diffusion via the Lamperti transform (see Iacus, 2009b, , for example). This process has a transition density that is available in closed-form, so we can use the true log-likelihood and MLE to evaluate the performance of SKBO and the naive method. We obtain our simulated data by first simulating from the stationary distribution of (16), given by We then sequentially simulate from the conditional distribution of (16), which is given by

| (17) |

where is chosen to be 1000 and , for . We use and for this analysis. After repeating the analysis for various combinations of and , we found the results presented below to be insensitive to the choice of these parameters.

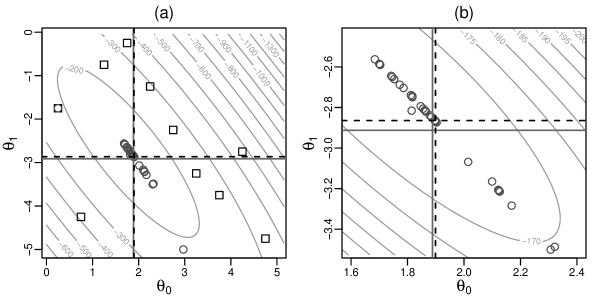

We first investigate how well the SKBO method finds the maximum for one simulated realization from (16). Panels (a) and (b) of Figure 1 displays, as a contour plot, the discretized log-likelihood for the realization of the OU process (Panel (b) is a zoomed in version of (a)). Looking at the figure, we can see that the likelihood is concentrated along a line of positive slope in the space. In Figure 1, the squares denote the initial sample of 10 points generated using a Latin hypercube and the circles denote the values added using SKBO method, maximizing the expected improvement as each new parameter value is added. The majority of the circles are concentrated along a ridge of high log-likelihood in the parameter space, which indicates that the method is able to isolate an estimate of the MLE. A few circles further away from the ridge have been added to decrease the uncertainty in estimating the discretized log-likelihood using the GP. On the figure the horizontal and vertical lines denote the exact MLEs (solid line) and SBO-based estimates (dashed line) of and , respectively. The estimates are close for this realization.

| , | , | |||||||||

| MLE | Naive | SKBO | Naive | SKBO | ||||||

| Initial pts | – | 50 | 2500 | 10 | 20 | 50 | 2500 | 10 | 20 | |

| Avg added | – | – | – | 24.9 | 13.4 | – | – | 21.7 | 10.6 | |

| Bias | 0.03 | 0.08 | 0.08 | 0.07 | 0.07 | 0.05 | 0.06 | 0.06 | 0.07 | |

| SD | 0.23 | 0.56 | 0.42 | 0.32 | 0.28 | 0.48 | 0.36 | 0.27 | 0.24 | |

| RMSE | 0.22 | 0.56 | 0.43 | 0.33 | 0.29 | 0.48 | 0.36 | 0.27 | 0.24 | |

| Bias | 0.06 | 0.12 | 0.13 | 0.07 | 0.05 | 0.08 | 0.09 | 0.05 | 0.07 | |

| SD | 0.28 | 0.66 | 0.55 | 0.42 | 0.36 | 0.61 | 0.47 | 0.35 | 0.31 | |

| RMSE | 0.29 | 0.67 | 0.57 | 0.43 | 0.36 | 0.61 | 0.48 | 0.35 | 0.32 | |

| Coverage | 98.1% | – | – | 75.6% | 84.5% | – | – | 82.9% | 88.6% | |

| Avg Time | – | 20.5 | 1030.7 | 20.8 | 18.6 | 164.9 | 8262.7 | 122.1 | 105.6 | |

Now we evaluate the general performance of SKBO-based estimation of relative to the exact MLE and naive space-filling methods. Table 1 compares the performance of each method as we vary the accuracy of the SMC approximation for the naive and SKBO methods (controlled by and – we compare with the case) and as we change the initial number of points sampled in the parameter space. For this simple process with parameters we are able to add a more computationally intensive design which samples points, a number that could prove to be computationally impractical for other processes.

In the table a number of different criteria are compared. To compare the quality of the estimates we summarize the bias, standard deviation (SD), and root mean square error (RMSE) for each method. The bootstrap standard error for the bias, SD, and RMSE is bounded above by 0.02. In addition to recording the average time to find the approximate MLE, and the number of points used initially for the SMC-based methods, we present the average number of points added for the SKBO method.

Comparing to the gold standard of the exact MLE, as expected, the approximate SMC-based methods (naive and SKBO methods) have a larger bias, SD, and RMSE. Accounting for the uncertainty of these measures, the SKBO method outperforms the naive space-filling methods, regardless of the choice of the number of initial points. Compared to the SKBO method the 2500-point naive method still has disappointing performance. Also, the SKBO method takes much less time and uses significantly less points (at least 32% less points on average) to get a better estimate than the naive space-filling method. In terms of obtaining a better estimate of the MLE using the SKBO method, we do better for a larger initial number of points, and we improve as the accuracy of the SMC approximation improves. Note that as we increase the approximation accuracy we need slightly less parameter values in total.

We also compared the coverage of 95% confidence regions for using the exact MLE with our SKBO-based method. The results are presented in the last line of Table 1. With 1000 replicates, testing that the coverage is equal to 95%, a rejection region for coverages is below 96.3% and above 96.4%. Thus the coverage for the exact MLE of 98.1% is too high. The SKBO-based coverages are too low, but the coverages increase to 88.6% as we increase the accuracy of the SMC approximation and we increase the initial number of points used. The accuracy of the SKBO-based estimate of the discretized log-likelihood will depend on the degree of difference between the specified GP model and the true log-likelihood. By focusing on the log-likelihood near the maximum, the shape of the confidence regions based on SKBO will be heavily influenced by the shape of the log-likelihood near the estimated peak. To the degree that the behavior of the log-likelihood near the maximum is not reflective of its behavior elsewhere, the confidence regions will be anti-conservative. Increasing the number of initial points alleviates this problem.

4.2 Generalized CIR Model

We now consider the generalized Cox-Ingersoll-Ross (GCIR) model, introduced in Chan et al., (1992), and analyzed in Roberts and Stramer, (2001). The process is defined by

| (18) |

where is the initial value of the process, , and is a standard Brownian motion. We note that (18) does not have a closed-form likelihood, except for when (the OU process) or (the Cox-Ingersoll-Ross model). To improve our exploration of the parameter space, we let and , and optimize over the real-valued parameters .

To simulate from the GCIR process we first simulate 100000 data points at time increments of 0.001 from (18) based on the Euler approximation with , , , and . Next, subsampling every 100 time points, we obtain a realization of length and sampling interval .

| , | , | ||||||

| Naive | SKBO | Naive | SKBO | ||||

| Initial pts | 100 | 20 | 40 | 100 | 20 | 40 | |

| Avg added | – | 60.3 | 47.0 | - | 56.2 | 46.3 | |

| Bias | 0.21 | 0.16 | 0.12 | 0.27 | 0.11 | 0.13 | |

| SD | 0.77 | 0.54 | 0.64 | 0.79 | 0.52 | 0.49 | |

| RMSE | 0.79 | 0.56 | 0.65 | 0.83 | 0.54 | 0.50 | |

| Bias | -0.06 | -0.10 | -0.05 | -0.10 | -0.08 | -0.11 | |

| SD | 1.11 | 0.80 | 0.85 | 1.05 | 0.72 | 0.76 | |

| RMSE | 1.11 | 0.81 | 0.85 | 1.06 | 0.72 | 0.77 | |

| Bias | 0.21 | 0.19 | 0.22 | 0.16 | 0.12 | 0.13 | |

| SD | 0.17 | 0.18 | 0.19 | 0.18 | 0.12 | 0.11 | |

| RMSE | 0.27 | 0.26 | 0.29 | 0.24 | 0.17 | 0.17 | |

| Bias | 0.21 | 0.25 | 0.18 | 0.18 | 0.22 | 0.22 | |

| SD | 0.83 | 0.75 | 0.79 | 0.87 | 0.79 | 0.71 | |

| RMSE | 0.85 | 0.80 | 0.81 | 0.89 | 0.82 | 0.74 | |

| Avg Time | 176.4 | 183.7 | 180.1 | 1430.0 | 1120.5 | 1245.5 | |

Table 2 compares the naive and SKBO methods for approximating the MLEs for the GCIR process. The format of the table is similar to that of Table 1, with the exception that we are not able to calculate an exact MLE. The table illustrates that the naive method and SKBO perform similarly with respect to estimating and when , but the SKBO method appears to slightly outperform the naive method when by these measures. For estimating and , similar to the OU case, SKBO noticeably outperforms the naive method, regardless of the accuracy of the SMC approximation. It is difficult to distinguish between the performance of the SKBO method on the basis of the number of initial points used. With a smaller initial design we evaluate less points on average, but the timing, bias, SD, and RMSE values are harder to discriminate. This suggests that the performance of the SKBO method can be improved by increasing the initial number of points up to some fixed number, but that there is relatively small benefit in increasing the initial number of points past this point. Overall we stress that this number (roughly 20 in both the OU and GCIR cases) is very small relative to the number of points required for the naive space-filling method.

5 An application to Modeling Stock Prices

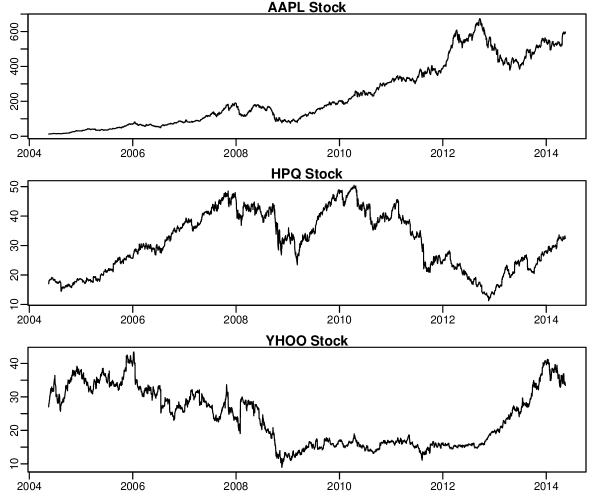

In this section we apply the methodology described above to modeling the stock price of three technology companies: Apple, Inc. (AAPL), Hewlett-Packard Co. (HPQ), and Yahoo! Inc. (YHOO). We consider the daily adjusted closing price of each stock from the ten-year period of May 17th, 2004 through May 16th, 2014 (2518 observations for each series). The data, shown graphically in Figure 2, were obtained from Yahoo! Finance (\urlhttp://finance.yahoo.com). All three series exhibit drift, local trends, and volatility.

An popular model for stock price is the geometric Brownian motion (GBM) process, which is the solution to

| (19) |

where is the initial closing price of the process, , and is a standard Brownian motion. Stock prices were modeled by (19) in the famous Black-Scholes model (Black and Scholes,, 1973) for option pricing and (19) is refered as “the model for stock prices” in Hull, (2012), a popular introductory finance text. We choose a sampling interval of as there are roughly 252 trading days per year. As the SDE described by (19) has a known transition density, we can compute the MLEs and the corresponding log-likelihood for each stock. These values are displayed in the columns of Table 3 with the heading “GBM”.

| GBM | Generalized GBM | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Stock | Log-lik. | AIC | Log-lik. | AIC | LRT stat. | |||||

| AAPL | 0.45 | 0.37 | -6797 | 13598 | 0.34 | 1.09 | 0.79 | -6740 | 13486 | 114 |

| HPQ | 0.12 | 0.33 | -2341 | 4686 | 0.30 | 1.27 | 0.61 | -2331 | 4668 | 20 |

| YHOO | 0.10 | 0.40 | -2149 | 4302 | 0.37 | 1.03 | 0.71 | -2135 | 4276 | 28 |

As a possible alternative model, we consider the generalized GBM given by the solution to

| (20) |

where is the initial closing price, , and is a standard Brownian motion. That is, we investigate whether the model for these three stock prices can be improved by allowing to differ from one. As (20) does not have a known transition density, we estimate the MLEs for each stock using SKBO with and . Once these estimated MLEs have been obtained, we estimate the log-likelihood using the modified Brownian bridge sampler with and . This highlights the important point that while the estimated MLE may be obtained for fairly small values of and , estimating the log-likelihood accurately will typically require larger values. Also, while the kriging mean is very useful for guiding the search of , we do not use it to estimate the maximized log-likelihood as this would essentially be underestimating the maximum using a mean. The parameter estimates and (estimated) maximized likelihood values are displayed in the columns of Table 3 with the heading “Generalized GBM”.

The log-likelihood for the generalized GBM model is higher than that modeled for the GBM for each of the three stock series. Evaluating the two models based on the Akaike Information Criterion (AIC), after accounting for an extra parameter, the generalized GBM model outperforms the usual GBM model for each of these three stocks. Using the fact that the models are nested, we can also compute the likelihood ratio statistic (LRT) to test the null hypothesis that the GBM model fits sufficiently well to each stock prices series versus the alternative hypothesis that the generalized GBM is required. The LRT statistics given in the last column of Table 3 confirm that the generalized model is more reasonable for all three series. We conclude that the future volatility in all of these technology stocks is dependent on the discounted current stock price.

6 Discussion and Future Work

In this research we introduce a sequential, kriging-based optimization strategy which provides a derivative-free method for approximating the MLE in SDE models, in cases where the likelihood function cannot be evaluated exactly, but can be estimated with some degree of statistical accuracy. Our work is primarily motivated by the case where the data are discrete-time observations of an SDE; however, what we suggest can be extended to other settings without difficulty. We judge the performance of our approach on two fronts: (1) statistical accuracy, as measured by the bias, SD, and RMSE of the estimated MLE, and (2) computational efficiency. Our findings show that the proposed method outperforms space-filling competitors, even in the cases where these methods use significantly more likelihood evaluations.

A significant component of the SKBO method is the assumption that the unobserved likelihood is a realization of a certain GP, specified via its mean and covariance structure. The validity of this assumption is difficult to establish. However, in the cases where we do have access to the exact likelihood function we do not find any evidence to disprove it. On the other hand, the Gaussian assumption offers the significant advantage of yielding a closed form expression for the expected improvement. In addition, the GP-method allows us to provide measure of uncertainty for our estimates (the MLE and the underlying estimates of the likelihood function). For the examples discussed above, we use simple and popular parametric functions to describe this underlying GP. We show that even a naive formulation leads to impressive results. We do however acknowledge that the parameterization of the GP process may be crucial in certain applications. For examples with a more involved log-likelihood function, a non-stationary GP process may be necessary to improve the estimation of the MLE. With more sophisticated GP processes, we would need to sample more parameter values to learn about the unknown log-likelihood function and its inherent uncertainty. We take a Bayesian viewpoint to learn and update the GP parameters, thus naturally incorporating uncertainty and allowing us to take advantage of prior knowledge.

From a computational perspective, we identify two bottlenecks: (1) maximizing the expected improvement and (2) updating the structure of the underlying GP given that a new parameter has been added to the procedure. For a specific application one can use state of the art software to reduce the computational overhead in each case. In the applications presented in this paper we implement the SKBO method using multi-core R routines. This is done in order to allow for a fair comparison to other approaches. Our method lends itself naturally to parallel computing, given that we make heavy use of Monte Carlo and importance sampling techniques. Thus, we expect that a more sophisticated approach which uses several CPUs or even a Graphical Processing Unit may offer significant improvements.

Modern statistical applications involve observational models with ever increasing complexity. In many cases, an exact evaluation of the likelihood function is impossible and thus one is forced to use an array of approximations. Our proposed method offers several advantages, making it a valuable addition to the MLE toolbox. We are currently investigating its application to the analysis of other statistical models.

Acknowledgments.

Thank you to Professor Thomas Santner for constructive discussions on this work. Herbei is supported in part by the US National Science Foundation under grant DMS-1209142.

Appendix A Appendix A

As noted in Stramer and Yan, 2007a , may have unbounded variance, causing the sampler to be inefficient. A common claim in the existing literature is that increasing will decrease the discretization error (bias) and increase the Monte Carlo error (variability) while increasing will reduce the variability. However, we have found that for any , increasing past some optimal choice actually increases the bias in the estimated likelihood. This problem grows worse as , the amount of data, increases. In Brandt and Santa-Clara, 2002b , the convergence of the simulated MLE to the true MLE is shown when , , and . The true MLE in turn converges to the true parameter vector as . From our investigation, the likelihood is most biased when is small and is large (which may or may not be reflected in the simulated MLE).

Durham and Gallant, (2002) propose two Monte Carlo samplers based on Brownian bridges. The Brownian bridge sampler is defined to be the Euler approximation of the solution to

| (21) |

For a constant , is a Brownian bridge on from to .

The modified Brownian bridge sampler is introduced based on the recursion

| (22) |

where , , and . Note that this sampler is identical to (21) except for the term in the variance. The authors state “it is not entirely obvious that this should be the case, [but] we will see that this modification results in much better performance”. To lend support to the heuristic arguments justifying (22), Stramer and Yan, 2007b show that when is constant, the modified Brownian bridge is also exactly a Brownian bridge on from to . As discussed in Chib and Shephard, (2002), based on this scheme can be interpreted as a simple Euler approximation multiplied by the expected value of the ratio of two predictive densities.

References

- Aït-Sahalia, (2002) Aït-Sahalia, Y. (2002). Maximum likelihood estimation of discretely sampled diffusions: A closed-form approximation approach. Econometrica, 70:223–262.

- Aït-Sahalia, (2008) Aït-Sahalia, Y. (2008). Closed-form likelihood expansions for multivariate diffusions. The Annals of Statistics, 36:906–937.

- Bally et al., (1995) Bally, V., Talay, D., et al. (1995). The law of the euler scheme for stochastic differential equations: Ii. convergence rate of the density. Rapport De Recherche-Institut National De Recherche En Informatique Et En Automatique.

- (4) Beskos, A., Papaspiliopoulos, O., and Roberts, G. O. (2006a). Retrospective exact simulation of diffusion sample paths with applications. Bernoulli, 12:1077–1098.

- Beskos et al., (2008) Beskos, A., Papaspiliopoulos, O., and Roberts, G. O. (2008). A factorisation of diffusion measure and finite sample path constructions. Methodology and Computing in Applied Probability, 10:85–104.

- (6) Beskos, A., Papaspiliopoulos, O., Roberts, G. O., and Fearnhead, P. (2006b). Exact and computationally efficient likelihood-based estimation for discretely observed diffusion processes. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 68:333–382.

- Beskos and Roberts, (2005) Beskos, A. and Roberts, G. O. (2005). Exact simulation of diffusions. The Annals of Applied Probability, 15:2422–2444.

- Black and Scholes, (1973) Black, F. and Scholes, M. (1973). The pricing of options and corporate liabilities. The journal of political economy, pages 637–654.

- Bladt and Sørensen, (2014) Bladt, M. and Sørensen, M. (2014). Simple simulation of diffusion bridges with application to likelihood inference for diffusions. Bernoulli, 20:645–675.

- (10) Brandt, M. W. and Santa-Clara, P. (2002a). Numerical techniques for maximum likelihood estimation of continuous-time diffusion processes: Comment. Journal of Business & Economic Statistics, 20:321–24.

- (11) Brandt, M. W. and Santa-Clara, P. (2002b). Simulated likelihood estimation of diffusions with an application to exchange rate dynamics in incomplete markets. Journal of financial economics, 63:161–210.

- Chan et al., (1992) Chan, K. C., Karolyi, G. A., Longstaff, F. A., and Sanders, A. B. (1992). An empirical comparison of alternative models of the short-term interest rate. The Journal of Finance, 47:1209–1227.

- Chib and Shephard, (2002) Chib, S. and Shephard, N. (2002). Numerical techniques for maximum likelihood estimation of continuous-time diffusion processes: comment. Journal of Business & Economic Statistics, 20:325–27.

- Cressie and Wikle, (2011) Cressie, N. and Wikle, C. K. (2011). Statistics for spatio-temporal data. John Wiley & Sons, New York.

- Durham and Gallant, (2002) Durham, G. B. and Gallant, A. R. (2002). Numerical techniques for maximum likelihood estimation of continuous-time diffusion processes. Journal of Business & Economic Statistics, 20:297–316.

- Eddelbuettel and Sanderson, (2013) Eddelbuettel, D. and Sanderson, C. (2013). RcppArmadillo: Accelerating R with high-performance C++ linear algebra. Computational Statistics and Data Analysis, in press.

- Elerian et al., (2001) Elerian, O., Chib, S., and Shephard, N. (2001). Likelihood inference for discretely observed nonlinear diffusions. Econometrica, 69:959–993.

- Hankin, (2005) Hankin, R. K. S. (2005). Introducing BACCO, an R bundle for Bayesian Analysis of Computer Code Output. Journal of Statistical Software, 14.

- Hull, (2012) Hull, J. C. (2012). Options, futures, and other derivatives. Pearson/Prentice Hall, Boston.

- Hurn et al., (2007) Hurn, A. S., Jeisman, J. I., and Lindsay, K. A. (2007). Seeing the wood for the trees: A critical evaluation of methods to estimate the parameters of stochastic differential equations. Journal of Financial Econometrics, 5:390–455.

- (21) Iacus, S. M. (2009a). sde: Simulation and inference for stochastic differential equations. R package version 2.0.10.

- (22) Iacus, S. M. (2009b). Simulation and inference for stochastic differential equations: with R examples, volume 1. Springer, New York.

- Jones et al., (1998) Jones, D. R., Schonlau, M., and Welch, W. J. (1998). Efficient global optimization of expensive black-box functions. Journal of Global optimization, 13:455–492.

- Kloeden and Platen, (1992) Kloeden, P. E. and Platen, E. (1992). Numerical solution of stochastic differential equations, volume 23. Springer.

- Lin et al., (2010) Lin, M., Chen, R., and Mykland, P. (2010). On generating Monte Carlo samples of continuous diffusion bridges. Journal of the American Statistical Association, 105:820–838.

- Lo, (1988) Lo, A. W. (1988). Maximum likelihood estimation of generalized Itô processes with discretely sampled data. Econometric Theory, 4:231–247.

- Pedersen, (1995) Pedersen, A. R. (1995). A new approach to maximum likelihood estimation for stochastic differential equations based on discrete observations. Scandinavian Journal of Statistics, 22:55–71.

- R Core Team, (2013) R Core Team (2013). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria.

- Roberts and Stramer, (2001) Roberts, G. O. and Stramer, O. (2001). On inference for partially observed nonlinear diffusion models using the Metropolis-Hastings algorithm. Biometrika, 88:603–621.

- Santa-Clara, (1997) Santa-Clara, P. (1997). Simulated likelihood estimation of diffusions with an application to the short term interest rate. Technical report, Anderson Graduate School of Management, UCLA.

- Santner et al., (2003) Santner, T. J., Williams, B. J., and Notz, W. I. (2003). The design and analysis of computer experiments. Springer, New York.

- Schonlau et al., (1998) Schonlau, M., Welch, W. J., Jones, D. R., et al. (1998). Global versus local search in constrained optimization of computer models. In New Developments and Applications in Experimental Design, pages 11–25. Institute of Mathematical Statistics.

- (33) Stramer, O. and Yan, J. (2007a). Asymptotics of an efficient Monte Carlo estimation for the transition density of diffusion processes. Methodology and Computing in Applied Probability, 9:483–496.

- (34) Stramer, O. and Yan, J. (2007b). On simulated likelihood of discretely observed diffusion processes and comparison to closed-form approximation. Journal of Computational and Graphical Statistics, 16:672–691.

- Uhlenbeck and Ornstein, (1930) Uhlenbeck, G. E. and Ornstein, L. S. (1930). On the theory of the Brownian motion. Physical review, 36:823.

- Williams et al., (2000) Williams, B. J., Santner, T. J., and Notz, W. I. (2000). Sequential design of computer experiments to minimize integrated response functions. Statistica Sinica, 10:1133–1152.