Importance Sampling and Statistical Romberg Method for Lévy Processes

Abstract

An important family of stochastic processes arising in many areas of applied probability is the class of Lévy processes. Generally, such processes are not simulatable especially for those with infinite activity. In practice, it is common to approximate them by truncating the jumps at some cut-off size (). This procedure leads us to consider a simulatable compound Poisson process. This paper first introduces, for this setting, the statistical Romberg method to improve the complexity of the classical Monte Carlo one. Roughly speaking, we use many sample paths with a coarse cut-off , and few additional sample paths with a fine cut-off . Central limit theorems of Lindeberg-Feller type for both Monte Carlo and statistical Romberg method for the inferred errors depending on the parameter are proved. This leads to an accurate description of the optimal choice of parameters with explicit limit variances. Afterwards, the authors propose a stochastic approximation method of finding the optimal measure change by Esscher transform for Lévy processes with Monte Carlo and statistical Romberg importance sampling variance reduction. Furthermore, we develop new adaptive Monte Carlo and statistical Romberg algorithms and prove the associated central limit theorems. Finally, numerical simulations are processed to illustrate the efficiency of the adaptive statistical Romberg method that reduces at the same time the variance and the computational effort associated to the effective computation of option prices when the underlying asset process follows an exponential pure jump CGMY model.

MSC 2010: 60E07, 60G51, 60F05, 62L20, 65C05, 60H35.

Keywords: Lévy processes, Esscher transform, Monte Carlo, Statistical Romberg, Variance reduction, Central limit theorems, CGMY model.

1 Introduction

Lévy processes arise in many areas of applied probability and specially in mathematical finance, where they become very fashionable since they can describe the observed reality of financial markets in a more accurate way than models based on Brownian motion (see e.g. Cont and Tankov [8] and Shoutens [27]). In particular in the pricing of financial securities we are interested in the computation of the real quantity , , where is a -valued pure jump Lévy process, and is a given function. In the literature, the computation of this quantity involves three types of methods: Fourier transform methods, numerical methods for partial integral differential equations and Monte Carlo methods. It is well known that the two first methods can not cope with high dimensional problems. This gives a competitive edge for Monte Carlo methods in this setting. Therefore, the focus of this work is to study improved Monte Carlo methods using the statistical Romberg algorithm and the importance sampling technique. The statistical Romberg method is known for reducing the time complexity and the importance sampling technique is aimed at reducing the variance.

The Monte Carlo method consists of two steps. In the first step, we approximate the Lévy process by a simulatable Lévy process with . If denotes the Lévy measure of the Lévy process under consideration, then it is common to take with Lévy measure and . This approximation is nothing but a compound Poisson process. In the second step, we approximate by where is a sample of independent copies of . Therefore, this Monte Carlo method (MC) is affected respectively by an approximation error and a statistical one

On one hand, for a Lipschitz function we have where (see relation (6) for more details). On the other hand, the statistical error is controlled by the central limit theorem with order . Hence, optimizing the choice of the sample size in the Monte Carlo method leads to . Moreover, if we choose we prove a central limit theorem of Lindeberg-Feller type (see Theorem 3.1). Therefore, if we denote by the cost of a single simulation of , then the total time complexity necessary to achieve the precision is given by (see subsection 3.3).

In order to improve the performance of this method we use the idea of the statistical Romberg method introduced by Kebaier [18] in the setting of Euler Monte Carlo methods for stochastic differential equations driven by a standard Brownian Motion which is also related to the well known Romberg’s method introduced by Talay and Tubaro in [28]. Inspired by this technique, we introduce a novel method for the computation of our initial target. The main idea of this new method is to consider two cut-off sizes and , and then approximate by

The samples and have to be independent of . Moreover, for , the process is nothing else the sum of and an independent Lévy process with Lévy measure which is also simulatable as a compound Poisson process. This new method will be referred as the statistical Romberg method (SR). Additionally, like for the MC method, we prove a central limit theorem of Lindeberg-Feller type for the SR algorithm with and (see Theorem 3.2). Then, according to subsection 3.3, the total time complexity necessary to achieve the precision is given by . It turns out that the complexity ratio vanishes as goes to zero.

Since the efficiency of the Monte Carlo simulation considerably depends on the smallness of the variance in the estimation, many variance reduction techniques were developed in the recent years. Among these methods appears the technique of importance sampling very popular for its efficiency. For the Gaussian setting, the importance sampling technique was studied by Arouna [1], Galasserman, Heidelberger and Shahabuddin [15] for MC method and by Ben Alaya, Hajji and Kebaier [3] for SR method. Concerning Lévy process without a Brownian component, Kawai [17] has already applied this technique for MC algorithm using the Esscher transform which is nothing but the well known exponential tilting of laws. From a practical point of view, his approach is exploitable only when the Lévy process is simulatable without any approximation. Note also that in his study there is no results on the rate of convergence of the obtained algorithm.

The main aim of the present work is to apply the idea of [17] to the approximation Lévy process for both MC and SR algorithms and to study the inferred error in terms of the cut-off ; a question which has not been addressed in previous research. Roughly speaking, thanks to the Esscher transform we produce a parametric transformation such that for all we have where is a suitable subset of and is a real function taking values in . Concerning the MC method it looks natural to implement the method with However, for the SR method the inferred error is controlled by . Then, in this case, it is natural to implement the first (resp. the second) empirical mean appearing in the SR estimator with (resp. . But what about the effective computation of ? To answer this question, we use a constrained version of the well-known stochastic approximation Robbins-Monro. All these ideas led us to introduce two new methods based on adaptive approximations. The first method concerns a combination of an adaptive importance sampling technique and the MC method that will be called Importance Sampling Monte Carlo method (ISMC) (see relation (22)). The second one concerns an original combination of an adaptive importance sampling technique with the SR algorithm that will be referred as Importance Sampling Statistical Romberg method (ISSR) (see relation (26)). The main point in favor of the ISSR method is that it inherits the variance reduction from the Importance sampling procedure and the complexity reduction from the SR method. A complexity analysis is also provided.

The rest of the paper is organized as follows. Section 2 introduces the general framework and recalls some useful results. In section 3, the central limit theorems of Lindeberg-Feller type are proved for both MC and SR methods (see Theorems 3.1 and 3.2). Similar results are derived for the setting of an exponential Lévy model (see Corollaries 3.1 and 3.2). A complexity analysis is included. In section 4, we recall the Esscher transform and the principle of importance sampling technique for the SR method. For and , we prove the convergence of the optimal choice to the optimal choice associated to the limit model (see Theorem 4.1). In section 5, we first study, for , the almost sure convergence of the stochastic recursive constrained Robbins-Monro algorithm given by the double indexed sequence as and (see Theorems 5.1 and 5.2 and Corollary 5.1). The rest of this section is devoted to prove the central limit theorems of Lindeberg-Feller type for both adaptive ISMC and ISSR methods (see Theorems 5.3 and 5.4). Section 6 illustrates the superiority of the ISSR method over all the other ones via numerical examples for both one and two-dimensional Carr, Geman, Madan and Yor (CGMY) process [6]. Finally, the last Section is devoted to discuss some future openings.

2 General Framework

We denote by our underlying probability space. A stochastic process on with values in such that is a Lévy process if it has independent and stationary increments. We endow the probability space with the canonical filtration where . The characteristic function of a Lévy process with generating triplet is given by the well known Lévy Kintchine representation

where , is a symmetric non-negative-definite matrix and is a Lévy measure on verifying . (Given vectors and , denotes the inner product of and associated to the Euclidean norm ). In this paper, we are interested in studying pure-jump Lévy processes, that is, we set throughout all the paper.Then, is a Lévy process with generating triplet . The simulation of a Lévy process with infinite Lévy measure is not straightforward. From the Lévy-Itô decomposition (see e.g. Theorem 19.2 in Sato [26]), we know that can be represented as a sum of a compound Poisson process and an almost sure limit of compensated compound Poisson process where for

| (1) |

Note that without the compensation , the sum of jumps may not converge as goes to zero. We denote the approximation error by

| (2) |

The process is also a Lévy process independent of with characteristic function

Consequently, and the variance-covariance matrix where

( denotes the transpose of a matrix ). The asymptotic behavior of the distribution of is firstly studied by Asmussen and Rosiński [2] in the one dimensional case and later extended to the multidimensional case by Cohen and Rosiński [7]. Throughout this paper is a standard Brownian motion in independent of .

Theorem 2.1.

Under the above notation, suppose that is invertible for every . Then as ,

if and only if for each

| (3) |

Here stands for the convergence in distribution.

If is given in polar coordinates by where is a measurable family of Lévy measures on and is a finite measure on the unit sphere , then

If we define and , then

| (4) |

Remark 1.

In the one dimensional case Assmussen and Rosiński [2] have obtained the convergence of to a standard Brownian motion if and only if for each , which is satisfied as soon as (see Theorem 2.1 and Proposition 2.1 in [2]). An extension to this sufficient condition in the multidimensional case is given by Theorem 2.5 in Cohen and Rosiński [7]. Suppose that the support of the measure is not contained in any proper linear subspace of , they proved that if

| (5) |

On the other hand, according to Proposition 2.1 of Dia [9], we have a -upper bound of the error approximation in the one dimensional case for any real . This result on the strong error approximation remains valid for the multidimensional case. More precisely, if we consider the -dimensional error Lévy process given by relation (2), then we can easily deduce that

| (SE) |

Concerning the weak error, if denotes a real valued Lipschitz continuous function with Lipschitz constant , then it is easy to see that

| (6) |

Moreover, under some regularity conditions on function we can obtain an expansion of the weak error as in Proposition 2.2 and Remark 2.3 of [9]. So, it is worth to introduce the following assumption: there exist and as such that

| () |

We recall, in what follows, an important moment property of Lévy processes. For this, we introduce before the below definition.

Definition 2.1.

A function is said to be submultiplicative if there exists a positive constant such that for . The product of two submultiplicative functions is also submultiplicative.

Theorem 2.2 (Sato [26], Theorem 25.3).

Let be a submultiplicative, locally bounded, measurable function on , and let be a Lévy process in with Lévy measure . Then, is finite for every if and only if .

3 Statistical Romberg method and Lévy process

In this section, we establish two central limit theorems of Lindeberg-Feller type, for the inferred errors associated to MC and SR algorithms, in terms of the cut-off . Similar results are derived for the setting of an exponential Lévy model. We also provide a complexity analysis for both algorithms.

3.1 Central limit theorem for the MC method

Proof.

At first, we write the total error as follows

Assumption () ensures that . Concerning the first term on the right hand side of the above relation, as depends on we plan to apply the Lindeberg-Feller central limit theorem (see Theorem 8.1).

In order to do that, we set

and we check assumptions and of Theorem 8.1.

Thus, the proof is divided into two steps.

Step 1. For assumption , it is straightforward that . Then, by the almost sure convergence of toward , the continuity of function and the uniform integrability condition given by , we obtain

| (8) |

Step 2. Concerning the Lyapunov condition , for , we have

Once again by the same arguments used in the previous step we prove the convergence of toward as tends to zero. Since , we obtain

| (9) |

By (8) and (9), we obtain thanks to Theorem 8.1 the desired convergence in law. ∎

In the corollary below, we will treat the special case where for all and is a Lipschitz continuous function. In finance this model is well known as an exponential Lévy model.

Corollary 3.1.

Assume that is finite for . Then, in the setting of an exponential Lévy model there is such that . Moreover, if we choose , with , then

| (10) |

Proof.

We denote by the exponential function element-wise of the vector , . Let denote the Lipschitz constant of function , since and are independent we obtain by standard calculations

Now, on the one hand thanks to Theorem 2.2, the assumption ensures the finiteness of . On the other hand by virtue of Lemmas 25.6 and 25.7 in Sato [26] we have the boundedness of . Concerning the term , we have , this last upper bound can be written as a sum of finite number of exponential functions evaluated at points which are a linear combination of the components of the vector . Therefore there exists a family of -valued vectors, such that

Note that the finiteness of the above upper bound is once again ensured by Lemmas 25.6 and 25.7 in Sato [26]. Since its limit exists we deduce that is finite. Now, thanks to the linear growth of and using the same arguments as above we check in the same manner the property . Hence, if we choose then Theorem 7 applies and this completes the proof. ∎

3.2 Central limit theorem for the SR method

We use the SR method to approximate by

Theorem 3.2.

Proof.

At first we write the total error as with

So, assumption () yields the convergence of toward as goes to zero and following step by step the proof of Theorem 7 the convergence law of to the normal distribution is easily obtained. Concerning the term , we plan to use Theorem 8.1 and we set In the following two steps, we will check assumptions and of Theorem 8.1.

Step 1. It is straightforward that . Now applying Taylor-Young’s expansion to the real valued function we get

where as . Now, by applying twice Theorem 2.1 to and and thanks to assumption we obtain . Since is independent from and , we obtain

| (11) |

For the second term, using the tightness of we deduce that Thanks to the inequality , for any , and we deduce the uniform integrability of . Therefore, we obtain the first condition

Step 2. For the Lyapunov condition, let , we get by standard evaluations

Once again we use the convergence in distribution given by relation (11) and the uniform integrability property to deduce the convergence of toward . Finally, since , we conclude that with . This gives the asymptotic normality of and completes the proof. ∎

Now, we get back to the exponential Lévy model setting introduced before Corollary 3.1 where for a given Lipschitz continuous function . Our aim is to deduce in this setting a central limit theorem for SR method.

Corollary 3.2.

Assume that is finite for . In the setting of an exponential Lévy model there is such that . Moreover, assume that for there exists such that , for all and condition of Theorem 3.2 is satisfied. Then, if we choose and we obtain

Proof.

According to Theorem 3.2 and Corollary 3.1 we only need to check that assumption is satisfied. Since is Lipschitz it is sufficient to find an upper bound for . To do so, we use the independence of and the couple and Cauchy-Schwartz’s inequality to get

By the same arguments given in the proof of Corollary 3.1 we have the finiteness of , and . Combining all these results together with assumption (SE) we deduce the existence of a constant not depending on such that

This completes the proof since , for . ∎

3.3 Complexity Analysis

Thanks to the above limit results we are able now to provide a complexity analysis for both MC and SR algorithm. To keep things simple, we consider the particular case , and we assume that the measure has a density of the form for a small , where is a slowly varying as and . Observe that the positive (resp. negative ) part of the approximation is essentially a compound Poisson process with intensity (resp. ). Then, the cost necessary of a single simulation is random, with expectation of order Hence, according to Theorem 3.1 the time complexity of the MC method necessary to achieve a total error of order is random with expectation of order

In the same way, thanks to Theorem 3.2 the time complexity of the SR method necessary to achieve a total error of order is random with expectation of order

By Karamata’s theorem (see e.g. Bingham, Goldie and Teugels [5] or Feller [14] )

Similarly we have

Consequently, we compute the time complexity ratio given by

If is constant in the neighborhood of zero, like for the CGMY model (see relation (28)), then we easily get

Optimizing the order of this last quantity yields which leads us to a gain of a complexity of order that asymptotically increases as soon as becomes small.

4 Importance Sampling and Statistical Romberg method

Let be a Lévy process in under the probability with generating triplet . We define the set

| (12) |

where the second equality holds by Theorem 2.2. Thanks to the convexity of the exponential function it is straightforward that the set is convex. In view to use importance sampling routine, based on exponential tilting, we define the family of , as all the equivalent probability measures with respect to such that

whee denotes the cumulant generating function given by . Under , the stochastic process is still a Lévy process with the exponential tilted triplet where and (see e.g. Cont and Tankov [8]). Hence, we obtain If we introduce the Lévy process with generating triplet under , then the random variable under has the same law as under and we get

Further, one can use this importance sampling twice in the SR algorithm with considering and in and approximate by

Miming the proof of Theorem 3.2 we establish a central limit theorem with limit variance Since (resp. ) under has the same law as under (resp. ) we rewrite this variance using once again the Esscher transform as

Hence, let us introduce for ,

| (13) |

Our aim now is to minimize separately these two quantities. To do so, for , we introduce a first set

to ensure the existence of and a second set

to make sens for the first and second derivatives of . For , if we assume that , then the convexity of sets and can be proved in a similar manner to the proof of Lemma 2.2 in [17]. Moreover, we prove the convexity of , .

Proposition 4.1.

Let . Assume Then, is a strictly convex function on and where

| (14) |

Proof.

For a fixed , the function is almost surely differentiable on with a first derivative equal to . Further, according to the properties of the moment generating function, the function is finite for and is differentiable with provided that is finite. Using Hölder’s inequality, this last condition is satisfied as soon as . In the same way, we prove that is of class on and we get for all ,

Note that is nothing but the variance-covariance matrix of the random vector under the probability measure and it is clearly definite positive. Finally, since , we conclude that is strictly convex on .

For , the same result holds for the approximated Lévy process by considering the associated sets , and and functions and , , with the canonical filtration defined by .

Proposition 4.2.

Let . Assume then the function is of class and strictly convex on with .

Now, let us introduce for

| (15) |

Our aim now is to study for the convergence of toward as tends to zero. For , we define the set

| (16) |

Remark.

-

1.

It is worth to note that for and we have . We also have for all .

-

2.

Further, for , if , , is finite then by Hölder’s inequality we easily get for all . The same result holds for the approximated Lévy process. Indeed, for , we have provided that .

According the above remark, choosing with ensures that will belong to the domain of convexity of both and . On the other hand it also guarantees the finiteness of the quantity which will be needed in each proof assuming condition .

In what follows, let denote the set of all interior points of a given set . We have the following result.

Theorem 4.1.

Let . Suppose that is continuous, that is for the case the function is continuous and for the function is of class . Moreover, assume , for all and there exists such that and are finite. Let be a compact set such that with and assume that the sequence . Then,

We prove Theorem 4.1 after the following technical lemma.

Lemma 4.1.

Let be a compact subset of with , we have is uniformly bounded in .

Proof.

Let us consider the two independent Lévy processes and and the submultiplicative function . There exists depending only on such that for any and

Since the function is continuous on the second expectation on the right hand side is uniformly bounded on . Concerning the first expectation, we start by establishing the uniform convergence of toward , where and denote the cumulant generating functions of respectively and . According to the Lévy Kintchine decomposition, we have and thanks to Taylor’s expansion we get

| (17) |

This ensures the uniform convergence of the family functions on any compact set of . Note that for all we have with some depending only on . This last upper bound can be written as a sum of finite number of exponential functions evaluated at points which are a linear combination of the components of the vector . Therefore there exists a family of deterministic -valued vectors, such that

Each term in the above sum is nothing else which in turn converges to as tends to zero. This gives us the desired claim. ∎

Proof of Theorem 4.1.

Let and be a sequence decreasing to zero. Note that is a -bounded sequence. So, we only need to prove that for any subsequence , if then . According to Proposition 4.2 above we have

Now, let , it is easy to check that , so by applying Hölder’s inequality we get

Note that . Hence, to get the uniform integrability it is sufficient to prove that the first expectation on the right hand side of the above inequality is uniformly bounded on and . Indeed, using the almost sure convergence of toward and the continuity of function , we easily get

and then we complete the proof using the uniqueness of the minimum ensured by Proposition 4.1. Consequently, noticing that , it remains now to prove the uniform boundedness of the quantity To do so, we establish first the uniform convergence of toward . According to the decomposition given by relation (2), we have that By Taylor’s expansion we deduce

| (18) |

Hence, the family functions is equicontinuous on any compact subset of and we deduce the convergence of toward when tends to infinity. Noticing that , we use once again the equicontinuity of on the compact set to get and then the problem is reduced to prove the uniform boundedness of which is ensured by Lemma 4.1. ∎

5 The adaptive procedure

5.1 Stochastic algorithms

The aim now is to construct family sequences converging almost surely to the optimal limits and of the previous section. For this, let (resp. , ), be i.i.d copies of the -valued random variable (resp. ). Let be a compact convex subset of with . For fixed and , we construct recursively the sequences of -valued random variables and defined by the system

| (19) |

where is the Euclidean projection onto the constraint set , and are given by relation (14) and the gain sequence is a decreasing sequence of positive real numbers satisfying

| (20) |

Theorem 5.1.

Let . Assume , for all and there exists such that and are finite. Let be a compact set such that then the following assertions hold.

-

•

If the unique satisfies then the sequence

-

•

If the unique satisfies then the sequence

Proof.

Both items can be proved in the same way, so we choose to give the proof only for the first one. According to Theorem A.1. in Laruelle, Lehalle and Pagès [20] on truncated Robbins Monro algorithm (see also Kushner and Yin [19] for more details): in order to prove that , we need to check firstly the mean-reverting property, namely

This is satisfied using and the convexity of ensured by Proposition 4.1. Secondly, we have to check the non explosion assumption given by

In fact, using Hölder’s inequality with the couple and , we obtain

Since is finite and , we deduce that which completes the proof. ∎

Theorem 5.2.

Considering the sequences given by relation (19), for , we have for all

Proof.

We proceed by induction. The base case is trivial and for the inductive step we suppose that for , , converges to as goes to and we prove the statement for . We have . By the continuity of the function given by (14), the almost sure convergence of to and the continuity of the projection function , we deduce that converges to as goes to . ∎

Corollary 5.1.

Remark.

Suppose for a while that we omit assumptions and in Theorem 5.1 above. According to Theorem 3.2. of Kawai [17] based on Theorem 2.1 of Kushner and Yin [19] there exist and in such that and Moreover, and for all . In this case we can prove that the constrained algorithm given by routine (19) satisfies relation (21) with instead of .

5.2 Central limit theorems

In what follows, we consider the filtration , where are independent copies of . Let us assume that there exists a family of sequences and satisfying

with deterministic limits and .

At first, we start with studying the MC setting. We use the adaptive importance sampling algorithm for the MC method to approximate our initial quantity of interest by

| (22) |

Our task now is to establish a central limit theorem for the adaptive importance sampling Monte Carlo method (ISMC).

Theorem 5.3.

Proof.

By assumption () we only need to study the asymptotic behavior of the martingale arrays given by To do so, we plan to apply the Lindeberg-Feller central limit theorem for martingales arrays (see Theorem 8.2 in the Appendix section). The proof is divided into two steps.

Step 1.

The quadratic variation of the martingale arrays is given by

| (24) |

Since is -measurable and , by Esscher transform we obtain

where for all , . On the one hand, using assumption (), we have . On the other hand, thanks to relation (18) we have the uniform equicontinuity of the family on the compact subset . So, we only need to check this last property for the family in view to use after that Lemma 8.1 and then deduce the convergence of toward as , where .

Thus, it remains to prove the uniform equicontinuity of the family functions defined on the compact set . Using Hölder’s inequality and the assumption , there exists not depending on such that

By Taylor’s expansion and standard calculations we easily get

Therefore, we have

Hence, according to Lemma 4.1 there exists a constant also not depending on and such that

| (25) |

This completes the proof of the first step.

Step 2.

We check now the Lyapunov condition given by assumption B3 in Theorem 8.2. So, let , it is easy to check that . Once again using the mesurability properties of the family and the sequence , we get using the Esscher transform

where for all , . Then, by Hölder’s inequality we get

Noticing that , it results from assumption that is uniformly bounded on the compact subset . Moreover, using once again relation (18) we deduce the uniform boundedness of the family on the compact subset . Hence, combining all these results together with assumption (), we deduce the existence of not depending on such that This completes the proof. ∎

Remark.

If one have in mind to reduce the variance by using an adaptive crude Monte Carlo method, it appears clear that the natural choice is

where and are presented in section 4. The construction of stochastic sequences converging almost surely to these desired targets and satisfying is ensured by Corollary 5.1.

Now, we use the adaptive importance sampling statistical Romberg method (ISSR) to approximate our initial quantity of interest by

| (26) |

Our second result is a central limit theorem for the adaptive ISSR method

Theorem 5.4.

Let be a function satisfying assumption () and such that and are finite, for . Suppose also that the following assumptions are satisfied.

-

For , we have and .

Moreover, assume that with and for there exists a double indexed family satisfying and belonging to some compact subset . If we choose and , then

where

Step 1.

Thanks to assumption and the Esscher transform, the quadratic variation of evaluated at is equal to

where for all , Using the convergence in law given by relation (11), the assumption and the independence of and , we deduce that the second term on the right hand side of the above equation vanishes when tends to zero. Concerning the first one, we aim to use Lemma 8.1. So, we only need to prove the equicontinuity of the family on any compact subset of . First, we prove the simple convergence of to with For this, we can proceed analogously to the proof of relation (11). More precisely, we use Taylor-Young’s expansion with function , the convergence in law given by (11), the independence of and and Slutsky’s theorem to get

Now, applying Hölder’s inequality with yields

Using assumptions and , it is easy to check the uniform boundedness with respect to of the first term on the right hand side of the above inequality. Concerning the second one, since we use relation (18) to deduce the same result. Hence, we have the simple convergence of toward when tends to zero. Therefore, it remains to prove the equicontinuity of the family functions on any compact subset . Replacing by in the steps of the proof of relation (25) and using assumptions and we prove the existence of a constant not depending on such that

| (27) |

Thus, under assumption , we get the almost sure convergence of toward as goes to infinity and vanishes. We complete the proof of the first step using the almost sure convergence of toward as goes to infinity and vanishes. This last convergence is obtained thanks to relation (18).

Step 2.

The second step of this proof consists on checking the Lyapunov condition B3 of Theorem 8.2. We proceed in the same way as in the second step of the proof of Theorem 5.3. We take and we get using the same arguments that is bounded by

where for all , . Then replacing by in the second step of the proof of Theorem 5.3, the same arguments remain valid thanks to assumptions and . So, we deduce the existence of not depending on such that

This completes the proof. ∎

Remark.

Similarly as in the MC case, we still have in mind to reduce the variance associated now to the SR method. This goes back to optimize separately and . Hence, the optimal choice corresponds to

where and are presented in section 4. In the same way, the construction of stochastic sequences converging almost surely to these desired targets and satisfying is ensured by Corollary 5.1.

6 Numerical results

Now, we present numerical simulations that illustrate the efficiency of the ISSR method throughout the pricing of vanilla options with an underlying asset following an exponential pure jump CGMY model. The CGMY process has been introduced by Carr, Geman, Madan and Yor [6] with the aim to develop a model for the dynamic of equity log-returns which is rich enough to accommodate jumps of finite or infinite activity, and finite or infinite variation. Monte Carlo simulation of the CGMY process has been tackled in the literature specifically by Madan and Yor [21], Poirot and Tankov [22] and Rosinski [25]. A CGMY process is a pure jump process with generating triplet where for and

| (28) |

Following the notations of [22], we consider the Lévy-Kintchine representation with a truncation function and a characteristic exponent given by

-

For and , we have and

-

For and , we have and

In what follows, we consider the risk neutral model with jumps generalizing the Black Scholes model by replacing the Brownian motion by the CGMY process with generating triplet , and define the asset price

To guarantee that is a martingale we have to impose the condition (which is satisfied as soon as ) and the condition

| (29) |

or in other words .

Now, let us recall that for , the approximation of is a Lévy process with generating triplet where . It is worth to note that can be seen as a compound Poisson process with drift , see (1). This compound Poisson process can be represented as the difference of two independent processes namely the positive part and the negative one. More precisely, the positive part (resp. the negative part) is a compound Poisson process with jump size (resp. ) and intensity (resp. ). To simulate these compound Poisson processes, we can use either the classical rejection method as described in Cont and Tankov [8] or an improved method used by Madan and Yor [21]. Indeed, when we simulate the positive part we choose so that Then, according to Rosinski [24] we may simulate the paths of from those of by only accepting all jumps in the paths of for which where is an independent draw from uniform distribution. Hence, we use following algorithm

In the same way, we simulate the negative jump part by replacing in the above algorithm the parameter by .

Our aim is to test our approximation methods for computing the price of a vanilla option with payoff . To do so, we use the importance sampling technique, introduced in section 4, to approximate the price by

| (30) |

where is also a Lévy process with generating triplet , where and . The choice of depends on using the classical MC method or the SR one. According to relation (15), is the optimal choice for the MC method. However, for the SR method, we omptize separately each quantity appearing in the associated variance and the optimal choice is given by the couple (see relation (15)) . To compute these optimal terms, we use the constrained algorithms introduced in the system (19). It is worth to note that in practice it is easier to use instead of .

6.1 One-dimensional CGMY process

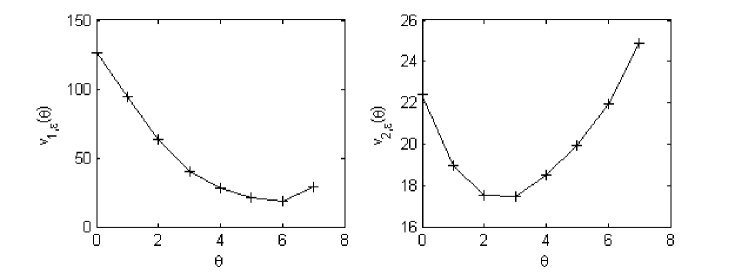

In this setting we consider the European call option with payoff . The parameters of the CGMY model are chosen as follows: , the free interest rate and maturity time . We run iteration for the constrained algorithm with the compact set . The obtained optimal values are given by (see Figure 1).

In order to compare the ISMC algorithm (22) and the ISSR one (26) we use the couple computed above. For this, we compute for each method the CPU time (per second) (the computations are done on a PC with a 2.5 GHz Intel core i5 processor) and an error measure given by the mean squared error (MSE) which is defined by

| (31) |

The real value is obtained using the Fourier-cosine method introduced by Fang and Oosterlee [13] for a one-dimensional CGMY with an accuracy of order . This method is available in the free online version of Premia platform (https://www.rocq.inria.fr/mathfi/Premia/index.html). For this setting, our ISSR algorithm (26) is now available in the latest premium version of Premia.

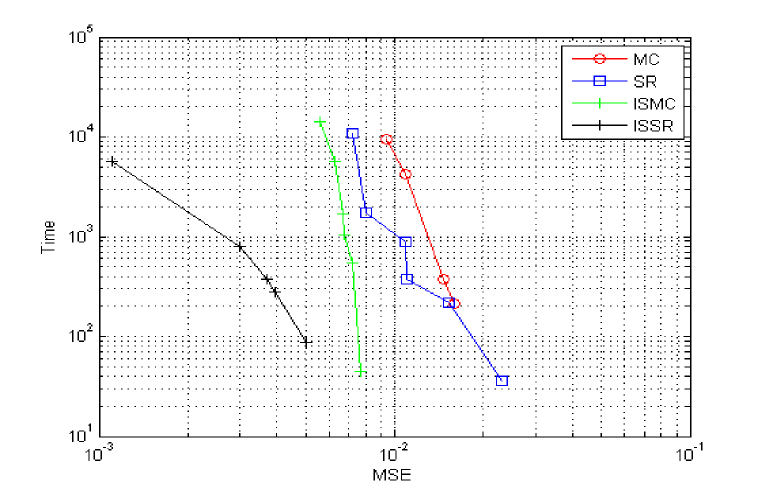

For different values of , we give in Figure 2 below the - plot of the obtained MSE versus the CPU time for the classical Monte Carlo (MC), the statistical Romberg (SR), the importance sampling Monte Carlo (ISMC) and the importance sampling statistical Romberg (ISSR) methods.

According to Table 1 and for a fixed MSE of order , the ISSR method reduces the CPU time by a factor of compared to the ISMC one.

Clearly the ISSR method is the most efficient compared to the other ones.

| Time complexity reduction | ||

|---|---|---|

| MSE | ISMC CPU time | ISSR CPU time |

6.2 Two-dimensional CGMY process

We focus now on the computation of a price of the form , where and the couple denotes the underlying asset process. In this setting we choose where and are two independent CGMY processes with generating triplets and such that the processes and are two martingales. So, it amounts to select and as in relation (29).

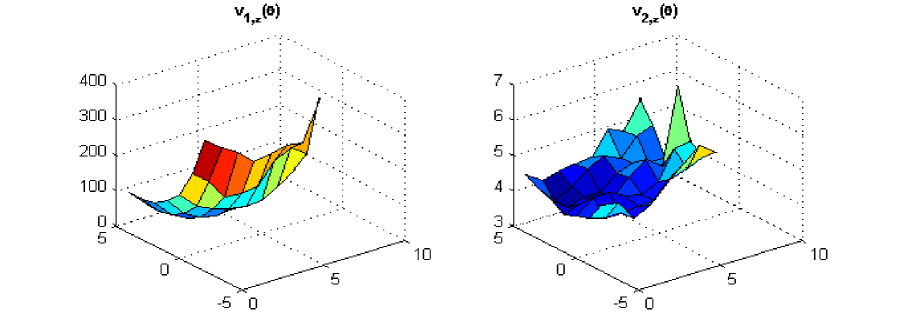

Since the Fourier-cosine method with high accuracy is no more available for the two-dimensional setting, the ”Benchmark” price is obtained by running the classical MC algorithm with a very small value of . Indeed, for the ”Benchmark” price is with a CPU time of seconds. The parameters of the considered two CGMY processes defined by and are chosen as follows: , , , and the maturity time . Using the constrained algorithms (19), we obtain the values of the optimal two-dimensional vectors given by relation (15) and we get and . In Figure 3, we plot the evolution of both variances and in terms of .

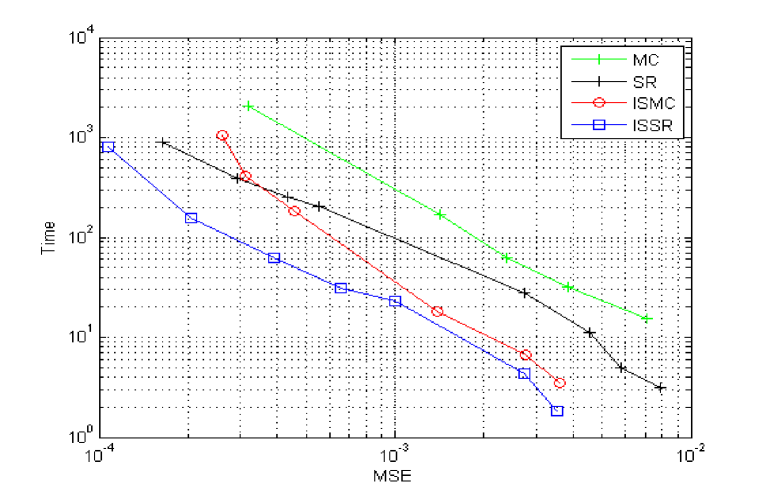

Now we proceed as in the one-dimensional case to compare the different methods. Figure 4 confirms the superiority of the ISSR method over the other ones and this holds even when we compare it to the ISMC method. Indeed, for a given MSE, the ISSR spends less time than the other methods to compute the desired option price. The difference in terms of computational time becomes more significant as soon as the MSE becomes very small, which corresponds to low values of (see Figure 4 below).

According to Table 2 and for a fixed MSE of order , the ISSR reduces the CPU time of the considered option price by a factor in comparison to the ISMC method. Moreover, this factor becomes more important when we consider a smaller MSE. In fact, for a fixed MSE of order , the ISSR reduces the CPU time by a factor in comparison to the ISMC one.

| Time complexity reduction | ||

|---|---|---|

| MSE | ISMC CPU time | ISSR CPU time |

7 conclusion

In this paper, we highlight the superiority of the ISSR method over the classical Monte Carlo approach for the setting of Lévy processes. It may be of interest to extend this study to the setting of Euler discretization schemes for Lévy driven diffusions developed by Protter and Talay [23] and Jacod, Kurtz, Méléard and Protter [16]. Also, a next natural question consists on developing analogous results for path dependent options in exponential Lévy models in the spirit of the works of Dia and Lamberton [10, 11]. These two points will be the object of a forthcoming works.

8 Appendix

We recall first the Lindeberg Feller Central Limit Theorem for independent random variables.

Theorem 8.1 (Lindeberg Feller Central Limit Theorem [4]).

Let be a sequence such that , as and for each we consider a sequence of independent centered and real square integrable random variables. We make the following two assumptions.

-

There exists a positive constant such that .

-

Lindeberg’s condition holds: that is for all , . Then

Remark.

The following assumption known as the Lyapunov condition implies the Lindberg’s condition A2..

-

There exists a real number sucht that

This result was generalized in the context of martingales arrays.

Theorem 8.2 (Central Limit Theorem for martingales arrays [12]).

Suppose that is a probability space and that for each , we have a filtration , a sequence and a real square integrable vector martingale which is adapted to and has quadratic variation denoted by . We make the following two assumptions.

-

B1.

There exists a deterministic symmetric positive semi-definite matrix , such that

-

B2.

Lindeberg’s condition holds: that is, for all ,

Then

Remark.

The following assumption known as the Lyapounov condition, implies the Lindberg’s condition B2.,

-

B3.

There exists a real number , sucht that

Moreover, we give a double indexed version of the Toeplitz lemma. For a proof of this result see Lemma 4.1 in [3]

Lemma 8.1.

Let a sequence of real positive numbers, where as tends to , and a double indexed sequence such that

-

(i)

-

(ii)

Then

References

- [1] B. Arouna. Adaptative Monte Carlo method, a variance reduction technique. Monte Carlo Methods Appl., 10(1):1–24, 2004.

- [2] S. Asmussen and J. Rosiński. Approximations of small jumps of Lévy processes with a view towards simulation. J. Appl. Probab., 38(2):482–493, 2001.

- [3] M. Ben Alaya, K. Hajji, and A. Kebaier. Importance sampling and statistical romberg method. Accepted at Bernoulli Journal, 2014.

- [4] P. Billingsley. Convergence of probability measures. John Wiley & Sons Inc., New York, 1968.

- [5] N. H. Bingham, C. M. Goldie, and J. L. Teugels. Regular variation, volume 27 of Encyclopedia of Mathematics and its Applications. Cambridge University Press, Cambridge, 1987.

- [6] P. Carr, H Geman, D. B. Madan, and M. Yor. The fine structure of asset returns: An empirical investigation, 2000.

- [7] S. Cohen and J. Rosiński. Gaussian approximation of multivariate Lévy processes with applications to simulation of tempered stable processes. Bernoulli, 13(1):195–210, 2007.

- [8] R. Cont and P. Tankov. Financial modelling with jump processes. Chapman & Hall/CRC Financial Mathematics Series. Chapman & Hall/CRC, Boca Raton, FL, 2004.

- [9] E. H. A. Dia. Error bounds for small jumps of Lévy processes. Adv. in Appl. Probab., 45(1):86–105, 2013.

- [10] E. H. A. Dia and D. Lamberton. Connecting discrete and continuous lookback or hindsight options in exponential Lévy models. Adv. in Appl. Probab., 43(4):1136–1165, 2011.

- [11] E. H. A. Dia and D. Lamberton. Continuity correction for barrier options in jump-diffusion models. SIAM J. Financial Math., 2(1):866–900, 2011.

- [12] M. Duflo. Random iterative models, volume 34 of Applications of Mathematics (New York). Springer-Verlag, Berlin, 1997. Translated from the 1990 French original by Stephen S. Wilson and revised by the author.

- [13] F. Fang and C. W. Oosterlee. A novel pricing method for European options based on Fourier-cosine series expansions. SIAM J. Sci. Comput., 31(2):826–848, 2008/09.

- [14] W. Feller. An introduction to probability theory and its applications. Vol. II. Second edition. John Wiley & Sons, Inc., New York-London-Sydney, 1971.

- [15] P. Glasserman, P. Heidelberger, and P. Shahabuddin. Asymptotically optimal importance sampling and stratification for pricing path-dependent options. Math. Finance, 9(2):117–152, 1999.

- [16] J. Jacod, T. G. Kurtz, S. Méléard, and P. Protter. The approximate Euler method for Lévy driven stochastic differential equations. Ann. Inst. H. Poincaré Probab. Statist., 41(3):523–558, 2005.

- [17] R. Kawai. Optimal importance sampling parameter search for Lévy processes via stochastic approximation. SIAM J. Numer. Anal., 47(1):293–307, 2008/09.

- [18] A. Kebaier. Statistical Romberg extrapolation: a new variance reduction method and applications to option pricing. Ann. Appl. Probab., 15(4):2681–2705, 2005.

- [19] H. J. Kushner and G. G. Yin. Stochastic approximation algorithms and applications, volume 35 of Applications of Mathematics (New York). Springer-Verlag, New York, 1997.

- [20] S. Laruelle, C. Lehalle, and G. Pagès. Optimal posting price of limit orders: learning by trading. Math. Financ. Econ., 7(3):359–403, 2013.

- [21] D. B. Madan and M. Yor. Representing the CGMY and Meixner Lévy processes as time changed Brownian motions. J. Comput. Finance, 12(1):27–47, 2008.

- [22] J. Poirot and P. Tankov. Monte carlo option pricing for tempered stable (cgmy) processes. J. Asia-Pacific Financial Markets, 13(4):327–344, 2006.

- [23] P. Protter and D. Talay. The Euler scheme for Lévy driven stochastic differential equations. Ann. Probab., 25(1):393–423, 1997.

- [24] J. Rosiński. Series representations of Lévy processes from the perspective of point processes. In Lévy processes, pages 401–415. Birkhäuser Boston, Boston, MA, 2001.

- [25] J. Rosiński. Tempering stable processes. Stochastic Process. Appl., 117(6):677–707, 2007.

- [26] K. Sato. Lévy processes and infinitely divisible distributions, volume 68 of Cambridge Studies in Advanced Mathematics. Cambridge University Press, Cambridge, 1999. Translated from the 1990 Japanese original, Revised by the author.

- [27] W. Schoutens. Levy Processes in Finance: Pricing Financial Derivatives. Wiley Series in Probability and Statistics. Wiley, 2003.

- [28] D. Talay and L. Tubaro. Expansion of the global error for numerical schemes solving stochastic differential equations. Stochastic Anal. Appl., 8(4):483–509 (1991), 1990.