Polynomial size linear programs for problems in P

Abstract

A perfect matching in an undirected graph is a set of vertex disjoint edges from that include all vertices in . The perfect matching problem is to decide if has such a matching. Recently Rothvoß proved the striking result that the Edmonds’ matching polytope has exponential extension complexity. In this paper for each we describe a polytope for the perfect matching problem that is different from Edmonds’ polytope and define a weaker notion of extended formulation. We show that the new polytope has a weak extended formulation (WEF) of polynomial size. For each graph with vertices we can readily construct an objective function so that solving the resulting linear program over decides whether or not has a perfect matching. With this construction, a straightforward implementation of Edmonds’ matching algorithm using bits of space would yield a WEF with inequalities and variables. The construction is uniform in the sense that, for each , a single polytope is defined for the class of all graphs with nodes. The method extends to solve polynomial time optimization problems, such as the weighted matching problem. In this case a logarithmic (in the weight of the optimum solution) number of optimizations are made over the constructed WEF.

The method described in the paper involves the construction of a compiler that converts an algorithm given in a prescribed pseudocode into a polytope. It can therefore be used to construct a polytope for any decision problem in P which can be solved by a well defined algorithm. Compared with earlier results of Dobkin-Lipton-Reiss and Valiant our method allows the construction of explicit linear programs directly from algorithms written for a standard register model, without intermediate transformations. We apply our results to obtain polynomial upper bounds on the non-negative rank of certain slack matrices related to membership testing of languages in P/poly.

keywords:

Polytopes, extended formulation, extension complexity, perfect matching, linear programming, non-negative ranks¿c

1 Introduction

A perfect matching in an undirected graph is a set of vertex disjoint edges from that include all vertices in . We let denote the number of vertices and assume is even throughout the paper. The perfect matching problem is to determine if contains a perfect matching and this can be decided in polynomial time by running Edmonds’ algorithm [9]. As well as this combinatorial algorithm, Edmonds also introduced a related polytope [10] which we will call the Edmonds’ polytope :

| (1) |

where is the convex hull operator.

For any and edge , we write that whenever exactly one of the vertices and is in . Edmonds [10] proved that has the following halfspace representation:

This description is exponential in size. Nevertheless, the perfect matching problem can be solved in polynomial time by solving a linear program (LP) over this polytope. Indeed, define an objective function , where if and otherwise. The LP is:

It is easy to verify that if has a perfect matching then otherwise . Since the inequalities defining can be separated in polynomial time, the LP can be solved in polynomial time [14].

Since the perfect matching problem is in P, it seemed possible that could be written as the projection of a polytope with a polynomial size description. This is the topic of extension complexity (see, e.g., Fiorini et al. [12]). We recall the basic definitions here, referring the reader to [12] for further details.

An extended formulation (EF) of a polytope is a linear system

| (3) |

in variables where are real matrices with columns respectively, and is a column vector, such that if and only if there exists such that (3) holds. The size of an EF is defined as the number of inequalities in the system.

An extension of the polytope is another polytope such that is the image of under a linear map. We define the size of an extension as the number of facets of . Furthermore, we define the extension complexity of , denoted by as the minimum size of any extension of

Rothvoß [18] recently proved the surprising result that is exponential. Since extension complexity seemed a promising candidate to obtain computational models that separate problems in P from those that are NP-hard, this was a setback. A way of strengthening extension complexity to handle this problem was recently proposed by Avis and Tiwary [3].

Dobkin et al. [8] and Valiant [19] showed that linear programming is P-complete from which it follows that every problem in P has an LP-formulation of polynomial size. We will review this result in Section 3 giving Valiant’s construction. This construction applies to P/poly, which is the class of all decision problems solvable by a family of polynomial size Boolean circuits such that solves the restriction of to inputs of length . From these circuits it is straightforward to construct a family of LPs.

The main contribution of this paper is to give a direct method to produce polynomial size LPs from polynomial time algorithms, not circuits. Specifically we will construct LPs directly from a polynomial time algorithm expressed in pseudocode that solves a decision problem. Of course a trivial LP formulation can be obtained by first solving the decision problem for a given input and setting if the answer is yes and otherwise. Then solving the one dimensional LP: solves the original problem. To avoid such trivial LPs we limit how much work can be done in constructing the objective function. One such limitation might be, for example, to insist that the objective function can be computed in linear time in terms of the input size. The objective functions we consider in this paper satisfy this condition.

For concreteness, we focus on an explicit construction of a polynomial size LP that can be used to solve the perfect matching problem. Firstly we describe another ‘natural’ polytope, , for the perfect matching problem. Then we will introduce the notion of a weak extended formulation (WEF). Instead of requiring projection onto we will simply require that LPs solved over the WEF solve the original problem. The objective function used is basically just a encoding of the input graph. The approach used is quite general and can be applied to any problem in for which an explicit algorithm is known. It extends to polynomial time solvable optimization problems also. However in this case a logarithmic (in the weight of the optimum solution) number of optimizations are made over the constructed WEF. Note that when an EF exists both the optimization and decision problems can be solved in a single LP optimization. Hence a WEF is weaker since a single LP solves only the decision problem. We discuss this further in Section 6.

The paper is organized as follows. In the next section we introduce a new polytope for the perfect matching problem and give some basic results about its facet structure. We define the notion of weak extended formulation and state the main theorem. In Section 3 we first give a simple example to illustrate the technique we use to build extended formulations from boolean circuits. Then we prove the main theorem of the paper. In Section 4 we generalize our method to algorithms given in pseudocode rather than as a circuit. We show how programs written in a simple pseudocode can be converted to WEFs. Our method is modeled on Sahni’s proof of Cook’s theorem given in [15]. Since our pseudocode is clearly strong enough to implement Edmonds’ algorithm in polynomial time, our method gives a polynomial size WEF for the perfect matching problem. In Section 5 we use our main theorem to show that the non-negative rank of certain matrices is polynomially bounded above. Finally in Section 6 we give some concluding remarks including a discussion of applying this technique to polynomial time optimization problems such as the maximum weighted matching problem.

2 Polytopes for decision problems

2.1 Another perfect matching polytope

We use the notation to denote the -dimensional vector of all ones, dropping the subscript when it is clear from the context. Let be an even integer and let be a binary vector of length . We let denote the graph with edge incidence vector given by , let be the number of its vertices and the number of its edges. Furthermore, let if has a perfect matching and zero otherwise. We define the polytope as:

| (4) |

may be visualized by starting with a hypercube in dimension and embedding it in one higher dimension with extra coordinate . For vertices of the cube corresponding to graphs with perfect matchings else . It is easy to see that has precisely vertices. Edmonds’ polytope is closely related to , in fact it defines one of its faces. Let

| (5) |

Proposition 1.

defines a face of and in fact

| (6) |

Proof.

To show that is a face we show that the inequality

| (7) |

is valid for . It suffices to verify it for the extreme points given in (4). If , (7) holds since . Since the inequality is strict, none of these extreme points lie on . Otherwise , is the incidence vector of graph containing a perfect matching, so . This shows that defines a face of .

The vectors with and are the incidence vectors of perfect matchings of and are precisely those used to define in (1). Hence lifted by adding the coordinate is precisely . ∎

For a given input graph we define the vector as follows:

| (8) |

and let be a constant such that . We construct the LP:

For any positive integer , by an -cube we mean the -dimensional hypercube whose vertices are the binary vectors of length .

Proposition 2.

For any edge incidence vector let . The optimum solution to (2.1) is unique, if has a perfect matching, and otherwise.

Proof.

Let be the vector defined by (8) and set . Note that and that for any other vertex of the -cube. If has a perfect matching then is a feasible solution to (2.1) with . Since , and so is the unique optimum solution.

If does not have a perfect matching then is a feasible solution to (2.1) with . Consider any other vertex of the -cube. Then . It follows that and is obtained by the unique solution . ∎

2.2 Polytopes for decision problems and weak extended formulations

The basic ideas above can be extended to arbitrary polynomial time decision problems. Let denote a polynomial time decision problem defined on binary input vectors , and an additional bit , where if results in a “yes” answer and if results in a “no” answer. We define the polytope as:

| (10) |

For a given binary input vector we define the vector by:

| (11) |

and let be a constant such that . As before we construct an LP:

The following proposition can be proved in an identical way to Proposition 2.

Proposition 3.

For any let . The optimum solution to (2.2) is unique, if has a “yes” answer and otherwise.

Definition 1.

Let be a polytope which is a subset of the -cube with variables labeled . We say that has the x-0/1 property if each of the ways of assigning 0/1 to the variables uniquely extends to a vertex of and, furthermore, is 0/1 valued. may have additional fractional vertices.

In polyhedral terms, for every binary vector , the intersection of with the hyperplanes is a 0/1 vertex. We will show that we can solve a polynomial time decision problem by replacing in (2.1) by a polytope of polynomial size, while maintaining the same objective functions. We call a weak extended formulation as it does not necessarily project onto .

Definition 2.

A polytope

is a weak extended formulation (WEF) of if the following hold:

-

1.

has the -0/1 property.

-

2.

For any vector let , let be defined by (11) and let . If has a “yes” answer the optimum solution of the LP

(13) is unique and takes the value . Otherwise .

The first condition states that any vertex of that has 0/1 values for the variables has 0/1 values for the other variables as well. The second condition connects to . For a 0/1 valued vertex of we have if encodes a “yes” answer since . If encodes a “no” answer then and we must have . The purpose of the coefficient is so that we can distinguish the two answers by simply observing the value of .

In the sequel we will be concerned with small positive constants which we will assume are rational and in reduced form , for positive integers and . The size of is .

In general will have fractional vertices and that is why the condition for “no” answers differs from that given in Proposition 3 (an example is given below). However, for small enough we can ensure that the LP optimum solution is unique in both cases and corresponds to that given in Proposition 3.

Proposition 4.

Let be a WEF of . There is a positive constant , whose size is polynomial in the size of , such that for all , , the optimal solution of the LP defined in (13) is unique, if has a “yes” answer and if has a “no” answer.

Proof.

The part of the proposition relating to the “yes” answers is already covered by Definition 2. So consider any corresponding to a “no” answer and its associated vector given by (11). Since has the 0/1 property uniquely extends to a 0/1 valued vertex of with as we saw above. So for any , , we have . Consider any other vertex of . Since , we have . Let taken over all vertices with . This minimum exists, since the number of vertices of is finite, and is positive. Furthermore, . We define

Now choose any , , and any vertex of with . If then . Otherwise and we have as noted above. Since the optimal solution for any LP can always be obtained at a vertex, it follows that the LP defined in (13) has a unique optimum solution whenever corresponds to a “no” answer.

If follows from standard linear programming theory that each vertex can be represented by a number of bits polynomial in the size of . Since is a vector and it follows that can also be so represented. Now is the minimum of a finite number of such quantities so has size polynomial in the size of . The proposition follows. ∎

This proof gives, at least in principle, a method of computing the constant from a list of the vertices of . An easier to compute bound can be obtained from the analysis of Khachian’s ellipsoid method, see, for example, the text [14]. Following this text, let be the number of bits required to represent . Then the proof of their Lemma 3.1.33 implies that the differences in the above proof are all at least and so we could choose this value for . This value will generally be much too small to be of practical use. However, if we are able to observe the value of in the optimum solution of (13) then we may in fact set . In this case for both answers and it follows from the 0/1 property that the optimum solution is unique and 0/1 valued. Since is a WEF of the value of in the optimum solution gives the correct answer. This is the preferred method in practice as it reduces the problem of floating point round off errors which may be caused by small values of .

We saw in the proof of Proposition 4, the reason that has to be small is to ensure that fractional vertices of do not lead to optimum solutions for valued object vectors . As an example, consider the perfect matching problem and the polytope defined earlier. Suppose is a WEF for . It follows from Propositions 2 and 4 that we can determine whether an input graph has a perfect matching by solving an LP over either or using the same objective function which is derived directly from the edge adjacency vector of . As a very simple case, consider giving . A possible WEF with is given by:

Initially let . When is an edge, , and obtains the same optimum solution of over both and . When is a non-edge, , and obtains the optimum solution of over and over , at the fractional vertex (1/4,1,1/2). However, if then is negative for the fractional vertex and obtains the unique optimum solution of over and also, of course, over . We see that projects onto a triangle in the -space, whereas is a line segment.

In the next section we prove the following result:

Theorem 1.

Every decision problem in P/poly admits a weak extended formulation of polynomial size.

3 From Circuits to Polytopes

In order to show that Linear Programming is P-complete, Valiant [19] gave a construction to transform boolean circuits into a linear sized set of linear inequalities with the -0/1 property (where are the variables corresponding to the inputs of the circuit); a similar construction was used by Yannakakis [20] in the context of the Hamiltonian Circuit problem. In this section we show that Valiant’s construction implies Theorem 1. Valiant’s point of view is slightly different from ours in that he explicitly fixes the values of the input variables before solving an LP-feasibility problem (as opposed to using different objective functions with a fixed set of inequalities). Showing that the result of this fixing is a -vertex is precisely our -0/1 property.

We begin with a standard definition, see for example the text by Arora and Barak [1]:

Definition 3.

A (boolean) circuit with input bits is a directed acyclic graph in which each of its nodes, called gates, is either an AND () gate, an OR () or a NOT () gate. We label each gate by its output bit. One of these gates is designated as the output gate and gives output bit . The size of a circuit is the number of gates it contains and its depth is the maximal length of a path from an input gate to the output gate.

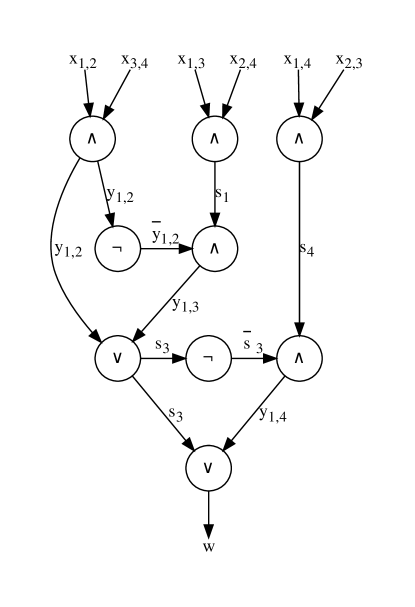

For example, the circuit shown in Figure 1 can be used to compute whether or not a graph on 4 nodes has a perfect matching. The input is the binary edge-vector of the graph and the output is if the graph has a matching (e.g. ) or if it does not (e.g. ). If the graph has a perfect matching, exactly one of or is one, defining the matching. For each gate we have labeled the output bit by a new variable. We will construct a polytope from the circuit by constructing a system of inequalities on the same variables.

From an AND gate, say , we generate the inequalities:

| (14) | |||||

The system (14) defines a polytope in three variables whose 4 vertices represent the truth table for the AND gate:

Note that the variables define a 2-cube and so the polytope is an extension of the 2-cube. In the terminology of the last section, it has the -0/1 property.

From an OR gate, say , we generate the inequalities:

| (15) | |||||

The system (15) defines a polytope in three variables whose 4 vertices represent the truth table for the OR gate, as can easily be checked. Indeed, this polytope has the -0/1 property.

From a NOT gate, say , we could generate the equation

| (16) |

However it is equivalent to just replace all instances of by in the inequality system, and this is what we will do in the sequel.

The circuit in Figure 1 contains 5 AND gates and 2 OR gates. By suitably replacing variables in (14) and (15) we obtain a system of 28 inequalities in 13 variables. As just mentioned, the NOT gates are handled by variable substitution rather than explicit equations. Let denote the corresponding polytope. It will follow by the general argument below that is a weak extended formulation (WEF) of .

We now show that the above construction can be applied to any boolean circuit to obtain a polytope which has the 0/1 property with respect to the inputs of .

Lemma 1 ([19]).

Let be a boolean circuit with input bits , gates labeled by their output bits and with circuit output bit . Construct the polytope with inequalities and variables using the systems (14) and (15) respectively. has the the -0/1 property and for every input the value of computed by corresponds to the value of in the unique extension of .

Proof.

Since is an acyclic directed graph it contains a topological ordering of its nodes (gates) and we can assume that the labeling is such an ordering. Note we can assume comes last since it cannot be an input to any other gate. For any given input the output of the circuit can be obtained by evaluating each gate in the order . Since it is a topological ordering, each input for a gate has been determined before the gate is evaluated.

We proceed by induction. Let be the polytope defined by the inequalities corresponding to gates . The inductive hypothesis is that for

-

1.

has the -0/1 property, and

-

2.

for each the value of calculated by corresponds to the value of in the unique extension of in .

This is clearly true for as the analysis following (14) and (15) shows. We assume the hypothesis is true for , where , and prove it for . Indeed, since has the -0/1 property for each the values of are uniquely defined and have 0/1 values. By induction they correspond to the values computed by . Therefore the analysis following (14) and (15) shows that will also be uniquely defined, 0/1 valued, and will correspond to the value computed by . This verifies the inductive hypothesis for and since the proof is complete. ∎

Lemma 2.

Proof.

In order to make the correspondence with Definition 2 we relabel the variables in , constructed in Lemma 1, so that and . By Lemma 1 we know has the -0/1 property so it remains to prove the second condition in Definition 2.

Let be any vector in and set . Since has the -0/1 property extends to a unique binary vertex of . Define as in (11). Fix some , and consider the optimum solution

Since has the -0/1 property the maximum of over is obtained at at the unique vertex of . For any other , since is in the -cube and not equal to , we have and, since , . Therefore, if has a “yes” answer then , and is the unique optimum solution. Otherwise . The lemma follows. ∎

Theorem 1 follows from Lemmas 1 and 2. Since there is no limitation of uniformity on the circuits used, the theorem holds for all decision problems in P/poly. Since each gate in the circuit gives rise to 4 inequalities and one new variable, we have the following corollary.

Corollary 1.

Let be a decision problem with corresponding polytope defined by (10). A set of circuits for with size generates a WEF for with at most inequalities and variables.

In this section we showed how to construct a polynomial size LP from a polynomial size circuit so that the optimum solution of the LP gives the output of the circuit. However it is not immediately clear how to use this to obtain a polytope for the perfect matching problem. It would be required to convert Edmonds’ algorithm to a family of circuits. In the next section we bypass this step by showing how to convert a simple pseudocode directly into a polytope without first computing a circuit (See Theorem 2). This can be used to convert polynomial time algorithms into polynomial size LPs directly.

We would like to remark that our construction in Theorem 2 of a WEF from a pseudocode may not be optimal. For example, it would be possible to get roughly - size circuits simulating a given -time bounded Turing machine (see, e.g., Chapter 1 of [1]) from which we can construct a WEF with inequalities. But since Turing Machines are not commonly used for designing algorithms, we leave the interested reader to check whether a similar idea can be used to define a WEF with smaller size.

4 Constructing an LP from pseudocode

In this section we introduce a rudimentary pseudocode that can be used for decision problems. This pseudocode follows the usual practices of specifying algorithms and the tradition of so-called register machines (see e.g. [7]). We show how the code can be translated into a linear program, in a way similar to that shown for circuits in the previous section. This translation works for any pseudocode, but since the focus of this paper is on the class P, we will assume there is a polynomial function so that the the code terminates within steps for any input of size . In this case we will show that the corresponding LP will also have polynomial size in .

The pseudocode we use and its translation into an LP is adapted from a proof of Cook’s theorem given in [15] which is attributed to Sartaj Sahni. In Sahni’s construction the underlying algorithm may be non-deterministic, but we will consider only deterministic algorithms. Furthermore, Sahni describes how to convert his pseudocode into a satisfiability expression. Although it would be possible to convert this expression into an LP, considerable simplifications are obtained by doing a direct conversion from pseudocode to an LP. In this section, for simplicity, we describe only those features of the pseudocode that are necessary for implementing Edmonds’ algorithm for the perfect matching problem. Additional features would be needed to handle more sophisticated problems, such as the weighted matching problem. For full details, the reader is referred to Section 11.2 of [15].

Our pseudocode has the following form. We assume is a fixed integer which will represent the word size for integer variables.

-

1.

Variables are binary valued except for indices, which are -bit integers. Arrays of binary values are allowed and may be one or two dimensional. Dimension information is specified at the beginning of . We let denote the maximum number of bits required to represent all variables for an input size of . Sahni argues that however in our case is significantly smaller. Statements in are numbered sequentially from to .

-

2.

An expression contains at most one boolean operator or is the incrementation of an index. Array variables are not used in expressions but may be assigned to simple variables and vice versa.

-

3.

Certain variables are designated as parameters and used to provide input to the program. All other variables are initially zero.

-

4.

may contain control statements go to and if then go to endif. Here is an instruction number and is a simple binary variable.

-

5.

terminates by setting a binary variable to one if the input results in a yes outcome and to zero otherwise. The program then halts.

In our implementation we also allow higher level commands such while and for loops which are first precompiled into the basic statements listed above. As a simple example, here is a pseudocode that produces essentially the same result as the circuit in Figure 1.

if then go to 50 endif

if then go to 50 endif

if then go to 50 endif

return

50:

return

Note that the lines of the pseudocode which are executed depend on the input values . This is different from the circuit where all gates are executed for every input. We return to this point below.

The variables in the LP are denoted as follows. They correspond to variables in as it is being executed on a specific input .

-

1.

Binary variables .

represents the value of binary variable in after steps of computation. For convenience we may group consecutive bits together as an integer variable . represents the value of the -th bit of integer variable in after steps of computation. The bits are numbered from right to left, the rightmost bit being numbered 1. -

2.

Binary arrays A binary array is stored in consecutive binary variables from some base location . The array index is stored as a -bit integer and so we must have .

-

3.

2-dimensional binary arrays A two dimensional binary array , , is stored in row major order in consecutive binary variables , from some base location . The array indices and are stored as -bit integers and so we must have .

-

4.

Step counter .

Variable represents the instruction to be executed at time . It takes value 1 if line of is being executed at time and otherwise.

All of the above variables are specifically bounded to be between zero and one in our LP. The last set of variables, the step counter, indicates an essential difference between the circuit model and the pseudocode model. In the former model, all gates are executed for each possible input. The gates can be executed in any topological order consistent with the circuit. For the pseudocode model, however, the step to be executed at any time will usually depend on the actual input. For each time step and line of pseudocode we will develop a system of inequalities which have the -0/1 property, for some subset of variables , if line is executed at time . I.e., the inequalities should uniquely determine a 0/1 value of all variables given any 0/1 setting of the variables. However, if step is not executed at time then the variables should be free to hold any 0/1 values and these values will be determined by the step that is executed at time . So in each set of inequalities a control variable (in our case the variable ) will appear for this purpose. More formally, we make the following definition which generalizes Definition 1:

Definition 4.

Let be a system of inequalities that satisfy the -0/1 property, i.e. each 0/1 setting of the variables uniquely defines a 0/1 setting of the variables. Suppose that is feasible for all 0/1 settings of and variables, and let be a binary variable. The system has the () controlled x-0/1 property.

Note that if the new system is always feasible for any 0/1 setting of and . If then the new system reduces to the old system that has the -0/1 property.

We now define the 5 different types of linear inequalities needed to simulate the pseudocode which, following Sahni, we label C,D,E,F and G.111Sahni also has a constraint set H which relates to the certificate checking function of his algorithm, and is not needed here. Recall that the -variables ensure that at each time a unique line is executed, taking the value if it is and 0 otherwise. The inequalities listed below all have the controlled -0/1 property, and so have the form for suitably chosen .

-

C:

(Variable initialization) The variables are set equal to their initial value, if any, else set to zero.

-

D:

(Step counter initialization) Instruction 1 is executed at time .

-

E:

(Unique step execution) A unique instruction is executed at each time .

-

F:

(Flow control) The instruction to execute at time is determined, assuming we are at line of at time , i.e. . If not, i.e. , then all inequalities below are trivially satisfied. This follows since the other variables are constrained to be between zero and one. There are 4 subcases depending on the instruction at line . Inequalities are generated for each , .

-

(i)

(assignment statement) Go to the next instruction.

-

(ii)

(go to )

-

(iii)

(return) Loop on this line until time runs out.

-

(iv)

(if then go to endif) We assume that bit is represented by variable .

When cases (i)-(iii) fix the next line to be executed and trivially have the controlled -0/1 property, where is empty. For (iv), note we have also the equations E above. When , if then the first inequality fixes otherwise the second inequality fixes . The inequalities (iv) have the controlled -0/1 property.

-

(i)

-

G:

(Control of variables) If we are at line of at time , i.e. , all variables are updated to their correct values at time following the execution of line . If not, i.e. , then all inequalities below are trivially satisfied. Again there are several cases depending on the instruction at line . Inequalities are generated for each , .

-

(i)

(Reassignment of unchanged variables) All variables left unchanged at a given step need to be reassigned their previous values. Let index some bit unchanged at step .

Note that when these inequalities imply that . They have the controlled -0/1 property. Similar inequalities are generated for each integer variable .

In what follows, the above inequalities need to be generated for all variables and not being assigned values at time in the particular instruction being considered.

-

(ii)

(assignment: and ) Assume that are stored in respectively. For we generate the two inequalities:

When the inequalities imply as desired. They have the controlled -property. For we generate the two inequalities:

The analysis is similar to that for .

-

(iii)

(assignment: ) Assume that are stored in respectively.

If then all constants on the right hand side are reduced by one and can be deleted. It is easy to check the inequalities have the controlled -0/1 property, and that for each such 0/1 assignment is correctly set.

-

(iv)

(assignment: ) Assume that are stored in respectively.

If then all constants on the right hand side are reduced by one and can be deleted. It is easy to check the inequalities have the controlled -0/1 property, and that for each such 0/1 assignment is correctly set.

-

(v)

(assignment: , )

Assume that are stored in respectively.The analysis is similar to G(iv) and is omitted. The inequalities have the controlled {B(q,t-1),B(r,t-1)}-0/1 property.

The -way or is an easy generalization which will be needed in the sequel, where we assume that is stored in . It is defined by the following inequalities:

-

(vi)

(increment integer variable) Assume that the integer variable is stored in and is to be incremented by 1. We require another integer to hold the binary carries. On overflow, and . The incrementer makes use of two previous operations, G(iii) and G(iv):

By appropriate formal substitution of variables, each of the above assignments is transformed into inequalities of the form G(iii) and G(iv), which are controlled by the step counter . It can be verified that the full system satisfies the controlled -0/1 property because for each 0/1 setting of these variables all other variables are fixed by the above system of equations.

-

(vii)

(equality test for integer variables) Assume that the integer variables are stored in and , . We require temporary variables w.l.o.g. . If the two integer variables are equal then is set to one else it is set to zero.

The first equations makes repeated use of G(iii) after appropriate substitution. By combining G(ii) and the -way or from we may implement the second equation by the inequalities.

The inequalities have the controlled {, }-0/1 property.

-

(viii)

(array assignment) (and ) We assume that has dimension , is stored in , and that is stored in . We further assume that is stored in an integer variable . We need additional binary variables to hold intermediate results. Initially we write down some equations and then we use previous results to convert these to inequalities. Firstly we need to discover the memory location for . For any let be the binary representation of . Then we formally define for

Note this definition is purely formal and has nothing to do with the execution of . We will assign a value via the -way or given in G(v). For :

(17) When , it can be verified that whenever and is one otherwise. Now we may update all array elements of at time and make the assignment by the system of inequalities, for all :

To understand these inequalities, first note that they are trivially satisfied unless . When we have and the first two inequalities are tight. We have updating the array element to . The second two inequalities are trivially satisfied. Otherwise , , the first two inequalities are trivially satisfied and the second two are tight. We have copying the array element over to time from time . We remark that there are inequalities generated above.

Finally note that we can implement by using the inequalities

and letting the array be copied at time using G(i). Both of these two inequality systems have the controlled {}-0/1 property.

-

(ix)

(2-dimensional array assignment) (or . This is a natural generalization of G(viii). We assume that has dimensions and , is stored in row major order in , and that is stored in . We further assume that and are stored in an integer variables respectively. We need additional binary variables and to hold intermediate results. Firstly we need to discover the memory location for . We again use the equations (17) for the row index.

For the column index, as in G(viii), for any let be the binary representation of . We formally define for

We will assign a value via the -way or given in G(v). For :

When , it can be verified that whenever and is one otherwise. Now we may update all array elements of at time and make the assignment by the following system of inequalities. For all , , :

The analysis is similar to G(viii). The above inequalities are all trivial unless . Note that for each and , index gives the relative location in the array. If , then , the first two inequalities are tight and the last four loose. The first two inequalities give . Otherwise either or or both, and the first two inequalities are trivially satisfied. In the former case the two middle inequalities are tight and we have the equation . In the latter case this equation is formed from the last two inequalities. We remark that there are inequalities generated above.

For the assignment we need the inequalities

for . All array elements of must also be copied from time to time as in G(i).

Both of these two inequality systems have the controlled {}-0/1 property.

Remark: In applications using graphs, a symmetric 2-dimensional array is often used to hold the adjacency matrix. Such symmetric matrices may be implemented in pseudocode by replacing a statement such as by the two statements and . Assignment statements such as may be left as is.

-

(i)

To show the correctness of the above procedure we give two lemmas that are analogous to Lemmas 1 and 2 of the last section. First we show that the above construction can be applied to any pseudocode , written in the language described, to produce a polytope which has the 0/1 property with respect to the inputs of .

Lemma 3.

Let be a pseudocode, written in the above language, which takes input bits , and terminates by setting a bit . Construct the polytope as described above relabeling as and the additional variables as for some integer . has the -0/1 property and for every input the value of computed by corresponds to the value of in the unique extension of .

Proof.

(Sketch) As with Lemma 1 the proof is by induction, but this time we use the step counter. By assumption terminates after steps. Let represent the step counter. Define to be the polytope consisting of precisely those inequalities in that use variables: , and .

-

1.

has the -0/1 property, and

-

2.

for each , at step , with input is executing line corresponding to the unique index where and all variables at that step have the values corresponding to the values of and .

The inequalities of consist of those in groups C, D, and part of E above and the induction hypothesis is readily verified. We assume the hypothesis is true for , where , and prove it for . Indeed, since has the -0/1 property for each the values of all variables with index have been correctly set. It follows that for precisely one index we have , meaning that line of the pseudocode is executed at time for this particular input. The inequalities defined in group G all have the controlled -0/1 property for the control variable . The variables and with index are correctly set by the analysis in group G above. The analysis in group implies that the values of will also be uniquely determined and 0/1, correctly indicating the next line of to be executed at . This verifies the inductive hypothesis for and since this concludes the proof. ∎

The next lemma is simply a restatement of Lemma 2 in the context of our pseudocode rather than circuits. The proof of Lemma 2 makes no reference to how was computed, so the same proof holds.

Lemma 4.

We now analyze the size of the WEF created. Recall that is the number of bits of storage required by the algorithm A, which of course consists of a constant number of lines of pseudocode. The variables of are the variables , and additional temporary variables created in some of the groups C–G. It can be verified that their number is . For fixed , each of the sets of inequalities described in groups C–G have size at most except possibly the array assignment inequalities described in G(viii) and G(ix). As remarked there, an array of dimension generates inequalities. A 2-dimensional array of dimension by generates inequalities. We may assume that . Then is an upper bound the number of inequalities generated in either G(viii) or G(ix). Since is bounded by we see that the WEF has at most inequalities also. We have:

Theorem 2.

Let be a decision problem with corresponding polytope defined by (10). An algorithm for written in the pseudocode described above requiring space and terminating after steps generates a WEF for with inequalities and variables.

Since Edmonds’ algorithm can be implemented in polynomial time in the pseudocode presented our method gives a polynomial size WEF for . So for example, a straightforward implementation of Edmonds’ algorithm using space would yield a WEF with inequalities and variables. If the time algorithm of Even and Kariv [11] can be implemented in our pseudocode it would yield a considerably smaller polytope.

Sparktope is a compiler built along the lines described above to automatically generate a WEF corresponding to any given pseudocode [2]. The elements described in C–G above have been implemented and tested as well as some complete examples of pseudocode. The polytopes generated are rather large even for short pseudocodes. For example, the pseudocode at the beginning of this section generated a polytope with about 3200 inequalities! This should be compared with 28 inequalities for the circuit in Figure 1 and 4 odd set inequalities for Edmonds’ polytope . Nevertheless the WEF generated by this method should be significantly smaller than even for relatively small . The details of the implementation of the compiler and its application to Edmonds’ algorithm will be described in a subsequent paper.

5 Connections to non-negative rank

In this section we reformulate the results in previous sections in terms of non-negative ranks of certain matrices. Non-negative rank is a very useful tool that captures the extension complexity of polytopes [20]. We will prove a necessary condition for membership testing in a language to be in P/poly based on the existence of a certain matrix with polynomially bounded non-negative rank. This characterization potentially opens the door to proving that a given problem does not belong to P/poly by demonstrating high non-negative rank of the associated matrix. Using a slightly stronger definition of non-negative rank we are also able to give a sufficient condition for membership testing in a language to be in P/poly.

A matrix is called non-negative if all its entries are non-negative. The non-negative rank of a non-negative matrix , denoted by , is the smallest number such that there exist non-negative matrices and such that has columns, has rows and . If we require the left factor in the above definition to only contain numbers that can be encoded using a number of bits only polynomial in the number of bits required to encode any entry of then the smallest such is called the succinct non-negative rank of . To see the usefulness of this apparently asymmetric restriction on the factors, note that when is the slack matrix of a polytope then such a factorization allows one to describe an extended formulation for the polytope using only the entries of and . So if is required to be polynomial in the bit complexity of the entries of then one can represent the polytope as the shadow of another polytope that can be encoded using a polynomial number of bits.

5.1 Polytopal sandwiches

Let and be two polytopes in such that We say that such a pair defines a polytopal sandwich. With every polytopal sandwich we can associate a non-negative matrix which encodes the slack of the inequalities defining with respect to the vertices of That is, if and then the slack matrix associated with the polytopal sandwich thus defined is with When and define the same polytope we denote the corresponding slack matrix simply as The next lemma shows the relation between the non-negative rank of the slack of a polytopal sandwich and the smallest size polytope whose shadow fits in the sandwich. We will assume that the polytopes defining our sandwiches are full-dimensional. The same lemma appears in [6] and has roots in [13, 16]. However the proof is simple enough to attribute it to folklore.

Lemma 5.

Let and Let be a polytope with smallest extension complexity such that . Then,

Proof.

Let be any polytope in the sandwich, i.e. We can describe as the convex hull of the vertices of together with the vertices of Similarly we can describe as the intersection of all its facet-defining inequalities and the facet-defining inequalities of Now the matrix is a submatrix of the slack matrix of this particular representation of Therefore, It is easy to see (see, for example, [12]) that the non-negative rank of the slack matrix of a polytope is not changed by adding redundant inequalities and points in its representation. Also, since the non-negative rank of the slack matrix of a polytope is equal to its extension complexity ([12]), we have that

Now, suppose that That is there exist non-negative matrices and with columns and rows respectively, such that Denote by the -th row of and the -th column of . Consider the polytope

and let

Since, by definition, is a projection of and has at most inequalities, we have that

Next we show that . Suppose Then That is and for all Since is non-negative, and therefore for all That is, Therefore, Suppose Then for some Consider Then, for each we have that Clearly since is non-negative. So and thus Therefore .

Since lies in the polytopal sandwich we have as proved in the first paragraph of the proof. Therefore the inequality is in fact an equation and we may set completing the proof. ∎

Note that given a polytopal sandwich , any lower bound on the non-negative rank of its slack matrix is also the lower bound on the succinct non-negative rank of . Conversely, any upper bound on the succinct non-negative rank of is also an upper bound on the non-negative rank of . In the next subsection we will define canonical polytopal sandwiches for binary languages and discuss the relation of the non-negative rank and succinct non-negative rank of the associated slack matrix with whether or not membership testing in the language belongs to P/poly.

5.2 Languages and their sandwiches

In the sequel we consider languages over the alphabet. Let be a such a language. For any positive integer define the set as

To make the connection with Section 2.2, plays the role of the decision problem and is the set of instances of size that have a ”yes” answer.

Corresponding to any language let us define a polytopal sandwich given by a pair of polytopes. The inner polytope is described by its vertices and is contained in the outer polytope, which in turn is described by a set of inequalities. Both the vertices of the inner polytope and the inequalities for the outer polytope depend only on the language We call such a sandwich the characteristic sandwich of .

For every language we define characteristic functions and with

In terms of Section 2.2, will play the role of and will play the role of the objective function vector . The inner polytope is defined by

| (18) |

In terms of Section 2.2, plays the role of and for the perfect matching problem it is .

For positive integer and , define

| (19) |

Note that the normal vectors of the inequalities defining are just the optimization directions that were used in Section 2.2.

By direct substitution we see that each vertex of satisfies the constraints of and so . We will show that the following matrix is its slack matrix. For every consider the non-negative matrix defined as follows. Rows and columns of are indexed by vectors of length and

where

Lemma 6.

The slack of with respect to is the matrix

Proof.

Consider two vectors The slack of the inequality corresponding to with respect to is

Observing that we can see that Therefore the slack of the inequality corresponding to with respect to is

∎

The following lemma is analogous to Proposition 3.

Lemma 7.

Let be a polytope such that Then, deciding whether a vector is in or not can be achieved by optimizing over along the direction (.

Proof.

Let be a given vector in Consider the maxima of when , and respectively. Since we have that

Since , . Furthermore, gives rise to the inequality

in and so . Since , .

Therefore whether or not tells us whether or not. ∎

Theorem 3.

Let be a language over the 0/1 alphabet and

let be any positive integer.

(a) If

belongs to the class P/poly then

there is a constant and slack matrix such that both the

the size of and

the non-negative rank of are

polynomial in .

(b) If there is a constant and slack matrix such that both

the size of and

the succinct non-negative rank of are

polynomial in then belongs to the class P/poly.

Proof.

(a) Suppose belongs to the class P/poly then by Lemma 1 there is a polytope that is a WEF of with size bounded by a polynomial in . Let be the projection of onto its first coordinates. Since is a WEF of we have . Applying Proposition 4 to we obtain a value , whose size is polynomially bounded in . Set For any vector this proposition implies that if we optimize over the maximum value obtained is . Therefore the inequality corresponding to this in the definition of is satisfied for all . It follows that and so lies in the polytopal sandwich defined by and . Since is the slack of with respect to , by Lemma 5 the non-negative rank of is upper bounded by the extension complexity of any polytope sandwiched between the two polytopes. Since the size of is bounded above by a polynomial in and is the extension of some polytope that can be sandwiched between and we have that the non-negative rank of is bounded by a polynomial in

(b) Suppose for some constant the slack matrix has succinct non-negative rank and that both and are polynomially bounded in . Since is the slack of with respect to by Lemma 5 there exists a polytope such that the extension complexity of is and In other words, there exist polytopes and such that has facets, projects to and . Furthermore, from the proof of Lemma 5 we know there exists such a whose description contains only numbers polynomially bounded in because the rank non-negative factorization is succinct by our assumption. Using the given value of , by Lemma 7 we can optimize over to decide whether or not for a given Furthermore, optimizing over can be done by optimizing over instead, since projects to . Since has polynomial bit complexity, we can use interior point methods to do the optimization and so determine membership in in polynomial time. ∎

Theorem 3(a) in principle paves a way to show that membership testing in a certain language is not in P/poly by showing that the non negative rank of associated slack matrices cannot be polynomially bounded. Various techniques exist to show lower bounds for the non-negative rank of matrices and have been used to prove super-polynomial lower bounds for the extension complexity of important polytopes like the CUT polytope, the TSP polytope, and the Perfect Matching polytope of Edmonds, among others [12, 18, 4, 17]. Whether one can apply such techniques to show super-polynomial lower bounds on the non-negative rank of the slack of the characteristic sandwich of some language is left as an open problem.

6 Concluding remarks

In this paper we have given a method for constructing polynomial size linear programs for solving decision problems in P from their underlying algorithms. As a concrete example we can construct an LP of size that decides whether an input graph on vertices has a perfect matching or not. This LP is based on an implementation of Edmonds’ algorithm and smaller polytopes can be obtained by using more efficient implementations. This raises the question of what is the smallest size LP for the perfect matching problem and whether or not there is an LP that has an explicit formulation. Along these lines we mention a recent result in [5] for 2SAT. The standard formulation for this problem has superpolynomial time extension complexity. Applying the method of Section 4 to a standard 2SAT algorithm yields an LP of size . However in [5] a simple compact WEF for 2SAT of size is given.

The discussion in this paper was centred around decision problems and one may wonder if it can be applied to optimization problems also. Before addressing this let us recall some discussion on the topic in Yannakakis’ paper [20]:

Linear programming is complete for decision problems in P; the question is equivalent to a weaker requirement of the LP (than that expressing the TSP polytope), in some sense reflecting the difference between decision and optimization problems. (P. 445, emphasis ours)

The term “expressing” in the citation refers to an extended formulation of polynomial size. The method we have described can indeed be used to construct polynomial sized LPs for optimization problems which have polynomial time algorithms. Consider, for example, the problem of finding a maximum weight matching for the complete graph , where the edge weights are integers of length bits. For simplicity we assume the weights are non-negative, but a small extension would handle the general case. We construct a polytope as defined by (10) as follows. The binary vectors have length , where the first bits encode the edge weights and the remaining bits encode an integer . The bit is defined by setting whenever the edge weights specified in admit a matching of weight or greater and otherwise. Note that the unweighted maximum matching problem for graphs on vertices fits into this framework by setting .

Applying the method of Section 4 to the weighted version of Edmonds’ algorithm we obtain a polynomial sized WEF for . We can decide by solving a single LP over if a given weighted has a matching of weight at least , for any fixed : the last coefficients of the objective function (11) vary depending on . Therefore, by binary search on we can solve the maximum weight matching problem for a given input by optimizing times over with objective functions depending on . We do not, however, know how to solve the weighted matching problem by means of a single polynomially sized linear program.

Acknowledgments

We would like to thank the referees of this paper for their detailed comments leading to several important improvements. This research is supported by a Grant-in-Aid for Scientific Research on Innovative Areas – Exploring the Limits of Computation(ELC), MEXT, Japan. Research of the second author is partially supported by NSERC Canada. Research of the third author is supported by project GA15-11559S of GA ČR.

References

- Arora and Barak [2009] S. Arora and B. Barak. Computational Complexity - A Modern Approach. Cambridge University Press, 2009.

- Avis and Bremner [2017] D. Avis and D. Bremner. Sparktope. https://gitlab.com/sparktope/sparktope and http://www.cs.unb.ca/~bremner/research/sparks_lp/, 2017.

- Avis and Tiwary [2015a] D. Avis and H. R. Tiwary. A generalization of extension complexity that captures P. Inf. Process. Lett., 115(6-8):588–593, 2015a.

- Avis and Tiwary [2015b] D. Avis and H. R. Tiwary. On the extension complexity of combinatorial polytopes. Math. Program., 153(1):95–115, 2015b.

- Avis and Tiwary [2017(European J. Combinatorics, to appear] D. Avis and H. R. Tiwary. Compact linear programs for 2SAT. CoRR, abs/1702.06723, 2017(European J. Combinatorics, to appear).

- Braun et al. [2012] G. Braun, S. Fiorini, S. Pokutta, and D. Steurer. Approximation limits of linear programs (beyond hierarchies). In 53rd Annual IEEE Symposium on Foundations of Computer Science, FOCS 2012, New Brunswick, NJ, USA, October 20-23, 2012, pages 480–489, 2012.

- Cook and Reckhow [1973] S. A. Cook and R. A. Reckhow. Time bounded random access machines. J. Comput. System Sci., 7:354–375, 1973. Fourth Annual ACM Symposium on the Theory of Computing (Denver, Colo., 1972).

- Dobkin et al. [1979] D. P. Dobkin, R. J. Lipton, and S. P. Reiss. Linear programming is log-space hard for P. Inf. Process. Lett., 8:96–97, 1979.

- Edmonds [1965a] J. Edmonds. Paths, trees, and flowers. Canad. J. Math., 17:449–467, 1965a.

- Edmonds [1965b] J. Edmonds. Maximum matching and a polyhedron with vertices. J. of Res. the Nat. Bureau of Standards, 69 B:125–130, 1965b.

- Even and Kariv [1975] S. Even and O. Kariv. algorithm for maximum matching in general graphs. In FOCS, pages 100–112, 1975.

- Fiorini et al. [2015] S. Fiorini, S. Massar, S. Pokutta, H. R. Tiwary, and R. de Wolf. Exponential lower bounds for polytopes in combinatorial optimization. J. ACM, 62(2):17:1–17:23, 2015.

- Gillis and Glineur [2012] N. Gillis and F. Glineur. On the geometric interpretation of the nonnegative rank. Linear Algebra and its Applications, 437(11):2685–2712, dec 2012.

- Grötschel et al. [1993] M. Grötschel, L. Lovász, and A. Schrijver. Geometric algorithms and combinatorial optimization, volume 2 of Algorithms and Combinatorics. Springer-Verlag, Berlin, second edition, 1993.

- Horowitz and Sahni [1978] E. Horowitz and S. Sahni. Fundamentals of Computer Algorithms. Computer Science Press, 1978.

- Pashkovich [2012] K. Pashkovich. Extended formulations for combinatorial polytopes. PhD thesis, Otto-von-Guericke-Universitẗ, Magdeburg, 2012.

- Pokutta and Vyve [2013] S. Pokutta and M. V. Vyve. A note on the extension complexity of the knapsack polytope. To appear in Operations Research Letters, 2013.

- Rothvoss [2017] T. Rothvoss. The matching polytope has exponential extension complexity. J. ACM, 64(6):41:1–41:19, 2017.

- Valiant [1982] L. G. Valiant. Reducibility by algebraic projections. Enseign. Math. (2), 28(3-4):253–268, 1982.

- Yannakakis [1991] M. Yannakakis. Expressing combinatorial optimization problems by linear programs. Journal of Computer and System Sciences, 43(3):441–466, 1991.

Appendix A Valid inequalities and facets of

We give here two classes of valid inequalities for . Firstly, let define a perfect matching in . We have:

| (20) |

To see the validity of this inequality, note that if is a perfect matching the sum becomes and the inequality states that , i.e. has a perfect matching. We show below that the each inequality of type (20) define a facet of . Since the number of perfect matchings in is the double factorial the number of facet defining inequalities of is therefore super-polynomial.

For a second set of valid inequalities, first let be the set of edges of . A proper subset is hypo-matchable if it has no matching of size but the addition of any other edge from to yields such a matching. Then we have:

| (21) |

To see the validity of this inequality note that if the sum is zero then no edges from are in . So has no perfect matching and so must be zero.

We now prove that the inequalities (20) are facet defining for , where we have replaced by to avoid fractions. For any integer we use the notations and to represent, respectively, the identity matrix, matrix of all ones, and matrix of all zeroes. With only one subscript, the latter two notations represent the corresponding vectors. For an integer we let . Without loss of generality, consider a perfect matching in consisting of the edges and let be the edges of that are not in . We construct a set of graphs for which inequality (20) is tight and for which the vectors are affinely independent. The corresponding -matrix of edge vectors is:

| (22) |

We label the columns of as follows. The first columns correspond to the edges in listed in lexicographical order by . The next columns are indexed by the edges of and the final column by . The first rows of consist of the edge vectors of graphs which contain and precisely one other edge not in , arranged in lexicographic order by . This means that the top left hand block in is the identity matrix. Since all these graphs contain , which is a perfect matching, all these remaining entries in the first rows of are ones.

The next rows of correspond to graphs with edge vectors , where ranges over the perfect matching . Clearly the first block of these rows are all zeroes and the second block is . The last column is all zero since none of these graphs has a perfect matching. The final row of corresponds to the graph .

It is straight forward to perform row operations on to transform it into an upper triangular matrix with on the main diagonal. This can be performed by subtracting the last row from the preceding rows. The middle block of is now . Finally these rows can then be added to the last row, which is then divided by . It is then all zero except for the last column, which is -1. This completes the proof.