A fast and accurate numerical method for the symmetric Lévy processes based on the Fourier transform and sinc-Gauss sampling formula

Abstract

In this paper, we propose a fast and accurate numerical method based on Fourier transform to solve Kolmogorov forward equations of symmetric scalar Lévy processes. The method is based on the accurate numerical formulas for Fourier transform proposed by Ooura. These formulas are combined with nonuniform fast Fourier transform (FFT) and fractional FFT to speed up the numerical computations. Moreover, we propose a formula for numerical indefinite integration on equispaced grids as a component of the method. The proposed integration formula is based on the sinc-Gauss sampling formula, which is a function approximation formula. This integration formula is also combined with the FFT. Therefore, all steps of the proposed method are executed using the FFT and its variants. The proposed method allows us to be free from some special treatments for a non-smooth initial condition and numerical time integration. The numerical solutions obtained by the proposed method appeared to be exponentially convergent on the interval if the corresponding exact solutions do not have sharp cusps. Furthermore, the real computational times are approximately consistent with the theoretical estimates. Lévy process; Kolmogorov forward equation; nonuniform FFT; fractional FFT; sinc-Gauss sampling formula.

1 Introduction

In this paper, we propose a fast and accurate numerical method based on the Fourier transform to solve the Kolmogorov forward equations of the symmetric scalar Lévy processes. To propose the method, we use Ooura’s accurate numerical formulas for the Fourier transform (Ooura, 2001, 2005), and propose a numerical indefinite integration formula based on the sinc-Gauss sampling formula (Tanaka et al., 2008) to compute the integrals with respect to the Lévy measures in the equation. Furthermore, we combine the fast Fourier transform (FFT) with these formulas to speed up the numerical computations.

A Lévy process is essentially a stochastic process with stationary and independent increments (Applebaum, 2009), which is used to describe uncertain phenomena in various fields. Let us consider a brief non-rigorous review of the scalar Lévy process . The Lévy-Khintchine theorem characterizes by reals , , and a Borel measure on as

| (1.1) |

where is the characteristic exponent of defined by

| (1.2) |

Here, we assume that the measure satisfies

| (1.3) |

Then, is called the Lévy measure. An operator semigroup is associated with , namely , where is a bounded continuous function on . The infinitesimal generator takes the form

| (1.4) |

Then, the function is the solution of the partial integro-differential equation (PIDE)

| (1.5) |

with initial condition . Assuming that there exist the transition probability measure of with appropriate continuity and differentiability for each and the adjoint operator of , we have

| (1.6) |

with initial condition , where is the Dirac delta function. Equation (1.6) is the Kolmogorov forward equation, which is also known as the Fokker-Planck equation. Furthermore, the equation

| (1.7) |

with initial condition is known as the Kolmogorov backward equation.

In various fields such as physics, chemistry, biology, engineering, and economics, the Kolmogorov forward equations including fractional derivatives are often considered to describe some unusual diffusion such as anomalous diffusion. For example, see Gardiner (2009); Kozubowski et al. (2006); Lenzi et al. (2003); Sabatier et al. (2007); Yan (2013) and the references therein. Such equations are related to -stable processes belonging to the Lévy processes. In finance, some Lévy processes are used to describe the prices of risk assets. Then, the Kolmogorov backward equations for these processes are considered as one of the useful methods for option pricing. See Cont & Voltchkova (2005); Garreau & Kopriva (2013); Lee et al. (2012) and the references therein.

In the fields mentioned above, many numerical methods for these Kolmogorov equations are studied. Popular examples of such methods are finite difference methods (Gao et al., 2013; Huang & Oberman, 2013; Li et al., 2012; Meerschaert, 2004), finite element methods (Zhao & Lib, 2012), spectral methods (Bueno-Orovio et al., 2014; Huang et al., 2014), and other methods (Yan, 2013) for the forward equations describing anomalous diffusion etc. Further, such methods have been proposed for the backward equations in finance (Duquesne et al., 2010; Garreau & Kopriva, 2013; Kwok et al., 2012; Lee et al., 2012). In many of these methods, first, a time-evolution system of ordinary differential equations is derived from the given PIDE by the discretization of the spatial variable with finite differences, finite elements, polynomial expansions, etc., and some quadrature formulas. Then, the system is numerically solved using some numerical time integration methods such as second-order finite difference methods. In addition, in the case where the closed form of the characteristic function of the Lévy process can be obtained, methods based on the Fourier series or the Fourier transform are used in option pricing (Carr & Madan, 1999; Chourdakis, 2005; Fang & Oosterlee, 2008; Kwok et al., 2012).

In this paper, we propose a method based on the Fourier transform for equation (1.6) for broader classes of the Lévy measure for which the closed form of the corresponding characteristic function may not be available. For simplicity, we consider the case in (1.4) and measure has the form

| (1.8) |

where or and . Then, the corresponding Lévy process becomes symmetric. As examples of the Lévy process with such measure, we can give the variance gamma (VG) process (Applebaum, 2009), also known as the symmetric Laplace motion (Kozubowski et al., 2006), with and , and the normal inverse Gaussian (NIG) process (Applebaum, 2009) with and , where is the modified Bessel function of the second kind. Then, applying (1.8) to the operator in (1.4) and taking its adjoint, we have a special form of equation (1.6) as

| (1.9) |

where is denoted by for conciseness, and

| (1.10) |

Note that the third term of the integrand in (1.4) vanishes because of the symmetry of . Furthermore, we assume that for simplicity and as for any so that

| (1.11) |

for any . Therefore, we consider equation (1.9) with initial condition and auxiliary condition (1.11) in the rest of this paper.

There are two main objectives of the method proposed in this paper. The first is to show that a fast and accurate Fourier-based method can be realized for equation (1.9) including a (seemingly) singular integral in (1.10). Using the Fourier transform, we do not need specific requirements for the non-smooth initial condition , whereas some of the existing methods with time integration cited above need a priori artificial approximation of the solution for a small time . In addition, since equation (1.9) is linear and contains only constant coefficients, which is also the case for the general in (1.4), the Fourier-based method does not need numerical time integration. Therefore, we can compute approximate solutions of for any with the same computational cost, and errors of numerical time integration do not occur. The second objective of the proposed method is to present new applications of Ooura’s methods (Ooura, 2001, 2005) for the Fourier transforms to obtain the solution of PIDEs. The high accuracy of the proposed method is due to the very fast convergence of Ooura’s methods, and speeding up of computations by Ooura’s methods is realized by combining them with the nonuniform FFT (Dutt & Rokhlin, 1993, 1995; Greengard & Lee, 2004; Potts et al., 2001; Steidl, 1998) or the fractional FFT (Bailey & Swarztrauber, 1991; Chourdakis, 2005; Tanaka, 2014a). In addition, in order to treat a (seemingly) singular integral in (1.10), we propose an indefinite integration formula using the sinc-Gauss sampling formula (Tanaka et al., 2008), which is also accurate and combined with the FFT. Thus, as shown precisely in Sections 2 and 3, all steps of the proposed method are executed by the FFT and its variants.

2 Outline of the proposed method

In order to obtain a fast and accurate numerical method to solve (1.9), we considered a method based on the Fourier transform for using the FFT. First, we derive the formula for the solution of (1.9) using the Fourier transform

| (2.1) |

Taking the Fourier transform for both sides of (1.9) with respect to the spatial variable , we have

| (2.2) |

where

| (2.3) |

For , noting that , we have

| (2.4) |

and therefore,

| (2.5) |

For , noting that

and , we have

| (2.6) |

Therefore, we have

| (2.7) |

Using expression (2.5) or (2.7), we can derive the form of the solution from (2.2) as

| (2.8) |

Then, we can consider the following numerical method to obtain an approximation of the solution (2.8). Let , , and be an integer, a grid spacing, and a time, respectively. Suppose that we need to compute approximate values of for .

- Step 1

-

Computation of the Fourier transform

(2.9) in (2.5) or (2.7). Choose a grid spacing and integers . Then, use the double exponential (DE) formula for the Fourier transforms (Ooura, 2005) with sampling points and the nonuniform FFT (Dutt & Rokhlin, 1993, 1995; Greengard & Lee, 2004; Potts et al., 2001; Steidl, 1998) to obtain approximate values of (2.9) for . The definitions of , and are presented in Sections 3.1 and 3.2.

- Step 2

-

Computation of the indefinite integral of (2.9) in (2.5) or (2.7). Use the computed values in Step 1 and an indefinite integration by the sinc-Gauss sampling formula proposed in Section 3.2 to obtain approximate values of for , where we suppose that can be divided by . Note that the approximate values on the equispaced grid are obtained from the approximate values of the integrand on the same grid. The definition of is presented in Section 3.2.

- Step 3

-

Computation of the inverse Fourier transform (2.8). Use the computed values in Step 2, the formula for the Fourier transform with continuous Euler transform (Ooura, 2001), and the fractional FFT (Bailey & Swarztrauber, 1991; Chourdakis, 2005; Tanaka, 2014a) to obtain the approximate values of the solution for .

In summary, the proposed method is illustrated by the diagram below. The details of the three steps are shown in Section 3.

3 Proposed method

3.1 Step 1: Computation of the Fourier transform (2.9) in (2.5) or (2.7)

The DE formula for the Fourier transforms and the nonuniform FFT for the Fourier transform (2.9) are described in Sections 3.1.1 and 3.1.2, respectively. The contribution of this paper is speeding up the computation through the use of the DE formula by combining it with nonuniform FFT.

3.1.1 DE formula for the Fourier transforms by Ooura

We begin with the review of the DE formula for the Fourier transforms (2.9) proposed by Ooura (2005). Let and be positive constants and let the function be defined by

| (3.1) |

where and

| (3.2) |

Then, the following formula approximates the integral (2.9) for for some :

| (3.3) |

where . The integers and are determined in an appropriate manner. Formula (3.3) is the DE formula for the Fourier transforms, which is derived as follows. First, applying the variable transformation to integral (2.9), we have

| (3.4) |

where . Let denote expression (3.4). Next, from subtract

| (3.5) |

which is very small for and a large . Then, discretizing

| (3.6) |

by the mid-point rule with grid spacing , we have (3.3). Since as and as , the factor in (3.6) converges rapidly (“double exponentially”) to as . Therefore, the discretization of (3.6) by the mid-point rule can yield accurate approximation (3.3) for some independent of , and sufficiently large and . In Ooura (2005), the error of approximation (3.3) is bounded by for some depending on , and it is illustrated by some numerical examples. A theoretically rigorous analysis for the error, however, is not described in Ooura (2005).

Then, noting that

| (3.7) |

we can achieve Step 1 by computing the values of (3.3) for and taking their complex conjugates for . In computing the values of (3.3), we need to choose so that for . The possible values of the nonnegative reals and , however, are not theoretically estimated. According to some numerical examples including those in Ooura (2005), when is small, can be taken as and can be small. As becomes large, unfortunately, and need to be large. These facts are illustrated by Figure 1. Therefore, if we let be a single value near to when is large, we cannot have accurate approximations of (2.9) for for ’s near to or . Then, we use

| (3.8) | |||

| (3.9) |

Figure 1 also illustrates these settings, which are experientially determined and not based on theoretical criteria.

Note that the naive computation of (3.3) for (3.8) and (3.9) requires operations if . Then, what remains in Step 1 is to speed up the numerical computation. Thus, we use the technique of the nonuniform FFT explained in Section 3.1.2 below.

(a)

(b)

3.1.2 Nonuniform FFT

Let the sum in (3.3) for be rewritten as

| (3.10) |

where

| (3.11) | ||||

| (3.12) |

The nonuniform FFT (Dutt & Rokhlin, 1993, 1995; Greengard & Lee, 2004; Potts et al., 2001; Steidl, 1998) is a fast method to compute the DFT in (3.10) with a nonuniform grid such as defined by (3.12). To use the technique of the nonuniform FFT, setting

| (3.13) | ||||

| (3.14) |

we note the following relation:

| (3.15) |

where , , , and are positive constants to be determined appropriately. To decrease the computational cost of the sum in in (3.15), we neglect the sufficiently small summands present in it

| (3.16) |

where is the set of the indexes defined by

| (3.17) |

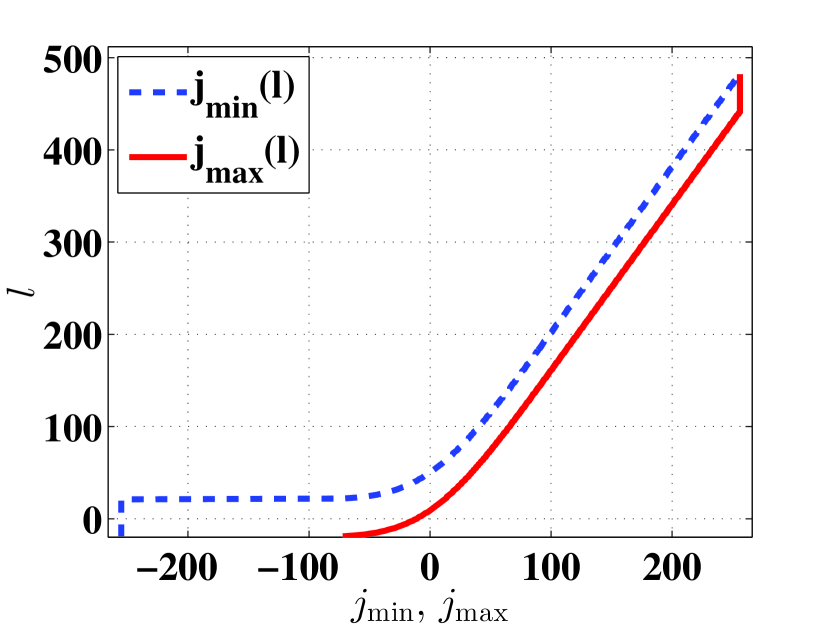

for some . Since is defined by in (3.1) as (3.12) and monotone increasing with respect to , the index set is contained in the slightly augmented set defined by

| (3.18) |

where

| (3.19) | ||||

| (3.20) |

Figure 2 shows examples of and . As explained in Remark 2 below, we can obtain for efficiently. The definition (3.18) of means that the truncation error of approximation (3.16) is . Then, in addition to , , , and , we need to choose the constant so that both the total error (i.e., the sum of the discretization error for (3.15) and the truncation error for (3.16)) and the computational cost are reasonably small. For and a sufficiently small such as , we can present one possible set of their choices:111When , and in (3.21).

| (3.21) | |||

| (3.22) |

Under these settings, the total error of approximations (3.15) and (3.16) is approximately . We may use larger than the value above. Then, we can obtain the approximate values of as

| (3.23) |

where we can use the FFT for the outer sum. Under the settings of and in (3.21), the period of expression (3.23) with respect to is . Therefore, we need to set

| (3.24) |

to compute the accurate approximations . Then, the computational cost is .

Remark 1.

In (3.15) and (3.23), we use the shifted index in (3.14) to avoid numerical instability in the actual computation of the approximate values in (3.23). In fact, if we use the factor in (3.23) as a usual manner of the nonuniform FFT, it becomes considerably large for a large and the approximation gets worse.

Remark 2.

The inequalities in (3.19) and (3.20) respectively defining and are nonlinear with respect to , and it is difficult to obtain their closed forms. Therefore, noting the monotonicity of with respect to , we use the following numerical algorithms to determine them efficiently.

Algorithm for

begin

for to

for to

if

else

break

end

end

end

end

Algorithm for

begin

for to

for to

if

else

break

end

end

end

end

3.2 Step 2: Computation of the indefinite integral of (2.9) in (2.5) or (2.7)

In this step, using the values , i.e., the approximate values of (2.9) for , we obtain the approximate values of the indefinite integral (2.9) in (2.5) or (2.7) for . Recall that is the integer determining the number of ’s for which we want to compute the values of the solution in (2.8). Noting (3.7), we have only to compute the approximate values for .

3.2.1 Sinc-Gauss indefinite integration formula

Let be a positive integer. As a tool for computing indefinite integrals, we use the sinc-Gauss sampling formula (Tanaka et al., 2008) for a function on

| (3.25) |

where . The error estimate of this formula is given by the following theorem, which is a combination of the special cases of Lemmas 3.1 and 3.2 in Tanaka et al. (2008).

Theorem 1 ((Tanaka et al., 2008, Lemmas 3.1, 3.2)).

Let be an analytic and bounded function in for some , and let . Then, for a sufficiently large and a sufficiently small , we have the following estimates of the discritization error (3.26) and the truncation error (3.27) of approximation (3.25):

| (3.26) | |||

| (3.27) |

where and are positive constants independent of , , and .

From formula (3.25), we derive a formula to approximate the indefinite integral of from to with . Partitioning the integral of as

| (3.28) |

and applying formula (3.25) to each term of the RHS in (3.28), we have

| (3.29) |

where

| (3.30) |

For , straightforwardly we have

| (3.31) |

For , setting and , we can rewrite the RHS of (3.29) as

| (3.32) |

where is the set of indexes defined by

| (3.33) |

Here, we partition this index set into three disjoint parts as

| (3.34) |

where

| (3.35) | ||||

| (3.36) | ||||

| (3.37) |

The type of this partition is illustrated by Figure 3. If we define as

| (3.38) |

we have

| (3.39) |

and

| (3.40) | ||||

| (3.41) | ||||

| (3.42) |

Then, combining (3.32) and (3.39)–(3.42), we have

| (3.43) |

Letting , we can regard the first term of (3.43) as a discrete convolution

| (3.44) |

Thus, rewriting as in (3.31) and (3.44), we finally have an indefinite integration formula:

| (3.45) |

where

| (3.46) |

To obtain the values of (3.45) for , we need the values of for .

Therefore, to compute the indefinite integral of (2.9) in (2.5) for , we set

| (3.47) |

and use formula (3.45) with and replaced by for . Furthermore, for the integral of (2.9) in (2.7), we set

| (3.48) |

and use formula (3.45) twice with for the first time and for the second time.

In terms of computational time, note that the second term in (3.45) and in (3.46) can be computed in time when or . Then, what remains is to speed up the computation of the discrete convolution of the first term in (3.45). Extending the sum to a convolution with length and using the FFT as shown in Section 3.2.2 below, we can compute the discrete convolution of the first term in time when or .

3.2.2 Fast computation of the convolution using the FFT

Consider the first term in (3.45) with replaced by :

| (3.49) |

We compute this convolution for , although its values for are not required. To use the FFT for this computation, we define the sequence as

| (3.50) |

Then, we have

| (3.51) |

for , where

| (3.52) | ||||

| (3.53) |

For the computation of (3.51), we need the values of in (3.30). In fact, they can also be computed accurately by a Fourier-based method and the FFT as presented in Appendix A.Therefore, we can compute (3.51) by the FFT in time when or .

Remark 3.

Since the indefinite integration formula (3.45) is derived from the sinc-Gauss sampling formula (3.25), formula (3.45) inherits the error of formula (3.25) estimated in Theorem 1. In particular, the error of formula (3.45) is bounded by one of formula (3.25) multiplied by . According to Theorem 1, the optimal settings of and for fixed are and , respectively, and the total error of formula (3.25) under these settings is (Tanaka et al., 2008, Theorem 3.3). In this paper, however, we use the grid spacing determined by (3.61) in Theorem 2 in Section 3.3 below, which results in . This choice gives priority to the theoretical settings of the parameters in formula (3.56) for the inverse Fourier transform (2.8) in Step 3. Then, this and yield the total error of formula (3.25), which has a similar exponential part to error (3.62) of formula (3.56) with respect to when or .

Remark 4.

The new formula (3.45) is introduced for fast computation of highly accurate approximations of an indefinite integral on the equispaced grid from the values of the integrand on the same grid. Among the traditional quadrature formulas, the Newton-Cotes formulas enable such computation. However, these formulas have errors for some , and become algebraic with respect to when for some , whereas the formula (3.45) realizes the exponential convergence as shown in Remark 3.

3.3 Step 3: Computation of the inverse Fourier transform

Let denote the approximations of (2.5) or (2.7) computed in Step 2. In order to approximate the inverse Fourier transform (2.8), we use the formula for the Fourier transform with a continuous Euler transform introduced by Ooura (2001). Define by

| (3.54) |

where is the complementary error function defined as

| (3.55) |

Using as a weight function, we consider the following approximations of (2.8):

| (3.56) |

The formula (3.56) is the formula for the Fourier transform with a continuous Euler transform. The role of the function is to realize the rapid decay of the integrand as on . Then, we need to compute the values of (3.56) for . Substituting this expression of into the factor in (3.56), we have

| (3.57) |

Unless the Nyquist condition holds, we cannot apply the FFT directly to the computation of (3.56). Therefore, for this computation, we use the fractional FFT (Bailey & Swarztrauber, 1991) that enables fast computation of the DFT without the Nyquist condition. Then, we can compute (3.56) in time. The details of the fractional FFT combined with the formula (3.56) is explained in Tanaka (2014a). The error bound of the formula (3.56) is given by Theorem 4 in Tanaka (2014a).

Theorem 2 ((Tanaka, 2014a, Theorem 4)).

Let be a function analytic and bounded in for some with and , where

| (3.58) | ||||

| (3.59) |

Moreover, assume that

| (3.60) |

and is square integrable on . Let and be real numbers with and . Then, for any with and a sufficiently large integer , defining , , by

| (3.61) |

we have

| (3.62) |

Remark 6.

Since the assumption of Theorem 2 includes the case that is not absolute integrable on , the Fourier transform of may be discontinuous or non-smooth at the origin . Then, we consider the positive lower bound of the absolute value of to avoid the error estimate around the origin. See Tanaka (2014a) for the details of the error estimate.

Remark 7.

We use the different formulas (3.3) and (3.56) for the Fourier transforms (2.9) and (2.8), respectively. This is because the former Fourier transform (2.9) is the integral on the semi-infinite interval whereas the latter Fourier transform (2.8) is one on the infinite interval . Further, we can also use formula (3.3) for (2.8) by partitioning the interval to and . However, we give priority to a brief implementation and lower computational cost of formula (3.56).

4 Numerical examples

In this section, we apply the proposed method to two examples of the PIDE (1.9) with initial condition . Let be the modified Bessel function of the second kind.

Example 1 (Variance gamma (VG) process (Applebaum, 2009)).

Example 2 (Normal inverse Gaussian (NIG) process (Applebaum, 2009)).

Using the proposed method, we compute the numerical solutions of these examples for and . Then, in Theorem 2 should be set as . In addition, we choose . To set equispaced grids on , we consider the sampling points with for

| (4.5) |

where for Example 1 and for Example 2. The other parameters in the proposed method are determined as described below.

- Step 1

- Step 2

- Step 3

-

According to Theorem 2, we set because .

In (4.6), is not set based on a theoretical criterion but it is determined experimentally in reference to the settings in the DE formulas for definite integration (Tanaka et al., 2009). All computations are performed through MATLAB R2013a programs with double precision floating point arithmetic on a PC with a GHz CPU and GB RAM. The Matlab codes used for the computations are exposed on web page Tanaka (2014b).

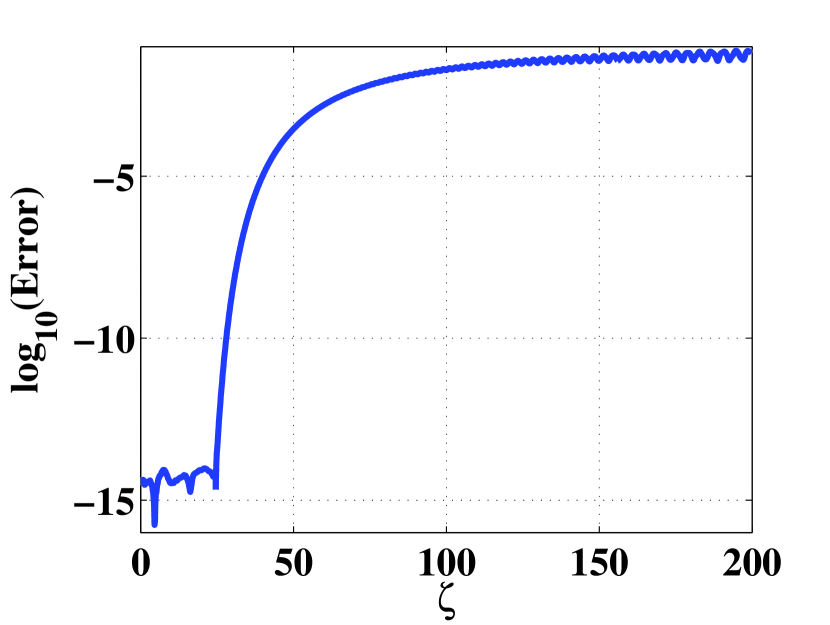

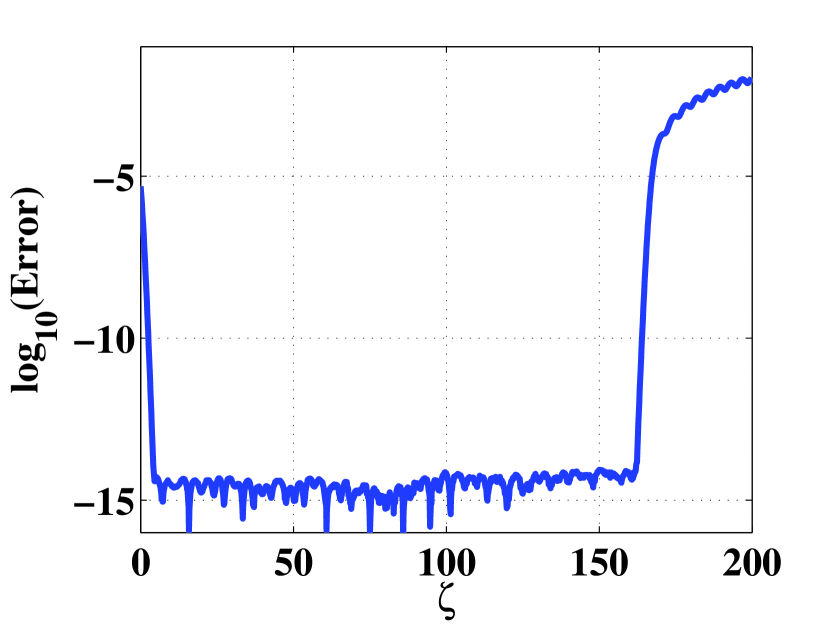

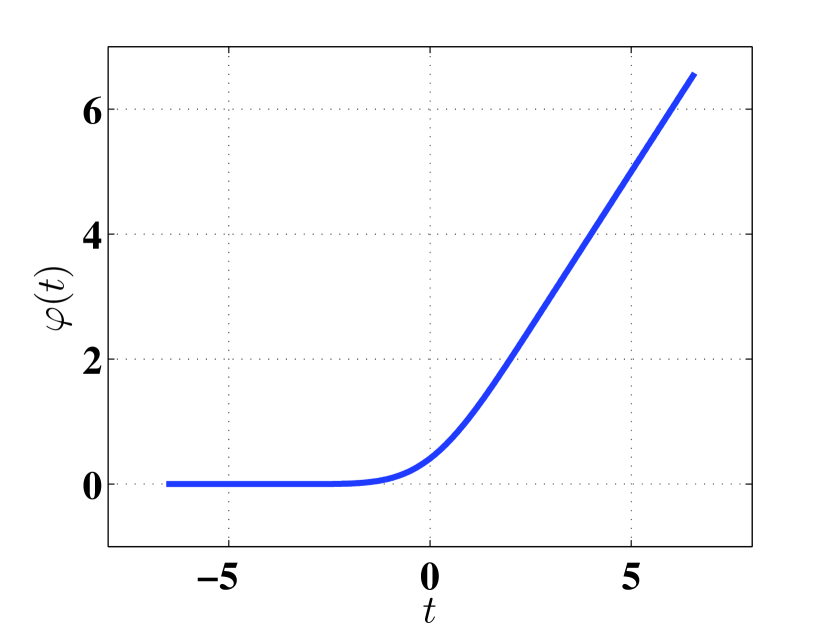

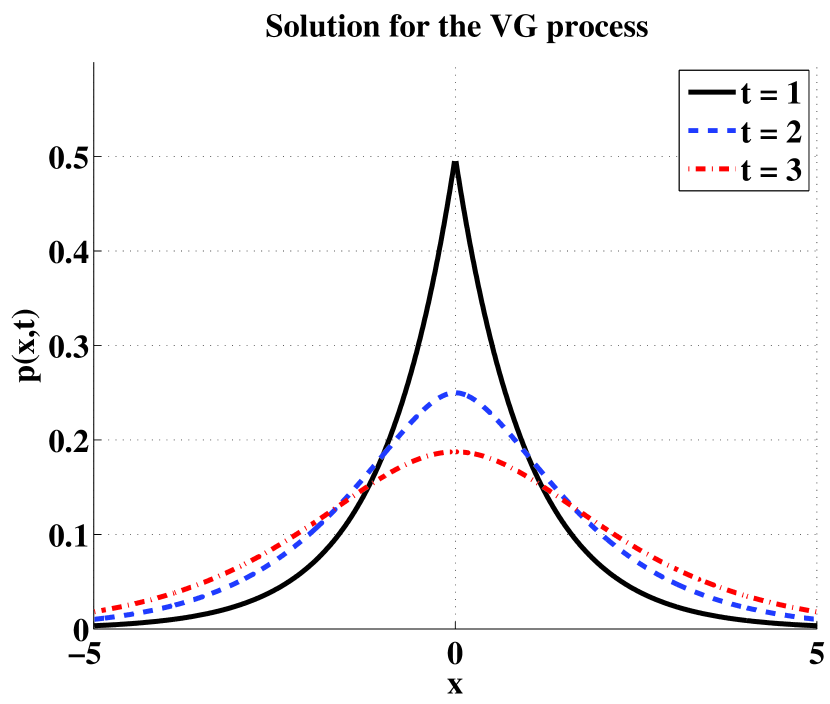

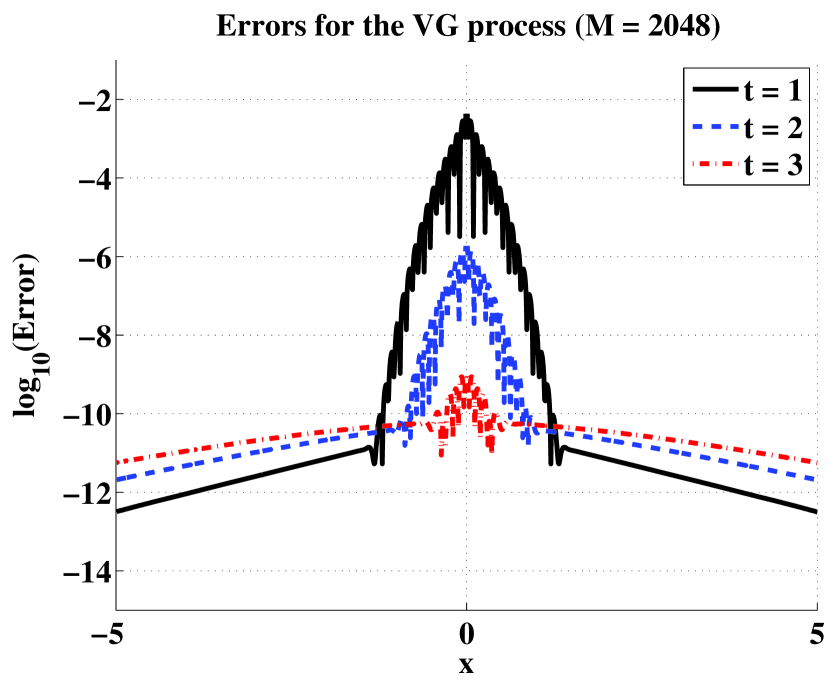

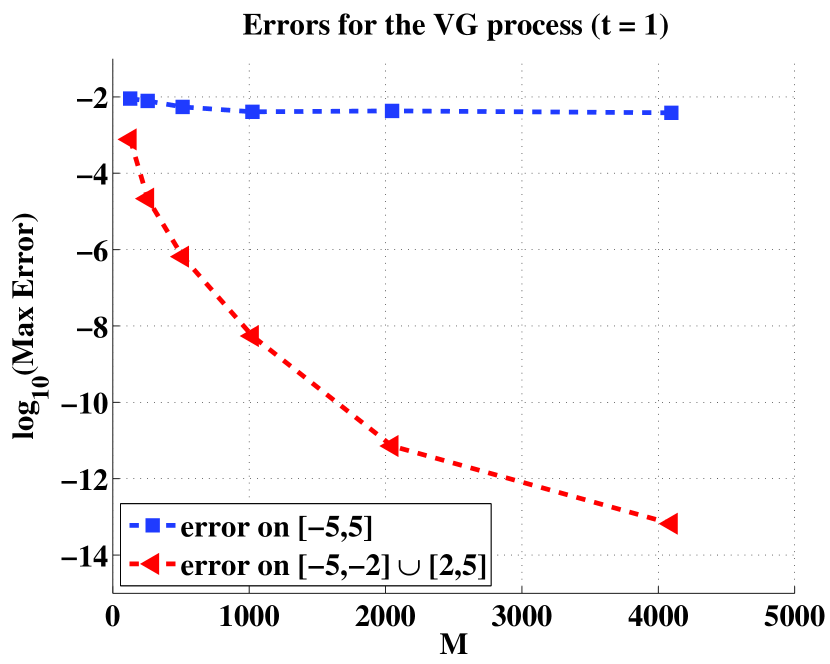

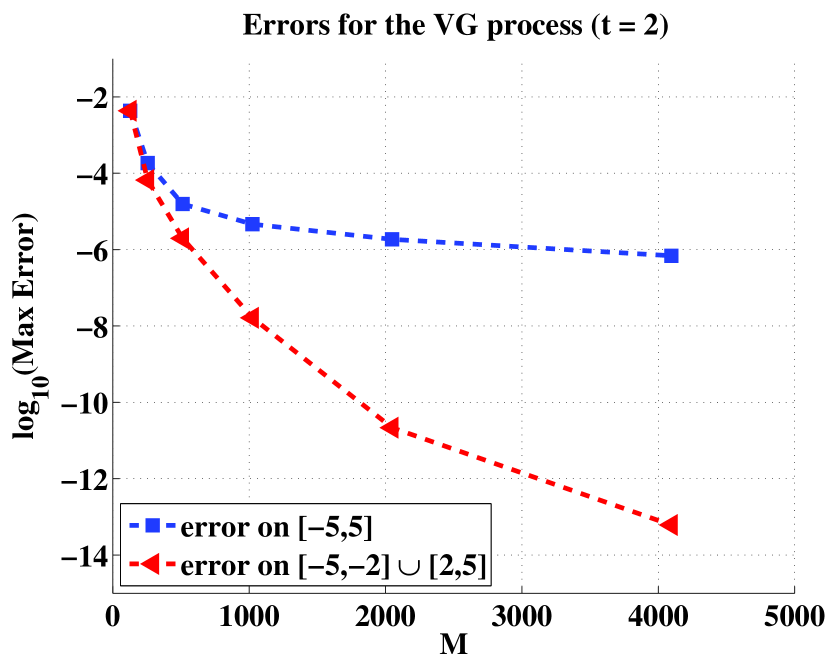

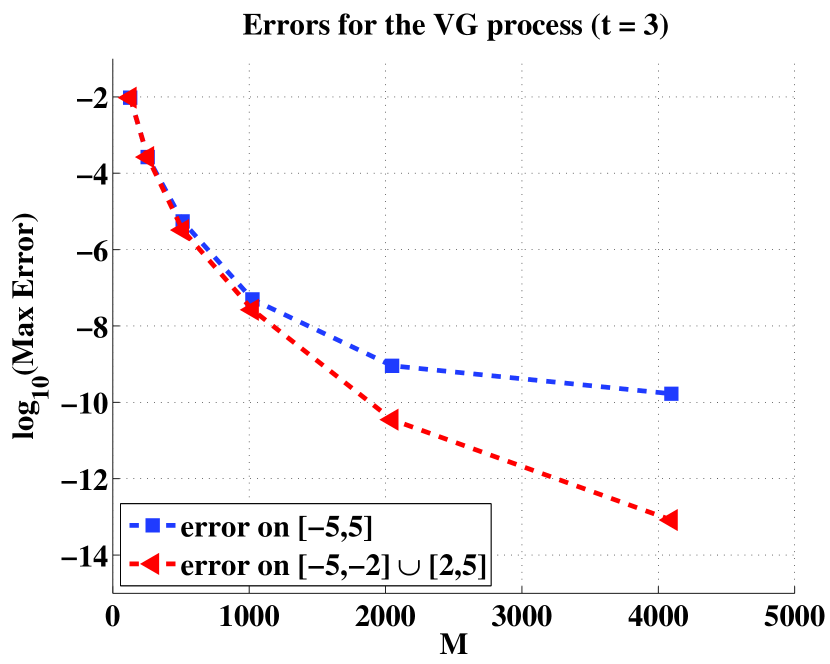

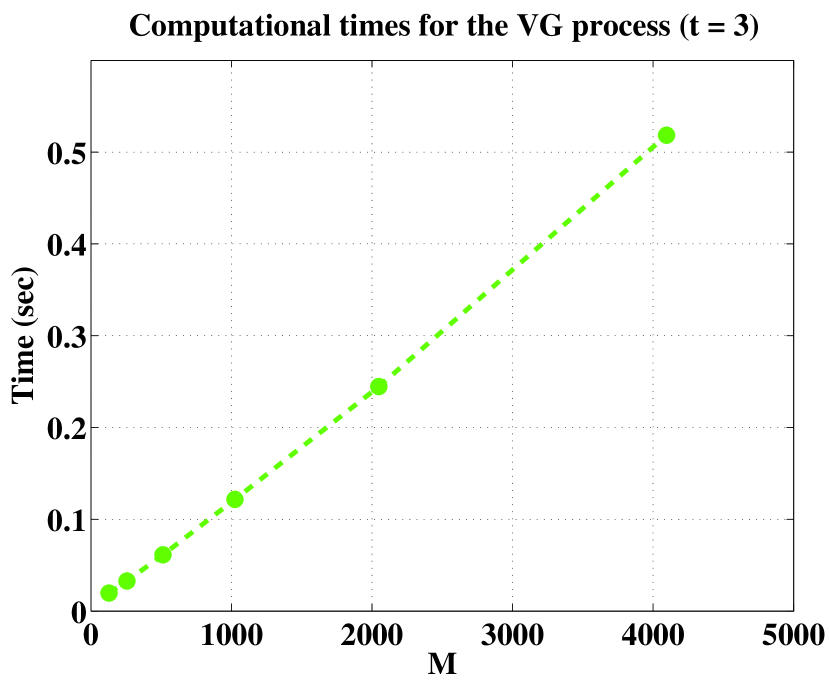

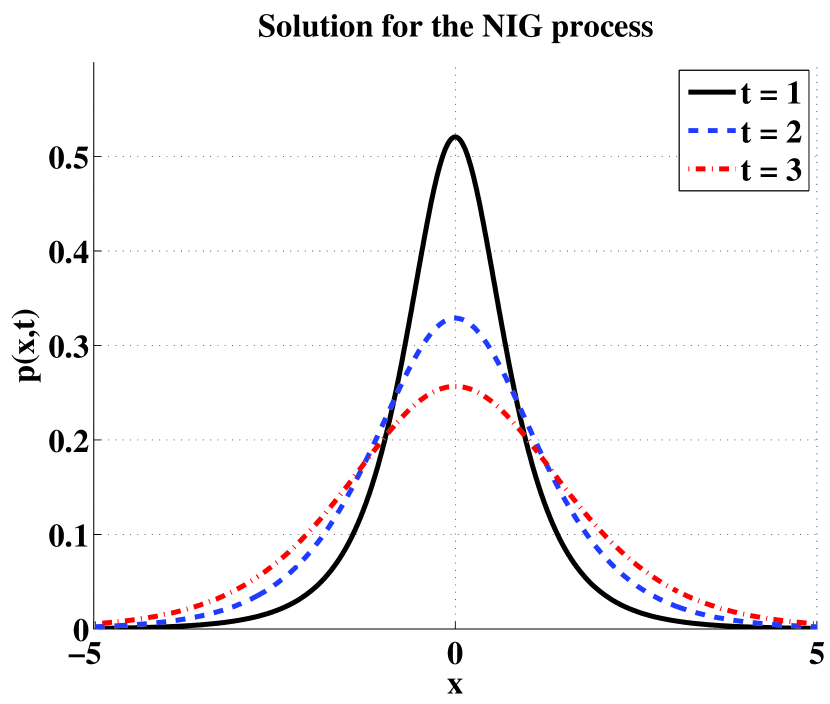

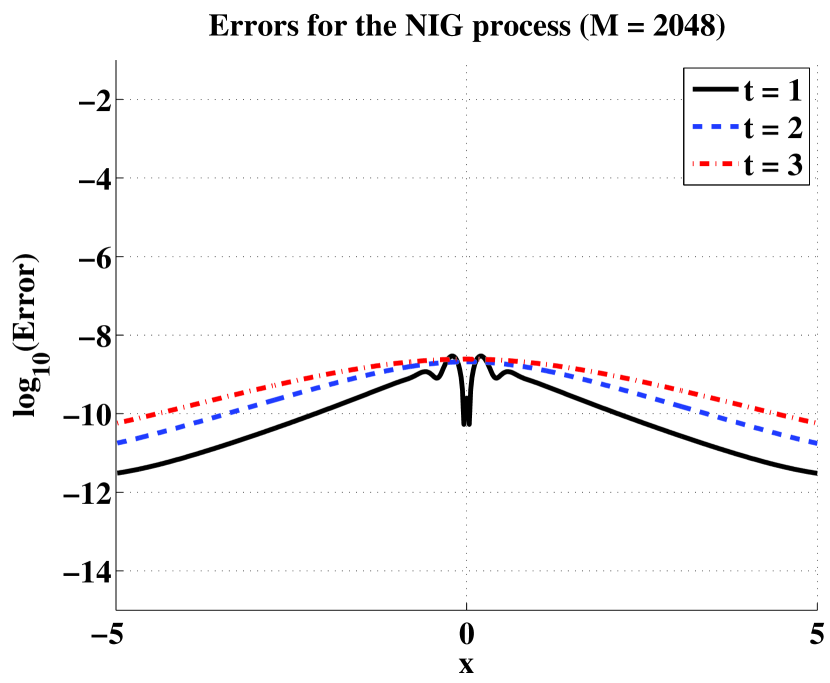

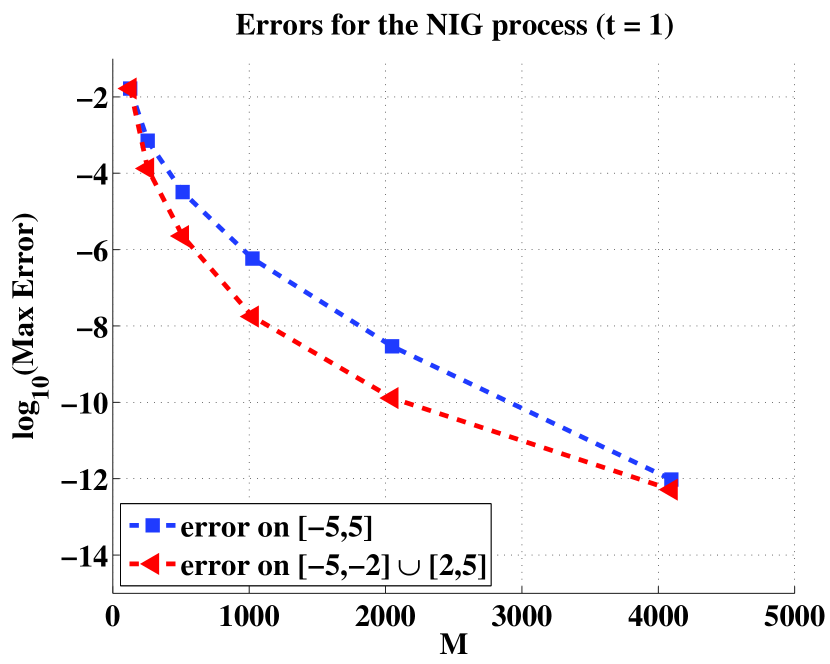

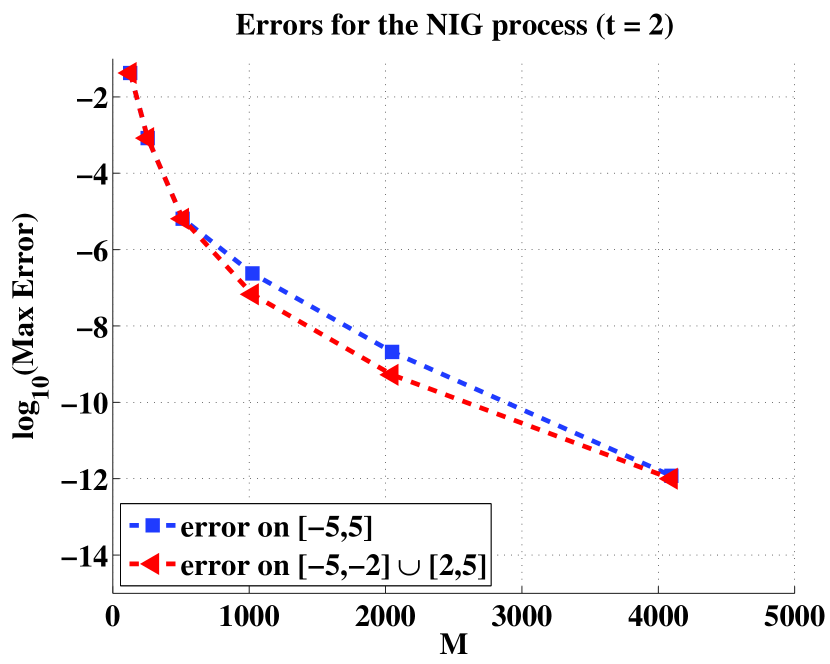

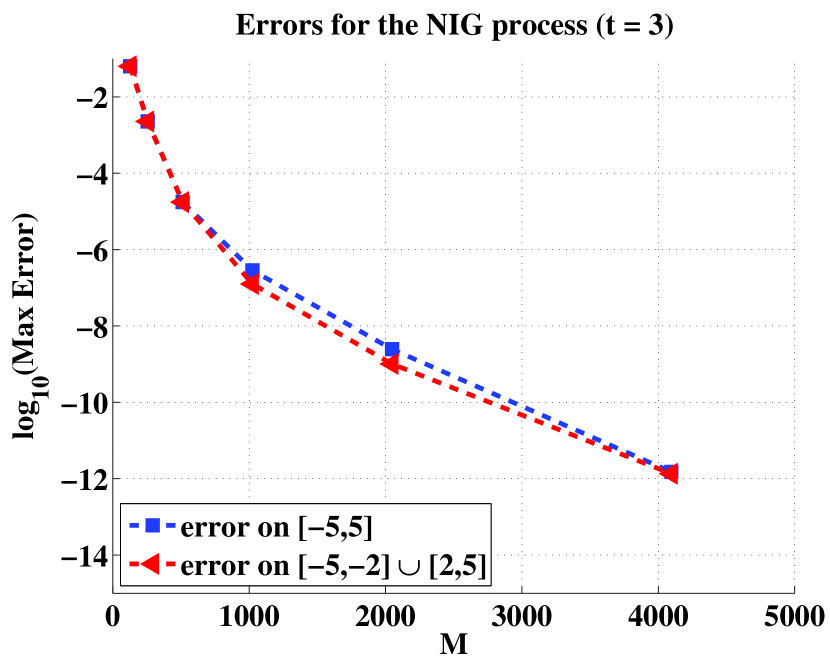

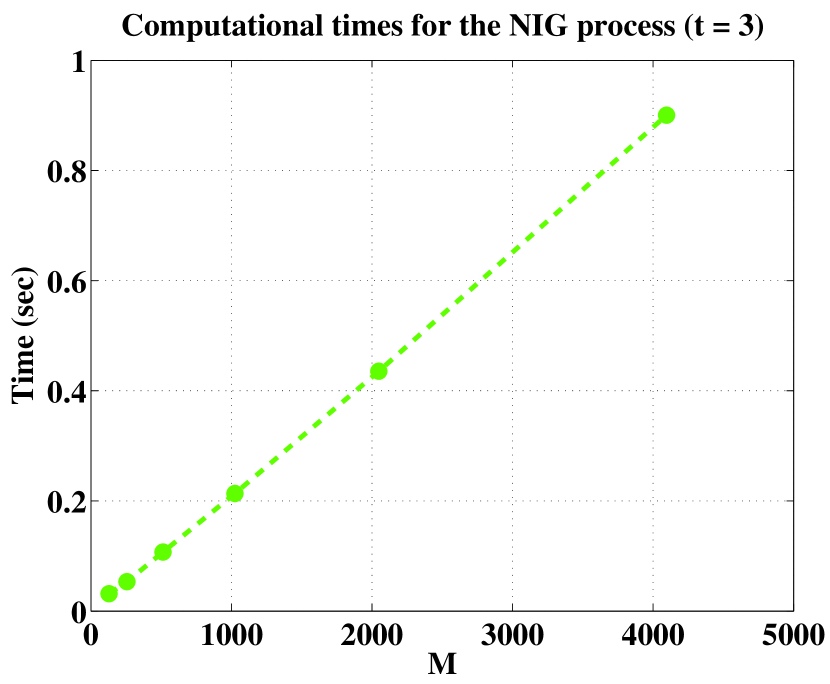

Results of these numerical experiments are shown below. First, for reference, the exact solutions of (4.2) of Example 1 for are displayed in Figure 5. The errors of Example 1 for and are plotted in Figure 5. The maximums of the errors of Example 1 on the intervals and for every ’s are plotted for , and in Figures 7, 7, and 9, respectively. The errors on are computed to observe the errors which are not estimated by Theorem 2. The computational times of Example 1 for only are shown by Figure 9 because ones for are considerably similar. Next, the exact solutions of (4.4) of Example 2 for are displayed in Figure 11. The errors of Example 2 for and are plotted in Figure 11. The maximums of the errors of Example 2 on the intervals and for every ’s are plotted for , and in Figures 13, 13, and 15, respectively. The computational times of Example 2 for only are shown by Figure 15 because ones for are considerably similar.

The errors of Example 1 on the interval seems to have order for some according to Figures 7–9. This observation, Theorems 1 and 2, and Remark 3 imply that the leading error occurs in Step 2 or 3 of the proposed method. On the other hand, in particular for , the errors of Example 1 on the interval are worse than ones on . We can guess that this phenomenon is due to the cusp of the solution (4.2) at the origin shown by Figure 5. In fact, as time increases, the peakedness of the solution becomes gentler and the errors around the origin improve. In addition, the computational times shown by Figure 15 are approximately consistent with the theoretical estimate . As for the results of Example 2, we can obtain similar observations for the errors on the interval and the computational times. However, the errors of Example 2 on the interval are as good as the ones on , which may be because solution (4.4) does not have sharp cusp for .

5 Concluding remarks

In this paper, we proposed a fast and accurate numerical method to solve the Kolmogorov forward equations (1.9) of the scalar Lévy processes with symmetric measures (1.8). The method consists of the three steps presented in Sections 2 and 3. Step 1 and 3 are respectively based on accurate numerical formulas (3.3) and (3.56) for the Fourier transform proposed by Ooura (2001, 2005), which are respectively combined with the nonuniform FFT and the fractional FFT to speed up the computations. Step 2 requires numerical indefinite integration on the equispaced grids. This computation is performed using formula (3.45) obtained by integrating the sinc-Gauss sampling formula (3.25) and combining the resultant convolution in (3.45) with the FFT. The numerical solutions by the proposed method seemed to be exponentially convergent on the interval without sharp cusps of the corresponding exact solutions. Furthermore, the real computational times were approximately consistent with the theoretical estimate , where is the half of the number of the points on which the approximations of the solutions were computed for a fixed . As subjects of future works, we can consider the followings: the rigorous theoretical estimate of the errors of the proposed method, the optimal determination of the parameters based on the estimate, the comparison of the proposed method with other similar methods, and the extension of the method to broader class of Lévy processes.

Acknowledgments

The author would like to thank Prof. L. N. Trefethen for his valuable comments regarding the sinc-Gauss indefinite integration formula in Step 2 of the proposed method in a private seminar at the University of Tokyo in March 2014. He also informed the author about reference Hale & Townsend (2014). This work is supported by JSPS KAKENHI Grant Number 24760064.

References

- Applebaum (2009) Applebaum, D. (2009) Lévy Processes and Stochastic Calculus, 2nd edn. Cambridge: Cambridge University Press.

- Bailey & Swarztrauber (1991) Bailey, D. H. & Swarztrauber, P. N. (1991) The fractional Fourier transform and applications. SIAM Rev., 33, 389–404.

- Bueno-Orovio et al. (2014) Bueno-Orovio, A., Kay, D. & Burrage, K. (2014) Fourier spectral methods for fractional-in-space reaction-diffusion equations. BIT Numer. Math., DOI 10.1007/s10543-014-0484-2.

- Carr & Madan (1999) Carr, P. & Madan, D. B. (1999) Option valuation using the fast Fourier transform. J. Comput. Finance, 2, 61–73.

- Chourdakis (2005) Chourdakis, K. (2005) Option pricing using the fractional FFT. J. Comput. Finance, 8, 1–18.

- Cont & Voltchkova (2005) Cont, R. & Voltchkova, E. (2005) Integro-differential equations for option prices in exponential Levy models. Finance Stochast., 9, 299–325.

- Duquesne et al. (2010) Duquesne, T., Reichmann, O., Sato, K. & Schwab, C. (2010) Lévy Matters I: Recent Progress in Theory and Applications: Foundations, Trees and Numerical Issues in Finance. Lecture Notes in Mathematics, vol. 2001. Heidelberg: Springer.

- Dutt & Rokhlin (1993) Dutt, A. & Rokhlin, V. (1993) Fast Fourier transforms for nonequispaced data. SIAM J. Sci. Comput., 14, 1368–1393.

- Dutt & Rokhlin (1995) Dutt, A. & Rokhlin, V. (1995) Fast Fourier transforms for nonequispaced data II. Appl. Comput. Harmon. Anal., 2, 85–100.

- Fang & Oosterlee (2008) Fang, F & Oosterlee, C. W. (2008) A novel pricing method for European options based on Fourier-cosine series expansions. SIAM J. Sci. Comput., 31, 826–848.

- Gao et al. (2013) Gao, T., Duan, J. & Li, X. (2013) Fokker-Planck equations for stochastic dynamical systems with symmetric Lévy motions. arXiv:1310.7677.

- Gardiner (2009) Gardiner, C. (2009) Stochastic Methods: A Handbook for the Natural and Social Sciences, 4th edn. Heidelberg: Springer.

- Garreau & Kopriva (2013) Garreau, P. & Kopriva, D. (2013) A spectral element framework for option pricing under general exponential Lévy processes. J. Sci. Comput., 57, 390–413.

- Greengard & Lee (2004) Greengard, L. & Lee, J. Y. (2004) Accelerating the nonuniform fast Fourier transform. SIAM Rev., 46, 443–454.

- Hale & Townsend (2014) Hale, N. & Townsend, A. (2014) An algorithm for the convolution of Legendre series. SIAM J. Sci. Comput., 36, A1207–A1220.

- Huang et al. (2014) Huang, J., Nie, N. & Tang, Y. (2014) A second order finite difference-spectral method for space fractional diffusion equations. Sci. China Math., 57, 1303–1317.

- Huang & Oberman (2013) Huang, Y. & Oberman, A. (2013) Numerical methods for the fractional Laplacian Part I: a finite difference-quadrature approach. arXiv:1311.7691.

- Kozubowski et al. (2006) Kozubowski, T. J., Meerschaert, M. M. & Podgórski, K. (2006) Fractional Laplace motion, Adv. Appl. Prob., 38, 451–464.

- Kwok et al. (2012) Kwok, Y. K., Leung, K. S. & Wong, H. Y. (2012) Efficient options pricing using the fast Fourier transform. Handbook of Computational Finance (J.-C. Duan et al. eds). Berlin: Springer, pp. 579–604.

- Lee et al. (2012) Lee, S. T., Liu, X. & Sun, H.-W. (2012) Fast exponential time integration scheme for option pricing with jumps. Numer. Linear Algebra Appl., 19, 87–101.

- Li et al. (2012) Li, C., Deng, W. & Wu, Y. (2012) Finite difference approximations and dynamics simulations for the Levy fractional Klein-Kramers equation. Numer. Methods Partial Differential Equations, 28, 1944–1965.

- Lenzi et al. (2003) Lenzi, E. K., Mendes, R. S., Kwok, S. F. & Malacarne, L. C. (2003) Anomalous diffusion: fractional Fokker-Planck equation and its solutions. J. Math. Phys., 44, 2179–2185.

- Meerschaert (2004) Meerschaert. M. M. & Tadjeran, C. (2004) Finite difference approximations for fractional advection-dispersion flow equations. J. Comput. Appl. Math., 172, 65–77.

- Ooura (2001) Ooura, T. (2001) A continuous Euler transformation and its application to Fourier transform of a slowly decaying function. J. Compt. Appl. Math., 130, 259–270.

- Ooura (2005) Ooura, T. (2005) A double exponential formula for the Fourier transforms. Publ. RIMS Kyoto Univ., 41, 971–977.

- Potts et al. (2001) Potts, D., Steidl, G. & Tasche, M. (2001) Fast Fourier transforms for nonequispaced data: A tutorial. Modern Sampling Theory: Mathematics and Applications. (J. J. Benedetto & P. Ferreira, eds). Boston: Birkhäuser, pp. 249–274.

- Sabatier et al. (2007) Sabatier, J., Agrawal, O. P. & Tenreiro Machado, J. A. (2007) Advances in Fractional Calculus: Theoretical Developments and Applications in Physics and Engineering. Springer.

- Steidl (1998) Steidl, G. (1998) A note on fast Fourier transforms for nonequispaced grids. Adv. Comput. Math., 9, 337–352.

- Tanaka (2014a) Tanaka, K. (2014a) Error control of a numerical formula for the Fourier transform by Ooura’s continuous Euler transform and fractional FFT. J. Comput. Appl. Math., 266, 73–86.

-

Tanaka (2014b)

Tanaka, K. (2014b)

Matlab codes for the symmetric Levy processes.

https://github.com/KeTanakaN/mat_symLevy_FT_codes (accessed 1 August 2014). - Tanaka et al. (2008) Tanaka, K., Sugihara, M. & Murota, K. (2008) Complex-analytic approach to the sinc-Gauss sampling formula. Japan J. Indust. Appl. Math., 25, 209–231.

- Tanaka et al. (2009) Tanaka, K., Sugihara, M., Murota, K. & Mori, M. (2009) Function classes for double exponential integration formulas. Numer. Math., 111, 631–655.

- Yan (2013) Yan, L. (2013) Numerical solutions of fractional Fokker-Planck equations using iterative Laplace transform method. Abstr. Appl. Anal., 2013, Art. ID 465160.

- Zhao & Lib (2012) Zhao, Z. & Lib, C. (2012) A numerical approach to the generalized nonlinear fractional Fokker-Planck equation. Comput. Math. Appl., 64, 3075–3089.

Appendix A. Computation of the integrals of the sinc-Gauss kernel

In this section, we propose an efficient method to compute the values of in (3.30), the integrals of the sinc-Gauss kernel. Let be the Fourier transform of the sinc-Gauss kernel

| (.1) |

Then, the function is written in the form

| (.2) |

where is the error function defined as

| (.3) |

Using the function in (.2), we have

| (.4) |

which is the inverse Fourier transform of the function . Since the function rapidly decays as on , applying the mid-point rule to integral (.4), we can accurately approximate its values as

| (.5) |

where . This approximation is based on a similar principle as that of formula (3.56). Then, applying the fractional FFT to (.5), we can obtain the approximate values of for in time. Finally, adding them sequentially from to , we can compute the approximations of for in time.