On triple intersections of three families of unit circles††thanks: Work on this paper by Orit E. Raz and Micha Sharir was supported by Grant 892/13 from the Israel Science Foundation. Work by Micha Sharir was also supported by Grant 2012/229 from the U.S.–Israel Binational Science Foundation, by the Israeli Centers of Research Excellence (I-CORE) program (Center No. 4/11), and by the Hermann Minkowski-MINERVA Center for Geometry at Tel Aviv University. Work by József Solymosi was supported by NSERC, ERC-AdG 321104, and OTKA NK 104183 grants. ††thanks: A preliminary version of this paper appeared in Proc. 30th Annu. ACM Sympos. Comput. Geom., 2014, pp. 198–205.

Abstract

Let be three distinct points in the plane, and, for , let be a family of unit circles that pass through . We address a conjecture made by Székely, and show that the number of points incident to a circle of each family is , improving an earlier bound for this problem due to Elekes, Simonovits, and Szabó [4]. The problem is a special instance of a more general problem studied by Elekes and Szabó [5] (and by Elekes and Rónyai [3]).

Keywords. Combinatorial geometry, incidences, unit circles.

1 Introduction

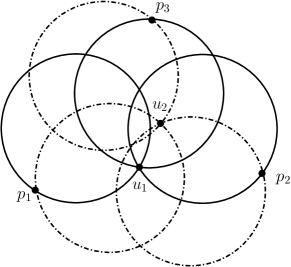

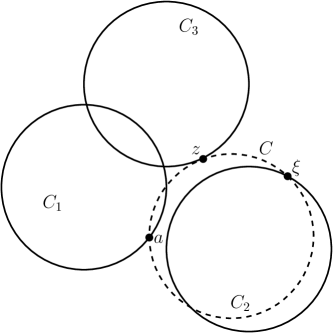

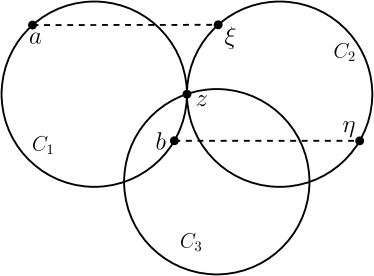

In this paper we re-examine the following problem. Let be three distinct points in the plane, and, for , let be a family of unit circles that pass through . The goal is to obtain an upper bound on the number of triple points, which are points that are incident to a circle of each family. See Figures 1 and 2(a) for an illustration. Recently, Elekes et al. [4] have shown that the number of such points is , for some constant parameter (that they did not make concrete); by this they settled a conjecture of Székely (see [2, Conjecture 3.41]), stipulating that this number should be . The problem is well motivated in [4], because it yields a combinatorial distinction between unit circles and lines. That is, there exist three families of lines passing through three respective points, which determine triple points, in contrast with the smaller bound of for unit circles.

Using a different technique, which appears to be simpler than the one in [4], we establish the following improved bound.

Theorem 1.

Let be three distinct points in the plane, and, for , let be a family of unit circles that pass through . Then the number of points incident to a circle of each family is .

The specific problem studied in this paper can be viewed as a special instance of a more general setup, which has been studied by Elekes and Rónyai [3] and by Elekes and Szabó [5] (see also [2, 4]). From a high-level point of view the setup is as follows. We have three sets , , , each of real numbers, and we have a trivariate real polynomial of some constant degree . Let denote the subset of where vanishes. The claim is that, unless and , , have some very special structure, is subquadratic. (For a simple example where is quadratic in , consider the case where , and where .)

Positive and significant results for this general problem have been obtained by Elekes and Rónyai [3] and by Elekes and Szabó [5], who showed that, unless has a very restricted form, is indeed subquadratic in . For example, in the case where is of the form , for some bivariate polynomial , if is quadratic in , then must be of one of the forms or , for suitable univariate polynomials , , (see [3] and [2]). Related representations, somewhat more complicated to state, for a polynomial with , have also been obtained for the general case (see [5] and [2]). We have recently studied in [10, 11] this specific problem and obtained improved bounds for , when does not have these special forms; see below.111The study in [11] has been conducted after the original preparation of this paper; see a discussion comparing these works in a concluding section.

The high-level approach used in this paper is similar to those used in several recent works that study problems in combinatorial geometry that are special instances of this general framework (see Sharir, Sheffer, and Solymosi [14] and Sharir and Solymosi [13]). However, the actual implementations of this approach in our paper, as well as in the other works just mentioned, are very problem-specific and exploit the special geometric structure of the relevant problem.

We will later detail the connection of our problem to the setup in [3, 5]. Roughly speaking, for each , its circles have one degree of freedom, and we parameterize them by a suitable single real parameter. Then, with a proper choice of these parameters, the condition that three circles, one from each family, have a common point can be expressed by an equation of the form , where is a real trivariate polynomial, and are the parameters representing the three relevant circles.

In both cases, the specific problem studied in this paper (and the specific problems studied in [13, 14]), and the general one in [3, 5], the approach is to double count the number of quadruples , such that, in our specific context, represent two circles in , represent two circles in , and there exists , representing a circle through , such that and . (In the general case too, the quadruples to be considered are such that , , and there exists such that .) A lower bound for , in terms of , is easy to obtain via the Cauchy-Schwarz inequality (see below for details), and an upper bound is obtained by regarding each such quadruple as an incidence between the point , in a suitable parametric plane, and a curve which is the locus of all points that satisfy with the above conditions. The comparison between the lower and upper bounds yields the asserted upper bound on .

The main issue that arises in bounding the number of incidences is the possibility that many curves overlap each other, in which case the standard techniques for analyzing point-curve incidences fail. A major part of the analysis in this paper is to show that the amount of overlap in our specific problem is bounded. In this case the standard incidence techniques do apply, and yield a sharp upper bound that leads to the aforementioned bound on ; see below for details.

In the general problem, the goal is to show that when there is a larger amount of overlap between the curves, the polynomial must have a special form, as the ones mentioned above and established in [3], and to establish a subquadratic upper bound on when this is not the case. As mentioned, this indeed has recently been shown in two companion papers, first in [10] for the special case where , for any constant-degree bivariate polynomial , and later in [11], for the general trivariate case, with the same subquadratic bound , in both cases, as the one established in this paper. In our problem, though, this part is not needed, and the argument that the overlap is bounded is an ad-hoc argument that exploits the geometric and algebraic structure of the problem.

2 Unit circles spanned by points on three unit circles

We begin by observing the following equivalent and, in our opinion, more convenient formulation of Theorem 1.

Theorem 2.

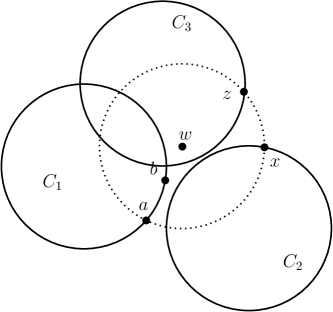

Let be three unit circles in , and, for each , let be a set of points lying on . Then the number of unit circles, spanned by triples of points in , is .

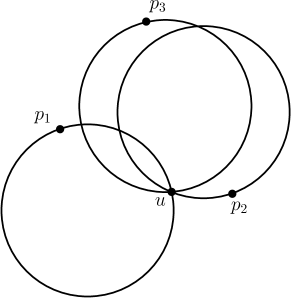

The equivalence between this formulation and the one in Theorem 1 is indeed trivial: For each , is the set of centers of the circles of , and the centers of the resulting “trichromatic” unit circles in the new formulation are the triple points in the previous one. See Figures 2(a) and 2(b) for an illustration of this connection between the two setups. In what follows we prove Theorem 2, and stick to the new equivalence formulation.

We note that the condition that three points span a unit circle can be expressed as a polynomial equation in their coordinates. That is, there exists a 6-variate real polynomial of degree 6, such that when , , span a unit circle. Indeed, put

Let denote the area of the triangle . Then the circumradius of this triangle is given by the formula

The area can be expressed by Heron’s formula, written as

That is, we have . With some algebraic manipulations, this can be expressed in terms of the squared distances , , , as

| (1) |

The left side of (1) is the desired polynomial in the coordinates of . It is of degree in these six variables.

For each , each point can be parameterized by (an appropriate algebraic representation of) the orientation of with respect to the center of (note that the centers are the points in the original formulation); denote the set of these orientations as . In what follows we will interchangeably use both notations, referring to a point , for , either by its corresponding parameter , when we want to stress the algebraic nature of the problem, or as itself, when geometry is concerned.

We call a triple , with , , a unit triple if the three corresponding points span a unit circle. We use the standard algebraic representation of the ’s, where we replace by , and the corresponding point on then becomes . With these representations, the property of being a unit triple can be expressed by a polynomial equation , obtained by the appropriate substitutions into the equation (1) of . In what follows we will refer to the ’s as orientations, also when substituting them in (the actual substitution should be of the corresponding parameters ). This slightly incorrect treatment is made to simplify the presentation, and has no real consequences in the analysis.

Clearly, has constant (and small) degree (which is at most , as is easily checked). This illustrates how our problem is indeed a special instance of the general problem mentioned in the introduction.

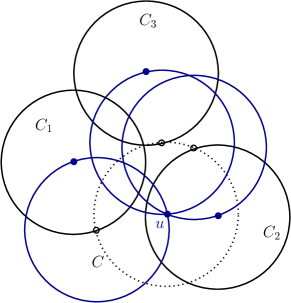

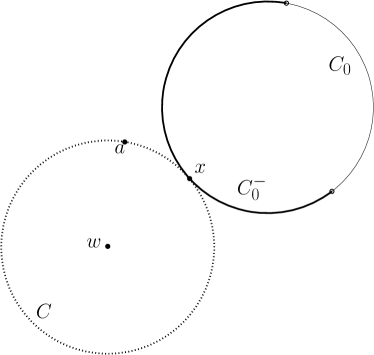

We next argue that, without loss of generality (with a possible re-indexing of the input circles and points), we may assume that the points of all lie in the portion of that lies outside the closed disk circumscribed by (this property will become handy for the forthcoming analysis). To see this, let denote the three (closed) unit disks circumscribed by , respectively, and consider the intersection region . Assume first that has a nonempty interior. As is well known, the boundary of is of the form , where is a single (possibly empty) connected arc of , for . More generally, in the intersection of any finite number of unit disks, each disk contributes at most one connected arc to . Let be a unit circle in the plane, which is not one of , and let denote the disk bounded by . Then, as just mentioned, contributes a single connected arc to . It follows that avoids the relative interior of at least one of the arcs , namely the arc not containing any endpoint of . (If one of those arcs is empty, trivially misses that arc.)

It follows that, for every triple spanning a unit circle , at least one of the points avoids , because neither of these points can lie in the interior of , and they lie on , which meets in at most two points. So, for one of the indices , and for at least a third of these triples , the point avoids ; without loss of generality assume . By discarding the other points of , we obtain a reduced configuration in which the points of lie outside and the number of unit triples is at least one third of its original value. That is, each point in (the reduced) lies either outside or outside . One of these subsets of participates in at least half the (remaining) unit triples. To recap, by removing the points of the other subset, and by re-indexing if needed, we may assume that all the points of lie outside the disk , and that the number of unit triples is at least one sixth of the original number. This reasoning also applies when is empty or is a singleton (with an empty interior), and in fact becomes much simpler in these cases.

We therefore continue the analysis under the assumption that the points of all lie outside .

Let denote the number of unit circles spanned by . Our strategy is to double count the quantity (mentioned in the introduction) that we are now going to define. For each , let denote the set of pairs such that is a unit triple, so . Note that we have . Indeed, there are at most eight triples in that span the same unit circle ( intersects each of in at most two points, and each triple of points, one from each pair, spans ), and clearly, by definition, at least one of these triples is counted in .

We now define

The quantity may be interpreted as the number of ordered pairs of unit triples of the form , with a common third component . Using the Cauchy-Schwarz inequality, we have

| (2) |

The curves .

To obtain an upper bound for , we use the following approach. Fix two points , with orientations , respectively, and define to be the algebraic curve given by the polynomial equation

where is the resultant of the two polynomials , with respect to (which is thus a real bivariate polynomial in , independent of ). By the properties of the resultant, the curve contains all points , with corresponding points , for which there exists (not necessarily in ) such that

| (3) | ||||

for more details see, e.g., Cox et al. [1]. However, might contain points where there is no real point that spans unit circles with both pairs , . In general, the curve is partitioned into a constant number of connected arcs of two kinds: real arcs, over which (3) has a real solution , and non-real arcs, over which there are no such real solutions. We refer to the endpoints of these arcs as transition points. We will analyze and handle these points later on.222In both real and non-real arcs, we only consider real values for . Only can assume non-real values for points on non-real arcs. In other words, ignoring its geometric interpretation, is a real curve.

Let denote the set , represented as a set of points in the above parametric plane, let denote the (multi-)set of the curves , and let denote the number of incidences between the curves of and the points of .

Note that, for any fixed and for any ordered pair of pairs , in , we have and . It follows that the number of point-curve incidences is at least . Indeed, there can be at most four values of that give rise to the same incidence (any of the pairs , say , defines at most two unit circles that pass through the two corresponding points, and each of these circles can intersect in at most two points), and only those values among them that belong to are reflected in the above sum; also, the fact that each pair of pairs in generate two incidences is “neutralized” by the fact that the same two incidences are generated for each of the two orderings of the pairs. That is, we have , so it suffices to obtain an upper bound for .

The number of incidences between curves of that are of the form , with , and the points of , is . Indeed, let and consider the curve . For , there exist at most two unit circles that pass through and , and these circles form at most four intersection points with . Then for each such intersection point , there exist at most two unit circles that pass through and , which form at most four intersection points with . Thus there are at most 16 values for which . It follows that, for each , the curve is incident to points of , and hence the total number of incidences that curves of this form contribute is .

Therefore, letting be the (multi-)set of the curves , with , and letting denote the number of incidences between the curves of and the points of , we get , and thus .

We reiterate that (and ) might include many irrelevant incidences, first, because the corresponding parameter does not belong to , and second, because is not real (the incidence occurs on a non-real arc of the relevant curve ). Still, an upper bound on the (overestimate) suffices for our purpose.

Hence the problem is reduced to obtaining an upper bound on . This is an instance of a fairly standard point-curve incidence problem, which can be tackled using the well established machinery, such as the incidence bound of Pach and Sharir [8], or, more fundamentally, the crossing-lemma technique of Székely [15] (on which the analysis in [8] is based). However, to apply this machinery, it is essential that the curves of have a constant bound on their multiplicity. More precisely, we need to know that no more than curves of can share a common irreducible component. In more detail, while the points of are clearly distinct, there might be potentially many pairs of curves of that coincide or overlap in a common irreducible component, in which case the aforementioned incidence-bounding techniques break down. Fortunately, this can be controlled through the following key proposition. (Recall that this arises as a key issue when applying this approach to the general setup of Elekes and Rónyai [3], as manifested in the companion paper [10], and the more general setup of Elekes and Szabó [5], as in the more recent study [11].)

Proposition 3.

There exists a subset of size at most such that the following holds. For any irreducible component , there are at most pairs such that contains a portion of a real arc of .

The proof of the proposition is given in Section 2.2. This allows us to derive an upper bound on the number of incidences, given in the following proposition.

Proposition 4.

Let and be as above. Then the number of incidences between and is .

2.1 Properties of the curves

In this section we provide a detailed analysis of the structure and properties of the curves , from both algebraic and geometric perspectives.

Explicit construction of the third point of a unit triple.

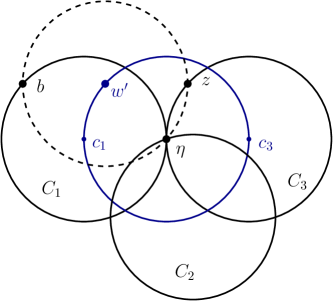

We slightly change the notation temporarily, and let be a point on , and be a point on . We derive below an explicit expression for a point on such that span a unit circle. This procedure will be used repeatedly in the forthcoming analysis. We note that the procedure consists of two similar substeps. Later on, we will formally break it into these substeps, and use them as the primitive building blocks for the analysis.

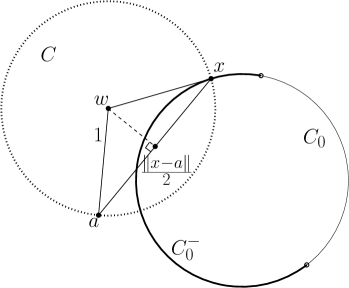

In full generality, let and be any pair of points in the plane, where we think of as fixed and of as a variable. Let be a unit circle that passes through and . The center of is the point

| (4) |

where ; see Figure 3(a). There can be zero, one, or two real solutions for . Denote this doubly-valued function as . In this notation, both and have two degrees of freedom. However, in our application will be assumed to lie on some unit circle, so it will have only one degree of freedom, and then also has one degree of freedom. We capture this extra constraint by using the modified notation , where now is constrained to lie on .

Let be the center of . Then, similar to (4), the point is given by . That is,

| (5) |

where ; again, for a given , there can be zero, one, or two real solutions for . Thus, the number of real values of the combined expression for , obtained by substituting (4) into (5), is between and .

Symmetric constructions give explicit expressions for the first or second point of a unit triple in terms of the two other points.

The primitive steps of the procedure.

A couple of additional remarks are in order. First, similar to what has just been remarked, the roles of and in defining are essentially identical. The above notation is supposed to signify that is considered as a fixed parameter and as a variable (along its circle ). Second, is in general 2-valued, unless (it has complex values when ). In what follows, we will always trace a single (real) branch of such a (over which ), but stop when becomes .

Explicit construction of points on a curve .

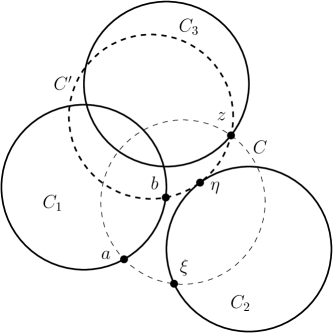

Let be one of our curves. The preceding construction immediately leads to the following 4-step procedure for constructing points on . Specifically, given and a point , we compute point(s) such that , as follows.

-

(i) We start with and , and construct the point(s) , each of which is the center of a unit circle passing through and . See Figure 4(a). We fix one of these points . (We terminate the procedure, with failure, when there are no real solutions; this also applies to each of the following steps.)

-

(ii) We then construct the point(s) , where is the unit circle centered at . By construction, we have ; again, there are (at most) two choices for and we fix one of them. See Figure 4(a).

-

(iii) We now construct the center(s) of the unit circle(s) passing through and . See Figure 4(b). Fix to be one of these centers.

-

(iv) Finally, we obtain the desired point(s) , where is the unit circle centered at . See Figure 4(b).

(Note that the circles appearing in the four applications of the -functions, namely, , , , and , are indeed fixed, regarding and themselves as fixed.)

The following lemma shows that the functions are well-behaved, in the sense made precise below, unless certain degenerate situations arise. In the lemma, the derivative of should have the expected interpretation. Concretely, let (resp., ) denote the orientation of (resp., of ) with respect to the center of (resp., ). Interpret as the corresponding functional relationship between and , which, with a slight abuse of notation, we also write as . Then is simply the corresponding derivative of at the respective orientation .

Lemma 5.

Let be a fixed point, a fixed (unit) circle, and assume . Put . Fix a parameterization of , , for , such that each of the functions is an analytic function on . Then each branch of the function is analytic, and

| (6) |

where , and and denote the unit tangent vectors to at and to at , respectively. In particular, has non-zero derivative, at each point for which the unit circle centered at is not tangent to at .

Proof. See Figure 3(a) for the general layout, and Figure 3(b) for the exceptional situation. First note that our assumption, combined with the explicit expression (3), implies that is analytic on . Fix a point and put . Let and denote the corresponding orientations, let be the point with , for a small increment , and put and . Clearly, since is continuous over , is also small when is small.

Put and (note that these are vector displacements, whereas , are scalars, and we have , ). We have

Let and denote the unit tangent vectors to at and to at , respectively. We then have

We thus have

That is,

The vector cannot be orthogonal to . Indeed, this is possible only when either coincides with , which has been ruled out in the lemma, or when , which is also excluded. Hence the coefficient of is nonzero, so we have

so in the limit we get

which is well defined and nonzero unless is orthogonal to (that is, the unit circle centered at is tangent to ), as asserted in the lemma.

Note that each of the numerator and the denominator of (6) can become as varies along : The numerator becomes when is at distance from the center of (the exceptional case depicted in Figure 3(b)), and the denominator becomes when is at distance from (the endpoints of , if they exist). Note that both situations are ruled out in the lemma. These kinds of degeneracy will play a central role in what follows.

Let be a pair of points on (outside the disk ), and let be a point on , for a respective pair of points . Consider the 4-step procedure that produces from , as described above, and write the outputs of its steps as , , , and . In each step we pick an appropriate branch of the relevant function, and assume that the degeneracies ruled out in Lemma 5 (and summarized in the preceding paragraph) do not arise (in suitable neighborhoods of the four respective points) in any of these four steps. With these notation, assumptions, and conventions, we obtain the composite function

which is well defined and analytic in a suitable neighborhood of , its graph over is a portion of , and is not a local -extremum or -extremum of that portion. The non-extremality properties are consequences of the chain rule, combined with a four-way application of (6) in the proof of Lemma 5. (See below for a more explicit repetition of this argument.)

2.2 Proof of Proposition 3

Let be an irreducible component of potentially many curves . The strategy is to identify (few) points along , from which we can reconstruct all the values of and in only a constant number of ways.

Fix a generic point on that is non-singular and non-extremal for , and which does not lie on any other irreducible component of any other curve. Let denote the subset of all pairs so that contains , and lies on a real arc of . The preceding discussion implies that, for each such curve , there is a unique way to define the corresponding function in a suitable neighborhood of (which may depend on and ), and the graph of each of these functions near (in the intersection of all these neighborhoods) is itself.

Now trace , along with all these functions, from in, say, increasing -direction, and stop at the first point at which one of the assumptions made in Lemma 5 is violated, for some pair , for one of the corresponding functions , , , or . The definition of the curves , and the property that all the points of lie outside the disk , imply that does indeed contain such a point (because the open disk of radius 2 centered at intersects but does not contain the circle ). As we will shortly argue, there are no transition points of any curve , for , between and , so still belongs to the same real subarcs of all the curves with pairs in (possibly being a transition point of some of these arcs).

Applying explicitly the chain rule, we have, for an arbitrary point on the relatively open portion of between and , with corresponding points ,

where , , and are as defined above. By (6), this is a product of four fractions, and the above assumption about means that the numerator or denominator of at least one of these fractions is zero at , but they all remain nonzero before reaching . Call an ultra-degenerate pair if (at least) one numerator and one denominator of vanish simultaneously at .

We will shortly show that ultra-degenerate pairs are sparse, and handle them all via a global argument that does not depend on . For the time being, we ignore all such pairs. (The exceptional set in the proposition will be the set of these ultra-degenerate pairs.)

In other words, excluding ultra-degenerate pairs, , which is equal to the slope of the tangent at the corresponding point on (assuming that point to be non-singular), becomes zero or tends to at , so has a (one-sided) horizontal or vertical tangent at .

For technical reasons that will become clearer later on, we trace from in both increasing and decreasing -direction.

It is important to note that the curve does indeed trace between and . Indeed, let be the (irreducible) polynomial equation defining . Let be such that the graph of , restricted to the subinterval , is an arc of , but this does not hold for , for any , arbitrarily close to . We thus have , for every . By Lemma 5, the function is analytic in some sufficiently small neighborhood of inside . Thus, letting , and since is a polynomial, we have that is analytic and , for every . In particular, the derivatives of at , of any order, are all zero (because is identically zero in a one-sided neighborhood of ). Thus, since is analytic, the Taylor series of at is identically zero, which means that is identically zero in some suitable neighborhood of (this time on both sides of ). In other words, the graph of continues to coincide with on the other side of too, contradicting our assumption on .

We note that the preceding argument also holds when the tracing of encounters a singular point of (before reaching ). Even if two branches of meet tangentially at , the graph of remains well defined, and follows a unique branch of , on either side of .

Transition points.

Recall that a point is a transition point of the curve if it connects a real arc and a non-real arc of . We argue that at a transition point we must have one of the degeneracies ruled out in Lemma 5, for one of the four -functions. Specifically, let be a point on which is a transition point along a containing curve . Each of the four functions , , , , whose composition yields , involves a square root (with a fixed sign). As long as none of these roots vanishes, the functions continue to be defined (as real functions) and produce real values, so the two unit circles that are spanned by the corresponding triples , , for a suitable point , are such that is real and the circles are real too, and this continues to hold in a suitable neighborhood of . Since this does not occur at a transition point, one of the square roots has to vanish at , and when this occurs one of the degenerate conditions in the lemma occurs for the corresponding function (where the denominator of one of the fractions in (6) vanishes). This establishes the promised claim.

Recap.

The preceding analysis leads to the following overall treatment of . We partition into maximal connected subarcs, each delimited by points with horizontal or vertical tangency (and does not contain any such point in its relative interior). Since has constant degree, there are only subarcs of this kind. For each of the containing curves , each such subarc is fully contained either in a real arc of or in a non-real arc of , and at least one subarc is contained in a real arc of .

In the next step of the analysis, we show that, for each of the locally extremal points , there are only pairs , for which is a (possibly delimiting) point of a real arc of . Altogether, we conclude that can be an irreducible component of only curves (with the additional requirements that overlaps at least one real arc of and that the pair is not ultra-degenerate).

The possible geometric scenarios near a locally extremal point of .

Let be a locally -extremal point of (locally -extremal points will be handled in a fully symmetric manner; see below), and let be the points in with orientations , respectively. Let be a fixed pair for which at least one of the subarcs of delimited by is a (portion of a) real arc of , and assume that is not an ultra-degenerate pair. Here we do not know and , and our goal is to reconstruct them from . This is done as follows.

We first note that, as argued earlier, the -extremality of means that for every such pair . That is, one of the denominators in the four expressions, as in (6), vanishes. We thus have the following four respective situations.

Case (i) .

In this case we can reconstruct in at most two possible ways, as an intersection point of with the circle of radius 2 centered at ; see Figure 5(a). We can then retrieve the corresponding point in two possible ways, as an intersection point of with the (unique) unit circle that passes through and . Since is also given, we can compute , as one of the intersection points of with one of the at most two unit circles that pass through and . Altogether, there are (at most) two ways to choose , two for , and four for , so in the present case we can reconstruct in at most 16 possible ways.

Case (ii) .

In this case, there is a unit circle that passes through and and is tangent to at ; see Figure 5(b). Hence is a tangency point of with one of the at most two unit circles that are incident to and tangent to . This allows us to reconstruct , as an intersection point of with one of these two unit circles. We then retrieve from and as in the preceding case. Altogether, there are (at most) two ways to choose , two for , and four for , so here too we can reconstruct in at most 16 possible ways.

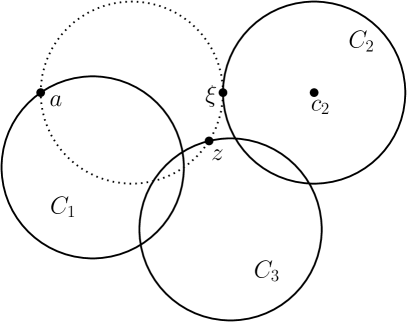

Case (iii) .

This is geometrically more challenging to analyze, because the points , at distance 2 apart, are both unknown. See Figure 6(a). We handle this case by observing that the lengths of the edges of the quadrilateral are fixed—they are 1,2,1 and , respectively, but this does not determine , because it can flex (with one degree of freedom) about its fixed edge . As flexes, the midpoint of traces an algebraic curve of some constant degree . Note that the unit circle that passes through and , has its center (which is the midpoint of ) on . Since the point is known, we can find , by computing the intersection points of with the unit circle centered at , and then retrieve , as the intersection point of with the unit circle centered at . We claim that, in general, there are at most intersection points of with , and hence at most a constant number of ways to reconstruct . Indeed, if this were not the case, then, by Bézout’s theorem (see, e.g., [1]), would have to contain as one of its components. This situation is controlled by the following simple claim.

Claim.

The curve does not contain any unit circle as one of its components, unless and are tangent to each other, in which case does indeed contain the unit circle centered at the point of tangency.

Proof. See Figure 6(a) for the exceptional situation in the claim. Let be a unit circle, centered at a point , such that . By the construction of , every point is the midpoint of a segment whose endpoints lie on and , respectively. This implies, in particular, that is contained in , the convex hull of , and since the three circles are of the same radius, it follows that the center of lies on . Moreover, as is easily checked (cf. Figure 6(a)), in this case must be the midpoint of , and we must have , and then and are tangent to each other at , implying that , , and must indeed be of the exceptional kind stated in the claim.

To complete the analysis, we recall that the only problematic case is when the unit circle centered at is contained in . By the claim, must be the midpoint of , so in particular is not tangent to (or else it would coincide with ). Note that in this special situation, the points of , with the possible exception of , clearly lie outside the disk circumscribed by . We can discard the tangency point of and from , if needed, losing at most unit triples spanned by the original sets . We now restart the whole analysis, switching the roles of and , and are now guaranteed that the exceptional situation described in the above claim does not occur.

We can then retrieve , as an intersection point of with a unit circle that passes through and , and, since is also given, compute , as one of the intersection points of with one of the unit circles that pass through and .

Case (iv) .

In this case, depicted in Figure 6(b), the unit circle that passes through and is tangent to at . Hence is one of the intersection points of and the unique unit circle (externally) tangent to at , and then can be reconstructed from and , as in the previous cases.

Handling -extremal points of .

The cases where is a -extremal point of are handled in a fully symmetric manner, as follows. Let denote the “transpose” of , that is,

Clearly, is an irreducible component of if and only if is an irreducible component of . Moreover, is a locally -extremal point of if and only if is a locally -extremal point of . We can therefore apply the preceding analysis, essentially verbatim, to and the “transposed” containing curves , and conclude that, from each locally -extremal point of , there are only curves such that and lies on a real arc of .

Ultra-degenerate pairs.

Let denote the set of all ultra-degenerate pairs; recall that a pair is said to be ultra-degenerate if there exists a point at which at least one numerator and one denominator of the four fractions that define vanish simultaneously at . The reason for singling out these pairs is that it is not clear what happens to the slope of the tangent to (that is, to ) at this point.

Fortunately, the overall size of , over all possible components , is only . The somewhat tedious case analysis that establishes this claim is given in Appendix A. Since each such curve has only incidences with the points of (an easy property which is a special case of the Schwartz–Zippel Lemma [12, 17]), we get a total of incidences that correspond to such pairs. This is a small bound, subsumed by the overall bound on that we derive.

Combining all the steps of the analysis, and excluding the pairs in , we finally conclude that overlap (a portion of a real arc of) , for at most a constant number of pairs . This completes the proof of Proposition 3.

2.3 Proof of Proposition 4

We apply Székely’s technique [15], which is based on the crossing lemma (see also Pach and Agarwal [7]). As noted, this is also the approach used in [8], but the possible overlap of curves requires some extra (and more explicit) care in the application of the technique. A similar argument is given in the companion paper [10], but we repeat it here to make the paper more self-contained.

Throughout this subsection, we completely ignore curves for which is an ultra-degenerate pair; as argued in Section 2.2, these curves contribute only to the incidence bound.

We begin by constructing a plane embedding of a multigraph , whose vertices are the points of , and each of whose edges connects a pair , of points that lie on the same curve and are consecutive along (some connected component of) ; the edge is drawn along the portion of the curve between the points. One edge for each such curve (connecting and ) is generated, even when the curves coincide or overlap. Thus there might potentially be many edges of connecting the same pair of points, whose drawings coincide. Nevertheless, by Proposition 3, this number is at most .

In spite of this control on the number of mutually overlapping (or, rather, coinciding) edges, we still face the potential problem that the edge multiplicity in (over all curves, overlapping or not, that connect the same pair of vertices) may not be bounded (by a constant). More concretely, we want to avoid edges whose multiplicity exceeds , where here denotes the degree of the curves of .

To follow this strategy, we pass to a dual parametric plane, in which the roles of and are interchanged, so curves of become dual points , and points of become dual curves , defined as the locus of all points , each corresponding to a pair of points , for which there exists (not necessarily in ) such that (compare with (3))

| (7) | ||||

we denote by and the sets of the dual points and of the dual curves, respectively. Clearly, we have if and only if . We recall our assumption that, for , the corresponding points and lie on the portion of which is outside . In view of this, we can ignore irreducible components of curves of which contain only “irrelevant” points , that is, only points for which one of or lies in .

Claim.

Let be a vertex of . Then there exist at most vertices , such that the number of curves of that pass through both is larger than .

Proof. For contradiction, assume there exist , , such that, for each , there are at least curves of passing through both . By construction (and using duality), every curve of connecting and corresponds to a dual point of that lies on both dual curves and . Thus, by the assumption on the pair , for each , the curves and have at least points in common, and hence, by Bézout’s theorem (see, e.g., [1]), the two curves share a common irreducible component. Note that , having degree , has at most irreducible components, and thus, by the pigeonhole principle, there exists an irreducible component of that is shared by at least curves ; by reindexing, if needed, assume these are , .

Let be the multiplicity bound obtained in Proposition 3. Let , , be (distinct) points on , having the property that, for each , the points lie on the portion of which is outside (but not necessarily in ); as already noted, we may assume that contains at least one such point, but then, by continuity, it contains infinitely many such points. We have , or, by duality, , for every . Similarly, we also have and so , for . Using Bézout’s theorem once again, we have that and , which intersect in at least points, share a common irreducible component, for each . Since is of degree , and thus has at most irreducible components, we conclude that there exists an irreducible component of that is shared by other curves . This however contradicts Proposition 3, and hence the claim follows.

Consider a point and one of its bad neighbors333We make the pessimistic assumption that they are (consecutive) neighbors along all these curves, which of course does not have to be the case in general. . Let be one of the curves along which and are neighbors. Then, rather than connecting to along , we continue along the curve from past until we reach a good point for (i.e., a point such that the number of curves of that pass through both is at most ), and then connect to that point (along ). We skip over at most points in the process, but now, having applied this “stretching” to each pair of bad neighbors, each of the modified edges has multiplicity at most (the factor 2 comes from the fact that a new edge can be obtained by stretching an original edge from either endpoint of ).

Note that this edge stretching does not always succeed: It will fail when the connected component of along which we connect the points contains fewer than points of , or when there are fewer than points of between , and the “end” of (recall the constraint in the definition of the curves ). Still, the number of new edges in is at least , for a suitable constant , where the term accounts for missing edges on connected components of the curves, for the reasons just discussed. By what have just been argued, the number of edges lost on any single component is at most .

The final ingredient needed for this technique is an upper bound on the number of crossings between the (new) edges of . Before doing so, we note that the way in which the edges are drawn, some of them may pass through vertices of (other than their endpoints), which was not allowed in Székely’s original work [15]. We resolve this issue by slightly perturbing the edges, so that they are drawn slightly off the curves. Each crossing between a pair of new edges, before this perturbation, is essentially a crossing between two curves of . Even though the two curves might overlap in a common irreducible component (where they have infinitely many intersection points, none of which is a crossing), the number of proper crossings between them is , as follows, for example, from the Milnor–Thom theorem (see [6, 16]), or from Bézout’s theorem. Finally, because of the way the drawn edges have been stretched, the edges, even those drawn along the same original curve , may now overlap one another, or, in the actual pertubed way in which they are drawn, may “tangentially cross” one another. In this case a crossing between two curves may be claimed by more than one pair of (stretched) crossing edges, and the tangential crossings need to be accounted for too. Nevertheless, since no edge straddles more than points, the number of pairs that claim a specific crossing is still a constant (that depends on ), and so is the number of their tangential crossings. Hence, we conclude that the total number of edge crossings in is .

We can now continue by applying the crossing lemma argument, exactly as done by Székely and in other works (e.g., see [8, 15]). The crossing lemma asserts that , for a suitable constant (that now depends on , to account for the possible overlap between edges), provided that , for another constant (that also depends on ). Combining the two possibilities, of a large and a small , and using the fact that , , and , we obtain

with the constant of proportionality depending on . This completes the proof of Proposition 4.

3 Conclusion

We do not know whether the bound in Theorems 1 and 2 is tight in the worst case, and suspect that it is not. Resolving this question is a major problem for further research, especially since it arises in all the related specific and general problems in [3, 4, 5, 10, 11, 13, 14].

This problem is clearly only one special instance of several related problems, in which we have three sets of points, each contained in some curve, and we want to bound the number of triples in that satisfy some property (that can be specified by polynomial equation, such as spanning a unit circle). As a simple example, consider the case where each is contained in some respective line , for , and the property is that the triple span a triangle of unit area. In a companion paper [9] we show that in this case the number of triples can be , but the bound is likely to drop when the sets are contained in other curves.

It is constructive to compare the study in this paper with the general setup studied in Elekes and Szabó [5] and in the recent paper [11] (prepared after the original submission of this paper). In principle, the results in this paper could be interpreted as a special case of the analysis in [5, 11]. That is, we have a trivariate polynomial over a Cartesian product of three sets of real numbers each, and the number of the unit circles (or triple points) under consideration is the number of zeros of in . The results in [11] assert that the number of such zeros is , unless has a special form. Although a general procedure for such a test can be provided (see, e.g., a discussion in [9]), its concrete execution is extremely complicated — at the moment we do not see any reasonable way to carry it out. We note that this is a general issue, that one will face in any specific application of the general theory of Elekes and Szabó.

Acknowledgment.

We would like to thank an anonymous referee, whose helpful and constructive comments helped us a lot to improve the paper. Part of this research was performed while the authors were visiting the Institute for Pure and Applied Mathematics (IPAM), which is supported by the National Science Foundation. The authors deeply appreciate the stimulating environment and facilities provided by IPAM.

References

- [1] D. A. Cox, J. Little and D. O’Shea, Using Algebraic Geometry, Springer-Verlag, 2nd Edition, Heidelberg, 2005.

- [2] G. Elekes, Sums versus products in number theory, algebra and Erdős geometry–A survey, in Paul Erdős and his Mathematics II, Bolyai Math. Soc., Stud. 11, Budapest, 2002, pp. 241–290.

- [3] G. Elekes and L. Rónyai, A combinatorial problem on polynomials and rational functions, J. Combinat. Theory Ser. A, 89 (2000), 1–20.

- [4] G. Elekes, M. Simonovits and E. Szabó, A combinatorial distinction between unit circles and straight lines: How many coincidences can they have? Combinat. Probab. Comput. 18 (2009), 691–705.

- [5] G. Elekes and E. Szabó, How to find groups? (And how to use them in Erdős geometry?), Combinatorica 32 (2012), 537–571.

- [6] J. Milnor, On the Betti numbers of real varieties, Proc. Amer. Math. Soc., 15(2) (1964), 275–280.

- [7] J. Pach and P. K. Agarwal, Combinatorial Geometry, Wiley-Interscience, New York, 1995.

- [8] J. Pach and M. Sharir, On the number of incidences between points and curves, Combinat. Probab. Comput. 7 (1998), 121–127.

- [9] O. E. Raz and M. Sharir, Unit-area triangles: Theme and variations, Proc. 31st Annu. Sympos. Comput. Geom., 2015, 569–583. Also in arXiv:1501.00379.

- [10] O. E. Raz, M. Sharir and J. Solymosi, Polynomials vanishing on grids: The Elekes-Rónyai problem revisited, Amer. J. Math. (2015), to appear. Also in arXiv:1401.7419.

- [11] O. E. Raz, M. Sharir, and F. de Zeeuw, Polynomials vanishing on Cartesian products: The Elekes-Szabó Theorem revisited, Proc. 31st Annu. Sympos. Comput. Geom., 2015, 522–536. Also in arXiv:1504.05012.

- [12] J. Schwartz, Fast probabilistic algorithms for verification of polynomial identities, J. ACM 27(4) (1980), 701–717.

- [13] M. Sharir and J. Solymosi, Distinct distances from three points, in arXiv:1308.0814.

- [14] M. Sharir, A. Sheffer, and J. Solymosi, Distinct distances on two lines, J. Combinat. Theory, Ser. A 20 (2013), 1732–1736.

- [15] L. Székely, Crossing numbers and hard Erdős problems in discrete geometry, Combinat. Probab. Comput. 6 (1997), 353–358.

- [16] R. Thom, Sur l’homologie des variétés algebriques réelles, in: S.S. Cairns (ed.), Differential and Combinatorial Topology, Princeton University Press, Princeton, NJ, 1965, 255–265.

- [17] R. Zippel, An explicit separation of relativised random polynomial time and relativised deterministic polynomial time, Inform. Process. Lett. 33(4) (1989), 207–212.

Appendix A Ultra-degenerate pairs

Recall that a pair is said to be ultra-degenerate if there exists a point at which at least one numerator and one denominator of the four fractions that define vanish simultaneously at . The reason for singling out these pairs is that it is not clear what happens to the slope of the tangent to at this point.

There are 16 cases of such a simultaneous vanishing of a numerator and a denominator. The four numerators are (where denotes the tangent vector to the circle at the point )

and the four denominators are

As noted earlier, the vanishing of any of these eight expressions means that a corresponding pair of points lie at distance from each other. Specifically, for the numerators, the corresponding constraints are, respectively,

and for the denominators, the corresponding constraints are, respectively,

Consider first the cases where the numerator and denominator of the same fraction both vanish. Consider for specificity the first fraction, so we have

In this case the four points , , and must be collinear, with . This is easily seen to imply that . In this case, is an intersection point of with the circle of radius centered at . Hence there are at most two choices for , for a total of pairs that fall into this subcase. A similar argument applies when the numerator and denominator of any of the three other fractions both vanish: The corresponding constraints are , , and , and in each of these cases it follows that there are at most two choices for either or , for a total of pairs of these types. (Note that in these cases the curves are singletons; see Figure 7(a).)

Therefore, in what follows, we assume that the vanishing numerator and denominator belong to distinct fractions. We use the mnemonic notation NtDs to mean that the numerator of the -th fraction and the denominator of the -th fraction both vanish, and consider the following possible cases.

N1D2: Here we have . In this case, is an intersection point of the two circles of radius centered at and at . Once is known, is an intersection point of with the unit circle centered at . Hence there are only ways to choose , for a total of ultra-degenerate pairs of this type.

N1D3: Here we have . We claim that each can be coupled with only ’s to form an ultra-degenerate pair of this type. Indeed, given , we find , as an intersection point of and a circle of radius centered at . Given , we find , as an intersection point of a unit circle centered at and a circle of radius centered at . From we can find , as an intersection point of and a unit circle centered at . Altogether, there are only choices for , as claimed.

N1D4: Here we have . Here each can be coupled with only ’s. Indeed, given , we find , as an intersection point of the unit circle centered at and a circle of radius centered at . From we find , as in the standard procedure, and from we find , as an intersection point of the unit circle centered at and a circle of radius centered at . From we find , as an intersection point of with the unit circle centered at . Altogether, there are only choices for , as claimed.

N2D1: Here we have . Since span a unit circle, we must have , which is thus an intersection point of and . This allows us to reconstruct , essentially as in case N1D2.

N2D3: Here we have . This case is easy: Given , we find , as an intersection point of and a circle of radius centered at , and from we find , as an intersection point of and a circle of radius centered at .

N2D4: Here we have . This case is symmetric to case N1D3, and is treated in a fully symmetric manner, starting from and reconstructing in ways.

N3D1: Here we have . Given , we find , as an intersection point of and a circle of radius centered at . From and we find , as an intersection point of and the diametral (unit) circle determined by . From we find , as the point that lies on the line through and at distance from (and from ). From we find , as an intersection point of and the unit circle centered at .

N3D2: Here we have . This case is treated exactly as case N1D4, except that here plays the role that was played there by .

N3D4: Here we have , so this is a symmetric version of case N1D2, with an essentially identical reconstruction process.

N4D1: Here we have . Given , we find , as an intersection point of with a circle of radius centered at . We then find , as an intersection of with the diametral (unit) circle determined by . In complete analogy with the treatment of case (iii) of the standard reconstruction process (at an extremal point of ), we note that the quadrilateral has edges of fixed lengths, namely, , , , and , and that it can flex around its fixed edge . As flexes, the midpoint of traces an algebraic curve of some constant degree, and the intersection(s) of with the unit circle centered at gives us the center(s) of the unit circle spanned by , from which is readily obtained, as in several preceding cases. If and do not overlap, the number of intersection points between them is finite and bounded by a constant, and there are only way to reconstruct .

As in case (iii), the situation where and do overlap can happen only when and are tangent to each other, and is this tangency point (see Figure 7(b)). In this case it is possible to have a superlinear (in fact, any) number of pairs , for which there exists , such that , and , are unit triples. We therefore do not exclude those pairs as ultra-degenerate. Instead, we claim that any such pair can be reconstructed from , using the reconstruction process described in Section 2.2. For this, we note that, for fixed, there exists at most one point , such that (and , are unit triples). Since, in the proof of Proposition 3, we trace from the point , in both increasing and decreasing -direction, we will not encounter this degeneracy in at least one of these traversals, and reach a locally - or -extremal point , from which can be reconstructed (if not excluded in one of the other ultra-degenerate cases), in at most a constant number of ways.

N4D2: Here we have . This case is symmetric to case N3D1, and is treated in an analogous manner, starting from and reconstructing in ways.

N4D3: Here we have . This is a symmetric variant of case N2D1, with an essentially identical treatment.

In summary, we have shown that the overall number of ultra-degenerate pairs is , as claimed.