Differentiability of Generalized Linear Models

Abstract

We derive conditions for differentiability of generalized linear models with error distributions not necessarily belonging to exponential families, covering both cases of stochastic and deterministic regressors. These conditions induce smoothness and integrability conditions for corresponding GLM-based time series models.

- Keywords

-

Generalized linear models; -differentiability; shape scale model; time series model for shape

- Subclass

-

MSC 62F12, 62F35

1 Motivation

Introduced by Nelder and Wedderburn (1972), generalized linear models (GLMs) have become one of the most frequently used statistical models with a vast amount of published results. Hence, trying to give a full account on relevant literature would be pretentious. We instead refer to the monographs McCullagh and Nelder (1989) and Fahrmeir and Tutz (2001). When it comes to regularity assumptions, though, this literature focuses on GLMs which are exponential families, compare Haberman (1974, 1977); Fahrmeir (1990); Fahrmeir and Kaufmann (1985), or uses quasi-likelihood or pseudo-likelihood techniques to account for over/under-dispersion effects, seeGouriéroux et al. (1984); Nelder and Pregibon (1987); McCullagh and Nelder (1989). In some situations, exponential families are a too narrow class, though: E.g., recently log-linear models for generalized Pareto distributions have found applications in operational risk (compare Dahen and Georges (2010)), but distributions of extreme value type with unknown shape parameter do not fall into the range of exponential families and so far are not yet covered.

Heading for asymptotic results and robustness, we are not only interested in consistency results for specific estimators like maximum likelihood estimators (MLEs), but rather in local asymptotic normality (LAN) in the sense of Le Cam (1970); Hájek (1972). With the LAN property at hand a very powerful asymptotic framework as pioneered by Le Cam is available: It gives a precise setup in which to obtain strong optimality results for (estimators behaving asymptotically like) the MLE, i.e., the Asymptotic Convolution Theorem and the Asymptotic Minimax Theorem, see, e.g. Rieder (1994, Thms. 3.2.3 & 3.3.8) or van der Vaart (1998, Thms. 8.8 & 8.11). The LAN property entails necessary expansions for asymptotic maximin tests with explicit terms for the asymptotic maximin power under local alternatives (Le Cam, 1986, Sec.11.9); it is the starting point for efficient and adaptive estimation in semiparametric models (compare Bickel et al. (1993)) and for a comprehensive theory of optimally-robust procedures (see Rieder (1994, Chs. 5 & 7)).

Now, a sufficient condition for the LAN property is given by -differentiability (see, e.g. Rieder (1994, Thm. 2.3.5)), and—at least in the i.i.d. setting—this is a necessary condition, too, compare Le Cam and Young (2000, Ch. 7, Prop. 3). Hence in this light, deriving smoothness of the model in terms of -differentiability would be a desirable goal; i.e., to consider GLMs as particular parametric models and to derive their -differentiability. For GLMs which are exponential families, this has already been achieved in Schlather (1994). Typically, however, scale-shape families as e.g. the generalized Pareto distributions are non-exponential. In this article, we hence generalize results of Rieder (1994, Sec. 2.4) on -differentiability for linear regression models to also cover error distributions with a -dimensional parameter and with regressors of possibly different length for each parameter. More specifically, we separately treat the case of stochastic regressors, which is of particular interest for incorporating (space-)time dependence, and of deterministic regressors as occurring in planned experiments.

While in principle -differentiability of these models could be settled by general auxiliary results from Hájek (1972, Lem. A.1–A.3), or be placed in the framework of Rieder and Ruckdeschel (2001), our goal are sufficient conditions directly exploiting the regression structure. More specifically, these conditions refer to (i) smoothness of the error distribution model, (ii) (uniform) integrability of the scores (-derivative) and (iii) suitably integrated continuity of the Fisher information of again the error distribution model.

At first glance, this might look like a technical exercise but setting up time series models where time-dependence is captured by a GLM-type link with (functions of) the own past observations as regressors, conditions (ii) and (iii) reveal to which extent the current error distribution may depend upon the past without making it “over-informative” for the present. More precisely, letting aside dimensionalities of the parameter of the error distribution and the regressors, the scores function of a GLM with errors from a distribution model , link function and regressor is of form , where are the parametric scores from model . Now even if has fat tails and non-existing moments, in many cases still is square integrable, see e.g. the case of -stable distributions as in DuMouchel (1973) or the generalized extreme value and Pareto distributions GEVD and GPD explicated later on in this paper. If however, as in a autoregressive (AR) time series context with identity link , comes again from a distribution within , the LAN property may fail due to a lack of integrability. This is the case in Andrews et al. (2009, Thm. 3.3), where in addition the authors obtain slower convergence rates for in an AR-model with -stable errors. One way to preserve the LAN property could consist in using a suitable link function such that the product becomes square integrable—see later in this paper for corresponding GPD and GEVD time series. This technique can be seen as an alternative / an extension to the approach using regression ranks as in Hallin et al. (2011), which in the respective case of a regression model with -stable errors and deterministic regressors achieves the same goal, i.e., extending the availabilty of the LAN property.

In this paper, we explicate the respective conditions (i)–(iii) for the cases of stochastic and deterministic regressors, respectively, in examples including—for reference and comparison—linear regression, Poisson, and Binomial regression, as well as scale-shape regression for the GPD and GEVD.

In particular for the latter distributions we give conditions which render a corresponding time series model accessible to the LAN type framework and thus contribute a new sort of GLM for extreme value type distributions where the tail weight respectively, the shape parameter depends on past observations in an autoregressive way. Thus, large extreme observations may foster or dampen the occurrence of future large extreme observations and controlling the extremal index (see Embrechts et al. (1997, p.413–423)) this way.

2 Main Results

Let be a measurable space and the set of all probability measures on . Consider a parametric model with open parameter domain . Following Le Cam and Rieder, we write for the densities w.r.t. some dominating measure on and denote the norm in the respective space by ; as usual, is suppressed from notation as the choice of has no effect on respective convergence assertions. In this context, differentiability in the case of i.i.d. observations is defined as follows.

Definition 2.1

Model is called differentiable at if there exists a function such that, as

| (2.1) |

Then, is the derivative and the matrix

is the Fisher information of at .

We say that is continuously differentiable at if, for any ,

| (2.2) |

Introducing regressors to explain parameter , we turn model into a regression model with parameter . To this end, for , let , be a partition of the coordinates into blocks of dimension , i.e., . Obviously, then each can unambiguously be indexed by the double index . For these blocks we define the following operators:

| (2.3) | |||

| (2.4) | |||

| (2.5) |

We also write for a matrix , meaning that we

apply to column by column as first argument, so that the result will be

the respective matrix .

Then, the case of a -dimensional parameter in Model and non-identically dimensional

regressors for each of the coordinates can be captured using a continuously differentiable link

function with derivative , so that for a -dimensional regressor

and -dimensional regression parameter we obtain a regression as for

. Applying the chain rule, the candidate derivative in this regression model

is

| (2.6) |

The case of the linear regression model treated in Rieder (1994, Sec. 2.4) is obtained as a special case for an -differentiable -dimensional location model and the identity. As in Rieder (1994, Sec. 2.4), we distinguish the cases of stochastic and deterministic regressors.

To apply conditions as in Hájek (1972), we need the notion of absolute continuity in dimensions: Let ; we call absolutely continuous, if for all the function , is absolutely continuous (as usual, see Rudin (1986, chap. 6)).

For later reference we recall the results of Hájek (1972, Lem. A.1–A.3):

Proposition 2.2 (Hájek)

Assume that in some surrounded by some open neighborhood , model satisfies

-

(H.1)

The densities are absolutely continuous in each for -a.e. .

-

(H.2)

The derivative exists in each for -a.e. .

-

(H.3)

The Fisher information exists, (i.e., the integral is finite) and is continuous in on .

Then, is continuously differentiable in with derivative and Fisher information .

2.1 Random Carriers

In this context the regressors are stochastic with distribution , but the observations are then modeled as i.i.d. observations. To this end, let model be a -dimensional -differentiable model with parameter and derivative and Fisher information . The corresponding GLM induced by the link function (with derivative ) and partition is given as

| (2.7) |

We state the following result.

Theorem 2.3

Let and for

as well as ; further define

.

Then model from (2.7) is differentiable in

if subsequent conditions (i)–(iii) hold.

-

(i)

Model fulfills (H.1)–(H.3) with “-a.e. ” replaced by “-a.e. ” in (H.1) and (H.2).

-

(ii)

(2.8) -

(iii)

for every ,

(2.9) where is the Frobenius matrix norm, i.e., .

Then model is continuously differentiable in with derivative and Fisher information

As just seen, the general GLM case comes with additional conditions for the link function and its derivative. For the linear regression case, they boil down to (i) differentiability of the one dimensional location case and (ii) finite second moment of w.r.t. . (iii) becomes void, as and does not depend on the parameter—compare Rieder (1994, Thm. 2.4.7).

2.2 Deterministic Carriers

The case of deterministic carriers canonically leads to triangular schemes of independent, but no longer identically distributed observations. To this end, we take up Rieder (1994, Def 2.3.8) and define a corresponding notion of -differentiability:

For and , let be general sample spaces and the set of all probability measures on . Consider the array of parametric families of probability measures .

Definition 2.5

The parametric array is called differentiable at if there exists an array of functions such that for all and the following conditions (2.10)–(2.12) are fulfilled.

| (2.10) |

Let and and for , we define and . Then, for all and all we require

| (2.11) |

Finally, for all we need

| (2.12) |

Then, in and at time , has derivative and

Fisher information .

is continuously differentiable in , if for each sequence ,

| (2.13) |

Our GLM with deterministic regressors correspondingly is defined as with

| (2.14) |

Rieder (1994, Theorem. 2.4.2) shows that in the linear regression case, conditions (2.11) and (2.12) follow from the (uniform) smallness of the hat matrix , which, as is a projector, reduces to the Feller type condition

| (2.15) |

In our more general framework, one may still define a corresponding projector locally (i.e., in ) as

| (2.16) |

and, locally, the (changes in the) fitted parameters (in a corresponding Fisher scoring procedure) then can be written as

However, contrary to the linear regression case, in the general GLM case, the distribution of the standardized scores is not invariant in . Therefore, the proof for the linear regression fails at this point and condition (2.15) is not sufficient—compare for instance the one-dimensional GLM at induced by the one-dimensional Poisson model with parameter , , the identity as link function and regressors . In fact, this is the standard example for a scheme satisfying the Feller condition but violating the Lindeberg condition. Also, not surprisingly, it is easy to see that Lindeberg condition (2.11) entails condition (2.15).

Theorem 2.6

Model from (2.14) is continuously differentiable in with derivative with from (2.6) and Fisher information as given in Definition 2.5 if the following conditions (i)–(iii) are fulfilled.

-

(i)

Model fulfills (H.1)–(H.3).

- (ii)

-

(iii)

Let for and introduce the abbreviations , , and . Then, for every it must hold

(2.17)

3 Examples

Example 3.1 (Linear regression)

It is obvious that Theorem 2.3 can be applied to the linear regression model

| (3.1) |

about the one dimensional location model

| (3.2) |

for some probability on with finite Fisher information of location where varies in the set of all continuously differentiable functions with compact support, see Huber (1981, Def. 4.1/Thm. 4.2)—finite Fisher information of location settles condition (i) of Theorem 2.3, condition (ii) as already noted boils down to and condition (iii) is void.

Example 3.2 (Binomial GLM with logit link and Poisson GLM with log link)

The Binomial model for known size , usually , and unknown success probability has error distribution with counting density (on ), hence condition (i) of Theorem 2.3 is obviously fulfilled with Fisher information . Choosing a logit link, i.e., , , conditions (ii) and (iii) become

| (ii) |

As in these expressions both integrands are bounded pointwise in , if is integrable w.r.t. , the Binomial GLM with logit-link is continuously differentiable.

The Poisson model () has error distribution with counting density (on ), hence condition (i) of Theorem 2.3 is obviously fulfilled with Fisher information . Choosing log link, i.e., , , conditions (ii) and (iii) become

Hence integrability of w.r.t. implies continuous differentiability of the Poisson GLM with log-link.

These two conditions, i.e., for Binomial logit and for the Poisson GLM with log-link recover the conditions mentioned in Fahrmeir and Tutz (2001, p.47).

Example 3.3 (GEVD and GPD joint shape-scale models with componentwise log link)

Both, the generalized extreme value distribution (GEVD) and the generalized Pareto distribution (GPD) come with a three-dimensional parameter for a location or threshold parameter , a scale parameter and a shape parameter . While for the GEVD, in principle the three dimensional model is -differentiable for and , respectively, in the GPD model, the model including the threshold parameter is not covered by our theory for -differentiable error models. The reason is basically, that observations close to the endpoint of the support in the GPD model carry overwhelmingly much information on the threshold. To deal with GEVD and GPD in parallel let us hence assume known in both models, and, for simplicity, . Then, parameter consists of scale and shape . In both models, the scores on the quantile scale, i.e., for the respective quantile function, include terms of order . Hence for condition (i), we need to assume that at least . Depending on the context, it can be reasonable to add further restrictions. E.g., in case of the GPD, we only obtain an unbounded support if ; similarly, if we restrict attention to the special case of Fréchet distributions for GEV distributions, is a natural restriction.

For parameter , we consider a continuously differentiable componentwise link function , i.e., the link function is of the form where we partition the -dimensional regressor and parameter accordingly to and so that . Then, based on the Fisher information matrix for joint scale and shape with entries , and , we obtain

That is, conditions (ii) and (iii) of Theorem 2.3 become

| (ii) | ||||

| (iii) | ||||

GEVD model: The scale-shape model has error distribution . As mentioned, condition (i) of Theorem 2.3 is fulfilled as long as or . This is reflected by the Fisher information matrix which reads

| (3.3) |

and has singularities in and .

GPD model: The scale-shape model , has a c.d.f. of and here, for and condition (i) is fulfilled with Fisher information matrix:

Again failure of condition (i) is reflected by a singularity at of the Fisher information.

The canonical link function for the scale is log link , whereas due to a lack of equivariance in the shape, there is no such canonical link for this parameter. For our GEVD and GPD applications, however, (non-regression-based) empirical evidence speaks for shape varying in . So a good link should not necessarily exclude values , but make them rather hard to attain. For this paper we even impose the sharp restriction .

Moreover, to use GLMs with GEVD and GPD errors in time series context to model parameter driven time dependencies in the terminology of Cox (1981), a real challenge is to design (smooth and isotone) link functions such that the regressors may themselves follow a GEVD or a GPD distribution, as this implies very heavy tails against which we have to integrate. More specifically, we aim at constructing an AR-type time series for the scale and shape of the form

| (3.4) |

In this model, negative values of would dampen clustering of extremes, as then usually a large value stemming from a large positive shape parameter will be followed by an observation with low or even negative shape hence with much lighter tails, thus in general a smaller value; correspondingly positive will foster clustering of extremes.

A straightforward guess would be to use the log link, but this does not work for GEVD or GPD time series, as then integrability (ii) fails. Thus, besides being smooth (for our theorem) and strictly increasing (for identifyability), an admissible link function must grow extremely slowly. To get candidates in case of the GEVD, note that all terms of the Fisher information matrix for GEVD are dominated by term , so conditions (ii) and (iii) are fulfilled if for large positive values , the link function grows so slowly to that , which for large amounts to a behavior like the iterated logarithm ; analogue arguments in case of the GPD suggest .

One possibility to achieve this for the GEVD for is where for is quadratic like and for behaves like for some such that is continuously differentiable in and always. As is shown in A.5, this choice indeed fulfills conditions (ii) and (iii).

With the singularity in of in (3.3), in many applications, it may turn out useful though to restrict shape to lie in either or in ; correspondingly, one could suggest a rescaled binomial link for the first case and shifting the link function sketched above to in the second.

Of course, given an admissible link function, the next question would be whether for given starting values a time series defined according to (3.4) for , using this link function is (asymptotically) stationary. This is out of scope for this paper and will be dealt with elsewhere.

Appendix A Proofs

A.1 Proof of Hájek’s auxiliary result Proposition 2.2

-

Proof : Apparently, (H.1) and (H.2) are implied by continuous differentiability of the densities w.r.t. . Hájek (1972) gives a proof of Proposition 2.2 for Lebesgue densities and for , but our notion of absolute continuity for from p. 2.2 reduces the problem to the situation of , which is possible here, as we require (H.1)–(H.3) on open neighborhoods. In addition, Hájek requires (H.1) for every . Looking into his proof of his Lemma A.2, though, one does not need that be Lebesgue densities, and in his Lemma A.3 one only needs absolute continuity for -a.e. . Finally, the asserted continuous differentiability (not mentioned in the cited reference) with regard to Definition 2.1 is just (H.3). A similar result, already for , but only for dominated and for continuous differentiability of w.r.t. for -a.e. , is Witting (1985, Satz 1.194). ////

A.2 Proof of the Chain rule

Lemma A.1 (Chain rule)

Let a parametric model with open parameter domain . Assume is differentiable in with derivative and Fisher information . Let with domain be differentiable in some such that and with derivative denoted by . Then is differentiable in with derivative and Fisher information . If is continuously differentiable in , so is in .

-

Proof : Let in , . We take , . Smoothness of link function implies:

(A.1) for some remainder function such that

(A.2) Let be dominated by some measure with density , i.e., . By differentiability of model for , we have

(A.3) But by (A.1) we may write as for

Now, Cauchy-Schwarz entails that Therefore

Hence, using (A.1), (A.2), and (A.3)

That is, by Definition 2.1 model is differentiable in . ////

A.3 Proof of Theorem 2.3

Let for such that for some with . We take , , . Let . By Definition 2.1 the GLM is differentiable at every if for the from Lemma A.1 now taking up the dependence on , i.e.,

| (A.4) |

Here (pointwise) existence (for -a.e. ) and form of the -derivative follow from (H.1) and the chain rule applied pointwise (in ). The proof of Lemma A.1 for -a.e. and small enough provides some function such that

Hence, for -a.e. fixed , . For Lebesgue measure , fixed and by the fundamental theorem of calculus for absolutely continuous functions, for -a.e. fixed we obtain

Now, introduce . By (ii) and (iii) is finite eventually in , and by (iii) and Fubini

Hence, by Vitali’s Theorem (e.g. Rieder (1994, Prop. A.2.2)),

is uniformly integrable (w.r.t. ), and, as ,

so is , and again by Vitali’s Theorem, which is (2.1).

Continuity (2.2) with regard to Vitali’s Theorem is just continuity of the Fisher information just shown.

The assertion of Remark 2.4 is shown similarly, replacing the and from above

with resp. .

////

A.4 Proof of Theorem 2.6

For selfcontainedness, we reproduce the argument for condition (2.10) from Rieder (1994, Thm. 2.3.7). In model , by (2.1), assuming -densities

Hence,

So , and hence also . Lindeberg condition (2.11) is assumed without change, so it only remains to show condition (2.12). Let be the -null set such that both (H.1) and (H.2) hold for all . Let . Then as in the case of stochastic regressors, from (H.1) and the chain rule applied pointwise (in ) we obtain (pointwise) existence and form of the -derivative. Let from (A.4) now take up the dependence on , i.e., (with from the preceding proof substituted by ) so that in particular, for every fixed , as . For condition (2.12) we have to show that . But, similarly as in the preceding proof for fixed , by the fundamental theorem of calculus for absolutely continuous functions, we have

Now, introduce and

note that ,

so and by (iii)

.

Hence, by Vitali’s Theorem, is uniformly integrable (w.r.t. the counting measure), and, as ,

so is , and again by Vitali’s Theorem, .

Finally, continuity (2.13) again with regard to Vitali’s Theorem is just continuity of the Fisher information

just proven.

////

A.5 Link function for the GEVD shape model

For GEVD for the shape we have chosen link function , for

for some . The constants are chosen so that is continuously differentiable in and always, i.e.

| (A.5) |

Since , to ensure the last inequality we let . Solving the system of equations we get , so and .

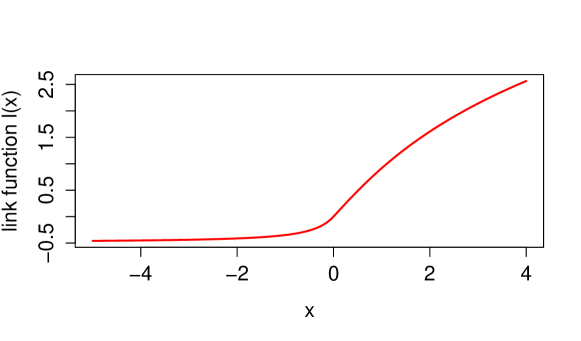

As said, shape is usually varying in . As visible from the Figure 1, this interval corresponds to an argument of the link function ranging in ; hence, for , is smaller than as long as and for .

To show that our choice of link function for GEVD, fulfills conditions (ii) and (iii), first we calculate its derivative and obtain for and for . Hence, for large , behaves like , while for , it essentially behaves like .

As mentioned, the term dominates all entries of all terms of in (3.3). Using the Stirling approximation, i.e., , due to the double application of the logarithm in the link function we get that is approximately . By equivariance in and , therefore the integral of condition (ii) turns into: for and, for , to . Finiteness of and follow from finiteness of for , . Reconsidering , at , for , we see that for , hence, condition (iii) is a consequence of dominated convergence and continuity of Fisher information in .

Acknowledgement

This article is part of the PhD thesis of Daria Pupashenko. All authors gratefully acknowledge financial support by the Volkswagen Foundation for the project “Robust Risk Estimation”, http://www.mathematik.uni-kl.de/~wwwfm/RobustRiskEstimation.

References

- (1)

- Andrews et al. (2009) Andrews, B., Calder, M., and Davis, R.A. (2009): Maximum Likelihood Estimation for -Stable Autoregressive Processes. Annals of Statistics 37: 1946–1982.

- Bickel et al. (1993) Bickel, P.J., Klaassen, C.A.J., Ritov, Y., and Wellner, J. A. (1993): Efficient and adaptive inference in semiparametric models. Springer. New York.

- Cox (1981) Cox, D.R. (1981): Statistical Analysis of Time Series: Some Recent Developments. Scand. J. Statist. 8: 93–115.

- Dahen and Georges (2010) Dahen, H., and Georges, D. (2010): Scaling models for the severity and frequency of external operational loss data. Journal of Banking & Finance 34(7): 1484–1496.

- DuMouchel (1973) DuMouchel, W.H. (1973): On the asymptotic normality of the maximum likelihood estimate when sampling from a stable distribution. Annals of Statistics 1: 948- 957.

- Embrechts et al. (1997) Embrechts, P., Klüppelberg, C., and Mikosch, T. (1997): Modelling extremal events for insurance and finance. Springer. New York.

- Fahrmeir (1990) Fahrmeir, L. (1990): Maximum likelihood estimation in misspecified generalized linear models. Statistics 21(4): 487–502.

- Fahrmeir and Kaufmann (1985) Fahrmeir, L., and Kaufmann, H. (1985): Consistency and asymptotic normality of the maximum likelihood estimator in generalized linear models. The Annals of Statistics 13(1) 342–368.

- Fahrmeir and Tutz (2001) Fahrmeir, L. and Tutz, G. (2001): Multivariate Statistical Modelling Based on Generalized Linear Models. 2nd Edn. Springer. New York.

- Gouriéroux et al. (1984) Gouriéroux, C., Monfort, A., and Trognon, A. (1984): Pseudo maximum likelihood methods: Theory. Econometrica 52(3): 681–700.

- Haberman (1974) Haberman, S.J. (1974): Log-linear models for frequency tables with ordered classifications. Biometrics 30(4): 589–600.

- Haberman (1977) Haberman, S.J. (1977): Maximum likelihood estimates in exponential response models. The Annals of Statistics 5(5): 815–841.

- Hájek (1972) Hájek, J. (1972): Local asymptotic minimax and admissibility in estimation. In Proceedings of the sixth Berkeley symposium on mathematical statistics and probability. Vol. 1, pp. 175–194.

- Hallin et al. (2011) Hallin, M., Swan, Y., Verdebout, T., and Veredas, D. (2011): Rank-based testing in linear models with stable errors. Journal of Nonparametric Statistics 23: 305- 320.

- Huber (1981) Huber, P. (1981): Robust Statistics. Wiley. New York.

- Le Cam (1986) Le Cam, L. (1986): Asymptotic Methods in Statistical Decision Theory. Springer. New York.

- Le Cam (1970) Le Cam, L. (1970): On the assumptions used to prove asymptotic normality of maximum likelihood estimates. The Annals of Mathematical Statistics 41(3): 802–828.

- Le Cam and Young (2000) Le Cam, L., and Yang, G.L. (2000): Asymptotics in Statistics. Some Basic Concepts. (2nd ed.) Springer. New York.

- McCullagh and Nelder (1989) McCullagh, P., and Nelder, J.A. (1989): Generalized linear models. Chapman Hall. London.

- Nelder and Pregibon (1987) Nelder, J.A., and Pregibon, D. (1987): An Extended Quasi-Likelihood Function. Biometrika 74(2): 221–232.

- Nelder and Wedderburn (1972) Nelder, J.A., and Wedderburn, R.W.M. (1972): Generalized linear models. Journal of the Royal Statistical Society. Series A, 370–384.

- Rieder (1994) Rieder, H. (1994): Robust Asymptotic Statistics. Springer. New York.

- Rieder and Ruckdeschel (2001) Rieder, H., and Ruckdeschel, P. (2001): Short proofs on -Differentiability. Statistics & Decisions, 19: 419–425.

- Rudin (1986) Rudin, W. (1986): Real and complex analysis. 3rd Edn. McGraw-Hill Inc. New York.

- Schlather (1994) Schlather, M. (1994): Glattheit von Generalisierten Linearen Modellen und statistische Folgerungen. Diplomarbeit Universität Bayreuth.

- van der Vaart (1998) van der Vaart, A. (1998): Asymptotic Statistics. Cambridge University Press. Cambridge.

- Witting (1985) Witting, H. (1985): Mathematische Statistik. Parametrische Verfahren bei festem Stichprobenumfang. Teubner. Stuttgart.