Regularized Tyler’s Scatter Estimator: Existence, Uniqueness, and Algorithms

Abstract

This paper considers the regularized Tyler’s scatter estimator for elliptical distributions, which has received considerable attention recently. Various types of shrinkage Tyler’s estimators have been proposed in the literature and proved work effectively in the “small n large p” scenario. Nevertheless, the existence and uniqueness properties of the estimators are not thoroughly studied, and in certain cases the algorithms may fail to converge. In this work, we provide a general result that analyzes the sufficient condition for the existence of a family of shrinkage Tyler’s estimators, which quantitatively shows that regularization indeed reduces the number of required samples for estimation and the convergence of the algorithms for the estimators. For two specific shrinkage Tyler’s estimators, we also proved that the condition is necessary and the estimator is unique. Finally, we show that the two estimators are actually equivalent. Numerical algorithms are also derived based on the majorization-minimization framework, under which the convergence is analyzed systematically.

Index Terms:

Tyler’s scatter estimator , shrinkage estimator, existence, uniqueness, majorization-minimization.I Introduction

Covariance estimation has been a long existing problem in various signal processing related fields, including multiantenna communication systems, social networks, bioinformatics, as well as financial engineering. A well known and easy to implement estimator is the sample covariance matrix. Under the assumption of clean samples, the estimator is consistent by the Law of Large Numbers. However, the performance of the sample covariance matrix is vulnerable to data corrupted by noise and outliers, which is often the case in real-world applications.

As a remedy, robust estimators are proposed aimed at limiting the influence of erroneous observations so as to achieve better performance in non-Gaussian scenarios [1, 2]. Recently, Tyler’s scatter estimator [3] has received considerable attention both theoretically and practically in signal processing related fields, e.g., [4, 5, 6, 7, 8] to name a few, see [9] for a comprehensive overview. Tyler’s estimator estimates the normalized scatter matrix (equivalently the normalized covariance matrix if the covariance exists) assuming that the underlying distribution is elliptically symmetric. The estimator is shown to enjoy the following advantages against the others: it is distribution-free in the sense that its asymptotic variance does not depend on the parametric form of the underlying distribution, and it is also the most robust estimator in a min-max sense.

In addition to non-Gaussian observations, another problem we face in practice is the “small n large p” problem, which refers to high dimensional statistical inference with insufficient number of samples. It is obvious that the sample covariance matrix is singular when the number of samples is smaller than the dimension, and Tyler’s estimator has the same drawback. In order to handle this problem, [10] borrowed the diagonal loading idea [11] and proposed a regularized Tyler’s estimator that shrinks towards identity. A rigorous proof for the existence, uniqueness, and convergence properties is provided in [12], where a systematic way of choosing the regularization parameter was also proposed. However, the estimator is criticized for not being derived from a meaningful cost function. To overcome this issue, a new scale-invariant shrinkage Tyler’s estimator, defined as a minimizer of a penalized cost function, was recently proposed in [13]. By showing that the objective function is geodesic convex, Wiesel proved that any algorithm that converges to the local minimum of the objective function is actually the global minimum. Numerical algorithms are provided for the estimator and simulation results demonstrate the estimator is robust and effective in the sample deficient scenario. Despite the good properties, the existence and uniqueness properties of the estimator remains unclear.

In this paper, we study the shrinkage Tyler’s estimator and try to answer the unsolved problems mentioned above. First, we give a proof that states the sufficient condition for the existence of shrinkage Tyler’s estimator with penalized cost function taking a general form. Second, we propose a Kullback-Leibler divergence (KL divergence) penalized cost function that results in a shrinkage Tyler’s estimator similar to the heuristic diagonal loading one considered in [10, 12]. We then move to these two specific estimators and show that under the condition and the shrinkage target matrix being positive definite, the estimators exist, where is the number of samples, is the dimension of the samples and controls the amount of penalty added to the cost function, stands for the proportion of samples contained in a proper subspace . In addition, we prove it is also a necessary condition, provided that . Although derived from different cost functions, and also with different estimation equation, we prove that the two shrinkage estimators are actually equivalent. Under the assumption that the underlying distribution is continuous, the condition simplifies to . Comparing with the existence condition for Tyler’s estimator, which is , or under continuity assumption, this result clearly demonstrates that regularization can relax the requirement on the number of samples, hence shows its capability of handling large dimension estimation problems. Algorithms for the shrinkage estimators based on majorization-minimization framework are provided, where the convergence can be analyzed systematically.

It is worth mentioning that in the work [14], where the same condition is also independently derived for the KL penalty based shrinkage estimator that shrinks the covariance matrix to identity in the complex field, assuming the samples are linearly independent. [14] refutes the additional trace normalization step in [12] by showing that the trace of the inverse of the estimator is equal to , and propose dropping the normalization step. Different from that approach, our work gives an interpretation of the estimator as the minimizer of a KL divergence penalized cost function. Starting from the cost function, we establish the existence condition with a different proof from [14]. In addition, we extend the result (in the real field), since the condition implies if the samples are linearly independent, and we consider a general positive definite shrinkage target matrix as in [13].

The paper is organized as follows: In Section II, we briefly review Tyler’s estimator for samples drawn from the elliptical family. In Section III, the two types of shrinkage estimators, i.e., one proposed in [13] and another derived based on KL divergence are considered, and a rigorous proof for the existence and uniqueness of the estimators is provided. Algorithms based on majorization-minimization are presented in Section IV. Numerical examples follow in Section V, and we conclude in Section VI.

Notation

stands for -dimensional real-valued vector space, stands for vector Frobenius norm. stands for symmetric positive semidefinite matrices, which is a closed cone in , denotes symmetric positive definite matrices. and stand for the largest and smallest eigenvalue of a matrix respectively. and stand for matrix determinant and trace respectively. is the matrix Frobenius norm.

The boundary of the open set is conventionally defined as , which contains all rank deficient matrices in . With a slightly abuse of notation, we also include matrices with all eigenvalues into the boundary of . Therefore a sequence of matrices converges to the boundary of iff or . In the rest of the paper, we will use the statement “ converges” equivalently as “a sequence of matrices converges” for notation simplicity.

II Robust covariance matrix estimation

In this paper, we assume a number of -dimensional samples are drawn from an elliptical population distribution with probability density function (pdf) of the form

| (1) |

with location and scatter parameter in . The nonnegative function , which is called the density generator, determines the shape of the pdf. In most of the popularly used distributions, e.g., the Gaussian and the Student’s t-distribution, is a decreasing function and determines the decay of the tails of the distribution. Given , our problem of interest is to estimate the covariance matrix. We can always center the pdf by defining , hence without loss of generality in the rest of the paper we assume We use the notation and for the empirical and the population distributions, respectively. It is known that the covariance matrix of elliptical distribution takes the form with being a constant that depends on [1], hence it is unlikely to have a good covariance estimator without prior knowledge of . In this paper, instead of trying to find the parametric form of and get an estimator of , we are interested in estimating the normalized covariance matrix .

The commonly used sample covariance matrix, which also happens to be the maximum likelihood estimator for the normal distribution, estimates asymptotically, however it is sensitive to outliers. This motivates the research for estimators robust to outliers in the data and, in fact, many researchers in the statistics literature have addressed this problem by proposing various robust covariance estimators like M-estimators [15], S-estimators [16], MVE [17], and MCD [18] to name a few, see [1, 2] for a complete overview. For example, in [15], Maronna analyzed the properties of the M-estimators, which are given as the solution to the equation

| (2) |

where the choice of function determines a whole family of different estimators. Under some technical conditions on (i.e., for and nonincreasing, and is strictly increasing), Maronna proved that there exists a unique that solves (2), and gave an iterative algorithm to arrive at that solution. He also established its consistency and robustness. A number of well known estimators take the form (2) and in [15] Maronna gave two examples, with one being the maximum likelihood estimator for multivariate Student’s t-distribution, and the other being the Huber’s estimator [19]. Both of them are popular for handling heavy tails and outliers in the data.

For all the robust covariance estimators, there is a tradeoff between their efficiency, which measures the variance (estimation accuracy) of the estimator, and robustness, which quantifies the sensitivity of the estimator to outliers. As these two quantities are opposed in nature, a considerable effort has to be put in designing estimators that achieve the right balance between these two quantities. In [3], Tyler dealt with this problem by proposing an estimator that is distribution-free and the “most robust” estimator in mini-max sense. Tyler’s estimator of is given as the solution of the following equation

| (3) |

where the results of [15] cannot be applied since is not strictly increasing. Tyler established the conditions for the existence of a solution to the fixed-point equation (3), as well as the fact that the estimator is unique up to a positive scaling factor, in the sense that solves (3) if and only if solves (3) for some positive scalar . The estimator was shown to be strongly consistent and asymptotically normal with its asymptotic standard deviation independent of .

Tyler’s fixed-point equation (3) can be alternatively interpreted as follows. Consider the normalized samples defined as , it is known that the probability distribution of takes the form [20, 21, 22]

| (4) |

Given samples from the normalized distribution , the maximum likelihood estimator of can be obtained by minimizing the negative log-likelihood function

| (5) |

which is equivalent to minimizing

| (6) |

If a minimum of the function exists, it needs to satisfy the stationary equation given in (3), which was originally derived by Tyler in [3]. In [3, 21], the authors provided the condition for existence of a nonsingular solution to (3) based on the following reasoning. Notice that must be nonsingular, and the function is unbounded above on the boundary of positive definite matrices, implies the existence of a minimum. Based on these observations, Kent and Tyler established the existence conditions by showing on the boundary. Specifically, under the condition that: (i) no lies on the origin, and (ii) for any proper subspace , , where stands for the proportion of samples in , then a nonsingular minimum of the problem (6) exists, which is equivalent to equation (3) having a solution. In words, the above mentioned conditions require the number of samples to be sufficiently large, and the samples should be spread out in the whole space.

To arrive at the estimator satisfying (3), Tyler proposed the following iterative algorithm:

| (7) |

that converges to the unique (up to a positive scaling factor) solution of (3).

The robust property of Tyler’s estimator can be understood intuitively as follows: by normalizing the samples, i.e., , the magnitude of an outlier is more unlikely to make the estimator break down. In other words, the estimator is not sensitive to the magnitude of samples, only their direction can affect the performance.

III Regularized Covariance Matrix Estimation

The regularity conditions for the existence of Tyler’s estimator leads to a condition on the number of samples that [21, 23]. In some practical applications the number of samples is not sufficient, in those cases Tyler’s iteration (7) may not converge. In these scenarios, a most sensible approach is to shrink Tyler’s estimator to some known a priori estimate of . In the literature of robust estimators, there exists two different shrinkage based approaches.

In the first approach, the authors in [10, 12] proposed the following estimator:

| (8) |

which is a slightly modified version of the original Tyler’s iteration in (7), with the modification being including an identity matrix in the first step of the iteration that aims at shrinking the estimator towards the identity matrix. This resembles the idea of regularizing an estimator via diagonal loading [11, 24]. In [12], Chen et al. proved the uniqueness of the estimator obtained by the iteration (8) based on concave Perron-Frobenius theory, and gave a method to choose the regularization weight . Although this estimator is widely used and performs well in practice, it is still considered to be heuristic as it does not have an interpretation based on minimizing a cost function.

As a second approach, in [13], the author took a different route and derived a new shrinkage-based Tyler’s estimator that has a clear interpretation based on minimizing the penalized negative log-likelihood function

| (9) |

where is a function with minimum at the desired target matrix , hence it will shrink the solution of (9) towards the target. By showing the cost function is geodesic convex, the author proved that any local minimum over the set of positive definite matrices is a global minimum [13]. He then derived an iterative algorithm based on majorization-minimization that monotonically decreases the cost function at each iteration:

| (10) |

Even though the author in [13] showed that the cost function is convex in geodesic space, the existence and uniqueness of the global minimizer remains unknown. Moreover, it is mentioned in [13] that for some values of the cost function becomes unbounded below and the iterations do not converge.

In this section, we address the following points: (i) we give the missing interpretation based on minimizing a cost function for the estimator in (8), and we also prove its existence and uniqueness; (ii) we prove the iteration in (10) with an additional trace normalization step converges to a unique point and also establish the conditions on the regularization parameter to ensure the existence of the solution. For both cases, the cost function takes the form of penalized negative log-likelihood function with different penalizing functions. Our methodology for the proofs hinges on techniques used by Tyler in [23, 21].

We start with a proof of existence for a minimizer of a general penalized negative log-likelihood function in the following theorem, the proof of existence of the two aforementioned cases and are just special cases of the general result.

The idea of proving the existence is to establish the regularity conditions under which the cost function takes value on the boundary of the set , a minimum then exists by the continuity of the cost function. The main result is established in Theorem 3, and the following lemma is needed.

Lemma 1.

For any continuous function defined on the set , there exists a such that if on the boundary of the set .

Definition 2.

For any continuous function defined on , define the quantities

| (11) |

and

| (12) |

In this paper we are particularly interested in the functions and with some positive scalar . For , and, for , , . We restrict our attention to the case .

Consider the penalized cost function takes the general form with original cost function

| (13) |

where is a continuous function, and the penalty term

| (14) |

where measures the difference between and the positive semidefinite matrix . is, in general, an increasing function that increases the penalty as deviates from , which is considered to be the prior target that we wish to shrink to.

We first give an intuitive argument on the condition that ensures the existence of the estimator. Since the estimator is defined as the minimizer to the penalized loss function, it exists if on the boundary of by Lemma 1, and clearly is nonsingular. We infer by the samples , if the samples are concentrated on some subspace, naturally we “guess” the distribution is degenerate, i.e., is singular. Therefore, the samples are required to be sufficiently spread out in the whole space so that the inference leads to a nonsingular . Under the case when we have a prior information that should be close to the matrix , to ensure being nonsingular we need to distribute more ’s in the null space of and hence less in the range of . To formalize this intuition, we give the following theorem.

Theorem 3.

For cost function

| (15) |

defined on positive definite matrices with and being continuous functions, define and for , and for ’s according to (11) and (12), then on the boundary of the set if the following conditions are satisfied:

(i) no lies on the origin;

(ii) for any proper subspace

where sets and are defined as , ;

(iii) and .

Proof:

See Appendix A.∎

Remark 4.

Condition (i) avoids the scenario when takes value and is undefined at , for example for the log-likelihood function. The first part in condition (ii), , ensures under the case that some but not all eigenvalues of tend to zero, and the second part in condition (ii), , ensures under the case that some but not all eigenvalues of tend to positive infinity. Together they force when . The first part of condition (iii) ensures when all and the second part ensures when all .

Corollary 5.

Assuming the population distribution is continuous, and the matrices are full rank, condition (ii) in Theorem 3 simplifies to:

Proof:

The conclusion follows easily from the following two facts: given that the population distribution is continuous, and no lies on the origin, any sample points define a proper subspace with with probability one; and since ’s are full rank, the set . ∎

Under the regularity conditions provided in Theorem 3, Lemma 1 implies a minimizer of exists and is positive definite, therefore it needs to satisfy the condition .

We then show how Theorem 3 works for Tyler’s estimator defined as the nonsingular minimizer of (6). Notice that the loss function is scale-invariant, we have for any positive definite . This implies that there are cases when goes to the boundary of and will not go to positive infinity. Due to this reason, condition (iii) is violated in Theorem 3. To handle the scaling issue, we introduce a trace constraint .

For the Tyler’s problem of minimizing (6), we seek for the condition that ensures when goes to the boundary of the set relative to . The condition implies that there is a unique minimizer that minimizes over the set , and by it is equivalent to the existence of a unique (up to a positive scaling factor) minimizer that minimizes over the set since is scale-invariant.

The constraint excludes the case that any of and the case all , hence we only need to let under the case that some but not all , which corresponds to the condition in Theorem 3. For Tyler’s cost function , we have and , , therefore Theorem 3 leads to the condition on the samples: , or if the population distribution is continuous, which reduces to the condition given in [21].

III-A Regularization via Wiesel’s penalty

In [13], Wiesel proposed a regularization penalty that results in a shrinkage estimator. Specifically, the penalty terms that encourage shrinkage towards an identity matrix and more generally towards an arbitrary prior matrix are defined as follows:

| (16) |

As can be seen the penalty terms are scale-invariant. Wiesel justified the choice of the above mentioned penalty functions by showing that the minimizer of the penalty functions would be some scaled multiple of (or ). Thus adding this penalty terms to the Tyler’s cost function would yield estimators that are shrunk towards (or ). In the rest of this subsection we consider the general case only, where the penalty term shrinks to scalar multiples of , and we make the assumption that is positive definite, which is reasonable since must be a positive definite matrix. The cost function is restated below for convenience

| (17) |

Minimizing gives the fixed-point condition

| (18) |

Recall that in the absence of regularization (i.e., ), a solution to the fixed-point equation exists under the condition . With the regularization, however, it is not clear. We start giving a result for the uniqueness and then come back to the existence.

Theorem 6.

If (18) has a solution, then it is unique up to a positive scaling factor.

Proof:

It’s easy to see if solves (18), is also a solution for . Without loss of generality assume is a solution, otherwise define and , and that there exists another solution . Denote the eigenvalues of as with at least one strictly inequality, then under the condition that is positive definite

where the inequality follows from the fact that for any positive definite matrix and the last equality follows from the assumption that is a solution to (18). We have the contradiction , hence all the eigenvalues of should be equal, i.e., . ∎

Before establishing the existence condition, we give an example when the solution to (18) does not exist for illustration.

Example 7.

Consider the case when all ’s are aligned in one direction. Eigendecompose and choose to be aligned with the ’s, let while others . Ignoring the constant terms, the boundedness of is equivalent to the boundedness of , hence it is unbounded below if .

The example shows that can be unbounded below implying that (18) has no solution if the data are too concentrated and is small. The following theorems gives the exact tradeoff between data dispersion and the choice of .

Theorem 8.

A unique solution to (18) exists (up to a positive scaling factor) if the following conditions are satisfied:

(i) no lies on the origin;

(ii) for any proper subspace , ,

and they are the global minima of the loss function (17).

Proof:

We start by rewriting the function including a the scaling factor w.r.t. (17) for convenience:

| (19) |

Invoke Theorem 3 with , , and , hence and . By the same reasoning as for the Tyler’s loss function, the condition , which is since is full rank, ensures the existence of a unique solution to (18) under the constraint and . Hence a unique (up to a positive scaling factor) solution to (18) exists on the set of by the scale-invariant property of . ∎

To make the existence condition checkable, we use Corollary 5, Theorem 8 then simplifies to or, equivalently , from which we can see that compared to the condition without regularization shrinkage allows less number of samples, and the minimum number depends on .

At last, we show that the condition is also necessary in the following proposition.

Proposition 9.

If (18) admits a solution on , then for any proper subspace , , provided that is positive definite and .

Proof:

For a proper subspace , define as the orthogonal projection matrix associated to , i.e., , . Assume the solution is . Multiplying both sides of equation (18) by matrix and taking the trace we have

If , then , and if . Moreover, since is positive definite. This therefore implies

Rearranging the terms yields . ∎

III-B Regularization via Kullback-Leibler Divergence Penalty

An ideal penalty term should increase as deviates from the prior target . Wiesel’s penalty function discussed in the last subsection satisfies this property and, in this subsection, we propose another penalty that has this property. The penalty that we choose is the KL divergence between and , i.e., two zero-mean Gaussians with covariance matrices and , respectively. The formula for the KL divergence is as follows [25, 26]

Ignoring the constant terms results in the following loss function:

| (20) |

with the following fixed-point condition:

| (21) |

Unlike the penalty function discussed in the last subsection, KL divergence penalty encourages shrinkage towards without scaling ambiguity. This can be easily seen, as the minimizer for the KL divergence penalty is just . Notice that (21) is similar to the diagonal loading in (8), but without the heuristic normalizing step.

Theorem 10.

If (21) has a solution, then it is unique.

Proof:

Without loss of generality, we assume solves (21). Assume there is another matrix that solves (21), and denote the largest eigenvalue of as and suppose . We then have the following contradiction:

which gives contradiction , hence . Similarly, suppose the smallest eigenvalue of satisfies . We then have

which is a contradiction and hence , from which follows.∎

Theorem 11.

A unique solution to (21) exists, if

(i) no lies on the origin;

(ii) ,

and it is the global minimum of loss function (20).

Proof:

Equivalently, we can define

| (22) |

Invoke Theorem 3 with , , and , hence , , . Since is full rank and , condition (ii) reduces to . Condition (iii) is satisfied, hence an interior minimum exists. Furthermore, it is the unique minimum, hence it is global.∎

Remark 12.

The only difference between the regularized estimator discussed in this subsection and the heuristic estimator in (8) is the extra normalizing step in (8). With the trace normalization, [12] proved that the iteration implied by (8) converges to a unique solution without any assumption of the data. However, the iteration implied by (21), which is based on minimizing a negative log-likelihood function penalized via the KL divergence function, requires some regularity conditions to be satisfied (cf. Theorem 11). According to Corollary 5, the condition simplifies to if the population distribution is continuous.

Proposition 13.

If (21) admits a solution on , then for any proper subspace , , provided that is positive definite and .

Proof:

Finally, we show in the following proposition that the Wiesel’s shrinkage estimator defined as solution to (18) and KL shrinkage estimator defined as solution to (21) are equivalent.

Proposition 14.

Proof:

If is zero, the statement is trivial. We consider the case . Following the argument of previous proposition we arrive at equation (23). It has been shown in [14] that the unique solution to (23) satisfies given , hence . Substitute it into equation (18) yields exactly equation (21) with solution , which indicates solves (18). The second part of the proposition follows from the fact that Wiesel’s fixed-point equation (18) has a unique solution up to a positive scaling factor. ∎

IV Algorithms

Before going the specific algorithms, we first briefly introduce the concepts of majorization-minimization [27, 28]. Consider the following optimization problem

| (24) |

where is assumed to be a continuous function, not necessarily convex, and is a closed convex set.

At a given point , the majorization-minimization algorithm finds a surrogate function that satisfies the following properties:

| (25) |

with stands for directional derivative. The surrogate function is assumed to be continuous in and 111Notice that if both and are continuously differentiable, then the first two conditions in (25) imply the third..

The majorization-minimization algorithm updates as

It is proved that every limit point of the sequence converges to a stationary point of problem (24), and under the assumption that the level set is compact, the distance between and the set of stationary points reduces to zero in the limit[28].

In the rest of this section, for any continuous differentiable function , we define when .

IV-A Regularization via Wiesel’s Penalty

In [13], Wiesel derived Tyler’s iteration (7) but without the trace normalization step, from the majorization-minimization perspective, with surrogate function for (6) defined as

| (26) |

A positive definite stationary point of satisfies the first equation of (7). By the same technique, to solve the problem

| (27) |

Wiesel derived the iteration (10) by majorizing (17) with function

| (28) | ||||

It is worth pointing out that if we do the change of variable in and linearize the term , this also leads to the same iteration (10).

In the rest of this subsection, we prove the convergence of the iteration (10) proposed by Wiesel, but with an additional trace normalization step, i.e., our modified iteration takes the form:

| (29) |

Denote the set .

-

1.

Initialize as an arbitrary positive definite matrix.

-

2.

Do iteration

until convergence.

Lemma 15.

The set is a compact set.

Proof:

implies the set is bounded. The set is closed follows easily from the fact that when tends to be singular.∎

Proof:

For surrogate function (28), its value goes to positive infinity when , since it majorizes and in this case. Now consider the case when . Define , then function (28) can be rewritten as

| (30) | ||||

The terms , and are all constants bounded away from both and . It is easy to see that when or , (30) goes to . Therefore we conclude that the value of Wiesel’s surrogate function (28) goes to when approaches the boundary of . The fact that given in (29) is the unique solution to the stationary equation implies that it is the unique minimizer of (28) on the set .∎

Proposition 17.

Proof:

It is proved in Theorem 8 that under the conditions provided in Theorem 8, the minimizer for problem

| (31) |

exists and is unique, furthermore, it solves problem (27). It is also proved that the objective function on the boundary of the set . We now show that the sequence converges to unique minimizer of (31).

Denote the surrogate function in general as , by Lemma 16 we therefore have the following inequality

which means is a non-increasing sequence.

Assume that there exists converging subsequence , then

Letting results in

which implies that the directional derivative . The limit is nonsingular since if is singular , but given that , which is a contradiction. Since and the function is continuously differentiable, we have . Since , .

The set is a compact set, and lies in this set, hence converges to . ∎

IV-B Regularization via Kullback-Leibler Penalty

Following the same approach, for the KL divergence penalty problem:

| (32) |

We can majorize at by function

| (33) |

the stationary condition leads to the iteration

| (34) |

Algorithm 2 summarizes the procedure for KL shrinkage estimator.

-

1.

Initialize as an arbitrary positive definite matrix.

-

2.

Do iteration

until convergence.

Proposition 18.

Proof:

We verify the assumptions required for the convergence of algorithm [28], namely (25) and the compactness of initial level set .

The first condition in (25) is satisfied by construction. To verify the second condition, we see that the gradient of the surrogate function has a unique zero. Since is a global upperbound for , as goes to the boundary of . By the continuity of , a minimizer exists and has to satisfy . Therefore the unique zero has to be the global minimum, i.e., . The last condition is satisfied since is continuously differentiable on .

It is proved in Theorems 10 and 11 that on set , has a unique stationary point and it is the global minimum. Furthermore, the conditions in Theorem 11 ensures when goes to the boundary of . The initial set is compact follows easily.

Therefore the sequence converges to the set of stationary points, hence the global minimum of problem (32). ∎

IV-C Estimation with Structure Constraints

In this subsection, we briefly discuss the covariance estimation problem with structure constraints. In general, the uniqueness of the estimator cannot be guaranteed. However, algorithms can still be derived based on majorization-minimization when the constraint set is convex. In this case, we can majorize the objective functions and by

and

respectively, ignoring the constant term. Without any additional constraint, setting the gradient of to zero yields update

where

and

Notice that is exactly the update we derived by only majorizing the terms in the previous subsection, and is the geometric mean between matrices and [29]. Intuitively can be viewed as a smoothed update of .

However, when constrained, a closed-form solution for cannot be obtained in general. The surrogate function is convex since is linear and is convex, can be found numerically if is convex. We consider two such examples.

IV-C1 Covariance Matrix with Toeplitz Structure

Toeplitz structure arises frequently in various signal processing related fields. For example, in time series analysis, the autocovariance matrix of a stationary process is Toeplitz. Imposing the Toeplitz structure on we need to solve

for each iteration. The additional constraint is linear.

IV-C2 Linear Additive Structure

Suppose can be decomposed as , where is signal covariance and with is noise covariance restricted to some interval. Then, at each iteration we solve

The additional constraint is convex.

IV-D Parameter Tuning

A crucial issue in regularized covariance estimator is to choose the penalty parameter . We have shown that if the population distribution is continuous, for both Wiesel’s penalty and KL divergence penalty, we require to guarantee the existence of the regularized estimator.

There is a rich literature discussing the rules of parameter tuning developed for specific estimators. A standard way is to select by cross-validation, method based on random matrix theory has also been investigated in a recent paper [30].

V Numerical Results

In all of the simulations, the estimator performance is evaluated according to the criteria in [13], namely, the normalized mean-square error

where all matrices are all normalized by their trace. The expected value is approximated by times Monte-Carlo simulations.

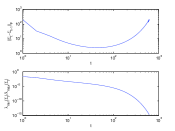

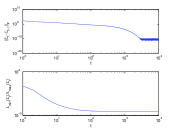

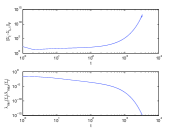

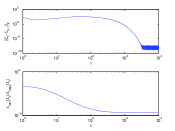

The first two simulations aims at illustrating the existence conditions for both Wiesel’s shrinkage estimator and KL shrinkage estimator. We choose and with the samples drawn a Gaussian distribution , where is a randomly generated positive definite covariance matrix. The shrinkage target is also an arbitrary positive definite matrix. According to the result in Section III, , i.e., , is the necessary and sufficient condition for the existence of a positive definite estimator. We simulate two scenarios with and . Fig. 1 plots and the inverse of the condition number, namely , as a function of the number of iterations in log-scale for Wiesel’s shrinkage estimator and with (left) and (right) respectively. Fig. 1 shows that for Wiesel’s shrinkage estimator, when diverges, and when converges to a nonsingular limit. Fig. 2 shows similar situation happens for KL shrinkage estimator.

For the rest of the simulations, the shrinkage parameter is selected by grid search. That is, we define and enumerate uniformly on interval , and select the (equivalently ) that gives the smallest error.

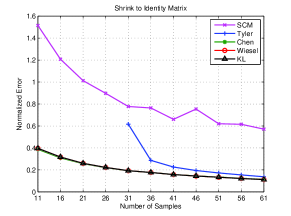

Fig. 3 demonstrates the performance of shrinkage Tyler’s estimator in the sample deficient case. The tuning parameter is selected to be the one that yields the smallest NMSE for each estimator as proposed in [13]. We choose the example

with . In this simulation, the underlying distribution is chosen to be a Student’s t-distribution with parameters , , and , and the shrinkage target is set to be an identity matrix. The number of samples starts from to . The curve corresponding to Tyler’s estimator starts at since the condition for Tyler’s estimator to exist is , i.e., in this case. The figure illustrates that both Tyler’s estimator and shrinkage Tyler’s estimator outperform the sample covariance matrix when all of them exist, shrinkage estimators exist even when and, moreover, achieve the best performance in all cases.

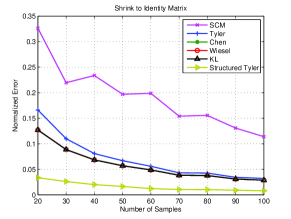

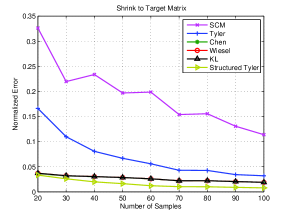

Fig. 4 and 5 compare the performance of different shrinkage Tyler’s estimators following roughly one of the simulation set-up in [13] for a fair comparison. The samples are drawn from a Student’s t-distribution with parameters , and . The number of samples varies from to . Fig. 4 shows the estimation error when setting and Fig. 5 shows that when setting , the searching step size of is set to be . The result indicates that estimation accuracy is increased due to shrinkage when the number of sample is not enough. Wiesel’s shrinkage estimator and KL shrinkage estimator yield the same NMSE. Interestingly, Chen’s shrinkage estimator gives roughly the same NMSE, although with a different shrinkage parameter . Chen’s and KL shrinkage estimator thus find their advantage in practice since an easier way of choosing rather than cross-validation has been investigated in the literature [12, 30], a detailed comparison of them from random matrix theory perspective has also been provided in [30].

In both of the simulations, we include Tyler’s estimator with a Toeplitz structure constraint as introduced in the previous section. The figures show that the structure constrained estimator achieves relatively better performance than all other estimators both when shrinking to and shrinking to . Although structure constraint can be imposed on shrinkage estimators to achieve potentially even smaller estimation error, we leave out this simulation due to the heavy computational cost introduced both by a lack of a closed-form solution per iteration (a SDP need to be solved numerically) and grid searching for the best regularization parameter. The problem of accelerating the algorithm and investigating the effect of imposing structure constraint on shrinkage estimator are left for future work.

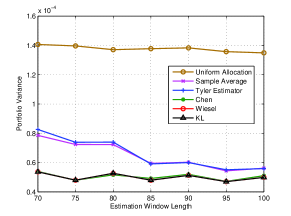

Finally, the performance of Tyler’s estimator is tested on a real financial data set. We choose daily close prices from Jan 1, 2008 to July 31, 2011, 720 days in total, of stocks from the Hang Seng Index provided by Yahoo Finance. The samples are constructed as , i.e., the daily log-returns. The process is assumed to be stationary. The vector is constructed by stacking the log-returns of all stocks. that is close to (all elements are less than ) is discarded. We compare the performance of different covariance estimators in the minimum variance portfolio set up, that is, we allocate the portfolio weights to minimize the overall risk. The problem can be formulated formally as

| (35) |

with being the covariance matrix of . Clearly the scaling of does not affect the solution to this problem.

The simulation takes the following procedure. For nonshrinkage estimators, at day , we take the ’s with as samples to estimate the normalized covariance matrix . For a particular shrinkage estimator, the target matrix is set to be and the tuning parameter is chosen as follows: for each value of , we calculate the shrinkage estimator with samples , and the corresponding by solving (35). We then take the ’s with as validation data and evaluate the variance of portfolio series in this period, the best is chosen to be the one that yields the smallest variance. Finally the shrinkage estimator is obtained using samples with and tuning parameter . With the allocation strategy for each of the estimators as the solution to (35), we construct portfolio for the next days and collect the returns. The procedure is repeated every days till the end and the variance of the portfolio constructed based on different estimators is calculated.

In the simulation, we choose and vary from to . Fig. 6 compares the variance (risk) of portfolio constructed based on different estimators, with one additional baseline portfolio constructed by equal investment in each asset. From the figure we can see shrinkage estimators achieves relatively better performance than the nonshrinkage ones.

VI Conclusion

In this work, we have given a rigorous proof for the existence and uniqueness of the regularized Tyler’s estimator proposed in [13], and justified the heuristic diagonal loading shrinkage estimator in [10] by KL divergence. Under the condition that samples are reasonably spread out, i.e., , or if the underlying distribution is continuous, the estimators have been shown to exist and unique (up to a positive scaling factor for Wiesel’s estimator). Algorithms based on the majorization-minimization framework have also been provided with guaranteed convergence. Finally we have discussed structure constrained estimation and have shown in the simulation that imposing such constraint helps improving estimation accuracy.

VII Appendix

VII-A Proof for Theorem 3

For the loss function

where the regularization term is written in general as . Define , for and , for as in Definition 2.

Define function

where is defined as the th row of with being the unitary matrix such that , , and , . The eigenvalues is arranged in descending order, i.e., , and denote the inverse of as , hence .

Denote the eigenvectors corresponding to as , the subspace spanned by as and with and . By definition, partition the whole space. Notice that by the assumption that no lies on the origin, we have and .

Partition the samples according to , is excluded hereafter, define function

and we have .

For the ’s, denote . For each , there exists some such that , since the ’s partition the whole space. Define to be the maximum index of that the ’s belongs to. Therefore we have and for .

We analyze the behavior of at the boundary of its feasible set , by Lemma 1, we only need to ensure , then there exists , and .

Consider the general case that some of the ’s go to zero, some remains bounded away from both and positive infinity, and the rests tend to positive infinity. Formally, define two integers and that , such that for , is bounded for and for . Denote some arbitrary small positive quantity by .

First we analyze the terms with . Consider the samples for some , then , which is . Since , we have . By definition

which implies , i.e., . Therefore, if , . For each we have

In the second step, we analyze the terms with . Consider the samples for some , we have shown that . Since , . Given that , by

Therefore for each we have

For the with being some constant, it is easy to see that , which does not affect the order of .

Now we have characterized the ’s, we move to the ’s. Since and for , by the same reasoning above, if and if . Therefore

with defined to be if the set is empty, and the same for .

We make the following assumption:

| (36) |

by the order hence , and base on the fact that

the order of is

and it goes to zero.

Now we simplify the assumption (36). Since and , and can take any value that satisfies , we end up with the following condition:

for all .

Define sets and , consider when , which means , by the definition of , is equivalent to , similarly for , which means , is equivalent to .

The condition should be valid for any and , tidy up the expression and let results in: for any proper subspace

where sets and are defined as , .

For the case , , which means no and some, not all , following the same reasoning gives condition

and for , , which means no and some, not all , gives condition

Notice that the above two conditions are included in the first one.

And finally under the scenario that all , it’s easy to see goes to zero if , and under the case that all , goes to zero if .

References

- [1] R. Maronna, D. Martin, and V. Yohai, Robust Statistics: Theory and Methods, ser. Wiley Series in Probability and Statistics. Wiley, 2006. [Online]. Available: http://books.google.com.hk/books?id=iFVjQgAACAAJ

- [2] P. Huber, Robust Statistics, ser. Wiley Series in Probability and Statistics - Applied Probability and Statistics Section Series. Wiley, 2004. [Online]. Available: http://books.google.com.hk/books?id=e62RhdqIdMkC

- [3] D. E. Tyler, “A distribution-free -estimator of multivariate scatter,” The Annals of Statistics, vol. 15, no. 1, pp. 234–251, 03 1987. [Online]. Available: http://dx.doi.org/10.1214/aos/1176350263

- [4] E. Ollila, H. Oja, and V. Koivunen, “Complex-valued ICA based on a pair of generalized covariance matrices,” Computational Statistics & Data Analysis, vol. 52, no. 7, pp. 3789 – 3805, 2008.

- [5] E. Ollila and V. Koivunen, “Influence function and asymptotic efficiency of scatter matrix based array processors: Case MVDR beamformer,” IEEE Transactions on Signal Processing, vol. 57, no. 1, pp. 247–259, Jan 2009.

- [6] E. Ollila and D. Tyler, “Distribution-free detection under complex elliptically symmetric clutter distribution,” in 2012 IEEE 7th Sensor Array and Multichannel Signal Processing Workshop (SAM), June 2012, pp. 413–416.

- [7] F. Pascal, Y. Chitour, J. Ovarlez, P. Forster, and P. Larzabal, “Covariance structure maximum-likelihood estimates in compound gaussian noise: Existence and algorithm analysis,” IEEE Transactions on Signal Processing, vol. 56, no. 1, pp. 34–48, Jan 2008.

- [8] A. Wiesel, “Geodesic convexity and covariance estimation,” Signal Processing, IEEE Transactions on, vol. 60, no. 12, pp. 6182–6189, Dec 2012.

- [9] E. Ollila, D. Tyler, V. Koivunen, and H. Poor, “Complex elliptically symmetric distributions: Survey, new results and applications,” Signal Processing, IEEE Transactions on, vol. 60, no. 11, pp. 5597–5625, Nov 2012.

- [10] Y. Abramovich and N. Spencer, “Diagonally loaded normalised sample matrix inversion (LNSMI) for outlier-resistant adaptive filtering,” in IEEE International Conference on Acoustics, Speech and Signal Processing, 2007. ICASSP 2007., vol. 3, 2007, pp. III–1105–III–1108.

- [11] O. Ledoit and M. Wolf, “A well-conditioned estimator for large-dimensional covariance matrices,” Journal of Multivariate Analysis, vol. 88, no. 2, pp. 365 – 411, 2004. [Online]. Available: http://www.sciencedirect.com/science/article/pii/S0047259X03000964

- [12] Y. Chen, A. Wiesel, and A. Hero, “Robust shrinkage estimation of high-dimensional covariance matrices,” IEEE Transactions on Signal Processing, vol. 59, no. 9, pp. 4097–4107, 2011.

- [13] A. Wiesel, “Unified framework to regularized covariance estimation in scaled Gaussian models,” IEEE Transactions on Signal Processing, vol. 60, no. 1, pp. 29–38, 2012.

- [14] F. Pascal, Y. Chitour, and Y. Quek, “Generalized robust shrinkage estimator and its application to STAP detection problem,” arXiv preprint arXiv:1311.6567, 2013.

- [15] R. A. Maronna, “Robust M-estimators of multivariate location and scatter,” The Annals of Statistics, vol. 4, no. 1, pp. pp. 51–67, 1976. [Online]. Available: http://www.jstor.org/stable/2957994

- [16] P. L. Davies, “Asymptotic behaviour of S-estimates of multivariate location parameters and dispersion matrices,” The Annals of Statistics, vol. 15, no. 3, pp. pp. 1269–1292, 1987. [Online]. Available: http://www.jstor.org/stable/2241828

- [17] S. Van Aelst and P. Rousseeuw, “Minimum volume ellipsoid,” Wiley Interdisciplinary Reviews: Computational Statistics, vol. 1, no. 1, pp. 71–82, 2009.

- [18] R. W. Butler, P. L. Davies, and M. Jhun, “Asymptotics for the minimum covariance determinant estimator,” The Annals of Statistics, vol. 21, no. 3, pp. 1385–1400, 09 1993. [Online]. Available: http://dx.doi.org/10.1214/aos/1176349264

- [19] P. J. Huber, “Robust estimation of a location parameter,” The Annals of Mathematical Statistics, vol. 35, no. 1, pp. 73–101, 03 1964. [Online]. Available: http://dx.doi.org/10.1214/aoms/1177703732

- [20] D. E. Tyler, “Statistical analysis for the angular central Gaussian distribution on the sphere,” Biometrika, vol. 74, no. 3, pp. 579–589, 1987. [Online]. Available: http://biomet.oxfordjournals.org/content/74/3/579.abstract

- [21] J. T. Kent and D. E. Tyler, “Maximum likelihood estimation for the wrapped cauchy distribution,” Journal of Applied Statistics, vol. 15, no. 2, pp. 247–254, 1988. [Online]. Available: http://www.tandfonline.com/doi/abs/10.1080/02664768800000029

- [22] G. Frahm, “Generalized elliptical distributions: theory and applications,” Ph.D. dissertation, Universität zu Köln, 2004.

- [23] J. T. Kent and D. E. Tyler, “Redescending -estimates of multivariate location and scatter,” The Annals of Statistics, vol. 19, no. 4, pp. 2102–2119, 12 1991. [Online]. Available: http://dx.doi.org/10.1214/aos/1176348388

- [24] M. Zhang, F. Rubio, D. Palomar, and X. Mestre, “Finite-sample linear filter optimization in wireless communications and financial systems,” IEEE Transactions on Signal Processing, vol. 61, no. 20, pp. 5014–5025, 2013.

- [25] S. Verdu, “Spectral efficiency in the wideband regime,” IEEE Transactions on Information Theory, vol. 48, no. 6, pp. 1319–1343, 2002.

- [26] T. M. Cover and J. A. Thomas, Elements of Information Theory. John Wiley & Sons, 2012.

- [27] D. R. Hunter and K. Lange, “A tutorial on MM algorithms,” The American Statistician, vol. 58, no. 1, pp. 30–37, 2004. [Online]. Available: http://amstat.tandfonline.com/doi/abs/10.1198/0003130042836

- [28] M. Razaviyayn, M. Hong, and Z. Luo, “A unified convergence analysis of block successive minimization methods for nonsmooth optimization,” SIAM Journal on Optimization, vol. 23, no. 2, pp. 1126–1153, 2013. [Online]. Available: http://epubs.siam.org/doi/abs/10.1137/120891009

- [29] T. Zhang, “A majorization-minimization algorithm for the karcher mean of positive definite matrices,” arXiv preprint arXiv:1312.4654, 2013.

- [30] R. Couillet and M. R. McKay, “Large dimensional analysis and optimization of robust shrinkage covariance matrix estimators,” arXiv preprint arXiv:1401.4083, 2014.