Discretization of Lévy semistationary processes with application to estimation

Abstract

Motivated by the construction of the Itô stochastic integral, we consider a step function method to discretize and simulate volatility modulated Lévy semistationary processes. Moreover, we assess the accuracy of the method with a particular focus on integrating kernels with a singularity at the origin. Using the simulation method, we study the finite sample properties of some recently developed estimators of realized volatility and associated parametric estimators for Brownian semistationary processes. Although the theoretical properties of these estimators have been established under high frequency asymptotics, it turns out that the estimators perform well also in a low frequency setting.

Keywords: Stochastic simulation, discretization, Lévy semistationary processes, stochastic volatility, estimation, finite sample properties.

2010 Mathematics Subject Classification: 65C05, 62M07 (primary), 62C07 (secondary)

1 Introduction

Barndorff-Nielsen and Schmiegel (2007) have recently introduced a general and flexible class of tempo-spatial random fields called ambit fields. These random fields have been applied in various areas, including modeling of tumour growth (Barndorff-Nielsen et al. (2007), Barndorff-Nielsen and Schmiegel (2007)), turbulence (Barndorff-Nielsen and Schmiegel (2003), Barndorff-Nielsen and Schmiegel (2009)) and finance (Barndorff-Nielsen et al. (2014), Barndorff-Nielsen et al. (2013)). For a general reference on the ambit stochastics framework, we refer to Barndorff-Nielsen et al. (2012).

In particular, attention has been given to a class of null-spatial ambit fields, Lévy semistationary () processes and their subclass of Brownian semistationary () processes. While these processes are typically neither Markovian nor semimartingales, they are naturally applicable to a wide range of fields including physics, biology and finance. An process is defined via a stochastic integral of a deterministic kernel function with respect to a driving Lévy process that is subject to volatility modulation. models provide a flexible, parsimonious and analytically tractable framework, which extends several well-known models, such as the Ornstein-Uhlenbeck (OU) model, continuous time autoregressive-moving-average (CARMA) processes, fractional Brownian motion and more, see e.g. Barndorff-Nielsen et al. (2013). In addition, the framework allows one to go beyond these familiar models and consider processes exhibiting non-standard features such as non-Markovianity, non-semimartingality and long-range dependence. Recently, models have succesfully been used in the modeling of electricity prices (Veraart and Veraart, 2014) whereas the sub-class of Brownian semistationary processes — i.e. processes driven by Brownian motion — have been used in the study of turbulence (Barndorff-Nielsen and Schmiegel, 2009) and of energy markets (Bennedsen et al., 2014). The generality and flexibility of the model together with promising early applications has prompted an increasing amount of interest and research in the theoretical properties of the model.

The strong correlations exhibited by the increments of a typical process cause the standard estimators of realized volatility introduced in the semimartingale framework to be inadequate. For this reason, Barndorff-Nielsen et al. (2009), Barndorff-Nielsen et al. (2011) and Barndorff-Nielsen et al. (2013) developed a theory of multipower variations (MPV) for processes which allowed Barndorff-Nielsen et al. (2013) to derive estimators of integrated volatility (IV) and of realized relative volatility (RRV), while parametric estimation in the model — in particular the estimation of the smoothness parameter — was developed by Barndorff-Nielsen et al. (2011) and Corcuera et al. (2013). These theoretical advances provide an important step towards applying -based models in practice. The theoretical underpinning of these estimators, however, relies on (high frequency) infill asymptotics, that is, on the assumption that the number of observations in a given interval approaches infinity. Naturally, this raises a question concerning the finite sample performance of these estimators — particularly relevant in applications where the number of observations can be relatively low, such as in (some areas of) finance and particularly in energy markets, where spot prices are observed daily. For this reason, we explore in this paper the finite sample properties of the aforementioned estimators in a low-frequency setting.

The contribution of this paper is twofold. First we present a thorough analysis of the natural method of simulating volatility modulated Lévy semistationary via discretizations inspired by the definition of the stochastic Itô integral. We highlight important features and pitfalls of the method with an emphasis on processes constructed using an integrating kernel with a singularity at the origin. Such processes are not semimartingales which affects the simulations significantly. To control the error that arises from the simulation scheme, we derive general estimates for the mean squared error of the simulated path and apply this to assess the error of our main example, where the integrating kernel is the so-called gamma kernel. Second, we analyze the finite-sample performance of various estimators and test statistics for processes based on power variations through a Monte Carlo study. In particular, we find that these methods perform well even with relatively few observations.

The paper is structured as follows. Section 2 introduces the process and its key properties, while Section 3 outlines a simple discretization and simulation scheme based on the step function approximation of the stochastic integral. Due to the process (possibly) being non-Markovian and a non-semimartingale, simulation can be time consuming and prone to error and we give examples of and recommendations for efficient and accurate simulation. Section 4 reviews the theory of power variations for processes and the associated estimators of the smoothness parameter and of integrated volatility before presenting the finite sample properties of these estimators. Section 5 concludes.

2 Lévy semistationary processes

We consider a filtered probability space satisfying the usual conditions of completeness and right continuity of the filtration, and a stochastic process defined on this space by

| (1) |

where is a constant, and are deterministic kernel functions such that for and are stochastic processes adapted to the filtration such that the integrals in (1) exists. We take to be a two-sided Lévy process on — that is, we take a Lévy process defined on and an independent copy of it, and define for and for The process in (1) is called a Lévy semistationary process; the name being derived from the fact that under suitable conditions, such as being stationary and independent of the resulting process will be (strictly) stationary. This is also the reason for the moving average type kernel and for starting the integration at minus infinity instead of at zero.

Stationarity is a desirable feature in a range of applications such as turbulence and commodity markets and (1) thus allows us to specify the model directly in stationarity as opposed to only achieving stationarity in the limit as which is the case for some other models, such as the OU process starting at a point The first integral in (1) is a Lebesgue integral and will pose no problems from a simulation standpoint and we will therefore only focus on the part coming from the second integral, that is, from now on we consider the driftless process

| (2) |

2.1 Autocorrelation structure

In the following we will make extensive use of the flexible autocorrelation structure that the model (2) provide. Assume for simplicity that has mean zero, is square integrable and that is stationary and independent of Now for all and, denoting we have for the covariance function

| (3) |

from which we see that the kernel function gives us control over the correlation function of the process. This allows us to capture, in a flexible way, a wide range of correlation structures inspired e.g. by theoretical or empirical considerations. An example of this is given in Section 3.4 where we show that for a particular choice of kernel function (3) gives rise to the well-known Matérn covariance function (Matérn, 1960) which is used in a variety of fields such as in machine learning and in the study of turbulence.

3 Simulation of Lévy semistationary processes

Consider the problem of simulating points of the process on an equidistant grid with step size The general simulation problem involves truncation and approximation of the integral and will be covered in Section 3.1 below, but consider first the (important) case of the process without stochastic volatility, i.e. where is a Brownian motion and volatility is constant, for all Now, the process in (2) is a mean zero Gaussian process with covariance given by (3). Denoting by the Toeplitz matrix arising from this covariance function we can obtain exact simulations of by drawing a -dimensional standard normal random vector and setting where is the Cholesky decomposition of

3.1 Discretizing the process

Although there do exist alternative schemes for simulating general processes (see Benth and Eyjolfsson (2013) and Benth et al. (2014)) we consider here the simpler route of a step function approximation of (2), which was also done by, e.g., Hedevang and Schmiegel (2013). To motivate this approach, write for

Now, if both and are approximately constant and equal to the left end point value on the intervals we get

| (4) |

where are the increments of the background driving Lévy process. Note that this approximation is quite natural as it is similar to the one used through simple (step) functions in the construction of the Itô integral in (2). Denoting and we now have

| (5) |

where denotes (discrete) convolution. In other words, given that the step function approximation is reasonable, the process is approximately a discrete convolution of the kernel function with the stochastic part consisting of the volatility process and the increments of the driving Lévy process, The upshot of the approximation (5) is that fast simulation becomes possible since most software packages come with extremely fast and efficient numerical methods for computing convolutions.111We used the MATLAB function fftconv available from the MATLAB Central which proved to be far superior in terms of a speed/accuracy trade-off as compared to the built-in MATLAB function conv. Further, these algorithms will not only output the simulated value of the process at a time point but will output the whole vector of desired values Appendix B contains a step-by-step routine for the simulations performed in this paper. Note, that in practice when simulating, we need to truncate the infinite sum (4) from below at a level for some see also the next section.

3.2 Controlling simulation error by subsampling

Unless we are in the Gaussian case of no stochastic volatility, we will naturally introduce error when simulating; both from the step function approximation as well as from the truncation of the sum at It is possible to derive some bounds on the errors introduced, which we consider in the following. Let be an approximation of where we have altered the kernel function and the stochastic volatility component in such a way as to make simulation of feasible. Now, for a given time the -error of the approximation is given by

where the constants are given by simply expanding the square and applying the stochastic Fubini theorem,

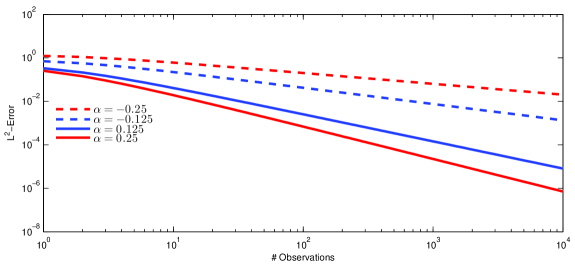

To recover the truncated step function approximation introduced in the previous section we let and where denotes the integer part of As an illustration, consider our main example, the gamma kernel with and Note, that for has a singularity at the origin and for will not be a semimartingale. To ease the exposition in deriving the following estimates on the error, we also assume that is a martingale (otherwise, the expression for will be more complicated). In this case we have

where we used equation (3.381.1) in Gradshteyn and Ryzhik (2007) and is the gamma function and the (lower) incomplete gamma function. In Figure 1 we see an illustration of how the error decreases when we increase the number of simulated points, in the interval The error estimates are done for (dashed lines) and (solid lines). We clearly see how the singularity of the integrating kernel at the origin for introduces a much higher -error in the simulations. Of course, it is possible to increase the number of simulated points until a desired level of accuracy is reached. For instance, if one is interested only in a fixed number of observations, say (which is the case in our finite sample investigations below), the solution to this problem is to sample at a very fine grid using a large number of observations for some and then subsample from these values to get the desired path with observations. That is, one picks out every -th observation from the simulated path consisting of points.

3.3 Illustration of simulations

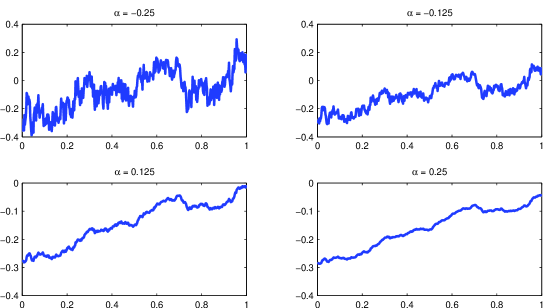

Consider a process with the gamma kernel, for and This kernel function has been shown to be useful in the study of turbulence in e.g. Corcuera et al. (2013) and in modelling electricity spot prices in Bennedsen et al. (2014). Note, that for the resulting process is neither a semimartingale nor Markovian. Also, for the process is a Lévy-driven Ornstein-Uhlenbeck (OU) process (so, our framework generalizes the popular OU models). Note further, that for the kernel has a singularity at which, as we shall see, significantly encumbers simulation due to the error illustrated in Figure 1. Figure 2 shows four simulated paths using for all with different values of . It is clear how the value of controls the smoothness of the process with large negative values of corresponding to a very rough path while positive values correspond to a smooth path.

3.4 Assessing the accuracy the simulations

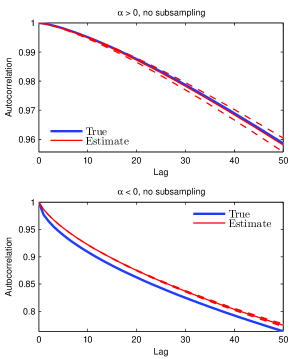

Using the correlation function (3) derived in Section 2.1 we can check how our simulations perform in terms of how they capture the second order structure of the target theoretical process to be approximated. As an illustration, consider again the process with a gamma kernel Supposing to be stationary and using equations (3.383.8), (8.331.1) and (8.335.1) in Gradshteyn and Ryzhik (2007), we find the variance of the process to be and the correlations to be given by the Matérn correlation function (Matérn (1960), Handcock and Stein (1993))

where is the modified Bessel function of the third kind. Figure 3 provides examples of how to assess the accuracy of the simulations and how problems arise when using a kernel with a singularity at the origin: the top plots are with while the bottom plots are with The two left plots are using the simulation algorithm without subsampling while we in the right plots simulate times as many time points as needed (i.e. ) and then subsample the desired time points from this path. The result is an accurate second order structure as can be seen from the bottom right figure. The remaining parameters in the simulation are and the stochastic volatility is the exponential of a Gaussian Ornstein-Uhlenbeck process, where and is a standard Brownian motion independent of

4 Application: estimation of processes

The following asymptotic results are valid only for processes, i.e. when in (2) is a Brownian motion and we will from now on work with this process. Analogous research in the general framework is ongoing. We note that the results also hold for processes with drift as in (1), assuming some smoothness conditions of the drift term, see Corcuera et al. (2013). In Section 4.2 we present the estimator of the smoothness parameter, , developed in Barndorff-Nielsen et al. (2011) and in Section 4.3 we present the estimator of the RRV together with a test for the presence of stochastic volatility in our process, developed in Barndorff-Nielsen et al. (2013), followed by a study of their finite sample properties.

4.1 Simulation setup

In what follows, we assume that where is a slowly varying function at i.e. for all In other words, we require that behaves as at This condition is obviously fulfilled for our main example, the gamma kernel, which we will use when simulating below. When a stochastic volatility component is present in the simulations, we specify this as the exponential of a Gaussian Ornstein-Uhlenbeck process, where and is a standard Brownian motion possibly correlated with This process is Gaussian and Markovian and can thus be simulated in an exact way incurring no simulation error using the recursion

where See e.g. Glasserman (2003) Section 3.3.1.

4.2 Estimation of the smoothness parameter

The parameter is called the smoothness parameter since it controls the small scale behavior of the paths of the process For , will exhibit very rough paths, while for they will be smooth whereas corresponds to paths of a process driven by a Brownian motion, see Figure 2 for examples. This behavior of the process for varying the value of is analogous to the role that the Hurst exponent plays for the fractional Brownian motion (fBm) and the small scale behavior of the process is actually similar to that of the fBm where the link between the smoothness parameter and the Hurst exponent, is given by See e.g. Nualart (2006) for more information about Hurst exponents and their connection to the fractional Brownian motion.

To estimate , let and suppose we have observed the process on an equidistant grid with grid size for all Define the second order differences at frequency to be For we also define the associated p’th power variations

Now, as proved in Barndorff-Nielsen et al. (2011), see also Corcuera et al. (2013), we have the following asymptotic result for the change of frequency (COF) estimator

as where ”ucp” means uniform convergence in probability on compact sets.

Remark 1.

This kind of asymptotics is known as infill asymptotics, i.e. we consider the time fixed and let the number of observations in go to infinity so that the time between successive observations, goes to zero.

Our estimator of the smoothness parameter, , thus becomes

| (6) |

and we have as for all The estimator (6) is a feasible estimator in the sense that it only depends on the observed data,

In addition to the estimator of , Corcuera et al. (2013) provide an associated central limit theorem for :

| (7) |

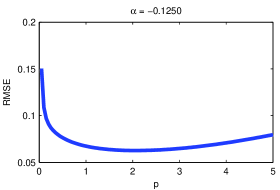

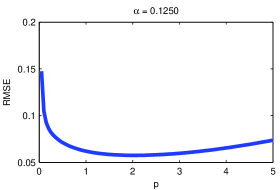

where and is a 2-by-2 matrix depending on . These results require a choice for the exponent, used in the calculations of the power variations, the standard choice being yielding squared returns in the power variations, and we will also do this here. In Figure 4 we see a justification of this as the root mean squared error of the estimator of in (6) is minimized for Furthermore, the entries of are continuous as a function of , which justifies the use of as an estimator of when using (7), see Appendix A where we also give the specific form of

Remark 2.

We can use the above estimator of to test the degree of smoothness of the paths as described above. In particular, we can test whether or not a process is a semimartingale by testing the null hypothesis In the specific case of the gamma kernel, this test can be used to decide whether the model can be reduced to the familiar Ornstein-Uhlenbeck model. We investigate the finite sample properties of this test in Section 4.2.1.

Remark 3.

Equation (7) specifies a CLT only for It is possible to extend the region to include by using gaps in sampling our observed process see Corcuera et al. (2013). This will, however, cause us to throw away some of the observations of leaving us with a sparser sample and ignoring some information and we will not pursue this in the present paper.

4.2.1 Finite sample properties concerning the COF estimator

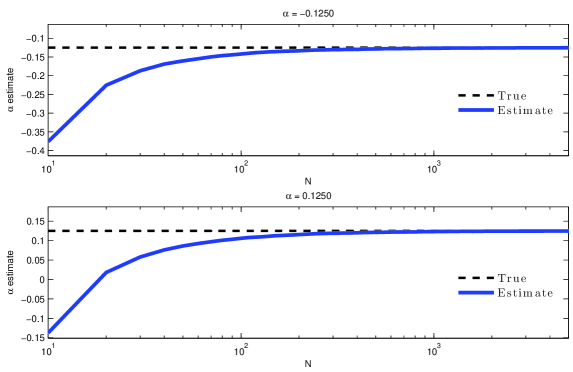

We now proceed to apply the discretization scheme of Section 3 to investigate the finite sample properties of the asymptotic results described above. That is, we consider how the Law of Large numbers (6) and Central Limit Theorem (7) of the COF estimator behave when the number of observations is finite, i.e. when we only observe the process on a discrete grid of finite length. In Tables 1-4 we see investigations of how the COF estimator of fares for a differing number of observations in the interval 20,000 Monte Carlo simulations have been done using the gamma kernel with and in three different regimes: (A) no stochastic volatility, (B) including stochastic volatility and (C) including stochastic volatility correlated with the driving Brownian motion of the process (this phenomenon is termed leverage in the finance literature). Table 1 shows that the COF estimator works satisfactorily when the number of observations are greater than 200, yielding a bias of the order and a root mean squared error (RMSE) of around We note two further things. Firstly, the bias that is incurred for small values of are in all cases negative and we conclude that the estimator is biased downwards in small samples. This is corroborated by Figure 5 where we see how the (absolute value of the) bias of the estimator decreases when increasing the number of observations of the process ; for small values of the estimator is severely biased downwards but as we increase the number of observations this bias vanishes. Secondly, we see that the bias and RMSE do not seem to depend on the particular regime we are in, from which we conclude that the estimator is robust to the presence of stochastic volatility and correlation effects between the stochastic volatility component and the driving noise Next, Tables 2-4 investigate the CLT of the COF estimator in the three regimes by testing the null hypothesis for and various values of the true used in the simulation of the process. Again we see that for values around the size of the test is satisfactory with a small upward size distortion (middle column) of the order The power of the test (non-middle columns), however, suffers for values of close to the true value unless we have many observations. We also tried varying the other parameters involved i.e. and the stochastic volatility parameter but this had basically no effect on the COF estimator. For the sake of brevity these results are not reported here but are available from the authors upon request.

| Panel A: constant volatility | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| N | Bias | RMSE | Bias | RMSE | Bias | RMSE | Bias | RMSE | Bias | RMSE |

| Panel B: stochastic volatility | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| N | Bias | RMSE | Bias | RMSE | Bias | RMSE | Bias | RMSE | Bias | RMSE |

| Panel C: stochastic volatility correlated with the driving noise | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| N | Bias | RMSE | Bias | RMSE | Bias | RMSE | Bias | RMSE | Bias | RMSE |

Bias and root mean squared error of the estimator of for varying values of true and in the three regimes; no stochastic volatility (Panel A), including stochastic volatility (Panel B) and including stochastic volatility which is also correlated with the driving noise of the process (Panel C). Monte Carlo simulations.

| Panel A: | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| True value of | |||||||||

| N | |||||||||

| 20 | 0.333 | 0.252 | 0.154 | 0.125 | 0.103 | 0.088 | 0.075 | 0.085 | 0.143 |

| 50 | 0.518 | 0.311 | 0.159 | 0.099 | 0.074 | 0.063 | 0.082 | 0.189 | 0.408 |

| 100 | 0.755 | 0.468 | 0.199 | 0.103 | 0.059 | 0.063 | 0.119 | 0.384 | 0.738 |

| 200 | 0.954 | 0.720 | 0.263 | 0.107 | 0.053 | 0.090 | 0.216 | 0.707 | 0.970 |

| 500 | 1.000 | 0.967 | 0.530 | 0.198 | 0.057 | 0.156 | 0.496 | 0.979 | 1.000 |

| 1000 | 1.000 | 0.999 | 0.799 | 0.300 | 0.047 | 0.278 | 0.806 | 1.000 | 1.000 |

| 2000 | 1.000 | 1.000 | 0.973 | 0.530 | 0.055 | 0.498 | 0.980 | 1.000 | 1.000 |

| Panel B: | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| True value of | |||||||||

| N | |||||||||

| 20 | 0.373 | 0.250 | 0.165 | 0.129 | 0.101 | 0.076 | 0.068 | 0.084 | 0.139 |

| 50 | 0.556 | 0.339 | 0.175 | 0.099 | 0.067 | 0.061 | 0.073 | 0.200 | 0.450 |

| 100 | 0.798 | 0.508 | 0.201 | 0.099 | 0.057 | 0.064 | 0.120 | 0.409 | 0.795 |

| 200 | 0.969 | 0.751 | 0.283 | 0.129 | 0.055 | 0.076 | 0.231 | 0.730 | 0.981 |

| 500 | 1.000 | 0.980 | 0.559 | 0.197 | 0.062 | 0.160 | 0.527 | 0.990 | 1.000 |

| 1000 | 1.000 | 1.000 | 0.828 | 0.323 | 0.049 | 0.275 | 0.838 | 1.000 | 1.000 |

| 2000 | 1.000 | 1.000 | 0.981 | 0.555 | 0.049 | 0.533 | 0.986 | 1.000 | 1.000 |

| Panel C: | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| True value of | |||||||||

| N | |||||||||

| 20 | 0.385 | 0.268 | 0.171 | 0.132 | 0.094 | 0.086 | 0.068 | 0.077 | 0.146 |

| 50 | 0.605 | 0.371 | 0.169 | 0.113 | 0.064 | 0.067 | 0.078 | 0.225 | 0.455 |

| 100 | 0.825 | 0.534 | 0.201 | 0.098 | 0.063 | 0.069 | 0.123 | 0.447 | 0.819 |

| 200 | 0.979 | 0.777 | 0.334 | 0.131 | 0.056 | 0.086 | 0.249 | 0.775 | 0.987 |

| 500 | 1.000 | 0.988 | 0.594 | 0.217 | 0.054 | 0.191 | 0.561 | 0.993 | 1.000 |

| 1000 | 1.000 | 1.000 | 0.864 | 0.358 | 0.054 | 0.312 | 0.872 | 1.000 | 1.000 |

| 2000 | 1.000 | 1.000 | 0.990 | 0.588 | 0.052 | 0.589 | 0.994 | 1.000 | 1.000 |

Simulations of the test at a nominal level of for (Panel A), (Panel B), (Panel C) and varying values of the true Numbers are rejection rates of the null when simulating the underlying process using the value of given in the top row; thus mid columns correspond to the size of the test while non-mid columns correspond to power. Simulations are with constant volatility, for all and with Monte Carlo simulations.

| Panel A: | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| True value of | |||||||||

| N | |||||||||

| 20 | 0.251 | 0.201 | 0.139 | 0.114 | 0.095 | 0.080 | 0.069 | 0.095 | 0.142 |

| 50 | 0.334 | 0.243 | 0.140 | 0.098 | 0.073 | 0.069 | 0.077 | 0.169 | 0.363 |

| 100 | 0.493 | 0.329 | 0.146 | 0.086 | 0.057 | 0.072 | 0.119 | 0.335 | 0.676 |

| 200 | 0.734 | 0.514 | 0.213 | 0.100 | 0.056 | 0.086 | 0.194 | 0.602 | 0.917 |

| 500 | 0.973 | 0.859 | 0.382 | 0.140 | 0.047 | 0.135 | 0.402 | 0.937 | 1.000 |

| 1000 | 1.000 | 0.988 | 0.624 | 0.196 | 0.049 | 0.244 | 0.717 | 0.999 | 1.000 |

| 2000 | 1.000 | 1.000 | 0.891 | 0.380 | 0.049 | 0.445 | 0.940 | 1.000 | 1.000 |

| Panel B: | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| True value of | |||||||||

| N | |||||||||

| 20 | 0.302 | 0.215 | 0.150 | 0.121 | 0.093 | 0.074 | 0.064 | 0.087 | 0.143 |

| 50 | 0.450 | 0.290 | 0.159 | 0.103 | 0.079 | 0.069 | 0.082 | 0.174 | 0.391 |

| 100 | 0.647 | 0.411 | 0.172 | 0.090 | 0.055 | 0.066 | 0.113 | 0.367 | 0.712 |

| 200 | 0.868 | 0.625 | 0.248 | 0.113 | 0.060 | 0.083 | 0.201 | 0.630 | 0.941 |

| 500 | 0.999 | 0.934 | 0.468 | 0.175 | 0.049 | 0.136 | 0.436 | 0.948 | 1.000 |

| 1000 | 1.000 | 0.997 | 0.718 | 0.240 | 0.047 | 0.251 | 0.752 | 0.999 | 1.000 |

| 2000 | 1.000 | 1.000 | 0.948 | 0.451 | 0.052 | 0.446 | 0.955 | 1.000 | 1.000 |

| Panel C: | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| True value of | |||||||||

| N | |||||||||

| 20 | 0.452 | 0.361 | 0.246 | 0.164 | 0.099 | 0.080 | 0.069 | 0.084 | 0.138 |

| 50 | 0.696 | 0.514 | 0.333 | 0.171 | 0.077 | 0.069 | 0.081 | 0.185 | 0.394 |

| 100 | 0.882 | 0.724 | 0.469 | 0.186 | 0.059 | 0.067 | 0.121 | 0.393 | 0.739 |

| 200 | 0.992 | 0.935 | 0.686 | 0.272 | 0.057 | 0.088 | 0.207 | 0.667 | 0.955 |

| 500 | 1.000 | 1.000 | 0.969 | 0.521 | 0.051 | 0.141 | 0.460 | 0.965 | 1.000 |

| 1000 | 1.000 | 0.998 | 0.758 | 0.271 | 0.046 | 0.273 | 0.788 | 1.000 | 1.000 |

| 2000 | 1.000 | 1.000 | 1.000 | 0.964 | 0.057 | 0.469 | 0.968 | 1.000 | 1.000 |

Simulations of the test at a nominal level of for (Panel A), (Panel B), (Panel C) and varying values of the true Numbers are rejection rates of the null when simulating the underlying process using the value of given in the top row; thus mid columns correspond to the size of the test while non-mid columns correspond to power. Simulations are with stochastic volatility with parameter and Monte Carlo simulations.

| Panel A: | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| True value of | |||||||||

| N | |||||||||

| 20 | 0.256 | 0.202 | 0.138 | 0.114 | 0.097 | 0.075 | 0.070 | 0.089 | 0.144 |

| 50 | 0.342 | 0.246 | 0.143 | 0.102 | 0.075 | 0.070 | 0.082 | 0.172 | 0.367 |

| 100 | 0.484 | 0.330 | 0.153 | 0.095 | 0.060 | 0.065 | 0.112 | 0.337 | 0.673 |

| 200 | 0.736 | 0.525 | 0.209 | 0.104 | 0.059 | 0.085 | 0.195 | 0.600 | 0.924 |

| 500 | 0.981 | 0.863 | 0.386 | 0.142 | 0.052 | 0.142 | 0.425 | 0.945 | 1.000 |

| 1000 | 0.999 | 0.988 | 0.628 | 0.203 | 0.051 | 0.255 | 0.719 | 1.000 | 1.000 |

| 2000 | 1.000 | 1.000 | 0.894 | 0.376 | 0.056 | 0.453 | 0.945 | 1.000 | 1.000 |

| Panel B: | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| True value of | |||||||||

| N | |||||||||

| 20 | 0.296 | 0.223 | 0.148 | 0.117 | 0.093 | 0.076 | 0.070 | 0.093 | 0.139 |

| 50 | 0.450 | 0.298 | 0.155 | 0.106 | 0.077 | 0.067 | 0.082 | 0.174 | 0.385 |

| 100 | 0.642 | 0.409 | 0.181 | 0.101 | 0.055 | 0.063 | 0.117 | 0.366 | 0.718 |

| 200 | 0.872 | 0.629 | 0.242 | 0.114 | 0.063 | 0.084 | 0.203 | 0.632 | 0.947 |

| 500 | 0.999 | 0.940 | 0.473 | 0.171 | 0.050 | 0.145 | 0.438 | 0.955 | 1.000 |

| 1000 | 1.000 | 0.995 | 0.722 | 0.254 | 0.047 | 0.275 | 0.747 | 1.000 | 1.000 |

| 2000 | 1.000 | 1.000 | 0.948 | 0.448 | 0.051 | 0.455 | 0.956 | 1.000 | 1.000 |

| Panel C: | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| True value of | |||||||||

| N | |||||||||

| 20 | 0.354 | 0.249 | 0.164 | 0.126 | 0.096 | 0.080 | 0.071 | 0.084 | 0.134 |

| 50 | 0.523 | 0.335 | 0.169 | 0.117 | 0.076 | 0.067 | 0.081 | 0.179 | 0.404 |

| 100 | 0.728 | 0.461 | 0.191 | 0.102 | 0.057 | 0.070 | 0.122 | 0.393 | 0.741 |

| 200 | 0.935 | 0.692 | 0.271 | 0.119 | 0.058 | 0.088 | 0.216 | 0.662 | 0.965 |

| 500 | 1.000 | 0.970 | 0.516 | 0.191 | 0.053 | 0.148 | 0.469 | 0.971 | 1.000 |

| 1000 | 1.000 | 0.998 | 0.768 | 0.281 | 0.046 | 0.288 | 0.784 | 1.000 | 1.000 |

| 2000 | 1.000 | 1.000 | 0.964 | 0.500 | 0.056 | 0.479 | 0.971 | 1.000 | 1.000 |

Simulations of the test at a nominal level of for (Panel A), (Panel B), (Panel C) and varying values of the true Numbers are rejection rates of the null when simulating the underlying process using the value of given in the top row; thus mid columns correspond to the size of the test while non-mid columns correspond to power. Simulations are including stochastic volatility correlated with the driving process of the process. The stochastic volatility parameter is and the correlation coefficient Monte Carlo simulations.

Next we investigate how the estimator performs when the number of total observations are fixed but the sampling frequency varies. Recall, that the COF estimator relies on infill asymptotics, hence a low sampling frequency could potentially be harmful to the performance. Therefore we perform simulations where the number of observations are held fixed at but the process is observed over the time period for various values of and thus different values for the step size of the observation grid, ; large corresponds to a large step size between succesive observations, i.e. to sampling at a low frequency. We present results using simulations with various step sizes ranging from to The results are shown in Table 5 where we see that for large values of the parameter the estimator suffers when the step size, is also large: the estimated values of become biased downwards. For low values of either or the performance is good — in particular we conclude that the departures from the infill regime is not crucial as long as the parameter is not too large.

| Panel A: | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Bias | RMSE | Bias | RMSE | Bias | RMSE | Bias | RMSE | Bias | RMSE | |

| 1.00 | ||||||||||

| 0.50 | ||||||||||

| 0.20 | ||||||||||

| 0.10 | ||||||||||

| 0.05 | ||||||||||

| 0.02 | ||||||||||

| Panel B: | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Bias | RMSE | Bias | RMSE | Bias | RMSE | Bias | RMSE | Bias | RMSE | |

| 1.00 | ||||||||||

| 0.50 | ||||||||||

| 0.20 | ||||||||||

| 0.10 | ||||||||||

| 0.05 | ||||||||||

| 0.02 | ||||||||||

| Panel C: | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Bias | RMSE | Bias | RMSE | Bias | RMSE | Bias | RMSE | Bias | RMSE | |

| 1.00 | ||||||||||

| 0.50 | ||||||||||

| 0.20 | ||||||||||

| 0.10 | ||||||||||

| 0.05 | ||||||||||

| 0.02 | ||||||||||

Investigation of the bias incurred when the process is sampled infrequently. The number of observations is held fixed at but the step size between successive observations varies. 20,000 Monte Carlo simulations.

4.3 Estimating integrated volatility

Here we follow Barndorff-Nielsen et al. (2013) and present an estimator of the integrated ’th power of the volatility process, and show how we can use this to test for the presence of stochastic volatility in the process In particular, we want to test a hypothesis of the type

| (8) | ||||

where

It is well known, see e.g. Barndorff-Nielsen et al. (2006), that if is a semimartingale, then as with as above. However, this does not hold when is not a semimartingale as is the case when To remedy this, we introduce the Gaussian core of the process, and define the normalization factor Now, as shown in Barndorff-Nielsen et al. (2011) we have

| (9) |

as (see also Barndorff-Nielsen and Schmiegel (2009) for the first results of this type with This estimator, however, is infeasible since we in general do not know the functional form of and/or its parameters, and hence we do not know For this reason Barndorff-Nielsen et al. (2013) introduce the realized relative power variation (RRV) over by for If (9) holds, then

| (10) |

uniformly in as Under some technical conditions Barndorff-Nielsen et al. (2013) also provide a feasible central limit theorem for Let

For any we have

| (11) |

as is a constant depending on and the form of which is given in Appendix A.

The RRV of equation (10) measures the amount of accumulated volatility in compared to the total accumulated volatility in and equation (11) can be used to construct confidence intervals for which allows us to test the null hypothesis that is a constant process, i.e. that there is no time varying volatility present in the process. We want to test this hypothesis, that is (8) above. Under the null, we have and therefore

| (12) |

where denotes stable convergence, see Rényi (1963) or Jacod and Shiryaev (2002) page 512 for information on this type of convergence. The right hand side of (12) is a Brownian bridge and we utilize this to construct the hypothesis test (8) by examining the distance between the empirical quantities and on the left hand side of (12) and compare it with the critical values of the limiting distribution, i.e. the distribution of the distance of the properly scaled Brownian bridge in (12). The question becomes, which distance metric to use, as different choices will lead to different distributions of the right hand side. Two obvious choices are the -distance and the -distance, yielding respectively the Cramér–von Mises distribution and the Kolmogorov-Smirnov distribution. Another choice would be the distance, although this causes the limiting distribution to be non-standard (involving the Airy function).

4.3.1 Finite sample properties of the test for constant volatility

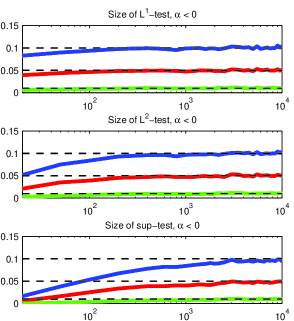

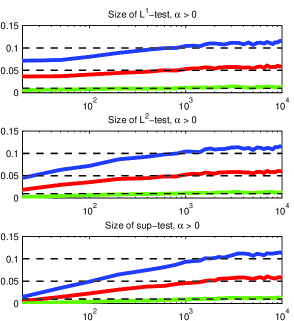

We explore now the finite sample properties of the test for constant volatillity, (8), in the process by studying the convergence in (12). In particular, we consider the size and power of the null of constant volatility using the -, - and -metrics respectively. Table 6 shows the size of the test, i.e. rejection rates of the null when simulating under the null, that is when is a constant process. We consider different values of the smoothness parameter to investigate its effect on the test — we similarly varied but this had practically no impact on the results, which is therefore not reported. An illustration of what is seen in the table is also given in Figure 6 where we plot the size of the test against the number of observations for the three different metrics. We see, that for (left plots) the size of the -based test is already quite accurate for around observations while the test needs around observations to achieve a size around the nominal value. The -test performs markedly worse needing about observations to reach the same accuracy as the two other tests. For (right plots) the relative picture between the tests is the same but the absolute picture is different: all tests need many more observations to achieve accurate sizes and even then the tests display a slight upwards size distortion. For instance it seems that the test needs around observations in this case.

Tables 7 and 8 show the power of the test, i.e. rejection rates of the null when simulating under the alternative when stochastic volatility is present in the process Simulations are presented for negative and postive values of respectively and for varying values of the stochastic volatility parameter — we refer to Section 4.1 for the details on simulating the stochastic volatility process. Using the log-normality of we have that and so that small values of correspond to a large variance (and variance of variance) of and vice versa. Also, the half-life of is so that low values of correspond to long half-lives (higher persistence) of the volatility of In the tables we see what we would expect: lower (higher volatility of ) results in greater power when testing the null of constant volatility. Although the tests do show some sensitivity to the level of stochastic volatility, the power is not affected that much; Panel A () corresponds to a mean of of while Panel C () corresponds to a mean of about and in light of this, the differences in the size of the tests seem rather small. Additionally, comparing the two tables, we see that the power of this test is not effected by the sign of ; the two tables — which are for and respectively — display similar numerical values accross the board. Lastly, it is worth mentioning that the three tests all display good power in finite samples with around power with observations. The test has a downward bias in size for small numbers of observations and, as expected, it has higher power than the two other tests, leading us to believe that the test rejects more often overall as compared to the two other tests. Looking closer at the tables and Figure 6, we conclude from size/power considerations that the -test is inferior to and tests, which perform almost exactly alike. Given that the test is based on the standard Cramér–von Mises distribution, which is widely implemented in statistical software, we recommend using the -metric when testing the null hypothesis of constant volatility in the path of a process.

| Panel A: | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| N | |||||||||

| Panel B: | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| N | |||||||||

| Panel C: | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| N | |||||||||

Size of the test for all with (Panel A), (Panel B) and (Panel C) and the three metrics and Nominal sizes shown in top row are and and Monte Carlo simulations.

| Panel A: | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| N | 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 |

| 50 | 0.540 | 0.451 | 0.299 | 0.545 | 0.460 | 0.308 | 0.484 | 0.401 | 0.258 |

| 100 | 0.747 | 0.670 | 0.533 | 0.755 | 0.690 | 0.550 | 0.729 | 0.663 | 0.533 |

| 200 | 0.880 | 0.825 | 0.715 | 0.886 | 0.842 | 0.741 | 0.883 | 0.840 | 0.753 |

| 500 | 0.965 | 0.944 | 0.887 | 0.969 | 0.953 | 0.906 | 0.970 | 0.958 | 0.922 |

| 1000 | 0.989 | 0.979 | 0.949 | 0.990 | 0.982 | 0.960 | 0.991 | 0.987 | 0.973 |

| 2000 | 0.998 | 0.996 | 0.987 | 0.999 | 0.996 | 0.991 | 0.999 | 0.996 | 0.993 |

| Panel B: | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| N | 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 |

| 50 | 0.523 | 0.423 | 0.274 | 0.528 | 0.436 | 0.281 | 0.460 | 0.380 | 0.231 |

| 100 | 0.733 | 0.650 | 0.506 | 0.748 | 0.664 | 0.535 | 0.716 | 0.642 | 0.513 |

| 200 | 0.864 | 0.811 | 0.702 | 0.875 | 0.830 | 0.727 | 0.876 | 0.831 | 0.741 |

| 500 | 0.966 | 0.942 | 0.881 | 0.972 | 0.953 | 0.901 | 0.974 | 0.963 | 0.918 |

| 1000 | 0.985 | 0.977 | 0.951 | 0.986 | 0.981 | 0.962 | 0.989 | 0.986 | 0.970 |

| 2000 | 0.998 | 0.990 | 0.982 | 0.998 | 0.995 | 0.986 | 0.999 | 0.998 | 0.990 |

| Panel C: | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| N | 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 |

| 50 | 0.341 | 0.234 | 0.121 | 0.329 | 0.239 | 0.121 | 0.272 | 0.190 | 0.096 |

| 100 | 0.503 | 0.393 | 0.226 | 0.524 | 0.417 | 0.259 | 0.484 | 0.391 | 0.254 |

| 200 | 0.706 | 0.606 | 0.435 | 0.729 | 0.626 | 0.469 | 0.715 | 0.635 | 0.483 |

| 500 | 0.898 | 0.828 | 0.693 | 0.905 | 0.850 | 0.733 | 0.915 | 0.870 | 0.774 |

| 1000 | 0.965 | 0.935 | 0.855 | 0.972 | 0.946 | 0.882 | 0.982 | 0.960 | 0.915 |

| 2000 | 0.993 | 0.980 | 0.941 | 0.994 | 0.987 | 0.954 | 0.997 | 0.992 | 0.976 |

Power of the test for all for (Panel A), (Panel B) and (Panel C), where we simulate the stochastic volatility process under the alternative hypothesis as see Section 4.1. and we consider the three metrics and Monte Carlo simulations.

| Panel A: | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| N | 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 |

| 50 | 0.495 | 0.417 | 0.265 | 0.499 | 0.428 | 0.285 | 0.441 | 0.364 | 0.234 |

| 100 | 0.699 | 0.625 | 0.493 | 0.712 | 0.645 | 0.516 | 0.676 | 0.618 | 0.491 |

| 200 | 0.850 | 0.802 | 0.688 | 0.857 | 0.817 | 0.715 | 0.855 | 0.812 | 0.725 |

| 500 | 0.964 | 0.944 | 0.882 | 0.968 | 0.954 | 0.904 | 0.968 | 0.956 | 0.919 |

| 1000 | 0.988 | 0.979 | 0.950 | 0.990 | 0.980 | 0.960 | 0.992 | 0.987 | 0.972 |

| 2000 | 0.998 | 0.996 | 0.986 | 0.999 | 0.997 | 0.990 | 0.999 | 0.998 | 0.992 |

| Panel B: | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| N | 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 |

| 50 | 0.470 | 0.384 | 0.251 | 0.472 | 0.394 | 0.253 | 0.421 | 0.339 | 0.207 |

| 100 | 0.682 | 0.611 | 0.470 | 0.703 | 0.627 | 0.488 | 0.666 | 0.598 | 0.469 |

| 200 | 0.838 | 0.787 | 0.672 | 0.855 | 0.803 | 0.690 | 0.845 | 0.804 | 0.702 |

| 500 | 0.967 | 0.944 | 0.876 | 0.971 | 0.951 | 0.896 | 0.970 | 0.959 | 0.919 |

| 1000 | 0.986 | 0.978 | 0.951 | 0.988 | 0.981 | 0.959 | 0.991 | 0.986 | 0.973 |

| 2000 | 0.998 | 0.991 | 0.981 | 0.999 | 0.995 | 0.985 | 1.000 | 0.999 | 0.992 |

| Panel C: | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| N | 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 | 0.10 | 0.05 | 0.01 |

| 50 | 0.297 | 0.209 | 0.104 | 0.288 | 0.216 | 0.113 | 0.232 | 0.172 | 0.086 |

| 100 | 0.478 | 0.377 | 0.208 | 0.496 | 0.396 | 0.242 | 0.454 | 0.373 | 0.235 |

| 200 | 0.687 | 0.590 | 0.413 | 0.703 | 0.617 | 0.445 | 0.688 | 0.610 | 0.456 |

| 500 | 0.901 | 0.836 | 0.690 | 0.907 | 0.859 | 0.731 | 0.918 | 0.875 | 0.769 |

| 1000 | 0.966 | 0.931 | 0.851 | 0.972 | 0.944 | 0.879 | 0.977 | 0.960 | 0.915 |

| 2000 | 0.992 | 0.981 | 0.943 | 0.994 | 0.988 | 0.954 | 0.996 | 0.992 | 0.976 |

Power of the test for all for (Panel A), (Panel B) and (Panel C), where we simulate the stochastic volatility process under the alternative hypothesis as see Section 4.1. and we consider the three metrics and Monte Carlo simulations.

5 Conclusion

We have presented a fast and simple simulation scheme for Lévy semistationary processes and analysed the error arising from the scheme. While, a part of the error obviously stems from the truncation of the integral towards minus infinity, a more pronounced error ensues from the step function approximation when the integrating kernel has a singularity at the origin. The singularity causes the process to be a non-semimartingale and we saw in Section 3.2 how this impacts the error in the simulations. In Section 3.4 we saw an illustration of how to remedy this by sampling the process on a finer grid and then subsampling to get the desired path.

After providing an illustration of the simulations and the error using our main example, the gamma kernel, we applied the simulation scheme to investigate the finite sample properties of two recently developed estimators based on power variations of Brownian semistationary processes. This paper marks the first time that these estimators have been investigated in a finite sample regime and we saw that despite the infill nature of their asymptotics, the estimators performed satisfactorily when one has about observations per time unit We also saw, however, that one must take caution when sampling the process infrequently; in this case, large values of the parameter will cause the estimator of to be downward biased.

Acknowledgements

The research has been supported by CREATES (DNRF78), funded by the Danish National Research Foundation, by Aarhus University Research Foundation (project “Stochastic and Econometric Analysis of Commodity Markets”) and by the Academy of Finland (project 258042). We would also like to thank Emil Hedevang for useful help and discussions regarding simulation of processes.

References

- Barndorff-Nielsen et al. (2007) Barndorff-Nielsen, O., E. Jensen, K.Ý.Jónsdóttir, and J. Schmiegel (2007). Spatio-temporal modelling — with a view to biological growth. In B. Finkenstädt, L. Held, and V. Isham (Eds.), Statistical Methods for Spatio-Temporal Systems, pp. 47–75. London: Chapman and Hall/CRC.

- Barndorff-Nielsen and Schmiegel (2003) Barndorff-Nielsen, O. and J. Schmiegel (2003). Lévy-based tempo-spatial modelling, with applications to turbulence. Russian Math. Surveys 59(1), 65–90.

- Barndorff-Nielsen et al. (2012) Barndorff-Nielsen, O. E., F. E. Benth, and A. E. D. Veraart (2012). Recent advances in ambit stochastics with a view towards tempo-spatial stochastic volatility/intermittency. Working paper.

- Barndorff-Nielsen et al. (2013) Barndorff-Nielsen, O. E., F. E. Benth, and A. E. D. Veraart (2013). Modelling energy spot prices by volatility modulated Lévy-driven Volterra processes. Bernoulli 19(3), 803–845.

- Barndorff-Nielsen et al. (2014) Barndorff-Nielsen, O. E., F. E. Benth, and A. E. D. Veraart (2014). Modelling electricity forward markets by ambit fields. Adv. Appl. Probab. 46(3), to appear.

- Barndorff-Nielsen et al. (2009) Barndorff-Nielsen, O. E., J. M. Corcuera, and M. Podolskij (2009). Power variation for Gaussian processes with stationary increments. Stochastic Process. Appl. 119(6), 1845–1865.

- Barndorff-Nielsen et al. (2011) Barndorff-Nielsen, O. E., J. M. Corcuera, and M. Podolskij (2011). Multipower variation for Brownian semistationary processes. Bernoulli 17(4), 1159–1194.

- Barndorff-Nielsen et al. (2013) Barndorff-Nielsen, O. E., J. M. Corcuera, and M. Podolskij (2013). Limit theorems for functionals of higher order differences of Brownian semistationary processes. In A. N. Shiryaev, S. R. S. Varadhan, and E. Presman (Eds.), Prokhorov and Contemporary Probability Theory, pp. 69–96. Berlin: Springer.

- Barndorff-Nielsen et al. (2006) Barndorff-Nielsen, O. E., S. E. Graversen, J. Jacod, M. Podolskij, and N. Shephard (2006). A central limit theorem for realised power and bipower variations of continuous semimartingales. In Y. Kabanov, R. Liptser, and J. Stoyanov (Eds.), From Stochastic Calculus to Mathematical Finance, pp. 33–68. Berlin: Springer.

- Barndorff-Nielsen et al. (2013) Barndorff-Nielsen, O. E., M. S. Pakkanen, and J. Schmiegel (2013). Assessing Relative Volatility/Intermittency/Energy Dissipation. Working paper.

- Barndorff-Nielsen and Schmiegel (2007) Barndorff-Nielsen, O. E. and J. Schmiegel (2007). Ambit processes: with applications to turbulence and tumour growth. In Stochastic analysis and applications, Volume 2 of Abel Symp., pp. 93–124. Berlin: Springer.

- Barndorff-Nielsen and Schmiegel (2009) Barndorff-Nielsen, O. E. and J. Schmiegel (2009). Brownian semistationary processes and volatility/intermittency. In Advanced financial modelling, Volume 8 of Radon Ser. Comput. Appl. Math., pp. 1–25. Berlin: Walter de Gruyter.

- Bennedsen et al. (2014) Bennedsen, M., A. Lunde, and M. S. Pakkanen (2014). Modelling electricity prices by Brownian semistationary processes. In preparation.

- Benth and Eyjolfsson (2013) Benth, F. E. and H. Eyjolfsson (2013). Simulation of volatility modulated Volterra processes using hyperbolic stochastic partial differential equations. Working paper.

- Benth et al. (2014) Benth, F. E., H. Eyjolfsson, and A. E. D. Veraart (2014). Approximating Lévy Semistationary Processes via Fourier Methods in the Context of Power Markets. SIAM J. Financial Math. 5(1), 71–98.

- Corcuera et al. (2013) Corcuera, J. M., E. Hedevang, M. S. Pakkanen, and M. Podolskij (2013). Asymptotic theory for Brownian semistationary processes with application to turbulence. Stochastic Process. Appl. 123(7), 2552–2574.

- Glasserman (2003) Glasserman, P. (2003). Monte Carlo Methods in Financial Engineering. New York: Springer.

- Gradshteyn and Ryzhik (2007) Gradshteyn, I. S. and I. M. Ryzhik (2007). Table of integrals, series, and products (Seventh ed.). Amsterdam: Academic Press.

- Handcock and Stein (1993) Handcock, M. S. and M. L. Stein (1993). A Bayesian analysis of kriging. Technometrics 35(4), 403–410.

- Hedevang and Schmiegel (2013) Hedevang, E. and J. Schmiegel (2013). A Lévy based approach to isotropic random vector fields. Working paper.

- Jacod and Shiryaev (2002) Jacod, J. and A. N. Shiryaev (2002). Limit theorems for stochastic processes. Springer.

- Matérn (1960) Matérn, B. (1960). Spatial variation: Stochastic models and their application to some problems in forest surveys and other sampling investigations. Meddelanden från Statens Skogsforskningsinstitut 49(5), 144 pp.

- Nualart (2006) Nualart, D. (2006). Fractional Brownian motion: stochastic calculus and applications. In International Congress of Mathematicians. Vol. III, pp. 1541–1562. Zürich: Eur. Math. Soc.

- Rényi (1963) Rényi, A. (1963). On stable sequences of events. Sankhya Ser. A 25, 293–302.

- Veraart and Veraart (2014) Veraart, A. E. D. and L. A. M. Veraart (2014). Modelling electricity day-ahead prices by multivariate Lévy semistationary processes. In F. E. Benth, V. A. Kholodnyi, and P. Laurence (Eds.), Quantitative Energy Finance, pp. 157–188. New York: Springer.

newpage

Appendix

Appendix A Calculating the constants and of Section 4

Let which is the case considered in the paper. From Barndorff-Nielsen et al. (2013) we know that is given by

where for is the correlation function of the fractional Brownian noise with Hurst parameter

See also Barndorff-Nielsen et al. (2013) for a proof of the continuity of which justifies the use of as an estimator of The matrix with from (7) is given by

where and is fractional Brownian motion with Hurst parameter For the above is considered with first order differences of i.e. fractional Gaussian noise, but for we consider 2nd-order differences of i.e. where the correlation function of is

As shown in Corcuera et al. (2013), for which is the case considered in this paper, the entries of are

Further, following the proof of the continuity of in Barndorff-Nielsen et al. (2013) it can be shown that is continuous which justifies the use of as an estimator of in the CLT (7).

Appendix B Simulation schemes

Simulating the process without stochastic volatility is straightforward and can be done without simulation error, see B.1. Simulation of the general process via the discretization procedure described in the paper is more involved and described in B.2.

B.1 Exact simulation of Gaussian process

For observations in a given time period with step size do:

-

1.

Calculate autocovariance function (3) for

-

2.

Form the Toeplitz matrix and calculate its square root (Cholesky) matrix

-

3.

Simulate a multivariate standard normal vector and set

B.2 Approximate simulation by convolution

To simulate the process with kernel function and driving Lévy process on a grid of step size in rewrite the integral as a sum as in Section 3

Now, to approximate a path for do:

-

1.

Truncate the sum towards at .

-

2.

Simulate the stochastic volatility on a grid, see e.g. Section 4.1.

-

3.

Simulate iid on a grid,

-

4.

Compute and

-

5.

Do discrete convolution: convolution

-

6.

Select relevant values of approximate path: .