Discrete, Non Probabilistic Market Models.

Arbitrage and Pricing Intervals.

Abstract.

The paper develops general, discrete, non-probabilistic market models and minmax price bounds leading to price intervals for European options. The approach provides the trajectory based analogue of martingale-like properties as well as a generalization that allows a limited notion of arbitrage in the market while still providing coherent option prices. Several properties of the price bounds are obtained, in particular a connection with risk neutral pricing is established for trajectory markets associated to a continuous-time martingale model.

Key words and phrases:

Key Words: Trajectory Based Market Models, Arbitrage, Martingales, Minmax1. Introduction

The market model introduced by Britten-Jones and Neuberger (BJ&N) in [11] incorporates several important market features: it reflects the discrete nature of financial transactions, it models the market in terms of observable trajectories and incorporates practical constraints such as jump sizes as well as methodological constraints in terms of the quadratic variation. Market frictions can also be included naturally. The book treatment in [25] also emphasizes the fundamental characteristics of the model’s assumptions. Our original interest in this approach stemmed from recent developments on non probabilistic market models ([3], [4]), the setting of [11] may be seen as a natural discrete version of these continuous-time models. The present paper develops a framework that generalizes and formalizes the original BJ&N model and, along the way uncovers some new phenomena not noticed in [11].

The framework of the paper is a discrete market model , is a sequence of real numbers and a sequence of functions acting on representing the portfolio holdings along . The set of trajectories plays a central stage in the developments; trajectories, as opposed to probabilities, are a basic observable phenomena, therefore, it is relevant to pursue developments based only on such characteristics of the market. The models are discrete in the sense that we index potential portfolio rebalances, , by integer numbers. Otherwise, stock charts and investment amounts can take values in general subsets of the real numbers, data could flow in a time continuous manner and portfolio rebalances could be triggered by arbitrary events without the need to be associated to a time variable.

For a given European option , we prove existence of a pricing interval (see Definition 5) under conditions that allow for arbitrage opportunities in the market. The co-existence of arbitrage and the price interval follows as a consequence of a worst case point of view and reflects a basic financial situation. Market players involved in the option’s transaction may need/prefer the option’s contract sure benefits against the potential arbitrage rewards. For market agents transacting in the option, any market price falling outside the proposed price interval generates an extended arbitrage opportunity (i.e. trading with the option is required) for one of the agents involved in the option’s transaction. This extended arbitrage provides a profit for all elements of and, so, it is riskless.

Part of the practical relevance of the interval depends on the relative sizes of the sets and , the collection of all trajectories and all portfolios, respectively, occurring in . On the one hand, we should design to be large enough so that it allows for arbitrarily close approximations of stock charts but not any larger so as not to artificially enlarge the bounding interval. On the other hand, should include only portfolios that can be implemented in practice (albeit in an idealized way) as the introduction of more powerful, but impractical, hedging strategies may artificially shrink the bounding interval. The fact that a minimization is required over the set of portfolios directs attention to the issue of membership to , it is well known that judicious choice of portfolio sets can change substantially the properties of the associated market in continuous-time (see for example results on non-semimartingale processes in [10]). We also present an instance of this phenomenon in Section 9.

We ask: what are the fundamental path properties, independent of the probability measure, of a discrete time martingale, that permits to obtain no arbitrage results? The simple notion of arbitrage-free node, contained in Definition 10, allows for probability free developments of arbitrage-free markets. The no arbitrage conditions obtained in our paper, see Corollaries 3 and 4, should be contrasted with the analogous conditions in [19] (see also [6]) in stochastic settings. Related no arbitrage results in terms of properties of paths are in [5].

As indicated, with a worst case point of view, we uncover the following phenomena: there exists a rational price interval for a given option that does not introduce a relative arbitrage (in the sense of [15]) even though there may be arbitrage opportunities in the market. In our setting, this is reflected on the fact that the set of portfolios allows to define the notion of -neutral market (introduced originally in [11], but, in that reference, associated with no arbitrage):

(for details see Definition 7). It turns out that this notion is a weakening of the no arbitrage property that still allows for a price interval (see Theorem 1) and many martingale-like properties to go through in a trajectory based setting while permitting a limited notion of arbitrage. One should compare -neutrality with the normalization for a convex measure of risk ([17]).

-neutral markets are closely related to trajectory sets obeying the local -neutral property (introduced in Definition 10); this latter condition should be contrasted with the notion of sticky processes ([18], [7]) which is fundamental to guarantee the removal of any possible arbitrage in a model with non-zero transaction costs. Reference [16] obtains a similar result for trajectory sets obeying the local -neutral property under the presence of transaction costs.

To obtain -neutral markets under the assumption of local -neutrality of , one notices the existence of contrarian trajectories, these are elements of that move in a contrarian manner to a given investment in such a way that makes the potential profits arbitrarily small (or negative). Under natural financial conditions, it also follows that the market player stops or liquidates her portfolio. These results are developed in Section 7.

A trajectory set is implicit in a stochastic process model; making trajectory sets a central object of interest is of relevance, in particular, when there is insufficient information to assign a probability distribution with confidence. An example is given by the modelling of crashes in [14] where, the number, timing and size of a downwards stock change (a crash) is treated without probabilistic assumptions. More importantly, giving trajectory sets a primary role changes the usual paradigm to model financial situations. Stochastic modeling relies on stochastic processes and the main input for their construction is a probability distribution; by contrast, the properties of their paths result as a by-product. References [3] and [4] present continuous-time examples of trajectory sets which do not correspond to semimartingales. In the present paper we describe a general discrete example of a class of trajectory sets extending substantially the model in [11], in particular, the example incorporates trajectory dependent volatility. A computational and more detailed analysis is developed in the companion paper [12]. Section 10 also introduces trajectory sets associated to continuous-time martingale processes.

In the absence of a probability measure, modelling objects (trajectories, portfolios, stopping times, etc.) are treated here through a robust perspective ([8]) and so are subject to relevant optimizations. The logical constraints imposed by arbitrage related notions can be encoded by the supremum and infimum operators; which, most of the times, are being used to ascertain the existence of an object with the prescribed properties. These operators also appear when we price options; in this respect, a minmax perspective can be perceived as too extreme ([28]) as it considers a worst scenario approach, this view can be deceptive as the meaning of worst scenario is tide up to the functional being optimized and the actual model. In the case of option pricing, the functional proposed in BJ&N is the pathwise error and thus reflects the underlying purpose behind risk neutral pricing, namely pathwise hedging approximation. To provide support for this point of view we show that, for a discretely attainable option in a given continuous-time martingale market model, the risk neutral pricing can be seen as an example of the minmax pricing described in our paper for an associated discrete model . We also prove that such a market is -neutral. Here, our approach becomes conceptually close to model uncertainty, we mention [22] (which deals with super-replication and model uncertainty) as a representative of this burgeoning literature. As mentioned, a main difference of our approach is that we give central stage to the set , natural hypothesis on this set imply fundamental properties of the pricing functional. Some minmax publications, with rather different points of view from our paper, with applications to finance are: [1], [13] and [26], among other references.

The emphasis of the paper is to establish basic theoretical properties that follow from the proposed framework. A detailed computational analysis of related examples is available in [12]; we expect to make clear that the present setting is quite flexible, several numerical examples and processing of market data can be found in [24].

A summary of the paper contents is provided next. Section 2 introduces trajectory and portfolio sets leading to the trajectory based discrete market models to be used in the paper and remarks on the scope and generality of the framework. Section 3 collects the main definitions and gives some hints of the relevance of these concepts for the rest of the paper. An augmented formalism, allowing for other sources of uncertainty, is also described. Section 4.1 describes an example illustrating the framework. Section 5 elaborates on the minmax price bounds, defines option payoffs and a class of minmax functions, playing the role of integrable functions, are introduced as well. Section 6 proves existence of a price interval under general -neutrality conditions. That section also compares the price interval with Merton’s bounds; Section 6.1 describes the meaning of the pricing interval when the market allows for arbitrage. Section 7 provides general and natural sufficient conditions leading to -neutral and no arbitrage markets. It also introduces concrete market assumptions leading to a price interval. Section 8 deals with attainable functions, a generalization of this notion and some implications. Some analogues of martingale-like results are proven: in a -neutral market, today’s stock price is the minmax price of future stock prices and we also establish a trajectory based version of the optional sampling theorem. Section 9 provides a general example of a discrete market free of arbitrage such that its trajectory set can not be the support of any martingale. Section 10 studies a general trajectory based market associated to a continuous-time martingale market model and draws connections between the introduced bounds and risk neutral pricing. Section 11 concludes. The appendices, collect further results, proofs, as well as some technical results needed in the main body of the paper.

2. General, Discrete, Trajectory Based Model

The paper concentrates entirely on discrete, non probabilistic, market models extending the model in [11]. The setting could be considered as a discrete version of the non probabilistic, trajectory based, continuous-time models recently introduced in [3] and further developed in [4]. An example is given in Section 4 illustrating a general approach to constructing trajectory sets without using a priori probabilistic assumptions.

2.1. General Setting

We now proceed with formal definitions.

Definition 1 (Trajectory Set).

Given a real number a set of (discrete) trajectories is a subset of the following set

is a family of fixed subsets of .

Definition 2 (Portfolio Set).

A portfolio is a sequence of (pairs of) functions with , where . is said to be self-financing at if for all

| (2.1) |

A portfolio is called non-anticipative if for all , satisfying for all , it then follows that .

Definition 3 (Trajectory Based Discrete Market).

For a given real number , a set of trajectories and a set of portfolios , a trajectory based discrete market is a set satisfying the following properties:

-

(1)

.

-

(2)

For each there exist an integer , such that

or .

-

(3)

For , is non-anticipative and self-financing at .

Let (where are the function ) denote the -portfolio; for any discrete market we will assume , with .

for all means rebalancing stops at, or prior to, . The condition for all means definite liquidation has taken place at, or prior to, ; such portfolio will be referred to as liquidated.

Shortly, we will extend the above setting to account for other sources of uncertainty, accommodating this extension is mostly a matter of notation and, hence, most of the paper will only employ the above introduced notation.

The mathematical definition of market model , when applied to an unfolding stock chart and bank account , uses the following obvious interpretations. The numbers and are interpreted, respectively, as the holdings on the stock and the balancing bank account just after the -th. trading has taken place. is the value taken by the unfolding chart at the -th trading. To summarize: the portfolio values are held in the trading period , the definition of includes trajectories and portfolio re-balancing, a trajectory dependent number of times, until the position in the stock is liquidated or rebalancing stops. When valuing options will be an instance before the European option expires.

Given , the self-financing property (2.1) implies that the portfolio value, defined by equals:

| (2.2) |

during the period for and valid over for the case . Of course, .

Observe that, for simplicity we have assumed in last equation and in (2.1), and it will remain in the sequel, that the interest rate of the bank account is zero, and that there are no transaction costs.

Remark 1.

As defined above, a portfolio is given by specifying the pairs of functions so that (2.1) holds. In the remaining of the paper, we will define more conveniently by specifying the non-anticipative functions and an initial portfolio value , this will provide , the remaining functions , , are then obtained by solving equations (2.1).

The above definitions are natural generalizations of the ones introduced in [11] (see also the book presentation of the material in [25]). The definitions make explicit the notion of market model by formalizing the notion of set of portfolios (left out informal in [11]).

Informally, we explain the rather general nature of the above introduced framework. Notice that nothing requires , in particular, actual rebalancing of the stock holdings could have stopped well before . is the stock value at which investors , that have invested so far , , may rebalance their holdings to . The set of values taken by the stock components can be an arbitrary fixed subset of , for example, values of could be represented by a finite number of decimal digits. Similarly, the values can belong to an arbitrary fixed subsets of , for example, integer multiples of a given real number.

Some results require that the functions , introduced in Definition 3, are stopping times, according to the following definition.

Definition 4 (Trajectory Based Stopping Times).

Given a trajectory space a trajectory based stopping time (or stopping time for short) is a function such that:

3. Global, Conditional and Local Concepts

This section collects most of the basic concepts needed in the remaining of the paper and makes comments on their relevance and interrelationship.

Definition 5 below provides fundamental, worst case, pricing definitions by means of a global minmax optimization; they were introduced in [11] in the context of trajectory based markets. Section 5 provides results showing the import of the minmax bounds, other properties are relegated to Appendix A.

Definition 5 (Price Bounds).

Given a discrete market and a function , define the following quantities:

| (3.1) |

and

Clearly, .

Notice that and are monotonic functions of . Essentially, the quantity is the smallest initial capital such that there exists a portfolio in that, when used along with this initial capital, will upper-hedge the function uniformly on the trajectory space . Similarly, is the largest initial capital such that there exists a portfolio in that, when used along with this initial capital, will lower-hedge the function uniformly. The precise statements are provided in Propositions 1 and 2 in Section 5.1.

The next definition is the notion of arbitrage used in the paper.

Definition 6 (Arbitrage-Free Market).

Given a discrete market , we will call an arbitrage strategy if:

-

•

, .

-

•

satisfying .

We will say is arbitrage-free if contains no arbitrage strategies.

It is customary to add the extra condition , by not imposing the constraint , Definition 6 reflects the fact that one could make a profit without risk even though an initial positive capital may be involved.

For we will use the notation for . Whenever convenient, the tuple or the triple will be referred generically as a node.

3.1. -Neutral Markets

Consider the function . Since the null portfolio belongs to , it results that . Then, Proposition 1 from Section 5, indicates that no positive or negative number could be a fair price (this notion is introduced in Defininition 12, Section 5.1) for as those situations will create a relative riskless profit. So, should be the unique fair price for the function , this imposes a restriction on the market which leads to the next definition.

Definition 7 (-Neutral Market).

A discrete market is called -neutral if

Notice that -neutrality means . It is easy to see that an arbitrage-free market is -neutral (Corollary 1, Section 7); it should also be clear that a general -neutral market allows for arbitrage, a brief discussion is presented following Corollary 1 in Section 7.

The following conditional spaces will play a key role. Given and for and fixed, set:

The multiplicity of these sets indicate the incomplete nature of the markets that we are introducing. The analogue to the sets in stochastic models are, in general, sets of measure zero.

We will need to generalize the above notions of minmax bounds to contemplate the possibility of conditioning on given values of and trading instance . We present the basic definitions next.

Definition 8 (Conditional Minmax Bounds).

Given a discrete market , as well as an integer , define

Also define .

Notice that and so, as well.

Definition 9 (Conditionally -Neutral).

We say that a discrete market is conditionally -neutral at , and , if

Observe that, for , the conditional -neutral property, which depends on only through , reduces to -neutral.

3.2. Local Notions

The next definition introduces two basic concepts: a local, and portfolio independent, analogue on of the -neutral property of and a strengthening of this notion representing the local analogue of the arbitrage-free property. These local notions are instrumental as conditions on ensuring to be -neutral or arbitrage-free (but conditions on , through , are needed as well, See Section 7).

Definition 10 (-Neutral & Arbitrage-Free Nodes).

Given a trajectory space and a node :

Remark 2.

The developments need to distinguish related notions applicable to , or to actual nodes (e.g. is arbitrage-free, is locally arbitrage-free, etc.). To help avoiding confusion we may use the words global when referring to properties of and local when referring to properties of .

An arbitrage-free node is clearly a -neutral node as well. If all nodes , and , are -neutral and is a set of portfolios, it follows that:

| (3.5) |

The local arbitrage-free property of plays the analogous role to the martingale property in a stochastic setting, with this in mind one can try to prove martingale-type results. We provide one such example with a trajectory based version of the optional sampling theorem in Section 8.

Given , and assuming to be bounded for each , the following results hold:

-

(1)

If all nodes in , , are -neutral then, is conditionally -neutral at .

-

(2)

If all nodes in , are arbitrage-free and is a stopping time, then is arbitrage-free.

Item follows as a special case of Theorem 2 and item is a special case of Corollary 3 (both results are found in Section 7.1). We note that these results hold more generally for cases when is not necessarily bounded.

3.3. Other Sources of Uncertainty

All results and definitions in the paper involving markets and trajectory sets can be generalized by incorporating another source of uncertainty besides the stock. This extra source of uncertainty will be denoted by which, in financial terms, will be considered to be an observable quantity. This is analogous to moving from the natural filtration to an augmented filtration in the stochastic setting.

The sequence elements are assumed to belong to abstract sets from which we only require to have defined an equality relationship. We provide next the simple changes to the previous definitions to accommodate for the new source of uncertainty. The arrow notation indicates how the objects change ( is fixed).

| (3.6) | ||||

Besides the above changes, that concern mostly trajectory sets and the functional dependency in terms of both variables (and some minor notational changes), all statements and properties appearing in the paper, only involve the first coordinate (in the tuples ) in all algebraic manipulations. Clearly, is required to be non-anticipative with respect two both variables and and the notion of trajectory based stopping time applies now to trajectories of the form . These remarks can be used to show that all the results in the paper stay true in the extended/augmented formalism. We explicitly use the extended formalism in subsection 4.1 and Section 10.

4. Example

To motivate and illustrate discrete markets , we introduce a family of examples. These examples model discretizations of stock charts which, for the moment, are assumed to be given as a family of continuous-time functions , with , and . We will rely on some defininitions.

Refining Sequence of Partitions: Consider a sequence , where is a finite partition of with and . Let .

Selected times: Let a sequence of functions such that ,

Observe that for any there exist such that . This is so because implies that there exists , the minimum such that , and .

Let , define the following general class of discrete trajectories

General Aspects. A refining sequence of partitions reflects a financial situation where the investor re-balances her/his portfolio with a certain minimum time resolution but is willing to refine it further if deemed necessary. The case of a fixed partition ( the same for all ) means that the investor will never rebalance more often than an a-priori given time resolution.

There is no essential result in our paper that requires , so there is no need to use the exponential function in the definition but, doing so makes it easier to connect with the usual geometric stochastic models as well as with [11].

We are interested in prescribing “structured” subsets of , we do this by means of an observable functional . For simplicity, the functional could be defined on (and could depend on other variables as well) and takes values on . As a particular case, the functional selects those such that has finite quadratic variation in the interval respect to , that is, the following limit exists

| (4.1) |

Other observable, additive, non-decreasing and non-negative quantities could be used as well, for example, the number of transactions from to , or the total number of shares transacted from to . Intuitively, each time a transaction takes place, the value for the observable quantity represents the tick of a trajectory based clock (usually interpreted as a “business clock” with trajectory dependent rate.)

The following is an example of a structured discrete trajectory set. For real numbers and , define:

| (4.2) |

For the case of the functional given by (4.1), the requirements defining can be interpreted as imposing constraints on the maximum consumed quadratic variation and on the maximum absolute value of the change on chart values, both in between consecutive trading instances. In addition, the condition means we deal with trajectories whose total quadratic variation in the interval belongs to the a-priori given subset . In effect, the imposed constraints restrict the outcomes resulting from the interaction between market fluctuations and portfolio rebalances.

4.1. Construction of Trajectory Sets From Augmented Data

Here we describe a set of trajectories that does not require a continuous time model for the charts. The general principle guiding the construction is to isolate an observable quantity (representing a variable of interest) and proceed to define a trajectory space by imposing constraints relating the trajectories and a free variable representing this observable. We work with observables given by a functional, still denoted by , but now defined on charts (i.e. the values of some unfolding financial data), may also depend on other variables as well.

The definition of in (4.2) depends on having access to the functions . We now turn the tables around and re-define as , a set which does not require any reference to a given class of continuous-time trajectories. We still allow observable charts to unfold in continuous-time, in order to achieve these goals, we use the augmented formalism introduced in Section 3.3. Trajectories are given by a sequence of tuples , which will be associated to samples of continuous-time charts. This is a natural way to proceed, information deemed important for modelling is lost when sampling hence, this information will be encoded by the variable (associated to the functional ).

The definition below assumes given: , and real numbers, and sets .

Definition 11.

will denote a subset of (this last set as in (3.6)) so that satisfies , and:

-

(1)

for all ,

-

(2)

for all .

Moreover, there exists at least one such that -

(3)

.

Associated discrete markets are required to satisfy: then .

Remark 3.

As already mentioned, the condition could equally be replaced by (of course with an appropriately chosen value for ).

We emphasize that , as characterized above, does not need to be, in general, the set of all trajectories satisfying the listed constraints in Definition (11); specific examples are described in [12]. Comparing with (4.2), we see that we have allowed to be an independent variable . For there could be multiple indexes .

The set is used for modelling the unfolding of a data chart by mapping , one index at a time (i.e. as the chart unfolds), to its closest path .

The trajectory set introduced in [11] can be recovered as a special case of Definition 11 by taking and defining

| (4.3) |

moreover we need to require the existence of satisfying . Therefore and the constraint in Definition 11 corresponds to . Moreover, as depends on there is no need to work with tuples in this case. Not imposing (4.3) allows to incorporate -neutral nodes which are arbitrage nodes (see Definition 10 and related comments afterwards.) An analysis of these considerations in the context of the example is outside the scope of the paper, details are given in [12].

A natural discretization leading to an implementation of is obtained by introducing real numbers . The coordinates are then restricted to belong to the sets and to , thus is now a set .

For implementation purposes we need a finite version of the above discrete space. Towards this end we will take, for convenience, a fixed integer. So, the jump bound is given as an integer multiple of . For given define

and for a finite of positive integers , , define

We then obtain a finite version of Definition 11, assuming that

Such finite versions of the sets will be denoted .

Local Behavior. The way of defining trajectory sets , or their finite versions, will make it easy to check if the local properties of -neutral or up-down are satisfied. This is so because our constraints are given locally (i.e. at each node) and the combinatorial definitions will allow trajectories to move up or down. Next, as examples, we provide some general arguments on how to argue for the validity of these local properties.

Assume that the the sets in the trajectory space of Definition 11 do not attain minimum nor maximum and fix a node of a trajectory . Clearly, there exists the possibility of choosing trajectories such that , and respectively, so any node is up-down, and in that case the market results locally arbitrage-free, see Definition 10. Specific instances of the sets or their discrete or finite versions will impose further constraints beyond the ones listed in Definition 11. In each such case, we will need to check the validity of the needed local requirements, -neutrality or arbitrage-free, so that our results hold.

Consider now , in this case we can assume that . First note, as previously indicated, that for any trajectory , since , then . Taking into account the constraint , the largest value that can attain corresponds to the value and, in that case, , which shows .

In the case that , could exist trajectories containing the node with (for example, by choosing for , when and at most ). Such trajectory satisfies and so, one more step is available. Moreover, given that for any trajectory it follows that , is an arbitrage node. These nodes present arbitrage opportunities.

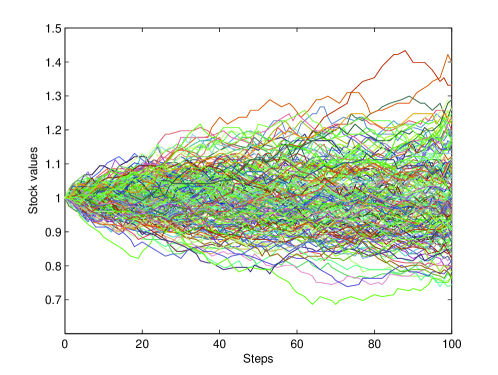

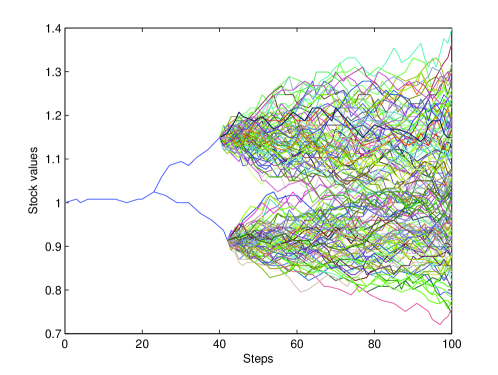

For display purposes, consider a finite space consisting of all trajectories satisfying the conditions in Definition 11 with , , , , , (and so ). Figure 1 shows random samples of trajectories from such trajectory space. Figure 2 shows random samples of trajectories from two conditional spaces from the above trajectory space.

5. Minmax Bounds

Given a future profile , Definition 5 provide the “price” bounds for the associated option. The present section develops basic results following from the definitions while Section 6 justifies the quantities introduced to be actually price bounds. Options and minmax functions are introduced as well.

5.1. Minmax Bounds

The price bounds can be recast in a more familiar way:

under the conventions that and .

The notion of relative arbitrage (see [15]) introduced below is useful in order to partially justify the above minmax definitions as price bounds.

Definition 12 (Relative Arbitrage).

Let be a function defined on and a discrete market. , with initial value , is a relative arbitrage with respect to if:

Or,

Comparing with Definition 6, with initial capital is an arbitrage strategy if and only if it is a relative arbitrage with respect to the derivative function .

Definition 13 (Fair Price).

We say that is a fair price for a function in a discrete market if there is no , with initial value , that is a relative arbitrage for .

It is useful to keep in mind the following obvious result.

Proposition 1.

Consider a discrete market , a function defined on and .

-

•

If , then there exists :

, where -

•

If , then there exists :

, where

Observe that by Proposition 1, neither nor , is a fair price for . In the next section we are going to show conditions under which the fair prices are confined to an interval, as it is known for stochastic models. The following simple result shows that the upper-hedging and lower-hedging results in Proposition 1 are tight in a trajectory based sense.

Proposition 2.

Assume a function defined on a discrete market model is given.

-

•

If satisfies , then:

-

•

If satisfies , then:

The following proposition shows that in a general discrete market the quantities may behave in an unexpected way (but not so in a -neutral market).

Proposition 3.

Given a discrete market model and an arbitrary constant, it follows that:

In contrast, notice that if is -neutral then, .

Proof.

Consider first the case that is not -neutral; it follows that in that case, this implies that there exists such that:

which leads to .

Consider now that is -neutral;

it is then clear that

Hence in all cases,

then

∎

5.2. Minmax Functions. Conditions for Boundedness of and

The integrability conditions, required for payoffs in a probabilistic setting, are replaced in the proposed framework by the, so called, minmax functions. The general setting works with a general function .

is called an European option when there exists an integer and and stopping times , , so that . The function will be called a payoff; the setting allows for path dependency. For a European call or put option (and so ) portfolios in could/should be required to satisfy for all and for all .

Definition 14 (Upper and Lower Minmax Functions).

Given a finite sequence of stopping times with for , a real sequence , and , we call an upper minmax function if

Similarly, is called a lower minmax function if

The following examples show that some common options belong to the class of minmax functions.

Examples:

(1) If is an European call option with strike price and a stopping time,

then is an upper minmax function with , , , and .

(2) If is an European put option with strike price and a stopping time,

then is an upper minmax function with , and .

Clearly, the above two examples are also lower minmax functions.

(3) Under the assumption for all and all ; if

and so, is an upper minmax function with for all .

(4) If

then is an upper minmax function with for all and .

Notice that, in particular, if is uniformly bounded from below by a constant, for all , then examples and are lower minmax functions as well.

Remark 4.

Under some assumptions on the market , such as conditionally -neutral, it can be proven that the conditional bounds and/or are finite when is an upper or lower minimax function, for reasons of space details are provided elsewhere ([12]).

6. Pricing with Arbitrage in -Neutral Markets

We provide general conditions resulting in a worst case price interval for the possible prices for an European option. The notion of conditionally -neutral market is the essential ingredient for the result to hold. We compare the minmax bounds with Merton’s bounds and give a detailed justification for the quantities introduced to be actual market prices. As already indicated, -neutrality is a weakening of the no arbitrage condition and indeed the price interval exists even when there is a certain kind of arbitrage opportunity in the market (see discussion after Corollary 1 in Section 7).

The definition of addition of two portfolios, implicitly required in the next theorem, is introduced just before the statement of Lemma 3 in Appendix A.

Theorem 1.

Consider a discrete market , a function defined on , and fixed. Assume either that is a stopping time for all or all are liquidated. If is conditionally -neutral at node , then

| (6.1) |

in particular,

Notice that assuming to be conditionally -neutral at node implies to be conditionally -neutral at that node as well. Assuming the stronger hypothesis is not necessary, as it is clearly shown by Corollaries 2 and 5 in

Section 7, which provide assumptions implying the conditional -neutral property; those conditions will also imply (6.1) and do not require

that is closed under addition.

The following is another condition on that also ensures (6.1); the proof is immediate and so omitted.

Proposition 4.

Consider a discrete market , a function defined on , a fixed and . If there exists a sequence such that for all , then, is conditionally -neutral at , and

We provide next the simple connection between the minmax bounds and Merton’s bounds [23]. For a call option , with , Merton’s bounds are and .

Proposition 5 (Merton’s Bounds Comparison).

Consider a discrete market , an integer valued function , , and a function defined on . Assume there exists such that for any and . We obtain:

() If and is -neutral then, .

() If for all , .

Proof.

Fix , -neutrality implies , so () is clearly valid if . If

Thus,

() , then

Consequently

∎

In a situation where Proposition 4 and Proposition 5, item , are both applicable, we obtain the interesting result . This shows that a characteristic of the trajectory space namely, the presence of a globally constant trajectory, implies that the lower Merton bound is attained.

6.1. Meaning of Option Prices in -Neutral Discrete Markets

Having in mind the assumptions leading to the conclusion (as in Theorem 1, Proposition 4, Corollary 2 and Corollary 5), we introduce the following definition of price interval.

Definition 15.

Consider a discrete market and a function on . Under the assumption that , we will call the price interval of relative to .

Observe that under the referred assumptions is a fair price for .

The assumptions in Theorem 1 guarantee a pricing interval and at the same time allow for arbitrage in the market (see Corollary 1 and discussion afterwards). It should be noted that the presence of arbitrage nodes will impact the actual value of the option bounds. Examples for the extent to which this could happen are documented in [12].

Under the assumption that an option contract has been traded, the existence of the minmax price interval, independently of the presence of an arbitrage strategy, is substantiated on the need to have enough funds to match the certainty of future financial obligations. This is in contrast to an investment in an arbitrage opportunity which profits are uncertain as they may not materialize in a -neutral market. In a general -neutral market, an investment following an arbitrage portfolio will not guarantee enough returns under all scenarios in order to cover the obligations required by .

The simplest mathematical example illustrating such a financial situation is given by a one-step market where for all and and that the infimum is realized at a unique . So, the market is locally -neutral; furthermore, if one can also see that where is a European call option. A risk neutral price is not available in this case but the minmax price provides a solution reflecting the needs of investors dealing with the option. Namely, if the option selling price is smaller than the potential obligation could not be matched under all scenarios through investing on the arbitrage (as actual profits may not materialize) resulting in a shortage of funds, under some scenarios, for the seller of the option. So, it is the worst case approach, requiring coverage under all scenarios, that allows for the co-existence of arbitrage and a price interval in a -neutral market. If -neutrality does not hold, it is easy to see that the minmax optimization falls back into the arbitrage opportunity by giving and the optimal investment given by in the above example.

See also related arguments in [20] where, in a context of portfolio selection, a numeraire portfolio is shown to exist under conditions that allow for arbitrage opportunities.

7. Trajectory Based Conditions for -neutral and arbitrage-free Markets

Theorem 1, in Section 6, shows the key role of conditional -neutrality in order to obtain a worst case price interval. The present section provides natural and general sufficient conditions that imply a discrete market to be conditionally -neutral or arbitrage-free. Under mild assumptions, these conditions are easily seen to be necessary conditions as well. The key ingredients are the local conditions, introduced in Definition 10, that allow trajectories to move in a contrarian way to an arbitrary investment. There is also a need for global conditions related to how market participants may stop their portfolio rebalances. We provide two general financial settings leading to such global conditions, these assumptions also imply existence of a price interval.

The following definition will be a main tool.

Definition 16 (-contrarian).

Given , and , if

| (7.1) |

we will say that and are -contrarian beyond .

Notice that trivially satisfies the above definition for the case and .

Remark 5.

When the portfolio is clearly understood from the context, we will just simply say is -contrarian beyond . Also, saying “beyond ” is synonymous to the fact that where, also, is understood from the context.

The following two propositions, presented without proofs, are stated so that they resemble each other, some of the similarity is lost because we have decided to deal only with the notion of arbitrage (and no arbitrage) starting only at (i.e. we have not introduced conditional versions of these concepts).

Proposition 6.

is conditionally -neutral at , with and if and only if for each and , there exists which is -contrarian beyond .

Proposition 7.

is arbitrage-free if and only if for each we have:

Clearly if and are -contrarian then, they will be also -contrarian if , this implies the following corollary, which shows that -neutral is a necessary condition for a discrete market to be arbitrage-free.

Corollary 1.

If is arbitrage-free, then is -neutral.

The converse of Corollary 1 does not hold in general. Consider a market with . If , it provides a clear arbitrage with , nonetheless the market is -neutral. We have seen in the previous section that a well defined option pricing methodology is still possible.

The local -neutral property of makes it possible to obtain trajectories which are almost -contrarian, this is shown in Lemma 4 in Appendix B. Nevertheless, this local property, which does not involve , is not enough to obtain conditions guaranteeing conditional (global) -neutrality of . We will tackle this shortcoming by imposing global financially-based conditions of a general nature that, when supplementing the trajectory based local conditions, will provide the existence of contrarian trajectories and of a price interval.

7.1. Initially Bounded

The following definition reflects the situation of an investor who decides conditionally on a bounded number of transactions, that he/she will stop trading after a certain fixed number of future trades. The setting allows for unbounded .

Definition 17 (Initially Bounded).

Given a discrete market and ; we will call initially bounded if there exists a bounded function (which may depend on ) such that for all :

| (7.2) |

If (7.2) holds, and is a stopping time, then . Also, if is bounded, then it is actually initially bounded by taking .

We are now able to provide a general setting ensuring that a discrete market is -neutral.

Theorem 2.

Given a market , and , assume that is initially bounded for any and each node , with and , is -neutral. Then, is conditionally -neutral at .

Proof.

From Proposition 6, for any and a given , it is enough to show the existence of an -contrarian trajectory with respect to , extending beyond . From the hypothesis on -neutrality of nodes and fixed , observe that Lemma 4 from Appendix B is applicable giving a sequence of trajectories verifying

| (7.3) |

Since and result -contrarian beyond if , we only need to consider the case where . The result then follows from Lemma 6 in Appendix B, taking in that lemma. ∎

The following corollary provides existence of the pricing interval in the setting of Theorem 2. The sum of portfolios, used in the proof, is presented before Lemma 3 in Appendix A.

Corollary 2.

Consider a discrete market , a function defined on , and fixed. Assume to be initially bounded for all and either is a stopping time for all or all are liquidated. Then, if each node , with and , is -neutral:

Proof.

Observe that the initially bounded property is closed under addition. Indeed, let , the functions required by Definition 17 for respectively. Then, set and ; since and so, is bounded in . Therefore, Theorem 2 applies implying is conditionally -neutral at . It follows that

where the innermost inequality follows from Theorem 1. ∎

Remark 6.

A more basic result is concealed in the proof of the last corollary, indeed, under those hypothesis is conditionally -neutral.

In order to obtain sufficient conditions implying that a market is arbitrage-free, it is conceptually clearer to work with the notion of local arbitrage. That concept represents the situation when we know a trajectory and an instance where an arbitrage opportunity will arise. It also assumes the existence of a portfolio that takes advantage of the arbitrage opportunity.

A discrete market model is said to have a local arbitrage if there exist , and satisfying:

| (7.4) |

The logical negation of the conditions in (7.4) will give local sufficient conditions leading to (global) no arbitrage results:

A discrete market is said to be free of local arbitrage if it has no local arbitrage at any node , that is, the following holds at any node :

| (7.5) |

or

| (7.6) |

Remark 7.

The above conditions and the requirement of being initially bounded ensure the existence of -contrarian trajectories with respect to a given ; that is, we have the following result.

Theorem 3.

Consider a discrete market free of local arbitrage. If for any , is an initially bounded stopping time, then is arbitrage-free.

Proof.

Fix , and .

First observe that by Lemma 5 item in Appendix B, for any either , or there exists a smallest integer such that (7.5) holds for (,H,). Consequently, under the latter scenario

If, for some , (7.5) does not hold or in case (7.5) holds and is verified, then the second condition in Proposition 7 is satisfied. Therefore, we may assume a case in which (7.5) is valid for some node with and . Applying Lemma 5, item (3), with as , we obtain a sequence of trajectories , verifying

Since , then . So by Lemma 6 with , there exist a trajectory such that and are -contarian beyond w.r.t. and also to , since which, by Proposition 7, concludes the proof. ∎

Observe that the proven result is actually more general than the result stated in the theorem, it proves that the market is arbitrage-free in a conditional sense, i.e. at each node . We have not needed to formally pursue this conditional notion in the paper.

The following result provides sufficient conditions, involving the local arbitrage-free property of , leading to arbitrage-free markets.

Corollary 3.

7.2. Debt Limited Portfolios

Here we introduce a second set of financially motivated hypothesis, of a general nature, that, when combined with the local -neutral (local arbitrage-free) assumption on , provide conditionally -neutral (arbitrage-free) markets . In fact, the following theorem shows that for all practical financial purposes, as long as the number of arbitrage and flat nodes are bounded along each trajectory, the assumption of existence of contrarian trajectories is always satisfied. The results rely on limiting the capital that a portfolio owner may be able to borrow; this condition is usually used to exclude arbitrage opportunities created by doubling strategies ([6]). The setting allows for unbounded .

The next theorem provides another natural and general setting, besides the one given in Theorem 2, ensuring that a discrete market is conditionally -neutral.

Theorem 4.

Given a market , and . Assume each node , with , is -neutral. We further assume:

-

(1)

The number of arbitrage -neutral and flat nodes (as per Definition 10) allowed in each trajectory is bounded by an absolute constant .

Also, for :

-

(2)

For given , a constant independent of and , we have:

(7.7) -

(3)

For given , an absolute constant, we have:

(7.8)

Then, for any , there exists so that and are -contrarian beyond . In particular, if hypothesis and above are satisfied for all , is conditionally -neutral at .

Item only allows a constant maximum of arbitrage -neutral and flat nodes along each trajectory but, those nodes, are allowed to be arbitrarily distributed along such trajectory.

Proof.

It is enough to consider the case for any , we will establish the existence of such that , this will conclude the proof.

Let be the smallest integer satisfying and . If such does not exist we take . There are two possibilities: a) is an arbitrage -neutral node, b) is an up-down node. In case , it follows from (7.8) that there exists satisfying hence

| (7.9) |

In case , from the up down property, there exists such that

| (7.10) |

If , since , then (7.9) or (7.10) show that satisfies the conditions of a contrarian trajectory we are looking for. So, assume .

Proceeding recursively, we may assume that we have either constructed the desired trajectory or we have at our disposal a trajectory , satisfying

as well as

We then look for the smallest satisfying and . If such does not exist the construction terminates by taking and so concluding the proof. Otherwise, there exists , and by means of the alternatives and , and other considerations above, we obtain that the following holds:

as well as

Continuing in this way, we have the following exclusive alternatives: we managed to construct the desired trajectory and, hence, the recursion terminates. The recursion continues indefinitely, in which case we have:

| (7.11) |

where we used the fact that for .

Let us show that (7.11) conflicts with (7.7): (recall )

| (7.12) |

where we obtained the last inequality by taking sufficiently large; let us denote the smallest integer satisfying (7.12) by . This argument just proves that we can not have as otherwise we have a contradiction with (7.7); it then follows that . To sum up: for all , hence is a contrarian trajectory that extends beyond . The conditionally -neutral property then follows from Proposition 6. ∎

Remark 8.

Notice that we have established more than is required in Definition 16 as each term in (7.1) has proven to be non-negative. The hypothesis (7.8) is only needed to extract the needed information from the up-down nodes, the fact that that hypothesis is also used for the arbitrage -neutral and flat nodes is not essential.

Corollary 4.

Assume the same hypothesis as in Theorem 4 and, furthermore, require . Then, is arbitrage-free.

The following corollary provides existence of the pricing interval in the setting of Theorem 4, we borrow all assumptions from that theorem but need to strengthen (7.8) so that the addition of portfolios obeys that equation as well.

Corollary 5.

Consider a discrete market , a function defined on , and fixed. Assume that all hypothesis of Theorem 4 are satisfied, and that either is a stopping time for all or all are liquidated. Moreover, we strengthen (7.8) by assuming there are absolute constants , :

| (7.13) |

Then:

Proof.

Let , we will argue that Theorem 4 is applicable to and borrow the notation used in that theorem. Assumption in Theorem 4 can be made to hold for by defininig whenever , . Also assumption in Theorem 4 holds with for given our assumption (7.13). Therefore, is conditionally -neutral at . It follows that

where the innermost inequality follows from Theorem 1. ∎

8. Attainability. Formal Martingale Properties

This section concerns the notion of attainability, as well as a generalization of this notion and some implications. Under the assumption of attainability the minmax bounds are additive and behave much like an integration operator. We also present results providing formal analogues of martingale properties, in particular, a trajectory based optional stopping theorem is proven. In some cases, for the sake of generality and clarity, we directly assume the existence of a worst case pricing interval, results providing such interval are given in: Theorem 1, Proposition 4, Corollary 2 and Corollary 5.

Definition 18.

Given a discrete market , and non-negative numbers , . A function is called -upward attainable if there exists and a number such that

| (8.1) |

Analogously, is called -downward attainable if there exists and a number such that

| (8.2) |

Finally is called attainable if it is -upward attainable, in such a case we use the notation and . Notice that is -upward attainable if and only if it is -downward attainable.

The next proposition shows that the distance separating the price bounds is bounded by the maximum profits.

Proposition 8.

Let be a discrete market, , and a function on . Consider the statements:

a) is -upward attainable

and .

b) is -downward attainable

and .

Then, the following holds:

| (8.3) |

where if holds, if holds and if and hold.

Proof.

In general, the bounds are not linear as functions of the payoff, the following proposition presents a case where the bounds are additive.

Corollary 6.

Consider a discrete market , , and a function on and assume the conditions for having

hold.

a) If is attainable with portfolio and then:

| (8.4) |

b) If , , are attainable with portfolios satisfying: and , then,

| (8.5) |

Proof.

By assumption,

Where we have used the abbreviation , with some abuse of notation (as may not be necessarily equal to ). It then follows that,

Similarly, since , , thus

Notice that Proposition 8 is applicable and (8.3), together with our hypothesis, gives . This equality combined with the above inequalities concludes the proof of (8.4).

The following result expresses a consistency result, namely today’s stock price is the minmax price in a -neutral discrete market . Assumptions leading to the conclusion , for any (as in Theorem 1, Proposition 4, Corollary 2 and Corollary 5), will be required. Moreover, under -neutrality, the minmax operator behaves much like an expectation, in particular the sequence of coordinate projections , behaves like a martingale with respect to this operator. A related result will be given later, the optional sampling theorem (see Theorem 5).

Corollary 7.

Let be a stopping time and a discrete market. Define by:

Fix , and assume the conditions on that assure the existence of a pricing interval.

If and belong to , then :

| (8.6) |

Where denotes the function , defined on by

Conversely. Assume , and for all , . Then if , it follows that is conditionally -neutral at .

Proof.

Notice that , for any , and is clearly non-anticipative. So is attainable. Therefore, Corollary 6 is applicable giving (8.6) since .

For the second statement, if , then

Last inequality holds, because for all , and then . Finally, since the portfolio , it follows that

Therefore, is conditionally -neutral at . ∎

8.1. Trajectory Based Optional Stopping Theorem

In our setting, the analogue of a martingale process is a trajectory set that obeys the locally arbitrage-free property (see Definition 10). With this analogy in mind, we re-cast the optional sampling theorem.

8.1.1. Stopped Trajectory Sets

We will make use of the following notation, given a trajectory space and a stopping time (see Definition 4 set:

Remark 9.

Making use of the notation introduced in (3.6), the augmented version of the above set is given by

Lemma 1.

Given a trajectory space and a stopping time defined on , fix , and assume . Then,

Proof.

Lemma 2.

Given a trajectory space and a stopping time defined on , fix , . The following holds

| (8.9) |

Proof.

Consider , so

| (8.10) |

We split the proof in two cases. Case I: consider that , hence the right hand side of (8.9) equals . Notice that if , then (8.10) implies for all but hence for all hence which gives a contradiction. Therefore, under current Case I, we should have so if it follows from (8.10) that

which implies, in either case or , that . It follows that the left hand side of (8.9) equals:

Case II: consider now , in this case the right hand side of (8.9) equals which we will prove also equals its left hand side. If and given that it follows from (8.10) that for all and this implies leading to a contradiction. Therefore, under current Case II, we should have , but then

∎

The following is our version of the optional stopping theorem for martingales.

Theorem 5.

Let be a trajectory space that satisfies the locally arbitrage-free property (locally -neutral) from Definition 10 and a stopping time defined on . Then, satisfies the locally arbitrage-free (locally -neutral) property as well.

Proof.

Usually, the optional stopping theorem involves the statement , where is a martingale and a filtration based stopping time. We have already established the analogue of this statement under the more general hypothesis of -neutrality see (8.6).

9. arbitrage-free Markets with Non Martingale Trajectory Sets

In this short section we follow the work of Cheridito [10] and impose a natural constraint on the portfolio set that allows to provide arbitrage-free markets but being such that can not be the support set of any martingale process.

Clearly, for finite sets the locally arbitrage-free property of reflects a basic property of the paths of discrete time martingales. We elaborate more on this connection in Section 10. Possible examples of discrete markets which are arbitrage-free but such that is not the support set of a martingale process require some additional structure. For example, if transaction costs are incurred each time is re-balanced, then it is possible to show that is arbitrage-free while at the same time contains arbitrage nodes and so can not be recovered, in general, as paths of a martingale process ([16]).

One can also impose some natural constraints on so that is still arbitrage-free for cases where is not related to a martingale process. Towards this goal, we present another no arbitrage result which will allow us to present examples of trajectory classes that are not the support set of a martingale process while, at the same time, the market being arbitrage-free.

The class of examples to be introduced are motivated by Cheridito’s result in a continuous-time setting ([10]) where a constraint is imposed so that transactions can not be performed consecutively if the time interval between them is smaller than an a-priori given real number . Under this constraint, fractional Brownian motion can be proven to be arbitrage-free (see also generalizations in [19] and [6]).

As motivation to the formal setting below, we think that there are continuous-time trajectories and a set of times interpreted as instances when a transaction occurs and, so, a new price is revealed. There are other sets of times corresponding to each investor who may potentially re-arrange her portfolio, these times are , we require and . The analogue of Cheridito constraint in this setting is to require . The results below incorporate this setting.

The conditions below allow to have a local upward or downward trend at some nodes as long as there is the possibility of an immediate opposite correction. Below, we use the short hand notation as a convenient way to impose the hypothesis that market participants did not have any stock holdings previous to their first trading instance at .

Definition 19.

A discrete market model is said to allow for local fast trends if is local -neutral and the following conditions are satisfied at all , and :

-

(1)

If then ).

-

(2)

For each choice of sign :

if , then there exists so that and

and .

Also assume that the stock holdings are liquidated at , and so for any .

We have the following result.

Theorem 6.

If a discrete market allows for local fast trends, and is an initially bounded stopping time for any then it is arbitrage-free.

Proof.

Fix . By Proposition 7, it is enough to show that for some .

Let be the smallest integer such that there exist so that . Since , property (1) from Definition 19 gives , so .

Consider first the case in which is up-down (i.e. the two inequalities in (3.2) are strict). Then, there exists verifying and by the local -neutrality of , property there exists satisfying , thus

| (9.1) |

On the other hand, if at least one inequality in (3.2) from Definition 10 is not strict, it follows that property (2) of Definition 19 holds for at least one of the signs ; we will handle both cases with the same argument. Therefore, there exist , satisfying and such that , so (9.1) holds also with this .

In either case , then again from property (1) from Definition 19, , so as well.

We can then apply Lemma 4 with and and , obtaining a sequence verifying

Moreover since for all , , there exists a -contrarian trajectory by an application of Lemma 6 in Appendix B, with , , , or , and . Since in that case we have for and

∎

Example: Fast Local Trend Market Free of Arbitrage.

In order to provide a general example of a discrete market satisfying the hypothesis of Theorem 6, consider

a trajectory set satisfying items 2 and 3 from Definition 19. Let be a non-decreasing sequence

of stopping times defined on satisfying

for all also, if ,

then . Given an arbitrary set of non-anticipative portfolios

define, for each :

Therefore, if it follows that . Indeed, , then , which implies or , thus . It also follows that the portfolios are non-anticipative: assume ; since it follows that , then (the largest such that ). By symmetry , thus and

Therefore, item from Definition 19 is satisfied and hence satisfies the hypothesis of Theorem 6 and so it is arbitrage-free.

Notice that condition from Definition 19, without imposing conditions and as well, allows for an arbitrage opportunity. Condition is the local -neutral condition introduced in previous sections.

10. Relation to Risk Neutral Pricing

This section defines a discrete market from a continuous-time martingale market. The results give some perspective to our approach and allow to establish connections between the minmax bounds and risk neutral pricing. Trajectory spaces are defined by stopping times samples of continuous-time martingale paths. A main point to emphasize is that the -neutral property holds due to the discrete sampling via stopping times and the martingale property.

Consider a stochastic market model consisting of a probability space where is a continuous-time filtration. Also there is an adapted process taking values on , we also assume is the trivial sigma algebra. Moreover, there exists a measure , equivalent to , such that is a martingale relative to and . This setting represents an arbitrage-free (in a stochastic sense), -dimensional market with a deterministic Bank account with interest rates. An European payoff is a real valued function defined on , non-negative, -measurable with respect to . A risk neutral price of such a claim is then given by , where the expectation is with respect to a measure .

Naturally, we assume that quantities defined on are only defined a.e., we will not explicitly indicate this fact in every instance but will do so in critical aspects of the constructions. The context should make it easy to realize if we are referring to filtration-based stopping times or trajectory-based stopping times.

10.1. Martingale Trajectory Market:

A sequence of (filtration-based) stopping times , relative to the filtration , is said to be admissible if , and, for a given , there exists a smallest integer such that . All sequences of stopping times considered in the remaining of this section are admissible, this fact may not be explicitly indicated. For simplicity, we may write , and related quantities, as .

On the stochastic side, at some points we will look at portfolios of the form

where the investment is -measurable. For technical reasons we will assume there exists a countable subset of , with , and the quantities depend only on , . This assumption is formalized next.

We will assume that all are such that the take values on . Let be a set of full measure where all random variables are defined and let be a set of full measure contained in where all random variables are defined.

For given and define:

also set

| (10.1) |

where

Recall that the Borel subsets of , denoted by , are generated by the family of cylinders

with .

Corollary 8.

Let . Assume is a stopping time. Then for all .

Proof.

Regarding the trajectories defined below: we sample, a finite (but arbitrary) number of times, every random trajectory, we record those values as well as other information that will be needed (see comments below).

Given , define:

| (10.2) |

Also define

The inclusion of and in allow the functions and (defined below) to be well defined and to be non-anticipative. Equality is defined as follows. Let , then: if and only if ,, and .

As a shorthand notation, the association, between martingale paths, the stopping time and the trajectory values, described in (10.2) will be denoted by .

Define:

| (10.3) |

where the functions are defined as follows: there exist a bounded Borel function with the property that, for

| (10.4) |

Proposition 9 below shows that and are well defined and is non-anticipative. We allow arbitrary values for , initial portfolio values, and define the bank account value sequence such that portfolios are self financing as indicated in Remark 1.

The association described in (10.4) will be denoted by .

Proposition 9.

Proof.

Let with and .

1. Assume that , then implies . Thus

Since the former reasoning is symmetric, , and is well defined.

Fix now , therefore by the previous statement, if and only if . Moreover, since , it follows that . This shows that is well defined.

2. To prove that is no anticipative, let fixed and assume , . We need to prove that . Observe that if and only if . Indeed, if , then so and, consequently, if that is the case.

On the other hand, since for , again

∎

Define the discrete martingale trajectory markets

where, in the case of , portfolios act on by restriction.

Remark 10.

To alleviate notation, we will write as . Similarly, we may write as .

As preparation for the next result, let be the set of all martingale probability measures equivalent to and denotes expectation with respect to probability measure .

For the next two results in this section, we are going to assume conditions under which behaves as a martingale with respect to ; namely:

Proposition 10.

Proof.

Notice that , and hence also , depends on only through null sets of ; therefore, it remains unchanged if defined through any .

For set , it is clear that , and if is bounded for some . Consider and with . For any , from definition (10.3), , with a bounded Borel function. Defining , it follows that , and by Corollary 8 . We have,

| (10.6) |

So, since it holds with , and is integrable by Lemma 8, also results integrable.

Remark 11.

The condition required in the previous Proposition, is equivalent to , so it is satisfied when an upper minimax function (see [12]).

For the case when is finite or, more generally, purely atomic, it should be clear that all nodes in are arbitrage-free nodes according to Definition 10 (this can readily obtained from Theorem 3.1 in [29]).

The next result represents the key property connecting martingale trajectory markets with the formalism of the paper.

Theorem 7.

Proof.

Notice that implies , where , this claim is obvious as we have , . Furthermore, and so , .

Given where is bounded and Borel and , define for . From the above claim, the following holds everywhere on :

Theorem 7 extends trivially to martingale trajectory sets of the form .

is called -attainable if there exists an admissible and such that

Theorem 8.

Proof.

Notice that the following holds for all ,

| (10.10) |

which, given that , is the same as:

We have used the notation .

Taking the conditional expectation of both sides of (10.10) with respect to and using Lemma 8, gives

| (10.11) |

The right hand side of (10.11) is only defined a.e. on ; in the case that is not defined everywhere on (which, we recall, is a set of probability one) we do extend to all of by means of the left hand side of (10.11).

Model uncertainty is usually treated by considering a subset of the set of equivalent measures. There are examples of stochastic market models for which the bounds and provide too large of an interval in order to be informative for practical purposes. From a trajectory point of view such a situation suggests: a) a deficiency of the market model (in particular the trajectory set may be too large) or b) the need to replace the super-hedging philosophy (and hence risk-free approach) for a risk taking philosophy. In this last case, the error functional used to define the bound has to be replaced by an appropriate, trajectory based, risk-functional. There are several other logical possibilities besides and , for example including liquid derivatives in the portfolio approximations (see [2]).

We have considered the set , it is natural to seek an extension of the above results to the case on non-equivalent martingale measures.

11. Conclusions and Extensions

The paper develops basic results on arbitrage and pricing in a trajectory based market model. The setting naturally allows one to resort to a worst case point of view which, in turn, permits arbitrage opportunities while at the same time providing coherent prices. This fact reveals a basic extension to the classical martingale market structure. The proposed framework has also a clear conceptual and formal relationship to the well established risk-neutral approach. Given the basic nature of the arguments it is expected that extensions to other settings are possible as well.

We have concentrated on bounding the price of an option through superhedging and underhedging, selecting an actual price inside of this interval may require to adopt a functional to accommodate the ensuing risk-taking.

Arguably, attempting a direct evaluation of the minmax optimization required in (3.1) and in related results, is a daunting task. Moreover, the minmax formulation of the problem gives no clues on how to construct the hedging values , for a given payoff , by means of the unfolding path values In the paper [12], and following [11], we propose another pair of numbers, obtained through a dynamic, or iterative, definition, each instance involving a local minmax optimization. Using the new dynamic minmax definitions we provide conditions under which the global and the iterated definitions coincide.

The manuscript [16] extends and generalizes some of the no arbitrage results to the case of transaction costs. We are also presently studying continuos-time versions of the main results as well.

Appendix A Further Results on Price Bounds

For completeness, we just state the following simple result

Proposition 11.

Consider a discrete -neutral market and functions , satisfying

where y are arbitrary real numbers. Then,

-

(1)

If and is closed under multiplication by positive numbers:

-

(2)

If y is closed under multiplication by positive numbers:

The following developments are stated and proven with two portfolio sets , the reader could take , as the extra generality is not used in the rest of the paper.

Define

where the sum is defined as follows

| (A.1) |

where is attained in , or . We now check that the portfolio sum is non-anticipative under the assumption that , are stopping times. Let ; if , it is clear that . Consider then and assume, without lost of generality, that , then . If , it would result that , and so , a contradiction.

In case that the functions are not sopping times, the portfolio sum is still non-anticipative if liquidation is assumed. Indeed, if the portfolios are liquidated at (i.e. for any for ), the sum definition in (A.1) reduces to

It is clear that if with , for some , then .

Observe also that for any and ,

Lemma 3.

Let and be discrete markets, and assume either: for all , , are stopping times or, all , , are liquidated. Set and and . Assume are real valued functions defined on then:

| (A.2) |

Moreover if is conditional -neutral at then

| (A.3) |

Appendix B Contrarian Trajectory Auxiliary Material

Lemma 4.

Given a discrete market , , , and . Assume each node , with and , is -neutral. Then, for any , there exists a sequence of trajectories , verifying, (7.3), it is

Proof.

Lemma 5.

Given a discrete market , , , and . Assume is free of local arbitrage. Then

Proof.

Item (2). If (7.5) holds for for some , choose as the first integer such that (7.5) holds for . On the other hand, by (1), .

Combining the -neutral, or free of local arbitrage conditions, of the nodes with being initially bounded we have.

Lemma 6.

Consider a discrete market , , , and with initially bounded. Assume there exist a sequence of trajectories verifying for , and , such that and

Then there exists verifying that.

and are -contarian beyond , if and .

and are -contarian beyond , if is a stopping time.

Proof.

Observe that it is enough to show the existence of such , with for , and for with .

If , and holds with . Let then assume that . Set , where is the bounded function required by Definition 17.

If , holds with . For , since because , then , using that is a stopping time and , so is also a desired integer.

Consider now the case that , and . Then from results and so . Then the conclusion is verified. Item is also valid with that , since , then and using that is a stopping time, .

∎

Appendix C Connections with Risk Neutral Pricing. Auxiliary Material

Lemma 7.

The function defined by is measurable.

Proof.

For , fix and let . Thus

For showing that , it is then enough to prove that, for any and , . This happens, if for any

To prove this, lets first define and consider two cases.

I. Assume , then for , which implies that . Conversely, if then , and . Now we are going to prove that

Indeed, if there exists such that and then . The converse is also clearly true. Finally, since for each ; , it follows that .

II. The case when follows from the decomposition of , as

Since , and , as well. ∎

Recall that is the set of all martingale probability measures equivalent to and denotes expectation with respect to probability measure .

Lemma 8.

Let and assume, for , are -measurable bounded functions, -integrable, and define

Then

() is a martingale w.r.t. and .

Assume is a -stopping time, and is bounded or is bounded uniformly by an integrable function. For any ,

() .

Proof.

For (), fix , then it holds that

since for , are -measurable, so .

For (), first observe that for , and if is also a martingale w.r.t. .

For , consider , defined as follows:

is clearly bounded, and also a -stopping time. It follows from

Since, if , the second and third sets in the union are empty, and the first one belongs to .

For , the third is empty, the first is in , and

On the other hand, if the first and third sets belongs clearly to , and

It follows, from [21, Prop 1.83], using the stopping time , that

Observe that if is bounded for some . In general, pointwise, and since results bounded by an integrable function, we have

∎

Lemma 9.

For a given and , the set , defined in Theorem 7, belongs to .

Proof.

We have to show that , for all . Setting , observe that can be decomposed in the following way

Note that if , then , thus . Consequently it is enough to consider . Let , it follows that and

Therefore . On the other hand, since for , then are -measurables [27], which concludes that . ∎

Acknowledgments: S. Ferrando would like to thank Zsolt Bihary and H.Föllmer for stimulating discussions.

References

- [1] J. Abernethy, P.L.Bartlett, R.M. Frongillo and A. Wibisono (2012), Minimax option pricing meets Black-Scholes in the limit. In H.J. Karloff and T. Pitassi, editors, STOC, pp. 1029-1040, ACM.

- [2] B. Acciaio, M. Beiglböck, F. Penker and W. Schachermayer (2013). A model-free version of the fundamental theorem of asset pricing and the super-replication theorem, arXiv:1301.5568v2 [math.PR].

- [3] A. Alvarez, S. Ferrando and P. Olivares (2013). Arbitrage and Hedging in a non probabilistic framework. Mathematics and Financial Economics, Vol 7, Issue 1, pp 1-28.

- [4] A. Alvarez and S. Ferrando (2015), Trajectory based models, arbitrage and continuity. arXiv:1403.5685v2 [math.PR] Submitted for Publication.

- [5] C. Bender (2012). Simple Arbitrage, The Annals of Applied Probability, 22, No. 5, 2067-2085.

- [6] C. Bender. T. Sottinen and E. Valkeila (2010). Fractional processes as models in stochastic finance, arXiv:1004.3106 [q-fin.PR].