Expandable Factor Analysis

Abstract

Bayesian sparse factor models have proven useful for characterizing dependence in multivariate data, but scaling computation to large numbers of samples and dimensions is problematic. We propose expandable factor analysis for scalable inference in factor models when the number of factors is unknown. The method relies on a continuous shrinkage prior for efficient maximum a posteriori estimation of a low-rank and sparse loadings matrix. The structure of the prior leads to an estimation algorithm that accommodates uncertainty in the number of factors. We propose an information criterion to select the hyperparameters of the prior. Expandable factor analysis has better false discovery rates and true positive rates than its competitors across diverse simulations. We apply the proposed approach to a gene expression study of aging in mice, illustrating superior results relative to four competing methods.

1 Introduction

Factor analysis is a popular approach to modeling covariance matrices. Letting , , and denote the true number of factors, number of dimensions, and covariance matrix, factor models set , where is the loadings matrix and is a diagonal matrix of positive residual variances. To allow computation to scale to large , is commonly assumed to be low rank and sparse. These assumptions imply that and the number of nonzero loadings is small. A practical problem is that and the locations of zeros in are unknown. A number of Bayesian approaches exist to model this uncertainty in and sparsity (Carvalho et al., 2008; Knowles and Ghahramani, 2011), but conventional approaches that rely on posterior sampling are intractable for large sample size and dimension . Continuous shrinkage priors have been proposed that lead to computationally efficient sampling algorithms (Bhattacharya and Dunson, 2011), but the focus is on estimating with treated as a non-identifiable nuisance parameter. Our goal is to build a computationally tractable approach for inference on that models the uncertainty in and the locations of zeros in . To do this, we propose a novel shrinkage prior and corresponding class of efficient inference algorithms for factor analysis.

Penalized likelihood methods provide computationally efficient approaches for point estimation of and . If is known, then many such methods exist (Kneip and Sarda, 2011; Bai and Li, 2012). Sparse principal components analysis estimates a sparse assuming , where is the identity matrix (Jolliffe et al., 2003; Zou et al., 2006; Shen and Huang, 2008; Witten et al., 2009). The assumptions of spherical residual covariance and known are restrictive in practice. There are several approaches to estimating . In econometrics, it is popular to rely on test statistics based on the eigenvalues of the empirical covariance matrix (Onatski, 2009; Ahn and Horenstein, 2013). It is also common to fit the model for different choices of , and choose the best value based on an information criterion (Bai and Ng, 2002). Recent approaches instead use the trace norm or the sum of column norms of as a penalty in the objective function to estimate (Caner and Han, 2014). Alternatively, Ročková and George (2016) use a spike and slab prior to induce sparsity in with an Indian buffet process allowing uncertainty in ; a parameter-expanded expectation-maximization algorithm is then used for estimation.

We propose a Bayesian approach for estimation of a low-rank and sparse , allowing to be unknown. Our approach relies on a novel multiscale generalized double Pareto prior, inspired by the generalized double Pareto prior for variable selection (Armagan et al., 2013) and by the multiplicative gamma process prior for loadings matrices (Bhattacharya and Dunson, 2011). The latter approach focuses on estimation of , but does not explicitly estimate or . The proposed prior leads to an efficient and scalable computational algorithm for obtaining a sparse estimate of with appealing practical and theoretical properties. We refer to our method as expandable factor analysis because it allows the number of factors to increase as more dimensions are added and as increases.

Expandable factor analysis combines the representational strengths of Bayesian approaches with the computational benefits of penalized likelihood methods. The multiscale generalized double Pareto prior is concentrated near low-rank matrices; in particular, a high probability is placed around matrices with rank . Local linear approximation of the penalty imposed by the prior equals a sum of weighted penalties on the elements of . This facilitates maximum a posteriori estimation of a sparse using an extension of the coordinate descent algorithm for weighted -regularized regression (Zou and Li, 2008). The hyperparameters of our prior are selected using a version of the Bayesian information criterion for factor analysis. Under the theoretical setup for high-dimensional factor analysis in Kneip and Sarda (2011), we show that the estimates of loadings are consistent, and the estimates of nonzero loadings are asymptotically normal.

2 Expandable Factor Analysis

2.1 Factor analysis model

Consider the usual factor model. Let , , and be the mean-centered data matrix, latent factor matrix, and residual error matrix, where and are unknown. We use index for samples, index for dimensions, and index for factors. If is the residual error variance matrix, then the factor model for is

| (1) |

where and are independent . Equivalently,

| (2) |

for sample and . Similarly, model (1) reduces to regression in the space of latent factors

| (3) |

for dimension . Unlike usual regression, the design matrix in (3) is unknown.

Penalized estimation of is typically based on (2) or (3). The loss is estimated as the regression-type squared error after imputing using the eigen-decomposition of the empirical covariance matrix or an expectation-maximization algorithm. The choice of penalty on presents a variety of options. If the goal is to select factors that affect any of the variables, then the sum of column norms of can be used as a penalty; a recent example is the group bridge penalty, , where and is an upper bound on . The selected factors correspond to the non-zero columns of the estimated (Caner and Han, 2014). To further obtain element-wise sparsity, a non-concave variable selection penalty can be applied to the elements in . The estimate of depends on the choice of criterion for selecting the tuning parameters (Hirose and Yamamoto, 2015).

Our expandable factor analysis differs from this typical approach in several important ways. We start from a Bayesian perspective, and place a prior on that is structured to allow uncertainty in while shrinking towards loadings matrices with many zeros and . If is an upper bound on , then the prior is designed to automatically allow a slow rate of growth in as the number of dimensions increases by concentrating in neighborhoods of matrices with rank bounded above by . To our knowledge, this is a unique feature of our approach, justifying its name. Expandability is an appealing characteristic, as more factors should be needed to accurately model the dependence structure as the dimension of the data increases.

2.2 Multiscale generalized double Pareto prior

We would like to design a prior on such that maximum a posteriori estimates of have the following four characteristics:

-

(a)

the estimate of a loading with large magnitude should be nearly unbiased;

-

(b)

a thresholding rule, such as soft-thresholding, is used to estimate the loadings so that loadings estimates with small magnitudes are automatically set to zero;

-

(c)

the estimator of any loading is continuous in the data to limit instability; and

-

(d)

the norm of the th column of the estimated does not increase as increases.

The first three properties are related to non-concave variable selection (Fan and Li, 2001). Properties (b) and (d) together ensure existence of a column index after which all estimated loadings are identically zero. Automatic relevance determination and multiplicative gamma process priors satisfy (d) but fail to satisfy (b). No existing prior for loadings matrix satisfies properties (a)–(d) simultaneously (Carvalho et al., 2008; Bhattacharya and Dunson, 2011; Knowles and Ghahramani, 2011).

In order to satisfy these four properties and obtain a computationally efficient inference procedure, it is convenient to start with a prior for a loadings matrix having infinitely many columns; in practice, all of the elements will be estimated to be zero after a finite column index that corresponds to the estimated number of factors. Bhattacharya and Dunson (2011) show that the set of loadings matrices that leads to well-defined covariance matrices is

We propose a multiscale generalized double Pareto prior for having support on . This prior is constructed to concentrate near low-rank matrices, placing high probability around matrices with rank at most .

The multiscale generalized double Pareto prior on specifies independent generalized double Pareto priors on (; ) so that the density of is

| (4) |

where is the generalized double Pareto density with parameters and (Armagan et al., 2013). This prior on ensures that properties (a)–(c) are satisfied. Property (d) is satisfied by choosing parameter sequences and () such that two conditions hold: the prior measure on has density in (4) and has as its support. These conditions hold for the form of and () specified by the following lemma.

Lemma 2.1

If , () and , then .

The proof is in the Supplementary Material, with the other proofs.

As in Bhattacharya and Dunson (2011), we truncate to a finite number of columns for tractable computation. This truncation is accomplished by mapping to , with retaining the first columns of . The choice of is such that is arbitrarily close to , where distance between and is measured using the norm of their element-wise difference. In addition, for computational convenience, we assume that the hyperparameters and () are analytic functions of parameters and , respectively, with these functions satisfying the conditions of Lemma 2.1.

The following lemma defines the form of and () in terms of and .

Lemma 2.2

If , , , and (), then , where has density in (4) with hyperparameters and (). Furthermore, given , there exists a positive integer for every such that for all , , , (), and , pr, where .

The penalty imposed on the loadings by the prior has exponential growth in terms of as the column index increases. This property of the prior ensures that all the loadings are estimated to be zero after a finite column index, which corresponds to the estimated number of factors.

3 Estimation algorithm

3.1 Expectation-maximization algorithm

We rely on an adaptation of the expectation-maximization algorithm to estimate and . Choose a positive integer of order as the upper bound on ; the estimate of the number of factors will be less than or equal to . Results are not sensitive to the choice of due to the properties of the multiscale generalized double Pareto prior, provided is sufficiently large. If is too small, then the estimated number of factors will be equal to the upper bound, suggesting to increase this bound. Given , define and for as in Lemma 2.2, with and being pre-specified constants.

We present the objective function as a starting point for developing the coordinate descent algorithm and provide derivations in the Supplementary Material. Let and , where the superscript denotes an estimate at iteration and denotes the conditional expectation given , , and based on (1). The objective function for parameter updates in iteration is

| (5) |

where and ().

3.2 Estimating parameters using a convex objective function

The objective (5) is written as a sum of terms. The th term corresponds to the objective function for the regularized estimation of the th row of the loadings matrix, , with a specific form of log penalty on (Zou and Li, 2008). Local linear approximation at of the log penalty on in (5) implies that each row of is estimated separately at iteration :

| (6) |

This problem corresponds to regularized estimation of regression coefficients with as the response, as the design matrix, as the error variance, and a weighted penalty on .

The solution of (6) is found using block coordinate descent. Let column of and row of without the th element be written and . Then the update to estimate is

| (7) |

where and . Fix at in (5) to update in iteration as

| (8) |

If any root- consistent estimate of is used instead of in (6), then it acts as a warm starting point for the estimation algorithm. This leads to a consistent estimate of in one step of coordinate descent (Zou and Li, 2008). An implementation of this approach for known values of and is summarized in steps (i)–(iv) of Algorithm 1 using R (R Development Core Team, 2016) package glmnet (Friedman et al., 2010).

The estimate of obtained using (7) satisfies properties (a)–(d) described earlier. The adaptive threshold in (7) ensures that property (a) is satisfied. The soft-thresholding rule to estimate ensures that property (b) is satisfied. The local linear approximation (6) has continuous first derivatives in the parameter space excluding zero, so property (c) is also satisfied (Zou and Li, 2008). The estimate satisfies property (d) due to the structured penalty imposed by the prior.

We comment briefly on the choice of prior and uncertainty quantification. We build on the generalized double Pareto prior instead of other shrinkage priors not only because the estimate of satisfies properties (a)–(d), but also because local linear approximation of the resulting penalty has a weighted form. We exploit this for efficient computations and use a warm starting point to estimate a sparse in one step using Algorithm 1. Uncertainty estimates of the nonzero loadings are obtained from Laplace approximation, and the remaining loadings are estimated as 0 without uncertainty quantification.

-

Algorithm 1 Estimation algorithm for expandable factor analysis Notation:

-

1.

is the diagonal matrix containing diagonal elements of a symmetric matrix .

-

2.

Chol() is the upper triangular Cholesky factorization of a symmetric positive definite matrix .

-

3.

is a block diagonal matrix with forming the diagonal blocks.

-

4.

, where .

Input:

-

1.

Data and upper bound on the rank of the loadings matrix.

-

2.

The - grid with grid indices (; ).

Do:

-

1.

Center data about their mean (; ).

-

2.

Let , then estimate eigenvalues and eigenvectors of : and .

-

3.

Define to be the matrix .

-

4.

Begin estimation of , , and across the - grid:

-

For

-

For

-

(i) Define , if , and if ().

-

(ii) Initialize the following statistics required in (7):

-

(iii) Define , , , and required to solve (6):

-

- result glmnet(x = , y = , weights = , intercept = FALSE, standardize = FALSE,

-

penalty.factor = ).

-

- coef(result, s = , exact = TRUE) [-1, ].

-

- ().

-

(v) Set , , , and estimate posterior weight in (10).

-

End for.

-

Set .

-

End for.

-

-

5.

Obtain grid index for the estimate of , where

Return:

-

1.

, , and .

3.3 Root- consistent estimate of

The root- consistent estimate of exists under Assumptions A.0–A.4 given in the appendix. If and () are the eigenvalues and eigenvectors of the empirical covariance matrix , then is the eigen decomposition of . It is known that is a root- consistent estimator of if is fixed and . If , , and , then is a root- consistent estimator of ; see the Supplementary Material for a proof. Scaling by is required because the largest eigenvalue of tends to infinity as (Kneip and Sarda, 2011). This scaling does not change our estimation algorithm for in (7), except is changed to ().

3.4 Bayesian information criterion to select and

The parameter estimates in (7) and (8) depend on the hyperparameters through and , both of which are unknown. To estimate and , we use a grid search. Let and form a - grid. If is the value of (, ) at grid index , then and are the hyperparameters of our prior defined using Lemma 2.2, and and are the parameter estimates based on this prior. Algorithm 1 first estimates and for every by choosing warm starting points and then estimates (, ) using all the estimated and . These two steps in the estimation of (, ) are described next.

The structured penalty imposed by our prior implies that has the maximum number of nonzero loadings. Algorithm 1 exploits this structure by first estimating and then other loadings matrices along the - grid by successively thresholding nonzero loadings in to 0. Let be the set that contains the locations of nonzero loadings in . The estimation path of Algorithm 1 across the - grid is such that () and .

After the estimation of and , is set to if has the maximum posterior probability. Let be the cardinality of set . Given , there are loadings matrices that have nonzero loadings but differ in the locations of nonzero loadings. Assuming that each of these matrices is equally likely to represent the locations of nonzero loadings in the true loadings matrix, the prior for is

| (9) |

Let be the posterior probability of . Then an asymptotic approximation to is

| (10) |

if terms of order smaller than are ignored, where is the joint density of and based on (1). The first term on the right in (10) measures the goodness-of-fit, and the last two terms penalize complexity of a factor model with samples and loadings with the locations of nonzero loadings in . Theorem 4.3 in the next section shows that and have the same asymptotic order under certain regularity assumptions, where is the extended Bayesian information criteria of Chen and Chen (2008) and is an unknown constant. The analytic forms of and are the same when and terms of order smaller than are ignored, so we use for estimating in our numerical experiments.

4 Theoretical properties

Let and be the fixed points of and The updates (7) and (8) define the map , where . The following theorem shows that our estimation algorithm retains the convergence properties of the expectation-maximization algorithm.

Theorem 4.1

Let and be the true loadings matrix and residual variance matrix. We define (; ) and express as having columns. The locations of true nonzero loadings are in the set . Let and be the estimate of and obtained using our estimation algorithm for a specific choice of and (), then is an estimator of . If and , then and retain elements of and with indices in the set . The following theorem specifies the asymptotic properties of , , and .

Theorem 4.2

If Assumptions A.0–A.6 given in the appendix hold and , , and , then for any and ,

-

1.

, , and are consistent estimators of , , and , respectively; and

-

2.

and in distribution, where is a symmetric positive definite matrix and .

Theorem 4.2 holds for any multiscale generalized double Pareto prior with hyperparameters and () that satisfies Assumption A.5. In practice, the estimate of depends on the choice of and . Restricting the search to the hyperparameters indexed along the - grid, Algorithm 1 sets the values of the hyperparameters to and (), where achieves its maximum at grid index . The following theorem justifies this method of selecting hyperparameters and shows the asymptotic relationship between and .

Theorem 4.3

Suppose the generalized double Pareto prior with hyperparameters defined using leads to estimation of . Let be another set that contains the locations of nonzero loadings in an estimated for a given . Define and . If Assumptions A.0–A.7 given in the appendix hold, then for any such that ,

-

1.

in probability as ; and

-

2.

pr as .

5 Data Analysis

5.1 Setup and comparison metrics

We compared our method with those of Caner and Han (2014), Hirose and Yamamoto (2015), Ročková and George (2016), and Witten et al. (2009). The first competitor was developed to estimate the rank of , and the last three competitors were developed to estimate . We used two versions of Ročková and George’s method. The first version used the expectation-maximization algorithm developed in Ročková and George (2016), and the second version added an extra step in every iteration of the algorithm that rotated the loadings matrix using the varimax criterion.

We evaluated the performance of the methods for estimating on simulated data using root mean square error, proportion of true positives, and proportion of false discoveries:

| (11) |

where and were the true and estimated loadings matrices and and were the true and estimated locations of nonzero loadings. We assume that for any and . Since and could differ in sign, mean square error compared their magnitudes.

5.2 Simulated data analysis

The simulation settings were based on examples in Kneip and Sarda (2011). The number of dimensions varied as . The rank of every simulated loadings matrix was fixed at . The magnitudes of nonzero loadings in a column were equal and decreased as , , , , and from the first to the fifth column. The signs of the nonzero loadings were chosen such that the columns of any loadings matrix were orthogonal, with a small fraction of overlapping nonzero loadings between adjacent columns:

The error variances increased linearly from to for . Varying the sample size as , data were simulated using model (1) for all combinations of and . The simulation setup was replicated ten times and all five methods were applied in every replication by fixing the upper bound on the number of factors at . The - grid had dimensions and increased linearly from to and increased linearly from to 3 when and from to when .

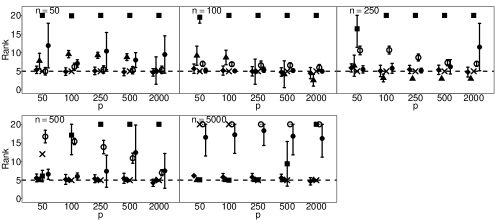

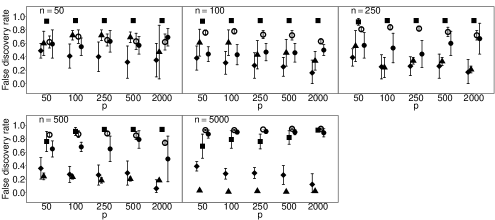

All five methods had the same computational complexity of for one iteration, but their run-time differed depending on their implementations, with Witten et al.’s method being the fastest. Figure 1 shows that Hirose & Yamamoto’s and both versions of Ročková and George’s method significantly overestimated for large . Witten et al.’s method slightly overestimated across all settings. Caner and Han’s method showed excellent performance and accurately estimated across all simulation settings, except when and . When was larger than 500, Assumption A.4 was satisfied and our method accurately estimated as 5 in every setting, performing better than Caner and Han’s method when .

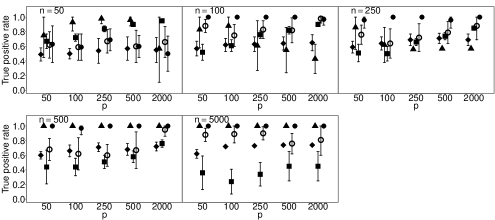

The four methods for estimating differed significantly in their root mean square errors, true positive rates, and false discovery rates; see Figures 2, 3, and 4. Hirose & Yamamoto’s method had the highest false discovery rates and the lowest true positive rates across most settings. Both versions of Ročková and George’s method estimated an overly dense across most settings, resulting in high true positive rates and high false discovery rates. The extra rotation step in the second version of Ročková and George’s method resulted in excellent mean square error performance; however, varimax rotation is a post-processing step. A similar step to reduce the mean square error could be added to our method; for example, by including a step to rotate the in step 3 of Algorithm 1 using the varimax criterion. When and were small, Witten et al.’s method achieved the lowest false discovery rates and our method achieved the highest true positive rates. When and were larger than 250 and 100, respectively, then Assumption A.4 was satisfied and our method simultaneously achieved the highest true positive rates and lowest false discovery rates while maintaining competitive mean square errors relative to the rotation-free methods.

5.3 Microarray data analysis

We used gene expression data capturing aging in mice from the AGEMAP database (Zahn et al., 2007). There were 40 mice aged 1, 6, 16, and 24 months in this study. Each age group included 5 male and 5 female mice. Tissue samples were collected from 16 different tissues, including cerebrum and cerebellum, for every mouse. Gene expression levels in every tissue sample were measured on a microarray platform. After normalization and removing missing data, gene expression data were available for all probes across microarrays. We used a factor model to estimate the effect of latent biological processes on gene expression variation.

AGEMAP data were centered before analysis following Perry and Owen (2010). Gene expression measurements were represented by , where and . Further, agei represented the age of mouse and genderi was 1 if mouse was female and was 0 otherwise. Least square estimates of the intercept, age effect, and gender effect in the linear model (), with idiosyncratic error , were represented as , , and . Using these estimates for , the mean-centered data were defined as

Four mice were randomly held out, and all tissue samples for these mice in were used as test data. The remaining samples were used as training data. This setup was replicated ten times. All four methods were applied to the training data in every replication by fixing the upper bound on the number of factors at . The - grid had dimensions and increased linearly from to , and increased linearly from to 6.

The results for all five methods were stable across all ten folds of cross-validation. Caner and Han’s, Hirose and Yamamoto’s, both versions of Ročková and George’s, Witten et al.’s, and our method selected 10, 10, 10, 4, and 1, respectively, as the number of latent biological process across all folds. Our result matched the result in Perry and Owen (2010), who confirmed the presence of one latent variable using rotation tests. Our simulation results and the findings in Perry and Owen (2010) strongly suggest that our method accurately estimated and the alternative methods overestimated .

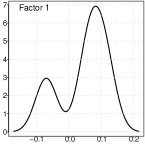

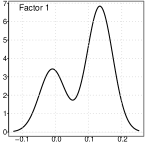

We also estimated the factors for the test data. With denoting test datum and denoting the singular value decomposition of , the factor estimate of test datum was , where was the number of samples in training data. Perry and Owen (2010) found that factor estimates for the tissue samples from cerebrum and cerebellum, respectively, had bimodal densities. We used the density function in R with default settings to obtain kernel density estimates of the factors. Hirose and Yamamoto’s and both version of Ročková and George’s method estimated the number of factors as 10, which made the results challenging to interpret. Witten et al.’s method recovered bimodal densities in all four factors for both tissue samples, but it was unclear which of these four factors corresponded to the factor estimated by Perry and Owen (2010). Our method estimated the number of factors as 1 and recovered the bimodal density in both tissue samples.

Acknowledgement

This work was supported by grants from the National Institute of Environmental Health Sciences, the National Institutes of Health, and the National Science Foundation. The code used in the experiments is available at https://github.com/blayes/xfa.

Appendix A Assumptions

Assumptions A.0–A.4 follow from the theoretical setup for high-dimensional factor models in Kneip and Sarda (2011). Assumption A.5 is based on results in Zou and Li (2008) for variable selection.

-

A.0

Let , , , , , , ().

-

A.1

There exist finite positive constants , , such that , , and (; ).

-

A.2

There exists a constant such that , , , are -subgaussian for every . A random variable is -subgaussian if for any .

-

A.3

Let be the eigenvalues of , then there exists a such that , , , and .

-

A.4

The sample size and dimension are large enough such that and .

-

A.5

Let be the upper bound on and , , , and () are defined as in Lemma 2.2. Then, , , , and () as , , and .

-

A.6

The elements of the set are fixed and do not change as or increase to .

Model (2) is recovered by substituting in A.0. Assumption A.1 ensures that is positive definite. Assumption A.2 ensures the empirical covariances are good approximations of the true covariances. Specifically, for any ,

hold simultaneously with probability at least . If , then as , and . Assumption A.3 guarantees identifiability of when is large and . Assumption A.4 is required to ensure that is a root- consistent estimator of as , , and .

One additional assumption is required to relate and ,

-

A.7

for a fixed constant such that .

Assumption A.7 and Equation 4.6 in Theorem 3 of Kneip and Sarda (2011) imply that for any such that because as .

References

- Ahn and Horenstein (2013) Ahn, S. C. and A. R. Horenstein (2013). Eigenvalue ratio test for the number of factors. Econometrica 81(3), 1203–1227.

- Armagan et al. (2013) Armagan, A., D. B. Dunson, and J. Lee (2013). Generalized double Pareto shrinkage. Statistica Sinica 23(1), 119–143.

- Bai and Li (2012) Bai, J. and K. Li (2012). Statistical analysis of factor models of high dimension. The Annals of Statistics 40(1), 436–465.

- Bai and Ng (2002) Bai, J. and S. Ng (2002). Determining the number of factors in approximate factor models. Econometrica 70(1), 191–221.

- Bhattacharya and Dunson (2011) Bhattacharya, A. and D. B. Dunson (2011). Sparse Bayesian infinite factor models. Biometrika 98(2), 291–306.

- Caner and Han (2014) Caner, M. and X. Han (2014). Selecting the correct number of factors in approximate factor models: The large panel case with group bridge estimators. Journal of Business & Economic Statistics 32(3), 359–374.

- Carvalho et al. (2008) Carvalho, C. M., J. Chang, J. E. Lucas, J. R. Nevins, Q. Wang, and M. West (2008). High-dimensional sparse factor modeling: applications in gene expression genomics. Journal of the American Statistical Association 103(484), 1438–1456.

- Chen and Chen (2008) Chen, J. and Z. Chen (2008). Extended Bayesian information criteria for model selection with large model spaces. Biometrika 95(3), 759–771.

- Dempster et al. (1977) Dempster, A. P., N. M. Laird, and D. B. Rubin (1977). Maximum likelihood from incomplete data via the EM algorithm. Journal of the Royal Statistical Society B 39(1), 1–38.

- Fan and Li (2001) Fan, J. and R. Li (2001). Variable selection via nonconcave penalized likelihood and its oracle properties. Journal of the American Statistical Association 96(456), 1348–1360.

- Friedman et al. (2010) Friedman, J. H., T. J. Hastie, and R. J. Tibshirani (2010). Regularization paths for generalized linear models via coordinate descent. Journal of Statistical Software 33(1), 1–22.

- Geyer (1994) Geyer, C. J. (1994). On the asymptotics of constrained M-estimation. The Annals of Statistics 22(4), 1993–2010.

- Hirose and Yamamoto (2015) Hirose, K. and M. Yamamoto (2015). Sparse estimation via nonconcave penalized likelihood in factor analysis model. Statistics and Computing 25(5), 863–875.

- Jolliffe et al. (2003) Jolliffe, I. T., N. T. Trendafilov, and M. Uddin (2003). A modified principal component technique based on the Lasso. Journal of Computational and Graphical Statistics 12(3), 531–547.

- Kneip and Sarda (2011) Kneip, A. and P. Sarda (2011). Factor models and variable selection in high-dimensional regression analysis. The Annals of Statistics 39(5), 2410–2447.

- Knight and Fu (2000) Knight, K. and W. Fu (2000). Asymptotics for Lasso-type estimators. The Annals of Statistics 28(5), 1356–1378.

- Knowles and Ghahramani (2011) Knowles, D. and Z. Ghahramani (2011). Nonparametric Bayesian sparse factor models with application to gene expression modeling. The Annals of Applied Statistics 5(2B), 1534–1552.

- Onatski (2009) Onatski, A. (2009). Testing hypotheses about the number of factors in large factor models. Econometrica 77(5), 1447–1479.

- Perry and Owen (2010) Perry, P. O. and A. B. Owen (2010). A rotation test to verify latent structure. The Journal of Machine Learning Research 11, 603–624.

- R Development Core Team (2016) R Development Core Team (2016). R: A Language and Environment for Statistical Computing. Vienna, Austria: R Foundation for Statistical Computing.

- Ročková and George (2016) Ročková, V. and E. I. George (2016). Fast Bayesian factor analysis via automatic rotations to sparsity. Journal of the American Statistical Association 111(516), 1608–1622.

- Shen and Huang (2008) Shen, H. and J. Z. Huang (2008). Sparse principal component analysis via regularized low rank matrix approximation. Journal of Multivariate Analysis 99(6), 1015–1034.

- van der Vaart (2000) van der Vaart, A. W. (2000). Asymptotic Statistics, Volume 3. Cambridge University Press.

- Witten et al. (2009) Witten, D. M., R. J. Tibshirani, and T. J. Hastie (2009). A penalized matrix decomposition, with applications to sparse principal components and canonical correlation analysis. Biostatistics 10(3), 515–534.

- Zahn et al. (2007) Zahn, J. M., S. Poosala, A. B. Owen, D. K. Ingram, A. Lustig, A. Carter, A. T. Weeraratna, D. D. Taub, M. Gorospe, K. Mazan-Mamczarz, et al. (2007). AGEMAP: a gene expression database for aging in mice. PLoS Genet 3(11), e201.

- Zou et al. (2006) Zou, H., T. J. Hastie, and R. J. Tibshirani (2006). Sparse principal component analysis. Journal of Computational and Graphical Statistics 15(2), 265–286.

- Zou and Li (2008) Zou, H. and R. Li (2008). One-step sparse estimates in nonconcave penalized likelihood models. The Annals of Statistics 36(4), 1509–1533.

Supplementary Material for Expandable Factor Analysis

Appendix 1 Expectation-maximization algorithm for expandable factor analysis

1.1 Estimation of and

Define the following quantities using mean-centered data:

where is the identity matrix. We place Jeffreys’ prior on the error variances, (). Let and be the estimates of and at iteration , then the conditional expectations of , , and complete data log likelihood at iteration are

| (12) |

where the superscript denotes the dependence on and . The objective (1.1) splits into separate terms, and term depends on and ; therefore, (1.1) is maximized by repeating the following two until steps until convergence to a fixed point:

- 1.

-

2.

Increment to .

1.2 Block coordinate descent algorithm for estimation of

We use local linear approximation of the objective (13) to derive a new block coordinate descent algorithm. We suppress the superscript in and to ease notation. The algorithm initializes at and updates using (13) as

successively for in the th cycle. This objective function is convex and its optimum is

| (14) |

where and . We also exploit the form of (14) and use it to update the th column of . This leads to block updates for in a single cycle of the coordinate descent algorithm. These updates are repeated until the change in is negligible. We then set . We have implemented this algorithm in R (R Development Core Team, 2016) using the glmnet package (Friedman et al., 2010).

1.3 Root- consistent estimates of and

Let be the empirical covariance matrix of mean-centered data and and () be its eigenvalues and eigenvectors, then

| (15) |

is the eigen decomposition of . Use (15) to define

An application of Theorem 2 in Kneip and Sarda (2011) shows that is a root- consistent estimator of when . Equations 4.3 and 4.4 in Kneip and Sarda (2011) and Assumptions A.1–A.4 in the main paper imply that there exist universal positive constants and such that

with probability at least as , , and . This implies that

| (16) |

with probability at least . Since , for large and and (16) reduces to

with probability at least as , , and . This shows that is a root- consistent estimator of . Theorem 3 in Kneip and Sarda (2011) implies that is a root- consistent estimator of for overfitted factor models.

We also prove a result that is used in the proof for asymptotic normality of nonzero loadings.

Lemma 1.1

If Assumptions A.0–A.4 in the main paper hold, then (; ).

Proof Using (15),

| (17) |

where follows because . Equation 4.1 of Theorem 2 in Kneip and Sarda (2011) implies that for some ,

where follows because by Assumption A.4 in the main paper. Substituting in (17) implies that

Therefore, for , which in turn shows that is bounded because .

1.4 Computational complexity

The computational complexity of the estimation algorithm equals the cost of performing penalized regression problems of dimension . Our estimation algorithm requires time upfront to calculate and its eigen decomposition. Estimation of , and in (1.1) involves -dimensional matrix multiplications and inversions of time complexity. Using these matrices, one iteration of the block coordinate descent algorithm has time complexity for dimension (). The total time complexity of each iteration is ; therefore, the time complexity of iterations of the expectation-maximization algorithm is .

Appendix 2 Properties of the multiscale generalized double Pareto prior

2.1 Proof of Lemma 1

If is the support of multiscale generalized double Pareto prior on , then

Since follows generalized double Pareto distribution with parameters , for and

| (18) |

This summation is finite if and for ; therefore, pr.

2.2 Proof of Lemma 2

Let be such that for any . Then,

where follows from the union bound and follows from Markov’s inequality and the independence of s. The assumptions in Lemma 2 of the main paper and (18) imply that

Appendix 3 Theoretical properties of and

3.1 Proof of Theorem 1

Let . Then, the objective function in (1.1) is

| (19) |

where is the log likelihood of scaled by . This leads to the -function

| (20) |

The local linear approximation of (20) is

| (21) |

where is the -function that corresponds to . Theorem 1 of Dempster et al. (1977) shows that , and using this in (19) and (21) shows that and . Subtracting (21) from (19) yields

| (22) |

where

| (23) |

The log function is concave and is majorized by its tangent, so for any ; therefore, because using Lemma 1 and Theorem 1 in Dempster et al. (1977). If maximizes , then

| (24) |

where the last equality follows from (21). The objective (1.1) is bounded in probability on the parameter space, so the sequence converges to some . Using Proposition 1 in Zou and Li (2008), converges to the stationary point .

3.2 Proof of asymptotic normality of nonzero loadings and consistency of estimated

The proof has two steps. First, we show asymptotic normality of nonzero loadings. Second, we use results of the first step to show consistency of the estimated loadings.

Step 1. Let and are the root- consistent sequence of estimators of and (; ) as , , and , then imputing based on the eigen decomposition of in (15) implies that

| (25) |

where is the estimate of obtained using the estimation algorithm of expandable factor analysis,

| (26) |

Again using (15),

| (27) |

If is a matrix independent of and and represents row of , then define

| (28) |

where vectors are added component-wise. Substitute ; ) in (28) to obtain

| (29) |

| (30) |

The limiting forms of all the terms in (30) are derived next. First, we obtain the limiting form of in (30). Because is a root- consistent estimator of , in probability as , , and using Slutsky’s theorem. Second, we obtain the limiting form of in (30). Lemma 1.1 shows that variance of (; ) is bounded, so using (15), Slutsky’s theorem, and the central limit theorem,

| (31) |

as , , and , where the convergence is in distribution and for some symmetric positive definite matrix . Let be the set of s such that is nonzero, then and . If denotes a sub-matrix that contains the rows and the columns of matrix with indices in , then the block partitioned form of the covariance matrix of in (31) based on is

| (32) |

where and include elements of with indices in and , respectively. Finally, the limiting form of is found using arguments in Zou and Li (2008). If , then , , and

in probability by Slutsky’s theorem and the continuous mapping theorem as , , and . Similarly, if , then , , and

| (33) |

in probability by Slutsky’s theorem and the continuous mapping theorem as , , and .

Let , then or . The limiting forms of , , and (; ), and Slutsky’s theorem imply that in distribution for every as , , and , where

| (34) |

Since is convex, the unique minimizer of is

| (35) |

Following the epi-convergence results of Geyer (1994) and Knight and Fu (2000), in distribution (; ) as , , and . Let , , and be the cardinality of set , then

in distribution as , , and using (32), (33), (35), and in distribution (; ). Further,

where is a block diagonal matrix with forming the diagonal blocks. This proves the asymptotic normality of nonzero loadings.

Step 2. We now prove the consistency of (; ). For every , asymptotic normality of implies that in probability, so , where is the estimated set of the locations of nonzero loadings based on . The proof is completed by showing that for all , . Let , then Karush-Kuhn-Tucker optimality condition implies that

| (36) |

The right hand side of (36) is unbounded in probability as , , and because . The left hand side of (36) is

| (37) |

Following arguments similar to those used to derive (31), the first term in (37) is asymptotically normal. The second term in (37) is also asymptotically normal from asymptotic normality of the estimates of nonzero loadings shown previously. By Slutsky’s theorem, the left hand side of (36) is asymptotically normal; therefore,

| (38) |

in probability because asymptotic normality of implies that it is bounded in probability. This proves the consistency of (; ).

3.3 Proof of asymptotic normality and consistency of estimated

We now prove asymptotic normality and consistency of (). We first show that is consistent. For the root- consistent sequence of estimators , (; ), Assumption A.5 in the main paper and the continuous mapping theorem imply that if , , and , then , where convergence is element-wise, and

| (39) |

which proves the consistency of .

The asymptotic normality of follows from Equation (5.19) and Exercise 5.20 in van der Vaart (2000) because the objective for estimating has two continuous derivatives with respect to for any and .

3.4 Lemma required to prove Theorem 3

We use the eigen decomposition of to impute and in Equation (3) of the main paper. Using the notation of Algorithm 1 in the main paper, impute by and by and let , , , and . Then, the hierarchical model for the joint distribution of and after scaling Equation (3) in the main paper by is

| (40) |

The density of the prior for loadings that are estimated to be nonzero in is , where is the density of the generalized double Pareto prior in Section 2.2 of the main paper. The log likelihood of given is

| (41) |

and the log joint density of and given is

| (42) |

The following lemma describes the order of and when is replaced by a consistent estimator of and , , and .

Lemma 3.1

If and are root- consistent estimators of and Assumptions A.0–A.7 in the main paper hold, then

Proof We first show that

Using (41),

where the last equality follows because and are consistent estimators of and (; ). Since and (; ) using Assumption A.1 in the main paper,

by an application of Markov’s inequality and

Therefore,

Proceeding similarly,

using the consistency of .

We complete the proof by showing that

Using the analytic form of in (42),

| (43) |

The first term on the right hand side of (43) after scaling by is

The last equality follows from Assumption A.5 in the main paper and using conditions that and . The second term on the right hand side of (43) after scaling by is

The last equality follows from Assumption A.5 in the main paper, from consistency of , and using conditions that and . The proof is completed by using (42) to obtain that

3.5 Proof of Theorem 3

The proof consists of three steps: derive the asymptotic form of ; show that ; and show that the sufficient condition for model selection consistency of ebicγ() holds under the assumptions of Theorem 3 in the main paper.

We use the following notation for ease of presentation. If is a set of indices and is a matrix, then is a sub-matrix that contains columns of with indices in and is a sub-matrix that contains rows and columns of with indices in .

Step 1. Using (40), the density of the prior for loadings that are estimated to be nonzero in is ; see Section 3.4 also. Use the Gaussian scale mixture representation for the density of generalized double Pareto prior to write in form of differentiable functions when ; see the equation for E-step in Section 4.4.1 of Armagan et al. (2013) for details related to the Gaussian scale mixture representation for the generalized double Pareto density. Define the diagonal matrix as

and let

be the diagonal element of corresponding to such that . If is the joint density of and defined using (40), then define another diagonal matrix as

| (44) |

If represents in (44) evaluated at , then the diagonal element of that corresponds to the index is

| (45) |

The equality in (45) follows because , , and from Theorem 2 in the main paper and Assumptions A.0–A.6 in the main paper. The posterior probability of , denoted as , equals

| (46) |

where is the marginal likelihood of the factor model in (40) with the locations of nonzero loadings contained in the set , , and is prior defined in Equation (9) in the main paper. Using Laplace approximation and (45),

| (47) |

where using Assumption A.1 in the main paper. Further, using (46),

Sterling’s approximation and Theorem 2 imply that ; therefore, the previous equation after using (47) reduces to

| (48) |

Step 2. The definition of in Chen and Chen (2008) for regression models implies that

| (49) |

where is a root- consistent estimate of (; ) in (40), is the Gaussian likelihood defined using (40), and is a tuning parameter such that . Lemma 3.4 implies that there exists a universal constant such that

| (50) |

Let . Then, Theorem 2 in the main paper and (50) imply that

| (51) |

Step 3. Let be an upper bound on in (40) such that . If has positive eigen values for any such that , , and , then uniformly for any such there is a universal positive constant and a positive constant depending on such that

| (52) |

see the definition of asymptotic identifiability condition on pages 762–763 in Chen and Chen (2008) and the proof of Theorem 1 in Chen and Chen (2008). Using (51) and (52), as for any such that and . The proof is completed by showing has positive eigen values for any such that . Assumption A.7 implies that has at least positive eigen values, so , which has positive eigenvalues equal to for any .

Appendix 4 Microarray data analysis

The AGEMAP data (Zahn et al., 2007) were obtained from http://statweb.stanford.edu/~owen/data/AGEMAP/.

The - grid in expandable factor analysis had 20 different and 20 different values: , where (), and , where (). Our estimation algorithm estimated at grid points (, ) (; ). The results of our estimation algorithm were stable in that the estimated rank of was the same at most points on the - grid across 10 folds of cross-validation (Table 1).

| 10 | 10 | 10 | 10 | 10 | 10 | 10 | 9 | 9 | 8 | 8 | 7 | 7 | 7 | 6 | 6 | 6 | 6 | 6 | 5 | |

| 10 | 10 | 10 | 10 | 10 | 10 | 9 | 9 | 8 | 8 | 7 | 7 | 6 | 6 | 6 | 6 | 6 | 5 | 5 | 5 | |

| 10 | 10 | 10 | 10 | 9 | 9 | 8 | 8 | 7 | 7 | 6 | 6 | 6 | 6 | 6 | 5 | 5 | 5 | 5 | 4 | |

| 10 | 10 | 10 | 9 | 9 | 8 | 7 | 7 | 7 | 6 | 6 | 6 | 6 | 5 | 5 | 5 | 5 | 4 | 4 | 4 | |

| 10 | 10 | 9 | 8 | 8 | 7 | 7 | 6 | 6 | 6 | 6 | 5 | 5 | 5 | 4 | 4 | 4 | 4 | 4 | 4 | |

| 10 | 9 | 8 | 7 | 7 | 6 | 6 | 6 | 6 | 5 | 5 | 4 | 4 | 4 | 4 | 4 | 4 | 4 | 4 | 3 | |

| 8 | 7 | 7 | 6 | 6 | 6 | 6 | 5 | 4 | 4 | 4 | 4 | 4 | 4 | 4 | 4 | 3 | 3 | 3 | 3 | |

| 7 | 6 | 6 | 6 | 6 | 5 | 4 | 4 | 4 | 4 | 4 | 4 | 4 | 3 | 3 | 3 | 3 | 3 | 3 | 3 | |

| 6 | 6 | 5 | 4 | 4 | 4 | 4 | 4 | 4 | 4 | 3 | 3 | 3 | 3 | 3 | 3 | 2 | 2 | 2 | 2 | |

| 5 | 4 | 4 | 4 | 4 | 4 | 3 | 3 | 3 | 3 | 3 | 3 | 2 | 2 | 2 | 2 | 2 | 2 | 2 | 2 | |

| 4 | 4 | 4 | 3 | 3 | 3 | 3 | 3 | 2 | 2 | 2 | 2 | 2 | 2 | 2 | 2 | 2 | 2 | 2 | 2 | |

| 3 | 3 | 2 | 2 | 2 | 2 | 2 | 2 | 2 | 2 | 2 | 2 | 2 | 2 | 1 | 1 | 1 | 1 | 1 | 1 | |

| 2 | 2 | 2 | 2 | 2 | 2 | 2 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | |

| 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | |

| 1 | 1 | 1 | 1 | 1 | 1 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |