Statistical Skorohod embedding problem and its generalizations

Abstract

Given a Lévy process , we consider the so-called statistical Skorohod embedding problem of recovering the distribution of an independent random time based on i.i.d. sample from Our approach is based on the genuine use of the Mellin and Laplace transforms. We propose a consistent estimator for the density of derive its convergence rates and prove their optimality. It turns out that the convergence rates heavily depend on the decay of the Mellin transform of We also consider the application of our results to the problem of statistical inference for variance-mean mixture models and for time-changed Lévy processes.

Keywords: Skorohod embedding problem, Lévy process, Mellin transform, Laplace transform, variance mixture models, time-changed Lévy processes.

1 Introduction

The so called Skorohod embedding (SE) problem or Skorohod stopping problem was first stated and solved by Skorohod in 1961. This problem can be formulated as follows.

Problem 1.1 (Skorohod Embedding Problem).

For a given probability measure on such that and find a stopping time such that and is a uniformly integrable martingale.

The SE problem has recently drawn much attention in the literature, see e.g. Obłój, [11], where the list of references consists of more than 100 items. In fact, there is no unique solution to the SE problem and there are currently more than different solutions available. This means that from a statistical point of view, the SE problem is not well posed. In this paper we first study what we call statistical Skorohod embedding (SSE) problem.

Problem 1.2 (Statistical Skorohod Embedding Problem).

Based on i.i.d. sample from the distribution of consistently estimate the distribution of the random time where and are assumed to be independent.

The independence of and is needed to ensure the identifiability of the distribution of from the distribution of . It is shown that the SSE problem is closely related to the multiplicative deconvolution problem. Using the Mellin transform technique, we construct a consistent estimator for the density of and derive its convergence rates in different norms. Furthermore, we show that the obtained rates are optimal in minimax sense. The asymptotic normality of the proposed estimator is addressed as well. Next, we generalize the SSE problem by replacing the standard Brownian motion with a general Lévy process. The generalized SSE problem turns out to be much more involved and its solution requires some new ideas. Using a genuine combination of the Laplace and Mellin transforms, we construct a consistent estimator, derive its minimax convergence rates and prove that these rates basically coincide with the rates in the SSE problem.

Some particular cases of generalized statistical Skorohod embedding problem have been already studied in the literature. For example, the case of the stopped Poisson process was considered in the recent paper of Comte and Genon-Catalot, [6].

2 Statistical Skorohod embedding problem

Let be a Brownian motion and let a random variable be independent of We then have,

| (1) |

and the problem of reconstructing is related to a multiplicative deconvolution problem. While for additive deconvolution problems the Fourier transform plays an important role, here we can conveniently use the Mellin transform.

Definition 2.1.

Let be a non-negative random variable with a probability density , then the Mellin transform of is defined via

| (2) |

for all with

Since is a density, it is integrable and so at least Under mild assumptions on the growth of near the origin, one obtains

for some Then the Mellin transform (2) exists and is analytic in the strip For example, if is essentially bounded in a right-hand neighborhood of zero, we may take The role of the Mellin transform in probability theory is mainly related to the product of independent random variables: in fact it is well-known that the probability density of the product of two independent random variables is given by the Mellin convolution of the two corresponding densities. Due to (1), the SSE problem is closely connected to the Mellin convolution. Suppose that the random time has a density and that we may take Since we derive for

As a result

and the Mellin inversion formula yields

| (3) | ||||

Furthermore, the Mellin transform of can be directly estimated from the data via the empirical Mellin transform:

| (4) |

where the condition guarantees that the variance of the estimator (4) is finite. Note however that the integral in (3) may fail to exist if we replace by We so need to regularize the inverse Mellin operator. To this end, let us consider a kernel supported on and a sequence of bandwidths tending to as Then we define, in view of (4), for some

| (5) |

For our convergence analysis, we will henceforth take the simplest kernel

but note that in principle other kernels may be considered as well. The next theorem states that converges to at a polynomial rate, provided the Mellin transform of decays exponentially fast. We shall use throughout the notation if is bounded by a constant multiple of , independently of the parameters involved, that is, in the Landau notation .

Theorem 2.2.

For any and , introduce the class of functions

Assume that for some and

| (6) |

Then for some constant depending on and only, it holds

| (7) |

By next choosing

| (8) |

we arrive at the rate

| (9) |

as

With a little bit more effort one can prove the strong uniform convergence of the estimate

Theorem 2.3.

Under conditions of Theorem 2.2 and for

Let us turn now to some examples.

Example 2.4.

Example 2.5.

Let us look at the family of densities

We have

Therefore, for all and implying

for any provided

If decays polynomially fast, we get the following result.

Theorem 2.6.

Consider the class of functions

and assume that for some and and as in (6). Then for some constant it holds

| (10) |

By choosing

| (11) |

if and

| (12) |

for we arrive at

| (13) |

Remark 2.7.

Due to the relation

the conditions and are closely related to the smoothness properties of the function For example, if then

and the function is called supersmooth in this case, see Meister [9] for the discussion on different smoothness classes in the context of the additive deconvolution problems.

The rates of Theorem 2.2 and Theorem 2.6 summarized in Table 1 are in fact optimal (up to a logarithmic factor) in minimax sense for the classes and respectively.

Theorem 2.8.

Fix some There are and such that

for some where the infimum is taken over all estimators (i.e. all measurable functions of ) of and is the distribution of the i.i.d. sample with and

2.1 Asymptotic normality

In the case of the estimate can be written as

where

The following theorem holds

Theorem 2.9.

Suppose that

and

then

for some where and for some as

3 Generalised statistical Skorohod embedding problem

In this section we generalize the statistical Skorohod embedding problem to the case of Lévy processes. In particular, we consider the following problem.

Problem 3.1.

Based on i.i.d. sample from the distribution of estimate the distribution of the random time independent of a Lévy process such that

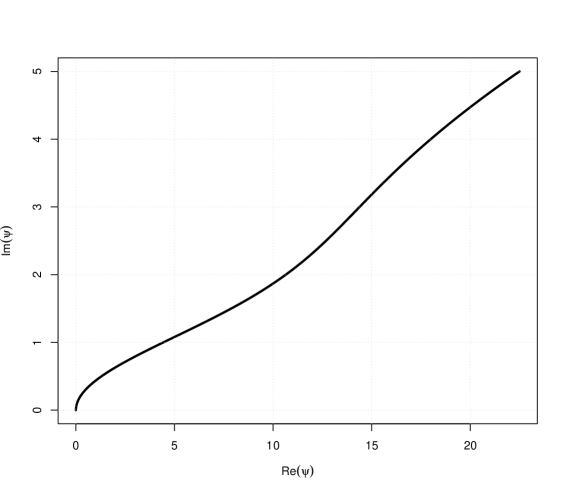

Note that the situation here is much more difficult than before, since the Lévy processes do not have, in general, the scaling property (1). Hence the approach based on the Mellin deconvolution technique can not be applied any longer. Let be a Lévy process with the triplet Define a curve in

where Our approach to reconstruct the distribution of is based on the simple identity

| (14) |

It is well known that the Laplace transform of is analytic in the domain

The following proposition shows that the object is well defined and that it can be related to the Fourier transform of which in turn can be estimated from the data.

Proposition 3.2.

Let us assume that as and that

| (15) |

for all and some Moreover, let be (essentially) bounded. Then, for it holds that

Remark 3.3.

The condition (15) is fulfilled if, for example, the diffusion part of is nonzero or if is real and as

Under the assumptions of Proposition 3.2 we may write,

where due to (14). On other hand, one may straightforwardly derive,

i.e.,

| (16) |

In principle, one can now replace the Fourier transform of in (16) by its empirical counterpart based on the data. However, in this case we need to regularize the estimate of to perform the inverse Mellin transform. To this end consider the approximation

and define in view of (16),

| (17) |

where in a suitable way as Note that in many cases the function can be found in closed form. For example, consider the case of a subordinated stable Lévy process with It then holds for

where is Kummer’s function. In the next two theorems we prove a remarkable result showing that the estimate converges to at the same rate (up to a logarithmic factor in the polynomial case) as in the case of the time-changed Brownian motion.

Theorem 3.4.

Remark 3.5.

Since

the condition (18) is, for example, fulfilled for some if for and is of bounded variation with

In the case we get exactly the same logarithmic rates as in Theorem 2.6.

Theorem 3.6.

Discussion

The rates in Theorem 3.4 and Theorem 3.6 are optimal in minimax sense, since they are basically coincides (up to a logarithmic factor) with the rates in Theorem 2.2 and Theorem 2.6, respectively. As can be seen from the proof of Theorem 2.8 and Remark 3.5, the lower bonds continue to hold true under the additional assumption (18). Let us also stress that the class is quite large and contains the well known families of distributions such as Gamma, Beta and Weibull families. It follows from Theorem 3.4 that for all these families our estimator converges at a polynomial rate.

4 Applications

4.1 Estimation of the variance-mean mixture models

The variance-mean mixture of the normal distribution is defined as

where is a mixing density on The variance-mean mixture models play an important role in both the theory and the practice of statistics. In particular, such mixtures appear as limit distributions in asymptotic theory for dependent random variables and they are useful for modeling data stemming from heavy-tailed and skewed distributions, see, e.g. [1] and [3]. As can be easily seen, the variance-mean mixture distribution coincides with the distribution of the random variable where is the random variable with density which is independent of The class of variance-mean mixture models is rather large. For example, the class of the normal variance mixture distributions () can be described as follows: is the density of a normal variance mixture (equivalently is the density of ) if and only if is a completely monotone function in The problem of statistical inference for variance-mean mixture models has been already considered in the literature. For example, Korsholm, [8] proved the consistency of the non-parametric maximum likelihood estimator for the parameters and being treated as an infinite dimensional nuisance parameter. In Zhang [14] the problem of estimating the mixing density in location (mean) mixtures was studied. To the best of our knowledge, we here address, for the first time, the problem of non-parametric inference for the mixing density in full generality and derive the minimax convergence rates. In fact, Theorem 3.4 and Theorem 3.6 directly apply not only to normal variance-mean mixture models, but also to stable variance-mean mixtures.

4.2 Estimation of time-changed Lévy models

Let be a one-dimensional Lévy process and let be a non-negative, non-decreasing stochastic process independent of with . A time-changed Lévy process is then defined as The process is usually referred to as time change or subordinator. Consider the problem of statistical inference on the distribution of the time change based on the low-frequency observations of the time-changed Lévy process Suppose that observations of the Lévy process at times are available. If the sequence is strictly stationary with the invariant stationary distribution then for any bounded “test function”

| (24) |

The limiting expectation in (24) is then given by

Taking we arrive at the the following representation for the c.f. of :

| (25) |

where with being the characteristic exponent of the Lévy process and being the Laplace transform of Suppose we want to estimate the invariant measure (or its density) from the discrete time observations of then we are in the setting of the generalized statistical Skorohod embedding with the only difference that the elements of the sample are not necessarily independent. However, under appropriate mixing properties of the sequence one can easily generalize the results of Section 3 to the case of dependent data (see, e.g. [2] for similar results). The problem of estimating the parameters of a Lévy process observed at low frequency was considered in Neumann and Reiß, [10] and Chen et al, [5]. Let us note that the statistical inference for time-changed Lévy processes based on high-frequency observations of has been the subject of many studies, see, e.g. Bull, [4] and Todorov and Tauchen, [12] and the references therein.

5 Numerical examples

Barndorff-Nielsen et al. [1] consider a class of variance-mean mixtures of normal distributions which they call generalized hyperbolic distributions. The univariate and symmetric members of this family appear as normal scale mixtures whose mixing distribution is the generalized inverse Gaussian distribution with density

| (26) |

for some and where is a modified Bessel function. The resulting normal scale mixture has probability density function

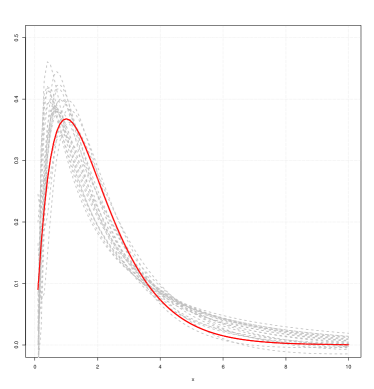

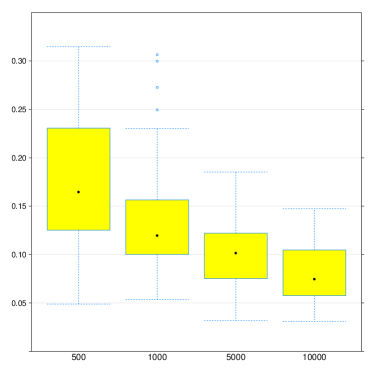

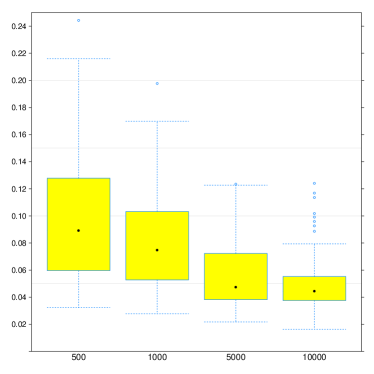

Let us start with a simple example, Gamma density which is a special case of (26) for and We simulate a sample of size from the distribution of and construct the estimate (5) with the bandwidth given (up to a constant not depending on ) by (8) and In Figure 2 (left), one can see estimated densities based on independent samples from of size together with in red. Next we estimate the distribution of the loss based on independent repetitions of the estimation procedure. The corresponding box plots for different are shown in Figure 2 (right).

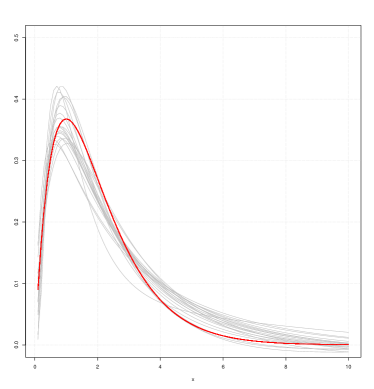

Let us now turn to a more interesting example of variance-mean mixtures. We take and choose to follow a Gamma distribution with the density The estimate (17) is constructed as follows. First note that In order to numerically compute the function for with we use the decomposition

| (27) | ||||

where is the empirical characteristic function and This decomposition follows from a Cauchy argument similar as in the proof of Proposition 3.2 and is quite useful to reduce the cost of computing the integral in (27), since the integral on the r.h.s. of (27) is much easier to compute due to the asymptotic relation Next we take and as in Theorem 3.4 with and (see Example 2.4). Figure 3 shows the performance of the estimate defined in (17): on the left-hand side independent realizations of the estimate for are shown together with the true density The box plots of the loss based on runs of the algorithm are depicted on the right-hand side of Figure 3. By comparing the right-hand sides of Figure 2 and Figure 3, we observe that the performances of the estimates (17) and (5) are similar, although the estimate (5) seem to have higher variance. This supports the claim of Theorem 3.4 about the same convergence rates in statistical Skorohod embedding and generalized statistical Skorohod embedding problems, given that

6 Proofs

6.1 Proof of Theorem 2.2

First let us estimate the bias of We have

Hence

and we then have the estimate,

| (28) |

As to the variance, by the simple inequality which holds for any random function with we get

| (29) |

Note that

due to (6). We obtain from (29) due to Corollary 7.4 (see Appendix) and by taking into account (6),

and so (7) follows with Finally, by plugging (8) into (7) we get (9) and the proof is finished.

6.2 Proof of Theorem 2.6

6.3 Proof of Theorem 2.8

Our construction relies on the following basic result (see [13] for the proof).

Theorem 6.1.

Suppose that for some and there are two densities such that

If the observations in model follow the product law under the density and

holds for some , then the following lower bound holds for all density estimators based on observations from model :

If the above holds for fixed and all , then the optimal rate of convergence in a minimax sense over is not faster than .

6.3.1 Proof of a lower bound for the class

Let us start with the construction of the densities and Define for any and two auxiliary functions

and

The properties of the functions and are collected in the following lemma.

Lemma 6.2.

The function is a probability density on with the Mellin transform

The Mellin transform of the function is given by

| (30) |

Hence

Set now for any

where stands for the multiplicative convolution of two functions and on defined as

The following lemma describes some properties of and

Lemma 6.3.

For any the function is a probability density satisfying

Moreover, and are in for all and with depending on

Proof.

Let and be two random variables with densities and respectively. Then the density of the r.v. is given by

For the Mellin transform of we get

| (31) |

Lemma 6.4.

The -distance between the densities and fulfills

Proof.

6.3.2 Proof of a lower bound for the class

Define for any and

and

The properties of the functions and can be found in the next lemma.

Lemma 6.5.

The function is a probability density on with the Mellin transform

The Mellin transform of the function is given by

| (34) |

where Hence

Set now for any

where stands for the multiplicative convolution of two functions and on defined via

Lemma 6.6.

For any the function is a probability density satisfying

where is a fixed number. Moreover, and are in for all and

Proof.

First note that

Furthermore, with

and

By taking we get for

The well known Erdélyi lemma implies

and

Hence

| (35) |

Analogously

Combining the previous estimates, we arrive at

It remains to note that the maximum of r.h.s of (35) is attained for and

The property for all and with depending on follows from the identity and (34). ∎

Let and be two random variables with densities and respectively. The the density of the r.v. is given by

For the Mellin transform of we have

| (36) |

Lemma 6.7.

The -distance between the densities and satisfies

Proof.

6.4 Proof of Proposition 2.3

6.5 Proof of Proposition 2.9

We have

Note that

and furthermore

Without loss of generality we may take (for the proof is similar). Observe that for

| (39) |

for some constants (depending on ), and that

| (40) |

for some Let for . By the estimates (39) and (40), one can straightforwardly derive that the integral

can be bounded from above as

for Similarly

and

for some Hence

Now let us study the asymptotic behaviour of the integral To this end, we will use the Stirling formula

First consider the integrand of in the case where

Then on the set

we define with to get

Note that due to the choice of and Using the asymptotic expansion

we derive

Analogously, on the set

we define with to get

Hence the integral can be decomposed as follows

where

with

Using the saddle point method (see, e.g., de Bruijn, [7]), it is easy to show that

uniformly in As a result

Combining all above estimates, we finally get

6.6 Proof of Proposition 3.2

Let be such that At the arc it holds that

for where

6.7 Proof of Proposition 3.4

7 Appendix

Proposition 7.1.

Let be a sequence of independent identically distributed random variables. Fix some and define

Furthermore let be a positive monotone decreasing Lipschitz function on such that

| (43) |

Suppose that and for some Then with probability

| (44) |

Proof.

Fix a sequence as Denote

where is a random variable with the same distribution as . The main idea of the proof is to show that

| (45) | |||||

| (46) |

under a proper choice of the sequence

Step 1. The aim of the first step is to show (45). Consider the sequence and cover each

interval by

disjoint small

intervals of

the length Let be the centers

of these intervals. We have for any natural

Hence for any positive ,

| (47) |

We proceed with the first summand in (47). It holds for any

| (48) | |||||

where is the Lipschitz constant of and is a random variable distributed as . Next, the Markov inequality implies

for any Note that

for some constant depending on and we obtain from (48)

Hence if and we get Now we turn to the second term on the right-hand side of (47). Applying the Bernstein inequality, we get

Similarly,

Therefore

Set now and then

Assuming that for some , we arrive at

Step 2. Now we turn to (46). Consider the sequence

By the Markov inequality we get for any

Set , then it holds for any

By the Borel-Cantelli lemma,

From here it follows that . This completes the proof. ∎

Lemma 7.2.

Let be a Lévy process with the triplet Suppose that and that and are not both zero. It then holds for

| (49) |

Further, if

| (50) |

we have

| (51) |

If we have in the case

| (52) |

and in the case

| (53) |

Proof.

In general we have

| (54) |

where

| (55) | ||||

Note that

with and that

by Riemann-Lebesgue. This yields (49)- It is not difficult to show by standard arguments that due to the integrability condition we have

Next, (49)- follows by observing that

where is bounded for Suppose By (50), and since we have (51)- and (51)- is obvious. Next suppose i.e. We then have,

and

If we thus have

and we observe that

so in particular while Hence (52)- is shown. Then,

and note again that is bounded, hence we have (52)- Finally, if and let us write

where

but due to dominated convergence also

Hence,

and from this (53)- For the derivative we have,

by similar arguments, i.e. (53)- ∎

Lemma 7.3.

For any there exist positive constants and such that uniformly for

| (56) |

Corollary 7.4.

For all and all it holds

| (57) |

for a constant For we have

| (58) |

where does not depend on

References

- [1] O Barndorff-Nielsen, John Kent, and Michael Sørensen. Normal variance-mean mixtures and z distributions. International Statistical Review, 50(2):145–159, 1982.

- [2] Denis Belomestny. Statistical inference for time-changed Lévy processes via composite characteristic function estimation. The Annals of Statistics, 39(4):2205–2242, 2011.

- [3] Nicholas H Bingham and Rüdiger Kiesel. Semi-parametric modelling in finance: theoretical foundations. Quantitative Finance, 2(4):241–250, 2002.

- [4] Adam D Bull. Estimating time-changes in noisy Lévy models. arXiv preprint arXiv:1312.5911, 2013.

- [5] Song X Chen, Aurore Delaigle, and Peter Hall. Nonparametric estimation for a class of Lévy processes. Journal of Econometrics, 157(2):257–271, 2010.

- [6] Fabienne Comte and Valentine Genon-Catalot. Adaptive Laguerre density estimation for mixed poisson models. Archives-Ouvertes, 2014.

- [7] Nicolaas Govert De Bruijn. Asymptotic methods in analysis, volume 4. Courier Dover Publications, 1970.

- [8] Lars Korsholm. The semiparametric normal variance-mean mixture model. Scandinavian journal of statistics, 27(2):227–261, 2000.

- [9] Alexander Meister. Deconvolution problems in nonparametric statistics, volume 193. Springer, 2009.

- [10] Michael H Neumann, Markus Reiß, et al. Nonparametric estimation for Lévy processes from low-frequency observations. Bernoulli, 15(1):223–248, 2009.

- [11] Jan Obłój et al. The Skorokhod embedding problem and its offspring. Probability Surveys, 1:321–392, 2004.

- [12] Viktor Todorov and George Tauchen. Realized Laplace transforms for pure-jump semimartingales. The Annals of Statistics, 40(2):1233–1262, 2012.

- [13] Alexandre B Tsybakov. Introduction to nonparametric estimation, volume 11. Springer, 2009.

- [14] Cun-Hui Zhang. Fourier methods for estimating mixing densities and distributions. The Annals of Statistics, pages 806–831, 1990.