Exact and Asymptotic Tests on a Factor Model in Low and Large Dimensions with Applications

Taras Bodnara††Corresponding Author: Taras Bodnar. E-Mail: taras.bodnar@math.su.se. Tel: +46 8 164562. Fax: +46 8 612 6717. This research was partly supported by the Deutsche Forschungsgemeinschaft via the Research Unit FOR 1735 ”Structural Inference in Statistics: Adaptation and Efficiency”. The first author appreciates the financial support of SIDA via the project 1683030302. and Markus Reißb

a Department of Mathematics, Stockholm University, Roslagsvägen 101, SE-10691 Stockholm, Sweden

a Department of Mathematics, Humboldt-University of Berlin, Unter den Linden 6, D-10099 Berlin, Germany

Zusammenfassung

In the paper, we suggest three tests on the validity of a factor model which can be applied for both, small-dimensional and large-dimensional data. The exact and asymptotic distributions of the resulting test statistics are derived under classical and high-dimensional asymptotic regimes. It is shown that the critical values of the proposed tests can be calibrated empirically by generating a sample from the inverse Wishart distribution with identity parameter matrix. The powers of the suggested tests are investigated by means of simulations. The results of the simulation study are consistent with the theoretical findings and provide general recommendations about the application of each of the three tests. Finally, the theoretical results are applied to two real data sets, which consist of returns on stocks from the DAX index and on stocks from the S&P 500 index. Our empirical results do not support the hypothesis that all linear dependencies between the returns can be entirely captured by the factors considered in the paper.

AMS 2010 subject classifications: 91G70, 62H25, 62H15, 62H10, 62E15, 62E20, 60B20

JEL Classification: C12, C38, C52, C55, C58, C65 G12

Keywords: factor model, exact test, asymptotic test, high-dimensional test, high-dimensional asymptotics, precision matrix, inverse Wishart distribution, random matrix theory.

1 Introduction

Factor models are widely spread in different fields of science, especially, in economics and finance where this type of models have been increasing in popularity recently. They are often used in forecasting mean and variance (see, e.g., Stock and Watson, 2002a [79]; Stock and Watson, 2002b [80], Marcellino et al., [62], Artis et al., [6], Boivin and Ng, [24], Anderson and Vahid, [5] and the references therein), in macroeconomic analysis (see, Bernanke and Boivin, [18], Favero et al., [45], Giannone et al., [47]), in portfolio theory (see, Ross, [71, 72], Engle and Watson, [37], Chamberlain, 1983b [30], Chamberlain and Rothschild, [31], Diebold and Nerlove, [35], Fama and French, [39, 40], Aguilar and West, [3], Bai, [7], Ledoit and Wolf, [58]). Factor models are also popular in physics, psychology, biology (e.g., Rubin and Thayer, [73], Carvalho et al., [28]) as well as in multiple testing theory (e.g., Friguet et al., [46], Dickhaus, [34], Fan et al., 2012a [42]).

Another stream of research related to factor models deals with the estimation of high-dimensional covariance and precision matrices. This approach is motivated by a rapid development of high-dimensional factor models during the last years (Bai and Ng, [10, 11], Bai and Li, [9], Bai, [8]). Fan et al., [41], Fan et al., 2012b [44], Fan et al., [43] among others have suggested several methods for estimating the covariance and precision matrices based on factor models in high dimensions and applied their results to portfolio theory, whereas Ledoit and Wolf, [58] have proposed to combine the sample covariance matrix with the single-factor model based estimator in order to improve the estimate of the covariance matrix. Here, they use the capital asset pricing model (CAPM) as a single-factor model. Ross, [71, 72] argues that the empirical success of the CAPM can be explained by the validity of the following three assumptions: i) there are many assets; ii) the market permits no arbitrage opportunity; iii) asset returns have a factor structure with a small number of factors. He also presents a heuristic argument that if an infinite number of assets is present on the market, then it is possible to construct sufficiently many riskless portfolios. In Chamberlain, 1983b [30], conditions are derived under which this heuristic argument of Ross is justified. Furthermore, Chamberlain and Rothschild, [31] suggest the so-called approximate -factor structure model where the number of assets is assumed to be infinite, while Fan et al., [41] and Li et al., [59] extend this model by considering an asymptotically infinite number of known and unknown factors, respectively.

Let be the observation data for the -th cross-section unit at time . For instance, in the case of portfolio theory, represents the return of the -th asset at time . Let be the observation vector at time and let be a -dimensional vector of common observable factors at time . Then the factor model in vector form is expressed as

| (1) |

where is the matrix of factor loadings and , , are independent errors with covariance matrix . It is also assumed that are independent in time as well as independent of . The estimation of the factor model or the covariance matrix resulting from the factor model with observable factors is considered by Fan et al., [41], whereas Bai, [7], Bai and Li, [9], Fan et al., [43] present the results under the assumption that the factors are unobservable. Moreover, Bai and Ng, [10], Hallin and Liška, [52], Kapetanios, [57], Onatski, [67], Ahn and Horenstein, [4] among others deal with the problem of determining the number of factors used in (1). Note that not in all models the factors are observable. For example, this is not the case in many applications in psychology or in multiple testing theory, and, consequently, the results derived in the present paper cannot be directly applied. On the other hand, factor models with observable variables are usually considered in economics and finance where we also provide two empirical illustrations of the obtained theoretical results.

Under the generic assumption that is a diagonal matrix, the dependence between the elements of is fully determined by the factors . This means that the precision matrix of has the following structure

| (2) |

where is a matrix and is a diagonal matrix, if the factor model (1) is true, i.e., if all linear dependencies among the components of are fully captured by the factor vector . As a result, the test on the validity of the factor model (1) is equivalent to testing

| (3) |

for some positive constants .

We contribute to the existing literature on factor models by deriving exact and asymptotic tests on the validity of the factor model which are based on testing (3). Furthermore, the distributions of the suggested test statistics are obtained under both hypotheses and also they are analyzed in detail when the dimension of the factor model tends to infinity as the sample size increases such that . This asymptotic regime is known in the statistical literature as double asymptotic regime or high-dimensional asymptotics.

Alternatively to the test (3), one can apply the classical goodness-of-fit test which is based on the estimated residuals given by

where is an estimate of the factor loading matrix. This approach, however, does not always lead to reliable results. To see this, let , , and . If is estimated by applying the least square method, i.e., , then

where is the -dimensional identity matrix. Under the assumption of normality it holds that ( dimensional matrix variate normal distribution with zero mean matrix and covariance matrix ) and, consequently, . Hence, are autocorrelated and their distribution depends on the factor matrix , although the true residuals are independent and their distribution does not depend on . This unpleasant property of surely influences testing procedures based on . It is remarkable that in contrast to the test based on the covariance matrix of the residuals, the suggested approach which is based on the precision matrix does not suffer from this problem. Moreover, our tests can be applied without imposing an additional identifiability condition on the model, i.e., it is not assumed that the factors are orthogonal, since the estimator for the matrix of factor loadings does not play any role in the derived test theory.

The rest of the paper is organized as follows. In the next section, we provide the mathematical motivation for the testing procedures (considered in the paper). In Section 3, two finite sample tests are suggested which are constructed in two steps. First, marginal test statistics are constructed and then the maxima of the marginal test statistics are calculated. We further prove that the distributions of the maxima do not depend on and, consequently, the corresponding critical values can be calibrated via simulations. In Section 4, the likelihood ratio test is investigated. Similarly to the tests of Section 3, the distribution of the likelihood ratio statistic does not depend on used in (3) under the null hypothesis. The results are extended to the case of high-dimensional factor models in Section 5. Here, the high-dimensional asymptotic distributions of the test statistics considered in Sections 3 and 4 are derived. The cases of and are treated separately in detail. The results of the simulation study in Section 6 illustrate the size and power of the suggested tests, whereas an empirical study is provided in Section 7. We summarize our findings in Section 8. Proofs are given in the appendix.

2 Mathematical Motivation of Three Tests

A test on the hypothesis (3) can be performed in different ways. Below, we provide a full mathematical motivation for the three approaches considered in the paper.

The first method is based on testing the hypothesis that all non-diagonal elements of are equal to zero, i.e.,

| (4) |

where .

The second approach is based on the following result

Lemma 1.

Let be a symmetric positive-definite matrix and let . Then holds for all and is a diagonal matrix if and only if for all .

The proof of Lemma 1 is given in the appendix. This result motivates the reformulation of the hypothesis (3) in the following way

| (5) |

where .

The third procedure is based on Hadamard’s inequality (see, e.g., Section 4.2.6 of Lütkepohl, [61]): for any positive definite symmetric matrix it holds that

with equality only if is a diagonal matrix. This approach leads to the hypothesis expressed as

| (6) |

3 Small Sample Tests: are Finite

Let

| (7) |

be the sample covariance matrix calculated for the sample with . It is used to estimate . In (7) the sample mean vector of is not subtracted since the population mean vector is zero following (1) and the assumptions that and . If model (1) is extended by adding a mean vector, i.e., to

| (8) |

then the covariance matrix should be estimated by

| (9) |

where is the matrix of ones.

Assuming that both and are independent and identically distributed sequences from a multivariate normal distribution, we get that (-dimensional Wishart distribution with degrees of freedom and covariance matrix ). Consequently, for (see, Theorem 3.4.1 in Gupta and Nagar, [49]).

Similarly, we get that in the case of model (8). Consequently, without loss of generality, we put in the rest of the paper, since the derived test statistics are fully determined by the elements of and in the case of only a minor adjustment is needed. We further note that the assumption of normality is not restrictive in many applications. For instance, the asset returns at weekly or smaller frequency are well described by the normal distribution (see, Fama, [38]). Moreover, Tu and Zhou, [81] find no benefits of heavy tailed distributions for the mean-variance investor and pointed out that the application of the normal assumption instead of a heavy tailed distribution leads to a relative small amount of losses.

Let and let be partitioned as

| (10) |

3.1 Test Based on Each Non-Diagonal Element of

Testing hypothesis (4) can also be considered as the global test of the marginal tests with hypotheses given by

| (11) |

for . In terms of multiple testing theory we are thus interested in testing the global hypothesis . For each hypothesis in (11), , we consider the following test statistic

| (12) |

The expression of corresponds to the statistic used in testing for the uncorrelatedness between two random variables (see Section 5 of Muirhead, [66]), although differences in the normalizing factor and in the distribution of the test statistics are present.

Let denote the -distribution with degrees and and let be the corresponding density function. In the following we make also use of the hypergeometric function given by (see, Abramowitz and Stegun, [1])

The distribution of the test statistic is obtained both under and under and it is presented in Theorem 1.

Theorem 1.

Let follow model (1) where and are independent and normally distributed. Then:

-

(a)

The density of is given by

where .

-

(b)

Under it holds that .

The proof of Theorem 1 is given in the appendix. Since the test statistics under the global hypothesis have the same distribution, we consider single-step multiple tests for testing (4). The test statistic is given by

| (13) |

The marginal critical values for the -marginal test are derived from the equality

| (14) |

Solving (14) is a challenging problem since the test statistics are dependent. The first possibility to deal with this problem is the application of a Bonferroni correction. This leads to

where stands for the -quantile of the -distribution with and degrees of freedom.

The second possibility is based on the observation that the expressions of the test statistics remain the same if is replaced by for any diagonal matrix of an appropriate order. Hence, the joint distribution of under the global hypothesis does not depend on . As a result, the critical values of the marginal tests can be calibrated via simulations by generating a sample from the inverse Wishart distribution with degrees of freedom and identity parameter matrix. Under the alternative hypothesis, however, the distribution of cannot be obtained explicitly and needs to be explored by simulations. This point is discussed in more detail in Section 6 where the powers of the suggested tests are compared with each other.

3.2 Test Based on the Product of Diagonal Elements of and

Testing hypothesis (5) can be considered as the global hypothesis of the multiple tests whose hypotheses are given by

| (15) |

for , i.e., .

Similarly to Section 3.1, we first consider a test for the marginal hypothesis . Let . Then the test statistic for testing (15) is given by

| (16) |

In Theorem 2 we present the exact distribution of under the null as well as under the alternative hypotheses.

Theorem 2.

Let follow model (1) where and are independent and normally distributed. Then:

-

(a)

The density of is given by

where .

-

(b)

Under it holds that .

For testing the global hypothesis in (5) we consider

| (17) |

where the critical value is obtained as a solution of

| (18) |

Since the derivation of the joint distribution of is a complicated task, we consider two procedures how can be determined. The first procedure makes use of a Bonferroni correction. In this case, using Theorem 2.(b) we get

The second procedure is based on the following result.

Theorem 3.

Let follow model (1) where and are independent and normally distributed with diagonal matrix . Then the distribution of under is independent of .

Therefore, the critical values for the multiple tests can be calibrated via simulations by generating a sample from the -dimensional inverse Wishart distribution with degrees of freedom and identity parameter matrix.

4 Likelihood-Ratio Test

In this section we derive a test statistics for testing (3) following the third approach outlined in Section 2. It is remarkable that this procedure leads to the likelihood ratio test.

Let denote the exponential of the trace and let be the -dimensional gamma function defined by

Then the density of is given explicitly by

where the last equality is obtained by following the proof of Theorem 3 in Bodnar and Okhrin, [23]. As the transformation from the set of parameters to , is one-to-one (see, e.g., Proposition 5.8 in Eaton, [36]), we rewrite the likelihood function of in terms of the parameters :

Let

| (20) |

It is noted that the third factor in (4) is always less than or equal to with equality if an only if for any given . Moreover, using the multiplicative representation of the likelihood function and noting that no restrictions are imposed under in (3) on and , we get that the likelihood ratio test statistics is then given by

| (21) | |||||

The maximum of the numerator is reached at , whereas the maximum of the denominator is attained at for where denotes the -th diagonal element of . Hence,

| (22) |

Due to (see, Theorem 3 in Bodnar and Okhrin, [23]), we get that . The last statement motivates the use of instead of which appears to be a well-known test statistic in multivariate analysis (see, e.g., Section 11 in Muirhead, [66]). It is used to test the null hypothesis that the elements of a normally distributed random vector are independent which equivalently can be expressed as

| (23) |

for some positive constants , whereas the sample of size is used. It is noted that if the null hypothesis in (3) is true then the null hypothesis in (23) is true and vice versa. Finally, we point out that testing (23) is also equivalent to testing whether the correlation matrix related to the covariance matrix is the identity matrix (see, Section 7.4.3 in Rencher, [70]).

We use the test statistic given by

| (24) |

which is asymptotically -distributed with degrees of freedom under the null hypothesis in (23) (see, e.g., Section 7.4.3 in Rencher, [70]). Since the expression of remains unchanged if is replaced by for any diagonal matrix of an appropriate order, the distribution of does not depend on under . Hence, the critical value of this test can be calibrated by generating a sample from the inverse Wishart distribution with degrees of freedom and identity parameter matrix.

Finally, let us point out that the critical value only depends on the dimension . The asymptotics that the number of factors tends to infinity such that is thus covered as well if the dimension remains fixed.

5 High-Dimensional Asymptotic Test

In this section we derive the distribution of the test statistics , , , , and in the case when both and tend to infinity as the sample size increases. This case is known in the statistical literature as the high-dimensional asymptotic regime. It is remarkable that in this case the results obtained under the standard asymptotic regime ( is fixed) can deviate significantly from those obtained under high-dimensional asymptotics (see, e.g., Bai and Silverstein, [15]).

Several papers deal with the problem of estimating the covariance and the precision matrices from high-dimensional data. The results are usually obtained by applying the shrinkage technique (see, e.g., Ledoit and Wolf, [58], Bodnar et al., 2014a [21]; Bodnar et al., 2014b [22]; bodnar2016direct) or by imposing some conditions on the structure of the covariance (precision) matrix (see, Cai and Liu, [25], Cai et al., [26], Agarwal et al., [2], Fan et al., [41], Fan et al., [43]). For instance, in Agarwal et al., [2] an assumption is imposed that the covariance matrix can be presented as a sum of a sparse matrix and a low rank matrix. This structure of the covariance matrix is similar to the one obtained assuming a factor model (see, e.g., Fan et al., [43] for discussion).

Although several tests on the covariance matrix under high-dimensional asymptotics have been suggested recently (see, e.g., Johnstone, [56], Bai et al., [14], Chen et al., [32], Cai and Jiang, [27], Jiang and Yang, [55], Gupta and Bodnar, [50]), we are not aware of any test on the precision matrix in the literature. The latter problem is closely related to the test theory developed in this paper since the suggested tests can be presented as tests on the specific structure of the precision matrix. Their distributions under high-dimensional asymptotics are derived in this section.

Later on, we distinguish between two cases, as and such that as . The number of factors could be both asymptotically finite or infinite, but must remain smaller than the sample size . Finally, it is also assumed that to ensure the invertibility of .

5.1 Asymptotic Distributions of

As the finite sample distribution of the test statistics depend on , , and through the difference only, we get the following result.

5.2 Asymptotic Distributions of

Let be the th column of leaving out and let be the matrix obtained from by deleting its th row and its th column. We define . Then using the results of Lemma 2 from the appendix (see Section 9), we get with that

for as under since if then as .

In Theorem 5 we derive the weak limit under high-dimensional asymptotics of a transformation of , , as as well as the weak limit of for as .

Theorem 5.

The marginal test based on the statistic rejects the null hypothesis if the value of the test statistic multiplied by is larger than (-quantile of the standard normal distribution). Using that (see Theorem 2), a finite sample correction of the statistic can be suggested. Since the expectation and the variance of a -random variable are given by

we get the following finite sample adjusted version:

Of course, under the high-dimensional asymptotics, we get and for as .

5.3 Likelihood Ratio Test under High-Dimensional Asymptotics

In this subsection we extend the results of Section 4 by deriving the asymptotic distribution of the likelihood ratio test statistics under the high-dimensional asymptotic regime. The results are obtained in case of as as well as in case of such that as .

First, we note that the statistic can be further rewritten. Let be the correlation matrix calculated from the Wishart distributed matrix , that is

Then the test statistic can be presented by

| (33) |

The asymptotic distribution in case of the likelihood ratio test under in (3) is given in Theorem 6.

Theorem 6.

6 Finite-Sample Performance

In this section we investigate the power of the three tests suggested in the previous sections. The analysis is performed for both, small (Section 6.1) and large (Section 6.2) values of .

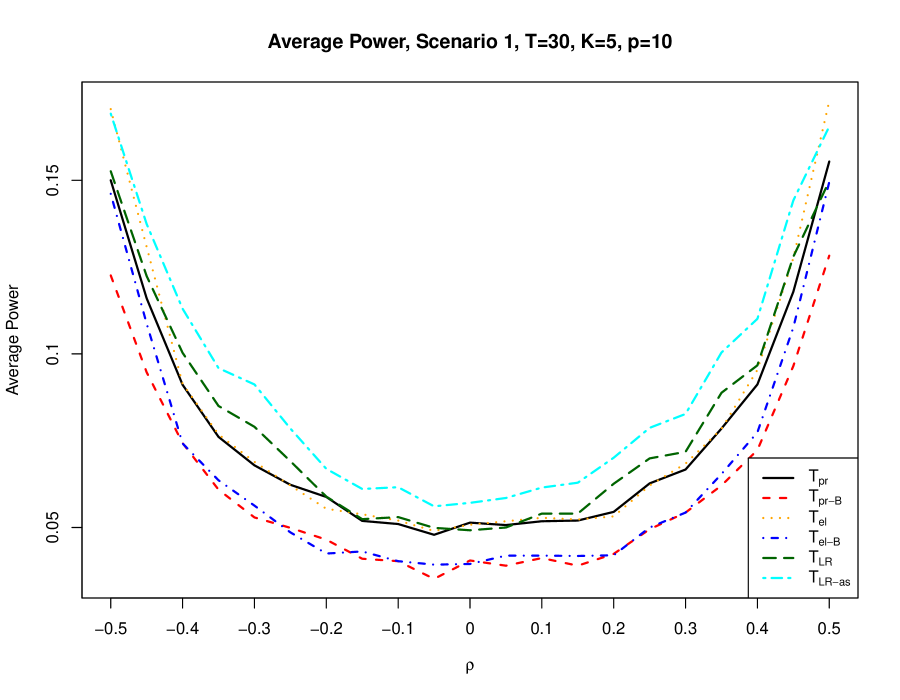

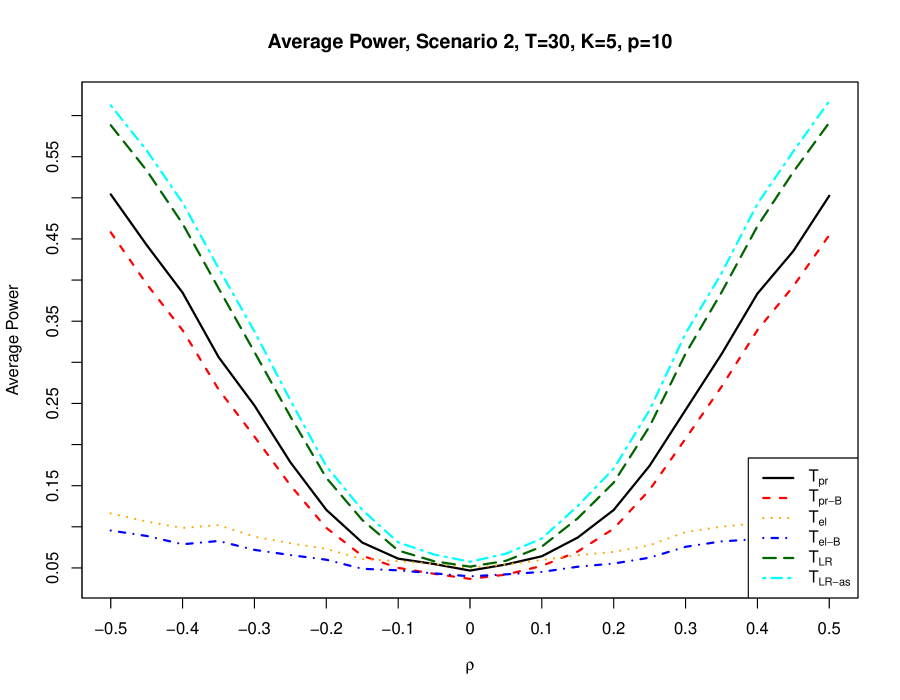

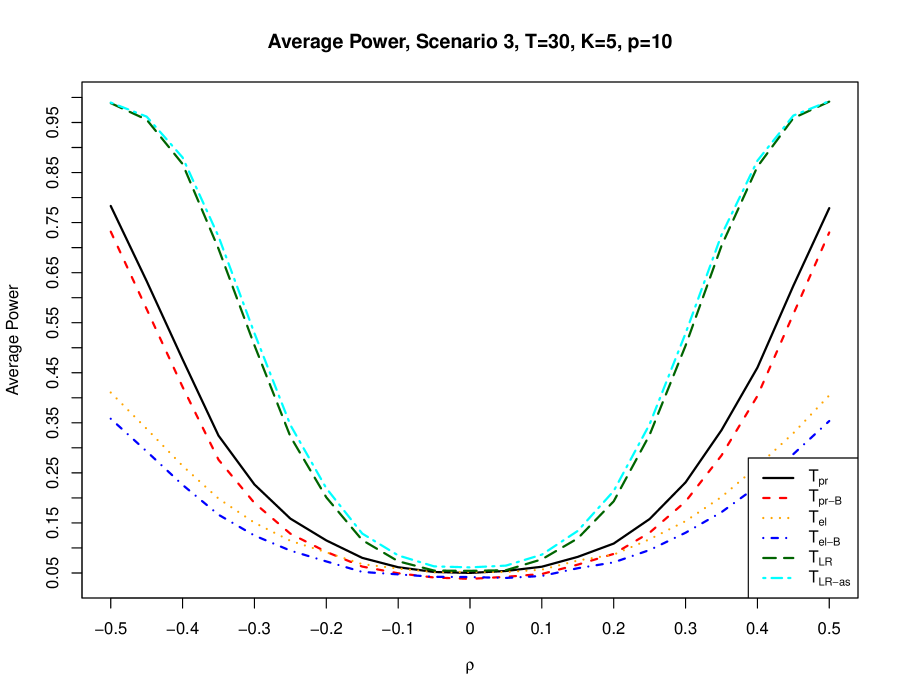

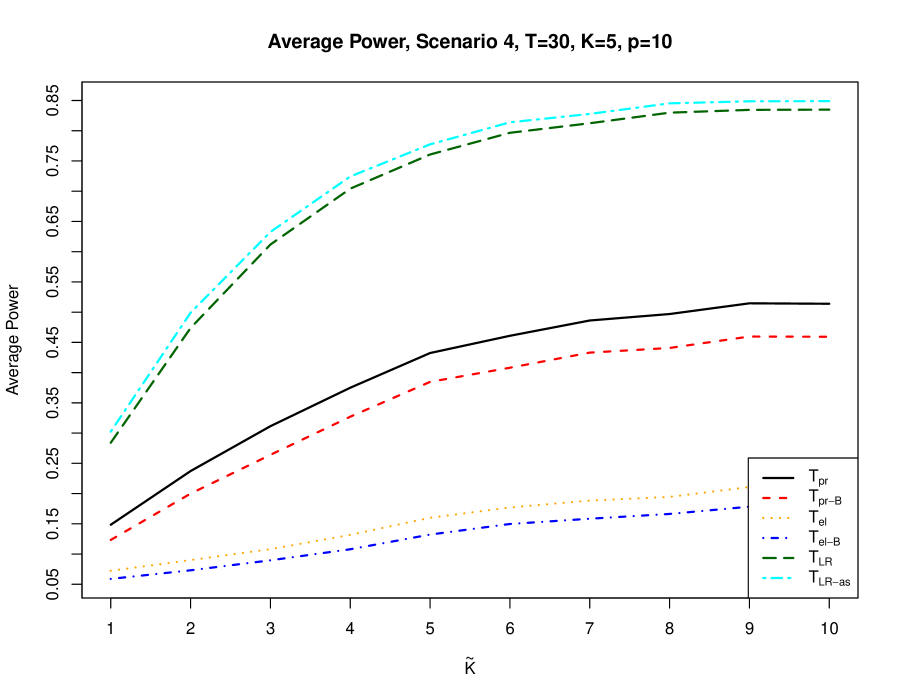

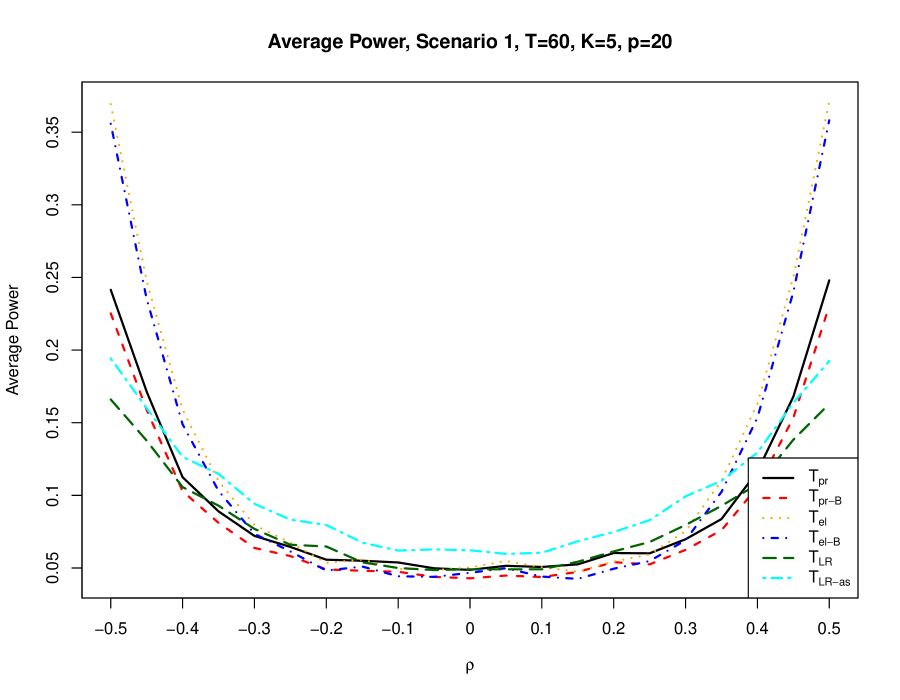

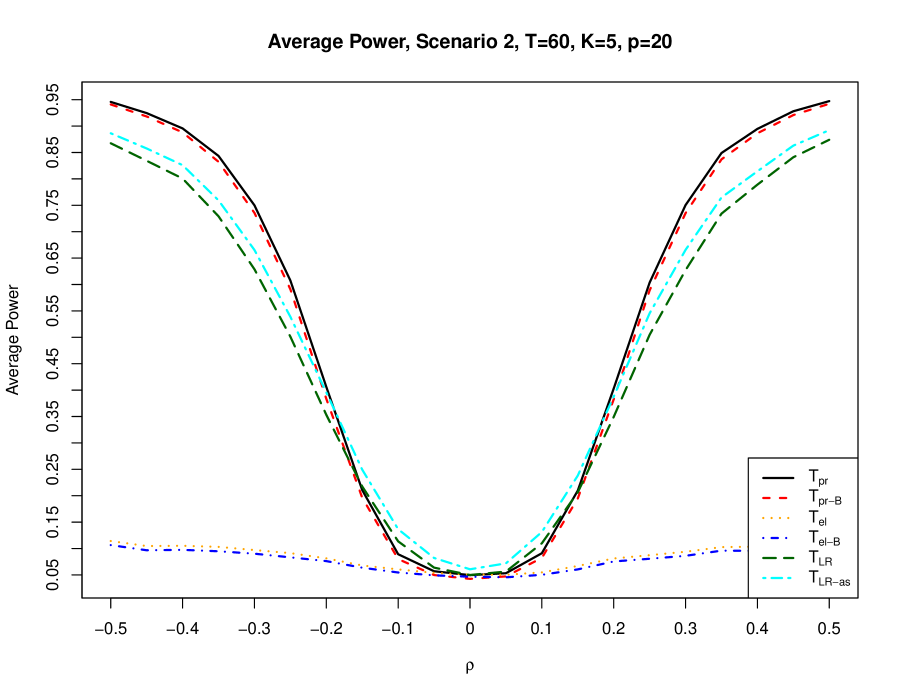

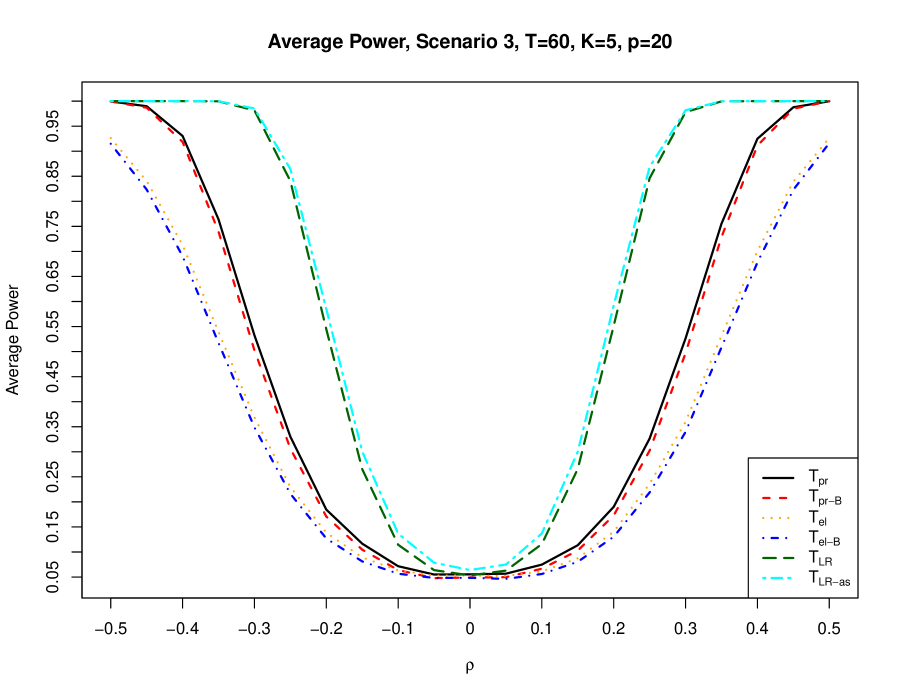

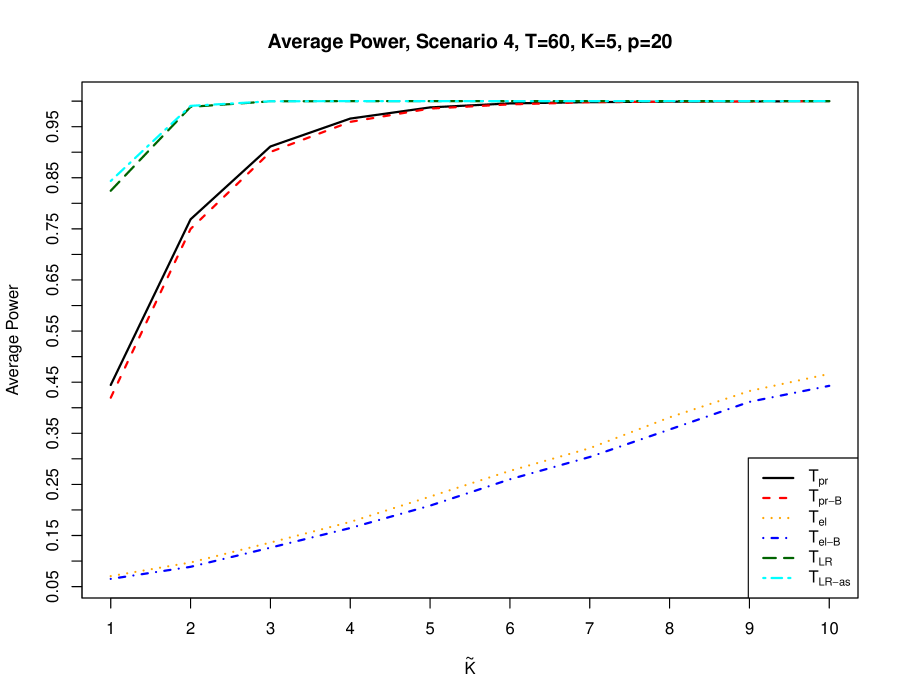

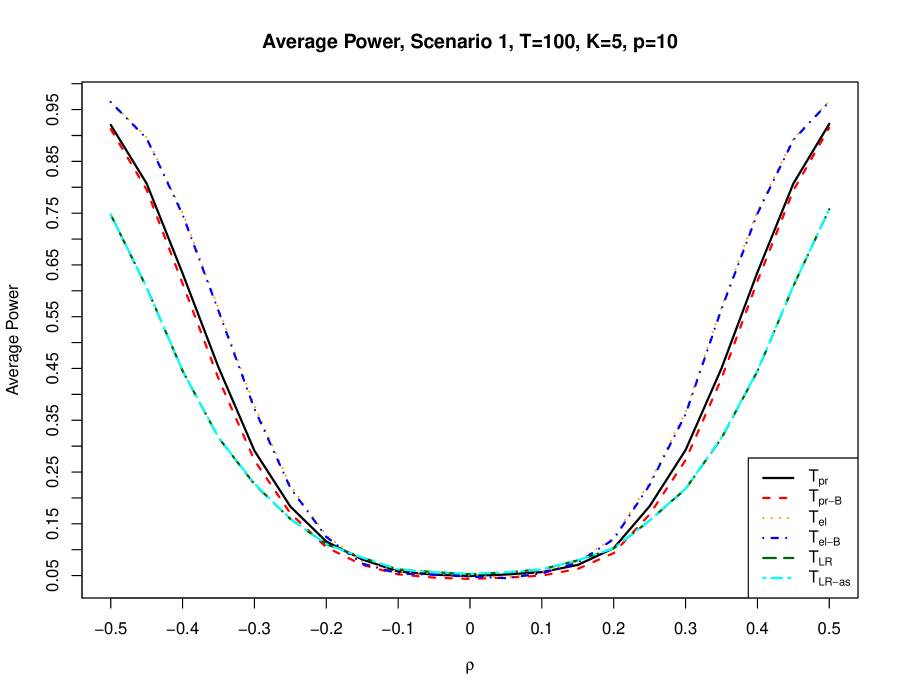

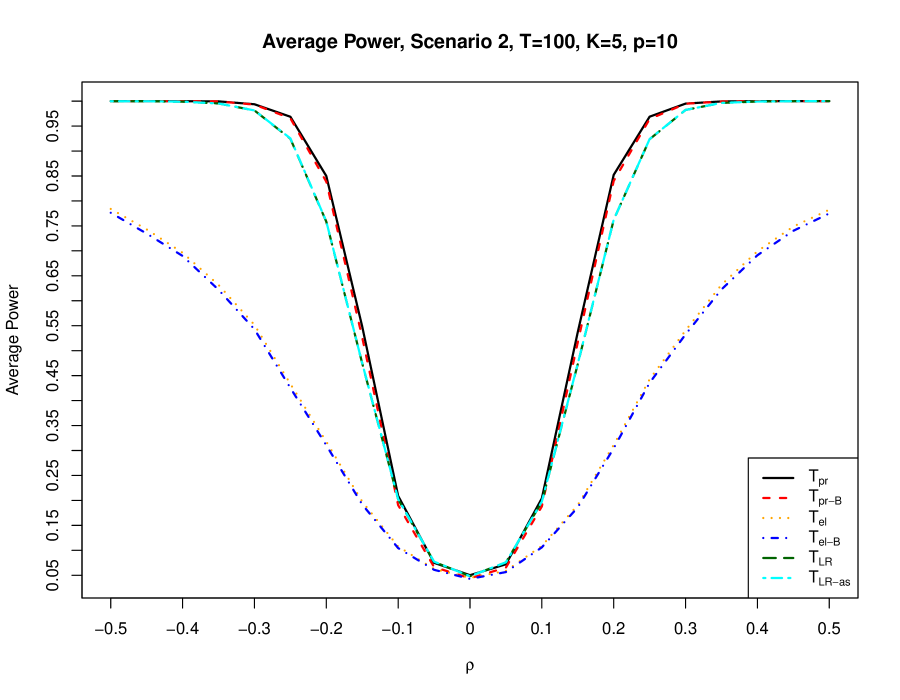

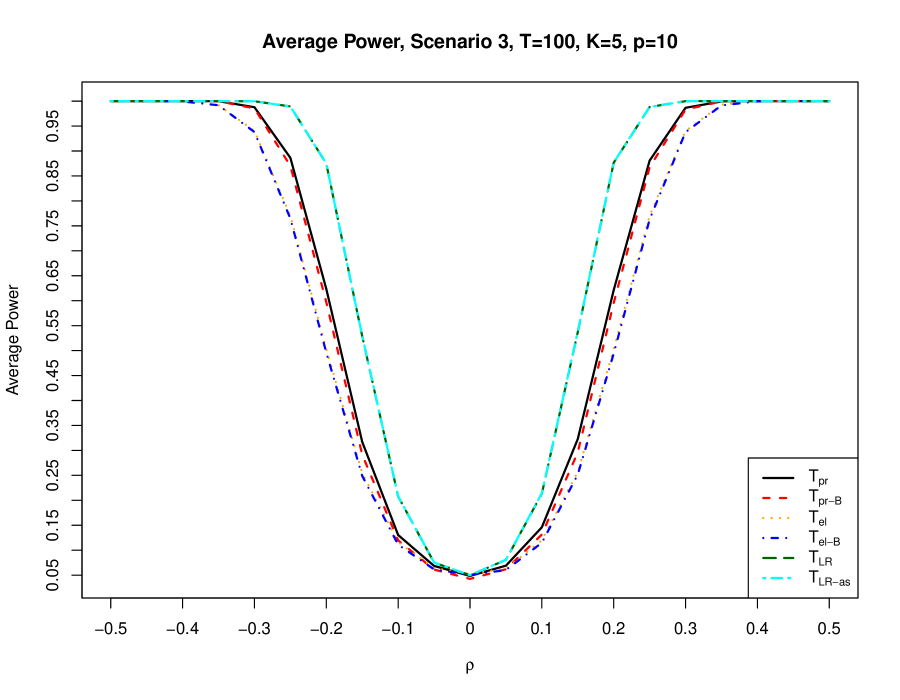

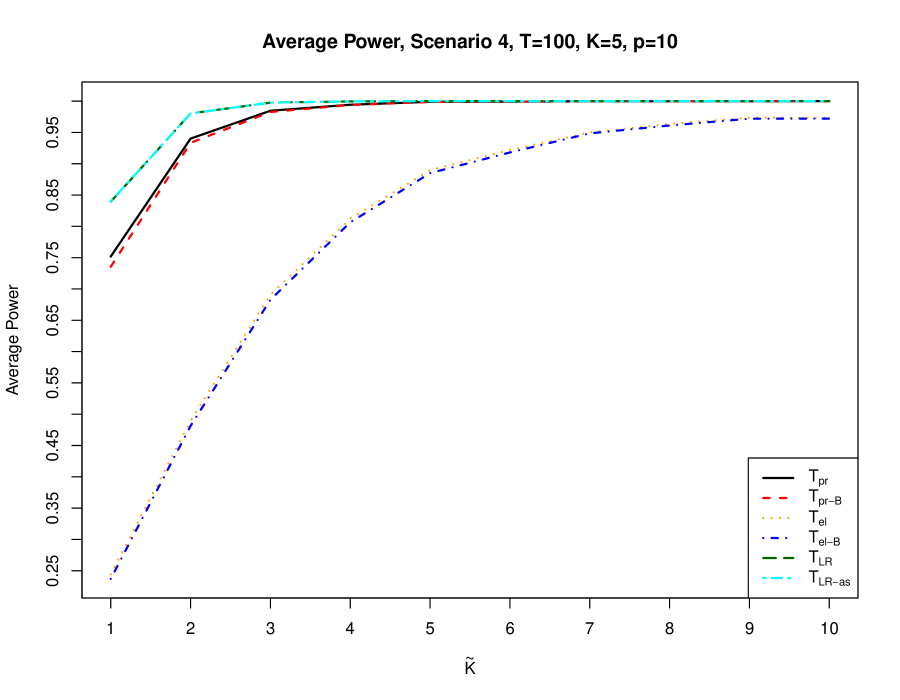

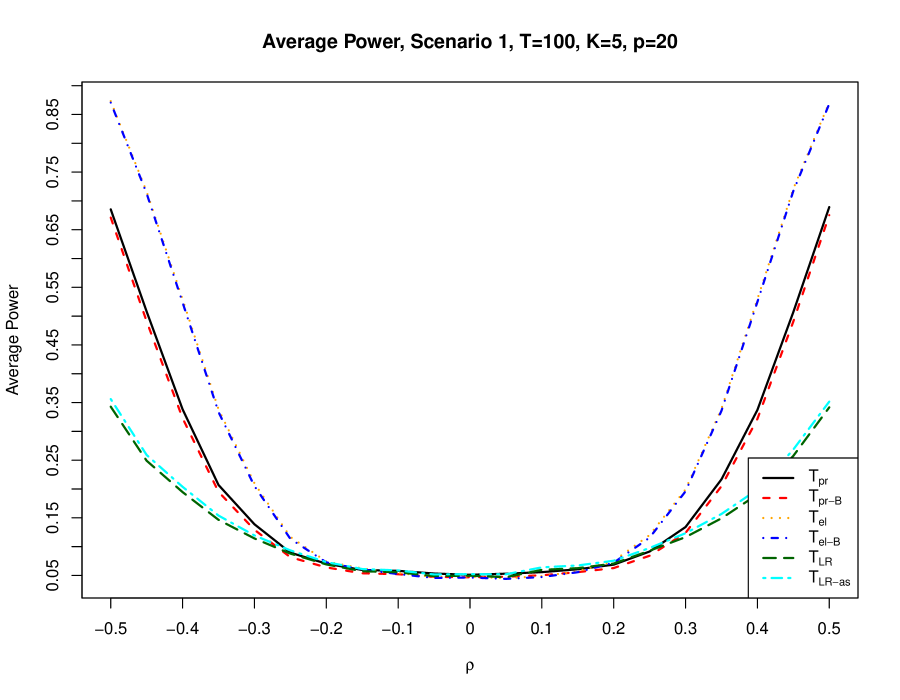

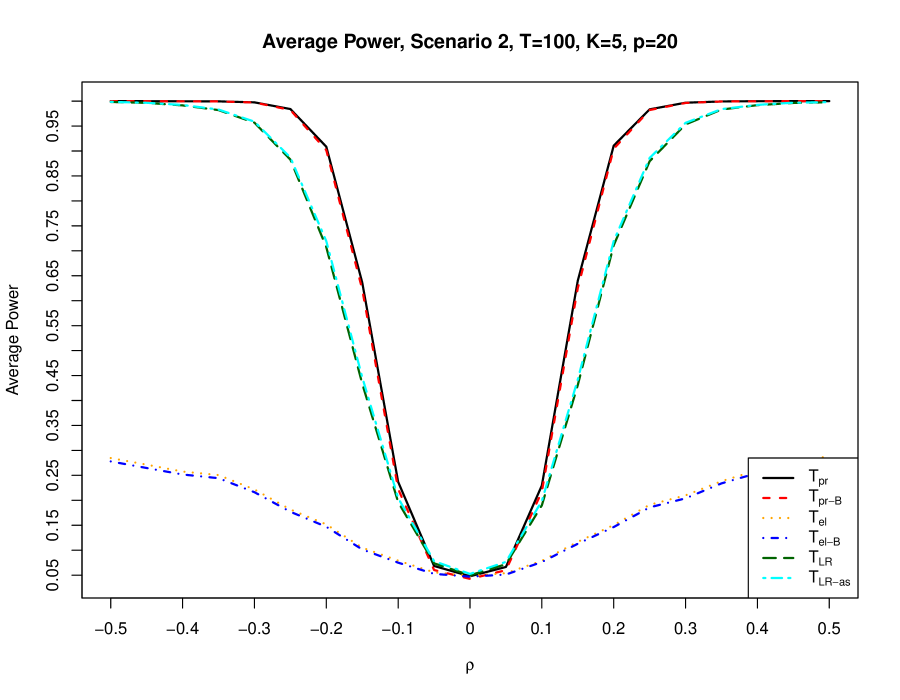

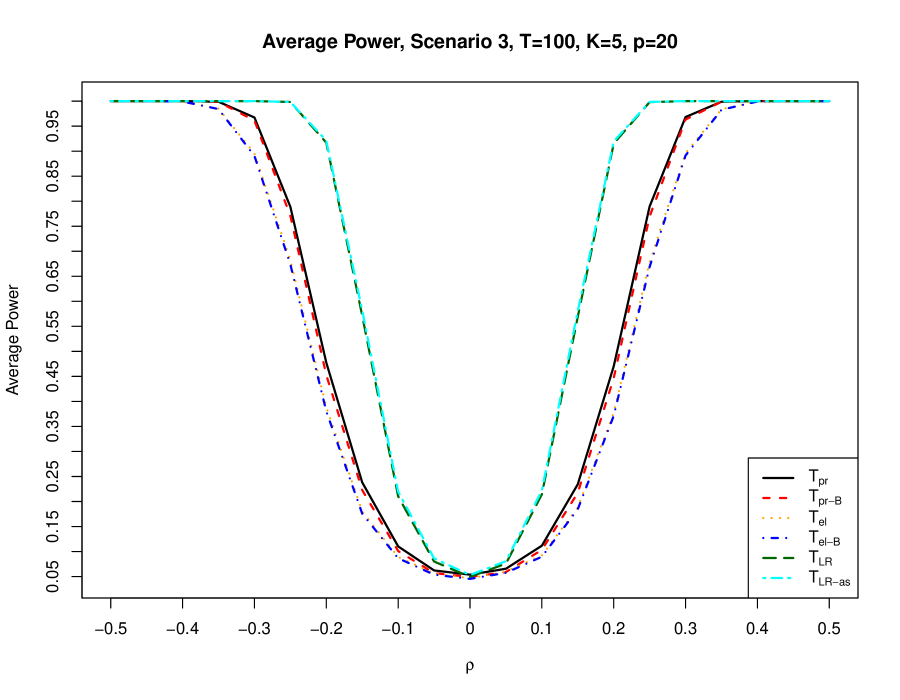

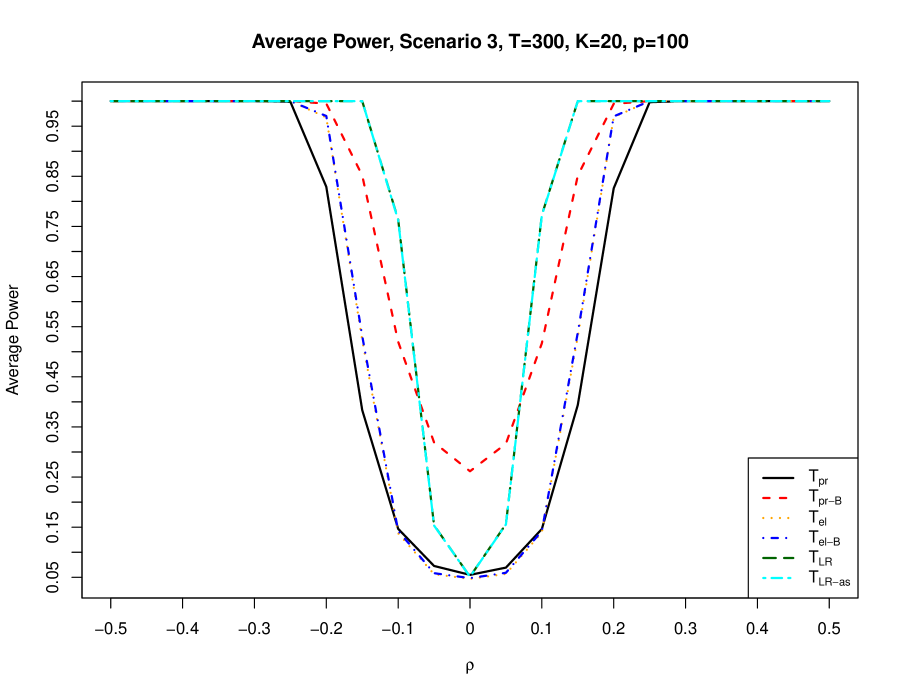

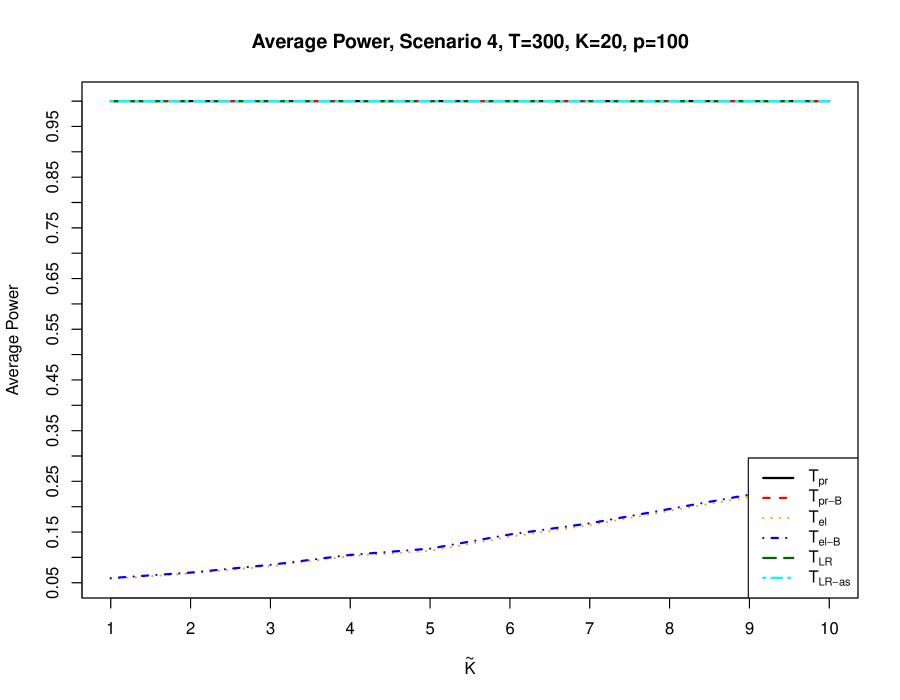

The critical values of each test are obtained via simulations or by using a Bonferroni correction in case of and as well as the asymptotic distribution for . Consequently, in all plots six lines are shown. The lines denoted by , , and correspond to the case of calibrated critical values of the tests, whereas the notations , , and mean that a Bonferroni correction or the asymptotic distribution was used. The critical values, which are based on simulations, are obtained by generating a sample of realizations from the inverse Wishart distribution with degrees of freedom and identity parameter matrix. Based on this sample, the sample quantiles of the corresponding test statistics are calculated and used as critical values.

The situation is more complex if the aim is to access the power of the suggested tests, since the powers depend on the model specified under the alternative hypothesis. In order to investigate the powers of the tests, we simulate data following (1). Namely, the vector of factors and the residual vector are generated independently from each other as well as independently in each repetition from in case of and from , with and , , in case of . Here, determine the standard deviations of , respectively, whereas stands for the correlation matrix. In order to get reliable results which do not depend on one model only, we take different parameters for and , in each repetitions. Namely, we specify all these quantities randomly following and . The correlation matrix has been chosen in three possible ways in order to account for the behaviour of the tests under different deviations from . We further increase the number of factors in model (1) and perform the test assuming that a lower number of factors is present.

We present four scenarios for generating data in detail which are used in the investigation of the test powers.

-

•

Scenario 1: Change in one correlation coefficient.

Here, it is assumed that with . The remaining correlations are set to zero. -

•

Scenario 2: Change in one column.

Let withThe remaining correlation coefficients are zero.

-

•

Scenario 3: All correlation coefficients are changed.

Here, we put for . -

•

Scenario 4: Change in the number of factors.

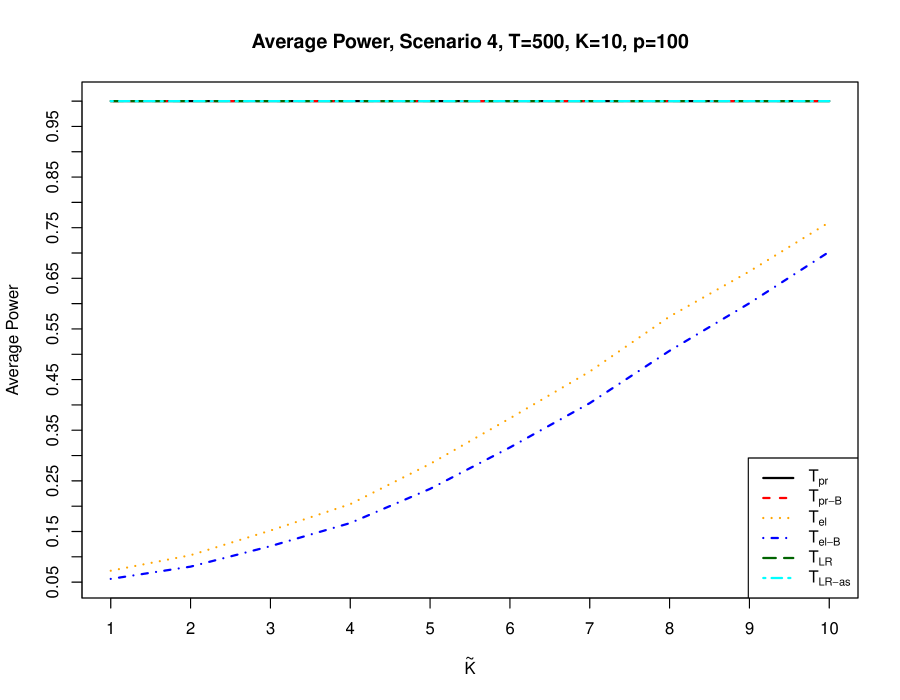

The number of factors in the true model is increased to with .

These four scenarios lead to different types of factor models under the alternative hypothesis. For instance, in case of Scenario 1, a single change in the correlation matrix of residuals is assumed, whereas Scenario 2 leads to changes in the first column (row) of . Scenario 3 corresponds to changes in all elements of although their magnitude becomes smaller as the difference between the row number and the column number increases. Here, the structure of corresponds to the structure of the correlation matrix of an AR(1)-process. Finally, Scenario 4 assumes that the true factor model consists of factors, whereas the factor model with factors is fitted.

For different scenarios, we expect different performances of the suggested three tests with respect to their powers. For the first scenario, the test is expected to be the best one, whereas the test should outperform the competitors in case of Scenario 2. Finally, when changes in the entire correlation matrix are present, the likelihood ratio test () should possess the best performance. Furthermore, the application of provides more information to the practitioners than in the case of and . Only the conclusion about the validity of the factor model can be drawn when the test is used, whereas the test can indicate the columns in the precision matrix which are responsible for the rejection of the null hypothesis. In contrast, the testing procedure determines the pairs of variables for which the null hypothesis is rejected.

6.1 Results for Small Dimension

In this subsection, we present the results of our simulation study under the assumption that is much smaller than and/or all quantities , , and are finite. Different values of , , and are considered. Moreover, we put and , as described above. Finally, the nominal size of the tests is set to .

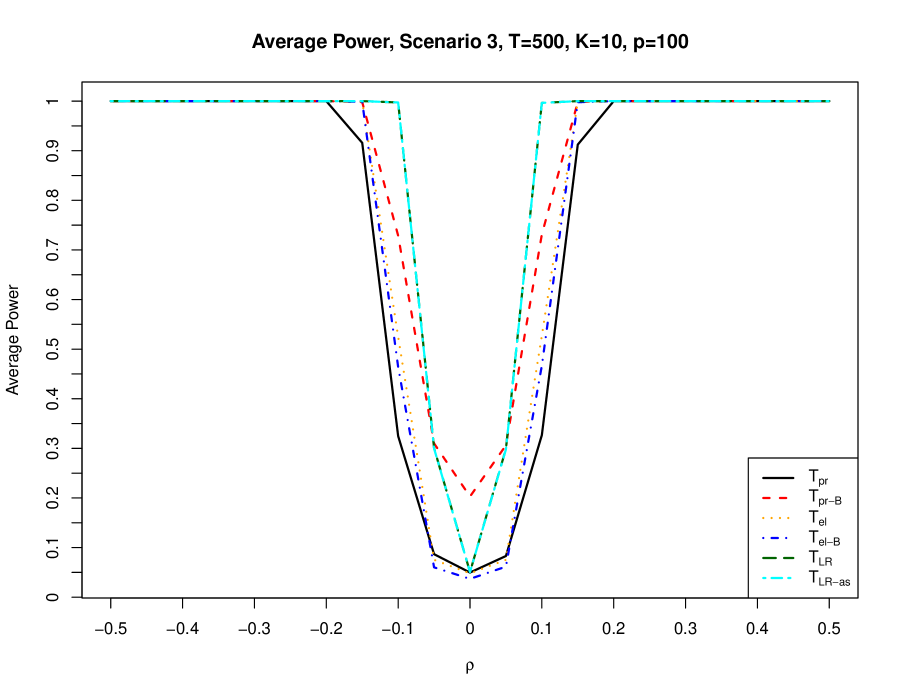

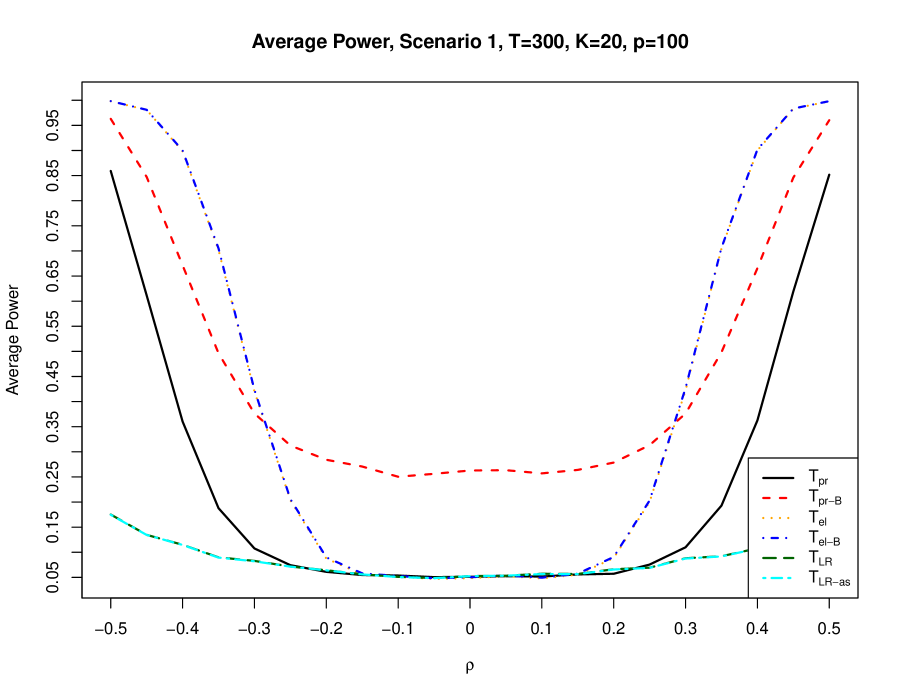

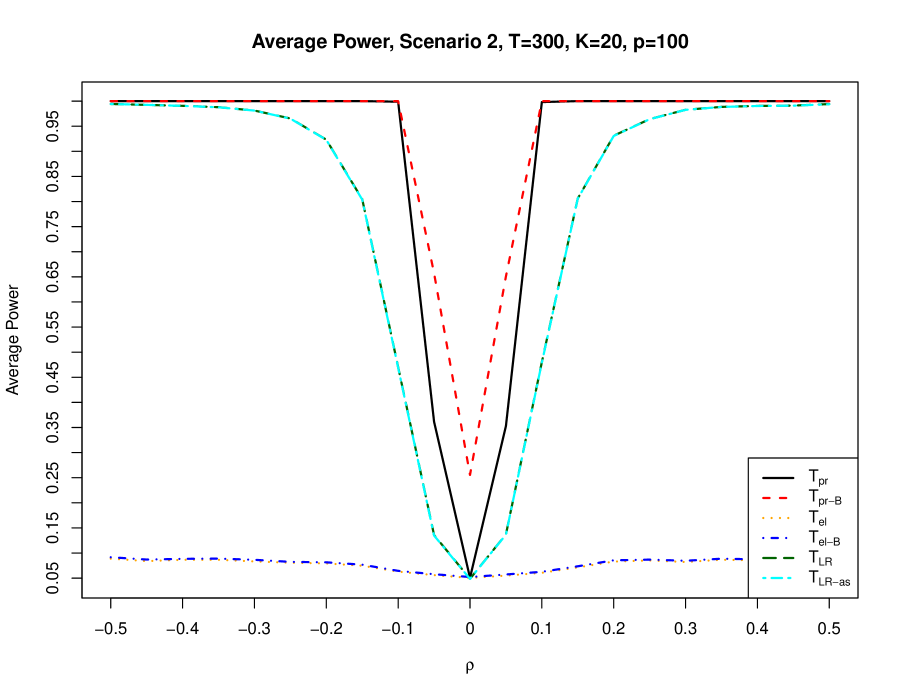

The resulting powers are shown in Figures 1-4. In Figures 1 and 2, we present the results for small sample size, whereas Figures 3 and 4 correspond to large with respect to . It is not surprising that if is relatively small with respect to , then the test based on the asymptotic distribution shows the probability of type 1 error larger than the nominal value of . Consequently, a finite sample adjustment for this test is required. This is achieved by calibrating the critical values of this test following the results of Section 4.

Figures 1 and 4 above here

The figures with the exception of Figure 2 confirm our expectation. In case of Scenario 1, the best approach is the test followed by the test, whereas for the rest of the considered scenarios this test shows the worst performance in almost all of the considered cases. For Scenario 2, the best approach is based on the application of the statistic, while in both, Scenario 3 and Scenario 4, the likelihood ratio test outperforms the competitors.

We also observe that the lines which correspond to the Bonferroni correction or which are obtained from the asymptotic distribution almost coincide with the corresponding lines obtained by calibrating the critical values under the null hypothesis if . This indicates that under the event that two marginal test statistics are simultaneously beyond the critical value is negligible. In contrast, for smaller sample sizes ( and ) this statement does not hold, especially for the -asymptotic test.

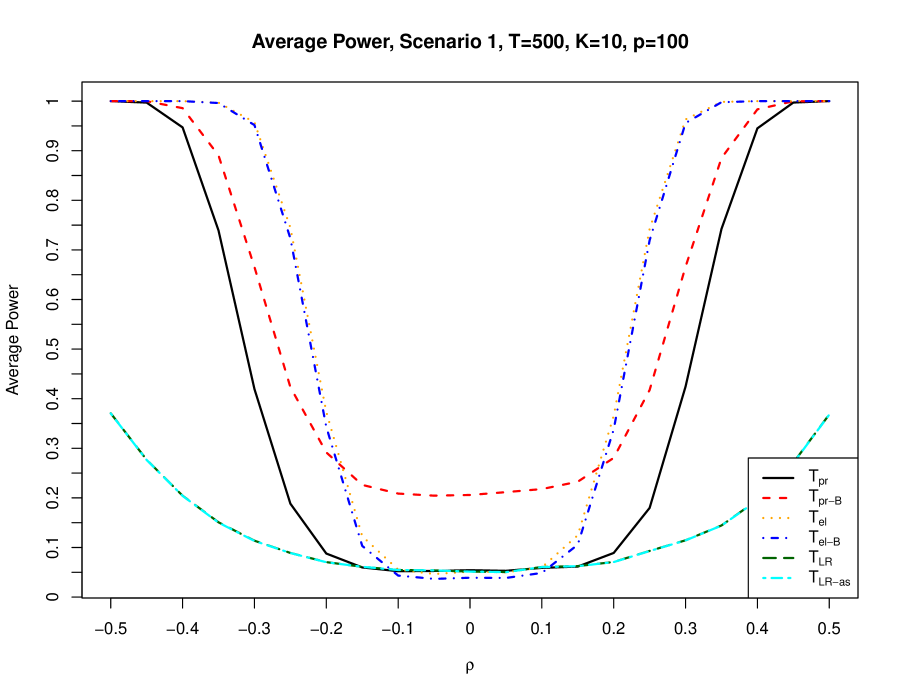

6.2 Results for Large Dimension

In this subsection we deal with the case of high-dimensional factor models. Two possible sets of values for , , and are considered, namely with and with . The nominal size of the tests is set to . Similarly to the previous subsection, six lines are plotted in each figure. Three of them correspond to the tests based on the calibrated critical values, whereas for the other three lines the asymptotic results of Theorems 4 and 6 together with the Bonferroni correction are used.

Figures 5 and 6 above here

The results of Figures 5 and 6 are even more pronounced than the ones in case of small . Namely, for Scenario 1, the best test is based on the statistic, clearly outperforming the rest of competitors. Here, a very poor performance of the likelihood ratio test is observed which is to be expected because the dimension of becomes large and a change in a single entry has only a minor impact on the determinant. On the other side, the test possesses very small power for the rest of the considered scenarios. The test based on the statistic is the best one in case of Scenario 2 and shows the same performance as the approach for Scenario 4. Finally, in case of Scenario 3, the likelihood ratio test clearly outperforms the other approaches.

Figure 7 above here

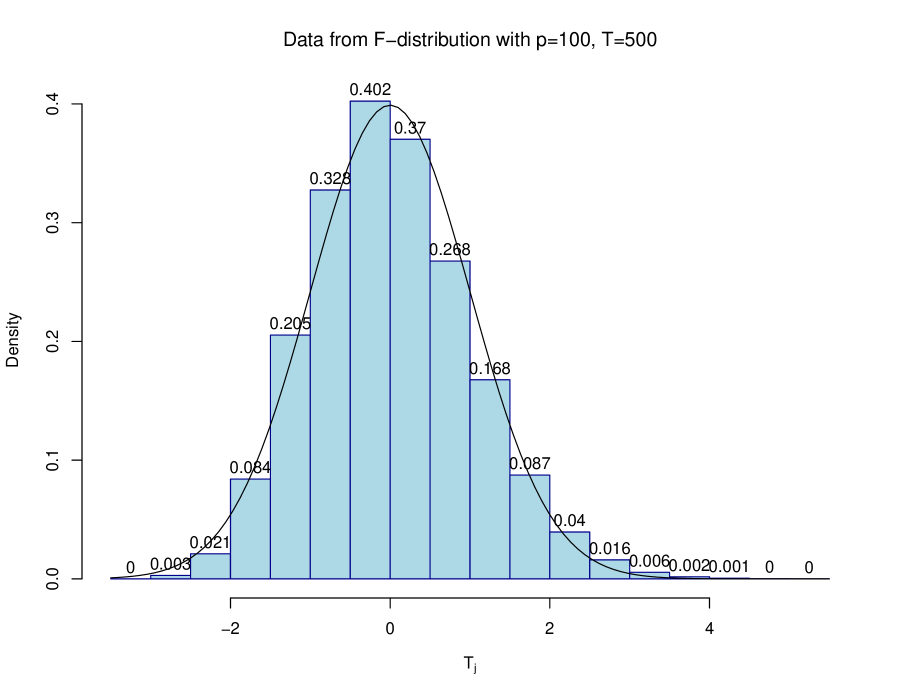

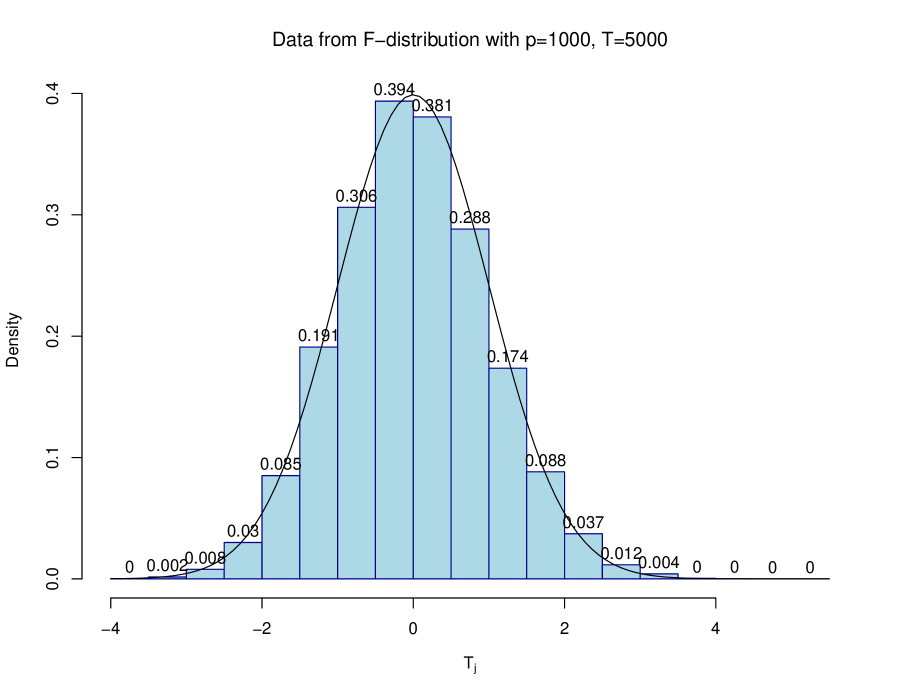

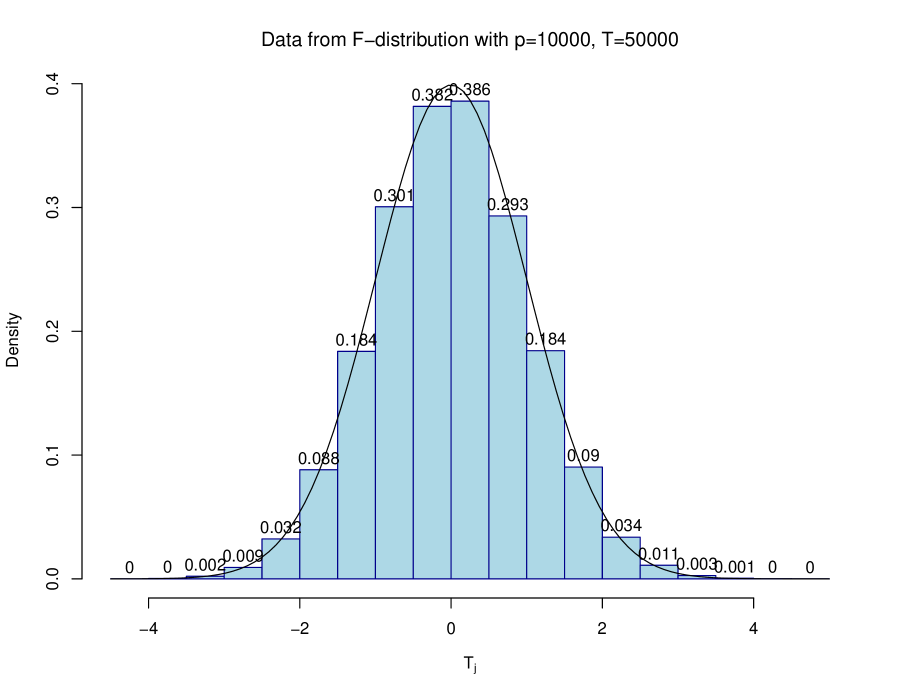

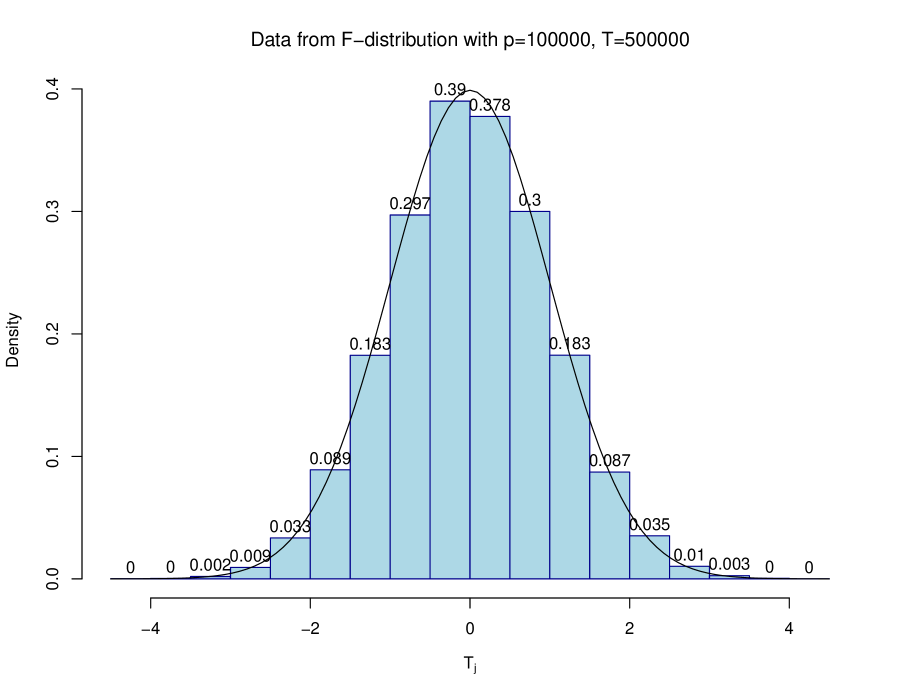

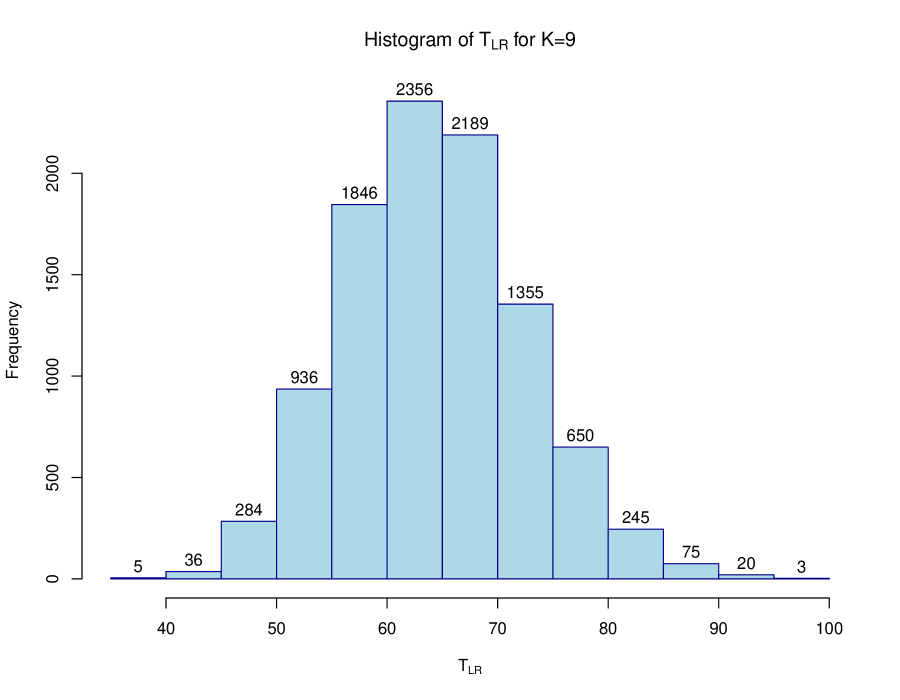

It is also noted that the Bonferroni correction does not work well in case of the test. This is explained by the problem of approximating the -distribution with both degrees of freedom large by the normal distribution under high-dimensional asymptotics (see Figure 7). Although the histograms for look like the ones which correspond to the normal distribution, they are slightly moved to the left and do provide a good approximation only if . Since the maximum of dependent -statistics is taken in the definition of under , this effect becomes even more pronounced. It is documented in Figures 5 and 6 by red lines which significantly deviate from the corresponding black lines obtained for calibrated -values. As a result, it is recommendable to apply the results of Section 5 only in case of very high-dimensional factor models. If is smaller than , then it is better to construct Bonferroni corrections based on the exact -distributions given in Theorems 1 and 2 instead of the asymptotic ones from Theorems 4 and 5.

7 Empirical Illustration

In this section, we apply the theoretical results of the paper to test if the market indices can be used as factors in describing the dynamics of the asset returns. This idea corresponds to the capital asset pricing model (CAPM) and the arbitrage pricing theory (APT) which are widely used in portfolio analysis.

Bai et al., [13] point out that Markowitz’s portfolio selection theory (see, Markowitz, [63, 64]) has already set up the foundation for the CAPM. These ideas are further extended by Sharpe, [78] and Lintner, [60] in case of the presence of a risk-free asset, whereas Black, [20] generalizes the CAPM to the case when a risk-free asset is not available by deriving the so-called zero-beta CAPM. As a proxy for the returns of the market portfolio, which plays a role of the factor in the CAPM, the returns of the market indices, like the DAX index or the S&P 500 index, are usually used.

The APT is an extension of the CAPM model which was suggested by Merton, [65] and Ross, [71]. In contrast to the CAPM, which is based on a single factor only, several factors are used in the APT in order to fit the dynamics in the asset returns. These factors are usually presented by other market or industry-sector indices, like the TecDAX index or the NASDAQ bank index. One of the main ideas behind the APT is that it is commonly not enough to model the asset returns by a single factor and, thus, further factors have to be included into the model. Finally, Chamberlain and Rothschild, [31] suggest a high-dimensional factor model for capturing the dynamics in the asset returns (see, Fan et al., [43]).

Estimation and testing the CAPM (APT) is an important topic in finance today (see, Shanken, [76, 75, 76], Velu and Zhou, [82], Shanken and Zhou, [77], Sentana, [74], Beaulieu et al., [16], Reiß et al., [69]). Recently, Sentana, [74] provides a survey of mean-variance efficiency tests which play a special role in the CAPM and have increased their popularity after the seminal paper of Gibbons et al., [48]. Beaulieu et al., [16] suggest exact simulation-based procedures for testing the zero-beta CAPM and constructing confidence intervals for the zero-beta rate.

We apply the theoretical results of the paper to test the validity of a factor model with specified factors in case of the returns on stocks included into the German DAX index (Section 7.1) as well as in case of the returns on stocks included into the USA S&P index (Section 7.2). The first empirical study corresponds to a factor model with , whereas the second one to the high-dimensional model with .

7.1 Analysis of Stocks Included into the DAX Index

We perform the , , and tests on the validity of factor models fitted to the returns of stocks included into the DAX index. These stocks are chosen randomly out of all stocks which determine the value of the DAX index. Repeating this procedure times, models are fitted and tests on the validity of each model are performed. As factors, we use the returns of the DAX index in the first approach. In the second approach, we included three further factors, namely, the STOXX50E index, the TecDAX index, and the MDAX index. In all cases, weekly returns are considered from the 11th of June 2012 to the 10th of June 2014 ( observations) obtained from the Yahoo! finance web-page.1 ††1 It has to be noted that the distribution of monthly returns is closer to the normal distribution compared to the shorter term returns. However, the application of monthly data over longer periods of time may lead to biased results due to non-constant parameters. In contrast, the daily data cause problems with the assumption of normality. For this reason we opt for the weekly frequency, which is a trade-off between the two extremes.

| Test | 0.1 | 0.05 | 0.01 | 0.005 |

|---|---|---|---|---|

| 12.7205 | 14.2748 | 18.0389 | 19.8171 | |

| 2.2581 | 2.4474 | 2.8415 | 2.9739 | |

| 215.7571 | 223.4439 | 239.7306 | 245.2959 | |

| Test | 0.1 | 0.05 | 0.01 | 0.005 |

| 12.9347 | 14.3680 | 17.8800 | 19.4064 | |

| 2.2821 | 2.4524 | 2.8275 | 3.0234 | |

| 216.2087 | 223.3710 | 236.5821 | 242.6313 | |

Using , as well as for one-factor models and for four-factors models, the critical values of the considered test are calibrated by generating a sample of size from the inverse Wishart distribution with degrees of freedom and the identity parameter matrix. These critical values are shown in Table 1. The resulting samples of test statistics are used in the determination of the empirical distribution functions of the test statistics which are then applied to the calculation of the -values. The most important quantiles of the obtained -values, namely the minimum and the maximum values, the lower and the upper quartiles as well as the median, are shown in Table 2. Here, we observe that most of the calculated -values are equal to zero which shows that the null hypothesis of the validity of a factor model with the selected factors is rejected in most cases for both, and . Only the test fails to reject the null hypothesis in a few cases, which is in-line with the results of the previous section where it is shown that this test is less powerful in many cases.

| Test Quantile | Minimum | Lower Quartile | Median | Upper Quartile | Maximum |

|---|---|---|---|---|---|

| 0.0000 | 0.0000 | 0.0000 | 0.0002 | 0.7296 | |

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0270 | |

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

| Test Quantile | Minimum | Lower Quartile | Median | Upper Quartile | Maximum |

| 0.0000 | 0.0002 | 0.0002 | 0.0011 | 0.9241 | |

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.1024 | |

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

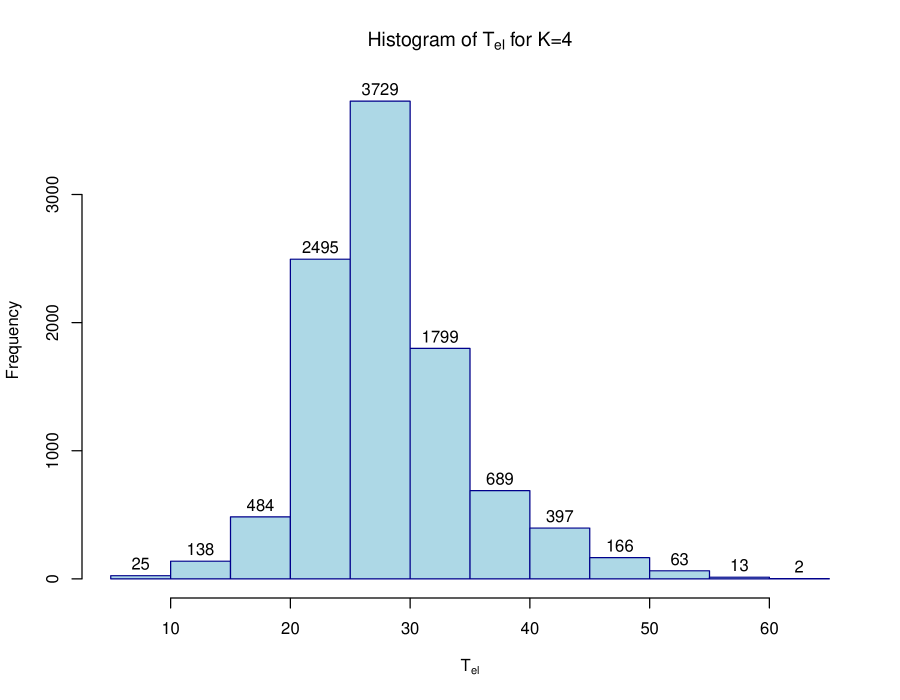

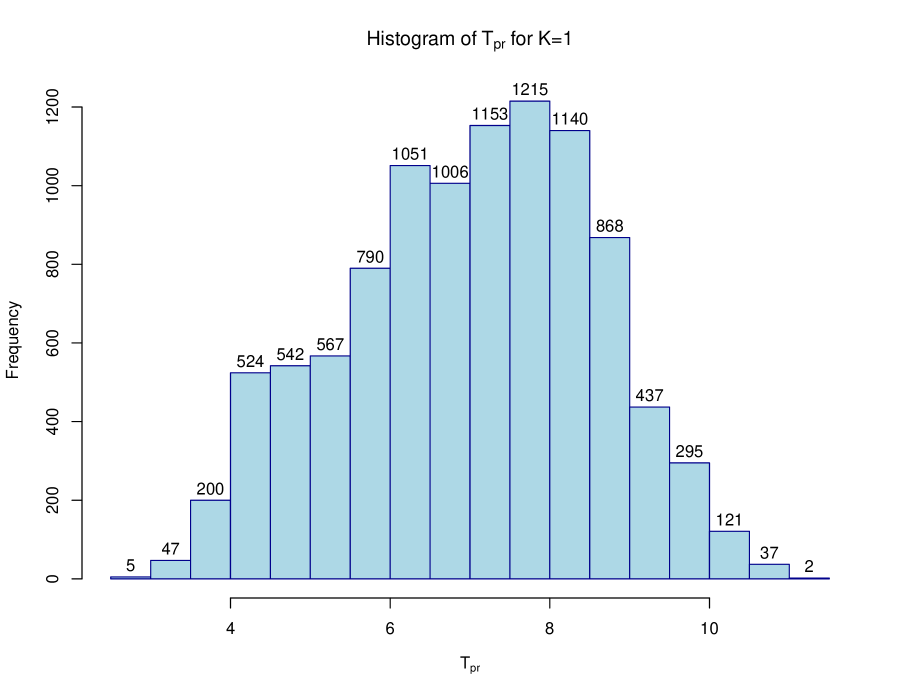

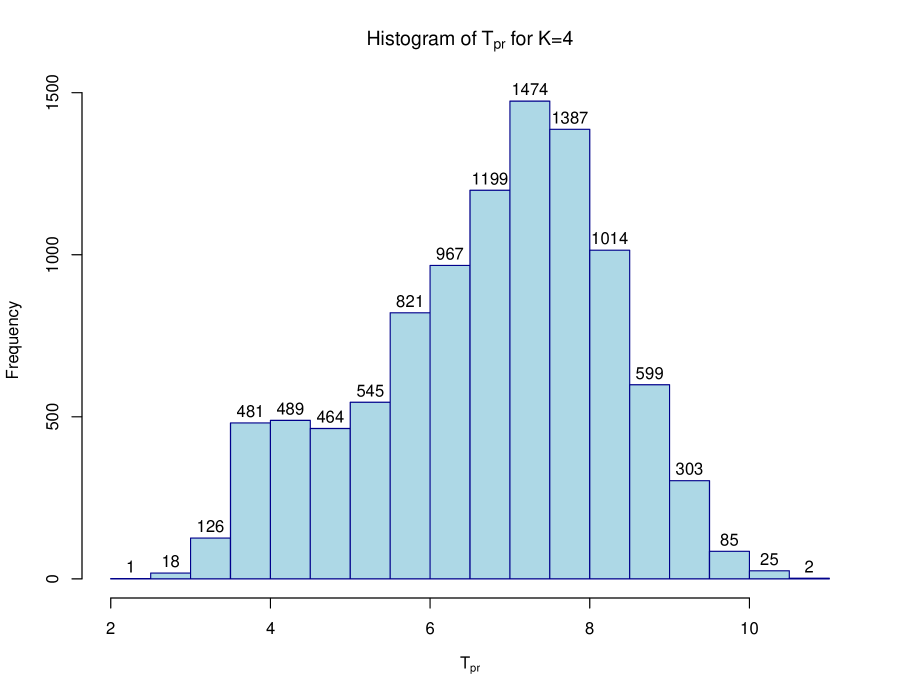

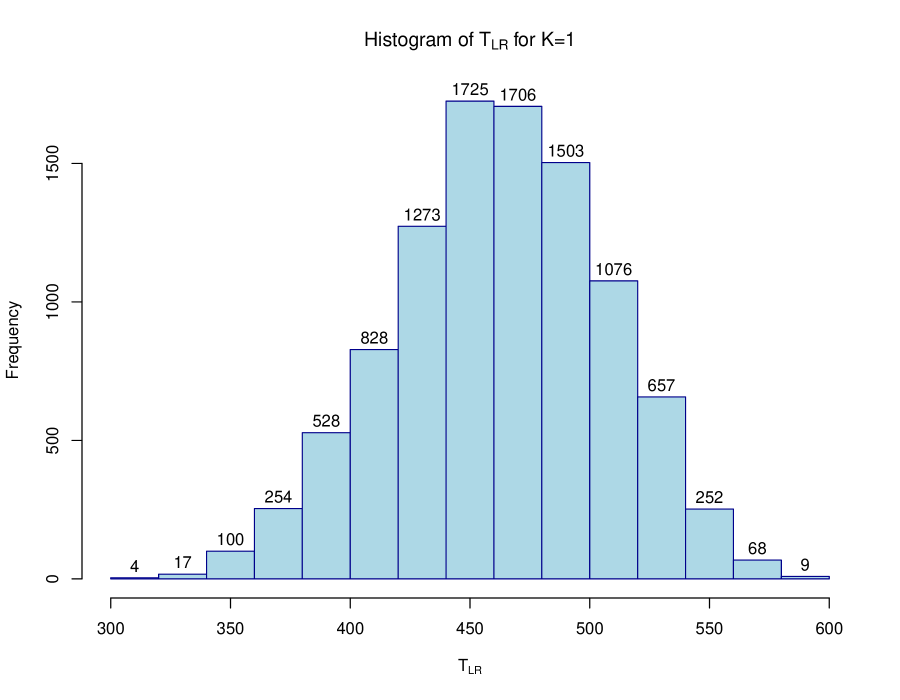

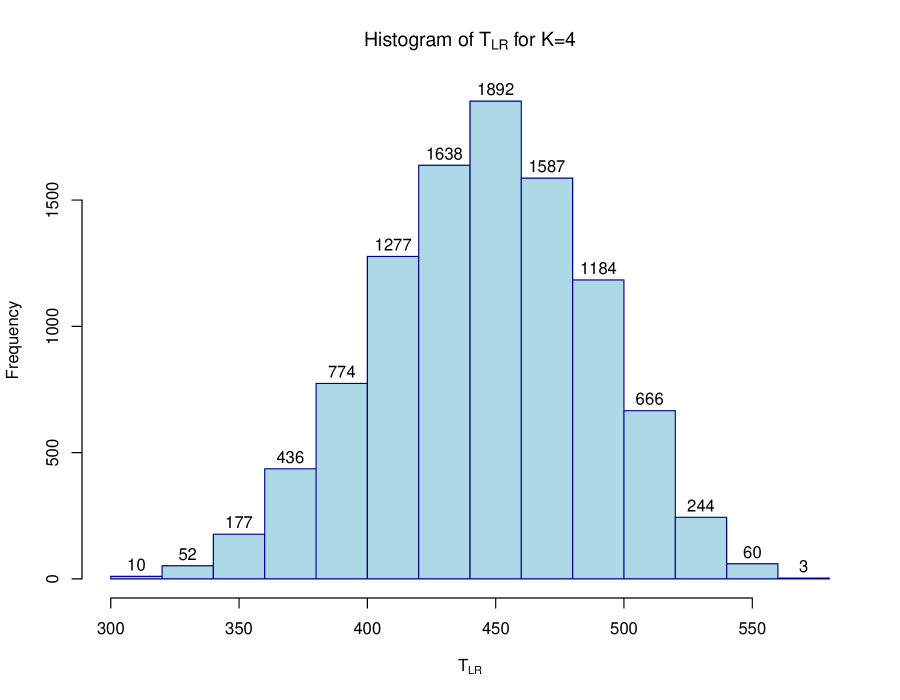

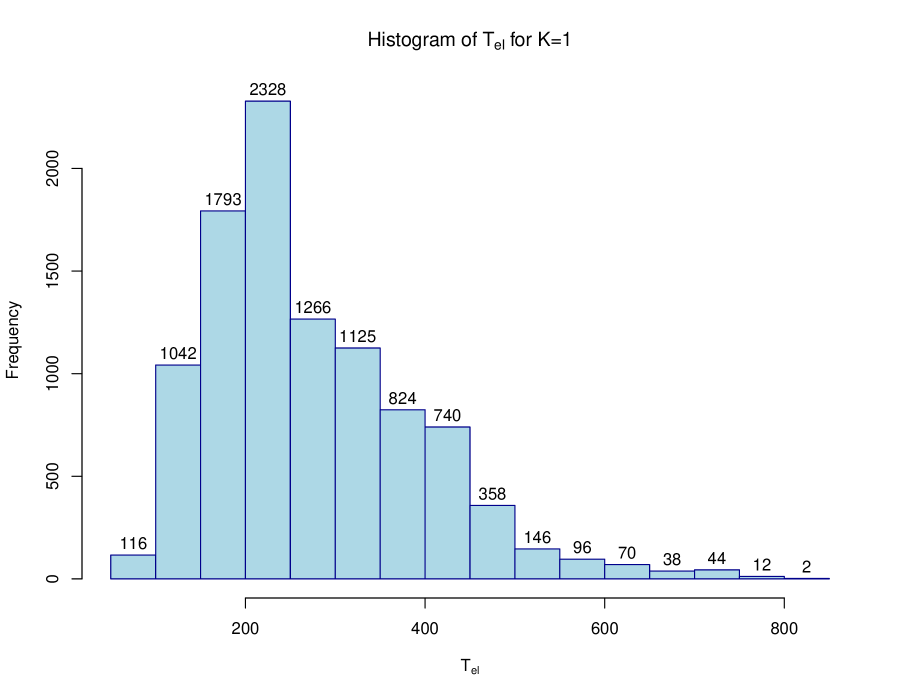

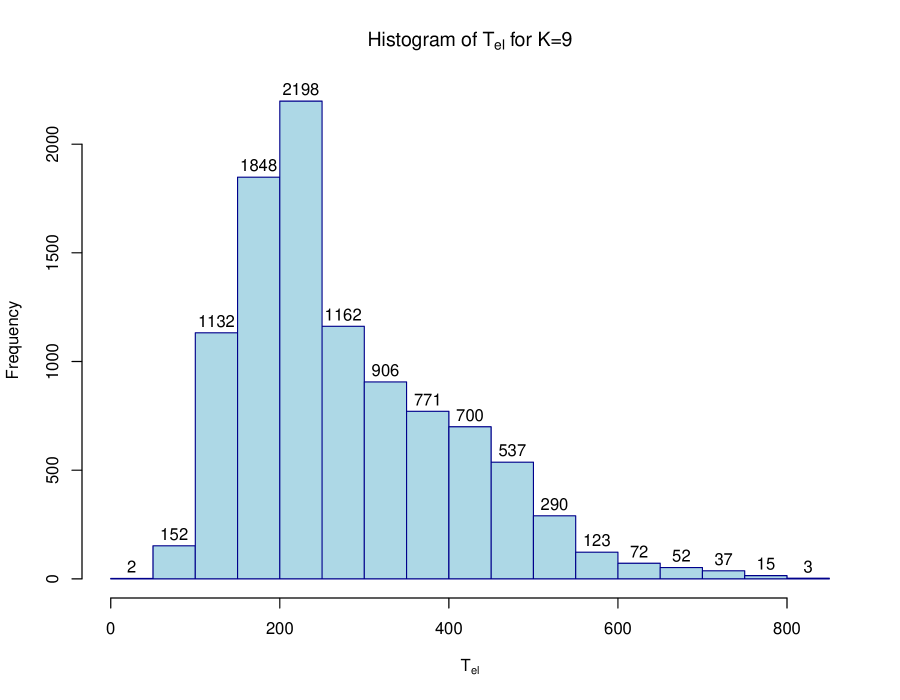

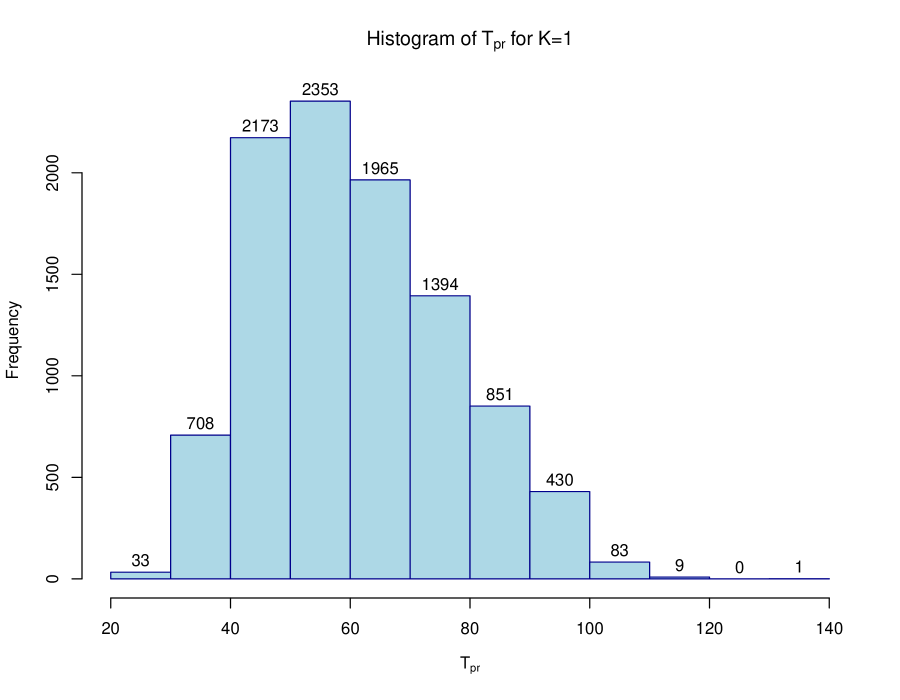

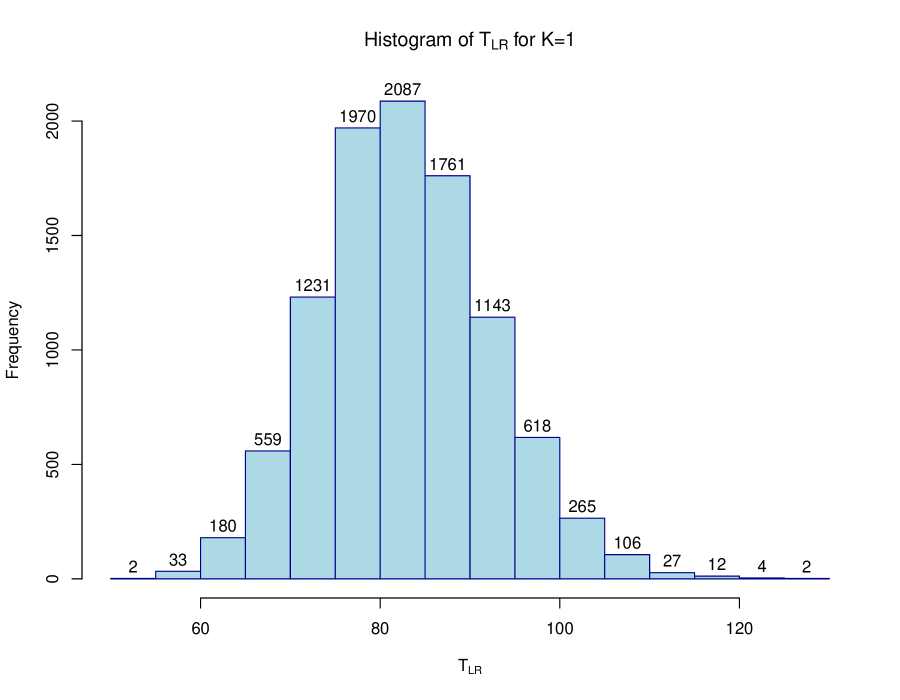

In order to get a better understanding of the obtained results, we also plot the histograms for the values of the test statistics in Figure 8 for (left hand-side plots) and for (right hand-side plots). Here, we observe that most of the values are much larger than the corresponding critical values presented in Table 1.

Figure 8 above here

7.2 Analysis of Stocks Included into the S&P 500 Index

In this subsection, we perform an analysis similar to the one provided in Section 7.1. In contrast to the models from Section 7.1, however, high-dimensional factor models are considered. These models are applied to model the dynamics in returns on stocks included into the S&P 500 index where stocks are chosen randomly out of stocks included into the S&P 500 index. As a result, models are fitted for which the high-dimensional tests of Section 5 are performed. We consider two types of factor models with one factor, the return of the S&P 500 index, and nine factors (the S&P 500 index, the NASDAQ-100, the NASDAQ bank index, the NASDAQ Composite index, the NASDAQ Biotechnology index, the NASDAQ Industrial index, the NASDAQ Transportation index, the NASDAQ Computer index, and the NASDAQ Telecommunications index). The weekly data are taken from the 11th of June, 2004 to the 10th of June, 2014 () from the Yahoo! finance web-page.

| Test | 0.1 | 0.05 | 0.01 | 0.005 |

|---|---|---|---|---|

| 17.4888 | 18.9975 | 22.4416 | 23.5609 | |

| 3.6521 | 3.9673 | 4.6190 | 4.9366 | |

| 1.2979 | 1.6562 | 2.3115 | 2.5480 | |

| Test | 0.1 | 0.05 | 0.01 | 0.005 |

| 17.6366 | 19.1353 | 22.5938 | 23.7658 | |

| 3.6266 | 3.9389 | 4.5929 | 4.8550 | |

| 1.2746 | 1.6037 | 2.3308 | 2.5761 | |

In Table 3, we show the critical values of the considered tests which are calculated via simulations based on independent samples from the inverse Wishart distribution. The resulting samples of the test statistics are used to determine the corresponding empirical distribution functions which are then applied to the calculation of the -values. The most important quantiles of the obtained -values are shown in Table 4. In contrast to Section 7.1, here all maxima of -values equal zero, meaning that the null hypothesis of the validity of the considered factor models are rejected by all tests in all of the considered cases.

| Test Quantile | Minimum | Lower Quartile | Median | Upper Quartile | Maximum |

|---|---|---|---|---|---|

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

| Test Quantile | Minimum | Lower Quartile | Median | Upper Quartile | Maximum |

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

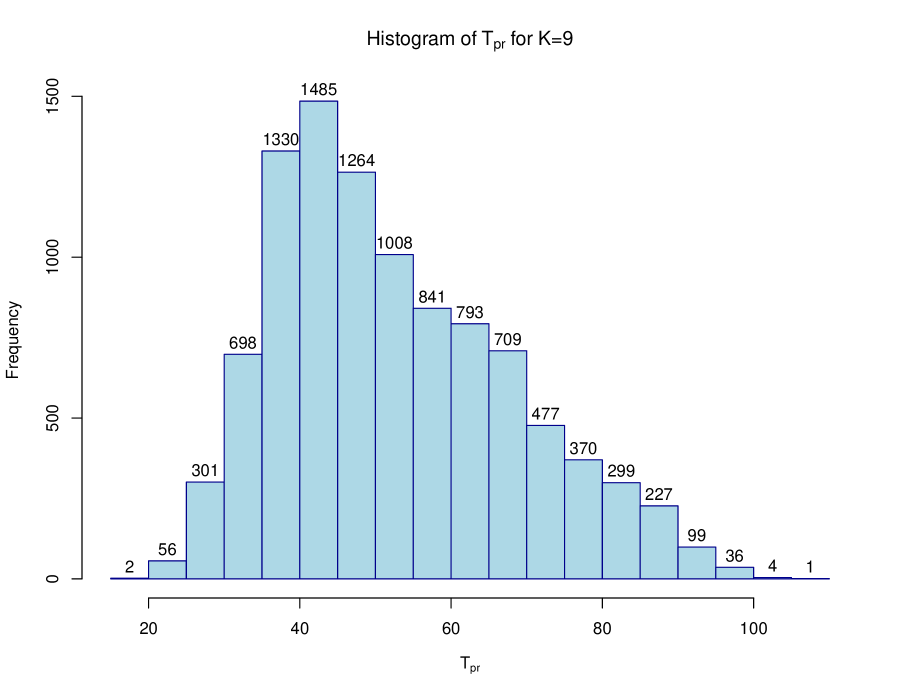

In Figure 9, we also plot the histograms for the values of the test statistics in case of (left-hand side plots) and (right-hand side plots). The histograms document that the values of the calculated test statistics are much larger than the critical values presented in Table 3. These findings do not support the hypothesis that the linear dependencies between the asset returns can be fully explained by the selected factors.

Figure 9 above here

8 Summary

Factor models of both small and large dimensions are a very attractive and popular modeling device nowadays. They are applied in different fields of science, like econometrics, economics, finance, biology, psychology, etc. While a lot of papers are devoted to the estimation of the parameters of factor models as well as to the determination of the number of factors, testing the validity of factor models has not been discussed widely in literature up to now. A notable exception is the test on the CAPM in low dimensions which is a special case of factor models.

In the present paper, we derive exact and asymptotic tests on the validity of factor models when the factors are observable. The results are obtained for both small-dimensional and high-dimensional factor models. The distributions of the suggested test statistics are derived under the assumption of normality and it is shown that they are independent of the diagonal elements of the precision matrix constructed from the dependent variables and factors. In order to investigate the powers of the considered tests, an extensive simulation study is performed. Its conclusion is that none of the tests performs uniformly better than the others and, consequently, the application of each test depends on the deviations to be detected under the alternative hypothesis. Finally, we apply the theoretical results of the paper in two empirical studies where factor models with different number of factors are fitted to the returns on stocks included into the DAX as well as the S&P index. Our empirical results do not support the hypothesis that all linear dependencies between the returns can be entirely captured by the considered factors. As a result, the factor models, which are based on the considered market indices, are not in general valid in practice and the investor can apply them with care only because they are not able to explain all linear dependencies between the asset returns.

It is remarkable that the tests suggested in the paper are also distribution-free for a large class of matrix-variate distributions. For instance, an application of Theorem 5.12 in Gupta et al., [51] shows that the distribution of the considered test statistics is the same if data follow a matrix-variate elliptically contoured distribution. This family of distributions includes plenty of well-known models, like the normal distribution, mixture of normal distributions, the multivariate -distribution, Pearson types II and VII distributions (see Gupta et al., [51]). Elliptically contoured distributions have been already applied in portfolio theory. Owen and Rabinovitch, [68] extend Tobin’s separation theorem and Bawa’s rules of ordering certain prospects to elliptically contoured distributions. Chamberlain, 1983a [29] shows that elliptical distributions imply mean-variance utility functions, whereas Berk, [17] argues that one of the necessary conditions for the CAPM is an elliptical distribution for the asset returns. Moreover, Zhou, [83] generalizes the test of Gibbons et al., [48] on the efficiency of a given portfolio to elliptically distributed returns. Hodgson et al., [54] propose a test for the CAPM under elliptical assumptions (see, also the textbook of Gupta et al., [51] for further results and applications to financial data). Finally, we point out that, since in the derivation of the high-dimensional asymptotic distributions of the test statistics their finite sample distributions are used, the above result holds true for both, low-dimensional and high-dimensional factor models.

The suggested tests and their distributions are derived under the assumption that the factors are observable which is motivated by the application of the CAPM and the APT. An important question is how to extend the suggested testing procedures to the case when the factors are unobservable, especially, when the number of factors is unknown as well. It is noted that the unknown factors can be estimated very accurately in high dimensions as shown in Bai and Ng, [10] and Bai and Ng, [12]. Consequently, the estimation of unknown factors is expected to have no large impact on the testing procedures suggested in the paper. The above two generalizations of our results are very attractive both, from a theoretical and a practical point of view and they will be treated in a consequent paper.

9 Appendix

In this section the proofs of lemmas and theorems are given.

Proof of Lemma 1

Beweis.

In the proof we deal with the case only and note that the other equalities can be derived similarly. Let and be partitioned as

The application of the inverse formula for the partitioned matrix (see Theorem 8.5.11 of Harville, [53]) yields

Since is positive definite, we deduce that its inverse is positive definite and, hence,

i.e., , where the equality is present only if . ∎

In the proofs of Theorems 2 and 3, we use the result of Lemma 2. In the following we consider several partitions of defined in (10) which are constructed with respect to its diagonal elements. In case of the first diagonal elements we get

| (37) |

whereas for the -th diagonal element, a similar partition is considered where the vector is obtained by deleting the th element form the th column of and is calculated by deleting the th column and the th row of .

Let be partitioned similar to (10) whose elements we denote by , , and for . Next, we consider the test statistic

| (38) |

for with in order to test the hypotheses

| (39) |

where is a matrix of constants.

Both test statistics and for and can be obtained from for some choices of the matrix . Later on, we make use of this result for proving Theorems 1 and 2.

In Lemma 2, the distribution of is derived under both the null and the alternative hypotheses.

Lemma 2.

Let follow model (1) where and are independent and normally distributed. Then:

-

(a)

The density of is given by

where with .

-

(b)

Under it holds that .

Beweis.

-

(a)

We consider

(40) From the proof of Theorem 3 in Bodnar and Okhrin, [23] we get that

and, consequently,

with which is independent of (see, e.g., Theorem 3 in Bodnar and Okhrin, [23]). Furthermore, it holds that and, hence,

Putting these results together we get

Because , we get

where denotes the density of the non-central -distribution with degrees and and noncentrality parameter ; stands for the density of the -dimensional Wishart distribution with degrees and covariance matrix . If we briefly write . It holds that (e.g., Theorem 1.3.6 of Muirhead, [66])

Let us denote

Using the notation for a square matrix , we get

where . From Theorem 3.2.8 of Muirhead, [66] we obtain that

Finally,

The result is proved.

-

(b)

The statement follows by noting that under and

∎

Proof of Theorem 1

Beweis.

The proof is based on the observation that the test statistic for each can be presented as from (40) with and (the vector of zeros with exception of the -th element which is one). In order to show this, we consider

Proof of Theorem 2

Proof of Theorem 3

Beweis.

Let and . We consider

Then, it holds that

Hence,

As the joint distribution of is fully determined by the distribution of which does not depend on , and as the distribution of coincides with the distribution of , we get that the distribution of is independent of . Finally, noting that the distribution of is fully determined by the distribution of , the statement of the theorem follows. ∎

Proof of Theorem 4

Beweis.

Next we prove the statement of Theorem 4.(b). It holds that

Since the conditional distribution given in the last equation does not depend on the condition it is also the unconditional distribution of the difference. Moreover, following the proof of Lemma 2 we get

Hence,

as . This leads to

and, hence,

The result in case of is obtained in the same way. ∎

Proof of Theorem 5

Beweis.

-

(a)

First, we consider the case . Then it holds that

From the proof of Lemma 2, we get that and it is independent of

Hence, from the law of large numbers and the central limit theorem we get as ,

(42) and

(43) as well as that both summands in the numerator are independent. Hence,

Now, let as . Then, we get

and

Putting these two results together we get the statement of the second part of Theorem 5.(a).

-

(b)

The proof of Theorem 5.(b) is achieved in the same way as the part (a) of this theorem. The only point which remains to be investigate is the asymptotic distribution of the numerator in the expression of .

Lemma 3.

Let with . Then for the random variable with such that , we get

-

(a)

(44) -

(b)

(45)

Beweis.

-

(a)

It holds that

Since from the law of large numbers we get that as . Furthermore, it holds that and, consequently

since . This completes the proof of the statement of Lemma 3.(a).

-

(b)

We get , , , and . This leads to

(46) Then, an application of the Lyapunov central limit theorem (see, e.g., Billingsley, [19, p. 362]) gives

∎

An application of Lemma 3.(b) leads to

-

(a)

∎

Acknowledgments

The authors are grateful to Professor Christian Genest, the associate editor and the referees for their suggestions, which have improved the presentation in the paper. We also thank David Bauder for his comments used in the preparation of the revised version of the paper.

Literatur

- Abramowitz and Stegun, [1964] Abramowitz, M. and Stegun, I. A., editors (1964). Handbook of Mathematical Functions with Formulas, Graphs and Mathematical Tables. Washington: U.S. Department of Commerce.

- Agarwal et al., [2012] Agarwal, A., Negahban, S., and Wainwright, M. J. (2012). Noisy matrix decomposition via convex relaxation: Optimal rates in high dimensions. Annals of Statistics, 40(2):1171–1197.

- Aguilar and West, [2000] Aguilar, O. and West, M. (2000). Bayesian dynamic factor models and portfolio allocation. Journal of Business & Economic Statistics, 18(3):338–357.

- Ahn and Horenstein, [2013] Ahn, S. C. and Horenstein, A. R. (2013). Eigenvalue ratio test for the number of factors. Econometrica, 81(3):1203–1227.

- Anderson and Vahid, [2007] Anderson, H. M. and Vahid, F. (2007). Forecasting the volatility of australian stock returns: Do common factors help? Journal of Business & Economic Statistics, 25(1):76–90.

- Artis et al., [2005] Artis, M. J., Banerjee, A., and Marcellino, M. (2005). Factor forecasts for the uk. Journal of Forecasting, 24(4):279–298.

- Bai, [2003] Bai, J. (2003). Inferential theory for factor models of large dimensions. Econometrica, 71(1):135–171.

- Bai, [2013] Bai, J. (2013). Fixed-effects dynamic panel models, a factor analytical method. Econometrica, 81(1):285–314.

- Bai and Li, [2012] Bai, J. and Li, K. (2012). Statistical analysis of factor models of high dimension. Annals of Statistics, 40(1):436–465.

- Bai and Ng, [2002] Bai, J. and Ng, S. (2002). Determining the number of factors in approximate factor models. Econometrica, 70(1):191–221.

- Bai and Ng, [2008] Bai, J. and Ng, S. (2008). Large dimensional factor analysis. Foundations and Trends (R) in Econometrics, 3(2):89–163.

- Bai and Ng, [2013] Bai, J. and Ng, S. (2013). Principal components estimation and identification of static factors. Journal of Econometrics, 176(1):18–29.

- Bai et al., [2014] Bai, Z., Fang, Z., and Liang, Y.-C. (2014). Spectral Theory of Large Dimensional Random Matrices and Its Applications to Wireless Communications and Finance Statistics. World Scientific Publishing Company.

- Bai et al., [2009] Bai, Z., Jiang, D., Yao, J.-F., and Zheng, S. (2009). Corrections to lrt on large-dimensional covariance matrix by rmt. Annals of Statistics, 37(6B):3822–3840.

- Bai and Silverstein, [2010] Bai, Z. and Silverstein, J. W. (2010). Spectral Analysis of Large Dimensional Random Matrices. New York, NY: Springer Science+ Business Media, LLC.

- Beaulieu et al., [2013] Beaulieu, M.-C., Dufour, J.-M., and Khalaf, L. (2013). Identification-robust estimation and testing of the zero-beta capm. The Review of Economic Studies, 80(3):892–924.

- Berk, [1997] Berk, J. B. (1997). Necessary conditions for the capm. Journal of Economic Theory, 73(1):245–257.

- Bernanke and Boivin, [2003] Bernanke, B. S. and Boivin, J. (2003). Monetary policy in a data-rich environment. Journal of Monetary Economics, 50(3):525–546.

- Billingsley, [1995] Billingsley, P. (1995). Probability and Measure. Chichester: John Wiley & Sons Ltd.

- Black, [1972] Black, F. (1972). Capital market equilibrium with restricted borrowing. Journal of Business, 45(3):444–455.

- [21] Bodnar, T., Gupta, A. K., and Parolya, N. (2014a). On the strong convergence of the optimal linear shrinkage estimator for large dimensional covariance matrix. Journal of Multivariate Analysis, 132:215–228.

- [22] Bodnar, T., Gupta, A. K., and Parolya, N. (2014b). Optimal linear shrinkage estimator for large dimensional precision matrix., pages 55–60. Contributions in Infinite-Dimensional Statistics and Related Topics. Bongiorno, E.G. and Goia, A. and Salinelli, E. and Vieu, P. (eds.), Società Editrice Esculapio.

- Bodnar and Okhrin, [2008] Bodnar, T. and Okhrin, Y. (2008). Properties of the singular, inverse and generalized inverse partitioned wishart distributions. Journal of Multivariate Analysis, 99(10):2389–2405.

- Boivin and Ng, [2005] Boivin, J. and Ng, S. (2005). Understanding and comparing factor-based forecasts. International Journal of Central Banking, 1(3):117–151.

- Cai and Liu, [2011] Cai, T. and Liu, W. (2011). Adaptive thresholding for sparse covariance matrix estimation. Journal of the American Statistical Association, 106(494):672–684.

- Cai et al., [2011] Cai, T., Liu, W., and Luo, X. (2011). A constrained minimization approach to sparse precision matrix estimation. Journal of the American Statistical Association, 106(494):594–607.

- Cai and Jiang, [2011] Cai, T. T. and Jiang, T. (2011). Limiting laws of coherence of random matrices with applications to testing covariance structure and construction of compressed sensing matrices. Annals of Statistics, 39(3):1496–1525.

- Carvalho et al., [2008] Carvalho, C. M., Chang, J., Lucas, J. E., Nevins, J. R., Wang, Q., and West, M. (2008). High-dimensional sparse factor modeling: applications in gene expression genomics. Journal of the American Statistical Association, 103(484):1438–1456.

- [29] Chamberlain, G. (1983a). A characterization of the distributions that imply mean-variance utility functions. Journal of Economic Theory, 29(1):185–201.

- [30] Chamberlain, G. (1983b). Funds, factors, and diversification in arbitrage pricing models. Econometrica, 51(5):1305–1323.

- Chamberlain and Rothschild, [1983] Chamberlain, G. and Rothschild, M. (1983). Arbitrage, factor structure in arbitrage pricing models. Econometrica, 51(5):1281–1304.

- Chen et al., [2010] Chen, S. X., Zhang, L.-X., and Zhong, P.-S. (2010). Tests for high-dimensional covariance matrices. Journal of the American Statistical Association, 105(490):810–819.

- DasGupta, [2008] DasGupta, A. (2008). Asymptotic Theory of Statistics and Probability. New York, NY: Springer.

- Dickhaus, [2012] Dickhaus, T. (2012). Simultaneous statistical inference in dynamic factor models. Technical report, SFB 649 Discussion Paper.

- Diebold and Nerlove, [1989] Diebold, F. X. and Nerlove, M. (1989). The dynamics of exchange rate volatility: a multivariate latent factor arch model. Journal of Applied Econometrics, 4(1):1–21.

- Eaton, [2007] Eaton, M. L. (2007). Multivariate statistics. A vector space approach. Beachwood, OH: IMS, Institute of Mathematical Statistics.

- Engle and Watson, [1981] Engle, R. and Watson, M. (1981). A one-factor multivariate time series model of metropolitan wage rates. Journal of the American Statistical Association, 76(376):774–781.

- Fama, [1976] Fama, E. (1976). Foundations of Finance. New York: Basic Books.

- Fama and French, [1992] Fama, E. F. and French, K. R. (1992). The cross-section of expected stock returns. The Journal of Finance, 47(2):427–465.

- Fama and French, [1993] Fama, E. F. and French, K. R. (1993). Common risk factors in the returns on stocks and bonds. Journal of Financial Economics, 33(1):3–56.

- Fan et al., [2008] Fan, J., Fan, Y., and Lv, J. (2008). High dimensional covariance matrix estimation using a factor model. Journal of Econometrics, 147(1):186–197.

- [42] Fan, J., Han, X., and Gu, W. (2012a). Estimating false discovery proportion under arbitrary covariance dependence. Journal of the American Statistical Association, 107(499):1019–1035.

- Fan et al., [2013] Fan, J., Liao, Y., and Mincheva, M. (2013). Large covariance estimation by thresholding principal orthogonal complements. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 75(4):603–680.

- [44] Fan, J., Zhang, J., and Yu, K. (2012b). Vast portfolio selection with gross-exposure constraints. Journal of the American Statistical Association, 107(498):592–606.

- Favero et al., [2005] Favero, C. A., Marcellino, M., and Neglia, F. (2005). Principal components at work: the empirical analysis of monetary policy with large data sets. Journal of Applied Econometrics, 20(5):603–620.

- Friguet et al., [2009] Friguet, C., Kloareg, M., and Causeur, D. (2009). A factor model approach to multiple testing under dependence. Journal of the American Statistical Association, 104(488):1406–1415.

- Giannone et al., [2006] Giannone, D., Reichlin, L., and Sala, L. (2006). Vars, common factors and the empirical validation of equilibrium business cycle models. Journal of Econometrics, 132(1):257–279.

- Gibbons et al., [1989] Gibbons, M. R., Ross, S. A., and Shanken, J. (1989). A test of the efficiency of a given portfolio. Econometrica, 57(5):1121–1152.

- Gupta and Nagar, [2000] Gupta, A. and Nagar, D. (2000). Matrix Variate Distributions. Boca Raton, FL: CRC Press.

- Gupta and Bodnar, [2014] Gupta, A. K. and Bodnar, T. (2014). An exact test about the covariance matrix. Journal of Multivariate Analysis, 125:176–189.

- Gupta et al., [2013] Gupta, A. K., Varga, T., and Bodnar, T. (2013). Elliptically Contoured Models in Statistics and Portfolio Theory. New York, NY: Springer.

- Hallin and Liška, [2007] Hallin, M. and Liška, R. (2007). Determining the number of factors in the general dynamic factor model. Journal of the American Statistical Association, 102(478):603–617.

- Harville, [1997] Harville, D. A. (1997). Matrix Algebra from a Statistician’s Perspective. New York, NY: Springer.

- Hodgson et al., [2002] Hodgson, D. J., Linton, O., and Vorkink, K. (2002). Testing the capital asset pricing model efficiently under elliptical symmetry: A semiparametric approach. Journal of Applied Econometrics, 17(6):617–639.

- Jiang and Yang, [2013] Jiang, T. and Yang, F. (2013). Central limit theorems for classical likelihood ratio tests for high-dimensional normal distributions. Annals of Statistics, 41(4):2029–2074.

- Johnstone, [2001] Johnstone, I. M. (2001). On the distribution of the largest eigenvalue in principal components analysis. Annals of Statistics, pages 295–327.

- Kapetanios, [2010] Kapetanios, G. (2010). A testing procedure for determining the number of factors in approximate factor models with large datasets. Journal of Business & Economic Statistics, 28(3):397–409.

- Ledoit and Wolf, [2003] Ledoit, O. and Wolf, M. (2003). Improved estimation of the covariance matrix of stock returns with an application to portfolio selection. Journal of Empirical Finance, 10(5):603–621.

- Li et al., [2013] Li, H., Li, Q., and Shi, Y. (2013). Determining the number of factors when the number of factors can increase with sample size. Manuscript.

- Lintner, [1965] Lintner, J. (1965). Security prices, risk, and maximal gains from diversification. The Journal of Finance, 20(4):587–615.

- Lütkepohl, [1996] Lütkepohl, H. (1996). Handbook of Matrices. John Wiley & Sons.

- Marcellino et al., [2003] Marcellino, M., Stock, J. H., and Watson, M. W. (2003). Macroeconomic forecasting in the euro area: Country specific versus area-wide information. European Economic Review, 47(1):1–18.

- Markowitz, [1959] Markowitz, H. M. (1959). Portfolio Selection: Efficient Diversification of Investments.

- Markowitz, [1991] Markowitz, H. M. (1991). Foundations of portfolio theory. The Journal of Finance, 46(2):469–477.

- Merton, [1973] Merton, R. C. (1973). An intertemporal capital asset pricing model. Econometrica, 41(5):867–887.

- Muirhead, [1982] Muirhead, R. J. (1982). Aspects of Multivariate Statistical Theory. Wiley Series in Probability and Mathematical Statistics. New York: John Wiley & Sons.

- Onatski, [2010] Onatski, A. (2010). Determining the number of factors from empirical distribution of eigenvalues. The Review of Economics and Statistics, 92(4):1004–1016.

- Owen and Rabinovitch, [1983] Owen, J. and Rabinovitch, R. (1983). On the class of elliptical distributions and their applications to the theory of portfolio choice. The Journal of Finance, 38(3):745–752.

- Reiß et al., [2014] Reiß, M., Todorov, V., and Tauchen, G. (2014). Nonparametric test for a constant beta over a fixed time interval. arXiv preprint arXiv:1403.0349.

- Rencher, [2002] Rencher, A. C. (2002). Methods of Multivariate Analysis. Chichester: Wiley.

- Ross, [1976] Ross, S. A. (1976). The arbitrage theory of capital asset pricing. Journal of Economic Theory, 13(3):341–360.

- Ross, [1977] Ross, S. A. (1977). The capital asset pricing model capm, short-sale restrictions and related issues. The Journal of Finance, 32(1):177–183.

- Rubin and Thayer, [1982] Rubin, D. B. and Thayer, D. T. (1982). Em algorithms for ml factor analysis. Psychometrika, 47(1):69–76.

- Sentana, [2009] Sentana, E. (2009). The econometrics of mean-variance efficiency tests: a survey. Econometrics Journal, 12(3):C65–C101.

- Shanken, [1986] Shanken, J. (1986). Testing portfolio efficiency when the zero-beta rate is unknown: A note. The Journal of Finance, 41(1):269–276.

- Shanken, [1992] Shanken, J. (1992). On the estimation of beta-pricing models. Review of Financial Studies, 5(1):1–33.

- Shanken and Zhou, [2007] Shanken, J. and Zhou, G. (2007). Estimating and testing beta pricing models: Alternative methods and their performance in simulations. Journal of Financial Economics, 84(1):40–86.

- Sharpe, [1964] Sharpe, W. F. (1964). Capital asset prices: A theory of market equilibrium under conditions of risk. The Journal of Finance, 19(3):425–442.

- [79] Stock, J. H. and Watson, M. W. (2002a). Forecasting using principal components from a large number of predictors. Journal of the American Statistical Association, 97(460):1167–1179.

- [80] Stock, J. H. and Watson, M. W. (2002b). Macroeconomic forecasting using diffusion indexes. Journal of Business & Economic Statistics, 20(2):147–162.

- Tu and Zhou, [2004] Tu, J. and Zhou, G. (2004). Data-generating process uncertainty: what difference does it make in portfolio decisions? Journal of Financial Economics, 72:385–421.

- Velu and Zhou, [1999] Velu, R. and Zhou, G. (1999). Testing multi-beta asset pricing models. Journal of Empirical Finance, 6(3):219–241.

- Zhou, [1993] Zhou, G. (1993). Asset-pricing tests under alternative distributions. The Journal of Finance, 48(5):1927–1942.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|