Spatial

discretization error in Kalman filtering for discrete-time infinite

dimensional systems

Atte Aalto

Abstract.

We derive a reduced-order state estimator for

discrete-time infinite dimensional linear systems with finite

dimensional Gaussian input and output noise. This state estimator is

the optimal one-step estimate that takes values in a fixed finite

dimensional subspace of the system’s state space — consider, for

example, a Finite Element space. We then derive a Riccati difference

equation for the error covariance and use sensitivity analysis to

obtain a bound for the error of the state estimate due to the state

space discretization.

In this paper, we consider the state estimation problem for infinite

dimensional discrete time linear systems with finite dimensional

Gaussian input and output noise. The objective is to find the optimal

one-step state estimate from a given subspace of the original state

space (for example a Finite Element space). We shall also find a bound

for the error due to the spatial discretization to the state estimate

at the infinite time limit.

The dynamics of the system under consideration is given by

(1)

where , , , and . The state space is a separable

Hilbert space.

The noise processes are assumed to be Gaussian, and

where and are positive-definite and symmetric. It is

also assumed that , , and are mutually independent, and the

noises at different times are independent.

When measurements for are known, the state estimate

minimizing the conditional expectation

is

given by . In the presented

Gaussian case, the conditional expectation can be computed

recursively from and . This recursive scheme is

known as the Kalman filter, originally presented in [12] in

the finite dimensional setting. For infinite dimensional systems, the

generalization is straightforward and it can be done, for example,

using the presentation by Bogachev [4: Section 3.10] or

the more explicit presentation [14] by Krug. Let us present a

short introduction. It is well known that linear combinations of

Gaussian random variables

are also Gaussian random variables. Further, if where and is finite

dimensional, then

(2)

and

(3)

Remark that

so that in fact,

(4)

Applying (2) and (3) to the jointly

Gaussian random variable and the block matrix

inversion formula

(5)

to

eventually leads to the full state Kalman filter equations

(6)

where for are called Kalman gains, and

they are given by , and the Riccati difference equation (RDE)

(7)

Here is the

(estimation) error covariance and

is the prediction error covariance. The initial values are

and .

The superscript refers to full Kalman filter estimate and it is

used for later purposes.

Numerical implementation of the Kalman filter to infinite dimensional

systems requires discretization of the state space. If the

implementation is then carried out directly to the discretized system,

the result is not optimal. In particular, if the state estimation is

performed online, the restrictions in computing power might prevent

using a very fine mesh for the simulations. In such cases it is

beneficial to take the discretization error into account in the state

estimation. The purpose of this paper is to derive the optimal

one-step state estimate that takes values in the discretized state

space, and to analyze the discrepancy between the proposed state

estimate and the full state Kalman filter estimate.

We tackle this task in Section 2 by first fixing the

structure of the filter in (8). In the spirit of

Kalman filtering, we require that the estimate

depends only on the previous estimate and the current measured output

. We then find the expression for a filter with such structure.

The rest of the paper is organized as follows: In

Section 3, we derive a Riccati difference equation

for the estimation error covariance for the proposed method. Compared

to (7), this equation contains an additional term due

to the discretization. In Section 4, we use sensitivity

analysis for algebraic Riccati equations — developed by Sun

in [23] — to determine a bound for the error due to the

discretization at the infinite time limit. In short, it is shown that

when the approximation properties of the subspace improve at some rate

as the spatial discretization is refined, then the finite dimensional

state estimate converges to the full state Kalman filter estimate at

least with the same convergence rate. In Section 5,

the proposed method is implemented to one dimensional wave equation

with damping, and the result is compared with the Kalman filter that

does not take into account the spatial discretization error.

The “engineer’s approach”, i.e., the direct Kalman filter

implementation to the discretized system is studied in

[1] by Bensoussan and in [7] by

Germani et al. The latter contains a convergence result for the

finite dimensional state estimate (in continuous time) with a

convergence rate estimate. They also show convergence of the solutions

of the corresponding Riccati differential equations in the space of

continuous Hilbert-Schmidt operator-valued functions. A method where

the discretization error is taken into account is proposed by

Pikkarainen in [17]. Their approach is based on

keeping track of the discretization error mean and covariance. Then

with certain approximations on the error distributions, they too end

up with a one-step method that is numerically implemented in

[11] by Huttunen and Pikkarainen.

Our method is very closely related to the reduced-order filtering

methods that have been studied since the introduction of the Kalman

filter itself; see e.g., [2; 3; 19; 20; 22]. The articles by Bernstein and Hyland,

[2; 3] yield a state estimator similar to ours

for continuous time. They obtain algebraic optimality equations for

the error covariance and Kalman gain limits as the time index , in terms of “optimal projections”. Our solution is somewhat

more straightforward, and we obtain the error covariances and Kalman

gains for all time steps. A similar method is developed by Simon in

[19] with a more restrictive assumption on the filter

structure. For a more thorough introduction and review on the earliest

results on reduced-order filtering techniques, we refer to [22]

by Stubberud and Wismer and to [20] by Sims.

Infinite dimensional Kalman filter has numerous applications. The

practical application that motivated the paper [17] is

the electrical impedance process tomography, studied by Seppänen

et al. in [18]. Infinite dimensional Kalman filter

implementation to optical tomography problem can be found in

[9] by Hiltunen et al. Quasiperiodic phenomena is

studied by Solin and Särkkä in [21] using the infinite

dimensional Kalman filter. They use a weather prediction model and

fMRI brain imaging as example cases. The numerical treatment is done

using truncated eigenbasis approach instead of using FEM as in the

example of this article.

Notation

We denote by the space of bounded linear

operators from to , and

. The subspace of self-adjoint

operators in is denoted by . The spectrum of

an operator is denoted by . The sigma algebra generated

by a random variable (or random variables) is denoted by

. The Moore-Penrose pseudoinverse of a matrix

is denoted by .

The covariance of square integrable random variables

and is the operator in

defined for by

.

2. The reduced-order state estimate

Let be an orthogonal projection from the state

space (a separable, complex Hilbert space) to an -dimensional

subspace of (e.g., a finite element space). Assume we have a

coordinate system in associated to this subspace, such

that the inner product is preserved, and denote by the representation of the projection in this

coordinate system. That is, for . Then it holds that

and .

Finding an exact solution to the estimation problem of the finite

dimensional would require solving the full state Kalman

filtering problem and then projecting the estimate by . This, of

course, doesn’t make much practical sense.

As mentioned above, we want to find the optimal state estimate in that can be computed from the previous state

estimate and the current measurement . More

precisely, we want to obtain ’s satisfying

(8)

where satisfy (1). One thing to notice here is

that in contrast to the full state filtering, the conditioning is not

done over a filtration, because — loosely speaking — we lose some

information when we only take into account the last measurement and

the last estimate of the state projection. Without loss of

generality, we may assume that (see Remark 2.1).

Note that this

also implies and further, and

for all .

We then proceed to find a concrete representation for . From (8) it can be inductively deduced that

is Gaussian and from (1),

also is Gaussian. The reasoning leading to

the full state Kalman filter equations utilizing equations

(2) and (3) together with the block matrix

inversion formula (5) can be generalized for any Gaussian

random variable with , and and

finite dimensional, to obtain

(9)

The corresponding equation can be obtained for the covariance

operator. The full state Kalman filter equations (6) and

(7) are obtained by applying (9) to

, , and . In what follows, we

obtain by applying (9) to ,

, and .

Since , there exists an operator such that

(10)

and the (estimation) error covariance

(11)

Using these we can make an orthogonal decomposition of the state

where and it is independent of the

estimate . Together with (1), this gives

decompositions for the state and output :

(12)

from which one can deduce and .

Then we need the two covariances in (9). To this end,

define the prediction error covariance for which we get a

representation from (12),

and the covariance of output prediction error from the second equation in

(12)

Now we have all the components for obtaining by

(9),

(14)

It remains to compute the error covariance defined in

(11), and the operator defined through

(10). By (4), is given by

where is the state covariance and is the state estimate

covariance. The state is a linear combination of mutually

independent Gaussian random variables and and so

can be obtained from the Lyapunov difference equation

(15)

and the first one, , is the initial state covariance in

(1). Also, by (12),

(16)

where , , and are mutually independent and also

independent with the state estimate . Thus, by

(14), also is obtained from a Lyapunov

difference equation,

The case when is not invertible is discussed in

Remark 2.2.

The cross covariance operator

in (18) can be computed by

“anchoring” and to using

equations (12) and (14) and the fact that

,

It is worth noting here that

implying the intuitive fact, in the case that

is invertible.

Let us conclude by presenting some remarks concerning the derivation

of the reduced-order state estimate and then collecting the relevant

equations to an algorithm.

Remark 2.1.

The assumption does not

restrict generality, since we can always always add to

and subtract from in

(12). However, this is how to make the

derivation accurate. In practical implementation, it is reasonable

to just start the state estimate from and then

proceed as described.

Remark 2.2.

If is not invertible, it means that , the range of , does not cover the whole space

. The estimate lies on

almost surely. Thus is not

determined uniquely in this case. By imposing additional

requirements and

then

is uniquely determined and it is given by where .

Algorithm 2.3.

As with the full state Kalman

filter, the following operator-valued equations can be computed

beforehand (offline):

The initial values are (given in (1)),

, , and .

The state estimate is given by

Practical implementation of the proposed method is discussed

in Section 6.1. An alternative equation for is

derived in the following section.

3. The error covariance equation

Motivated by the main theorem of [2], we next seek for a

Riccati difference equation satisfied by the error covariance

. This equation will be needed later for determining a bound for

the error in the state estimate due to the spatial discretization. To

this end, define the augmented state

for which we have dynamic equations

The augmented state covariance satisfies the Lyapunov difference equation

(19)

where . This covariance can be written

as a block operator by where and are the state and state estimate

covariances, given in (15) and (17),

respectively. Now it holds that (or if is not

invertible) and thus for the reduced-order error covariance defined in

(11), it holds that . Also, for the prediction error covariance we have

by

(13).

Using these notations we get from (19)

and similarly . Using the state

covariance Lyapunov equation (15) and the equations above

and noting that , we see that the error covariance satisfies the

Riccati difference equation (RDE)

(20)

This equation is posed in . Note that this is not a

complete set of equations, but the last equation in

Algorithm 2.3 can be replaced by the second equation in

(20). Compared to the RDE (7) for the

full state Kalman filter, this equation contains the additional load

term in the last line of (20). In the next section we

find an upper bound for the effect of this additional term to the

solution at the infinite time limit but first we need to go through

some auxiliary results.

Proposition 3.1.

Let and be sigma algebras, such that

and an integrable random

variable. Then

.

If is quadratically integrable then

Lemma 3.2.

Assume that the state covariance

defined in (15) satisfies for all for some

trace class operator . For the

discretization error term in the RDE (20), it holds

that

(21)

Proof.

Note that . Then by (14) and

(16) it can be seen that

It holds that

where the first equality follows by (8), the second

by the definition of , (10), and the third by

Proposition 3.1 and which, in turn, can be seen from

(8).

Thus minimizes

over for all .

Since , it holds that

where the middle inequality holds by Proposition 3.1.

∎

Lemma 3.3.

Let for , be the solutions of the RDEs

(22)

where and . Then for all .

This follows from [6: Lemma 3.1] by de Souza

in the finite dimensional setting. The proof is just algebraic

manipulation and it holds also in the infinite dimensional setting (if

the output is finite dimensional). However, we shall present a

straightforward proof.

Proof.

We show . For larger the result follows by

induction. Define the block diagonal covariances in

and . Then define

Now implies . Then and so . Now and

so .

∎

The following lemma is due to Hager and Horowitz,

[8]:

Lemma 3.4.

Assume that for all

for some trace class operator where

is defined in (15). Let be the solution of

(7) and be the solution of

(22) with where is

defined in (21). Assuming , then

strongly as . Also, the

limit operators are the unique nonnegative

solutions of the discrete time algebraic Riccati equation (DARE)

(23)

where .

If with where

is the limit of the full state Kalman gain, that is

(24)

then

strongly, starting from any .

The first part follows from [8: Theorem 1]

because , and the second part from

[8: Theorem 3].

Even the weak convergence would suffice for the dominated convergence

of trace class operators:

Lemma 3.5.

If , , and for

are trace class operators in , for all , and , then .

The proof is rather straightforward after noting that

as , for

all where is an

orthonormal basis for .

4. Error analysis

Next we use sensitivity analysis for DAREs and the results of the

preceding section to show a bound for the discrepancy

of the full and

reduced-order state estimates, defined in (6) and

(8), respectively. The results of this section are

based on bounding the effect of the perturbation in

(21) caused by the spatial discretization. Such bound is

possible if we have additional information about the smoothness of the

state . That is, it is assumed that lies in a subspace

of — which is a Hilbert space itself — and that the

projection approximates well the vectors in that subspace,

meaning that the norm

becomes small as the spatial discretization is refined.

We show two theorems — first (Thm. 4.1) is

an a priori type estimate on the convergence rate of

, and the second

(Thm. 4.2) is an a posteriori estimate of the

error .

Theorem 4.1.

Consider the system (1) and the reduced order state

estimator derived in Sections 2 and

3. Make the following assumptions:

(i)

a.s. for all where is a Hilbert

space that is a vector subspace of and

.

(ii)

The state covariance defined in (15)

converges to the solution of the Lyapunov equation ,

that is, and for

all . Use this in the definition of in

(21).

(iii)

The converged full state Kalman filter is exponentially

stable, meaning for some

where is the Kalman gain of the converged full

state Kalman filter, introduced in (24).

Assume first that the initial state is completely known, that is,

. Let be the error covariance of the reduced order

method, satisfying the RDE (20) and be defined

in (21). It is easy to confirm that the shifted

covariance satisfies the RDE

Then denote by and the solution of a

similar RDE but with the term replaced by where

is the upper bound for , defined in (21). Finally,

let be the error covariance of the full Kalman filter

estimate, given in (7) and is given in (6).

By computing the trace of both sides of (4), we see

that for a Gaussian random variable it holds that

Now depends linearly on and thus clearly

. By

Proposition 3.1, it holds that . Thus it holds that

By Lemmas 3.2 and 3.3, and thus . By

Lemma 3.4, and strongly (recall ) where and are

the solutions of the corresponding DAREs, that is,

equation (23) with and

. Also, by Lemma 3.5, and . Denote and note

that is a positive (semi-)definite

trace class operator. Then an upper bound for the discrepancy is given

by

(25)

Equation (30) in Lemma A.2 gives a representation

for . The next step is to use this equation to find a bound

for .

Because the full Kalman filter is assumed to be exponentially stable,

by Lemmas A.1 and A.2, we have

where is defined in

Lemma A.1 and , , and are

defined in Lemma A.2. The term in

(30) is excluded here because it is negative definite (see

the discussion after Lemma A.1).

where is defined in Lemma A.1, , and .

By the last part of Lemma A.2, we have

(26)

where

Collecting these inequalities we finally get

(27)

where

To complete the proof under the assumption , use

(25), (27), and note that by the definition

of in (21) and in assumption (ii),

In case , the convergence has to be

established. Denote and . Pick from the resolvent set of

. Then using the Woodbury formula, we get

and

where is the spectral radius of . The invertibility of

is then guaranteed if which implies that the

spectral radius of is at most . So when is small enough, then

also is exponentially stable and

strongly.

∎

The assumption (iii) in Theorem 4.1 is very

difficult to check. Also, it is hard to say what it means that

“ is small enough”

which is related to the denominator in Eq. (27) and the

exponential stability of .

Consequently, this theorem should be considered as an a priori

convergence speed estimate when the discretization is refined, that

is, when .

However, if one has already computed the operators and and

they have converged to and and it has turned

out that for some , then by the same argument as in Theorem 4.1 we get the

following improved error estimate:

Theorem 4.2.

Make the assumptions (i) and (ii) in Theorem 4.1.

Assume also that the operators , , and related to

the reduced order filter have converged to , and

, respectively, and

for some .

Then

The covariances and defined in the

proof of Theorem 4.1 converge to and that are the solution of the DARE

Now bounding by using the alternative

expression (31) for given in

Lemma A.2 and otherwise proceeding as in the proof of

Theorem 4.1 leads to the result. Note that

but since for all , it holds that

.

∎

Remark 4.3.

The coefficients and

in the above theorem depend on and which

is not desirable. It is possible to bound these coefficients from

above without computing them. Firstly, we have

In this section, Algorithm 2.3 is implemented to the

temporally discretized 1D wave equation with damping,

(28)

where and are the formal

derivatives of Brownian motions with incremental covariances and

, respectively. The initial state is a Gaussian random variable

, and , , and are mutually

independent. The input operator is a multiplication operator but

we define its structure only on the discrete-time level. The output

operator is given by

where

and .

The equation is transformed to a first order differential equation

with respect to the time variable by introducing the augmented state

where is the velocity

variable. The natural augmented state space is . In

we use the norm . The

equation is then temporally discretized using the implicit Euler

method with time step . The state space discretization is

carried out by Finite Element Method using piecewise linear elements

on two meshes on the interval . The first one is a finer mesh

with equispaced discretization points. The fine mesh solution is

regarded as the true solution. The second, coarse mesh consists of

discretization points, also equally spaced with discretization

intervals of length . It is required that the function

space consisting of the piecewise linear elements on the coarse mesh

is a subspace of the fine mesh space. This is satisfied when for some integer . The coarse mesh space is the range

of . In the augmented state of the discretized system, the input

operator is where

, , and . The input noise covariance for the discrete time system is

.

The solution of (28) actually has additional smoothness,

namely almost surely — note that . It is well known that the piecewise

linear elements approximate -functions in one dimension so that

and

-functions so that , see for example [15: Section 5.1].

Fig. 1 (left) shows the state together with

the three different state estimates in one simulation. The full state

Kalman filter estimate (F) and the reduced-order state estimate (A)

cannot be distinguished from each other. The third state estimate (C)

is computed in the coarse mesh without taking the discretization error

into account. The simulation parameters are shown in

Table 1 (left). The spectral radius was .996 for

both the full state Kalman filter and the reduced-order filter. We

are interested in the stationary Kalman filter and so the

simulations were first run 2000 steps to get rid of initial

transitions. The expected (squared) errors of the different methods

are shown in Table 1 (right) separately for the

position variable and the velocity variable .

As , the expected squared difference between the

reduced-order estimate and full state Kalman filter estimate, , tends to

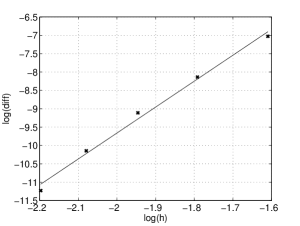

zero. Fig. 1 (right) illustrates this convergence in

the example case. Regression analysis gives

whereas Theorem 4.1 gives convergence

rate.

Figure 1. Left: The true solution and estimates given by the three

filtering methods. Right: The convergence of as

is shown with the x-markers. The solid line is a fitted regression

line. The plot is in logarithmic scale.

6. Conclusions and remarks

When the system at hand is infinite dimensional (or its dimension is

very large), one needs to make some finite (or lower) dimensional

approximation of the system in order to be able to actually compute

something. For what comes to the Gaussian state estimation problem,

the spatial discretization introduces a bias in the Kalman filter but

the result can be improved by taking that error into account when

determining the Kalman gain.

In this paper, we derived the optimal one-step state estimator for an infinite dimensional system that takes values in a

pre-defined finite dimensional subspace of the system’s

state space . The presented method also gives an operator

that gives . This operator can be

used as a sort of post-processor of the obtained state estimate.

Sections 3 and 4 were devoted to

finding a bound for the error caused by the discretization. The error

measure is the -distance between the reduced-order

state estimate and the full state Kalman filter

estimate , that is, . It was found that this distance converges to

zero as the approximation abilities of the projection improve.

A numerical example on temporally discretized 1D wave equation was

presented in Section 5. It was noted that the

presented method worked well even with fairly low level of

discretization. The spatial discretization was done using piecewise

linear hat functions whose approximating properties were noted to

converge with rate when the discretization is

refined. By Theorem 4.1 this would imply convergence rate

for the

reduced-order state estimate. However, numerical simulations showed

that this convergence was actually of order in the

example case.

6.1. On practical implementation

Even though all the computations needed for the update of the state

estimate are carried out in the finite dimensional subspace

in the presented method, the offline computations needed for

determining the Kalman gains and the operators are still

formally carried out in the infinite dimensional . In practice,

there are very few cases where this can be done analytically, and even

then it is hardly worth the effort. A practical approach is proposed

in the example, namely introducing two computational meshes for the

problem at hand — a fine mesh and a coarse mesh. The fine mesh

discretization is then regarded as the true system and and

are computed using this discretization. This mesh should be as fine

as reasonably possible. The online state estimation is then carried

out in the coarse mesh. Of course, the criterion for this mesh is that

the time evolution of the state estimator has to be solvable with the

available computing power in time before the next measurement arrives.

In practical implementation of the presented method, one weak point is

the computation of which in theory requires computation of the

(pseudo)inverse of the matrix , see

(18). As noted in Remark 2.2, when

is not invertible then . This

equation for could also be used if the pseudoinverse is not

computed accurately, but by using some approximative or regularizing

scheme. Then the part that maps to is readily taken

care of and from one can compute an approximation to

a couple of the most important dimensions in the null space of .

We also remark that there is no guarantee that and would

converge. Further, even if they do converge, there are no algebraic

equations for obtaining the limits directly. Thus, the only way to

obtain them is to iterate the recursive equation sufficiently many

times. However, consider the case that we are given and we

want to recover . Then (assuming ) the optimal

solution is given by where

Now converges and the limit can be obtained as the

solution of the Lyapunov equation .

Of course, the error is correlated but making the (false)

assumption that it is not, leads to an approximate reduced order error

covariance (in converged form)

It was found that using this approximative state estimate worked

reasonably well in the presented example. With the parameters on the

left in Table 1, the error was in average over 500

simulations .6148 for the position variable and .8179 for the velocity

variable (cf. the right panel of Table 1).

6.2. Further work

Let us end the paper by briefly discussing topics that would require

further work. An immediate question is whether a similar result can be

obtained for the Kalman–Bucy filter, that is, for continuous time

systems. Here the discrete time systems were studied for technical

convenience but, in principle, there should not be any reasons why it

couldn’t be done. For example the results of [2],

[3] and [7] were obtained in the

continuous time setting. In particular [7] might

give useful tools for treating this problem.

The dual problem to the Gaussian state estimation problem is the

optimal control problem for linear systems with quadratic cost

functions. A natural question is whether the results of this paper can

be translated to that problem. For example Mohammadi et al. use

truncated eigenbasis approach to approximately solve the algebraic

Riccati equation arising from optimal control of a

diffusion-convection-reaction in [16].

One topic that was not given much attention in this paper is the

optimality of the assumptions on the system. It is well known that the

classical Kalman filter might work just fine even though the

underlying system is not stable. We, on the other hand, used many

times the input stability of the system, i.e., the state

covariance is uniformly bounded by some trace class operator . Also, we had to state as an assumption that the full state Kalman

filter is exponentially stable, that is, for some . Relaxing this assumption would be

desirable since for example strong (that is, asymptotical) stability

of the full state filter is proved in [10: Theorem 4.2]

— although under a controllability assumption that would exclude

finite dimensional control.

Acknowledgements

The author has been supported by the Finnish Graduate School in

Engineering Mechanics. The author thanks Dr. Jarmo Malinen for

valuable comments on the manuscript.

Appendix A Auxiliary results

Lemma A.1.

Define the operator by

where for . This

operator has the following properties:

(i)

is boundedly invertible.

(ii)

If , then implies .

(iii)

There exists a constant s.t. for all positive definite trace class operators . Denote by the smallest possible

constant. Denote . We have .

Define also

where is the converged gain of the reduced order filter

(if it converges) and denote by the corresponding trace

bound for .

Proof.

(i): The inverse of is given by

(29)

By Gelfand’s formula (see [13: Theorem 7.5-5]), the sum

converges in operator topology because for some .

(ii): Assume that is positive

semidefinite. From (29)

it is easy to see that is positive

semidefinite. Clearly also if is negative semidefinite then is

negative semidefinite.

(iii): If is a positive definite trace

class operator and then . This together with

(29) imply (iii).

∎

If where then

where and . Of course . Thus, if the right hand side can be

represented as a sum of a positive definite and a negative definite

part, then only the positive definite part needs to be taken into

account when computing an upper bound for the trace of the solution.

Lemma A.2.

The perturbation in the proof of Theorem 4.1

satisfies

(30)

where

where , and

Alternatively, the equation (30) can be written as

(31)

The perturbation of the Kalman gain is given by

For a proof, see [23: Lemma 2.1]. There everything is

finite-dimensional but the proof of this Lemma is based on just

algebraic manipulation and it holds also in the infinite-dimensional

setting. Note that the matrix is

invertible because and . In the proof of [23: Lemma 2.1], some additional assumptions

on the perturbations is needed to guarantee the invertibility of the

corresponding matrix (denoted by there). To get

(31), note that

For the last part, see in

particular [23: Eq. (A.8)].

References

Bensoussan [1971] Bensoussan,

A. (1971). Filtrage Optimal des Systèmes linéaires,

Dunod, Paris.

Bernstein and Hyland [1985]

Bernstein, D. and Hyland, D. (1985). “The optimal projection

equations for reduced-order state estimation,” Transactions on Automatic

control 30, 583–585.

Bernstein and Hyland [1986]

Bernstein, D. and Hyland, D. (1986). “The optimal projection

equations for finite-dimensional fixed-order dynamic compensation of

infinite-dimensional systems,” SIAM Journal on Control and Optimization

24, 122–151.

Bogachev [1998]

Bogachev, V. (1998). Gaussian Measures, American Mathematical Society,

Mathematical Surveys and Monographs, 62.

Da Prato and Zabczyk [1979]

Da Prato, G. and Zabczyk, J. (1979). Stochastic Equations in

Infinite Dimensions, Encyclopedia of Mathematics and its Applications, 44, Cambridge University Press.

De Souza [1989]

De Souza, C. (1989). “On stabilizing properties of solutions

of the Riccati difference equation,” Transactions on Automatic control

34, 1313–1316.

Germani et al. [1988]

Germani, A., Jetto, L., and Piccioni, M. (1988). “Galerkin

approximation for optimal linear filtering of infinite-dimensional linear

systems,” SIAM Journal on Control and Optimization 26, 1287–1305.

Hager and Horowitz [1976]

Hager, W. W. and Horowitz, L. L. (1976). “Convergence and

stability properties of the discrete Riccati operator equation and the

associated optimal control and filtering problems,” SIAM Journal on Control

and Optimization 14, 295–312.

Hiltunen et al. [2011]

Hiltunen, P., Särkkä, S., Nissilä, I., Lajunen, A., and Lampinen, J.

(2011). “State space regularization in the nonstationary

inverse problem for diffuse optical tomography,” Inverse Problems

27.

Horowitz [1974]

Horowitz, L. L. (1974). Optimal Filtering of Gyroscopic Noise, PhD.

thesis, Massachusetts Institute of Technology.

Huttunen and Pikkarainen [2007]

Huttunen, J. and Pikkarainen, H. (2007). “Discretization error

in dynamical inverse problems: one-dimensional model case,” Journal of

Inverse and Ill-posed Problems 15, 365–386.

Kalman [1960]

Kalman, R. (1960). “A new approach to linear filtering and

prediction problems,” Journal of Basic Engineering 82, 35–45.

Kreyszig [1989]

Kreyszig, E. (1989). Introductory Functional Analysis with

Applications, Wiley & Sons.

Krug [1991]

Krug, P. (1991). “The conditional expectation as estimator of

normally distributed random variables with values in infinitely dimensional

Banach spaces,” Journal of Multivariate Analysis 38, 1–14.

Larsson and Thomée [2005]

Larsson, S. and Thomée, V. (2005). Partial Differential Equations

with Numerical Methods, Texts in Applied Mathematics 45, Springer-Verlag.

Mohammadi et al. [2012]

Mohammadi, L., Aksikas, I., Dubljevic, S., and Forbes, J. (2012).

“LQ-boundary control of a diffusion-convection-reaction system,”

International Journal of Control 2, 171–181.

Pikkarainen [2006]

Pikkarainen, H. (2006). “State estimation approach to

nonstationary inverse problems: discretization error and filtering problem,”

Inverse Problems 22, 365–379.

Seppänen et al. [2001]

Seppänen, A., Vauhkonen, M., Somersalo, E., and Kaipio, J. (2001).

“State space models in process tomography — approximation of state

noise covariance,” Inverse Problems in Engineering 9, 561–585.

Simon [2007]

Simon, D. (2007). “Reduced order kalman filtering without

model reduction,” Control and Intelligent Systems 35, 169–174.

Sims [1982]

Sims, C. (1982). “Reduced-order modelling and filtering,”

Control and Dynamic Systems 18, 55–103.

Solin and Särkkä [2013]

Solin, A. and Särkkä, S. (2013). “Infinite-dimensional

Bayesian filtering for detection of quasiperiodic phenomena in

spatiotemporal data,” Physical Review E 88, 052909.

Stubberud and Wismer [1970]

Stubberud, A. and Wismer, D. (1970). “Suboptimal Kalman

filter techniques,” in C. Leondes, ed., “Theory and Applications of

Kalman Filtering,” Advisory Group for Aerospace Research and Development,

105–117.

Sun [1998]

Sun, J. (1998). “Sensitivity analysis of the discrete-time

algebraic Riccati equation,” Linear Algebra and its Applications

275–276, 595–615.