Optimal Portfolio Problem Using Entropic Value at Risk: When the Underlying Distribution is Non-Elliptical

Abstract

This paper is devoted to study the optimal portfolio problem. Harry Markowitz’s Ph.D. thesis prepared the ground for the mathematical theory of finance [10]. In modern portfolio theory, we typically find asset returns that are modeled by a random variable with an elliptical distribution and the notion of portfolio risk is described by an appropriate risk measure.

In this paper, we propose new stochastic models for the asset returns that are based on Jumps- Diffusion (J-D) distributions [11, 14]. This family of distributions are more compatible with stylized features of asset returns. On the other hand, in the past decades, we find attempts in the literature to use well-known risk measures, such as Value at Risk and Expected Shortfall, in this context. Unfortunately, one drawback with these previous approaches is that no explicit formulas are available and numerical approximations are used to solve the optimization problem. In this paper, we propose to use a new coherent risk measure, so-called, Entropic Value at Risk(EVaR) [2], in the optimization problem. For certain models, including a jump-diffusion distribution, this risk measure yields an explicit formula for the objective function so that the optimization problem can be solved without resorting to numerical approximations.

Keywords. Optimization portfolio problem, Coherent risk measure, Entropic value at risk, Conditional value at risk, Elliptical distribution, Jump-diffusion distribution.

1 Introduction

The problem of optimal portfolio which is nowadays introduced in a new framework, called Modern Portfolio Theory (MPT), has been extensively studies in the past decades. The MPT is one of the most important problems in financial mathematics. Harry Markowitz [10] introduced a new approach to the problem of optimal portfolio so called Mean-Variance analysis. He chose a preferred portfolio by taking into account the following two criteria. The expected portfolio return and the variance of the portfolio return. In fact, Markowitz preferred one portfolio to another one if it has higher expected return and lower variance.

Later, we find attempts in the literature to replace variance with well-known risk measures, such as Value at Risk and Expected Shortfall. For instance, Embrechts et al.[6] have shown that replacing mean-variance with any other risk measure having the translation invariant and positively homogeneous properties under elliptical distributions yields to the same optimal solution.

Basak and Shapiro [3] studied an alternative version of Markowitz problem by applying VaR for controlling the incurred risk in an expected utility maximization framework which allows to maximize the profit of the risk takers. Studying the Markowitz model has been done in the same framework by considering the CVaR as risk measure. [13]. Later, Acerbi and Simonetti [1] studied the same problem as the one studied in [3] with spectral risk measures. Recently, Cahuich and Hernandez [5] solved the same problem within the framework

of utility maximization using the class of distortion risk measures [15].

There are both practical and theoretical weaknesses that can be made about the relevant framework of optimal portfolio problem in the literature. One of such criticisms relates to the asset returns model itself. In fact, elliptical distribution is the most and relevant distribution which is used to model asset returns in MPT. One of the reason for choosing this distribution ties with the tractability of this class of distribution. But, in practice financial returns do not follow an elliptical distribution. A second objection focuses in the choice of a measure of risk for the portfolio. Unfortunately, one drawback with the previous works, for instance [3, 13], is that no explicit formulas are available and numerical approximations are used to solve the optimization problem. The stochastic models which we are proposing for the asset returns in this paper are based on Jumps- Diffusion (J-D) distributions [11, 14]. This family of distributions are more compatible with stylized features of asset returns and also allows for a straight-forward statistical inference from readily available data. We also tackle the second issue by choosing a suitable (coherent) risk measure as our objective function. In this paper, we propose to use a new coherent risk measure, so-called, Entropic Value at Risk(EVaR) [7, 2], in the optimization problem. As this risk measure is based on Laplace transform of asset returns, applying it to the jump-diffusion models yields an explicit formula for the objective function so that the optimization problem can be solved without using numerical approximations.

The organization of this paper is as follows. In Section 2, we provide a summary of properties about coherent risk measures and Entropic Value at Risk measure. We also continue this section by presenting a typical representation of optimal portfolio problem where we minimize the risk of the portfolio for a given level of portfolio return. In Section 3, we introduce our two models to fit as asset returns and we apply them into the optimization problem. We also derive some distributional properties for these models and finish Section 3 by discussing about the KKT conditions and optimal solutions. In Section 4, we discuss about parameters estimation method which we have used in this paper. We also provide a numerical example for three different stocks and analyze the efficient frontiers for EVaR, mean-variance and VaR for these three stocks. In this paper we use optimization package in MATLAB to do the computations.

2 Preliminaries

2.1 Coherent Risk Measures

We are considering as the set of all bounded random variables representing financial positions. The following definition is taken from [8].

Definition 1.

. A function is a Coherent Risk measure if

for any and .(Convexity)

for any and .(Positive Homogeneity)

for any and .(Translation Invariant)

and .(Decreasing)

In this paper, we propose to use the Entropic Value at Risk measure (EVaRα) which is a coherent risk measure. Following [2] we now give a first definition.

Definition 2.

Let be a random variable in such that

Then the Entropic Value at Risk, denoted by EVaRα, is given by

| (1) |

For a given level .

Theorem 3.

The risk measure EVaRα from Definition 2 is a coherent risk measure. Moreover, for any having Laplace transform, its dual representation has the form

where and

2.2 Optimal Portfolio Problem

Consider a portfolio in a financial market with different assets. Denote the assets returns by the vector in which shows the return of the i-th asset. The returns are random variables and their mean is denoted by where is the the expected return of the i-th asset, . Moreover, assume as a risk measure. Then following [13]

Definition 4.

the optimal portfolio problem can be written mathematically as follows.

| subject to | (2) | ||||

where is a given level of return.

Applying various risk measures along with different models for random returns yields to interesting problems in both theoretical and practical point of views. For instance, the classical mean-variance model introduced by Markowitz [10] is a special case of the model introduced in Definition 4. In fact, Markowitz used variance as a risk measure and apply it into the objective function given in (4) and he also considered returns from the portfolio are normally distributed.

Remark 5.

It has been shown in [6] that if we assume the return variables follow elliptical distributions(like multivariate normal distribution), then the solution for the Markowitz mean-variance problem will be the same as the optimal solution for optimal portfolio problem (4) by minimizing any other risk measure having the translation invariant and positively homogeneous properties for a given level of return.

[9] has shown in his PhD thesis that for two different examples of elliptical distributions(normal and Student t) the portfolio decomposition for Expected Shortfall and Value at Risk are the same as the one for standard deviation.

3 Set up the Models

In this section, we propose two multivariate models which do not follow elliptical distributions. These models which are based on jump-diffusion distributions can be fitted as the underlying models for returns. Distributional properties of these models will be also studied.

3.1 Non-Elliptical Multivariate Models 1,2

Multivariate Model 1. Consider the following multivariate model:

| (3) |

where are -variate vectors such that

Here, follows the normal distribution with and ’s are mutual independent for . is assumed to follow the multivariate normal distribution with for each where is mean and is covariance matrix. Moreover, ’s are assumed to be mutually independent. The random variable follows the Poisson distribution with intensity and is independent of for each . are assumed to have Poisson distribution with intensity and mutually independent for . The are assumed to be mutually independent for all k and all and is normal distributed with . Finally, and are mutually independent as well as .

This model can be driven from a jump-diffusion model which is the solution for a stochastic differential equation [11]. We can rewrite this multivariate model as follows.

Multivariate Model 2. The model in [14] prepared the ground to introduce another non-elliptical multivariate model which can be fitted for portfolio returns. This proposed model is given as follows.

| (4) |

Here, are -variate vectors such that

where follows the multivariate normal distribution with with covariance matrix . is assumed to follow the multivariate normal distribution with for each where is mean and is covariance matrix. Moreover, ’s are assumed to be mutually independent. The random variable follows the Poisson distribution with intensity and is independent of for each . Also, are mutually independent.

3.2 Distributional Properties of the Multivariate Models 1, 2

Consider the multivariate models (3) and (4). As these models are given in terms of summation of multivariate normal and compound Poisson distributions we can provide the joint density functions for each of these models. [12] gives the following presentation for the density function of model (3) and also provides a proof but we give a proof here for the sake of completeness.

Proposition 1.

Consider the model (3). Then the joint density functions of the vector is given by

| (5) |

where , and .

Proof.

The idea we put forward to prove this proposition is using conditional density function. Since the are mutual independent with normal distribution so the vector follows a multivariate normal distribution with mean and covariance matrix where is the identity matrix of order n. Moreover by conditioning on each of and using independency between we obtain

| (6) |

for each . Thus, independency between and for all and yields

| (7) |

Conditioning on the random variable and using the independency between and gives the following conditional distribution.

| (8) |

Putting (7) and (8) together and using independency between and provide the conditional distribution of given . i.e.,

| (9) |

(9) gives the conditional density of given . To get the density function of we need to multiply the conditional density by the probability functions associated to each and and add them up. This completes the proof. ∎

If we follow the same procedure done for Proposition 1 and apply it for the model (4) we can obtain the density function for the vector .

Remark 6.

Lemma 7.

Consider the multivariate model (3). Then the Laplace exponent for the vector at is

| (11) |

where and are the column vectors associated to the row vectors and respectively.

Proof.

The independency between and and using this point that Laplace transform for normal and compound Poisson distributions exists, yield the result. ∎

Proof.

The Laplace transform for Gaussian distributions and compound Poisson distributions exists. So, (12) can be driven by using the independency between and . ∎

Now, we apply EVaRα along with the model proposed in to the optimal portfolio problem . Thus, is written as follows.

| subject to | (13) | ||||

Applying EVaRα and the model (4) into the optimal portfolio problem yield to

| subject to | (14) | ||||

3.3 Necessary and Sufficient Conditions for Optimal Problems, KKT Conditions

In this section we would like to identify the necessary and sufficient conditions for optimality of problems and . In fact, we want to examine the Karush-Kuhn-Tucker (KKT) conditions for these problems and study whether the constrained problems in the last two sections have optimal solutions. Being the objective functions for both problems and smooth enough (they are continuously differentiable functions), will help us to verify the KKT conditions much easier.

3.3.1 KKT Conditions for Optimal Problem with the multivariate model 1

The KKT conditions provide necessary conditions for a point to be optimal point for a constrained nonlinear optimal problem. We refer to Chapter 5 page 241 [4] for a comprehensive study of KKT conditions for nonlinear optimal problems. Here, we study these conditions for the model by using the same notation used in page 200 [4]. We rewrite problem as follows.

| subject to | (15) | ||||

Let be a regular point333Let be a feasible point. Then, is said to be a regular point if the gradient vectors for are linearly independent. for the problem . Then, the point is a local minimum of subject to the constraints in if there exists Lagrange multipliers and for the Lagrangian function such that the followings are true.

-

1.

-

2.

-

3.

-

4.

-

5.

where is the ith entry of the row vector .

Remark 9.

Since, the functions and in (3.3.1) are linear and the functions for are convex, then by referring to Section of [4] we see that the feasible region is a convex set. On the other hand, the risk measure is a convex function subject to the variables and for all . We refer to [2] for a proof. Thus, the objective function in problem is convex too. We see that any local minimum for problem is a global minimum too and the KKT conditions are also sufficient. See [4] page 212.

3.3.2 KKT Conditions for Optimal Problem with the multivariate 2

In this section we will provide the KKT conditions for the optimal problem . We show that these conditions are also sufficient for a solution to be an optimal one. First, we rewrite the problem in the following way.

| subject to | (16) | ||||

By applying the same definition and notation used in the previous section we can provide the KKT conditions as follows.

-

1.

-

2.

-

3.

-

4.

-

5.

where and are the ith entry of the row vectors and respectively.

4 Efficient Frontier Analysis

In this section we study the optimization problem (4) for multivariate model 1 given in . In fact, we analyze the efficient frontier for this problem when the risk measures are EVaR and standard deviation. Our analysis shows that we have different portfolio decomposition corresponding to EVaR and standard deviation as the underlined model for returns is followed a non-elliptical distribution(model 1). Thanks to the closed form for EVaR we can use optimization packages in mathematical software to solve the optimization problem (3.2) without using simulation techniques like Monte Carlo simulation.

4.1 Parameters Estimation

Studying the optimization problems (3.2) and (3.2) requires knowing the parameters of the multivariate models (3) and (4). To estimate these parameters we use a method of estimation for joint parameters so called Extended Least Square(ELS)[16]. In fact, assume that we are given a sample of individuals. Let denote the subject’s vector of repeated measurements where the are assumed to be independently distributed with mean and covariance matrices given by

| (17) | |||||

where and are vectors of unknown parameters which should be estimated. Extended Least Square(ELS) estimates are obtained by minimizing the following objective function.

| (18) |

where and are defined in (17) and is the determinant of the positive definite covariance matrix . Following [16] it can be seen that ESL is joint normal theory maximum likelihood estimation. In fact, minimizing (18) is equivalent to maximizing the log-likelihood function of the when the are independent and normally distributed with mean anc covariance matrices given by (17).

4.2 Data Sets

We construct the portfolio by choosing 3 stocks. They are APPLE, INTEL and PFIZER(PFE). We use the close data ranged from 20/09/2010 to 26/08/2013. The weekly close data are converted to log return. i.e., if we consider as the close price for the week then log return is .

Now consider the model (3). We try to apply this model to these three stocks and determine the parameters in (17) in order to solve the optimization problem (18). In this case we have , the number of our sample and is a row vector associated to the mean of returns. Then the vector is,

| (19) |

for all . Let be the covariance matrix for the multivariate normal distribution . Then, the covariance matrix in (17) has the following representation.

| (20) |

for all . Therefore, by plugging (19) and (20) into (18) we get the objective function for the ELS method. Doing the same procedure for the model (4) we can find the parameters in (17). Let and be the covariance matrices for the multivariate normal distribution and respectively. Then we have,

| (21) |

and

| (22) |

for all .

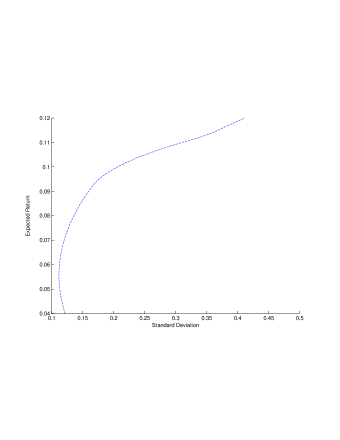

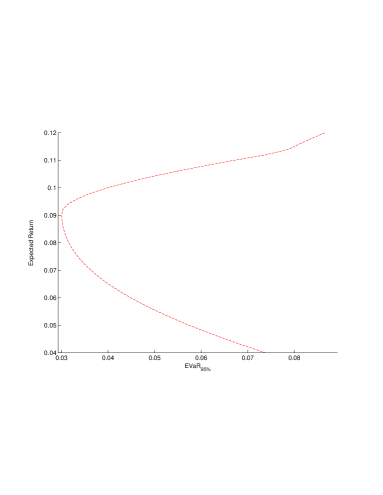

In the following we provide the results for the portfolio decomposition corresponding to the three stocks, EVaR95% and standard deviation. This results have been driven for the model 1 given in . In order to estimate our parameters for the model 1 we call fminsearch in Matlab, where the function to be optimized is the objective function introduced in (18). To find the efficient frontiers of EVaR95% we also call fmincon in Matlab, where the function to be optimized is the objective function in (3.2). Figure 1 shows the two efficient frontiers based on model 1 for EVaR95% and standard deviation. Table 1 and 2 show the portfolio compositions and the corresponding EVaR95% and standard deviation respectively.

|

|

References

- [1] Acerbi, C., Simonetti, P., Portfolio optimization with spectral measures of risk. arXiv:cond-mat/0203607v1, 2002.

- [2] Ahmadi-Javid A., Entropic Value-at-Risk: A New Coherent Risk Measure. Journal of Optimization Theory and Application, Springer. 2011.

- [3] Basak, S., Shapiro, A., Value-at-risk based risk management: optimal policies and asset prices. Rev. Financ. Stud. 14, 371–405, 2001.

- [4] Belegundu A. D., Chandrupatla R. T., Optimization Concepts and Applications in Engineering. Cambridge University Press, 2nd edition, 2011.

- [5] Cahuich, L.D., Hernandez, D.H., Quantile Portfolio Optimization Under Risk Measure Constraints. Appl Math Optim 68:157–179, 2013.

- [6] Embrechts, P., McNeil, A., Straumann. Correlation and dependency in risk management: properties and pitfalls. In Risk Managemenmt: Value at Risk and Beyond, ed. by M. Dempster, and H. Moffatt. Cambridge University Press, 2001.

- [7] Follmer, H., Knispel, T.,Entropic risk measures: coherence vs. convexity, model ambiguity, and robust large deviations. Stoch. Dyn. 11, no. 2-3, 333-351, 2011.

- [8] Follmer, H., Schied A., Stochastic finance, An introduction in discrete time. volume 27 of de Gruyter Studies in Mathematics. Walter de Gruyter & Co., Berlin, extended edition, 2004.

- [9] Hu, W.,Calibration of multivariate generalized hyperbolic distributions using the EM algorithm, with applications in risk management, portfolio optimization and portfolio credit risk. Thesis (Ph.D.)-The Florida State University. 115 pp. ISBN: 978-0542-66575-2, 2005.

- [10] Markowitz, H.M., Portfolio Selection. The Journal of Finance 7 (1): 77-91, 1952.

- [11] Press S. J., A Compound Events Model for Security Prices. Journal of Business, Vol. 40, No. 3, 1967.

- [12] Press S. J., A Compound Poisson Process For Multiple Security Analysis. Random Counts in Scientific Work: Random Counts in Physical Science, Geo Science and Business v. 3, 1971.

- [13] Rachev, S.T., Stoyanov, S.V., Fabozzi, F.J., Advanced Stochastic Models, Risk Assessment, and Portfolio Optimization: The Ideal Risk, Uncertainty, and Performance Measures. Wiley, ISBN: 978-0-470-05316-4, 2008.

- [14] Ruijter M. J., Oosterlee C. W., Two-dimensional Fourier cosine series expansion method for pricing financial options. SIAM J. Sci. Comput. 34, no. 5, 2012, P. 642-671

- [15] Tsukahara, H. One-parameter families of distortion risk measures. Math. Finance 19, 691–705, 2009.

- [16] Vonesh, E., Chinchilli, V.M., Linear and Nonlinear Models for the Analysis of Repeated Measurements. CRC Press, 1996.